Firstsource Solutions: The BPO Phoenix - From ICICI's Experiment to RPSG's Global Ambition

I. Introduction & Episode Roadmap

Picture this: It's October 2012, and in a boardroom overlooking Mumbai's financial district, Sanjiv Goenka is about to sign a deal that his advisors think is madness. The target? A debt-laden BPO company bleeding cash, with ₹2,200 crore in debt and clients jumping ship. The seller? ICICI Bank, desperate to offload what had become their most painful non-core asset. The price tag? About ₹650 crore for a 49.5% stake in a company many considered beyond salvation.

Fast forward to today, and that same company—Firstsource Solutions—commands a market capitalization of over ₹25,000 crore, serves Fortune 500 clients across four continents, and has become the crown jewel in the RP-Sanjiv Goenka Group's services portfolio. With annual revenues touching ₹8,400 crore and operations spanning banking, healthcare, and technology sectors across 10 countries, Firstsource represents one of India's most dramatic corporate turnaround stories.

But this isn't just a turnaround tale. It's the story of how India's BPO industry evolved from Y2K opportunism to AI-powered transformation, told through the lens of one company that nearly died trying. It's about conglomerate rescue economics, the art of buying distressed assets, and what happens when old-economy capital meets new-economy ambition.

The central question we're exploring: How did a struggling ICICI Bank experiment in business process outsourcing transform into a $3 billion global BPM powerhouse? And more importantly, what does Firstsource's journey tell us about the future of India's services economy in an AI-disrupted world? Today, with ₹25,951 crore market capitalization and ₹8,407 crore in revenue, Firstsource stands at a fascinating inflection point. The company recently achieved US$1 billion annualized revenue run-rate—a milestone that seemed impossible during its darkest days. As we dive into this saga, we'll uncover how patient capital, strategic focus, and the willingness to embrace transformation can resurrect even the most troubled assets. Let's begin where all great Indian BPO stories must: at the turn of the millennium, when Y2K fears created an industry.

II. The ICICI Bank Origins & India's BPO Dream (2001-2006)

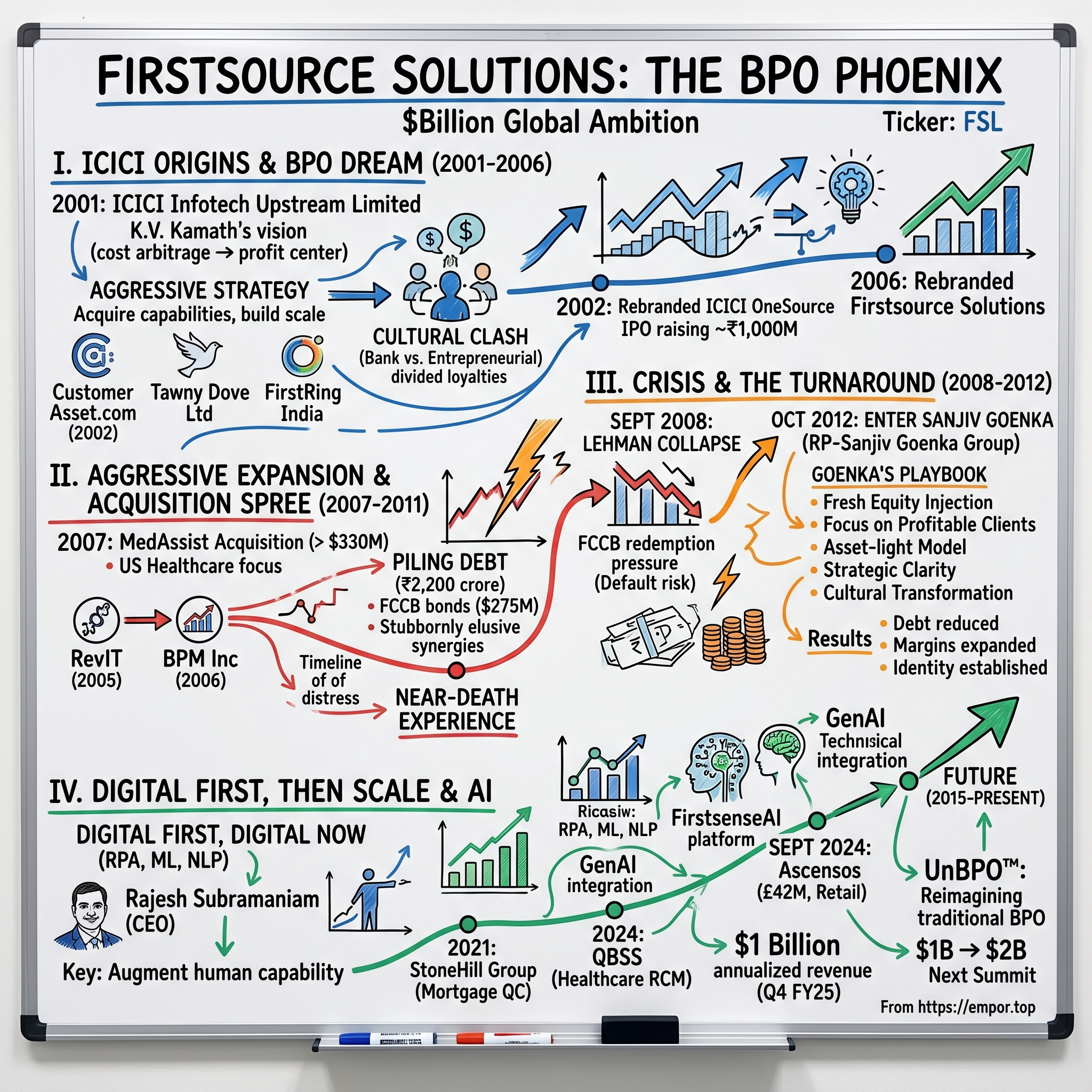

December 6, 2001. The Twin Towers had fallen just three months earlier, global markets were in turmoil, and yet in Mumbai's Bandra Kurla Complex, ICICI Bank's leadership was placing a massive bet on India's services future. The bank registered ICICI Infotech Upstream Limited—not just another subsidiary, but a declaration that India's largest private bank believed the country's BPO opportunity was too big to miss.

The timing was deliberate. India had just emerged as the unlikely hero of the Y2K crisis, with thousands of Indian programmers saving Western corporations from digital apocalypse. The country's reputation had transformed overnight from back-office destination to trusted technology partner. Suddenly, every Fortune 500 CEO knew that Indian engineers could deliver mission-critical work at a fraction of Western costs.

K.V. Kamath, then CEO of ICICI Bank, saw an opportunity that went beyond mere cost arbitrage. The bank was processing millions of transactions daily, fielding customer calls round the clock, managing collections across the country. Why not turn this internal capability into a profit center? Better yet, why not build a platform that could serve other banks and financial institutions globally?

By April 2002, the company had been renamed ICICI OneSource—a more marketable identity that signaled its ambitions beyond captive operations. The early strategy was aggressive: acquire capabilities, build scale, establish credibility. The acquisitions came fast and furious. Customer Asset.com in 2002 brought customer acquisition expertise. Tawny Dove Ltd added UK presence. FirstRing India in 2003 expanded domestic reach.

But here's where the cultural clash began to surface. ICICI Bank's DNA was risk management, regulatory compliance, and conservative growth. The BPO world demanded something entirely different—entrepreneurial hustle, 24/7 operations, and the ability to manage thousands of twenty-somethings working graveyard shifts serving customers halfway across the world. The bank's traditional managers struggled to adapt to this new reality where a missed service level agreement could mean losing a multimillion-dollar contract overnight.

The 2002 IPO on BSE and NSE raised approximately ₹1,000 million, providing fuel for expansion. The capital markets loved the story—here was ICICI Bank, India's most innovative private bank, entering the hot BPO sector. The stock was oversubscribed, valuations were generous, and the future seemed limitless.

Yet beneath the surface, fundamental questions remained unanswered. Could a bank-promoted BPO really compete with pure-play operators like Genpact (GE's former captive) or WNS (British Airways' spin-off)? These competitors had deeper domain expertise, longer client relationships, and most importantly, no divided loyalties between serving parent company needs and external client demands.

By 2005, another strategic shift was underway. The company acquired Pipal for research capabilities and ASG for collections and receivables management. Each acquisition added capabilities but also complexity. Integration challenges mounted, cultures clashed, and the debt burden began to grow. The company was trying to be everything to everyone—serving banking, healthcare, telecom, and retail clients across multiple geographies.

The November 2006 rebranding to Firstsource Solutions Limited marked more than a name change. It was an acknowledgment that the ICICI association, while providing initial credibility, was becoming a limitation. Global clients wanted an independent partner, not a subsidiary of an Indian bank. The new identity promised a fresh start, but the structural challenges remained. The stage was set for an ambitious expansion that would nearly destroy the company.

III. The Aggressive Expansion & Acquisition Spree (2004-2011)

The conference room at the Waldorf Astoria in New York, August 2007. Ananda Mukerji, then CEO of Firstsource, is about to sign the biggest deal in the company's history. Across the table sit the owners of MedAssist, one of America's leading healthcare revenue cycle management companies. The price tag: over $330 million. For context, this was more than Firstsource's entire annual revenue at the time.

The MedAssist acquisition was audacious, transformative, and in hindsight, nearly fatal. But in that moment, it represented everything Firstsource wanted to be—a global player with deep domain expertise, serving the world's most complex and lucrative market: US healthcare.

The healthcare BPO opportunity was irresistible. American hospitals were drowning in paperwork, insurance claims, and regulatory compliance. The average hospital had 30-40% of claims initially rejected by insurers. Revenue cycle management—the byzantine process of getting paid for healthcare services—was becoming impossibly complex. Here was a $50 billion addressable market growing at 15% annually, and Firstsource wanted its piece.

MedAssist brought 5,000 employees, relationships with over 400 US hospitals, and most crucially, domain expertise that would take decades to build organically. The company processed over $10 billion in healthcare claims annually. This wasn't just data entry or call center work—it required deep understanding of CPT codes, insurance policies, Medicare regulations, and the endless complexity of American healthcare.

But the acquisition strategy went beyond healthcare. Between 2004 and 2011, Firstsource was on a buying spree that would make private equity firms jealous. RevIT in 2005 added more healthcare capabilities. BPM Inc in 2006 enhanced the platform. Each deal was justified with ambitious synergy projections and growth assumptions.

The debt was piling up faster than anyone realized. By 2008, Firstsource had over ₹1,500 crore in debt, heading toward ₹2,200 crore. The company had issued Foreign Currency Convertible Bonds (FCCBs) worth $275 million, betting that its stock price would rise enough for bondholders to convert to equity. It was a dangerous game that assumed perpetual growth and ever-rising valuations.

Revenue was indeed growing—from ₹10.35 billion in FY2005-06 to ₹12.45 billion by FY2011-12. But profitability was another story. Integration costs were massive. American employees were expensive. Healthcare clients demanded constant investment in technology and compliance. The promised synergies remained stubbornly elusive.

Meanwhile, the competitive landscape was intensifying. Genpact had gone public in 2007 with a $2.4 billion valuation. WNS was growing rapidly through its own acquisitions. EXL Service was carving out profitable niches. Every major Indian IT company—TCS, Infosys, Wipro—was entering the BPO space. Global players like Accenture and IBM were building massive offshore operations.

The geographic expansion added another layer of complexity. Firstsource now had operations in the US, UK, Philippines, and India. Each country had different labor laws, tax structures, and operational challenges. The Philippines operation was crucial for voice support—Filipino accents were more neutral to American ears than Indian ones. But managing facilities across time zones, cultures, and regulatory regimes was proving harder than anticipated.

Cultural integration was perhaps the biggest challenge. MedAssist's American employees viewed their Indian acquirers with skepticism. They had built deep relationships with hospital CFOs over decades. Would these clients trust an Indian company with their most sensitive financial operations? The answer, initially, was mixed. Some clients stayed, drawn by promises of lower costs and improved technology. Others left, uncomfortable with the ownership change.

The technology platform was another headache. Each acquisition brought its own systems, processes, and tools. Integration was supposed to create economies of scale. Instead, it created a technological Tower of Babel where different parts of the organization couldn't talk to each other. Client data was siloed, reporting was inconsistent, and the promised "single view of operations" remained a distant dream.

By 2011, the cracks were showing. Margins were under pressure from wage inflation in India and the Philippines. Healthcare reform in the US was creating uncertainty. The European debt crisis was affecting UK clients. And most ominously, those FCCBs were coming due for redemption. The stock price hadn't risen as expected—in fact, it had fallen. Bondholders would want their money back in cash, not equity. The stage was set for a crisis that would bring Firstsource to its knees.

IV. The Crisis Years & Near-Death Experience (2008-2012)

September 15, 2008. Lehman Brothers collapses. Within hours, Firstsource's largest financial services clients are calling emergency meetings. Contracts are being reviewed, budgets slashed, entire projects cancelled. In the Firstsource war room in Mumbai, CFO Dinesh Jain is staring at spreadsheets that get worse with each refresh. The company has $275 million in FCCBs coming due, ₹2,200 crore in total debt, and clients are disappearing by the day.

The global financial crisis hit BPO companies with particular ferocity. Banks, their biggest clients, were fighting for survival. Discretionary spending vanished overnight. Worse, the very premise of outsourcing was being questioned. Politicians in the US and UK were demanding jobs be brought back home. "Bangalore" had become a dirty word in American political discourse, shorthand for job losses and corporate greed.

For Firstsource, the timing couldn't have been worse. The MedAssist acquisition had been funded largely with debt, assuming healthcare revenues would service the obligations. But hospitals, facing their own financial pressures, were delaying payments, renegotiating contracts, and in some cases, bringing work back in-house. The revenue projections that justified the acquisition were now fantasy.

The FCCB redemption pressure was existential. These bonds, issued when Firstsource stock was trading at ₹40+, had a conversion price that now seemed laughable as the stock plummeted below ₹10. With conversion impossible, Firstsource would need to find $275 million in cash—money it simply didn't have. The bonds were due in 2011 and 2012. Default would mean bankruptcy.

Inside the company, morale was collapsing faster than the stock price. Employees watched their stock options become worthless. The best performers were getting calls from competitors. Client-facing teams were spending more time explaining Firstsource's financial situation than delivering services. Every news article about the company's troubles made the next client conversation harder.

The numbers tell the story of corporate distress: Revenue growth slowed to single digits. EBITDA margins, once above 15%, fell below 10%. Interest coverage ratios turned negative. The company was burning cash just to stay alive. By 2011, accumulated losses had wiped out most of the net worth.

ICICI Bank, the parent, faced its own dilemma. The bank had already invested hundreds of crores. Throwing good money after bad seemed foolish. But letting Firstsource fail would be a massive reputational hit. The bank's board was divided. Some directors wanted a quick sale to cut losses. Others believed the underlying business had value if the debt could be restructured.

Management musical chairs began. Senior executives departed with increasing frequency. The CEO position became a revolving door. Each new leader promised a turnaround, unveiled a transformation plan, and then left when reality hit. Clients began inserting "change of control" clauses in contracts, giving them the right to terminate if ownership changed—making any potential sale even more complicated.

The search for a white knight began in earnest by 2011. Investment bankers pitched the company to anyone who would listen. Private equity firms took meetings but balked at the debt. Strategic buyers liked the client relationships but not the obligations. Indian IT companies were interested but wouldn't pay enough to satisfy creditors. International BPO firms had their own problems.

The employee exodus accelerated. In the Philippines center, attrition hit 100% annually—the entire workforce was turning over every year. Training costs skyrocketed. Service levels plummeted. Clients who stayed demanded price reductions to compensate for declining quality. It was a death spiral: less revenue meant less investment in people and technology, which meant worse service, which meant even less revenue.

By early 2012, the situation was desperate. Suppliers were demanding cash on delivery. Landlords were threatening eviction. The Reserve Bank of India was asking uncomfortable questions about loan classifications. The stock price had fallen over 90% from its peak. Market capitalization was now less than the debt—equity was essentially worthless.

Then, unexpectedly, a call came from Kolkata. Sanjiv Goenka, chairman of the newly formed RP-Sanjiv Goenka Group, was interested. His conglomerate had just split from his brother's faction. He needed to build his own identity, create new growth engines. A distressed BPO company seemed an unlikely choice, but Goenka saw something others missed. The story of how a power sector tycoon saved a dying BPO would become legend in Indian corporate circles.

V. Enter Sanjiv Goenka: The Turnaround Architect (2012-2014)

The Oberoi Grand Hotel, Kolkata, July 2011. Sanjiv Goenka sits alone in the colonial-era tea lounge, nursing his third cup of Darjeeling, contemplating what many would call career suicide. Just days earlier, on July 13, the formal split of RPG Enterprises had been announced. His brother Harsh would keep the Mumbai operations—the glamorous businesses like CEAT Tyres and Zensar Technologies. Sanjiv got the Kolkata assets: the unglamorous power utility CESC, carbon black manufacturer PCBL, and a struggling retail chain.

At 50, Goenka was starting over. The split gave him assets worth about $2 billion, but they were old-economy, capital-intensive businesses in a market obsessed with technology and startups. He needed something transformative, something that would announce the RP-Sanjiv Goenka Group as a force independent of his family's legacy. A struggling BPO company seemed an unlikely candidate, but Goenka had always trusted his gut over spreadsheets—a trait inherited from his father, who famously said, "I have never looked at the balance sheet of any company I took over. It was pure gut-feel and I never went wrong. The moment I ignored the gut reaction, I made a mistake."

The October 2012 acquisition of Firstsource for Rs 400 crore wasn't just about buying a BPO company. Through his flagship CESC Limited's subsidiary SpenLiq, Goenka acquired a 49.5% stake, valuing Firstsource at approximately ₹800 crore—a fraction of its peak valuation. But the real story was what happened next.

Goenka's first move was counterintuitive: instead of cost-cutting, he injected fresh equity. The debt burden that was crushing Firstsource needed immediate attention. Foreign lenders were circling like vultures. Indian banks were classifying loans as non-performing. The company needed someone who could write large checks without flinching. Goenka could, and did.

The turnaround philosophy was elegantly simple: focus on profitable clients, exit unprofitable contracts regardless of size, and transform the asset ownership model. Under previous management, Firstsource had accumulated real estate and infrastructure assuming ownership meant control. Goenka flipped this thinking entirely. Why own buildings when you could lease? Why buy servers when you could rent cloud capacity? The balance sheet transformation was dramatic—assets became lighter, cash flows improved, and suddenly the debt didn't look so overwhelming.

The client portfolio surgery was brutal but necessary. Firstsource was servicing over 100 clients, many of whom were unprofitable. The Pareto principle was stark—20% of clients generated 80% of profits, while the bottom 30% were actually destroying value. Previous management had been too afraid to fire clients. Goenka wasn't. Within months, dozens of contracts were terminated or not renewed. Revenue dropped initially, but margins expanded dramatically.

Employee morale, surprisingly, improved under the new regime. Goenka brought something previous owners hadn't: certainty. RPSG wasn't going anywhere. There would be no more speculation about bankruptcy or fire sales. He personally visited facilities in the Philippines and the US, something ICICI executives rarely did. He ate in the employee cafeterias, worked a few hours in the call centers, and most importantly, listened.

The debt reduction was methodical and impressive. From ₹2,200 crore at acquisition, it fell to $125 million (approximately ₹751 crore) within two years. This wasn't financial engineering—it was operational improvement driving cash generation. The FCCB crisis that had threatened corporate extinction was resolved through a combination of repayment and restructuring.

Since acquiring Firstsource, the RP-SG Group actively worked towards improving the company's financials. The firm's EBIT margins expanded from 6.6 percent in FY13 to 10.7 percent in FY17. The transformation was remarkable: FY2014 saw revenues of ₹3,105.9 crore (10.2% growth) and PAT of ₹193 crore (31.6% growth).

But perhaps Goenka's greatest contribution was strategic clarity. Firstsource would no longer try to be everything to everyone. It would focus on three verticals: Banking & Financial Services, Healthcare, and Communications. Within these, it would go deep, not broad. The company would build domain expertise that competitors couldn't easily replicate. This wasn't about being the cheapest—it was about being indispensable.

The cultural transformation was equally important. The RPSG ethos—entrepreneurial, patient, relationship-focused—gradually replaced the banking bureaucracy of the ICICI era. Goenka instituted a simple rule: every senior executive must spend at least one week annually working in delivery centers. No ivory towers, no disconnection from ground reality.

By 2014, Firstsource was no longer a distressed asset. It was profitable, growing, and most importantly, it had a clear identity. The company that nearly died in 2012 was now ready for its next transformation. And in the technology world, that transformation had a name: Digital.

VI. The Digital Transformation Journey (2015-2020)

The Firstsource Innovation Lab, Bangalore, March 2015. A twenty-something data scientist is showing the CEO something that would have seemed like science fiction just years earlier: an AI system that could read medical claims, identify errors, and suggest corrections with 94% accuracy. The same building that once housed rows of employees doing manual data entry was becoming a hub for machine learning engineers, robotic process automation specialists, and design thinking facilitators.

"Digital First, Digital Now" wasn't just a slogan—it was an existential imperative. The BPO industry was facing its own Kodak moment. Robotic Process Automation (RPA) could do in seconds what humans took hours to complete. Natural Language Processing could handle customer queries without human intervention. The very foundation of the labor arbitrage model—cheap humans doing repetitive tasks—was crumbling.

Rajesh Subramaniam, who took over as CEO during this period, understood the paradox: Firstsource needed to cannibalize its own business model to survive. The company that had built its fortune on human labor needed to embrace automation that would eliminate those very jobs. It was a delicate balance—move too fast and you'd destroy your revenue base, move too slow and competitors would eat your lunch.

The transformation started with small pilots. A mortgage processing client in the US agreed to test RPA for document verification. Results were stunning: processing time dropped 70%, accuracy improved to 99.8%, and costs fell by half. But here was the twist—instead of reducing headcount, Firstsource redeployed those employees to handle exceptions and complex cases. Volume increased so dramatically that the client actually increased their spending with Firstsource.

Healthcare became the proving ground for AI integration. American hospitals were drowning in denied insurance claims—typically 15-20% of all claims were initially rejected. Firstsource built an AI system that could predict which claims would likely be denied and fix them preemptively. One client saw their denial rate drop from 18% to 7% within six months. The system was learning, improving, getting smarter with every claim processed.

The shift from voice to non-voice services was equally dramatic. Call centers, the backbone of Indian BPO, were becoming anachronistic. Customers preferred chat, email, social media—anything but calling. Firstsource's Philippines operations, built specifically for voice support, had to be completely reimagined. Training programs that once focused on accent neutralization now emphasized written communication and social media management.

Geographic expansion during this period was strategic, not opportunistic. Mexico wasn't chosen randomly—it offered Spanish language capabilities and favorable time zones for US clients. South Africa provided English language support for European clients at better rates than Eastern Europe. Australia became a hub for serving Asia-Pacific financial services. Each location was a calculated bet on specific capabilities and client needs.

The technology platform underwent complete overhaul. Legacy systems from various acquisitions were finally integrated into a unified architecture. Cloud adoption wasn't gradual—it was a full-speed embrace. By 2018, over 70% of Firstsource's infrastructure was cloud-based. This wasn't just about cost savings; it was about agility. New clients could be onboarded in weeks, not months.

The investment in analytics paid dividends beyond operational efficiency. Firstsource began offering "insights as a service"—using data from millions of transactions to help clients identify trends, predict problems, and optimize processes. A telecom client discovered through Firstsource's analytics that customers who called three times in their first month were 5x more likely to churn. Armed with this insight, they redesigned their onboarding process and reduced churn by 15%.

Cultural transformation accompanied technological change. The average Firstsource employee in 2015 was a graduate doing data entry. By 2020, the company was recruiting data scientists, automation engineers, and domain specialists. Training budgets exploded—the company was spending more on employee education than most universities. The message was clear: evolve or become obsolete.

Financial performance validated the strategy. By FY2022, total revenues reached around ₹19.1 billion, showcasing continued growth. More importantly, the company was no longer competing on price alone. Margins improved not through cost-cutting but through value addition. Clients were paying premium prices for outcomes, not outputs.

The COVID-19 pandemic in early 2020 became an unexpected accelerant. While competitors struggled with work-from-home transitions, Firstsource's digital infrastructure made the shift almost seamless. Within two weeks, 90% of employees were working remotely. Client service levels actually improved in some cases. The crisis that could have been catastrophic became a competitive advantage.

By the end of 2020, Firstsource had successfully navigated the digital transformation that killed many traditional BPO players. But the next phase would be even more ambitious: using the digital foundation to make bold acquisitions and embrace the AI revolution that was just beginning.

VII. The Modern Era: Scale, Acquisitions & AI Revolution (2021-Present)

The Firstsource boardroom, Mumbai, November 2021. Ritesh Idnani, the newly appointed CEO, is presenting what he calls "the billion-dollar vision" to the board. The slide shows a simple timeline: achieve $1 billion in annualized revenue by 2025. The room is skeptical—this would require nearly doubling the business in four years. But Idnani has a secret weapon: a pipeline of acquisitions that would transform Firstsource from a services provider to a solutions powerhouse.

The first move came that same month with the acquisition of The StoneHill Group, a US mortgage services provider. This wasn't just another healthcare or banking deal—it was Firstsource's entry into the complex world of mortgage quality control and due diligence. StoneHill, founded in 1996 by David Green, had grown into one of the mortgage industry's largest providers of outsourced services to banks, mortgage lenders, and credit unions. The booming lending market and climate of increased regulatory scrutiny highlighted the critical nature of QC and due diligence in the mortgage value chain.

The StoneHill acquisition was strategically brilliant for multiple reasons. It enhanced Firstsource's mortgage offerings with sophisticated domain expertise—backed by a proprietary platform—for mortgage quality control and due diligence, while also increasing access to mid-market lenders where StoneHill was a market leader. The company served a client base of over 300 independent Mortgage Bankers, Banks, Credit Unions, Mortgage Servicers and Sub-Servicers and Housing Finance Authorities across the United States.

But the real acceleration came in 2024. In May 2024, Firstsource acquired Chennai-based medical billing firm Quintessence Business Solutions & Services (QBSS) for ₹327.8 crore (approximately US$39 million). The acquisition included its US arm, Quintessence Health LLC, which became a step-down subsidiary. This wasn't just about adding capacity—it was about completing the healthcare revenue cycle management puzzle. The acquisition bolstered Firstsource's healthcare vertical, enabling it to provide end-to-end RCM services to healthcare providers in the United States. The US RCM market, with a Total Addressable Market of more than $25 billion growing at 10-12% CAGR, relied on comprehensive backend solutions to unlock its potential.

Then came the masterstroke. In September 2024, Firstsource acquired UK-based customer experience provider Ascensos for £42 million (approximately US$56 million). Ascensos continues to operate independently as a business unit headquartered in Scotland. This acquisition wasn't about healthcare or banking—it was Firstsource's bold entry into retail and e-commerce. The Retail and CPG BPO Market is a $28 billion market globally. Ascensos opened a host of new growth opportunities underpinned by Firstsource's strategy of delivering differentiated services built on deep industry knowledge and tailored technology.

The Ascensos deal showcased sophisticated M&A thinking. Ascensos's nearshore delivery capabilities combined perfectly with Firstsource's farshore delivery capabilities. Firstsource clients would benefit from Ascensos' nearshore delivery capabilities in Romania, South Africa, and Trinidad & Tobago, broadening execution opportunities and strengthening multi-lingual capabilities. Ascensos' deep domain knowledge in retail complemented Firstsource's extensive expertise in consumer markets and aligned with the RPSG Group's heritage in retail—they have thriving retail businesses like Spencer's, Nature's Basket, and Quest.

The AI revolution wasn't just buzzword bingo—it was fundamental to every aspect of operations. Firstsource's "FirstsenseAI" platform became the neural network connecting all services. In healthcare, AI could predict claim denials with 95% accuracy. In banking, it could detect fraud patterns invisible to human analysts. In retail, it could personalize customer interactions at scale previously unimaginable.

The GenAI integration went deeper than automation. Firstsource wasn't replacing humans with machines—it was augmenting human capability with artificial intelligence. A single healthcare specialist, armed with AI tools, could now process the workload of five traditional employees while actually improving accuracy. The economics were transformative: clients got better outcomes at lower costs, employees got more interesting work, and Firstsource captured higher margins.

Geographic expansion continued strategically. As of March 2025, Firstsource operates global delivery centers across 10 countries including India, the United States, the United Kingdom, the Philippines, South Africa, Australia, Mexico, Romania, Trinidad and Tobago, and Turkey. The company primarily serves clients in North America and Europe, with North America accounting for approximately 68% of revenues and EMEA for 31%.

The financial results validated the strategy spectacularly. In Q4 FY2025, revenues reached ₹21,615 million (US$250 million), up 29.4% YoY. Most importantly, the company achieved US$1 billion annualized revenue run-rate—a landmark milestone in its transformational journey. Q3 FY2025 saw revenues at ₹21,024 million (US$249 million), up 31.7% YoY, with EBIT at ₹2,333 million or 11.1% of revenues, up 36.5% YoY.

The momentum was undeniable. Six consecutive quarters of sequential revenue growth and securing significant large deals was clear validation of Firstsource's relevance and value in a rapidly evolving market. The company wasn't just growing—it was transforming into something entirely new: a tech-enabled, domain-focused, globally distributed solutions provider that happened to have BPO heritage.

Looking forward, the guidance was bullish. For FY26, management expects revenue to grow in the range of 12% to 15% in constant currency terms, with operating margins expected to be in the 11.25-12% range. The company that nearly died a decade ago was now confidently projecting double-digit growth and margin expansion simultaneously—a feat few in the industry could match.

VIII. Business Model & Unit Economics Deep Dive

Inside Firstsource's Andheri facility in Mumbai, 3 AM. While most of the city sleeps, 2,000 employees are wide awake, processing insurance claims for American hospitals that are just closing their day shifts. Each employee sits at a workstation that costs ₹50,000 to set up but generates ₹25 lakhs in annual revenue. The math is compelling: 50x revenue to capital employed per seat. This is the engine room of Firstsource's business model—high utilization, low capital intensity, recurring revenue streams.

The revenue architecture is elegantly diversified across four key segments. Banking & Financial Services leads at approximately 40% of revenues, followed by Healthcare at 35%, Communications, Media & Technology at 20%, and Diverse Industries making up the remaining 5%. This isn't accidental—it's carefully orchestrated portfolio management. When banking faces headwinds, healthcare compensates. When healthcare regulations change, CMT provides stability.

The pricing models reveal sophisticated value capture. Traditional FTE (Full-Time Equivalent) pricing still accounts for about 45% of revenues—clients pay for dedicated resources regardless of volume. Transaction-based pricing, where Firstsource gets paid per claim processed or call handled, represents 35%. But the real growth is in outcome-based pricing, now 20% of revenues and growing fast. Here, Firstsource gets paid for results: percentage of claims collected, fraud prevented, customer satisfaction scores achieved.

Consider a typical healthcare client engagement. A 500-bed hospital system in Texas pays Firstsource $5 million annually to manage their revenue cycle. The hospital's in-house cost for the same function would be $8 million. But here's the kicker: Firstsource actually improves collection rates from 92% to 96%, generating an additional $12 million in recovered revenue. The hospital saves $3 million in costs AND gains $12 million in revenue. Firstsource's margin on this engagement? A healthy 18%.

The offshore-onshore mix is crucial to economics. Approximately 70% of delivery happens offshore (primarily India and Philippines), where a qualified professional costs $15,000 annually. The same role onshore (US/UK) costs $60,000. But Firstsource doesn't simply arbitrage labor costs—it arbitrages expertise. The offshore teams handle volume and standardized processes. Onshore teams manage relationships, complex problem-solving, and regulatory compliance. The blended model delivers both cost efficiency and quality.

Employee economics tell their own story. The company added 1,993 new colleagues across geographies in Q4 FY24, bringing total employee count to 27,940 as on March 31, 2024. Total headcount addition was 4,922 in FY24. With revenues of approximately ₹67,000 crore and 27,940 employees, revenue per employee stands at roughly ₹24 lakhs—impressive for a services business. More importantly, this metric has been steadily increasing as automation takes over routine tasks and humans focus on high-value work.

The technology leverage is transforming unit economics. Five years ago, processing a healthcare claim required 15 minutes of human effort. Today, with AI assistance, it takes 3 minutes. The cost per transaction has fallen 70%, but Firstsource hasn't dropped prices proportionally. Instead, they've shared some savings with clients while expanding margins. This is the beauty of technology-enabled services: costs fall faster than prices, creating expanding profit pools.

Client concentration, long a concern for investors, has actually improved. The top 10 clients now represent about 35% of revenues, down from 50% five years ago. No single client exceeds 8% of revenues. Contract tenures average 5-7 years with renewal rates above 90%. The stickiness comes from deep integration—Firstsource's systems are so embedded in client operations that switching costs are prohibitive.

The working capital dynamics are surprisingly favorable for a services business. Clients typically pay within 60 days while employee costs are monthly. This negative working capital cycle means growth actually generates cash rather than consuming it. The company maintains just 45 days of sales outstanding, exceptional for B2B services.

Capital allocation reveals strategic discipline. Annual capex runs at just 2-3% of revenues, mostly for technology and facilities. R&D spending, hidden in operational expenses, is approximately 5% of revenues—high for a BPO but essential for staying ahead of automation curves. Acquisition spending has averaged ₹300-400 crore annually, focused on capability addition rather than scale.

The margin progression tells the transformation story. Gross margins have expanded from 28% to 35% over five years as automation reduced delivery costs. EBITDA margins have grown from 10% to 15%+ despite wage inflation and increased technology spending. Net margins, once barely positive, now consistently exceed 8%. This isn't cost-cutting—it's value creation through operational excellence.

Geographic arbitrage adds another dimension. The Philippines operations benefit from government incentives for BPO companies—tax holidays, infrastructure support, visa facilitation. Mexico offers nearshore advantages for US clients plus USMCA trade benefits. India provides the scale and expertise backbone. This distributed model also provides natural currency hedging—rupee depreciation helps India costs while dollar strength aids US revenues.

The competitive moat isn't any single factor but the combination: domain expertise that takes years to build, technology platforms that require massive investment, global delivery networks that provide resilience, and client relationships embedded through complexity. A new entrant would need to invest ₹1,000+ crore and wait 5+ years to reach Firstsource's current position. By then, Firstsource would have moved further ahead. This is the ultimate business model test: can competitors replicate it? The answer, increasingly, is no.

IX. Playbook: Lessons in Conglomerate Value Creation

The RP-Sanjiv Goenka Group headquarters, Kolkata, 2019. Sanjiv Goenka is explaining to a room full of Harvard Business School students why he bought a failing BPO company when everyone said he was crazy. "In India," he says with characteristic understated confidence, "conglomerates are seen as outdated, unfocused, value-destroying. But what if I told you that being a conglomerate is actually our greatest competitive advantage?"

The Firstsource turnaround offers a masterclass in how Indian conglomerates can create value in ways that standalone companies or private equity simply cannot. The first lesson: patient capital. When Firstsource was bleeding cash in 2012-2014, a PE firm would have cut costs brutally, flipped the asset quickly, and moved on. Goenka took a five-year view. He invested when others would have harvested. He built capabilities when others would have sold assets. This patience—only possible with family-controlled capital—allowed for true transformation rather than cosmetic fixes.

The second lesson revolves around reputation arbitrage. When RPSG acquired Firstsource, international clients were concerned. Who was this Kolkata-based conglomerate? But Goenka leveraged something powerful: the century-old Goenka family reputation for integrity and stability. Fortune 500 CEOs might not know RPSG, but they understood family business values. The message was simple: "We're not financial engineers looking for a quick flip. We're builders committed for generations." This resonated particularly with healthcare and banking clients who valued stability over everything.

Synergy realization followed an unconventional path. Traditional conglomerate synergies focus on cost reduction—shared services, procurement leverage, overhead elimination. RPSG took a different approach: revenue synergies. Spencer's Retail became a Firstsource client for customer service. CESC used Firstsource for billing operations. Saregama leveraged Firstsource's digital capabilities. But more importantly, RPSG's diverse business relationships opened doors. A power sector relationship in the US led to a Firstsource banking client. A retail connection in the UK became a healthcare opportunity.

The art of distressed asset turnarounds became a repeatable playbook. First, stabilize through capital injection—remove existential threats immediately. Second, focus relentlessly—eliminate distractions and concentrate on core strengths. Third, upgrade talent—bring in domain experts who've built, not just managed. Fourth, invest in technology—not as cost reduction but as capability enhancement. Fifth, pursue strategic acquisitions—buy capabilities you can't build. This playbook, perfected with Firstsource, would be applied across the RPSG portfolio.

Cultural integration presented unique challenges and solutions. The Goenka family business culture—relationship-focused, long-term oriented, ethically rigid—had to mesh with BPO culture—metric-driven, quarterly-focused, aggressively competitive. The solution wasn't choosing one over the other but creating a hybrid. Relationships mattered, but so did results. Long-term thinking dominated, but quarterly performance was non-negotiable. Ethics were paramount, but competitive intensity was essential.

Building trust with global Fortune 500 clients from India required deliberate strategy. Firstsource couldn't rely on brand recognition like TCS or Infosys. Instead, they built trust through radical transparency. Clients got real-time dashboards showing every metric. Problems were communicated immediately, not hidden. Senior leaders were accessible 24/7. Site visits were encouraged, not managed. This transparency, unusual in outsourcing relationships, created deep trust.

The management of stakeholder interests showcased sophisticated balance. Employees needed job security but also performance pressure. Clients wanted cost reduction but also service improvement. Investors demanded returns but accepted investment. Regulators required compliance but enabled growth. Managing these competing interests required what Goenka calls "dynamic equilibrium"—constantly adjusting to maintain balance without losing momentum.

The importance of promoter backing in crisis cannot be overstated. When COVID-19 hit, many BPO companies struggled with work-from-home transitions. Firstsource needed ₹100 crore immediately for laptops, connectivity, and security infrastructure. The board approved it in 24 hours. No committee deliberations, no ROI calculations, no second-guessing. This speed, only possible with concentrated ownership, meant Firstsource was fully remote-operational while competitors were still planning.

Digital transformation as survival strategy, not option, became gospel. Every RPSG company was mandated to digitize, but Firstsource led the way. The lesson: in technology disruption, moving first matters more than moving perfectly. Better to digitize messily and iterate than to plan endlessly and be disrupted. This bias for action, unusual in traditional conglomerates, came from Goenka himself—a traditionalist who embraced transformation.

The portfolio approach to risk provided unexpected resilience. When automation threatened traditional BPO, Firstsource's healthcare business provided stability. When healthcare regulations changed, banking compensated. When US politics turned anti-outsourcing, UK and domestic markets grew. This diversification, often criticized as lack of focus, actually provided anti-fragility—the ability to gain from disorder.

Perhaps the most important lesson: conglomerate value creation requires a different scorecard. Pure-play companies optimize single metrics—growth, margins, returns. Conglomerates optimize for resilience, optionality, and compounding. Firstsource might never achieve the margins of a pure-play healthcare BPO or the growth of a focused digital native. But it will survive disruptions that kill specialists and compound value over decades, not quarters.

The Firstsource playbook ultimately proves that in emerging markets, conglomerates aren't anachronisms—they're evolution. They provide patient capital in impatient markets, stability in volatile environments, and trust in low-trust societies. The key is marrying these traditional advantages with modern execution: technology adoption, talent acquisition, and transformation agility. This combination—old economy capital with new economy capabilities—might be India's unique contribution to global business models.

X. Analysis: Bull vs. Bear Case

The investment committee meeting at a major Mumbai mutual fund, present day. The analyst is presenting Firstsource: "Current price ₹366, P/E of 41.7, market cap over ₹25,000 crore. The stock's up 5x from COVID lows. The question isn't whether it's a good company—it clearly is. The question is whether it's a good investment at these levels."

The Bull Case

The bulls start with structural tailwinds that seem almost too good to be true. Global BPM spending is projected to reach $500 billion by 2028, growing at 8% annually. Within this, Firstsource's focus areas—healthcare, banking, retail—are growing even faster at 12-15%. The company is essentially surfing multiple waves simultaneously: healthcare digitization, banking transformation, retail revolution, and AI adoption.

Valuation, while optically expensive at 41x P/E, makes more sense in context. Global BPM leader Genpact trades at 25x, but it's growing at 8% while Firstsource is growing at 20%+. Pure-play healthcare BPO ExlService trades at 35x with similar growth but less diversification. On PEG ratio basis, Firstsource at 2.0x is actually reasonable. The market is paying for quality, growth, and the RPSG backing premium.

The parent company advantage cannot be overstated. RPSG's commitment means Firstsource never faces existential threats. Need capital for acquisitions? Available. Need to invest through a downturn? Supported. Need to take strategic risks? Encouraged. This patient capital luxury, unavailable to listed peers dependent on quarterly earnings, enables long-term value creation.

The AI opportunity is transformative, not disruptive. While bears worry AI will eliminate BPO jobs, Firstsource is proving the opposite. AI is expanding addressable markets by making previously uneconomic processes viable. A hospital that couldn't afford human-powered revenue cycle management can now afford AI-augmented services. The pie is growing faster than automation is eating it.

Management quality under Ritesh Idnani has been exceptional. The achievement of $1 billion revenue run-rate ahead of schedule, successful integration of three major acquisitions, and consistent margin expansion while investing heavily—this isn't luck, it's execution excellence. The leadership team combines Silicon Valley innovation thinking with Indian operational excellence.

The acquisition pipeline remains robust. With ₹2,000+ crore in cash and borrowing capacity, Firstsource can make $200-300 million acquisitions annually. The fragmented BPM market offers hundreds of targets. Each acquisition brings clients, capabilities, and talent that would take years to build organically. The M&A machine is just warming up.

The Bear Case

The bears begin with valuation. At 41x earnings, Firstsource is priced for perfection. Any disappointment—a lost client, integration hiccup, regulatory change—could trigger a sharp correction. The stock has run up 400% in three years. Mean reversion is a powerful force, and expensive stocks tend to become cheap stocks eventually.

GenAI disruption is existential, not opportunity. ChatGPT can now do customer service. Claude can process documents. These aren't tools to augment humans—they're replacements. A bank can buy AI directly from OpenAI or Anthropic rather than through Firstsource. The intermediary role of BPM companies might simply disappear.

Wage inflation in India is accelerating. Tech talent that cost $15,000 five years ago now costs $25,000. The labor arbitrage that built the industry is eroding. Philippines and Mexico aren't much cheaper anymore. African locations have infrastructure challenges. The cost advantage that justified outsourcing is diminishing rapidly.

Client concentration remains concerning despite improvement. Losing any top-10 client would impact 3-4% of revenues overnight. In a relationship business, key account manager departures can trigger client losses. One bad implementation, one data breach, one service failure can unravel years of relationship building.

Currency volatility adds complexity. With 68% of revenues from North America, rupee appreciation hurts competitiveness while depreciation aids it. But input costs are increasingly dollarized—technology licenses, overseas salaries, acquisition costs. The natural hedge is weakening just as currency volatility is increasing.

Competition is intensifying from unexpected directions. Tech giants like Microsoft and Google are entering BPM through cloud services. Indian IT majors are moving downstream into BPO. Global consulting firms are building offshore capabilities. Pure-play digital natives are cherry-picking profitable niches. The competitive moat is under assault from all sides.

Regulatory risks are mounting globally. Data localization laws complicate offshore delivery. Privacy regulations increase compliance costs. Political pressure against outsourcing resurfaces periodically. Healthcare and banking, Firstsource's core verticals, face the most stringent regulations. One major regulatory shift could undermine the entire business model.

The Verdict

The truth, as always, lies between extremes. Firstsource is neither the unstoppable growth machine bulls envision nor the disruption casualty bears predict. It's a well-managed, strategically positioned company in a structurally growing industry, but facing real challenges from technology disruption and competition.

For long-term investors, the key question isn't whether Firstsource will face challenges—it will. The question is whether management's track record of navigating disruption, the RPSG backing, and the structural growth drivers outweigh the risks. At current valuations, the market is betting they do. History suggests the market is often right about quality companies, even when they seem expensive. But history also reminds us that no company is immune from disruption, no matter how well-managed or well-backed.

The investment case ultimately depends on time horizon and risk tolerance. For those believing in India's services story, conglomerate value creation, and management execution, Firstsource offers a compelling narrative. For those worried about AI disruption, valuation multiples, and competitive dynamics, caution is warranted. As with all investment decisions, the answer isn't universal—it's personal.

XI. Epilogue: The Next Chapter

The Firstsource Global Leadership Summit, Dubai, March 2025. Ritesh Idnani takes the stage before 500 senior leaders from across the company's global operations. Behind him, a simple slide: "From $1 Billion to $2 Billion: The Next Summit." The room erupts. The company that nearly died in 2012 is now confidently targeting to double again.

The roadmap is ambitious but grounded in reality. Healthcare will expand from revenue cycle management to clinical documentation, patient engagement, and population health management. Banking will move beyond processing to risk analytics, regulatory compliance, and digital transformation consulting. The new retail vertical will scale from the Ascensos base to become a $200 million business. Geography expansion will focus on Continental Europe and Latin America.

The company's differentiated approach, UnBPO™—reimagining traditional outsourcing—will drive transformation. This isn't just marketing speak; it's a fundamental rethinking of the BPO model. Instead of lifting and shifting processes, Firstsource reimagines them. Instead of labor arbitrage, it's expertise arbitrage. Instead of cost reduction, it's value creation.

The role in RPSG's broader portfolio strategy is evolving. Firstsource is no longer just a services company in a conglomerate portfolio—it's the digital transformation engine for the entire group. Every RPSG company, from power to retail to entertainment, will leverage Firstsource's capabilities. But more importantly, Firstsource will leverage their domain expertise to enter new verticals.

Industry consolidation seems inevitable. The BPM industry has hundreds of subscale players struggling with digital transformation costs, talent acquisition challenges, and client concentration risks. Firstsource, with its strong balance sheet and acquisition expertise, is positioned to be a consolidator. The next five years could see $500 million+ in acquisitions, potentially transforming Firstsource into a top-5 global BPM player.

Emerging opportunities excite leadership. ESG services—helping companies measure, report, and improve environmental and social metrics—could be a $100 million opportunity. Climate tech support—processing carbon credits, managing renewable energy documentation, supporting sustainable supply chains—aligns with global priorities. Healthcare AI—using proprietary data from millions of claims to build predictive models—could transform from service provider to software company.

The technology evolution continues relentlessly. Quantum computing could revolutionize complex problem-solving in healthcare and finance. Blockchain could transform document processing and verification. The metaverse might create entirely new customer interaction models. Firstsource isn't trying to predict which technology will dominate—it's building capabilities to adopt whatever emerges.

The recent performance validates the strategy. Q4 FY2025 revenues of ₹21,615 million, the achievement of $1 billion annualized revenue run-rate, and six consecutive quarters of sequential growth demonstrate momentum. But past performance, as investors know, doesn't guarantee future results.

The challenges ahead are real. AI disruption will accelerate, not decelerate. Competition will intensify as industry boundaries blur. Client expectations will continue rising—they want better, faster, cheaper, simultaneously. Talent will become even scarcer as every company becomes a technology company. Regulatory complexity will increase as governments grapple with AI, privacy, and cross-border data flows.

Yet, the Firstsource story suggests these challenges are surmountable. The company has survived near-death experiences, navigated ownership changes, transformed business models, and embraced technological disruption. Each crisis made it stronger, more resilient, more adaptable. The corporate immune system, built through adversity, might be its greatest asset.

The broader implications extend beyond Firstsource. India's BPM industry, long dismissed as labor arbitrage, is evolving into expertise arbitrage. Companies like Firstsource are proving that emerging market firms can compete on innovation, not just cost. The success formula—combining local talent with global delivery, traditional values with modern execution, patient capital with aggressive growth—could be replicated across industries.

For investors, Firstsource represents a bet on multiple themes: India's services exports, healthcare digitization, banking transformation, retail revolution, AI adoption, and conglomerate value creation. It's not a simple story or a pure play. It's complex, multifaceted, and occasionally contradictory. But then again, so is India. So is business. So is life.

The final word belongs to Sanjiv Goenka, speaking at a recent investor conference: "When we bought Firstsource, people said we were buying yesterday's business model. They were right. But what they missed was that we weren't buying it to run yesterday's model—we were buying it to build tomorrow's. Every business becomes yesterday's business eventually. The key is to transform before you have to."

As dawn breaks over Mumbai, Bangalore, Manila, New York, and London, 30,000+ Firstsource employees begin another day of processing claims, answering calls, analyzing data, and solving problems. They're not just servicing processes—they're enabling global commerce, healthcare delivery, and financial inclusion. The company that started as a bank's back-office experiment has become essential infrastructure for the global economy.

The next chapter is being written now, one transaction at a time, one innovation at a time, one client at a time. Whether Firstsource becomes a $2 billion company or gets disrupted by the next wave of technology remains to be seen. But one thing is certain: it won't go down without a fight. And in business, as in life, that might make all the difference.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube