Gateway Distriparks: The Story of India's Container Revolution

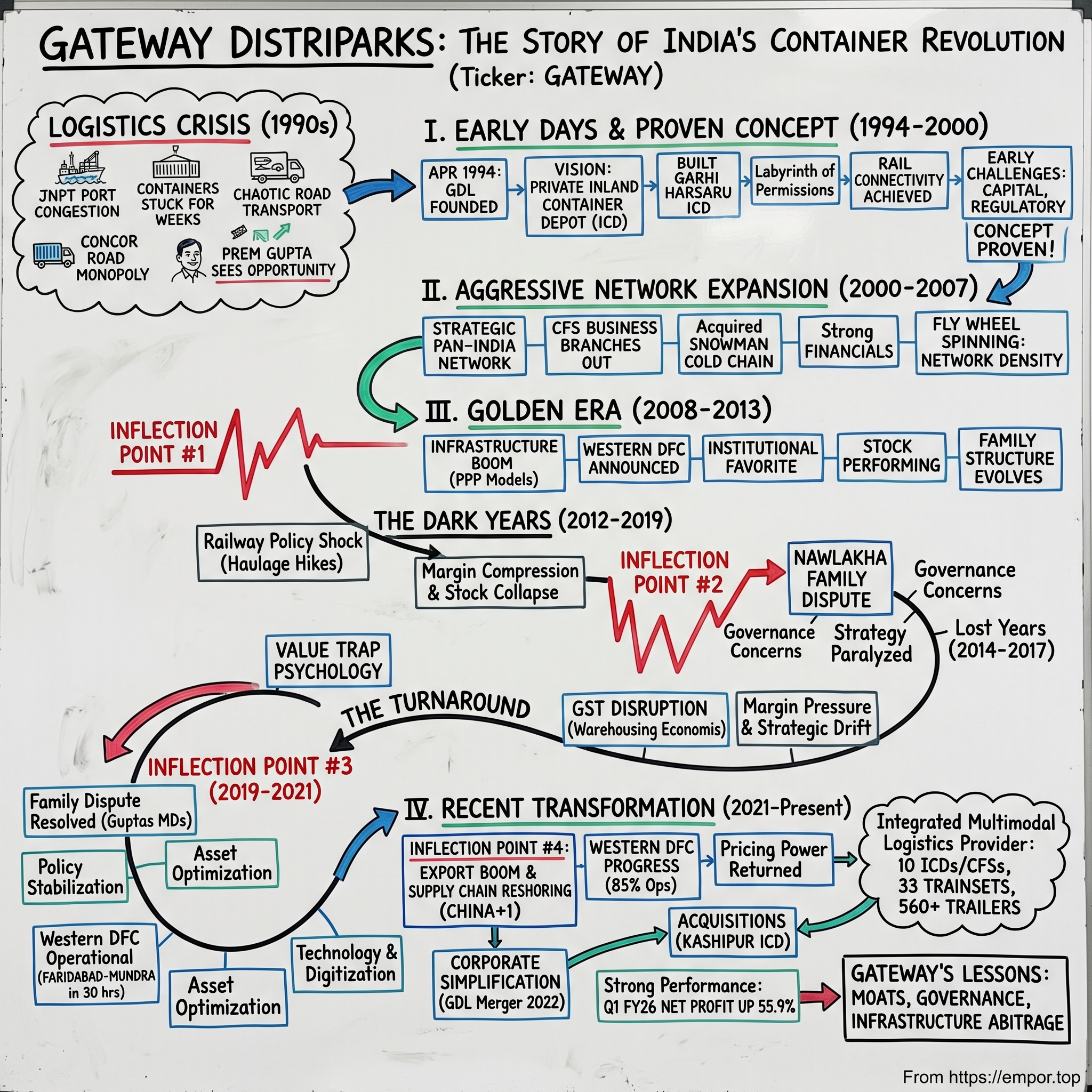

The monsoon rains pounded the cramped storage yards at Jawaharlal Nehru Port in Mumbai during the summer of 1993. Containers stacked four-high sat waterlogged and immobile, their contents trapped in a bureaucratic and infrastructural nightmare that had become synonymous with India's trade infrastructure. Importers waited weeks—sometimes months—to clear cargo that had traveled halfway around the world only to languish a few kilometers from its final destination.

This was the India that Prem Kishan Dass Gupta witnessed firsthand. A businessman running a newsprint trading operation, Gupta knew every chokepoint in India's supply chain intimately. The country had flung open its economic doors in 1991, but the plumbing to handle the resulting trade surge simply didn't exist. Road transport was chaotic, ports were congested, and the Indian Railways monopoly on container movement offered little hope for change.

In that dysfunctional landscape, Gupta saw not frustration but opportunity—a massive infrastructure arbitrage waiting to be exploited. The question wasn't whether India needed better logistics. It was whether a private entrepreneur could navigate the Railway's stranglehold, assemble the capital, and build the missing link in India's freight chain before the opportunity vanished.

I. Introduction & Episode Roadmap

Gateway Distriparks Limited, founded in April 1994, pioneered India's private container rail and logistics infrastructure, becoming one of the first companies to break the government monopoly on containerized freight movement. Over three decades, the company has survived—and sometimes thrived through—a gauntlet of challenges that would have destroyed lesser businesses: sudden railway policy reversals that eviscerated margins overnight, a bitter family feud that paralyzed management for years, the GST's unintended disruption of warehousing economics, and the global supply chain chaos of the COVID era.

Today, Gateway stands as an integrated multimodal logistics provider with a network of 10 ICDs and container freight stations strategically located across India, operating a fleet of 33 trainsets (21 owned and 12 on long-term lease) along with over 560 trailers. The company's story is more than a corporate biography—it's a window into the transformation of Indian logistics, the perils of capital-intensive businesses in regulatory environments, and the peculiar dynamics of family-controlled infrastructure companies.

This is the story of how Gateway Distriparks became a proxy for India's logistics revolution, why it nearly collapsed multiple times, and what its resurrection tells us about investing in emerging market infrastructure.

II. The Founding Context: India's Logistics Crisis (1990s)

The India of 1991 was an economy gasping for breath. Foreign exchange reserves had dwindled to barely two weeks of imports. The country stood on the precipice of default. Then came the reforms—a forced economic liberalization that would reshape the nation.

Finance Minister Manmohan Singh's budget speech that July dismantled the License Raj, slashed import tariffs, and opened sectors to foreign investment. Almost overnight, India transformed from a closed economy into one hungry for global trade. Container volumes at Indian ports, which had grown sedately for decades, suddenly exploded.

But India's infrastructure couldn't keep pace. The containerization revolution that had transformed global shipping in the 1960s and 70s had barely touched India's hinterlands. Importers faced a Kafkaesque reality: containers would arrive at Mumbai's Jawaharlal Nehru Port (JNPT) or Chennai Port, then sit for weeks in congested port yards. The "last mile"—actually the last few hundred kilometers—became the most expensive and time-consuming part of international supply chains.

Road transport, the default option, was a nightmare of its own. Trucks crawled through state border checkpoints, where octroi taxes and entry permits required mountains of paperwork. A journey from Mumbai to Delhi that should have taken 30 hours often stretched to four or five days. The fragmented, unorganized trucking sector meant finding reliable capacity was a daily scramble.

Container movement by rail was a monopoly of Indian Railways until 2005, with its subsidiary Container Corporation (CONCOR) the sole operator of container trains since 1989. CONCOR, while competent, operated like a government entity because it was one. Service orientation took a back seat to procedures. Customers complained about problems in first and last mile connectivity, reliability and customer orientation, partly due to the monopoly status of CONCOR.

The regulatory backdrop was Byzantine. Indian Railways controlled not just the trains but the tracks, the terminals, the pricing, and the allocation of slots. Private participation in railway operations was virtually nonexistent. The concept of an entrepreneur running container trains on Railway tracks seemed as likely as someone opening a private post office.

Yet the opportunity was immense. India's containerized trade was projected to grow at double-digit rates for years. Someone who could crack the code—who could build private infrastructure that plugged into the Railway network while delivering superior service—would capture enormous value.

This was the landscape that drew Prem Kishan Dass Gupta's attention.

III. The Birth of Gateway Distriparks (1994-2000)

Prem Kishan Dass Gupta wasn't a logistics professional by training, but he understood trade. Gupta operated a newsprint business, Newsprint Trading & Sales Corporation since 1978, importing massive rolls of paper through Indian ports. Every shipment was an exercise in patience and problem-solving. He saw firsthand how India's logistics bottlenecks added weeks of delay and layers of cost to every transaction.

The insight that sparked Gateway was deceptively simple: what if you could build a facility inland—away from the congested ports—where containers could be moved, stored, and cleared through customs more efficiently? The concept was called an Inland Container Depot (ICD), and while CONCOR operated a few, the model remained underdeveloped.

In April 1994, Gateway Distriparks was founded, originally promoted by Newsprint Trading & Sales Corporation (NTSC), CWT Distribution Limited, NUR Investment and Trading Pvt. Ltd. and Intercontinental Forest Products Pte. Ltd. (IFP) as a joint venture company to conduct the business of warehousing, container freight stations and all related activities.

The founding vision was audacious for its time: build India's first significant private Inland Container Depot with rail connectivity to major ports. The value proposition combined several services that were typically fragmented—storage, customs clearance, stuffing and unstuffing of containers, and importantly, rail movement to ports.

The first major project was the ICD at Garhi Harsaru, near Delhi. The ICD at Garhi Harsaru spread over 31 hectares (later noted as 21 hectares) and was road-linked, catering to the rich hinterlands of Northern India, including Delhi, Haryana, Punjab and Rajasthan. Getting it operational required navigating a labyrinth of permissions—land acquisition, environmental clearances, and crucially, an agreement with Indian Railways for rail connectivity.

The facility attained a milestone in terms of rail connectivity with its own rail siding connecting the ICD to the main Delhi-Jaipur Broad Gauge lines. In February 2006, Gateway received an in-principle approval from Indian Railways to move container trains, and the first full rake train carrying export containers railed out of ICD Garhi in early 2006, followed by import movement in May 2006.

The business model was elegantly bundled: Gateway would handle everything from the moment a container arrived at a port until it reached the customer's warehouse (or vice versa for exports). Customers paid a single, transparent fee instead of dealing with multiple vendors. For a country where supply chain visibility was virtually nonexistent, this was revolutionary.

The early challenges were formidable. Capital requirements were crushing—land, rail sidings, container handling equipment like reach stackers and gantry cranes, warehousing space. The company was formerly incorporated as Gateway Rail Freight Limited on April 6, 1994 and got Certificate of Commencement of Business on October 24, 1994. The company name later changed from Gateway Rail Freight Limited to Gateway Distriparks Limited on February 11, 2022 through a merger.

Gateway went public early, listing in 1994 to fund its expansion. This was unusual for an infrastructure startup, but necessary—the capital intensity of the business demanded it. Convincing customers to trust a new private operator when they could use the government's CONCOR was another battle. Many shipping lines and large importers had established relationships and were risk-averse.

Regulatory hurdles were constant. Every expansion required Railway approvals, and the bureaucracy moved at glacial speed. The Railways was simultaneously regulator, infrastructure provider, and competitor (through CONCOR), creating obvious conflicts of interest.

But Gateway had two advantages: Gupta's deep understanding of customer pain points, and timing. As India's containerized trade surged through the late 1990s, CONCOR simply couldn't keep pace with demand. Capacity constraints created space for a nimble private operator who could deliver better service.

By the end of the decade, Gateway had proven the concept. The Garhi Harsaru ICD was operational, containers were moving by rail, and customers were seeing tangible benefits in cost and time savings. The company had survived the high-mortality early years and established itself as a legitimate player in India's logistics infrastructure.

IV. Expansion Phase: Building the Network (2000-2007)

The new millennium brought Gateway into its growth phase. Having proven that private ICDs could work, the company moved aggressively to build a pan-India network before competitors could establish footholds.

The strategic expansion followed India's trade geography. The company operated container freight stations at Navi Mumbai, Chennai, Visakhapatnam and the Inland Container Depot at Garhi Harsaru. These four facilities made Gateway the only private sector CFS operator with a Pan-India presence.

The crown jewel was the Nhava Sheva connection. JNPT (Jawaharlal Nehru Port Trust) at Navi Mumbai handled roughly 60% of India's containerized cargo. The CFS at Navi Mumbai, spread over 14 hectares, had a capacity to handle 216,000 TEUs per annum. The CFS at Chennai spread over 7.5 hectares had capacity to handle 40,000 TEUs. Being adjacent to the country's busiest port meant Gateway could capture massive volumes.

Container Freight Stations (CFS) became Gateway's second major business line alongside ICDs. While ICDs were inland facilities connected by rail to ports, CFSs were located near ports and handled the immediate stuffing, destuffing, and temporary storage of containers. The economics were different—lower capex per unit but more competitive and port-dependent—but the CFS business provided steady cash flow and diversification.

The company also made a bold diversification bet: cold chain logistics. In 2006, Gateway announced the acquisition of a majority stake of 50.1 percent in Snowman Frozen Foods Ltd for Rs 48.12 crore. The logic was compelling: India's retail sector was booming, organized food retail was emerging, and the cold chain infrastructure was primitive. Gateway entered into agreements with Snowman's shareholders—Mitsubishi Corporation, Mitsubishi Logistics Corporation and Nichirei Logistics Group—who continued to hold 48.69 percent.

Financial performance through this period was strong. Revenue grew at healthy double-digit rates, margins expanded as facilities reached scale, and return ratios improved. The stock performed well, rewarding patient investors who had believed in the infrastructure story.

Competition began to emerge. The trade and industry realized CONCOR alone couldn't meet demand, and the Ministry of Railways decided to open the sector for competition in 2005, announcing in February 2005 that the government would permit private operators to run container trains. Companies like Adani Logistics, Allcargo, and regional players entered the fray. But Gateway maintained leadership through its first-mover advantage, established rail connectivity, and superior location strategy.

The business model's flywheel was spinning: more terminals meant more network density, which meant better service and lower costs, which attracted more customers, which funded more expansion. Gateway was building a moat through physical infrastructure and relationships—two advantages that were hard for new entrants to replicate quickly.

By 2007, Gateway had established itself as India's leading private container logistics player, a remarkable achievement just over a decade after founding.

V. The Golden Era & Infrastructure Boom (2008-2013)

If there was a golden era for Gateway Distriparks, it was the period from 2008 to 2013. India's infrastructure boom was in full swing, government policy was supportive, and Gateway rode the wave to its peak performance.

The broader context was critical. Despite the 2008 global financial crisis, India's economy remained relatively resilient. The government doubled down on infrastructure spending, viewing it as both countercyclical stimulus and long-term growth enabler. The Planning Commission pushed Public-Private Partnership (PPP) models. The government actively promoted PPPs during the 12th Five-Year Plan (2012-17) by raising INR 1 trillion through PPP projects.

For logistics specifically, several catalysts aligned. Port modernization projects expanded capacity at JNPT, Mundra, and other major ports. Most importantly, the government announced plans for Dedicated Freight Corridors (DFCs)—separate rail lines dedicated to freight that would transform Indian Railways' capacity and speed. The Dedicated Freight Corridors Corporation of India Limited (DFCCIL) was incorporated on October 30, 2006, with the Union Cabinet approving both the Eastern and Western corridors in February 2008.

Gateway's performance during this period was exceptional. Revenue growth accelerated, margins expanded as operational leverage kicked in, and the stock delivered multi-bagger returns. The company became an institutional favorite—a pure play on India's logistics transformation with established operations, unlike the speculative infrastructure stocks that littered the market.

Key developments reinforced the bull case. The Western Dedicated Freight Corridor (DFC), planned to connect Delhi with Mumbai via Gujarat and Rajasthan, would pass through regions where Gateway had ICDs. Once operational, the DFC would offer faster transit times and lower costs, directly benefiting Gateway's rail operations.

The cold chain business through Snowman also showed promise. India's food retail was evolving—organized players like Big Bazaar and Reliance Fresh were expanding, quick-service restaurants like McDonald's and Pizza Hut were opening hundreds of outlets, and dairy companies needed temperature-controlled logistics. Gateway operated Snowman in partnership with Mitsubishi Logistics, providing temperature-controlled storage to customers like HUL, Baskin Robbins, Pizza Hut, and Mother Dairy. While contributing only 15% to revenues, it saw 58% y-o-y growth and was expected to generate 54% CAGR revenue growth.

The family business structure evolved during this period. Prem Kishan Dass Gupta served as Chairman and Managing Director, and also served as Chairman at Snowman Logistics Ltd. and Gateway Distriparks (Kerala) Ltd. Samvid Gupta became Joint Managing Director with six years of experience in various aspects of business including Financial Planning, Sales, Projects, Business Analysis and Strategic Planning. The sons were joining the leadership, setting the stage for generational transition.

International expansion was occasionally discussed but never seriously pursued. Gateway's thesis remained focused: India's logistics opportunity was so vast and underpenetrated that going overseas would dilute focus. Better to dominate the home market.

By 2012-2013, Gateway seemed unstoppable. The infrastructure story, long-term contracts, hard assets, and operating leverage created a compelling investment narrative. The stock traded at premium valuations, reflecting expectations of continued growth as DFCs commenced and India's trade expanded.

Then the wheels came off.

VI. INFLECTION POINT #1: The Railway Policy Shock (2012-2014)

The blow came suddenly and from an unexpected direction. In 2012-2013, Indian Railways, facing its own mounting financial crisis, dramatically hiked the charges it levied on private container train operators.

The context was India Railways' deteriorating finances. While passenger services accounted for 67 percent of total passenger-kilometer traffic, they generated only one-third of total earnings, causing sustained fiscal deficits. In FY 2013-14 alone, losses on passenger and coaching services amounted to INR 31,727 crore. The Railways had been cross-subsidizing cheap passenger fares with higher freight charges for decades, but the model was buckling.

The Railway administration responded by squeezing private operators. Haulage charges—the fees private operators paid to use Railway tracks, locomotives, and signaling systems—were raised dramatically. Management expected to pass on the cost impact from Indian Railways removing the 5% rebate on haulage of loaded containers and 25% rebate on haulage of empty containers.

For Gateway, the impact was immediate and severe. The company's business model depended on charging customers competitive rates for door-to-door service. Sudden spikes in railway haulage costs couldn't be instantly passed through—contracts with shipping lines and major customers had fixed terms. Even when renegotiations were possible, customers had alternatives: road transport became relatively more attractive when rail costs surged.

Margin compression was brutal. The rail business, which had been Gateway's highest-margin segment, saw EBITDA margins shrink by several percentage points almost overnight. The stock, which had been a darling, collapsed. From peaks around Rs 300-350 in 2010-2011, shares plunged 60-70% over the next two years.

The existential question loomed: was the rail-based ICD model fundamentally broken? If the Railways could arbitrarily raise charges whenever it needed revenue, private operators would never have pricing power or predictable economics. Why invest in capital-intensive rail infrastructure when the regulator could expropriate returns through administrative fiat?

Gateway's response was multi-pronged but constrained. The company negotiated with customers to pass through cost increases, with mixed success. It launched cost optimization drives, reducing overhead and improving operational efficiency. Industry associations lobbied the Railway Board, arguing that killing private operators would reduce competition and ultimately harm the sector.

But the deeper problem was structural. CTOs had to pay haulage charges to Indian Railways for using its facilities such as track, locomotive and signaling systems, making them largely dependent on the Railways. CTOs also felt the Railways had an overlap of professional interests, being simultaneously interpreter, policy maker and implementing body.

The policy shock exposed the fundamental vulnerability of Gateway's business model: regulatory risk. No matter how good the operations, how strong the customer relationships, or how strategic the locations, the company operated at the mercy of Indian Railways' policy decisions. And those decisions were driven not by economic logic but by the Railways' own fiscal desperation and political pressures.

Investor confidence evaporated. Institutional investors who had championed the stock began quietly exiting. The growth story that had seemed so compelling now looked like a value trap. Analysts downgraded ratings, questioning whether the rail ICD model had any sustainable competitive advantage when the regulator was also the competitor.

The Railway policy shock of 2012-2014 marked Gateway's first near-death experience. The company survived, but the scars ran deep. The premium valuation disappeared, replaced by skepticism that would linger for years. Worse was yet to come.

VII. INFLECTION POINT #2: The Nawlakha Family Dispute (2014-2017)

Even as Gateway struggled with railway policy headwinds, an internal crisis exploded that would paralyze the company for years: a bitter family dispute over control and succession.

The roots ran deep in Indian family business dynamics. Gateway, while professionally managed, remained family-controlled through the promoter entities. As of November 2015, Prism International Private Limited (same group as NTSC) became the sole promoter of the company. But within the family structure, tensions simmered between different branches.

The dispute pitted Prem Kishan Dass Gupta and his sons against relatives, reportedly from the Nawlakha branch of the extended family. The specifics involved allegations of corporate governance violations, disputes over shareholding, and fundamentally, who would control Gateway's future. Legal battles erupted. SEBI investigations were reportedly initiated examining related party transactions and disclosure issues.

For a company trying to navigate challenging business conditions, the family warfare was catastrophic. Management attention was diverted from operations to litigation. Strategic decisions were delayed or paralyzed as different factions jockeyed for position. Key hires were put on hold. Expansion plans stalled.

The impact on investor confidence was devastating. Institutional investors, already spooked by the railway policy issues, now faced governance concerns. Family disputes in Indian companies rarely end cleanly, and the risk of wealth destruction through infighting was very real. Shareholders couldn't tell who was really in charge or what the company's strategy actually was.

The stock languished in the doldrums. From 2014 to 2017, Gateway shares traded between Rs 100-150, roughly half the pre-crisis levels, despite the broader market recovering strongly. Trading volumes were thin—a sign that investors had lost interest entirely.

The resolution process dragged on. Family settlements in such disputes typically involve complex negotiations over shareholding, board representation, and management control. While details of Gateway's family settlement were not fully disclosed publicly, regulatory filings show directors including family members during this period, and by late 2021 the status changed to "Amalgamated", suggesting corporate restructuring was part of the resolution.

The lessons were painful. Gateway's story illustrated the hidden costs of family business structures in Indian companies. Even well-governed firms could be derailed by succession disputes. The value destruction was immense—not just stock price declines but lost opportunities as competitors gained ground.

Perhaps most damaging, the family dispute delayed Gateway's response to industry changes. While management fought internal battles, the external environment was shifting dramatically. GST implementation was approaching, the DFC construction was progressing, and competitive dynamics were evolving. Gateway needed to be adapting its strategy, but instead, it was paralyzed.

By 2017, as the family dispute finally resolved, Gateway had lost nearly three years. The company had gone from industry leader to damaged goods. The question was whether it could recover—or whether the damage was permanent.

VIII. The Dark Years: Margin Pressure & Strategic Drift (2015-2019)

The period from 2015 to 2019 represented Gateway Distriparks' nadir—a perfect storm of external challenges and internal dysfunction that left the company adrift.

The railway policy uncertainty never fully resolved. While the most dramatic hikes moderated, the pricing remained unpredictable. Private operators like Gateway existed in regulatory limbo, never quite sure what costs they would face next quarter. This made long-term planning nearly impossible and deterred the kind of aggressive capacity expansion that had characterized Gateway's earlier growth phase.

Then came GST in July 2017, and with it, an unintended consequence that hammered the warehousing sector. Prior to GST, companies had to set up warehouses in nearly every state to dodge inter-state taxes like CST, leading to redundant infrastructure. GST replaced this patchwork with a unified system, removing inter-state tax barriers so businesses could consolidate into fewer, larger, strategically placed warehouses.

For the broader logistics industry, GST was transformational and positive. But for companies with significant warehousing exposure, the transition was painful. The main impact of GST on warehousing was the reduced number of warehouses. Tax efficiencies affected warehouse quantity and location more than operating efficiencies. Suddenly, customers who had maintained small warehouses in multiple states started consolidating. Demand for warehousing space temporarily plummeted as companies rationalized their networks.

Gateway felt this acutely in its CFS business and warehousing operations. Utilization rates declined. Pricing power evaporated. Revenue stagnation set in—a stark contrast to the double-digit growth of earlier years.

Competition intensified from multiple directions. Road transport, always a competitor, became relatively more attractive as highway infrastructure improved and GST removed inter-state checkpoints. Prior to 2017, highways were filled with checkpoints where trucks waited for hours. GST removed these obstacles, and average transportation times decreased significantly by approximately 20 to 33%. Faster, more reliable road transport narrowed rail's advantage for many routes.

New logistics models emerged. Tech-enabled platforms like Rivigo and eventually Delhivery built asset-light models that threatened traditional infrastructure plays. E-commerce logistics, booming with Amazon and Flipkart's growth, followed different patterns than traditional EXIM containerized freight.

Port congestion, ironically, eased. As ports invested in expansion and better equipment, the urgency of moving containers to inland depots diminished. Some large importers and shipping lines found it more economical to process containers at port-adjacent facilities rather than moving them inland.

Gateway's cold chain business through Snowman struggled as well. The segment required continuous capex to expand capacity, but utilization remained stubbornly low. Margins compressed as newer, regional cold chain operators entered the market. The partnership with Adani Logistics that was announced in late 2019 to sell Gateway's stake ultimately fell apart. The proposed sale of entire 40.25 percent stake in Snowman Logistics to Adani Logistics for Rs 296 crore was called off due to repudiation of the agreement by the acquirer.

Financial performance deteriorated markedly. The company delivered a poor sales growth of -0.70% over past five years as of certain periods. EBITDA margins compressed by several percentage points from peak levels. Return on equity, once in healthy teens, collapsed into single digits. Debt levels crept up, not dramatically but enough to worry credit rating agencies.

Management changes added to the instability. While the Gupta family remained in control post-settlement, operational leadership saw turnover. CFO changes were noted, with resignations occurring. Strategy seemed reactive rather than proactive—cost-cutting dominated over growth initiatives.

The stock became a value trap in the classic sense. At Rs 100-120, Gateway traded at single-digit P/E ratios and below book value. Value investors would periodically nibble, seeing "cheap" assets. But the stock would languish or decline further as each quarterly result disappointed. The thesis that DFC commissioning would rescue Gateway seemed perpetually "just around the corner" but never quite materialized.

Analysts and investors increasingly questioned whether the structural decline was irreversible. Maybe containerized rail freight's moment had passed. Maybe GST had permanently reduced warehousing demand. Maybe the capital intensity simply couldn't generate adequate returns in a competitive, regulated environment. "Why catch a falling knife?" became the prevailing view.

The value trap psychology was reinforced by comparison to other logistics stocks. Newer, asset-light tech platforms like Delhivery were drawing investor attention and capital. The "old economy" infrastructure play that Gateway represented seemed hopelessly outdated.

But beneath the surface, tectonic shifts were beginning that would ultimately vindicate the patient. The question was whether Gateway could survive long enough to benefit from them.

IX. INFLECTION POINT #3: The Turnaround Begins (2019-2021)

Gateway's renaissance didn't arrive with fanfare. It emerged gradually from a combination of external catalysts and internal restructuring that few investors initially noticed.

The most important external catalyst was railway policy stabilization. After years of unpredictable hikes, the Railways' approach to private operators moderatedmore, partly because the financial crisis eased and partly because the Dedicated Freight Corridor was finally nearing operational status. As of April 2024, the Eastern Freight Corridor became fully operational whereas the Western Freight Corridor reached 85% operational status. Overall 90% of the network was operational, with 300 trains running daily.

The DFC's commissioning was transformational. Gateway successfully operated a container train on the Western DFC from its ICD in Faridabad to Mundra Port. The train was flagged off on June 2, 2023 and arrived on June 3, 2023, with a transit time of 30-32 hours—compared to 56 hours previously using the traditional Indian Railways network. Nearly halving transit times while improving reliability was a game-changer for Gateway's value proposition.

Internally, management refocused under Samvid Gupta and Ishaan Gupta as Joint Managing Directors, with the family dispute resolved. Strategic initiatives centered on three priorities: asset optimization, operational efficiency, and customer relationships.

Asset optimization meant exiting non-core and underperforming assets. Gateway let a Punjab government CFS contract expire without renewal because pricing didn't make sense, and sold one smaller CFS in Chennai. The Krishnapatnam CFS was also planned for monetization as the port shifted from containerized to bulk cargo. The focus shifted decisively toward high-return ICD assets and away from lower-margin, competitive CFS operations.

Technology investments accelerated. Gateway implemented automation and digitization across operations—warehouse management systems, track-and-trace capabilities, digital documentation. Gateway launched E-Forwarding during a customer meet held on January 12, 2024, introducing a paperless alternative to traditional documentation. The initiatives promised benefits to stakeholders while contributing to sustainability.

Customer relationships deepened. A big chunk of customers were shipping lines. With the amalgamation of Gateway Distriparks with Gateway Rail Freight onto one platform, the company could offer volume discount schemes and 11 terminals on one platform, making customers happier. Long-term contracts with major exporters, importers, and shipping lines provided revenue visibility.

Cost restructuring targeted bloated overheads accumulated during the growth years. Headcount was rationalized, unprofitable routes were cut, and operational processes were streamlined. The leaner cost base meant Gateway could be profitable even at lower utilization rates.

Then came the COVID surprise. When lockdowns hit in early 2020, many feared logistics would collapse. Instead, the company seemed to benefit as essential services gained priority, and e-commerce boomed, driving container demand. Supply chain disruptions globally meant companies valued reliability over cost, benefiting established operators like Gateway.

Financial inflection became visible in fiscal 2021-2022. EBITDA margins started recovering toward historical levels. Debt reduction began—not dramatically, but consistently. Cash generation improved as working capital management tightened.

Critically, Gateway completed the acquisition of Blackstone's 49% stake in subsidiary Gateway Rail Freight for Rs 8.5 billion (Rs 850 crore) in 2019, making it a 99.93% subsidiary. While the delay in closure to March 31, 2019 attracted an interest penalty taking the total payout to Rs 8.5 billion, Gateway paid via Rs 3 billion internal accruals and Rs 5.5 billion debt in the form of NCDs with 11.25-11.5% coupon rate and 7-year tenor. This consolidated control and simplified the corporate structure, though it temporarily increased leverage.

Market recognition lagged. Even as fundamentals improved through 2020-2021, the stock remained undervalued. Investors scarred by years of disappointment were skeptical. The "value trap" label stuck. But patient, contrarian investors who looked past the damaged reputation saw improving return ratios, strengthening cash flow, and a company positioned to benefit from multiple tailwinds.

Gateway had survived its near-death experience and was quietly positioning for the next phase.

X. The Recent Transformation (2021-Present)

The transformation accelerated dramatically from 2021 onward, driven by a convergence of factors that turned Gateway from value trap to multi-bagger.

INFLECTION POINT #4: The Export Boom & Supply Chain Reshoring

Global supply chain disruptions, initially seen as crisis, became opportunity. The pandemic exposed over-reliance on single-source manufacturing, particularly China. Container freight rates exploded globally—a 40-foot container from Asia to Europe that cost $2,000 pre-pandemic hit $20,000 at peaks. Port congestion worldwide created backlogs.

India benefited from the "China+1" strategy. Multinationals and Indian exporters expanded manufacturing capacity, driving export volumes. Container traffic through Indian ports surged, and Gateway's rail operations saw record volumes.

The Western DFC's progressive commissioning transformed economics. 325 trains ran daily on the DFC network—a 60% increase year-over-year. With 93.2% of the WDFC completed and key feeder routes supporting major ports like Mundra, Kandla, Pipavav, and Hazira, freight movement was transformed. Gateway's rail freight business, housed under Gateway Rail Freight Limited, emerged as the key growth driver with the DFC commencement. Gateway was well positioned across the Western DFC with ICDs covering the entire industrial corridor of Northern India.

Pricing power returned as capacity tightened. With more demand than rail capacity, Gateway could negotiate better terms with customers. The years of being price-takers reversed.

Corporate restructuring simplified the entity. Through a Scheme of Amalgamation approved by shareholders on September 28, 2021, the company name changed from Gateway Rail Freight Limited to Gateway Distriparks Limited on February 11, 2022, with Gateway East India and Gateway Distriparks merging into Gateway Rail Freight. With effect from December 28, 2021, the merger brought Container Freight Station, rail and Inland Container Depot businesses under one umbrella.

The CFS business revived. Port congestion returned with the global trade surge, and suddenly proximity to ports was valuable again. Gateway's CFS assets at Navi Mumbai, Chennai, and other locations saw utilization rates climb.

Acquisitions strengthened the network. In 2022, Gateway acquired Kashipur Infrastructure And Freight Terminal (KIFTPL). The acquisition of ICD Kashipur added volumes to rail operations and connected to the Western Dedicated Freight Corridor via the company's ICD in Gurgaon. Gateway planned to spend Rs 180 crore on two inland container depots by FY25, either acquiring them or buying land and constructing ICDs.

Financial performance reached new heights. For the full year ended March 2025, net profit rose 44.74% to Rs 370.86 crore compared to Rs 256.23 crore in the prior year. Sales rose 9.40% to Rs 1,680.56 crore from Rs 1,536.13 crore. For Q1 FY26 ended June 30, 2025, the company recorded net profit of Rs 62.2 crore, a significant increase from Rs 49.1 crore in the same quarter prior year.

Margins expanded to historical highs as operational leverage kicked in. The fixed-cost nature of the business meant incremental volumes dropped heavily to the bottom line. Gateway approached debt-free status, having paid down the Blackstone-related borrowings ahead of schedule.

ESG became a narrative advantage. The DFC's rail infrastructure allowed double-stacked shipping containers on flatcars with 400-container capacity, versus road transport. Rail freight produces dramatically lower carbon emissions per ton-kilometer than trucking. As corporates faced pressure to decarbonize supply chains, rail became attractive beyond pure economics.

The stock market re-rating was dramatic. From the Rs 100-120 levels of 2019-2020, shares climbed steadily, reaching Rs 66-67 range as of mid-2025 post-split, but representing multi-bagger gains from the lows when adjusted for corporate actions. Trading volumes surged as institutional investors who had abandoned the stock returned.

Capital allocation shifted toward returns. Gateway announced a first interim dividend of Rs 1.25 per share for FY 2025-26, with record date of August 2, 2025, translating to a dividend yield of 4.90%. For a company that had struggled to generate cash just years earlier, paying dividends signaled confidence in sustainable profitability.

The "new Gateway" that emerged was fundamentally different: leaner, focused, operationally excellent, and better governed. Management demonstrated they had learned from the dark years. The company exited marginal businesses, doubled down on rail ICDs where competitive advantages were strongest, and maintained financial discipline.

Gateway signed a 15-year agreement to operate container trains at the Multi Modal Logistics Park in Ankleshwar, enhancing logistics efficiency. Q1 FY26 results showed revenue up 55.9% to Rs 550.4 crore, demonstrating continued momentum.

XI. The Broader Logistics Revolution in India

Gateway's transformation mirrored—and benefited from—a broader revolution in Indian logistics that accelerated through the 2020s.

The context was sobering: India's logistics costs remained stubbornly high at 13-14% of GDP compared to 7-8% in developed markets. This represented massive economic friction—trillions of rupees wasted annually on inefficient movement and storage of goods. For an economy aspiring to become a $5 trillion powerhouse, logistics reform was essential.

Government initiatives proliferated. The National Logistics Policy launched in 2022 aimed to create a single-window e-logistics market, reduce costs to single digits as a percentage of GDP, and improve India's ranking in the Logistics Performance Index. PM Gati Shakti, announced in 2021, envisioned integrated infrastructure planning across ministries. Port-led development models like Sagarmala aimed to transform India's 7,500 km coastline into an economic driver.

The infrastructure buildout was unprecedented. The DFCs were just the beginning. The Golden Quadrilateral Freight Corridor has six DFCs; two were being implemented with funding for the remaining four approved in January 2018. These corridors—linking Delhi, Mumbai, Chennai and Kolkata—carry 55% of Indian Railways' freight traffic over 10,122 km route length. The detailed project reports for three new corridors—East Coast, East-West, and North-South—were submitted with an estimated cost of Rs 4 lakh crore. The East Coast corridor (Paradip to Vijayawada) would take priority.

Port modernization continued. JNPT's expansion, Mundra's rise as India's largest commercial port, and new deep-water ports coming online all increased capacity and efficiency. The DFC system was built to handle speeds up to 100 kmph—double the average speed of Indian Railways' freight trains. Currently averaging 50 kmph on operational segments, DFCCIL was already clocking 85% capacity utilization and expected to push to 96-99% by mid-2026, handling 480 trains daily.

The competitive landscape evolved dramatically. CONCOR remained the dominant player with its government backing and extensive terminal network. CONCOR had a 72% share of container traffic with extensive assets including 15,500 container wagons, 80 container terminals, 26,000 containers and 14 gantry cranes. But its share was gradually eroding to private operators.

Allcargo emerged as a diversified competitor, combining container logistics with freight forwarding and contract logistics. Adani Logistics leveraged its parent's port ownership to build an integrated model. Adani held a 12-13 percent market share while Gateway had about 10-12 percent market share.

Tech-enabled logistics startups disrupted traditional models. Delhivery, which went public in 2022, built an asset-light platform connecting shippers with truck capacity. Rivigo pioneered relay-based trucking to reduce driver fatigue and improve asset utilization. BlackBuck created a digital marketplace for trucking. These platforms threatened to disintermediate traditional logistics providers.

But road vs. rail economics still favored rail for long-haul container movements. Trucks in India covered 250-300 km per day versus 800 km in the USA and 450 km in Brazil. Approximately 60% of travel time was lost due to unorganized paperwork and tax compliance, causing logistics costs to hover at two to three times the international benchmark. Even after GST improvements, rail offered superior economics for distances over 500-600 kilometers and full container loads.

The modal shift opportunity remained massive. Just 5% of freight in India was transported by containers, compared to the global average of 25 to 40% of intermodal transport. As India's economy formalized and supply chains matured, containerization would inevitably increase, benefiting rail operators.

Where Gateway fit in this landscape was increasingly clear: the essential, "boring" infrastructure layer. While tech platforms grabbed headlines, someone needed to physically move containers from ports to hinterlands. Gateway's network of rail-linked ICDs, accumulated over decades, was nearly impossible to replicate quickly. The capital requirements, railway approvals, and operational expertise created durable moats.

The DFC era might finally fulfill the promise that had tantalized investors for over a decade. With dedicated tracks, higher speeds, and greater reliability, rail's advantages over road would become overwhelming for appropriate cargo. Gateway, positioned along the Western DFC with ICDs at strategic nodes, was ideally placed to capture this shift.

XII. Business Model Deep Dive & Unit Economics

Understanding Gateway requires dissecting the economics of its distinct business lines, which have very different capital requirements, competitive dynamics, and return profiles.

Revenue Streams Breakdown

As of certain periods, rail transport accounted for 63.80% of revenue, road transport for 3.45%, container storage, handling, and ground rent for 32.20%, and others for 0.55%. The split varies quarter to quarter based on volumes and mix, but rail freight operations typically contribute 50-55% of revenues, CFS business 30-35%, and cold chain and others 10-15%.

The Economics of an ICD

An Inland Container Depot is a capital-intensive but high-return business when operating at scale. The components include:

Capex Requirements: - Land acquisition: Typically 20-50 acres depending on expected volumes. Land costs vary dramatically by location but represent the single largest upfront investment. - Rail infrastructure: Rail sidings connecting to the main railway line, signaling systems, and trackside equipment can cost Rs 50-100 crore depending on complexity. - Handling equipment: Reach stackers (mobile cranes that lift and move containers) cost Rs 2-3 crore each. Empty handlers, forklifts, weighbridges, and other equipment add tens of crores. - Warehousing and paving: Covered warehouses for cargo consolidation, paved container stacking areas, and administration buildings. - Total capex: A greenfield ICD typically requires Rs 200-400 crore in total investment, though acquisitions of existing facilities can sometimes be done for less.

Variable Costs: - Railway haulage: The largest variable cost, paid to Indian Railways for track usage, locomotives, and crew. This historically ranged from 50-65% of rail freight revenue, though the exact percentage depended on negotiated rates and rebates. - Labor: Operators for handling equipment, administrative staff, security, customs brokers. - Maintenance: Equipment repairs, track maintenance contributions, facility upkeep. - Utilities and other variable costs: Power for reefer containers, diesel for handling equipment, etc.

Operating Leverage: The magic of the ICD business is operating leverage. Once built, an ICD has significant fixed costs (depreciation, minimum staffing, base maintenance) but limited variable costs for incremental containers. A facility operating at 40% utilization might barely break even, but at 75-80% utilization, incremental volumes drop heavily to EBITDA. This explains both the feast-or-famine nature of the business and why scale matters enormously.

CFS Economics

Container Freight Stations have different economics: - Lower capex: CFSs don't require extensive rail infrastructure since they're located near ports. A typical CFS might require Rs 100-200 crore versus Rs 300-400 crore for an ICD. - Port-dependent: Volume and viability depend entirely on the servicing port's traffic. If the port shifts cargo patterns or a terminal closes, the CFS suffers. - Competitive intensity: Lower barriers to entry mean more competition. Pricing power is limited, and margins are typically lower than ICD operations. - Service mix matters: CFSs that offer value-added services (customs brokerage, container repair, specialized cargo handling) earn better margins than pure storage operations.

Return Profiles

Historical return on capital employed (ROCE) for Gateway varied dramatically: - Peak years (2010-2013): ROCEs in the high teens to low twenties as utilization was high and pricing stable. - Crisis years (2015-2019): ROCEs collapsed to single digits as margins compressed and underutilized assets dragged returns. - Recovery (2021-present): ROCEs recovering toward mid-teens as volumes surged and operational efficiency improved.

The path to sustained ROE improvement depends on: 1. Volume growth: The DFC driving modal shift from road to rail. 2. Price stability: Railway haulage costs remaining predictable. 3. Mix improvement: Higher-margin ICD revenues growing faster than lower-margin CFS. 4. Asset turns: Better utilization of existing facilities before adding new capacity.

Capital Allocation

Gateway's capital allocation evolved through different phases: - Growth phase (2000-2010): Most cash reinvested in new ICDs and CFS facilities. - Crisis phase (2015-2020): Minimal growth capex, debt repayment prioritized. - Current phase (2021-present): Balanced approach—selective expansion in high-return opportunities (Kashipur acquisition, Jaipur greenfield), maintenance capex to sustain operations, and returns to shareholders via dividends now that balance sheet is strong.

In early FY23, Gateway allocated Rs 500 crore towards capital expenditure to be utilized by fiscal 2025, with about Rs 200 crores already invested toward acquisition of ICD Kashipur and land procurement and initial development of ICD Jaipur. The goal was investing the remaining amount in new projects in Northern and Central India to expand the ICD network.

Why This is a "Real Asset" Infrastructure Business

Unlike asset-light logistics platforms, Gateway owns tangible, hard-to-replicate physical infrastructure. The value resides in: - Land in strategic locations: Nearly impossible to acquire today at reasonable costs near major cities. - Railway connectivity approvals: Multi-year processes unlikely to be repeated for new entrants. - Installed equipment and facilities: Depreciated assets generating cash. - Network effects: More locations mean better service, attracting more customers, funding more locations.

The business is fundamentally about earning a return on large, lumpy capital investments over 20-30 year time horizons. It's unglamorous, capital-intensive, and regulated—but those same characteristics create barriers to entry that protect returns once established.

XIII. Playbook: Business & Investing Lessons

Gateway Distriparks' three-decade journey offers rich lessons for entrepreneurs, operators, and investors navigating emerging market infrastructure businesses.

The Infrastructure Arbitrage Play

Gateway's founding exploited a structural inefficiency: India had opened to trade, but lacked the logistics infrastructure to handle the flow. This arbitrage opportunity was massive but required patient capital willing to invest years before payback. The lesson: the biggest opportunities in emerging markets often lie in basic infrastructure that developed economies take for granted. Look for structural demand-supply mismatches where capital and execution can capture decades of growth.

Regulatory Risk is Real—and Mispriced

The railway policy shocks of 2012-2014 demonstrated that regulatory risk in government-adjacent businesses is not theoretical. When the regulator is also your customer (Indian Railways provided infrastructure) and your competitor (through CONCOR), conflicts of interest are inevitable. Gateway's stock collapsed because investors underestimated this risk in the good years, then overestimated it in the bad years. The lesson: properly pricing regulatory risk requires understanding the political economy, not just reading policy documents. And even fair pricing may not be enough—sometimes the risk is simply unquantifiable.

Family Business Governance Matters—A Lot

The Nawlakha family dispute destroyed billions in market capitalization and set Gateway back years. The hidden costs of succession issues in family-controlled businesses are massive: diverted management attention, paralyzed strategy, spooked investors, lost opportunities. The lesson: governance quality in family businesses should be weighted heavily in valuation. Clear succession plans, independent directors with real power, and transparent related-party protocols matter enormously. Their absence can destroy wealth faster than operational mistakes.

Patience and Positioning in Cyclical, Capital-Intensive Businesses

Gateway's value trap phase from 2015-2020 tested investor patience. Those who sold in frustration missed the subsequent multi-bagger returns. Those who bought during max pessimism did extraordinarily well. The lesson: capital-intensive, cyclical businesses often trade well below intrinsic value during downturns because near-term results look terrible and the cycle feels permanent. Patient investors who can withstand the psychological pain and accurately assess long-term earnings power capture exceptional returns. Position sizing is critical—these investments require conviction to hold through darkness.

The Importance of "Boring" Infrastructure

In an era celebrating asset-light tech platforms and marketplace models, Gateway's story reminds us that someone still needs to physically move containers from ports to warehouses. Boring infrastructure—rail tracks, container yards, warehouses—generates real cash flow and proves surprisingly durable. The lesson: don't dismiss capital-intensive businesses as "old economy." When they have genuine competitive moats (location, regulation, scale), they can compound capital for decades. The premium attached to capital-light models can create opportunities to buy hard assets cheaply.

India's Logistics Transformation: Multi-Decade Theme, Non-Linear Progress

Gateway's journey from 1994 to 2025 tracked India's logistics evolution—and showed that progress is never linear. The DFC, announced in 2005, took 18-20 years to substantially complete. GST, transformational in the long run, caused short-term disruption. India's journey from 13-14% logistics costs to developed-market levels will take decades and feature setbacks. The lesson: transformational themes in emerging markets play out over 20-30 year timeframes with multiple false starts. Investors need either permanent capital or willingness to trade around positions. The trend is real; the path is jagged.

Operating Leverage Thesis: How Fixed-Cost Businesses Scale

Gateway's financial inflection from 2020-2023 demonstrated operating leverage's power. With largely fixed infrastructure and overhead, incremental volume growth dropped disproportionately to EBITDA. Margins expanded by several percentage points as utilization improved. The lesson: when analyzing fixed-cost businesses, focus intensely on utilization and volume trajectory. The unit economics at 80% capacity look radically different than at 50% capacity. Buying during volume troughs, when margins are compressed but assets remain valuable, can generate extraordinary returns as the cycle turns.

The Contrarian Opportunity: Buying "Structurally Declining" Narratives

From 2015-2019, the consensus was that Gateway's ICD model was structurally impaired. Railway policy risk was unmanageable, GST permanently reduced warehousing demand, and competition would prevent margin recovery. This consensus was wrong—or at least premature. The lesson: "structurally declining" narratives often overshoot. If management can survive to the inflection, patient contrarians win big. The key is distinguishing temporary cyclical weakness (Gateway) from true structural decline (print newspapers). Capital allocation during the tough years matters—Gateway survived by cutting costs and avoiding major mistakes.

Second-Order Effects: Connecting Macro Dots

Gateway's recovery stemmed from connecting disparate trends: GST's long-term logistics benefits, DFC commissioning, China+1 manufacturing shift, and supply chain reliability premiums post-COVID. None of these factors individually would have saved Gateway, but together they created a powerful tailwind. The lesson: emerging market investing requires connecting macro developments (government policy, global trade shifts, infrastructure timelines) to company-specific implications. The ability to synthesize second- and third-order effects separates great investors from good analysts.

Myth vs Reality: The "Cash-Free, Debt-Free" Fallacy

During Gateway's dark years, some investors avoided it despite cheap valuation because "the business just burns cash." Reality: Gateway's free cash flow was negative during heavy expansion or when utilization collapsed, but the business was fundamentally cash-generative at normalized utilization. The confusion stemmed from not adjusting for growth capex versus maintenance capex. The lesson: distinguish between businesses that destroy cash (retailers with structurally negative unit economics) and cyclical businesses that invest during downturns. Gateway's 2023-2025 free cash flow generation, enabling dividends and debt paydown, validated that the underlying economics were sound.

XIV. Analysis & Bear vs. Bull Case

As Gateway enters 2025-2026, the investment debate crystallizes around competing narratives about the company's future and India's logistics evolution.

Bull Case: The Golden Decade Ahead

India's Trade Growth and Manufacturing Renaissance

India's merchandise trade crossed $1.2 trillion in recent years and is projected to hit $2 trillion by 2030. The government's Production Linked Incentive (PLI) schemes are driving manufacturing capacity in electronics, pharmaceuticals, and textiles. Every percentage point of manufacturing growth drives disproportionate containerized freight growth. Gateway, with established infrastructure, captures this with minimal incremental capex.

DFC Operational Ramp-Up Creates Structural Cost Advantage

The Western DFC's completion by December 2025 marks a paradigm shift. The DFC allows double-stacked containers with 400-container capacity and features GSM-based tracking—a first in Indian Railways. Transit times have already halved on operational sections. As the full network goes live and kinks are worked out, rail's advantage over road will become overwhelming for long-haul moves. Gateway's ICDs along the corridor become essential nodes, gaining pricing power.

Pricing Power in Tight Capacity Environment

With DFCCIL now handling over 10% of Indian Railways' total freight volume, capacity utilization is high and growing. Gateway faces limited competition for established routes and can pass through cost increases. Unlike the 2012-2014 squeeze, pricing power has shifted toward operators who can guarantee capacity and reliability.

Strong Cash Generation and Capital Returns

Gateway is approaching a debt-free balance sheet after years of deleveraging. With maintenance capex of Rs 50-100 crore annually and minimal growth capex required (existing land banks can handle expansion), free cash flow generation could reach Rs 300-400 crore annually. This supports a 3-4% dividend yield with room for buybacks or growth when opportunities arise.

ESG Tailwinds Favor Rail Over Road

Corporate sustainability mandates increasingly drive logistics decisions. Rail freight emits 2-3x less CO2 per ton-kilometer than trucking. As Indian exporters to Europe and USA face carbon border adjustment mechanisms, rail transport becomes not just economical but necessary for supply chain decarbonization. Gateway can charge premiums for certified green logistics.

Valuation Remains Reasonable vs. Infrastructure Peers

At current valuations around 13-15x P/E, Gateway trades at discounts to infrastructure peers and logistics platforms. If it can sustain 15%+ ROEs and mid-single-digit revenue growth, the stock deserves 18-20x P/E—implying significant upside from current levels. The market still underestimates the DFC's transformational impact and Gateway's operating leverage.

Management Proven Through Crisis

The Gupta family guided Gateway through near-death experiences—railway policy shocks, family disputes, GST disruption. Having survived the worst, they've demonstrated capital discipline, operational focus, and strategic patience. The corporate simplification and family dispute resolution removed major overhangs.

Bear Case: Structural Headwinds Remain

Railway Policy Risk Never Disappears

Indian Railways' financial problems are far from solved. Passenger losses reached Rs 33,000 crore in 2014-15 and gross budgetary support from central government was proposed at Rs 53,060 crore in 2018-19. Post 2015-16, over 56% of capital expenditure was being met through borrowings. If finances deteriorate again, Railways might squeeze private operators. The 2012-2014 playbook could repeat. Regulatory risk hasn't been eliminated—it's been dormant.

Competition from Road Transport and New Entrants

GST-induced improvements in highway logistics narrowed rail's advantage. Modern trucks with GPS tracking, organized fleet operators, and improving road quality make road competitive for many routes. Tech-enabled platforms like Delhivery can aggregate truck capacity at lower costs than asset-heavy rail operators. Adani's logistics ambitions, backed by deep pockets, pose growing competitive threats.

Capex Requirements May Pressure Returns

While bulls emphasize existing capacity, bears note that capturing growth requires continuous investment. Gateway planned Rs 180 crore on two ICDs by FY25. Rs 500 crore was allocated for capex through FY25. If every volume increment requires proportionate capex, return ratios may disappoint. The DFC may simply shift where bottlenecks occur rather than eliminating them.

GST Long-Term Impact on Warehousing Demand Unclear

The rationalization of warehouse networks post-GST may be permanent. Companies discovered they could operate with fewer, larger facilities. This structural reduction in warehousing demand per unit of GDP hurts Gateway's CFS business and any warehouse expansion plans. The pre-GST model isn't coming back.

Port Operations Evolution Could Disintermediate

As ports develop direct rail connectivity and inland logistics capabilities, they may reduce reliance on independent ICDs. Ports that build their own container handling facilities at strategic inland locations could bypass Gateway entirely. The company's role as intermediary may erode as ports vertically integrate.

Family Business Concerns Never Fully Go Away

Despite the resolution, Gateway remains family-controlled with promoter holding at 32.3%—low for a family business, potentially signaling reduced commitment. Succession to the next generation always carries execution risk. Will the younger Guptas prove as capable in navigating crises? Minority shareholders remain at the mercy of family dynamics.

Global Trade Slowdown Risk

India's trade growth isn't guaranteed. Global recession, geopolitical fragmentation, or China's rebound could slow India's export momentum. The China+1 narrative might prove temporary. If trade volumes stagnate, Gateway's volumes suffer and utilization drops, destroying margins through operating deleverage.

Single-Country Concentration Risk

Gateway has no international operations and negligible diversification beyond India. Any India-specific shock—political instability, fiscal crisis, conflict—would devastate the company. Unlike global logistics players with geographic diversification, Gateway is a pure, undiversified bet on India.

Competitive Positioning Assessment

vs. CONCOR:

CONCOR retains advantages: government backing, 72% market share, 80 terminals, 15,500 wagons, and political support. However, Gateway offers superior private sector efficiency, customer service orientation, and operational flexibility. As the government potentially privatizes CONCOR, this competitive dynamic may shift dramatically.

vs. Allcargo:

Allcargo's diversified logistics platform (freight forwarding, contract logistics, EXIM services) reduces dependence on any single business. But this diversification creates complexity. Gateway's focused strategy on rail ICDs may deliver superior returns in its niche, even if Allcargo grows faster overall.

vs. New-Age Logistics Platforms:

Delhivery, Mahindra Logistics, and tech-enabled players own little physical infrastructure, giving them asset-light scalability. However, they remain dependent on underlying infrastructure providers like Gateway for actual rail movement. The platforms aggregate demand; Gateway provides supply. These are complementary more than competitive—though platforms could eventually integrate backward if attractive.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube