Ganesha Ecosphere: The Alchemy of India's Plastic Waste

I. Introduction & Episode Roadmap

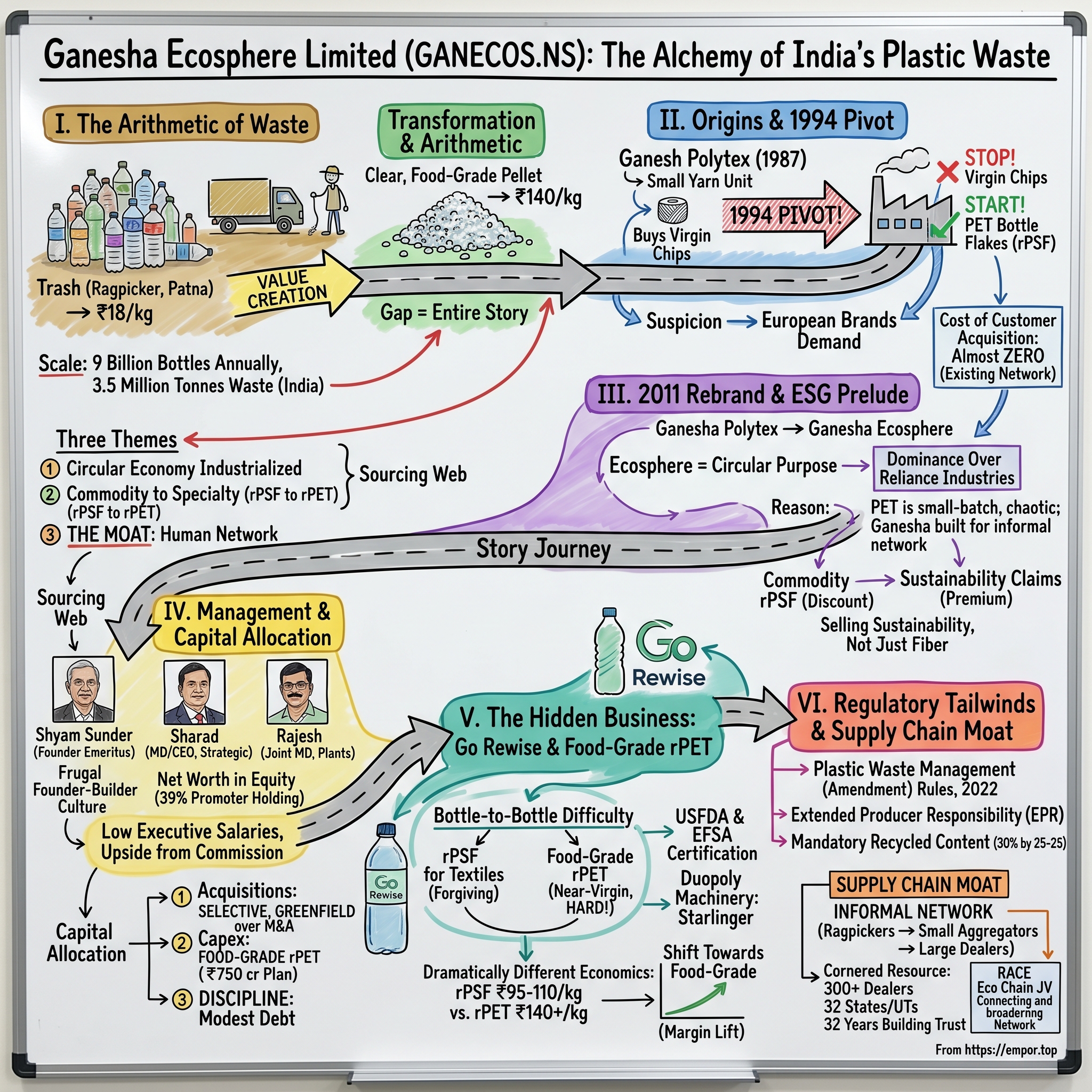

Picture a railway siding outside Kanpur on a humid afternoon in 2026. A tempo truck pulls in piled high with what looks, at first glance, like the entire colour wheel of misery — flattened Bisleri bottles, faded Coca-Cola red, the translucent green of an old Limca, fragments of a Pepsi label still clinging to one corner. A worker tips the bale onto a conveyor. Within forty-eight hours, the polyethylene terephthalate from that pile will exist as something else entirely — either as a fluffy white fibre destined for a Decathlon t-shirt in Bengaluru, or, more remarkably, as a clear, food-grade pellet that will end up inside a fresh sealed Coke bottle on a shelf in Delhi. The ragpicker who picked the original bottle off a Patna sidewalk earned perhaps eighteen rupees per kilo. The transformed pellet will sell for around one hundred and forty.[^1]

That arithmetic — the gap between trash and treasure — is the entire story of Ganesha Ecosphere गणेश इकोस्फीयर. India generates roughly 3.5 million tonnes of plastic waste every year, and a substantial slice of the country's discarded PET bottles flows through Ganesha's plants in Kanpur, Bilaspur, Warangal, and now Odisha.[^2] At full run-rate, the company has processed close to nine billion bottles annually. Read that again. Nine billion. If you laid them end to end, you could wrap them around the earth more than ten times.

But this article is not really about plastic. It is about a quiet, almost stubborn family business from Kanpur that figured out — three decades before "ESG" became a McKinsey deck and a Goldman conference — that the most overlooked resource in India was not lithium, not rare earths, not even data. It was waste. Specifically, the discarded PET bottle, picked up by hand from a landfill, a riverbank, a temple gate, by a network of informal kabaadi waalas कबाड़ी वाले that operates with the efficiency of a Swiss watch and the visibility of a ghost.

The Ganesha Ecosphere story has three big themes we will pull on through this piece. The first is the चक्रीय अर्थव्यवस्था circular economy — not as a slogan, but as a real industrial system being assembled, in real time, on Indian soil. The second is the migration from commodity to specialty: how a yarn spinner from Uttar Pradesh slowly, patiently, climbed from selling ₹100-a-kilo polyester staple fibre to ₹140-a-kilo USFDA-grade food-contact resin. And the third — the most interesting one for a long-term investor — is the moat. Not the machines. Not the patents. The moat is human: 300+ scrap dealers, thousands of ragpickers, a sourcing web that took thirty-two years to build and which, as we will see, no amount of Reliance or Indorama capex can replicate in a hurry.[^6]

The roadmap for the next two hours. We will start in Kanpur in 1987, when Shyam Sunder Sharma श्याम सुंदर शर्मा borrowed against the family textile business to set up Ganesh Polytex. We will work through the 1994 pivot — the moment a small yarn maker bet the company on recycled polyester at a time when "recycled" was a slur in the textile market. We will pause at 2011 for the rebrand, look hard at the Sharma family's capital allocation philosophy, and then turn to the present — the Go Rewise brand, the ₹750-crore capex plan funded partly by a ₹350-crore QIP, the RACE Eco Chain joint venture, and the regulatory tailwind that is the Extended Producer Responsibility framework.1[^4]

If you only remember one image from this episode, make it the one we opened with: that bottle, that ragpicker, that eighteen-rupee-to-one-hundred-and-forty-rupee arc. Everything else — the QIPs, the Starlinger machines, the EBITDA margins — is just the scaffolding that makes the arc possible.

II. Origins: The Yarn Beginnings & The 1994 Pivot

The Sharma family was not, in any obvious sense, a "tech" family. Kanpur in the 1980s was a city of leather tanneries on the Ganga, of cotton mills slowly dying, of small traders who lived above their shops in Naya Ganj and kept their ledgers in Hindi. Shyam Sunder Sharma was a textile man — a yarn man, more specifically. He understood denier and tenacity the way a Bombay broker understood futures contracts. And in 1987, he set up Ganesh Polytex with a single, conventional ambition: to spin synthetic yarn for the burgeoning Indian apparel industry.2

For the first seven years, Ganesh Polytex was utterly unremarkable. It was one of perhaps a hundred small-to-mid-sized polyester yarn units that dotted northern India in the late eighties — buying virgin polyester chips from the petrochemical majors, melting them, extruding them, selling the resulting yarn to weavers in Bhiwandi and Surat. Margins were thin. Competition was knife-fight close. The Sharmas were, at best, a survivor in a brutal commodity business.

Then came 1994. Manmohan Singh's reforms were three years old. The licence raj was crumbling. And in Europe, something interesting was happening: textile mills had begun experimenting with recycled polyester staple fibre — rPSF — spun from washed and shredded PET bottle flakes. It was a niche product, viewed with suspicion, but it had one unimpeachable advantage. The feedstock — empty bottles — could be sourced for a fraction of the price of virgin chips, because globally, almost nobody wanted them.

Shyam Sunder Sharma made a decision that, in hindsight, looks visionary, and which, at the time, looked simply nuts. He stopped buying virgin chips. He started buying bottles. He retrofitted his yarn line to handle the rougher, less consistent recycled feedstock. And he began to sell rPSF to a market that did not, at that moment, know it wanted to buy it.

The first five years were a slog. Textile buyers in Surat and Tirupur sniffed at the very idea. "Trash-based fibre" carried a stigma that no amount of lab certification could fully erase. Salesmen for Ganesh Polytex would carry rPSF samples in their bags, walking into mills that already had relationships with Reliance and IPCL, and try to convince a foreman that fibre made from a Pepsi bottle could perform identically to fibre made from naphtha. Often they were laughed out of the room.

What saved the company was the price gap and a quiet realisation about the textile market itself. Recycled fibre, by virtue of cheaper feedstock, could be priced ten to fifteen percent below virgin — and the apparel buyers downstream of the spinners, particularly those exporting to Europe and the US, were beginning to ask quiet questions about supply chain sustainability. By the late 1990s, certain European brands had started writing "recycled content" requirements into procurement contracts. The trickle would become a flood.

There is a useful detail here that explains how Ganesha survived where many would-be recyclers failed. The Sharmas already had a textile distribution network. They knew the mill owners personally. They had been selling yarn into the same buyers for years. So when they pivoted to rPSF, they did not have to build a sales organisation from scratch — they simply had to convince existing customers to try a new product. The cost of customer acquisition, in other words, was almost zero. The legacy yarn business, far from being a millstone, turned out to be the distribution DNA that the recycling business needed to find its feet.

By 2000, Ganesh Polytex had quietly become the largest PET recycler in northern India, with a footprint that, even then, suggested the eventual shape of the moat to come. Bottle aggregators in Lucknow, Allahabad, Jaipur, Delhi all knew the Ganesh trucks. The relationships were transactional, cash-on-delivery, often unrecorded — and they were utterly unduplicable by any glossy MBA business plan written from a Mumbai office.

The 1994 pivot was the company's defining act. Every strategic decision the Sharmas would make over the next three decades would, in some way, be a continuation of that single bet — that "trash to treasure" was not just a slogan but a viable industrial thesis. The next chapter would be about scaling it.

III. The 2011 Rebranding & The ESG Prelude

By the late 2000s, Ganesh Polytex had a problem of its own success. The company that had started life as a yarn maker was now selling almost no virgin yarn at all. It was a recycling company that, technically, was named after polymer extrusion. Investors trying to understand the story would land on the website and see the old textile branding. Customers in Europe — increasingly the most lucrative buyers — would ask, politely, whether the company had a sustainability narrative they could put in their own annual reports. The disconnect was becoming expensive.

In 2011, the family pulled the trigger on a rebrand. Ganesh Polytex became Ganesha Ecosphere. The new name was, on its face, a marketing exercise. In practice, it was a declaration of identity. The "Polytex" in the old name had implied polyester textiles — a description of input, not output. "Ecosphere" implied a circular system — a description of purpose. The capitalised "Ganesha", with its echo of the elephant-headed remover of obstacles, was unchanged. The family ethos remained. What changed was the framing of what the family did.

The rebrand coincided, almost serendipitously, with a deeper operational reality. Between roughly 2008 and 2014, Ganesha Ecosphere quietly out-competed the recycling arms of much larger players in the northern Indian market. Reliance Industries रिलायंस Reliance Industries had a recycling vertical. So did smaller players such as Polygenta and JBF Industries. None of them matched Ganesha on the dimensions that mattered: cost per kilo of finished fibre, consistency of feedstock supply, and crucially, relationships with the kabaadi network.

Why did the giants struggle? Because PET recycling in India is, paradoxically, a small-batch business pretending to be an industrial one. A Reliance plant manager wants a truck of feedstock with consistent grade, consistent moisture content, consistent contamination profile. Ragpicker-sourced bottles are not consistent. They arrive in chaotic, multi-coloured, mixed-grade bales from a thousand different micro-aggregators. To process them economically, you need a sorting and washing line that is forgiving — and you need people who, at the plant gate, can negotiate the spot price for a particular batch in the local dialect, in cash, with a handshake. Reliance was not, culturally, built for that. Ganesha was. The Sharmas were merchants first, industrialists second, and that order mattered.

The other thing that happened around 2011 was a slow rewriting of what the customer was actually buying. Through the 2000s, Ganesha had been selling commodity rPSF at a discount to virgin polyester — a price-led proposition. By the early 2010s, the leading global brands had started to publish sustainability reports with hard targets: Coca-Cola's PlantBottle ambitions, Unilever's commitments to recycled content in packaging, H&M's pledges on circular fibres. Sustainability had become a procurement line item. Buyers were no longer asking "is your fibre cheaper?" They were asking "can you certify the recycled content, and can you commit to volume?"

That changed the economics. Recycled fibre that had once been priced at a discount to virgin began, in certain grades and certain channels, to command a premium. Not a huge premium — but enough to invert the unit economics of the recycling business. The Sharmas understood, perhaps earlier than most domestic peers, that they were no longer selling fibre. They were selling sustainability credits, packaged as a physical product. The product was the receipt; the value was the story.

This is the under-appreciated point about the 2011 rebrand. It was not a vanity exercise. It was a recognition that the company's most valuable output was not the rPSF flake or the chip — it was the verifiable, certifiable claim to circularity. And to monetise that claim, the company needed an identity that put the circle, not the polymer, in the centre of the brand. Hence "Ecosphere".

By 2014, Ganesha Ecosphere had achieved a kind of category dominance in domestic rPSF. The next ten years would be about something harder — moving up the value chain into food-grade rPET, into filament yarn, into bottle-to-bottle. But before we get there, we need to understand the family that runs the show.

IV. Management: The Sharma Dynasty & Capital Allocation

There is a particular kind of Indian promoter family that western analysts often misread. They are not the flamboyant Mumbai-based, private-jet-flying, headline-grabbing variety. They are the second- and third-tier-city merchant clans — Kanpur, Indore, Ludhiana, Coimbatore — who have spent three generations building one business, who live in modest homes a short drive from their factories, and whose entire net worth is, almost without exception, locked inside the equity of the listed entity. The Sharma family of Ganesha Ecosphere fits this template precisely.

Shyam Sunder Sharma, the founder, remained chairman emeritus through the 2010s, but operational control had by then passed to his sons. Sharad Sharma शरद शर्मा took the role of Managing Director and CEO; his brother Rajesh Sharma राजेश शर्मा became Joint Managing Director. The transition was characteristically quiet — no investor day, no glossy press release, just a slow handing over of operational dossiers, plant-level decisions, customer relationships. The brothers had both, in effect, been training inside the business since their twenties.2

Sharad is the strategic and external-facing brother. He handles the investor conferences, the relationships with multinational FMCG buyers, the cross-border negotiations with European brands. He has, in published interactions, the manner of a chartered accountant who happened to inherit a factory — measured, slightly understated, prone to using phrases like "calibrated approach" and "asset-light expansion where possible". Rajesh runs the plants. He is the one who, by all accounts, knows the precise yield of the wash line in Bilaspur on a given Tuesday in August.

Read across the management ecosystem and a pattern emerges. The independent directors are seasoned but unflashy — retired bureaucrats, textile-industry veterans, chartered accountants. The CFO is a long-tenured insider. There is no chief sustainability officer with a Stanford MBA being paid an absurd dollar package. The salaries paid to the executive directors are conservative by listed-company standards — base remuneration in the range of about ₹40-something lakh per annum for the brothers, with the upside tied to a commission capped at roughly 1% of net profits.2 By Mumbai or Bengaluru CEO standards, this is almost laughably modest. It tells you exactly where the family thinks its wealth lives. Not in the salary line. In the equity.

The promoter shareholding sits steady around the high-thirties percentage — close to 39% — and has been remarkably stable for years.2 There is a pledge component, which we will flag in the bear case later, but the gross shareholding has not been diluted aggressively. Even the 2024 QIP, which brought in around ₹350 crore of fresh capital, was structured to fund growth without forcing the family to sell down meaningfully.[^4]

Now, capital allocation. This is where the family's character expresses itself most cleanly. There are three big buckets to look at.

The first is acquisitions. Ganesha Ecosphere has made selective M&A moves — the most notable being the acquisition of Ganesha Overseas, a washing plant in Nepal that gave the company access to feedstock from a geography where the formal recycling supply chain was even thinner than in India.[^14] But there is a striking absence of large, hubristic domestic acquisitions. The Sharmas have repeatedly chosen greenfield expansion — Warangal in Telangana, the new Odisha facility — over buying out competitors. The reasoning, articulated in various investor settings, is that domestic targets are priced too high relative to the cost of building fresh capacity, and that greenfield gives you exactly the technology stack you want rather than someone else's legacy machinery.[^8]

The second is technology capex. The 2024 capex programme of roughly ₹750 crore, partly funded by the QIP, was deliberately weighted toward food-grade rPET capacity rather than additional rPSF.1[^4] This is the strategic chess move that will define the next decade — moving company-level margins from the steady, thin-margin textile feedstock business into the higher-margin, regulation-driven food-grade resin business.

The third is working capital and balance sheet discipline. The company has historically run with modest debt, sufficient operating cash flow to fund maintenance capex, and a willingness to slow expansion when feedstock or end-product pricing turns adverse. There is no swashbuckling acquirer here. There is, instead, a family that watches the cost of every bale of bottles coming in the gate.

If you want a single image to remember the Sharma capital allocation philosophy by, it is this: they prefer to spend ₹100 crore on a new wash line in Odisha that they will run themselves for thirty years, over spending ₹150 crore acquiring a competitor whose technology they will have to rip out and replace. It is, in other words, a builder's mindset rather than a deal-maker's. That mindset will matter enormously as the next chapter — the food-grade rPET pivot — unfolds.

V. The "Hidden" Business: Go Rewise & Food-Grade rPET

For most of its history, the part of Ganesha Ecosphere that the market knew about was the textile fibre business. Predictable, somewhat boring, a workhorse generating cash. But buried inside the company, slowly being built and capitalised through the late 2010s and early 2020s, was something more interesting: a food-grade recycled PET resin business that would, if it scaled the way management believes it could, fundamentally reprice the entire stock.

The catalyst was a brand launch in November 2022. Ganesha unveiled "Go Rewise", a new umbrella identity for its bottle-grade and food-contact rPET output.2 At first glance, this looked like just another corporate sub-brand. In substance, it was the public coming-out of a multi-year industrial project to install European super-clean recycling technology at scale on Indian soil.

A short tutorial, because this matters and is genuinely interesting. Recycling a PET bottle into a t-shirt fibre is, in industrial terms, relatively forgiving. The end product will be dyed, woven, stitched, washed; minor impurities are tolerable. Recycling a PET bottle into another PET bottle — bottle-to-bottle — is dramatically harder. The new bottle will hold a beverage that a human will drink. The recycled resin must be free of contaminants at near-virgin levels. It must meet the food-contact migration standards set by the US Food and Drug Administration and the European Food Safety Authority. The polymer chains must be lengthened back, via solid-state polymerisation, to match the intrinsic viscosity of virgin chips. The whole process is, in effect, taking a contaminated post-consumer feedstock and producing a clinical-grade output.

The machinery that does this at scale is essentially a duopoly globally — Erema and Starlinger, both Austrian. Ganesha chose Starlinger.[^8] Why Starlinger matters: the Starlinger "iV+" line uses a continuous high-vacuum decontamination process that scrubs residual contaminants out of the melt at the molecular level. It is not cheap. A single full line costs a meaningful fraction of a year's free cash flow. And it is the gate through which a recycler has to pass to be allowed, by law and by FDA letter of non-objection, to sell food-grade pellets to Coca-Cola or PepsiCo or Bisleri.

Ganesha cleared the gate. By 2023, its food-grade rPET facility — initially at Warangal — was operational, with USFDA letters of non-objection and EFSA approvals in hand.[^8] Then the second leg of expansion began in Odisha, designed to substantially scale the bottle-to-bottle capacity through 2025 and 2026.1

The margin economics are the part that should make a long-term investor sit forward in their chair. Textile-grade rPSF in India sells, broadly, in the ₹95-110 per kilo range, depending on grade and feedstock costs. Food-grade rPET resin commands ₹140+ per kilo on the same feedstock base.[^7] That is roughly a 30-40% revenue uplift on the same input bottle, with somewhat — but not proportionally — higher processing costs. Net of incremental opex, the EBITDA margin on a kilo of food-grade rPET resin can be roughly double that of textile-grade fibre. Same feedstock. Same family. Same factory district. Dramatically different unit economics.

Let us segment the business as it stands now, in mid-2026. The first segment, rPSF for textiles, remains the cash cow — high volumes, steady demand, captive customer base in the Indian and export apparel industry. The second segment, rPET chips for packaging — the Go Rewise franchise — is the high-growth engine, where regulatory tailwinds and FMCG procurement contracts will drive volume through the late 2020s. The third segment, filament yarn, is the value-added downstream play — converting some of the recycled chip into woven-ready filament for technical textiles, automotive interiors, and home furnishings.2

The key conceptual point for an investor: this is no longer a single-product company. It is a three-segment chemicals-and-materials franchise where the segments share a feedstock — the discarded bottle — but diverge sharply in pricing, customer profile, and growth trajectory.

There is a useful analogy here, borrowed from the semiconductor industry. The bottle is the wafer. The wash-and-flake line is the foundry's front end. The polymerisation-and-pelletisation line is the back end. And the three end-products — fibre, food-grade chip, filament — are different SKUs sold into different customer geographies at different price points. The factory does not care which one you order. The strategic question, year by year, is what mix the company chooses to produce.

The mix is shifting toward food-grade. And every percentage point of mix shift drops disproportionately to the bottom line. This is the engine investors are paying for. It is also why the next chapter — regulation — is so important. Because without the tailwind of mandatory recycled content, all of this Austrian capex would be a bet on goodwill alone.

VI. Regulatory Tailwinds: EPR & The Supply Chain Moat

In February 2022, the Indian Ministry of Environment, Forest and Climate Change notified the Plastic Waste Management (Amendment) Rules, which formalised the country's विस्तारित उत्पादक उत्तरदायित्व Extended Producer Responsibility framework for plastic packaging.[^7] Read in a Delhi conference room, it sounded like another bureaucratic document. Read inside the Ganesha Ecosphere boardroom in Kanpur, it sounded like a starting gun.

Here is what the rules did, stripped of legalese. They told every brand that puts plastic packaging into the Indian market — Coca-Cola, Pepsi, Bisleri, Hindustan Unilever, Britannia, Dabur, everyone — that they would be legally responsible for collecting back and recycling a defined percentage of that plastic, on a graduated schedule that ramps up year by year. By 2025-26 financial year, rigid PET packaging was required to incorporate 30% recycled content. The schedule then steps up further toward 60% over subsequent years through the late 2020s.[^7] If a brand failed to meet the obligation, it would have to pay an environmental compensation charge — effectively a fine that, by design, was set high enough to make compliance cheaper than non-compliance.

In one stroke, the regulation converted recycled PET resin from a discretionary procurement item — bought by virtuous Western brands and reluctantly by domestic ones — into a regulatory necessity. The buyer's question shifted from "should we use rPET?" to "where, urgently, do we source the certified rPET volume we are now legally required to embed in our packaging?"

There is a sub-clause in the EPR architecture that matters even more for Ganesha. The certification chain. To count as compliant recycled content under the EPR rules, the resin has to be sourced from a registered recycler, with traceable feedstock, and with audited yield ratios. A brand cannot simply buy generic rPET from an unlicensed processor and claim credit. The certification regime — the EPR credit market — created an entirely new asset class: verifiable recycling credits, attached to the physical resin sold, traded between obligated brands and approved recyclers.

This is the second leg of the moat. The first is the sourcing network. The second is the certification position. Together, they create something that is genuinely hard to copy in any plausible 24-to-36-month window.

Let us go deeper on the sourcing piece, because this is the part of the Ganesha story that gets least attention and matters most.

India does not have municipal kerbside recycling. There is no green bin program. There is no neighbourhood truck that comes by on Wednesdays to pick up sorted plastics. Instead, India has the kabaadi network — roughly 1.5 to 4 million informal waste workers spread across the country, organised in a loose pyramid: the ragpicker at the bottom who walks landfills and streets, the small aggregator (the "godown" operator) in the middle who buys from a few hundred ragpickers, and the large dealer at the top who consolidates from many godowns and sells, in truckloads, to the recyclers. The system is informal, cash-based, often unrecorded, and absolutely remarkable in its efficiency. It moves millions of tonnes of recyclable material per year on essentially zero formal infrastructure.

Ganesha plugs into this system through a network reported to include more than 300 scrap dealers across roughly 32 states and union territories.[^6] That number sounds modest. It is not. Each of those dealers is a node that aggregates from dozens or hundreds of micro-aggregators below them, who in turn aggregate from thousands of ragpickers. The effective reach is in the millions of human collectors.

What makes this a Hamilton Helmer-style "Cornered Resource" is not the count of dealers but the duration of the relationships. The Ganesha sourcing team has, in many cases, worked with the same families of dealers for two decades. The pricing trust, the credit terms, the dispute resolution norms — all of it is unwritten and culturally embedded. A new entrant cannot walk in with a higher offer and pull the supply away, because the relationship is not purely transactional. It is a long-tenured trade network with the loyalty profile of a Marwari trading guild.

This is precisely why the joint venture with RACE Eco Chain matters strategically. RACE — operating across the formal collection layer — brings additional sourcing reach in the more "organised" segments of the waste stream, including bulk collection from large institutions, malls, airports, and corporates that prefer to deal with a registered counterparty.3 The Ganesha-RACE structure layers formal collection on top of the informal kabaadi base. The combined network is wider, deeper, and harder to disintermediate than either piece alone.

The implication for the moat. As EPR enforcement tightens and as demand for compliant recycled content rises faster than supply, the price-setting power in the chain migrates upstream — toward whoever controls the feedstock. The companies that own the bottle access, not just the wash lines, will earn the rents. That is, by happy coincidence and three decades of patient relationship building, exactly where Ganesha sits.

VII. Playbook: Porter's 5 Forces & Hamilton's 7 Powers

Let us turn the analytical lens up a notch and walk the Ganesha story through the two frameworks that long-term investors most often reach for: Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces. Not as an academic exercise — but because the frameworks force precision about what, exactly, would have to be true for the moat to widen, hold, or erode over the next decade.

Start with 7 Powers. The first and most obvious is Cornered Resource. We have just walked through it: the kabaadi sourcing network, the dealer relationships, the cultural embedding of trust and credit terms.[^6] In Helmer's strict definition, a cornered resource is access to a coveted asset on terms not available to others. The Ganesha access is not legally exclusive — there are no signed exclusivity contracts with ragpickers — but in practice, it is sticky in a way that capital alone cannot replicate. A would-be competitor in Mumbai trying to enter PET recycling at scale tomorrow could buy the same Starlinger line that Ganesha bought; what they could not buy was thirty years of dealer Diwali greetings and credit forbearance during the GST transition.

The second power is Process Power. Recycling PET sounds simple — wash, shred, melt, pelletise — but the yield curve is brutal. The difference between a wash line that delivers 88% useable flake from a given bottle bale, versus one that delivers 79%, is the difference between making money and losing money on the kilo. Those yield improvements come from thousands of small operational tweaks accumulated over years — slight changes to wash chemistry, conveyor speeds, sorting algorithms, dryer residence times. They are not patentable. They are not documented in a manual. They live in the heads of plant supervisors. Ganesha has been refining its process for over thirty years. A new entrant starts at 79%.

The third power, and one of the most under-appreciated, is Counter-Positioning. This is the Helmer concept that an incumbent cannot fully respond to a challenger because doing so would cannibalise their own existing business. Apply it here: the virgin polyester industry in India is dominated by Reliance, with Indorama, JBF, and a few smaller players. For Reliance to pivot aggressively into recycled PET would mean undermining the demand for its own virgin chip output. Every kilo of rPET that displaces virgin PET in a Coke bottle is a kilo of revenue lost from the petrochemical complex at Jamnagar. The incumbents can dabble in recycling — they cannot whole-heartedly attack the recycled segment without internal civil war. Ganesha, with no virgin business to protect, is unambiguously a "pure-play" recycler. Its incentives are perfectly aligned with the regulatory direction of travel. The incumbents' are not.

The fourth power worth flagging is Switching Costs, modest but real. For an FMCG brand that has gone through the trouble of certifying Ganesha's resin under its product specifications, has run multiple commercial batches, and has built a procurement workflow around the Ganesha grades, switching to a new recycler is a non-trivial undertaking. Certification cycles take months. Quality regression risks are real. Procurement teams, like all procurement teams everywhere, prefer the devil they know.

Now Porter's 5 Forces. Bargaining power of buyers: structurally low, and getting lower. The EPR rules have created a captive demand profile in which FMCG giants must buy a defined volume of certified recycled content. The buyer cannot credibly walk away.[^7]

Bargaining power of suppliers: rising. This is the bear-case side of the moat. As waste becomes a recognised valuable commodity, the kabaadi network is, slowly, formalising and pricing itself more aggressively. Bottle prices at the godown gate are higher in 2026 than they were in 2020. The supplier side is moving from "we are happy to be paid anything" to "we know our value". Ganesha's response — the JV with RACE, the equity-or-loyalty-style arrangements with key dealers — is precisely an attempt to manage this rising supplier power.3

Threat of substitutes: theoretically present, practically diminishing. Virgin polyester is the obvious substitute — same physical performance, often slightly cheaper on a pure cost-per-kilo basis. But the regulatory penalty for under-compliance with EPR makes virgin substitution increasingly expensive over the planning horizon.[^7] Glass and aluminium exist as alternative beverage packaging, but they trade off cost and weight in ways that make them niche rather than displacement threats.

Threat of new entrants: this is the one to watch most closely. Capital is not the barrier — a Mumbai family office can write the cheque for a Starlinger line. The barrier is the sourcing network and the certification position. Both take years to build. The combination of EPR enforcement (which raises demand) and informal-supply consolidation (which makes feedstock harder to access for newcomers) makes the entrant's ramp particularly painful.

Industry rivalry: moderate but increasing. The number of EPR-certified PET recyclers in India has grown materially since the rules came in. But the certified-and-at-scale subset — players who can deliver multi-thousand-tonne contracts to a large FMCG buyer — remains small. Ganesha is among the largest in that subset, alongside a handful of regional peers.

Synthesising: Ganesha sits at an unusually favourable point in its industry structure. The buyer side is captive. The supplier side, while rising in power, is being actively managed. The substitute and entrant sides are constrained by regulation and by the cornered-resource moat. The rivalry side is the main locus of competitive risk — and that is precisely where management's investment in food-grade capacity is meant to create separation.

VIII. Analysis: Bull Case, Bear Case, and the KPIs That Matter

We have now built up enough context to walk the bull and bear scenarios with discipline. Long-term fundamental investors care less about quarter-to-quarter print and more about whether the structural story holds. So let us do exactly that.

The bull case. Start with the demand backdrop. The EPR ramp from 30% recycled content in 2025-26 to 60% over the back half of the decade implies a multi-fold expansion in required volumes of certified rPET across the Indian FMCG sector.[^7] That demand is regulatory, not discretionary. Now lay on top of it the global commitments by Coca-Cola, Unilever, PepsiCo, and others to recycled content targets in their global packaging mix — commitments that, while voluntary, are tracked by activist investors and ESG funds. The total addressable market for food-grade rPET in India, on these tailwinds, is on a steep curve.

Against that demand backdrop, Ganesha has assembled a supply-side position that is structurally hard to displace. The Warangal food-grade line is operational. The Odisha facility is commissioning through 2025-26.1 The sourcing network is in place. The certifications — USFDA, EFSA — are in hand.[^8] Capacity utilisation, as the Odisha line ramps, will swing margins meaningfully. The mix shift from rPSF to rPET resin lifts blended EBITDA margin into a higher band than the historic textile-only profile.

The "Indorama of India" comparison is worth dwelling on, briefly. Indorama Ventures, the Thai-listed petrochemicals group, took a strategic decision a decade ago to lean heavily into recycling, including bottle-to-bottle. Its share of revenue from recycled product has climbed steadily, and the segment commands a margin premium that has supported group multiples. The Ganesha bull case is essentially that Indian-listed recycling, with the EPR regulatory tailwind and a Cornered Resource moat that Indorama does not have access to in India, can produce a comparable mix shift over the next decade with materially higher unit economics.

Now the bear case. Pick this up carefully because the risks are real and worth respecting.

First, feedstock cost. The same rising EPR demand that lifts Ganesha's selling prices also lifts the bid for raw bottles. Bottle prices at the dealer gate have been moving up. If they move up faster than rPET selling prices — which is plausible if multiple new recycling capacities come online simultaneously chasing limited feedstock — the margin compression is on the input side.

Second, the promoter pledge. A non-trivial portion of the promoter shareholding has historically been pledged.[^11] This is not, in itself, a sign of distress — pledges are commonly used by Indian promoter families to fund expansion, personal liquidity, or family settlements — but it is a structural overhang. In a sharp share price drawdown, pledged shares can trigger forced sales, which can cascade. Investors should track the pledge percentage as a continuous variable, not a one-time check.

Third, execution risk on the Odisha ramp. Greenfield capex projects in India routinely slip on timeline. The Odisha plant is the company's largest single capacity addition in years. Delays in commissioning, ramp-up to nameplate utilisation, or first-pass yield issues on the new line would push out the margin uplift.

Fourth, competitive entry at the high end. As the food-grade rPET segment becomes visibly profitable, larger competitors — including the recycling arms of integrated petrochemical players — will be tempted to step up their investment. The Counter-Positioning power we discussed limits the speed of this entry but does not eliminate it.

Fifth, raw economic sensitivity. Ganesha sells into FMCG and textile customers whose volumes flex with consumer demand. A meaningful slowdown in Indian consumption would soften order books even with the EPR floor in place.

Sixth, the second-layer diligence overlay. Watch the auditor's notes carefully each year for changes in revenue recognition on EPR credits — the accounting treatment of certificate-style revenue is still evolving, and any restatement risk would show up there first. Watch also for any change in the related-party transaction profile around the Nepal subsidiary or future JVs; small disclosures here can reveal a lot about governance discipline.

Three KPIs to track ongoing. Long-term investors should resist the temptation to track twenty metrics and instead focus on the small number that genuinely move the thesis.

The first is the food-grade rPET mix as a percentage of total sales volume. This is the single most important variable for blended EBITDA margin. If the mix moves from the current low-double-digit percentage toward 40-50% of volumes by the late 2020s, the company's earnings power steps up substantially. If it stalls, the textile-fibre profile dominates.

The second is feedstock cost per kilo of finished output. This is the input-side variable. A widening spread between feedstock and selling price implies the moat is doing its job. A narrowing spread implies competitive pressure on supply.

The third is capacity utilisation at the new food-grade lines, particularly Odisha as it ramps.1 Capex-heavy projects only earn their cost of capital when utilisation crosses the threshold. This is the most direct read on whether the ₹750-crore programme is delivering on its return-on-capital pitch.

These three numbers, watched in tandem over the next eight quarters, will tell the long-term investor more about the trajectory of Ganesha Ecosphere than any quarterly profit beat or miss.

A brief myth-versus-reality. The consensus narrative on Ganesha tends to focus on "ESG winner" and "circular economy play". The reality is that the moat is not the ESG branding — it is the Marwari trading network in Kanpur that funnels bottles to the gate. The branding monetises the moat; it is not the moat itself.

IX. Epilogue

Back to the railway siding outside Kanpur. The tempo truck has long since unloaded and rumbled back toward the highway. The bottles are now flakes; the flakes are about to become pellets; some of the pellets will be in Coke bottles, some in Decathlon t-shirts, some in the carpeting of a Maruti Suzuki cabin. The kabaadi who picked the original bottle off the Patna sidewalk is, somewhere in the supply chain, twenty rupees richer than he was yesterday.

There is a phrase in Hindi that the Sharma family is fond of in their investor communications: कचरे से कंचन — "wealth from waste". It is the kind of phrase that, in another business, would feel like marketing. Here, it is just description. The company has, for thirty-two years, taken the most overlooked and devalued material in the Indian economy and turned it into a polymer that ends up in the supply chains of the largest consumer brands in the world. The arithmetic is the strategy. The strategy is the moat. The moat is human, cultural, and slow to build — which is precisely why it is hard to replicate.

What should an investor watch in the next twenty-four months? Three concrete things. The commissioning of the Odisha plant, on time and at nameplate yield. The signing of named long-term offtake contracts with the major FMCG and beverage brands for the Go Rewise resin. And the first publicly-visible 100% recycled Coke bottle on an Indian shelf — a symbolic milestone, perhaps, but one that will tell a lot about how quickly the regulatory ambition turns into commercial reality.

The deeper question is whether Ganesha can sustain its founder-builder culture as it transitions from a regional Kanpur business into a national-scale specialty chemicals franchise. The Sharma brothers have so far kept the family's frugal, plant-floor-oriented DNA intact even as the balance sheet has grown by an order of magnitude. The next decade will test whether that culture survives professionalisation, the addition of expatriate technical talent, and the inevitable noise of being a market-cap stock that institutional funds want to own and have opinions about.

The smart money will keep its eyes on three places. The wash line in Odisha. The bottle bid at the godown gate in Gwalior. And the silent, patient arithmetic of a family business in Kanpur that figured out, three decades before anyone else in India, that the most valuable molecule in the country was the one being thrown into a drain.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube