Glenmark Pharmaceuticals: The Innovation Gambit of India's Risk-Taking Pharma

I. Introduction & Episode Roadmap

Picture this: February 2024, Glenn Saldanha walks into a boardroom knowing he's about to sign away one of his company's most prized assets. On the table—a $700 million upfront check from AbbVie, one of the world's pharmaceutical giants. The asset? ISB 2001, a multi-specific antibody that Glenmark had been nurturing for years. For most CEOs, this would be a moment of triumph. For Glenn, it was both vindication and necessity—a lifeline that would finally make his innovation subsidiary self-sufficient while his parent company battled a cascade of FDA warning letters.

How did a generic drug company founded in 1977—named rather endearingly after the founder's two sons—end up here? This is the story of Glenmark Pharmaceuticals, a company that embodies the audacious contradictions of Indian pharma. It's a tale of a family business that dared to dream beyond copying molecules, of regulatory nightmares that could have killed lesser companies, and of a second-generation entrepreneur who bet everything on innovation when prudence suggested otherwise.

The paradox is striking: Here's a company with FDA warning letters at multiple manufacturing sites—citations so severe that one facility was blocked from US imports entirely. Yet simultaneously, this same organization convinced AbbVie to write the largest upfront check in Indian pharma out-licensing history. It's as if Glenmark operates in two parallel universes—one where it struggles with basic manufacturing compliance that generic makers mastered decades ago, and another where it develops cutting-edge biologics that attract Silicon Valley-sized valuations.

Today's journey takes us from a modest API manufacturer in Maharashtra to a global pharmaceutical player with operations across five continents. We'll explore how Gracias Saldanha built the foundation, how his son Glenn transformed it into an innovation powerhouse, and why this Rs. 4,000 crore company might represent either the future of Indian pharma or a cautionary tale about flying too close to the sun. The roadmap ahead traces family dynamics, regulatory battles, scientific breakthroughs, and billion-dollar bets—all wrapped in the larger narrative of India's pharmaceutical ambitions on the world stage.

II. The Founding Story & Gracias Saldanha Era (1977–2001)

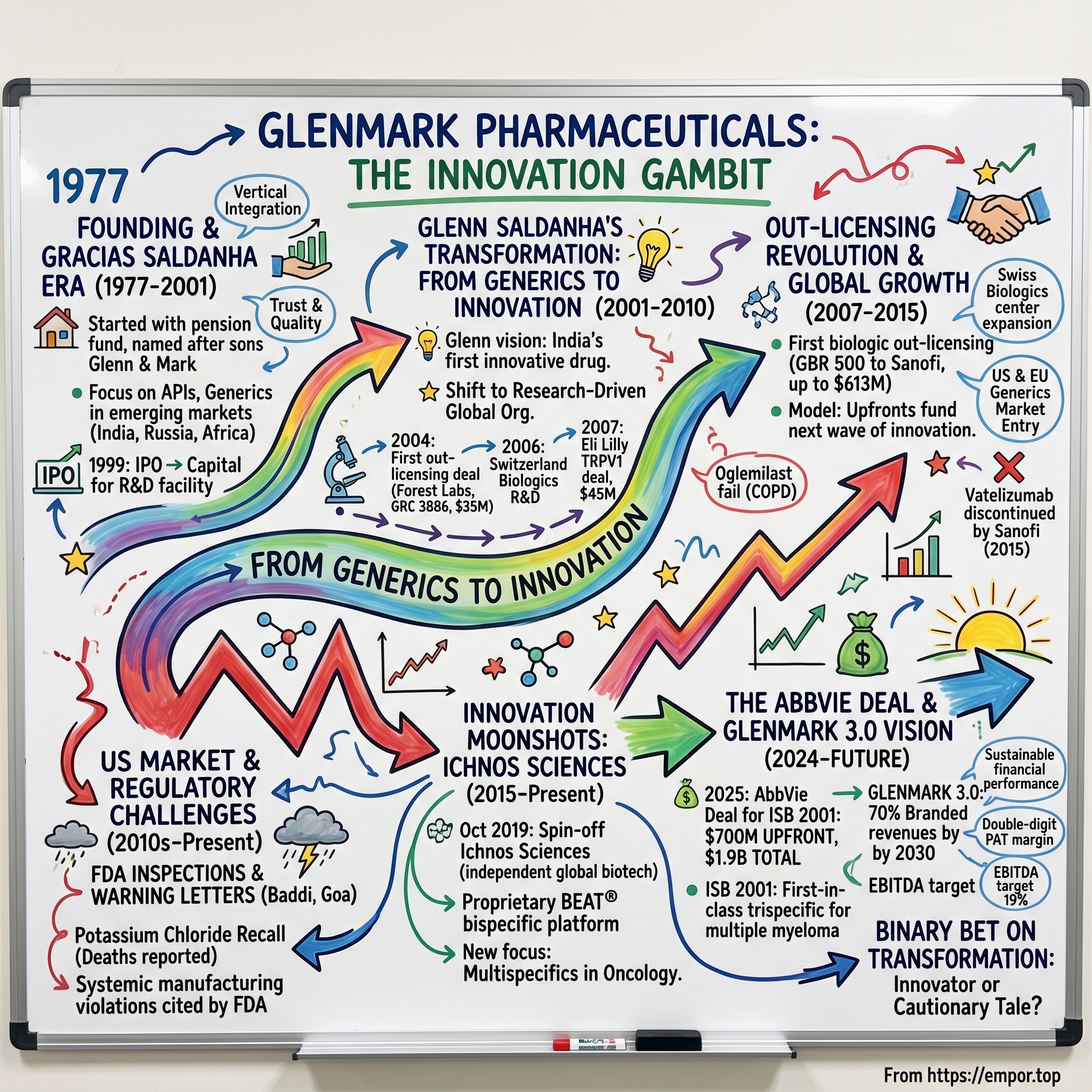

The sun had barely risen over Mumbai's textile mills in 1977 when Gracias Saldanha made a decision that would transform his family's fortunes. Armed with his pension fund—the accumulated savings from over a decade working at various pharmaceutical companies—he founded a small generic drug manufacturing operation. The company was started with his pension fund in 1977, a remarkably modest beginning for what would become a global pharmaceutical enterprise. The name he chose carried deep personal significance: Glenmark, combining the names of his two sons—Glenn and Mark.

Saldanha wasn't just another entrepreneur chasing quick profits in India's nascent pharmaceutical sector. After earning a Master's degree in Science from Bombay University and a Diploma in Management Studies from Jamnalal Bajaj Institute, he had acquired practical knowledge by working in multiple pharmaceutical companies for over 12 years. This combination of theoretical knowledge and hands-on experience shaped his vision for Glenmark—not as a fly-by-night generic operation, but as a foundation for something larger.

The strategic choices Saldanha made in those early years reveal a man who understood both opportunity and constraint. The company initially sold its products in India, Russia, and Africa—markets that Western pharmaceutical giants largely ignored, where generic medicines could make the difference between treatment and suffering. This wasn't accidental. These emerging markets offered less regulatory complexity, lower barriers to entry, and enormous unmet medical needs.

The late 1970s and early 1980s saw Glenmark establishing its manufacturing backbone. The company built API (Active Pharmaceutical Ingredient) facilities at strategic locations: Kurkumbh in Maharashtra and Ankleshwar in Gujarat. These weren't just factories; they were the foundations of vertical integration that would later distinguish Glenmark from competitors who relied entirely on imported raw materials. The Kurkumbh facility, in particular, would become crucial—acquired in 2001 when Glenmark started its API business unit, though operations had begun earlier.

By 1979, merely two years after founding, Glenmark made its first significant therapeutic move. The company launched 'Candid Cream' in dermatology, a seemingly simple antifungal product that would establish Glenmark's presence in a therapeutic area it would dominate decades later. This wasn't high science—Candid Cream was a basic clotrimazole formulation—but it demonstrated Saldanha's pragmatic approach: start with what works, build trust, then innovate.

The 1980s and 1990s saw steady, unglamorous growth. Blanche Saldanha, likely Gracias's wife, joined the company and managed Glenmark's international operations from 1982 to 2005, responsible for developing and growing the company's export business during her 23-year tenure. This family involvement would become a hallmark of Glenmark's culture—personal stakes creating accountability that public companies often lack.

The decision to go public in 1999 marked a inflection point. The company went public in India in 1999 at a market capitalization of just $40 million. To put this in perspective, that's roughly the value of a single successful drug molecule today. Yet this IPO provided crucial capital for expansion and, importantly, the company used some of the proceeds to build its first research facility.

What's remarkable about this era is what Saldanha didn't do. He didn't chase the lucrative US market immediately. He didn't attempt to compete head-to-head with Indian giants like Cipla or Dr. Reddy's in their strongholds. Instead, he built capabilities methodically—APIs first, then formulations, then slowly expanding geographic reach. This patience would prove invaluable when his son Glenn took the reins.

By the end of Gracias Saldanha's active leadership, Glenmark had transformed from a pension-fund startup to a respectable mid-sized pharmaceutical company. By the time he died in 2012, he had a fortune of $805 million and was the wealthiest Goan in the world. The boy from Saligao village in Goa had built something substantial, but the real transformation—and the real risks—were about to begin. The foundation was solid, the manufacturing infrastructure was in place, and most importantly, his son Glenn had returned from America with ideas that would either catapult Glenmark to greatness or destroy everything his father had built.

III. Glenn Saldanha's Transformation: From Generics to Innovation (2001–2010)

When Glenn Saldanha walked into Glenmark's Mumbai headquarters in 2001 to assume the CEO role, he carried more than just an MBA from NYU's Leonard Stern School of Business. He held a bachelor's degree in pharmacy from Mumbai University and had worked with Eli Lilly, USA and PricewaterhouseCoopers, USA—experiences that gave him a unique vantage point on both the pharmaceutical industry's scientific underpinnings and its financial architecture. His father had built a solid generic drug company. Glenn saw something different: a launchpad for India's first truly innovative pharmaceutical enterprise.

The boardroom tension was palpable when Glenn first proposed his vision. Glenn envisions discovering, developing and introducing India's first innovative drug for the world. Under his leadership, Glenmark evolved from an Indian-branded generics business into a research-driven and innovation-led global organization. This wasn't just corporate evolution—it was revolution. In an industry where Indian companies had built fortunes copying Western molecules, Glenn wanted to create them.

The numbers tell a story of transformation: He joined Glenmark in 1998 and subsequently became the Managing Director & CEO in 2000. He transformed Glenmark into a truly multinational company with revenues of over USD 1.5 Bn. But revenue growth was merely the visible outcome of a deeper metamorphosis. Glenn was rebuilding Glenmark's DNA, shifting from a manufacturing-focused operation to an R&D-driven enterprise.

The first major validation came in 2004—a moment that would define Glenmark's trajectory. Glenmark created history where it sealed its first out-licensing deal with Forest Laboratories for GRC 3886. Glenmark received USD 35Mn as upfront and milestone payments. For context, this was extraordinary. An Indian company had developed a novel molecule—an oral PDE4 inhibitor for respiratory diseases—and convinced a US pharmaceutical company to pay substantial upfront money for it. This wasn't contract manufacturing or generic production; this was original science.

The momentum built quickly. In 2005, Glenmark entered into a deal with Teijin Pharma for the Japan rights of its molecule Oglemilast for which it received an upfront payment of USD 6 Mn. Then came 2006, a pivotal year when Glenn made two bold moves. First, To focus on development of novel biologics, Glenmark established its first R&D center for NBE research in Switzerland. Second, Glenmark entered into an out-licensing deal with Merck KGaA for its molecule Melogliptin and received a total payment of USD 31 million.

The strategy was crystallizing: develop novel molecules, out-license them to Big Pharma for global markets while retaining rights for emerging markets, and use the upfront payments to fund further research. It was venture capital thinking applied to pharmaceutical R&D—portfolio theory where a few winners could pay for many experiments.

By 2007, the model was attracting serious attention. Eli Lilly acquired the rights to a portfolio of TRPV1 antagonist molecules developed by Glenmark. Glenmark received an upfront fee of USD 45 Mn. The deals weren't just bringing in money; they were validating Glenmark's science on the global stage. Each partnership was a vote of confidence from companies that had been developing drugs when Glenmark was still a startup.

In 2008 Glenmark was the fifth-biggest pharmaceutical company in India. But size wasn't the metric Glenn cared about. He was building something unprecedented—an Indian pharmaceutical company that could stand toe-to-toe with global innovators. The R&D spending reflected this ambition, consuming resources that could have delivered immediate profits through generic expansion.

Not everything worked. The Oglemilast story turned cautionary. Forest Laboratories and Glenmark announced top-line results from a Phase IIb dose range-finding study of oglemilast in patients with Chronic Obstructive Pulmonary Disease (COPD). Once-daily treatment with oglemilast did not show a statistically meaningful increase from baseline compared to placebo in the primary endpoint. The molecule that had brought Glenmark its first major validation had failed in late-stage trials.

Yet Glenn persisted. The failures were learning experiences, the cost of playing in the high-stakes game of drug discovery. By 2010, the innovation engine he had built was hitting its stride. The company had multiple molecules in development, partnerships with major pharmaceutical companies, and a growing reputation as India's most ambitious pharmaceutical innovator.

What Glenn Saldanha achieved in this first decade wasn't just business transformation—it was a reimagining of what an Indian pharmaceutical company could be. He had taken his father's solid foundation and built something audacious on top of it: a company that didn't just make drugs, but invented them. The stage was set for even bigger bets, larger partnerships, and ultimately, the regulatory challenges that would test whether innovation and compliance could coexist in the same organization.

IV. The Out-Licensing Revolution & Building the Innovation Engine (2007–2015)

The conference room at Glenmark's Swiss biologics facility hummed with nervous energy in May 2011. Glenn Saldanha was about to announce something unprecedented: This is the first biologic out licensing deal by any Indian company. The molecule in question was GBR 500, and the partner was Sanofi—the same French pharmaceutical giant that had already validated Glenmark's small molecule research a year earlier.

The numbers were staggering for an Indian pharmaceutical company: Glenmark will receive an upfront payment of US$ 50 million, of which US$ 25 million will be paid upon closing of the transaction and US$ 25 million, which is contingent upon Sanofi's positive assessment of certain data to be provided by Glenmark. In addition, Glenmark could receive potential success-based development, regulatory and commercial milestone payments. The total of these payments could reach US$613 Mn.

This wasn't just another licensing deal—it was a statement. GBR 500 is an antagonist of the VLA-2 (alpha2-beta1) integrin. It is a first-in-class therapeutic monoclonal antibody and has established proof of concept in animal models across a range of anti-inflammatory conditions. An Indian company had developed a novel biologic, a feat that required capabilities far beyond generic manufacturing or even small molecule innovation.

The out-licensing model that Glenn had pioneered was now a well-oiled machine. By 2011, the strategy had generated substantial capital: the outlicensing model earned Glenmark $230 million through partnerships. Each deal followed a similar template—retain rights for emerging markets where Glenmark had distribution strength, license to Big Pharma for developed markets, and use the upfront payments to fund the next wave of innovation.

The year 2011 proved pivotal in multiple ways. Beyond the GBR 500 triumph, Glenmark entered into an out-licensing deal with Sanofi-Aventis for its molecule GRC 15300, a first-in-class TRPV3 antagonist. Glenmark received an upfront payment of USD 25 million. This was actually a continuation of a relationship that had begun in 2010, when the French drugmaker is making an upfront fee of $20 million and with milestone payments, Glenmark could pocket $325 million, plus royalties.

The geographic rights structure revealed sophisticated thinking about global pharmaceutical markets. Sanofi will have exclusive marketing rights in North America, the European Union and Japan, subject to Glenmark's right to co-promote in the USA and five Eastern European countries. Sanofi also has have co-marketing rights in 10 additional countries including Brazil, Russia and China, while the Mumbai-headquartered firm retains exclusivity in India and other countries.

What made these deals remarkable wasn't just the money—it was what they represented. this is "our first partnership agreement in India in the pharmaceutical research area", noted Marc Cluzel, head of R&D at Sanofi. For a company that had started making generic copies just decades earlier, Glenmark was now a source of innovation for one of the world's largest pharmaceutical companies.

The infrastructure supporting this innovation wasn't accidental. To focus on development of novel biologics, Glenmark established its first R&D center for NBE research in Switzerland. By 2014, the company was expanding its manufacturing capabilities globally, opening new facilities in North Carolina, US, and La Chaux-de-Fonds, Switzerland—moves that would prove crucial for supporting its growing pipeline.

Not everything succeeded. The vatelizumab story—GBR 500's development name—turned cautionary. following the results of a pre-planned interim analysis that revealed that the primary effectiveness outcome was not met, Sanofi decided to discontinue the development of vatelizumab in 2015. The potential $663 million deal evaporated, though As this decision was not due to safety concerns, Glenmark intends to continue the development of vatelizumab once it is returned from Sanofi.

Yet the failures didn't slow the momentum. The company had built something unique: an innovation engine that could produce both small molecules and biologics, partner with global pharmaceutical giants, and still maintain a profitable generics business. By 2014, The auto-immune disease market worldwide is expected to be $25 billion by 2014, and Glenmark had positioned itself as one of the few companies from the developing world capable of creating novel treatments for these conditions.

The financial impact was transformative. The upfront payments weren't just revenue—they were validation that Indian science could compete globally. The upfront from the Sanofi deal will be used to pay down debt, Glenmark said today, which stood at Rs19bn ($421m) at the end of March. This financial discipline would prove crucial as the company entered its next phase—aggressive US market expansion that would bring both opportunity and unprecedented regulatory scrutiny.

V. The US Market Entry & Regulatory Challenges (2010s–Present)

The April 2019 FDA inspection at Glenmark's Baddi facility in Himachal Pradesh should have been routine. Instead, it became the opening chapter of a regulatory nightmare that would span years and multiple continents. The U.S. Food and Drug Administration (FDA) inspected the drug manufacturing facility from April 15 to 20, 2019, and the warning letter summarized significant violations of current good manufacturing practice (CGMP) regulations for finished pharmaceuticals.

The juxtaposition was stark: While Glenn Saldanha was celebrating billion-dollar innovation deals and expanding into the US generics market—by 2011 Glenmark had worldwide sales of $778 million, a 37% increase over the last year's sales; the growth was driven by Glenmark's entry into the US and European generics markets—the quality control systems at his manufacturing facilities were unraveling.

What made the situation particularly damaging was its systemic nature. FDA cited similar CGMP violations at other facilities in the company's network. Glenmark Pharmaceuticals Limited (Himachal Pradesh, India) was issued a warning letter dated October 3, 2019, for failing to adequately investigate multiple OOS test results for critical product attributes. This site was placed on import alert 66-40 on October 25, 2022. Glenmark Pharmaceuticals Limited (Goa, India) was issued a warning letter dated November 22, 2022.

The Goa facility inspection revealed particularly troubling findings. In the Warning Letter, the FDA writes that the company "rejected 14 batches of 0.1mg and 0.2mg strength desmopressin acetate tablets for out-of-specification (OOS) results [...] and content uniformity results" during 2018 to 2021. Glenmark "attributed the content uniformity failure to the lack of defined compression parameters", but "failed to test other batches or drug products that used the same [...] process and compression equipment."

But the most catastrophic crisis emerged from the Madhya Pradesh facility—a plant that would become synonymous with one of the most serious drug safety failures in recent Indian pharmaceutical history. The potassium chloride debacle began quietly but escalated dramatically. The drug potassium chloride has been on the market for decades, widely prescribed to help the nerves and muscles function properly in patients with low potassium. Glenmark knew there was a problem with its potassium chloride at least a month before a patient died. On May 29, a Glenmark executive wrote a letter to distributors saying a batch of potassium chloride had failed to dissolve correctly in a test. The executive told the distributors that the recall was "being made with the knowledge of the Food and Drug Administration" and used red capital letters to mark the notice "URGENT."

The scale of the recall was staggering: Glenmark Pharmaceuticals Inc., USA, Mahwah, NJ is voluntarily recalling 114 batches of Potassium Chloride Extended-Release Capsules, USP (750 mg) 10 mEq K, to the consumer level. The product is being recalled because of failed dissolution. The failed dissolution of potassium chloride extended release capsules may cause high potassium levels, also known as hyperkalemia, which can result in irregular heart beat that can lead to cardiac arrest.

The human cost became devastatingly clear. Since the May recall, Glenmark told regulators it has received reports of three deaths, three hospitalizations and four other serious problems in patients who took the recalled potassium chloride capsules. Since Glenmark's potassium chloride recall in May, the company has told federal regulators it received reports of eight deaths in the U.S. of people who took the recalled capsules.

One case crystallized the tragedy: A lawsuit alleges Glenmark's potassium chloride pills were responsible for the death last year of Mary Louise Cormier, a 91-year-old Maine woman. A letter alerting Cormier that her pills had been recalled arrived three weeks after she died. In court filings, Glenmark has denied responsibility for her death.

The FDA's delayed response raised serious questions about regulatory oversight. ProPublica reported that a Glenmark Pharmaceuticals factory in central India was responsible for an outsized share of recalls for pills that didn't dissolve properly and could harm American patients. Among the string of recalls, federal regulators had determined that more than 50 million potassium chloride extended-release capsules sold in the U.S. could be deadly. Yet, federal drug inspectors at that point hadn't set foot in the Madhya Pradesh factory for more than four years.

When inspectors finally arrived in 2025, their findings were damning. The United States Food and Drug Administration (FDA) inspected the drug manufacturing facility, Glenmark Pharmaceuticals Limited, located at Phase – II, Sector III, Plot No 2, Pharma Zone, SEZ, Pithampur, Madhya Pradesh, from February 3 to 14, 2025. This warning letter summarizes significant violations of Current Good Manufacturing Practice (CGMP) regulations for finished pharmaceuticals.

The July 2025 FDA letter delivered the most scathing assessment yet: "These repeated failures at multiple sites demonstrate that management oversight and control over the manufacture of drugs is inadequate." This wasn't just about isolated incidents—it was about a company that had systematically failed to maintain the basic standards required to safely manufacture medicines for human consumption.

The pattern was undeniable: The concerning string of recalls stemming from products made at the Madhya Pradesh factory in central India began in October 2023. Over the next 12 months, that single plant accounted for more than 30% of all FDA recalls for pills that didn't dissolve correctly and could harm patients.

The regulatory challenges decimated Glenmark's US ambitions. The Baddi facility is expected to contribute 30 million dollars in total sales for this financial year which is about 7 per cent of the total US sales. But with warning letters, import alerts, and massive recalls, the US market that was supposed to drive Glenmark's growth had become its greatest liability.

VI. The Innovation Moonshots: Biologics, Biosimilars & Specialty (2015–Present)

October 2019 marked a defining moment in Glenmark's innovation journey. While the world was focused on their regulatory troubles, Glenn Saldanha made a strategic decision that would redefine the company's future: In October 2019, Glenmark took the significant step of spinning its innovative biologics research division into a wholly-owned subsidiary, Ichnos Sciences Inc., an independent company headquartered in the USA, with a heightened focus on accelerating novel biologics entities (NBE) research.

The name Ichnos—meaning 'footprint' in Greek—was chosen deliberately. Ichnos (īk-nōz) Sciences officially opened its doors to the world today as an independent, fully integrated, global biotech company. A spin-off of Glenmark Holding SA created to focus on innovation, the new entity launched with impressive assets: Ichnos Sciences, headquartered in Paramus, N.J., launches with a firm global footprint that includes two research centers (Biologics in Switzerland and small molecules in Mahape, Navi Mumbai, India), a development site (Paramus, N.J.) and a GMP biologics manufacturing facility (Switzerland). Approximately 350 employees work at the Company and are dedicated to accelerating candidates in the pipeline toward commercialization.

What made Ichnos particularly compelling was its leadership. Former Gilead Sciences (Nasdaq: GILD) executive, Dr Alessandro Riva, is chief executive of Ichnos Sciences. He joined Glenmark six months ago. Riva wasn't just any pharmaceutical executive—he had been After an illustrious career in oncology R&D, contributing greatly to the development of cutting-edge cancer therapies at Novartis and Gilead, Alessandro Riva, MD joined biotech Ichnos Sciences as its founding CEO in 2019.

The pipeline Ichnos inherited was substantial: Ichnos Sciences' current pipeline includes three new biological entities (NBE) and two new chemical entities (NCE) in various stages of development across oncology, autoimmune disease and pain. The crown jewel was their bispecific antibody platform: The immuno-oncology biologics pipeline is developed through the Company's proprietary BEAT® (Bispecific Engagement by Antibodies based on the T cell receptor) platform.

The scientific ambition was clear. The cancer pipeline includes three bispecific antibodies, which could undercut CAR-T therapies by delivering comparable efficacy without the toxicity, logistical complications and associated costs. The lead programs were advancing rapidly: The company's bispecifics pipeline is led by two treatments in phase 1. It is testing a HER2xCD3 bispecific in HER2-positive cancers and a CD38xCD3 bispecific in multiple myeloma, as well as solid cancers. It expects those trials to read out in 2021.

But Glenmark's innovation wasn't limited to biologics. The respiratory franchise, in particular, was showing tremendous promise. The star asset was Ryaltris, and in January 2022, the company achieved a major milestone: Glenmark Pharmaceuticals Limited, a research-led, global integrated pharmaceutical company announced that its fully owned subsidiary Glenmark Specialty S.A. (Switzerland), received FDA approval on its New Drug Application (NDA) for Ryaltris™, an innovative, fixed-dose (metered), prescription, combination drug product nasal spray for the treatment of symptoms of Seasonal Allergic Rhinitis in adults and pediatric patients 12 years of age and older in the United States.

This wasn't just another generic approval—it was validation of Glenmark's ability to develop innovative combination therapies. Ryaltris™ is a metered, fixed-dose, aqueous suspension, prescription drug product nasal spray approved by the FDA for the treatment of symptoms associated with Seasonal Allergic Rhinitis. Each unit of Ryaltris™ nasal spray contains 665 mcg of olopatadine hydrochloride, a histamine-1(H1)-receptor inhibitor, and 25 mcg of mometasone furoate, a corticosteroid.

The global reach of Ryaltris demonstrated Glenmark's commercial sophistication: Ryaltris™ has been approved and is marketed in Australia, the Czech Republic, Poland, Russia, South Africa, Ukraine, the United Kingdom, and Uzbekistan. In April 2021, Glenmark concluded the DCP regulatory procedure in Europe, enabling approval in 17 countries across EU and UK. Glenmark has entered into commercial agreements with several partners around the world, including Menarini for the commercialization of Ryaltris™ in select EU markets, and with Bausch Health in Canada (where it is under review by Health Canada).

The transformation of Ichnos continued to evolve. To further explore groundbreaking solutions in the treatment of cancer, Glenmark and Ichnos took a collaborative leap in January 2024 and formed 'Ichnos Glenmark Innovation' (IGI). This alliance combines Glenmark's research and development proficiencies in small molecule research with those of Ichnos in NBEs

The new entity was focused and ambitious: IGI, Inc. is a global, fully integrated clinical-stage biotechnology company focused on developing innovative biologics in oncology. Headquartered in New York, NY, IGI is advancing a robust pipeline of novel, first-in-class Multispecifics™ aimed at addressing complex diseases and treating patients holistically. Powered by its proprietary BEAT® technology platform, IGI is committed to delivering breakthrough, curative therapies to improve and extend the lives of patients battling hematological malignancies and solid tumors.

The organizational challenge was significant. As Riva explained: This process has involved transforming the organisation itself, our people, and – most importantly – our mindset. As essentially a spinoff from Glenmark, the organisation had the pace of a generic company and was largely opportunistic, reacting to what was happening in the innovation world. Changing this to a long-term, innovation-focused biotech mindset has been challenging and has taken time but has been achieved.

By 2024, this transformation bore fruit with ISB 2001—the molecule that would ultimately attract AbbVie's $700 million investment. The innovation moonshots weren't just scientific experiments; they were strategic bets on Glenmark's ability to transcend its generic heritage and compete with the world's most sophisticated pharmaceutical companies.

The juxtaposition was striking: While FDA warning letters piled up at manufacturing facilities, Glenmark's innovation units were producing world-class science. Glenmark's key therapeutic areas of focus are respiratory, dermatology and oncology. It ranks among the world's top 50 Generics and Biosimilar companies (Top 50 Company Rankings, 2020, from Informa's Generics Bulletin). The company had built centers of excellence that operated almost independently from the troubled manufacturing operations—a deliberate separation that would prove crucial for the company's survival and future growth.

VII. The AbbVie Deal & Glenmark 3.0 Vision (2024–Future)

VII. The AbbVie Deal & Glenmark 3.0 Vision (2024–Future)

The July 10, 2025 announcement sent shockwaves through the Indian pharmaceutical industry. IGI will receive an upfront payment of $700 million and is eligible to receive up to $1.225 billion in development, regulatory, and commercial milestone payments, along with tiered, double-digit royalties on net sales. For context, this wasn't just the largest out-licensing deal in Glenmark's history—it was validation at the highest level that Indian pharmaceutical innovation had arrived on the global stage.

ISB 2001 is a first-in-class trispecific T-cell engager that targets BCMA and CD38 on myeloma cells and CD3 on T cells currently in Phase 1 for relapsed/refractory multiple myeloma. The science behind ISB 2001 represented a quantum leap from traditional cancer therapies. Developed using IGI's proprietary BEAT® protein platform, ISB 2001 was engineered with two distinct binders against myeloma-associated antigens to enhance avidity, even at low target expression levels, while aiming to improve safety over first-generation bispecific antibodies.

The clinical data that caught AbbVie's attention was compelling. Recently presented at the 2025 American Society of Clinical Oncology (ASCO) Annual Meeting as a Rapid Oral Presentation (Abstract #7514), data from 35 patients demonstrated a sustained overall response rate (ORR) of 79% and a high complete/stringent complete response (CR/sCR) rate of 30% at active doses ≥ 50 µg/kg in a heavily pretreated population of relapsed/refractory myeloma patients, with a favorable safety profile. These weren't just numbers—they represented hope for patients who had exhausted other treatment options.

The regulatory validation was equally impressive. U.S. Food & Drug Administration granted ISB 2001 Orphan Drug Designation in July 2023 and Fast Track Designation for the treatment of relapsed/refractory myeloma patients in May 2025. These designations weren't merely bureaucratic milestones; they represented the FDA's acknowledgment that ISB 2001 addressed a critical unmet medical need.

What made the deal structure particularly sophisticated was its global commercialization strategy. Under the terms of the agreement, AbbVie will receive exclusive rights to develop, manufacture, and commercialize ISB 2001 across North America, Europe, Japan and Greater China. Meanwhile, Glenmark Pharmaceuticals will develop, manufacture and lead commercialization of ISB 2001 across Emerging Markets including the rest of Asia, Latin America, Russia/CIS region, Middle East, Africa, Australia, New Zealand and South Korea.

This wasn't just a licensing deal—it was a strategic partnership that played to each company's strengths. AbbVie brought its expertise in navigating complex regulatory environments and commercializing innovative therapies in developed markets. Glenmark leveraged its deep understanding of emerging markets where the burden of cancer was growing rapidly but access to cutting-edge treatments remained limited.

The financial impact was transformative for IGI's independence. The research arm is self-funded for at least the next three-four years if not more as it uses $70 mn annually. Glenn Saldanha's comment was telling: "this deal puts India in the world map". The pride was palpable—an Indian company had developed a molecule that one of the world's pharmaceutical giants deemed worth nearly $2 billion in total potential payments.

But the AbbVie deal was just one piece of a larger transformation. The unveiling of "Glenmark 3.0" represented Glenn Saldanha's most ambitious vision yet. Under "Glenmark 3.0," the company plans to raise the share of its branded products from 60% to 70% by 2030. This wasn't incremental improvement—it was a fundamental restructuring of the company's revenue model.

The focus will remain on three core therapeutic areas—dermatology, respiratory, and oncology—where Glenmark is investing heavily to strengthen its leadership position. Each of these areas represented not just current strength but future opportunity. In respiratory, Ryaltris was gaining traction globally. In dermatology, decades of expertise were being leveraged for new innovations. In oncology, the IGI pipeline promised multiple breakthrough therapies.

The ambition was breathtaking in scope. These include territories where ISB 2001 alone could generate $5 billion in revenue. To put this in perspective, that single molecule could potentially generate revenues exceeding Glenmark's entire current market capitalization.

Glenn Saldanha's vision extended beyond mere numbers. "Glenmark 3.0 is about moving up the value chain, building a large commercial footprint, and transforming into a global innovation-led company". The transformation he envisioned wasn't just about developing new drugs—it was about fundamentally changing what an Indian pharmaceutical company could be.

"The next 10 years will be about creating something transformational. We will launch branded products, strengthen innovation, and move up the value chain". The timeline was ambitious but deliberate—a decade to complete a transformation that many companies never achieve.

The financial discipline underlying this vision was crucial. Operationally, Glenmark is targeting an EBITDA margin of approximately 19 percent. The company is also eyeing a double-digit profit after tax (PAT) margin while focusing on sustainable financial performance to provide value to stakeholders.

The capital allocation strategy reflected this discipline. Glenmark has earmarked Rs 700 crore for consolidated capital expenditures (CAPEX) to bolster its operational infrastructure. The allocation will be utilised to augment the company's capabilities to meet growing demand efficiently and sustain long-term growth.

Yet challenges remained formidable. The FDA warning letters hadn't disappeared with the AbbVie announcement. The quality issues at multiple manufacturing sites still needed resolution. The company faced the delicate balance of investing in innovation while fixing fundamental compliance problems.

Glenn Saldanha acknowledged the stakes with unusual candor: "One wrong move takes you back by four or five years." This wasn't corporate pessimism—it was the hard-won wisdom of someone who had navigated both spectacular successes and near-catastrophic failures.

The market's response to the AbbVie deal was electric. Glenmark Pharmaceuticals hit an upper limit of 10% to a record high of Rs 2095.65 after its subsidiary Ichnos Glenmark Innovation (IGI) unveiled a global commercialization strategy for its lead investigational oncology asset, ISB 2001. The stock price movement reflected not just the immediate financial windfall but the validation of Glenmark's innovation strategy.

Looking ahead, the pathway was clear but challenging. The asset may take another 4-5 years to be commercialized if timelines are met. Glenmark expects the molecule to transform the multiple Myeloma space, which can become a $50 billion market by 2030.

The Glenmark 3.0 vision represented more than corporate strategy—it was a bet on India's ability to compete at the highest levels of pharmaceutical innovation. With the AbbVie validation in hand and a clear roadmap ahead, Glenn Saldanha was attempting what no Indian pharmaceutical company had achieved: the transition from generic manufacturer to global innovator, all while maintaining profitability and fixing past mistakes. The next decade would determine whether this audacious vision could become reality.

VIII. Playbook: Business & Investing Lessons

The Glenmark story offers a masterclass in both the possibilities and perils of pharmaceutical ambition. The lessons extracted from this journey speak not just to pharmaceutical executives but to any leader attempting to transform a commodity business into an innovation powerhouse.

The Out-Licensing Model as Financial Engineering

Glenn Saldanha's greatest innovation wasn't scientific—it was financial. The out-licensing model he pioneered solved a fundamental problem that plagued emerging market pharmaceutical companies: how to fund expensive R&D without the cash flows of blockbuster drugs. By developing molecules to proof-of-concept and then licensing them to Big Pharma, Glenmark created a self-funding innovation engine. The $230 million earned through partnerships by 2011 wasn't just revenue—it was validation that de-risked future investments.

The genius lay in the deal structures. Retaining emerging market rights meant Glenmark kept territories it understood while monetizing developed markets through partners with established infrastructure. This wasn't giving away the crown jewels—it was strategic capital allocation that recognized comparative advantages.

Family Business Dynamics in Professional Management

The transition from Gracias to Glenn Saldanha illustrates both the strengths and complications of family enterprises. The personal commitment was undeniable—Promoter Holding: 46.6% meant the Saldanha family's wealth was directly tied to Glenmark's success. This skin in the game created accountability that hired CEOs rarely match.

Yet family dynamics also created blind spots. The rapid expansion under Glenn—from generics to innovation, from emerging markets to the US—reflected entrepreneurial ambition that might have been tempered by professional management. The question remains whether an independent board would have pushed harder on compliance issues before they metastasized into FDA warning letters.

The Innovation Paradox: Capability vs. Compliance

Glenmark's simultaneous excellence in innovation and failure in manufacturing compliance presents a fascinating paradox. How could a company developing cutting-edge trispecific antibodies fail at basic tablet dissolution testing? The answer lies in organizational focus and resource allocation.

Innovation captured management attention and resources. Manufacturing facilities, especially those serving generic markets, became afterthoughts—cost centers to be optimized rather than excellence centers to be nurtured. The multiple FDA warning letters weren't just regulatory failures; they were symptoms of an organization that had mentally moved beyond its manufacturing roots without ensuring those roots remained healthy.

Risk Calibration in Regulated Industries

Glenn Saldanha's appetite for risk transformed Glenmark but also nearly destroyed it. The simultaneous pursuit of novel drug development, US market entry, global expansion, and complex generics stretched the organization beyond its capabilities. Each initiative alone was reasonable; together, they created unsustainable complexity.

The potassium chloride crisis crystallized this overreach. The eight deaths weren't just tragedies—they were preventable failures that resulted from pushing manufacturing facilities beyond their quality control capabilities. In pharmaceutical manufacturing, unlike software, "move fast and break things" literally kills people.

Capital Allocation in Dual-Model Businesses

Running both innovative R&D and generic manufacturing creates competing capital demands. Every rupee spent on novel drug development is a rupee not invested in manufacturing quality systems. Glenmark's resolution—spinning off innovation into IGI—recognized this fundamental tension.

The separation allowed each business to optimize for its specific needs. IGI could think like a biotech, burning cash for breakthrough science. Glenmark could focus on operational excellence and compliance. The $700 million AbbVie payment validated this structural solution.

The Cost of Regulatory Non-Compliance

The FDA warning letters taught an expensive lesson: regulatory compliance isn't optional overhead but existential necessity. The immediate costs were visible—blocked facilities, massive recalls, legal liabilities. But the hidden costs were larger: damaged reputation, lost customer trust, management distraction, and depressed valuations.

Consider the opportunity cost. While management fought fires at FDA-cited facilities, competitors launched products, signed partnerships, and captured market share. The years spent remediating quality issues were years not spent on growth. In regulated industries, compliance isn't a cost center—it's the foundation that enables everything else.

Building Global Brands from Emerging Markets

Ryaltris demonstrated that emerging market companies could create global brands, but the path required careful orchestration. The strategy—develop internally, validate through regulatory approvals, then partner for commercialization—leveraged Glenmark's R&D capabilities while acknowledging its commercial limitations.

The key insight: brand building requires different capabilities than drug development. Glenmark could create Ryaltris but needed Hikma for US commercialization and Menarini for Europe. Recognizing what you can't do is as important as knowing what you can.

Managing the Generics-to-Innovation Transition

The attempted transformation from generic manufacturer to innovative pharmaceutical company is littered with failures. Glenmark's partial success offers lessons in managing this transition:

First, maintain the cash cow while building the future. Glenmark's generic business funded innovation experiments, providing the financial cushion to absorb failures like oglemilast.

Second, separate organizationally but integrate strategically. The IGI spinoff created focus while maintaining strategic alignment through ownership.

Third, partner rather than compete with Big Pharma. The out-licensing model turned potential competitors into customers.

Fourth, pick battles carefully. Glenmark focused on specific therapeutic areas—respiratory, dermatology, oncology—rather than attempting broad innovation.

The Platform Value of Failed Experiments

Not every molecule succeeded, but every failure taught lessons. The oglemilast failure informed future respiratory programs. The vatelizumab discontinuation refined biologics development. In pharmaceutical R&D, failures aren't waste—they're education.

The BEAT® platform that produced ISB 2001 was built on years of experimentation, much of it unsuccessful. The $700 million AbbVie payment wasn't just for one molecule—it was for the capability to create such molecules, a capability built through countless failures.

Managing Stakeholder Expectations During Transformation

Glenn Saldanha's public pronouncements—discovering India's first innovative drug, achieving 30% innovation revenues—created accountability but also pressure. Public goals motivated the organization but also locked in strategies that might have benefited from flexibility.

The lesson: transformation narratives should balance ambition with adaptability. Directional commitments ("becoming more innovative") preserve flexibility while specific targets ("30% by 2030") create rigidity that may not survive market realities.

The Glenmark playbook ultimately teaches that transformation requires not just vision but execution discipline, not just ambition but risk management, not just innovation but operational excellence. The company's journey—from pension-funded startup to billion-dollar deals—demonstrates both the potential and perils of pharmaceutical ambition. Whether Glenmark 3.0 succeeds will depend on learning these lessons rather than just teaching them.

IX. Analysis & Bear vs. Bull Case

The Glenmark investment thesis presents one of the most complex risk-reward equations in global pharmaceuticals. The company simultaneously embodies the promise of emerging market innovation and the perils of regulatory overreach, creating a binary outcome scenario that demands careful analysis.

Bear Case: Systematic Failures Compounding

The bear case begins with a simple observation: Glenmark's quality control failures aren't isolated incidents but systemic cultural problems. The FDA's July 2025 assessment was damning in its clarity—"management oversight and control over the manufacture of drugs is inadequate." This isn't about one bad facility or one failed batch; it's about an organization that has repeatedly demonstrated inability to maintain basic pharmaceutical manufacturing standards.

The human cost amplifies the concern. Eight deaths from recalled potassium chloride capsules aren't just statistics—they're litigation liabilities, reputational damage, and regulatory scrutiny that could persist for years. Each family affected represents potential lawsuits that could drain resources and management attention. The case of Mary Louise Cormier, whose recall notice arrived three weeks after her death, symbolizes a system failure that no amount of innovation can offset.

The FDA trust deficit may be irreparable. When multiple facilities receive warning letters, when import alerts block products, when recalls become routine, regulators stop giving benefit of the doubt. Every new submission faces heightened scrutiny. Every inspection assumes problems. This regulatory skepticism becomes a competitive disadvantage that compounds over time.

Generic pricing pressure adds economic headwinds. The global generic market has become commoditized, with Indian manufacturers competing primarily on price. Glenmark's US generic struggles—revenue declining 12.4% in Q4 FY24—reflect this reality. Without differentiation, generics become a race to the bottom that destroys margins and limits reinvestment capacity.

The R&D burn rate presents another concern. Despite decades of investment and multiple partnerships, Glenmark hasn't yet commercialized a novel drug independently. The successful out-licensing deals, while generating upfront payments, also mean Glenmark captures only a fraction of the value from its innovations. The opportunity cost is substantial—resources spent on failed molecules like oglemilast and vatelizumab could have upgraded manufacturing facilities or expanded generic portfolios.

Execution risk looms large over Glenmark 3.0. The vision to achieve 70% branded revenues by 2030 requires flawless execution across development, regulatory approval, and commercialization. History suggests Glenmark struggles with operational complexity. Adding more ambitious targets without fixing fundamental issues risks accelerating failure rather than transformation.

The financial metrics remain concerning. Despite the $700 million AbbVie windfall, Glenmark's return on equity averaged -9.94% over the last three years. Sales growth of 4.6% over five years barely exceeds inflation. These numbers suggest a company struggling to generate sustainable returns even before considering the costs of compliance remediation.

Bull Case: Innovation Validation at Inflection Point

The bull case begins with a powerful vindication: AbbVie's $700 million upfront payment represents the largest single validation of Indian pharmaceutical innovation. This isn't speculative value—it's a sophisticated buyer's assessment that ISB 2001 could address a $50 billion market opportunity by 2030. The potential $1.225 billion in additional milestones suggests AbbVie sees high probability of success.

The deeper significance lies in capability validation. IGI's BEAT® platform isn't just one molecule—it's a proprietary technology that could generate multiple breakthrough therapies. The platform's ability to create trispecific antibodies, when no such drugs are currently marketed, positions Glenmark at the frontier of cancer treatment. This isn't incremental improvement but potential paradigm shift.

The current financials underscore hidden value. With revenues of $1.6 billion and 60% already from branded products, Glenmark has successfully pivoted from pure generics. The branded focus provides pricing power and margin expansion potential that commodity generics lack. The target of 70% branded revenues by 2030 isn't fantasy—it's an extrapolation of existing trajectory.

Geographic diversification provides resilience. While US operations struggle, emerging markets continue growing. India revenues grew 12.9% in Q4 FY24, outperforming industry averages. The rest of world segment grew 9.7%. This multi-market presence provides cushion against single-market regulatory or economic challenges.

The manufacturing footprint, despite quality issues, represents substantial asset value. Ten world-class facilities across five continents provide capacity for both current products and future growth. The quality problems, while serious, are fixable with proper investment and focus. Many successful pharmaceutical companies have recovered from similar challenges.

The promoter commitment cannot be ignored. With 46.6% ownership, the Saldanha family has enormous incentive to fix problems and capture value. This isn't hired management optimizing quarterly earnings—it's owners building generational wealth. Such alignment often drives superior long-term outcomes.

The innovation pipeline extends beyond ISB 2001. Multiple molecules in development, partnerships already generating revenues, and the Ryaltris global rollout provide multiple shots on goal. In biotechnology, one success can offset multiple failures. Glenmark has created enough opportunities that probability favors eventual breakthrough.

Synthesis: A Binary Bet on Transformation

The Glenmark investment case ultimately reduces to a binary question: Can the company fix its operational issues while its innovation initiatives mature? The bear and bull cases aren't opposing views of the same reality—they're different bets on whether transformation or degradation happens first.

The next 24 months appear critical. FDA reinspections will determine whether quality remediation succeeds. ISB 2001's clinical progression will validate or invalidate the innovation thesis. Glenmark 3.0's early execution will signal whether vision translates to reality.

For investors, this creates an unusual risk-reward profile. The downside—continued quality failures leading to market exclusion—could destroy 50-70% of value. The upside—successful innovation commercialization plus operational improvement—could triple or quadruple the current valuation.

The prudent approach might be portfolio positioning rather than binary betting. For those believing in Indian pharmaceutical innovation, Glenmark offers leveraged exposure to that theme. For those skeptical of operational turnarounds, the regulatory overhang provides clear avoidance signals.

What's undeniable is that Glenmark sits at an inflection point. The company will either emerge as India's first true pharmaceutical innovator or become a cautionary tale about ambition exceeding capability. There's little middle ground—transformation or failure, breakthrough or breakdown. In this stark choice lies both the opportunity and the terror of the Glenmark story.

X. Epilogue & Reflections

Standing at the crossroads of pharmaceutical history, Glenmark embodies the contradictions and possibilities of an entire industry in transition. The company's journey from a pension-funded startup to a player commanding $700 million upfront payments from Big Pharma isn't just a corporate story—it's a reflection of India's pharmaceutical ambitions, the global industry's evolution, and the eternal tension between innovation and execution.

The Indian Pharma Paradox

Glenmark crystallizes a paradox that defines Indian pharmaceuticals: world-class scientific capability coexisting with questionable operational discipline. Indian scientists develop trispecific antibodies that attract billion-dollar valuations while Indian factories fail tablet dissolution tests that generic manufacturers mastered decades ago. This isn't cognitive dissonance—it's the reality of an industry that learned to innovate before it learned to operate.

The paradox has historical roots. Indian pharmaceutical companies emerged through reverse engineering, developing sophisticated chemistry capabilities to copy complex molecules while circumventing patents. This created a culture that celebrated intellectual achievement over operational excellence. Breaking down molecular structures required genius; maintaining clean rooms required discipline. The industry systematically selected for the former while undervaluing the latter.

Glenmark amplifies this paradox through the Saldanha family's ambitions. Glenn didn't want to build India's best generic company—he wanted to build India's first innovative pharmaceutical company. This aspiration, noble as it was, led to resource allocation that favored R&D over manufacturing, innovation over operation, future possibility over present reality.

Glenn Saldanha's Legacy: Visionary or Overreacher?

History will judge Glenn Saldanha through the lens of outcomes still unknown. If ISB 2001 becomes a blockbuster, if Glenmark 3.0 succeeds, if quality issues fade into memory, he'll be celebrated as the visionary who transformed Indian pharmaceuticals. If facilities remain under import alert, if innovations fail to commercialize, if compliance costs consume profits, he'll be remembered as the executive who flew too close to the sun.

Yet this binary framing misses nuance. Glenn's greatest contribution might not be what he achieved but what he attempted. By pushing Glenmark toward innovation, he demonstrated that Indian companies could aspire beyond generics. The out-licensing model he pioneered created a template others now follow. The partnerships he negotiated proved Indian science could attract global capital.

His failures teach equally important lessons. The quality crises demonstrate that operational excellence can't be sacrificed for innovation ambitions. The regulatory troubles show that compliance isn't optional overhead but existential necessity. The execution struggles reveal that transformation requires not just vision but organizational capability.

Glenn Saldanha emerges neither as pure visionary nor simple overreacher, but as something more complex: an entrepreneur whose ambitions exceeded his organization's capabilities but whose attempts expanded the realm of possibility for an entire industry.

Can Glenmark Become India's First True Global Innovator?

The question isn't whether Glenmark can develop innovative drugs—ISB 2001 proves it can. The question is whether it can build the organizational infrastructure to repeatedly discover, develop, and commercialize novel therapies while maintaining operational excellence. This requires capabilities beyond science: regulatory expertise, commercial sophistication, operational discipline, and cultural transformation.

The structural solutions Glenmark has implemented—spinning off IGI, partnering for commercialization, focusing on specific therapeutic areas—suggest learning from past mistakes. The separation of innovation from operations acknowledges that different businesses require different cultures. The partnership model recognizes that collaboration trumps competition when entering new domains.

Yet structural solutions alone don't guarantee success. Culture eats strategy for breakfast, and Glenmark's culture—entrepreneurial, risk-taking, innovation-obsessed—enabled both its greatest successes and most devastating failures. Transforming culture while maintaining entrepreneurial spirit requires delicate balance that few organizations achieve.

The global pharmaceutical landscape provides context for Glenmark's ambitions. As Western pharmaceutical companies increasingly outsource R&D and manufacturing, opportunities emerge for companies that can combine emerging market cost structures with developed market quality standards. Glenmark sits at this intersection—if it can achieve operational excellence.

Lessons for Emerging Market Companies Going Global

Glenmark's journey offers hard-won wisdom for emerging market companies with global ambitions:

First, operational excellence must precede innovation ambitions. The temptation to leapfrog developmental stages—moving directly from low-cost manufacturing to high-value innovation—ignores that operational discipline provides the foundation for everything else. Without quality systems, regulatory compliance, and operational excellence, innovation becomes impossible to commercialize.

Second, partnerships can accelerate capability development but don't replace it. Glenmark's out-licensing model generated capital and validation but also revealed limitations. True global success requires building capabilities internally, not just accessing them through partners.

Third, regulatory compliance in developed markets isn't negotiable. The FDA warning letters teach that regulatory standards can't be met selectively or temporarily. Compliance must be embedded in organizational DNA, not treated as a hurdle to overcome.

Fourth, family businesses face unique challenges in globalization. The alignment and commitment that family ownership provides can accelerate transformation, but family dynamics can also create blind spots and resistance to necessary changes. Professional management and independent oversight become more critical as complexity increases.

Fifth, transformation timelines are longer than anticipated. Glenn Saldanha has been pursuing innovation for over two decades, and Glenmark still hasn't independently commercialized a novel drug. Patience, persistence, and financial resources must align with ambitious timelines.

The Future of Indian Pharma Innovation

Glenmark's story, still being written, will influence how Indian pharmaceutical companies approach innovation. Success would demonstrate that emerging market companies can compete globally in drug discovery, potentially unleashing a wave of innovation investment. Failure would reinforce that operational excellence must precede innovation ambitions, possibly delaying India's pharmaceutical evolution.

The broader implications extend beyond India. As pharmaceutical innovation becomes increasingly expensive and complex, new models are needed. Glenmark's approach—leveraging emerging market cost advantages for drug discovery while partnering for commercialization—could provide a template for global pharmaceutical innovation.

The next decade will be decisive. If Glenmark can fix its quality issues, successfully commercialize innovations, and achieve its 3.0 vision, it will have completed one of business history's most remarkable transformations. If it stumbles, it will join the long list of companies whose ambitions exceeded their abilities.

What's certain is that Glenmark has already changed the conversation. An Indian pharmaceutical company developing molecules worth $700 million to AbbVie was unthinkable a generation ago. That it's now reality, despite all of Glenmark's challenges, suggests the future holds possibilities we're only beginning to imagine.

The sun has set on the era when Indian pharmaceutical companies were content being the world's generic pharmacy. Whether it rises on an era of Indian pharmaceutical innovation depends partly on whether Glenmark can navigate the treacherous passage from vision to reality. In that navigation lies not just one company's future but clues to an entire industry's evolution.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube