Federal Bank: The Kerala Powerhouse That Built India's Remittance Highway

I. Introduction & Episode Framework

Picture this: A small bank in Kerala, tucked away in India's southwestern coast, quietly processes nearly one out of every five rupees that overseas Indians send back home. Not HDFC with its towering presence, not ICICI with its tech prowess, but Federal Bank—a name most Indians outside Kerala might struggle to place. Yet this institution handles 19.3% of India's total NRI remittances, a staggering ₹1.5 lakh crore annually flowing through its systems like digital monsoons feeding the subcontinent's economy.

The story of Federal Bank reads like a paradox wrapped in an enigma. How does a bank that began in 1931 with just ₹5,000 in capital—roughly the price of a decent smartphone today—evolve into a ₹48,000+ crore market cap institution? How does a regional player from India's smallest major state become the undisputed king of cross-border remittances, beating giants ten times its size?

This isn't just another bank that grew big. This is a masterclass in finding your niche and owning it so completely that competitors don't even try to dislodge you. It's about understanding diaspora psychology better than anyone else, about building trust networks that span continents, and about transforming from a village lender to a digital pioneer without losing your soul.

Federal Bank's journey spans India's entire modern history—from British colonial rule through independence, the License Raj, liberalization, and into the digital age. It's witnessed princely states dissolve into democratic republics, watched millions of Keralites board flights to the Gulf, and surfed every wave of banking regulation the RBI could throw at it. Through it all, the bank didn't just survive; it found ways to thrive by zigging when others zagged.

What makes this story particularly fascinating for students of business strategy is how Federal Bank repeatedly turned apparent weaknesses into competitive moats. Too small to compete nationally? Dominate your region so thoroughly that you become irreplaceable. Can't match the marketing budgets of private bank giants? Build relationships so deep that marketing becomes redundant. Technology infrastructure lagging? Leapfrog everyone with strategic digital bets that actually work.

The modern Federal Bank stands as India's sixth-largest private sector bank, punching far above its weight in profitability and efficiency metrics. Its digital transformation story—from being one of the last banks to computerize to becoming the first to digitalize all branches—offers lessons for any traditional institution grappling with technological disruption. The bank processes 86% of its transactions digitally today, a remarkable achievement for an institution whose average customer still remembers when passbooks were handwritten.

But perhaps the most intriguing aspect is how Federal Bank maintains dual identities without contradiction. It's simultaneously hyperlocal and international, traditional and cutting-edge, relationship-driven and algorithm-powered. In an era when banks either go fully digital or double down on branches, Federal Bank chose both—and made it work through what they call "Digital at the Fore, Human at the Core."

As we dive into this epic spanning nine decades, we'll uncover how a lawyer named K.P. Hormis transformed a failing village bank into a financial institution, how Kerala's unique social dynamics created perfect conditions for banking innovation, and how understanding migration patterns better than demographers helped build an unassailable competitive position. We'll explore acquisition strategies executed when computers were the size of rooms, digital transformations that actually delivered ROI, and strategic pivots that anticipated market shifts by decades.

This is the story of how Federal Bank built India's remittance highway—one relationship, one innovation, one calculated risk at a time.

II. The Pre-Independence Origins & Kerala's Banking Culture

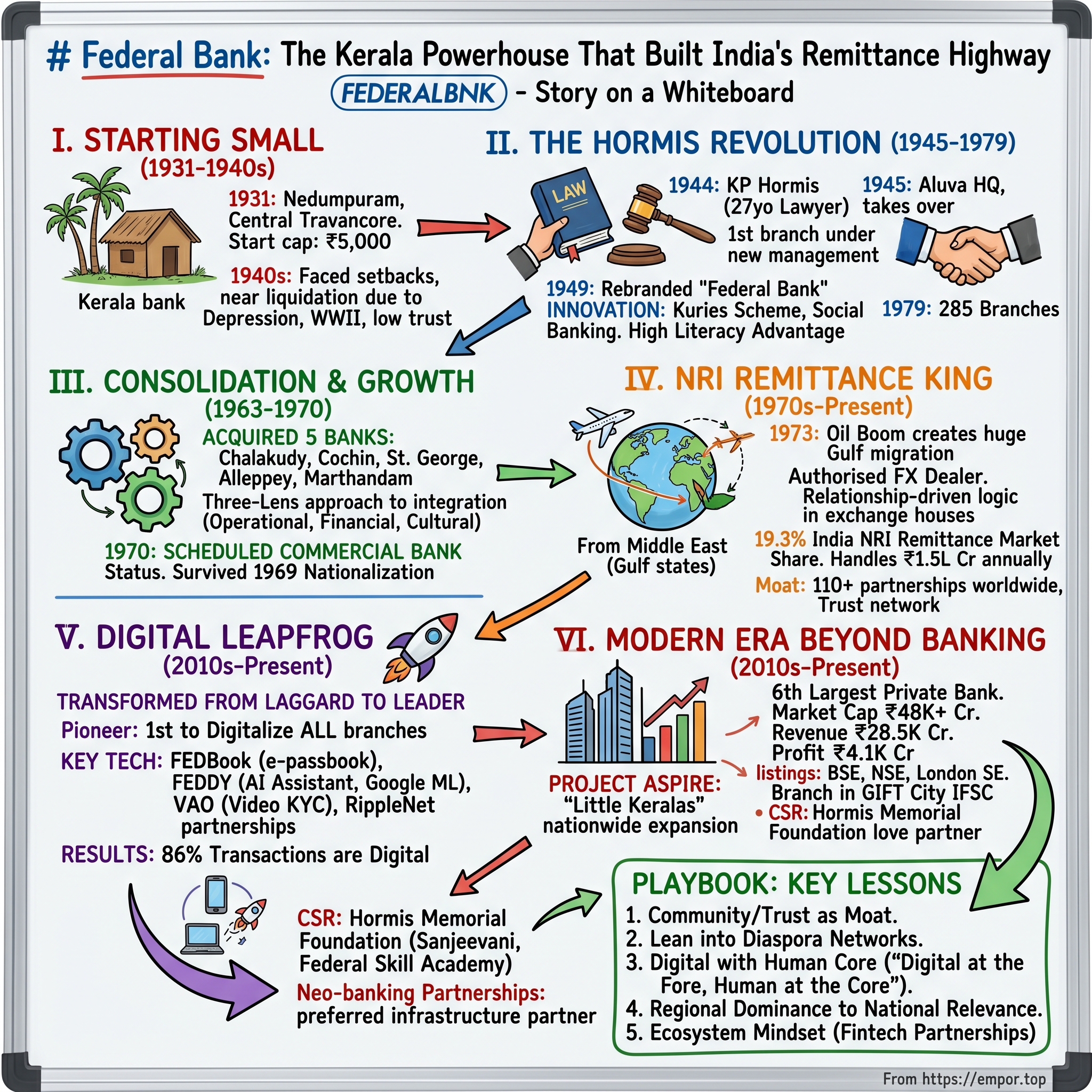

The summer of 1931 brought more than just monsoons to the princely state of Travancore. On April 23rd, in the small town of Nedumpuram, a group of local merchants and landowners gathered to sign the incorporation documents for what they ambitiously called the Travancore Federal Bank Limited. The initial capital: ₹5,000. The grand vision: to serve the financial needs of their immediate community. None of them could have imagined they were laying the foundation for what would become India's remittance superhighway.

Travancore in the 1930s was a world unto itself—a princely state under the Maharaja's rule but effectively controlled by British advisors, an economy built on spices and coir, a society stratified by caste but surprisingly progressive in education. The state boasted India's highest literacy rates, a detail that would prove crucial to the bank's later success. While the rest of India struggled with literacy rates below 10%, Travancore pushed past 40%, creating a population uniquely equipped to engage with formal banking.

The banking ecosystem in Kerala was unlike anywhere else in India. Where northern India had zamindari banking serving large landowners, and Bombay had merchant banking funding trade, Kerala developed what could only be called "community solidarity banking." The Syrian Christian community, to which many of the bank's founders belonged, had a centuries-old tradition of collective financial support—informal lending circles, community treasuries for emergencies, and rotating credit associations that predated modern microfinance by generations. The bank's founding documents, written in Malayalam and preserved in yellowing ledgers, reveal the modest ambitions of its creators. The Federal Bank Limited (the erstwhile Travancore Federal Bank Limited) was incorporated with an authorised capital of ₹5,000 at Nedumpuram, a place near Thiruvalla in Central Travancore on 23 April 1931 under the Travancore Companies Act. They wanted to provide "banking facilities to the agricultural and industrial classes"—noble goals, but hardly the makings of a future remittance giant.

But here's where the story takes its first unexpected turn. The bank though successful in the earlier periods, suffered set backs and was on the verge of liquidation. By the early 1940s, this experiment in community banking was failing. Deposits were drying up, loans were going bad, and the directors were contemplating closure. The Travancore Federal Bank seemed destined to join the long list of forgotten financial institutions that couldn't survive India's tumultuous pre-independence era.

The factors behind this near-death experience were multiple and interconnected. The global depression of the 1930s had devastated commodity prices, particularly rubber and spices that formed the backbone of Travancore's economy. World War II created further disruptions—shipping lanes were blocked, export markets vanished, and the colonial administration imposed wartime controls that strangled credit flow. The bank's original promoters, mostly small merchants and landowners, lacked both the capital to weather the storm and the expertise to navigate complex financial headwinds. Yet Kerala's banking culture proved remarkably resilient. Banking was one of the most preferred lines of business in the princely states of Travancore and Cochin, and the Malabar Province of British India — the area that later became the state of Kerala — during the twentieth century. This wasn't just about making money; it was about social mobility in a rigidly stratified society. For Syrian Christians, Nairs, and emerging merchant communities, establishing a bank meant staking a claim to economic and social relevance in a changing world.

The collapse of numerous banks in the late 1930s should have killed Federal Bank before it could truly begin. Several banks had collapsed in the late 1930's in Travancore, undermining public confidence in the banking system. The Quilon Bank had failed in 1937, merged and then liquidated. The economic pressures were mounting—It was also the time when the Princely State was waking up to industrialisation. This created a paradox: just as capital was most needed for industrial development, the banking system was losing public trust.

What made Federal Bank different from the dozens of other small banks that failed during this period? The answer lies partly in timing and partly in the unique social dynamics of central Travancore. The bank's location in Nedumpuram, near Thiruvalla, placed it at the heart of Kerala's Syrian Christian belt—a community with deep trading traditions, high literacy rates, and crucially, extensive family networks that would later span continents. These weren't just depositors; they were stakeholders in a community institution.

The pre-1945 Federal Bank also benefited from what economists would later call "social capital." In a society where formal contracts were difficult to enforce and legal systems were inconsistent across princely and British territories, trust became the ultimate currency. The bank's early lending practices—largely to local farmers and small traders known personally to the directors—might seem primitive by modern standards, but they created a web of mutual obligation that proved more durable than formal collateral.

Yet by 1944, even these advantages weren't enough. The bank's capital had dwindled, several large loans had gone bad, and younger members of the founding families were reluctant to throw good money after bad. The directors were discussing liquidation, preparing to join the long list of failed Kerala banks. The Travancore Federal Bank Limited seemed destined for a footnote in banking history—another well-intentioned experiment that couldn't survive the harsh realities of colonial economics.

That's when a 27-year-old lawyer from Mookkannoor made a decision that would alter the trajectory of not just one bank, but the entire Indian remittance ecosystem. K.P. Hormis was about to enter the picture, and nothing would ever be the same.

III. The K.P. Hormis Revolution (1945-1979)

The morning of March 15, 1944, found Kulangara Paulo Hormis sitting in the cramped quarters of the Munisiff Court in Perumbavoor, methodically working through a stack of property dispute cases. At 27, he had built a respectable legal practice, the kind that provided steady income and social standing in pre-independence Kerala. By noon, he had made a decision that his family thought was insane: he would quit law to save a failing bank.

In 1944 it was taken over by Shri KP Hormis, a 28 year old lawyer, and in 1949, its name was changed to Federal Bank. But this clinical sentence barely captures the audacity of what Hormis attempted. Born on October 18, 1917, in the village of Mookkannoor, Hormis came from a family of modest means but considerable ambition. His legal training had given him something more valuable than courtroom skills—an understanding of how contracts worked, how disputes arose, and crucially, how trust could be institutionalized.

The acquisition itself was a masterclass in financial engineering before the term existed. Hormis didn't have significant capital of his own. Instead, he convinced a group of relatives and close friends to pool resources, leveraging personal relationships to raise enough to buy controlling stakes from dispirited shareholders who were eager to exit. The share capital was increased from ₹5,000 to ₹71,000—still tiny by any standard, but enough to signal serious intent.

His first acts as the controlling force were both symbolic and strategic. On May 18, 1945, he relocated the bank's headquarters from the sleepy village of Nedumpuram to Aluva, a bustling commercial town at the intersection of major trade routes. Aluva wasn't just geographically strategic; it was where the modern Kerala economy was being born, where roads, railways, and rivers converged. The same day, the bank opened its first branch under new management—a statement that Federal Bank was no longer a village cooperative but an institution with ambitions.

The name change came later but was equally significant. On December 2, 1949, after completing all formalities under the new Banking Regulation Act, the institution officially became Federal Bank Limited. Dropping "Travancore" from the name wasn't just about brevity; it was about vision. Hormis understood that the princely states were history, that modern India would be built on different foundations. A bank named after a defunct kingdom would always be looking backward; Federal Bank could look forward.

But Hormis's true genius lay in his innovation of financial products tailored to Kerala's unique social structure. The most revolutionary was the "Kuries" scheme—a formalized version of the traditional chit funds that had operated informally in Kerala for centuries. The brilliance of Kuries wasn't in its novelty but in its institutionalization. By bringing these rotating credit associations into the formal banking system, Hormis accomplished multiple objectives simultaneously: he provided credit access to farmers and small businessmen who couldn't qualify for traditional loans, created a savings mechanism that resonated culturally, and most importantly, built deep community engagement that went beyond transactional banking.

The Kuries system worked on elegant simplicity. Groups of participants would contribute regular amounts, with the pooled sum going to the highest bidder at a discount—typically 50% for early bidders. This meant a farmer needing ₹1,000 for seeds could access it immediately by accepting ₹500, paying back the full amount over time. For the bank, it meant predictable cash flows, minimal default risk (social pressure ensured repayment), and deep community penetration. For customers, it meant dignity—they weren't beggars seeking loans but participants in a mutual support system.

By the time Shri KP Hormis retired in 1979 (35 years), he had built the bank from a one branch bank to a 285 branch-bank. This expansion wasn't random or opportunistic; it followed a deliberate strategy that would become the Federal Bank playbook. First, dominate your home region completely. Second, follow your community wherever it goes. Third, build trust before you build business.

The numbers tell only part of the story. Each of those 285 branches represented a carefully calculated bet on India's changing geography. When Kerala's educated youth began migrating to Bombay (now Mumbai) in the 1950s for industrial jobs, Federal Bank followed, opening branches in Vile Parle and Bandra before larger banks recognized the opportunity. When the rubber boom created wealth in the high ranges, Federal Bank was there. When the Gulf migration began in the 1970s, Federal Bank had already built the infrastructure to handle remittances.

Hormis's management philosophy was deceptively simple but revolutionary for its time. He believed in what he called "social banking"—the idea that a bank's primary obligation was to its community, with profits being a byproduct of fulfilling that obligation properly. This wasn't corporate social responsibility as a marketing gimmick; this was CSR as core business strategy, decades before the term was coined.

Consider his hiring practices. In an era when banks recruited from elite institutions, Hormis deliberately hired from local communities. The branch manager in Thodupuzha would be from Thodupuzha, would know every family's financial situation, every farmer's cropping pattern, every merchant's business cycle. This hyperlocal knowledge became Federal Bank's greatest asset—while other banks relied on financial statements, Federal Bank relied on relationships.

The cultural transformation Hormis engineered was equally remarkable. Federal Bank became known for two things that seemed contradictory: extreme conservatism in lending and extreme innovation in products. The bank would spend months evaluating a loan application, sending managers to inspect not just collateral but character. Yet it would launch new savings schemes and deposit products at a pace that left competitors scrambling.

This dual personality was intentional. Hormis understood that in banking, trust is built slowly and destroyed instantly. Conservative lending protected the institution's foundation, while product innovation kept it relevant. The bank's NPAs remained below 2% throughout the Hormis era, remarkable for a period that saw numerous banking crises.

The relationship-first approach extended to how the bank dealt with defaults. Rather than immediate legal action, Federal Bank pioneered what would later be called "restructuring." Managers would work with struggling borrowers to find solutions—extended payment periods, converting debt to equity stakes, even helping find buyers for distressed assets. This wasn't softness; it was strategic. A restructured loan that eventually got repaid built more loyalty than ten smooth transactions.

By the late 1970s, Federal Bank had become more than a financial institution in Kerala—it had become part of the social fabric. Families banked with Federal across generations. Opening a Federal Bank account for a newborn was as much a ritual as the naming ceremony. The bank's passbooks became informal identity documents, more trusted than government-issued papers.

Hormis's retirement in 1979 marked the end of an era but not the end of his influence. The culture he built—customer-first, community-centered, conservative yet innovative—would survive and thrive through subsequent decades. The foundation he laid would prove strong enough to support expansions he probably never imagined: international operations, digital transformation, capital market listings.

But perhaps his greatest achievement was recognizing, before anyone else, that Kerala's greatest export wouldn't be spices or rubber or coconut oil—it would be people. And wherever Keralites went, they would need a trusted way to send money home. Hormis didn't just build a bank; he built the first sections of what would become India's remittance highway.

IV. The Acquisition Spree & Consolidation (1963-1970)

The registered letter that arrived at Federal Bank's Aluva headquarters on a humid September morning in 1963 contained an opportunity disguised as a crisis. The Chalakudy Public Bank, with eight branches and deposits of ₹2.3 crores, was on the verge of collapse. The Reserve Bank of India's inspection report was damning—capital adequacy below critical levels, NPAs exceeding 30%, management in disarray. The RBI's message was clear: find a buyer or face liquidation.

For K.P. Hormis, this wasn't a distress sale; it was the opening move in a chess game that would transform Federal Bank from a regional player to a banking powerhouse. Over the next seven years, Federal Bank would execute one of the most ambitious consolidation strategies in Indian banking history, acquiring five banks and integrating their operations in an era when computers were science fiction and integration meant manually reconciling thousands of handwritten ledgers.

The Chalakudy acquisition set the template. Rather than cherry-picking assets, Federal Bank absorbed the entire institution—employees, branches, bad loans, and all. Hormis personally visited each Chalakudy branch, meeting staff and major customers. His message was consistent: "You're not being acquired; you're joining a family." It sounds like corporate PR speak today, but in 1963 Kerala, where bank failures had destroyed countless families' savings, this personal guarantee from Hormis carried weight.

The integration challenges were staggering. Each bank had its own accounting methods, interest calculation systems, and even different ways of writing receipts. Federal Bank deployed teams of senior managers who spent months at acquired branches, not to impose new systems but to understand existing ones. Only after mapping every process did they begin standardization—gradually, gently, with minimal disruption to customers.

The second acquisition came in 1964: Cochin Union Bank, with its prestigious client base of spice traders and shipping companies. This wasn't a distressed sale but a strategic merger. Cochin Union brought something Federal Bank desperately needed—sophisticated corporate banking experience and connections to international trade. The spice traders who banked with Cochin Union weren't just moving local produce; they were part of global supply chains stretching from Kerala's hills to European kitchens.

Integrating Cochin Union required a different approach. These weren't rural farmers grateful for basic banking; these were sophisticated businessmen who could move their accounts to Imperial Bank or Bank of India at the first sign of service deterioration. Federal Bank created its first "specialized banking unit," staffing it with Cochin Union's best relationship managers and giving them autonomy to maintain service standards while gradually aligning backend processes.

The 1965 acquisition of St. George Union Bank marked Federal Bank's entry into what would become its greatest strength: understanding and serving the Syrian Christian diaspora. St. George Union, which operated from 1927–1965 before being amalgamated with Federal Bank, had deep roots in the community's merchant networks. Its loan books read like a directory of families who would, within a decade, establish businesses across India and eventually across the world.

The human dimension of these acquisitions deserves special attention. Federal Bank retained virtually every employee from acquired banks, a decision that seemed financially reckless but proved strategically brilliant. These weren't just employees; they were walking repositories of local knowledge, relationship managers who knew three generations of every family's financial history. In an era before credit bureaus and data analytics, this human intelligence was priceless.

The Alleppey Bank acquisition in 1967 brought Federal Bank into Kerala's coir and cashew industries—sectors that would soon become major export earners. But more importantly, it brought expertise in trade finance and foreign exchange operations. Alleppey Bank had been financing exports since the 1940s, maintaining correspondent relationships with banks in London and Hamburg. This expertise would prove crucial when Federal Bank began its push into NRI banking.

The final and most complex acquisition was Marthandam Commercial Bank in 1968. Marthandom Commercial Bank Ltd operated from 1950–1968 before being amalgamated with Federal Bank. Located in what was then southern Travancore (now Tamil Nadu), Marthandam brought geographic diversity and exposure to different regulatory regimes. It also brought complexity—different state laws, different languages, different business cultures. The integration took three years and required Federal Bank to develop capabilities in multi-state operations that would serve it well in future expansions. The crowning achievement of this consolidation phase came in 1970 when Federal Bank became a Scheduled Commercial Bank. The Bank became a Scheduled Commercial Bank in 1970, which also coincided with the Silver Jubilee Year, since the Bank commenced its operation in Aluva. This wasn't just a regulatory milestone; it was validation that Federal Bank had arrived as a serious player in Indian banking. Scheduled bank status meant access to RBI refinancing facilities, participation in clearing houses, and most importantly, the ability to maintain government accounts—a massive credibility boost.

The timing was perfect. India was about to embark on bank nationalization in 1969, and many wondered if Federal Bank would be swept up. But with deposits just below the ₹50 crore threshold, Federal Bank escaped nationalization by a whisker. This near-miss would prove to be a blessing—Federal Bank retained the agility of a private institution while gaining the stability and reach that came from absorbing five other banks.

The strategic logic behind this acquisition spree was multilayered. First, geographic expansion without the cost of building new branches from scratch. Second, talent acquisition—each absorbed bank brought specialized skills, from trade finance to agricultural lending. Third, customer base consolidation—instead of competing for the same depositors, Federal Bank absorbed the competition. Fourth, and perhaps most importantly, building institutional capability that would be crucial for the next phase of growth.

The risk management lessons from this period shaped Federal Bank's culture permanently. The bank developed what it called the "three-lens approach" to integration: operational (can we merge the systems?), financial (can we absorb the bad loans?), and cultural (can we retain the people?). If any lens showed red flags, the acquisition didn't proceed. This discipline meant Federal Bank walked away from several opportunities, including banks with attractive branch networks but toxic loan books.

The technology challenges of integration in a pre-computer era deserve special mention. Federal Bank pioneered what it called "parallel processing"—maintaining old and new systems simultaneously for six months to ensure no transaction was lost. Armies of clerks worked night shifts, manually reconciling every account, every transaction, every penny. It was expensive and exhausting, but it worked. Not a single customer lost money during any of the integrations, a record that built tremendous trust.

By 1970, Federal Bank had transformed from a single-district rural bank to a multi-state financial institution with over 100 branches, diverse business lines, and deep expertise across retail, agricultural, and corporate banking. But more importantly, it had built the organizational muscle memory for integration and expansion that would serve it well in the decades to come. The acquisition spree wasn't just about getting bigger; it was about getting better, broader, and building the foundation for what would become Federal Bank's greatest competitive advantage—understanding and serving the Indian diaspora.

V. The NRI Remittance Domination Strategy

The year 1973 changed everything. Oil prices quadrupled overnight, sending shockwaves through the global economy. For most of India, it was a crisis—fuel shortages, inflation, economic turmoil. But for Kerala, it was the beginning of an unprecedented transformation. The Gulf states, suddenly flush with petrodollars, needed workers—engineers for their refineries, nurses for their hospitals, laborers for their construction boom. And Kerala, with its educated, English-speaking population, was perfectly positioned to supply them.

Federal Bank's leadership didn't just observe this migration; they saw its implications before anyone else. The Bank became an Authorised Dealer in Foreign Exchange in 1972.International Banking Department started functioning from Mumbai in 1973.Since then, the Bank could substantially increase its market share of the NRI business. The timing was no coincidence. Federal Bank had positioned itself at the departure gates just as the planes started taking off.

Consider the numbers: In 1970, roughly 10,000 Keralites worked in the Gulf. By 1980, it was over 500,000. By 1990, nearly 1.5 million. Each of these migrants needed to send money home—for families, for houses, for investments. The remittance market wasn't just growing; it was exploding exponentially. And Federal Bank was ready with infrastructure, relationships, and most importantly, trust.

The bank's approach to capturing this market was brilliantly simple yet devastatingly effective. Instead of competing on rates or technology (which it couldn't afford), Federal Bank competed on relationships and convenience. When a carpenter from Thrissur landed in Dubai, he found a Federal Bank representative at the exchange house. When his wife in Kerala needed to withdraw money, she could walk to the Federal Bank branch where the manager knew her by name. When it was time to build a house with Gulf savings, Federal Bank's loan officers understood NRI documentation better than anyone else.

With a customer base of over 19 million, and a large network of remittance partners around the world, Federal Bank handles more than one fifth of India's total personal inward remittances, approximately. The bank has remittance arrangements with more than 110 banks and exchange companies around the world. But these partnerships weren't built overnight. Each relationship required years of cultivation, trust-building, and often, creative problem-solving.

Take the example of how Federal Bank cracked the UAE exchange house network. In the early 1980s, exchange houses were dominated by banks from the Indian subcontinent's north and west. Federal Bank's breakthrough came through what managers internally called "the tea shop strategy." Bank representatives would spend hours in the tea shops frequented by Kerala workers, not selling products but solving problems—helping with documentation, explaining exchange rates, even helping write letters home. This grassroots approach built loyalty that no amount of advertising could buy. The formalization of Federal Bank's Gulf presence came much later but was equally strategic. In January 2008, Federal Bank opened its first overseas representative office in Abu Dhabi. In November 2016, Federal Bank opened its second UAE representative office, in Dubai. These weren't branches—regulatory restrictions prevented that—but they served as crucial liaison offices, helping NRIs navigate the complex documentation required for investments back home.

The technology infrastructure Federal Bank built for remittances was revolutionary for its time. In the 1980s, when most banks took weeks to process international transfers, Federal Bank pioneered the use of telex confirmations that reduced transfer time to days. By the 1990s, they were among the first to adopt SWIFT, further cutting transfer times. But the real innovation wasn't in the technology itself—it was in making complex technology simple for users who might be semi-literate construction workers sending their first international transfer.

Federal Bank's remittance products evolved with the changing needs of the diaspora. In the early days, it was simple inward remittances—getting money from Dubai to Kochi. Then came NRE (Non-Resident External) and NRO (Non-Resident Ordinary) accounts, allowing NRIs to maintain rupee accounts that could earn interest. The FCNR (Foreign Currency Non-Resident) deposits came next, letting NRIs hedge currency risk. Each product innovation was a response to a real customer pain point, identified through thousands of conversations in exchange houses and community centers.

The competitive moat Federal Bank built in remittances had multiple layers. First, the physical presence—by the 2000s, Federal Bank had relationships with virtually every major exchange house in the Gulf. Second, the trust factor—generations of families had used Federal Bank for remittances, creating powerful network effects. Third, the knowledge base—Federal Bank understood NRI documentation, regulations, and pain points better than any competitor. Fourth, the Kerala connection—while other banks saw NRIs as a segment, Federal Bank saw them as family.

The numbers tell a staggering story of dominance. Today, with remittance arrangements with more than 110 banks and exchange companies worldwide, Federal Bank processes nearly 20% of India's total inward remittances. To put this in perspective, Federal Bank, with less than 2% of India's banking assets, handles one-fifth of the country's remittance flows. It's as if a regional U.S. bank handled 20% of all dollar transfers globally—an almost impossible level of market concentration.

But this dominance wasn't built on technology or pricing alone. It was built on understanding the psychology of migration. Federal Bank understood that remittances weren't just financial transactions—they were emotional lifelines. The construction worker in Kuwait sending money home wasn't just transferring funds; he was fulfilling family obligations, maintaining social status, building dreams. Federal Bank's marketing reflected this understanding, focusing not on interest rates but on trust, reliability, and the pride of supporting family back home.

The bank also pioneered what would later be called "lifecycle banking" for NRIs. When someone left for the Gulf, Federal Bank helped with foreign exchange for initial expenses. When they started earning, the bank facilitated remittances. When they wanted to invest, Federal Bank offered NRI-specific fixed deposits and investment products. When they wanted to buy property in India, Federal Bank provided home loans with NRI-friendly documentation. When they returned, Federal Bank helped repatriate funds. From departure to return, Federal Bank was present at every step.

The strategic foresight to focus on remittances when other banks were chasing corporate loans or urban retail has paid off spectacularly. Remittances are sticky, recurring, low-risk, and generate steady fee income. They create deep customer relationships that lead to cross-selling opportunities. Most importantly, they're largely immune to Indian economic cycles—when India's economy slows, NRIs often send more money home to support struggling families.

Today, Federal Bank's remittance network spans from the construction sites of Saudi Arabia to the hospitals of London, from the IT corridors of Silicon Valley to the plantations of Malaysia. It's a network built over five decades, relationship by relationship, transfer by transfer. And while fintech companies and global banks now eye this lucrative market, Federal Bank's moat—built on trust, community, and deep understanding of the diaspora psyche—remains formidable. In the remittance game, Federal Bank isn't just a player; it's the house.

VI. Digital Transformation: From Laggard to Leader

The year 2010 found Federal Bank in an uncomfortable position. While the bank dominated remittances and had strong regional presence, its technology infrastructure was embarrassingly outdated. Competitors like HDFC and ICICI had modern core banking systems, internet banking, and mobile apps. Federal Bank still processed many transactions manually. Industry conferences had a running joke: "Federal Bank—where banking meets archaeology." The transformation that followed would be one of the most dramatic digital turnarounds in global banking history.

The catalyst wasn't technology enthusiasm but existential fear. A internal study in 2010 showed that 67% of NRI customers under 35 were considering switching banks due to poor digital services. The children of Federal Bank's core customers—second-generation NRIs raised on smartphones and instant gratification—found their parents' bank impossibly antiquated. Federal Bank faced a stark choice: transform or become irrelevant within a generation.

The transformation began with a bold decision that seemed insane at the time. Instead of gradual modernization, Federal Bank decided to digitalize all branches simultaneously. Pioneer in banking sector by being first bank to digitalize all branches in India—this wasn't marketing hyperbole but a massive operational undertaking. Between 2010 and 2013, Federal Bank upgraded every single branch, trained every employee, and migrated every account to a modern core banking platform. The cost was staggering, the disruption immense, but the alternative was slow death.

But Federal Bank's digital transformation wasn't just about catching up—it was about leapfrogging. The bank made a strategic decision to skip intermediate technologies and jump straight to cutting-edge solutions. Why build traditional internet banking when you could build mobile-first platforms? Why create plastic cards when you could pioneer virtual cards? This approach required more investment upfront but avoided the technical debt that plagued banks with legacy digital systems.

The first breakthrough product was FedBook, launched in 2012. FedBook: First electronic passbook launched by a bank in India might sound mundane today, but it solved a massive pain point. Indians, especially older ones, loved their passbooks—physical proof of their savings, tangible evidence of financial prudence. But maintaining and updating physical passbooks was a nightmare. FedBook digitized this experience while maintaining the familiar passbook interface. Customers could see their transactions in the familiar passbook format on their phones, print them when needed, and most importantly, trust them.

The real digital revolution came with FEDDY, launched in 2017. FEDDY: AI powered Virtual Assistant backed by Google's machine learning algorithms represented Federal Bank's first serious foray into artificial intelligence. But unlike other banks' chatbots that could barely handle balance inquiries, FEDDY was built to handle complex queries. It could process remittance requests, explain NRI tax implications, even help with documentation for property purchases. FEDDY spoke Malayalam, Hindi, and English, understanding context and nuance in ways that surprised even skeptics.

The development of FEDDY revealed Federal Bank's new approach to technology: partner with the best rather than build everything in-house. The bank partnered with Google for AI capabilities, with startups for specific features, with fintechs for payment solutions. This ecosystem approach allowed Federal Bank to move at startup speed while maintaining banking stability.

The COVID-19 pandemic accelerated Federal Bank's digital push in unexpected ways. Within weeks of lockdown, the bank launched VAO: Video-KYC for paperless, contactless account opening. This wasn't just a pandemic response but a solution to a long-standing problem: how to onboard NRI customers who couldn't visit branches. VAO allowed someone in Dubai to open an account in India through a video call, with AI-powered document verification and real-time approval. Account opening time dropped from weeks to minutes. The blockchain revolution at Federal Bank wasn't just about cryptocurrency hype but strategic positioning for the future of remittances. Recognizing a need to enhance the cross-border payments experience in one of the biggest remittance corridors in the world, LuLu Exchange, a leading Abu Dhabi-based financial services provider partnered with leading Indian private sector financial institution Federal Bank. "Disruptive technology innovation is the mantra at Federal Bank & the bank continuously invests in technology, which benefits all our partnerships, including the remittance industry partners. We believe such innovations will benefit the larger Indian diaspora who can enjoy a modern, low cost, fast, easy and more reliable way of transferring money to India," said Nilufer Mullanfiroze, Senior Vice President & Country Head – Deposits, Cards & Unsecured Lending at Federal Bank. Through RippleNet partnerships, Federal Bank reduced cross-border transfer times from days to seconds while cutting costs by up to 60%.

But the real measure of Federal Bank's digital transformation isn't in the technology deployed but in the behavioral change achieved. By 2023, 86% share of digital transactions achieved—a remarkable transformation for a bank whose customer base includes elderly pensioners in rural Kerala. This wasn't accomplished through force but through thoughtful design. Every digital product had an "assisted mode" where bank staff could help customers navigate the interface. The bank ran thousands of "digital literacy camps" in villages, teaching not just Federal Bank's apps but basic smartphone usage.

The partnership strategy that emerged during this transformation was particularly sophisticated. Instead of viewing fintechs as threats, Federal Bank saw them as force multipliers. The bank became the preferred banking partner for dozens of fintech startups, providing them with banking infrastructure while learning from their agility and user experience design. This symbiotic relationship gave Federal Bank access to innovation without the risk and cost of internal development.

Federal Bank's approach to API banking was equally forward-thinking. While other banks grudgingly opened APIs to comply with regulations, Federal Bank embraced open banking enthusiastically. By 2022, the bank had over 200 APIs available to partners, enabling everything from embedded banking in e-commerce platforms to white-label banking services for corporates. This platform approach transformed Federal Bank from a service provider to an infrastructure player.

The cultural transformation required for digital success was perhaps the hardest part. Federal Bank had to convert relationship managers who'd spent decades doing in-person banking into digital evangelists. The bank's solution was elegant: instead of replacing people with technology, it augmented people with technology. Relationship managers got tablets with AI-powered insights about customer needs. Branch staff became "digital ambassadors," teaching customers to use apps rather than processing transactions manually.

The results speak for themselves. Customer acquisition costs dropped by 70%. Transaction costs fell by 85%. Most importantly, customer satisfaction scores increased—the digital experience wasn't replacing the human touch but enhancing it. Young NRIs who'd considered leaving Federal Bank for sexier alternatives stayed because the digital experience finally matched their expectations. Older customers who'd feared technology embraced it because Federal Bank made it accessible and non-threatening.

By 2024, Federal Bank's digital transformation was complete—or rather, institutionalized as an ongoing process. The bank that industry observers had written off as a digital dinosaur in 2010 was now winning awards for innovation. Federal Bank proved that digital transformation isn't about technology—it's about reimagining how technology can serve human needs. For a bank built on relationships, digital became just another way to strengthen those relationships, not replace them.

VII. Modern Era: Beyond Banking (2010s-Present)

The boardroom at Federal Bank's Aluva headquarters in early 2010 was tense. The global financial crisis had passed, but its aftershocks were reshaping Indian banking. New private banks were expanding aggressively, foreign banks were eyeing India's growing middle class, and payment companies were disrupting traditional revenue streams. Federal Bank, despite its remittance dominance, faced an existential question: remain a regional champion or transform into a national contender?

The answer came not through grand strategy documents but through systematic execution of what insiders called "Project Aspire"—Federal Bank's ambitious plan to become one of India's top five private banks by 2025. Rising to 6th largest private bank in India wasn't an accident but the result of deliberate choices that often went against conventional banking wisdom.

The geographic expansion strategy was counterintuitive. Instead of carpet-bombing metros with branches, Federal Bank identified "Little Keralas"—pockets of Kerala diaspora across India. Bangalore's Koramangala, Mumbai's Chembur, Delhi's Karol Bagh—neighborhoods where Kerala communities had established themselves. Each new branch in these areas immediately had a customer base, turning what should have been a 3-year breakeven into profitable operations within months.

Leadership transitions in this period were handled with unusual sophistication. When K.P. Hormis retired in 1979, he had already groomed successors who understood his philosophy. But by 2010, Federal Bank needed professional management that could navigate modern complexity while preserving cultural DNA. The appointment of Shyam Srinivasan as MD & CEO in 2010 marked this transition. An outsider from a multinational bank, Srinivasan did something unusual—he spent his first six months visiting branches, talking to long-time employees, understanding what made Federal Bank special before making any changes. The financial transformation under professional management has been remarkable. Market Cap of ₹48,217 Crore represents a valuation multiple that places Federal Bank among India's most valuable financial institutions. Revenue: 28,529 Cr and Profit: 4,137 Cr demonstrate the bank's ability to generate consistent returns despite operating in an increasingly competitive environment.

The expansion beyond Kerala required Federal Bank to solve a fundamental problem: how to maintain its relationship-banking DNA while scaling nationally. The solution came through what the bank called "hub and spoke with a twist." Major cities got full-service branches that looked and felt like any modern bank. But surrounding these hubs were smaller "relationship centers"—not traditional branches but spaces where customers could meet relationship managers, discuss financial planning, or simply have coffee while discussing loan applications.

The listing on multiple exchanges marked Federal Bank's arrival on the global stage. The bank is also listed in the Bombay Stock Exchange, National Stock Exchange of India and London Stock Exchange and has a branch in India's first International Financial Services Centre (IFSC) at the GIFT City. The London Stock Exchange listing was particularly strategic—it gave NRI investors in Europe direct access to Federal Bank equity, strengthening the emotional and financial bonds with the diaspora.

But perhaps the most important development in the modern era has been Federal Bank's approach to corporate social responsibility. Federal Bank has instituted a public charitable trust by name Federal Bank Hormis Memorial Foundation to perpetuate the fond memory of late K. P. Hormis, the founder of the bank. For Federal Bank, Corporate Social Responsibility (CSR) has been an inherited and inbuilt element of its culture from the day the bank was founded. The founder's values and ethos based on trust got embedded in the bank's policies and principles which reflect on its day-to-day business. CSR in Federal Bank began with the first act of cultivating banking habits in an agrarian society - to effectively utilise idle money for productive purposes.

The Federal Bank Hormis Memorial Foundation, established in 1996, represents more than corporate charity—it's an institutionalization of the bank's social mission. The foundation's activities range from healthcare initiatives like 'Sanjeevani- United against Cancer' mission to build awareness, encourage screening and testing for Cancer. Through this initiative, the bank aims to raise awareness of the prevention of cancer, helping individuals fight the social stigma associated with the disease and the hesitation to opt for early detection and diagnosis to skill development through Federal Skill Academy (FSA), aiming to contribute significantly to India's skilling ecosystem. The bank initiated the launch of its 5th and 6th Skill Academy in Chennai and Belagavi in October 2023. The existing 4 centres are in Kochi, Coimbatore, Faridabad and Kolhapur.

The neo-banking partnerships that Federal Bank has cultivated represent a sophisticated understanding of financial services' future. Rather than seeing fintech startups as threats, Federal Bank became the "bank behind the bank" for numerous digital-first financial services. These partnerships provide Federal Bank with access to younger demographics and innovative business models while giving fintechs the regulatory infrastructure and balance sheet they need to scale.

The geographic expansion strategy has been remarkably disciplined. Unlike peers who pursued branch-led growth in metros, Federal Bank focused on profitability over presence. Each new market entry followed extensive analysis of NRI populations, remittance flows, and competitive dynamics. The bank would rather be the dominant player in 15 states than a marginal player in 30. This focused approach has resulted in industry-leading metrics—cost-to-income ratios below 50%, ROE consistently above 15%, and asset quality that rivals the best in the industry.

Federal Bank's evolution from regional player to national contender hasn't diluted its core identity. Walk into any Federal Bank branch, and you'll still find the personal touch that Hormis insisted upon. The difference is that this personal touch is now augmented by AI-powered insights, delivered through digital channels, and backed by a balance sheet that can compete with anyone. It's proof that in banking, as in life, you can grow without losing your soul.

VIII. Playbook: Strategic Lessons

After nine decades of evolution, Federal Bank's journey offers a masterclass in strategic positioning that transcends banking. The lessons embedded in its DNA—forged through princely states, colonial transitions, economic liberalization, and digital disruption—provide a playbook for any institution seeking sustainable competitive advantage in rapidly changing markets.

Community Banking as Competitive Advantage

Federal Bank's deepest moat isn't technology or scale—it's the trust embedded in community relationships spanning generations. While global banks pursued standardization and efficiency, Federal Bank understood that banking in India is fundamentally about social capital. The bank's managers don't just know their customers' creditworthiness; they know their children's names, their business cycles, their family histories. This intimate knowledge creates switching costs that no interest rate differential can overcome.

Consider how Federal Bank evaluates loan applications. While competitors rely on credit scores and algorithmic decisioning, Federal Bank supplements data with what they call "social underwriting"—understanding the borrower's reputation in the community, family support systems, and character assessments from long-term observation. This approach has resulted in NPAs consistently below industry averages while serving segments other banks consider too risky.

The Power of Diaspora Networks

Federal Bank's dominance in remittances reveals a profound truth: diaspora communities are not just customer segments but economic ecosystems. The bank understood before anyone else that migration creates financial highways—money flows from destination to origin, but along with it flows information, opportunity, and eventually, investment. By positioning itself as the toll booth on these highways, Federal Bank captured value far beyond transaction fees.

The network effects are powerful and compounding. Each NRI customer Federal Bank acquires becomes a node in a network that attracts more customers. The construction worker in Dubai tells his colleague about Federal Bank's service. That colleague tells his family back home. The family opens accounts. When the colleague's nephew goes to Dubai, he already knows where to bank. This organic growth requires no marketing spend yet generates customer acquisition costs near zero.

Digital Transformation as Marathon, Not Sprint

Federal Bank's digital journey offers a contrarian lesson: sometimes being late is an advantage. While peers rushed to digitize in the 2000s, accumulating technical debt and legacy systems, Federal Bank waited until technologies matured and then leapfrogged everyone. By avoiding intermediate technologies, the bank built modern, cloud-native systems without the burden of migration.

The transformation strategy was distinctly human-centric. Instead of replacing people with technology, Federal Bank used technology to make people more effective. Relationship managers became armed with predictive analytics. Branch staff transformed into digital coaches. This approach avoided the cultural antibodies that kill most digital transformations while maintaining the human touch that differentiates Federal Bank.

Building Trust Over Generations

In an era obsessed with quarterly earnings, Federal Bank's multi-generational perspective seems almost quaint. Yet this long-term orientation has created compounding advantages. The bank doesn't optimize for maximum extraction from each customer but for lifetime value across generations. A education loan to a student today becomes a home loan tomorrow, a business loan eventually, and banking relationships for their children in the future.

This generational approach extends to employees. Federal Bank rarely hires laterally for senior positions, preferring to grow talent internally. Employees join as probationary officers and retire as general managers, accumulating decades of institutional knowledge. This creates continuity that customers value—their relationship manager might change, but the relationship with the institution endures.

Regional Dominance Before National Expansion

Federal Bank's expansion strategy violates conventional wisdom about growth. Instead of rapidly scaling nationally to achieve size, the bank spent decades dominating Kerala before venturing out. This patient approach built unassailable market position in the home market, generating cash flows to fund expansion while maintaining a fortress to retreat to if expansion failed.

The expansion, when it came, followed customers rather than pursuing new ones. Federal Bank didn't enter Mumbai to compete with HDFC for local customers; it entered to serve Keralites who'd migrated there. This following-the-diaspora strategy meant every new market had built-in demand, reducing execution risk and accelerating profitability.

Digital at the Fore, Human at the Core

This philosophy, which sounds like marketing speak, actually represents sophisticated strategic thinking. Federal Bank recognized that pure digital banks struggle with trust while pure traditional banks struggle with convenience. The solution isn't choosing one or the other but creating seamless integration where customers can move between channels based on context.

A customer might open an account digitally but want to discuss a home loan in person. They might check balances on an app but want human advice for investment decisions. Federal Bank built infrastructure that makes these channel transitions invisible—the digital assistant knows about branch conversations, the branch manager sees digital behavior. This omnichannel approach creates stickiness that neither pure digital nor pure physical models can match.

Managing Regulatory Complexity

Operating across nine decades of Indian banking means Federal Bank has survived every regulatory regime imaginable—from princely state regulations to colonial banking acts, from nationalization threats to Basel III requirements. This experience has created institutional expertise in regulatory navigation that younger banks lack.

The bank's approach to regulation is proactive rather than reactive. Federal Bank often exceeds regulatory requirements, maintaining capital buffers above mandated levels and implementing compliance systems before they're required. This conservative approach might reduce short-term returns but creates optionality—when regulations tighten, Federal Bank is already compliant while competitors scramble to adapt.

The Ecosystem Mindset

Modern Federal Bank doesn't see itself as a standalone institution but as a platform enabling an ecosystem. The bank provides infrastructure for fintechs, partners with technology companies, collaborates with government programs, and supports social enterprises. This ecosystem approach multiplies Federal Bank's reach without proportionally increasing costs or risks.

Each partnership is carefully structured to align incentives. Fintech partners get access to banking infrastructure; Federal Bank gets innovation and customer acquisition. Technology partners provide capabilities; Federal Bank provides domain expertise and distribution. These symbiotic relationships create value that neither party could generate alone.

The playbook that emerges from Federal Bank's journey is deceptively simple: understand your customers deeply, serve them completely, evolve deliberately, and think generationally. In a world obsessed with disruption, Federal Bank proves that sustainable success comes from evolution, not revolution—from deepening roots, not just spreading branches.

IX. Bear vs. Bull Case Analysis

As Federal Bank stands at the intersection of traditional banking excellence and digital transformation, investors face a complex calculus. The institution that built India's remittance highway now navigates an environment where highways are becoming digital, competitors are becoming platforms, and customers are becoming algorithms. The investment case for Federal Bank requires weighing structural advantages against emerging challenges.

Bull Case: The Resilient Remittance Machine

The bull thesis starts with mathematical inevitability. India receives over $100 billion in remittances annually, growing at 8-10% yearly. Federal Bank processes nearly 20% of these flows. Even if the bank merely maintains share in a growing market, remittance revenues will compound predictably. But the reality is even more favorable—Federal Bank's share has been growing, not shrinking, despite increased competition.

The moat around remittances is wider than it appears. New entrants like Wise or Remitly might offer better rates or slicker apps, but they can't replicate Federal Bank's last-mile presence in rural Kerala, the trust built over generations, or the ability to handle complex compliance requirements across multiple jurisdictions. When a construction worker in Saudi needs to ensure his mother in rural Idukki receives money for medical treatment, he doesn't experiment with startups.

The digital transformation, initially a drag on returns, is now bearing fruit. Federal Bank's cost-to-income ratio has dropped from 65% to below 50% in five years. Digital transactions at 86% mean marginal transaction costs approaching zero. The bank is essentially operating two models—a high-touch relationship bank for complex products and a digital utility for routine transactions—and executing both profitably.

The underpenetrated corporate banking opportunity is massive. Federal Bank has less than 2% share of Indian corporate banking despite being the sixth-largest private bank. As Kerala-origin entrepreneurs build billion-dollar companies across India, their emotional connection to Federal Bank creates natural entry points. The bank doesn't need to win Reliance or Tata; capturing mid-sized corporates with Kerala connections could double the corporate book.

Asset quality metrics support the bull case. Gross NPAs at 2.11% and net NPAs at 0.60% reflect the conservative underwriting culture Hormis embedded. The provision coverage ratio above 70% provides buffers for potential stress. Unlike peers who've faced asset quality shocks from corporate lending or retail exuberance, Federal Bank's steady approach has avoided blowups that destroy value.

Capital adequacy at 15.57% provides runway for growth without dilution. The bank can grow advances at 20% annually for years without raising capital, allowing returns to compound for existing shareholders. With ROE at 13.64% and improving, Federal Bank can generate capital faster than it consumes it—the hallmark of a compounding machine.

Bear Case: The Squeeze of the Middle

The bear thesis centers on Federal Bank's precarious position between giants and specialists. Large private banks like HDFC and ICICI have scale advantages in technology investment, product development, and brand building. Small finance banks and payment banks have regulatory advantages in serving the underbanked. Federal Bank sits in the middle—too small to match the giants' scale, too large to be nimble like specialists.

The overdependence on Kerala and NRI segments is a ticking time bomb. Kerala's population is aging and birth rates are below replacement. The Gulf economies are diversifying away from foreign labor, implementing nationalization policies that reduce Indian workers. If NRI remittances plateau or decline, Federal Bank's core growth engine stalls. The bank's attempts at geographic diversification have been modest—over 60% of branches remain in Kerala despite decades of expansion.

Competition from global fintech players in remittances is intensifying. Companies like Wise offer transparent pricing, real-time transfers, and superior user experience. While Federal Bank's relationship moat protects current customers, acquiring young NRIs becomes increasingly difficult. The next generation of migrants might have no emotional connection to Federal Bank, choosing providers based purely on price and convenience.

The concentration risk extends beyond geography to customer segments. Federal Bank's loan book is heavily exposed to Kerala real estate, NRI investments, and gold loans—all connected to remittance flows. An external shock that reduces remittances would cascade through multiple business lines simultaneously. The 2018 Kerala floods demonstrated this vulnerability when multiple revenue streams were impacted concurrently.

Technology spend requirements keep escalating while returns remain uncertain. Federal Bank must match competitors' digital capabilities just to maintain position, not gain share. The bank spends hundreds of crores annually on technology yet faces constant pressure to spend more. Unlike manufacturing where capital investment eventually slows, banking technology requires perpetual investment with no end in sight.

Regulatory headwinds pose additional challenges. The RBI's restrictions on unsecured lending, tightening of NPA recognition norms, and pressure on interest margins all disproportionately impact mid-sized banks. Federal Bank lacks the scale to absorb regulatory compliance costs easily or the political influence to shape policy. Each new regulation adds costs without corresponding revenue opportunities.

The Balanced View: Navigating Contradictions

The reality likely lies between extremes. Federal Bank's structural advantages in remittances won't disappear overnight, but they will erode gradually. The bank's digital transformation is real but expensive to maintain. Geographic concentration is a risk but also a source of competitive advantage.

The key question isn't whether Federal Bank can survive—its conservative culture and strong franchise ensure survival. The question is whether it can generate returns that justify investment versus alternatives. With the stock trading at modest multiples reflecting neither extreme optimism nor pessimism, the market seems equally uncertain.

For investors, Federal Bank represents a classic "sleep well" versus "eat well" dilemma. Conservative investors might appreciate the steady remittance flows, strong asset quality, and deep moats. Growth investors might be frustrated by geographic concentration, competitive pressures, and the structural challenges of being mid-sized. Value investors might see opportunity in the disconnect between Federal Bank's franchise value and market valuation.

The investment case ultimately depends on time horizon and worldview. Believers in India's demographic dividend and continued global migration might see Federal Bank as perfectly positioned. Skeptics about traditional banking's future might view Federal Bank as a melting ice cube, generating cash today but facing inevitable decline. Both could be right—just on different timelines.

X. Epilogue & Future Horizons

As the sun sets over the Arabian Sea, visible from Federal Bank's new technology center in Kochi, the institution stands at an inflection point that would have seemed impossible to its founders in 1931. The bank that began with ₹5,000 in capital now processes transactions worth that amount every fraction of a second. The ledgers once maintained by hand now exist in quantum-encrypted databases. Yet somehow, improbably, the soul of the institution—that peculiar Kerala mix of conservatism and ambition, tradition and innovation—remains intact.

The next chapter of Federal Bank's story will be written by leaders who never met K.P. Hormis but inherit his legacy. The current management faces challenges he couldn't have imagined: competing with algorithms that make credit decisions in milliseconds, serving customers who might never visit a branch, navigating regulations written for risks not yet invented. Yet they also have tools Hormis could only dream of: artificial intelligence that predicts customer needs, blockchain networks that settle transactions instantly, partnerships that extend Federal Bank's reach to every smartphone in India.

The strategic question facing Federal Bank isn't whether to abandon its regional roots for national ambitions—that's a false choice. The real question is how to leverage regional dominance into national relevance. Can Federal Bank become to India what regional champions like Santander became to Europe—institutions that maintained local character while achieving continental scale? The template exists, but execution requires threading needles between growth and prudence, innovation and tradition, global ambition and local presence.

Central bank digital currencies (CBDCs) represent both opportunity and threat. As the RBI develops the digital rupee, Federal Bank's remittance infrastructure could become either obsolete or essential. If CBDCs enable direct peer-to-peer international transfers, Federal Bank's role as intermediary diminishes. But if CBDCs require trusted validators and compliance partners, Federal Bank's expertise becomes more valuable. The bank is hedging both scenarios, building CBDC capabilities while deepening customer relationships that transcend transaction processing.

The evolution of cross-border payments through platforms like RippleNet and real-time payment systems changes the remittance game fundamentally. Speed becomes table stakes—instant transfers are expected, not exceptional. Federal Bank's advantage must shift from operational efficiency to value-added services: tax optimization for NRIs, investment advisory for repatriated funds, seamless integration between foreign earnings and Indian investments. The bank that built highways must now build the destinations that make travel worthwhile.

Climate change poses an underappreciated risk to Federal Bank's model. Kerala's vulnerability to flooding, as demonstrated in 2018 and 2019, threatens not just loan portfolios but the entire economic ecosystem Federal Bank depends upon. The bank's response has been thoughtful—developing climate risk models, supporting sustainable development, financing renewable energy projects. But the fundamental question remains: can a bank so dependent on one geography survive that geography's environmental challenges?

The talent war represents another frontier. Federal Bank must compete for engineers with tech giants, for relationship managers with global banks, for risk managers with fintech unicorns. The bank's solution has been cultural rather than just financial—offering purpose alongside paychecks, impact alongside incentives. Young professionals join Federal Bank not for the highest salary but for the chance to shape Indian banking's future while maintaining its soul.

Artificial intelligence and machine learning will transform banking in ways we're only beginning to understand. Federal Bank's experiments with AI for credit underwriting, fraud detection, and customer service are promising but preliminary. The real revolution comes when AI doesn't just automate existing processes but invents new ones—products we haven't imagined, services we don't yet know we need. Federal Bank must balance being fast enough to matter but slow enough to be safe.

The partnership ecosystem Federal Bank is building could become its greatest asset or biggest vulnerability. Each fintech partnership, while bringing innovation and reach, also creates dependency and complexity. Managing dozens of partnerships across technology stacks, business models, and regulatory regimes requires capabilities traditional banks never needed. Federal Bank must become not just a bank but a platform orchestrator—a fundamentally different organizational capability.

Looking ahead to 2030 and beyond, several scenarios seem plausible. In the optimistic case, Federal Bank successfully transforms into a national digital powerhouse while maintaining regional strength, becoming India's answer to DBS or Santander. The realistic case sees Federal Bank as a strong regional champion with selective national presence, profitable but not transformational. The pessimistic case envisions Federal Bank gradually marginalized by digital natives and global giants, surviving but not thriving.

What seems certain is that Federal Bank will remain quintessentially Kerala—conservative yet entrepreneurial, traditional yet innovative, local yet global. The institution that survived princely states and colonial rule, that thrived through nationalization threats and liberalization, that transformed from ledger books to artificial intelligence, has demonstrated remarkable adaptability within cultural continuity.

The Federal Bank story ultimately transcends banking. It's about how institutions can evolve without losing identity, how regional champions can achieve national relevance, how traditional businesses can embrace digital transformation. It's about the possibility that in a world racing toward standardization and automation, there remains space for institutions that remember banking is ultimately about people trusting other people with their dreams.

As monsoon clouds gather over Kerala, bringing the rains that have sustained this land for millennia, Federal Bank prepares for whatever storms or sunshine await. The bank that began as a solution to village credit problems has become integral to India's financial architecture. Whether it becomes more than that—a truly national champion, a global player, a platform that transcends banking—remains unwritten. But if history is any guide, Federal Bank will find a way to survive, adapt, and thrive, maintaining its soul while embracing whatever future emerges.

The next nine decades promise to be at least as interesting as the last nine. And somewhere, in a tea shop in Aluva or a exchange house in Abu Dhabi, in a startup office in Bangalore or a farm in Wayanad, Federal Bank will be there—quietly, competently, consistently turning financial transactions into human connections, one relationship at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube