Globus Spirits: The Distillation of a Premium Powerhouse

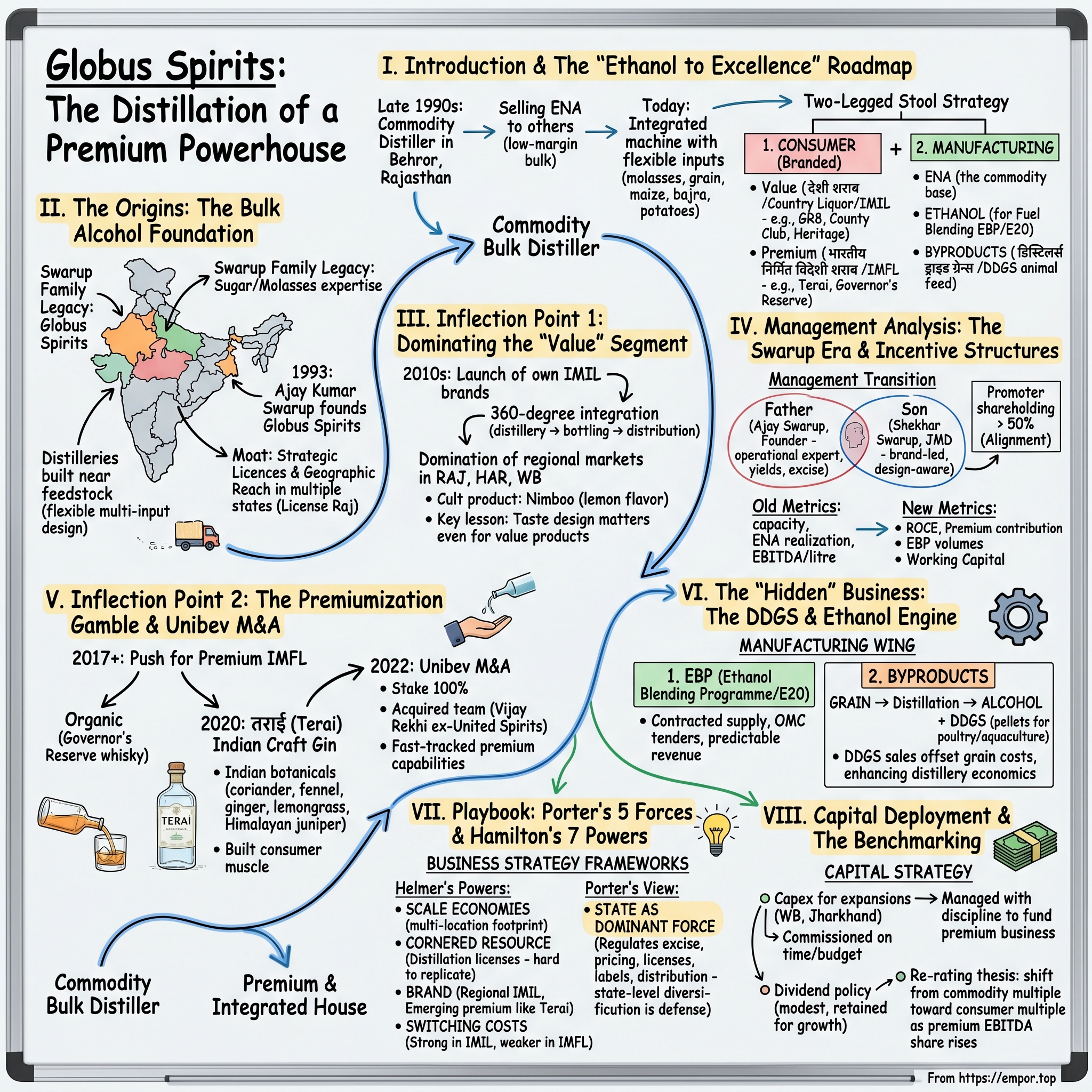

I. Introduction & The "Ethanol to Excellence" Roadmap

Picture a dusty highway in रajasthan in the late 1990s. A truck loaded with steel drums rumbles out of a nondescript industrial estate in Behror, headed to bottling plants across North India. Inside those drums is something almost no consumer has ever heard of: अतिरिक्त तटस्थ अल्कोहल Extra Neutral Alcohol (ENA), the colourless, scentless, 96%-strength base liquid that goes into everything from cheap rum sold in single-use pouches to the most expensive single malt on a Delhi bar shelf. The truck does not carry a brand. It does not carry a story. It is, in every sense, a commodity. The man who owns the plant — स्वरूप Ajay Kumar Swarup — has, by this point, spent two decades quietly mastering the unglamorous craft of fermenting molasses and broken rice into industrial ethanol. He sells what he makes to other people, who put their labels on the bottle.

Now jump forward to a bar at The Leela in Mumbai, on a humid evening in 2022. A bartender pours a clear spirit over a long shard of ice, drops in a slice of pink grapefruit, and slides it across the polished teak. "Terai," he says. "Indian craft gin. Made in Rajasthan." The guests, a mix of consultants and venture investors, lean in. The label, with its monsoon-grass illustration and a price point above ₹2,000 a bottle, looks like something out of London or Brooklyn. Almost none of them know that the same company quietly distilling the gin also runs one of the largest country-liquor operations in India, supplies ethanol to Indian Oil, sells dried distillers' grain to poultry farms, and operates plants that can turn आलू potatoes, bajra millet, broken rice, or maize into alcohol depending on which feedstock is cheapest that fortnight.1[^2]

That is the puzzle of Globus Spirits Limited. On the surface it looks like three different companies stapled together: a low-margin bulk distiller, a regional mass-market liquor empire, and a small but premium craft-brand house. The thesis of this episode is that what looks like sprawl is, in fact, a deliberate machine. Globus is the story of "re-rating": taking the cash flow from a regulated, commoditised manufacturing base and using it to fund a slow, patient migration up the value chain — into premium consumer brands on one side, and into India's strategic इथेनॉल सम्मिश्रण कार्यक्रम Ethanol Blending Programme on the other.3

The two-legged stool is worth holding in your head for the next ninety minutes. One leg is the Consumer business — what the company calls "branded" — covering both देशी शराब Country Liquor (IMIL) for the value segment and भारतीय निर्मित विदेशी शराब Indian Made Foreign Liquor (IMFL) for the premium segment. The second leg is the Manufacturing business — ENA, ethanol for fuel blending, and the byproduct डिस्टिलर्स ड्राइड ग्रेन्स विद सॉल्यूबल्स DDGS (Distillers Dried Grains with Solubles), a high-protein animal feed that sounds boring until you realise it has quietly become a profit centre in its own right.[^2][^3]

The market, until very recently, refused to give Globus credit for the consumer leg. It traded the stock the way it trades a sugar mill: on EBITDA and capacity, not on brands and aspiration. The bet management is making — and the bet investors are now trying to handicap — is that the next decade of growth will come precisely from the gap between how Globus is valued today and how it would be valued if you stripped out the consumer business and listed it separately. To understand whether that gap will close, we have to start in a cane field in उत्तर प्रदेश Uttar Pradesh, nearly a century ago.

II. The Origins: The Bulk Alcohol Foundation

The Swarup name is not new to Indian alcohol. The family's commercial roots wind back into the sugar industry of pre-Independence North India, where molasses — the dark, viscous residue left after sugar is crystallised from cane — was treated for decades as a problem, not a product. Mills paid to have it carted away. The ones who paid attention realised that molasses, mixed with water and yeast in a fermenter, became something else entirely: industrial alcohol. The Swarups were among the families who paid attention. By the time Ajay Kumar Swarup formally established the entity that would become Globus Spirits Limited in 1993, three generations of accumulated process knowledge — what temperature the wash should hold at, how to manage the foam in a continuous fermenter, which copper plates inside a distillation column degrade fastest — already sat inside the family.4

The early Globus business model was almost monastically simple: build a low-cost distillery as close as possible to the feedstock, run it twenty-four hours a day, and sell the output to anyone who held the consumer-facing license. ENA is the un-poetic centre of the Indian alcohol industry. Every IMFL whiskey, every बैंगनी desi rum, every gin and vodka eventually starts as ENA. The buyer adds flavouring, ageing (or, more often in India, not ageing), water, and a label. The economics, on the surface, are brutal: ENA is sold by the bulk litre, priced off a moving average of grain and molasses inputs, and the customer base is concentrated among large bottlers and state corporations. There is essentially no brand premium. The only way to win is to be the lowest-cost producer in your geography, and to never, ever miss a delivery to a bottling line that is running to a state-mandated quota.[^9]

But there is a second layer that makes Indian alcohol manufacturing interesting in a way that, say, refining sugar is not, and that is the License Raj legacy. Alcohol in India is governed not by the Centre but by the States. Each state runs its own excise department, its own licensing regime, its own labelling rules, its own distribution channel — sometimes a state corporation, sometimes a quota-restricted private wholesaler, sometimes a public-sector retail chain. The system is a patchwork inherited from the 1950s, when the founding fathers of the Republic, uncertain whether to honour Mahatma Gandhi's instinct for prohibition or to capture the obvious tax revenue, compromised by placing the question in the State List.6 Seven decades later, that compromise still defines the industry. A licence to manufacture grain alcohol in Haryana does not let you make a single rupee in Bihar. A pouch brand that dominates West Bengal may be illegal in Gujarat. And every five years, when a state government changes, the rules of the game can change with it.

For an entrepreneur, the regulatory complexity is either a wall to scream at or a moat to live behind. Ajay Swarup chose the second framing. The family invested in the painstaking, deeply unglamorous work of acquiring distillery licences in multiple states — a process that can take years, requires environmental clearances, water allocations, and pollution-board sign-offs, and is in practice almost impossible for a new entrant without political relationships and balance-sheet patience. The thesis was simple: in a country where the licence is harder to get than the technology, the licence is the technology. Build the moat once, defend it forever.

Operationally, the founding vision was efficiency. Swarup obsessed over the unit economics of distillation: the conversion ratio of grain to alcohol (typically around 380–400 litres of ENA per metric ton of broken rice, depending on starch content), the steam consumption per litre, the fermentation cycle time. He pushed for multi-feedstock plants — designs that could swing between molasses, broken rice, maize, and even अनाज bajra, depending on which input the कमोडिटी commodity cycle had made cheapest that quarter. That flexibility, which sounds like a small engineering detail, would later become a structural advantage. When a drought spiked sugar prices in 2009, Globus could shift to grain. When grain prices spiked in 2022, Globus could shift back to molasses. Single-feedstock competitors did not have that option.

What this period built was a chassis: low-cost, flexible, regulator-tested, with installed capacity in the right states. What it did not build was a brand. By the late 2000s, with the chassis ready, the question on the dinner table at the Swarup household was no longer "how do we make ENA cheaper." It was: "Should we ever make our own bottle?"

III. Inflection Point 1: Dominating the "Value" Segment

Walk into a thekha — a state-licensed country-liquor shop — in a small town in Rajasthan on a weekday evening, and the visual cue tells you everything. The shop is a metal grille, the customers are construction workers, farm labourers, auto-rickshaw drivers. There is no shelving and no consultative selection. The product moves in 200-millilitre pouches, sold for less than the price of a McDonald's coffee in Delhi, and consumed often within metres of the counter. This is the IMIL market — Indian Made Indian Liquor — and for most of the urban analyst community, it is invisible. It is also, by volume, several times larger than the entire IMFL premium segment. India drinks far more cheap country liquor than it drinks Black Label.[^9]

In the early 2010s, Globus made the decision that would define the next decade of its consumer story: instead of selling its ENA to other bottlers and watching them capture the margin, it would launch its own IMIL brands and sell directly into this enormous, underserved market. The mathematics was obvious. ENA sold to a bottler at, say, ₹40 a litre delivered. The same litre, bottled into a pouch with a flavouring, a label, and a story, retailed at three to four times that, of which the manufacturer captured a meaningful slice after state excise. The catch was that the customer was loyal, regional, and price-sensitive in a way that did not respect Mumbai-style brand-building. You could not parachute a Delhi advertising agency into rural Haryana and expect to win.

So Globus built the brands inside the regions where it already had distilleries. The result was a portfolio that almost no Reuters-reading investor could name — Heritage, GR8, County Club Punjab Medium — but which dominated specific corners of specific maps. In Rajasthan, in Haryana, in West Bengal, the company became one of the largest IMIL players, in some districts the single largest.[^11] The integration was almost surgical: the distillery, the bottling line, the brand, and in some states the depot relationship with the state corporation, all under one roof. The company called this "360-degree integration." Anyone who has tried to run a fast-moving consumer goods business in rural India with a third-party supply chain understands why that integration mattered. It collapsed a five-link supply chain into a two-link one and squeezed the working capital out of the middle.

The cult product of this era was the lemon — नींबू nimboo — flavour variant. On paper, it should not have worked. The Indian IMIL drinker, the conventional wisdom said, wanted "plain" — the rougher the better. But the Globus marketing instinct, informed by years of distributor feedback, sensed a different truth: the drinker wanted the burn of strong alcohol covered up by a familiar taste, and नींबू, the universal Indian palate cleanser, was the perfect mask. The lemon variant became a runaway hit in Rajasthan. The success embedded a quiet strategic insight that would reappear later in the premium gin story: even at the value end, taste design matters. A commodity, presented with the right sensory wrapper, becomes a brand.

The financial signature of this period was distinctive. Operating margins in the manufacturing segment were thin — high single digits, swinging with the molasses cycle — but the consumer segment, once at scale, threw off materially higher per-litre contribution.[^11] Peers in the broader Indian liquor space, who had stayed asset-light, were structurally locked out: they could spend on marketing, but they could not match a vertically integrated producer's ability to absorb a feedstock spike without raising the shelf price. In the cyclical trough years of the mid-2010s, when ENA prices collapsed across the industry, the Globus consumer business effectively subsidised the manufacturing business and kept the company's return on capital ahead of pure-play distillers.

The Value segment did one other thing for Globus that, in retrospect, was even more important than the margin lift: it taught a manufacturing organisation how to be a consumer organisation. Trade marketing, distributor incentives, label refresh cycles, depot-level inventory management — none of these are things a bulk-ENA seller ever has to think about. By the time the company turned its attention upmarket, that consumer muscle, built first in the most price-sensitive corner of the industry, was real. That migration upmarket would, however, require not just operational change. It would require new people, new incentives, and a new generation in the corner office.

IV. Management Analysis: The Swarup Era & Incentive Structures

There is a particular type of Indian family-business handover that does not show up in MBA case studies because it does not look like a handover at all. It looks like a slow, almost imperceptible reweighting of who speaks first in the room. At Globus, that reweighting has been happening for the better part of a decade, between Ajay Kumar Swarup and his son, Shekhar Swarup.

Ajay Swarup is the archetype of the first-generation Indian manufacturing CEO: trained in the language of yields, cycle times, and excise officers, with the kind of operational instinct that you only acquire by walking the factory floor for forty years. In investor calls, his temperament is recognisable — patient, slightly understated, more comfortable talking about a recovery rate of broken rice than a brand campaign. He is, fundamentally, an operator. The moat he built — multi-state licences, multi-feedstock flexibility, low-cost positioning — is the moat of a man who believes the most reliable form of competitive advantage is unglamorous excellence at things competitors find boring.[^12]

Shekhar Swarup, the Joint Managing Director, represents a different sensibility. He came into the business at a moment when the parent industry was being reshaped — by the entry of foreign majors after liberalisation, by the early signs of premiumisation, by the digital-first habits of a younger Indian consumer who would not drink what his father drank. Shekhar's instinct, on the public record across interviews and earnings calls, is more brand-led, more design-aware, more willing to invest in things that do not return capital in the next financial year.[^12] The internal joke, in private conversations with bankers covering the company, has been that the father runs the plant and the son runs the label. It is a caricature, but like all good caricatures it contains a truth: the management transition has been, in effect, the transition of Globus's strategic centre of gravity from the still to the bottle.

Crucially, the family did not delegate this transition to professional outsiders. Promoter shareholding has stayed concentrated — north of half of the equity remains with the promoter group, an ownership structure that, in an Indian context, signals durable alignment with minority shareholders.2 The Swarups are not pulling their wealth out of the business; the great majority of their net worth is inside the stock. That alignment matters enormously, because the strategic bet — funding low-return-on-capital brand investment today for high-return-on-equity brand earnings tomorrow — is exactly the kind of bet a hired CEO on a three-year contract would refuse to make, and exactly the kind a family with a generational horizon will sign off on.

The professionalisation of the board, however, is real, and worth noticing. Over the past several years, Globus has added independent directors with backgrounds in consumer goods, financial services, and the spirits industry specifically — including, notably, the founder of the Unibev premium business, Vijay Rekhi, whose decades at United Spirits make him one of the most experienced executives in Indian alcohol.[^5] The combination of a founder-led operating culture and a board with genuine consumer-industry depth is not common in the listed Indian distilling space.

The incentive structure has shifted too. Where, in the bulk-alcohol era, the metrics that defined a good year were straightforward — installed capacity utilisation, ENA realisation per litre, EBITDA per litre — management commentary in recent reporting cycles has visibly leaned toward different language: return on capital employed, contribution from premium brands, ethanol blending volumes contracted, working capital days.[^2][^10] These are the metrics of a capital-allocator rather than the metrics of a still operator. The shift is more than cosmetic. It tells you what the boardroom is actually trying to optimise for.

The lurking risk in any family-controlled Indian business is succession pathology — the second generation either overspends to prove themselves, or underspends to preserve the founder's legacy. Globus, on the evidence so far, looks like it has avoided both traps. The capital plan has remained disciplined, but the cultural pivot — from "distiller" to "brand-builder" — has been allowed to run. That pivot found its most visible expression in two decisions: the move into भारतीय निर्मित विदेशी शराब Indian Made Foreign Liquor, and the acquisition of Unibev.

V. Inflection Point 2: The Premiumization Gamble & Unibev M&A

If the IMIL play was Globus learning to walk as a brand owner, the IMFL premiumisation move was Globus deciding to run. The strategic logic was, in hindsight, almost forced. The Indian whisky and brandy market had bifurcated by the late 2010s: the bottom end, where Globus already dominated, threw off cash but capped at modest growth; the top end, where global majors like Diageo's United Spirits and Pernod Ricard's Seagram's India operated, was growing in double digits as a generation of Indian drinkers traded up from cheap rum to mid-tier whisky and from mid-tier whisky to single malts.[^11] Sit out the premiumisation, and you watch the value pool migrate to a competitor. Participate, and you take on the most ruthless, best-marketed competitors in the global beverage industry on their home turf — except their home turf is, technically, your home turf.

The first move was organic. Globus launched, with measured experimentation, a set of premium IMFL labels — including Governor's Reserve in the whisky category and Hannibal in the rum/brandy adjacency.[^2] The early results were modest. Building a premium spirits brand in India from scratch is one of the most capital-intensive marketing exercises in consumer goods. The drinker who reaches for a brand at the back of a high-end bar is not making a value-conscious decision; they are buying a story, a heritage, sometimes literally a coat of arms on the label. Globus, for all its operational excellence, did not have the heritage assets. It needed either to acquire them or to invent them.

It did both. The acquired piece arrived in May 2022, when Globus announced that it would take a 100 percent stake in Unibev — a premium spirits business founded by Vijay Rekhi, the former Managing Director of United Spirits during the Vijay Mallya era and one of the most respected operators in Indian alcohol.[^5] The Unibev deal was, structurally, classic "buy a team, buy a thesis." Rekhi had spent his life building IMFL brands at scale. He had the relationships across the on-trade and off-trade channels that take a generation to acquire. Folding Unibev into Globus did three things simultaneously: it added a starting portfolio of premium labels, it imported senior brand-building talent with a track record, and — perhaps most importantly — it sent a signal to the trade that Globus was a serious counterparty in the premium conversation, not just an ENA supplier moonlighting as a brand owner.

Whether Globus overpaid is the question every analyst initially asked. The honest answer, looking at the disclosed terms in the public filings around the transaction and reading them against the implied revenue and operating profile of Unibev, is that it was a small-ticket deal by global spirits M&A standards — closer to a tuck-in than a bet-the-company acquisition.[^5] The acquisition cost, relative to the multi-decade strategic value of compressing the brand-building cycle by ten or fifteen years, is the kind of trade that looks expensive on a one-year IRR and cheap on a fifteen-year one. The bear case is that Indian premium spirits is a brutal category to scale against entrenched majors; the bull case is that you do not have to win the category, you only have to capture a defensible slice and trade on consumer multiples instead of commodity multiples.

The invented piece was, in many ways, the more interesting story, and it had a name: तराई Terai. Conceived as an Indian craft gin — distilled with botanicals like coriander seed, fennel, ginger, lemongrass, and Himalayan juniper — Terai was launched in late 2020 into a category that, at the time, barely existed in India.[^6] The conventional view was that Indian drinkers did not drink gin. The unconventional view, which a small wave of Indian craft distillers including Greater Than, Hapusa, Stranger & Sons, and Terai itself helped prove, was that Indian drinkers did not drink the gin that had been available to them — bottom-shelf imports and unloved domestic mixers — and that, given a product designed around the Indian palate and the Indian story, they would absolutely pay ₹2,000 a bottle for it.[^6]

Terai was significant for Globus not because it moved the financial needle in any single quarter; the gin contribution remains modest in absolute revenue terms. It was significant because of what it did to the internal culture. Building Terai required Globus to acquire, almost from scratch, the skills of a modern consumer brand: design, sensory development, hospitality-channel marketing, storytelling, mixology partnerships. Those skills are non-fungible. Once a manufacturing organisation has learned how to sell a craft gin, it has, in some real sense, transformed into a different kind of company. The Terai exercise was strategic education paid for with shareholder capital, and the lesson it taught — that an Indian distiller could go shoulder to shoulder with a London import — sits underneath every premium ambition the company now states publicly.

But beneath the premiumisation story, a quieter, larger transformation was happening in the manufacturing wing of the company, and it had nothing to do with consumer brands at all. It had to do with cattle feed and petrol pumps.

VI. The "Hidden" Business: The DDGS & Ethanol Engine

There is a piece of distillery economics that almost never gets explained on a consumer-investing podcast, and it is worth taking thirty seconds to be concrete about, because it is where the entire bull case for Indian grain-based distillers quietly lives. When you ferment broken rice or maize into alcohol, the alcohol is only one of the three products you get out of the column. The second is carbon dioxide, which can be captured and sold to bottlers of carbonated soft drinks. The third — and this is the one almost nobody talks about — is the residue of the grain itself: protein, fibre, oil, and minerals, with most of the starch removed because the starch is what became the alcohol. Dry that residue, granulate it, and you get डिस्टिलर्स ड्राइड ग्रेन्स विद सॉल्यूबल्स DDGS, a beige, pellet-like animal feed with a crude protein content typically in the high twenties percent.5

If you are a poultry farmer or an aquaculture operator in India, DDGS is one of the most attractive protein sources you can buy: cheaper than soybean meal, comparable in nutritional value for many species, and increasingly available domestically as grain-based distilleries have scaled.5 If you are a distillery operator, DDGS is essentially a free option on your residual stream. The grain you bought to make alcohol you have already paid for; the energy to dry the residue is marginal; the revenue from selling the DDGS effectively lowers the net cost of your alcohol production. Some industry estimates suggest the DDGS sale can offset a meaningful percentage of the raw material cost of the underlying ENA — the difference between a distillery being profitable and a distillery being a write-off in a bad grain year.

Globus, because it had built its grain-based plants in regions with developing animal-protein supply chains, sat in an enviable position. The company's segmental reporting in recent annual cycles has started disclosing DDGS as a meaningful contributor to manufacturing-segment revenue.[^2][^3] The strategic genius of the integration is that it converts a feedstock cost line into a co-product revenue line. The distillery, in effect, has two customers for every ton of grain it buys: the alcohol buyer and the chicken farmer.

The other half of the manufacturing-side transformation is the इथेनॉल सम्मिश्रण कार्यक्रम Ethanol Blending Programme, which is one of the most consequential industrial policies the Government of India has executed in the past decade. The headline mandate: blend ethanol into petrol — first 5 percent, then 10 percent, then 20 percent (E20) — to reduce crude oil imports, support farmer incomes, and lower urban tailpipe emissions.3 The programme has triggered an enormous, government-underwritten capex cycle across Indian distillation. Oil Marketing Companies (OMCs) — Indian Oil, BPCL, HPCL — are mandated buyers; they tender for ethanol supply on annual cycles, with offtake guarantees, government-set floor prices for different feedstock-derived ethanol, and interest subvention schemes that subsidise the financing cost of new distillation capacity.3

For an established grain-based distiller, the EBP is essentially a second, parallel demand curve grafted onto the existing manufacturing business. Globus has leveraged its grain-handling, multi-feedstock infrastructure to position significant capacity for ethanol supply.[^2][^3] The economics are worth understanding clearly: ethanol contracted for fuel blending sells at a regulated price that is typically less margin-rich than ENA sold into the consumer alcohol channel, but it is also vastly more contracted, more predictable, and more counter-cyclical. When the consumer alcohol cycle softens — say, because a state government raises excise sharply, or a Bihar-style prohibition shock takes a market off the map — the ethanol leg keeps running, the OMC pays on its annual tender cycle, the plant utilises its capacity, the operating leverage holds. The ethanol leg is, in effect, a base load.

This is the floor that the bear case on the company has historically underweighted. A diversified, multi-feedstock distillery with simultaneous exposure to value IMIL, premium IMFL, DDGS, and OMC-contracted ethanol is structurally less volatile than any of those four businesses standing alone. The trick management has had to pull off is to allocate capex across the four legs without overbuilding any one of them — and to time the ethanol-capacity expansion against the policy trajectory of the blending mandate. Plants take eighteen to thirty months to build. The capex committed in 2022, in expectation of E20 by 2025-26, is the capex that produces revenue today.[^2][^3]

The "hidden" businesses, in other words, are not hidden because management is concealing them; they are hidden because the equity narrative has, until recently, been dominated by the consumer brand story. The patient industrial economics of byproduct revenue and policy-anchored ethanol contracts deserve more weight. They are what make the consumer bet survivable.

VII. Playbook: Porter's 5 Forces & Hamilton's 7 Powers

Pull back from the company specifics for a moment and apply the strategy frameworks. The Indian alcohol industry is a textbook case for both Porter and Hamilton Helmer, partly because it has been protected in the technical sense — by regulation, geography, and capital intensity — and partly because, within that protection, the competitive dynamics are unusually intense. Let us walk the powers.

Scale Economies. Indian distillation is, at the unit-economics level, a scale game. A 100-kilolitre-per-day grain-based plant has materially worse unit economics than a 600-kilolitre-per-day plant of the same vintage. The fixed costs of compliance, environmental clearance, lab infrastructure, and senior plant management are roughly the same; the variable cost advantages compound on every additional litre. Globus's multi-location footprint — Behror, Samalkha, West Bengal, Bihar, and Jharkhand — gives it both production scale and geographic reach into the most regulated state markets.[^2][^11] A new entrant trying to replicate that footprint today would need a billion-dollar-plus capex budget and a decade of regulatory groundwork. That is the textbook definition of Scale Economies in the Helmer framework: the leader's cost position is structurally unmatched by any rational new entrant.

Cornered Resource. The licence is the cornered resource. India does not issue distillation licences freely. The states that historically allowed private distillation did so under licensing regimes that effectively grandfathered incumbents. New manufacturing licences for grain-based ENA capacity are not impossible, but they are slow, politically contingent, and frequently subject to environmental and pollution-board capacity caps. Globus's portfolio of licences is, in the Helmer sense, an asset that the company controls and that competitors cannot replicate by simply outspending it.[^9]6 This is part of why the consolidated Indian alcohol industry has so few large players relative to the size of the market.

Switching Costs. At the value (IMIL) end, switching costs are real but cultural rather than contractual. A drinker in rural Haryana who has bought County Club नींबू for ten years does not switch to a competing brand because of a small price difference. The taste association, the label recognition, the depot-level availability — all of these create stickiness. At the premium IMFL end, switching costs are weaker; drinkers experiment with new brands, especially in gin and the entry-level whisky bands, and the global majors have proven they can win loyalty through marketing spend. So the Switching Costs power is bifurcated: strong at the bottom, weak at the top.

Brand. This is where the story is still being written. The IMIL portfolio brands are regionally strong but not nationally aspirational. Governor's Reserve is a credible mid-tier IMFL brand but has not yet broken into the iconic tier where Royal Stag or Officer's Choice operate.[^2][^11] Terai, the craft gin, has achieved the most genuine "brand" power in the portfolio in the strict Helmer sense — a consumer is willing to pay a premium beyond the functional value of the liquid because of what the brand means.[^6] The strategic question is whether the company can extend Terai's playbook — design, story, premium positioning, hospitality-channel cultivation — to additional categories.

Counter-Positioning, Process Power, Network Economies. These three powers in the Helmer framework are largely absent from Globus's situation. Network effects do not really apply to a manufactured consumer good. Process power is partially present — multi-feedstock plant design is a genuine operational capability — but it is replicable. Counter-positioning would require a competitor unable to match Globus's business model for structural reasons, which is not really the case.

Porter's view: the State as the dominant force. Of the five Porter forces — supplier power, buyer power, threat of new entrants, threat of substitutes, and competitive rivalry — none of them is the truly dominant force in Indian alcohol. The dominant force is a sixth force that Porter himself, in his 2008 update, formally added: the role of the regulator. In India, the State, in each of its twenty-eight forms, sets the production licence, the wholesale margin, the retail price, the excise duty, the permissible advertising, the allowed channels of sale, and — in some states — whether the product is permitted to exist at all. The 2016 बिहार Bihar prohibition decision, which overnight removed an entire consumer market from every distiller serving the state, is the single most vivid example of this risk in the past decade.[^9]6 No competitive moat, however deep, survives an excise decision taken in a state cabinet meeting on a Tuesday. The defensive answer is diversification — by state, by category, by channel — and Globus has built exactly that diversification more by necessity than by choice.

VIII. Capital Deployment & The Benchmarking

If you wanted to evaluate Globus the way a private-equity investor would, you would ignore the income statement for the first half hour and stare at two things: the capex schedule and the working capital cycle. Both reveal more about management's true strategy than any quarterly call.

The capex story over the past several years has been weighted heavily toward two flagship expansions: the West Bengal plant build-out and the Jharkhand greenfield capacity, both designed with multi-feedstock flexibility and significant ethanol-blending exposure.[^2][^3] The capital intensity of distillation is uncompromising — a new grain-based distillery of meaningful scale runs into the hundreds of crores of rupees — and the gestation period from groundbreaking to fully utilised capacity is typically two to three years. Globus has, on the public record, executed these projects close to budget and timeline, which in the Indian industrial context is itself a competitive moat. Cost overruns and delayed commissioning are common in this industry. Bringing capacity online when promised, at the cost promised, is not.[^10][^11]

The working capital cycle is the second tell. The Indian alcohol business is structurally working-capital-intensive for reasons that surprise people unfamiliar with state-level distribution. Excise duty is paid up front, often when the liquid leaves the distillery for the state-controlled wholesaler, and the wholesaler typically pays the manufacturer on a deferred schedule. Inventory of high-value premium IMFL — whisky in particular, where ageing is part of the value proposition — can sit on the balance sheet for years before realising revenue. The "inventory versus ageing" trap is real: every additional year of ageing improves the per-bottle margin but consumes working capital that could have funded another plant.

Globus's choice in recent years has been to manage that trap with discipline. The company has prioritised cash-generative product categories — IMIL, ethanol, DDGS — to fund the working-capital absorption of the premium business. That is the right sequencing. Many Indian premium-spirits aspirants over the past two decades have tried to scale ageing portfolios without a cash-generative base business underneath, and most have ended up sold to a global major after running out of working-capital runway. Globus has the underlying engine to fund a multi-year premium build without a forced sale.

Dividend policy versus reinvestment is a useful tell about how management views the next decade. Globus has historically run a modest dividend payout — meaningful but not generous — and retained most of its earnings to fund capacity and brand investment.[^2]2 That is rational given where the company sits in its growth arc. The implicit signal to shareholders is: do not expect a yield story, expect a re-rating story.

The re-rating thesis is, at its core, a multiple thesis. The Indian listed alcohol space has historically traded at a wide dispersion of multiples. United Spirits, the Diageo-controlled premium pure-play, has traded at a meaningful premium to the rest of the industry, reflecting its brand portfolio, distribution reach, and free-cash-flow profile.[^11] Radico Khaitan, the historically family-controlled premium-and-mass mix, has earned a higher multiple than the pure-bulk distillers as its premium portfolio has scaled. Globus, with its commodity legacy and capital-intensive footprint, has traded historically closer to a manufacturing multiple than a consumer multiple. The bet is that as the premium brand contribution to EBITDA crosses a critical threshold — historically a transition point at which consumer-staples investors begin to take a serious look at a stock — the multiple compresses upward toward the premium pure-plays.

What the market is implicitly asking, and what management has been steadily answering quarter by quarter, is: what fraction of the EBITDA is structurally consumer, and what fraction is structurally industrial? The trajectory matters more than the level. If the consumer share is rising on a multi-year trend line, the re-rating mechanic eventually engages.

IX. Analysis & Bear vs. Bull Case

Now to the war-gaming. Stand at the bull's lectern first.

The bull case writes itself in three sentences. India is, by alcohol volume per drinker, a structurally under-consumed market with a rising young middle class that will premiumise; the इथेनॉल सम्मिश्रण कार्यक्रम Ethanol Blending Programme is a multi-decade tailwind anchored by government policy and energy security; and Globus is one of a very small number of operators positioned across all three legs of the trade — value, premium, and ethanol.3[^11] The bull's mental model is something like a "mini-United Spirits with better manufacturing efficiency": consumer optionality, with a captive industrial base under it that the pure-play premium operators do not have. Add the DDGS option, layer on the regional moats in IMIL, accept that Terai may not be the only premium brand the company breaks out over the next decade, and the long-duration earnings power looks visibly larger than the multiple suggests.

The bull's specific catalysts to track are clear. First, the premium share of revenue and especially EBITDA — the moment that crosses a structurally noticeable threshold, the equity story changes from "diversified distiller" to "branded alcohol house." Second, ethanol contracted volumes and the trajectory of the E20 mandate; every uptick in the national blending percentage flows into capacity utilisation at grain-based distillers. Third, the trajectory of the consumer business margin in IMIL, which functions as the cash engine for everything else.[^10][^11]

The bear case is equally coherent, and any honest investor in this company should know it cold.

The first leg of the bear case is regulatory volatility. The Bihar prohibition shock of 2016 is the canonical example, and it is not the last one of its kind that the industry will ever see. State-level excise changes, in any direction, can move a year's earnings within a single quarter.[^9]6 A national prohibition is extremely unlikely; a sharp excise hike in a major market is not. The diversification across states is the defence, but no diversification is perfect.

The second leg is raw material cost cyclicality. Broken rice, maize, and molasses prices are driven by the monsoon, by the Minimum Support Price decisions of the केंद्रीय बजट Union Budget cycle, and by the export policy on grain. A single bad monsoon year or a sudden grain-export ban can compress manufacturing margins severely.[^11] Globus's multi-feedstock plant design helps, but it does not insulate the business from a generalised agri-commodity shock.

The third leg is competitive intensity at the premium end. Diageo's United Spirits is not going to cede shelf space in the Indian on-trade without a fight, and Pernod Ricard, the privately controlled Bacardi, and the resurgent Allied Blenders & Distillers are all marketing-heavy operators with deep pockets and long brand histories. Scaling Governor's Reserve, Terai, and the post-Unibev portfolio into nationally meaningful brands against that competitive field is the hardest, longest, and most expensive task on management's plate.[^11]

The fourth leg, often underweighted, is governance and capital allocation risk inherent to family-controlled Indian companies. Globus has executed well on this dimension for many years, but the structural risk that promoter interests and minority interests can diverge — for example, in related-party transactions, acquisitions of unlisted family assets, or executive compensation — never goes to zero in this kind of ownership structure. The defence is the visible track record. The risk is that track records are looking-backward signals, not forward guarantees.

The KPIs to watch, narrowed down, are short. The single most important is the share of revenue and especially EBITDA contributed by the premium consumer segment — IMFL plus craft brands. This is the lever that, mechanically, re-rates the multiple. A close second is ethanol contracted offtake and blending-related utilisation — the structural floor of the business, the part that turns a cyclical distiller into a base-load infrastructure-like supplier. And a third, often ignored, is net working capital days — because if working capital balloons faster than revenue scales, the cash-generation story stalls regardless of how good the brand traction looks on a deck.[^2][^10]

Almost everything else — quarterly volumes, regional excise blips, individual brand launches — is noise around those three signals.

Myth vs. reality. A persistent market narrative is that Globus is "primarily an ethanol play" — a beneficiary of policy, no more. The reality, looking at the segmental disclosure, is that the consumer business has quietly become a much larger share of the value-add than the surface narrative implies, and that ethanol is the base, not the story.[^2][^3] A second narrative is that Terai is "just a marketing exercise." The reality is that Terai has been a strategic education for the entire organisation, and the operational and creative capabilities it has embedded inside the company will be deployed across multiple future brand launches. A third narrative is that the Unibev acquisition was a vanity buy. The reality is that, given the multi-decade compression of brand-building time it enabled, the acquisition is best evaluated on a strategic-option basis, not a one-year IRR.[^5]

X. Epilogue & Final Reflections

Stand back from the granular financials, the segmental EBITDA, the licence portfolios and the ethanol tenders, and look at the long arc.

A century ago, the Swarup family was solving a sugar industry problem — what to do with molasses. Three decades ago, that accumulated expertise was channelled into a bulk-ENA distillery in Behror that, by design, never carried a brand. A decade and a half ago, the company quietly built a regional country-liquor empire that almost nobody outside the industry had heard of, in markets that the urban analyst community had never visited. Five years ago, it launched a craft gin that sat shoulder to shoulder, on the back-bar of a five-star hotel, with imports from London distilleries founded in the 1830s. Three years ago, it acquired the strategic asset and the senior brand-building talent of a former United Spirits managing director. And throughout all of it, in the basement of the business model, the company kept getting paid by Indian Oil for every kilolitre of ethanol it blended into the country's petrol supply.1[^5][^6]3

The Swarups have done something quietly unusual in Indian industry. They have not tried to be the largest. They have not tried to be the loudest. They have not tried to be the most fashionable. They have tried to be, in every part of the value chain they touch, the most efficient possible operator — and they have used the cash thrown off by that efficiency to slowly, patiently, expensively buy themselves an option on becoming a consumer brand house.

Whether that option pays off in the multiple the bulls expect is, of course, not yet known. India's premium spirits market has, in different decades, been the graveyard of more than one ambitious domestic challenger. The regulatory environment is, structurally, the most volatile force any participant in this industry faces. The competitive set at the top end is the toughest competitive set in global consumer goods.

But if you accept that the Swarups will keep doing in the next decade what they have done in the past three — under-promising, over-executing, allocating capital with patience, and using a commodity engine to finance a brand journey — then the most interesting question about Globus Spirits is not whether the strategy will work. It is whether the equity market, which has historically valued the company on the commodity engine, will eventually wake up to the brand journey that has been building inside it all along.

The distillation, in the end, is the metaphor. Globus has spent thirty years separating signal from noise — alcohol from water, value from commodity, brand from byproduct. The next decade is whether, in the perception of the people who buy the stock, the same separation finally happens.

References

References

-

Globus Spirits Corporate Profile — National Stock Exchange of India ↩↩

-

Ethanol Blending Program in India: A Regulatory Overview — Ministry of Petroleum & Natural Gas ↩↩↩↩↩

-

History of the Swarup Family in the Sugar Industry — Globus Spirits Corporate History ↩

-

Understanding DDGS: The high-protein byproduct of distilleries — Feed Strategy, 2022 ↩↩

-

India's Alcohol Regulation and State-wise Taxation — ICRA Research Report ↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube