Gujarat Mineral Development Corporation (GMDC): From State Enterprise to Mining Powerhouse

I. Opening & Episode Framework

Picture this: In the dusty, mineral-rich landscapes of Gujarat, where the earth holds treasures formed over millions of years, a state-owned enterprise quietly built one of India's most formidable mining operations. Today, Gujarat Mineral Development Corporation commands a ₹13,159 crore market capitalization, stands as India's number one merchant seller of lignite, and ranks second in production. But the real story isn't just about scale—it's about how a company born from post-independence idealism transformed itself into a mining powerhouse while remaining majority government-owned.

The central question driving this narrative: How did a state enterprise that started with a single silica sand quarry in 1963 evolve into a diversified mining and energy conglomerate now expanding beyond Gujarat's borders for the first time in its six-decade history?

GMDC's journey mirrors India's own industrial evolution—from socialist state planning to market liberalization, from regional focus to national ambitions, from pure extraction to value addition and renewable energy. Founded on May 15, 1963, the company now stands at an inflection point, having won three major coal blocks in Odisha with combined reserves exceeding 2 billion tonnes. This isn't just geographic expansion; it's a fundamental reimagining of what a state-owned mining company can become.

The roadmap ahead traces an arc from humble beginnings in silica sand to solar panels on reclaimed mining land, from regional lignite dominance to a national coal mining strategy, from a pure PSU to a listed entity balancing commercial imperatives with social responsibilities.

II. Gujarat's Industrial Vision & GMDC's Genesis (1960s)

The monsoon of 1960 brought promise to newly formed Gujarat state. Just months after the state's creation from the partition of the bilingual Bombay State, the air in Gandhinagar buzzed with ambition. During the period 1960–90, Gujarat established itself as a leader in various industrial sectors – textiles, engineering, chemicals, petrochemicals, drugs & pharmaceuticals, dairy, cement & ceramics, gems & jewellery, etc. But beneath this industrial revolution lay an untapped treasure: Gujarat's vast mineral wealth, waiting in the earth like seeds of prosperity.

The vision was audacious yet practical. Such a massive scale of industrial development has been possible on account of judicious exploitation of natural resources, such as minerals, oil and gas, marine, agriculture and animal wealth. The state's leadership recognized that raw materials formed the backbone of industrialization. Without a reliable supply of minerals—silica for glass factories, limestone for cement plants, lignite for power generation—Gujarat's industrial dreams would remain just that: dreams.

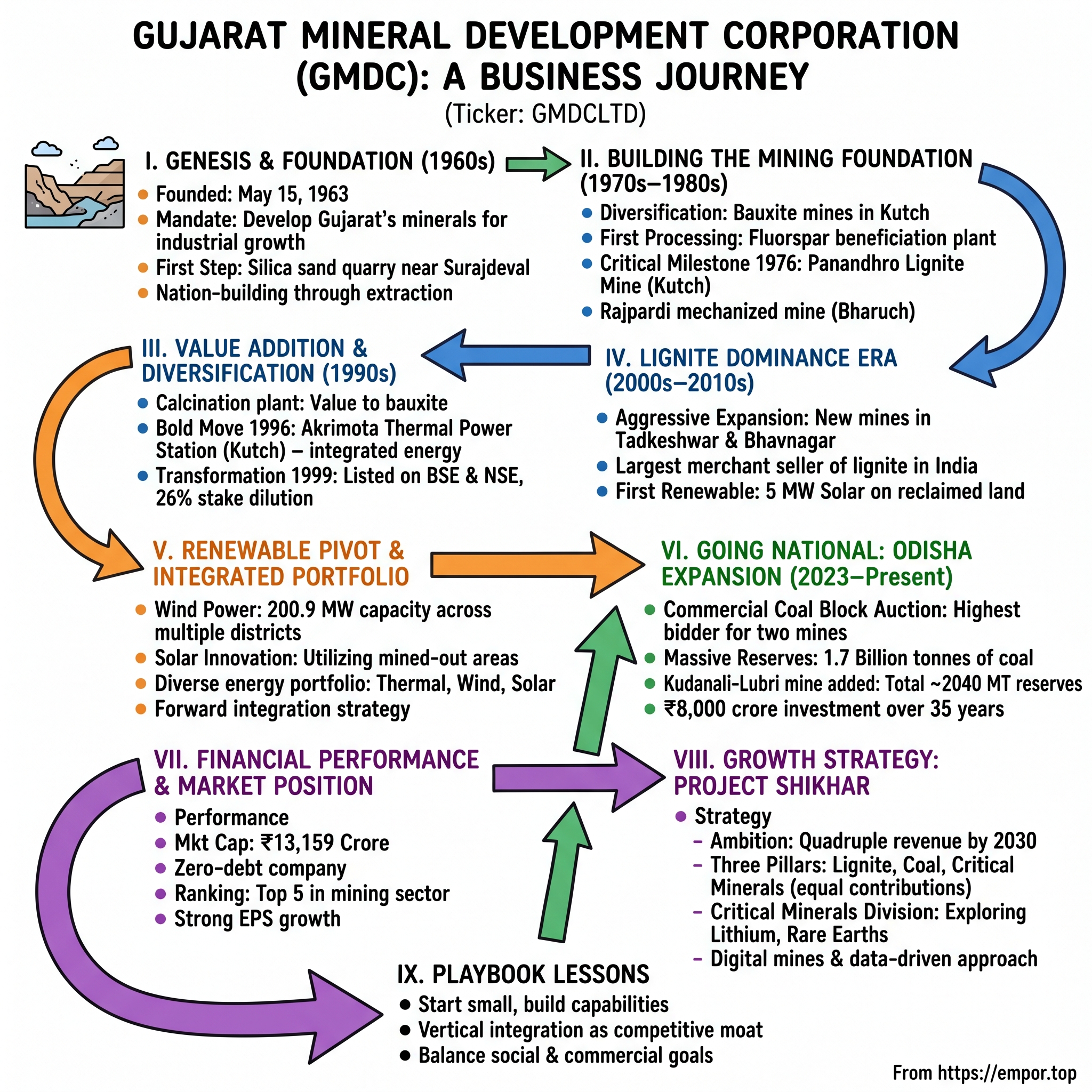

On May 15, 1963, the Gujarat Mineral Development Corporation came into being, incorporated with a mandate that seemed almost quaint in its simplicity: develop the major mineral resources of Gujarat for the state's industrial growth. The company's first act was modest—establishing a silica sand quarrying plant near Surajdeval to feed the nascent glass industry. Picture the scene: bulldozers cutting into virgin earth, the first trucks loaded with silica sand rumbling toward glass factories, workers who had never operated mining equipment learning on the job.

This was state-building through extraction, quite literally. The newly independent India operated on a philosophy of self-reliance, and Gujarat embodied this spirit. The state operating companies like GNFC, GSPC, GSFC, GMDC are a few among flagship companies of the state. GMDC wasn't just another public sector undertaking; it represented Gujarat's determination to control its own industrial destiny.

The challenges were monumental. Mining expertise was virtually non-existent in the state. Equipment had to be imported or sourced from other parts of India. Safety standards needed to be established from scratch. Environmental regulations were minimal, a blessing and curse that would haunt the industry decades later. The company had to build not just mines but an entire ecosystem—training institutes for miners, supply chains for equipment, transportation networks for minerals.

Yet GMDC had advantages that private enterprises lacked. Patient capital from the state government meant it could invest in long-gestation projects. Its monopolistic position in certain minerals provided guaranteed revenues. Most importantly, it had a social mandate that went beyond profit—developing backward regions, creating employment, and feeding Gujarat's industrial machine.

The Surajdeval silica sand operation became the template for GMDC's expansion strategy: identify a mineral resource, establish extraction capabilities, create linkages with consuming industries, and reinvest profits into new ventures. This wasn't sophisticated financial engineering; it was basic industrial capitalism executed with bureaucratic precision.

By the late 1960s, GMDC had proven the model worked. The silica sand fed glass factories in Vadodara and Ahmedabad. Employment in mining regions reduced rural distress. Tax revenues from mineral extraction funded further industrial development. The State is rich in calcite, gypsum, manganese, lignite, bauxite, limestone, agate, feldspar and quartz sand and successful mining of these minerals is done in their specified areas.

What made GMDC unique wasn't just what it extracted from the ground, but how it fit into Gujarat's broader industrial ecosystem. The discovery of oil and gas in Gujarat in the decade of 60s has played an important role in setting up of petroleum refineries, fertilizer plants and petrochemical complexes. During the same period, the state government has also established a strong institutional network. While GIDC built industrial estates and GSFC produced fertilizers, GMDC provided the raw materials that kept the wheels turning.

The company's early employees speak of a pioneering spirit—engineers who slept at mine sites, geologists who trekked through unexplored territories with nothing but survey maps and intuition, accountants who managed operations from makeshift offices. This wasn't glamorous work, but it was nation-building at its most fundamental level.

As the 1960s drew to a close, GMDC had established itself as more than just a mining company. It had become the bedrock—literally and figuratively—of Gujarat's industrial revolution. The single-product silica sand company was ready for its next transformation, one that would take it from extraction to energy, from one mineral to many, from a state enterprise to a commercial powerhouse.

III. Building the Mining Foundation (1970s–1980s)

The 1970s began with GMDC venturing beyond silica sand. In 1964 it started with bauxite mines in Kutch and now operates six bauxite mines, laying the groundwork for what would become a diversified mining empire. But the real transformation came through serendipity and geological surveys.

In 1971, a beneficiation plant was commissioned by GMDC to process 500 M.T of fluorspar ore and to produce calcium fluoride used for the manufacture of Hydro-fluoric acid and as flux in metallurgical industries. This wasn't just adding another mineral to the portfolio; it was GMDC's first foray into value addition—taking raw ore and processing it into industrial-grade products. The fluorspar operations at Kadipani and Ambadungar represented a philosophical shift: why sell raw materials when you could capture more value through beneficiation?

Then came 1976—the year that would define GMDC's future. Allotted Lignite Mining Lease at Panandhro, Kutch; developed first lignite mine to cater to fuel demand of several industries. The discovery of lignite in Gujarat wasn't just finding coal; it was discovering energy independence. Panadhro is famous for its Lignite mines, which were developed in early 1970s and are run by Gujarat Mineral Development Corporation Limited.

Picture the scene at Panandhro: a remote corner of Kutch, where geological surveys had indicated the presence of brown coal deposits. The first cores brought up confirmed it—millions of tonnes of lignite lay beneath the arid landscape. For an energy-starved state dependent on imported coal, this was liquid gold, or rather, solid brown gold.

The challenges of lignite mining were unique. Unlike the hard coal of Jharia or Raniganj, Gujarat's lignite was softer, with lower calorific value but easier to extract. It couldn't power steel plants, but it could fuel cement factories, textile mills, and eventually, power plants. GMDC had to develop entirely new mining techniques suited to Gujarat's geological conditions.

By 1980, GMDC made another strategic move—establishing a captive copper refining plant near Ambaji. This represented the company's first venture into metallic minerals and vertical integration in base metals. The Ambaji copper operations, though modest in scale, demonstrated GMDC's willingness to experiment with different business models.

The crown jewel of this period came in 1983 with the commissioning of the Rajpardi lignite mine near Bharuch, designed with a 1 million metric ton (MMT) annual capacity. Rajpardi wasn't just another mine; it was GMDC's first large-scale mechanized lignite operation. The mine employed modern equipment—draglines, shovels, and conveyor systems—that set new standards for mining operations in Gujarat.

What made Rajpardi special was its location—close to the industrial belt of South Gujarat, reducing transportation costs for textile and chemical factories that had previously relied on expensive imported coal. The economics were compelling: lignite from Rajpardi cost a fraction of imported coal, even accounting for its lower energy content.

The technical expertise built during this period cannot be overstated. GMDC developed in-house capabilities in geological surveying, mine planning, equipment maintenance, and safety management. Engineers who had started as fresh graduates in the 1960s were now seasoned professionals training the next generation. The company established training centers, safety protocols, and operational standards that would serve it for decades.

Environmental considerations, though not as prominent as today, began appearing on GMDC's radar. The company started experimenting with mine reclamation—converting exhausted quarries into water bodies or attempting revegetation. These early efforts, primitive by modern standards, showed an awareness that mining couldn't be purely extractive.

The financial performance during this period validated the expansion strategy. From a single-product company generating modest revenues, GMDC had grown into a multi-mineral enterprise with steady cash flows. The lignite operations, in particular, provided predictable revenues through long-term supply contracts with industries.

By the mid-1980s, GMDC operated across multiple sites: lignite mines at Panandhro and Rajpardi, bauxite operations in Kutch, fluorspar mining and processing at Ambadungar, copper exploration near Ambaji, and the original silica sand operations. Each operation had its own logistics challenges, customer base, and technical requirements.

The company's organizational structure evolved to match this complexity. Regional offices were established, specialized departments for different minerals were created, and a corporate headquarters in Ahmedabad coordinated operations. The bureaucratic structure, often criticized for slowness, provided stability and systematic growth.

What's remarkable about this period is how GMDC balanced commercial objectives with developmental goals. Mines were often located in backward areas where they became the primary source of employment. The company built schools, hospitals, and housing colonies around major mining sites. The town of S.K. Varmanagar, developed near the Panandhro mines, exemplified this approach—a planned township serving the mining community.

The state government's support remained crucial. Mining leases were allocated preferentially to GMDC, geological surveys were shared freely, and patient capital allowed long-gestation projects. This wasn't crony capitalism but strategic state support for resource development. All Manganese-bearing areas of Gujarat have been reserved for GMDC, ensuring the company's monopolistic position in certain minerals.

As the 1980s progressed, GMDC's leadership began thinking bigger. The success in lignite mining had proven that Gujarat had substantial mineral resources. The technical capabilities built over two decades meant the company could handle complex projects. Most importantly, the industrial growth of Gujarat created insatiable demand for raw materials and energy.

The foundation was set, the capabilities built, and the market ready. GMDC stood poised for its next transformation—from a mining company to an integrated energy enterprise. The lignite wouldn't just be sold; it would be burned to generate power. The minerals wouldn't just be extracted; they would be processed into value-added products. The stage was set for GMDC's most ambitious phase yet.

IV. Value Addition & Diversification Strategy (1990s)

The 1990s opened with India's economic liberalization, and GMDC seized the moment to reinvent itself. In 1992, it established a calcination plant to add value to the bauxite mined by it at Gadhsisha in Kutch. With a capacity of 50,000 tonnes per annum, this wasn't just another processing facility—it was GMDC's declaration that raw material extraction alone wouldn't define its future.

The calcination plant transformed raw bauxite into calcined bauxite, a value-added product commanding premium prices in refractory and abrasive industries. The economics were compelling: while raw bauxite fetched modest prices, calcined bauxite sold for three to four times more. This single facility demonstrated how vertical integration could multiply margins without expanding mining operations.

But the real game-changer came in 1996. In 1996, to use the lignite mined by it, GMDC also started thermal power plant at Nani-Chher in Kutch. The Akrimota Thermal Power Station, with its 2x125 MW capacity, represented GMDC's boldest move yet—transforming from a mining company into an integrated energy producer.

Picture the boardroom debates that must have preceded this decision. Building a power plant required capabilities GMDC had never possessed: operating boilers and turbines, managing grid connections, understanding power markets. The capital investment dwarfed anything the company had previously undertaken. Yet the logic was irresistible—why sell lignite at ₹800 per tonne when you could burn it to generate electricity worth ₹3,000-4,000 in equivalent value?

GMDC's 2X125 MW thermal power project at Nani Chher in Lakhpat Taluka, Kutch, is an important component of its initiatives at forward integration. Operational since March 2006, it obtains Lignite from its own mines located at Panandhro, Mata no Madh and Umarsar. The plant used Circulating Fluidized Bed Combustion (CFBC) technology, specifically chosen for its ability to handle Gujarat's high-sulfur lignite while meeting environmental standards.

The power plant's location at Nani Chher, though remote, offered strategic advantages. The water requirement for the power plant is taken from the nearest Kori Creek through a 1.4 KM long sea water intake channel. This eliminated freshwater dependency—crucial in water-scarce Kutch. The proximity to GMDC's lignite mines at Panandhro meant minimal transportation costs, creating a captive fuel supply chain.

Then came 1999—a watershed year that would fundamentally alter GMDC's character. In 1999, the company's sole owner, the Government of Gujarat, diluted 26% of its stake and made GDMC a listed entity on the Bombay Stock Exchange and the National Stock Exchange. This wasn't just a financial transaction; it was a philosophical transformation.

The IPO process forced GMDC to adopt corporate governance standards, quarterly reporting, and shareholder accountability. For an organization accustomed to the leisurely pace of government decision-making, this was culture shock. Suddenly, stock analysts questioned capital allocation, institutional investors demanded growth strategies, and quarterly results became report cards judged by markets.

The listing brought benefits beyond capital. It imposed discipline on operations, forced transparency in financial reporting, and created a currency (shares) for potential acquisitions. The stock price became a daily referendum on management performance, a concept alien to traditional PSUs.

In 1999, the government of Gujarat being the sole owner, divested 26% of its stake and the GMDC became a listed entity (BSE&NSE) and is occupying a position within the top fortune 500 companies in our country with an annual turnover surpassing 10 billion with considerable annual growth rate.

What's fascinating about this period is how GMDC managed the dual transformation—operational (power generation) and structural (public listing)—simultaneously. The company had to build power plant expertise while learning capital market dynamics. Engineers had to understand megawatts and merchant power rates; finance teams had to master investor relations and earnings calls.

The thermal power plant's commissioning coincided with India's power deficit era. Gujarat's industries, facing chronic power shortages, welcomed additional generation capacity. GMDC's lignite-fired electricity, though not the cleanest, provided reliable baseload power when alternatives were scarce. The company secured long-term Power Purchase Agreements (PPAs) with Gujarat Electricity Board, ensuring stable revenues.

Environmental considerations, increasingly prominent in the 1990s, shaped the power plant's design. The CFBC boiler is used here as it is environment friendly and controls sulphur in the flue gas emission. A 100 metre thick green belt surrounds the entire site. These measures, while adding costs, positioned GMDC as a responsible corporate citizen—important for a newly listed company seeking institutional investors.

The diversification strategy extended beyond power and processing. GMDC explored joint ventures, including discussions with international players for alumina refining. Gujarat government has given its green signal to GMDC to form a joint venture with NALCO for a 1 mtpa refinery. Though not all ventures materialized, they demonstrated ambition to leverage mineral resources for downstream industries.

By decade's end, GMDC had transformed from a traditional mining PSU into a diversified natural resources company. The portfolio now included: - Six lignite mines producing over 5 million tonnes annually - Bauxite mining and calcination operations - A 250 MW thermal power station - Fluorspar and manganese mining operations - Listed entity status with private shareholders

The financial metrics validated the strategy. Revenues had grown from hundreds of crores to approaching the thousand-crore mark. The power business, despite initial skepticism, contributed significantly to profitability. Market capitalization, now determined by stock markets rather than book value, reflected investor confidence in the integrated model.

Yet challenges remained. The power plant faced technical issues common to lignite-based generation—high ash content, corrosion, frequent maintenance. The stock price, while respectable, traded at PSU discounts. Private sector competition in mining and power generation intensified. Environmental regulations tightened, threatening traditional mining practices.

As the millennium approached, GMDC stood at another crossroads. The foundation for the next phase was set—the company had proven it could operate beyond traditional mining, manage market expectations, and execute complex projects. The question now was scale: could GMDC leverage its integrated model to become a national player, or would it remain a regional champion confined to Gujarat?

V. The Lignite Dominance Era (2000s–2010s)

The new millennium brought an aggressive expansion phase for GMDC, centered on establishing lignite dominance across Gujarat. In 2005 & 2009 more lignite mines were started by GMDC at Tadkeshwar near Surat and near Bhavnagar, respectively. A lignite mine of 2.5 MMT per annum capacity was opened at Tadkeshwar, Surat to cater to sustainable and committed fuel demand of industries in South Gujarat

Tadkeshwar represented a strategic masterstroke. The Lignite Mines in Tadkeshwar is strategically located in Surat, a large industrial belt. South Gujarat's textile and chemical industries had long suffered from energy shortages and coal transportation costs. Now, lignite from Tadkeshwar could reach factories within hours, not days. The 2.5 million tonne annual capacity wasn't just a number—it represented energy security for hundreds of small and medium enterprises that formed Gujarat's industrial backbone.

Also in 2006 it developed manganese ore mines at Shivarajpur in Panchmahals. All manganese bearing areas in Gujarat reserved for GMDC. A project to handle manganese waste dump was established to cater to the requirement of industries in Gujarat This monopolistic position in manganese, while small in national context, gave GMDC pricing power and guaranteed revenues from steel and battery manufacturers.

The real transformation came in 2009 with the Bhavnagar mine. A lignite mine of 2.4 MMT per annum capacity was opened at Mata No Madh, District Kutch, to cater to the fuel d The Bhavnagar operation showcased GMDC's evolved capabilities—modern mining equipment, sophisticated geological modeling, and environmental management systems that would have been unimaginable in the 1960s.

A lignite mine of 1 MMT per annum capacity was opened at Umarsar, District Kutch, to cater to fuel demand of industries By 2010, GMDC operated six major lignite mines: Panandhro, Rajpardi, Tadkeshwar, Mata No Madh, Umarsar, and Bhavnagar. Combined annual production exceeded 8 million tonnes, making Emerged as the largest merchant seller of lignite in India by developing 6 operating lignite mines in the state

The numbers tell a story of systematic dominance. GMDC/GSRC is operating six lignite mines, three in Kutch with annual production capacity of about 50 Lakh Tonnes and the other at village Amod in Bharuch district with annual production capacity of 10 Lakh Tonnes. The Tadkeshwar Lignite mine in Surat district is having capacity of 25 Lakh Tonnes. GSRC is also operating Lignite mine at Bhavnagar having production capacity of above 30 Lakh Tonnes.

What distinguished this era wasn't just scale but operational sophistication. Set up a 1.5 million TPA Pyrite Removal Plant at Bhavnagar Lignite Project on Built Own Operate (BOO) basis for removal of pyrite nodules Pyrite contamination had long plagued Gujarat's lignite, causing equipment corrosion and environmental issues. The removal plant represented technical problem-solving at industrial scale.

Embarked on a sophisticated Enterprise Resource Planning system covering mining operations throughout Gujarat to achieve efficiency with minimum resources The ERP implementation brought real-time visibility to operations spread across hundreds of kilometers. Mine managers could track production, equipment utilization, and inventory from centralized dashboards—a digital transformation for a traditional mining company.

The period also saw GMDC's first serious foray into renewable energy. A 5 MW solar power plant was installed on the reclaimed mined out land of Panandhro Lignite Mine in Kutch, the first-of-its-kind in the country, to utilise reclaimed land of mined out area This wasn't just greenwashing; it demonstrated how mining companies could reimagine exhausted assets. The Panandhro solar plant became a template for sustainable mining practices, attracting attention from environmental regulators and investors alike.

Customer relationships evolved during this period. GMDC wasn't just a supplier but an energy partner to Gujarat's industries. Long-term supply agreements provided price stability to customers while ensuring revenue visibility for GMDC. The company developed customized lignite grades for different industries—lower ash content for textiles, specific size fractions for cement plants, consistent quality for power generation.

The financial performance validated the strategy. The annual turnover of the Corporation in FY 2015 was about INR 1419 Crores. From a few hundred crores in 2000, revenues had grown five-fold. More importantly, GMDC had become systemically important to Gujarat's economy—any disruption in lignite supply would impact thousands of factories and millions of livelihoods.

Market dynamics during this period favored GMDC. Coal India's inability to meet growing demand, railway capacity constraints, and international coal price volatility made domestic lignite increasingly attractive. GMDC's proximity advantage—mines located within 200-300 km of consuming industries—provided unbeatable economics compared to coal transported from Jharkhand or imported from Indonesia.

The environmental challenge grew more complex. Mining six major sites meant managing six different ecological impacts. GMDC invested in dust suppression systems, water treatment plants, and green belts around mines. The company pioneered the use of conveyor systems to reduce truck movement, cutting both costs and emissions.

The demand of Lignite is growing fast and the Corporation is planning to double its production in next three years. This ambitious target reflected confidence in continued industrial growth and GMDC's ability to scale operations. Recently Ministry of coal has granted three lignite blocks, two in Kutch and one in Surat district to GSRC. In addition another two lignite block in Bharuch district is under consideration for allotmernt in fevour of GSRC

Technology adoption accelerated. GPS-based vehicle tracking optimized transportation routes. Drone surveys improved geological modeling. Automated weighbridges reduced pilferage. Laboratory networks ensured consistent quality testing. These incremental improvements, individually minor, collectively transformed operational efficiency.

The human dimension remained central. By 2015, GMDC employed thousands directly and supported tens of thousands indirectly through contractors, transporters, and ancillary services. Mining townships had evolved into small cities with schools, hospitals, and recreational facilities. Second-generation GMDC employees, children of original miners, brought professional education and modern perspectives to traditional operations.

Competition, while limited, began emerging. Private players explored lignite deposits in Rajasthan and Tamil Nadu. Coal India expanded operations. Imported coal became more accessible with port capacity additions. GMDC's response was to deepen customer relationships, improve service quality, and leverage its incumbent advantages—established mines, logistics networks, and government support.

As the decade progressed, strategic questions emerged. Could GMDC sustain growth within Gujarat's limited lignite reserves? Should it expand beyond state boundaries? How should it balance fossil fuel revenues with renewable energy ambitions? The answers would shape GMDC's next chapter, but the foundation built during the lignite dominance era—operational excellence, financial strength, and market leadership—provided the platform for transformation.

VI. Renewable Energy Pivot & Power Portfolio

The renewable energy pivot began not with grand proclamations but with pragmatic recognition of Gujarat's natural advantages. GMDC ventured into harnessing the wind energy as its commitment towards environment care and to have green footprints. It commissioned 200.9 MW Wind Power turbines in Kutch, Porbandar, Devbhoomi, Dwarka, Jamnagar, Rajkot and Bhavnagar up to 2016.

This wasn't a sudden green awakening but calculated diversification. Gujarat's coastal winds, particularly in Kutch and Saurashtra, ranked among India's best wind resources. GMDC's mining sites often occupied windy ridges and plateaus—perfect for turbines. The company could leverage existing land holdings, grid connections, and operational expertise to enter renewable energy with minimal additional investment.

The numbers were compelling. In the last fiscal 2010-11, GMDC generated 51 million units of power, which reaped revenues of Rs 18 crores for the company. While modest compared to lignite revenues, wind power offered superior margins—no fuel costs, minimal operating expenses, and accelerated depreciation benefits that reduced tax liabilities.

The company's wind power units are located in different districts of Saurashtra region and the additional capacities are coming up in Kutch. Each location was carefully selected through wind mapping studies, ensuring capacity utilization factors above 25%—the threshold for economic viability. GMDC partnered with turbine manufacturers like Suzlon and Enercon, leveraging their technical expertise while retaining operational control.

The solar initiative proved even more innovative. Towards generating power from renewable sources of energy, GMDC initiated a first-of-its-kind 5 MW Solar Power Project in 2011. It was installed on the reclaimed mined-out land of Panandhro Lignite mine in Kutch. This wasn't just adding solar capacity; it was reimagining mining's lifecycle. Exhausted lignite mines, previously liabilities requiring expensive reclamation, became assets generating clean energy.

Picture the Panandhro site: where excavators once extracted lignite, solar panels now captured sunlight. The symbolism was powerful—fossil fuel extraction sites transforming into renewable energy generators. International mining companies studied GMDC's model, recognizing its potential for global replication.

The Akrimota Thermal Power Station, meanwhile, anchored GMDC's baseload generation. GMDC's 2X125 MW thermal power project at Nani Chher in Lakhpat Taluka, Kutch, is an important component of its initiatives at forward integration. Operational since March 2006, it obtains Lignite from its own mines located at Panandhro, Mata no Madh and Umarsar.

State-of-the-art DCS technology is being used here. The Distributed Control System represented significant technological advancement—automated boiler controls, real-time performance monitoring, predictive maintenance algorithms. This wasn't your grandfather's power plant but a modern facility competing with private sector operations.

Environmental management became increasingly sophisticated. The CFBC boiler is used here as it is environment friendly and controls sulphur in the flue gas emission. A 100 metre thick green belt surrounds the entire site. These measures, while adding costs, positioned GMDC as a responsible energy producer at a time when environmental consciousness was becoming mainstream.

The power portfolio's diversity provided resilience. When monsoons failed and wind generation dropped, thermal plants compensated. During coal shortages, captive lignite ensured uninterrupted generation. Solar provided predictable daytime generation, reducing peak power purchases. This wasn't just risk management but strategic positioning—GMDC could offer customers reliable, round-the-clock power from multiple sources.

Financial performance validated the strategy. Power generation, which contributed negligibly in 2000, now represented a significant revenue stream. More importantly, it provided stable, long-term cash flows through Power Purchase Agreements with state utilities. While mining revenues fluctuated with commodity cycles, power revenues offered predictability that equity markets valued.

The renewable push aligned with broader trends. Gujarat government's focus on tapping renewable energy has led to a sharp rise in the wind power capacity in the last few years. According to official data, wind power generation capacity in the state has increased a staggering ten times in the last six years. Gujarat has the highest share (around 26%) of the total installed wind power capacity of the country, accounting for 12.5 GW out of 48.16 GW.

GMDC's renewable journey wasn't without challenges. Wind turbines required specialized maintenance expertise. Solar panels degraded faster in Kutch's harsh desert conditions. Grid integration posed technical challenges when renewable generation exceeded local demand. The company had to build new capabilities—meteorological forecasting, grid management, equipment optimization.

The human dimension evolved too. Mining engineers learned power plant operations. Geologists became wind resource assessors. The company recruited power sector professionals, creating cultural tensions between traditional mining personnel and new energy experts. Managing this transition required delicate balancing—respecting legacy expertise while embracing new competencies.

Competition intensified as private players entered renewable energy. Companies like Adani Green and ReNew Power offered aggressive tariffs in competitive bidding. GMDC's advantage lay not in cost leadership but in integrated operations—mining sites doubling as power generation locations, shared infrastructure reducing capital costs, operational synergies enhancing returns.

The strategic implications extended beyond immediate financials. Renewable energy provided social license to operate in an era of increasing environmental scrutiny. It demonstrated GMDC's ability to evolve beyond extractive industries. Most importantly, it positioned the company for India's energy transition—as coal gradually phases out, GMDC's renewable portfolio would become increasingly valuable.

By 2016, GMDC operated a unique energy portfolio: 250 MW thermal, 200.9 MW wind, 5 MW solar. Combined with lignite mining operations supplying fuel to numerous industries, the company had transformed from a mining enterprise to an integrated energy company. The foundation was set for the next phase—expanding beyond Gujarat's borders into India's vast coal reserves.

VII. The Odisha Expansion: Going National (2023–Present)

March 2023 marked GMDC's most significant strategic shift in six decades. Gujarat Mineral Development Corporation (GMDC) announced that it emerged as the highest bidder for two coal mines in Odisha in the recently concluded commercial coal block auction by the Ministry of Coal, Government of India. This wasn't just geographic expansion—it was a fundamental reimagining of GMDC's identity from a regional player to a national mining company.

The numbers were staggering. Baitarani West is one of two coal blocks GMDC secured in March 2023, with the second being the Burapahar block in Sundargarh district, which holds a geological reserve of 548 million tonnes. GMDC anticipates that the mine, with a geological reserve of 1,152 million tonnes, will rank among the top 20 coal mines in India. Combined, these two blocks contained 1.7 billion tonnes of coal—more than double GMDC's entire lignite reserves accumulated over 60 years.

The investment commitment reflected the scale of ambition. This hearing is crucial for the project, which represents a significant ₹8,000 crore investment by GMDC over 35 years. For context, this single project investment exceeded GMDC's entire market capitalization just a few years earlier. The board's approval of such massive capital allocation demonstrated confidence in long-term coal demand despite global energy transition narratives.

In March 2024, GMDC unveiled a ₹663-crore Land and Resettlement and Rehabilitation plan to support the 1,500 families affected by the project. This wasn't corporate social responsibility theater but hard-learned expertise from decades of land acquisition in Gujarat. GMDC understood that successful mining required community buy-in, and the R&R budget—nearly 10% of total project cost—reflected this reality.

The strategic logic was compelling. GMDC, which typically handles 6-9 MTPA of various minerals, including lignite in Gujarat, aims to reach the peak rated capacity of 15 MTPA at this Odisha coal block by 2030, as per sources. A single Odisha mine would double GMDC's total production, transforming scale economics and market positioning.

Then came July 2024, with another game-changing announcement. "Gujarat Mineral Development Corporation (GMDC)...marks a significant milestone with the successful execution of Coal Mining Development and Production Agreement with Ministry of Coal for 'Kudanali-Lubri' coal mine, Odisha," the PSU said in a statement. The mine is a partially explored block with an estimated reserve of 396.10 million tonnes (MT) of thermal coal.

With the addition of this coal mine, the estimated coal reserves with GMDC now stand at around 2040 MT. From zero coal reserves to 2 billion tonnes in 18 months—this wasn't incremental growth but quantum expansion. "Kudanali-Lubri" coal mine in Angul district is in close proximity to GMDC's existing coal mine "Baitarni West", which will allow GMDC to optimize its resources in developing and operationalizing these coal mines.

The operational synergies were crucial. Spanning 1,196 hectares, the mine encompasses areas in Chhendipada tehsil of Angul district, including Chhendipada Jangal, Handigora, Machhakuta Jangal, Porapara, Porapara Jangal, and Tentuloi-Korasahi. Clustering three major mines in Angul and Sundargarh districts enabled shared infrastructure—railways sidings, processing plants, townships, equipment yards. This wasn't just cost optimization but risk mitigation through operational integration.

"We are committed to driving growth and security in the energy sector. The addition of...coal mine in our portfolio is a significant milestone for us, as it not only strengthens our resource portfolio but also enables us to maximize our operational efficiencies and cost effectiveness in a single state outside Gujarat," GMDC MD Roopwant Singh said.

The challenges of operating 1,500 kilometers from home base were substantial. Odisha's mining culture differed from Gujarat's. Local politics, labor unions, environmental activists—all required careful navigation. Language barriers, regulatory differences, and logistics complexity multiplied operational challenges. GMDC had to build an entirely new organizational capability for interstate operations.

Land acquisition emerged as the critical path. The land acquisition plan for the Baitarani mine includes 154 hectares of government land and approximately 200 hectares of private land. Government land transfer, while procedurally simpler, required inter-state coordination. Private land acquisition meant negotiating with hundreds of small farmers, each with emotional attachments beyond monetary compensation.

Environmental clearances posed another hurdle. Ahead of the ceremony, the State Pollution Control Board of Odisha will hold a pivotal environmental public hearing on September 24 for the 15 million tonnes per annum (MTPA) coal project in Angul district. Public hearings in mining-affected Odisha were contentious affairs, with NGOs, activists, and affected communities voicing concerns about water table depletion, air pollution, and livelihood displacement.

The technology requirements for coal mining differed substantially from lignite operations. Coal's higher density required different excavation equipment. Processing needs were more complex. Transportation economics changed with longer haulage distances to consumption centers. GMDC had to recruit coal mining experts, many from Coal India, creating cultural integration challenges within the organization.

Financial structuring reflected the project's complexity. The ₹8,000 crore investment would be funded through internal accruals, debt, and potentially strategic partnerships. Banks viewed the project favorably—coal demand remained robust, GMDC's track record was solid, and government backing provided comfort. Yet the quantum of debt would fundamentally alter GMDC's balance sheet, transitioning from near-zero debt to significant leverage.

Market dynamics favored the expansion. India's coal demand continued growing despite renewable capacity additions. Domestic coal production lagged consumption growth, necessitating expensive imports. GMDC's Odisha coal, while not metallurgical grade, suited power generation and cement manufacturing—sectors with sustained demand visibility.

The competitive landscape had shifted too. Private miners like Adani and Jindal had emerged as formidable players through commercial auctions. GMDC's PSU status, once an unquestioned advantage, now faced scrutiny. The Odisha expansion was partly a response to this competition—scale would determine survival in India's consolidating mining sector.

The Gujarat Mineral Development Corporation (GMDC) is gearing up for the groundbreaking ceremony of its first coal mine in Odisha, the Baitarani West Opencast Coal Mine, set to take place in the next financial year, according to official sources. This groundbreaking wouldn't just inaugurate a mine but symbolize GMDC's transformation from regional champion to national player.

The strategic implications extended beyond immediate economics. At GMDC, we are dedicated to empowering India's future, a future that supports the nation's vision of a $5 trillion GDP, fuels the aspirations of 1.4 billion people and contributes to the rise of the world's third-largest economy. In alignment with India's commitment to achieving Net-Zero emissions by 2070, we recognise the importance of meeting immediate energy demands to sustain ongoing industrial and societal development. Therefore, we have strategically ventured into coal mining as a crucial step in the nation's energy journey. With every ton of coal that we mine, we are lighting the way forward for an Energy Self-reliant India.

This messaging carefully balanced energy security with environmental responsibility—acknowledging coal's transitional role while affirming commitment to eventual net-zero goals. GMDC positioned itself not as a climate villain but as a pragmatic enabler of India's development journey.

As 2024 progressed, execution became paramount. Mine development timelines stretched 3-4 years from land acquisition to commercial production. Equipment procurement, given global supply chain constraints, required careful planning. Recruitment and training of thousands of workers necessitated establishing training centers in Odisha. Every delay would impact returns on the massive capital deployed.

The Odisha expansion represented more than geographic diversification—it was GMDC's bid for relevance in India's evolving energy landscape, a bold bet that coal's sunset would be longer than markets anticipated, and a test of whether a 60-year-old PSU could reinvent itself for the next chapter of India's growth story.

VIII. Financial Performance & Market Position

The numbers tell a story of quiet excellence rarely seen in India's PSU landscape. Mkt Cap: 13,214 Crore (up 16.3% in 1 year); Revenue: 2,765 Cr; Profit: 666 Cr These metrics position GMDC among India's most efficient state-owned enterprises, generating returns that rival private sector competitors.

The standout feature remains GMDC's balance sheet strength. A zero-debt company, we're ranked 469th among India's Fortune 500 companies and among the top five organisations in the mining sector. In an industry notorious for capital intensity and leveraged balance sheets, GMDC's debt-free status represents extraordinary financial discipline. This wasn't luck but deliberate strategy—funding expansion through internal accruals, maintaining conservative capital structures, and prioritizing cash generation over aggressive growth.

Recent performance validates this approach. The company posted a net profit of ₹226.22 crore, up 20.79% from ₹187.24 crore in the same quarter last year. For the full financial year FY25, GMDC reported a net profit of ₹685.79 crore, up 14.8% from ₹597.36 crore in FY24. Total income for the year grew to ₹2,850.84 crore, an increase of 15.7% from ₹2,462.88 crore in FY24.

The margin profile reflects operational efficiency rarely associated with PSUs. The net profit margin has fluctuated between 19.97% and 27.18%, showcasing the company's profitability. These aren't commodity trader margins but reflect genuine value addition through integrated operations—mining, processing, and power generation each contributing to the margin stack.

Promoter Holding: 74.0% The government's continued majority stake provides stability while the 26% public float ensures market discipline. This ownership structure—neither fully government nor fully private—creates unique dynamics. The government backing provides access to mineral rights and patient capital, while public shareholders demand performance and transparency.

Dividend policy demonstrates commitment to minority shareholders. GMDC has been consistent with its dividend payouts, with a final dividend of ₹11.45 per share declared in September 2023. The company maintains a healthy dividend yield of 2.74%, making it an attractive option for income-focused investors. The 42.1% dividend payout ratio balances shareholder returns with growth capital retention.

Earnings include an other income of Rs.373 Cr. This substantial other income, primarily from treasury operations and investments, highlights GMDC's financial management sophistication. With significant cash reserves and no debt servicing obligations, the company generates meaningful returns from surplus fund deployment.

Earnings momentum continues strengthening. Earnings Per Share (EPS) have increased from ₹2.40 in Sep 2023 to ₹4.07 in Sep 2024, reflecting improved performance. This 70% EPS growth in a single year reflects both operational improvements and the earnings leverage from debt-free operations.

The market's response has been measured but positive. While the stock trades at modest multiples compared to private sector peers, the valuation discount typical of PSUs persists. Institutional investors appreciate the financial strength and dividend yield, while growth investors question the pace of expansion and capital allocation efficiency.

Analyst coverage remains limited—a common challenge for mid-cap PSUs. GMDC target price ₹237, a slight downside of -45.55% compared to current price of ₹435.3. According to 1 analysts rating. The wide divergence between analyst targets and market prices reflects differing views on GMDC's growth potential post-Odisha expansion.

The capital allocation framework demonstrates strategic evolution. On CNBC Awaaz: Shri Roopwant Singh details GMDC's INR 3000 Cr. CapEx Plan for FY25, along with other future growth strategies This ₹3,000 crore capex program—substantial for a company with ₹2,765 crore annual revenue—signals transformation ambitions. The investment spans Odisha coal mine development, renewable energy expansion, and technology upgradation.

Operational metrics validate financial performance. The company produces 8-9 million tonnes of lignite annually, operates at high capacity utilization, and maintains long-term supply contracts providing revenue visibility. Power generation adds ₹400-500 crore annual revenue with superior margins. The diversified revenue streams—lignite (60%), power (20%), other minerals (20%)—provide resilience against commodity cycles.

Working capital management deserves recognition. Despite operating in a business requiring significant inventory (extracted minerals) and extended credit periods to industrial customers, GMDC maintains negative working capital cycles through advance payments and efficient collections. This cash generation capability funds growth without external capital.

The ongoing Russia-Ukraine war has pushed coal prices higher, which impacts GMDC's pricing and profitability. Additionally, GMDC's low debt levels, strong revenue growth, and healthy profit margins contribute to its financial stability Global energy market disruptions, while challenging for energy importers, benefit domestic producers like GMDC through improved realizations and market share gains.

Tax efficiency adds another dimension. The effective tax rate saw a decline in the most recent quarter, contributing to higher net profit. Accelerated depreciation on mining equipment, depletion allowances, and renewable energy incentives reduce the tax burden, enhancing post-tax returns.

The sustainability of financial performance hinges on several factors. Lignite reserves in Gujarat, while substantial, face depletion over 15-20 years. The Odisha expansion addresses this through 2 billion tonnes of coal reserves, providing 30+ years of production visibility. Renewable energy investments hedge against fossil fuel transition risks.

Comparative analysis with peers reveals GMDC's unique position. Unlike Coal India (massive scale but lower margins), NMDC (iron ore focus), or Vedanta (high debt, aggressive growth), GMDC combines reasonable scale with financial conservatism and operational diversity. The company occupies a sweet spot—large enough for operational efficiency, small enough for agility.

Risk factors remain material. Commodity price volatility can impact profitability despite long-term contracts. Environmental regulations may increase compliance costs or restrict expansion. The Odisha projects require successful execution of the largest capital program in GMDC's history. Competition from private miners and renewable energy could pressure market share and margins.

The investment thesis crystallizes around transformation potential. Current valuation reflects a regional lignite miner with steady but unspectacular growth. Successful Odisha execution could rerate GMDC as a national coal producer with multi-decade reserves. The debt-free balance sheet provides flexibility to fund this transformation without diluting returns.

Yes, Gujarat Mineral Development Corporation Ltd (GMDC) is essentially debt-free and has maintained this position for the past five years. GMDC's low debt levels indicate a solid financial standing, enhancing its credibility and stability in the market. This debt-free status is one of the key factors contributing to the company's ability to maintain a strong financial position and continue with its investments in the mining sector.

This financial fortress, built over six decades of conservative management, now enables GMDC's boldest phase—a phase where accumulated strengths deploy toward national ambitions, where patient capital meets massive opportunity, where a PSU attempts to prove that government ownership need not mean mediocre returns.

IX. Growth Strategy & Future Roadmap

The transformation blueprint crystallizes in Project Shikhar—GMDC's audacious plan to reinvent itself for the next decade. GMDC's Project Shikhar outlines an ambitious goal to quadruple revenues by 2030, with equal contributions from lignite, coal, and critical minerals. This isn't incremental improvement but fundamental reimagination—from ₹2,765 crore to over ₹11,000 crore in five years.

GMDC has embarked on an ambitious journey with Project SHIKHAR - a strategic transformation initiative aimed at building a diversified portfolio across minerals and power assets, while also expanding its presence across the value chain through downstream integrations. The three-pillar strategy—lignite, coal, and critical minerals—each contributing equally to revenues represents portfolio theory applied to mining, hedging against commodity cycles and technological disruption.

The lignite pillar, despite being the legacy business, targets aggressive growth. The company is strategically transforming its operations, aiming to quadruple revenues by 2030 while maintaining a strong focus on its core lignite business, which is projected to reach 15 million tons annually. This 67% production increase from current levels requires expanding existing mines, developing new deposits, and improving extraction efficiency through technology adoption.

The coal pillar leverages the Odisha expansion. With 2 billion tonnes of reserves across three blocks, GMDC targets 15-20 MTPA production by 2030. This alone could generate ₹3,500-4,000 crore annual revenue at current coal prices. The strategic positioning near industrial corridors in eastern India provides market access advantages over imported coal.

But the most intriguing pillar is critical minerals. GMDC has set up a dedicated critical minerals division, marking its intent to play a key role in India's rare earth and energy transition strategy. Projects are underway to explore lithium, rare earths, copper, and phosphate, both independently and in partnership with PSUs like MECL, NALCO and GSI.

The rare earth opportunity deserves special attention. China controls approximately 49% of global rare earth reserves and 69–90% of refining capacity, giving it substantial influence over the supply chain. Recent moves by China to restrict rare earth exports have raised concerns for industries reliant on these materials, such as electric vehicles (EVs), wind turbines, and high-performance electronics.

In response, the Indian government, led by the Prime Minister's Office (PMO), held a high-level meeting in July 2025 to address the rare earth crisis. This development has spotlighted GMDC, which is actively exploring opportunities in the critical minerals sector. The company has reportedly allocated Rs 3,000-4,000 crore for critical mineral projects.

A JV with NALCO for rare earths and bauxite in Gujarat has been signed, while a MoU with the Ministry of Mines targets collaborative exploration. Gujarat's geology, particularly in Kutch and Saurashtra, shows promising rare earth potential. GMDC's existing mining leases and exploration expertise position it advantageously for quick deployment once deposits are confirmed.

Digital transformation underpins the growth strategy. GMDC has made significant strides in developing digital mines of the future through the deployment of digital productivity solutions for mine operations. There is increased focus on adopting a data-based approach with the development of a digital integrated control tower. This isn't IT modernization but fundamental operational reimagination—AI-powered geological modeling, IoT-enabled equipment monitoring, predictive maintenance algorithms.

In order to unlock value and achieve multifold expansion at GMDC, over 30 opportunities are being explored. These opportunities span across multiple strategic imperatives, including sales acceleration, achieving best-in-class efficiencies, embedding digital solutions and analytics deeply into the organisation's culture, and creating a positive impact on society.

Downstream integration represents another growth vector. Additionally, to future-proof the organisation's growth, multiple green-field initiatives have been prioritised, including the set-up of beneficiation plants, manufacturing of value-added and downstream products such as cement and building additional capacities for renewable power generation.

The cement opportunity is particularly compelling. GMDC's limestone reserves, combined with captive power generation and logistics infrastructure, create competitive advantages for cement manufacturing. A 2-3 MTPA cement plant could add ₹1,500-2,000 crore revenue while capturing value currently leaked to cement manufacturers buying GMDC's limestone.

GMDC has a huge stock of mined out Silica Sand and similar in-situ deposits in one of its upcoming projects. As a part of forward integration, GMDC is seeking to explore new avenues in diversified sector in silica sand as well as other allied industries by value addition for manufacturing of float glass, solar panels, etc. The solar glass opportunity aligns with India's renewable energy push, potentially creating a captive market for value-added silica products.

Capital allocation reflects these priorities. With ambitious capital expenditure plans exceeding INR 3,000 crores, management is optimistic about enhancing production capabilities and diversifying revenue streams The funding mix—internal accruals, strategic debt, and potential partnerships—maintains balance sheet strength while enabling transformation.

The human capital strategy evolves in parallel. Become employer of choice, with ample opportunities for people enablement and upskilling. GMDC needs geologists for rare earth exploration, data scientists for digital mines, chemical engineers for beneficiation plants, and finance professionals for complex project structuring. This talent transformation, perhaps more than capital investment, will determine success.

Risk management becomes increasingly sophisticated. Portfolio diversification across minerals like Manganese, Base metals, etc. to future-proof GMDC's growth. Geographic diversification (Gujarat and Odisha), commodity diversification (lignite, coal, rare earths), and value chain integration (mining to manufacturing) create multiple risk hedges.

The partnership strategy leverages ecosystem strengths. Collaborations with NALCO for alumina, potential JVs for rare earth processing, technology partnerships for digital transformation—GMDC recognizes that going alone limits growth potential. Strategic partnerships provide technology, market access, and risk sharing.

Supporting the inclusive growth of society remains the key focus area for GMDC, while paying special attention towards the MSME segment, thus leading the way from Aatmanirbhar Gujarat to Aatmanirbhar Bharat. This isn't CSR rhetoric but business strategy—MSMEs provide stable demand for lignite, local community support enables smooth operations, and government backing depends on developmental impact.

Market reception to Project Shikhar has been mixed but increasingly positive. Venture Securities, a prominent brokerage, issued a bullish report, projecting a long-term price target of ₹700, implying a 60% upside from the July 2025 closing price of ₹435. This aggressive target reflects confidence in GMDC's ability to capitalize on the critical minerals boom.

The execution challenges are substantial. Scaling production 4x requires flawless project execution across multiple sites. Technology adoption demands cultural change in a traditional PSU. Talent acquisition competes with private sector pay scales. Environmental clearances grow more stringent. Competition intensifies as private players recognize opportunities.

Yet the strategic logic remains compelling. India's energy transition requires both traditional fuels (coal for baseload power) and new materials (rare earths for EVs and renewables). GMDC's portfolio spans this spectrum. The International Energy Agency (IEA) forecasts that demand for critical minerals will need to triple by 2030 and quadruple by 2040 if we are to achieve net-zero emissions.

Five companies that could gain as India invests Rs 10 billion to build a domestic rare earth magnet ecosystem... Last on the list is GMDC... Its access to Gujarat's rich mineral belts, coupled with a clean balance sheet and state backing, make it one of the more quietly strategic plays in this space. In an ecosystem where India is racing to build rare earth magnet capacity, GMDC's early moves could pay off.

The transformation timeline is aggressive but achievable. 2025-2026 focuses on Odisha mine development and critical mineral exploration. 2027-2028 sees commercial production from coal mines and pilot rare earth processing. 2029-2030 targets full-scale integrated operations across all three pillars. Each milestone de-risks the transformation while building credibility.

As GMDC embarks on this journey, it attempts something rare in Indian corporate history—a PSU transforming itself not through privatization but through strategic reinvention, leveraging accumulated strengths while embracing new opportunities. Project Shikhar isn't just GMDC's growth plan; it's a test case for whether India's state-owned enterprises can lead rather than follow in the country's economic transformation.

X. Playbook: Lessons in State-Led Industrial Development

The GMDC story offers a masterclass in patient, strategic industrial development—a playbook increasingly relevant as nations grapple with resource security, energy transitions, and the role of state capital in strategic sectors. These lessons, distilled from six decades of evolution, transcend mining to offer insights for any long-gestation, capital-intensive industry.

Building from Zero: The Power of Starting Small

GMDC's journey from a single silica sand quarry to a ₹13,000 crore enterprise demonstrates the compound effect of consistent execution. The company didn't attempt to become a mining giant overnight. Each decade brought measured expansion—first silica sand, then bauxite, fluorspar in the 1970s, lignite dominance in the 1980s, power generation in the 1990s. This stepping-stone approach reduced execution risk while building organizational capabilities incrementally.

The lesson: ambitious visions require modest beginnings. GMDC's early leaders resisted the temptation to pursue every mineral simultaneously. They mastered one operation before expanding to the next, creating a foundation of operational excellence that enabled later rapid scaling. Private enterprises often fail by attempting too much too soon; GMDC succeeded by doing less, better.

Vertical Integration as Competitive Moat

The decision to build the Akrimota Thermal Power Station transformed GMDC from a commodity supplier to an integrated energy company. This wasn't just value addition—it was strategic positioning. By consuming its own lignite for power generation, GMDC captured the entire value chain from extraction to electron. The 250 MW plant generates returns far exceeding simple mining, while providing a captive market for lower-grade lignite unmarketable to external customers.

The integration extends beyond power. Bauxite calcination plants, fluorspar beneficiation facilities, and planned cement manufacturing create multiple value-capture points. Each integration step reduces market risk (captive consumption), improves margins (eliminating middlemen), and creates competitive advantages (lower input costs than standalone operators).

Managing the PSU-to-Listed Transition

GMDC's 1999 IPO, divesting 26% government stake, created a unique hybrid—majority state-owned but market-disciplined. This structure balanced competing objectives: government's developmental goals with minority shareholders' return expectations. The company had to evolve from bureaucratic processes to quarterly earnings calls, from five-year plans to market guidance.

The transition succeeded because GMDC retained PSU advantages (preferential mining rights, patient capital, government support) while adopting private sector practices (performance metrics, investor relations, competitive procurement). The 74% government holding provided stability; the 26% public float enforced discipline. This hybrid model—neither fully public nor fully private—may offer a template for other strategic sector PSUs.

Patient Capital's Underappreciated Advantage

Mining requires decades-long investment horizons. Exploration takes years, mine development another 3-5 years, and payback periods stretch over decades. Private capital, focused on quarterly returns, often struggles with such timelines. GMDC's government backing provided patient capital willing to wait for returns—a crucial advantage in a business where rushing means failure.

Consider the Odisha expansion: ₹8,000 crore investment over 35 years, with meaningful returns only after year five. Private miners might struggle to fund such projects without excessive leverage. GMDC's state backing enables conservative financing structures that survive commodity downturns. Patient capital isn't just about funding—it's about strategic flexibility to pursue long-term value over short-term profits.

Balancing Social Responsibility with Commercial Objectives

GMDC operates in some of Gujarat's most backward regions. Mining projects became catalysts for regional development—roads, schools, hospitals, and employment followed the mines. The company spent significantly on community development, not as charity but as operational necessity. Social license to operate, particularly in tribal areas, required genuine developmental impact.

The ₹663 crore R&R budget for Odisha (nearly 10% of project cost) reflects learned wisdom: community opposition can destroy projects regardless of legal rights. GMDC's approach—generous compensation, skill development, local employment preference—transforms potential opponents into stakeholders. This isn't altruism but pragmatic risk management.

Land Acquisition Expertise as Core Competency

Over six decades, GMDC has acquired thousands of hectares across Gujarat and now Odisha. This expertise—understanding land records, navigating state regulations, managing stakeholder negotiations—represents invaluable institutional knowledge. In India, where land acquisition often derails projects, GMDC's track record stands out.

The company's approach combines legal process with relationship management. Local officials trust GMDC's commitments based on decades of fulfilled promises. Farmers accept GMDC's compensation packages knowing the company's reputation for fair dealing. This soft infrastructure—trust, relationships, reputation—takes decades to build and represents an uncopiable competitive advantage.

Diversification Timing: When Geography Meets Opportunity

GMDC's expansion followed a clear pattern: first, dominate home geography (Gujarat), then expand products (multiple minerals), then integrate vertically (power generation), and finally expand geographically (Odisha). This sequencing wasn't accidental but strategic—each phase built capabilities for the next.

The Odisha expansion came only after GMDC had exhausted growth opportunities in Gujarat and built operational excellence across multiple minerals. Geographic expansion without operational mastery invites failure; GMDC waited until it had both capabilities and capital to succeed outside home territory.

Technology Adoption in Traditional Industries

Mining seems antithetical to technology—an industry of explosives and excavators, not algorithms and analytics. Yet GMDC's digital transformation demonstrates how traditional industries benefit from technology. ERP systems coordinate operations across dispersed sites. Drone surveys improve geological modeling. IoT sensors optimize equipment utilization. AI algorithms predict equipment failures.

The key insight: technology adoption in traditional industries requires different approaches than in tech-native sectors. Change management matters more than change itself. GMDC's gradual technology adoption—starting with basic IT systems, progressing to ERP, then IoT, now AI—respected organizational capacity for change while continuously modernizing operations.

The Regulatory Navigation Advantage

Operating as a PSU provides unique advantages in navigating India's complex regulatory environment. GMDC understands government processes, has relationships with regulatory bodies, and benefits from inter-departmental coordination. Environmental clearances, mining leases, and land acquisitions—all move faster for a government entity than private players.

This isn't corruption but institutional alignment. Regulators trust GMDC to follow rules, knowing government ownership ensures compliance. Politicians support GMDC projects, understanding the developmental impact. Bureaucrats facilitate GMDC operations, recognizing shared objectives. This regulatory navigation capability—built over decades—represents a sustainable competitive advantage in a highly regulated industry.

Crisis Management Through Diversification

GMDC survived multiple crises through portfolio diversification. When lignite prices crashed, bauxite provided cushion. When power plant operations faced challenges, mining revenues sustained profitability. When environmental regulations threatened mining expansion, renewable energy provided growth. This diversification wasn't random but strategic—related enough for synergies, different enough for risk mitigation.

The lesson extends beyond minerals. Geographic diversification (multiple mining sites), customer diversification (hundreds of industrial customers), and temporal diversification (long-term contracts with varied expiry dates) create resilience. GMDC's boring stability—no dramatic booms or busts—reflects sophisticated risk management through diversification.

Building Institutional Knowledge

GMDC's true asset isn't mineral reserves but institutional knowledge—how to explore, extract, process, and market minerals in India's complex environment. This knowledge, accumulated over six decades, resides in processes, relationships, and organizational culture. New entrants can buy equipment and hire talent but cannot replicate decades of learning.

Consider lignite mining expertise: understanding Gujarat's geology, optimal extraction techniques for local conditions, quality requirements of different customer segments, logistics optimization for dispersed mines. This tacit knowledge—undocumented, experiential, contextual—creates sustainable competitive advantages that financial capital cannot buy.

The Partnership Paradox

Despite being a monopoly in several minerals, GMDC increasingly embraces partnerships. JVs with NALCO for alumina, collaborations for rare earth exploration, technology partnerships for digital transformation—the company recognizes that dominance requires collaboration, not isolation.

Partnerships provide what GMDC lacks: technology (international mining companies), market access (downstream manufacturers), and specialized expertise (rare earth processing). In return, GMDC offers what partners need: mineral rights, regulatory navigation, and operational infrastructure. This partnership approach—leveraging strengths while acknowledging limitations—enables faster growth than organic expansion alone.

Succession Planning in PSUs

GMDC's leadership transitions, typically IAS officers on deputation, could disrupt continuity. Yet the company maintains strategic consistency across leadership changes. This reflects robust institutional processes—strategic plans outlive individual leaders, professional management ensures operational continuity, and board oversight provides strategic stability.

The lesson: sustainable organizations transcend individual leaders. GMDC's boring consistency—no dramatic strategy reversals with leadership changes—reflects institutional maturity. Strong processes, clear strategies, and professional management create organizational resilience that survives leadership transitions.

These lessons—patience, integration, diversification, partnership, and institutional strength—offer a playbook for industrial development in emerging markets. GMDC's journey demonstrates that state-owned enterprises, despite their limitations, can create substantial value when strategy, execution, and governance align. The playbook isn't about choosing between state and private ownership but understanding each model's strengths and designing hybrid structures that capture both advantages.

XI. Analysis: The Bull & Bear Cases

The Bull Case: A Decade of Exceptional Growth Ahead

The optimistic view on GMDC rests on a convergence of favorable factors that could drive exceptional returns over the next decade. At the core lies 2.1 billion tons of reserves in Odisha alone—a resource base that transforms GMDC from a regional player depleting Gujarat's lignite over 15-20 years into a national mining company with 30+ years of growth visibility. These aren't speculative resources but proven reserves acquired through competitive bidding, providing clear volume growth trajectory.

The debt-free balance sheet providing flexibility represents GMDC's hidden superpower. While competitors struggle with 2-3x debt-to-equity ratios, GMDC can fund its entire ₹8,000 crore Odisha expansion through internal accruals and modest leverage. This financial flexibility enables countercyclical investment—expanding when competitors retreat during downturns, acquiring distressed assets, and pursuing opportunities without dilution.

Government backing and strategic importance provides advantages beyond capital. In critical minerals, government support translates to preferential exploration rights, faster environmental clearances, and diplomatic support for international partnerships. As rare earth becomes a national security priority, GMDC's PSU status transforms from bureaucratic burden to strategic asset. The government won't let GMDC fail—an implicit guarantee valuable during crisis periods.

GMDC emerges as an energy transition beneficiary through a paradoxical dynamic. Near-term, coal demand surges as India builds baseload capacity for renewable integration. Thermal power generation increases 5-7% annually despite renewable capacity additions, driving coal demand. Long-term, GMDC's critical minerals position it for the post-carbon economy. The company plays both sides of the energy transition—coal for today's baseload, rare earths for tomorrow's EVs.

The critical minerals opportunity could transform GMDC's valuation multiple. Current valuation reflects a traditional mining company; successful rare earth development could trigger rerating as a strategic minerals player. Consider MP Materials in the US—trading at 5x revenue despite being pre-revenue until recently. GMDC with proven rare earth production could command similar premiums given India's strategic imperatives.

Operational leverage provides earnings explosion potential. Mining's high fixed costs mean incremental production drops directly to bottom line. If GMDC achieves 15 MTPA coal production by 2030, with ₹500 per tonne EBITDA, that alone adds ₹750 crore to profits. Combined with lignite growth, rare earth development, and power expansion, earnings could triple by 2030.

The renewable energy hedge protects against stranded asset risk. With 200 MW wind and 5 MW solar, GMDC generates ₹100+ crore annual profit from renewables. Planned expansion to 500 MW renewable capacity by 2030 could generate ₹300-400 crore annual profit. Even if coal becomes stranded, renewable assets provide value floor.

Valuation remains undemanding despite recent appreciation. At ₹13,000 crore market cap, GMDC trades at 20x P/E, 1.5x book value—reasonable for 15% ROE business. Comparable private miners trade at 25-30x P/E. If GMDC delivers on Project Shikhar, earning ₹1,500-2,000 crore by 2030, the stock could triple even at current multiples.

Hidden assets provide additional upside. Land banks around mining sites, especially near expanding cities, hold substantial value. Water rights in water-scarce regions become increasingly valuable. Mining rights for unexploited minerals could be monetized through partnerships. These options, unvalued by markets, provide free upside.

The ESG transformation potential surprises skeptics. GMDC's reclaimed mine solar projects, commitment to net-zero, and community development programs position it as a responsible miner. ESG funds, currently excluded due to coal exposure, might reconsider as GMDC's renewable and critical mineral exposure increases. ESG inclusion would expand the investor base and valuation multiples.

The Bear Case: Structural Challenges and Execution Risks

The pessimistic view highlights substantial risks that could impair GMDC's transformation ambitions. Commodity price volatility remains the primary concern. Lignite and coal prices fluctuate 30-50% through cycles. A sustained downturn, driven by renewable energy acceleration or economic slowdown, would devastate profitability. Unlike diversified miners with precious metals exposure, GMDC depends entirely on industrial minerals tied to economic cycles.

Environmental and regulatory pressures intensify annually. Courts increasingly restrict mining in ecologically sensitive areas. Environmental clearances that took months now take years. Compliance costs escalate with stricter pollution norms. The Odisha coal mines face particular scrutiny given the state's history of mining conflicts. One adverse court ruling could strand billions in investments.

Operational challenges with Akrimota Power Station highlight execution risks. The plant operates below capacity due to technical issues and grid constraints. Lignite's high ash content causes frequent breakdowns. Maintenance costs exceed budget. If GMDC struggles with a single power plant, can it execute multiple coal mines simultaneously?

Competition from private miners erodes GMDC's advantages. Adani, Vedanta, and JSW bid aggressively for coal blocks, often outbidding PSUs. These companies move faster, operate more efficiently, and access capital markets better. In critical minerals, international giants like Rio Tinto and Glencore bring superior technology and processing expertise. GMDC's PSU culture may prove inadequate against nimble private competition.

Geographic concentration risk persists despite Odisha expansion. 70% of revenues still derive from Gujarat operations. Customer concentration adds another layer—top 10 customers account for 60% of lignite sales. Loss of key customers to imported coal or renewable energy would disproportionately impact revenues.

Execution risk on Odisha projects looms large. GMDC has never operated outside Gujarat, never managed coal mining at scale, never handled projects of this magnitude. Land acquisition in Odisha, with its history of mining conflicts, poses unique challenges. Local political dynamics differ from Gujarat. Labor relations, contractor management, and stakeholder engagement—all require capabilities GMDC must build from scratch.

Stranded asset risk accelerates with energy transition. India's net-zero commitment by 2070 implies coal phase-out post-2040. With 25-30 year mine development cycles, Odisha coal mines might never recover investments if coal phase-out accelerates. Lignite, with lower energy content and higher emissions, faces obsolescence first. GMDC could own billions in stranded assets within 15-20 years.