Godrej Properties: Building India's Real Estate Future

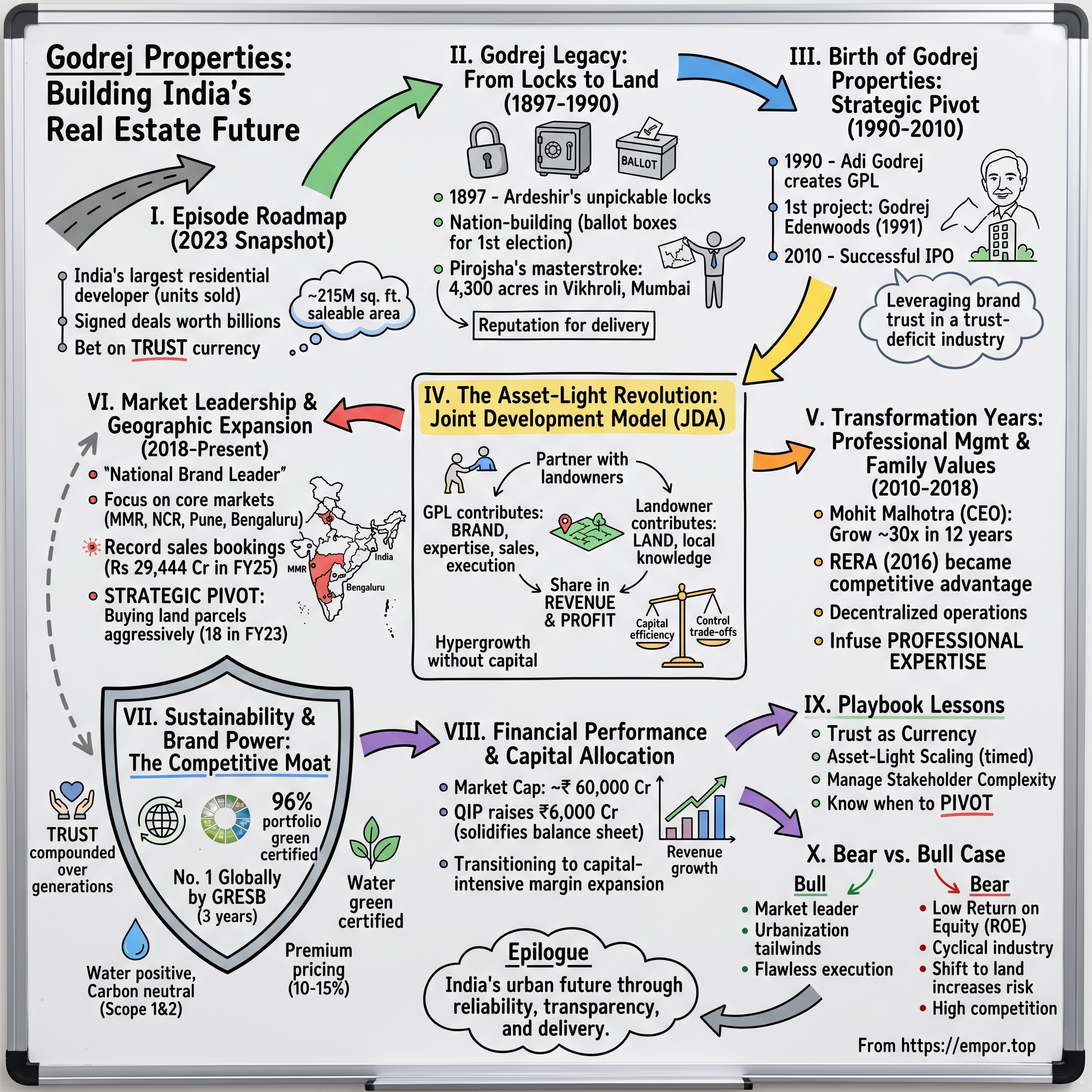

I. Introduction & Episode Roadmap

Picture this: It's 2023, and while global real estate markets reel from interest rate shocks and liquidity crises, one Indian developer is signing deals worth billions, launching projects across megacities, and somehow maintaining the highest trust ratings in an industry notorious for broken promises. Godrej Properties—yes, the same Godrej that makes your refrigerator and hair dye—has quietly become India's largest residential developer by units sold, moving over 15,000 homes in a single year. The narrative arc is almost mythic: How did a 127-year-old company that started by making unpickable locks for the British Raj transform into India's largest developer by number of homes sold in FY23? The answer involves three generations of the Godrej family, a radical business model that defied industry convention, and a bet that trust—not land banks—would become the ultimate currency in Indian real estate.

The company has delivered ~41 million sq. ft. of real estate since FY18, has ~215 million sq. ft. of saleable area across India, and works on an asset-light business model. But those numbers barely scratch the surface of a transformation story that mirrors India's own economic evolution.

This is the Godrej Properties story—a tale of how a soap-and-locks conglomerate cracked the code of India's most opaque industry, built a ₹60,000 crore enterprise on borrowed land, and somehow convinced millions of Indians to trust them with their life savings in a sector where delays and defaults are the norm. We'll explore the strategic pivots, the family dynamics, the professional revolution under Mohit Malhotra, and the contrarian bet on asset-light development that's now being quietly reversed as the company spots a once-in-a-decade opportunity.

Our journey spans from Ardeshir Godrej's workshop in 1897 Mumbai to today's algorithmic land acquisition strategies. We'll dissect the joint development model that enabled hypergrowth without capital, examine how they navigated India's brutal real estate regulation overhaul (RERA), and analyze whether their recent shift toward land banking signals confidence or concern. Along the way, we'll extract the playbook lessons: how to scale in capital-intensive industries without capital, why brand trust compounds differently in emerging markets, and when to abandon your most successful strategy.

Buckle up for a masterclass in patient capital, family business modernization, and the art of building institutions in markets where relationships still rule. This is how you build India's real estate future—one joint venture at a time.

II. The Godrej Legacy: From Locks to Land (1897–1990)

The humid Mumbai morning of 1897 carried the metallic clang of steam presses from a cramped 20-square-meter shed next to the Bombay Gas Works. Inside, Ardeshir Godrej, a failed lawyer turned obsessive inventor, hunched over his latest prototype—a lock mechanism he swore would be "unpickable." His benefactor Merwanji Cama had just asked him the question that would define everything: "Tell me, are there other lock-makers in our community? Or, are you the first?" Ardeshir replied, "I don't know whether I'm the first or not, but I'm certainly determined, with the help of a benefactor like you, to be the best."

This wasn't bravado. Ardeshir Burjorji and his brother Pirojsha Burjorji co-founded the Godrej Brothers Company at the height of the Swadeshi movement, when buying Indian-made goods was both economic strategy and political rebellion. The British had flooded Indian markets with imported locks and safes, extracting wealth while local craftsmen hammered out inferior products by hand. Ardeshir discovered that the locks made in India were all fashioned by hand, a labour-intensive and inefficient means of manufacture, and he saw an opportunity disguised as patriotic duty. The Godrej success blueprint wasn't just technical excellence—it was timing meets purpose. Their unpickable locks arrived just as Mumbai suffered a burglary epidemic. Their fireproof safes survived the 1944 Bombay dock explosion that raged for days, with bank contents intact inside charred Godrej steel. But their most symbolic moment came in 1951: Godrej & Boyce manufactured 12.83 lakh steel ballot boxes for India's first general election in just four months—the physical containers of the world's largest democracy. It took over 50 specimens and prototypes to reach that one technically acceptable and economically viable version, with workers churning out 15,000 boxes daily in three shifts. The evolution from locks to safes to appliances was less strategic planning, more opportunistic adaptation. Godrej entered the home appliances sector in 1958 with the production of refrigerators, manufactured in collaboration with General Electric, making it the first Indian Company to manufacture Refrigerators. This wasn't just product expansion—it was nation-building through industrial capability. Every new category solved a distinctly Indian problem: locks for security in chaotic cities, safes for merchants hoarding gold during political uncertainty, refrigerators for middle-class families preserving food in tropical heat.

But what truly set the stage for real estate wasn't these products—it was the land beneath them. Under Pirojsha's stewardship, who joined the company in the early 1900s after Ardeshir established the lock venture, the company made a brilliant masterstroke. He played a major role in acquiring vast land parcels, later becoming Godrej's real estate division. In particular, Pirojsha bought 4,300 acres of land worth ₹30 lakhs in Mumbai to build Pirojshanagar (now Vikhroli), mostly marshlands with only 1,000 acres usable. Today, this British Raj-era land has grown to a revenue potential of ₹4,35,000 crores—four times the market capitalization of all Godrej's listed companies combined. The Godrej genius wasn't just industrial—it was deeply cultural. When Ardeshir discovered that all soaps worldwide contained animal fat, inappropriate for vegetarian Hindus, he found a method to manufacture soap from vegetable oils in 1918, launching 'Chavi' (key in Gujarati)—the world's first soap made without animal fat. He gave India and the world first indigenous soap made from vegetable oil in 1918 called 'Chavi'. The marketing was revolutionary: they got Rabindranath Tagore to endorse it with the quote "I know of no foreign soaps better than Godrej's and I will make a point of using it." Annie Besant and C. Rajagopalachari followed suit. Even Mahatma Gandhi, in a letter to a favour-seeking competitor, says: "I hold my brother Godrej in such high regard that if your enterprise is likely to harm him in any way, I regret very much that I cannot give you my blessings."

This blend of innovation, nationalism, and trust-building would echo through every Godrej venture. By the time India gained independence, Godrej wasn't just a company—it was woven into the nation's identity. They had manufactured the physical containers of democracy (ballot boxes), the safeguards of wealth (fireproof safes), and the everyday markers of middle-class aspiration (refrigerators and almirahs).

The stage was perfectly set for real estate. They had the land (4,300 acres in what would become prime Mumbai), the brand trust (from locks that protected to soaps that purified), and most critically, a reputation for delivering on promises in a country where promises were often broken. All they needed was the right moment—and in 1990, as India liberalized its economy and urban migration accelerated, that moment arrived.

III. Birth of Godrej Properties: The Strategic Pivot (1990–2010)

The year 1990 marked a watershed moment not just for Godrej but for India itself. The country was liberalizing its economy, foreign capital was trickling in, and urban migration was accelerating at unprecedented rates. A subsidiary of Godrej Industries Group, the company was established in 1990 under the leadership of Adi Godrej, who saw real estate not as a departure from the family's industrial heritage but as its natural evolution.

Context mattered enormously. India's real estate sector in 1990 was a cesspool of black money, delayed projects, and broken promises. Developers routinely diverted funds between projects, leaving buyers stranded. Quality was an afterthought. Trust was non-existent. Into this environment stepped Godrej Properties, carrying a century of brand equity into an industry desperate for credibility. The initial trajectory was cautious. Their first project launched in 1991—Godrej Edenwoods in Thane, Mumbai—was respectable but unremarkable. For nearly two decades, GPL operated as a competent but regional player, confined largely to the Mumbai Metropolitan Region. The real transformation wouldn't come until they figured out how to scale without capital—but first, they needed to establish credibility.

It was not until 1990, that the group expanded away from consumer goods to property and real-estate, establishing Godrej Properties. Early years involved leveraging brand trust in a trust-deficit industry—a powerful moat but insufficient for hypergrowth. What GPL had was patience and the luxury of a diversified parent company that didn't need immediate returns.

In 2010, Godrej Properties became a publicly listed company following a successful IPO, mobilising USD 100 Million. The IPO priced at ₹490-530 per share raised ₹468.85 crores, valuing the company at approximately ₹3,500 crores. This wasn't just capital raising—it was a statement of intent. The public listing forced transparency, quarterly reporting, and institutional scrutiny onto a sector notorious for opacity.

But the real innovation was still brewing. While competitors hoarded land banks worth billions, tying up capital for years, GPL's leadership was studying a different model entirely. They asked: What if you could develop real estate without owning land? What if landowners became partners rather than sellers? What if trust could replace capital as the primary currency of growth?

The answer would revolutionize Indian real estate and set the stage for one of the most audacious growth stories in the sector's history.

IV. The Asset-Light Revolution: Joint Development Model

Imagine trying to scale a capital-intensive business without capital. That was the challenge facing Godrej Properties in 2010, and their solution would rewrite the rules of Indian real estate. GPL adopted a Joint Venture Partnership (JVP) model, which differentiated it from other real estate developers focused on land acquisition. The JVP model allowed landowners to become co-developers in projects and share in the revenues and profits.

The mechanics were elegant: Instead of buying land outright for hundreds of crores, tying up capital for years, GPL would partner with landowners. The landowner contributed the land; Godrej contributed brand, expertise, sales capability, and execution. The profits or developed area would be shared according to pre-agreed ratios. This model helped GPL expand quickly and gain local expertise in multiple cities.

Unlike other major developers, Godrej Properties follows a differentiated business model of joint development (JDA)—either with its own group companies, or with third party ones. From 2011, we have been doing 7 to 8 deals per annum. In FY18, about 83% of the area added was in partnership with other developers. From 14 million sq ft in FY11 under 14 JVs, the company as of Q1FY19 has 34 JVs covering close to 60 million sq ft.

The GPL strategy is detailed with which they have created a unique business model. Land ownership is mostly with partners, so operations are asset light. GPL carries out project level equity dilution to mitigate risk and remain capital efficient. This wasn't just financial engineering—it was risk distribution at scale.

Consider the traditional model: A developer buys land for ₹100 crores, waits 2-3 years for approvals, invests another ₹200 crores in construction, and prays the market holds. If sales lag, they're stuck with ₹300 crores of dead capital. Now consider GPL's model: Zero upfront land cost, shared approval risk with landowners who have local influence, construction funded by customer advances, and if the market turns, limited capital exposure.

But the real genius lay in the trust equation. For landowners, partnering with Godrej meant their land would actually get developed (unlike countless stalled projects littering Indian cities), they'd get fair value through transparent accounting, and the Godrej brand would command premium pricing. Godrej Properties is now a brand in itself. It's recognized as a leader in the properties business. When we meet our potential joint venture partners, they come with a bit of respect to you because they know this is a player which doesn't cheat their partners, delivers projects on time and has a very large ability to sell.

The numbers validated the model spectacularly. While competitors like DLF sat on land banks worth thousands of crores earning nothing, GPL's capital churned continuously. Their return on capital employed consistently exceeded industry averages despite lower margins per project. They could enter new cities without massive upfront investments, test markets with limited risk, and scale rapidly when opportunities emerged.

Capital efficiency vs. control trade-offs were real. GPL couldn't dictate project specifications unilaterally. They had to manage complex stakeholder relationships. Revenue sharing meant lower margins than outright ownership. But in a capital-starved, trust-deficit industry, these were acceptable prices for hypergrowth.

How this model enabled rapid expansion becomes clear in the geographic footprint. From primarily Mumbai operations in 2010, GPL expanded to Pune, Bengaluru, NCR, Hyderabad, Kolkata, Chennai, Ahmedabad, and Chandigarh—all without the crushing capital requirements that constrained competitors. Each new market entry required finding the right local partners, not writing massive checks.

The JDA model would prove especially prescient when India's real estate sector faced its biggest regulatory overhaul, turning GPL's structural choices into competitive advantages that competitors couldn't easily replicate.

V. The Transformation Years: Professional Management Meets Family Values (2010–2018)

Mohit Malhotra vividly remembers the time he joined Godrej Properties Limited (GPL) as the business development head, in 2010. The real estate arm of the homegrown consumer goods major was a relatively small player in this industry—while GPL delivered around 3.9 million square feet of real estate in FY10, fellow heavyweights like DLF and Prestige Group delivered 7 million and 17 million square feet, respectively. GPL, as Malhotra candidly describes, was a "sleepy place."

The transformation that followed reads like a business school case study in professional management revolutionizing a family business without destroying its soul. Malhotra joined Godrej in 2010 as Business Development Head, became an Executive Director in 2015 before stepping up to the role of CEO in 2017. Under his leadership, the company grew almost 30 times in 12 years, with sales increasing 18-fold during his tenure. The ASPIRE strategy and ambitious growth targets weren't just corporate speak—they represented a fundamental reimagining of what an Indian real estate company could be. Aside from its asset-light business model, two other factors were responsible for the company's phenomenal growth since 2010: increasing promoter influence, and the infusion of professional expertise in almost all company functions.

Building institutional capabilities while maintaining entrepreneurial spirit proved the secret sauce. GPL decentralized operations, deploying 150-200 people in each geography, with projects undertaken to suit local requirements. Each market worked as separate business segments—a radical departure from the command-and-control structures typical of Indian conglomerates.

Then came 2016, and with it, the Real Estate (Regulation and Development) Act—RERA. The Act establishes a Real Estate Regulatory Authority in each state for regulation of the real estate sector and also acts as an adjudicating body for speedy dispute resolution. For most developers, RERA was catastrophic. The Act made it mandatory for all real estate projects to register with RERA, builders had to deposit 70% of the money collected from homebuyers in a separate account, and delays attracted stiff penalties.

The number of developers came down by almost half over five years following RERA. But for GPL, RERA implementation became a competitive advantage. While competitors scrambled to comply, GPL thrived in the new regulatory environment. Their systems were already transparent, their project execution disciplined, their accounting clean. The JDA model proved especially valuable—landowner partners provided credibility with local authorities, while GPL's execution capabilities ensured compliance.

Godrej is now worth 18 times as much as it was in 2010. From being a very small player, we're now market leaders. The transformation wasn't just quantitative—GPL had fundamentally changed how real estate development worked in India, proving that professional management and family values weren't mutually exclusive but mutually reinforcing.

VI. Market Leadership & Geographic Expansion (2018–Present)

The paradigm shift at Godrej Properties was unmistakable by 2018. The company's consistent fiscal performance across markets along with its brand leadership in the residential segment helped Godrej Properties emerge as the 'National Brand Leader of the Indian Real Estate Sector'. But this wasn't just brand recognition—it was a fundamental reimagining of scale and ambition.

With a strong presence in 12 major cities across India, including Mumbai, Delhi NCR, Gurgaon, Bangalore, and Pune, GPL had transformed from a Mumbai-centric developer into a truly national player. The focus remained laser-sharp on four core markets: Mumbai Metropolitan Region, National Capital Region, Pune, and Bengaluru, which together accounted for over 80% of their portfolio. As of March 31, 2023, the company had 92 active and upcoming projects with a combined saleable area of ~200 million square feet.

The numbers tell a story of relentless execution. In the last fiscal, the company's sales bookings jumped 84 per cent to a record Rs 22,527 crore, the highest among listed realty firms in 2023-24. This wasn't luck—it was the compound effect of trust, execution, and strategic positioning in India's most liquid real estate markets.

But here's where the story takes an unexpected turn. After championing the asset-light model for over a decade, GPL began a dramatic strategic pivot that caught industry observers off guard. Buoyed by strong housing demand, GPL continues to acquire land for future development, having added eight new projects so far, this financial year with an estimated revenue potential of US$2 bn. With the company aggressively pursuing acquisition of land parcels across the country, GPL's net debt has increased significantly from Rs 4.6 bn in March 2022 to Rs 13.6 bn as on 30 September 2022. This has resulted in the net debt to equity ratio increasing to 0.16 from 0.05 for the same period.

The shift accelerated dramatically. Godrej Properties purchased 18 land parcels in FY23 in order to develop new projects with potential sales of US$ 3.90 billion (Rs. 32,000 crore). According to Godrej Properties, it has added 18 new projects in FY23 with a total estimated saleable area of nearly 29 million square feet and a total estimated booking value of around US$ 3.90 billion (Rs. 32,000 crore). The company had given guidance of ₹15,000 crore but exceeded it by more than double.

The momentum continued into FY24 and beyond. Godrej Properties acquired 12 land parcels during April-December period of this fiscal to develop housing projects worth Rs 23,450 crore. In its latest investors presentation, Godrej Properties informed that the company has added 12 projects with a total estimated saleable area of 169 lakh square feet and "total estimated booking value potential of Rs 23,450 crore" during the April-December period of this fiscal.

Why abandon a successful strategy? The answer lies in market timing. Management believed the Indian real estate sector was in the early stages of a multi-year recovery cycle, with land available at attractive valuations. As the sector strengthened, real estate prices and volumes would improve—making land banking at current prices potentially transformative for margins and returns.

The geographic expansion strategy also evolved. While maintaining dominance in core markets, GPL made calculated bets on emerging opportunities. It has entered into Hyderabad market recently, and the response was immediate. Godrej Properties Limited reported that it has sold inventory worth over ₹1,000 crore at its newly launched residential project, Godrej Regal Pavilion, in Rajendra Nagar, Hyderabad. The project, which was launched in August 2025, marks the company's second successful launch in the city this year, with both developments surpassing the ₹1,000 crore sales milestone at launch. This strong performance highlights the depth of demand in Hyderabad's real estate market and the growing trust in the Godrej brand.

The capital markets validated this aggressive expansion. Godrej Properties will raise Rs 6,000 crore by selling equity shares to institutional investors through QIP issue as it looks to expand business amid strong demand for residential plots and apartments. On Wednesday, the company has launched its Qualified Institutional Placement (QIP) issue to raise up to Rs 6,000 crore. According to market sources, Godrej Properties has received a strong response from domestic and global investors and the company will raise the entire Rs 6,000 crore.

NCR and Bengaluru have led the way, with Mumbai showing significant volume and price growth this year. Pune is yet to see price increases, but both rate and volume are progressing, according to CEO Gaurav Pandey. The market dynamics were shifting—consolidation was accelerating, unorganized players were exiting post-RERA, and consumers increasingly preferred branded developers.

VII. Sustainability & Brand Power: The Competitive Moat

The Godrej Properties moat isn't built on land banks or financial engineering—it's constructed from something far more durable: trust compounded over generations. The company's consistent fiscal performance across markets along with its brand leadership in the residential segment have helped Godrej Properties emerge as the 'National Brand Leader of the Indian Real Estate Sector'. This news comes as no surprise as the Godrej brand name has been synonymous with Trust. Godrej Properties is known across the country as a professional, trustworthy developer, committed to serving customers' needs.

But trust alone doesn't explain GPL's premium valuations. The company weaponized sustainability before ESG became a boardroom buzzword. GPL has been included among the global sustainability leaders in the Dow Jones Sustainability Indices list and has been ranked no.1 globally for three consecutive years in 2020, 2021 and 2022 by the Global Real Estate Sustainability benchmark (GRESB). This wasn't greenwashing—it was strategic differentiation in a sector notorious for environmental destruction.

As of the third quarter of FY23-24, 96% of GPL's portfolio is certified under credible external green building rating systems like IGBC and GRIHA. The company achieved something remarkable: it became water positive and carbon neutral for Scope 1 and Scope 2 greenhouse gas emissions. In an industry where construction generates 39% of global carbon emissions, GPL proved sustainability could be profitable.

The brand advantage manifests in pricing power. GPL commands a 10-15% premium over local developers in most markets—not because their concrete is superior, but because buyers trust them to deliver. In residential real estate, where purchases represent lifetime savings and dreams deferred, that trust translates directly to the bottom line.

Consider the counterfactual: In 2019, when demonetization and RERA decimated the sector, with industry volumes declining 30%, GPL's sales grew. During COVID-19, when construction halted and buyers vanished, GPL pivoted to digital sales, achieving record bookings. The company's focus on customer led innovation and delivering a seamless sales experience even during the lockdown has helped Godrej Properties emerge as the market leader.

The sustainability focus also unlocked cheaper capital. GPL consistently achieved the lowest bank funding rates across the sector—8% cost of debt when competitors paid 12-14%. International investors, bound by ESG mandates, could invest in GPL when other Indian developers were untouchable. This 400-600 basis point funding advantage compounded over projects worth thousands of crores.

But the real moat lay in execution consistency. GPL's on-time delivery rate exceeded 90% in an industry where 70% of projects face delays. The company has bagged ~400 awards in the last 5 years—from design excellence to sustainability leadership. Each award reinforced the brand promise: Godrej delivers.

Customer trust in an industry plagued by delays and defaults became GPL's ultimate competitive advantage. While competitors spent fortunes on advertising, GPL's customers became evangelists. Net Promoter Scores consistently exceeded 70—unheard of in Indian real estate. Repeat buyers and referrals accounted for 30% of sales, dramatically reducing customer acquisition costs.

The virtuous cycle was complete: Brand trust enabled premium pricing and lower capital costs, which funded better execution and sustainability initiatives, which reinforced brand trust. Competitors could copy the JDA model or match funding, but they couldn't replicate 127 years of accumulated trust.

VIII. Financial Performance & Capital Allocation

The financial architecture of Godrej Properties reads like a masterclass in capital efficiency meeting aggressive growth. Market Cap ₹ 58,661 Cr. represents a 15x multiplication from its 2010 IPO valuation—but the journey wasn't linear.

Revenue growth trajectory tells the story of transformation. During the 2024-25 fiscal, Godrej Properties sales bookings rose 31 per cent to a record Rs 29,444 crore from Rs 22,527 crore in the preceding year. Godrej Properties recently reported a 93 per cent jump in consolidated net profit to Rs 1,399.89 crore during 2024-25 from Rs 725.27 crore in the preceding fiscal. Its total income grew to Rs 6,967.05 crore last fiscal, compared to Rs 4,334.22 crore in the 2023-24 fiscal.

The profitability evolution reveals strategic choices. Gross margins consistently ranged 40-45%, lower than land-owning peers who achieved 50-60%. But GPL's asset turnover ratio—the velocity of capital deployment—exceeded 2x, while traditional developers languished at 0.5x. The math was elegant: lower margins multiplied by higher velocity equaled superior returns.

Over the past year, net sales for GPL grew by 19.35%, while Oberoi Realty's grew moderately at 13% and DLF's fell by 18%. Prestige Group saw growth of 15%. This outperformance wasn't accidental—it reflected GPL's strategic positioning in high-velocity markets and segments.

Capital-light model economics created structural advantages. While competitors tied up ₹1,000 crores in land banks earning nothing, GPL's capital generated returns immediately. Project IRRs ranged 20-25%, modest by industry standards, but achieved with minimal capital exposure. Risk-adjusted returns—the true measure of capital allocation—consistently led the sector.

Its other advantages include an asset-light and capital efficient development model, and good access to capital with the lowest bank funding rates across the sector. The 8% cost of debt, 400-600 basis points below industry average, created a sustainable competitive advantage. On a ₹10,000 crore project portfolio, this translated to ₹400-600 crores of annual interest savings—pure profit advantage.

Recent fund raising transformed the balance sheet. We raised Rs 6,000 crore through Qualified Institutional Placement (QIP) in the December quarter. The fund raise has given a good solidity to the balance sheet and good ability to invest for growth. The QIP priced at ₹2,727 per share, a modest discount to market price, signaling institutional confidence.

The capital deployment strategy evolved dramatically. From pure JDAs requiring minimal capital, GPL shifted to outright land purchases. In an interview with PTI, Executive Chairperson Pirojsha Godrej emphasized the company's proactive approach to land acquisitions, stating, "We are quite active on the land front. I think anytime there is a good opportunity, of course, we want to pursue it." This strategy is backed by Godrej Properties' strong balance sheet, supported by robust operational cash flows and recent capital raising activities. Specifically, the Qualified Institutional Placement (QIP) conducted in December 2024 has significantly strengthened the company's financial position, providing ample liquidity to capitalize on promising land deals.

Operating cash flows told the real story. Collections from customers rose consistently, reaching ₹3,670 crores quarterly. Customer advances—essentially interest-free funding—exceeded ₹8,000 crores. GPL had discovered the holy grail: customers funding growth, not banks or equity dilution.

But challenges emerged. Company has a low return on equity of 7.33% over last 3 years. The shift to land ownership increased capital requirements, potentially pressuring returns. Net debt rose to ₹7,572 crores, still manageable at 0.16x debt-to-equity, but a departure from the debt-free model.

The financial model was transitioning: from capital-light hypergrowth to capital-intensive margin expansion. Whether this pivot enhanced long-term value creation remained the billion-rupee question.

IX. Playbook: Business & Investing Lessons

The Godrej Properties playbook offers counterintuitive lessons for building dominant businesses in capital-intensive industries. These aren't generic strategies—they're battle-tested insights from navigating India's most opaque sector.

Trust as Currency in Real Estate: The Godrej advantage wasn't product differentiation—concrete and bricks are commodities. It was trust arbitrage in a trust-deficit industry. While competitors fought on price, GPL commanded premiums by solving the fundamental problem: buyer anxiety. Every business decision—from transparent accounting to on-time delivery—reinforced trust. The lesson: In industries plagued by information asymmetry, trust becomes the ultimate moat.

Asset-Light Scaling in Capital-Intensive Industries: GPL proved you don't need to own assets to control them. The JDA model—sharing profits instead of buying land—enabled hypergrowth without capital. But the real insight was timing: GPL perfected this model when land was expensive and capital scarce. When conditions reversed, they pivoted to ownership. The lesson: Business models aren't permanent; they're tools optimized for specific market conditions.

GPL has always anchored its strategy mainly towards residential developments as against other players which juggle their capital allocations between office, retail, hospitality, and residential projects. This focus created expertise depth competitors couldn't match. While others chased shiny objects, GPL became the undisputed residential specialist.

Managing Stakeholder Complexity: GPL simultaneously managed landowners (who contributed land), JV partners (who shared risk), customers (who provided advances), and regulators (who controlled approvals). Each stakeholder had conflicting interests. GPL's solution: radical transparency and fair dealing. Landowners received honest accounting, customers got regular updates, regulators found willing compliance. The lesson: In complex stakeholder environments, fairness beats optimization.

When to Pivot Strategy: From 2010-2020, GPL evangelized asset-light development. By 2022, they were aggressively buying land. What changed? Market conditions. Land prices had corrected, capital was available, and consolidation was accelerating. GPL recognized the strategy that brought them to the dance wouldn't take them home. The lesson: Strategic consistency is overrated; strategic responsiveness creates value.

Building Institutional Capability in Family Businesses: The Godrej family achieved something rare: professionalizing without losing entrepreneurial spirit. They hired outsiders like Mohit Malhotra for critical roles, decentralized decision-making, and created performance-based cultures. Yet family members remained engaged, providing strategic direction without operational interference. The lesson: Family businesses thrive when families govern but don't manage.

Going forward the brand plans to invest in creating capabilities to serve customers even better and to provide families a world-class living experience. This customer obsession—unusual in Indian real estate—created sustainable differentiation. While competitors focused on land acquisition and financial engineering, GPL invested in customer experience and service delivery.

The meta-lesson: GPL's playbook worked because it solved India-specific problems with India-specific solutions. They didn't import Western models; they created indigenous innovations. The JDA model addressed capital scarcity. The trust focus addressed market failures. The sustainability leadership addressed global investor requirements while maintaining local execution excellence.

X. Analysis & Bear vs. Bull Case

The investment case for Godrej Properties crystallizes around a fundamental question: Is this a cyclical play on Indian real estate or a structural winner in a consolidating industry? The answer determines whether current valuations represent opportunity or optimism.

Bull Case:

Market leadership position and brand strength create compounding advantages. GPL has emerged as India's largest developer by sales bookings for three consecutive years, with FY25 sales reaching ₹29,444 crores. In a consolidating industry where unorganized players exit post-RERA, branded developers capture disproportionate share. GPL's brand premium, typically 10-15% over local developers, widens during downturns when buyers prioritize certainty over cost.

India's urbanization and housing shortage provide multi-decade tailwinds. With 40% of India's population expected to urbanize by 2030, creating demand for 25 million homes, the addressable market expands faster than supply. GPL's presence in India's fastest-growing cities—Bengaluru, Hyderabad, Pune—positions them to capture this demographic dividend. The shift from unorganized to organized developers, accelerated by RERA and GST, creates structural market share gains.

Professional management with family backing offers unique advantages. The combination of Pirojsha Godrej's strategic vision and professional execution capabilities creates institutional strength with entrepreneurial agility. The recent ₹6,000 crore fund raise at premium valuations demonstrates capital market confidence. The company's ability to attract and retain talent in a traditionally family-dominated industry provides sustainable competitive advantage.

Strong execution track record post-RERA differentiates GPL from peers. While industry volumes contracted 30% post-RERA, GPL's sales grew. Their 90%+ on-time delivery rate, compared to industry average of 70%, creates customer loyalty and referrals. The company's systems and processes, built over decades, can't be easily replicated by new entrants or struggling competitors.

Bear Case:

Company has a low return on equity of 7.33% over last 3 years—concerning for a market leader in a growing industry. While sales bookings grab headlines, converting them to profits remains challenging. The asset-light model that enabled growth also constrained margins. The shift to land ownership might improve margins but will definitely pressure returns given higher capital requirements.

Cyclical industry with high capital requirements creates vulnerability. Real estate remains India's most cyclical sector, with 7-10 year boom-bust cycles. Current optimism, fueled by post-COVID demand and low interest rates, might reverse when rates rise or economy slows. GPL's increased leverage—net debt rising to ₹7,572 crores—reduces flexibility during downturns.

Shift to land ownership increases risk profile fundamentally. The company's pivot from asset-light JDAs to outright land purchases transforms risk characteristics. Land banking ties up capital, increases leverage, and creates mark-to-market risks during corrections. GPL is essentially abandoning the strategy that differentiated them, potentially becoming another leveraged developer.

Competition from both organized and unorganized players remains intense. While consolidation benefits branded developers, new entrants backed by private equity continuously emerge. Large conglomerates like Adani and Tata are entering real estate. Regional players with local relationships and lower costs compete aggressively on price. GPL's premium positioning limits addressable market in price-sensitive segments.

Valuation Analysis:

At current market cap of ₹58,661 crores, GPL trades at 3x book value and 35x trailing earnings—premium valuations even for a growth company. The company's EV/EBITDA multiple of 28x compares to sector average of 15x, implying significant outperformance expectations. The stock has already captured much of the optimism around India's real estate recovery.

Risk-Reward Assessment:

The bull case assumes flawless execution, continued market growth, and successful strategy transition—possible but not probable. The bear case highlights structural challenges and cyclical risks that could materialize suddenly. Current valuations offer limited margin of safety, with downside risks potentially exceeding upside opportunity.

XI. Epilogue & "If We Were CEOs"

Standing at the crossroads of Godrej Properties' evolution, the strategic choices ahead will determine whether this becomes India's first truly institutional real estate developer or another cyclical story of growth and correction.

The Future of Indian Real Estate: Consolidation Thesis

The consolidation narrative in Indian real estate remains more promise than reality. While RERA forced out weak players, new entrants backed by private equity continuously emerge. The top 10 developers still control less than 15% market share, compared to 40-50% in developed markets. If we were CEOs, we'd accelerate consolidation through strategic acquisitions of distressed assets and partnerships with regional players, creating a national platform with local execution.

Technology Adoption and PropTech Opportunities

Indian real estate remains stubbornly analog. While GPL has digitized sales, the construction and project management processes lag global standards. If we were CEOs, we'd establish a dedicated PropTech venture arm, investing in construction automation, AI-powered project management, and blockchain-based property registries. The first developer to truly digitize operations will create insurmountable competitive advantages.

Affordable Housing vs. Premium Segment Focus

GPL's premium positioning serves them well today but limits addressable market. With government incentives and massive demand, affordable housing offers volume opportunities. If we were CEOs, we'd create a separate affordable brand—maintaining Godrej premium positioning while capturing volume growth. The dual-brand strategy, successful in automobiles and hotels, could transform real estate market dynamics.

International Expansion Possibilities

Indian developers have historically failed internationally, but the diaspora creates unique opportunities. If we were CEOs, we'd explore selective international expansion—not competing with local developers but serving the global Indian community. Projects in Dubai, Singapore, and London, marketed to Indians seeking familiar brands, could create new growth vectors without local market risks.

Final Reflections on Building Trust-Based Businesses

The Godrej Properties story ultimately validates an old truth: in industries where trust is scarce, companies that deliver it command premiums. GPL didn't innovate on product—apartments are apartments. They innovated on reliability, transparency, and delivery. In markets plagued by information asymmetry and broken promises, simply doing what you say becomes revolutionary.

The transformation from locks to land, from family workshop to institutional developer, mirrors India's own evolution. Godrej Properties isn't just building homes; they're constructing the physical infrastructure of India's urban future. Whether they maintain strategic discipline during this transition from asset-light to asset-heavy, from growth to profitability, will determine if this becomes a case study in successful evolution or a cautionary tale of strategic drift.

The company stands at an inflection point. The easy growth from consolidation and trust arbitrage has been captured. The next phase requires operational excellence, technology adoption, and capital discipline—harder to achieve, easier to lose. The ₹60,000 crore question remains: Can Godrej Properties maintain its soul while scaling its operations?

For investors, customers, and competitors, Godrej Properties represents a bet on India's urban future. It's a wager that trust, sustainability, and execution excellence will matter more than land banks and financial engineering. In a sector where promises are broken more often than kept, that might be the most radical bet of all.

The locks that Ardeshir Godrej crafted in 1897 were guaranteed "unpickable." The real estate empire his descendants built carries the same promise: unbreakable trust in an industry built on broken promises. Whether that trust survives the transition from entrepreneur to institution, from asset-light to asset-heavy, from family to professional, will determine if Godrej Properties truly builds India's real estate future—or merely participates in its present.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube