Godfrey Phillips India: The Marlboro Maker of India

I. Introduction & Cold Open

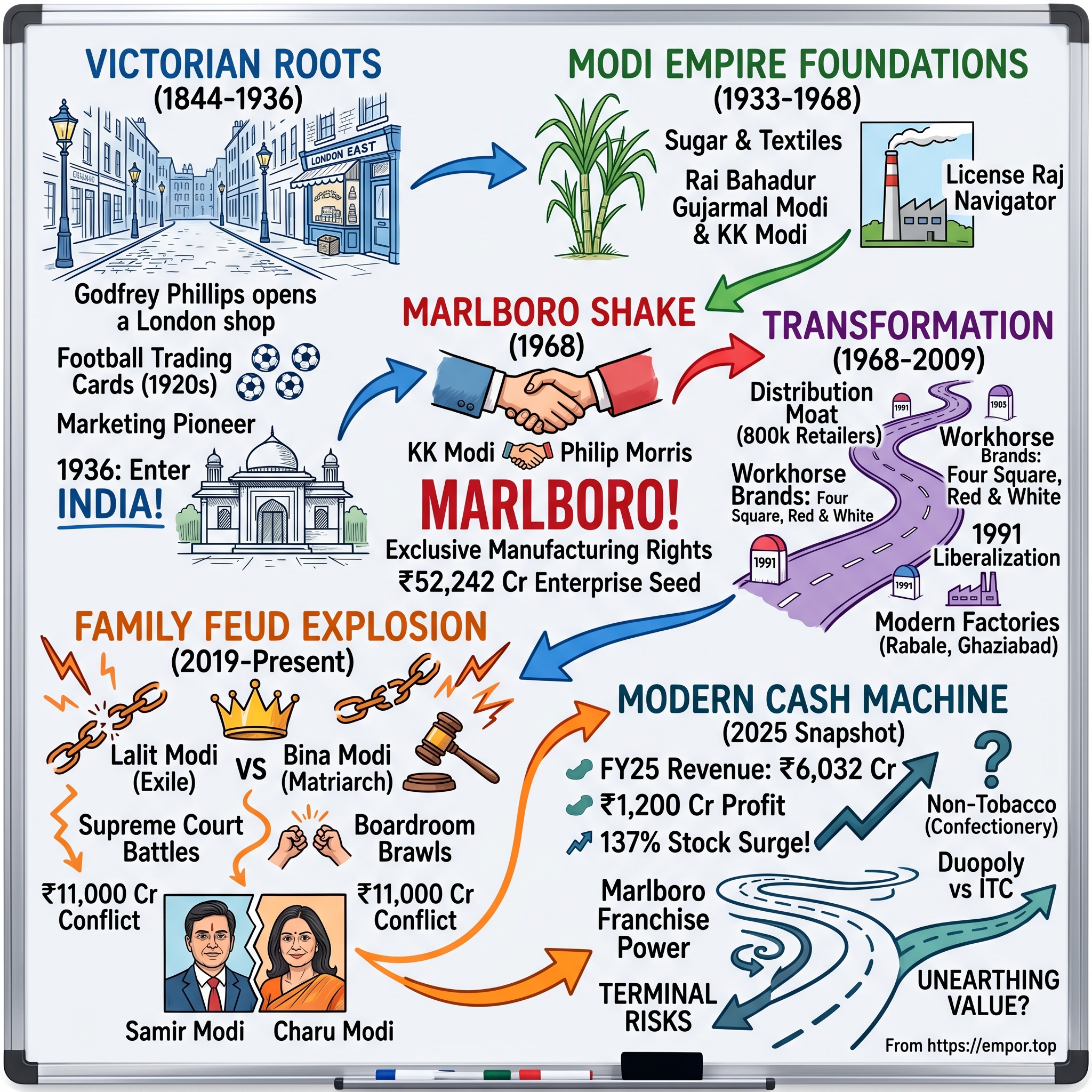

Picture this: In a nondescript boardroom in Delhi, 1968, two men from vastly different worlds shake hands over a deal that would reshape India's tobacco landscape. One is KK Modi, a shrewd Indian industrialist navigating the labyrinthine License Raj. The other represents Philip Morris, the American tobacco giant seeking a foothold in the world's second-most populous nation. Their handshake seals an arrangement that would bring Marlboro—the world's most valuable cigarette brand—to India, creating a partnership that would endure for over five decades and spawn a ₹52,242 crore enterprise.

Today, Godfrey Phillips India commands approximately 14% of India's domestic cigarette market, a David to ITC's Goliath. But this isn't just another tobacco story. It's a tale of colonial commerce morphing into Indian enterprise, of family feuds worth ₹11,000 crores, and of a company that somehow maintains the exclusive rights to manufacture Marlboro in a country of 1.4 billion people.

The numbers tell one story: ₹6,032 crores in revenue for FY25, ₹1,200 crores in profit, a stock price that surged 137% year-over-year to hit an all-time high of ₹11,444 in August 2025. But the real narrative runs deeper—through Victorian London trading floors, Indian independence struggles, IPL cricket controversies, and Supreme Court succession battles.

How did a British cigarette company founded in 1844 at Bevis Marks in Aldgate become the crown jewel of Modi Enterprises? Why does Philip Morris still hold 25% of this Indian company? And what does the bitter family feud between Lalit Modi—yes, the IPL founder—and his mother Bina Modi mean for shareholders?

This is the story of Godfrey Phillips India: part colonial legacy, part family saga, part strategic masterclass in navigating one of the world's most regulated industries. It's about building distribution moats across 800,000 retailers, managing global joint ventures through political upheavals, and extracting value from what many consider a sunset industry.

The company stands at a fascinating crossroads. On one side, mounting ESG pressures and regulatory headwinds threaten the tobacco industry globally. On the other, India's consumption story continues unabated, with millions of adults entering the formal economy each year. Meanwhile, a family drama worthy of a Netflix series plays out in courtrooms and boardrooms, with control of one of India's most profitable companies hanging in the balance.

Over the next several hours, we'll unpack how a Victorian entrepreneur's legacy became entangled with Indian ambition, American corporate might, and family dysfunction. We'll examine how this company built a business generating 26% return on capital employed while navigating everything from British colonialism to Indian socialism to modern ESG activism. And we'll analyze whether this controversial cash machine represents opportunity or risk for investors in 2025.

Buckle up. This journey takes us from the foggy streets of Victorian London to the gleaming towers of modern Mumbai, with stops at cricket stadiums, courtrooms, and cigarette factories along the way.

II. Victorian Origins: The Godfrey Phillips Legacy (1844–1936)

The year is 1844, and in the Jewish quarter of London's East End, at Bevis Marks in Aldgate, a young entrepreneur named Godfrey Phillips opens what seems like just another tobacco shop. Queen Victoria has been on the throne for seven years. The industrial revolution is transforming Britain into the world's first superpower. And cigarettes—those neat little paper-wrapped tobacco sticks—are still a novelty, overshadowed by pipes and cigars among London's gentlemen.

Phillips wasn't born into tobacco royalty. He was a Jewish immigrant's son, part of the wave of European Jews who found refuge and opportunity in Victorian London's relatively tolerant commercial environment. While the Rothschilds were financing governments and the Sassoons were building opium fortunes, Phillips started small—hand-rolling cigarettes in a cramped workshop, selling them to dock workers and clerks who couldn't afford the gentleman's cigar.

By the time Phillips died in 1900, his small shop had evolved into a modest but profitable enterprise. His sons faced a choice: liquidate and move on, or double down on father's legacy. They chose the latter, formally incorporating Godfrey Phillips Ltd in 1908, just as cigarettes were beginning their transformation from working-class vice to universal habit.

The 1920s marked the company's golden age of innovation—not in tobacco, but in marketing. While American companies like Lucky Strike were hiring Edward Bernays to manipulate public opinion, Godfrey Phillips pioneered something more innocent yet equally effective: football trading cards. Between 1920 and 1923, they issued an astonishing 4,502 different cards—1,100 in 1920, 2,462 in 1922, and 940 in 1923. Young boys across Britain would badger their fathers for Godfrey Phillips cigarettes, not for the tobacco but for the cards tucked inside featuring their football heroes. These football card collections became legendary among collectors—the company issued 1,100 cards in 1920, followed by 2,462 in 1922 and 940 in 1923. This wasn't just marketing; it was cultural engineering. Working-class boys who'd never set foot in a stadium could name every player in the league, their positions, their clubs. The cards created Britain's first truly national sports conversation, decades before television.

The strategy worked brilliantly until World War II's paper shortages killed the practice. But by then, Godfrey Phillips had achieved something remarkable: brand loyalty that transcended the product itself. People didn't just smoke Godfrey Phillips cigarettes; they collected them, traded them, passed them down to their children.

The company went public on the London Stock Exchange sometime before 1936, transforming from a family business into a corporate entity with shareholders to satisfy and quarterly reports to file. This was the era when British companies were discovering the intoxicating possibilities of empire—access to raw materials, captive markets, and populations eager for metropolitan sophistication.

Which brings us to 1936, the pivotal year when Godfrey Phillips (India) Limited was created, with a building of native-style architecture devoted to manufacturing the group's brands Cavander's, De Reszke and Greys. This wasn't just market expansion; it was cultural colonization wrapped in architectural sensitivity. The "native-style" building—a patronizing term that reveals the colonial mindset—was meant to signal that this was a British company that understood India, or at least wanted to appear so.

India in 1936 was still the Jewel in the Crown, eleven years away from independence. The Indian cigarette market was nascent but growing, driven by urbanization and the aspirational middle class's desire to emulate British habits. Godfrey Phillips saw opportunity where others saw only poverty and tradition. They weren't selling cigarettes; they were selling modernity, sophistication, a ticket to the global conversation.

The brands they chose to manufacture—Cavander's, De Reszke, Greys—weren't random. Each targeted a different segment of the Indian market. Cavander's for the upwardly mobile clerk, De Reszke for those with continental pretensions, Greys for the practical man who wanted quality without ostentation. This wasn't one-size-fits-all colonialism; it was sophisticated market segmentation decades before business schools would teach it.

But here's what makes this story fascinating from an investor's perspective: Godfrey Phillips wasn't following the typical colonial playbook of resource extraction. They were building manufacturing capacity in India, creating jobs, developing local supply chains. Whether by design or accident, they were positioning themselves for a post-colonial world where being seen as exploitative would become a liability.

As Europe descended into war in 1939, Godfrey Phillips India operated in a strange bubble—technically at war as part of the British Empire, but physically removed from the bombing and rationing that devastated the parent company. This geographic arbitrage would prove crucial. While London burned, the Indian subsidiary kept manufacturing, kept selling, kept generating cash.

The death of empire was already visible to those who cared to look. Gandhi's salt march had happened in 1930. The Quit India movement would launch in 1942. Smart British companies were already hedging their bets, creating structures that could survive the end of the Raj. Godfrey Phillips, perhaps inadvertently, had created exactly such a structure—an Indian company with British DNA, perfectly positioned for the transition ahead.

III. The Modi Empire Foundation (1933–1968)

In 1933, while Godfrey Phillips was shipping cigarettes to India, a different story was unfolding in the dusty plains of Uttar Pradesh. Rai Bahadur Gujarmal Modi, a Marwari businessman with the honorary British title that marked successful native collaborators, was building what would become one of India's great industrial houses. He started with sugar mills—unglamorous, capital-intensive, but essential. Sugar wasn't just a commodity; it was a gateway drug to industrialization.

The Marwaris were India's great merchant caste, often compared to the Jews of Europe—dispersed, commercially minded, maintaining their own networks across vast distances. Gujarmal Modi embodied their virtues: thrift elevated to an art form, relationships as currency, and an almost mystical ability to spot opportunity where others saw only chaos.

By the time his son Kedar Nath Modi—KK to everyone who mattered—took the reins, the Modi empire had expanded beyond sugar into vanaspati (hydrogenated vegetable oil), textiles, and heavy industries. But KK was different from his father. Where Gujarmal was content to be a big fish in the Indian pond, KK had global ambitions. He'd been educated in the Western style, understood capital markets, and most importantly, grasped that post-independence India would need a new kind of businessman—one who could navigate both the socialist rhetoric of Nehru's government and the capitalist reality of running profitable enterprises.

The 1950s and 60s were the high noon of the License Raj, that Byzantine system of permits, quotas, and permissions that turned Indian business into a game of political chess. You needed a license to import machinery, a permit to expand production, permission to enter new industries. The system was designed to prevent concentration of economic power, but in practice, it created exactly that—those who could navigate the bureaucracy thrived, while others withered.

KK Modi was a master navigator. He understood that in Nehru's India, you couldn't just be a businessman; you had to be a nation-builder. Every expansion had to be framed as serving the national interest. Every new venture needed to create employment, substitute imports, or earn foreign exchange. It was capitalism dressed in socialist clothing, and KK wore it well.

The turning point came in 1967-68. Godfrey Phillips Ltd. of London made an arrangement with International Tobacco Co. who opened a factory in Northern India to manufacture on the company's behalf. Upon the merger of D. Macropolo & Co. Ltd. with the company, International Tobacco Co. Ltd. became a subsidiary of it. This was corporate maneuvering at its finest—creating structures within structures, subsidiaries within subsidiaries, all designed to maximize opportunity while minimizing risk.

But the real coup came in 1968, when Philip Morris Inc. made a takeover bid for Godfrey Phillips Plc and the family shareholders were unable to prevent the company being sold. Suddenly, KK Modi found himself in partnership with one of the world's largest tobacco companies. Both Modi and Philip Morris would hold approximately 36% of Godfrey Phillips India, a perfectly balanced joint venture that would endure for over four decades.

Think about what this meant. In 1968, India was still largely closed to foreign investment. The Foreign Exchange Regulation Act would come in 1973, forcing companies like Coca-Cola and IBM to leave rather than dilute their ownership. Yet here was KK Modi, structuring a deal that gave him equal partnership with Philip Morris, ensuring both local control and global expertise.

The Philip Morris partnership brought more than just capital and technology. It brought Marlboro—the world's most valuable cigarette brand, the embodiment of American masculinity, the Marlboro Man riding across the prairies. In India, where American culture was both coveted and suspect, having the license to manufacture Marlboro was like having a license to print money.

But KK Modi was too smart to rely solely on foreign brands. He understood that India would always have a complex relationship with Western products—desiring them while resenting them, adopting them while adapting them. So even as he manufactured Marlboro for the elite, he was building indigenous brands for the masses. Four Square, Red & White, Cavanders—these became the workhorses of the Godfrey Phillips stable, generating the cash that would fund further expansion.

The distribution infrastructure built during this period was perhaps KK's greatest achievement. India in the 1960s and 70s wasn't one market but thousands—each state with its own language, regulations, and consumer preferences. Building a network that could deliver cigarettes from Kashmir to Kanyakumari, from Gujarat to Assam, required more than logistics. It required relationships, trust, and an understanding of India's infinite complexity.

KK Modi built this network retailer by retailer, distributor by distributor. He understood that in India, business wasn't just about transactions but about relationships that spanned generations. A distributor wasn't just a business partner but part of an extended family, invited to weddings, consulted on important decisions, protected during difficult times.

This period also saw the emergence of what would become a Modi trademark: the ability to operate in controversial industries while maintaining social respectability. Tobacco was already becoming problematic—health concerns were mounting, social attitudes were shifting. But the Modis positioned Godfrey Phillips not as a tobacco company but as an Indian success story, a company that provided livelihoods to farmers, employment to thousands, tax revenue to the government.

By the end of the 1960s, KK Modi had transformed what could have been a colonial remnant into a modern Indian corporation. He'd secured a partnership with Philip Morris that gave him both global reach and local control. He'd built distribution infrastructure that would prove to be an unassailable moat. And most importantly, he'd positioned himself and his company for the next phase of India's economic evolution—one that would bring both enormous opportunity and unexpected challenges.

IV. The Philip Morris Deal & Transformation (1968–2009)

The handshake between KK Modi and Philip Morris executives in 1968 created one of the most enduring and profitable joint ventures in Indian corporate history. For forty-one years, until 2009, both parties would maintain their delicate balance at 36% ownership each—a structure that gave neither complete control but forced both into a marriage of convenience that would generate billions in value.

To understand the genius of this arrangement, you need to understand the India of 1968-1991. This was peak License Raj, when Indira Gandhi's government viewed private enterprise with deep suspicion and foreign companies with outright hostility. The Foreign Exchange Regulation Act of 1973 would force Coca-Cola to leave India rather than dilute its ownership below 60%. IBM packed up and left. But Godfrey Phillips India, with its carefully balanced ownership structure, sailed through unscathed.

Philip Morris got what it desperately wanted: access to a market of 500 million people (in 1968) that would grow to over a billion, with smoking rates that, unlike the West, were still rising. They got manufacturing facilities that could produce at Indian cost structures. Most crucially, they got KK Modi—a partner who could navigate the labyrinthine Indian bureaucracy, manage relationships with everyone from tobacco farmers to cabinet ministers, and build distribution networks in places Philip Morris executives couldn't even pronounce.

Modi got the Marlboro license—a brand so valuable that in some years it was worth more than the entire company's physical assets. He got access to Philip Morris's legendary marketing expertise, their understanding of brand building, their R&D capabilities. But perhaps most importantly, he got credibility. Being partners with Philip Morris meant you were playing in the global leagues.

The 1970s and 80s were the golden years of this partnership. While the Indian economy grew at what was derisively called the "Hindu rate of growth"—3.5% annually—cigarette consumption was growing at double digits. Rural India was urbanizing. Women were entering the workforce and, quietly, beginning to smoke. The middle class, though still small, was aspirational and brand-conscious.

Four Square became the workhorse brand, positioned as the cigarette for the common man but with aspirations. The marketing was subtle but effective—associating the brand with success without ostentation, progress without abandoning tradition. Red & White targeted a slightly more premium segment, while Cavanders maintained its colonial-era positioning for those who valued heritage.

But it was Marlboro that captured the imagination of India's elite. In a country where foreign travel was restricted and foreign goods were either banned or prohibitively expensive, smoking Marlboro was a statement. It said you were global, sophisticated, successful enough to afford the premium. The brand became so aspirational that people would save empty Marlboro packs as status symbols, displaying them in their homes like trophies.

The real transformation came with India's economic liberalization in 1991. Finance Minister Manmohan Singh, under Prime Minister Narasimha Rao, dismantled decades of socialist planning almost overnight. Suddenly, India was open for business. Foreign companies rushed in. Competition intensified. But Godfrey Phillips, with its two-decade head start, its distribution network, its understanding of Indian consumers, was perfectly positioned.

The 1990s saw explosive growth. Revenue doubled, then doubled again. The company expanded beyond cigarettes into related products—pan masala, confectionery, anything that could leverage their distribution network. They modernized manufacturing, with facilities at Rabale in Navi Mumbai and two units in Ghaziabad near Delhi, plus an R&D centre in Mumbai and a food R&D in Ghaziabad, and a tobacco-buying unit in Guntur, Andhra Pradesh.

This geographic spread wasn't random. Rabale gave them access to India's commercial capital and its ports. Ghaziabad covered North India, the Hindi heartland where volumes were highest. Guntur, in Andhra Pradesh, was the center of India's tobacco cultivation, ensuring quality control from leaf to cigarette.

The 2000s brought new challenges. Health consciousness was rising even in India. The government, following global trends, began imposing restrictions—advertising bans, pictorial warnings, smoking bans in public places. The industry that had once advertised freely on television and in newspapers was pushed into the shadows.

But KK Modi and Philip Morris adapted. If you couldn't advertise directly, you built brand equity through surrogate advertising—promoting pan masala or confectionery with the same brand names. If pictorial warnings reduced pack appeal, you focused on the product experience itself. If public smoking was banned, you made sure your cigarettes were available at every possible retail point for private consumption.

The financial engineering during this period was equally sophisticated. Transfer pricing arrangements ensured that profits were optimized across jurisdictions. Royalty payments for brand usage created steady income streams. The company maintained minimal debt, generating cash that was either reinvested or returned to shareholders through dividends.

By 2009, when Modi increased his stake from 36% to 47% by acquiring an additional 11%, the transformation was complete. What had started as a colonial cigarette manufacturer had become a modern Indian corporation with global partnerships, generating billions in revenue and employing thousands. The company had survived colonialism, socialism, and liberalization. It had navigated health concerns, regulatory changes, and competitive pressures.

The Philip Morris partnership had been more than just a business arrangement. It was a forty-year marriage that produced enormous value for both parties. Philip Morris got access to one of the world's last growing cigarette markets without the political and regulatory hassles of direct ownership. Modi got global expertise and brands while maintaining Indian control.

V. Modern Modi Era & Control Consolidation (2010–2019)

The year 2010 marked a turning point that would set in motion a decade of family drama worthy of a Shakespearean tragedy. KK Modi, now in his seventies and having built one of India's great business empires, made an announcement that shocked corporate India: Lalit Modi would be his successor at Godfrey Phillips India.

Yes, that Lalit Modi—the flamboyant, controversial creator of the Indian Premier League, who had turned cricket from a gentleman's game into a $6 billion entertainment juggernaut. The same Lalit Modi who would, within months, be banned for life from cricket administration amid allegations of financial irregularities, fleeing to London where he remains to this day.

The announcement revealed the complex dynamics within the Modi family. KK had three children—Lalit, Samir, and Charu—but it was Lalit who had inherited his grandfather's entrepreneurial flair and his father's ambition. While Samir quietly managed parts of the family business and Charu pursued her own interests, Lalit had always been the chosen one, groomed from childhood to take over the empire.

In 2011, Modi Enterprises gained majority control of Godfrey Phillips India, with Philip Morris's stake reduced to between 21-25%. This shift in ownership was more than just numbers on a shareholding pattern. It represented KK Modi's vision of creating a truly Indian company, no longer dependent on foreign partnerships for legitimacy.

The IPL controversy that erupted in 2010 complicated this succession plan dramatically. Lalit Modi, who had created perhaps the most successful sports league in history, found himself embroiled in allegations of bid rigging, money laundering, and proxy ownership. The BCCI banned him for life. The Enforcement Directorate launched investigations. Lalit fled to London, conducting board meetings via video conference, running companies from exile.

Despite the controversy—or perhaps because of it—KK Modi stood by his son initially. Family loyalty trumped corporate governance. Board meetings became surreal affairs, with Lalit participating from London, other directors in Delhi, and lawyers scrambling to determine the legality of it all.

The business, remarkably, continued to thrive during this period. Revenue grew from ₹42.2 billion in 2013-14 to new heights year after year. The company's diversification strategy accelerated. Beyond cigarettes, they pushed into confectionery with brands like Funda, into pan masala, into any fast-moving consumer good that could leverage their distribution network.

This diversification wasn't just about growth; it was about survival. The writing was on the wall for tobacco companies globally. ESG investing was becoming mainstream. Pension funds and sovereign wealth funds were divesting from tobacco. In India, regulations were tightening every year—higher taxes, larger warnings, more restrictions on where cigarettes could be sold and consumed.

KK Modi's strategy was to build what he called a "house of brands"—using Godfrey Phillips's cash generation and distribution muscle to create a broader FMCG company. The tobacco business would fund the transformation, much like how Philip Morris International was trying to move "beyond nicotine" globally.

The manufacturing excellence during this period was noteworthy. The Rabale facility in Navi Mumbai became one of the most advanced cigarette manufacturing plants in Asia, capable of producing millions of cigarettes daily with minimal human intervention. The Ghaziabad units focused on product innovation, creating new variants, experimenting with filters and flavors within regulatory constraints.

The company also built significant R&D capabilities, unusual for what many considered a sunset industry. The Mumbai R&D center worked on tobacco products, while the Ghaziabad food R&D facility developed new confectionery and snack products. This dual focus—optimizing the declining but profitable tobacco business while building new growth engines—required delicate balance.

Distribution remained the company's greatest strength. By 2015, Godfrey Phillips products were available at over 800,000 retail points across India. The company employed 6,000 salespeople who visited these retailers regularly, ensuring product availability, managing inventory, collecting market intelligence. This feet-on-street presence was something e-commerce giants like Amazon and Flipkart could only dream of replicating.

The financial performance during this period was impressive by any measure. The company maintained returns on capital employed above 25%, net margins in double digits, and generated substantial free cash flow despite regulatory headwinds. The balance sheet remained fortress-like—minimal debt, substantial cash reserves, conservative accounting.

But beneath this operational success, family tensions were building. Lalit's exile complicated succession planning. Samir and Charu began asserting their own claims to the inheritance. Bina Modi, KK's wife and the family matriarch, emerged as a power center in her own right. Board meetings became battlegrounds, with independent directors caught in the crossfire.

KK Modi tried to maintain control, but age and illness were taking their toll. He attempted various structures to ensure smooth succession—trusts, holding companies, elaborate legal arrangements. But in a family where everyone felt entitled to everything, no structure could contain the ambitions and resentments building over decades.

By 2019, as KK Modi's health declined, the family was effectively in civil war. Lalit, from London, claimed his birthright as the chosen successor. Bina Modi, in Delhi, asserted her position as the widow and natural heir. Samir and Charu had their own claims and grievances. Lawyers enriched themselves as the family spent millions litigating against each other.

The company, caught in this crossfire, continued operating but strategic decision-making slowed. Major investments were deferred. Potential acquisitions were abandoned. The organization, unclear about its future leadership, became conservative, focused on protecting what existed rather than building for the future.

VI. The Family Drama & Succession Battle (2019–Present)

On November 2, 2019, KK Modi died at the age of 80, leaving behind an empire worth ₹11,000 crores and a family in complete disarray. His death didn't resolve the succession battle—it escalated it into open warfare. Within hours of his passing, lawyers were filing cases, family members were issuing contradictory statements, and corporate India watched in fascination as one of its great dynasties tore itself apart.

The battle lines were clearly drawn. In one corner: Lalit Modi, the eldest son, IPL creator, and KK's announced successor, fighting from his London exile. In the other: Bina Modi, the widow, backed by daughter Charu and, intermittently, son Samir. The prize: control of Godfrey Phillips India and the broader Modi Enterprises empire.

Bina Modi moved swiftly. As KK's widow and a significant shareholder in her own right, she claimed the chairmanship of Modi Enterprises and by extension, influence over Godfrey Phillips India. The board, dominated by family members and loyalists, acquiesced. Dr. Bina Modi—she had a PhD in literature, an interesting qualification for running a cigarette company—became the de facto leader of the empire.

Lalit's response was predictable and fierce. From London, he launched a barrage of legal challenges. He claimed his father's will clearly designated him as successor. He alleged that his mother and siblings were conspiring to deprive him of his inheritance. He accused the board of Godfrey Phillips of breaching fiduciary duties. The Supreme Court, various High Courts, the Company Law Board—every possible legal forum became a battlefield. The legal battles have been extraordinary in their complexity and viciousness. Samir Modi, the executive director of Godfrey Phillips, had accused his mother of orchestrating an attack on him to gain leverage in the ongoing inheritance dispute. In May 2024, during a board meeting, the family feud over the Rs 11,000 crore fortune of the late KK Modi turned violent when Samir Modi accused his mother of orchestrating an attack on him. He lodged a complaint with the Delhi Police, alleging that his mother, along with her personal security officer (PSO) and others, caused him "grievous hurt". The incident reportedly took place on Thursday, May 30, during a board meeting.

The trust deed at the center of this dispute, created by KK Modi in 2014, proposed that KK Modi's wife and three children share the inheritance equally. If the wife dies, her share will be divided equally among the three children, ensuring that Charu, Lalit, and Samir each receive one-third of the family inheritance. The deed also provided the option of dissolving the trust and distributing the wealth accordingly.

But Bina Modi had other ideas. As managing trustee of the KK Modi Family Trust, which holds 47% of Godfrey Phillips, she effectively controlled the company. Her strategy was simple: maintain control, marginalize the sons, and ensure daughter Charu's interests were protected. The board, stacked with loyalists, rubber-stamped her decisions.

The corporate maneuvering during this period was Byzantine. In April 2024, Godfrey Phillips announced its exit from the retail business 24Seven, a move Samir opposed as it would reduce the company's value. The company announced exit from retail business 24Seven in April 2024. However, a Delhi Court restrained the company from going ahead with the move in June and granted protection to Samir Modi's position in the board.

The battle reached a climax in August 2024. A Delhi court ruled that Modi is not entitled to remain perpetually in his position without following the due process of reappointment. Godfrey Phillips has appointed Charu Modi to the company's board in place of Samir Modi. Charu, Samir and Lalit Modi are children of the late KK Modi.

This wasn't just a board change; it was a palace coup. Samir, who had been executive director for years, was replaced by his sister Charu, cementing Bina Modi's control over the company. The September 2024 AGM became a flashpoint, with the Delhi High Court clearing the way for Bina Modi to vote as a managing trustee of the K K Modi Family Trust at the 87th annual general meeting. The AGM will decide on the leadership of GPI. The K K Modi Family Trust has nearly a 47.5 per cent stake in the company, with its partner, global giant Philip Morris International, holding just over 25 per cent.

Throughout this drama, Philip Morris has maintained a studied silence. Their 25% stake gives them significant influence but not control. They've watched the family tear itself apart, presumably calculating that as long as cigarettes keep getting manufactured and sold, the family drama is irrelevant. This is classic Philip Morris—pragmatic, focused on returns, willing to work with whoever controls the company.

The impact on corporate governance has been severe. Independent directors have found themselves in impossible positions, forced to choose sides in a family war. Board meetings have become theatrical productions, with accusations, counter-accusations, and occasionally, physical violence. The company's reputation, carefully built over decades, has been tarnished by headlines about family feuds and boardroom brawls.

Yet remarkably, the business has continued to perform. The inheritance battle between Samir Modi and Bina Modi seems to have little impact on Godfrey Phillip's share price. On year-to date basis, the shares of the group have delivered multibagger returns of more than 200 per cent on the bourses.

This disconnect between family drama and stock performance reveals something fundamental about the tobacco business: it's remarkably resilient. Customers don't stop smoking because the controlling family is fighting. Distributors keep distributing. Retailers keep selling. The cash keeps flowing.

For investors, the family feud presents both risk and opportunity. The risk is obvious—dysfunctional governance, strategic paralysis, potential value destruction through infighting. But there's also opportunity. If the family ever resolves its differences, or if one faction gains clear control, there could be significant value unlocking. A sale to Philip Morris or another strategic buyer could happen at a substantial premium. A professional management team, freed from family interference, could optimize operations and accelerate growth.

The human cost of this battle has been enormous. A family that once stood together at weddings and festivals now communicates only through lawyers. Lalit Modi, once the crown prince, remains in exile. Samir, who dedicated his life to the family business, has been unceremoniously ejected from the board. Bina Modi, now in her seventies, spends her days fighting her own children rather than enjoying her wealth and status.

As 2025 unfolds, the battle continues. Court cases proliferate. Lawyers get richer. And somewhere, KK Modi's ghost must be wondering how his carefully constructed empire became a battlefield for his heirs. The company he built to last generations may not survive the second generation intact.

VII. Business Model & Market Position Today

Strip away the family drama and courtroom theatrics, and Godfrey Phillips India remains a formidable business machine. With a market capitalization of ₹52,242 crores and approximately 14% share of India's cigarette market, the company has built a business model that generates extraordinary returns despite operating in one of the world's most regulated industries.

The numbers tell a story of ruthless efficiency. In FY25, the company generated ₹6,032 crores in revenue and ₹1,200 crores in profit—a net margin of nearly 20%. The return on capital employed stands at 26.3%, while return on equity is 19.9%. These aren't just good numbers; they're exceptional for any business, let alone one facing constant regulatory assault.

The cigarette portfolio remains the beating heart of the operation. Four Square and Red & White dominate the regular segment, competing directly with ITC's Gold Flake and Navy Cut. These aren't premium products; they're workhorses, generating volume in tier-2 and tier-3 cities where price sensitivity is high but brand loyalty, once earned, is fierce. Cavanders targets the premium segment, while Stellar and Focus fill specific niches. And then there's Marlboro—manufactured under license, sold at premium prices, generating margins that would make luxury goods companies envious.

But here's what most analysts miss: Godfrey Phillips isn't really in the cigarette business. It's in the distribution business. Those 800 distributors and 6,000 salespeople don't just move cigarettes; they move anything the company chooses to manufacture. The 800,000 retail points aren't just cigarette outlets; they're the last mile of a distribution network that reaches into every corner of India.

This distribution moat is virtually impossible to replicate. You can't build it with venture capital or technology. It requires decades of relationships, trust earned over millions of transactions, credit extended and repaid, promises kept during shortages and surpluses. When a small paan shop owner in rural Bihar knows he can count on his Godfrey Phillips distributor to deliver product on time, extend credit during tough times, and take returns without question, that's not just business—it's a relationship that Amazon or Reliance Retail can't algorithm their way into.

The manufacturing infrastructure is equally impressive. The Rabale facility in Navi Mumbai is a marvel of automation—machines that can produce millions of cigarettes daily with minimal human intervention, quality control systems that catch defects invisible to the human eye, packaging lines that can switch between brands in minutes. The Ghaziabad units focus on innovation within regulatory constraints—new filter technologies, flavor innovations that don't technically violate regulations, packaging that maximizes brand visibility despite pictorial warnings covering 85% of the pack.

The near debt-free status—the company operates with minimal borrowings—provides enormous strategic flexibility. In an industry where a single regulatory change can destroy billions in value overnight, having a fortress balance sheet isn't just conservative; it's survival. The company can weather regulatory storms, invest countercyclically when competitors are struggling, and return cash to shareholders without worrying about debt covenants.

The non-cigarette diversification, while still small, shows promise. The confectionery business, marketed under the Funda brand, leverages the same distribution network but targets a completely different consumer. Pan masala, controversial but profitable, provides another revenue stream. The company has experimented with tea, chewing gum, and other FMCG products—not all successful, but each teaching valuable lessons about leverage and limitations of the distribution network.

The regulatory environment remains the elephant in the room. India has some of the world's strictest tobacco regulations—85% pictorial warnings, complete advertising bans, prohibition of smoking in public places, regular tax increases. The industry operates under constant threat of further restrictions. There's perpetual talk of plain packaging, where all branding would be removed. Some states have attempted to ban cigarettes entirely, though black markets quickly emerge.

Yet paradoxically, these regulations create barriers to entry. No rational new player would enter the Indian cigarette market today. The capital requirements are enormous, the regulatory hurdles insurmountable, the social opprobrium guaranteed. This leaves the existing players—primarily ITC and Godfrey Phillips—with an effective duopoly.

The tax structure is particularly interesting. Cigarettes contribute over ₹30,000 crores annually to government coffers through excise duties, VAT, and GST. This creates a perverse incentive—governments publicly discourage smoking while privately depending on tobacco taxes. It's a devil's bargain that has persisted for decades and shows no signs of resolution.

Competition from ITC remains the biggest challenge. With over 70% market share, ITC is the undisputed king of Indian tobacco. They have deeper pockets, broader product portfolios, and political connections that Godfrey Phillips can't match. But Godfrey Phillips has survived by being nimble, focusing on specific segments, and maintaining lower costs.

The informal sector presents another challenge. Bidis and chewing tobacco, largely unregulated and untaxed, command huge market shares in rural India. As cigarette taxes increase, some consumers downgrade to these alternatives rather than quitting, limiting the pricing power of organized players.

International expansion remains limited. Unlike ITC, which exports globally, Godfrey Phillips is primarily India-focused. The company does have an International Business Division for exporting cigarette brands, cut tobacco, and tobacco leaf, but volumes remain modest. This India-centric approach is both a limitation and a strength—the company knows its market intimately but lacks geographic diversification.

Looking forward, the company faces an existential question: What is Godfrey Phillips without cigarettes? Can it transform into a broader FMCG company like ITC has attempted? Or is it destined to be a slowly declining but highly profitable cigarette company, returning cash to shareholders while the industry gradually shrinks?

The answer likely lies somewhere in between. The cigarette business will continue generating cash for years, possibly decades. That cash can fund diversification, though success is far from guaranteed. The distribution network provides optionality—the ability to launch new products with guaranteed shelf space. But execution will be critical, and with the family fighting among themselves, strategic clarity is in short supply.

VIII. Stock Performance & Financials Deep Dive

The stock chart of Godfrey Phillips India over the past year looks like a rocket ship defying gravity. From around ₹4,800 in August 2024 to an all-time high of ₹11,444 on August 7, 2025—a staggering 137% return that has left analysts scrambling to explain what changed. The answer, paradoxically, might be that nothing changed, and that's exactly the point.

At a P/E ratio of 43.0, the market is pricing Godfrey Phillips at a premium that would make even technology companies blush. For context, ITC, with its dominant market position and diversified portfolio, trades at a P/E of around 25. The book value per share stands at ₹1,009, meaning investors are paying nearly 6x book value for a tobacco company in an industry supposedly in terminal decline.

The dividend yield of 0.97% seems paltry, especially for a cash-generative business in a mature industry. This is where the story gets interesting. Unlike ITC, which returns substantial cash to shareholders through dividends, Godfrey Phillips has been conservative with payouts. The company is sitting on cash reserves that could support much higher dividends, but the family feud has paralyzed capital allocation decisions.

FY25's performance was remarkable by any measure—34% sales growth and 24% profit rise in an industry where single-digit growth is considered good. Part of this was price increases passing through, part was volume growth in specific segments, and part was the low base effect from previous years. But the consistency of margin expansion suggests operational improvements beyond just price increases.

The promoter holding at 72.6% is both a strength and weakness. It provides stability—no hostile takeover is possible—but also locks in the family drama. The free float of just 27.4% means relatively small trades can move the stock significantly, explaining some of the volatility.

Breaking down the revenue composition reveals interesting trends. While cigarettes still contribute about 90% of revenues, the growth rates in non-cigarette segments are higher. The confectionery business, though small, is growing at 40% annually. Pan masala, despite regulatory challenges, maintains steady growth. These green shoots suggest potential for transformation, though execution remains uncertain.

The cost structure shows remarkable discipline. Raw material costs have been managed through long-term contracts with tobacco farmers, ensuring stable supply at predictable prices. Employee costs, despite inflation, have grown slower than revenues, indicating productivity improvements. Marketing expenses, constrained by advertising bans, are minimal, allowing more money to flow to the bottom line.

Working capital management is exemplary. The company operates with negative working capital in many quarters—collecting cash from distributors before paying suppliers. This cash conversion cycle, typically 20-30 days negative, provides free financing for operations. In a capital-intensive industry, this efficiency is a significant competitive advantage.

The return ratios deserve deeper analysis. The 26.3% ROCE isn't just high; it's sustained over years despite regulatory headwinds. This suggests a business with genuine competitive advantages, not just benefiting from temporary favorable conditions. The 19.9% ROE, while lower than ROCE due to the equity base, still represents exceptional value creation for shareholders.

Comparing Godfrey Phillips to global tobacco peers reveals interesting disparities. Philip Morris International trades at a P/E of about 15, British American Tobacco at 8, and Altria at 9. Even adjusting for India's growth premium, Godfrey Phillips's valuation seems stretched. Either the market knows something analysts don't, or there's a bubble building.

The bear case for the valuation is straightforward: regulatory risk, family dysfunction, limited growth runway, and ESG concerns should warrant a discount, not a premium. The cigarette industry globally trades at single-digit P/Es precisely because of these structural headwinds. Why should Godfrey Phillips be different?

The bull case is more nuanced. India's per capita cigarette consumption is among the world's lowest, suggesting room for growth despite health concerns. The distribution network has option value beyond cigarettes. The family feud might resolve with a sale to Philip Morris or another strategic buyer at a premium. The company's pricing power, demonstrated by successful price increases despite competition, suggests the moat is stronger than it appears.

There's also a scarcity premium at play. For investors wanting exposure to India's consumption story but unable to stomach ITC's conglomerate complexity, Godfrey Phillips offers a purer play. The limited free float creates technical support—any institutional buying moves the stock significantly.

The valuation disconnect might also reflect different time horizons. Short-term traders see a stock with momentum, breaking all-time highs, with potential catalysts from family resolution. Long-term investors see terminal value problems, regulatory risks, and governance concerns. The stock price reflects this tug-of-war between narratives.

Recent quarterly results show the momentum continuing. Q1 FY26 saw revenue growth of 28% year-on-year, with margins expanding despite input cost inflation. Volume growth, usually negative for the industry, was flat to slightly positive, suggesting market share gains from smaller players.

The cash pile presents its own puzzle. With nearly ₹2,000 crores in cash and investments, the company could easily double its dividend, make strategic acquisitions, or buyback shares. But the board, paralyzed by family disputes, has done none of these. This cash trap—valuable assets earning minimal returns—is a classic symptom of governance failure.

For fundamental investors, Godfrey Phillips presents a fascinating dilemma. The business quality is undeniable—high returns, strong moat, consistent cash generation. But the valuation seems to price in perfection in an imperfect industry with imperfect governance. The risk-reward balance has shifted dramatically with the stock's rise.

The options market tells its own story. Implied volatility remains elevated, suggesting traders expect continued large moves. The put-call ratio skews bearish, indicating sophisticated investors are hedging against a correction. Yet the stock keeps rising, defying skeptics and rewarding momentum players.

IX. Strategic Challenges & Future Positioning

The future of Godfrey Phillips India sits at the intersection of multiple tectonic shifts—regulatory, social, technological, and generational. Each presents existential challenges that would terrify most CEOs, yet also opportunities for those bold enough to reimagine what a tobacco company can become in the 21st century.

The regulatory trajectory is unambiguous and unforgiving. Every year brings new restrictions—higher taxes, larger warnings, more smoking bans. The recent proposal to convert the compensation cess to a health or green cess isn't just semantic; it's a philosophical shift that could justify even more punitive taxation. Some states are experimenting with prohibition-style bans, though black markets immediately emerge. The endpoint of this regulatory march seems clear: a world where legal cigarette sales become practically impossible.

Yet history suggests linear extrapolation is dangerous. Prohibition failed in America not because people loved alcohol but because bans create worse problems than the vices they're meant to cure. India's massive informal tobacco sector—bidis, chewing tobacco, illegal cigarettes—already accounts for 80% of tobacco consumption. Further restrictions on legal cigarettes might simply shift consumption to these unregulated alternatives, reducing tax revenues without improving public health.

The ESG (Environmental, Social, and Governance) movement presents a different but equally serious challenge. Global investors are increasingly excluding tobacco from portfolios, regardless of returns. Norwegian sovereign wealth fund, Dutch pension funds, and numerous others have divested. This ESG exclusion raises capital costs, limits strategic options, and creates a valuation ceiling regardless of business performance.

But India isn't Norway. ESG considerations, while growing, remain secondary to returns for most Indian investors. The domestic institutional investor base—mutual funds, insurance companies, retail investors—hasn't embraced ESG exclusions with Western fervor. This creates an interesting dynamic: Godfrey Phillips might become uninvestable globally but remain attractive domestically.

Competition from ITC remains the most immediate strategic challenge. With 70%+ market share, ITC enjoys economies of scale Godfrey Phillips can't match. They can outspend on distribution, absorb regulatory costs better, and cross-subsidize from their diversified portfolio. Every year, the gap widens. Godfrey Phillips's market share has been slowly eroding, from about 16% a decade ago to 14% today.

The strategic response options are limited but not exhausted. Godfrey Phillips could focus on specific niches where ITC is weak—premium segments, specific geographies, or demographic groups. They could accelerate non-tobacco diversification, though ITC's own mixed record here is cautionary. Or they could pursue consolidation, acquiring smaller players to gain scale, though regulatory approval would be challenging.

The digital transformation of retail presents both opportunity and threat. E-commerce platforms can't sell cigarettes in India, protecting traditional distribution. But as retail digitizes, the value of physical distribution networks diminishes for non-tobacco products. The 800,000 retail points that are Godfrey Phillips's greatest asset for cigarettes become less relevant for selling confectionery or FMCG products.

The company's response has been tentative. Some experiments with digital ordering systems for distributors, data analytics for demand prediction, and digital marketing for non-tobacco products. But these feel like incremental improvements rather than transformation. The company lacks the digital DNA that native digital companies possess.

Succession planning—or its absence—remains the elephant in the boardroom. The family feud has created a leadership vacuum at the worst possible time. Strategic decisions are deferred, investments delayed, opportunities missed. Competitors and regulators move fast; Godfrey Phillips moves at the speed of court proceedings.

The international expansion opportunity remains largely unexplored. While ITC exports globally, Godfrey Phillips remains India-centric. There's logic to this—why complicate life with international regulations when India itself is so challenging? But it also means missing opportunities in markets where tobacco regulation is less stringent and growth prospects better.

The cannabis revolution happening globally presents an intriguing possibility. As marijuana gets legalized across American states and other countries, tobacco companies are positioning themselves to enter this market. Philip Morris, Altria, and others are making investments. Could Godfrey Phillips leverage its manufacturing and distribution capabilities for cannabis products if India ever liberalizes? It's speculative but not impossible.

The harm reduction narrative offers another strategic avenue. Globally, tobacco companies are pivoting to "reduced risk products"—e-cigarettes, heated tobacco, nicotine pouches. These products, while not harmless, are arguably less harmful than combustible cigarettes. Philip Morris has declared its intention to stop selling cigarettes entirely, focusing on smoke-free alternatives.

In India, this transition faces unique challenges. E-cigarettes are banned, ostensibly to prevent youth addiction. The government views any nicotine product with suspicion. But consumer demand exists—a thriving black market in vaping products suggests latent demand. Could Godfrey Phillips lead regulatory change, positioning itself as a responsible company transitioning away from combustibles?

The demographic dividend that has powered India's growth presents a paradox for Godfrey Phillips. Millions of young Indians enter the workforce annually, potential new customers. But this generation is more health-conscious, environmentally aware, and socially responsible than their parents. They might drink craft beer and organic coffee but view smoking as antiquated and harmful.

The company's attempts at youth engagement through non-tobacco products have been mixed. The Funda confectionery brand hasn't achieved breakthrough success. Pan masala, while profitable, carries its own health and image baggage. The company needs products that leverage its distribution but appeal to modern consumers—easier said than done.

Climate change adds another layer of complexity. Tobacco farming is water-intensive and soil-depleting. As water becomes scarcer and climate patterns shift, tobacco cultivation will become more challenging and expensive. The company needs to think about supply chain resilience in a climate-changed world.

The strategic options facing Godfrey Phillips can be summarized in three scenarios. First, the "steady decline" scenario—continue operating as a cigarette company, maximize cash extraction, and manage decline professionally. Second, the "transformation" scenario—use cigarette cash flows to build a new identity, whether in FMCG, cannabis, or reduced-risk products. Third, the "exit" scenario—sell to Philip Morris or another buyer while the asset still has value.

Each path has merit and risks. The steady decline guarantees cash flows but eventual irrelevance. Transformation offers growth but requires capabilities the company may not possess. Exit provides immediate value realization but depends on buyer appetite and regulatory approval.

X. Playbook: Lessons from a Colonial-to-Conglomerate Journey

The Godfrey Phillips story, stripped of its specifics, offers a masterclass in corporate evolution, survival, and value creation across radically different eras. Each transition—from colonial enterprise to independence-era survivor, from License Raj navigator to liberalization beneficiary, from family business to public company—required different skills, strategies, and sacrifices.

Lesson 1: Regulatory Arbitrage as Core Competency

Most companies view regulation as a constraint; Godfrey Phillips turned it into a moat. During the License Raj, while others complained about restrictions, KK Modi mastered the system. He understood that in a controlled economy, the ability to navigate bureaucracy was more valuable than operational efficiency. When liberalization came, this regulatory expertise didn't become obsolete—it evolved. The company that once navigated socialist planning now manages one of the world's most restrictive tobacco regulatory regimes.

The playbook here is subtle but powerful: don't just comply with regulations; shape them. Participate in policy discussions. Build relationships with regulators. Understand the political economy behind rules. Most importantly, structure your business so regulatory changes that destroy competitors strengthen your position.

Lesson 2: Joint Ventures with Giants—Dancing with Elephants

The Philip Morris partnership lasted over four decades, creating billions in value for both parties. This wasn't luck; it was carefully orchestrated balance. KK Modi understood that in a JV with a global giant, you need something they can't replicate—in this case, Indian market knowledge, regulatory relationships, and distribution networks.

The key was maintaining equilibrium. At 36% each, neither party could dominate. This forced collaboration, compromise, and mutual respect. Too many Indian companies either become subordinate to foreign partners or try to dominate them. Godfrey Phillips found the middle path—equal partnership based on complementary strengths.

The lesson extends beyond tobacco. In any industry where global expertise meets local complexity—retail, financial services, technology—this balanced JV model can create extraordinary value. The challenge is finding partners who respect boundaries and maintaining equilibrium as power dynamics shift.

Lesson 3: Distribution as Destiny

In the digital age, physical distribution seems antiquated. Yet Godfrey Phillips's 800,000 retail points remain its greatest asset. This network wasn't built through technology or capital but through decades of relationships, trust, and reciprocity. It's a asset that can't be replicated by algorithm or acquisition.

The playbook insight is that in markets with infrastructure challenges, regulatory complexity, and relationship-based commerce, distribution remains king. Whether selling cigarettes, confectionery, or eventually cannabis, the ability to reach every corner of the market is invaluable. Companies that own the last mile own the customer.

Lesson 4: Family Business Succession—The Achilles Heel

The Modi family feud offers a cautionary tale repeated across Indian business—from the Ambanis to the Hindujas. The very qualities that make family businesses successful—trust, long-term thinking, aligned interests—become liabilities during succession. The founder's children, raised in privilege, often lack the hunger and cohesion that built the empire.

The playbook lesson is brutal: succession planning can't start too early or be too explicit. Clear structures, independent boards, and professional management aren't betrayals of family values; they're prerequisites for survival. The best time to plan succession is when the founder is healthy and heirs are united. Once illness or discord strikes, it's too late.

Lesson 5: Managing Controversial Industries

Tobacco is increasingly indefensible from a social perspective. Yet Godfrey Phillips has maintained legitimacy and profitability. How? By never pretending cigarettes are healthy but focusing on legal compliance, tax contribution, and employment generation. By diversifying gradually rather than abandoning the core business abruptly. By maintaining fortress balance sheets that ensure survival regardless of regulatory changes.

The playbook applies to any controversial industry—alcohol, gambling, fossil fuels. Acknowledge social concerns without abandoning shareholders. Diversify without losing focus. Maintain financial strength to weather storms. Most importantly, be prepared for an endgame where your core business becomes socially unacceptable.

Lesson 6: Capital Allocation in Mature Industries

With minimal growth prospects and massive cash generation, tobacco companies face a capital allocation puzzle. Godfrey Phillips's approach—conservative dividends, minimal buybacks, cash hoarding—seems suboptimal. ITC's massive diversification seems expensive. Global peers' aggressive returns to shareholders seem short-sighted.

The playbook suggests a balanced approach: return enough cash to keep shareholders happy, retain enough for strategic flexibility, and invest carefully in adjacent opportunities. The key is recognizing that in mature industries, the hurdle rate for new investments should be exceptionally high. Better to return cash than destroy it chasing growth.

Lesson 7: The Scarcity Premium

Godfrey Phillips trades at valuations that seem irrational for a tobacco company. Part of this is the scarcity premium—there are only two listed cigarette companies in India. For investors wanting exposure to this market, options are limited. This scarcity creates pricing power beyond fundamental value.

The playbook insight: in markets with high barriers to entry and limited listed players, scarcity itself becomes valuable. This applies whether you're the only listed hospital chain, cement company, or casino operator in a market. The key is maintaining the barriers that create scarcity—regulatory, capital, or operational.

Lesson 8: Technology Adoption in Traditional Industries

Godfrey Phillips's tentative digital experiments highlight a common challenge—how traditional industries adopt technology without losing their core advantages. The company's strength is physical distribution and manufacturing excellence, not algorithms and apps.

The playbook suggests selective adoption. Use technology to enhance core strengths—data analytics for distribution optimization, automation for manufacturing efficiency—rather than trying to become a technology company. The goal is evolution, not revolution.

Lesson 9: Building Moats in Regulated Industries

Counterintuitively, heavy regulation can create the strongest moats. The more complex compliance becomes, the harder for new entrants. Godfrey Phillips has turned regulatory burden into competitive advantage. The playbook: embrace regulation rather than fighting it. Build compliance into your DNA. Make regulatory expertise a core competency. Structure operations to benefit from rules that constrain competitors.

Lesson 10: The Exit Option Value

Throughout its history, Godfrey Phillips has maintained strategic value to potential acquirers—first Philip Morris, potentially others. This exit option has value even if never exercised. It provides negotiating leverage, strategic flexibility, and a floor to valuations.

The playbook lesson: always maintain strategic value to potential buyers. This means clean structures, valuable assets (brands, distribution, licenses), and avoiding entanglements that complicate transactions. The best time to sell is when you don't need to.

XI. Bear vs. Bull Investment Case

The Bull Case: Hidden Value in Plain Sight

The bulls see Godfrey Phillips as a misunderstood cash machine trading at a discount to intrinsic value despite the recent rally. Start with the basics: ₹1,200 crores of annual profit, growing at 20%+, with minimal capital requirements. At current valuations, you're paying about 40x earnings for a business generating 26% returns on capital. Expensive? Perhaps. But consider the alternatives in India—technology companies with no profits trading at infinite P/Es, infrastructure companies with 8% returns trading at 30x.

The Marlboro franchise alone could be worth ₹10,000 crores. This isn't just a brand; it's a license to print money. In a country where foreign brands carry prestige premiums, manufacturing the world's most valuable cigarette brand is like having exclusive rights to Louis Vuitton in luxury or Mercedes in automobiles. Philip Morris could decide tomorrow to pay billions just to consolidate this franchise.

The distribution network—800,000 retail points reached by 6,000 salespeople—would cost tens of billions to replicate and decades to build. This isn't reflected on the balance sheet but represents enormous option value. As India formalizes and GST compliance improves, this network becomes even more valuable. Whether selling cigarettes, confectionery, or eventually cannabis products, this distribution is a permanent competitive advantage.

The family feud, rather than destroying value, might unlock it. These disputes typically end one of three ways: a buyout by one faction, a sale to outsiders, or professional management. Any resolution removes the current governance discount. If Bina Modi consolidates control, she might professionalize management. If Lalit Modi wins, he might engineer a sale. Either way, shareholders benefit.

The regulatory endgame might be further away than bears assume. India isn't the West—different cultural attitudes, enforcement challenges, and fiscal dependencies. The government collects ₹30,000+ crores annually from cigarette taxes. State governments depend on this revenue. Complete prohibition seems unlikely; more likely is a slow, manageable decline that generates cash for decades.

The balance sheet provides enormous safety margin. Near-zero debt means the company can survive any regulatory shock. ₹2,000 crores in cash provides acquisition currency or dividend capacity. Book value of ₹1,009 per share provides downside protection. This isn't a leveraged bet on regulatory forbearance; it's a conservative investment in a cash-generative business.

Market share gains are possible despite ITC's dominance. In specific segments—premium cigarettes, certain geographies—Godfrey Phillips competes effectively. As smaller players exit due to regulatory pressure, the organized sector gains. Even maintaining 14% share in a consolidating industry creates value.

The non-tobacco optionality is underappreciated. Yes, diversification has been slow, but the company is learning. Each experiment—confectionery, pan masala—builds capabilities. The right acquisition or product launch could transform perception overnight. ITC took decades to build its FMCG business; Godfrey Phillips is just starting.

India's consumption story remains intact. Per capita cigarette consumption is among the world's lowest, suggesting room for growth despite health concerns. Rural to urban migration, rising incomes, and stress of modern life all support volume growth. The social acceptability might decline, but absolute consumption could still increase.

The technical setup is bullish. The stock has broken all-time highs on strong volumes. Momentum begets momentum in Indian markets. Institutional ownership is low, suggesting room for accumulation. The limited float means any serious buying moves the stock significantly.

The Bear Case: Terminal Decline Masked by Multiple Expansion

The bears see Godfrey Phillips as a melting ice cube trading at bubble valuations. The 137% rally has disconnected from fundamentals, driven by momentum traders and retail speculation rather than institutional conviction. At 43x P/E, the market is pricing in growth that's impossible for a cigarette company facing existential threats.

The regulatory noose tightens every year. 85% pictorial warnings today, plain packaging tomorrow, complete prohibition eventually. This isn't speculation; it's the trajectory globally. Australia, UK, France—every developed market shows the endgame. India might be delayed but won't be different. Each restriction reduces volumes, increases costs, and destroys brand value.

ITC's dominance is insurmountable. With 70%+ market share, they enjoy economies of scale that grow stronger every year. They can absorb regulatory costs better, invest more in distribution, and cross-subsidize from other businesses. Godfrey Phillips's market share has declined from 16% to 14% over the past decade—this trend will accelerate.

The family dysfunction is value-destructive, not value-creating. Court battles cost millions in legal fees. Board paralysis prevents strategic decisions. Management attention is diverted from business to politics. Talented executives leave rather than navigate family dynamics. This isn't a temporary problem but a permanent handicap.

ESG exclusions will eventually matter in India too. As foreign institutional ownership increases and domestic institutions professionalize, tobacco becomes uninvestable. The cost of capital rises, valuations compress, and strategic options narrow. Being excluded from indices reduces passive buying. The stock becomes a value trap—optically cheap but permanently impaired.

The diversification story is fantasy. After decades of trying, non-tobacco remains marginal. The company lacks FMCG capabilities—brand building, innovation, consumer understanding. The distribution network, while valuable for cigarettes, doesn't translate to other categories where modern trade and e-commerce dominate. ITC's own struggles with diversification, despite far greater resources, should temper expectations.

The cash generation narrative ignores reinvestment needs. As volumes decline, maintaining market share requires higher spending on trade promotions. Regulatory compliance costs increase every year. The manufacturing facilities need modernization. The distribution network requires investment to stay relevant. Free cash flow is overstated.

The Philip Morris stake is a ceiling, not a floor. At 25%, they have blocking power for major decisions but no obligation to buy more. They're happy collecting dividends while the Modi family fights. A full takeover would face regulatory hurdles and reputational risks. The stake is a strategic option for Philip Morris, not a commitment to shareholders.

Demographics are destiny, and destiny is bearish. Young Indians don't smoke like their parents. Health consciousness is rising. Social acceptability is declining. The customer base is literally dying off faster than it's being replaced. Volume declines will accelerate, and price increases can't offset forever.

The valuation makes no sense relative to global peers. Philip Morris trades at 15x, British American at 8x, Altria at 9x. These companies have better positions, cleaner governance, and more diversification. Why should Godfrey Phillips trade at 3x the multiple? The answer is it shouldn't and won't—mean reversion is inevitable.

The recent rally is technical, not fundamental. Retail speculation, momentum algorithms, and limited float have created a bubble. When the music stops—and it always does—the crash will be spectacular. Long-term investors should remember: trees don't grow to the sky, especially when they're tobacco plants.

XII. Power & Grading

Applying Hamilton Helmer's 7 Powers framework to Godfrey Phillips reveals a business with significant structural advantages offset by existential threats—a combination that explains both the company's historical success and uncertain future.

Scale Economies: B+

Godfrey Phillips benefits from scale economies, though not to the extent of ITC. The cigarette manufacturing process has high fixed costs—factories, distribution networks, regulatory compliance—that become more efficient with volume. The company produces billions of cigarettes annually, spreading these costs effectively. However, at 14% market share versus ITC's 70%+, Godfrey Phillips operates at subscale relative to its main competitor. The grade reflects good absolute scale but poor relative scale.

Network Economies: D

Cigarettes don't benefit from network effects. One person smoking doesn't make the product more valuable to others—if anything, the opposite is true as smoking becomes less socially acceptable. There's no platform dynamic, no viral growth, no increasing returns to user adoption. This is a fundamental limitation of the business model that no amount of innovation can overcome.

Counter-Positioning: C+

Historically, Godfrey Phillips counter-positioned against ITC by being more agile, focused, and willing to operate in segments ITC ignored. The Marlboro license was brilliant counter-positioning—accessing a global premium brand ITC couldn't match. Today, this advantage has eroded. ITC has become more aggressive, and regulatory constraints limit strategic differentiation. The company maintains some counter-positioning in specific niches but lacks a broad strategic advantage.

Switching Costs: A-

Cigarette brands enjoy surprisingly high switching costs—not financial but psychological. Smokers develop strong brand loyalty, associating their brand with identity, ritual, and satisfaction. A Four Square smoker doesn't casually switch to Gold Flake. This brand loyalty, built over decades, provides pricing power and customer retention. The minus reflects that determined competitors can still win converts through promotion and innovation.

Branding: A

The brand portfolio—Four Square, Red & White, Cavanders, Marlboro—represents decades of investment and consumer trust. In a category where products are physically similar, branding is everything. These brands command price premiums, ensure distribution priority, and create emotional connections that transcend rational evaluation. The Marlboro license alone is worth billions. Even with advertising banned, these brands retain power through legacy association and word-of-mouth.

Cornered Resource: B+

The manufacturing licenses, distribution network, and Marlboro agreement constitute cornered resources. New entrants can't easily obtain cigarette manufacturing licenses in India. The distribution network, built over decades, can't be replicated. The Marlboro license is exclusive. However, these resources are wasting assets—valuable today but potentially worthless if cigarettes are banned. The grade reflects current value discounted for terminal risk.

Process Power: B-

Godfrey Phillips has developed processes for navigating India's complex regulatory environment, managing distributor relationships, and optimizing manufacturing within constraints. These embedded capabilities took decades to develop and would be difficult for new entrants to replicate. However, these processes are largely defensive—maintaining position rather than creating advantage. ITC has superior processes in most areas.

Overall Power Grade: B

Godfrey Phillips possesses real structural advantages—strong brands, switching costs, cornered resources—that generate superior returns. However, these powers are defensive rather than offensive, protecting existing position rather than enabling expansion. More concerning, these powers are eroding as regulation tightens, social acceptance declines, and competition intensifies.

Execution Grade: B-

Management execution has been competent but uninspiring. The company has navigated regulatory changes, maintained profitability, and returned cash to shareholders. However, diversification efforts have disappointed, market share has slowly eroded, and governance has deteriorated. The family feud represents a massive execution failure that offsets operational competence.

Strategy Grade: C+

The strategy—milk the cigarette business while attempting diversification—is logical but unimaginative. There's no bold vision, no transformative moves, no breakthrough innovations. The company is managing decline professionally rather than reimagining its future. The Marlboro partnership was the last truly strategic coup, and that was in 1968.

Luck Grade: B+

Godfrey Phillips has been remarkably lucky. The Indian government hasn't banned cigarettes despite pressure. Philip Morris remained a patient partner for decades. The company avoided nationalization during socialist periods and survived liberalization's competitive pressures. The recent stock rally, disconnected from fundamentals, represents continued good fortune. However, luck eventually runs out.

Comparison to Global Peers:

Versus Philip Morris International: PMI is executing a transformation to smoke-free products that Godfrey Phillips can't match. PMI's innovation, scale, and strategic clarity make Godfrey Phillips look provincial.

Versus British American Tobacco: BAT's global diversification and harm reduction investments provide options Godfrey Phillips lacks. However, BAT faces similar terminal value problems.

Versus ITC: ITC's conglomerate structure, while complex, provides resilience Godfrey Phillips lacks. ITC's execution, scale, and diversification are superior.

Versus Altria: Altria's focused U.S. approach and cannabis investments offer lessons, but regulatory environments differ too much for direct comparison.

What Could Have Been Done Differently:

-

Earlier, bolder diversification: Waiting until cigarettes were under siege to diversify was too late. The company should have aggressively diversified in the 1990s when cash flows were strong and time was ample.

-

Cleaner governance structures: The family should have separated ownership from management earlier, bringing professional leadership while maintaining control through board seats.

-

International expansion: Building presence in less regulated markets would have provided growth options and risk diversification.

-

Innovation investment: Developing reduced-risk products, even if not immediately commercializable in India, would have created options.

-

Strategic clarity: Either commit to transformation or to harvest—the middle path satisfies no one.

Final Assessment:

Godfrey Phillips is a good business in a bad industry with terrible governance—a combination that makes investment challenging despite apparent value. The company's powers are real but waning. Execution is competent but uninspired. Strategy is logical but timid. The stock price reflects momentum rather than fundamentals.

For investors, this presents a clear choice: bet on continued momentum and near-term catalysts (family resolution, Philip Morris buyout) or avoid based on terminal value concerns and governance risks. There's no middle ground with Godfrey Phillips—it's either a bargain or a value trap, and time will tell which narrative proves correct.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube