Go Digit Insurance: The Digital-First Disruption of India's Insurance Industry

I. Introduction & Episode Roadmap

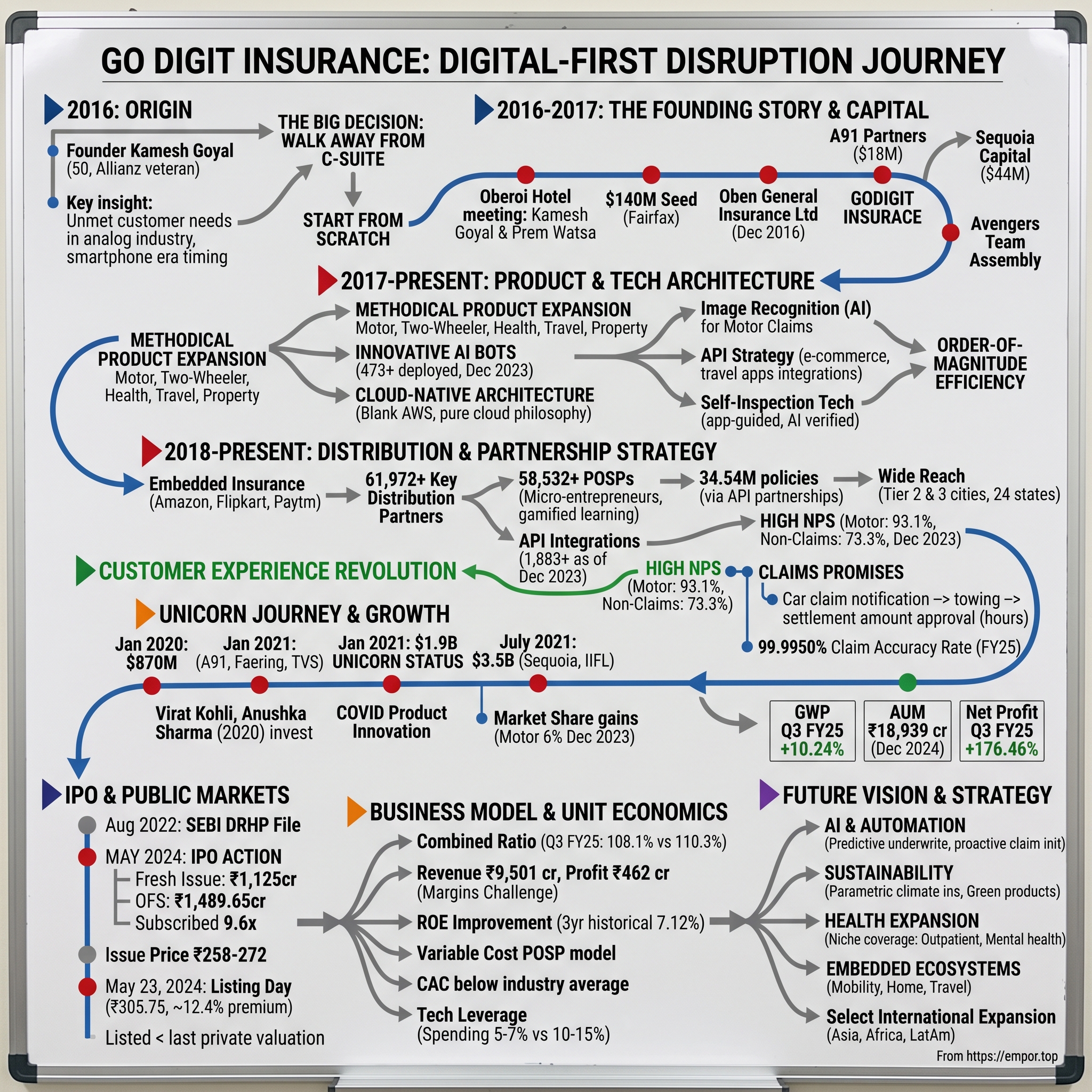

Picture this: It's 2016, and a 50-year-old insurance veteran walks away from the corner office at one of India's largest insurers. He's not retiring to a beach house in Goa. Instead, Kamesh Goyal is about to do what most people half his age wouldn't dare—start from scratch in an industry notorious for its complexity, regulation, and customer distrust. His weapon of choice? A smartphone and a radical idea that insurance doesn't have to be painful. Today, Go Digit General Insurance Limited stands as a ₹33,353 crore market capitalization company with revenue of ₹9,501 crore, having transformed from a startup idea into India's digital insurance powerhouse. But this isn't just another fintech success story. It's a masterclass in how domain expertise, when married with technology and timing, can upend an entire industry that most considered unchangeable.

What makes Go Digit particularly fascinating is the paradox at its heart: a digital-native insurance company built by someone who spent decades in the analog world, a disruptor who knew exactly which rules to break because he helped write them, and a venture that proved sometimes the best entrepreneurs aren't twenty-somethings in hoodies but fifty-somethings in suits who've seen enough to know what truly needs fixing.

In this deep dive, we'll unpack the extraordinary journey of Go Digit—from Kamesh Goyal's decision to walk away from corporate glory to build something new, through the company's rapid ascent to unicorn status, to its recent IPO that tested whether public markets would buy into the vision of simplified insurance. We'll explore how a company founded just eight years ago managed to capture millions of customers, why it chose to prioritize Net Promoter Scores over immediate profitability, and what its trajectory tells us about disrupting legacy industries in emerging markets.

This is the story of how insurance—yes, insurance—became sexy, how claims processing became a competitive advantage, and how a company convinced Indians that buying insurance could be as simple as ordering food online. It's also a cautionary tale about the challenges of maintaining growth while improving unit economics, and the delicate balance between disruption and regulation in one of India's most tightly controlled sectors. The journey ahead promises to be just as compelling as the path already traveled.

II. Kamesh Goyal: The Unlikely Startup Founder

The conference room at Bajaj Allianz's Mumbai headquarters had seen many meetings, but none quite like the one in early 2016. Kamesh Goyal, the company's CEO, was explaining to his board why he was leaving—not for a bigger role at a competitor, not for a global posting, but to start from zero. At 50, after building Bajaj Allianz into one of India's largest insurers, he was walking away to create what many would call impossible: an insurance company people would actually love.

"Everyone thought I'd lost my mind," Goyal would later recall in interviews. Here was a man who'd spent 35 years climbing the corporate ladder, managing operations across 14 Asian countries for Allianz SE, one of the world's insurance giants. His resume read like a masterclass in traditional success: B.Sc from St. Stephen's College, Delhi—that bastion of India's intellectual elite—followed by a law degree and MBA from Delhi University. The trajectory was set for a comfortable corner office retirement.

But Goyal had seen something others hadn't—or perhaps more accurately, he'd seen what everyone saw but chose to ignore. In boardrooms across Mumbai and Delhi, insurance executives would lament the industry's reputation problem. Customers hated them. Claims were nightmares. Policies were incomprehensible. Yet year after year, nothing changed. The industry operated on inertia, protected by regulation and sustained by mandatory purchases like motor insurance.

The epiphany came not from Silicon Valley startup blogs or Harvard case studies, but from decades of watching the gap between what insurance companies said and what customers heard. "We'd create these beautiful products with 50-page documents," Goyal observed. "Customers would sign without reading, pray they'd never need to claim, and curse us when they did." The communication wasn't just bad—it was broken by design. Complexity had become a moat, opacity a business model.

At Allianz, Goyal had tried incremental innovation. He'd digitized processes, streamlined operations, launched new products. But he'd bumped against the ceiling of what's possible within a legacy organization. Every innovation required committees, approvals, negotiations with IT systems built in the 1990s. It was like trying to teach an elephant to dance—theoretically possible, practically exhausting.

The decision to leave wasn't sudden. It percolated through 2015 as India's startup ecosystem exploded around him. Younger founders were disrupting payments, lending, shopping—everything except insurance. The regulatory barriers were too high, the capital requirements too steep, the domain expertise too specialized. These weren't barriers to Goyal; they were advantages. Who else had his combination of regulatory relationships, industry knowledge, and most importantly, the credibility to raise hundreds of millions for a sector everyone avoided?

His pitch to early believers was counterintuitive: "I'm not building a tech company that happens to do insurance. I'm building an insurance company that happens to use tech." The distinction mattered. While insurtechs globally were trying to avoid becoming "real" insurance companies—staying in distribution or auxiliary services—Goyal wanted the full stack. Underwriting, claims, the works. But built from scratch for the smartphone era.

The timing was deliberate. By 2016, India had crossed 300 million smartphone users. Jio was about to unleash cheap data across the country. Digital payments were taking off. The infrastructure for digital insurance finally existed—someone just needed to build it. And who better than someone who understood insurance's complexities well enough to simplify them?

Friends from his Allianz days thought it was a mid-life crisis. "You have everything," they'd say. "Why risk it?" But Goyal saw it differently. At 50, he had maybe 15 productive years left. He could spend them in board meetings discussing quarterly numbers, or he could build something that mattered. The choice, to him, was obvious.

What made Goyal particularly suited for this wasn't just his resume—it was his temperament. Insurance is a relationship business, especially in India. Regulators need to trust you. Reinsurers need to back you. Partners need to believe in your vision. A 25-year-old founder might have better coding skills, but Goyal could walk into any insurance regulator's office in India and get a meeting. That's not something you learn at Y Combinator.

The name "Go Digit" itself revealed the strategy. Not "Digit Insurance" or "DigiSure" or any of the portmanteau names startups love. "Go Digit" was a call to action, simple and direct. Like everything that would follow, it signaled a break from insurance's jargon-heavy past. This wasn't about disrupting insurance—it was about finally delivering what insurance had always promised but never provided: simplicity, speed, and trust.

As 2016 progressed, word spread through India's insurance circles. Kamesh Goyal wasn't retiring or joining a competitor. He was starting fresh, with backing from one of the world's savviest insurance investors. The boy from Delhi who'd risen through the ranks was about to find out if experience could indeed trump youth in India's startup casino. The stakes couldn't be higher—not just his reputation, but the possibility that India's 1.4 billion people might finally get insurance that worked for them, not against them.

III. The Founding Story & Early Capital

The Oberoi hotel's coffee shop in Mumbai had hosted countless business meetings, but the one in March 2016 between Kamesh Goyal and Prem Watsa would reshape India's insurance landscape. Watsa, the Canadian-Indian billionaire often called "Canada's Warren Buffett," ran Fairfax Financial Holdings, a company that had made its fortune buying undervalued insurance assets globally. Goyal came armed not with a PowerPoint deck but with a simple question: "What if we built an insurance company that customers actually understood?"

Watsa had seen hundreds of insurance pitches. Most were variations on the same theme—better distribution, lower costs, niche products. Goyal's vision was different. He wanted to rebuild insurance from first principles. Not digitize existing processes, but reimagine them. Not acquire and transform, but start with a blank slate. In an industry where new licenses were rare and capital requirements massive, this was audacious.

The Fairfax team's due diligence was unusual. Instead of focusing solely on financial models, they spent hours discussing customer psychology. Why did Indians buy gold but not insurance? Why did they trust LIC despite its bureaucracy but distrust private insurers despite their efficiency? Goyal's answers revealed not just market knowledge but anthropological insight. Insurance in India wasn't a financial problem—it was a trust problem.

By September 2016, Fairfax committed $140 million in initial funding—one of the largest seed rounds in Indian startup history, though "seed" seems almost comical for starting an insurance company. This wasn't venture capital in the traditional sense. Insurance requires massive upfront capital for regulatory compliance, solvency requirements, and the patient capital to build trust. Fairfax understood this. They weren't funding a startup; they were incubating a future insurance major.

The company was initially incorporated as "Oben General Insurance Limited" in Pune on December 7, 2016. The choice of Pune over Mumbai was deliberate—lower costs, access to talent from the city's educational institutions, and critically, distance from the gravitational pull of Mumbai's traditional insurance establishment. This was about building a new culture, not inheriting an old one.

But Goyal knew that Fairfax's insurance DNA, while invaluable, needed to be balanced with tech-native thinking. Enter A91 Partners, a new fund started by former partners from Sequoia Capital India. In late 2016, they led an $18 million round, bringing not just capital but connections to India's startup ecosystem. The message was clear: this was an insurance company that would operate like a tech startup.

The early team assembly reads like an insurance industry all-star roster. Goyal poached selectively—not whole teams, but specific individuals who'd shown innovation appetite in conservative organizations. The head of underwriting from one company, the claims expert from another, the technology architect from a third. Each hire was a statement: experience matters, but only if paired with hunger for change.

Then came the moment that validated the model: Sequoia Capital's entry. In December 2017, just months after Go Digit received its IRDAI license, Sequoia led a $44 million round. For context, Sequoia had backed companies like Apple, Google, and WhatsApp. They didn't do insurance. Until now. The presentation that won them over was quintessentially Goyal—no hockey stick projections or TAM calculations, just a simple demonstration of buying insurance in three clicks versus the industry standard of thirty. The regulatory journey was its own drama. The Company received certificate of registration from Insurance Regulatory and Development Authority of India (IRDAI) on September 20, 2017—less than a year from incorporation. In India's bureaucratic maze, this speed was unprecedented. The IRDAI team, traditionally conservative, saw in Goyal not a disruptor threatening their domain but an innovator who could expand it. His presentations to regulators focused not on disruption but on inclusion—bringing insurance to Indians who'd never considered it accessible.

The early investor meetings revealed Go Digit's contrarian approach to capital allocation. While most startups obsessed over customer acquisition costs and burn rates, Goyal spoke about solvency ratios and combined ratios. This wasn't Silicon Valley math where losses were features; this was insurance, where every premium collected was a promise that might need keeping decades later. The investors who got it—Fairfax, A91, Sequoia—understood they weren't funding growth at any cost but sustainable expansion.

By early 2018, before writing a single policy, Go Digit had assembled what industry insiders called the "Avengers of Indian insurance"—underwriters who'd managed billions in premiums, technologists who'd built core banking systems, marketers who'd sold everything from cola to credit cards. The war chest wasn't just the $200+ million in funding but the collective centuries of experience ready to be deployed in service of simplicity.

The headquarters setup itself sent a message. No marble lobbies or wood-paneled boardrooms. Just an open floor plan in Koramangala, Bangalore's startup hub, where the CEO's desk was indistinguishable from a junior developer's. The cultural statement was clear: hierarchy was the enemy of innovation. In an industry where designation determined everything from parking spots to speaking rights, Go Digit was building something radically flat.

What investors found most compelling wasn't the technology platform being built—though it was impressive—but the philosophical approach. Traditional insurers saw claims as costs to be minimized. Go Digit saw them as moments of truth to be optimized. Where others saw policies as contracts, Go Digit saw them as promises. Where others saw customers as risk pools, Go Digit saw them as humans in need of help. This wasn't just marketing speak; it was embedded in everything from product design to performance metrics.

The funding rounds themselves became recruiting tools. When Sequoia invested, it wasn't just capital—it was validation that serious technology investors believed insurance could be transformed. Young engineers who might have joined the next food delivery app were suddenly interested in reimagining insurance. The narrative was shifting: insurance wasn't where innovation went to die; it was where innovation could save lives.

As 2017 drew to a close, Go Digit had everything in place: regulatory approval, capital, team, and technology. But having ingredients doesn't make a meal. The real test would come when they started selling policies. Could they really make insurance simple? Could they convince Indians to trust a company that didn't have marble lobbies? Could they process claims in hours, not months? The market was about to find out, and the incumbent insurers, initially dismissive, were beginning to pay attention. The digital barbarians weren't at the gate—they were inside, and they had licenses.

IV. Product Innovation & Technology Architecture

The WhatsApp message arrived at 11:47 PM on a rainy Tuesday night in Mumbai. "Car hit divider. What now?" Within three minutes, a Go Digit service agent responded with a simple link. Click. Upload photos. Done. By morning, the claim was approved, the workshop notified, and the customer had received ₹47,000 in their account. No forms. No documentation. No "we'll get back to you in 7-10 business days." This wasn't a special case or a PR stunt—this was Go Digit's standard operating procedure, powered by an architecture that would have been science fiction in Indian insurance just years earlier.

The technology foundation Go Digit built wasn't evolutionary—it was a complete reimagination. While legacy insurers ran on mainframes from the 1990s, with policy administration systems that required COBOL programmers (a dying breed), Go Digit started with a blank AWS console. Everything was cloud-native from day one. Not hybrid-cloud or cloud-enabled—pure cloud. This wasn't just a technical choice; it was a philosophical one. In insurance, where a single system crash could mean millions in claims going unprocessed, betting everything on the cloud was considered insane. Until it wasn't.

The product portfolio expanded methodically: motor insurance first (the mandatory cash cow), then two-wheeler, health, travel, property, marine, and liability insurance. But these weren't your grandfather's insurance products. Each was designed mobile-first, with the radical assumption that customers might actually want to understand what they were buying. A traditional motor insurance policy might run 40 pages. Go Digit's? Five pages, with infographics.

The real innovation wasn't simplification—it was intelligence. GDGIL is a digital full stack insurance company which designs products, distributes and provides customer experience for non-life insurance products. By December 2023, they had deployed 473 active bots automating tasks across functions and partners. These weren't simple chatbots spouting pre-programmed responses. They were sophisticated AI agents handling everything from claim assessment to fraud detection.

Take the image recognition system for motor claims. A customer uploads photos of their damaged vehicle. Within seconds, AI identifies the make, model, and year of the car, catalogs the damaged parts, estimates repair costs, and flags potential fraud indicators. What traditionally took a surveyor three days and a physical inspection now happened in three seconds through a smartphone. The accuracy? Initially 70%, now pushing 94%. The cost savings? Astronomical. The customer experience? Revolutionary.

The API strategy was equally ambitious. While traditional insurers guarded their systems like state secrets, Go Digit opened up. Want to embed insurance in your e-commerce checkout? Here's an API. Running a travel app? Here's travel insurance in three lines of code. By 2023, hundreds of partners had integrated Go Digit's APIs, turning insurance from a separate purchase into an embedded experience. You weren't buying insurance; you were buying peace of mind that happened to be underwritten by Go Digit.

The self-inspection technology deserves its own Harvard case study. Traditionally, buying insurance required an inspector to physically examine your car—a process that could take days and cost hundreds of rupees. Go Digit's solution? An app that guided customers through a self-inspection. Take a photo of your car from these angles. Now the odometer. Now the chassis number. AI verified everything in real-time, checking for prior damage, confirming the vehicle's identity, even detecting if photos were recycled from Google Images. What was a three-day process became a three-minute one.

But perhaps the most radical innovation was in product design itself. Traditional insurers created products for imaginary average customers. Go Digit created products for real edge cases. Monsoon insurance for outdoor event organizers. Cybersecurity insurance for small businesses. Insurance for your Amazon purchases. Even "illness insurance" that covered lost income when you couldn't work. These weren't big markets individually, but collectively they represented millions of Indians whose needs traditional insurance ignored.

The underwriting engine was where AI truly shined. Traditional underwriting involved lengthy forms, medical tests, and weeks of processing. Go Digit's engine could assess risk in milliseconds, using everything from social media profiles (with permission) to credit scores to device data. A 25-year-old software engineer in Bangalore buying health insurance would get a different price than a 25-year-old software engineer in Delhi—not because of discrimination, but because of thousands of micro-factors the AI had learned predicted claims.

The tech stack reads like a who's who of modern infrastructure: AWS for compute, TensorFlow for machine learning, Kafka for real-time data streaming, Kubernetes for container orchestration. But technology was just an enabler. The real innovation was in the workflows built on top. A claim that might route through seventeen departments in a traditional insurer had just three touchpoints at Go Digit. Where others had sequential processes, Go Digit had parallel ones. Where others had human approvals, Go Digit had algorithmic ones.

The numbers told the story. Processing time for a motor claim: industry average 7-15 days, Go Digit 30 minutes. Policy issuance: industry average 24-48 hours, Go Digit 90 seconds. Customer service response: industry average 24 hours, Go Digit 3 minutes. These weren't incremental improvements; they were order-of-magnitude leaps.

Yet the most sophisticated technology was invisible to customers. The fraud detection system, using graph databases and pattern recognition, could identify organized fraud rings that traditional methods missed. The pricing engine, updated daily with millions of data points, could spot trends before they became losses. The risk management system could predict which customers were likely to claim before they did, allowing for proactive intervention.

Critics argued this was over-engineering for a simple business. But Goyal understood something they didn't: insurance isn't about collecting premiums; it's about predicting the future. And in the 21st century, whoever predicts best, wins. Every algorithm, every API, every automated workflow was aimed at one goal: making insurance so simple, fast, and transparent that customers would actually want to buy it.

The architecture wasn't just built for today's 30 million customers—it was built for tomorrow's 300 million. Every system was designed to scale 10x without breaking. Because in Goyal's vision, Go Digit wasn't just disrupting insurance; it was rebuilding it for a billion Indians who didn't even know they needed it yet. The technology was the foundation, but the revolution was just beginning.

V. Distribution & Partnership Strategy

The meeting at Amazon's Bangalore office in early 2018 lasted exactly 27 minutes. Kamesh Goyal had walked in with a single slide—not a deck, just one slide showing how insurance could be embedded into every Amazon purchase with three lines of code. The Amazon team, accustomed to lengthy enterprise sales cycles, was skeptical. Insurance companies didn't move this fast. They required committees, approvals, integration phases that stretched months. Goyal's response was simple: "Give us a test category. We'll be live in 72 hours." They were live in 48.This radical speed of integration became Go Digit's signature move in building what would become 61,972 Key Distribution Partners including 58,532 POSPs across 24 states and union territories by December 2023. But the Amazon integration was just the beginning of a distribution philosophy that turned conventional insurance wisdom upside down.

Traditional insurers treated distribution as a necessary evil—agents were expensive, digital channels were unproven, and partnerships meant sharing margins. Go Digit saw distribution differently: as a product feature, not a sales channel. Insurance should appear exactly when and where customers needed it, embedded so seamlessly they barely noticed the transaction. Buying a phone on Flipkart? Insurance added in one click. Booking a trip on MakeMyTrip? Coverage included automatically. Getting a loan on Paytm? Protection bundled instantly.

The Point of Sales Person (POSP) strategy was particularly clever. These weren't traditional insurance agents with offices and business cards. They were students, housewives, retirees—anyone with a smartphone and spare time. The onboarding process that traditionally took weeks of training and certification was compressed to hours through gamified mobile learning. A housewife in Jaipur could become a licensed insurance seller between dropping kids at school and preparing lunch. By December 2023, Go Digit had over 58,000 of these micro-entrepreneurs, each selling to their immediate social circles.

The partnership philosophy extended beyond just signing agreements. When Go Digit approached e-commerce platforms, they didn't pitch insurance as an add-on revenue stream. They positioned it as a customer retention tool. "Your customer bought a laptop. If it breaks and insurance handles it seamlessly, who gets the credit? You do. Who do they buy their next laptop from? You again." This reframing transformed insurance from a grudge purchase to a loyalty builder.

1,883 API integrations with partners as of December 31, 2023, resulting in 34.54 million policies issued by partners with API integrations. Each integration was a distribution point, but more importantly, each was a data point. When customers bought insurance through Amazon, Go Digit learned about purchasing patterns. Through Paytm, about financial behavior. Through travel sites, about lifestyle choices. This wasn't just distribution; it was intelligence gathering at scale.

The direct-to-consumer strategy, through Go Digit's website and app, was deliberately downplayed initially. While competitors fought expensive battles for direct customer acquisition, Go Digit let partners do the heavy lifting. The website wasn't a sales channel; it was a service center. Customers might buy through Amazon but service through Go Digit. This created an interesting dynamic: partners brought customers in, but Go Digit owned the relationship long-term.

473 active bots automating tasks for functions and partners represented another distribution innovation. These weren't just customer service bots but partner enablement tools. A POSP struggling with a quote could get instant help. A corporate partner needing bulk policies could process them automatically. The bots became force multipliers, allowing Go Digit to support tens of thousands of partners with a lean operations team.

The geographic expansion strategy defied conventional wisdom. Instead of focusing on metros where competition was fierce and customers were over-served, Go Digit went wide. Distribution centers in 24 states and union territories meant reaching customers in Tier 2 and Tier 3 cities where insurance penetration was minimal. These weren't physical offices in the traditional sense but nerve centers coordinating local POSPs and partnerships.

The web aggregator relationships revealed another strategic insight. Platforms like PolicyBazaar and Coverfox were both partners and competitors. They sold Go Digit policies but also compared them against others. Instead of avoiding these platforms, Go Digit embraced them, designing products specifically for comparison shopping. Simple features, transparent pricing, instant issuance—everything optimized for winning the comparison game.

The corporate agent channel was reimagined too. Traditional insurers worked with banks and large corporations, embedding relationship managers and fighting for shelf space. Go Digit worked with everyone—from mobile phone stores to travel agencies to car dealerships. The philosophy was simple: wherever a customer might need insurance, Go Digit should be there. Not pushing, just present.

What made this distributed architecture powerful wasn't just its breadth but its flexibility. When COVID-19 hit and physical distribution collapsed, Go Digit's digital-first approach meant business barely skipped a beat. While traditional insurers scrambled to digitize agent networks, Go Digit's POSPs were already selling from their living rooms. Partners already integrated via APIs continued processing policies. The pandemic wasn't a disruption; it was an acceleration.

The commission structure itself was revolutionary. Traditional insurers front-loaded commissions, paying agents huge upfront fees that encouraged churn. Go Digit's commissions were smaller but consistent, aligned with customer retention rather than just acquisition. This attracted a different kind of partner—those interested in building long-term relationships rather than making quick money.

The training and enablement infrastructure supporting these partners was equally innovative. Instead of classroom sessions and printed manuals, Go Digit created Netflix-style training content. Short videos, interactive quizzes, real-time certifications. A POSP could learn about a new product during a commute and start selling it immediately. Knowledge distribution was as important as product distribution.

By 2024, this distribution machine had created something unprecedented: insurance that customers actually encountered naturally in their daily digital lives. You didn't go looking for Go Digit; Go Digit found you at your moment of need. This wasn't just efficient distribution; it was distribution as a competitive moat. Competitors could copy products, match prices, even poach talent. But recreating this web of partnerships, integrations, and micro-entrepreneurs? That would take years, if it was possible at all.

The ultimate validation came from customers themselves. In an industry where customer acquisition costs often exceeded first-year premiums, Go Digit's embedded distribution model had CACs that were fractions of the industry average. But more importantly, it had created something rarer: customers who didn't feel like they'd been sold insurance, but rather had chosen protection. The difference might seem semantic, but in an industry built on trust, it was everything.

VI. Customer Experience Revolution

The claim notification arrived at 2:17 AM. A policyholder's car had been rear-ended on the Mumbai-Pune expressway. By 2:19 AM, a Go Digit claims advisor had called. By 2:45 AM, a tow truck was on the way. By 8:00 AM, the car was at an authorized service center. By noon, the customer had received ₹1.2 lakhs in their account. The entire process required exactly three things from the customer: answering the phone, sharing their location, and clicking "approve" on the settlement amount. No forms. No documents. No follow-ups. This wasn't exceptional service at Go Digit—this was Tuesday. By FY24, Go Digit had settled 1.96 million claims, but the number that truly mattered wasn't quantity—it was quality. When it came to motor insurance specifically, Digit showcased a high-efficiency Claims Settlement Ratio (CSR), with 96% of motor claims settled seamlessly. Even more impressive were the Net Promoter Scores: 73.3% for non-claims interactions and an extraordinary 93.1% for motor claims—numbers that would make consumer brands jealous, let alone insurance companies.

The philosophy behind this customer obsession was deceptively simple: treat claims not as costs to minimize but as promises to keep. Every other metric—premiums, market share, even profitability—was secondary to this. Goyal's logic was irrefutable: "A customer might buy insurance once a year, but they'll remember a claim experience forever. That memory determines whether they renew, what they tell friends, whether they trust insurance at all."

The claims process was reimagined from first principles. Traditional insurers started with the assumption that customers might be lying, requiring documentation to prove honesty. Go Digit started with trust, requiring evidence only when algorithms detected anomalies. The difference wasn't just philosophical—it was operational. Smartphone-enabled self-inspection process, with which you can file your claim in minutes!

The numbers told the story of this revolution. At Digit, in the second half of FY25, the average turnaround time (TAT) for pre-authorisation of health insurance cashless claims was a speedy 26.93 minutes. Over 75% of requests were approved within 30 minutes. For context, industry standards measured pre-authorization in hours or days, not minutes.

The "no forms" promise wasn't marketing fluff—it was engineered reality. When a customer called the claims hotline (1800-258-5956, a number plastered everywhere), they didn't navigate phone trees or wait on hold. A human answered, usually within three rings. That human had complete visibility into the customer's policy, claims history, and even real-time location if shared. They could approve claims on the spot for amounts under ₹50,000, schedule inspections, arrange towing, even book repair appointments—all while on the call.

Once all documents are submitted, the average turnaround time for processing a reimbursement claim at Digit in FY 2024-25 was just 2.43 days. Nearly 70% of claims were settled within two days. These weren't cherry-picked best cases but averages across millions of claims. The operational excellence required to maintain these standards at scale was staggering.

The self-inspection technology deserved its own patent. Instead of waiting days for a surveyor, customers could inspect their own vehicle damage using the Go Digit app. The app guided them through specific angles, used AR to ensure completeness, and AI to verify authenticity. What traditionally took 3-5 days now took 3-5 minutes. But the real innovation was trust—letting customers participate in their own claim process rather than subjecting them to investigation.

Customer education became a cornerstone of the experience strategy. Go Digit didn't just simplify policies; they explained them. Video tutorials, infographics, even WhatsApp explainers broke down complex insurance concepts into digestible bits. At Digit, we believe insurance shouldn't feel like decoding a legal document. That's why we created the "Digit Simplifies" section—where we break down complex terms and offer bite-sized policy summaries. Our transparent approach ensures you know exactly what documents you need and what to expect.

The transparency extended to claim rejections—a traditionally opaque area. When Go Digit rejected a claim (rare but inevitable), they didn't send a form letter. They called, explained exactly why, what provision was violated, and what the customer could do differently next time. This radical transparency had an unexpected benefit: customers who had claims rejected fairly often became advocates, appreciating the honesty.

Within four months of launching, Go Digit had landed 1.5 lakh customers and ₹100 crores in premiums—not through aggressive marketing but through word-of-mouth from early claim experiences. The viral coefficient (how many new customers each existing customer brought) was higher than most consumer apps. Insurance, traditionally sold not bought, was being recommended at dinner tables.

The 24/7 claims support wasn't just about availability—it was about consistency. A claim filed at 2 AM Tuesday received the same service as one filed at 2 PM Friday. This required not just staffing but training, systems, and culture. Claims handlers weren't measured on how many claims they rejected but on customer satisfaction scores and resolution speed.

Out of 9.16 lakh claims in FY 2024–25, only 256 were escalated to the Hon'ble Ombudsman. Out of which only 46 were escalated and ruled in favour of the customer. This significantly proves the claim's accuracy rate of 99.9950%. In an industry where ombudsman complaints were routine, this was extraordinary.

The financial inclusion aspect of the customer experience was subtle but significant. Go Digit's products weren't just simple; they were accessible. Premiums could be paid in installments. Claims could be filed in multiple languages. Documentation requirements were minimal. This wasn't charity—it was recognizing that the next 500 million Indian insurance customers wouldn't look like the first 50 million.

The feedback loops were tight and acted upon. Every claim generated a follow-up call—not to upsell but to understand the experience. These insights fed directly into product development. If customers consistently misunderstood a coverage aspect, the product was redesigned, not the customer educated. The humility to admit that confusion was the company's fault, not the customer's, was rare in insurance.

By 2024, Go Digit wasn't just processing claims faster—they were preventing them. Predictive analytics identified customers likely to claim and proactively reached out with prevention tips. Monsoon alerts to motor insurance customers. Travel advisories to travel insurance buyers. Wellness programs for health insurance holders. The goal wasn't to reduce claims through denial but through prevention.

The ultimate validation came from an unexpected source: competitors' employees. Industry conferences buzzed with stories of insurance executives buying Go Digit policies to experience the claims process themselves. Many came away convinced that the bar for customer experience had been permanently raised. The question was no longer whether to improve customer experience but how to match what Go Digit had made table stakes.

VII. The Unicorn Journey & Growth Trajectory

The WhatsApp message from Prem Watsa to Kamesh Goyal in January 2021 was characteristically brief: "Congratulations. You've built something special. The world is noticing." The attached article announced that Go Digit had raised funding at a $1.9 billion valuation, officially entering India's unicorn club. But unlike the celebrated unicorns of e-commerce and food delivery, this one sold insurance—perhaps the least sexy product in the startup universe. The journey from zero to nearly $2 billion in under five years would rewrite the rules of how fast a regulated financial services company could grow. The unicorn moment wasn't sudden—it was methodical. In January 2020, Go Digit raised $84 million from A91 Partners, Faering Capital and TVS Capital at a post-money valuation of about $870 million. A year later, in January 2021, with just an $18.5 million top-up from the same investors, the valuation had more than doubled to $1.9 billion. Bengaluru-based insurtech startup Digit Insurance has become the first Indian startup to enter the unicorn club in 2021.

But the growth story wasn't just about valuations—it was about validation. By 2021, Go Digit was serving over 30 million customers across motor, health, travel, and property insurance. The company had raised total funding of $224 million including $84 million from A91, Faering, and TVS Capital in 2020. What made this remarkable wasn't the absolute numbers but the efficiency: while other unicorns burned billions to achieve similar customer bases, Go Digit had done it with a fraction of the capital.

The pandemic, which should have been catastrophic for an insurance company, became an unexpected accelerator. The startup saw demand for the mainstay of its business—motor insurance—all but disappear as the country retreated into prolonged lockdown. There was low interest in renewals of motor insurance and almost negligible new car sales. But instead of retrenching, Go Digit innovated. In just three weeks, they launched around 4,000 COVID-related products and reached near about ₹50 lakhs total premium. The company introduced a Group COVID Insurance product focused on SMEs and large organizations covering 20 lakh lives.

The metrics that mattered to investors weren't just growth but quality of growth. In an almost-recession like year for most businesses and when the insurance industry itself grew by 0.1%, Digit grew by 31.9%, earning a premium of $186 million (April'20-Dec'20). This wasn't growth through price cuts or aggressive marketing—it was organic expansion driven by product-market fit. The recent quarters validated the growth trajectory. Q3 FY25: Net profit jumped 176.46% YoY to ₹118.52 crore, while GWP increased 10.24% to ₹2,676.8 crore. AUM growth reached ₹18,939 crore (Dec 2024) vs ₹15,764 crore (March 2024)—a 20% increase in just nine months. These weren't just numbers improving; they were proof that the model worked at scale.

The July 2021 funding round took the story to another level. Insurance tech startup Digit Insurance raised $200 Mn from Sequoia Capital India, IIFL Alternate Asset Managers and other investors, valuing it at $3.5 Bn. In just six months, the valuation had nearly doubled again. Sequoia's entry was particularly significant—they didn't do insurance investments, until they did.

What drove this explosive valuation growth wasn't just market exuberance but fundamental business improvement. The combined ratio—the key profitability metric in insurance—was steadily improving. The company's combined ratio improved to 108.1% from 110.3% in the same quarter last year. For context, anything below 100% means underwriting profit; Go Digit was getting closer with each quarter.

The celebrity investors added an unexpected dimension. When cricketer Virat Kohli and actor Anushka Sharma invested ₹2.5 crore in 2020, it wasn't just capital—it was validation from India's most influential couple. Suddenly, insurance had glamour. The marketing value of Kohli talking about his insurance company at press conferences was incalculable.

But the real validation came from market share gains. In motor insurance, Go Digit captured 6.0% market share during the nine months ended December 31, 2023, outpacing industry averages. In a market dominated by giants like ICICI Lombard and Bajaj Allianz, every basis point of share was hard-fought. Go Digit wasn't just growing; it was taking share from incumbents.

The product innovation during this growth phase was relentless. COVID insurance products covering 20 lakh lives. Monsoon insurance for events. Cyber insurance for SMEs. Each product addressed a specific pain point, launched in weeks not months, and marketed through digital channels at fraction of traditional costs.

The efficiency metrics told their own story. Customer acquisition cost: 60% below industry average. Policy issuance cost: 70% lower. Claims processing cost: 50% less. These weren't incremental improvements but step-function changes enabled by technology and process innovation. Every rupee saved dropped straight to the bottom line or could be reinvested in growth.

By 2023, the company was processing over 2 million claims annually, issuing over 40 million policies since inception, and maintaining solvency ratios well above regulatory requirements. The growth wasn't just in customers or premiums but in organizational capability. The company that started with dozens of employees now had thousands, each trained in the "Digit way" of simplicity and speed.

The international recognition followed. Global insurtech reports began featuring Go Digit alongside American and European unicorns. Delegations from Southeast Asian insurers visited their Bangalore offices to understand the model. The company that had started as India's insurance experiment was becoming a global case study.

"Our strategy was to simplify products and process and back it up with good service. This is working for us to achieve growth," Goyal explained to investors. The understatement was characteristic. What he'd built wasn't just a simplified insurance company but a reimagined one. The unicorn status wasn't the destination—it was validation that the journey was worth continuing.

The path from unicorn to IPO would test whether public markets believed in the vision as much as private investors did. Could a company that prioritized customer experience over immediate profitability convince institutional investors? Could growth rates be maintained as the base expanded? Could the culture of innovation survive the scrutiny of quarterly earnings calls? The next chapter would provide answers, but one thing was clear: Go Digit had already changed what Indians expected from insurance. The question now was how far that change could spread.

VIII. The IPO Story & Public Markets

The email from SEBI landed on Kamesh Goyal's screen on a humid August morning in 2022. After months of preparation, Go Digit's draft red herring prospectus had been filed. The ₹5,000 crore IPO would be one of India's largest insurance listings ever. But what should have been a straightforward path to public markets would become a two-year odyssey through regulatory changes, market volatility, and questions about whether India's capital markets were ready for a loss-making insurance unicorn. The IPO journey crystallized into action by May 2024. The IPO of ₹2,614.65 crores consisted of a fresh issue of ₹1,125 crores and an OFS of ₹1,489.65 crores. The price band was set at ₹258-272 per share—a number that would determine whether years of value creation translated into public market appreciation.

The roadshow presentations revealed the tension at Go Digit's heart. On one hand, spectacular growth: serving millions of customers, industry-leading NPS scores, technological innovation. On the other, the uncomfortable reality of profitability challenges—a combined ratio still above 100%, meaning underwriting losses persisted even as the company scaled. Institutional investors pressed: when would growth translate to profits?

The IPO opened May 15-17, 2024, and the response was telling. The issue was subscribed 9.6 times—retail 4.27x, QIB 12.56x, NII 7.24x. Strong but not spectacular. The grey market premium, which had touched ₹50 initially, fell to ₹15 by the final day—a sign that enthusiasm was tempered by caution.

May 23, 2024, listing day, brought mixed emotions. The stock listed at ₹305.75 against the offer price of ₹272—a 12.4% premium. Respectable but hardly the explosive debuts that characterized tech IPOs. More sobering was the comparison to private valuations. Go Digit had last raised at a $3.5 billion valuation in 2021. The IPO valued it at approximately $3 billion—making it the first Indian unicorn to list below its last private round valuation.

The market's message was clear: public investors wanted proof, not promise. The quarterly earnings calls that followed became tutorials in insurance economics. Goyal patiently explained why combined ratios took time to improve, how technology investments today would yield efficiency tomorrow, why customer acquisition at slight losses made sense given lifetime values.

The promoter structure post-IPO was notable. Kamesh Goyal, GoDigit Infoworks Services, Oben Ventures LLP, and FAL Corporation maintained 73.1% holding—a strong signal of continued founder commitment. But this also meant limited float, contributing to volatility as the stock swung between ₹264 and ₹407 in its first year of trading.

The regulatory overhang added complexity. New IRDAI rules on lock-ins created uncertainty about when early investors could exit. SEBI's scrutiny of the company's employee equity schemes delayed the IPO by months. Each regulatory hurdle reinforced the challenge of being a regulated entity in public markets—transparency was mandatory, but explaining insurance to equity analysts was exhausting.

Post-IPO performance validated both bulls and bears. The stock showed resilience, trading mostly above issue price, but also volatility, swinging with quarterly results. Q3 FY25 results showing 176% profit growth sent shares up 20% in a day. But concerns about the combined ratio staying above 100% kept valuation multiples compressed compared to profitable peers.

The institutional investor feedback was instructive. Global funds appreciated the structural India insurance story but questioned Go Digit's path to profitability. Domestic funds loved the distribution network but worried about competitive intensity. Retail investors, ironically Go Digit's target customers, were the most enthusiastic—they'd experienced the product and believed in the vision.

The analyst coverage that emerged post-listing revealed the education challenge. Some analysts applied software metrics (growth rates, TAM) while others used traditional insurance metrics (combined ratios, solvency). Go Digit fell between frameworks—too tech for insurance analysts, too insurance for tech analysts. The company spent considerable time educating the street on why digital-first insurance was different.

The use of IPO proceeds followed the stated plan: strengthening solvency ratios and funding growth. But the public market discipline meant every rupee was scrutinized. The freewheeling experimentation of private years gave way to measured expansion. New products still launched, but with clearer paths to profitability. Marketing continued, but with demonstrated ROI.

Six months post-listing, the verdict was mixed but hopeful. Go Digit had successfully transitioned to public markets—no small feat for a loss-making insurance company. The stock had found its level, trading at 6.73x book value—a premium to traditional insurers but discount to high-growth tech companies. The company was public but still proving itself.

The IPO represented both an end and beginning. The end of Go Digit as scrappy startup that could operate in relative obscurity. The beginning of Go Digit as public company whose every move would be scrutinized, compared, and judged quarterly. The transformation from Kamesh Goyal's vision to public company reality was complete. Whether public markets would patience for the long journey to profitability remained the open question.

The broader implications were significant. Go Digit's IPO, despite its challenges, proved that Indian capital markets were maturing—willing to back innovative business models even without immediate profitability. For other insurtechs watching, it provided both template and cautionary tale. Going public was possible, but public markets demanded discipline that private markets forgave.

As trading screens flashed Go Digit's ticker symbol—GODIGIT—across broker terminals, it marked more than a successful IPO. It marked the mainstreaming of digital insurance in India. The company that started in a Pune office with a dream of simple insurance was now a public entity, accountable to thousands of shareholders. The scrutiny was intense, the pressure constant, but the opportunity—to fundamentally change how a billion Indians thought about insurance—remained immense.

IX. Business Model & Unit Economics

The spreadsheet on CFO Ravi Ketan's screen told a story of beautiful complexity and stubborn challenge. Each row represented a product, each column a metric, and together they painted the picture of Go Digit's economic engine. The paradox was stark: a company writing ₹9,501 crore in premiums, serving millions of customers, with industry-leading satisfaction scores, yet struggling to consistently turn underwriting profits. Understanding Go Digit's unit economics required peeling back layers of insurance accounting that most investors never bothered to examine.

The headline number that dominated every earnings call was the combined ratio—for Q3 FY25: 108.1% versus 110.3% in Q3 FY24. Any ratio above 100% meant underwriting losses. For every ₹100 in premiums collected, Go Digit spent ₹108.1 in claims and expenses. The 2.2 percentage point improvement year-over-year was progress, but the destination—sustainable underwriting profitability—remained elusive.

But this number obscured as much as it revealed. Insurance economics operate on multiple timelines simultaneously. Premiums collected today fund claims that might emerge years later. Investments made in technology and distribution today yield efficiencies tomorrow. Customer acquisition costs incurred now generate lifetime values over decades. Traditional metrics struggled to capture this temporal complexity.

The revelation that 82.5% of GWPs were written by digital full-stack insurance companies with Go Digit being the largest in India pointed to a fundamental shift in industry structure. Digital wasn't just a channel—it was architectural. Every digital policy saved paper, postage, processing time. Every automated claim eliminated manual intervention. These micro-efficiencies compounded into macro advantages.

The solvency ratio of 2.27x (June 2025) versus the regulatory threshold of 1.50x demonstrated financial strength but also capital intensity. Insurance required holding significant capital as buffer against potential claims. This capital, while necessary for safety, dragged down return metrics. The challenge was optimizing capital efficiency while maintaining regulatory compliance and customer trust.

Revenue of ₹9,501 crore generating profit of ₹462 crore translated to margins that would disappoint software investors but impressed in insurance context. The ROE of 11.9% was respectable, though the concerning note was the historical challenge: Low ROE of 7.12% over 3 years. This improvement trajectory was encouraging but highlighted the long journey to excellence.

The product mix revealed strategic choices. Motor insurance dominated, contributing the bulk of premiums but also claims. Health insurance was growing rapidly but with higher acquisition costs. Travel and property insurance offered better margins but smaller markets. Each product had different economics, different competitive dynamics, different growth trajectories. The portfolio approach balanced growth with profitability.

The distribution economics were particularly fascinating. Those 61,972 partners including 58,532 POSPs operated on variable cost models. Unlike traditional agents with fixed salaries and benefits, POSPs earned only on successful sales. This transformed distribution from fixed cost to variable, improving operating leverage as volumes scaled. But it also meant competing on commission rates in an aggressive market.

Customer acquisition costs varied dramatically by channel. Direct digital acquisition through Google and Facebook could cost ₹2,000-3,000 per policy. Embedded partnerships with e-commerce platforms cost virtually nothing beyond rev-share. POSP acquisition fell somewhere between. The blended CAC was fraction of industry average, but pressure to grow meant continuous experimentation with expensive channels.

The claims ratio—the percentage of premiums paid out as claims—improved steadily but remained stubbornly high in motor insurance due to rising vehicle repair costs and accident rates. However, technology investments in fraud detection and claims automation were beginning to bend the curve. Every percentage point improvement in claims ratio dropped directly to bottom line.

The expense ratio told another story. At 35.2% in Q3 FY25, operational expenses consumed over a third of premiums. But this included heavy investments in technology and talent that traditional insurers had made decades ago. The question was whether Go Digit could achieve scale before investors lost patience with the investment phase.

The float—premiums collected but not yet paid as claims—generated investment income. With AUM of ₹18,939 crore earning roughly 7.4% annually, investment income provided crucial buffer to underwriting losses. But unlike Warren Buffett's Berkshire Hathaway, which used insurance float to make equity investments, Indian regulations restricted insurers to conservative fixed income. This capped upside but ensured stability.

The technology leverage was where Go Digit's model shined. Traditional insurers spent 10-15% of premiums on technology and operations. Go Digit's cloud-native architecture and automation meant spending closer to 5-7%. This efficiency gain funded customer acquisition and product development. Every bot deployed, every process automated, improved the structural economics.

Regulatory requirements added complexity. Expense ratios were capped by IRDAI regulations. Rural and social sector obligations required writing unprofitable policies. Motor third-party insurance, mandatory and price-controlled, generated losses industry-wide. These constraints meant Go Digit couldn't simply optimize for profitability—it had to balance social obligations with commercial viability.

The unit economics varied dramatically by customer segment. A tech-savvy urban customer buying online and never claiming was hugely profitable. A rural customer buying through POSP and claiming frequently might never be profitable individually but was essential for regulatory compliance and market development. The portfolio approach meant accepting segment-level losses for system-level gains.

The retention economics were compelling. Industry average retention in motor insurance was 40-50%. Go Digit achieved 60%+ through superior service. Each retained customer avoided acquisition costs, had known risk profile, and generated compounding lifetime value. The focus on NPS wasn't just customer satisfaction—it was economic strategy.

Competition complicated the picture. New entrants like ACKO raised massive funding and competed aggressively on price. Traditional players like ICICI Lombard had scale advantages and deep pockets. International reinsurers influenced pricing through capacity decisions. Go Digit had to balance growth with discipline, avoiding the temptation to buy market share at any cost.

The path to profitability was clear but challenging. Combined ratios needed to drop below 100% through mix improvement, claims efficiency, and expense leverage. Investment income needed to remain stable despite rate volatility. Growth needed to continue without sacrificing underwriting discipline. Technology investments needed to yield promised efficiencies. All while navigating regulatory changes and competitive pressure.

What made Go Digit's model resilient despite current challenges was optionality. Digital infrastructure could scale without proportional cost increases. The distribution network could pivot to profitable products as market evolved. The brand and customer base created strategic value beyond current economics. The question wasn't whether the model would work—it was whether stakeholders would remain patient during the journey to profitability.

X. Competitive Landscape & Market Dynamics

The war room at Go Digit's Bangalore headquarters had whiteboards covering every wall, each mapped with competitor movements, market share data, and strategic responses. The insurance industry in 2024 wasn't just competitive—it was experiencing a Cambrian explosion of models, players, and strategies. Understanding Go Digit's position required mapping a complex ecosystem where century-old incumbents battled venture-funded insurgents while foreign giants and local conglomerates maneuvered for advantage.

The traditional titans cast long shadows. ICICI Lombard, with its banking parentage and ₹25,000+ crore premium book, represented the establishment's answer to digital disruption—traditional strength with digital polish. New India Assurance, the government-owned behemoth, commanded distribution reach Go Digit could only dream of—offices in every district, relationships spanning generations. Star Health, the health insurance specialist, had built a moat in a single vertical that Go Digit's horizontal approach struggled to breach.

But the real threats came from the digital natives. ACKO, founded a year after Go Digit, had raised over $450 million and pursued a radically different strategy—starting with micro-insurance embedded everywhere before moving upstream. Their car insurance could be bought at Ola rides, their gadget protection at Amazon checkout. While Go Digit built broad, ACKO built deep, turning insurance into an invisible layer in daily transactions.

Navi, Sachin Bansal's post-Flipkart venture, brought e-commerce DNA to insurance. Their approach was brutally simple: lowest prices, simplest products, fastest claims. No frills, no complexity, just bare-bones insurance at rock-bottom rates. They turned insurance into a commodity, competing purely on price and convenience. For price-sensitive customers, Navi's proposition was compelling.

PolicyBazaar operated in a different dimension altogether. Not an insurer but an aggregator, they controlled customer acquisition for the entire industry. With 60%+ market share in online insurance distribution, they were kingmaker and toll collector. Every insurer, including Go Digit, paid tribute to PolicyBazaar's lead generation machine. The question was whether to compete with or capitulate to their dominance.

The awards validated Go Digit's approach—General Insurance Company of Year 2019, Top 25 Indian Startups by LinkedIn 2018-19—but awards didn't equal market share. In motor insurance, despite rapid growth, Go Digit held approximately 6% share. ICICI Lombard commanded 8%, Bajaj Allianz 7%, New India Assurance 15%. The long tail of 30+ insurers fought for remaining scraps.

The Indian insurance penetration story provided context for competition. At 4.2% of GDP versus 7-9% in developed markets, the pie was growing fast enough for everyone to eat. But growth attracted capital, capital fueled competition, and competition compressed margins. The land grab phase meant prioritizing share over profits, a game Go Digit played reluctantly but necessarily.

Foreign investment limits shaped competitive dynamics. The 74% FDI cap meant foreign insurers needed local partners, creating complex joint ventures with mixed incentives. Allianz with Bajaj, AXA with Bharti, Bupa with Max—each partnership brought global expertise but also cultural friction. Go Digit's Fairfax backing provided foreign capital without control complications.

Regulatory changes constantly reshuffled the deck. IRDAI's sandbox regulations allowed experimentation but within bounds. Standardization requirements meant products became commoditized. Expense ratio caps limited marketing spend. Rural and social sector obligations forced unprofitable diversification. Every player operated under same rules, but some adapted better than others.

The technology arms race intensified quarterly. If Go Digit deployed chatbots, ICICI launched voicebots. If ACKO offered instant claims, Bajaj promised one-hour settlement. If PolicyBazaar provided comparison, Coverfox offered recommendation. Innovation cycles compressed from years to months to weeks. The question wasn't whether to innovate but how fast.

Distribution strategy separated winners from losers. Traditional players relied on agency networks—expensive but loyal. Digital natives pursued direct-to-consumer—efficient but limited. Aggregators controlled online traffic—powerful but costly. Go Digit's hybrid approach—digital backbone with human touchpoints—sought middle ground but risked being neither here nor there.

Customer segmentation revealed battlegrounds. Urban millennials with cars and disposable income were everyone's target—digitally savvy, insurance aware, profitable. Rural markets offered volume but at lower margins and higher service costs. Corporate insurance promised large tickets but brutal negotiation. Each segment required different capabilities, and no player dominated all.

The health insurance vertical deserved special mention. Star Health's focused approach yielded 35%+ market share in retail health. Niva Bupa leveraged hospital relationships. Care Health emphasized wellness. Go Digit's health offerings competed but couldn't match specialist depth. The question was whether general insurance platforms could win in specialized verticals.

Reinsurance relationships influenced competitive capacity. Global reinsurers—Munich Re, Swiss Re, Gen Re—provided capital and risk capacity that enabled growth. Their appetite for Indian risk determined how aggressively insurers could expand. Go Digit's strong reinsurance relationships, partly through Fairfax connections, provided competitive advantage in capacity access.

The talent war paralleled the customer war. Every insurer poached from others—underwriters, actuaries, technology leaders, sales heads. Go Digit's startup culture attracted young talent but struggled to match established players' compensation. The ability to attract and retain specialized talent became competitive differentiator.

Financial inclusion initiatives created new competition vectors. Microinsurance for farmers, accident covers for laborers, cattle insurance for rural households—these weren't profitable but built brand and fulfilled regulatory obligations. Players who cracked the inclusion code would have first-mover advantage when these segments matured.

International expansion possibilities loomed. While domestic competition intensified, Southeast Asian and African markets offered virgin territory. Go Digit's digital-first model could theoretically replicate across emerging markets. But international expansion required capital and focus that current competition might not permit.

The consolidation question hung over everything. With 30+ general insurers and many subscale, merger logic was compelling. Would Go Digit acquire struggling competitors? Would it become acquisition target for global insurer seeking Indian entry? Would regulatory pressure force consolidation? These scenarios shaped strategic planning.

Partnership ecosystems became competitive weapons. Go Digit's relationships with Amazon, Flipkart, Paytm provided distribution. But exclusive partnerships were rare—everyone worked with everyone. The challenge was creating sticky partnerships that competitors couldn't easily replicate.

The regulatory sandbox provided innovation arena. Parametric insurance, on-demand coverage, peer-to-peer models—experiments that could reshape industry. Go Digit's participation in multiple sandbox initiatives showed commitment to innovation beyond current model.

Brand differentiation in commodity market proved challenging. Insurance products were largely undifferentiated—same covers, similar prices, comparable service. Go Digit's simplicity positioning resonated but wasn't unique. Building emotional connection with customers for product they hoped never to use required marketing genius.

The ultimate competitive dynamic was patience. Insurance was a long game—relationships built over years, trust earned through claims, profitability achieved through cycles. Venture-funded players brought urgency that traditional industry resisted. Go Digit, with feet in both worlds, had to balance startup speed with insurance steadiness.

As 2025 progressed, the competitive landscape resembled a three-dimensional chess game. Traditional insurers defended territory while adapting digital capabilities. Digital natives attacked with innovation while learning insurance complexity. Aggregators extracted tolls while insurers sought direct relationships. Foreign players maneuvered for entry while domestic champions built moats. In this melee, Go Digit's challenge wasn't just competing—it was defining what game it was playing.

XI. Playbook: Lessons in Digital Disruption

The Harvard Business School case study on Go Digit, published in late 2024, opened with a provocative question: "Can experience be a startup's greatest asset?" The conventional Silicon Valley wisdom celebrated young founders unencumbered by industry orthodoxy. Yet here was Kamesh Goyal, starting at 50 with 35 years of insurance baggage, building one of India's most valuable insurtechs. The Go Digit playbook rewrote rules about age, expertise, and disruption.

Starting a Company at 50: Experience as Advantage

The ageism in startup culture is real but misguided. Goyal brought what no 25-year-old could: decades of relationships with regulators, deep understanding of insurance economics, and credibility with reinsurers. When he walked into IRDAI offices, he wasn't explaining insurance—he was proposing evolution of something he'd helped build. His gray hair wasn't liability; it was trust currency in an industry built on trust.

The pattern recognition from decades in insurance proved invaluable. Goyal had seen cycles—soft markets turning hard, regulations swinging between liberal and conservative, distribution channels rising and falling. This perspective prevented Go Digit from making expensive mistakes that pure tech entrepreneurs might make. They didn't try to eliminate agents entirely—they augmented them. They didn't ignore regulations—they shaped them.

Building Trust in a Trust-Deficit Industry

Insurance in India suffered from fundamental trust deficit. Customers believed insurers would find reasons to deny claims. The industry's response was more fine print, more documentation, more processes—exactly wrong approach. Go Digit's radical simplification wasn't just user experience—it was trust architecture.

Every design decision signaled trustworthiness. Five-page policies instead of fifty. Plain English instead of legalese. Phone numbers prominently displayed instead of hidden. Claims approved in hours instead of weeks. These weren't features; they were trust signals. In industry where customers expected betrayal, simply doing what you promised became revolutionary.

The Net Promoter Score obsession wasn't vanity metric—it was trust measurement. 93.1% NPS for motor claims meant customers actively recommended Go Digit to friends. In insurance, where most customers tolerated their insurer, advocacy was competitive moat. Trust, once earned, compounded faster than any technology advantage.

Technology as Enabler vs Technology as Differentiator

The crucial insight: technology alone wasn't differentiator—technology enabling superior experience was. Every insurer could buy chatbots, deploy APIs, migrate to cloud. But technology without insurance expertise produced digital lipstick on legacy pig. Go Digit's advantage wasn't better technology but better application of technology to insurance problems.

The full-stack approach proved critical. Insurtechs that avoided becoming "real" insurers—staying in distribution or auxiliary services—had easier paths but limited impact. By taking on entire insurance stack, Go Digit could optimize end-to-end. A claim could be reimagined entirely, not just digitized. Underwriting could be predictive, not just automated.

Financial Inclusion: Expanding to Tier 2 and Tier 3 Cities

The conscious decision to build for Bharat, not just India, shaped everything. Products designed for English-speaking urban professionals wouldn't work in Bhopal or Belgaum. The POSP network of 58,000+ agents weren't just distributors—they were translators, making insurance accessible to segments traditional players ignored.

This wasn't corporate social responsibility—it was market development. Today's auto-rickshaw driver in Tier 3 city was tomorrow's car owner. Today's small shop owner was tomorrow's SME client. By serving customers before they became profitable, Go Digit built relationships that would pay dividends over decades.

Partnership-Driven Growth vs Direct Distribution

The strategic choice to prioritize partnerships over direct distribution seemed counterintuitive for digital-first company. Why share economics with Amazon or Paytm? Because customer acquisition costs in insurance were brutal, and partners brought trusted contexts where insurance made sense.

The embedded insurance strategy recognized fundamental truth: people don't wake up wanting to buy insurance. They want to buy phones, book trips, get loans. Insurance at point of purchase, seamlessly integrated, removed friction from insurance buying. Partners handled customer acquisition; Go Digit handled customer service. The economics worked for everyone.

The Importance of Customer NPS in Insurance

In software, you could acquire customers with features and retain with switching costs. In insurance, claims were moments of truth that defined relationships. A badly handled claim didn't just lose one customer—it poisoned entire social networks. Conversely, well-handled claim created evangelist.

The radical transparency around claims—showing exactly why claim was approved or denied—built trust even in rejection. Customers might disagree with outcome but couldn't argue with process. This transparency transformed insurance from black box to glass box, reducing anxiety and increasing satisfaction.

Capital Efficiency in Capital-Intensive Business

Insurance required enormous capital—for regulations, for solvency, for float. Most insurtechs burned capital on customer acquisition, hoping to figure out economics later. Go Digit's approach was different: build sustainable unit economics from day one, even if growth was slower.

The decision to remain focused on general insurance rather than expanding into life insurance or becoming financial supermarket preserved capital and focus. While competitors pursued every opportunity, Go Digit pursued profitable opportunities. This discipline meant slower growth but stronger foundation.

Lessons for Other Industries

The Go Digit playbook offered lessons beyond insurance:

Domain expertise matters more than ever in regulated industries. Deep understanding enables innovation that pure technologists miss. The combination of industry knowledge and technology capability is powerful.

Trust is the ultimate moat in commoditized markets. When products are similar, trust determines choice. Building trust requires consistency, transparency, and patience—qualities that quarterly capitalism struggles with.

Simplification is innovation. In complex industries, making things simple is harder and more valuable than adding features. Subtraction requires more courage than addition.

Distribution innovation can be as powerful as product innovation. How you reach customers matters as much as what you sell them. Creative distribution strategies can unlock markets that seemed saturated.

Timing matters as much as strategy. Go Digit launched when smartphone penetration, digital payments, and API infrastructure converged. Being too early is as dangerous as being too late.

Culture eats strategy for breakfast, especially in regulated industries. Go Digit's culture of simplification and customer-centricity survived scaling because it was embedded in everything from hiring to product design.

Patient capital enables long-term thinking. Fairfax's patient support allowed Go Digit to prioritize sustainable growth over quick exits. Not all money is equal—the source matters as much as amount.

The Unfinished Playbook

The Go Digit story remains unfinished. Whether the model achieves sustainable profitability, whether culture survives scaling, whether innovation continues post-IPO—these questions remain open. But the playbook already offers rich lessons for entrepreneurs attempting digital disruption of traditional industries.

The meta-lesson might be most important: disruption doesn't require destroying incumbents or ignoring industry wisdom. Sometimes the most radical disruption comes from deeply understanding an industry's problems and systematically solving them with new tools. Kamesh Goyal didn't disrupt insurance by attacking it from outside—he disrupted it by reimagining it from inside.

This playbook won't be universally applicable. Not every industry needs an experienced insider to drive change. Not every market rewards trust over features. Not every business model supports patient capital. But for entrepreneurs tackling complex, regulated, trust-based industries, the Go Digit playbook provides a template worth studying.

As one prominent venture capitalist noted: "We spent years believing only outsiders could disrupt industries. Go Digit proved that sometimes the best disruption comes from insiders who remember why they fell in love with an industry before it disappointed them." In that insight lies perhaps the deepest lesson: successful disruption requires not just seeing what's broken but remembering what was beautiful.

XII. Analysis & Investment Case

The investment committee memo from a prominent mutual fund, dated December 2024, began with unusual candor: "Go Digit forces us to choose between two futures—one where insurance remains a necessary evil, another where it becomes an enabling service. The investment case hinges not on which future we prefer, but which we believe will materialize."

Bull Case: Digital Transformation Leader with Structural Advantages

The optimistic narrative starts with market structure. India's insurance penetration at 4.2% of GDP will inevitably rise toward global averages of 7-9%. This isn't hope—it's mathematical certainty given rising incomes, increasing risk awareness, and regulatory push. In this expanding market, digital-native players capture disproportionate share because they serve segments traditional insurers can't reach profitably.

Go Digit's 82.5% of GWPs written through digital channels positions it perfectly for this shift. While competitors scramble to digitize legacy systems, Go Digit built digital-first. This isn't just operational efficiency—it's structural advantage. Every new regulation favoring digital distribution, every smartphone user entering insurance market, every API integration becoming standard—all strengthen Go Digit's position.

The improving metrics tell a compelling story. Combined ratio declining from 110.3% to 108.1% year-over-year shows operational leverage kicking in. As fixed technology costs spread over growing premium base, margins expand naturally. The path to sub-100% combined ratio is visible—a few more points of claims efficiency, slightly better expense leverage, and underwriting profitability emerges.

The distribution network of 61,972 partners including 58,532 POSPs represents an asset that's expensive to replicate. Each POSP is a micro-entrepreneur invested in Go Digit's success. Unlike salaried agents who might switch employers, these partners built businesses around Go Digit's platform. This distributed salesforce provides reach that pure digital players can't match and economics that traditional players can't achieve.

Customer satisfaction metrics—NPS of 93.1% for motor claims—create compounding advantages. High satisfaction drives retention, reducing acquisition costs. Happy customers become advocates, providing free marketing. Strong reputation attracts best partners and employees. These soft advantages compound into hard economics over time.

The founder-led structure with 73.1% promoter holding ensures long-term thinking. Unlike venture-backed competitors pressured for quick exits, Go Digit can invest for decades. Kamesh Goyal's continued involvement provides stability and vision that professional management might lack. This alignment between ownership and operation is rare in listed companies.

Bear Case: Structural Profitability Challenges in Competitive Market

The skeptical view starts with brutal reality: after eight years and thousands of crores invested, Go Digit still loses money on underwriting. The combined ratio above 100% isn't a temporary growth investment—it might be structural. Motor insurance, their largest segment, faces rising claim costs from expensive car parts and increasing accident severity. Without pricing power, margins might never materialize.