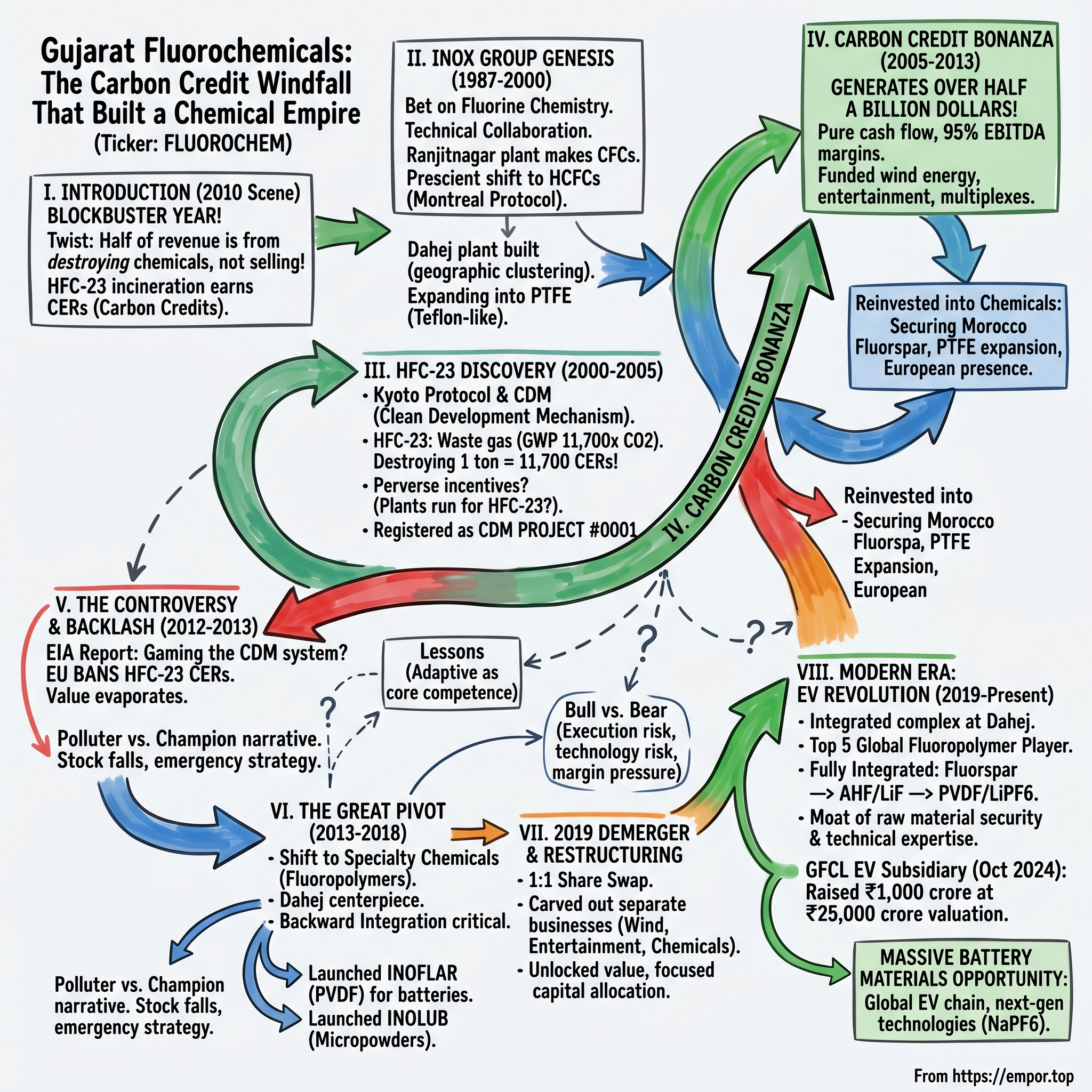

Gujarat Fluorochemicals: The Carbon Credit Windfall That Built a Chemical Empire

I. Introduction & Opening Scene

Picture this: It's 2010, and a chemicals company in Gujarat is celebrating another blockbuster year. But here's the twist—nearly half their revenue isn't from selling chemicals at all. It's from destroying them.

Gujarat Fluorochemicals Limited had stumbled upon one of the most lucrative regulatory arbitrages in corporate history. By incinerating a waste gas called HFC-23—a byproduct so potent that one ton equals 11,700 tons of CO2 in greenhouse effect—they were minting money through carbon credits. Between 2005 and 2013, this single activity generated over half a billion dollars. The company was literally getting paid to burn trash, and getting paid handsomely.

This is the story of how a refrigerant manufacturer rode the carbon credit gold rush to build one of India's most valuable chemical empires, only to face the music when European regulators pulled the plug on what environmentalists called "perverse incentives." It's a tale of regulatory arbitrage at industrial scale, strategic reinvestment of windfall profits, and ultimately, corporate reinvention when the party ended.

Why does this matter? Because Gujarat Fluorochemicals represents something profound about modern capitalism: how temporary regulatory frameworks can create massive wealth transfers, how smart management teams use windfalls to build lasting businesses, and how companies can successfully pivot when their cash cow gets slaughtered. Today, with a market cap of ₹40,710 crores, GFL stands as one of the top five global players in fluoropolymers—a position built on the foundation of what critics called an environmental accounting trick.

The journey from CDM Project #0001 to fluoropolymer powerhouse is a masterclass in turning regulatory windows into permanent competitive advantages. Let's dive into how a company that once made more money from waste disposal than product sales transformed itself into a critical supplier for everything from semiconductors to electric vehicle batteries.

II. The INOX Group Genesis & Early Days (1987-2000)

The year was 1987, and India was still navigating the twilight of the License Raj. In this environment of controlled capitalism, a new company was incorporated as a subsidiary of Inox Leasing and Finance Limited—Gujarat Fluorochemicals. The INOX Group, helmed by the Jain family, had ambitions beyond typical Indian conglomerates. They weren't looking at textiles or steel; they were betting on specialty chemicals, specifically the arcane world of fluorine chemistry.

The following year, 1988, GFL launched its public issue—a modest affair by today's standards but significant for a specialty chemicals venture in that era. The proceeds went toward establishing a manufacturing plant at Ranjitnagar, near the small town of Ghoghamba in Panchmahal district. This wasn't just any chemical plant; it was designed to produce chlorofluorocarbon (CFC) refrigerant gases, entering into a technical collaboration with Stauffer Chemicals' Pennwalt Corporation, an American giant in fluorochemicals.

The timing was prescient, if accidental. The Montreal Protocol had just been signed in 1987, setting the stage for the phase-out of ozone-depleting CFCs. While this might seem like bad news for a CFC manufacturer, it actually positioned GFL perfectly for the transition to hydrochlorofluorocarbons (HCFCs) and eventually hydrofluorocarbons (HFCs)—the next generation of refrigerants.

By 1991, GFL commissioned its first manufacturing facility in Dahej, Gujarat's emerging chemical hub. This wasn't just geographic expansion; it was product diversification. The Dahej facility would become the cornerstone of their fluoropolymer ambitions. Five years later, in 1996, they expanded into specialty fluoropolymers, including polytetrafluoroethylene (PTFE)—better known by DuPont's brand name, Teflon.

The 1990s Indian chemical landscape was dominated by commodity players and subsidiaries of multinationals. GFL was charting a different course. While others competed on volume and price in basic chemicals, the company was building technical expertise in fluorine chemistry—one of the most challenging and dangerous branches of chemical engineering. Fluorine is so reactive it can burn through glass and concrete; handling it requires specialized equipment and deep technical knowledge.

What made fluorochemicals attractive wasn't just their complexity but their criticality. Refrigerants were essential for India's growing middle class acquiring their first refrigerators and air conditioners. PTFE was finding applications everywhere from non-stick cookware to industrial gaskets. The company was positioning itself at the intersection of India's consumption boom and industrial modernization.

The strategic framework was clear even then: backward integration for raw material security, forward integration for value addition, and geographic clustering for operational efficiency. The Ranjitnagar plant handled refrigerants; Dahej focused on polymers. Each facility developed its own expertise while sharing overhead and management resources.

By 2000, GFL had established itself as India's leading fluorochemicals player. Revenue had grown steadily, operations were profitable, and the technical capabilities were world-class. But what came next would transform this respectable chemical company into something entirely different—a carbon credit machine that would generate more profits from environmental accounting than from selling products.

III. The HFC-23 Discovery: Turning Waste into Gold (2000-2005)

The Kyoto Protocol, signed in 1997 and entering into force in 2005, created something unprecedented in industrial history: a global market for not producing pollution. Under its Clean Development Mechanism (CDM), companies in developing countries could earn Certified Emission Reductions (CERs)—carbon credits—by reducing greenhouse gas emissions. These credits could then be sold to companies in developed nations struggling to meet their emission targets.

For most industrial companies, CDM was a nice-to-have, a way to offset some environmental compliance costs. For Gujarat Fluorochemicals, it was about to become a goldmine.

Here's where chemistry meets finance in spectacular fashion. GFL operated an HCFC-22 plant—HCFC-22 being a common refrigerant used in air conditioners. The production process inevitably created a byproduct: HFC-23, or trifluoromethane. This waste gas had no commercial use and was simply vented into the atmosphere. Standard practice, completely legal, done by every HCFC-22 manufacturer globally.

But HFC-23 had a peculiar property: its global warming potential was 11,700 times that of CO2. One ton of HFC-23 in the atmosphere was equivalent to releasing 11,700 tons of carbon dioxide. Under CDM rules, destroying that one ton of HFC-23 would earn 11,700 carbon credits.

The math was staggering. Carbon credits were trading at €10-20 per ton of CO2 equivalent. Destroying one ton of HFC-23 could generate €117,000 to €234,000 in carbon credit revenue. The cost of installing and operating a thermal oxidizer to destroy HFC-23? A few thousand dollars per ton at most. The margin was essentially 98%.

GFL's management team, led by the Jain family, recognized this opportunity earlier than most. They moved swiftly to register their HFC-23 destruction project with the UN's CDM Executive Board. The registration number speaks volumes: CDM Project #0001. They weren't just early; they were first.

The thermal oxidation system was relatively simple—essentially a high-temperature incinerator that broke down HFC-23 into less harmful compounds. The capital investment was modest, perhaps a few million dollars. The operational costs were minimal. But the revenue potential was extraordinary.

Between project registration and credit issuance, GFL had to navigate a complex verification process. UN-appointed auditors would verify baseline emissions, monitor destruction rates, and certify the credits. Every molecule of HFC-23 destroyed had to be documented, measured, and validated. The company built sophisticated monitoring systems, hired environmental consultants, and created an entire division dedicated to carbon credit management.

What made this particularly lucrative was the perverse incentive structure. The more HCFC-22 you produced, the more HFC-23 byproduct you generated, and the more carbon credits you could earn. Some critics would later argue that plants were being run not to meet refrigerant demand but to maximize HFC-23 generation. GFL and others vehemently denied these allegations, but the incentive alignment was undeniable.

By 2005, as the Kyoto Protocol came into force and carbon credit trading began in earnest, GFL was perfectly positioned. They had the first-mover advantage, operational systems in place, and verified credits ready to sell. The transformation from chemical manufacturer to carbon credit generator was complete. What followed would be eight years of unprecedented profitability that would fundamentally reshape the company's trajectory.

IV. The Carbon Credit Bonanza Years (2005-2013)

The numbers tell a story of corporate alchemy. Between 2005 and 2013, Gujarat Fluorochemicals' CDM project was awarded more than 55 million carbon offset credits. At prevailing prices, these credits generated over half a billion US dollars in revenue. To put this in perspective, the company's entire chemical operations—the plants, the products, the decades of manufacturing expertise—were generating less revenue than the simple act of destroying a waste gas.

The cash flow dynamics were unlike anything in traditional manufacturing. Chemical plants require constant working capital—raw material purchases, inventory management, customer credit periods. Carbon credits were pure cash. Once verified and issued, they could be sold immediately to European utilities and trading houses desperate to meet their Kyoto commitments. No inventory, no receivables, no working capital. Just wire transfers hitting the bank account.

In fiscal year 2009-2010, carbon credit sales accounted for nearly 50% of GFL's total revenue. The EBITDA margins on these sales approached 95%. The company was generating more free cash flow than it knew what to do with—a problem most CFOs dream of but few experience.

The Jain family and GFL's management team faced a critical decision: what to do with this windfall? They could have paid special dividends, bought back shares, or simply accumulated cash. Instead, they chose to build.

The reinvestment strategy was methodical and ambitious. In 2009, using carbon credit proceeds, GFL incorporated wholly-owned subsidiaries in the Americas. The same year, the INOX Group launched Inox Wind Limited, betting that renewable energy would be India's next growth frontier. The timing was perfect—wind turbine installations in India were about to explode, driven by renewable purchase obligations and accelerated depreciation benefits.

The entertainment business, Inox Leisure, which had been struggling since its 1999 inception, suddenly found itself flush with capital for multiplex expansion. What started as a small chain of theaters would grow into one of India's largest multiplex operators, all funded by HFC-23 destruction.

But the most strategic investments went back into chemicals. In 2011, GFL entered into a joint venture with Moroccan companies for a fluorspar beneficiation project. Fluorspar is the primary raw material for all fluorochemicals—whoever controls fluorspar controls the entire value chain. While competitors were celebrating carbon credit revenues, GFL was quietly securing raw material sources that would matter long after carbon credits disappeared.

The company launched HFC-134a production in 2005, anticipating the automotive air conditioning market's transition away from older refrigerants. They expanded PTFE capacity at Dahej, added new fluoropolymer grades, and built technical capabilities in specialty applications. Every expansion was funded by carbon credits, but designed for a post-carbon credit world.

The German subsidiary, incorporated in 2013, was particularly strategic. Europe was both the largest buyer of carbon credits and a major market for specialty fluoropolymers. Having a European presence allowed GFL to serve customers directly, understand application requirements, and build technical partnerships that would outlast the CDM mechanism.

Throughout this period, GFL's stock price reflected the carbon credit bonanza. Investors valued the company not as a chemical manufacturer but as a carbon credit generator with a chemical business attached. The P/E multiples were astronomical for an industrial company, but perhaps justified for what was essentially a regulatory arbitrage machine printing money.

Yet beneath the carbon credit headlines, a transformation was occurring. The company was using its windfall to build one of the most integrated fluorochemical operations outside of China and the developed world. They were acquiring technology, developing products, and building customer relationships that would matter when the music stopped.

And stop it would. By 2012, European environmental groups were raising alarms about the HFC-23 credit system. They argued, with increasing support from data, that the CDM was creating perverse incentives—companies were producing HCFC-22 not to meet refrigerant demand but to generate HFC-23 for destruction. The European Union, the largest buyer of these credits, was listening. The countdown to the end of the carbon credit era had begun.

V. The Controversy & Regulatory Backlash

The Environmental Investigation Agency (EIA) report landed like a bombshell in 2012. Titled "Offsetting Lives," it accused chemical companies in India and China of gaming the CDM system—deliberately producing excess HCFC-22 to maximize HFC-23 generation and carbon credit revenues. The report included damning charts showing HCFC-22 production spiking far above market demand, particularly at facilities with CDM projects.

The accusations were serious and specific. Plants were allegedly operating at low efficiency to maximize HFC-23 generation, running production lines that would otherwise be uneconomical, and timing production to coincide with carbon credit verification periods. The EIA calculated that the carbon credit revenues were so lucrative that companies could give away HCFC-22 for free and still make enormous profits from HFC-23 destruction.

GFL and other Indian fluorochemical companies pushed back hard. They argued that HCFC-22 demand was genuinely growing in India and other developing countries, that their production was driven by market needs, not carbon credits, and that the CDM was working exactly as intended—incentivizing emission reductions in developing countries.

But the political momentum in Europe was unstoppable. Environmental groups had found their villain—industrial companies profiting from a system meant to combat climate change. The narrative was compelling: European consumers were paying higher electricity bills to fund carbon credits that were enriching chemical companies while potentially increasing overall emissions.

In January 2013, the European Commission announced its decision: from May 1, 2013, the EU Emissions Trading System would no longer accept CERs from HFC-23 destruction projects. The decision was final, non-negotiable, and devastating. Europe represented over 80% of the global carbon credit market. Without European buyers, HFC-23 credits were essentially worthless.

The numbers were staggering. CDM Watch, an environmental NGO, estimated that Indian and Chinese chemical companies stood to lose $1.5 billion in carbon credit revenues. For GFL specifically, this meant the evaporation of hundreds of crores in annual revenue—money that required no raw materials, no manufacturing, no marketing, just the operation of a thermal oxidizer.

The local environmental controversies added another dimension to the crisis. Communities near GFL's plants had long complained about emissions, water pollution, and health impacts. While the company maintained that it operated within all regulatory requirements, the carbon credit controversy emboldened local activists. The narrative shifted from GFL as an environmental champion destroying greenhouse gases to GFL as a polluter profiting from environmental regulations.

The stock market reaction was swift and brutal. GFL's share price, which had been riding high on carbon credit revenues, began a steady decline as investors grappled with the post-carbon credit reality. Analysts scrambled to revalue the company based solely on its chemical operations—a business that suddenly looked far less attractive without the carbon credit subsidy.

Inside GFL's headquarters, emergency strategy sessions were convened. The company had known this day might come—the strategic investments in chemicals, wind energy, and entertainment were partly insurance against this scenario. But the speed and completeness of the European ban caught everyone off guard. There was no phase-out period, no grandfathering of existing projects, just a hard stop.

The immediate financial impact was severe but manageable—the company had built substantial reserves from eight years of carbon credit sales. The strategic impact was more complex. GFL had to transform from a carbon credit company with chemical operations to a pure-play chemical company competing on product quality, cost, and innovation rather than regulatory arbitrage.

The era of easy money was over. What remained was a test of whether the investments made during the bonanza years had created a sustainable competitive advantage, or whether GFL would struggle without its carbon credit crutch. The next phase of the company's evolution would answer that question definitively.

VI. The Great Pivot: From Credits to Chemicals (2013-2018)

The morning of May 1, 2013, marked a new reality for Gujarat Fluorochemicals. The carbon credit tap had been turned off completely. But unlike a distressed company scrambling for survival, GFL's management team executed a pivot they had been preparing for years. The strategic investments made during the carbon credit windfall were about to be tested.

The shift to fluoropolymers and specialty chemicals wasn't reactive—it was the acceleration of a plan already in motion. The company's Dahej facility, commissioned back in 1991 and expanded in 1996 for specialty fluoropolymers, became the centerpiece of the new strategy. While competitors were still mourning the loss of carbon credits, GFL was shipping PTFE micropowders to European manufacturers, FKM rubber to automotive companies, and PVDF resins to chemical processors.

The backward integration strategy proved particularly prescient. The 2011 joint venture with Moroccan companies for fluorspar beneficiation now looked genius. Fluorspar, the essential raw material for all fluorochemicals, was becoming increasingly scarce. China, which controlled 60% of global fluorspar production, was restricting exports. Having secured access to Moroccan fluorspar, GFL could guarantee raw material availability while competitors scrambled for supplies.

In 2013, just as carbon credits ended, GFL launched INOFLAR, their brand of PVDF (polyvinylidene fluoride). PVDF was a high-performance polymer used in chemical processing, lithium-ion batteries, and water treatment membranes. The timing was fortuitous—the lithium-ion battery market was beginning its exponential growth phase, driven by smartphones and the early stages of electric vehicle adoption.

The transformation required more than just product launches; it demanded a fundamental restructuring of the organization. The carbon credit division was disbanded, its employees redeployed to chemical operations and business development. The company hired polymer engineers from competitors, application specialists from customer industries, and sales professionals with global experience. GFL was rebuilding itself as a technology-driven chemical company.

By 2018, the transformation was evident in the numbers. Chemical revenues had grown to fill much of the gap left by carbon credits. More importantly, the company had diversified its customer base globally—no longer dependent on European carbon credit buyers, GFL was selling to chemical processors in Germany, automotive manufacturers in Japan, and battery producers in South Korea.

The launch of INOLUB in 2018 marked a significant milestone. These PTFE micropowders were highly specialized additives used in high-performance plastics, inks, and coatings. The technology required to produce consistent, high-quality micropowders was sophisticated—particle size distribution, surface modification, and purity levels all had to be precisely controlled. GFL had moved from commodity chemicals to specialty products where technology and quality mattered more than just price.

The financial metrics during this transition period told a story of successful but costly transformation. Margins compressed as chemical operations could never match the 95% EBITDA margins of carbon credits. Capital expenditure increased as new plants and technologies required substantial investment. Return on equity declined from the astronomical levels of the carbon credit era to more pedestrian industrial company levels.

Yet what emerged was arguably more valuable than carbon credit revenues—a sustainable, technology-driven business with genuine competitive advantages. The company had used its windfall wisely, building capabilities that would endure long after regulatory arbitrage opportunities disappeared. The stage was set for the next phase: corporate restructuring to unlock the value that had been created.

VII. The 2019 Demerger & Corporate Restructuring

The INOX Group had a problem—a good problem, but a problem nonetheless. They had built three distinct businesses under the GFL umbrella: chemicals, wind energy, and entertainment. Each business had different capital requirements, growth trajectories, and investor bases. The conglomerate structure that had made sense during the carbon credit era—when cash from HFC-23 destruction could fund diverse ventures—no longer served any strategic purpose.

The demerger announced in 2019 was surgical in its precision. The chemical business would be carved out from the original GFL Ltd and placed into a new entity, initially called Inox Fluorochemicals Limited. In a move that confused some but delighted tax advisors, this new entity would then take on the Gujarat Fluorochemicals Limited name, while the original GFL would be renamed. Shareholders would receive one share of the new chemical-focused GFL for every share of the old conglomerate GFL they owned—a clean 1:1 swap.

Why go through this complex corporate restructuring? The answer lay in valuation and capital allocation. Chemical companies trade at different multiples than wind energy or entertainment businesses. Investors interested in specialty chemicals had no interest in multiplex theaters; renewable energy funds couldn't invest in a company where chemicals dominated the revenue. The conglomerate discount—where the whole is valued less than the sum of its parts—was becoming increasingly apparent.

The demerger also solved a capital allocation problem. The chemical business was entering a heavy investment phase, with new capacities planned for battery materials and specialty polymers. Wind energy needed capital for turbine manufacturing expansion. Entertainment required funds for digital transformation and new screen additions. Under the conglomerate structure, every investment decision became a zero-sum game between divisions. Post-demerger, each business could raise capital independently, aligned with its specific needs and investor base.

For minority shareholders, the demerger was generally well-received. They could now choose their exposure—keep all three businesses, sell one or two, or adjust weightings based on their investment thesis. The market responded positively, with the combined market capitalization of the demerged entities exceeding the pre-demerger conglomerate value within months.

The new Gujarat Fluorochemicals Limited that emerged from this restructuring was a pure-play fluorochemicals company for the first time in its history. No more explaining to chemical industry analysts why multiplex occupancy rates mattered. No more confusion about wind turbine order books affecting chemical valuations. The company could now be properly benchmarked against global fluorochemical peers like Solvay, Daikin, and Chemours.

Management structure and incentives were also aligned post-demerger. The chemical business got its own CEO, board, and employee stock options tied to chemical business performance. The focus sharpened dramatically—from managing a conglomerate to building a global fluorochemicals leader.

The timing of the demerger, completed in April 2019, proved fortuitous. Within a year, the COVID-19 pandemic would create massive volatility across industries. Having separate entities allowed each business to respond independently—the chemical business could focus on supply chain continuity for essential industries, while entertainment dealt with theater closures, and wind energy navigated project delays. The strategic flexibility provided by the demerger proved invaluable during the crisis.

VIII. Modern Era: Battery Materials & EV Revolution (2019-Present)

Today, Gujarat Fluorochemicals stands as one of the leading producers of Fluoro-polymers, Fluoro-specialities, Chemicals and Refrigerants in India. It is one of the top five global players in the fluoropolymers market with a market capitalization of ₹40,436 crores, revenue of ₹4,842 crores, and profit of ₹622 crores.

The transformation from carbon credit beneficiary to fluorochemicals powerhouse is most evident in the company's strategic positioning for the electric vehicle revolution. In October 2024, GFL's wholly-owned subsidiary, GFCL EV Products Ltd., raised ₹1,000 crore at a remarkable equity valuation of ₹25,000 crore—a valuation that speaks to investor confidence in the battery materials opportunity ahead.

The product portfolio has evolved dramatically from the refrigerant-focused days. GFL now has a diverse portfolio of fluoropolymers comprising PTFE, PFA, FEP, FKM, PVDF and fluoropolymer additives. More critically, with a fully integrated manufacturing process, including backward integration into anhydrous hydrogen fluoride (AHF), lithium fluoride (LiF), and captive fluorspar, GFCL EV offers a robust product portfolio encompassing battery chemicals (electrolyte salts, formulations, performance-enhancing additives), cathode active materials (LFP), and binders (PVDF and PTFE).

The battery materials opportunity is massive. The global market for EV battery chains is projected to reach $300 billion by 2030. Global lithium battery demand is expected to surge from approximately 1,100 GWh to 5,000-6,000 GWh by 2030. GFL's subsidiary has committed to substantial investments to capture this opportunity—announcing an investment of INR 6000 crore (₹60 billion) over the next 4-5 years to enable the global supply of ~200GWh EV and ESS battery solutions.

The technical capabilities built over decades now position GFL uniquely in the battery supply chain. The company's integrated battery chemicals complex at Dahej in Gujarat is nearing completion, which is expected to produce LiPF6, an important electrolyte salt meant for lithium-ion batteries, with an initial capacity of 1,800 tonnes per annum in the first phase. LiPF6 is one of the most critical and technically challenging components of lithium-ion batteries—its production requires handling extremely corrosive hydrogen fluoride and maintaining ultra-high purity standards.

Beyond traditional lithium-ion chemistry, GFL is positioning for next-generation technologies. GFCL EV's current product portfolio includes electrolyte salts LiPF6, additives, electrolyte formulations, cathode active materials such as LFP, and cathode binders such as PVDF and PTFE along with specialized offerings of NaPF6 for sodium-ion batteries and proprietary additives for fast charging. This diversification across battery chemistries provides optionality as the energy storage market evolves.

The company's global footprint has expanded significantly. With three manufacturing facilities in India, a captive fluorspar mine in Morocco, offices and warehouses in Europe and the USA, and a marketing network spread across the world, GFL has transformed from an Indian chemical company to a global fluorochemicals player. The recent incorporation of a German subsidiary in 2024 further strengthens their European presence, critical for serving the rapidly growing European EV market.

The investment in research and development has been substantial. The product innovation thrust aims at application development at two fully-equipped modern research centres at Dahej and Ranjitnagar, Gujarat. These facilities aren't just testing labs but application development centers where GFL works with customers to develop specialized grades and formulations for specific applications—a capability that differentiates them from commodity chemical producers.

The financial transformation, while less spectacular than the carbon credit era, shows a sustainable business model emerging. Gujarat Fluorochemicals' revenue jumped 10.04% year-over-year to ₹1,304 crores in Q1 2025-2026, with net profit jumping 70.37% to ₹184 crores. While the company has a low return on equity of 13.4% over the last 3 years—a far cry from the carbon credit days—this reflects the heavy investment phase as the company builds capacity for the battery materials opportunity.

The strategic bet on vertical integration continues to pay dividends. Having secured fluorspar through the Moroccan joint venture, built backward integration into AHF and LiF, and forward integration into specialized products, GFL has created a moat that's difficult for new entrants to replicate. In an industry where raw material security and technical expertise determine success, these investments made during the carbon credit windfall now provide sustainable competitive advantages.

IX. Investment Analysis & Financial Deep Dive

The financial evolution of Gujarat Fluorochemicals tells two distinct stories: the extraordinary carbon credit era and the current reality of building a specialty chemicals business. Understanding both is crucial for evaluating the investment case today.

During the carbon credit bonanza (2005-2013), GFL's cash flow statement read like a software company's rather than a chemical manufacturer's. Carbon credits required minimal working capital, generated 95% EBITDA margins, and converted immediately to cash. The company was essentially printing money through regulatory arbitrage, generating over $500 million from destroying a waste gas that cost perhaps $10 million to incinerate.

The post-2013 reality is starkly different. In the fiscal year ending March 31, 2024, Gujarat Fluorochemicals had annual revenue of ₹42.81 billion, down 24.70%. The decline reflects both the base effect of losing carbon credit revenues and the cyclical downturn in certain chemical segments. More concerning for investors, profit margin fell to 10.0% (down from 23% in FY 2023), with EPS declining to ₹39.60 (down from ₹121 in FY 2023).

The cash flow dynamics have fundamentally changed. Chemical operations require substantial working capital—raw material inventory, customer credit periods, and operational cash cycles typical of manufacturing businesses. The company's cash flow from operations declined from ₹7,389 million in FY23 to ₹6,264 million in FY24, reflecting both lower profitability and increased working capital requirements.

Capital allocation has shifted dramatically toward growth investments. The company is in the midst of a massive capital expenditure cycle, with ₹60 billion planned over 4-5 years for battery materials, of which ₹6.5 billion was already invested by December 2023. This heavy reinvestment phase explains the low return on equity of 13.4% over the last 3 years—the company is essentially building tomorrow's earnings base today.

The balance sheet tells a story of transformation. Net debt has been increasing, reaching ₹1,766 crores as of March 2025. This leverage isn't concerning given the company's cash generation ability and the strategic nature of investments, but it represents a departure from the debt-free balance sheet of the carbon credit era.

Valuation multiples reflect market skepticism about the transition. Despite the massive battery materials opportunity, the stock trades at a significant discount to global fluorochemical peers like Chemours and Solvay. The market seems to be waiting for evidence that battery material investments will generate returns comparable to specialty chemical industry standards.

The dividend policy reflects management's confidence and capital allocation priorities. Dividend payout has been low at 5.64% of profits over the last 3 years, with retained earnings being plowed back into growth investments. The recent dividend of ₹3 per share represents a modest yield, suggesting management sees better returns from internal investment than cash distribution.

Analyst sentiment is notably divergent. Revenue is forecast to grow 23% annually on average during the next 2 years, compared to a 12% growth forecast for the Chemicals industry in India. Yet some analysts remain skeptical—UBS maintains a Sell rating, citing slow ramp-up in EV materials and cutting earnings estimates.

The working capital cycle deserves special attention. Unlike the carbon credit business, chemical operations tie up significant capital in inventory and receivables. The company maintains 60-90 days of raw material inventory, extends 45-60 days credit to customers, and manages supplier payments over 30-45 days. This working capital intensity means growth requires proportional increases in working capital funding.

Segment analysis reveals the transformation underway. Fluoropolymers now generate the highest margins, followed by specialty chemicals, with refrigerants being the most commoditized. The battery materials segment, while still small, shows the highest growth rates and commands premium valuations in subsidiary funding rounds.

The currency exposure adds another dimension. With significant exports to Europe and the US, plus imports of certain raw materials, GFL faces material foreign exchange risk. The company uses natural hedging where possible but remains exposed to major currency movements, particularly the Euro and US Dollar against the Rupee.

For investors, the key question isn't whether GFL can succeed in battery materials—the technical capabilities and customer relationships suggest they can. The question is whether the returns will justify the massive capital deployment and whether the timeline aligns with investor expectations. The next 2-3 years will be critical as battery material revenues scale and margins become apparent.

X. Playbook: Lessons in Regulatory Arbitrage & Reinvention

The Gujarat Fluorochemicals story offers a masterclass in corporate strategy that extends far beyond chemicals and carbon credits. It's a playbook for navigating regulatory windfalls, managing dramatic transitions, and building sustainable competitive advantages from temporary opportunities.

Lesson 1: Recognizing and Capturing Regulatory Arbitrage

GFL's management demonstrated exceptional foresight in recognizing the CDM opportunity early. They didn't stumble upon carbon credits; they actively pursued CDM Project #0001 status. The lesson: regulatory changes create massive wealth transfers, but only for those positioned to capture them. While competitors were focused on operational improvements yielding 2-3% margin gains, GFL captured a regulatory arbitrage worth 95% margins.

The key insight is that regulatory arbitrage opportunities are often hiding in plain sight. The Kyoto Protocol was public, the CDM mechanism was transparent, and the chemistry of HFC-23 was well-known. What separated GFL from others was the speed of execution and the willingness to invest in a seemingly bureaucratic UN certification process.

Lesson 2: The Temporary Nature of Regulatory Advantages

GFL's management seemed to understand from day one that carbon credits wouldn't last forever. Unlike companies that become dependent on subsidies or regulatory advantages, GFL treated carbon credits as a windfall to be invested, not a permanent revenue stream to be consumed. This mindset—that all regulatory advantages are temporary—shaped their entire capital allocation strategy.

The European ban in 2013 wasn't a surprise to management; it was an eventuality they had planned for. The lesson for other businesses: any revenue stream dependent on regulatory frameworks should be treated as finite. The question isn't if it will end, but when and how to prepare.

Lesson 3: Strategic Reinvestment of Windfall Profits

The most crucial decision GFL made was how to deploy carbon credit proceeds. They could have paid special dividends, bought back shares, or made unrelated acquisitions. Instead, they chose to build capabilities in their core business—fluorochemicals—while taking measured bets in adjacent areas like wind energy and entertainment.

The backward integration into fluorspar through the Moroccan JV was particularly astute. While carbon credits were flowing, GFL was securing the one raw material that would matter most post-carbon credits. They were using temporary profits to build permanent competitive advantages.

Lesson 4: Managing Stakeholder Expectations Through Transitions

The period from 2013-2019 was brutal for GFL's stock price and stakeholder confidence. Revenues collapsed, margins compressed, and the growth story seemed over. Yet management maintained consistent communication about the long-term strategy, continued investing in R&D and capacity, and gradually rebuilt credibility through operational execution.

The lesson: major transitions require years, not quarters. Management teams need to prepare stakeholders for extended periods of subpar financial performance while transformation investments mature. GFL's ability to maintain investor support through this transition—without activist interventions or hostile takeovers—speaks to their stakeholder management skills.

Lesson 5: Building Global Scale from Emerging Markets

GFL's expansion from an Indian manufacturer to a global player offers lessons for other emerging market companies. Rather than competing on cost alone, they focused on technical capabilities, customer relationships, and strategic assets (like the Moroccan fluorspar mine). The German and American subsidiaries weren't just sales offices but technical centers that could work directly with customers on application development.

The key insight: emerging market companies can build global scale, but it requires investing in capabilities that matter to global customers—quality, technical support, supply security—not just low prices.

Lesson 6: The Importance of Technical Moats

Fluorine chemistry is genuinely difficult. It's dangerous, requires specialized equipment, and demands deep technical expertise. GFL spent decades building these capabilities, creating a moat that's difficult for new entrants to cross. The lesson: in commodity-prone industries, technical complexity can be the best defense against competition.

The battery materials pivot leverages this same principle. LiPF6 production is technically challenging, requiring handling of hydrogen fluoride and maintaining ultra-high purity. GFL's decades of fluorine chemistry experience gives them advantages that battery companies or new entrants can't easily replicate.

Lesson 7: Vertical Integration as Strategic Defense

GFL's integration from fluorspar mining through to specialized fluoropolymers provides multiple strategic benefits: raw material security, quality control, cost advantages, and the ability to capture value across the chain. In an industry where China controls much of the raw material, this integration provides strategic resilience.

The lesson extends beyond chemicals: in industries with concentrated suppliers or critical raw materials, vertical integration can be the difference between thriving and surviving during supply shocks.

Lesson 8: The Conglomerate Question

The 2019 demerger decision offers insights into corporate structure. During the carbon credit era, the conglomerate structure made sense—excess cash needed deployment, and diversification reduced risk. Post-carbon credits, each business needed focused management and targeted capital. The demerger unlocked value by allowing each business to be valued appropriately.

The broader lesson: corporate structure should match business reality. Conglomerates make sense when there are genuine synergies or capital allocation advantages. When these disappear, simplification often unlocks value.

The Meta-Lesson: Adaptability as Core Competence

Perhaps the most important lesson from GFL's journey is that adaptability itself can be a core competence. The company that started making CFCs in 1987 successfully navigated the Montreal Protocol, captured the CDM opportunity, survived the carbon credit collapse, and is now positioning for the EV revolution. Each transition required different capabilities, strategies, and mindsets.

This adaptability wasn't accidental but cultivated through consistent investment in technical capabilities, maintaining financial flexibility, and building a culture that could handle dramatic change. For companies facing disruption—technological, regulatory, or competitive—GFL's playbook offers a template for not just surviving but thriving through transformation.

XI. Bear vs. Bull Case

Bull Case: The Fluorine Chemistry Platform for the Electric Age

The bulls see Gujarat Fluorochemicals as perfectly positioned for the electric vehicle and renewable energy revolution. Start with the market opportunity: the global EV battery supply chain is projected to reach $300 billion by 2030, with battery demand surging from 1,100 GWh to 5,000-6,000 GWh. GFL isn't trying to compete in commodity battery cells but focusing on high-value, technically complex materials where their fluorine chemistry expertise provides genuine differentiation.

The subsidiary valuation tells a compelling story. GFCL EV raised ₹1,000 crore at a ₹25,000 crore valuation—nearly 60% of the parent company's entire market cap. If sophisticated investors are willing to value just the battery materials business at these levels, the parent company appears significantly undervalued. This suggests the market hasn't fully appreciated the transformation underway.

The technical moat is real and deepening. Producing battery-grade LiPF6 requires handling hydrogen fluoride at extreme purity levels—capabilities that take years to develop and perfect. GFL's three decades of fluorine chemistry experience can't be replicated quickly. As one industry executive noted, "You can't just build a LiPF6 plant; you need years of experience handling HF safely and efficiently."

Vertical integration provides strategic resilience in an increasingly fragmented world. With their own fluorspar mine in Morocco, backward integration into AHF and LiF, and forward integration into specialized products, GFL controls their entire value chain. As geopolitical tensions increase and supply chains fragment, this integration becomes increasingly valuable.

The customer base is evolving favorably. GFL isn't just selling to chemical distributors anymore but directly to battery manufacturers, automotive OEMs, and energy storage companies. These customers value security of supply, technical support, and quality consistency—areas where GFL can differentiate beyond price.

The product portfolio extends beyond just EVs. PVDF is used in solar panel backsheets, hydrogen fuel cell membranes, and water treatment systems. PTFE finds applications in semiconductors, aerospace, and medical devices. The company is building a platform for multiple growth vectors, not betting everything on one technology.

Management's track record of capital allocation deserves credit. They recognized the carbon credit opportunity early, reinvested windfall profits wisely, and executed a complex demerger successfully. The same team is now deploying capital into battery materials with clear strategic logic.

The India advantage is understated. As global companies seek to diversify supply chains away from China, India becomes an increasingly attractive alternative. GFL offers the scale, technology, and track record that global customers need when making critical supply chain decisions.

Bear Case: The Costly Transition to Nowhere

The bears see a company struggling to justify massive capital investments with mediocre returns. Return on equity at 13.4% over three years is hardly impressive for a supposedly high-tech specialty chemicals company. The company is deploying ₹60 billion into battery materials, but there's no evidence yet that returns will exceed the cost of capital.

The revenue decline is concerning. Annual revenue fell 24.70% to ₹42.81 billion in fiscal 2024, and while some of this reflects carbon credit loss, it also suggests core chemical operations aren't growing fast enough to offset declines. The promised battery materials boom remains largely promise rather than reality.

Competition in battery materials is intensifying rapidly. Chinese producers have massive scale advantages, Korean and Japanese companies have deeper customer relationships, and well-funded startups are developing next-generation technologies. GFL is entering a brutal competitive landscape where being "good enough" won't suffice.

The technology risk is substantial. The company is betting heavily on LiPF6 and current lithium-ion chemistry, but battery technology is evolving rapidly. Solid-state batteries might not need liquid electrolytes. Sodium-ion batteries use different materials. Alternative chemistries could make GFL's investments obsolete before they generate adequate returns.

Environmental and regulatory risks haven't disappeared. The fluorochemicals industry faces increasing scrutiny over PFAS (per- and polyfluoroalkyl substances) contamination. European and US regulations are tightening. The company that once benefited from regulatory arbitrage could find itself on the wrong side of environmental regulations.

The execution risk in battery materials is significant. Building chemical plants is one thing; achieving the quality standards required for automotive batteries is another. A single quality issue could destroy customer relationships that take years to build. The company has no track record in serving automotive OEMs directly.

Margin pressure appears structural, not cyclical. Profit margins fell to 10.0% from 23%, and while management blames temporary factors, the reality is that commodity chemical dynamics are asserting themselves. Without carbon credits, GFL looks increasingly like a typical chemical company with typical returns.

The valuation already reflects significant optimism. Despite declining revenues and profits, the stock trades at premium multiples to book value. The market is pricing in successful execution of the battery materials strategy, leaving little room for error or delays.

The capital intensity is concerning. Unlike the carbon credit era, where capital generated extraordinary returns, the current investment phase requires massive capital for uncertain returns. The company is essentially betting its future on battery materials without clear evidence of competitive advantage.

The Verdict: A Calculated Bet on Transformation

Both cases have merit. The bulls are betting on successful execution of a logical strategy—leveraging fluorine chemistry expertise for the energy transition. The bears see a company struggling to replace easy carbon credit profits with difficult chemical manufacturing returns.

The truth likely lies somewhere between. GFL has real capabilities and genuine opportunities in battery materials, but the transition will be longer, costlier, and more difficult than bulls expect. The question for investors isn't whether GFL can succeed in battery materials—they probably can—but whether the returns will justify the risk and capital deployed.

The stock appears to be a bet on execution and timing. If battery material revenues scale quickly and margins prove sustainable, the current valuation will look cheap. If the transition takes longer or margins disappoint, the stock could languish for years. For risk-tolerant investors with long time horizons, the asymmetry might be attractive. For those seeking near-term catalysts or predictable returns, better opportunities likely exist elsewhere.

XII. Epilogue: What Would You Do?

Standing at the helm of Gujarat Fluorochemicals today, you face decisions that will define the company for the next decade. The carbon credit party is long over. The battery materials investment is committed but not yet proven. The core fluorochemicals business generates cash but faces commoditization pressure. What strategic choices would you make?

The Specialty vs. Commodity Dilemma

The fundamental tension in GFL's portfolio is between scale and specialization. Refrigerants like R-32 and R-125 are becoming increasingly commoditized, with Chinese producers dominating on cost. Yet these products generate significant revenue and utilize existing assets. Do you double down on specialty products with higher margins but smaller markets, or maintain scale in commodities while accepting lower returns?

The battery materials bet suggests management has chosen specialization, but the continued investment in refrigerant capacity suggests hedging. Perhaps the answer isn't either/or but a barbell strategy—maintain efficient commodity operations for cash generation while investing growth capital in specialties. The risk is being mediocre at both.

Geographic Expansion vs. Domestic Focus

India's chemical market is growing rapidly, driven by import substitution, pharmaceutical growth, and industrial expansion. Yet the most attractive opportunities in battery materials and specialty fluoropolymers are in developed markets—Europe, US, Japan, Korea. Where do you place your bets?

The subsidiary structure suggests a hybrid approach—manufacture in India for cost advantage, but maintain technical and commercial presence in developed markets. The challenge is building credibility with demanding customers who have alternatives. Can an Indian chemical company convince a German automotive OEM to depend on them for critical battery materials?

The Sustainability Imperative

The irony is palpable—a company that once profited from destroying greenhouse gases now faces scrutiny over environmental impact. Fluorochemicals are under increasing regulatory pressure, with PFAS regulations tightening globally. How do you position for a world that increasingly questions the environmental cost of fluorinated compounds?

The answer might be to lean into the sustainability narrative. Battery materials enable electric vehicles. PVDF membranes enable hydrogen production. Advanced fluoropolymers enable renewable energy. Position GFL not as a chemical company but as an enabler of the energy transition. The risk is greenwashing accusations if the environmental impact doesn't match the narrative.

The Capital Allocation Puzzle

With ₹60 billion committed to battery materials, the die is largely cast. But execution decisions remain. Do you build massive scale quickly to achieve cost leadership, or phase investments to match market development? Do you develop proprietary technology or license from leaders? Do you partner with battery manufacturers or maintain independence?

The subsidiary funding round suggests a clever approach—use external capital to fund growth while maintaining control. But this creates complexity and potential conflicts. What happens when GFCL EV needs more capital? Do you dilute further, fund from the parent, or slow growth?

The Innovation Challenge

GFL's R&D spending is modest by global standards. In battery materials, innovation cycles are rapid—new chemistries, new formulations, new applications emerge constantly. Do you significantly increase R&D investment to stay at the frontier, or focus on efficient manufacturing of proven technologies?

The partnership approach might be optimal—collaborate with universities, customers, and startups rather than trying to innovate everything internally. GFL's strength is scaling and manufacturing, not necessarily breakthrough innovation. Partner for innovation, own the production.

The Human Capital Question

Transforming from a chemical manufacturer to a technology-driven materials company requires different capabilities. Do you hire expensive talent from global competitors, develop internal capabilities through training, or acquire companies with the needed expertise?

The track record suggests organic development—GFL has successfully built capabilities in fluorine chemistry over decades. But battery materials move faster than traditional chemicals. The company might need to accelerate capability building through targeted hiring and partnerships.

The Exit Strategy Consideration

Here's the question few ask but all should consider: is GFL better as an independent company or part of a larger platform? Global chemical giants like Solvay, Arkema, or Chemours might pay substantial premiums for GFL's integrated fluorochemicals platform. Chinese strategics might value the non-China manufacturing base. Battery companies might want to secure supply.

The subsidiary structure suggests management is thinking about optionality—GFCL EV could be spun off, sold, or taken public independently. The parent company could focus on traditional fluorochemicals. Or everything could be sold to a strategic buyer at the right price.

Final Reflections

The Gujarat Fluorochemicals story is far from over. The company that rode carbon credits to prosperity and survived their disappearance now bets on battery materials for the next chapter. It's a story of adaptation, reinvention, and strategic courage.

What would you do? Perhaps the answer lies in GFL's history. The company has consistently succeeded by recognizing major transitions early—from CFCs to HCFCs, from manufacturing to carbon credits, from carbon credits to specialty materials. The next transition might already be visible to those watching carefully.

The electric vehicle revolution seems obvious, but is it? Perhaps the real opportunity is in hydrogen, where fluoropolymer membranes are critical. Or in semiconductors, where ultra-pure fluorinated compounds enable next-generation chips. Or in something not yet imagined.

For GFL, the constant has been change. The company that adapts fastest wins. The strategic choices made today—in capital allocation, technology development, and market positioning—will determine whether Gujarat Fluorochemicals' most interesting chapter is history or yet to be written.

The carbon credit windfall was extraordinary, unrepeatable, and ultimately temporary. What remains is a company with real capabilities, genuine opportunities, and difficult choices. The next decade will reveal whether GFL can build something permanent from a temporary advantage—a fitting test for one of India's most unusual business stories.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube