Gujarat Narmada Valley Fertilizers & Chemicals (GNFC): India's Chemical and Fertilizer Powerhouse

I. Introduction & Episode Roadmap

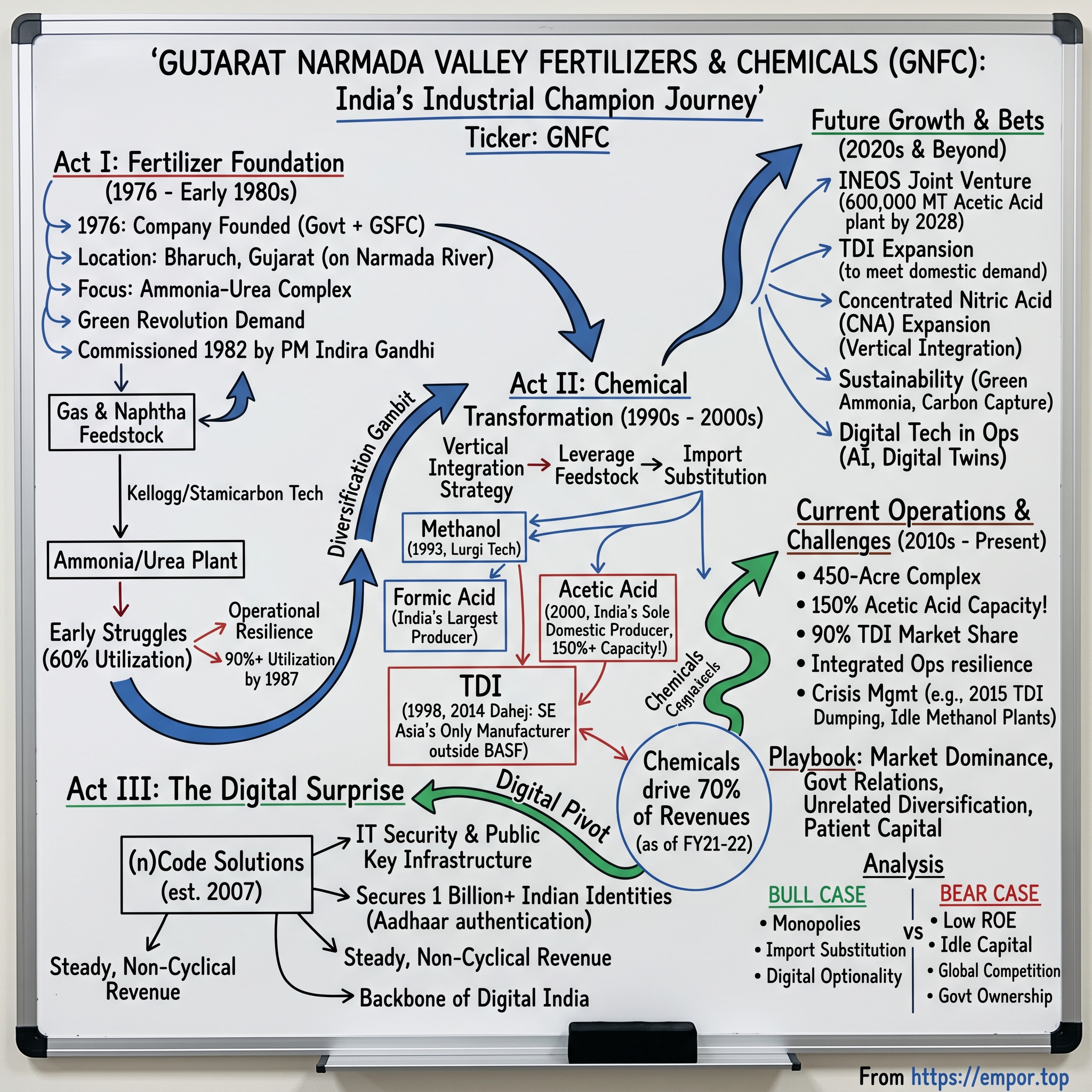

Picture this: A sprawling 450-acre complex on the banks of the Narmada River in Bharuch, Gujarat. Steam billows from cooling towers while a maze of steel pipes carries chemicals that touch nearly every aspect of modern Indian life—from the urea feeding the nation's wheat fields to the acetic acid in your nail polish remover, from the TDI foam in your car seat to, surprisingly, the digital signature authenticating your Aadhaar card. This is GNFC, a company that embodies India's industrial ambitions in ways both predictable and utterly unexpected.

Founded in 1976 as a government-backed fertilizer venture, GNFC has morphed into something far more complex: India's sole domestic producer of acetic acid, Southeast Asia's only TDI manufacturer outside of BASF's small facility, and through an unlikely twist, the digital backbone securing over a billion Indian identities. As of fiscal 2021-22, chemicals now drive 70% of revenues while fertilizers—the original raison d'être—contribute just 29%. It's a transformation story that reads like industrial fiction, except the numbers are real and the implications profound.

The company operates as India's manufacturer of fertilizers and chemicals, producing everything from urea and nitrophosphate fertilizers to methanol, formic acid, nitric acid, and acetic acid. Add in their neem-based products and a thriving IT subsidiary, and you have what might be India's most eclectic industrial conglomerate. Yet beneath this diversity lies a coherent strategy: vertical integration where possible, import substitution where profitable, and government relationships as both shield and sword.

This episode traces GNFC's evolution from a single-product fertilizer dream to a chemical powerhouse with a digital surprise. We'll explore how government backing created opportunities and constraints, why some bets paid off spectacularly while others sit idle, and what happens when you ask a chemical company to secure a nation's digital identity. It's a story of industrial policy meeting market reality, of commodity cycles clashing with political imperatives, and ultimately, of building national champions in emerging markets.

Our journey spans five decades and three distinct acts: the fertilizer foundation that justified the company's existence, the chemical diversification that transformed its economics, and the digital pivot that nobody saw coming. Along the way, we'll unpack the playbook for managing cyclical commodities, the art of technology transfer in chemicals, and why sometimes the best diversification is the one that makes no sense at all.

II. Origins & The Gujarat Industrial Vision

The year was 1976. India was barely a year out from Indira Gandhi's Emergency, the economy was struggling with the aftershocks of the 1973 oil crisis, and agricultural productivity remained the nation's most pressing challenge. In this environment, the Gujarat government made a bet: partner with Gujarat State Fertilizers and Chemicals (GSFC) to create another fertilizer giant. The logic was compelling—India imported most of its fertilizers, the Green Revolution demanded massive quantities of nutrients, and Gujarat's Bharuch district offered proximity to both feedstock and ports.

But GNFC's origin story really begins with geography. Bharuch sits at the mouth of the Narmada River, roughly equidistant from Mumbai and Ahmedabad. By the 1970s, it had already emerged as Gujarat's chemical corridor—Indian Petrochemicals Corporation Limited (now Reliance) had set up shop nearby, creating an ecosystem of suppliers, skilled workers, and infrastructure. The location offered access to natural gas from the Bombay High fields, proximity to the Kandla and Mumbai ports for imports, and crucially, state government support that went beyond mere permissions.

The founding vision was audacious: build one of the world's largest single-stream ammonia-urea fertilizer complexes. Not just large for India, but globally significant. The numbers were staggering for the time—a planned investment of over ₹400 crores (roughly $500 million in 1970s dollars), targeting annual production capacities that would dwarf existing Indian facilities. Construction began in 1978, but it would take until 1982 for the complex to start operations, a delay that would prove both costly and instructive.

What made GNFC different from other public sector undertakings was its hybrid structure. While the Gujarat government held majority control, it operated with unusual commercial flexibility. Board appointments mixed bureaucrats with industry professionals. Pricing decisions, while influenced by subsidy regimes, retained some market orientation. This governance model—neither fully public nor truly private—would shape every strategic decision that followed.

The early years were marked by a fascinating tension. Even as engineers worked round-the-clock to complete the fertilizer complex, management was already plotting diversification. Meeting minutes from 1981 reveal heated debates about whether to focus on fertilizer excellence or hedge bets with chemicals. The pragmatists won: GNFC would pursue both, using fertilizer cash flows to fund chemical ambitions. This decision, made before the first bag of urea was sold, would define the company's trajectory for the next four decades.

The 1982 commissioning was a landmark moment. Prime Minister Indira Gandhi herself inaugurated the facility, declaring it a testament to Indian engineering capability. Local newspapers ran headlines about "Bharuch's Industrial Revolution." But behind the ceremony, operational reality was harsh. The complex ran at barely 60% capacity in its first year, plagued by technical glitches, feedstock shortages, and a workforce learning on the job. Yet by 1985, capacity utilization crossed 90%, a turnaround that established GNFC's reputation for operational resilience—a trait that would prove invaluable as the company ventured into more complex chemicals.

III. Building the Fertilizer Foundation (1982–1990s)

The ammonia-urea complex that came online in 1982 was an engineering marvel that deserves proper appreciation. The heart of the operation was a 1,350 metric tons per day ammonia plant paired with a 2,100 MTPD urea facility—making it one of the largest single-stream ammonia-urea fertilizer complexes in the world. The technology, licensed from Kellogg and Stamicarbon, represented the cutting edge of fertilizer production. But technology alone doesn't explain what happened next.

In its first full year of operations, GNFC produced 381,000 metric tons of urea against a nameplate capacity of 630,000 MT—a 60% utilization that had board members sweating. The problems were manifold: erratic gas supply from ONGC, equipment failures in the high-pressure synthesis loops, and a workforce that, while enthusiastic, was still climbing the learning curve. One particularly memorable crisis came in August 1983 when the primary reformer developed cracks, shutting down the entire complex for 47 days. Engineers worked in shifts through Gujarat's brutal summer heat, racing against mounting losses and farmer complaints.

The turnaround began with small victories. By late 1984, the technical team had identified and fixed most design flaws—many through ingenious local modifications that improved on the licensed technology. They developed protocols for managing gas supply interruptions, including the ability to rapidly switch between natural gas and naphtha as feedstock. Most importantly, they built relationships with local farmers, establishing the "Narmada" brand not just as a product but as a promise of quality and availability.

The numbers tell the story: capacity utilization rose from 60% in 1983 to 78% in 1984, 89% in 1985, and by 1987, GNFC was operating at 94% capacity—among the highest in India's fertilizer sector. The company was producing over 590,000 MT of urea annually, generating revenues that crossed ₹200 crores. But this success created its own challenges. The fertilizer business, while profitable, was heavily dependent on government subsidy policies that could change with political winds. Management knew they needed to diversify, and they had been preparing for this moment even while solving the fertilizer puzzle.

The late 1980s saw GNFC master the art of incremental improvement. They pioneered energy conservation measures that reduced gas consumption per ton of urea by 12% between 1985 and 1989. They developed innovative packaging that reduced moisture damage—a chronic problem in India's humid climate. They even created a farmer education program that taught optimal fertilizer usage, building brand loyalty that transcended price considerations. The Narmada brand became synonymous with quality in Gujarat and neighboring states, commanding a premium even in the subsidy-controlled market.

Yet even as the fertilizer business flourished, management was laying groundwork for transformation. Internal documents from 1988 reveal extensive studies on downstream chemical opportunities. The logic was compelling: they already had ammonia, they could make nitric acid, and from there, a world of specialty chemicals opened up. The fertilizer success had given them credibility with lenders, technical partners, and most crucially, the Gujarat government. The stage was set for the chemical gambit that would redefine GNFC.

IV. The Chemical Diversification Gambit (1990s–2000s)

The board meeting in March 1991 was tense. India was in the midst of a balance of payments crisis, liberalization was upending decades of industrial policy, and here was GNFC proposing to invest hundreds of crores in chemical plants with uncertain markets. The fertilizer business was generating steady cash, but the subsidy regime's future was uncertain. The chairman's argument was simple but powerful: "We can remain a single-product company at the government's mercy, or we can build a portfolio that survives policy changes." The board approved the chemical diversification plan, setting in motion a transformation that would take two decades to fully realize.

The strategy was methodical: start with chemicals that leveraged existing feedstocks, then gradually move up the value chain. Methanol came first—a 100,000 MT per annum plant commissioned in 1993, using natural gas as feedstock. The technology came from Lurgi, but GNFC's engineers modified the process to handle variable gas quality, a chronic problem with domestic supply. Within two years, they had pushed production to 115,000 MT, becoming India's largest methanol producer.

But methanol was just the beginning. The real prize was the downstream chemicals it enabled. Formaldehyde and formic acid plants followed in quick succession. By 1996, GNFC was producing 40,000 MT of formic acid annually, capturing 60% of the domestic market. The integration was elegant: methanol to formaldehyde to formic acid, each step adding value and reducing import dependence. They became India's largest formic acid producer, a position they maintain today.

The masterstroke came in 1998 with the TDI (Toluene Diisocyanate) project. TDI is essential for polyurethane foams used in furniture, automobiles, and mattresses—a market growing at 15% annually in India but entirely import-dependent. The technology was complex, the investment massive (over ₹300 crores), and the risks substantial. No Indian company had attempted TDI production. GNFC licensed technology from Rhone-Poulenc, sent engineers to France for training, and built a 14,000 MT facility that made them Southeast Asia's only TDI producer outside Japan.

The TDI plant's early years were rocky. Operating rates barely touched 50% in 1999, as the team struggled with the complex chemistry and strict quality requirements of automotive customers. But by 2001, they had cracked the code, achieving 85% utilization and even exporting to Southeast Asian markets. The success prompted an ambitious expansion: TDI-2, a 50,000 MT plant in Dahej, commissioned in 2014, cementing GNFC's dominance with 67,000 MT of combined capacity against BASF India's modest 7,500 MT facility.

The acetic acid story deserves special mention. Commissioned in 2000 with 50,000 MT capacity, the plant used methanol carbonylation technology—a process so efficient that GNFC could compete with imports despite India's high energy costs. They progressively expanded capacity to 100,000 MT, and remarkably, have operated at over 150% of nameplate capacity for several years—a testament to both process optimization and market demand. Today, GNFC remains India's sole acetic acid producer, a monopoly position that generates outsized returns even in down cycles.

By 2005, the transformation was complete. Chemicals contributed over 50% of revenues, up from zero in 1990. The portfolio spanned industrial chemicals (methanol, acetic acid, formic acid), specialty chemicals (TDI, aniline), and even niche products like methyl formate. The fertilizer business, while still important, no longer defined the company. GNFC had successfully evolved from a government-mandated fertilizer producer to a diversified chemical company competing on commercial terms. But the most surprising transformation was yet to come.

V. The Surprising Digital Play: (n)Code Solutions

The meeting in 2006 seemed routine—another technology vendor pitching services to GNFC's IT department. But when executives from Entrust, a Canadian digital security firm, finished their presentation on public key infrastructure and digital certificates, GNFC's leadership saw something others missed. India was on the cusp of a digital revolution. E-governance initiatives were proliferating. Digital signatures would soon be mandatory for corporate filings. Someone would need to provide the cryptographic backbone for this transformation. Why not a chemical company with a reputation for operational excellence and government trust?

The logic was counterintuitive enough to be brilliant. GNFC had zero experience in IT services, but they had something equally valuable: credibility with government agencies, a track record of executing complex projects, and critically, the financial strength to invest in infrastructure that wouldn't generate returns for years. In 2007, they incorporated (n)Code Solutions as a subsidiary, partnering with Entrust to bring enterprise-grade digital security to India.

The early years were about building credibility in an entirely new domain. (n)Code started by providing digital signature certificates to corporations for MCA21—the Ministry of Corporate Affairs' ambitious e-governance initiative. The numbers were modest—a few thousand certificates generating revenues of ₹5-10 crores. But the team was learning, building relationships with government IT departments, understanding the unique challenges of Indian digital infrastructure.

The breakthrough came in 2009 when the Unique Identification Authority of India (UIDAI) began planning Aadhaar—the world's largest biometric identity program. The authentication system required cryptographic keys that would secure over a billion identities. The tender requirements were stringent: proven technology, financial stability, and absolute reliability. (n)Code Solutions, backed by GNFC's balance sheet and Entrust's technology, won a critical contract to provide authentication services.

What followed was a scaling challenge unlike anything in GNFC's chemical operations. Aadhaar enrollment exploded from thousands to millions to hundreds of millions. Every authentication request—whether for opening a bank account or receiving government benefits—passed through (n)Code's infrastructure. The subsidiary built data centers, hired hundreds of engineers, and created redundancy systems that achieved 99.99% uptime. By 2015, they were processing over 100 million authentication requests monthly.

The financial impact was transformative. (n)Code's revenues grew from ₹12 crores in 2010 to over ₹200 crores by 2020. More importantly, it provided a steady, non-cyclical income stream uncorrelated with chemical prices. The subsidiary expanded beyond Aadhaar into e-procurement, digital lockers, and enterprise security services. They became the backbone of India's digital public infrastructure, an position as strategically important as any chemical monopoly.

The cultural impact within GNFC was equally profound. A company that had defined itself through physical products—fertilizers you could touch, chemicals you could smell—now employed software engineers and cryptographers. Board meetings that once focused on plant utilization rates now included discussions on server uptime and API response times. It was a transformation that challenged every assumption about what GNFC could be. And it worked, generating returns that matched or exceeded traditional chemical investments while positioning the company at the heart of Digital India.

VI. Operations Excellence & Market Dominance

Walking through GNFC's Bharuch complex today feels like witnessing industrial symphony in motion. The numbers are staggering: 450 acres of interconnected plants where a methanol molecule's journey might end as acetic acid in a pharmaceutical factory or formic acid in a leather tannery. The company has achieved production records that seemed impossible a decade ago—TDI output touching 65,000 MT, acetic acid plants running at 150% of nameplate capacity, and formaldehyde units that haven't had an unplanned shutdown in three years.

The acetic acid operation deserves deeper examination. GNFC runs India's only facility, a 100,000 MT per year plant that should, by all conventional metrics, struggle against Chinese imports. Instead, it operates at over 150% capacity—producing 150,000+ MT annually through a combination of process optimization, catalyst improvements, and operating philosophy that pushes equipment to its absolute limits while maintaining safety standards. The plant runs 350 days a year, stopping only for mandatory maintenance. When Chinese imports flood the market, GNFC responds not by cutting production but by finding new customers in pharmaceuticals, textiles, and food preservation.

The TDI dominance is equally impressive. With 67,000 MT capacity across two plants, GNFC controls over 90% of domestic production (BASF's 7,500 MT facility serving specialized segments). The company has mastered the delicate chemistry of isomer ratios—producing the precise 80:20 blend of 2,4 and 2,6 isomers that foam manufacturers demand. They've developed relationships with every major automotive OEM in India, becoming so integral to supply chains that customers often co-locate warehouses near GNFC facilities.

Yet operational excellence extends beyond headline products. Consider calcium carbonate—a humble product that GNFC has turned into a high-margin business through quality consistency that pharmaceutical companies prize. Or methyl formate, where production records were broken three consecutive years through catalyst modifications that increased yields by 8%. Even in commodity chemicals like nitric acid, GNFC has differentiated through concentrated grades (98% concentration) that command premium pricing from explosive manufacturers and metal processing units.

The integrated nature of operations creates remarkable resilience. When methanol imports made standalone production uneconomical, GNFC could still run plants to feed downstream acetic and formic acid production. When TDI markets softened, they could adjust product mix toward aniline and other intermediates. This operational flexibility—the ability to optimize across products rather than individual plants—has helped maintain EBITDA margins even during severe downturns.

But perhaps the most impressive operational achievement is workforce productivity. GNFC produces this vast array of chemicals with just 1,800 employees—a ratio of output to workforce that matches global benchmarks. They've achieved this through automation certainly, but also through a culture of continuous improvement. Operators are trained across multiple plants, engineers rotate between facilities, and best practices spread rapidly. The company runs an internal "excellence awards" program where teams compete to improve efficiency, with winning ideas implemented company-wide.

The reliability statistics tell their own story: unplanned downtime below 2%, capacity utilization consistently above 85% across the portfolio, and safety metrics that earned GNFC multiple national awards. This operational excellence translates directly to financial performance—lower conversion costs that provide cushion during price downturns and higher realizations when markets tighten. It's the unsexy foundation that enables everything else, turning commodity chemicals into a sustainably profitable business.

VII. Challenges & Crisis Management

The year 2015 marked a watershed—GNFC reported its first-ever annual loss, a ₹28 crore deficit that shocked investors accustomed to decades of profitability. The perfect storm had arrived: Chinese chemical dumping, collapsing oil prices that made imports cheaper than domestic production, and a fertilizer subsidy crisis that delayed payments for months. Board meetings that year read like crisis management sessions, with every assumption about the business model under assault.

The TDI crisis was particularly acute. Chinese producers, facing their own overcapacity, dumped product in India at prices below GNFC's raw material costs. The company's new 50,000 MT Dahej plant, commissioned just a year earlier with great fanfare, operated at barely 30% capacity. Management faced an agonizing choice: match Chinese prices and bleed cash, or cede market share in a product where they'd invested ₹500 crores. They chose a middle path—maintaining minimum operations to preserve customer relationships while lobbying aggressively for anti-dumping duties.

The methanol situation was even more stark. Global capacity additions, particularly in Iran and Trinidad, had crashed prices from $500 per ton to below $250. GNFC's three methanol units in Bharuch, with combined capacity of 130,000 MT, simply couldn't compete. The decision was painful but clear: shut down all methanol production, import requirements for downstream units, and wait for markets to recover. Two years later, the plants remain idle—a ₹400 crore investment generating zero returns, though management insists they could restart within 60 days if economics improve.

Fertilizer subsidy delays added another layer of complexity. The government owed GNFC over ₹800 crores in subsidy arrears by March 2016, forcing the company to borrow working capital at commercial rates while waiting for government payments that carried no interest. Cash flow management became a daily challenge. The CFO later recalled reviewing cash positions every morning, juggling supplier payments, managing bank relationships, and ensuring enough liquidity for operations.

The crisis forced brutal prioritization. Expansion projects were frozen, discretionary spending eliminated, and workforce reduced through voluntary retirement schemes. Yet GNFC also used the downturn to accelerate operational improvements. They renegotiated gas supply contracts, implemented energy conservation projects that reduced costs by ₹50 crores annually, and surprisingly, increased investment in (n)Code Solutions, recognizing that digital services offered countercyclical stability.

The recovery, when it came, was gradual but decisive. Anti-dumping duties on TDI provided breathing room. Acetic acid demand surged as pharmaceutical exports grew. Fertilizer subsidy payments resumed with a new direct benefit transfer system. By 2017, GNFC was back in the black, reporting ₹250 crores in profit. But the crisis had changed the company's DNA—risk management became paramount, diversification accelerated, and management developed a healthy paranoia about commodity cycles that influences decisions to this day.

The lessons were expensive but valuable: geographic concentration of production means nothing when global overcapacity exists; government support can delay but not prevent market forces; and operational excellence, while necessary, isn't sufficient when input costs are structurally disadvantaged. GNFC emerged leaner and more focused, but also more realistic about the challenges of competing in global commodity markets from an Indian manufacturing base.

VIII. Growth Strategy & Future Bets

The November 2024 announcement sent ripples through India's chemical industry. GNFC and INEOS Acetyls signed an MOU to explore building a world-scale 600,000 MT acetic acid plant at GNFC's Bharuch site, with operations forecast to begin in 2028. The partnership structure—a 50-50 joint venture signed on November 20, 2024—reflects both confidence and shared risk in a project that could fundamentally alter India's chemical import dynamics.

The context makes the deal even more significant. India currently imports approximately 85% of its annual acetic acid requirements, a dependency that drains foreign exchange and leaves downstream industries vulnerable to supply disruptions. For GNFC, already operating its existing 100,000 MT facility at over 150% capacity, the expansion represents not just growth but strategic consolidation of a monopoly position that has proven remarkably profitable even through commodity downturns.

The INEOS partnership builds on a technology relationship spanning nearly 30 years but now evolves into equity participation. David Brooks, CEO of INEOS Acetyls, framed it clearly: "India is recognised as being a key growth market for our products over the coming years". For INEOS, a global leader in acetic acid production, the JV provides entry into one of the world's fastest-growing chemical markets without bearing full capital risk. For GNFC, it brings world-class technology and operational expertise that could accelerate the learning curve on a project six times larger than their current facility.

The TDI expansion story runs parallel but with distinct dynamics. "TDI consumption is growing," said GNFC's additional general manager Manish Upadhyay at India Chem 2024, noting demand driven by mattress and automotive sectors with consumption growing about 10% annually. The numbers support aggressive expansion: current Indian demand stands at 115,000 MT annually against domestic production of just 74,500 MT (GNFC's 67,000 MT plus BASF's 7,500 MT). About 48,000 MT of TDI entered India last year to bridge this gap, primarily from Japan, South Korea, China, and the EU.

GNFC's TDI journey hasn't been smooth. The original plant at Bharuch, installed in 1998 with 14,000 MT nameplate capacity, now produces at 19,500 MT, while the larger Dahej facility commissioned in 2014 with 50,000 MT capacity produced 40,100 MT in 2019. But the real story is volatility—"Overall, TDI market sentiment remained unfavourable during the whole year reflecting oversupply," with "dumping of imports affecting the viability of TDI-2 operation" during the 2019 downturn. Yet GNFC persists, planning another 50,000 MT expansion that would take total capacity to 117,000 MT, effectively meeting all domestic demand with room for exports.

The concentrated nitric acid (CNA) expansion represents a different bet—vertical integration taken to its logical conclusion. GNFC currently produces 115,000 MT of CNA annually from three plants at Bharuch and began constructing a fourth 50,000 MT facility that would increase production to 165,000 MT by end-2022. The strategic logic is compelling: 90% of CNA production is consumed internally, feeding into ammonium nitrate and other downstream products, creating a natural hedge against price volatility.

Technology partnerships anchor these expansions. KBR's MAGNAC concentrated nitric acid technology, successfully commissioned at GNFC's second plant, offers 150 MT per day capacity while recycling process water without treatment, improving energy efficiency and reducing emissions. ThyssenKrupp Uhde secured the contract for a new 600 MTPD weak nitric acid plant featuring their EnviNOx technology to eliminate nitrogen oxides—a three-decade partnership that speaks to GNFC's preference for proven relationships over lowest-cost bidders.

Sustainability has moved from afterthought to centerpiece. The nitric acid plants incorporate N2O abatement technology, critical as environmental regulations tighten. The TDI facilities are being retrofitted with energy recovery systems. Even the idle methanol plants are being evaluated for conversion to use renewable feedstocks. It's partly regulatory compliance, partly customer demand, but increasingly, it's about maintaining the social license that comes with government ownership.

The capital allocation strategy reveals management's thinking. Rather than betting everything on one mega-project, GNFC is pursuing multiple mid-sized expansions across different chemicals. The ₹600 crore INEOS joint venture, the potential ₹500 crore TDI expansion, the ₹300 crore nitric acid investments—each significant but not company-defining. It's a portfolio approach that acknowledges both the opportunities in import substitution and the risks of global overcapacity.

Digital initiatives continue to surprise. (n)Code Solutions keeps expanding beyond Aadhaar into e-procurement, blockchain applications for supply chain tracking, and even AI-powered plant optimization systems. The subsidiary generated over ₹200 crores in FY2020, providing cash flow stability that proved invaluable during chemical market downturns. Management hints at international expansion, leveraging Indian digital public infrastructure expertise to emerging markets facing similar identity and authentication challenges.

The thread connecting these investments is import substitution with a twist. Unlike the 1970s version that emphasized self-sufficiency at any cost, GNFC's strategy focuses on products where India has sustained competitive advantage—access to feedstocks, growing domestic demand, or technological differentiation. They're not trying to make everything; they're choosing battles where structural factors favor domestic production.

IX. Playbook: Business & Investing Lessons

Walking through GNFC's Bharuch complex with a longtime plant manager, you hear stories that MBA textbooks miss. "The government backing?" he says, watching steam rise from the acetic acid plant running at 150% capacity. "It's not what outsiders think. Yes, it helps with land and permits. But it also means every expansion needs political consensus, every layoff becomes front-page news, and profitability gets sacrificed for farmer votes." This tension—between commercial ambition and political reality—defines GNFC's playbook in ways that pure private sector comparables never capture.

The first lesson is that government backing operates as both shield and sword. The shield is obvious: preferential access to feedstock allocations, faster environmental clearances, and implicit guarantee that systemic importance prevents failure. During the 2015 crisis when GNFC posted its first-ever loss, banks didn't panic. Suppliers extended credit. Customers maintained orders. The government connection provided breathing room that private competitors wouldn't have enjoyed. But the sword cuts too—fertilizer prices frozen during election years, pressure to maintain employment despite automation opportunities, and strategic decisions filtered through political feasibility rather than pure economics.

Vertical integration in chemicals reveals nuanced truths. GNFC's methanol-to-acetic-acid chain works brilliantly—methanol feeds formaldehyde which creates formic acid while also supplying acetic acid production. When methanol plants shut due to import competition, having downstream facilities provided flexibility to source externally while maintaining higher-margin production. But integration also creates complexity. The TDI chain requires precise coordination across seven intermediate steps. One disruption cascades through the entire system. The lesson: integrate where chemistry creates genuine synergies, not just because you can.

Managing cyclicality in commodity chemicals requires accepting uncomfortable realities. GNFC learned that operational excellence can't overcome structural disadvantages—their methanol plants, despite technical competence, sit idle because Middle Eastern gas costs one-fifth of Indian prices. But they also discovered that local monopolies in specialized products (acetic acid, TDI) provide pricing power even during global downturns. The playbook: dominate niches where logistics costs or technical barriers provide natural protection, abandon commodities where you lack feedstock advantage.

The unexpected value of unrelated diversification challenges portfolio theory orthodoxy. (n)Code Solutions contributes just 3% of revenues but provided critical cash flow during chemical downturns. More importantly, it forced organizational learning—agile development methodologies from IT improved chemical plant maintenance scheduling, cybersecurity expertise protected industrial control systems, and digital customer interfaces enhanced chemical sales processes. Sometimes the best diversification is the one that makes no sense on paper.

Import substitution versus global competitiveness presents false choices. GNFC's success came not from replacing all imports but from selecting products where domestic production made enduring sense. Acetic acid works because India has methanol and growing demand. TDI succeeds because customers value supply security over marginal price differences. But methanol production failed because no amount of protection overcomes 5x feedstock cost disadvantages. The lesson: import substitution works when it aligns with competitive advantage, not when it fights it.

Capital allocation in capital-intensive industries requires patient courage. GNFC's major investments—the TDI complex, acetic acid expansion, digital infrastructure—took 5-7 years from conception to profitability. The TDI-2 plant, commissioned in 2014, didn't generate positive returns until 2017. Management had to defend these investments through multiple down cycles, political changes, and board skepticism. The companies that win in chemicals are those that can fund through cycles, not those that time them perfectly.

Technology partnerships and licensing reveal strategic subtleties. GNFC consistently chose proven technology from established partners over cheaper alternatives. The INEOS relationship for acetic acid, KBR for nitric acid, ThyssenKrupp for ammonia—each represents decades-long commitments. They pay premium licensing fees but receive continuous process improvements, operational support, and credibility with customers. In chemicals, the technology provider becomes a silent partner whose interests align with yours. Choose carefully and commit completely.

The portfolio approach suggests broader applicability. Rather than betting everything on one mega-facility, GNFC built multiple mid-sized plants across different products. When TDI stumbled, acetic acid compensated. When fertilizers faced subsidy delays, chemicals generated cash. This diversification within focus—multiple products but consistent capabilities—provides resilience without complexity. It's focused diversification, not conglomerate sprawl.

Government relations management emerges as a core competency. GNFC navigates between state government ownership, central government policies, and local political pressures. They've learned to frame commercial decisions in policy language—the INEOS JV emphasizes "Make in India" and forex savings, not profit margins. They time announcements around political cycles, accelerating projects before elections, deferring controversial decisions after. It's stakeholder management where the stakeholder can change laws.

The human capital paradox surprises—GNFC operates world-scale facilities with local talent. Their engineers, trained at regional colleges rather than IITs, master complex chemistry through apprenticeship and experience. The company runs extensive training programs, sponsors international assignments, and maintains technical libraries that rival universities. The lesson: in process industries, organizational learning matters more than individual credentials. Build capability systematically and locally.

Finally, GNFC demonstrates that building industrial champions in emerging markets requires accepting contradictions. You need government support but must operate commercially. You must import technology but develop local expertise. You should focus strategically but diversify tactically. You must optimize for profit but satisfy political objectives. Managing these paradoxes, rather than resolving them, becomes the meta-capability that enables everything else.

X. Analysis & Bear vs. Bull Case

The investment case for GNFC presents a fascinating study in contradictions. Here's a company that dominates multiple chemical niches yet generates returns that barely exceed its cost of capital. It enjoys government backing that ensures survival yet faces political constraints that prevent optimization. It has demonstrated operational excellence yet sits on idle assets worth hundreds of crores. Understanding GNFC requires embracing these paradoxes rather than resolving them.

The Bull Case:

GNFC's monopoly positions create moats that are widening, not narrowing. As India's sole acetic acid producer operating at 150% of nameplate capacity, they could double prices tomorrow and customers would still buy—the logistics costs of importing 1,000 MT from China exceed GNFC's entire production cost advantage. The new 600,000 MT INEOS joint venture will cement this dominance for decades. At $800 per ton, that's $480 million in annual revenue from a single product where they control pricing.

The TDI story is even more compelling. With 90% market share domestically and demand growing 10% annually, GNFC essentially controls the polyurethane foam supply chain for India's automotive and furniture industries. Every car made in India contains GNFC molecules. Every premium mattress depends on their consistent supply. The planned 50,000 MT expansion would generate ₹2,000 crores in additional revenue at current prices, with EBITDA margins exceeding 20% once operational.

Import substitution dynamics favor GNFC structurally. India's chemical imports exceeded $65 billion in FY2023, growing 8% annually. Every percentage point of import substitution represents massive opportunity. With government policies increasingly favoring domestic production—from anti-dumping duties to production-linked incentives—GNFC sits at the intersection of policy support and commercial viability. They don't need to capture much of this opportunity to double earnings.

The digital transformation through (n)Code Solutions provides optionality worth multiples of its current contribution. As India digitizes everything from land records to healthcare, authentication and security become critical infrastructure. (n)Code's position securing Aadhaar—the world's largest biometric database—creates credibility that money can't buy. International expansion into Africa and Southeast Asia, where similar digital identity projects are emerging, could make IT services GNFC's largest profit contributor within a decade.

Management quality shows in crisis response. The 2015 loss could have triggered political intervention, asset sales, or strategic drift. Instead, management used the crisis to accelerate operational improvements, cutting costs by ₹200 crores annually while maintaining capacity for recovery. They've demonstrated the ability to navigate both political pressures and market forces—a rare combination in public sector enterprises.

The valuation implies pessimism that seems overdone. Trading at 13x earnings and 1.2x book value, GNFC is priced like a declining commodity producer, not a growing specialty chemical company with digital optionality. Private sector peers trade at 20-25x earnings. Even adjusting for government ownership discount, the valuation gap seems excessive given GNFC's market positions and growth investments.

The Bear Case:

The return on equity tells the real story—9.98% over the last three years, barely covering the cost of capital. For all the operational excellence and market dominance, GNFC struggles to generate returns that justify investment. The methanol plants sitting idle represent ₹400 crores of dead capital. The TDI complex took five years to generate positive returns. This isn't value creation; it's capital allocation destruction with occasional bright spots.

Import competition remains an existential threat. Chinese producers, facing their own overcapacity, can dump products at prices GNFC can't match. The 2015-2016 TDI crisis, when imports crashed prices below GNFC's production costs, could repeat anytime. Anti-dumping duties provide temporary relief but can't overcome structural disadvantages—Chinese plants are newer, larger, and have access to cheaper feedstock. GNFC survives on regulatory protection that could vanish with trade agreements.

Fertilizer subsidy dependency creates earnings volatility that financial engineering can't solve. With fertilizers still contributing 30% of revenues, delayed government payments can cripple cash flows. The new direct benefit transfer system improves timing but doesn't address the fundamental issue: GNFC's fertilizer business exists at political whim. One policy change could transform profits into losses overnight.

Limited pricing power constrains margins even in monopoly products. Yes, GNFC is India's only acetic acid producer, but customers know imports provide alternatives. They can't push prices beyond import parity plus logistics costs—a ceiling that compressed margins whenever global prices fall. The monopoly is geographic, not economic, providing protection but not pricing power.

The methanol paradox exposes strategic confusion. Management insists the plants could restart within 60 days if economics improve, but economics haven't improved in seven years and won't given Middle Eastern gas cost advantages. Meanwhile, ₹400 crores of capital generates zero returns while maintenance costs accumulate. It's the sunk cost fallacy played out in industrial scale—an inability to accept mistakes and move forward.

Government ownership creates invisible constraints that compound over cycles. Salary caps prevent hiring top talent from private sector. Procurement rules slow decision-making. Political considerations override commercial logic. These constraints don't appear in financial statements but shape every strategic decision. GNFC competes against private companies with one hand tied behind its back.

The commodity cycle vulnerability persists despite diversification. Chemicals contribute 70% of revenues, but they're still commodity chemicals subject to global supply-demand dynamics. When the next downturn arrives—and it will—GNFC's fixed costs and government constraints will prevent the aggressive restructuring private competitors undertake. They'll survive but won't thrive.

ESG concerns lurk beneath sustainability rhetoric. Chemical production generates significant emissions, consumes massive water resources, and produces hazardous waste. As environmental regulations tighten and customers demand cleaner supply chains, GNFC's older plants face expensive retrofitting or closure. The capital required for environmental compliance could exceed growth investment needs, constraining returns further.

The Verdict:

GNFC embodies the challenges and opportunities of industrial development in emerging markets. The bull case rests on structural advantages—monopoly positions, import substitution tailwinds, and digital optionality. The bear case highlights structural disadvantages—low returns, government constraints, and commodity exposure. Neither narrative is complete; both are true simultaneously.

For investors, GNFC represents a bet on India's industrial ambitions with a margin of safety from government backing but limited upside from ownership structure. It's a value trap for growth investors and a growth trap for value investors. The company will likely continue generating modest returns, occasionally surprising with digital success or disappointing with commodity collapses, but never quite fulfilling the promise its market positions suggest. In investing, as in chemicals, catalyst matters—and GNFC lacks the catalyst to transform potential into performance.

XI. Epilogue & "If We Were CEOs"

Standing at the crossroads of GNFC's next decade, the strategic choices write themselves in the tension between what's possible and what's permissible. If we were CEOs—a thought experiment worth indulging—the path forward would require equal parts courage and pragmatism, innovation and tradition, disruption and continuity.

The methanol question demands resolution, not perpetual deferral. Those three idle plants represent not just ₹400 crores of dead capital but organizational paralysis—an inability to admit failure and move forward. The strategic response isn't restart or write-off but transformation. Convert one plant to bio-methanol production using agricultural waste, positioning for the renewable chemicals future. Repurpose another for specialty chemicals that leverage existing infrastructure but escape commodity dynamics. Demolish the third, using the space for the INEOS acetic acid expansion. Turn stranded assets into strategic options.

Chemical portfolio optimization requires brutal honesty about competitive advantage. GNFC should double down where it has structural moats—acetic acid, TDI, concentrated nitric acid—and exit where it doesn't. The commodity chemicals that generate volume but destroy value need strategic buyers who can achieve global scale. Use divestment proceeds to fund specialty chemical ventures where GNFC's operational excellence and government relationships create genuine differentiation. Think specialty, not commodity; margins, not volumes.

International expansion deserves serious consideration but not conventional execution. Rather than building plants abroad, export Indian operational expertise. GNFC engineers who've made 40-year-old plants run at world-class efficiency have knowledge worth monetizing. Create a technical services subsidiary that helps emerging market chemical companies optimize operations. License the (n)Code Solutions platform to African governments building digital identity systems. Become an expertise exporter, not just a chemical producer.

The sustainability transformation can't remain peripheral—it must become central. India's net-zero commitments by 2070 will reshape chemical production. GNFC should lead, not follow. Establish India's first green ammonia facility using renewable electricity for hydrogen production. Develop carbon capture systems for existing plants, turning CO2 emissions into feedstock for downstream chemicals. Create a circular economy hub where waste from one process becomes input for another. Make sustainability a competitive advantage, not compliance burden.

Digital integration should extend beyond (n)Code Solutions into core operations. Deploy AI for predictive maintenance, reducing downtime and extending asset life. Build digital twins of chemical plants, optimizing processes in simulation before implementation. Create blockchain-based supply chain systems that track molecules from production to end-use, providing transparency that commands premium pricing. Make GNFC the most digitally advanced chemical company in India, leapfrogging global giants through focused innovation.

Government relationship management needs sophisticated evolution. Rather than fighting political constraints, align with policy objectives. Position expansions as employment generators in election years. Frame environmental investments as public health initiatives. Present digital ventures as Digital India enablers. Become so strategically important to government objectives that political support becomes structural, not situational.

The capital allocation framework requires zero-based redesign. Every rupee should compete for returns—whether invested in chemical plants, digital ventures, or returned to shareholders. Establish hurdle rates that reflect true cost of capital, not government-subsidized rates. Create internal venture funds that let entrepreneurial employees pursue adjacent opportunities. Institute buyback programs when stock trades below intrinsic value. Make capital allocation a competitive advantage, not administrative function.

The human capital strategy needs revolutionary thinking within evolutionary constraints. GNFC can't match private sector salaries but can offer unique development opportunities. Create an internal university that partners with IITs for advanced chemical engineering programs. Establish international rotation programs with technology partners like INEOS and KBR. Build an alumni network that becomes India's chemical industry talent pipeline. Make GNFC the learning organization that ambitious engineers join for experience, even if they leave for compensation.

ESG transformation should anticipate rather than respond to regulations. Set science-based targets for emission reduction that exceed government mandates. Establish water recycling systems that achieve zero liquid discharge. Create biodiversity offset programs that make GNFC carbon-negative by 2040. Publish integrated reports that link environmental performance to financial returns. Lead India's chemical industry toward sustainability, setting standards others follow.

The strategic North Star should be becoming India's BASF—not in size but in scope, innovation, and importance. A company that defines Indian chemical industry ambitions while competing globally. A bridge between government policy and market reality. A trainer of talent, developer of technology, and creator of value that transcends financial returns.

This transformation won't be easy. Government ownership creates constraints that can't be wished away. Commodity cycles will continue causing volatility. Import competition won't disappear. But GNFC has survived and occasionally thrived through five decades of India's economic evolution. It has operational excellence that matches global standards, market positions that provide strategic flexibility, and digital capabilities that offer unprecedented optionality.

The next decade will determine whether GNFC remains a solid but unspectacular public sector enterprise or transforms into India's chemical champion for the 21st century. The ingredients exist—operational expertise, market position, government support, and financial strength. What's needed is catalytic leadership that can synthesize these elements into something greater than their sum.

If we were CEOs, we'd embrace GNFC's contradictions rather than resolve them. Use government backing to take risks private companies can't. Leverage operational excellence to enter adjacent markets. Deploy digital capabilities to reimagine chemical production and distribution. Build on the foundation previous generations created while preparing for futures they couldn't imagine.

The ultimate metric wouldn't be ROE or stock price but strategic importance—becoming so essential to India's industrial ecosystem that success becomes inevitable. It's an ambitious vision for a company that started as a fertilizer producer in Gujarat. But then again, GNFC's history is full of unlikely transformations. The next one might be the most improbable—and important—yet.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube