GMR Airports: The Sky-High Bet on India's Infrastructure

I. Introduction: The Gateway to the Subcontinent

Walk through the soaring glass atrium of Terminal 3 at Indira Gandhi International Airport in New Delhi on a busy Tuesday evening, and the scale starts to land in a physical way. Marble floors stretch toward distant gates. The retail concourse — duty-free shops lit up like a Singaporean luxury mall, with Hermès, Bvlgari and Johnnie Walker arrayed under careful spotlights — feels less like an airport than a downtown promenade with airline gates attached. Outside, the runway lights blink in the haze, dispatching well over a thousand aircraft movements a day at India's busiest single-asset gateway.1

What you are standing inside is not run by the Government of India. It is operated, under a thirty-year concession with a thirty-year extension option, by a private company that three decades ago was a sleepy jute-and-sugar trader headquartered in a dusty Andhra Pradesh railway town called राजम Rajam.2

That company is GMR Airports Infrastructure Limited, listed in Mumbai under the ticker GMRAIRPORT.NS. Its story, in many ways, is the story of India's last twenty years: a small-town entrepreneur winning the right to operate the country's most important infrastructure asset, then nearly losing the empire to a balance sheet groaning with debt, and ultimately persuading one of the world's most prestigious airport operators — the French state-backed Aéroports de Paris — to bet over ten thousand crore rupees on his comeback.

The thesis worth interrogating today is deceptively simple. Is GMR Airports a regulated utility, a real-estate developer, or a retail conglomerate that happens to own runways? Because depending on which lens you use, the same business looks completely different. As a utility, it earns a guaranteed post-tax return on equity on its aero asset base under regulation by the Airport Economic Regulatory Authority. As a developer, it sits on more than two thousand acres of contiguous commercial land at the gateways to Delhi and Hyderabad. As a retailer, it has a captive footfall of tens of millions of Indian flyers a year, many on their first international trip and primed to spend.2

That ambiguity is the source of both its appeal and its complexity. Over the next two-and-a-half hours we will trace the arc from G. M. Rao's family jute mill to a globally relevant airport platform operating, building, or bidding for terminals across India, the Philippines, Indonesia, and Greece.[^3] We will walk through the pivot from agri-trading to power, the audacious 2006 airport bids that changed the company forever, the debt-fuelled near-death experience of the mid-2010s, the demerger that finally let the airport business fly free, and the question now hanging over every long-term investor in Indian aviation: in a duopoly increasingly defined by GMR versus अदाणी समूह the Adani Group, who wins the next decade of the world's fastest-growing aviation market?[^4]

Buckle in. This one is going to take a while.

II. Origins: From Jute Mills to Power Plants

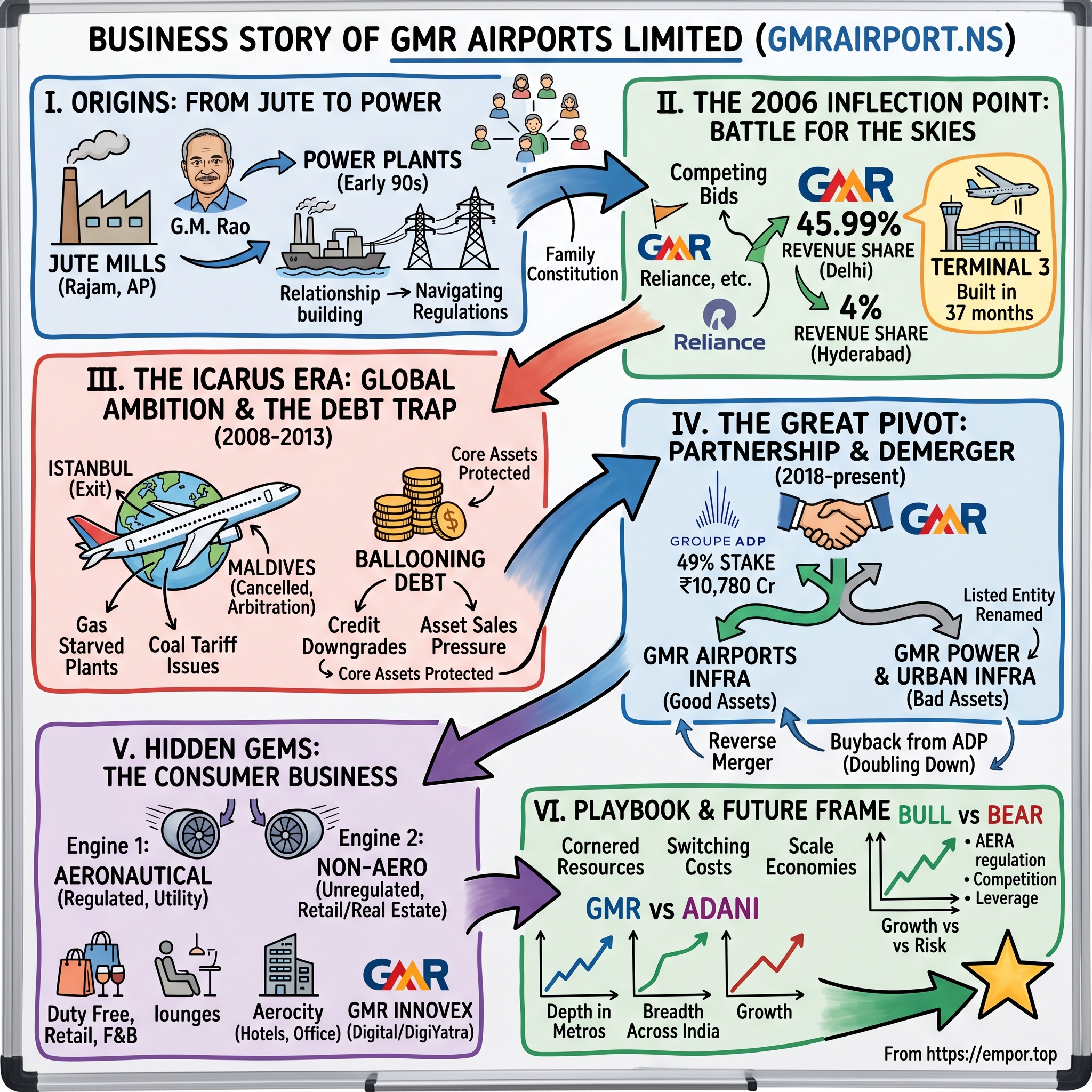

To understand GMR, you have to start with a man who in the late 1970s was running a jute mill in a town most Indians have never visited. Rajam, in the Srikakulam district of northern Andhra Pradesh, is the kind of place where the railway station is the social centre and the most exciting building is the local cooperative bank. Grandhi Mallikarjuna Rao — universally known as G. M. Rao — was raised there into a family of small traders, trained as a mechanical engineer at Andhra University, and then did what any ambitious young engineer in 1970s India did with limited capital. He started a small industrial business. In Rao's case, that was a jute mill, followed by a small bank, and eventually rice and sugar trading.[^3]

For roughly fifteen years, Rao operated in the shadows of Indian commerce. Nothing about this period suggested an airport empire was on the way. What it did do was teach him three lessons that would define every subsequent move: how to assemble capital from local relationships in a country where institutional finance was scarce, how to operate a license-heavy business under the lingering bureaucracy of लाइसेंस राज the License Raj, and how to build trust with public-sector banks that would later finance billion-dollar concessions.

The pivot came in the early 1990s. After the Narasimha Rao liberalization opened Indian infrastructure to private capital, Rao divested the small bank he had built and used the proceeds to enter the power sector, betting that a country running on chronic electricity shortages would eventually let private operators generate it.[^3] The first asset was a barge-mounted plant on the Kakinada coast — an unglamorous start, but it gave him a foothold in independent power production at a time when the sector was being defined deal by deal in New Delhi.

The early power years did two things. First, they gave GMR practical experience in the dark arts of Indian infrastructure: navigating central and state regulators, negotiating power purchase agreements with creditworthy and not-so-creditworthy state electricity boards, and structuring project finance with consortia of Indian and international lenders. Second, and more importantly, the power business gave Rao a relationship with a generation of Indian bureaucrats and policymakers — relationships that would prove invaluable when the airport bids opened a decade later.

By the early 2000s, GMR had layered highways and an energy trading arm on top of the original power assets. Yet Rao was already restless about the bigger question every Indian family business eventually faces: what happens to all this when he is gone? In a country where the so-called "third-generation curse" has dismantled storied conglomerates, Rao took the unusual step of drafting a written family constitution.[^5] Sons, son-in-law and brothers were given clearly delineated zones of responsibility, with explicit rules about who could enter the management track, what education was required, and how disputes would be arbitrated. It was, in Indian business circles, almost taboo to put any of this on paper. Rao did it anyway, and it would later prove essential to the orderly handover of the airport business — first to his son-in-law Srinivas Bommidala and ultimately to the daily running of the platform under his son ग्रंथी किरण कुमार Grandhi Kiran Kumar.[^5]

The "Work is Worship" credo — emblazoned on GMR plant gates from Vemagiri to Vizag — sounds like the kind of corporate hagiography that doesn't survive contact with quarterly earnings. In Rao's case, though, it was the connective tissue between an engineer who didn't enjoy Mumbai cocktail circuits and a workforce that had to deliver concrete at remote sites under monsoon conditions. By the time the Indian government opened up its airports in the mid-2000s, GMR had become exactly the kind of company that knew how to pour foundations on schedule — and exactly the kind of company that would soon be tested to its breaking point.

III. The 2006 Inflection Point: The Battle for the Skies

For decades, Indian airports were the punchline of every business traveller's horror story. Delhi's old Palam terminal was a cramped, low-ceilinged warren where international arrivals waited an hour for baggage in air so warm that suit jackets came off the moment passport control was cleared. Mumbai was worse. Hyderabad's Begumpet was a charming relic that doubled as an Air Force base. India in 2003 was a country with a fast-growing middle class but a Soviet-era aviation backbone — which is precisely why the privatization decision, when it finally came, was such a watershed.

After years of internal debate, the Manmohan Singh government greenlit the privatization of Delhi and Hyderabad through public-private partnerships, with the Airports Authority of India retaining a minority stake.[^6] Two greenfield concessions — for Bengaluru and Hyderabad — and two brownfield ones — Delhi and Mumbai — would be tendered. The terms, when they were published, were striking even by global standards: thirty-year concessions, with a thirty-year extension option, on a build-operate-transfer basis.[^6] Sixty years is not a contract; it is a generational lease on national infrastructure.

Five consortia lined up for Delhi. The GMR-led group brought together Germany's Fraport, Malaysia Airports and India Development Fund as partners. The reigning industrial heavyweight, Reliance, then under Anil Ambani, partnered with Mexico's ASA. A third bid was anchored by DS Constructions. Within the Indian establishment, GMR was the dark horse. Reliance had brand and bank balance. GMR had jute mills.

When the financial bids opened, GMR won Delhi by committing to share an unusually aggressive 45.99% of gross revenue with the government for the life of the concession — a number so steep that even seasoned infrastructure analysts blinked.[^7] Hyderabad, won under a separate process, was structured on a much more modest 4% revenue share. The decision was rational only if GMR believed, against the conventional wisdom of the time, that Indian air traffic was about to compound at double-digit rates for two decades. They believed exactly that, and they bet the company on it.

What happened next is the part that any operator who has ever attempted Indian infrastructure construction will tell you was the real miracle. Delhi's new Terminal 3 — at the time the sixth-largest passenger terminal in the world — was built in roughly thirty-seven months, in time for the October 2010 Commonwealth Games.[^3] India had built nothing of comparable scale and complexity before. Most international aviation observers expected GMR to miss the deadline; missing it would have been a national embarrassment with the Games already on the calendar.

They didn't miss it. Terminal 3 opened on schedule, and the execution did two things at once. It validated GMR's claim that an Indian private operator could build to global standards. And it gave G. M. Rao the political and reputational capital to push for international expansion, just as the balance sheet was beginning to creak under the cost of all this concrete.

The deeper strategic insight — the one that gets lost in the construction story — is what those 2006 concessions actually were. A sixty-year monopoly on a metropolitan airport is, in Hamilton Helmer's framework, a textbook Cornered Resource: a uniquely valuable asset that competitors cannot replicate.2 Building a second international airport at Delhi is functionally impossible without state action; even Noida, the new entrant, sits forty kilometres out. That single insight — that the concession itself was the asset, and everything else was an option on top of it — is what would eventually attract Aéroports de Paris a decade and a half later.

But before that rescue arrived, GMR was going to make almost every mistake an emerging-market infrastructure company can make.

IV. The Icarus Era: Global Ambition & The Debt Trap

There is a particular kind of corporate intoxication that hits emerging-market champions in their first decade of global success. You execute one impossible project, the financial press anoints you a national champion, foreign banks line up to lend, and suddenly the world feels smaller than it actually is. From roughly 2008 through 2013, GMR lived inside this hall of mirrors.

The first international move was Istanbul. GMR partnered with Malaysia Airports and Limak Holding to win the operating rights for Sabiha Gökçen, Istanbul's secondary airport on the Asian side of the Bosporus.[^3] The bet was that Istanbul, with its booming Turkish carrier base, would become a regional crossroads between Europe, the Middle East and Central Asia. The bet was even right in the long run — Sabiha Gökçen is now one of the world's busiest secondary airports — but GMR didn't stay around to enjoy the upside. With the Indian balance sheet straining, GMR exited the Istanbul concession to Malaysia Airports in 2014.[^3] It was the right sale for the cash-flow situation and arguably the wrong sale for the long-term thesis. Both can be true at once.

Then came the Maldives. A GMR-led consortium won the right to modernize and operate Malé's Ibrahim Nasir International Airport in 2010, structured as the largest single foreign direct investment in the country's history.[^3] Then, in late 2012, the new Maldivian government under Mohamed Waheed unilaterally cancelled the concession, declaring it void from inception.[^3] GMR's staff were given seven days to leave the country. The episode dragged through international arbitration in Singapore, where GMR ultimately prevailed and was awarded substantial damages, payable over years.[^3] The cash amount mattered, but the lesson mattered more. Political risk in small, transitioning democracies could vaporize a concession even when the contract paperwork was airtight.

Domestically, the damage was being done by businesses that had nothing to do with airports. GMR had built out a sprawling power portfolio: gas-fired plants in Andhra Pradesh starved of fuel after the KG-D6 gas disappointments, coal-fired plants whose tariffs were locked in below the realities of imported coal after Indonesia's 2010 export policy shift, and a highways business carrying its own working capital burden.3 The conglomerate had become exactly what every Indian business school case study warned against — an unfocused mid-cap competing simultaneously against pure-play giants in three separate industries.

By the middle of the 2010s, consolidated net debt at GMR Infrastructure had ballooned into the tens of thousands of crores, with interest costs eating up the lion's share of operating cash flow.3 The market did what markets do to "house of debt" stories. The stock spent the better part of half a decade trading like a perpetual option on survival. Credit rating agencies repeatedly downgraded individual project-level debt. Public-sector banks with concentrated exposures pressed for asset sales. The Indian financial press, which had crowned Rao a national champion in 2010, now ran cover stories questioning whether the family would lose the airport assets to lenders altogether.

What is striking, in hindsight, is what GMR did not do during these years. It did not panic-sell the airport concessions. It did not allow Delhi or Hyderabad to slip into operational underperformance even as the parent balance sheet imploded. Aero traffic kept growing. Non-aero revenue per passenger kept inching up. The asset that mattered most — the one Helmer would have called the Cornered Resource — was kept clean. Everything else was sacrificed to protect it.

That discipline mattered, because by 2018 the Indian aviation cycle was turning sharply. Domestic passenger traffic was compounding at double-digit rates and international capacity at the Indian metros was structurally undersupplied.[^4] The world's most sophisticated airport operator was about to come knocking.

V. The Great Pivot: The ADP Partnership & Demerger

The conversations that ultimately reshaped the company began quietly. Augustin de Romanet, the chairman and chief executive of Groupe ADP — the French state-backed operator of Charles de Gaulle and Orly, and one of the few truly global airport platforms — opened a dialogue with the Rao family.4 ADP had been searching for years for an Asian growth engine. India offered the structural tailwinds the European market could no longer provide: a population larger than Europe and North America combined, a per-capita flying penetration still a fraction of Brazil's or Turkey's, and a regulatory framework — for all its complexity — that actually permitted private operation of metropolitan airports.

The deal that emerged, and that closed in tranches across 2020 and 2021, gave Groupe ADP a 49% economic stake in GMR Airports Limited for total consideration of approximately ₹10,780 crore.4 The structure was carefully calibrated. ADP got minority economic interest and meaningful board representation but no operating control. GMR retained the chair and the management franchise. Crucially, ADP also committed an earn-out tied to traffic recovery — money that would flow only if Indian aviation came back the way both parties expected.4

The strategic logic was almost too clean. GMR got a globally respected industrial partner whose presence on the cap table made every lender, regulator and counterparty more comfortable. ADP got a foothold in what would, by mid-decade, be the world's third-largest aviation market.[^4] And both got an alignment device — neither could exit cleanly without the other's consent — that locked them into operating the business together for at least a decade.

But the deal was only half the pivot. The other half was structural. The board approved a composite scheme of arrangement that separated GMR's airport business from its energy, EPC and urban infrastructure operations.5 After regulatory and court approvals, the demerger took effect, with the listed entity renamed GMR Airports Infrastructure Limited and a separate listing, GMR Power and Urban Infra Limited, set up to house the "bad" assets.5

For shareholders, the demerger was a revelation. For the first time, the market could price the airport platform on its own multiples — comparable to global peers like Aena, Fraport, or Airports of Thailand — without the discount imposed by stranded gas plants and arbitration-prone toll roads. The stock's re-rating began almost immediately. The pure-play structure also unlocked a strategic move that had been impossible inside the conglomerate: a reverse merger of GMR Airports Limited (the operating company in which ADP held its 49%) into the listed parent. After that scheme was completed, ADP became a direct shareholder of the listed entity alongside the Rao family.6

Inside the executive suite, the era is defined by Grandhi Kiran Kumar. G. M. Rao's son — an engineer with an MBA from Purdue — took over as managing director of the airports business as the demerger was being finalized.2 His incentive structure, disclosed in the FY24 annual report, ties a meaningful share of total compensation to performance-linked metrics centred on non-aero revenue growth and return on equity.2 The exact percentage is less interesting than the fact that an Indian family-controlled business voluntarily disclosed the metric at all, an act of transparency that would have been almost unthinkable in 2010.

Which brings us to the most recent chapter, and the one that has surprised even seasoned watchers. Beginning in early 2024, GMR began buying back tranches of equity from ADP, starting with a transaction reported at roughly USD 1 billion in headline value.7 The optics were initially confusing — why would you bring in a strategic partner and then immediately start buying them out? — until you looked at the math. By the time the buyback was negotiated, the implied valuation of the airport platform was several multiples of what ADP had paid in 2020. Buying back equity at expensive prices is rational only if the family believes the next decade looks even better. G. M. Rao, now in his mid-seventies, was doubling down with personal capital on the runway he had spent twenty years building.7

VI. Hidden Gems: The Consumer Business Within the Airport

If you have spent any time in a modern hub airport — Changi, Incheon, Dubai International — you already know the secret of contemporary aviation economics. The runway is the loss leader. The mall is the business. And nowhere is that truer than at the Indian metros, where the regulatory framework explicitly caps aero returns but lets the non-aero side run on commercial terms.

Inside the terminal, GMR's commercial revenue is split across a familiar palette: duty-free, retail, food and beverage, lounges, advertising, car parking and ground transport.[^13] The duty-free business at Delhi is now among the largest by passenger-spend outside the Gulf hubs, helped by a single structural fact about Indian travellers: a large share of international departures from Delhi are long-haul to the Gulf, Europe, North America and Southeast Asia — and bringing back gifts is a culturally entrenched practice that converts directly into per-passenger basket size. The result is that Indian non-aero spend per international passenger has been growing at high single digits to low double digits annually, with management treating the gap to global hubs as the central long-duration growth lever.2

But the real prize is outside the terminal building. The Delhi concession came bundled with a contiguous land bank that GMR has spent the better part of a decade developing as GMR Aerocity.[^14] Hotels — Andaz, JW Marriott, Pullman, Holiday Inn — anchor the existing footprint, and the next phase, branded internally as "Aerocity 2.0," extends that footprint with Grade A office space, premium retail and entertainment.[^14] Hyderabad has its own version under the GMR Aerotropolis umbrella, with a similar mix of hospitality, IT parks, healthcare and education campuses. Combined, the contiguous land bank that GMR controls under the airport concessions runs into thousands of acres — a real-estate position any pure-play developer in India would consider career-defining if they could acquire it.

The framing matters. If you think of GMR as a utility, the regulatory price cap on aero charges feels like a ceiling on the equity story. If you think of it as a real-estate developer with airport-driven captive demand, that same price cap becomes a floor — the protected utility return underwrites the cost of capital, while the upside lives in unregulated commercial real estate and retail. Management talks about this explicitly in investor presentations as the "twin engine" model.2

Layered on top is a digital push. GMR Innovex, the group's technology arm, has been integrating biometric boarding, baggage tracking and the government-backed डिजी यात्रा DigiYatra facial recognition system across its terminals.2 The strategic value isn't the technology itself, which is well understood. It is the data exhaust. Knowing what a passenger does between security and boarding makes you better at pricing retail concessions, scheduling lounges and selling advertising. The same playbook is what made Changi's commercial yield the highest in Asia.

Internationally, the portfolio is being reshaped. Cebu, in the Philippines, was monetized. Maldives is gone. The new bets are Crete's Kasteli, a greenfield airport in Greece where GMR is a consortium partner, and the operating concession at Indonesia's Kualanamu International Airport at Medan.[^3] These are deliberately smaller bets than the original Istanbul–Maldives swing. The lesson from the Icarus era has been learned. The new international strategy is: take minority or co-developer positions in strategically located gateways where political risk is manageable, and let the Indian portfolio carry the equity story.

The contrast with the rival across town could not be sharper. The Adani Group, which entered airports only in 2019 by winning six AAI concessions in a single round, has built a domestic-only portfolio anchored by Mumbai's Chhatrapati Shivaji Maharaj International and the under-construction Navi Mumbai International Airport.[^4] Adani's model is breadth across India; GMR's model is depth in two Indian metros plus selective international optionality. Both can work. The question for the next decade is which model attracts more flying capacity per rupee of capex deployed.

VII. Playbook: Business & Strategy Lessons

Step back from the operating detail and the playbook starts to come into focus. Apply Hamilton Helmer's 7 Powers framework and GMR scores meaningfully on three of them, marginally on a fourth, and not at all on the rest.

The Cornered Resource is the concession itself. Sixty-year exclusive operating rights on a single-runway metropolitan gateway are functionally non-replicable.[^6] Even the much-discussed Noida International Airport, being built by Zurich Airport, sits at a distance from Delhi that makes it complementary to IGI rather than a substitute for the foreseeable future. Hyderabad has no challenger inside a hundred-kilometre radius. The Switching Cost is the airline's. Once an airline has based crews, maintenance, slot portfolios and frequent-flyer infrastructure at a hub, the cost of moving is staggering — which is why hub airports tend to retain anchor carriers across decades. Scale Economies show up in two places: in technology and procurement, where the ADP partnership gives GMR access to global airport systems at a fraction of standalone cost; and in the non-aero retail concessions, where larger passenger volumes attract better brand partners on better commercial terms.

Where the framework is more equivocal is on Counter-Positioning — there is no obvious incumbent business model that the company is uniquely structured to disrupt — and Process Power, which is harder to verify externally. Branding is a non-factor. Network Effects exist in a weak sense for the duty-free and retail business, but not in the strong, multi-sided form you see in, say, a payment network.

Run Porter's Five Forces and the picture sharpens. Bargaining power of buyers — in this case airlines and passengers — is weak, because neither can take their landing slot elsewhere. Bargaining power of suppliers is mixed; key airport equipment vendors are global oligopolies, but in any given concession cycle the construction labour market is highly competitive. The threat of substitutes is real only over very long horizons; India's high-speed rail build is decades from displacing aviation between metros. The threat of new entrants is constrained by the concession structure. And the intensity of competitive rivalry — the most interesting force in the Indian context — is concentrated almost entirely on the bidding for new concessions, where Adani and GMR slug it out for every new tender that comes to market, and where ADP's presence on the GMR cap table is an under-appreciated competitive advantage.[^4]

The deeper capital-allocation lesson from GMR is about partner selection. There is a meaningful difference between bringing in a financial sponsor — a private equity fund whose mandate is to exit in five to seven years — and bringing in a strategic partner whose interests are structurally aligned with the long-term thesis. Earlier rounds of capital raising in the airport vehicle, with names such as Tata, GIC and SSG Capital in the mid-2010s, were largely financial in nature; the ADP transaction was industrial.4 The exit overhang is different, the operational support is different, and the regulatory signalling — to AERA, to DGCA, to lenders — is different. For long-term holders of any infrastructure platform, who is on the cap table next to you is almost as important as what you paid.

A small but material second-layer note belongs here. The demerger collapsed a long-running accounting tangle in the parent: minority interests, deferred tax assets that had built up against unpaid liabilities at non-airport subsidiaries, and contingent obligations from the Maldives and KG-gas disputes were finally reallocated to the right entity.5 For credit analysts, the listed airport entity post-demerger is a meaningfully cleaner credit than the predecessor, and rating actions have begun to reflect that, even as new capex pushes leverage back up.

VIII. Myth vs Reality and the Bull–Bear Frame

Several persistent narratives swirl around GMR. They are worth fact-checking before laying out the bull and bear cases.

The first myth is that GMR Airports is "just" a regulated utility with limited equity upside. The reality is more nuanced. The regulated post-tax return on equity applies to the aeronautical asset base, which is roughly half to two-thirds of total invested capital depending on the airport.[^15] Non-aero — retail, food and beverage, advertising, car parks, lounges, real estate — is essentially unregulated and routinely earns multiples of the regulated return.[^13] The blended return on the platform, properly measured, is structurally above the headline cap.

The second myth is that the GMR–Adani rivalry is zero-sum. The reality is that India's air traffic growth is so steep that both can scale meaningfully without taking share from each other in their core hubs. Where they do compete head-to-head is in greenfield concessions — the Noida bid won by Zurich, the Navi Mumbai construction held by Adani, and future tenders for tier-two cities. Even there, the constraint on each operator is balance sheet capacity, not market access.[^4]

The third myth is that Indian airport regulation is implacably hostile to private capital. The track record of AERA is mixed and litigation has been chronic, but the underlying compact — a generous regulated return on equity in a country whose risk-free rate has spent most of the last decade between six and seven percent — is, on its face, a workable bargain.[^15] The friction is in implementation: tariff orders are appealed, true-ups lag, and individual control periods can be contentious. The architecture itself is intact.

The bull case writes itself once those myths are set aside. India is on track to be the world's third-largest aviation market by passenger volume by the late 2020s.[^4] GMR owns the best gateway in the largest metropolitan market (Delhi), a second monopoly in a fast-growing southern hub (Hyderabad), a new greenfield concession at Bhogapuram in Andhra Pradesh under active construction8, and consortium positions in Crete and Medan.[^3] Non-aero revenue per passenger remains a fraction of comparable international hubs — at Indian airports it runs in low single digits in US dollar terms versus the much higher levels at Changi or Dubai International — which is itself the bull thesis in one number.2 Close that gap halfway and the platform's EBITDA expands materially. Layer on the Aerocity real estate monetization and the optionality on additional Indian concessions, and the long-duration compounder thesis is intact.

The bear case is equally legible. Regulatory risk is real; if AERA decides to tighten the calculation of the asset base or the cost-of-equity assumption, equity returns could compress.[^15] Capex intensity is high — Delhi's continuing expansion, Hyderabad's expansion, and the multi-phase Bhogapuram build together represent commitments in the thousands of crores that will keep free cash flow constrained for several years.8 Competitive intensity for the next round of concessions, against an Adani Group with deeper pockets and equally aggressive bidding behaviour, could erode returns on incremental bids.[^4] And the buyback of ADP equity, however strategically defensible, leaves the listed entity carrying incremental leverage at exactly the moment when global rate cycles are normalizing.7

For investors trying to monitor the business between annual reports, three key performance indicators do most of the work. First, non-aero revenue per international passenger — the single best gauge of the consumer-business thesis. Second, the pace of commercial property monetization across Aerocity and the Hyderabad land bank — the real-estate optionality made concrete. And third, leverage at the listed entity level relative to platform EBITDA — the de-risking story. Watch those three lines across quarters and you are tracking the substance of the GMR story rather than the noise around it.

A short word on second-layer diligence. ESG ratings for the listed entity have been improving as the airport-only structure simplifies disclosure, even as construction-phase capex keeps the embodied-carbon profile elevated. The auditor reports across recent years have been clean, but the company carries meaningful disclosed contingent liabilities tied to historical disputes — a reminder that even a re-rated platform still carries legacy debris from the conglomerate years.2 Concentrated promoter ownership remains the dominant feature of the cap table, with ADP and institutional shareholders the principal counterweights.6

IX. Epilogue & Conclusion

There is a particular kind of Indian business story where the founder, well into his seventies, sits in a glass-walled office somewhere in Bangalore or Gurgaon, looks out at the runway he won the right to operate two decades ago, and decides whether the empire he built will outlive him. G. M. Rao is squarely in that chair.[^5] He has spent the last five years deliberately institutionalizing what he built: a written family constitution, a demerged listed entity, a globally respected strategic partner on the cap table, and a successor in his son already running the franchise day-to-day. The transition is more complete than at almost any comparable Indian conglomerate of similar vintage.

The bigger arc is about what GMR's existence means for India. When the country privatized Delhi and Hyderabad in 2006, the unstated question was whether an Indian private operator could run mission-critical national infrastructure at global standards. Two decades later, the answer is unambiguous. Terminal 3 is benchmarked alongside Singapore and Dubai in passenger surveys, and the model has been copied with variations by Adani in Mumbai and Bengaluru.[^4] Whether GMR continues to compound at the pace of the last five years depends on the boring stuff — execution, capital discipline, regulatory equilibrium — rather than any single dramatic event.

There is also a quietly radical implication in the aerotropolis idea. If you take the Delhi and Hyderabad commercial development plans to their logical conclusion, India will, within a decade, have two genuinely new urban cores built from scratch around airports, housing offices, hotels, conference space, retail, healthcare campuses and entertainment districts.[^14] Singapore did this around Changi. Dubai did it around DXB. Atlanta and Hong Kong followed. For India, GMR's Aerocity may end up being a more lasting urban legacy than any single terminal.

The final framing is this. GMR Airports is no longer a story about whether the company can survive. It survived. It is now a story about what the next twenty years of Indian aviation, retail and urban real estate look like — and whether the platform that built itself in the last twenty years can compound through the next twenty without losing the discipline that finally arrived in the demerger.

The runway is open. The traffic is coming.

References

References

-

Annual Report FY 2023-24 — GMR Airports Infrastructure Limited ↩↩↩↩↩↩↩↩↩↩

-

Investor Presentation Q3 FY25 — GMR Airports Platform Performance ↩↩

-

NSE India — Corporate Filings for GMR Airports Infrastructure (GMRAIRPORT) ↩↩

-

Reuters — GMR Group to buy back stake from Groupe ADP in airport unit, 2024-03-19 ↩↩↩

-

Business Standard — GMR's Bhogapuram Airport progress and construction milestones ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube