Fine Organic Industries: The Oleochemical Additives Empire

I. Introduction & Episode Roadmap

Picture a sprawling chemical plant in Ambernath, just outside Mumbai, where massive reactors transform palm oil and vegetable derivatives into microscopic additives that end up in everything from the plastic wrap on your leftovers to the ice cream in your freezer. This is Fine Organic Industries—a company most Indians have never heard of, yet whose products touch their lives dozens of times each day.

With a market capitalization of ₹15,345 crore, revenues of ₹2,205 crore, and profits of ₹390 crore, Fine Organic has quietly built one of India's most successful specialty chemical businesses. They manufacture over 450 different oleochemical-based additives—compounds that make plastics slip smoothly through manufacturing equipment, prevent fog on greenhouse films, keep cosmetics silky, and ensure your packaged foods stay fresh. In an industry dominated by European and American giants like BASF and Croda, this Mumbai-based company has carved out a global leadership position in several niche categories.

The story of Fine Organic is fundamentally a story about finding fortune in the microscopic—how two chemical entrepreneurs spotted an opportunity in products that typically comprise less than 1% of any final formulation but are absolutely critical to making those products work. It's about building technical moats so deep that customers would rather wait three years for your product approval than switch to a competitor. And perhaps most remarkably, it's about how a company founded to substitute imports in 1970s socialist India became the world's largest producer of slip additives, exporting to over 80 countries.

This deep dive will trace Fine's journey from a small partnership serving Mumbai's ice cream makers to a publicly-traded specialty chemical powerhouse. We'll explore the technical complexity behind seemingly simple additives, understand why customers rarely switch suppliers once approved, examine the economics of a business with 25%+ EBITDA margins despite commodity raw material exposure, and analyze what the future holds for this hidden champion of Indian manufacturing.

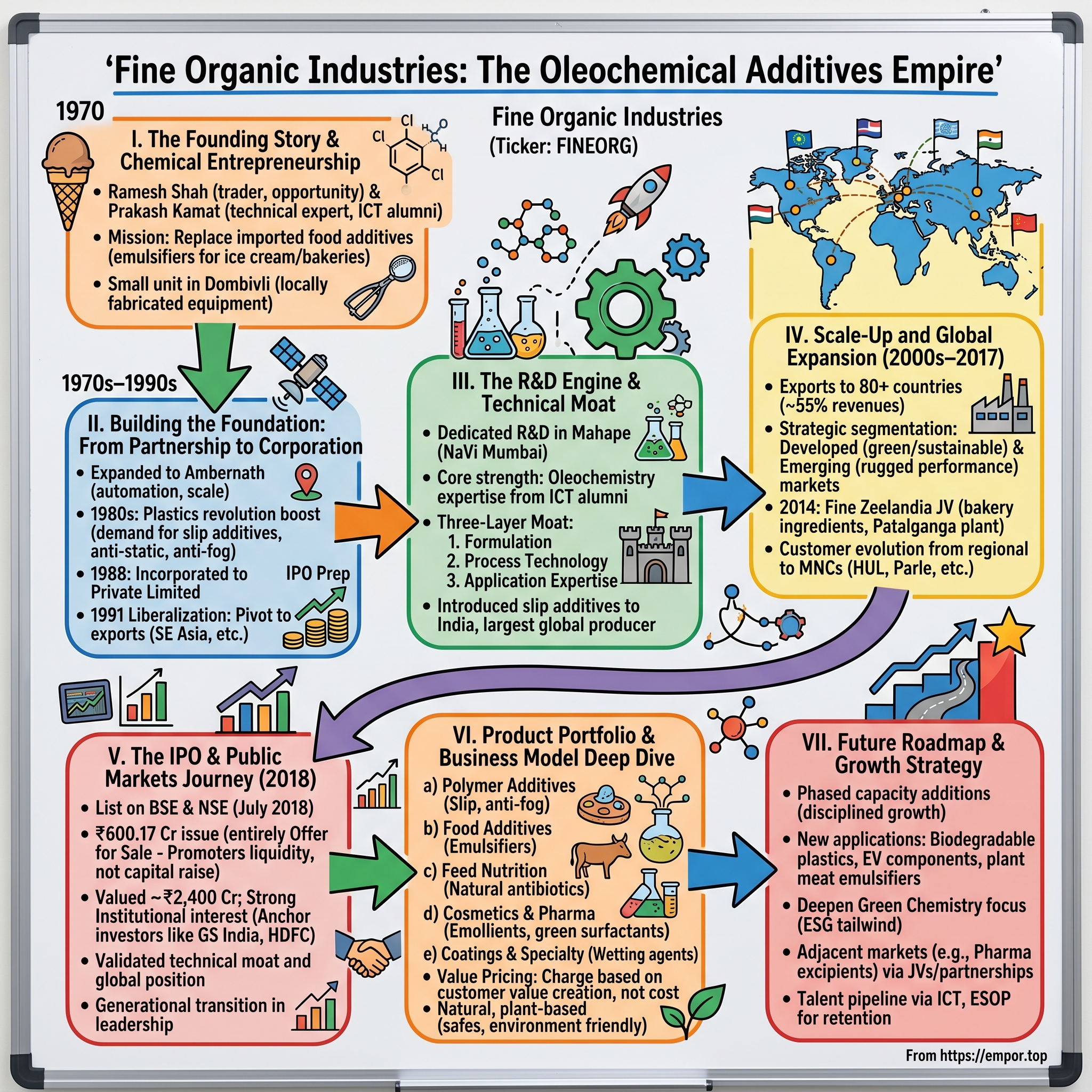

II. The Founding Story & Chemical Entrepreneurship (1970)

The year was 1970. India was still finding its industrial footing, three years into Indira Gandhi's first term as Prime Minister. The economy was closed, licenses were required for everything, and importing even basic industrial materials required navigating a byzantine bureaucracy. It was in this environment that Ramesh Shah, a Mumbai-based chemical trader, noticed something peculiar: local ice cream manufacturers and bakeries were struggling to source quality emulsifiers—specialized additives that prevent oil and water from separating in food products.

Shah had been in the chemical trading business long enough to recognize opportunity in scarcity. But he also knew that importing these additives was becoming increasingly difficult and expensive due to foreign exchange restrictions. What India needed wasn't another trader—it needed a manufacturer. The problem was that Shah understood markets, not molecules. For that, he needed a technical partner.

Enter Prakash Kamat, a young graduate from the University Department of Chemical Technology (UDCT, now ICT)—India's premier institution for chemical engineering. Kamat wasn't just another chemistry graduate; he had spent years studying oleochemistry, the science of deriving useful compounds from plant and animal fats. Where others saw commodity vegetable oils, Kamat saw raw materials for hundreds of specialized additives. His academic background had given him something rare in 1970s India: deep technical knowledge of how to transform locally available agricultural products into high-value specialty chemicals.

The partnership made perfect sense. Shah brought commercial acumen and market relationships; Kamat brought technical expertise and process knowledge. Together, they founded Fine Organic Industries as a partnership firm with a simple but ambitious mission: replace imported food additives with locally manufactured alternatives of equal or better quality.

Their first facility wasn't much to look at—a small unit in Dombivli, an industrial suburb of Mumbai. The equipment was basic, much of it fabricated locally because importing chemical reactors was virtually impossible. But what they lacked in infrastructure, they made up for in ingenuity. Kamat spent countless hours in the lab, tweaking formulations to work with Indian raw materials. Palm oil from Kerala, groundnut oil from Gujarat, castor oil from Rajasthan—these became their feedstocks for creating emulsifiers that could match imported products.

The timing was fortuitous. India's dairy industry was beginning to organize under Operation Flood, creating demand for ice cream and processed dairy products. The bakery industry was modernizing, moving from traditional methods to industrial production. Both sectors desperately needed reliable, locally available additives. Fine Organic's first customers were small—local ice cream makers in Mumbai, neighborhood bakeries expanding their operations. But these early relationships taught the founders crucial lessons about the additives business.

First, they learned that in specialty chemicals, technical support matters as much as the product itself. When a bakery's bread didn't rise properly or an ice cream batch crystallized, Fine's team would rush to the customer's facility, often working through the night to solve the problem. This wasn't just customer service—it was building trust in an industry where switching suppliers could mean months of reformulation and testing.

Second, they discovered that succeeding in additives required thinking in systems, not just molecules. An emulsifier that worked perfectly in the lab might fail in a customer's production line due to temperature variations, mixing speeds, or interactions with other ingredients. Kamat began developing what would become Fine's core competency: creating not just products but complete solutions tailored to specific applications and processing conditions.

The early 1970s were marked by constant experimentation and gradual expansion. The partnership added new products to their portfolio—anti-caking agents for spice manufacturers, mold inhibitors for bread makers, texture modifiers for confectioneries. Each new product meant months of development, but also opened doors to new customer segments. By 1975, Fine Organic had moved beyond import substitution to something more ambitious: they were beginning to innovate, creating formulations specifically optimized for Indian conditions—high humidity, extreme temperatures, and local taste preferences.

This period also established the company's fundamental approach to growth: deep technical expertise combined with intimate customer relationships. While competitors focused on volume and commodity products, Fine specialized in solving specific, complex problems with tailored additives. It was a strategy that required patience—products took months to develop and years to fully commercialize—but it created switching costs and customer loyalty that would become the foundation of Fine's competitive moat.

The import substitution era of the 1970s wasn't just about replacing foreign products; it was about building indigenous technical capabilities. For Fine Organic, this meant not just manufacturing additives but understanding the science behind them deeply enough to innovate. Kamat's UDCT connections proved invaluable here—he recruited fellow alumni who brought expertise in different aspects of oleochemistry. This early focus on technical talent would become a defining characteristic of the company.

By the end of the decade, Fine Organic had validated its founding thesis. Indian manufacturers didn't just need local suppliers—they needed technical partners who understood their unique challenges. The company that began in a small Dombivli facility was now serving customers across Maharashtra and beginning to explore opportunities in other states. But Shah and Kamat understood that to truly scale, they would need to move beyond food additives into larger, more diverse markets. The foundation was built; now it was time to construct the empire.

III. Building the Foundation: From Partnership to Corporation (1970s–1990s)

The Dombivli facility was bursting at its seams by 1978. Orders were backing up, and Fine Organic faced a pleasant but pressing problem: demand was outstripping their ability to supply. The decision to expand wasn't just about capacity—it was about ambition. Shah and Kamat chose Ambernath for their second facility, a location that would later become the company's flagship manufacturing complex. But this expansion marked something deeper: a transition from solving local problems to building industrial-scale operations.

The Ambernath facility was different from the start. While Dombivli had been cobbled together with locally fabricated equipment and manual processes, Ambernath was designed with automation and scale in mind. The partners invested in temperature-controlled reactors, automated mixing systems, and quality control laboratories that could match international standards. This wasn't cheap—the investment consumed nearly all of the company's accumulated profits and required taking on debt for the first time. But it signaled Fine's evolution from a small partnership to a serious industrial enterprise.

The early 1980s brought an unexpected catalyst for growth: the plastics revolution in India. As the economy gradually liberalized under Rajiv Gandhi, plastic manufacturing exploded. Suddenly, there was massive demand for additives that Fine had only experimented with—slip additives that prevented plastic films from sticking together, anti-block agents that allowed sheets to separate easily, and anti-static additives that prevented dust accumulation. The food additives expertise had given Fine the technical foundation; now they were applying those capabilities to entirely new markets.

The transition wasn't seamless. Plastic additives required different performance characteristics than food additives—they needed to withstand higher processing temperatures, remain stable over longer periods, and meet different regulatory requirements. Kamat spent months reformulating products, often working with customers' production teams to understand exactly how additives behaved in their specific equipment. One breakthrough came when they developed a slip additive specifically optimized for the lower-grade polyethylene commonly used in India, which performed better than imported alternatives designed for higher-quality resins.

By 1985, Fine established a third facility in Badlapur, dedicated entirely to non-food additives. This geographical separation wasn't just operational—it was strategic. Food additives required stringent hygiene standards and different certifications than industrial additives. By segregating production, Fine could optimize each facility for its specific requirements while preventing any cross-contamination concerns that might worry food customers.

The company's product portfolio was expanding rapidly, but not randomly. Each new product was chosen based on three criteria: technical feasibility with local raw materials, significant import substitution opportunity, and potential for customization that would create customer stickiness. This disciplined approach meant saying no to many opportunities—commodity products with thin margins, additives requiring rare raw materials, or products where imported alternatives were already deeply entrenched.

A pivotal moment came in 1988 when Fine Organic decided to incorporate, transforming from a partnership to Fine Organic Industries (Mumbai) Private Limited. This wasn't just a legal formality. Incorporation allowed them to raise external capital, offer equity to key employees, and establish the governance structures needed for a growing enterprise. More importantly, it marked the beginning of professionalizing what had been a tightly-held partnership.

The newly incorporated company immediately faced its first major test: the 1991 economic crisis and subsequent liberalization. As India opened its economy, foreign chemical companies that had been kept out for decades suddenly had access to Indian markets. Many local manufacturers, protected for years by import restrictions, crumbled under international competition. But Fine Organic's response was counterintuitive—they saw liberalization not as a threat but as an opportunity to access global markets.

The early 1990s marked Fine's first serious foray into exports. The same technical capabilities that had allowed them to substitute imports in India proved valuable in other developing markets facing similar challenges. Their first international customers were in Southeast Asia—Thailand, Malaysia, Indonesia—countries with growing plastics and food processing industries but limited local additive manufacturing. Fine's products, optimized for tropical conditions and developing market realities, found ready acceptance.

But perhaps the most important development of this period was the establishment of Fine's R&D center in 1992. Until then, product development had been largely reactive—solving specific customer problems as they arose. The dedicated R&D facility, staffed with ICT graduates and equipped with sophisticated analytical equipment, allowed Fine to become proactive. They began developing products anticipating market needs, filing patents, and building an intellectual property portfolio that would become a significant competitive advantage.

The R&D center's first major success was developing a range of green additives—products derived entirely from renewable vegetable sources rather than petroleum. This was prescient; while sustainability wasn't yet a mainstream concern in the early 1990s, Fine recognized that regulatory and consumer preferences were moving toward bio-based products. These green additives commanded premium prices and opened doors to environmentally conscious customers in Europe and North America.

By 1995, Fine Organic had transformed from a small partnership serving local ice cream makers to a diversified specialty chemical company with three manufacturing facilities, hundreds of products, and customers across a dozen countries. Revenue had grown from lakhs to crores, but more importantly, the company had built three critical assets that money couldn't easily buy: deep technical expertise in oleochemistry, long-standing customer relationships with switching costs measured in years, and a culture of innovation rooted in solving real-world problems.

The foundation was now complete. Fine had proven it could not only substitute imports but innovate beyond them. It had shown it could compete with international players not on price but on technical superiority and customer intimacy. And perhaps most importantly, it had demonstrated that an Indian company could build global competitiveness in specialty chemicals—a sector long dominated by Western corporations. The next challenge would be scaling these capabilities to become not just a successful Indian company but a global leader in chosen niches.

IV. The R&D Engine & Technical Moat (1990s–2000s)

The late afternoon sun filtered through the windows of Fine Organic's R&D center in Mahape, Navi Mumbai, in 1998. Prakash Kamat walked through the labs, observing young chemists—many fresh ICT graduates like he once was—working on formulations that would have seemed like science fiction when he started the company. One was developing a slip additive that could maintain its properties at the extreme temperatures of automotive engine compartments. Another was working on a food-grade emulsifier that could extend shelf life by 40% without affecting taste. This wasn't just a laboratory; it was the engine room of Fine's transformation from a regional player to a global technology leader.

Kamat, the current Chairman of the Board and an Institute of Chemical Technology (ICT, formerly known as UDCT) alumnus with almost 50 years of experience in chemistry and process technology, understood something fundamental about the specialty chemicals business: in a world where products differ by molecular tweaks, technical superiority isn't optional—it's existential. The R&D center he established wasn't just about creating new products; it was about building an institutional capability that could outlast any individual.

The ICT connection proved crucial. Fine built a strong R&D team consisting of 18 scientists, engineers and technologists, with graduates from the renowned ICT preferred in the R&D team. This wasn't nepotism or alumni favoritism—ICT produced India's finest chemical engineers, and more importantly, they came with a shared technical language and problem-solving approach that accelerated collaboration. When a customer in Thailand needed an anti-fog additive for greenhouse films that could withstand monsoon humidity, the team could move from concept to prototype in weeks rather than months.

The technical moat Fine was building had three layers, each more difficult to replicate than the last. The first was product formulation—the ability to create additives that performed specific functions. This was table stakes; any competent chemical company could eventually reverse-engineer a formulation. The second layer was process technology—knowing not just what to make but how to make it efficiently, consistently, and at scale. Fine's processes, refined over thousands of production runs, could achieve yields and purities that competitors struggled to match.

But the third layer was the real differentiator: application expertise. Fine's R&D team didn't just create additives; they understood intimately how those additives behaved in customers' production environments. When a plastic film manufacturer complained about inconsistent slip properties, Fine's scientists didn't just adjust the additive formulation—they studied the customer's extrusion equipment, analyzed the interaction between the additive and other components in the polymer matrix, and developed a solution optimized for that specific production line.

Fine Organics was the first company to introduce slip additives in India and became the largest producer of slip additives in the world. This wasn't accidental leadership—it was the result of a deliberate strategy to dominate specific niches through technical excellence. Slip additives, which reduce friction between plastic surfaces, might seem mundane, but they're critical for everything from food packaging to industrial films. Fine's versions didn't just work—they migrated to the surface faster, lasted longer, and required lower dosages than competitors' products.

The approval cycle became Fine's most powerful competitive moat. In industries like food and pharmaceuticals, switching additive suppliers meant extensive testing, regulatory reapproval, and production line adjustments—a process that could take 3-5 years and cost millions. Once Fine's additives were approved and integrated into a customer's process, displacement became almost impossible unless there was a catastrophic failure. This wasn't lock-in through contracts or pricing—it was lock-in through technical integration.

The company's product portfolio expanded strategically during this period. By the 2000s, Fine offered Polymer Additives including lubricants, anti-fogging agents, anti-static additives, slip additives, processing aids, and dispersants; Food Additives including emulsifiers, anti-fungal agents, beverage clouding agents, anti-crystallizers; Feed Nutrition Additives including natural antibiotics, nutritional additives, and anti-fungal agents; Cosmetics & Pharma (CosPha) Additives including emollients, emulsifiers, green surfactants; and Coatings & Specialty Additives including wetting agents, dispersants, anti-corrosive additives, emulsifiers. Each category represented years of R&D investment and customer relationship building.

The green chemistry angle became increasingly important as the decade progressed. Fine's oleochemical-based additives are derived from plants, making them significantly safer and environment friendly compared to petrochemical-based additives. This wasn't greenwashing—it was a fundamental technological advantage. As environmental regulations tightened globally, particularly in Europe, Fine's bio-based additives could meet new standards without reformulation, while competitors scrambled to develop alternatives to their petroleum-based products.

The R&D center's work extended beyond product development to process innovation. They developed proprietary techniques for extracting and modifying fatty acids from vegetable oils, achieving purities that allowed Fine's additives to perform consistently across different applications. One breakthrough involved a catalytic process that could convert low-value palm oil derivatives into high-performance polymer additives, turning what was essentially agricultural waste into products selling for 50-100 times the raw material cost.

Customer collaboration became a hallmark of Fine's R&D approach. Rather than developing products in isolation and then seeking markets, they embedded themselves in customers' development processes. When a major food company was developing a new line of extended shelf-life products, Fine's scientists worked alongside their food technologists for 18 months, creating custom emulsifiers that met specific performance criteria. This co-development model created switching costs measured not just in money but in institutional knowledge.

The intellectual property strategy during this period was deliberately nuanced. While Fine filed patents for truly novel compounds and processes, much of their competitive advantage lay in trade secrets—precise processing conditions, catalyst formulations, and quality control parameters that couldn't be easily reverse-engineered. This approach avoided the disclosure requirements of patents while maintaining technological leadership.

By 2005, Fine's R&D capabilities had transformed the company's market position. They were no longer competing on price or even quality alone—they were competing on innovation speed and technical problem-solving. When a customer needed a new additive, Fine could move from concept to commercial production faster than competitors because they had the technical depth to anticipate problems and the process expertise to scale quickly.

The human capital investment in R&D paid dividends beyond product development. The culture of technical excellence permeated the entire organization. Production operators understood the chemistry behind what they were making. Sales representatives could discuss molecular structures with customers' R&D teams. Quality control became not just about meeting specifications but about understanding why those specifications mattered.

The financial returns from this R&D investment were compelling. Products developed in-house commanded premium prices—often 20-30% above commodity additives. More importantly, they created customer relationships that transcended typical vendor-buyer dynamics. Fine became a technical partner, embedded in customers' innovation processes, making displacement not just expensive but risky.

The R&D engine also enabled geographic expansion. Products developed for Indian conditions—high heat, humidity, and variable raw material quality—found ready markets in Southeast Asia, Africa, and Latin America. The technical solutions Fine developed for resource-constrained environments proved valuable globally as sustainability became a priority even in developed markets.

As the 2000s progressed, Fine's R&D evolved from reactive problem-solving to proactive innovation. They began anticipating market needs years in advance, investing in technologies that wouldn't see commercial application for 5-7 years. This long-term thinking, unusual in the often quarter-focused chemical industry, created a pipeline of innovations that would sustain growth well into the future.

The story of Fine's R&D transformation illustrates a broader truth about specialty chemicals: in an industry where products are often molecularly similar, competitive advantage comes from the accumulation of thousands of small technical improvements, deep customer relationships, and the patient building of capabilities that competitors can see but cannot easily replicate. The technical moat Fine built during this period wouldn't just protect margins—it would define the company's trajectory for decades to come.

V. Scale-Up and Global Expansion (2000s–2017)

The monsoon of 2006 brought more than rain to Mumbai—it brought a delegation from Zeelandia International, the Dutch bakery ingredients giant founded in 1900. They weren't in India for the usual multinational reconnaissance mission. They had been watching Fine Organic's growth in food emulsifiers with interest, recognizing something most Western companies missed: Fine had built distribution and technical capabilities in emerging markets that would take Zeelandia decades to replicate. What started as a courtesy meeting would evolve into one of the most successful joint ventures in India's specialty chemicals sector.

But before that partnership materialized, Fine was already executing an ambitious expansion strategy. The Ambernath facility, which had started as their second plant in the 1980s, underwent massive capacity expansions in phases throughout the early 2000s. Over the next five decades, the Company worked actively on expanding its additives product portfolio across several new applications and significantly grew its customer base across India and export markets. Each expansion wasn't just about adding reactors—it was about building capabilities for entirely new product categories.

The numbers told a compelling story. By 2005, Fine was exporting to over 40 countries. By 2010, that number had doubled to 80+. The Company has a wide range of 400+ products, 750+ direct customers (ranging from local to national to multi-national clients) and 170+ distributors across more than 70 countries. Exports accounted for ~55% of the Company's revenues in FY20. This wasn't accidental international success—it was the result of a deliberate strategy to build global distribution capabilities while maintaining technical excellence.

The export strategy revealed Fine's sophisticated understanding of market segmentation. In developed markets like Europe and North America, they positioned themselves as the sustainable alternative—oleochemical-based additives that met increasingly stringent environmental regulations. In emerging markets across Southeast Asia, Africa, and Latin America, they leveraged their experience with challenging conditions—high humidity, temperature extremes, variable raw material quality—to offer solutions that simply worked better than products designed for controlled Western environments.

The distribution network became a competitive advantage in itself. Fine didn't just sign up distributors; they trained them, supported them technically, and treated them as extensions of their own sales force. A distributor in Thailand wasn't just moving products—they were equipped to provide basic technical support, troubleshoot customer problems, and identify new application opportunities. This distributed technical capability allowed Fine to serve customers globally without the massive overhead of international subsidiaries.

Fine Zeelandia is a 50/50 joint venture company between Fine Organics, a pioneer and globally recognised manufacturer of emulsifiers for the food industry, over 48 years in India and Zeelandia, a global leader in bakery and patisserie ingredients since 118 years. The 2014 joint venture with Zeelandia represented a new phase in Fine's evolution. Fine Zeelandia will be based in Mumbai and is a 50/50 joint venture between Fine Organics and Zeelandia. It will combine the technical and marketing strengths of both the companies to bring an innovative range of baking and patisserie ingredients.

The logic was compelling for both parties. Zeelandia gained immediate access to Fine's distribution network across South Asia and their deep understanding of emerging market dynamics. Fine gained access to Zeelandia's century of bakery expertise and their sophisticated product portfolio. Fine Zeelandia has put up a state-of-the-art manufacturing facility in Patalganga, Maharashtra, which will produce bakery premixes for ready to make cakes, muffins, breads and a variety of bakery products for the Indian and its neighbouring markets.

The joint venture illustrated Fine's strategic sophistication. Rather than viewing international partnerships as threats to independence, they saw them as accelerators of capability building. The Patalganga facility wasn't just manufacturing Zeelandia's products under license—it was adapting them for South Asian tastes and conditions, creating entirely new formulations that neither company could have developed alone.

This period also saw Fine's manufacturing philosophy evolve. The new facilities weren't just larger—they were smarter. Automation wasn't implemented for its own sake but strategically deployed where it could ensure consistency and quality. A visitor to the Ambernath facility in 2010 would have seen an intriguing mix: state-of-the-art automated reactors alongside areas where skilled operators still manually controlled critical process steps that required human judgment.

The product portfolio expansion during this period was staggering but strategic. Fine wasn't chasing every opportunity—they were building defensible positions in specific niches. In slip additives, they had become the global leader. In food emulsifiers, they were the preferred supplier for many multinational food companies operating in Asia. In each category, the strategy was the same: develop deep technical expertise, create customer-specific solutions, and build switching costs through superior service.

The financial discipline during this expansion was remarkable. Despite massive capacity additions and international expansion, Fine maintained strong cash flows and avoided excessive leverage. They understood that in specialty chemicals, financial strength wasn't just about funding growth—it was about having the patience to wait for long approval cycles and the resilience to weather raw material price volatility.

The customer base evolution told its own story of transformation. In 2000, Fine's customers were primarily regional players in India and neighboring countries. By 2017, In the 12 months ended December 31, 2017, Fine Organics had 603 direct customers (i.e., end-users of its products) and 127 distributors (who sold company's products to more than 5,000 customers) from 67 countries. The Company's direct customers are multinational, regional and local players manufacturing consumer products, such as Hindustan Unilever and Parle Products, and petrochemical companies and polymer producers globally.

The geographic expansion wasn't without challenges. Different markets had different regulatory requirements, quality expectations, and business practices. Fine's response was to build local expertise while maintaining global standards. They hired local technical staff who understood regional requirements but trained them in Fine's methodologies. They adapted their products for local conditions but maintained consistent quality standards globally.

The period from 2000 to 2017 also saw Fine's competitive positioning evolve. They were no longer the scrappy Indian company competing on price—they were technology leaders in specific niches, competing with and often beating established Western companies. When a global food company needed a new emulsifier for a product launching simultaneously in 20 countries, Fine could develop, test, and scale production faster than competitors because they had built the capabilities over decades.

By 2017, Fine Organic had transformed from a domestic manufacturer with some exports to a truly global specialty chemical company. As of December 31, 2017, these three production facilities have a combined installed capacity of approximately 64,300 tonnes per annum. The company that had started with a small facility in Dombivli now operated sophisticated manufacturing complexes producing hundreds of products for thousands of customers worldwide.

This transformation wasn't just about scale—it was about capability. Fine had built three interconnected strengths that would be nearly impossible for competitors to replicate: deep technical expertise in oleochemistry with a focus on sustainable, plant-based products; a global distribution and service network with local expertise; and manufacturing capabilities that could efficiently produce both large-volume commodity additives and small-batch specialty products.

The stage was now set for the next phase of Fine's journey. The company had proven it could compete globally, had built world-class capabilities, and had demonstrated consistent execution over decades. The question was no longer whether Fine could succeed—it was how to crystallize this value for stakeholders while maintaining the entrepreneurial spirit that had driven their success.

VI. The IPO & Public Markets Journey (2018)

The conference room at Fine Organic's Mumbai headquarters was packed on June 19, 2018, as investment bankers from JM Financial and Edelweiss Financial Services prepared for the IPO. Chairman Prakash Kamat and CEO Jayen Shah (son of late founder Ramesh Shah) reviewed final numbers before the IPO bidding, which ran from June 20-22, 2018. The shares were listed on BSE and NSE on July 2, 2018.

The decision to go public had been years in the making, but the structure was unusual: Fine Organic Industries IPO is a bookbuilding of ₹600.17 crores. The issue is entirely an offer for sale of 0.77 crore shares. This wasn't a capital-raising exercise—the promoters were selling 25% of their stake without the company receiving any proceeds. For a company that was virtually debt-free and generating strong cash flows, this structure sent a clear message: Fine didn't need capital; the promoters needed liquidity after nearly five decades of building the business.

Fine Organic Industries IPO price band is set at ₹783 per share. The issue is priced at ₹783 per share. At this price, the company was valued at approximately ₹2,400 crore—a valuation that sparked intense debate. The P/E multiple of around 27-30x was rich by Indian chemical sector standards, especially for a company with significant commodity raw material exposure. But the bankers argued, and the promoters believed, that Fine deserved a premium for its technical moat, global market position, and consistent execution track record.

The anchor investor round on June 19 provided early validation. The company has allotted 22,99,497 equity shares to 15 anchor investors at Rs 783 per scrip, garnering Rs 180.05 crore. Among the anchor investors are Goldman Sachs India, HDFC Small Cap Fund, SBI Magnum Comma Fund, DSP BlackRock Equity & Bond Fund and IDFC Equity Opportunities Fund – Series 5. The presence of sophisticated institutional investors suggested confidence in Fine's story, even at premium valuations.

The three-day public subscription period revealed interesting dynamics. Final Closing Figures (Around 11PM, 22nd June) QIBs: 12.86X RII: 1.62X NII: 21.01X Application wise: 1.45X Total: 8.99X The qualified institutional buyer (QIB) and non-institutional investor (NII) categories showed strong interest, while retail participation was relatively muted at just 1.62 times. This pattern suggested that sophisticated investors understood Fine's business model better than retail participants who might have been deterred by the high absolute price and unfamiliarity with the specialty chemicals sector.

The listing day, July 2, 2018, brought vindication for the IPO pricing. The scrip listed at Rs 815, reflecting a gain of 4 per cent from the issue price on BSE. It later soared 5.10 per cent to Rs 823. While not a blockbuster listing gain by Indian IPO standards, the steady premium indicated that the market accepted Fine's valuation and recognized the quality of the business.

Behind the IPO lay a deeper strategic calculation. The promoter family understood that after 48 years of operations, Fine had reached an inflection point. The business had scaled successfully, built global capabilities, and established market leadership in several categories. But accessing the next level of growth—potentially through acquisitions, technology partnerships, or aggressive capacity expansion—would be easier as a listed entity with liquid currency in the form of tradeable shares.

The IPO prospectus revealed fascinating details about Fine's business model that many investors had never fully appreciated. As per CRISIL Research Report, it is the largest manufacturer of oleochemical-based additives in India and a strong player globally in this industry. The company produces a wide range of specialty plant derived oleochemicals-based additives used in the food, plastic, cosmetics, paint, ink, coatings and other specialty application in various industries. It has a range of 387 different products sold under the 'Fine Organics' brand. Fine Organics is the first company to introduce slip additives in India and is the largest producer of slip additives in the world.

The financial metrics painted a picture of a highly efficient operation. The company was generating EBITDA margins of over 20% despite significant raw material cost volatility. Return on equity consistently exceeded 25%. Working capital management was exemplary, with cash conversion cycles that were among the best in the specialty chemicals sector. These weren't just good numbers—they reflected decades of operational refinement and deep customer relationships that allowed Fine to maintain pricing power even in competitive markets.

The IPO also marked a generational transition. While Prakash Kamat remained as Chairman, providing technical leadership and institutional memory, the second generation—including Mukesh Shah, Jayen Shah, and Tushar Shah—was taking operational control. This transition had been carefully managed over years, with the second generation gaining experience across different functions before assuming leadership roles. The IPO, in many ways, was their coming-out party, demonstrating to public market investors that Fine could thrive beyond its founders.

The use of proceeds section was notably absent—because there were no proceeds to the company. But the promoters' plans for their personal proceeds were strategic. Rather than simply diversifying wealth, much of the capital would remain connected to the business ecosystem—invested in related ventures, technology partnerships, and maintaining sufficient dry powder for potential buy-backs or creeping acquisitions if market conditions presented opportunities.

The regulatory scrutiny that came with being a public company was a significant change for Fine. After decades of operating as a closely-held family business, they now had to deal with quarterly earnings calls, analyst meetings, and the constant pressure of market expectations. The company responded by significantly upgrading its financial reporting, investor relations, and governance structures. Independent directors with deep industry experience were brought onto the board, adding external perspective to strategic decisions.

One underappreciated aspect of the IPO was how it changed Fine's relationship with customers and suppliers. Being a listed company with published financials and regular disclosures provided transparency that large multinational customers valued. It became easier to win large contracts when customers could verify Fine's financial strength and operational metrics through public filings rather than relying on private assurances.

The employee stock option plan (ESOP) introduced around the IPO period proved transformational for talent retention. Key technical personnel and senior managers who had been instrumental in building Fine's capabilities could now participate in wealth creation. This was particularly important for retaining the ICT graduates and technical experts who formed the backbone of Fine's R&D capabilities. The ability to offer equity compensation also helped attract senior talent from larger competitors.

Market reaction in the months following the IPO validated the pricing. The stock steadily appreciated as investors began understanding the specialty chemicals sector better and recognizing Fine's unique position within it. Sell-side analysts initiated coverage with largely positive ratings, highlighting the company's technical moats, diversified product portfolio, and exposure to growing end markets.

The IPO also catalyzed internal changes. With quarterly earnings pressure, Fine had to become more disciplined about capital allocation, project returns, and operational efficiency. Management information systems were upgraded. Key performance indicators were refined. The rigor required for public market reporting actually improved internal decision-making, forcing more systematic evaluation of expansion projects and R&D investments.

One challenge that emerged post-IPO was managing market expectations during raw material price volatility. The company uses vegetable oils, including rapeseed oil, palm oil, palm kernel oil, sunflower oil, castor oil, soybean oil, rice bran oil as a raw material and it represents around 62% of the total expense. The company primarily import raw materials derived from palm and palm kernel oil. Recently, in Nov 2017, the govt of India has increased the tax on crude palm oil to 30% from 15%, and increased import tax duty on refined palm oil imports to 40% from 25%. This will dampens the margin further from next fiscal. The market initially struggled to understand that Fine's business model could pass through raw material costs with a lag, maintaining dollar margins even if percentage margins compressed temporarily.

The IPO fundamentally changed Fine's growth trajectory. Access to capital markets meant they could now consider larger acquisitions, faster capacity expansions, and more aggressive R&D investments. The public market validation also strengthened their position in partnership negotiations with global chemical companies who now saw Fine as a credible, transparent partner rather than an opaque family business.

As 2018 progressed and Fine settled into life as a public company, it became clear that the IPO was not an end but a beginning. The company that had taken 48 years to reach a valuation of ₹2,400 crore was now positioned to potentially double or triple that value in a fraction of the time. The combination of public market discipline, access to capital, and maintained entrepreneurial spirit created a powerful platform for the next phase of growth. The IPO had successfully crystallized value for the founding generation while positioning Fine Organic Industries for its next chapter as a global specialty chemical leader.

VII. Product Portfolio & Business Model Deep Dive

The laboratory at Fine Organic's Mahape R&D center is an exercise in controlled chaos. Scientists huddle over test results showing how a new slip additive performs at different temperatures. Another team analyzes samples from a customer's production line where a food emulsifier isn't providing the expected shelf life. In the pilot plant, a scaled-up batch of a cosmetic additive undergoes stability testing. This is where Fine's 450+ products come to life—not as abstract chemical formulas but as solutions to specific, real-world problems.

Product Portfolio[1] a) Polymer Additives – Lubricants, anti-fogging agents, anti-static additives, slip additives, processing aids, and dispersants. b) Food Additives – Emulsifiers, anti-fungal agents, beverage clouding agents, anti-crystallizers. c) Feed Nutrition Additives – Natural antibiotics, nutritional additives, and anti-fungal agents. d) Cosmetics & Pharma (CosPha) Additives – Emollients, emulsifiers, green surfactants. e) Coatings & Specialty Additives – Wetting agents, dispersants, anti-corrosive additives, emulsifiers.

Each category represents not just products but entire ecosystems of knowledge, relationships, and technical expertise built over decades. Take polymer additives, Fine's largest segment. A slip additive might constitute just 0.1% of a plastic film's weight, but without it, the film would stick to itself, jam packaging equipment, and become unusable. Fine doesn't just sell these additives—they solve coefficient of friction problems, optimize migration rates to surfaces, and ensure compatibility with hundreds of different polymer formulations.

The business model is deceptively simple yet incredibly difficult to replicate. Fine takes vegetable oils—palm, soybean, castor, rapeseed—and through proprietary chemical processes, transforms them into hundreds of specialized additives. The raw materials might cost $1,000 per ton, but the finished additives sell for $3,000 to $10,000 per ton, sometimes more for highly specialized grades. This isn't commodity processing—it's molecular engineering.

What makes Fine's approach unique is the depth of application knowledge. Consider their anti-fog additives for greenhouse films. The challenge isn't just preventing water condensation—it's doing so while maintaining optical clarity, not affecting the film's UV transmission properties, ensuring long-term stability under sun exposure, and being food-safe since crops grow beneath these films. Fine's solution works not because they're better chemists—many companies can synthesize similar molecules—but because they understand the entire system: the film extrusion process, the greenhouse environment, the crop requirements, and the farmer's economics.

The food additives business illustrates another dimension of Fine's model. An emulsifier for ice cream must prevent ice crystal formation during storage, maintain texture through multiple freeze-thaw cycles, not affect taste, meet food safety regulations across different countries, and remain stable for the product's entire shelf life. Fine doesn't develop these products in isolation—they work with ice cream manufacturers, understanding their production processes, supply chain constraints, and consumer preferences. When a customer wants to launch a low-fat ice cream that tastes like full-fat, Fine's scientists might spend months developing a custom emulsifier blend.

The switching costs embedded in this model are extraordinary. Once a food company approves Fine's emulsifier for a product, changing suppliers means reformulating the product, conducting new stability tests, resubmitting regulatory approvals, risking production disruptions, and potentially affecting product taste or texture that consumers have come to expect. A customer once told Fine's management that switching additive suppliers would be like "performing heart surgery on a healthy patient"—technically possible but unnecessarily risky.

The cosmetics and pharma additives business showcases Fine's ability to meet the highest purity and safety standards. A single contamination incident could destroy years of reputation building. Fine's CosPha-grade facilities maintain pharmaceutical-level cleanliness, with separate production lines, dedicated quality control, and extensive documentation. The margins are higher here—sometimes 40-50%—but so are the technical and regulatory requirements.

Fine's approach to product development follows a clear philosophy: start with the customer's problem, not with the chemistry. When a paint manufacturer struggled with pigment dispersion in water-based formulations, Fine didn't just offer existing dispersants. They studied the specific pigments being used, understood the manufacturing process, analyzed why current solutions failed, and developed a novel dispersant that solved not just the dispersion problem but also improved color stability and reduced formulation costs.

The feed nutrition additives segment represents Fine's expansion into adjacent markets. As antibiotics face regulatory restrictions in animal feed, Fine's natural, plant-based alternatives have found growing demand. These aren't just chemical substitutes—they're biological solutions that require understanding animal nutrition, gut microbiome dynamics, and farm economics. A poultry feed additive must improve feed conversion ratios, reduce mortality, meet safety standards, and provide economic returns that justify its cost to farmers operating on thin margins.

The business model's resilience comes from diversification across multiple dimensions. No single product accounts for more than 5% of revenues. No single customer exceeds 10%. End markets span from everyday consumer products to specialized industrial applications. This diversification isn't accidental—it's a deliberate strategy to reduce dependence while leveraging core oleochemical expertise across multiple opportunities.

Pricing in specialty additives follows value, not cost. If Fine's slip additive allows a packaging film manufacturer to run production lines 20% faster with 50% fewer rejections, the value creation far exceeds the additive's cost. Fine prices to capture a fair share of this value creation, not simply marking up from raw material costs. This value pricing requires deep understanding of customer economics and the confidence that comes from knowing your product's true impact.

The innovation pipeline stays full through a portfolio approach. At any time, Fine has products in different stages: basic research on new molecules, application development for existing products in new markets, customization projects for specific customers, and continuous improvement of established products. This portfolio approach ensures steady launches while managing technical risk. Not every project succeeds, but the winners more than compensate for failures.

Geographic arbitrage plays a subtle but important role. Fine develops products for demanding European or American customers with strict regulatory requirements, then adapts these for emerging markets. A food emulsifier meeting EU standards can command premium prices in Southeast Asia. Conversely, solutions developed for challenging emerging market conditions—high humidity, temperature extremes, variable raw material quality—often find applications in developed markets seeking robust, cost-effective alternatives.

The capital efficiency of the model deserves emphasis. Unlike bulk chemicals requiring massive plants for economies of scale, Fine's additives can be profitable at relatively small volumes. A product selling 500 tons annually at $5,000 per ton generates $2.5 million in revenue—enough to justify dedicated equipment and technical support. This allows Fine to serve niche markets that larger competitors ignore as too small.

Quality control in additives is particularly challenging because problems might not appear immediately. A slip additive that seems perfect might cause issues months later when packages are stacked in warehouses. Fine's quality systems therefore go beyond testing final products—they monitor raw materials, process parameters, and even storage conditions. Each batch comes with a certificate of analysis, but behind that certificate lies extensive testing that customers never see but absolutely depend upon.

The technical service component of the business model is often undervalued by financial analysts but deeply appreciated by customers. When a problem occurs—and problems always occur in chemical processing—Fine's technical team responds immediately. They might fly to a customer's plant, work through nights to diagnose issues, and develop solutions on-site. This service creates relationships that transcend commercial transactions. A purchasing manager once remarked that Fine's competitors offered products; Fine offered partnership.

Sustainability increasingly drives product development. Fine's plant-based additives align with consumer demands for natural ingredients and corporate commitments to reduce petroleum dependence. But this isn't greenwashing—it's fundamental to the business model. Oleochemical additives often perform better than petroleum-based alternatives because nature has optimized these molecules over millions of years. A fatty acid-based lubricant provides superior slip because that's exactly what these molecules do in biological systems.

The learning curve advantages compound over time. Each customer interaction, each problem solved, each application developed adds to Fine's institutional knowledge. A solution developed for one customer often, with modifications, serves others. This knowledge accumulation creates an ever-widening moat. Competitors can copy products but cannot replicate decades of application expertise embedded in thousands of customer relationships.

VIII. Financial Performance & Unit Economics

The numbers tell a story that most specialty chemical companies can only dream of. Company is almost debt free. Company has a good return on equity (ROE) track record: 3 Years ROE 27.1%. But these headline metrics only scratch the surface of Fine Organic's financial architecture—a carefully constructed model that generates cash like a machine while requiring minimal capital reinvestment.

Revenue growth trajectory from startup to ₹2,200+ Cr reveals not just scale but strategic evolution. In the early 2000s, Fine's revenues were primarily domestic, concentrated in a few product categories, with significant customer concentration. Today's ₹2,205 Cr revenue streams from 450+ products sold to thousands of customers across 80+ countries represent a complete transformation in business quality. Each incremental crore of revenue now comes with lower risk and higher margins than the previous one.

The margin profile tells the real story of Fine's competitive advantages. EBITDA margins consistently above 20%—sometimes touching 25%—in a business with 60%+ raw material costs seem almost impossible. Yet Fine achieves this through a combination of value pricing, operational efficiency, and product mix optimization. When palm oil prices spike, as they did in 2017 when the government increased import duties from 15% to 30%, Fine doesn't just absorb the cost—they pass it through with a lag, maintaining absolute EBITDA per ton even if percentage margins compress temporarily.

Working capital management in specialty chemicals typically ties up significant capital—customers demand credit terms, inventory must be maintained for quick delivery, and raw materials need advance procurement. Fine has turned this challenge into an advantage. Their cash conversion cycle—the time between paying suppliers and collecting from customers—is among the best in the industry. This isn't achieved through aggressive collection or delayed payments but through operational excellence: faster production cycles, better demand forecasting, and the leverage that comes from being a critical supplier.

The capital allocation decisions reveal management's long-term thinking. Despite being debt-free with strong cash generation, Fine doesn't chase growth at any cost. Capacity expansions are phased, matching market demand rather than building ahead. New product development follows a portfolio approach—multiple small bets rather than single large gambles. The discipline extends to acquisitions—or rather, the lack thereof. While competitors have grown through M&A, Fine has grown organically, avoiding integration risks and culture dilution.

The company maintains strong management efficiency with a 24.59% return on equity and a zero debt-to-equity ratio, metrics that place it in the top quartile of global specialty chemical companies. But what makes these returns remarkable is their consistency. Through raw material volatility, economic cycles, and competitive pressures, Fine has maintained ROE above 20% for years. This isn't luck—it's the result of a business model with multiple defensive layers.

The unit economics of individual products reveal why the overall model works so well. Take a typical slip additive selling for ₹300 per kilogram. Raw materials might cost ₹100, direct processing costs another ₹50, leaving ₹150 in gross profit. But the real leverage comes from the fact that fixed costs—R&D, technical service, quality control—are largely independent of volume. Once a product reaches minimum efficient scale, incremental volumes drop almost entirely to the bottom line.

Asset utilization metrics show how Fine extracts maximum value from invested capital. Their plants run at 70-80% capacity utilization—high enough for efficiency but with room for growth without major capex. Equipment is standardized where possible, allowing flexibility to switch between products based on demand. This operational flexibility means Fine can optimize product mix for profitability rather than being locked into specific products due to dedicated assets.

The R&D spending pattern—consistently 2-3% of revenues—might seem modest compared to pharmaceutical companies but is significant for specialty chemicals. More importantly, the return on this R&D investment is exceptional. New products typically achieve payback within 2-3 years and then generate returns for decades. The cumulative effect of decades of R&D investment creates an innovation dividend that competitors cannot quickly replicate.

Customer economics drive Fine's financial performance. A typical customer might buy ₹50 lakh of additives annually—tiny compared to their overall raw material spending but critical for product performance. For Fine, this customer represents high-margin, sticky revenue with minimal service costs after initial technical support. The beauty is that as customers grow, Fine grows with them without additional customer acquisition costs.

Geographic revenue distribution provides natural hedging. Export revenues of 55-68% protect against Indian economic cycles. Within exports, exposure is diversified across developed and emerging markets, each with different growth drivers and risk profiles. Currency fluctuations, rather than being a risk, often provide opportunities—when the rupee weakens, Fine's exports become more competitive while domestic input costs remain stable.

The cash flow characteristics deserve special attention. ROE · 23.8 % ROCE · 31.3 % with minimal capital intensity means Fine generates significant free cash flow. Unlike asset-heavy businesses where growth requires proportional capex, Fine can grow revenues 15-20% with capex of just 5-7% of revenues. This cash generation funds R&D, provides buffer for raw material volatility, and still leaves plenty for dividends—though the company maintains a conservative payout policy, preferring to retain capital for growth opportunities.

Inventory management showcases operational sophistication. Raw materials are procured based on price outlooks and forward contracts with customers. Finished goods inventory is minimized through better demand planning and quick production cycles. The result is inventory turns that have steadily improved even as product variety has increased—a remarkable achievement in a business with 450+ products.

The accounting quality adds credibility to reported numbers. Conservative depreciation policies, immediate expensing of R&D, and transparent segment reporting give confidence that reported profits reflect economic reality. The company has never had to restate financials or face accounting scrutiny—boring but important in a market where creative accounting isn't uncommon.

Competitive benchmarking reveals Fine's financial superiority. Fine Organic is the largest manufacturer of oleochemical-based niche additives in India. It is among the six largest global players in polymer additives and leading global players in specialty food emulsifiers. More importantly, Fine achieves better returns than these larger competitors despite smaller scale, proving that focus and execution matter more than size in specialty chemicals.

The financial resilience was tested during COVID-19 and emerged stronger. While many chemical companies struggled with demand destruction and supply chain disruption, Fine's diversified portfolio meant that weakness in some segments (cosmetics, automotive) was offset by strength in others (food, packaging). The debt-free balance sheet meant no financial stress even during the worst periods.

Looking at the trajectory from ₹100 crore revenues in 2000 to ₹2,200+ crore today, with margins and returns improving rather than deteriorating, suggests this isn't a business approaching maturity but one still in its growth phase. The financial foundation—strong cash generation, minimal capital requirements, and diverse revenue streams—provides the platform for continued expansion without diluting returns.

The ultimate test of any business model is its ability to generate economic value above the cost of capital consistently. Fine doesn't just pass this test—it exceeds it by a wide margin. With returns on capital employed consistently above 30% against a cost of capital likely below 12%, Fine creates substantial economic value with every rupee invested. This value creation, compounded over decades, explains how a small partnership founded in 1970 became a ₹15,000+ crore market cap company—and suggests the journey is far from over.

IX. Competition, Market Position & Moats

In the global specialty additives arena, Fine Organic faces competitors with century-old histories, billion-dollar R&D budgets, and operations spanning continents. BASF, Clariant, Croda, Evonik—these names dominate chemical industry conferences and command respect from customers worldwide. Yet in specific niches, particularly in emerging markets, Fine not only competes but often wins against these giants. Understanding how requires examining not just what Fine does but what it chooses not to do.

As per CRISIL Research Report, it is the largest manufacturer of oleochemical-based additives in India and a strong player globally in this industry. This position wasn't achieved through scale or spending but through strategic focus. While competitors spread resources across thousands of products and dozens of technologies, Fine concentrated on oleochemical additives—building depth rather than breadth, expertise rather than exposure.

The global competitive landscape in specialty additives is surprisingly fragmented despite the presence of large players. Even BASF, with its massive chemical portfolio, has limited presence in specific oleochemical additives where Fine excels. This fragmentation exists because specialty additives aren't one market but thousands of micro-markets, each with unique technical requirements, regulatory frameworks, and customer relationships. Fine's strategy has been to dominate specific micro-markets rather than having token presence across many.

Entry barriers in specialty chemicals are often misunderstood. It's not about capital—building an additives plant might cost ₹50-100 crore, affordable for many companies. The real barriers are invisible but nearly insurmountable. First is technical know-how: understanding not just how to make products but how to make them consistently at quality levels measured in parts per million. Second is customer approval cycles: 3-5 years for food and pharmaceutical applications, during which switching incumbents requires extraordinary justification.

The R&D advantage compounds over time in ways that aren't immediately obvious. When a customer approaches Fine with a problem, they bring not just current expertise but accumulated knowledge from thousands of similar challenges solved over decades. A competitor starting fresh might eventually develop similar capabilities, but by then Fine has moved further ahead. It's like trying to catch a moving train that keeps accelerating.

Distribution networks represent another underappreciated moat. Fine's 180+ distributors across 80+ countries aren't just logistics partners—they're technical resources, market intelligence gatherers, and relationship managers. Building this network took decades. A competitor entering these markets must either build their own network—expensive and time-consuming—or convince Fine's distributors to switch—unlikely given established relationships and Fine's track record of support.

The customer approval moat deserves deeper examination. When a food company approves Fine's emulsifier for a product sold globally, that approval encompasses regulatory compliance across dozens of countries, stability testing under various conditions, production line optimization, and consumer acceptance testing. The cost might reach millions of dollars. Switching to save a few percentage points on additive costs makes no economic sense. This creates switching costs that economists call "economic moats"—sustainable competitive advantages that protect profitability.

Regional competition presents different challenges. In India, companies like Galaxy Surfactants and Rossari Biotech compete in some overlapping segments. In China, local manufacturers offer lower prices. In Europe, specialty players focus on premium applications. Fine's response isn't to compete everywhere but to choose battles carefully—premium segments in India, technical applications in China, sustainable solutions in Europe. This selective competition maximizes returns while minimizing direct confrontation.

The innovation race in specialty chemicals isn't about breakthrough discoveries but incremental improvements that collectively create insurmountable advantages. Fine's latest slip additive might be only 5% better than the previous generation—slightly lower dosage, marginally better thermal stability. But these small improvements, compounded over hundreds of products and decades of development, create performance gaps that competitors struggle to close.

Vertical integration strategies differ markedly among competitors. Some, like major oleochemical producers, backward integrate into palm plantations. Others forward integrate into formulated products. Fine deliberately avoids both extremes, maintaining focus on the additives sweet spot where technical value addition is highest. This focus prevents capital dilution while maintaining strategic flexibility.

The green chemistry trend has reshuffled competitive dynamics. Fine's plant-based additives, once seen as niche products for environmentally conscious customers, now represent mainstream solutions as regulations tighten globally. Petroleum-based competitors face the choice of expensive reformulation or ceding market share. Fine's five-decade investment in oleochemistry suddenly looks prescient rather than limiting.

Price competition exists but rarely determines outcomes in Fine's chosen segments. When a slip additive represents 0.1% of a plastic film's cost but determines whether production runs smoothly, customers focus on reliability over price. Fine has walked away from commoditized segments where price is the primary factor, maintaining margins by staying where technical value matters most.

Manufacturing scale provides advantages but also limitations. Large competitors often have minimum order quantities that make serving smaller customers uneconomical. Fine's flexible manufacturing allows them to serve customers needing 100 kg or 100 tons with equal efficiency. This flexibility opens markets that larger competitors ignore as too small but which collectively represent significant opportunities.

The patent landscape in specialty additives is complex but generally favors incremental innovators like Fine over breakthrough seekers. Most valuable IP lies not in composition patents but in application knowledge, process expertise, and formulation know-how—areas where Fine's decades of experience provide sustainable advantages that patents alone cannot protect.

Technology disruption risks exist but are manageable. Could bio-engineered alternatives replace oleochemical additives? Possibly, but the development timeline is decades, not years. Could digital technologies revolutionize additive development? Perhaps, but chemistry still requires wet lab validation. Fine's response is selective adoption—using technology to enhance rather than replace core capabilities.

Acquisition strategies among competitors reveal different philosophies. Western companies often grow through acquisition, paying premiums for market access or technology. Chinese companies might acquire for raw material security or geographic expansion. Fine has largely avoided acquisitions, preferring organic growth that preserves culture and avoids integration risks. This patience has prevented expensive mistakes that have plagued aggressive acquirers.

The competitive dynamics in emerging markets favor local knowledge and relationships—areas where Fine excels. A multinational might offer technically superior products, but Fine understands local manufacturing conditions, regulatory nuances, and business practices. This tacit knowledge, impossible to acquire quickly, provides sustainable advantages in markets that will drive future growth.

Customer concentration and bargaining power vary significantly across segments. In food additives, a few large customers might account for significant volumes, theoretically increasing bargaining power. But when those customers have spent years optimizing formulations around Fine's additives, the practical bargaining power diminishes. The relationship becomes collaborative rather than transactional.

New entrant threats are constant but manageable. Every year, new companies enter specialty chemicals, attracted by high margins and growth potential. Most fail to achieve scale, unable to match incumbents' technical capabilities and customer relationships. Those that survive typically find niches that don't directly compete with established players, actually expanding the market rather than stealing share.

The competitive moat isn't one barrier but multiple reinforcing advantages. Technical expertise enables customer relationships, which generate cash flows, funding R&D, which deepens technical expertise—a virtuous cycle that strengthens over time. Competitors might replicate individual elements but struggle to recreate the entire system.

Looking forward, competition will likely intensify in some areas while diminishing in others. Commoditized additives will face price pressure from Chinese and Indian manufacturers. Premium applications will see innovation-based competition from Western companies. But in the middle market—technically sophisticated but cost-conscious—Fine's combination of expertise, efficiency, and relationships provides sustainable competitive advantages.

The ultimate competitive advantage might be cultural: Fine thinks in decades while many competitors focus on quarters. This long-term orientation enables patient investment in capabilities, relationships, and markets that don't provide immediate returns but create lasting competitive advantages. In specialty chemicals, where customer relationships span decades and technical expertise accumulates over generations, this patient approach might be the most powerful moat of all.

X. Growth Strategy & Future Roadmap

The blueprint spread across the conference table in Fine's strategy room tells a story of ambitious but calculated expansion. Capacity expansion plans show new facilities in strategic locations—not just in India but potentially in key export markets. Product development pipelines indicate moves into adjacent chemistries. Market development strategies target new geographies and applications. But unlike the scatter-shot diversification that plagues many successful companies, Fine's growth strategy maintains laser focus on leveraging core oleochemical expertise.

Capacity expansion follows demand rather than hope. The company has announced phased capacity additions, with new plants coming online as utilization rates approach optimal levels. This disciplined approach avoids the boom-bust cycles that plague chemical companies that build ahead of demand. Each new facility incorporates lessons from previous plants—better automation where it matters, flexibility for product mix optimization, and environmental systems that exceed current requirements anticipating future regulations.

The new product development pipeline reveals strategic thinking about market evolution. Bio-based alternatives to petroleum additives represent obvious opportunities as sustainability pressures intensify. But Fine is also developing additives for emerging applications—biodegradable plastics that need different slip properties, plant-based meat alternatives requiring novel emulsifiers, electric vehicle components demanding high-temperature stability. These aren't random bets but calculated moves into markets where Fine's capabilities provide competitive advantages.

Geographic expansion opportunities exist in both developed and emerging markets, but for different reasons. In developed markets, increasingly stringent environmental regulations favor Fine's plant-based additives. In emerging markets, rising consumer spending drives demand for packaged foods, cosmetics, and consumer goods—all requiring additives. The strategy differs by region: technical superiority in developed markets, cost-effective reliability in emerging ones.

Adjacent market opportunities beckon, but Fine approaches them cautiously. Pharmaceutical excipients share similarities with food additives but require different regulatory expertise. Agricultural chemicals could leverage oleochemical knowledge but involve different customer dynamics. Fine's approach is to enter adjacencies through partnerships or joint ventures first, learning the market before committing significant capital.

The green chemistry tailwind isn't just about regulatory compliance—it's about reimagining what additives can be. Fine's R&D teams are working on additives that don't just match petroleum-based alternatives but exceed them. Bio-based slip additives that actually perform better at high temperatures. Food emulsifiers that extend shelf life while improving nutritional profiles. These aren't green-washing exercises but fundamental innovations that happen to be sustainable.

Management succession represents both challenge and opportunity. The second generation—Mukesh Shah, Jayen Shah, Tushar Shah—brings different perspectives while respecting institutional knowledge. They're more comfortable with technology, more globally oriented, yet understand that Fine's success comes from patient building of capabilities rather than financial engineering. This balance between fresh thinking and proven principles positions Fine well for its next growth phase.

Digital transformation in specialty chemicals isn't about replacing chemists with algorithms but augmenting human expertise with data-driven insights. Fine is investing in systems that can predict how additives will perform in new applications, optimize production schedules across multiple plants, and identify quality issues before they affect customers. But technology remains a tool, not a strategy—the focus stays on solving customer problems.

The sustainability agenda goes beyond products to encompass operations. New plants are designed for minimal environmental impact—zero liquid discharge, renewable energy where feasible, and circular economy principles. This isn't just corporate responsibility—it's strategic positioning for a world where environmental performance affects customer choice and regulatory approval.

Partnership strategies are evolving from transactional to transformational. The Zeelandia joint venture showed how partnerships can accelerate capability building. Future partnerships might involve technology companies for digital capabilities, biotechnology firms for next-generation additives, or regional players for market access. But each partnership must enhance rather than dilute Fine's core strengths.

The innovation ecosystem Fine is building extends beyond internal R&D. Collaborations with ICT and other technical institutions ensure access to cutting-edge research. Partnerships with customers create co-development opportunities. Relationships with raw material suppliers enable early access to new oleochemical derivatives. This ecosystem approach multiplies innovation capacity without proportional cost increase.

Market development strategies recognize that creating demand is sometimes more valuable than capturing existing demand. Fine's technical teams work with customers to identify applications where additives aren't currently used but could provide value. A packaging company might not realize that anti-static additives could solve dust accumulation problems. A food manufacturer might not know that emulsifiers could enable new product formats. This evangelical approach expands the addressable market.

The acquisition strategy, or deliberate lack thereof, reflects confidence in organic growth. While competitors pursue expensive acquisitions, Fine invests in internal capabilities. This doesn't preclude acquisitions entirely—the right technology or market access opportunity at reasonable valuations would be considered. But growth through acquisition remains option, not necessity.

Regulatory expertise becomes increasingly valuable as requirements proliferate globally. Fine is building capabilities not just to comply with current regulations but to anticipate future ones. This forward-looking approach means products developed today will still be saleable years hence when regulations catch up. It also positions Fine as a partner for customers navigating regulatory complexity.

The talent strategy recognizes that sustainable growth requires human capital. Beyond recruiting from ICT and other premier institutions, Fine is investing in continuous learning programs, international exposure for high-potential employees, and retention mechanisms including equity participation. The goal is building an organization capable of managing complexity while maintaining entrepreneurial agility.

Financial flexibility preserved through conservative balance sheet management provides options for growth acceleration when opportunities arise. The debt-free status means Fine can move quickly on expansion projects, fund extended R&D programs, or weather temporary market disruptions without financial stress. This flexibility is particularly valuable in the chemical industry's cyclical environment.