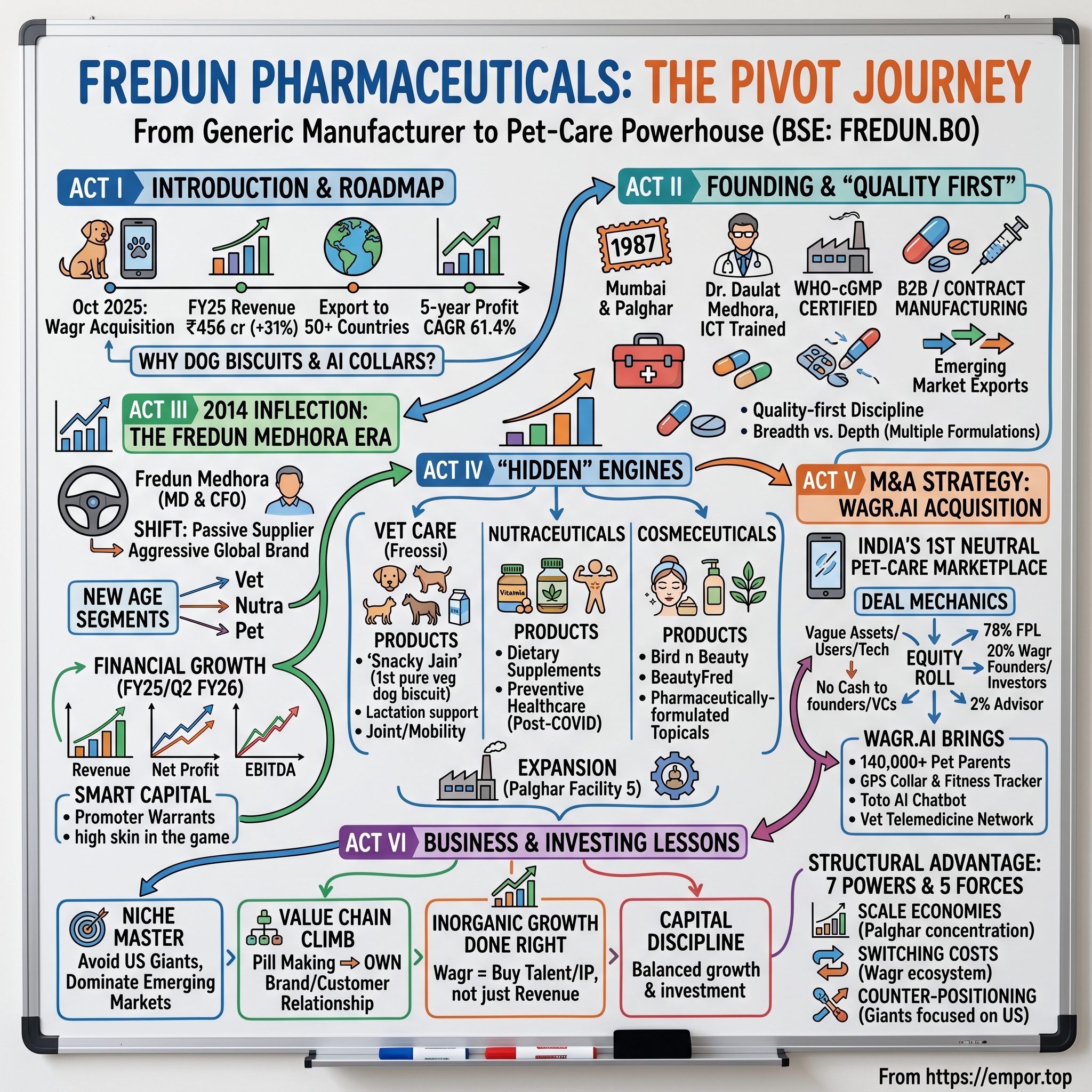

Fredun Pharmaceuticals: The Pivot from Generics to a Pet-Care Powerhouse

I. Introduction & Episode Roadmap

Picture a small, family-run pharmaceutical company in Palghar, Maharashtra — a dusty industrial town two hours north of Mumbai, where the Western Ghats start to break the monotony of the coastal plain. For nearly three decades, this company quietly pressed tablets and filled syrup bottles for some of the biggest names in Indian and global pharma. It made the medicine; somebody else's logo went on the box. The kind of company most retail investors would scroll right past on the BSE small-cap screen.

Now picture this same company, in October 2025, walking into a conference room in Bengaluru and acquiring a venture-backed pet-tech startup — a startup with a 4G-enabled GPS collar, an AI chatbot named Toto, 140,000 pet parents on its app, and a nationwide veterinary network — and doing it without writing a single rupee of cash for the assets.12 The founders rolled their stock into the listed entity. The VCs rolled their stock into the listed entity. And a 39-year-old contract manufacturer, founded the same year as Microsoft Excel, suddenly owned 78% of what management has been calling "India's first neutral pet care marketplace."2

That company is फ्रेडुन फार्मास्युटिकल्स Fredun Pharmaceuticals Limited, BSE ticker FREDUN.BO. As of FY25, it manufactures more than 700 formulations, exports to over 50 countries, and reported revenue of ₹456 crore, up 31% year-over-year — in a sector where mid-cap Indian pharma has been gasping at single-digit growth.3 Its five-year profit CAGR sits at 61.4%, an absurd number for a generics-and-formulations business that competes head-on with the likes of Cipla, Abbott, Sun, and Mankind.3

How did a 1987-vintage contract manufacturer get here? Why is the founder's son betting the company's future on dog biscuits and AI-powered collars? And what does it tell us about the playbook for Indian small-cap pharma in 2026 — a year when the US generic market has been crushed by price erosion, when Chinese API competitors are squeezing margins, and when the only way out for the smart operators is up the value chain?

This is the Fredun story in three acts. Act one: the founding heritage of डॉ दौलत मेधोरा Dr. Daulat Medhora, the ICT-trained scientist who built a quality-first formulations factory in an era when "make-do" was the Indian pharma standard. Act two: the 2014 inflection, when his son फ्रेडुन मेधोरा Fredun Medhora took the wheel and turned a passive supplier into an aggressive global brand. And act three — the most interesting one — the October 2025 Wagr acquisition, the launch of the Freossi pet-care brand, and a stated ambition that "every pet in India should be using a Fredun product or service."4

Along the way we'll dig into the hidden engines (vet, nutra, cosmeceutical) that management expects to deliver more than half of revenue by FY30, the moat math behind the Palghar manufacturing complex, and the Hamilton Helmer 7-Powers and Porter framework that explains why a sub-$200-million-market-cap pharma can credibly aim for a multi-billion rupee top line. Let's start at the beginning.

II. Founding & The "Quality First" Heritage

It is 1987 in Mumbai. Rajiv Gandhi is prime minister. The Indian pharmaceutical industry is in the middle of one of the most consequential structural shifts in its history — the 1970 Patent Act has been in force for a decade and a half, India recognises only process patents (not product patents), and a generation of homegrown chemists is busy reverse-engineering Western branded drugs at a fraction of the cost. This is the era that birthed Sun Pharma, Cipla's modern resurgence, Dr. Reddy's, Lupin, Aurobindo. But for every Sun Pharma, there are a hundred quieter shops — small formulation manufacturers in Maharashtra and Gujarat industrial belts, doing the unglamorous work of actually putting molecules into tablet form for the brands that sell them.

Into this world walks Nariman Medhora and his son डॉ दौलत मेधोरा Dr. Daulat Medhora. Dr. Daulat is not a typical Indian pharma promoter of the era. He is a doctorate-holding chemist trained at the Institute of Chemical Technology — ICT Mumbai, the legendary पदार्थ-शास्त्र institute formerly known as UDCT, whose alumni built large parts of the Indian chemical and pharmaceutical industry. The father-son duo incorporates Fredun Pharmaceuticals Limited on June 8, 1987, with the corporate identification number L24239MH1987PLC043662.[^5] The name "Fredun," it turns out, is the Parsi-rooted name of Dr. Daulat's son, who would one day take over the business — a tell, in retrospect, that this was always built as a generational project, not a quick hit.

The early Fredun playbook is as un-glamorous as Indian small-cap pharma gets. The company sets up a formulations plant in Palghar, an industrial cluster in coastal Maharashtra north of Thane, and builds a contract-manufacturing relationship with the giants. Tablets, capsules, syrups, ointments, dietary supplements — multiple dosage forms, multiple therapeutic areas. The brands move; Fredun makes. For decades, the rhythm of the business is set by the rhythm of orders coming in from larger players who needed manufacturing capacity but didn't want to build their own.

But two things happened in those first three decades that would matter enormously later. First, Dr. Daulat enforced a quality discipline that was, by the standards of small Indian pharma at the time, almost paranoid. The company invested in WHO-cGMP-grade manufacturing infrastructure long before it was strictly necessary for the domestic market. The reasoning, as the family has retold it, was essentially that you cannot build a "make-it-cheaper" moat in pharma — the only durable moat is "make-it-better-and-reliably-pass-inspection." That paid for itself the moment Fredun started seeking emerging-market export approvals — Africa, Southeast Asia, Latin America — where regulators may not be FDA-strict, but they demand WHO certifications as table stakes.

Second, the company built breadth instead of depth. Most Indian generics players in this period chose a niche — anti-infectives, cardio-vascular, derma — and went deep. Fredun did the opposite. It built a platform plant capable of cranking out anti-diabetics, anti-retrovirals, antibiotics, vitamins, NSAIDs, and dosage forms ranging from solid tablets to liquid syrups to topical ointments.3 In the contract-manufacturing era this looked like a lack of focus. In the 2020s, when the company started exporting its own brands to fifty-plus countries, it turned out to be exactly the right design — because emerging market customers wanted a one-stop shop, not a specialist.

The "quality at any cost" culture also did something subtle to the balance sheet. For most of the 1990s and 2000s, Fredun was tiny and unfashionable, but it never blew itself up. There is no scandal in the corporate filings, no FDA warning letter, no reckless leverage cycle. The company quietly compounded — slowly, but with the kind of margin discipline that would later support a 60%+ EBITDA growth quarter without requiring a dilutive equity raise.5 That foundation — the boring decades — is the unsexy reason Fredun can credibly underwrite a pet-tech leap in 2025. The plant works. The audits pass. The chassis is sound. What it needed was a driver willing to step on the accelerator.

III. The 2014 Inflection: The Fredun Medhora Era

The leadership transition at Fredun did not happen in a single dramatic moment. There was no press release, no boardroom showdown, no anointing ceremony. What happened, quietly, in the years around the company's BSE main-board listing in 2015, was that the founder's son फ्रेडुन मेधोरा Fredun Medhora — the young man for whom the company was named — moved into the operational driver's seat as Managing Director. Dr. Daulat stayed on as Chairman and Joint Managing Director, the elder statesman; Fredun the younger took on the day-to-day, plus the CFO function, an unusual but telling combination for a small-cap promoter.6

If you want to understand the personality difference between father and son, consider their respective responses to the same strategic question — "what business are we in?" Dr. Daulat's answer, by every account, has always been "we are a pharmaceutical manufacturer." Fredun's answer, by 2024, had become "we are a healthcare brand company that happens to manufacture." That single linguistic shift is the entire 2014–2026 strategy in one sentence. Stop renting capacity to other people's brands. Start building your own.

The first phase was geographic expansion. Between 2015 and 2022, Fredun pushed aggressively into emerging markets where the cost of regulatory entry was manageable and the cost of brand-building was orders of magnitude cheaper than in the US or Europe. By the time of the FY25 reporting cycle, the company was registered in 50+ countries spanning Anglophone and Francophone Africa, Southeast Asia, Latin America, and the CIS region, with a portfolio approaching 700 formulations.3 These are not the headline-grabbing markets that get analyst attention, but they share an attractive trait: regulatory complexity is high enough to keep amateur exporters out, while the price-erosion dynamics that have crushed margins in US generics simply don't exist. A company that wins in Vietnam or Kenya or Côte d'Ivoire keeps its pricing power for years.

Then came the discipline shift. Fredun stopped being purely opportunistic and started building a portfolio strategy. The company segmented its business along two axes: legacy formulations (the cash-cow B2B and emerging-market generics business, growing at low-to-mid teens) and what management has been calling its "New Age" segments — animal health, nutraceuticals, cosmeceuticals, mobility/orthopaedic devices, and now pet care. The legacy business funds the New Age businesses. The New Age businesses grow faster, carry better margins, and increasingly attach to brands that Fredun owns rather than makes for someone else. Brands like Bird n Beauty and BeautyFred in cosmeceuticals. Freossi in animal health and pet nutrition.

The financial fingerprints of this strategy are now visible on the income statement. FY25 revenue of ₹456 crore, up 31% from ₹348 crore in FY24. Net profit of ₹21 crore, also up 31%. Operating profit margins inching from 11% to 12%.3 In the most recent print — Q2 FY26 — revenue grew 45% and net profit jumped 128% year-over-year, with EPS more than doubling.7 The half-year FY26 picture: total income ₹265 crore (up 42%), EBITDA ₹39.3 crore (up 61%), EBITDA margin expanding 171 basis points to 14.83%, and net profit nearly doubling.5 That margin trajectory is the most important single number in the business — because it is the smoking gun for the mix-shift thesis. The legacy business cannot, by itself, drive 170 bps of annual margin expansion. The New Age stack can.

What also defines the Fredun Medhora era is a willingness to use the public market intelligently. The company's promoters have repeatedly used preferential warrants and capital infusions to fund growth without distress dilution. The board approved a warrant scheme in October 2025 that the promoter group then began converting through 2026 — a structure where promoters paid hard cash to increase their stake at a pre-set strike, signaling that they personally believed the share price was going higher.8 We'll come back to that in the management section. For now, the takeaway is simpler: the boring contract-manufacturer of the 1990s has, over the last decade, been deliberately turned into a multi-segment branded healthcare platform. The next question is what those new segments actually look like.

IV. The "Hidden" Engines: Vet, Nutra, & Beyond

If the Fredun thesis can be reduced to a single observation, it is this: the most interesting parts of the income statement are the smallest parts. Walk through the Palghar facility today and you'll see the same tablet presses, blister packs, and quality labs you would have seen a decade ago. But look at what is actually coming off those lines — and increasingly, off dedicated lines built specifically for new product categories — and you will see the company's future.

Start with Fredun Vet. Animal health, in the Indian context, is a structurally underbuilt category. The country has a livestock population in the hundreds of millions — cattle, buffalo, goats, poultry — and a companion-animal population (dogs and cats) that has roughly tripled in urban India over the last decade. Yet for most of Indian pharma's history, animal health was treated as a step-child: lower priority, lower investment, lower glamour than human formulations. Fredun saw the inversion early. Animal health products carry better gross margins than commodity human generics for two reasons. First, the channel is far less price-regulated; there is no NPPA-equivalent body forcing price ceilings on dog supplements. Second, the buyer is rarely shopping on price — a pet parent who has decided their dog needs a joint supplement is buying that supplement, not the cheapest equivalent.

Under the Freossi brand, Fredun has moved into both companion-animal and large-animal segments. October 2025 saw the launch of "Snacky Jain" — branded as India's first pure Jain (vegetarian, no root vegetables, no animal-derived ingredients) functional dog biscuit, manufactured at the company's WHO-GMP-certified Palghar facility, initially distributed across six cities through veterinary clinics, online marketplaces, and Fredun's retail partners.9 On the large-animal side, the company rolled out Freossi Tone+ for lactation and milk quality and Freossi Power for joint and mobility support in cattle, buffaloes, horses, and other livestock.10 These are not me-too SKUs; they are positioned products with a story, and they sell at branded margins.

Then there's the nutraceutical and cosmeceutical stack. Fredun Nutrition has built a portfolio of dietary supplements and herbal products targeting the "preventive healthcare" consumer — the Indian middle-class household that, post-COVID, started spending real money on immunity, joint health, gut health, and women's wellness. Fredun's cosmeceutical brands Bird n Beauty and BeautyFred sit in the same intersection: pharmaceutically-formulated topical and consumed products that are sold through pharmacies and online channels, not just in the beauty aisle. The unifying logic is "regulated category, branded margin, sticky consumer." Each product line costs incremental working capital but compounds gross profit at a rate the underlying generics business never could.

Why does this matter for the consolidated P&L? Because legacy formulations grow at roughly 15% in a good year — solid, but uninspiring. The New Age segments are growing materially faster, with gross margins typically several hundred basis points higher than the contract-manufacturing base. Management's stated ambition is for these "New Age" segments to contribute the majority of revenue by FY30 — a deliberate inversion of the current mix. If executed, the consolidated EBITDA margin trajectory becomes a function of segment mix, not unit-cost optimisation. That is the cleanest possible setup for sustained margin expansion in a sector famous for the opposite.

To support this, the company has been steadily expanding its Palghar manufacturing footprint. In April 2026, Fredun announced its fifth facility at Palghar — a 40,000-square-foot block expected to be operational by October 2026, with an additional 50,000-square-foot expansion planned, dedicated to veterinary products, supportive nutraceuticals, and pharmaceutical formulations.11 Concentrating capacity at a single complex isn't an accident; it's a deliberate scale-economy bet that we'll dig into in the Hamilton Helmer section. For now, the relevant fact is this: the same plant that makes a humble paracetamol tablet for an export client now also makes the dog biscuits in the next bay over. The fixed cost is shared. The brand premium is not.

The remaining question, and the one that most distinguishes Fredun from other small-cap pharma stories, is what to do once you own the brand. Owning a brand means you can sell it directly. But the moment you have a direct relationship with the end customer — the pet parent, the immunity-conscious adult, the cosmeceutical buyer — the question becomes whether you can climb one more rung up the value chain and actually own the interface. Which is where Wagr comes in.

V. M&A Strategy: The Wagr.ai Acquisition

The conference room in Bengaluru where the Wagr deal closed in October 2025 had a particular kind of energy. On one side sat Siddharth Darbha, Advaith Mohan, and Ajith Kochery — the three founders of Wagr, a pet-care super-app they had built from a 2016 idea (allegedly born after Mohan's dog went missing) into a venture-backed company that had raised ₹4.2 crore in a 2022 round led by Inflection Point Ventures with participation from IvyCap Ventures and Stanford Angels.12 On the other side sat Fredun Medhora, leading a 39-year-old listed pharmaceutical company most pet-tech founders had never heard of. The deal that emerged from that room is, structurally, one of the more clever pieces of small-cap M&A India has seen in recent memory.

Here is the mechanics. Fredun did not write a cheque for Wagr's assets. There was no "₹X crore acquisition price" for the Wagr business, the technology, the user base, the IP. Instead, every Wagr stakeholder — the founders, the early angels, IvyCap, IPV — had their economics rolled into a new ownership structure for the combined platform. Fredun Pharmaceuticals Limited took 78% of the new entity. The original Wagr shareholders collectively took 20%. The transaction advisor, tal64.com, took 2%.2 No cash to founders, no cash to VCs, no cash leaving Fredun's balance sheet for goodwill. What Fredun deployed instead was equity, brand, manufacturing, and balance sheet.

Why did the Wagr side accept that? Two reasons. First, the Indian pet-tech market had cooled hard between 2022 and 2025 — DTC valuations compressed, late-stage capital dried up, and a standalone path to either profitability or an IPO had become a very long road. Second, Wagr's founders had built a great front-end (the app, the AI chatbot, the GPS collar, the telemedicine network) but had no realistic way to vertically integrate into the supply side of pet nutrition and pharmaceuticals at scale. Joining Fredun gave them an instant manufacturing partner, a regulated distribution backbone, and a listed-company currency. It is the sort of deal that happens when the rational bull case for the standalone has weakened, but the rational bull case for the combination has strengthened.

What Fredun got was significant. Wagr brought a user base of 140,000+ pet parents, a patented GPS and fitness tracker for dogs (described as India's first), an AI-powered pet care chatbot named Toto that had handled 10,000+ queries, and a telemedicine platform that had completed more than 11,000 fifteen-minute veterinary video consultations.12 Crucially, it brought a nationwide veterinary professional network that Fredun could plug its own Freossi product line into immediately. The relaunch of the Wagr marketplace and services was scheduled for Q4 FY26, with the patented fitness-tracking technology slated for re-launch in FY27.13

The strategic positioning is more subtle than it looks. Fredun's pet-care portfolio sits in functional food, wet food, prescription food, and supplements — categories where it competes on formulation, not commodity. It deliberately stays out of dry food and biscuits, which are commodity-feed categories dominated by global majors. Because Fredun does not have a dry-food brand, it can credibly host competing dry-food brands on the Wagr marketplace without conflict of interest. That neutrality — combined with Fredun's proprietary nutraceutical, prescription, and functional offerings — is the thesis behind what management is calling India's first end-to-end neutral pet-care ecosystem.2 If that frame holds, Fredun is not building "another DTC pet brand." It is building the platform that other DTC pet brands will pay rent on — while also seeding it with its own captive Freossi inventory.

The ambition was crystallised in a single line management has used repeatedly since the deal: "FPL's long-term vision is that every pet in India should be using a Fredun product or service."414 In a country where India's pet care industry is projected to reach $6 billion by 2030, with companion-animal ownership growing at double-digit rates in urban metros, that ambition is not as outlandish as it sounds.1 What it requires is execution — a marketplace that doesn't degrade into a price-driven race-to-the-bottom, a tech stack that can scale beyond 140,000 users, and a brand that pet parents trust. Whether Fredun can deliver all three is the next eighteen months' KPI.

VI. Current Management & Skin in the Game

Indian small-cap pharma is a sector where promoter alignment is everything. The ones that compound for decades almost universally have promoters with a high personal stake, low pledged shareholding, and a habit of putting fresh capital into their own company at premium prices. The ones that blow up — and the BSE has a graveyard of these — typically show the opposite signal: promoter selling on the way up, share pledges with weak collateral, related-party transactions that drift outside the consolidated entity. Fredun's management profile lands firmly on the right side of that distribution.

Start with the basic fact pattern. As of the March 31, 2026 shareholding pattern, the promoter group held approximately 44.57% of the company.3 After the April 2026 warrant conversion event, that figure rose to 45.54%.8 The remaining float is roughly 51% public, 1% FII, and 3% DII — a profile that means liquidity is real but limited, and that institutional ownership is still in its early innings. For a multi-decade compounder thesis, that combination — high insider ownership, modest but rising institutional ownership, no concentration of activist or short-term holders — is close to ideal.

Now look at how that promoter holding has moved. In December 2025, following shareholder approval in October, the company allotted convertible warrants to the promoter group at a fixed strike price.8 Through Q4 FY26 and into FY27, the promoter group has been actively converting those warrants into equity — paying real cash, at a premium to the issue date market price, to increase their stake. The April 9, 2026 board meeting approved the allotment of 40,000 equity shares to Mrs. Daulat Nariman Medhora at ₹1,250 per share, for a consideration of ₹3.75 crore.815 This is the cleanest possible promoter-confidence signal — the family is buying more of its own company at the moment when the company is also asking the public market to underwrite a multi-segment growth story. They are not selling into strength; they are buying into strength.

Where it gets interesting is the leadership style split. Dr. Daulat Medhora, the founder, the ICT chemist, remains Chairman and Joint Managing Director — a "founder's mentality" presence in the boardroom, the institutional memory of the manufacturing discipline that has defined the company for nearly four decades.6 His role today is more strategic-anchor than day-to-day operator: setting the long-term quality and capital-allocation principles, and sitting in the seat that says "we will not compromise on the things that have made us durable." He has been at the company since incorporation in 1987, which is a tenure measured not in years but in industry cycles.6

Fredun Medhora, the son and namesake, runs the company day-to-day as Managing Director and CFO. The CFO portion of his title is unusual and worth pausing on. Most Indian listed pharma promoters delegate finance to a hired professional — partly for institutional comfort, partly because the operational side is plenty for one person. Fredun keeps the keys. That gives him direct authority over capital allocation decisions — preferential warrants, working-capital deployment, M&A structure (including the cashless Wagr deal) — without intermediation. It also means investors and analysts on calls deal directly with the person who made the decision and is personally on the hook for the outcome.

Below the promoter pair, the company has been gradually building out a professional team — heads of veterinary, nutrition, exports, and now pet-tech (post-Wagr integration, the founders Siddharth Darbha and Advaith Mohan have stayed actively involved in the combined entity).2 The professionalisation is real but unfinished — and that is, frankly, the lens long-term investors should track. A founder-led mid-cap that is successfully professionalising looks exactly like Fredun does today: heavy promoter equity, growing managerial bench, repeatable capital-raising mechanics. A founder-led mid-cap that is failing to professionalise looks similar from the outside but doesn't show the margin expansion or the segment diversification that Fredun has actually delivered. The numbers, so far, validate the structure.

If there is a single behavioural test for promoter alignment in Indian small-caps, it is this: when the company raises capital, does the promoter participate or get diluted? In Fredun's case, the promoter has been the most aggressive participant in every recent capital event. That fact alone places the management chapter of this story on a different shelf than ninety percent of the BSE small-cap universe.

VII. Analysis: Hamilton's 7 Powers & Porter's 5 Forces

Strip the Fredun story of its narrative gloss and ask the cold, structural question: where do the durable advantages come from? Hamilton Helmer's 7 Powers framework is the right scalpel for this, because it forces a discipline that Indian small-cap analysis often skips — distinguishing between things that look like advantages and things that actually keep competitors out for years at a stretch.

Of the seven powers — scale economies, network economies, switching costs, branding, counter-positioning, cornered resource, process power — Fredun maps cleanly to three, and is in the process of building a fourth. Start with scale economies. The Palghar manufacturing complex, with its now-five facilities and the 40,000- and 50,000-square-foot expansion blocks, represents the highest single-location formulations capacity in the company's history.11 Concentrated capacity at one site has two structural effects: fixed-cost dilution as utilisation rises, and shared infrastructure (utilities, QA, warehousing, logistics) across product categories — meaning the unit cost of the next product line added (say, a new pet supplement) is materially lower than a greenfield plant would imply. For a competitor trying to match Fredun's breadth across human formulations, animal health, nutraceuticals, and cosmeceuticals, the capex required to recreate a Palghar-equivalent footprint is in the tens of crores at minimum — and that's before factoring in the years of WHO-cGMP audit history that come bundled with an existing approved facility.

Switching costs are where the Wagr acquisition unlocks the second power. A standalone formulations exporter has effectively zero switching costs — a customer in Tanzania who buys your generic ibuprofen today can buy Aurobindo's tomorrow with one purchase order. But a pet parent who has put a Wagr GPS collar on their dog, has the Toto chatbot answering 3am health queries, has a registered telemedicine relationship with a vet on the platform, and is auto-replenishing Freossi-branded supplements on subscription — that pet parent has a switching cost measured in the hassle of moving every node of their pet's health stack to a competing platform. None of those switching costs existed at Fredun before October 2025. Building them is the entire strategic logic of the Wagr deal.

Counter-positioning is the third power, and it is the most under-appreciated in the Fredun story. The large-cap Indian generics players — Sun, Cipla, Lupin, Aurobindo — are structurally locked into a US-and-developed-markets-first strategy. Their cost structures, their compliance teams, their sales architectures, their investor narratives are all built around defending and growing US generic share, even as the price-erosion environment there has gotten brutal over the last decade. None of them can credibly pivot to a 50-country emerging-market formulations strategy combined with a domestic pet-care play, because the unit economics that work at Fredun's scale would be irrelevant to a multi-billion-dollar pharmaceutical major. This is classic counter-positioning: the dominant incumbents cannot match the strategy without cannibalising their own core. Fredun has built a kingdom in markets the giants have effectively conceded.

The fourth power, still under construction, is branding. Freossi, Snacky Jain, BeautyFred, and the consolidated Wagr platform are early-stage brands today. They have shelf presence and marketing momentum, but not yet the unconscious-association power of, say, Pedigree or Royal Canin. If management executes on the Q4 FY26 marketplace re-launch and the FY27 fitness-tracker re-launch, the trajectory of brand power is up and to the right. If they fumble it, the brands stay regional and the moat stays thin.

Now apply Porter's five forces — buyer power, supplier power, threat of substitutes, threat of new entrants, competitive rivalry — to the consolidated entity. Buyer power is the most important variable in pharma export businesses, and Fredun has explicitly mitigated it by diversifying across 50+ countries.3 No single distributor in any single market has leverage to force pricing, because the company's revenue is fragmented across hundreds of relationships. Supplier power is moderate — Indian active-pharmaceutical-ingredient supply has been periodically disrupted by Chinese export controls, but Fredun's procurement is broad enough across molecule classes to absorb single-supplier shocks. Threat of substitutes is high on the commodity human-generics side (this is why margins there are mid-teens) but low on the prescription pet care and specialised nutraceutical side, which is precisely why management is reweighting the mix. Threat of new entrants is meaningful — Indian formulations is not a moated industry — but the WHO-cGMP regulatory capital and 50-country registration footprint are real barriers to anyone trying to replicate Fredun's emerging-markets footprint quickly. And rivalry is, for now, geography-fragmented enough that it doesn't compress margins the way US rivalry does.

The picture that emerges is consistent. Fredun has structural advantages that are real, multi-layered, and getting deeper as the New Age segments scale. It does not have the brute-force advantages of a Sun Pharma. But it doesn't need them — it is competing in a different game.

VIII. The Playbook: Business & Investing Lessons

Step back from the specific Fredun facts for a moment, and the company turns out to be a clean case study of three separate playbooks executed simultaneously. They are worth naming, because the same patterns appear in successful small-cap healthcare companies across emerging markets — and recognising them in real time is half the battle for long-term investors.

The first is the "Niche Master" playbook. The conventional Indian generics narrative since the late 1990s has been a US-or-bust story: get ANDAs, fight Para IV battles, build US distribution, grow into a multibillion-dollar company by riding the largest pharmaceutical market on earth. That playbook still works for the giants. But for a sub-thousand-crore-revenue company in 2026, fighting Sun, Cipla, Aurobindo, and Indian-listed competitors plus Teva and Sandoz on US soil is a recipe for capital incineration. Fredun's choice — Africa, Southeast Asia, Latin America, where regulatory complexity creates a moat against amateurs and pricing power has not been crushed by FDA-driven price erosion — is not a default-to-easier choice. It is a deliberate selection of markets where the capital efficiency of the next dollar invested is materially higher than the equivalent dollar fighting in the US. The lesson: don't fight giants where their advantages are strongest. Build a kingdom where they're not paying attention.

The second is the "Value Chain Climb" playbook. For three decades, Fredun was a step-three player in a five-step pharmaceutical value chain — API supply, formulation, branding, distribution, customer relationship. It made the pill; somebody else owned the customer. Step by step, the company has climbed: from making generics for others, to making and selling its own branded generics in emerging markets, to building proprietary brands in adjacent categories (Freossi, Bird n Beauty, BeautyFred), to — with Wagr — directly owning the customer interface for an entire vertical. Each rung up the value chain captures more economics per unit of underlying product, and each rung makes the next rung structurally easier because the brand and the customer relationship are the inputs to the next move. The lesson: the long-term compounders in any commoditised industry are the ones who systematically refuse to stay in the commodity layer.

The third is the "Inorganic Growth Done Right" playbook. The Wagr acquisition is the cleanest possible illustration. There are two ways to do M&A in a small-cap. The bad way is to write a check at peak valuation, take on debt, dilute equity, and pray that the cultural integration works out. The graveyard of Indian small-caps is full of companies that took this path. The good way is to use M&A as a talent-and-IP acquisition mechanism, structuring deals so the selling counterparty becomes a long-term partner in the combined upside. The cashless Wagr structure, where Fredun deployed equity in the new combined platform rather than cash on the existing balance sheet, did three things at once: it preserved Fredun's balance sheet for organic capex (the Palghar fifth facility, for example), it aligned the Wagr founders for a multi-year integration, and it brought the Wagr investors in as long-term holders rather than one-time sellers.2 The lesson: small-cap M&A is a tool for buying talent and capability, not revenue. If the deal structure prioritises "consolidating top line" it will destroy value; if it prioritises "buying capability the company couldn't build in-house" it can compound for years.

There is a fourth pattern worth flagging because it shows up in everything Fredun does, even though it is not formally part of the playbook taxonomy: capital discipline matched to growth. Most small-cap promoters either underinvest (and stagnate) or overinvest (and dilute aggressively). Fredun has run a different cadence: modest preferential issuances, promoter participation in those issuances, debt levels that have stayed manageable as a percentage of revenue, and capex announcements (the fifth Palghar block) that match the pace at which the company can actually fill the new capacity. The discipline is reflected in the financial metrics — ROCE of 19% and ROE of 15.8% are strong for a company that is also growing 30%+, because growth has not been bought at the expense of return on capital.3 In a sector where it is depressingly common to see ROCE fall as revenue grows, that combination is meaningful.

Take all four together and you have, in essence, the operating manual for how a 1987-vintage contract manufacturer becomes a relevant healthcare brand company in 2026. None of the moves required heroic insight. They required patience, discipline, and a willingness to do unfashionable things — like building emerging-market export rails when everyone else was chasing the US, or buying a pet-tech startup with stock instead of cash when the market expected another expensive headline acquisition.

IX. Bear vs. Bull Case

Every investment narrative has a bull case so seductive it is almost embarrassing to write it out, and a bear case so plausible it should keep the bulls humble. Fredun's are unusually clear, which is itself a useful feature — clarity at this size is rare.

Myth vs. Reality. The first thing to clear out is the consensus framing. The bull pitch on Fredun in financial media has tended toward "small-cap pharma riding pet humanisation tailwinds" — a soft, demographic-tailwind story. The bear pitch in the comment sections of brokerage forums has tended toward "tiny pharma stretching into segments it has no business being in." Both miss the point. The reality is that Fredun is neither a pure pharma compounder nor a pet-tech startup: it is a manufacturing-and-distribution platform deliberately reweighting toward higher-margin branded categories, using a single physical asset (Palghar) and a cashless M&A structure to fund the transition. The investment question is whether that reweighting plays out at the pace and margin profile management implies — not whether dogs are cute.

The Bull Case. The most aggressive bull case rests on three assumptions stacking. One: legacy human formulations continue to grow at 15%-ish CAGR, extending the export footprint without major margin compression — defensible given the diversified geographic mix. Two: New Age segments (animal health, nutraceuticals, cosmeceuticals, pet platform) grow at 25%+ CAGR and reach majority of revenue by FY30 — the management roadmap. Three: gross margin and EBITDA margin expand by another 200–400 basis points as the New Age mix dominates, taking EBITDA margin from the current ~15% area into the high teens. If those three stack, you get a revenue trajectory that takes the company well past current scale, with an EBITDA growth rate that runs ahead of revenue growth — the textbook definition of operating leverage. The pet-care platform is the call option on top: if Wagr's relaunch in FY26 and FY27 builds a defensible marketplace at scale, the platform carries a different valuation multiple than the pharmaceuticals base. The bull view treats the company as a branded healthcare platform, not a generics manufacturer.

The Bear Case. Three risks, in declining order of weight. First and most material: working capital intensity in emerging-market exports. Selling formulations into 50+ countries at 30%+ revenue growth means receivables that are growing fast and not always at the cleanest payment terms. The H1 FY26 numbers showed strong P&L growth, but the balance sheet trajectory — borrowings of ₹171 crore at the September 2025 cut — is something to watch as the company scales.3 If working capital cycles stretch faster than EBITDA, the cash conversion deteriorates and the equity story becomes a debt story. Second: regulatory risk in the emerging-market footprint. Fifty countries is fifty different regulatory regimes; a single major market — say, Nigeria, or Kenya, or Brazil — imposing a new local-content rule, currency restriction, or registration freeze can disproportionately affect the export segment. Diversification mitigates the worst-case but does not eliminate the cluster risk. Third, and the most novel: execution risk on the pet-tech platform. Wagr is not just a brand integration; it is a tech platform that must scale in users, transactions, and gross merchandise value. A pharmaceutical company has never run a marketplace at scale in India. The Q4 FY26 marketplace relaunch and the FY27 device relaunch are the binary execution events that will validate or falsify the platform thesis.

There are also some second-layer diligence items worth holding in mind. The Infomerics credit rating environment around Fredun has been stable-to-improving over recent cycles, which is consistent with the financial trajectory.16 The promoter group has been net buyers, not sellers, which is structurally bullish but should still be checked at every shareholding pattern release. The auditor has been R.H. Nisar & Co., and the H1 FY26 limited review was completed without material misstatements flagged.14 None of those are red flags; they are simply the standard hygiene checks that distinguish a real compounder from a paper one.

KPIs to Watch. If you can track only two or three things on Fredun, track these. First, EBITDA margin trajectory — the cleanest single proxy for whether the New Age mix-shift is actually translating into the operating leverage management has implied. Reported margins have gone from 11% (FY24) to ~15% (H1 FY26); the question is whether the next thousand basis points come at the same trajectory or stall.35 Second, the share of New Age segments in consolidated revenue — disclosed in the annual report and quarterly investor updates. The 51% target by FY30 is the central thesis number; deviation from that path either way is signal. Third, for those who care about the platform call option specifically, Wagr platform engagement metrics post-relaunch — registered pet parents, transactions, and gross merchandise value run-rate. These will be the leading indicators for whether the Hamilton Helmer "switching costs" power is actually being built or just claimed.

X. Conclusion & Final Reflections

The most striking thing about Fredun Pharmaceuticals in 2026 is how unspectacular it looks from a distance. There is no charismatic billionaire promoter, no headline-grabbing US generics fight, no IPO roadshow drama, no government-of-India strategic-priority designation. Just a Palghar plant, a multi-decade founder, a son who took the wheel a decade ago, and a slowly-widening fan of branded healthcare segments radiating out from the legacy manufacturing core.

And yet, when you stack up the elements — five-year profit CAGR north of 60%, ROCE north of 19%, EBITDA margin expanding 170+ basis points in a single half-year, promoters paying real cash to increase their stake at premium prices, a cashless acquisition that gave the company India's first end-to-end pet-care platform without touching the cash balance, a manufacturing footprint that is being deliberately concentrated for scale economies — what emerges is one of the more competently engineered small-cap healthcare stories on the BSE.358 Not the loudest. Not the largest. But, by most measures of capital allocation discipline, structural advantage construction, and management alignment, one that meets the criteria long-term fundamental investors look for in the early innings of a compounding story.

The bigger reflection is about what kind of company can emerge in Indian healthcare in this decade. The 1990s belonged to the reverse-engineering generics champions. The 2000s belonged to the US-ANDA expansion specialists. The 2010s belonged to the specialty and biosimilar pioneers. The 2020s, increasingly, will belong to the platform builders — the companies that figure out how to combine regulated manufacturing, multi-segment branded portfolios, and direct customer relationships into something durable. That is exactly what Fredun has spent the last decade quietly assembling.

Whether the company hits its FY30 ambitions is a question for the next four annual reports. The pet-tech relaunches in Q4 FY26 and FY27, the Palghar fifth-facility commissioning by October 2026, and the trajectory of New Age segment contribution will all matter.1113 But the underlying machine — the manufacturing discipline, the geographic diversification, the cashless M&A structure, the promoter alignment — is already in place. The contract manufacturer of 1987 and the pet-care platform of 2026 are, on the surface, almost unrecognisably different businesses. The thread that connects them is the Medhora family's willingness, across two generations, to keep climbing the value chain when staying still would have been easier. That, more than the dog biscuits or the GPS collars, is the actual story.

References

-

Fredun Pharmaceuticals Acquires Wagr.ai — ANI News, 2025-10-10 ↩↩↩

-

Fredun Pharma acquires Wagr.ai — tal64.com (Priyadarshan Banjan) ↩↩↩↩↩↩↩

-

Fredun Pharmaceuticals Ltd — Screener.in company page ↩↩↩↩↩↩↩↩↩↩↩

-

Fredun Pharmaceuticals Acquires Wagr.ai, Launching India's First Neutral Pet Care Marketplace — SmallCap Spotlight ↩↩

-

Fredun Pharmaceuticals Reports 61% YoY Growth in EBITDA to INR 39.33 Cr in H1 FY26 — The Tribune ↩↩↩↩

-

Fredun Pharmaceuticals Reports 128% Surge in Q2 Profit, Revenue Up 45% — ScanX ↩

-

Fredun Pharma Promoters Raise Stake to 45.54% via Warrant Conversion — Whalesbook ↩↩↩↩↩

-

Fredun Pharmaceuticals launches 'Snacky Jain' for pets — Business Standard, 2025-10-13 ↩

-

Pharma stock jumps over 5% after foraying into animal veterinary segment — Trade Brains ↩

-

Fredun Pharmaceuticals Expands Manufacturing Base with Fifth Facility at Palghar — ANI News, 2026-04-29 ↩↩↩

-

Wagr raises Rs 4.2 cr led by Inflection Point Ventures — Free Press Journal ↩

-

Fredun Pharmaceuticals Acquires Wagr.ai — BSE Filing PDF, 2025-10-09 ↩↩

-

Fredun Pharmaceuticals Reports Robust Q2 FY26 Growth Amid Expansion Plans — Devdiscourse ↩↩

-

Fredun Pharma Issues 40,000 Shares To Promoter After Warrant Conversion At ₹1,250 — ScanX ↩

-

Fredun Pharmaceuticals Limited — Infomerics Ratings Press Release, 2024-03-04 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube