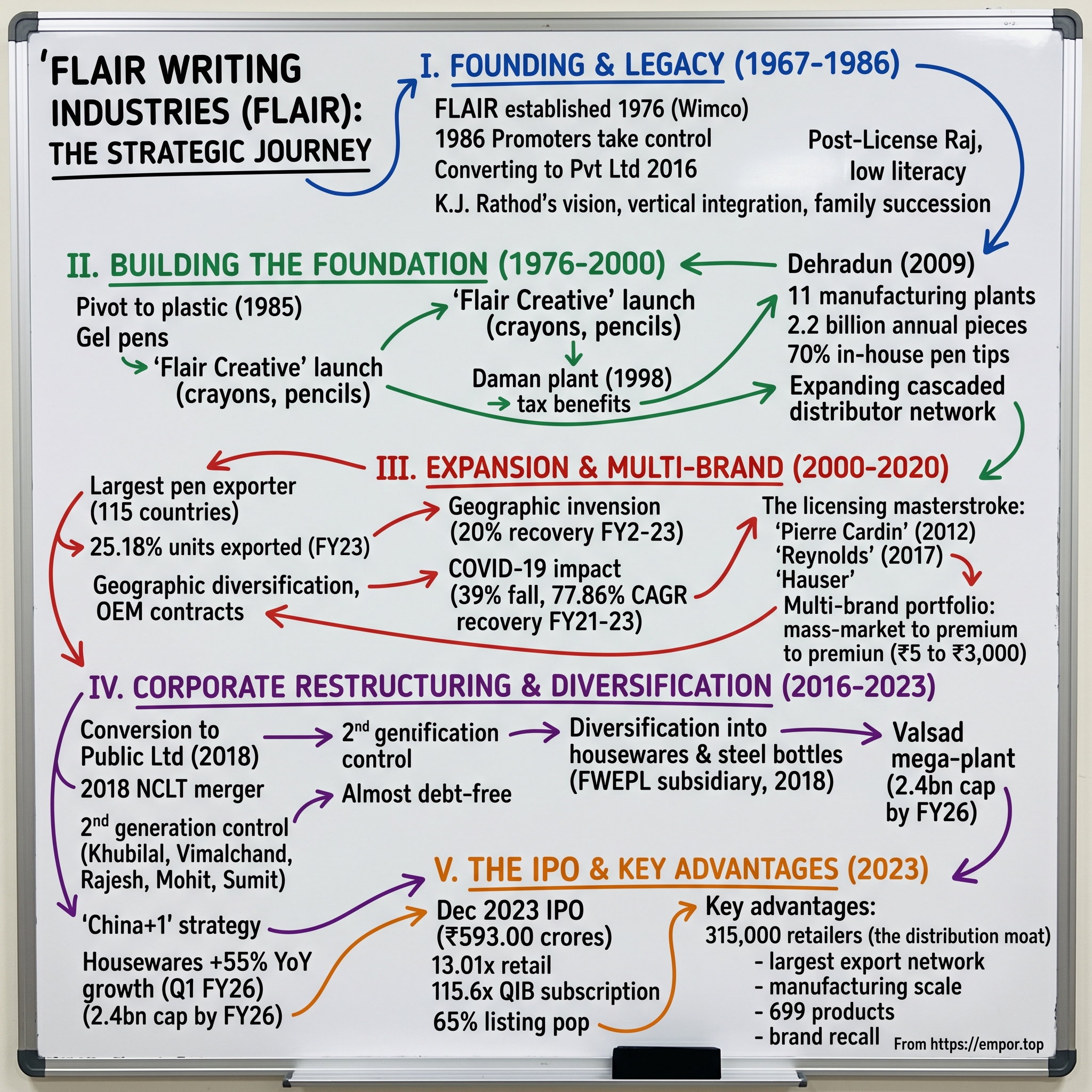

Flair Writing Industries: From Metal Pens to Market Leadership

I. Introduction & Episode Roadmap

Picture a metal pen rolling off a production line in 1976 Mumbai—clunky, functional, built for the masses flooding India's newly liberalized education system. Fast-forward nearly five decades: that same brand now commands a 9% share of India's writing instruments market, exports to 115 countries, and pulled off a spectacular 65% listing pop when it went public in December 2023. This is the story of Flair Writing Industries, a family business that survived the License Raj, navigated digital disruption, and turned licensing international brands into an art form.

What makes Flair's journey compelling isn't just longevity—it's strategic reinvention. While peers obsessed over domestic penetration, Flair became India's largest pen exporter. When premium seemed impossible for a mass-market player, they brought Pierre Cardin and Reynolds to India. When "paperless office" became the Silicon Valley mantra, they doubled down on distribution depth and diversified into steel bottles and housewares. And when they finally listed on public markets, institutional investors scrambled—the IPO opened November 22-24, 2023, with allotment finalized November 29 and shares listing December 1, 2023.

This is about more than pens. It's about building moats in unsexy categories, playing the long game across generations, and recognizing that in emerging markets, distribution trumps innovation—until it doesn't, and then you innovate like hell.

II. Founding Context & The Rathod Family Legacy (1967-1986)

The Rathod story begins not in 1976, but earlier—in 1967, when FLAIR was established in 1976 with the intention of producing writing instruments with precision, though the family's involvement in writing instruments traced back to their association with Wimco Pen Co, a Partnership Firm that engaged in manufacturing metal pens and other writing instruments. The "Flair" brand, originally established in 1976 by Wimco, has been owned and operated since 1986 by the Promoters.

This was post-License Raj India, where industrial licenses determined who could manufacture what, and in what quantities. Writing instruments mattered profoundly—literacy was climbing, schools were proliferating, and every student needed affordable pens. The Rathod family, led by patriarch K.J. Rathod, saw an opportunity not just in manufacturing but in building a brand that would outlast the regulatory constraints choking Indian industry.

The key transition came on January 6, 1986, when the business was originally carried on as a Partnership Firm under the name M/s Flair Writing Instruments. The Company converted into a Private Limited Company on August 12, 2016. This wasn't merely a legal formality—it represented the family's long-term vision of institutionalization. From day one, the Rathods structured for succession, with second-generation members K.J.'s sons groomed to take operational control.

Metal pens were the bread and butter—simple, durable, affordable. In a country where disposable income was scarce and products needed to last, metal construction made sense. But the family understood that markets evolve, and staying relevant meant embracing new materials and technologies even as the regulatory environment remained Byzantine.

What set Flair apart early was the family's commitment to vertical integration. Rather than relying solely on component suppliers—a risky proposition in an economy where supply chains were unreliable—they began building manufacturing capabilities in-house. This would prove decisive decades later when margins compressed and competitors struggled with vendor dependence.

III. Building the Foundation: Product Innovation & Manufacturing (1976-2000)

The first major pivot came in 1985. The manufacturing of plastic ball pens using plastic injection-molding machines and gel pens appeared as key developments in the industry, and Flair moved aggressively into plastic. This wasn't just technology adoption—it was strategic repositioning. Plastic pens were lighter, cheaper to produce at scale, and offered design flexibility that metal couldn't match.

Then came Flair's bold move: the company launched a range of "Flair Creative" products in Financial Year 2021 which include water colours, crayons, sketch pens, erasers, wooden pencils and geometry boxes, fine liners, sharpeners and scales. Company offered 727 different products as of June 30, 2023. But the foundation for this product breadth was laid decades earlier. By the late 1980s, Flair had introduced gel pens to the Indian market—a first-mover advantage in a category that would become massive. They followed with highlighters and correction pens, reading consumer trends and responding faster than larger, more bureaucratic competitors.

In year 1998, the Company established a manufacturing plant in Daman. Later on in 2008, Flair Calculators were launched. In 2009, manufacturing plant was set up in Dehradun, Uttarakhand. The Daman plant was particularly strategic—located in a union territory with favorable tax treatment, it gave Flair cost advantages that would compound over decades. Dehradun provided proximity to northern markets and access to a different labor pool, reducing concentration risk.

This era was about building manufacturing muscle. The company operates 11 strategically located manufacturing plants with a capacity of 2.20 billion pieces annually. Flair manufactures approximately 70% of its pen tips in-house, providing better quality control and cost efficiency. That 70% in-house tip manufacturing is a quiet superpower—most competitors outsource, creating quality variability and margin leakage.

Distribution strategy during this period focused on penetrating India's notoriously fragmented retail landscape. Flair didn't have the capital for direct retail or company-owned stores. Instead, they built a cascading distributor network—super-stockists feeding distributors feeding wholesalers feeding tiny mom-and-pop retailers. It was low-tech, relationship-intensive, and incredibly difficult to replicate. By the late 1990s, that network was becoming a moat.

The technology leap from metal to plastic injection molding also meant capital intensity. But rather than rely entirely on debt—expensive and scarce in pre-liberalization India—the family reinvested profits, growing deliberately. This financial conservatism would become a signature Flair trait, allowing them to weather downturns that killed more leveraged competitors.

IV. Expansion Era: Geographic & Product Diversification (2000-2016)

The 2000s marked Flair's transition from regional player to national brand with international ambitions. The export journey began quietly but accelerated dramatically when Vimalchand Jugraj Rathod served 40+ years, and was Chairman of the Pen & Stationery Association of India. His tenure between 2003 and 2005 as Chairman of the Plastics Export Promotion Council proved transformative—he understood export mechanics, built relationships with international distributors, and positioned Flair to capitalize on "Make in India" decades before it became a government slogan.

By FY23, Flair Writing Industries achieved substantial sales, with 1,303.60 million units of pens. Of this, 74.82% (975.30 million units) were sold domestically, while 25.18% (328.30 million units) were exported globally. A quarter of volumes going overseas is remarkable for a company born in the License Raj. As of March 31, 2023, Flair had established relationships with 54 international distributors, facilitating product distribution and sales in 97 countries.

The export strategy was shrewd: target developing markets where price sensitivity matched India's cost structure. Africa, Southeast Asia, Latin America—regions where Flair's value proposition resonated. They also pursued OEM contracts with international brands, manufacturing pens sold under other labels. The company contract manufactures writing instruments as an OEM for export and for sale in India, which contributed 16.87%, 19.94%, 33.37% and 38.67% to revenue from operations in the three-month period ended June 30, 2023 and the Financial Years 2023, 2022 and 2021, respectively. Notice the declining OEM percentage—a deliberate shift toward own-brand sales with higher margins.

The manufacturing footprint expanded deliberately. The company operates 11 manufacturing plants located in Valsad, Gujarat; Naigaon (near Mumbai), Maharashtra; Daman, Union Territory of Dadra and Nagar Haveli and Daman and Diu; and Dehradun, Uttarakhand. This geographic diversification wasn't just about capacity—it was risk management. Labor strikes in one location? Production continues elsewhere. Tax regime changes? Shift volume between jurisdictions.

Then came COVID. The Company's revenue from operations increased from Rs. 297.99 crores in FY 2020-21 to Rs. 942.66 crores in FY 2022-23 indicating a CAGR growth of 77.86%. That's not a typo—77.86% CAGR. FY21 saw a 39% collapse as schools and offices shut. But the recovery was explosive. Management made a bet: this was temporary demand destruction, not permanent structural decline. They held the line on distribution, kept factories running at reduced capacity, and prepared for the snapback. When schools reopened in FY22-23, Flair's distribution muscle meant they captured disproportionate share.

V. The Licensing Masterstroke: Premium Brand Acquisitions (2010-2020)

Here's where Flair's story gets fascinating. By 2010, they were a well-established mass-market player—solid, profitable, growing. But mass-market means thin margins. How do you move upmarket when your brand screams "affordable"? You don't. You bring in brands that already own the premium space.

Company's products are sold under their principal brands "Flair", "Hauser" and "Pierre Cardin", as well as other brands like "Rudi Kellner" and "Landmark". Company is also a manufacturer and the exclusive distributor of certain "Reynolds" branded pens in India. They own the exclusive rights to the "Pierre Cardin" trademark in India for class 16 products, including pens.

Start with Pierre Cardin. Flair Writing Industries Limited has been offering "Pierre Cardin" Writing Products since 2012. Previously, Flair Pens Limited, a Promoter Group Company, manufactured and sold "Pierre Cardin" writing products in India since 1994. Pierre Cardin pens retail for ₹100-₹3,000—10x to 600x the price of a basic Flair pen. The gross margins are obscene by writing instruments standards. More importantly, the brand allows Flair to access corporate gifting, luxury retail channels, and aspirational consumers who'd never consider "Flair" for personal use.

Hauser came next—a German heritage brand with credibility among professionals. Then Rudi Kellner. Then the big one: Reynolds. The Company has been a manufacturer since March 2017 and the exclusive distributor since January 2017 of certain Reynolds branded pens in India. Reynolds was iconic in India during the 1990s, then faded as ownership changed hands. Flair saw an opportunity: bring back a beloved brand with their manufacturing efficiency and distribution reach.

The Reynolds deal was brilliant for several reasons. First, brand recall was massive—an entire generation remembered Reynolds as the "good pen" from childhood. Second, unlike Pierre Cardin or Hauser, Reynolds could span mid-market to premium, giving Flair coverage across price points. Third, nostalgia is powerful, and Flair marketed the Reynolds return as a homecoming.

The multi-brand portfolio strategy created something unusual: Products are sold under "Flair" brand, "Hauser" and "Pierre Cardin" and recently introduced "ZOOX" in India. "Flair" and "Hauser" offer mass-market and premium pen and stationery products, "ZOOX" focuses on mid-premium and premium writing instruments, and "Pierre Cardin" brand offers premium pen and stationery products. Flair now had a complete portfolio from ₹5 mass-market to ₹3,000 luxury. This meant they could walk into a modern retail chain or e-commerce platform and negotiate for shelf space across categories.

Margin expansion followed predictably. While in 2022, the company boasted the highest operating and net income margins, reaching 17.8% and 9.6%, respectively, surpassing other key players, those margins were significantly higher on licensed premium brands. The licensing model was capital-light—Flair paid royalties but leveraged existing manufacturing and distribution. Every Reynolds or Pierre Cardin pen sold drove better blended margins than 100% own-brand sales.

The strategic insight was profound: in a category facing digital disruption, fight on multiple fronts. If volumes decline, shift mix toward higher-value products. If premium slows, push volume in mass-market. The portfolio became a hedge against uncertainty.

VI. Corporate Restructuring & Consolidation (2016-2018)

By 2016, Flair had grown organically and through multiple partnership entities, creating legal and operational complexity. The Company converted into a Private Limited Company on August 12, 2016 as Flair Writing Industries Private Limited, which then converted to a Public Limited Company and its name was changed to Flair Writing Industries Limited vide fresh Certificate of Incorporation dated May 30, 2018 issued by the RoC, Mumbai.

The real consolidation came via merger. A Scheme of Amalgamation was approved by the NCLT, Mumbai Bench by an Order dated March 15, 2018, certain companies i.e., Flair Pen and Plastic Industries Private Limited, Flair Stationeries Private Limited, Flair Pens and Stationery Industries Private Limited, Flair Pen and Plastic (UK) Private Limited and Flair Impex Industries Private Limited (Transferor Companies) got merged.

Why restructure? Public listing was the obvious endgame, and investors hate complexity. Multiple entities meant opaque financials, inter-company transactions requiring scrutiny, and governance headaches. The merger streamlined operations, simplified tax planning, and created a clean corporate structure for institutional investors.

But restructuring was also about family succession. The second generation—promoters Mr. Khubilal Jugraj Rathod, Mr. Vimalchand Jugraj Rathod, Mr. Rajesh Khubilal Rathod, Mr. Mohit Khubilal Rathod and Mr. Sumit Rathod—were assuming control. Chairman: Khubilal Jugraj Rathod (48+ yrs). MD: Vimalchand Jugraj Rathod (40+ yrs). Directors: Rajesh (international sales), Mohit (domestic sales, product dev), Sumit (new biz & steel bottles). CFO: Alpesh Porwal. Each had defined domains: international sales, domestic sales, product development, new businesses. This clarity prevented the infighting that destroys family businesses during generational transitions.

The 2016-2018 restructuring also prepared for scale. Institutional governance—independent directors, audit committees, formal board processes—was baked in. Financial reporting moved from partnership-style accounting to rigorous corporate standards. By the time they filed IPO papers in 2023, these systems were battle-tested.

Most critically, restructuring allowed deleveraging. Company has reduced debt. Company is almost debt free. Going public with heavy debt would have scared investors and limited valuation. The clean balance sheet coming out of restructuring was a statement: we don't need your money to survive; we want your money to grow explosively.

VII. The Diversification Bet: Beyond Writing Instruments (2018-2023)

Around 2018, Flair made its most controversial move: diversification into housewares and steel bottles. To understand why, consider the threats facing writing instruments. Digitization was accelerating. Tablets in classrooms. Cloud notes replacing physical notebooks. The "paperless office" had been predicted for decades; maybe it was finally arriving.

The company has also recently entered the household goods sector, including casseroles, bottles, storage containers, serving solutions, cleaning solutions, baskets, and paper bins. This expansion was made possible through one of the subsidiaries, FWEPL. FWEPL—Flair Writing Equipments Private Limited—became the vehicle for houseware ambitions.

The strategic logic was compelling. First, leverage existing capabilities: The company plans to utilize proceeds to fund the expansion of manufacturing capacity for writing instruments and to further optimize the business of houseware products and steel bottles. The steel bottle industry in India is projected to grow, and the company has received a letter of intent from a key OEM customer. Injection molding for pens translates directly to injection molding for plastic storage containers. Stainless steel pen barrels? Not far from steel bottles.

Second, leverage distribution. The company boasts the largest distributor/dealer network and wholesale/retailer network in the writing instruments segment in India. As of March 31, 2023, it comprises approximately 7,700 distributors/dealers and approximately 315,000 wholesalers/retailers. Those 315,000 retailers sell stationery but also housewares. Cross-selling became the unlock.

Third, ride the China+1 wave. Company has received a letter of intent from one of our key OEM customers with whom Company has a relationship of more than 15 years. One manufacturing line has been commissioned in the month of March 2023. Company intends on commissioning two more manufacturing lines during the third quarter of Financial Year 2024. As Western buyers diversified supply chains away from China, Indian manufacturers with proven quality and scale became attractive. OEM steel bottle contracts offered volume and margin predictability.

Results were encouraging. Portfolio doubled in FY25, from 22 SKUs to 52 SKUs. FY25: First major year of operations. Q1 FY26: +55% YoY growth, with sequential momentum. Housewares grew 55% YoY in the first quarter of FY26—a validation that the strategy was working.

But diversification brings risks. It's a new category requiring different go-to-market strategies. Retailers that stock pens don't automatically promote casseroles. E-commerce channels differ. And management bandwidth is finite—focusing on housewares means less attention to core pens business. Critics questioned whether Flair was losing focus or smartly hedging.

The Valsad mega-plant represented commitment to scale across both verticals. The New Valsad Unit is being set up with the objective of leasing to subsidiary FWEPL for manufacture of a wide range of writing instruments. This expansion would benefit the Company by increasing overall manufacturing capacities and enhance competitive position. The total land required is approximately 150,000 square feet with a total built-up area of approximately 180,000 square feet. Capacity would reach 2.2 bn units → rising to 2.4 bn by FY26.

VIII. Financial Turnaround & Hyper-Growth Phase (2020-2023)

COVID-19 was an existential moment. FY21 revenue crashed as schools and offices shut. But management's response defined Flair's trajectory. Rather than panic-cut costs, they held distribution relationships, maintained production flexibility, and bet on mean reversion.

The bet paid off spectacularly. The company's EBITDA expanded from Rs. 23.00 Crores in FY 2020-21 to Rs. 183.51 Crores in FY 2022-23, with a CAGR of 182.59%. Also, the company's EBITDA margin has increased from 7.72% in FY 2020-21 to 19.47% in FY 2022-23. That's an 8x increase in absolute EBITDA in two years, with margins more than doubling. The company's Net Profit expanded from Rs. 0.99 Crores in FY 2020-21 to Rs. 118.1 crores in FY23—a stunning recovery.

Volume explosion drove the turnaround. The company has seen significant growth in sales, selling 62 crore pens in FY21 and increasing to 130 crore pens in FY23. Volume doubled in two years. Capacity utilization surged, fixed costs got leveraged, and margins expanded.

But volume wasn't just recovery—it was market share gains. While the industry demonstrated a compounded annual growth rate of 5.5% from FY 2017 to 2023, the company's growth reached approximately 14%. Flair grew 2.5x faster than the industry, a sign they were taking share from competitors who hadn't maintained distribution during COVID.

Export strength accelerated. In 2023, Flair Writing Industries achieved substantial sales, with 1,303.60 million units of pens. Of this, 74.82% (975.30 million units) were sold domestically, while 25.18% (328.30 million units) were exported globally. That 25% export mix was meaningfully higher margin than domestic, given the OEM contracts and international brand partnerships.

Debt reduction was deliberate. The company's current liabilities during FY24 decreased to Rs 1 billion compared to Rs 2 billion in FY23, a decrease of -23.5%. Long-term debt decreased to Rs 307 million compared to Rs 418 million during FY23, a fall of 26.6%. Going into an IPO nearly debt-free was a massive signal: we're not capital-starved; we're opportunity-rich.

Return on capital metrics were stunning. Flair Writing Industries Ltd's ROCE averaged 22.1% from the FY ending March 2022 to 2024, with a median of 18.3%. It peaked at 30.5% in March 2023, reflecting strong capital efficiency. A 30.5% ROCE is exceptional in a manufacturing business, indicating pricing power and operational leverage.

The FY21-FY23 period wasn't just a recovery—it was proof that Flair's model had compounding advantages. Distribution reach meant faster volume recapture. In-house manufacturing meant margin expansion. Brand portfolio meant mix shift to premium. And looming IPO meant attracting institutional capital at peak momentum.

IX. The IPO Journey: Going Public in 2023

By mid-2023, the IPO decision was made. Why now? Timing was perfect. In the March 2025 quarter, net profit declined 10.17% to Rs 30.84 crore versus Rs 34.33 crore in the March 2024 quarter, while sales rose 19.17% to Rs 298.05 crore—but in 2023, they were coming off peak growth with pristine financials.

Flair Writing Industries IPO is a book build issue of ₹593.00 crores. The issue is a combination of fresh issue of 0.96 crore shares aggregating to ₹292.00 crores and offer for sale of 0.99 crore shares aggregating to ₹301.00 crores. The structure was balanced—₹292 crores fresh capital for expansion, ₹301 crores offer-for-sale giving founders liquidity.

Pricing was set at ₹304.00 per share with lot size of 49 shares. The minimum investment required by retail was ₹14,112 (49 shares). The lot size investment for sNII was 14 lots (686 shares), amounting to ₹2,08,544, and for bNII, 68 lots (3,332 shares), amounting to ₹10,12,928.

Reception was euphoric. The public issue subscribed 13.01 times in the retail category, 115.6 times in the QIB category, and 33.37 times in the NII category. QIB subscription at 115x signaled institutional conviction—sophisticated investors were backing Flair's story aggressively.

Flair Writing Industries IPO raised ₹177.90 crore from anchor investors. Flair Writing Industries IPO Anchor bid date was November 21, 2023. Anchors provided validation pre-IPO, ensuring strong opening momentum.

Listing day delivered. The stock jumped 65% on debut—a massive pop suggesting the issue was significantly underpriced or demand vastly exceeded expectations. For long-term investors, that pop was bittersweet—great for optics, but it meant money left on the table. For the company, it created positive sentiment and liquid trading, essential for future capital raises.

Use of proceeds was clear: Setting up a new manufacturing facility for writing instruments in District Valsad, Gujarat (New Valsad Unit); Funding capital expenditure of the company and its subsidiary, FWEPL; Funding working capital requirements; Repayment/pre-payment of certain borrowings; General corporate purposes. The Valsad plant was the centerpiece—capacity expansion to 2 billion pens annually positioned Flair for continued volume growth.

The IPO transformed Flair from a family-controlled private business into a public company with institutional shareholders, analyst coverage, and quarterly scrutiny. It also provided currency for acquisitions, employee stock options, and brand-building at scale.

X. The Distribution Moat & Competitive Advantages

Strip away the brands, the plants, the product breadth. Flair's true competitive advantage is distribution. The company boasts the largest distributor/dealer network and wholesale/retailer network in the writing instruments segment in India. As of March 31, 2023, it comprises approximately 7,700 distributors/dealers and approximately 315,000 wholesalers/retailers.

That 315,000 retailer number is staggering. India has roughly 12 million retail outlets; Flair reaches nearly 3% directly. The reach extends to 2,424 cities, towns, and villages in India as of June 30, 2023. This isn't just metro coverage—it's Tier 2, Tier 3, rural penetration where competitors fear to tread.

The distribution model is cascading. Super-stockists hold inventory and credit risk for regions. They supply distributors who supply wholesalers who supply retailers. Each layer adds a small margin but also adds reach. Flair's challenge is managing this complexity—ensuring no stock-outs, minimizing working capital tied up in channel inventory, preventing gray-market leakage.

Working capital intensity is a valid concern. While competitors have 67-93 working capital days, Flair stands at 160 days. That's the cost of deep distribution—you're financing retailer inventory. But it's also the moat—once those relationships exist, displacing Flair means offering better credit terms, better margins, or better products. All three simultaneously? Nearly impossible.

Manufacturing scale is the second pillar. Flair operates 11 manufacturing plants across India with a total installed capacity of 2.20 billion pieces of writing instruments annually. Installed capacity: 2.2 bn units → rising to 2.4 bn by FY26. Capacity at 2.4 billion pens annually is massive—enough to supply every Indian with 1.5 pens per year internally, with surplus for exports.

In-house component manufacturing is the third pillar. Flair manufactures approximately 70% of its pen tips in-house, providing better quality control and cost efficiency. Pen tips are precision components; quality variability kills brand reputation. Vertical integration ensures consistency and captures margin that would otherwise go to suppliers.

Product breadth is pillar four. As of March 31, 2023, they offer 699 different items across all their categories. Seven hundred SKUs means Flair can be a one-stop shop for retailers. Want basic ball pens, gel pens, highlighters, correction fluid, calculators, geometry boxes, and casseroles? Flair supplies all of it. Single invoice, single delivery, single relationship. That convenience is a lock-in.

Brand recall rounds out the advantages. Their flagship brand, has enjoyed a market presence for over 45 years now. Multiple generations of Indians grew up using Flair pens. That embedded brand recall is incredibly sticky—parents buy the brands they remember, passing preferences to kids.

XI. Industry Dynamics & Competitive Landscape

The Indian writing instruments market is peculiar—dominated by organized players but still plagued by unorganized competition. Indian writing and creative instruments industry to grow at 7.7 – 8.4% CAGR over Financial Years 2023 – 28. That 7.7-8.4% projected growth suggests steady demand driven by education expansion, rising literacy, and population growth.

Market structure matters. The organized sector—companies like Flair, Cello, Linc, Camlin—hold roughly 78-80% market share. The remaining 20-25% is unorganized: local manufacturers, unbranded pens sold at rock-bottom prices. Unorganized players compete on price, often cutting corners on quality. They lack brand power or distribution reach but survive by serving ultra-price-sensitive segments.

Competitive landscape is concentrated at the top. Flair Writing holds a 9% market share in the overall market. Cello World is the largest listed player by revenue, roughly 2x Flair's size. Linc Limited and Kokuyo Camlin round out the top tier. Each has distinct positioning: Cello is aggressive in mass-market and housewares, Linc focuses on innovation and design, Camlin has art supplies heritage.

Flair's edge versus peers is export dominance and brand portfolio. Flair has established itself as India's largest pen exporter, serving 77 countries globally. In FY23, the company sold 1,303.60 million units of pens, with 975.30 million units (74.82%) sold domestically and 328.30 million units (25.18%) exported. That export exposure is higher than competitors, providing currency diversification and insulation from domestic slowdowns.

Margin comparison is revealing. According to CRISIL, they boasted the highest operating and net income margins in FY22, standing at 17.8% and 9.6%, respectively, outshining other notable players. Premium brand licensing and in-house manufacturing drive those superior margins.

Industry growth drivers are durable. The India Writing Instruments market is witnessing significant growth, driven by rising literacy rates, expanding educational initiatives, and increased enrollment in schools and colleges. Government investments in education infrastructure and schemes promoting digital and traditional learning are further fueling demand. India's literacy rate climbing to 77.7% in 2021, per government data, means millions entering formal education annually—all needing pens.

Digital threat is real but overstated. Yes, tablets and styluses gain adoption. But A primary driver of this market is the enduring appeal of handwritten communication and the culture surrounding penmanship. While digital devices have revolutionized communication, the art of writing has not lost its charm. Exams still require pen-and-paper in most Indian institutions. Professionals still prefer handwritten notes for memory retention. Pens aren't dying—they're evolving.

XII. Playbook: What Flair Got Right

Family business with institutional discipline: The Rathod family maintained control while professionalizing operations. Second-generation leadership had clear domains, preventing destructive infighting. Conversion to public company structure forced governance rigor years before listing.

Export-led growth: While competitors fought domestically, Flair built international distribution. Becoming India's largest pen exporter created diversification, margin enhancement, and scale that compounded advantages.

Smart licensing over brand-building: Rather than spend decades building premium credibility organically, Flair licensed Pierre Cardin, Reynolds, Hauser. Instant access to premium segments, corporate gifting, luxury retail—with capital-light royalty model.

Distribution as moat: Building 315,000 retailer relationships took decades and is nearly impossible to replicate. The network's depth—reaching 2,424 towns and villages—provides volume resilience and pricing power.

Manufacturing excellence and vertical integration: Operating 11 plants with 2.2 billion unit capacity, manufacturing 70% of pen tips in-house, created quality control and cost advantages competitors struggle to match.

Timely diversification: Seeing long-term digital threats, Flair moved into housewares and steel bottles, leveraging manufacturing capabilities and distribution reach into adjacent categories before pen growth stalled.

Financial discipline: Deleveraging before IPO, maintaining conservative balance sheet through growth, avoiding equity dilution until scale was achieved—all showed patient capital allocation.

Market timing on IPO: Listing at peak post-COVID performance with strong margins, volume growth, and clear capital deployment plan maximized valuation and created public market momentum.

XIII. Bear Case & Risk Factors

Digitization is structural, not cyclical: While pens survived "paperless office" predictions before, tablets, cloud notes, and digital styluses are finally good enough. Long-term secular decline in writing instrument usage—especially in developed markets—is real. Flair's export exposure means this threat isn't just domestic.

Working capital intensity limits ROIC: More than 50% of the revenue is generated from a single 'Flair' brand. That brand concentration is risky—any reputation damage hits hard. Additionally, 160 working capital days versus competitors' 67-93 days means Flair ties up more capital per unit of revenue, limiting return on invested capital.

Supplier concentration and lack of contracts: The company lacks long-term supplier contracts and depends on limited suppliers for certain raw materials. In an environment of commodity price volatility (plastics, steel, inks), this creates margin compression risk.

Execution risk on diversification: Housewares is a new category with different competitive dynamics. Success in pens doesn't guarantee success in casseroles or steel bottles. Management bandwidth is finite; diversification could distract from core business optimization.

Unorganized sector competition: Local manufacturers and unbranded items at lower prices or combo-offers remain a persistent threat, especially in rural markets where price sensitivity is extreme and brand loyalty weaker.

Commodity price volatility: Pens require plastic, ink, metal components—all subject to crude oil and commodity price fluctuations. Flair can't always pass through cost increases immediately, compressing margins during input cost spikes.

XIV. Bull Case & Growth Opportunities

Proven execution through cycles: Company has delivered good profit growth of 24.1% CAGR over last 5 years. Management navigated COVID collapse and recovery, demonstrating adaptability and operational skill.

Export runway is long: Serving 115 countries with only 25% of volumes exported means significant headroom. Deepening penetration in existing markets and entering new geographies offers sustained growth without heroic domestic market share gains.

Premium mix shift drives margin expansion: Licensed brands—Pierre Cardin, Reynolds, Hauser—carry higher margins. As consumers trade up, Flair's portfolio positioning captures that shift, expanding blended margins structurally.

Housewares leveraging China+1 trend: Company has received a letter of intent from one key OEM customer with whom Company has a relationship of more than 15 years. Western buyers de-risking China supply chains creates tailwinds for Indian OEM manufacturers with proven quality.

Valsad capacity expansion: Doubling capacity to 2 billion pens positions Flair for market share gains. In a market growing 7-8% annually, having excess capacity means capturing competitor volume during supply crunches.

Market share gains accelerating: While the industry demonstrated a CAGR of 5.5%, the company's growth reached approximately 14%. Growing 2.5x faster than industry is a sign of gaining share from weaker competitors.

Post-pandemic structural tailwinds: Return to offices and schools, government education spending, rising literacy—all boost baseline demand. Flair's distribution reach captures disproportionate share.

E-commerce penetration still nascent: Modern retail and e-commerce channels are opening up, especially post-COVID. Flair's SKU breadth and brand portfolio position well for online shelf space domination.

Recent industry recognition: Flair Writing Industries received Plastics Export Promotion Council export award for 2023-24 and 2024-25, validating export excellence and opening doors for larger OEM contracts.

XV. Recent Developments & Future Trajectory (2024-2025)

Post-IPO, Flair faced the reality of quarterly public scrutiny. Flair Writing Industries Ltd's net profit fell -10.17% since last year same period to ₹30.84Cr in the Q4 2024-2025. On a quarterly growth basis, Flair has generated 5.08% jump in its net profits since last 3-months. Year-over-year profit decline raised eyebrows, but sequential growth suggested stabilization.

Full-year FY25 results showed resilience. Annual sales crossed ₹1,000 crores for the first time, demonstrating continued volume momentum despite margin pressures. The company maintained its focus on capacity utilization and mix management.

Sustainability became a strategic pillar. Management launched the "Move 2MM" refillable, non-wood mechanical pencil and initiated "The Right Move" sustainability campaign. In an era where consumers—especially urban youth—care about environmental impact, offering refillable and eco-friendly products isn't charity; it's competitive positioning.

Integration of the houseware business accelerated. Portfolio doubled in FY25, from 22 SKUs to 52 SKUs. Q1 FY26: +55% YoY growth, with sequential momentum. Dedicated distribution team of 25 added. Adding a dedicated 25-person sales team signals commitment—this isn't a side project; it's a growth engine.

Capacity expansion milestones were achieved. The Valsad facility became operational, adding flexibility between pens and Creative products. New Valsad facility: 2 lakh sq. ft., 60 injection moulding & assembly machines; fungible between pens and Creative. Fungibility matters—management can shift production mix based on demand signals, reducing idle capacity risk.

Management's vision for the next phase emphasizes three priorities: margin expansion through premium mix shift, accelerating houseware growth via OEM and own-brand channels, and digital transformation to reduce working capital intensity. The ERP upgrade and Field Force App for real-time sales tracking suggest operational rigor improving.

XVI. Epilogue: Lessons for Founders & Investors

Family succession done right: Clear roles, professional governance, long-term vision over short-term extraction. The Rathod family built for generations, not quarters.

Export as growth lever for Indian SMEs: Domestic markets are crowded and competitive. Export diversification provides scale, margin enhancement, and resilience. Flair proved Indian manufacturing can compete globally on quality, not just price.

Distribution is a durable moat: In fragmented, low-tech markets, relationships matter more than technology. Flair's 315,000 retailer network took 40+ years to build and can't be replicated quickly.

Licensing beats brand-building sometimes: Organic premium brand creation takes decades and massive capital. Licensing established brands is faster, capital-light, and accesses credibility immediately.

Diversification as insurance, not distraction: Flair's houseware bet hedges against digital disruption in pens. The key is leveraging existing capabilities—manufacturing, distribution—not venturing into unrelated businesses.

Timing public listings matters profoundly: Going public at peak performance with strong narrative maximizes valuation and creates momentum. Flair's December 2023 timing was masterful.

Manufacturing excellence as sustainable advantage: In an era obsessed with asset-light models, Flair's capital-intensive manufacturing with vertical integration created cost and quality advantages competitors can't easily match.

Betting against "digital kills everything": Analysts predicted pen death for decades. Flair's growth proves physical products can thrive alongside digital alternatives when they serve distinct needs.

XVII. Outro & Context

As of late October 2025, Flair Writing Industries represents a fascinating case study in strategic evolution. From metal pens in 1976 Mumbai to a diversified consumer products company with ₹1,079 crore revenue in FY25, the journey embodies resilience, adaptability, and patient capital deployment.

The company faces headwinds—margin pressure from commodity inflation, competitive intensity, digital substitution risks. But its distribution moat, brand portfolio, export positioning, and diversification hedges provide multiple paths to sustained growth. Whether housewares becomes the next chapter or pens continue surprising skeptics, Flair has earned its place among India's enduring business stories.

For long-term investors, the question isn't whether pens are dying—it's whether Flair's management can keep reinventing while maintaining the discipline that got them here. The track record suggests they can.

Note: This analysis is for informational purposes only and does not constitute investment advice. Investors should conduct their own due diligence and consult qualified professionals before making investment decisions. All data presented reflects publicly available information as of October 30, 2025.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube