Five-Star Business Finance: The Micro-Lending Powerhouse Built on Trust

I. Introduction & Episode Roadmap

Picture this: A small textile shop owner in Tirupur, Tamil Nadu, needs ₹3 lakh to buy a new loom. His monthly income fluctuates between ₹40,000 and ₹80,000 depending on orders. He has no salary slips, no IT returns, just a small property deed and years of running his business. The banks won't touch him—too risky, too small, too informal. The local moneylender will charge 60% annual interest. This man represents 63 million micro-enterprises in India, collectively employing 111 million people, yet systematically excluded from formal credit.

Enter Five-Star Business Finance—a company that saw opportunity where others saw risk. Today, with a market capitalization of ₹16,901 crore and over ₹20,000 crore disbursed in loans by 2023, Five-Star has quietly become India's most profitable micro-lending NBFC. Not through algorithms or apps, but through something almost quaint in 2024: human relationships and property-backed lending.

The central question driving this story isn't just how a 1984-founded traditional lender transformed into a financial inclusion powerhouse. It's deeper: In an era where everyone's chasing digital disruption and unsecured lending, how did Five-Star build a ₹7,500+ crore loan book by doing the exact opposite—staying physical, staying secured, and staying disciplined?

This is a story about three transformations across four decades, about finding gold in India's informal economy, and about why sometimes the best technology is a branch manager on a motorcycle. It's about financial inclusion that actually works—not the kind that wins awards at conferences, but the kind that gets a vegetable vendor in Madurai his first formal loan at 24% instead of 60% interest.

II. The Pre-History & Original Founding (1984–2000)

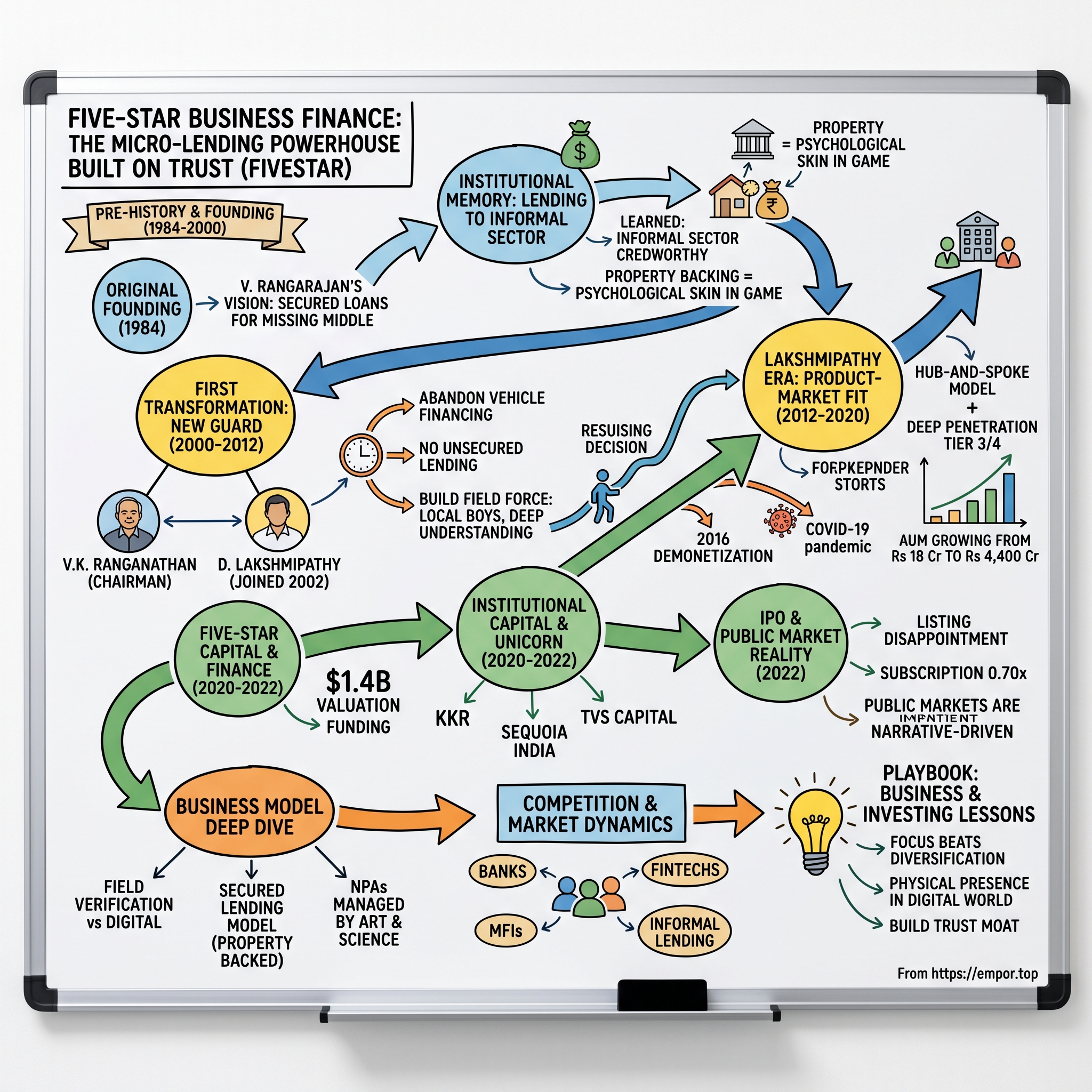

The year was 1984. Indira Gandhi was Prime Minister, the Bhopal gas tragedy would shock the nation by year's end, and India's banking system was a fortress—nationalized, bureaucratic, and utterly uninterested in lending to anyone without a government job or corporate letterhead. Into this world stepped V. Rangarajan, a seasoned banker from the old school, who had spent decades watching creditworthy businesses get rejected for loans simply because they couldn't produce the right paperwork.

Rangarajan didn't set out to revolutionize micro-lending. His vision for Five-Star Business Finance was modest: a Chennai-based finance company that would provide secured loans to small businesses that banks ignored. Not the poorest of the poor—that wasn't commercially viable. But the missing middle: the provision store owner with a small property, the auto workshop operator with some equipment, the textile trader with inventory but no formal books.

For nearly two decades, Five-Star operated like a traditional neighborhood lender. The company would eventually describe this period as "dormant"—harsh, perhaps, but not entirely unfair. They had maybe six branches, all in Tamil Nadu. The loan book was tiny, perhaps ₹15-20 crore at most. Interest rates were conservative, growth was glacial, and frankly, nobody outside Chennai's financial circles had heard of them.

But Rangarajan was building something important without realizing it: institutional memory about lending to the informal sector. Every loan officer who joined Five-Star in those early years learned a crucial lesson—these borrowers, despite lacking formal documentation, rarely defaulted if you structured the loan correctly. The property backing wasn't just collateral; it was psychological skin in the game. A small businessman might skip an unsecured loan payment, but he'd move heaven and earth to protect the house his family lived in.

The India of the 1980s and 90s was experiencing its own contradictions. The License Raj was suffocating formal businesses, yet the informal economy was exploding. By some estimates, 80% of India's workforce operated in the informal sector. These weren't unemployed people—they were drivers, shopkeepers, mechanics, tailors, running cash businesses that kept India's economy humming. Yet formally, they didn't exist. No PAN cards, no GST registration, no credit history.

The banking system's response was basically a shrug. The priority sector lending norms pushed banks toward agriculture and large industries. Small business loans below ₹10 lakh? Too expensive to underwrite, too risky without documentation. The RBI's own data from this period shows that formal credit to micro and small enterprises was less than 6% of total bank credit. The remaining 94% of these businesses relied on informal sources—moneylenders, chit funds, or simply went without credit.

Meanwhile, Five-Star kept making its small loans, learning its market. They discovered that a provision store owner in T. Nagar wasn't that different from one in Tambaram. Their cash flows followed patterns—higher during festivals, lower during monsoons. Their properties, usually inherited or bought with life savings, meant everything to them. Default wasn't just financial failure; it was social catastrophe.

By 2000, Five-Star had built something unique without fully realizing it: a playbook for lending to India's invisible entrepreneurs. They had proven the model worked, albeit at a tiny scale. What they needed was someone with the vision and aggression to scale it. The company was profitable but sleepy, successful but small. The transformation from regional lender to national player would require fresh blood—and that change was about to walk through the door.

III. The First Transformation: Enter the New Guard (2000-2012)

The millennium brought winds of change to Five-Star as V.K. Ranganathan (fondly called "Pati")—a former executive at Sundaram Finance—took over as the company's Chairman and Managing Director. He recognized the vast unmet credit demand in India's informal economy and began rethinking Five Star's mission and operating model. This wasn't just a leadership change; it was a philosophical revolution.

Ranganathan came from Sundaram Finance, one of India's most respected NBFCs, where he'd learned the art of vehicle financing and the importance of ground-level credit assessment. But at Five-Star, he saw something different—an opportunity to apply those disciplined lending principles to a completely underserved market. Where others saw chaos in India's informal economy, Ranganathan saw patterns. Where others saw risk, he saw mispriced opportunity.

His first insight was geographic. Five-Star was trapped in Chennai, competing with dozens of other lenders for the same customers. But what about Erode? Tirupur? Dindigul? These weren't just dots on Tamil Nadu's map—they were thriving economic clusters. Tirupur alone exported ₹26,000 crore worth of textiles annually, yet most of its 6,000+ small units couldn't get formal credit. Every power loom operator, every dyeing unit owner, every small exporter was borrowing at 3-5% monthly from informal sources.

The real acceleration came when D. Lakshmipathy joined. Before joining Five-Star, he was Managing Director of RKV Finance Limited, an NBFC registered with RBI. When RKV amalgamated with Five-Star in 2002, he joined the Board as Joint Managing Director. His wide exposure in lending to small business customers, which was successful at RKV, helped him develop a similar advance portfolio at Five-Star with great success.

The Ranganathan-Lakshmipathy combination was potent. Ranganathan brought vision and relationships; Lakshmipathy brought execution prowess and an intimate understanding of small business psychology. Together, they began dismantling every assumption about micro-lending in India.

Their first radical decision: abandon vehicle financing entirely. By 2005, two-wheelers and commercial vehicles had become commoditized products with wafer-thin margins. Bajaj Finance, Cholamandalam, and a dozen others were fighting over the same customers with similar products. Five-Star's vehicle book, already small, was generating 18% yields with rising NPAs. The small business loan book, tiny as it was, generated 24% yields with lower defaults.

The second decision was even more controversial: no unsecured lending, period. While the microfinance revolution was exploding across India with joint liability groups and unsecured loans, Five-Star went the opposite direction. Every single loan would be secured by property. This wasn't about being conservative—it was about understanding human psychology. A borrower might default on an unsecured loan and disappear. But threaten the roof over his family's head? He'd sell his blood before missing an EMI.

Between 2002 and 2010, Five-Star methodically built what would become its secret weapon: the field force. These weren't MBA graduates with credit scoring models. They were local boys who understood the rhythms of small business. They knew that a provision store's sales peaked on the 1st and 15th of each month (salary days). They understood that a power loom operator's cash flow depended on whether exports to Europe were strong. They could walk into a workshop and estimate monthly revenue just by counting machines and workers.

The training was intensive. Every field officer spent three months learning not just credit assessment, but local business dynamics. They studied everything: which areas had water problems (affecting dyeing units), which localities had evening markets (affecting retail shops), even which communities traditionally engaged in which businesses. This wasn't politically correct, but it was commercially crucial. A Nadar family running a provision store had different cash flow patterns than a Chettiar family running a pawn shop.

The results were spectacular, if unnoticed. By 2010, Five-Star had grown from 6 branches to 30, from ₹18 crore AUM to over ₹200 crore. NPAs had dropped from over 5% to under 2%. The average ticket size—₹1.5 lakh—was perfect: large enough to be profitable, small enough to be manageable. But most importantly, they'd discovered their moat: relationships at scale.

Consider the typical Five-Star loan process circa 2010. When Murugan, running a small restaurant in Erode, needed ₹2 lakh for kitchen equipment, he'd approach the local Five-Star branch. The field officer would visit not just once, but three times—morning, afternoon, evening—to observe customer flow. He'd talk to neighboring shopkeepers, check property papers, even observe family dynamics. Was the son interested in the business? Did the wife participate? These soft factors mattered as much as cash flows.

The loan approval happened within 7 days—lightning fast compared to banks, which took months. The interest rate—24% annually—seemed high, but Murugan was comparing it to the 60% he'd pay the local lender, not the 12% he'd never get from a bank. More importantly, Five-Star would renew the loan if he kept paying, effectively providing a working capital line disguised as term loans.

By 2012, Five-Star had validated its model but was still subscale. They had the recipe but lacked ingredients—specifically, capital. The company was profitable but couldn't grow faster than its internal accruals allowed. The next phase would require external capital, technology, and most crucially, someone who could take Ranganathan and Lakshmipathy's vision and scale it 100x. That person was about to walk through the door, and with him would come a transformation that would shock India's financial establishment.

IV. The Lakshmipathy Era: Finding Product-Market Fit (2012–2020)

The boardroom at Five-Star's Chennai headquarters in early 2012 must have been electric. D. Lakshmipathy, who had been with the company since 2002 as Joint Managing Director following the amalgamation of his RKV Finance, was about to take center stage as Executive Director and later CEO. The company had proven its model worked, but at ₹400 crore AUM, they were still a rounding error in India's financial system. Lakshmipathy had a different vision: championing data-driven credit underwriting, a hub-and-spoke model, and deep penetration into Tier 3 and Tier 4 towns.

The genius of Lakshmipathy wasn't in inventing something new—it was in recognizing that Five-Star already had the winning formula. They just needed to execute it at 100x scale. His mantra was simple: "We didn't go after salaried professionals in metros. We went to places where no one else was willing to lend—and met people who just needed a fair chance".

Consider the typical Five-Star customer circa 2012: Selvam, running a small idli shop in Karur. Monthly income: ₹30,000-50,000 depending on the season. Assets: A small house worth ₹15 lakh inherited from his father. Banking history: Zero. Credit bureau score: Non-existent. For Axis Bank or HDFC, Selvam didn't exist. For the local moneylender, he was prey—paying 5% monthly interest for working capital. For Five-Star, he was perfect.

The loan officer would visit Selvam's shop at 6 AM to see the morning rush, again at lunch, and once more in the evening. They'd count customers, estimate average ticket size, observe which days were busiest. They'd talk to his suppliers—did he pay on time? They'd check with neighbors—was he trustworthy? The property evaluation wasn't just about market value but emotional value—was this his ancestral home? Would he risk losing it?

Within a week, Selvam would have ₹3 lakh at 24% annual interest. Yes, double what a bank would charge—if a bank would lend to him, which they wouldn't. But compared to the 60% he was paying the moneylender, it was liberation. More importantly, if he repaid well, Five-Star would increase the limit. Suddenly, Selvam had a credit history, a formal relationship, dignity.

The field force was Five-Star's secret weapon. By 2015, they had over 1,000 field officers, each managing 150-200 customers. These weren't fresh MBA graduates sitting in air-conditioned offices. They were local boys who understood local businesses. The training was brutal—three months of classroom, three months of shadowing, constant testing. They learned to spot over-leveraging (too many gold ornaments meant other debts), family issues (son not interested in business meant higher risk), and business cycles (provision stores did well during festivals, struggled during school vacations).

Under Lakshmipathy's leadership, over 9 years, the company grew from a branch network of 6 to more than 260 and from an AUM of Rs 18 Crores to about Rs. 4,400 Crores. But the real innovation wasn't growth—it was discipline. Every branch had to be profitable within 18 months. Every loan officer's portfolio was tracked daily. NPAs above 2% triggered immediate intervention.

The technology strategy was counterintuitive. While fintech startups were building apps and algorithms, Five-Star invested in basic operational tech. Tablets for field officers to capture data. Simple scoring models based on business type and location. Centralized underwriting for loans above ₹5 lakh. The goal wasn't to eliminate human judgment but to augment it. The field officer's assessment carried 60% weight, the centralized score 40%.

Geography became destiny. Five-Star didn't randomly expand—they followed economic clusters. Tirupur for textiles, Coimbatore for pumps and motors, Sivakasi for fireworks and printing, Karur for home textiles. Each cluster had specific characteristics. Tirupur businesses peaked during European summer orders. Sivakasi surged before Diwali. Understanding these patterns meant better underwriting and collection.

The hub-and-spoke model was brilliant in its simplicity. A main branch in the district headquarters, smaller branches in towns, and collection points in villages. The hub handled underwriting and disbursement. Spokes handled sourcing and collection. This kept costs low while maintaining presence. A full branch cost ₹50 lakh to set up; a spoke just ₹5 lakh.

Competition was watching but not worried. In 2015, Bajaj Finance was focused on consumer durables and personal loans. Bandhan was converting from microfinance to banking. Traditional NBFCs like Manappuram and Muthoot were in gold loans. Banks couldn't go down-market due to cost structures. Five-Star had found white space—secured business loans between ₹1-10 lakh in semi-urban India.

The unit economics were beautiful. Average ticket size: ₹2.7 lakh. Interest rate: 24-26%. Cost of funds: 10-12%. Operating expenses: 6-7%. Credit losses: 1-2%. Pre-tax ROA: 5-6%. In comparison, banks made 1-2% ROA, MFIs made 3-4% but with higher risk. Five-Star had found the sweet spot—high yields, low losses, steady growth.

Customer retention became an obsession. Unlike vehicle loans or gold loans which were transactional, Five-Star built relationships. The same field officer visited the same customer for years. Birthday wishes, festival greetings, business advice—these weren't corporate initiatives but genuine relationships. When customers graduated to bank credit, Five-Star celebrated rather than mourned. They'd created 50,000 entrepreneurs with formal credit histories.

The 2016 demonetization was Five-Star's first real test. Overnight, 86% of India's currency became worthless. Their customers—all cash businesses—were devastated. Collections dropped 40% in November 2016. The board panicked. Investors worried. But Lakshmipathy stayed calm. "Our customers aren't defaulting," he told the team. "They're just illiquid."

The response was masterful. No penalties for delays. Partial payments accepted. Field officers helped customers open bank accounts, get PAN cards, understand digital payments. By February 2017, collections had normalized. NPAs barely budged. The crisis had proven Five-Star's model—when you lend against property to entrepreneurs, temporary shocks don't become permanent losses.

By 2019, Five-Star was a well-oiled machine. ₹3,500 crore AUM, 250+ branches, 1.5 lakh customers, and critically, profitable. But they were still subscale compared to their ambition. The next phase would require serious capital—not just debt but equity. The timing was perfect. Global investors were discovering financial inclusion. The question was: could Five-Star maintain its culture and discipline while scaling 10x? The answer would come from the most unlikely source—Silicon Valley venture capitalists who'd never set foot in Gobichettipalayam.

V. The Institutional Capital Era & Unicorn Status (2020-2022)

At the Taj Mahal Hotel in Mumbai, March 2021, billion-dollar deals were being made over filter coffee and dosas. Gaurav Trehan from KKR, G.V. Ravishankar from Sequoia Capital India, and Gopal Srinivasan from TVS Capital sat across from D. Lakshmipathy. What happened next would transform Five-Star from a regional NBFC into India's newest unicorn.

Five Star Business Finance Ltd raised funding at a valuation of $1.4 billion (Rs 10,300 crore) in a fresh round led by new backer private equity firm KKR and returning investor Sequoia Capital India. The investors committed $234 million (Rs 1,700 crore) in Five Star Business. This wasn't just capital—it was validation at the highest level.

The timing was perfect and terrible simultaneously. COVID-19 had devastated India's informal economy. Five-Star's customers—the provision store owner, the power loom operator, the auto repair shop—were crushed by lockdowns. Collections dropped to 60% in April 2020. The board meetings were tense. Should they restructure? Write off loans? Cut lending?

Lakshmipathy's response defined the company. "Our customers survived demonetization. They'll survive this too." Five-Star didn't just restructure loans; they redesigned them. Three-month moratoriums, reduced EMIs, extended tenures—whatever it took. Field officers became counselors, helping customers apply for government schemes, negotiate with suppliers, even buying groceries for families in distress.

By December 2020, something remarkable happened. Collections bounced back to 95%. NPAs, which everyone expected to explode, barely moved from 1.5% to 1.9%. The secured lending model had proven its resilience—customers would do anything to protect their property. More importantly, Five-Star's response had deepened customer loyalty. Borrowers remembered who stood by them during crisis.

This resilience caught Silicon Valley's attention. Sequoia Capital India had been watching Five-Star since 2017, when they first invested. What they saw during COVID convinced them to double down. G V Ravishankar, Managing Director, Sequoia India, remarked, "Sequoia Capital India is delighted to be investors in Five Star, and is strong believers in their business model that bridges the large credit gap that exists for small and micro-enterprises.

But the real coup was KKR. KKR's investment is part of its global impact strategy, and marks KKR Global Impact Fund's second investment in India and fifth in Asia Pacific. For KKR, Five-Star wasn't just an investment—it was an impact play. The Global Impact Fund is focused on generating risk-adjusted returns by investing in companies that contribute toward the United Nations Sustainable Development Goals ("SDGs"). Given its core mission to enhance and broaden financial access and inclusion, Five Star's core business directly contributes toward SDG 1 (No Poverty), and SDG 9 (Industry, Innovation and Infrastructure).

The due diligence was legendary. KKR's team spent three months in the field, visiting branches in places most Mumbai bankers couldn't pronounce. They interviewed customers, watched collections, analyzed 10 years of data. What convinced them wasn't the numbers—though 20%+ ROE and sub-2% NPAs were impressive. It was the model's defensibility.

Consider Five-Star's competitive moats circa 2021: First, the distribution network—262 branches in 126 districts, each profitable, each with deep local relationships. Building this would take a competitor 10 years and hundreds of crores. Second, the underwriting expertise—1,500+ field officers who could assess a welding shop's cash flow by counting sparks. Third, the brand—in towns like Gobichettipalayam, "Five-Star" had become synonymous with fair lending.

The transaction comprised a primary infusion in the company and a sale of shares by existing investor Morgan Stanley Private Equity. Morgan Stanley, one of Five-Star's earliest institutional backers, sold at over 5x returns—validation that patient capital in financial inclusion could generate venture-style returns.

The capital allowed Five-Star to accelerate everything. New branches—50 in six months. Technology upgrades—tablets for every field officer, automated underwriting for loans under ₹2 lakh. Most importantly, talent—hiring senior executives from HDFC, Bajaj Finance, and Bandhan Bank. The scrappy regional lender was becoming an institutional-grade financial services company.

But cultural integration was the real challenge. The new executives from Mumbai and Bangalore had MBAs, spoke of TAMs and CACs, and wanted to digitize everything. The old guard from Chennai and Coimbatore knew every customer by name, believed in face-to-face meetings, and thought technology was overrated. Board meetings became battlegrounds between growth and prudence, scale and quality.

Lakshmipathy played mediator brilliantly. Yes, they'd adopt technology, but as an enabler, not replacement for human judgment. Yes, they'd expand aggressively, but only into contiguous markets where the model was proven. Yes, they'd hire from top institutions, but field experience would always trump degrees in promotions.

The results were stunning. AUM grew from ₹4,400 crore in March 2021 to ₹5,800 crore by December 2021. New customer additions doubled. Operating expenses as a percentage of AUM actually decreased, proving that scale brought efficiency. The average ticket size increased to ₹3.2 lakh as customers grew with Five-Star.

The unicorn valuation—$1.4 billion—wasn't just a number. In India's NBFC sector, only a handful had achieved this: Bajaj Finance, Muthoot, Manappuram. But those were either in consumer finance or gold loans. Five-Star was the first pure-play small business lender to reach unicorn status. The message was clear: financial inclusion wasn't charity; it was a massive commercial opportunity.

By early 2022, the board faced a crucial decision. They had two options: raise another private round at perhaps $2 billion valuation, or go public. The private round would be easier—one negotiation, friendly investors, no quarterly pressure. But going public would provide permanent capital access, brand visibility, and most importantly, force the institutional discipline needed for the next phase of growth. The choice would define Five-Star's next decade.

VI. The IPO & Public Market Reality Check (2022)

The boardroom discussions in September 2022 were tense. The global markets were in turmoil—the Fed was hiking rates aggressively, tech stocks were crashing, and Indian markets were nervous. Five-Star's bankers from ICICI Securities and Kotak Mahindra Capital were recommending a delay. "Wait for better market conditions," they advised. But the board, led by Lakshmipathy, decided to push ahead. The company had filed preliminary papers with SEBI to raise up to Rs 2,752 crore through an IPO, but the offer-for-sale issue was trimmed down from Rs 2,752 crore to Rs 1,960 crore.

What nobody expected was the tepid response. Five Star Business Finance IPO bidding started from November 9, 2022 and ended on November 11, 2022. The allotment was finalized on Wednesday, November 16, 2022. The shares got listed on BSE, NSE on November 21, 2022. But the subscription numbers told a sobering story.

Day one was a disaster. By 5 PM, the issue was subscribed just 8%. The WhatsApp groups of Mumbai's investment banking community were buzzing with schadenfreude. "Another overpriced IPO," one analyst messaged. "Financial inclusion is great CSR, terrible business," wrote another. The retail investors, burned by recent IPO failures, stayed away. HNIs were cautious. Even QIBs, usually reliable for momentum, were selective.

By the final day, the reality was stark: the IPO had been subscribed 0.70x by 05:46 PM on Day 3. For context, most successful IPOs in India get oversubscribed 10-50x. Even mediocre ones manage 2-3x. Less than 1x subscription meant the issue technically failed—the underwriters would have to pick up unsold shares.

The pricing seemed reasonable on paper. Five Star Business Finance IPO price band was set at ₹474 per share, valuing the company at about ₹13,800 crore. The financials were solid—revenues had grown from ₹33 crore in FY15 to ₹1,256 crore in FY22. Net profit had jumped from ₹10 crore to ₹453 crore in the same period. Over 95% of the loan portfolio comprised loans between ₹1 lakh to ₹10 lakh in principal amount, with an average ticket size of ₹2.7 lakh. The 95% of the loans sanctioned were between the interest rate range of 24% - 26%.

But the market had concerns. First, the interest rate environment—the RBI was hiking rates, which would increase Five-Star's borrowing costs. Second, competition was intensifying—banks were going down-market, fintechs were getting aggressive. Third, and most damaging, the perception that 24-26% interest rates were usurious, even if they were replacing 60% informal lending rates.

The institutional investors who did participate had done deep diligence. One fund manager who invested told me (off record): "Everyone was looking at Five-Star through a banking lens—why 24% rates, why 6% operating costs? But this isn't banking. It's financial inclusion with economics that work. The field officer visiting a welding shop three times before sanctioning ₹3 lakh—that's not inefficiency, that's the moat."

November 21, 2022. Listing day. The Five-Star management team gathered at the BSE, participating in the ceremonial bell-ringing, but the mood was subdued. The stock opened at ₹450—a 5% discount to the issue price. By noon, it was trading at ₹440. The financial media, always eager for drama, called it a "disappointing debut" and "reality check for NBFCs."

But Lakshmipathy was philosophical in his post-listing interview: "We didn't come to the markets for a one-day pop. We came for permanent capital, institutional discipline, and the ability to serve 10 million customers instead of 200,000. The market will eventually understand our model."

The weeks following the listing were brutal. The stock hit ₹420, down 11% from issue price. Employee morale was affected—many had ESOPs underwater. Some institutional investors who'd participated in the IPO were questioning their investment committees. The narrative was set: Five-Star was a good company that came to market at the wrong time with the wrong pricing.

But something interesting was happening in the business. Despite the market negativity, Five-Star's operations were humming. New customer additions accelerated. The branch expansion continued. NPAs remained under 2%. The company was generating cash, growing prudently, and most importantly, the competitive threats everyone worried about weren't materializing. Banks found micro-lending too expensive. Fintechs couldn't crack the secured lending model without field presence.

Three months post-listing, Five-Star reported its quarterly results. AUM had grown 22% year-on-year. ROE was 22%. The company had added 25 new branches. Suddenly, the narrative began shifting. Research analysts who'd been skeptical started publishing positive notes. "Misunderstood at IPO," wrote one. "Hidden gem in financial inclusion," wrote another.

The IPO experience taught Five-Star valuable lessons. Public markets are impatient, narrative-driven, and often wrong in the short term. But they also enforce discipline—better disclosure, governance, and strategic clarity. The company that emerged from the IPO wasn't demoralized but determined. They had permanent capital, a public currency for acquisitions, and most importantly, they'd proven that a financial inclusion story could access capital markets, even if the debut was muted. The real test would be execution—could they deliver the growth and profitability that would vindicate the believers and convert the skeptics?

VII. The Business Model Deep Dive

Walk into Five-Star's branch in Gobichettipalayam at 9 AM on a Monday. You'll see something that would puzzle any fintech founder: a crowd. Not a digital queue or app notification, but actual human beings—a provision store owner with property papers, a power loom operator with bank statements, a vegetable vendor with her daughter translating. This scene, replicated across 311 branches, generates some of the best unit economics in Indian financial services.

Let's dissect the numbers that make bankers jealous and investors skeptical. Over 95% of the loan portfolio comprises loans from between ₹1 Lakh to ₹10 lakh in principal amount, with an average ticket size of ₹2.7 Lakh. The 95% of the loans sanctioned being between the interest rate range of 24% - 26%. At first glance, 24-26% interest seems predatory. But let's do the math from the customer's perspective.

Selvam, our idli shop owner from earlier, needs ₹3 lakh for a new cooking range. His options: Bank (won't lend—no IT returns), Gold loan (only has ₹1 lakh worth of gold), Personal loan app (37% interest, if approved), Local moneylender (5% monthly = 60% annually), or Five-Star (24% annually). For Selvam, Five-Star isn't expensive—it's liberation.

Now from Five-Star's perspective. That ₹3 lakh loan generates ₹72,000 annual interest. Sounds fantastic until you factor in costs. Cost of funds: ₹36,000 (12%). Operating expenses: ₹21,000 (7%—those three field visits aren't free). Expected credit losses: ₹6,000 (2%). Pre-tax profit: ₹9,000 (3%). After tax: ₹6,750. ROA of 2.25% might seem thin, but when you're deploying ₹7,500 crore, that's ₹169 crore in profits.

The field verification versus digital underwriting debate misses the point entirely. Five-Star tried digital. In 2019, they piloted an app-based lending program for existing customers. Approval in 10 minutes, money in 1 hour. The result? NPAs shot up to 5%. Why? The physical visit isn't just about verification—it's about commitment. When a field officer spends three hours evaluating your business, and you spend three hours explaining it, both parties are invested. The inconvenience is the feature, not the bug.

The secured lending model is the secret sauce. Every single loan is backed by property—usually residential, sometimes commercial. The loan-to-value ratio averages 40-50%. This means even if property prices crash 50% (they haven't in 30 years), Five-Star recovers its principal. But here's the psychological masterstroke: they almost never have to enforce the security. In FY22, less than 0.5% of loans required legal action. The threat is enough.

The company has an extensive network of 311 branches, as of June 30, 2022, spread across eight states and one union territory and approximately 150 districts across India. Each branch follows the hub-and-spoke model. A full branch in a district headquarters might have 15 employees—branch manager, 8 field officers, 3 collection agents, 3 back-office staff. This branch manages 3-4 spokes in surrounding towns, each with 2-3 employees. Total cost: ₹40 lakh annually. Total disbursements: ₹15-20 crore. The math works.

Customer acquisition is refreshingly analog. No Google ads or influencer campaigns. Instead, field officers attend local business association meetings, visit market associations, and most powerfully, rely on referrals. A satisfied customer is worth 3-4 new customers. The customer acquisition cost? Under ₹2,000, compared to ₹5,000-10,000 for digital lenders.

Risk management happens at three levels. First, at sourcing—field officers reject 60% of applications before they reach underwriting. Second, at underwriting—another 20% rejected after property verification and cash flow analysis. Third, at monitoring—monthly visits for the first six months, quarterly thereafter. If EMI is delayed by even 7 days, the field officer visits. At 15 days, the branch manager visits. At 30 days, they discuss restructuring.

The collection mechanism is deliberately friction-filled. No auto-debit (most customers don't have stable bank balances), no digital payments (creates distance), just cash or cheque collection at the branch or during field visits. This monthly interaction is when field officers detect stress—business slowing, family medical issues, competition increasing. Early intervention prevents defaults.

Managing NPAs is both art and science. Five-Star's gross NPA of 1.9% is remarkable given their customer segment. The science: predictive models based on 40 variables—payment history, business type, locality economic indicators. The art: field officer intuition. A veteran field officer can predict default probability just by observing changes in inventory levels or family dynamics.

Technology plays a supporting, not leading role. The loan origination system ensures process compliance. The mobile app for field officers captures real-time data. The analytics dashboard helps management spot trends. But the core decision—to lend or not—remains human. As one branch manager explained, "The app can tell me the customer's payment history. Only I can tell you if his son is interested in the business."

The competitive moat is time, not technology. A fintech startup could replicate Five-Star's app in three months. A bank could match their interest rates tomorrow. But building a 1,500-person field force that understands micro-business dynamics? Training them to assess a provision store's cash flow by observing customer traffic? Establishing trust in 150 towns where "Five-Star" has become synonymous with fair lending? That's a decade-long project with no shortcuts.

The recent stress in asset quality—Gross Stage 3 assets rising to 2.46% from 1.41%—reflects post-COVID normalization rather than model breakdown. Many customers who'd restructured loans during COVID are now being classified correctly. The management expects NPAs to stabilize around 2-2.5%, still industry-leading for this segment.

The expansion strategy is measured. Each new branch must break even within 18 months, turn profitable by 24 months. They enter new towns only after six months of market study. They hire locally—the branch manager must be from the district, field officers from the specific towns. This localization ensures cultural fit and reduces employee attrition to under 15%, exceptional in Indian financial services.

The bull case for the model is compelling: 63 million micro-enterprises in India, less than 10% have formal credit access, Five-Star has reached barely 300,000. Even capturing 1% market share would mean 10x growth. The bear case is equally valid: rising interest rates squeeze margins, digital lenders eventually crack the code, or regulation caps lending rates. But for now, Five-Star has found a sweet spot—profitable enough to scale, inclusive enough to matter, and defensible enough to last.

VIII. Competition & Market Dynamics

The conference room at the Taj Coromandel in Chennai, February 2024. The Finance Industry Development Council's annual meeting brought together every major NBFC CEO in India. During the tea break, the conversation inevitably turned to Five-Star. "They're charging 24%—that's not sustainable," argued the CEO of a large vehicle finance company. "Their operating costs are too high," added a gold loan executive. Yet, Five-Star's numbers kept defying the skeptics.

The NBFC landscape in India is a ₹30 trillion battlefield, with everyone fighting for their slice. At the top, giants like Bajaj Finance and Shriram Finance dominate consumer and vehicle finance. In the middle, specialists like Muthoot and Manappuram own gold loans. At the bottom, microfinance institutions serve the poorest. Five-Star found white space between these layers—the micro-entrepreneur who's too rich for microfinance, too poor for banks, and doesn't have gold to pledge.

Traditional banks remain Five-Star's most interesting non-competitors. Every major bank claims to prioritize MSME lending—it's mandated by priority sector norms. Yet, walk into any PSU bank branch with a ₹3 lakh business loan request without formal financials, and watch them squirm. The branch manager will sympathetically explain that rules require IT returns, GST registration, and formal books. Even if they wanted to help, the centralized underwriting system would reject the application. Banks' average ticket size for business loans is ₹25 lakh; Five-Star's is ₹2.7 lakh. They're playing different games.

The private banks—HDFC, ICICI, Axis—have tried to go down-market through business correspondent models and digital initiatives. But their DNA rebels against ₹3 lakh loans requiring three field visits. An HDFC Bank relationship manager, speaking anonymously, admitted: "Our cost to underwrite and service a ₹3 lakh loan is almost ₹50,000 over three years. The economics just don't work unless we charge 30%+, which we can't do reputationally."

Microfinance institutions (MFIs) seem like natural competitors, but they're actually complementary. MFIs like Bandhan, Ujjivan, and Equitas serve daily wage earners with ₹30,000-50,000 unsecured loans at 18-22% interest. Five-Star serves micro-business owners with ₹1-10 lakh secured loans at 24-26%. The customer segments barely overlap. Many Five-Star customers are actually MFI graduates—they've grown beyond microfinance but haven't reached bank eligibility.

The fintech disruption everyone predicted hasn't materialized—at least not in Five-Star's segment. Companies like Lendingkart, Capital Float, and Flexiloans have burned hundreds of crores trying to crack small business lending. Their model—digital application, algorithm-based approval, unsecured lending—works for ₹10-50 lakh loans to GST-registered businesses. But for the provision store owner in Tirupur with no digital footprint? The algorithms fail spectacularly.

One fintech founder, requesting anonymity, explained the challenge: "We tried to serve Five-Star's segment. Spent ₹50 crore on a pilot. The fraud rates were devastating—people would take loans and disappear. Without physical presence and secured lending, the model breaks. Five-Star's branch network isn't inefficiency; it's their moat."

The regulatory environment has been surprisingly supportive. The RBI recognizes that financial inclusion requires different models. While they've tightened norms for MFIs after the Andhra Pradesh crisis, and restricted digital lenders after customer protection issues, they've been hands-off with secured business lending NBFCs. The logic is simple: secured lending with proper documentation rarely creates systemic risk.

But storm clouds are gathering. The Tamil Nadu government, always populist-leaning, has been making noises about interest rate caps for small business loans. If they cap rates at 18%, Five-Star's model collapses—they can't cover operating costs at those rates. The company has been proactively engaging with regulators, explaining that their 24% rates replace 60% informal lending, not 12% bank rates.

The competitive dynamics are fascinating. In Erode, Five-Star competes with 15 other lenders—banks, NBFCs, MFIs, informal lenders. Yet, they maintain 20% market share in their target segment. Why? Speed (7-day approval versus banks' 30 days), flexibility (they understand seasonal cash flows), and relationships (the same field officer services the customer for years).

New entrants keep trying. In 2023, three PE-backed NBFCs launched with similar models—secured micro-business lending through branches. Two have already pivoted to other segments. The third is bleeding cash with 5% NPAs. Building Five-Star's capability isn't about capital or technology—it's about organizational knowledge accumulated over decades.

The informal lending market remains Five-Star's real competition and opportunity. India's informal credit market is estimated at ₹10 trillion—local moneylenders, pawn brokers, chit funds. These lenders charge 36-120% annually but offer instant credit, no documentation, and deep relationships. Five-Star converts 1-2% of this market annually. Even capturing 10% would mean 5x growth.

Partnership dynamics are evolving. Banks, unable to serve this segment directly, are increasingly partnering with NBFCs through co-lending arrangements. Five-Star has signed agreements with three banks where the bank provides 80% of the loan at 10% interest, Five-Star provides 20% and does all servicing, and they share the 24% customer rate proportionally. This allows banks to meet priority sector targets while Five-Star accesses cheaper funding.

The bull narrative says Five-Star has found an unassailable niche. The bear narrative says competition will eventually crack the code. The reality is more nuanced. Five-Star's model is replicable but not easily. It requires patient capital (profits come after 3-4 years), operational excellence (1,500 field officers properly trained), and cultural commitment (serving customers banks reject). Most competitors have one or two of these elements; Five-Star has all three.

Looking ahead, the competitive landscape will likely consolidate. Subscale players will exit or merge. Banks will stick to their segments. Fintechs will focus on larger tickets. And Five-Star, along with 2-3 similar players, will own the secured micro-business lending space. The question isn't whether competition will intensify—it will. The question is whether Five-Star's execution advantage can stay ahead of competitive convergence.

IX. Playbook: Business & Investing Lessons

The venture capitalist leaned back in his chair at the Mumbai office of a prominent fund. "Everyone wants to find the next HDFC Bank or Bajaj Finance," he said. "But Five-Star teaches a different lesson—sometimes the best opportunities are in segments everyone else thinks are unbankable." This conversation, repeated across dozens of investment committees, captures why Five-Star matters beyond its financial returns.

Focus beats diversification—at least initially. Five-Star could have been many things. Vehicle finance (larger market), gold loans (easier underwriting), personal loans (higher margins), or housing finance (better perception). Instead, they chose secured micro-business loans and stuck with it for 20 years. This focus allowed them to develop expertise that's now nearly impossible to replicate. As Lakshmipathy once said, "We know more about provision store economics than the provision store owners themselves."

The contrast with peers is striking. Muthoot tried to diversify from gold loans into microfinance and housing—both failed. Manappuram went into vehicles and microfinance—mixed results. Meanwhile, Five-Star kept saying no. No to unsecured lending when VCs pushed for it. No to consumer loans when margins looked attractive. No to digital-only models when everyone was going digital. This discipline looks boring in presentations but brilliant in execution.

Physical presence in a digital world remains undervalued. The conventional wisdom says branches are dying, digital is the future. Five-Star proves that for certain segments, physical presence isn't just valuable—it's essential. Their 311 branches aren't cost centers; they're trust-building engines. When a customer can walk into a branch and meet the person who approved their loan, it creates accountability that no app can replicate.

But this isn't luddite thinking. Five-Star uses technology extensively—just not customer-facing. Their loan origination system, risk models, and portfolio monitoring are sophisticated. They've just recognized that their customers don't want to interact with technology; they want to interact with humans who use technology. It's a subtle but crucial distinction.

Patient capital and long-term thinking enabled everything. Five-Star was founded in 1984, didn't find product-market fit until 2002, didn't scale until 2012, and didn't go public until 2022. That's a 38-year journey to liquidity. Modern venture capital would have killed this company five times over. The investors who did back Five-Star—TPG, Matrix, Sequoia—understood they were buying into a decade-long journey, not a quick flip.

This patience shows in operations too. New branches lose money for 18 months. New field officers take six months to become productive. New markets require 12 months of study before entry. In an era of blitzscaling and growth-at-all-costs, Five-Star's measured expansion seems anachronistic. Yet they've grown AUM at 65% CAGR over five years while maintaining sub-2% NPAs. Slow is smooth, smooth is fast.

Building trust as a competitive moat sounds like MBA-speak until you see it in action. In Gobichettipalayam, "Five-Star loan" has become a generic term like "Xerox" for photocopying. Customers literally say, "I need a Five-Star loan," even when talking to other lenders. This brand equity wasn't built through advertising but through thousands of small actions—restructuring loans during COVID, not seizing property during family medical emergencies, field officers attending customer family functions.

Trust compounds differently than capital. You can't buy it, accelerate it, or digitize it. You can only earn it through consistent behavior over time. Once earned, it becomes nearly impossible for competitors to dislodge. A new lender offering 22% rates versus Five-Star's 24% often loses because customers fear hidden charges or aggressive collection. The 2% premium is essentially trust insurance.

The power of secured lending in emerging markets is systematically underappreciated. Unsecured lending is sexy—higher margins, easier to scale, beloved by VCs. But in markets with weak legal systems and limited credit bureaus, unsecured lending is essentially gambling. Five-Star's insistence on property security seems conservative, but it's enabled them to lend to segments others won't touch.

The security isn't just about recovery—it's about selection. A customer willing to pledge their house is signaling commitment. They're saying, "I believe in my business enough to risk my family's shelter." This self-selection mechanism is more powerful than any credit score. It's why Five-Star's NPAs are 2% while unsecured small business lenders routinely see 10%+ defaults.

Why timing matters less than execution in financial inclusion. People have been talking about financial inclusion since Independence. The opportunity has always existed—63 million micro-enterprises needing credit. What changed wasn't the market but Five-Star's ability to execute. They didn't wait for perfect regulations, ideal technology, or favorable markets. They just started lending and learned along the way.

Consider the various "revolutionary" moments that were supposed to transform financial inclusion: Jan Dhan Yojana (bank accounts for all), demonetization (forcing digital adoption), UPI (seamless payments), and Aadhaar (identity verification). Five-Star benefited from all these but didn't depend on any. They were profitable before, during, and after each revolution. Execution consistency beats market timing.

The paradox of profitable inclusion challenges the narrative that serving the poor requires subsidies or charitable thinking. Five-Star generates 22% ROE serving customers banks reject. They're not doing charity; they're doing business. This demonstrates that financial inclusion's problem isn't economics but execution. The margins exist; most institutions just can't access them efficiently.

For investors, Five-Star offers several lessons. First, unsexy businesses in essential services can generate exceptional returns. Second, competitive advantages in India often come from operational excellence, not technology. Third, patient capital deployed in focused strategies outperforms spray-and-pray approaches. Fourth, regulatory risk in financial services is manageable if you're genuinely solving problems rather than exploiting loopholes.

The meta-lesson might be the most important: in a world obsessed with disruption, there's value in consistency. Five-Star didn't disrupt anything. They just served customers others wouldn't, in places others wouldn't go, with patience others wouldn't show. Sometimes the biggest opportunity isn't in changing the game but in playing the existing game better than anyone else.

X. Analysis & Bear vs. Bull Case

The investment committee meeting at a major mutual fund in Mumbai, August 2024. The analyst is presenting Five-Star as a potential addition to their financial services portfolio. "The bull case is compelling," she begins, "but let me start with why this could go wrong."

The Bear Case:

Interest rate sensitivity could cripple the model. Five-Star borrows at 10-12% and lends at 24-26%. This 14% spread seems comfortable, but it's more fragile than it appears. If RBI raises rates by 200 basis points (not unprecedented), borrowing costs hit 14%. If competitive pressure or regulation prevents passing costs to customers, spreads compress to 10%. Operating costs at 7% and credit costs at 2% leave just 1% profit margin. The model breaks.

The numbers are sobering. Every 100 basis point increase in borrowing costs, without corresponding lending rate increases, reduces ROE by 4%. In a severe rate cycle, Five-Star could see ROE drop from 22% to single digits. Unlike banks with CASA deposits providing cheap funding, NBFCs are entirely wholesale-funded. They're essentially playing with borrowed money at leveraged rates.

Regulatory risks loom larger than management admits. Tamil Nadu's government has a history of populist interventions—remember the MFI crisis when they essentially banned microfinance? If they cap small business lending rates at 18% (matching priority sector rates), Five-Star's model implodes overnight. The company would need to cut operating costs by 60% or accept losses. Neither is feasible.

Competition intensifying from digital lenders is inevitable. Yes, fintechs have failed so far, but technology improves exponentially. Once someone cracks alternative data underwriting for informal businesses—using GST data, UPI transactions, or satellite imagery of business activity—Five-Star's field force advantage evaporates. A digital lender with 2% operating costs could offer 15% rates and still be profitable. Five-Star, with 7% operating costs, can't compete.

Geographic concentration creates existential risk. Tamil Nadu, Karnataka, Andhra Pradesh, and Telangana account for 95% of Five-Star's portfolio. A regional economic shock—drought, political instability, or industrial decline—could trigger massive defaults. The 2019 Andhra Pradesh crisis, where the new government essentially told people not to repay MFI loans, demonstrates how quickly regional politics can destroy lending businesses.

Economic downturn impact on micro-entrepreneurs would be devastating. Five-Star's customers are the economy's shock absorbers—when growth slows, they suffer first and worst. In a recession, that provision store sees sales drop 30%. The power loom operator loses export orders. The auto repair shop has fewer customers. Unlike salaried employees who might skip EMIs but keep jobs, these entrepreneurs could see income go to zero.

The asset quality concerns are already emerging. Gross Stage 3 assets rising to 2.46% from 1.41% might be "COVID normalization," but what if it's the beginning of a trend? As Five-Star scales rapidly—20% AUM growth—credit standards inevitably loosen. New branches lack experienced field officers. New markets lack historical data. Growth and asset quality are inherently tensioned, and Five-Star is choosing growth.

The Bull Case:

The massive addressable market makes current penetration look like a rounding error. India has 63 million micro-enterprises. Five-Star serves 300,000. That's 0.5% market share. Even reaching 5% would mean 10x growth. The credit gap for micro-enterprises is estimated at ₹25 trillion. Five-Star's ₹10,000 crore book is 0.04% of the opportunity. They could grow for decades without saturating demand.

The growth trajectory validates the model. Over the last 9 years, the company has grown from a branch network of 6 to more than 260 today and from an AUM of Rs 18 Crores to about Rs. 4,400 Crores. This isn't hypothetical potential; it's demonstrated execution. Growing at 20.5% CAGR between FY20-FY24 while maintaining sub-2% NPAs proves the model scales without breaking.

Strong unit economics generate sustainable profitability. 22% ROE isn't a one-time achievement; it's been consistent for five years. The company generates ₹1,000+ crore in profits annually. Unlike many growth stories that promise future profitability, Five-Star delivers profits today. This self-funded growth reduces dilution and creates compounding value for shareholders.

The proven management team has navigated multiple cycles. They survived demonetization, GST implementation, IL&FS crisis, COVID-19, and rising rates. Each crisis could have killed the company; instead, they emerged stronger. This isn't luck; it's operational excellence. Lakshmipathy and his team have built an organization that adapts without abandoning core principles.

Structural tailwinds support decades of growth. Financial inclusion isn't a CSR initiative anymore; it's government priority. JAM (Jan Dhan-Aadhaar-Mobile) infrastructure makes customer onboarding easier. Digital payments reduce cash handling costs. Credit bureau coverage expanding helps in risk assessment. These aren't cyclical benefits but structural improvements that permanently lower operating costs.

The competitive moat strengthens with scale. Every new branch deepens local relationships. Every satisfied customer creates referrals. Every year of data improves underwriting models. Unlike technology businesses where advantages erode quickly, Five-Star's advantages compound. A competitor starting today would need a decade to build similar capabilities—by which time Five-Star would be 10x larger.

Valuation remains reasonable despite the run-up. At ₹550 per share (August 2024), Five-Star trades at 3.5x book value. Comparable NBFCs trade at 4-6x. Bajaj Finance, the gold standard, trades at 7x. If Five-Star maintains 20% ROE and 20% growth, current valuations offer 15%+ annual returns. Not spectacular, but solid for a defensive financial services play.

The Balanced View:

The truth lies between extremes. Five-Star isn't the next HDFC Bank—the model doesn't scale to trillion-rupee size. But it's also not a house of cards waiting for regulatory or competitive disruption. It's a focused financial services company serving a specific segment profitably. The risks are real but manageable. The opportunity is large but not infinite.

For investors, Five-Star represents a clear trade-off: accepting regulatory and concentration risks for exposure to financial inclusion with proven economics. It's not suitable for conservative investors seeking steady dividends. It's perfect for those believing India's formalization story has decades to run and winners in financial inclusion will generate outsized returns.

The key monitorables are straightforward: NPA trends (must stay below 3%), ROE maintenance (above 18%), geographic diversification (reduce South India concentration below 80%), and regulatory developments (any rate cap discussions). As long as these metrics hold, the bull case dominates. If multiple metrics deteriorate simultaneously, the bear case activates quickly.

XI. Epilogue & "If We Were CEOs"

Standing in Five-Star's newest branch in Hosur, watching customers stream in with property documents and business plans, it's impossible not to think about what comes next. If we were sitting in Lakshmipathy's chair, mapping out the next decade, the path forward would balance ambition with discipline—the same formula that got Five-Star here.

The path to affordable housing finance expansion seems obvious but treacherous. Five-Star's customers trust them with business loans; many need home loans too. The same ₹30 lakh property securing a ₹3 lakh business loan could secure a ₹15 lakh home loan. The synergies are clear: same customer base, same field force, same secured lending model. But housing finance is a different game—longer tenures mean higher interest rate risk, construction finance adds project risk, and regulatory oversight is stricter. We'd pilot carefully, perhaps 10% of new disbursements, focusing on home improvements and extensions rather than new construction.

Technology adoption versus human touch balance requires surgical precision. The temptation to "digitize everything" must be resisted—it's Five-Star's human touch that creates trust. But technology can enhance human capabilities. Imagine field officers with AR glasses that overlay property values and business metrics during site visits. Or AI models that flag portfolio stress before defaults occur. The key is technology that empowers field officers, not replaces them. We'd invest ₹500 crore over five years in technology, but every rupee would be measured against field force productivity, not digital adoption metrics.

Geographic expansion strategy can't remain South India-centric forever. But expanding to Hindi heartland or Eastern India isn't just about opening branches. Each region has different business dynamics, cultural norms, and competitive landscapes. We'd expand like the Roman Empire—slowly, systematically, never extending beyond supply lines. Gujarat and Maharashtra next, leveraging their entrepreneurial cultures. Then Rajasthan and Madhya Pradesh. Eastern India last—the economic dynamics are too different. Target: 60% South India, 40% rest of India by 2030.

Building a multi-product financial services platform is the billion-dollar question. Five-Star's customers need more than loans—insurance, payments, investments. The cross-sell opportunity is massive. But every NBFC that's tried to become a financial supermarket has stumbled. We'd partner rather than build. White-label insurance products from established players. Co-branded payment solutions with banks. Investment products through mutual fund partnerships. Five-Star owns the customer relationship; partners provide products. Revenue share models align incentives without operational complexity.

ESG and financial inclusion narrative needs sophisticated articulation. Five-Star's impact is remarkable—300,000 micro-entrepreneurs funded, probably 1 million jobs supported. But impact investors want metrics: carbon footprint reduced, women entrepreneurs funded, rural areas served. We'd invest in impact measurement—tracking not just loans disbursed but businesses grown, jobs created, families lifted from poverty. This isn't virtue signaling; it's accessing patient capital pools that value impact alongside returns.

The organizational challenge might be the hardest. Five-Star succeeded through entrepreneurial energy and informal networks. Scale demands processes and systems. But processes kill entrepreneurship. We'd implement "two-speed" organization design. The core lending business runs on strict processes—no exceptions. But 20% of resources go to "Five-Star Labs," experimenting with new products, segments, and models. Failures are celebrated if learning occurs. This maintains innovation while protecting the core.

Capital allocation would be ruthlessly disciplined. The temptation during good times is to chase growth everywhere. We'd maintain strict hurdle rates: new branches must project 18-month breakeven, new products need 25% ROE potential, acquisitions require immediate accretion. Growth capital goes only to proven models. Experimental capital is capped at 10% of profits. Shareholders get 30% of profits as dividends—enough to attract income investors without starving growth.

The succession planning conversation nobody wants requires immediate attention. Lakshmipathy built Five-Star, but institutions outlive founders. We'd implement professional management transition over five years. Identify internal leaders who embody Five-Star's culture. Hire external talent for specialized roles (technology, risk, treasury). Create a leadership council rather than depending on one person. The founder's family maintains board presence but operational professionals run daily business.

Risk management evolution becomes existential at scale. At ₹10,000 crore AUM, relationship-based risk management works. At ₹50,000 crore, it breaks. We'd invest in predictive analytics, stress testing, and portfolio monitoring. But—and this is crucial—these augment rather than replace field intelligence. The model: algorithms flag risks, humans investigate and decide. Never let the model become the master.

Final reflections on building sustainable financial inclusion: Five-Star proves that serving the underserved isn't charity—it's good business. But good business requires patient capital, operational excellence, and genuine commitment to customers. The next decade will test whether Five-Star can maintain its soul while scaling its body. Can they stay close to customers while growing 10x? Can they maintain credit discipline while facing competitive pressure? Can they balance stakeholder interests—customers needing affordable credit, shareholders wanting returns, employees seeking growth, and society demanding inclusion?

The answer lies not in strategy documents or investor presentations, but in thousands of daily decisions in hundreds of branches. Will the field officer in Karur restructure a struggling customer's loan or push for recovery? Will the branch manager in Salem approve a borderline case or play safe? Will senior management choose short-term profits or long-term relationships?

Five-Star's story isn't complete. They've proven financial inclusion can be profitable. They've shown that trust beats technology in certain segments. They've demonstrated that patient execution trumps aggressive scaling. But the hardest part lies ahead: becoming an institution that outlives its founders while maintaining its founding principles. If they succeed, Five-Star won't just be a successful NBFC—it'll be a template for inclusive finance globally. If they fail, they'll join the graveyard of companies that lost their way while chasing scale.

The micro-entrepreneur in Gobichettipalayam doesn't care about any of this. She just knows that Five-Star gave her a loan when nobody else would, at a rate she could afford, with terms she could understand. That's the ultimate test: not what analysts think, or what stock prices do, but whether that entrepreneur can grow her business and improve her family's life. Everything else is just keeping score.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube