GMM Pfaudler: The Subsidiary That Swallowed Its Global Parent

I. Introduction: The "Tail Wags the Dog"

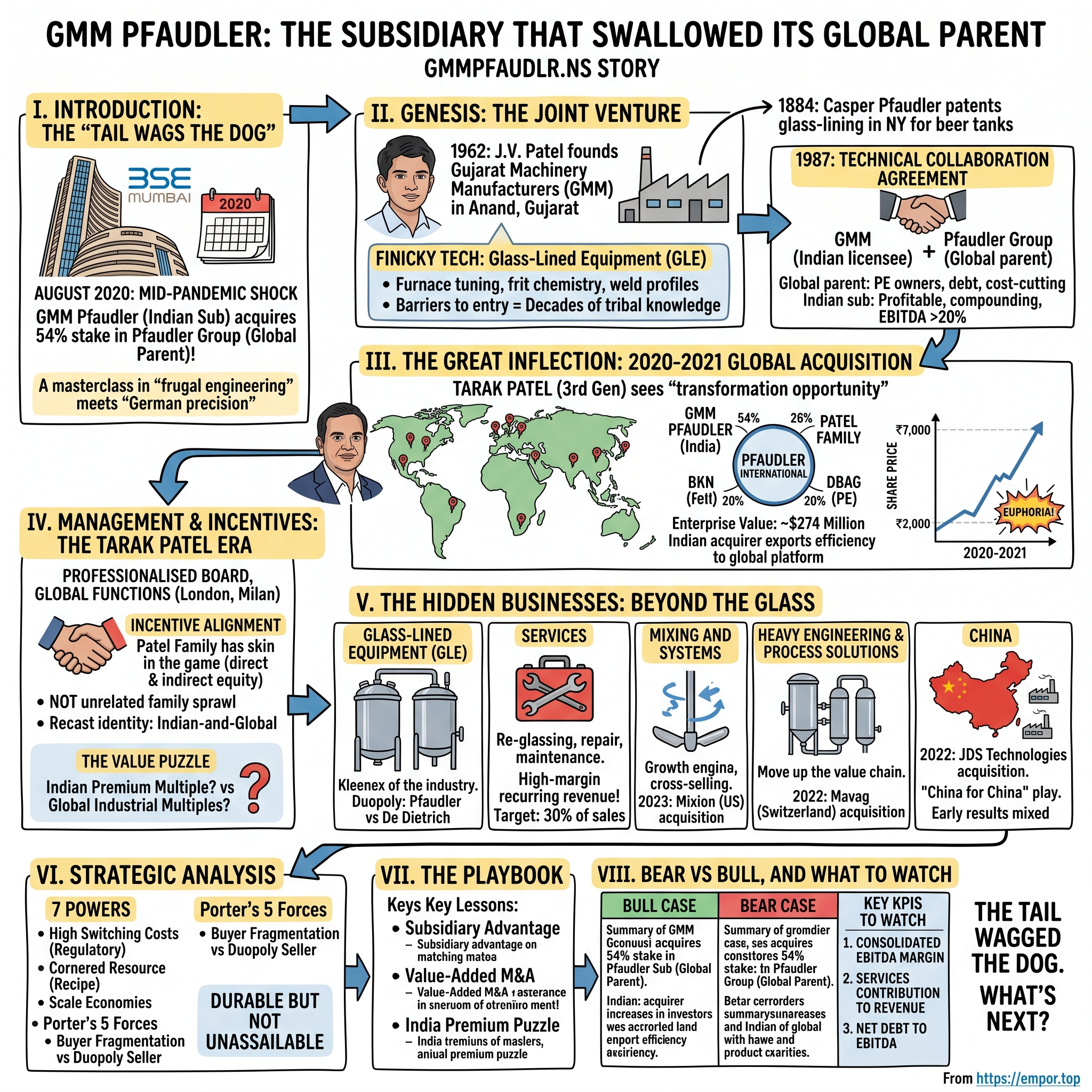

Picture the scene. It is August 2020. The world is mid-pandemic, locked down, terrified, and trading in tight spreads. In Mumbai, the BSE Sensex has clawed its way back from the March lows but nobody really trusts the rally yet. And then, on a Thursday morning, a regulatory filing lands at the Bombay Stock Exchange that reads less like a corporate announcement and more like a plot twist from a corporate thriller.[^1]

The filing is from GMM Pfaudler Limited, a mid-cap engineering company headquartered in the small Gujarati town of Karamsad. The announcement is short. GMM Pfaudler — the Indian subsidiary, with a market capitalisation that on its best day might brush ₹6,000 crore — has just signed papers to acquire a controlling 54% stake in its own German-American parent, the Pfaudler Group, from the European private equity firm Deutsche Beteiligungs AG.[^2]

Read that sentence twice. The subsidiary has bought the parent.

If you are a corporate finance professional, you already know how rare this is. The dominant flow of global M&A runs the other direction: Western multinationals buying emerging-market operators, parent companies consolidating long-arm subsidiaries, capital cascading from the centre to the periphery. The reverse trade — a sub-scale developing-country licensee writing the cheque for the 130-year-old global inventor whose technology it was originally licensing — is so unusual that the deal almost immediately got tagged with a single, sticky phrase in the Indian business press. The Ken called it "the tail wagging the dog."[^3] Moneycontrol led with "a story of reverse acquisition."1 Forbes India eventually wrote a profile that began, simply, with the Indian entity that bought its global parent.2

This is the story of how it happened. But to understand it, you have to understand what GMM Pfaudler actually makes — and why one of the most boring product categories in industrial manufacturing has quietly become the unsung backbone of the world's pharmaceutical and specialty chemical supply chain.

What GMM Pfaudler makes is glass-lined equipment. GLE in industry shorthand. In plain English: enormous steel vessels — reactors, storage tanks, heat exchangers, columns — whose inner surfaces are fused with a chemically resistant glass coating thick enough to survive boiling hydrochloric acid for years on end. If you have ever taken a generic medicine, applied a crop protection chemical to a field, drunk a vitamin out of a capsule, or used almost any cosmetic ingredient that started life as a small molecule, the odds are uncomfortably high that the chemistry happened inside a glass-lined reactor. And the odds are equally high that the reactor came from either Pfaudler or its German rival De Dietrich Process Systems. It is a two-firm global duopoly that almost nobody outside the industry has heard of.[^6]

That is the niche. A 140-year-old technology, a near-duopoly, a sticky regulatory moat, and a customer base that absolutely cannot afford for the equipment to fail. It is exactly the kind of unsexy, mission-critical, capital-intensive business that an Acquired-style episode was invented to celebrate. And it is exactly the kind of business that, when you look at the numbers, makes you realise the Karamsad factory was not the junior partner. It was, by any honest measure of capital efficiency, the better company.

This is a masterclass in what happens when "frugal engineering" meets "German precision" — and the frugal engineers turn out to be holding the chequebook.

II. Genesis: The Joint Venture

The story begins, as so many great Indian industrial stories do, with a young man returning home in the 1960s with a foreign engineering degree, a head full of ideas, and the suffocating regulatory blanket of the License Raj wrapped tightly around him.

The young man was J.V. Patel. The town was Anand, Gujarat — better known to Indians as the home of Amul, the dairy cooperative that would soon make the region famous. In 1962, Patel founded a small machinery workshop and gave it a name that promised more than it could yet deliver: Gujarat Machinery Manufacturers, or GMM.[^7] In its earliest avatar, the company was a generalist fabricator, the kind of regional engineering shop that built whatever local industry needed — tanks, mixers, structural assemblies. There was nothing particularly special about it, except for the patience of its founder and the slow, careful accumulation of metallurgical know-how.

That accumulation mattered more than it looked. Glass-lined equipment is not a product you can simply decide to make. The technology is brutally finicky. You take a steel pressure vessel, spray a slurry of specialty glass frit onto its inner surface, and then fire the whole assembly inside a furnace at temperatures approaching 900 degrees Celsius. The glass has to fuse uniformly. The thermal expansion coefficients of the glass and the underlying steel have to be matched within fractions of a percent, otherwise the lining cracks the moment the reactor starts heating and cooling cycles in customer service. A single pinhole defect, invisible to the naked eye, is enough to turn a six-figure reactor into industrial scrap on its very first acid run.

This is why, when GMM Pfaudler talks about "barriers to entry" in its investor presentations, it is not marketing copy. The entry barrier is decades of furnace tuning, frit chemistry, weld profiles, and quietly perfected manufacturing tribal knowledge. You cannot Google your way to this. You cannot poach a couple of senior engineers and replicate it inside two years. You can spend a hundred million dollars on a green-field plant and still produce vessels that customers refuse to qualify.

Which brings us to 1884, and to the second half of the origin story. In that year, in Rochester, New York, an engineer named Casper Pfaudler patented a process for fusing glass to steel to line beer brewing tanks — at the time, an attempt to solve the very prosaic problem that beer kept tasting like the metal vat it sat in.[^8] Pfaudler the company spent the next century quietly migrating from brewing to pharmaceuticals to specialty chemicals, becoming, in the unglamorous way that industrial inventors do, the global benchmark for the entire category.

In 1987, GMM signed a technical collaboration agreement with the Pfaudler Group. The deal was the very archetype of the Indian licensee model of that decade: the Western parent contributes brand, IP, drawings, and process know-how; the Indian partner contributes cheap manufacturing labour, a domestic distribution network, and the politically necessary local face for selling into Indian industry. License Raj rules meant foreign equity ownership was capped; the venture had to be substantially Indian-controlled. The Patel family held the operating control. Pfaudler, eventually, held a strategic minority stake.

What happened next is the part of the story that is easy to underrate. While the Patel family settled into the patient, multi-decade grind of running a manufacturing business in small-town Gujarat — building furnaces, qualifying steel mills, training welders, slowly winning Indian pharma customers one at a time — the global Pfaudler parent went through a very different kind of journey. It was bought, sold, and bought again by a procession of private equity owners. It moved headquarters. It restructured. It cut costs. It loaded up on debt, paid down debt, and reloaded again, in the way that PE-owned industrial assets do. By the late 2010s, the global Pfaudler Group was sitting under Deutsche Beteiligungs AG, the German PE firm that had bought it in 2014, and the equity was looking for a home.[^2]

Meanwhile, in Karamsad, the unflashy Indian licensee had been compounding. Quietly, methodically, decade after decade. By the 2010s the Indian business was running EBITDA margins north of 20% — almost unheard of for a heavy engineering company — and generating prodigious free cash flow on a barely levered balance sheet. The licensee had become more profitable per dollar of capital than the inventor.[^9] And the inventor's PE owner needed an exit.

The set-up was complete. Now the game could begin.

III. The Great Inflection: 2020–2021 Global Acquisition

Tarak Patel — J.V. Patel's grandson, the third-generation custodian of the family business — had been Managing Director of GMM Pfaudler since 2015. By his own telling in subsequent interviews, the idea of buying the global parent did not arrive as a single dramatic insight. It arrived in pieces, over years, as he sat in board meetings of the Pfaudler Group in his capacity as a representative of the Indian subsidiary and watched the global business struggle with problems the Indian business had long ago solved.2

The global Pfaudler was a beast of a thing. Plants in Germany, the US, Brazil, Mexico, Italy, China. A century-old brand. The deepest IP library in the industry. But also: heavy overheads. Underutilised European factories. A cost structure designed for a world where you could charge a premium and customers would simply pay. Margins that had been sliding for years and that, by the late 2010s, were sitting in single digits at the EBITDA line. It was, in the polite language of private equity, a "transformation opportunity."1

DBAG had bought Pfaudler in 2014, attempted the transformation, and by 2019 was ready to monetise. The conventional exit playbook would have been a secondary sale to another European PE fund, or perhaps a strategic sale to a larger industrial conglomerate. What actually happened was that Tarak Patel walked into the room with a different idea.

The deal that emerged in August 2020 was structurally elegant. GMM Pfaudler, the Indian listed company, acquired 54% of the equity of Pfaudler International, the global holding company. The Patel family — through their personal holding vehicle, separate from the listed entity — picked up another 26%. DBAG retained 20%.[^1] The implied enterprise value of the global parent was approximately $274 million.[^2] Funded through a combination of internal accruals from the Indian business, a fresh equity infusion at the holding level, and term debt at the global parent, the deal closed in September 2020. The licensee owned the licensor.

The market reaction was — and this is the polite word — euphoric. GMM Pfaudler's share price had been climbing through 2020 in anticipation, and after the deal closed, the stock ran from roughly ₹2,000 a share in early 2020 to a peak above ₹7,000 by 2021 as Indian investors digested the implications.[^9] The Indian story had become a global story, and Indian small-cap multiples being what they are, the re-rating was savage.

But the most interesting question is not what investors did. It is whether the deal was actually a good one. So let us walk through the underwriting.

At an enterprise value of roughly $274 million against trailing global EBITDA in the high-$20 millions, the multiple paid was approximately 8x EBITDA.1 That is not a cheap multiple for a low-growth industrial business in absolute terms. Comparable European specialty chemical equipment players were trading in the 6 to 8x range at the time. But it is also not an unreasonable one — and crucially, that 8x was being paid on a depressed earnings base. The Indian acquirer's thesis was not that they were buying a cheap business; it was that they were buying an under-managed one. If you could take a $300 million revenue global platform with single-digit margins and push margins toward the 20% range that the Indian operation was already running, then the de facto entry multiple, on normalised post-synergy earnings, would collapse to something closer to 4 or 5x. That is the trade. The export of Indian efficiency to the world.

The synergy logic was specific. The Indian business had built, over thirty years, a manufacturing cost structure that simply could not be replicated in a German factory operating under German labour rules. The opportunity was not to shut down European production — the technical and customer-validation costs of doing so were prohibitive — but to selectively shift component manufacturing, sub-assembly work, and, crucially, the engineering hours for global projects to India. Karamsad would become the design and fabrication hub for the lower-complexity work. Schwetzingen, Germany, would keep the heavy stuff. Rochester, New York, would keep the US-validated capacity for FDA-regulated pharma customers. China would serve China. The footprint would be rationalised, not razed.

The financial profile, of course, changed dramatically. A company that had been functionally net-cash for most of its modern history found itself carrying meaningful consolidated debt — though, in management's defence, the leverage ratios were modest by global PE standards, and the deleveraging trajectory through FY22 and FY23 was rapid as the global business stabilised.[^9] The other thing that changed was the geographic mix of revenue. Pre-deal, GMM Pfaudler the Indian listed entity was essentially an India story. Post-deal, India would be roughly a third of consolidated revenue, with Europe, the Americas, and China accounting for the rest. The company had gone, in a single transaction, from a domestic mid-cap to a global mid-cap.

For investors, this is the moment that defines everything that comes after. The bull case and the bear case, the playbook and the pitfalls, all flow from the same source: a frugal Indian operator betting that the operating discipline that worked in Karamsad would travel.

IV. Management & Incentives: The Tarak Patel Era

Tarak Patel does not look the part of a global industrial CEO. He is, by all accounts, soft-spoken, more comfortable in a factory than at a Davos panel, and visibly more at home talking about glass-lining furnace temperatures than about quarterly earnings narratives. He was educated in the United States, returned to India in his twenties, and worked his way through GMM Pfaudler the long way — sales, operations, eventually corporate strategy — before being elevated to the Managing Director's chair in 2015.2 In a country where many third-generation promoters arrive in the corner office via direct elevator from the family Sunday lunch, the apprenticeship matters.

What Tarak built is interesting precisely because of what he chose not to build. He did not move the listed company's headquarters to Mumbai. He did not turn GMM Pfaudler into a vehicle for unrelated family-business sprawl. He did not, in the language Indian corporate governance analysts use, indulge in diworsification. Instead, he made a series of decisions that look — in retrospect, and even in foresight — almost suspiciously aligned with what a textbook outside CEO of a global industrial would do.

He professionalised the board. He brought in independent directors with global industrial backgrounds. He moved key global functions — strategy, M&A integration, certain corporate roles — to London and Milan, leaving manufacturing leadership in Karamsad and engineering leadership in Schwetzingen.[^9] He embraced the slightly awkward reality that "Indian promoter-led global multinational" is a category that barely exists, and built the operating model from first principles rather than trying to graft Indian habits onto a global org.

The incentive alignment is worth dwelling on. The Patel family, through Gujarat Investments and related holding vehicles, retains a controlling shareholding in GMM Pfaudler the listed entity. They also hold direct equity in the global Pfaudler Group at the holding company level, alongside the listed company's 54% stake. This dual holding structure has been mildly controversial — minority shareholders periodically raise questions about whether the family's interests at the global level might diverge from the listed entity's interests — but in practice the family has navigated it cleanly so far, and management has been transparent about the structure in disclosures.[^1] On balance, the structure means that the controlling shareholders are personally and substantially exposed to the success of the global business in a way that mere salary or stock options would not produce. This is skin in the game in its most literal Indian-promoter sense.

There is another, subtler thing Tarak did. He took the corporate identity of GMM Pfaudler — long defined by its Gujarati factory roots and its German-American technology licence — and recast it as something different. Not Indian, not global, but Indian-and-global. In investor presentations and earnings calls he refers, without much ceremony, to "our German team," "our American business," "our Chinese plant," in exactly the way an American or European multinational CEO would.[^10] It is a small linguistic tic, but it tells you something about how he sees the company. He is not the Indian subsidiary's leader trying to manage a foreign parent. He is the global CEO who happens to be listed in Mumbai.

This matters because Indian capital markets do not naturally know how to value such an entity. Indian investors have historically applied a robust valuation premium to high-quality manufacturing franchises with domestic moats — 30 to 40 times earnings is not unusual for the best names in the bucket. Global industrial peers trade at 12 to 20 times. The question of which lens GMM Pfaudler should be viewed through has become a structural debate among Indian portfolio managers, and the answer determines an enormous range of fair-value outcomes.3

For management, the implication is uncomfortable. The Indian listing gave them a multiple that funded the global acquisition. But the global acquisition has, mathematically, diluted the proportion of the business to which the Indian multiple naturally applies. As the global business scales — and as the Indian business becomes a minority slice of the consolidated whole — the question of whether Indian investors will continue to apply Indian multiples to a substantially global enterprise becomes existential to the equity. That tension sits underneath every strategic decision the company makes.

V. The Hidden Businesses: Beyond the Glass

If you spend any time reading the Pfaudler investor presentations, you start to realise that "glass-lined equipment" is the headline product but not, in any meaningful sense, the whole story. The company has been quietly diversifying for years, layering new revenue streams on top of the core GLE franchise, and the resulting business mix is significantly more interesting — and significantly less cyclical — than the casual investor assumes.

Let us walk the segments.

The first and largest is Glass-Lined Equipment itself, which still accounts for the majority of consolidated revenue. This is the Kleenex of the industry. When a pharmaceutical company in India, the US, or Europe needs a reactor for active pharmaceutical ingredient synthesis, the procurement team writes "Pfaudler-equivalent" into the technical specification and lets the vendors fight from there. The brand has the kind of category-defining ubiquity that compounds across decades — pharma customers train their engineers on Pfaudler equipment, pharma engineering consultants design new plants around Pfaudler specifications, and pharma regulators have implicitly validated Pfaudler reactors for thousands of approved drug processes. The competitive set is essentially two firms globally — Pfaudler itself and De Dietrich Process Systems of France — plus a handful of smaller regional players (Thaletec in Germany, Tycon in Italy, several Chinese operators) that compete on price rather than full-stack capability.[^6]

The second segment, and arguably the most underrated, is Services. Every glass-lined reactor that has ever been sold is, by definition, a potential service customer. The glass lining wears, chips, or develops pinholes over years of use. Re-glassing, repair, on-site maintenance, and full reactor refurbishment is a high-margin recurring revenue stream that scales with the installed base. Pfaudler has been installing reactors for 140 years; the installed base is enormous; and the proportion of consolidated revenue from services has been climbing steadily.[^10] The strategic significance of this is immense. Services revenue is less cyclical than equipment sales, runs at higher margins, and constitutes the closest thing the GLE industry has to a recurring software-like revenue line. Management has been explicit that growing the services contribution toward 30% of revenue is a priority — and it is not hard to see why.

The third segment, Mixing and Systems, is the growth engine. This is the bet that GMM Pfaudler can move beyond its glass-lining heritage and become a broader provider of mixing technology — including non-glass-lined mixing solutions — across pharma, specialty chemicals, food, and adjacent industries. The 2023 acquisition of Mixion, a US-based mixing technology firm, was a clear signal of intent.[^12] Mixing is a larger global market than GLE; the competitive set is more fragmented; and Pfaudler can sell mixing solutions to the same procurement teams that already buy its reactors. The cross-selling logic is obvious, and the margin profile is similar.

The fourth segment, Heavy Engineering and Process Solutions, is where GMM Pfaudler is making its most ambitious move up the value chain. Through acquisitions including Mavag AG in Switzerland, the company has expanded into filtration, drying, and tablet pressing equipment — adjacent technologies that integrate naturally with glass-lined reactors in pharma plants. The strategic message is: stop being a tank-maker, become a process solution provider. Sell the customer not just the reactor, but the entire small-molecule synthesis line.[^9] This is a higher-value, higher-margin position, and it competes more directly with players like Glatt, IMA, and the larger Western pharma equipment houses.

And then there is China. The 2022 acquisition of JDS Technologies — a Chinese GLE maker — was framed as both a market access play and a turnaround project.[^13] China is the world's largest specialty chemicals market by volume, and the local GLE industry is dominated by domestic players who compete on price. The Pfaudler bet is that bringing the global brand, the technology, and the manufacturing discipline to a Chinese operating platform creates a serious "China for China" franchise — selling Pfaudler-quality equipment, made in China, at China-competitive prices. The early results were mixed; the Chinese chemicals industry hit a brutal overcapacity cycle in 2023–2024 that hurt new equipment orders across the board, and JDS's turnaround timeline has stretched longer than initial guidance suggested.[^10] But the strategic logic is sound. China cannot be ignored, and the only way to play it credibly is local.

Add all of this up and what you have is a company that, while still nominally a glass-lined equipment maker, is on a multi-year journey to become something more interesting: a globally diversified, services-heavy, multi-technology process solutions provider. The cyclicality of the equipment business gets dampened by services. The geographic concentration in India gets diversified by Europe, the US, and China. The product concentration in glass-lining gets broadened by mixing, filtration, and drying. It is a far more resilient model than the one Tarak Patel inherited.

VI. Strategic Analysis: 7 Powers and 5 Forces

So how durable is this business, really? It is worth applying the standard analytical frameworks rigorously rather than waving in their general direction.

Start with Hamilton Helmer's 7 Powers. The first and most important power GMM Pfaudler enjoys is Switching Costs — and these are not garden-variety switching costs. When a pharmaceutical company files a Drug Master File with the US FDA or the European Medicines Agency, the filing specifies the equipment used in the manufacturing process. A Pfaudler reactor of a specific design, lined to a specific specification, sitting in a specific plant, is part of the regulatory dossier for that drug. Replacing that reactor with a different supplier's reactor, after the drug is approved, is not merely a procurement decision; it is a regulatory event that can trigger requalification, revalidation, and in some cases a fresh round of stability testing. The economic cost to the customer of switching, for an approved commercial process, can run into millions of dollars and years of regulatory delay. For new drug processes still in development, the bias toward whichever reactor brand the customer's process engineering team already knows is similarly strong. This is not a one-quarter switching cost. This is a one-decade switching cost.

The second power is Cornered Resource. The "recipe" for Pfaudler's glass lining — the precise frit chemistry, firing temperatures, layer thicknesses, and quality control protocols — is not patented in any conventional sense. Glass-lining patents from the original era expired long ago. But the operational know-how, accumulated through 140 years of furnace runs and millions of vessel-hours of customer feedback, constitutes a trade secret that no competitor can simply lift. De Dietrich has its own equivalent — a different but comparably good recipe — which is why the global market is a duopoly rather than a Pfaudler monopoly. But the cornered resource is real, and it is the reason there are two global leaders rather than ten.[^6]

The third power is Scale Economies. With manufacturing footprints in India, Germany, the US, Brazil, Mexico, Italy, and China, GMM Pfaudler now enjoys a globally distributed production base that competitors cannot easily replicate. The scale shows up in three places: shared engineering across plants (a design developed for a German customer can be quickly localised and produced in India), shared procurement of specialty inputs (steel grades, glass frit), and shared R&D investment amortised across a larger revenue base.[^9] In a low-growth, high-fixed-cost industrial business, scale is decisive.

The remaining four powers — Network Economies, Counter-Positioning, Branding, and Process Power — apply with varying force. Branding is meaningful within the pharma engineering community but largely irrelevant outside it. Process Power, in the sense of accumulated manufacturing learning curves, is closely related to the Cornered Resource argument above. Counter-Positioning is the interesting question: does GMM Pfaudler's combination of Indian cost structure plus global brand actually counter-position it against incumbents who cannot easily replicate the model? Arguably yes. De Dietrich, sitting in France with French labour rules and no Indian manufacturing base, cannot easily match GMM Pfaudler's blended cost-to-serve. That structural cost advantage, if it persists, is a real counter-positioning power.

Now Porter's Five Forces. Threat of New Entrants is low to almost negligible. The capital requirements are large, the technical learning curve is years long, and customer qualification cycles for new GLE suppliers run into many quarters. Bargaining Power of Suppliers is moderate — specialty steel and specialty glass are commoditised enough that no single supplier holds the company hostage. Bargaining Power of Buyers is the most interesting force: the global pharmaceutical and specialty chemicals industry is fragmented at the buyer level, with thousands of customers ranging from Pfizer-scale majors to small Indian API specialists, none of whom individually constitute more than low-single-digit revenue concentration for Pfaudler. Buyer fragmentation against a near-duopoly seller is a structurally favourable position. Threat of Substitutes is low — alternative reactor technologies (stainless steel, Hastelloy, tantalum-lined, PTFE-lined) exist, but each has narrower process applicability than glass-lined, and the cost-performance profile for the broad mass of acid-handling chemistry favours GLE for the foreseeable future. Industry Rivalry, finally, is the global duopoly's blessing and curse: rivalry with De Dietrich is real, but it is a two-player game in which both sides have learned to compete on engineering quality and service rather than on price.

Pull these threads together and you get a defensible but not unassailable franchise. The moats are real, especially in the regulated pharmaceutical sub-segment. The duopoly structure is genuinely favourable. The biggest unknown is China — whether the local players, given enough time and government policy support, can climb up the quality curve and start competing globally rather than just locally. That is a five-to-ten-year question, not a next-quarter question, but it is the one that should haunt every long-term holder.

VII. The Playbook: Business and Investing Lessons

Step back from the specifics of GMM Pfaudler and the broader playbook becomes legible. There are three lessons here that travel well beyond this single company.

The first is the Subsidiary Advantage. The reverse acquisition was not an accident; it was the predictable outcome of a structural arbitrage. When a high-quality local operator builds a profitable, cash-generative subsidiary inside a sub-scale developing market, and the global parent is owned by financial sponsors who eventually need an exit, the local subsidiary can — under the right conditions — find itself in the unusual position of being both the natural buyer and the better operator. GMM Pfaudler is not unique in this respect. Indian subsidiaries of foreign multinationals have, in several other industries, ended up either buying their parents outright or buying significant chunks of global businesses from parents who have lost interest. The pattern works when three conditions hold: the local business runs higher margins than the global parent; the local listing trades at a higher multiple than the parent's private valuation; and the family or controlling shareholder of the local entity has the appetite, sophistication, and balance sheet to execute a cross-border deal. All three conditions held here. The result was an asymmetric trade for the Indian acquirer.

The second is the discipline of Value-Added M&A. The Pfaudler global acquisition was the headline, but in the years that followed, GMM Pfaudler also executed a string of smaller bolt-on acquisitions: Hydro-Québec equipment in Canada, Mavag in Switzerland, Mixion in the US, JDS in China.[^12][^13] Each was an acquisition of a technology or a geographic position that complemented the core GLE franchise. None was transformational on its own. None was paid for with a billion-dollar cheque. But cumulatively, they have meaningfully reshaped the company's product mix and geographic footprint. The pattern is the classic industrial roll-up applied with discipline: target sub-7x EBITDA multiples on a post-synergy basis, focus on businesses where the existing Pfaudler distribution network creates revenue synergies, and avoid the temptation to chase scale for its own sake.[^14] This is the kind of M&A that, executed well over a decade, can compound shareholder value at rates that pure organic growth cannot match. Executed poorly, it can also destroy enormous amounts of capital. Investors should grade the company quarter by quarter on integration execution and post-deal margin trajectories, not on the announcement-day press releases.

The third is the puzzle of the India Premium. This is the trickiest of the three. Indian listed equities, especially in the manufacturing and capital-goods sectors, have for years traded at multiples that look generous by any global benchmark. A 35 to 45 times earnings multiple is not unusual for a high-quality Indian engineering name. The same business, sitting inside a European private equity portfolio, might be valued at 8 to 12 times EBITDA — a small fraction of the Indian listed multiple.3 The arbitrage was the engine of GMM Pfaudler's deal: the Indian entity could use its high-multiple equity (or, more precisely, its access to low-cost debt collateralised by that equity) to buy a global asset valued at a much lower multiple. The accretive math worked from day one.

But the arbitrage cuts both ways. If the global business grows faster than the Indian business — which, given the relative sizes of the global versus Indian addressable markets, is the structural expectation — then the consolidated entity becomes, over time, mostly global. And global industrial businesses do not naturally trade at Indian small-cap multiples. The question of whether the market will continue to apply an Indian premium to a substantially global enterprise is, in many ways, the central investment question for GMM Pfaudler over the next five years. If the answer is yes, the equity has room to compound. If the answer is no, the multiple will compress even if the underlying business performs well.3 This is the kind of valuation question that does not lend itself to a clean answer; it depends on what the marginal Indian investor decides over time.

VIII. Analysis: Bear vs. Bull, and What to Watch

Let us be honest about the disagreement.

The Bull Case is built on three pillars. First, services revenue continues its march toward 30% of consolidated sales, structurally lifting margins and reducing earnings cyclicality.[^10] Second, the "China for China" strategy through JDS eventually delivers a serious local Chinese franchise that captures meaningful share in the world's largest chemicals market — even if the timing is slower than initially planned. Third, share gains in the United States and Europe accelerate as Pfaudler's Indian-blended cost-to-serve advantage compounds against De Dietrich's purely European cost base, and as the broader bolt-on acquisitions create cross-selling tailwinds. Layer in the long-term tailwind from pharmaceutical and specialty chemical capex globally — driven by biologics, generics in emerging markets, and reshoring of strategic supply chains away from a single country of origin — and the demand backdrop is structurally favourable. In this case, the consolidated business compounds at attractive rates for a decade, the services contribution rises, and the equity rerates upward despite the geographic mix becoming more global.

The Bear Case is equally coherent and worth taking seriously. The most acute risk is the cyclicality of the chemical industry. China's specialty chemicals overcapacity cycle, which began biting in 2023 and has continued through 2024 and into 2025, has crushed equipment order books across the global GLE industry. If the overcapacity persists — and Chinese chemicals capex cycles have historically taken three to five years to clear — then GMM Pfaudler faces a multi-year headwind on its largest growth market. Add the integration risks of multiple bolt-on acquisitions executing simultaneously, the working capital strain of running a global manufacturing network through a downcycle, and the interest cost of carrying meaningful consolidated debt in a higher-for-longer rate environment, and the risk profile becomes uncomfortable.3 There is also the structural concern about whether the Patel family's dual exposure — at the listed entity level and at the global holding level — creates governance ambiguity that minority shareholders should price into the multiple.

There is a third issue, often underweighted: key-person risk. Tarak Patel's personal involvement in the transformation has been central. The company's professionalisation has come a long way, and the global management team is no longer dependent on any single individual for day-to-day operations. But the strategic direction, the M&A choices, the capital allocation decisions — these still bear the imprint of one Managing Director's worldview. Succession is a question that long-term holders should at least think about, even if the answer today is that Tarak is fifty-something and presumably running the business for many more years.

For investors who want to track the company without drowning in disclosure detail, three KPIs matter more than any others:

First, the consolidated EBITDA margin, with particular attention to the gap between the India segment margins and the rest-of-world margins. The thesis of the entire reverse-acquisition deal hinges on closing that gap. If consolidated margins drift upward over multiple years and the rest-of-world business approaches Indian-segment margin levels, the thesis is working. If the gap stays wide or widens, it is not.

Second, the services contribution to total revenue. Management has been explicit that growing services toward 30% is a priority; the trajectory of that ratio is a clean signal of whether the business is structurally becoming more recurring and less cyclical.[^10]

Third, net debt to EBITDA. The company moved from net-cash to leveraged through the global acquisition. The pace of deleveraging — and the discipline of not re-leveraging through further M&A faster than cash flows can deliver — is the simplest test of capital allocation discipline.

If you watch those three numbers over the next several years, you will know almost everything you need to know about whether the GMM Pfaudler thesis is unfolding as planned.

There is also a quieter overlay worth mentioning. The global specialty chemicals industry is being reshaped by regulatory pressure around per- and polyfluoroalkyl substances (PFAS), environmental compliance for older chemistry plants, and the slow shift of fine-chemical capacity out of China toward India, Vietnam, and selective US reshoring. Each of these dynamics affects, in different directions, the long-term demand for glass-lined equipment. Investors who track the company should pay attention not just to GMM Pfaudler's own disclosures but to the broader signal coming out of Indian pharma, US specialty chemical capex, and European environmental regulation. The reactor maker is, in a real sense, a leveraged play on global chemistry capex — and that capex is being shaped by forces well outside any single company's control.

IX. Epilogue

There is a moment, somewhere in every Acquired episode, where the story zooms back out and the listener is invited to ask the meta-question: what does this tell us about the world?

For GMM Pfaudler, the meta-question is unusually rich. This is, on its surface, a story about a Gujarati machinery workshop that bought a 130-year-old Western industrial brand. But it is also a story about a broader inversion in global manufacturing: the slow, partial, occasionally lurching transfer of operating capability from the developed world to a handful of disciplined operators in emerging markets, who learned the technology under licence and then, having learned it, built better businesses with it than the inventors did. India is one such operator. There are others.

If you are an Indian mid-cap investor looking for the playbook, GMM Pfaudler is the canonical case. A local listing, a high-quality cash-generative business, a patient promoter family, a global parent that loses its way, and an opportunistic reverse acquisition that uses Indian valuation multiples to buy a global business at lower multiples. The blueprint is replicable in narrow circumstances, and a handful of Indian companies are at various stages of attempting variations on it. None has yet pulled it off as cleanly as GMM Pfaudler did in 2020.

If you are a long-term holder, the question is no longer whether the reverse acquisition was the right deal. That question has been answered: the deal closed five years ago, the integration is largely done, and the consolidated business is materially stronger than the standalone Indian business would have been. The question now is whether the next chapter — services growth, China turnaround, the Mavag and Mixion integrations, the continued professionalisation of a globally distributed organisation — can deliver another decade of compounding.

From a single factory in Karamsad to 14 manufacturing facilities across four continents.[^9] From a regional licensee to the majority owner of the global brand whose technology it once paid royalties to use. The trajectory is, in its own quiet industrial way, one of the more remarkable corporate stories of modern Indian capitalism. The tail did, in fact, wag the dog. The interesting question is what the dog learns to do next.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube