FACT: The Story of India's Pioneer Fertilizer Giant

I. Introduction & Episode Roadmap

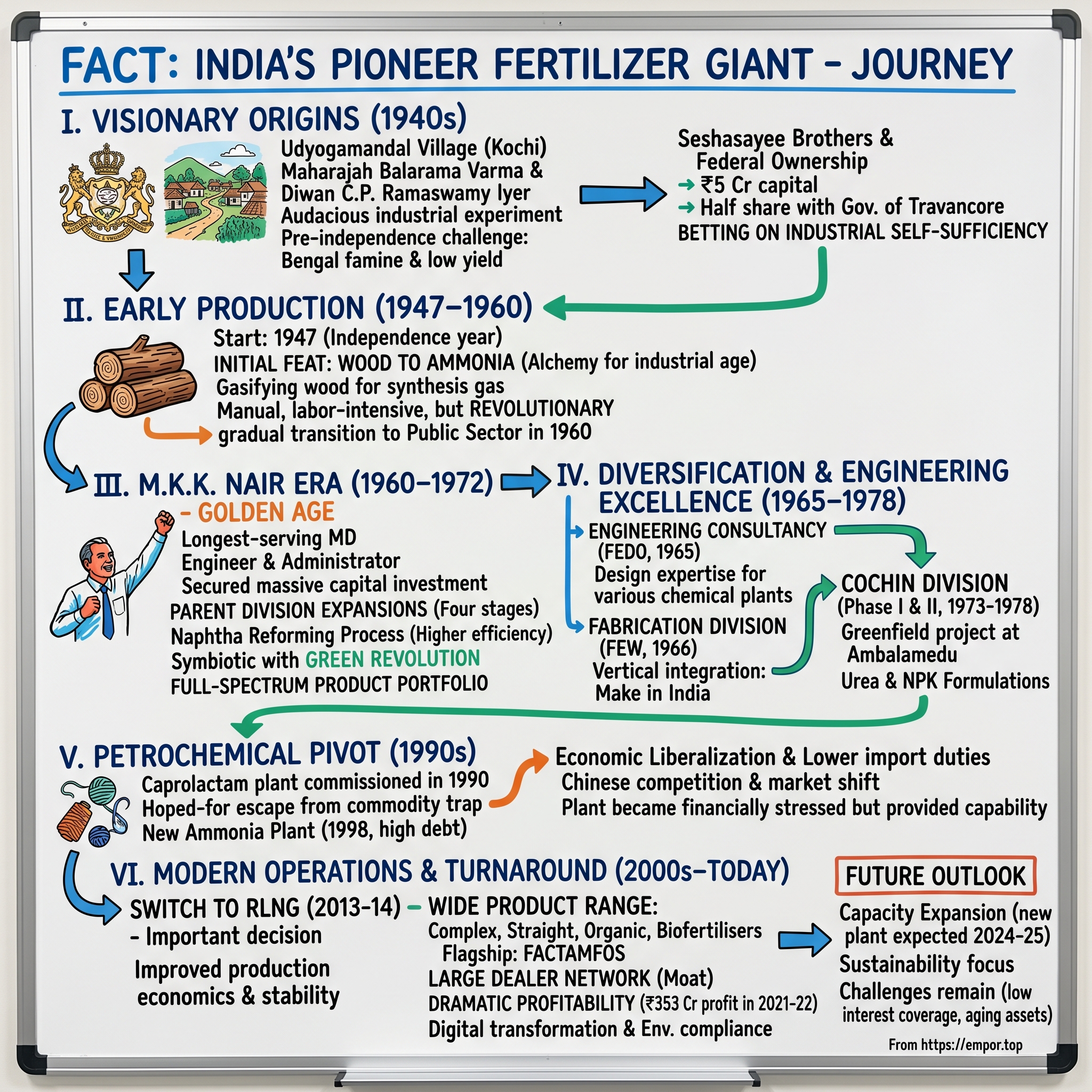

In the narrow lanes of Udyogamandal, a sleepy village near Kochi in 1943, an improbable industrial revolution was taking shape. While the world was engulfed in war and India remained under colonial rule, a visionary Maharajah and his ambitious Diwan were laying the foundation for what would become India's first large-scale fertilizer plant. Today, that audacious experiment—Fertilizers and Chemicals Travancore Limited—stands as Kerala's largest Central Public Sector Undertaking, commanding a market capitalization of ₹59,356 crores. Today, that audacious experiment—Fertilizers and Chemicals Travancore Limited—stands as Kerala's largest Central Public Sector Undertaking, commanding a market capitalization of approximately ₹59,356 crores.

Here's the remarkable paradox: A company with a P/E ratio of -660.7 and a PB ratio of 46—metrics that would make any traditional investor's head spin—has delivered a stock price appreciation of over 1,070% in the past three years. How did a princely state's industrial vision, conceived in the final years of the British Raj, transform into one of India's most enigmatic stock market stories?

This is the chronicle of FACT—a company that began by converting wood into ammonia when India couldn't feed itself, survived the socialist era's bureaucratic maze, weathered economic liberalization's competitive storms, and somehow emerged as a retail investor darling in the 2020s. It's a story about nation-building through nitrogen, about how a Maharajah's gamble became modern India's agricultural backbone, and about what happens when public sector legacy meets private market exuberance.

As we unpack this eight-decade saga, we'll explore the visionary leadership of forgotten heroes, the technological pivots that saved the company from obsolescence, the diversification bets that both defined and distracted from its mission, and the curious case of how a fertilizer PSU became a momentum stock. From the royal courts of Travancore to the trading screens of Mumbai, this is FACT's improbable journey.

II. Pre-Independence Vision & Royal Origins (1940s)

The year was 1943, and the world was at war. While Allied forces battled in Europe and the Pacific, a different kind of revolution was brewing in the princely state of Travancore. In the royal court of Thiruvananthapuram, Maharajah Sree Chithira Thirunal Balarama Varma was having intense discussions with his Diwan, Sir C.P. Ramaswamy Iyer—a man whose vision would forever alter the agricultural landscape of India.

Sir C.P. Ramaswamy Iyer stood in the forefront, cleared all obstacles and paved the way for setting up of FACT in a till then unheard of village in Kerala, Udyogamandal. The choice of location itself was audacious—a sleepy hamlet that most bureaucrats in Travancore couldn't even locate on a map. But Iyer saw what others couldn't: proximity to water transport, availability of land, and crucially, a strategic position that would serve independent India's agricultural heartland.

The context was dire. Pre-independence India was trapped in a vicious cycle of agricultural decline. The yield was getting lower and lower and in the early half of 20th century India found it had to depend on imports to meet out minimum food grain requirement. Bengal had just emerged from a devastating famine that killed millions. The British colonial administration, focused on extracting resources for the war effort, showed little interest in agricultural modernization. Food security wasn't just an economic issue—it was an existential crisis for a nation on the cusp of independence.

Enter the Seshasayee Brothers, industrialists from Tamil Nadu who had already made their mark in textiles and consumer goods. The royal court didn't just invite them; they actively courted and persuaded them to take on this unprecedented challenge. The financial structure reflected both ambition and pragmatism: FACT was incorporated with a share capital of ₹5 crores—a staggering sum for 1943. The ownership structure was deliberately federal: half the shares with the Government of Travancore, and the rest distributed among the governments of Cochin, Madras, and other states.

This wasn't just a business venture; it was a confederacy of princely states betting on industrial self-sufficiency before anyone knew what independent India would look like. The Maharajah and his Diwan were essentially venture capitalists, using royal treasuries to fund what private capital wouldn't touch. They were building India's first large-scale fertilizer plant without knowing whether there would even be an India to serve.

The technical challenges were monumental. In 1943, fertilizer technology was closely guarded by a handful of Western companies. The war had disrupted global supply chains, making it nearly impossible to import equipment. Yet somehow, through a combination of diplomatic maneuvering, technical improvisation, and sheer determination, the foundations were laid. Sir C.P. Ramaswamy Iyer personally intervened to clear bureaucratic hurdles, leveraging his connections across British India and the princely states.

What made this venture truly revolutionary was its timing. While the rest of India was consumed by the Quit India movement and political upheaval, Travancore was quietly laying the groundwork for agricultural independence. The Maharajah understood something profound: political freedom without economic self-sufficiency would be hollow. By investing in fertilizers, he was investing in India's ability to feed itself—a prerequisite for any meaningful independence.

The symbolism wasn't lost on contemporary observers. Here was an ancient kingdom, traditionally associated with spices and trade, pivoting to industrial chemistry. It was a statement of intent: the new India wouldn't just inherit the past but would forge its own industrial future. The fact that this happened in Kerala—a region that would later become known for its social progressivism—added another layer of significance.

By 1947, as India gained independence and Travancore merged with the Indian Union, FACT was ready to begin production. The timing was almost providential. A new nation, born amid partition's chaos and faced with feeding hundreds of millions, suddenly had access to indigenous fertilizer production. What started as a princely whim had become a national necessity.

III. Early Years: Wood to Ammonia (1947–1960)

FACT started production in 1947—the same year India gained independence. The synchronicity was profound: as a new nation raised its flag, its first fertilizer plant fired up its reactors. The initial setup was both ingenious and desperate: producing ammonium sulfate with an installed capacity of 50,000 metric tons per annum at Udyogamandal.

But the real story was in the raw material: wood. Yes, wood. In what might seem absurd to modern chemical engineers, FACT's pioneering technicians had figured out how to gasify wood to produce ammonia. Picture this: trucks loaded with timber from Kerala's forests, feeding into gasification units that would break down cellulose into synthesis gas, which would then be converted to ammonia. It was alchemy for the industrial age—turning trees into the building blocks of agricultural productivity.

The wood gasification process was a marvel of adaptation. Without access to natural gas or established petroleum infrastructure, FACT's engineers had to work with what Kerala had in abundance: forests. The process involved heating wood in controlled conditions to produce a mixture of carbon monoxide and hydrogen—synthesis gas—which could then be catalytically converted to ammonia. It was inefficient, labor-intensive, and environmentally questionable by today's standards, but in 1947, it was nothing short of revolutionary.

The early years were marked by a peculiar duality. On one hand, FACT was a cutting-edge industrial facility, one of the most advanced chemical plants in Asia. On the other, it operated like a cottage industry, with workers manually feeding wood into gasifiers, ash being cleared by hand, and quality control depending more on experienced operators' intuition than sophisticated instrumentation. The plant ran 24/7, with three shifts of workers keeping the gasifiers fed and the ammonia flowing.

The numbers tell a story of gradual progress. From the initial 50,000 MT capacity, production steadily increased as operators learned to optimize the wood gasification process. But by the mid-1950s, the fundamental economics began to shift. Kerala's forests were being depleted, wood prices were rising, and the energy efficiency of wood gasification—never great to begin with—was becoming untenable. The plant was consuming enormous quantities of timber to produce relatively small amounts of ammonia.

Initially in the Private Sector, promoted by M/s.Seshasayee Brothers, FACT became a Public Sector company in 1960. This transition wasn't sudden but gradual, reflecting the broader transformation of India's industrial policy. The Seshasayee Brothers, who had shepherded FACT through its birth pangs, found themselves increasingly constrained by the capital requirements of expansion and the government's growing role in strategic sectors.

The shift from wood to naphtha was FACT's first major technological pivot. By the late 1950s, it became clear that wood gasification had no future. The decision to switch to naphtha reforming—using petroleum products to produce ammonia—required not just new equipment but a complete reimagining of the plant's operations. This wasn't a simple upgrade; it was essentially building a new plant within the shell of the old one.

The naphtha reforming process was dramatically more efficient. Where wood gasification might achieve 20-30% efficiency, naphtha reforming could reach 60-70%. The new process also allowed for better quality control, higher production volumes, and integration with India's emerging petroleum infrastructure. Cochin Refineries, which would later become a key supplier, was being planned, creating a potential synergy that would define FACT's operations for decades.

The human dimension of this transition was profound. Workers who had spent years perfecting the art of wood gasification had to be retrained in petroleum chemistry. The plant's culture shifted from forestry-adjacent to petrochemical. Safety protocols changed dramatically—working with high-pressure naphtha reformers required different skills than managing wood gasifiers. Yet remarkably, the transition was accomplished without major incidents, a testament to the quality of FACT's early technical leadership.

By 1960, as FACT transitioned to public sector ownership, it had proven something crucial: India could not only operate sophisticated chemical plants but could also adapt and upgrade them. The journey from wood to naphtha wasn't just a technical evolution; it was a metaphor for India's industrial maturation. The company that began by literally burning trees for fertilizer was now ready to integrate with the global petrochemical economy.

The timing of the public sector transition was critical. Nehru's socialist vision for India was in full swing, and fertilizers were deemed too important to be left to private capital. The government takeover of FACT wasn't hostile—it was almost inevitable given the strategic importance of food security. As India entered the 1960s, facing growing population pressure and agricultural challenges, FACT's role would only become more central to national planning.

IV. Government Takeover & The M.K.K. Nair Era (1960–1972)

FACT became a Public Sector company in 1960 and the Government of India became the major shareholder in 1962. The transformation from Kerala state control to central government ownership reflected a larger truth: fertilizers had become too strategic for state-level management. This was the era of Five-Year Plans, where every ton of ammonia was accounted for in national spreadsheets.

Enter M.K.K. Nair—a name that deserves far more recognition in India's industrial history. Nair took charge in 1960, just as FACT was navigating its most complex transition. Unlike the typical IAS officers who ran PSUs as temporary postings, Nair would stay for eleven years, becoming FACT's longest-serving Managing Director. His tenure from 1960 to 1971 would define the company's golden age.

Nair was an unusual leader for a PSU. Trained as an engineer but gifted as an administrator, he understood both the technical minutiae of ammonia synthesis and the byzantine politics of Delhi's planning commission. His first challenge was immediate: convincing skeptical bureaucrats that FACT needed massive capital investment, not just maintenance budgets. The plant inherited from the private sector was already showing its age, and the naphtha conversion, while successful, had exposed numerous bottlenecks.

The parent division at Udyogamandal underwent four stages of expansion until the year 1972, upgrading technology and increasing capacity. Each expansion was a battle—fought in Delhi's corridors, not Udyogamandal's reactors. Nair became famous for his detailed presentations, arriving at Planning Commission meetings with hand-drawn charts showing exactly how each rupee would increase fertilizer output. He spoke the language of socialist planning fluently: import substitution, self-reliance, food security.

The first expansion focused on debottlenecking—identifying and eliminating production constraints. This wasn't glamorous work, but it was devastatingly effective. By optimizing heat exchangers, upgrading compressors, and improving catalyst management, FACT increased production by 30% without building new plants. The second expansion was more ambitious: adding new synthesis loops and reformers, pushing capacity to levels the original designers never imagined.

But Nair's real genius lay in understanding that FACT needed to be more than a single-product company. Through a series of expansions, FACT began producing multiple fertilizer grades. This wasn't just product diversification—it was agricultural science. Different crops needed different nutrient ratios. Rice paddies in Kerala required different fertilizers than cotton fields in Gujarat. Under Nair's leadership, FACT became India's first "full-spectrum" fertilizer producer, offering customized products for various soil types and crops.

The socialist context of the 1960s shaped everything. FACT wasn't just expected to produce fertilizers; it was expected to embody socialist ideals. The company built townships for workers, schools for their children, hospitals for the community. The Udyogamandal complex became a miniature socialist utopia, with subsidized housing, cooperative stores, and cultural centers. This paternalistic approach would later become a burden, but in the 1960s, it attracted India's best chemical engineers.

Labor relations during this period were surprisingly harmonious. Nair had a gift for managing unions, understanding that in a PSU, workers were stakeholders, not just employees. He institutionalized worker participation in productivity improvements, creating suggestion schemes that actually worked. The story goes that a plant operator's suggestion about reactor cooling saved FACT millions—and the operator was publicly honored by Nair himself.

The technical achievements were remarkable. By 1970, FACT was producing over 200,000 MT of fertilizers annually—a four-fold increase from 1960. The plant's efficiency metrics matched international standards, a stunning achievement for a PSU operating with indigenous technology and government procurement rules. FACT became a training ground for India's chemical engineers, with its operators and engineers later seeding fertilizer plants across the country.

The relationship with the Green Revolution was symbiotic. As Norman Borlaug's high-yielding varieties spread across India, they created massive demand for fertilizers. FACT's production fed directly into this agricultural transformation. The company's extension services—teams that educated farmers about fertilizer use—became as important as production itself. FACT wasn't just manufacturing chemicals; it was evangelizing scientific agriculture.

Yet challenges were mounting. The 1971 Indo-Pak war disrupted supply chains. The global oil crisis was beginning to affect naphtha prices. Competition from new private and public sector plants was emerging. When M.K.K. Nair retired in 1971, he left behind a transformed company—but also one facing an uncertain future. The cozy socialism of the 1960s was giving way to harder economic realities.

The numbers from this era tell a story of remarkable growth. Revenue increased ten-fold. Employment grew from a few hundred to several thousand. FACT's fertilizers were reaching every corner of South India. But beneath these achievements lay structural issues that would haunt the company: over-staffing, aging equipment despite upgrades, and dangerous dependence on government support. The Nair era had built FACT into an industrial giant, but giants, as mythology teaches us, can fall.

V. Diversification & Engineering Excellence (1965–1978)

The consultancy unit known as FACT Engineering and Design Organisation (FEDO) was set up in 1965. This move was visionary—perhaps too visionary for a fertilizer company. The logic was seductive: FACT had built India's expertise in chemical engineering; why not monetize that knowledge? FEDO would design plants not just for fertilizers but for chemicals, petrochemicals, pharmaceuticals—anywhere process engineering mattered.

The creation of FEDO reflected a deeper truth about Indian PSUs in the 1960s: they weren't just production units but capability builders. Every major PSU was expected to spawn expertise that could seed broader industrialization. FEDO's early projects were internal—designing FACT's own expansions—but soon external clients came calling. State governments wanted feasibility studies for chemical plants. Private companies needed process optimization. Even international agencies sought FEDO's expertise for Third World development projects.

The fabrication division, FACT Engineering Works (FEW) was established in 1966. If FEDO was the brain, FEW was the muscle. The logic was vertical integration taken to its extreme: why import pressure vessels and heat exchangers when you could build them yourself? FEW started by fabricating equipment for FACT's own expansions but quickly found external markets. The "Make in India" ethos, five decades before the slogan, was already driving procurement preferences toward indigenous suppliers.

Meanwhile, the main game—fertilizer expansion—was accelerating. The Cochin Division represented FACT's most ambitious bet yet. Unlike incremental expansions at Udyogamandal, this was a greenfield project, built from scratch on a new site at Ambalamedu. The scale was unprecedented for FACT: Phase-I, with the Ammonia-Urea Complex commissioned in 1973 and Phase-II consisting of Sulphuric Acid, Phosphoric Acid and Complex Fertiliser Plant commissioned during 1976-78.

The Cochin Division was conceived during the euphoria of the Green Revolution's early success. India's wheat production had soared, but rice—the staple for most Indians—lagged behind. Rice cultivation required different fertilizers, particularly urea and complex NPK formulations. The Cochin Division was designed specifically for these products, with massive ammonia and urea plants that would dwarf Udyogamandal's capacity.

The technology choices were fascinating. For ammonia, FACT selected the Haber-Bosch process with modern improvements—high-pressure synthesis loops, advanced catalysts, and heat recovery systems that pushed energy efficiency to new levels. The sulfuric acid plants used the contact process, converting sulfur to SO2 and then to SO3 before absorption. The phosphoric acid facility used the wet process, reacting phosphate rock with sulfuric acid. Each technology was proven globally but needed adaptation for Indian conditions—different raw material qualities, monsoon humidity, and maintenance practices suited to local skills.

The construction of Cochin Division coincided with India's most turbulent period since independence. The 1975 Emergency created an unusual dynamic: authoritarian efficiency combined with socialist planning. Projects moved faster—land acquisition that might have taken years happened in months. Labor disputes were suppressed. Environmental clearances were rubber-stamped. The Cochin Division, which might have taken a decade under normal circumstances, was completed in record time.

Yet this wasn't just about speed. The technical achievements were genuine. The urea plant at Cochin Division incorporated energy-saving features that were cutting-edge for the 1970s: CO2 recovery from flue gases, advanced steam systems, and process integration that minimized waste. FACT's engineers, many trained abroad but committed to indigenous development, created innovations that would later be exported through FEDO to other developing countries.

The human story of this expansion was equally compelling. Thousands of workers—welders, fitters, engineers—converged on Cochin. The construction site became a melting pot: Bengali engineers who had worked on Durgapur Steel Plant, Tamil technicians from petroleum refineries, Malayali workers providing local expertise. The project management, handled entirely by Indians despite the era's preference for foreign consultants, became a case study in indigenous capability.

But diversification came with costs. FEDO, while prestigious, distracted management attention from the core fertilizer business. FEW, despite early success, struggled with capacity utilization—FACT's own projects were cyclical, and external customers were inconsistent. The Cochin Division, while technically successful, was capital-intensive beyond initial projections. Interest payments began eating into operational profits.

The broader context was India's evolving agricultural policy. The initial Green Revolution focus on wheat and rice was giving way to more nuanced approaches. Pulse cultivation needed different nutrients. Cash crops like cotton and sugarcane had their own requirements. FACT's product portfolio expanded to match: DAP (diammonium phosphate), complexes with micronutrients, specialty grades for plantation crops. The company that once produced simple ammonium sulfate now offered dozens of formulations.

By 1978, FACT had transformed from a single-plant fertilizer manufacturer to a diversified chemical conglomerate. Three major production complexes, an engineering consultancy, a fabrication division—the company employed over 10,000 people directly and supported thousands more indirectly. Annual production exceeded 500,000 MT across all products. FACT had become not just Kerala's largest industrial enterprise but one of India's flagship PSUs.

Yet storm clouds were gathering. The global oil crisis had made naphtha-based production increasingly uneconomical. Natural gas, the global feedstock of choice, wasn't available in Kerala. Newer plants in Gujarat and along the HBJ pipeline had significant cost advantages. The very diversification that seemed strategic in the 1960s was becoming a liability. FACT was trying to be everything—producer, consultant, fabricator—and risking being excellent at nothing. The stage was set for the crises and transformations of the coming decades.

VI. Petrochemical Pivot: The Caprolactam Story (1990s)

The year 1991 changed everything. As P.V. Narasimha Rao and Manmohan Singh dismantled the License Raj, FACT faced an existential question: How does a socialist-era PSU survive in a liberalized economy? The answer, controversially, was caprolactam—a petrochemical used in nylon production that seemed to promise escape from the commodity fertilizer trap.

The Caprolactam plant in Udyogamandal was commissioned in 1990. The timing was either prescient or disastrous, depending on your perspective. Conceived in the protected 1980s but born into the liberalized 1990s, the caprolactam project embodied all the contradictions of India's economic transition.

The investment decision had been made in the mid-1980s when caprolactam commanded premium prices and India imported nearly all its requirements. The logic seemed unassailable: leverage FACT's ammonia production (caprolactam synthesis requires ammonia), enter a high-margin business, and reduce import dependence. The Ministry of Chemicals and Fertilizers, eager to showcase PSU dynamism, fast-tracked approvals. The plant would produce 50,000 MT annually, making FACT India's largest caprolactam producer.

The technology selection process revealed PSU decision-making at its most complex. Multiple technologies existed: the Japanese HPO process, the Dutch DSM process, the Italian SNIA process. Each came with different capital costs, operating efficiencies, and technology transfer terms. FACT ultimately chose a proven European technology, but the negotiation took three years—by which time global caprolactam markets had shifted.

Construction began in 1987, just as India was experiencing its worst fiscal crisis since independence. Foreign exchange was scarce, import licenses were gold dust, and the government was mortgaging gold reserves. Yet somehow, FACT managed to import critical equipment, navigate bureaucratic mazes, and complete construction. The plant's commissioning in 1990-91 coincided almost exactly with economic liberalization—a cosmic irony that wouldn't be lost on later analysts.

The early operations were promising. Indian textile manufacturers, particularly tire cord producers, welcomed domestic caprolactam supply. The quality matched international standards—a significant achievement for a first-time producer. FACT's caprolactam found markets not just in India but in Southeast Asia, where rapidly growing economies were hungry for synthetic fiber intermediates.

But liberalization changed the game fundamentally. Import duties on caprolactam, once prohibitive, were slashed. Chinese producers, with massive scale and state subsidies, began dumping product in Asian markets. Global petrochemical giants, previously locked out of India, established trading offices in Mumbai. FACT's captive market evaporated almost overnight.

The financial impact was severe. The caprolactam plant had cost over ₹500 crores—FACT's largest single investment. Debt servicing consumed cash flows. Worse, caprolactam production required consistent operations at high capacity for economics to work. Any disruption—maintenance, feedstock shortage, market downturn—turned profits into losses. The plant that was supposed to be FACT's salvation became its albatross.

The new Ammonia Plant was set-up at Udyogamandal at a cost of Rs.638 crore and commissioned during March 1998. This investment, coming on top of caprolactam, pushed FACT's debt to dangerous levels. The new ammonia plant was necessary—the old units were obsolete—but the timing was terrible. The Asian Financial Crisis of 1997 had crushed demand, the Indian government was cutting fertilizer subsidies, and private sector competitors were gaining market share.

The human dimension of this period was particularly poignant. FACT's engineers had successfully mastered complex petrochemical technology, only to find that technical competence wasn't enough in a market economy. Marketing teams, used to allocated fertilizer sales in a controlled economy, struggled to sell specialty chemicals in competitive markets. The organization, built for stability, had to learn agility—a painful transformation for a PSU culture.

Yet the caprolactam venture wasn't entirely misguided. It created unexpected capabilities: FACT became expert in high-pressure, high-temperature operations beyond traditional fertilizer parameters. The quality systems required for petrochemical customers upgraded the entire organization. Environmental management, critical for petrochemical operations, improved dramatically. These capabilities would prove valuable in unexpected ways.

The strategic debate around caprolactam revealed deeper tensions. Should PSUs stick to their core mandate—in FACT's case, fertilizer production for food security? Or should they pursue commercial diversification to ensure financial viability? The government, as owner, sent mixed signals: demanding both public service and profitability. The market, meanwhile, was unforgiving of strategic confusion.

By the decade's end, FACT's caprolactam business had stabilized but at lower margins than projected. The plant operated at 70-80% capacity, enough to cover variable costs but not to justify the investment. The diversification into petrochemicals had neither failed completely nor succeeded convincingly—a limbo that would characterize FACT's strategic position for years to come.

The broader lesson was sobering: In a liberalized economy, good intentions and technical competence weren't enough. Market timing, competitive positioning, and financial structuring mattered as much as engineering excellence. FACT had learned to produce world-class caprolactam just as the world decided caprolactam wasn't worth very much. The 1990s ended with FACT financially stressed, strategically confused, but somehow still standing—a testament to both PSU resilience and inertia.

VII. Modern Operations & Product Portfolio (2000s–Today)

The turn of the millennium found FACT at a crossroads. The company was operating two major production complexes—Udyogamandal and Cochin Division—but both were showing their age. The caprolactam adventure had left deep financial scars. Private competitors like Coromandel International and Chambal Fertilizers were eating into market share with more efficient operations. Something had to change.

Company was shifted from Naphtha based operations to RLNG based operations in 2013-14. This transition to Regasified Liquefied Natural Gas (RLNG) was perhaps FACT's most important operational decision of the 21st century. For decades, the company had struggled with naphtha's price volatility and inefficiency. Natural gas, the global standard for ammonia production, had finally arrived in Kerala through LNG terminals. The conversion required significant capital investment but promised dramatic improvements in production economics.

The RLNG transition wasn't just about changing feedstock; it required reimagining the entire supply chain. FACT tied up with Indian Oil Corporation Limited (IOCL) for long-term RLNG supply, creating stability after decades of spot market volatility. To reduce import dependence further, FACT also secured agreements with Bharat Petroleum Corporation Limited (BPCL) for 60% of its sulfur requirements from the Kochi Refinery, and began sourcing additional sulfur from Mangalore Refinery and Petrochemicals Limited (MRPL).

The company produces a wide range of fertilisers like Complex fertilisers (Factamfos), Straight fertilisers (Ammonium Sulphate), Organic fertilisers, Biofertilisers and Imported fertilisers (Muriate of Potash). This product portfolio evolution reflected changing agricultural practices. The old model of pushing whatever the plant could produce was dead. Modern farming demanded customized nutrient solutions.

FACTAMFOS, the company's flagship complex fertilizer brand, became the cornerstone of operations. FACT has an annual installed capacity of 6.33 lakh MT of complex fertilizers (NP 20:20:0:13), 2.25 lakh MT of Ammonium Sulphate and 0.5 lakh MT of Caprolactam. The 20:20:0:13 grade (20% Nitrogen, 20% Phosphorus, 0% Potassium, 13% Sulfur) was specifically formulated for South Indian soils, which are often sulfur-deficient.

The move into organic and bio-fertilizers represented both market opportunity and image rehabilitation. FACT PDM is a natural source of Potash. The manure is produced from sugarcane molasses having 14.5% Potassium. It also contains small quantities of Nitrogen, Phosphorus as well as secondary and micronutrients. Application of PDM will increase plant growth by activating enzymes. The product helps to improve soil texture, water-holding capacity and overall soil health, thereby increasing nutrient uptake of plants. Once applied in soil,it also enhances soil fertility by multiplication of microorganisms. PDM is suitable for all crops, all soils and all seasons. It is also good for drought resistant crops. PDM is the best suitable manure for Organic farming.

PROM is an organic-based natural manure and the product is a Govt. of India's initiative under PM-PRANAM. PROM is marketed by FACT and the product specifications are confirming to FCO Standard. It is a high-quality, slow-releasing organic manure which provides essential nutrients to enrich the soil. These initiatives aligned with the government's push toward sustainable agriculture while opening new market segments beyond traditional chemical fertilizers.

The distribution network underwent massive expansion. FACT is having 5935 dealers for distribution of fertilizers. FACT is encouraging SC/ST category dealers to apply for the dealership in accordance with policy of Department of Fertilizers, Government of India. This dealer network, spreading across Kerala and neighboring states, became FACT's competitive moat. While private players might have better plants, FACT had deeper rural penetration.

The financial turnaround was dramatic. With the excellent production and marketing performance, FACT could register a profit of ₹353.28 Crore during the year 2021-22. After years of losses, the company was finally generating substantial profits. The combination of RLNG conversion, operational efficiency improvements, and favorable fertilizer policies had worked.

But the most ambitious move was yet to come. Company is also expanding its fertilizer production capacity by setting up and additional Complex NP plant of 1650 TPD capacity. The work is in progress and plant is expected to be productive by 2024-25. This expansion, funded through internal accruals and land sale proceeds, would add 5.45 lakh MT to annual capacity—nearly doubling complex fertilizer production.

The modernization wasn't limited to production. FACT embraced digital transformation in distribution and farmer engagement. Mobile apps for dealers, SMS-based advisory services for farmers, soil testing laboratories providing customized fertilizer recommendations—the company that once distributed fertilizers through government allocation was now using data analytics to optimize sales.

Environmental compliance, once an afterthought, became central to operations. Effluent treatment plants were upgraded, stack emissions were monitored continuously, and green belts were expanded around production facilities. The company that had started by gasifying wood was now pursuing carbon neutrality goals, however distant they might be.

The caprolactam business, after years of struggle, found its niche. Rather than competing with global giants on commodity grades, FACT focused on specialty applications and regional markets. The petrochemical segment comprises of caprolactam for use in manufacturing nylon tire cords, filament yarns, and engineering plastics. The business would never justify its initial investment, but it was no longer bleeding cash.

Yet challenges remained formidable. Company has low interest coverage ratio. Despite operational improvements, FACT's financial metrics remained weak by private sector standards. The company was profitable but not sufficiently so to service its accumulated debt comfortably. Competition from imports, particularly from countries with natural gas advantages, continued to pressure margins.

The workforce, while skilled and dedicated, was aging. Young engineers preferred private sector opportunities or startups over PSU careers. The average age of FACT employees had crossed 45, and succession planning was becoming critical. The company that had once attracted India's brightest chemical engineers was struggling to recruit fresh talent.

Looking at current operations, FACT remains Kerala's fertilizer lifeline. Its Cochin division has a production facility of over 485,000 tons-per-annum (TPA) of complex fertilizer, approximately 330,000 TPA of sulfuric acid and over 115,200 TPA of phosphoric acid. Combined with Udyogamandal's output, the company supplies the majority of Kerala's fertilizer needs—a strategic position that provides both stability and responsibility.

VIII. Public Sector Challenges & Governance

FACT is under the administrative control of the Department of Fertilizers, Ministry of Chemicals & Fertilizers, Government of India. This simple statement conceals a byzantine governance structure that has shaped—and often constrained—the company's destiny for six decades.

The subsidy regime represents FACT's fundamental challenge. In India, fertilizers are sold at controlled prices far below production costs, with the government compensating manufacturers through subsidies. Total subsidies to farmers in India is in the range of $45 billion to 50 billion, to the tune of 2%-2.5% of GDP. But per farmer the subsidy just about touches $48 in India, compared to over $7,000 in the U.S. This system, designed to ensure affordable fertilizers for farmers, creates perverse incentives for manufacturers.

For FACT, the subsidy mechanism works like this: The company produces fertilizers at market costs—for natural gas, phosphoric acid, labor—but sells at government-mandated prices, often 40-60% below cost. The difference is supposed to be reimbursed through subsidies, but delays are endemic. Subsidies often arrive 6-12 months late, forcing FACT to borrow working capital at commercial rates. The interest burden from this delay isn't fully compensated, creating a structural disadvantage versus private players with deeper pockets.

The political economy of fertilizer subsidies is particularly complex. Every government promises cheaper fertilizers to farmers—a powerful vote bank. But finance ministries, facing fiscal pressures, delay or reduce subsidy payments. FACT, as a PSU, cannot refuse to supply fertilizers even when subsidies are delayed. Private companies can and do reduce production when subsidy payments lag, but FACT must maintain supply as a "national duty."

Competition from private players has intensified dramatically since liberalization. Companies like Coromandel International, Chambal Fertilizers, and Gujarat State Fertilizers Corporation operate with greater operational flexibility. They can hire and fire based on market conditions, close unprofitable plants, and pivot to more lucrative products. FACT, bound by PSU regulations, carries legacy costs—surplus labor, aging infrastructure, social obligations—that private competitors don't bear.

The numbers are telling: FACT employs roughly 2,500 permanent employees for production levels that private players achieve with half that workforce. This isn't about individual productivity—FACT's workers are skilled and dedicated—but about structural overstaffing inherited from an era when PSUs were employment providers as much as producers. Every voluntary retirement scheme costs crores in severance, money that could fund modernization.

Labor relations present another layer of complexity. FACT has multiple unions representing different employee categories, each with distinct demands and political affiliations. Wage negotiations follow government pay commission recommendations, not market dynamics. A junior engineer at FACT might earn more than counterparts at private fertilizer companies, but senior technical talent is grossly underpaid versus private sector alternatives. This inverted compensation structure—overpaying at the bottom, underpaying at the top—makes it difficult to attract and retain leadership talent.

Environmental compliance has become increasingly stringent and expensive. FACT's plants, particularly the older units at Udyogamandal, require constant upgrades to meet pollution norms. The location itself—in densely populated areas that have grown around the plants—makes compliance challenging. Effluent treatment, air quality management, and waste disposal consume resources that newer plants, built in industrial zones with modern technology, don't face.

The Pollution Control Board regularly issues notices for violations, some legitimate, others reflecting changing standards applied retroactively. Each notice triggers a compliance process involving technical fixes, legal proceedings, and often, production disruptions. The reputational damage from being labeled a polluter affects employee morale and community relations, even when violations are minor or technical.

Political interference, while less overt than in the past, remains a reality. Board appointments often reflect political considerations rather than technical competence. Marketing decisions—which dealers to appoint, which regions to prioritize—face political pressure. Local politicians expect FACT to sponsor community events, provide employment to constituents, and maintain loss-making facilities for social reasons.

The autonomy granted to FACT's management varies with political cycles. Reformist governments push for commercial performance, encouraging tough decisions on costs and efficiency. Populist administrations emphasize social obligations, restricting layoffs and demanding expanded fertilizer distribution regardless of economics. This policy uncertainty makes long-term planning nearly impossible.

Yet FACT has shown remarkable resilience. The company has remained profitable in recent years despite these constraints, a testament to operational improvements and favorable fertilizer policies. The management, working within tight boundaries, has achieved efficiency gains through technology upgrades, better capacity utilization, and improved marketing. But the question remains: How much more could FACT achieve with private sector flexibility?

The governance structure itself—reporting to the Department of Fertilizers, oversight by the Comptroller and Auditor General, scrutiny by parliamentary committees—creates multiple veto points for decisions. A capacity expansion that a private company might approve in weeks takes FACT years to navigate through bureaucratic approvals. By the time investments are sanctioned, market conditions have often changed.

The recent profitability has created its own challenges. As a profitable PSU, FACT faces pressure to pay higher dividends to the government, reducing retained earnings for modernization. The government's disinvestment agenda periodically includes FACT, creating uncertainty about ownership and strategic direction. Employees worry about privatization; investors wonder about the government's commitment.

Looking ahead, FACT exemplifies the broader challenge of PSU reform in India. The company has commercial potential—strategic location, established brand, technical competence—but operates within a governance framework designed for a different era. Reform attempts face resistance from multiple stakeholders: unions fearing job losses, politicians losing patronage opportunities, bureaucrats protecting turf.

The irony is palpable: FACT, created by a princely state as a commercial venture, has become more governmental over time, even as India's economy has liberalized. The company that pioneered industrial development in Kerala now struggles with the very governance structures meant to ensure public accountability. It's a cautionary tale about how institutional frameworks, once established, persist long after their original rationale has vanished.

IX. Stock Market Phenomenon & Recent Performance

The transformation of FACT from a sleepy PSU into a momentum darling is one of Indian capital markets' most bewildering stories. Fertilizers & Chemicals Travancore Ltd share price moved up by 1070.77% on BSE over last 3 years—a performance that would make tech unicorns envious. Yet the fundamentals tell a different story: The P/E ratio of The Fertilisers and Chemicals Travancore is -660.7 As on 26 May, 2025 | 15:11 · The PB ratio of The Fertilisers and Chemicals Travancore is 46 As on 26 May, 2025 | 15:11.

These metrics defy conventional valuation logic. A P/E ratio of -660.7 suggests either negative earnings or such minimal profits that the ratio becomes meaningless. A PB ratio of 46 means investors are paying 46 rupees for every rupee of book value—extraordinary for a capital-intensive manufacturing company. In comparison, efficiently run private fertilizer companies trade at PB ratios of 2-4x. What explains this disconnect?

The story begins in 2020-21, when FACT was trading around ₹50-60, largely ignored by institutional investors. The company had just emerged from years of losses, its balance sheet was stressed, and privatization rumors kept serious investors away. Then came the perfect storm of factors that would transform FACT into a retail investor phenomenon.

First, the COVID-19 pandemic created an unusual dynamic. The landscape changed in 2020, with net inflows of INR 52,897 crore, as retail participation soared due to low interest rates, liquidity-driven rallies, and the rise of digital trading platforms. Millions of new retail investors, armed with smartphone apps and stimulus savings, entered the market seeking "undervalued" PSUs.

FACT fit the narrative perfectly: a government-owned company (seemingly safe), in fertilizers (essential sector), trading at "cheap" absolute prices (under ₹100), with improving financials. The fact that it was Kerala's largest PSU added regional pride to the investment thesis. Social media groups and YouTube channels began promoting FACT as the "next multibagger."

The operational turnaround provided fundamental justification for the initial price surge. With the excellent production and marketing performance, FACT could register a profit of ₹353.28 Crore during the year 2021-22. After years of losses, genuine profitability attracted attention. The RLNG conversion was bearing fruit, global fertilizer prices were rising, and government policies favored domestic producers.

But what started as fundamental improvement morphed into momentum trading. From 2020 to 2024, the participation of retail investors in the stock market has grown from 15% to an estimated 35%. This surge in retail participation created new dynamics. Stocks with high retail ownership often exhibit extreme volatility, driven more by sentiment than fundamentals.

The mathematics of FACT's float amplified these dynamics. Promoter Holding: 90.0% With the government holding 90%, only 10% of shares were available for trading. This tiny float—roughly 6.4 crore shares—meant that even modest buying pressure could spike prices. When lakhs of retail investors decided FACT was the next big thing, the supply-demand imbalance became extreme.

Upper circuits became routine. Days when FACT would hit its 20% upper circuit, locking buyers out and creating FOMO (fear of missing out), became common. Each locked upper circuit created more media attention, more YouTube videos, more WhatsApp forwards about the "rocket stock." The feedback loop was self-reinforcing: rising prices attracted attention, attention brought buyers, buyers pushed prices higher.

The valuation disconnect widened progressively. By mid-2023, FACT was trading at valuations that implied either massive hidden assets or explosive future growth—neither of which was evident from company disclosures. The market capitalization exceeded ₹50,000 crores for a company generating profits of a few hundred crores. Traditional metrics became meaningless.

Institutional investors largely stayed away, recognizing the bubble dynamics. Mutual funds, which typically hold significant stakes in large-cap companies, had minimal exposure to FACT. Foreign institutional investors were absent. The ownership structure became increasingly concentrated among retail investors, creating an echo chamber where skepticism was drowned out by euphoria.

The quarterly results began attracting unusual attention. Fertilizers & Chemicals Travancore Ltd's net profit fell -73.61% since last year same period to ₹8Cr in the Q3 2024-2025. Despite deteriorating financials, the stock continued its momentum through much of 2024, demonstrating the disconnect between price and performance.

Exchange interventions became frequent. 21 Apr - Exchange has sought clarification from Fertilizers and Chemicals Travancore Ltd on April 21, 2025, with reference to Movement in Volume. Clarification sought from Fertilizers and Chemicals Travancore Ltd · 7 Sep 2023 - Exchange has sought clarification from Fertilizers and Chemicals Travancore Ltd on September 7, 2023, with reference to Movement in Volume. Clarification sought from Fertilizers and Chemicals Travancore Ltd · 15 Jun 2023 - Exchange has sought clarification from Fertilizers and Chemicals Travancore Ltd on June 15, 2023, with reference to Movement in Volume. These repeated queries about unusual volume and price movements highlighted regulatory concern about potential manipulation or irrational exuberance.

The analyst community struggled to make sense of the phenomenon. Traditional analysts, using DCF models and peer comparisons, calculated fair values of ₹200-300—a fraction of peak prices. But momentum traders and technical analysts, reading charts rather than balance sheets, kept setting higher targets. Analyst Palviya recommends buying FACT stock, noting its recovery and sustained performance above the 100-day moving average. A target price of Rs 940-960 is set, with a stop loss at Rs 760.

The social dynamics were fascinating. FACT became a cultural phenomenon in Kerala's investment community. Family WhatsApp groups discussed FACT's daily movements. Local tea shops buzzed with FACT price predictions. Employees of the company, watching their employer's stock skyrocket, felt vindicated after years of being dismissed as working for a "sick PSU."

Yet the risks were mounting. Company has low interest coverage ratio. Despite the stratospheric valuations, fundamental challenges remained. Competition from imports, subsidy dependencies, and aging infrastructure hadn't disappeared. The stock price had decoupled from business reality.

The correction, when it came, was swift. FACT has experienced a significant decline of 52% from its peak but is showing early signs of recovery. Key indicators, including a double bottom pattern and bullish RSI momentum, suggest a potential upward movement, indicating a shift towards a bullish trend. From peaks above ₹1,800, the stock corrected sharply, burning late entrants who had bought at elevated levels.

The broader lesson is sobering. However, investors may be overlooking the outsized role that the "momentum factor" played in the market's 2024 advance. "Momentum" refers to the tendency for stocks that have recently performed well to continue rising in the near term, often amid easy financial conditions like those that prevailed for much of last year. Consider that while the S&P 500 rose about 23% in 2024, the stocks with the strongest 12-month momentum (i.e., those rising the fastest for that time frame) were up an extraordinary 58% for the year, outperforming all other "factors," including growth- and value-oriented equities, by at least 38 percentage points. When momentum drives stock gains this powerfully, it indicates investors are avidly chasing the market's trends—and potentially overlooking its risks, particularly if financial conditions are set to tighten.

FACT's journey from ₹50 to ₹1,800 and back to ₹900 encapsulates the era of retail investing in India—democratized access creating both opportunities and bubbles. The company that started as a Maharajah's industrial vision had become a vehicle for retail speculation, its fundamental business almost irrelevant to its stock price.

For long-term investors, FACT presents a paradox. The operational improvements are real—RLNG conversion, capacity expansion, and market position in Kerala provide genuine value. But at current valuations, even assuming perfect execution, the stock appears priced for perfection and beyond. The momentum game might continue, but it's increasingly divorced from investment fundamentals.

X. Social Impact & CSR Legacy

Medical Oxygen Plants were installed during COVID-19. Tablet computers were distributed to under privileged school children. Company supplied provisions to community kitchen. These CSR initiatives during the pandemic represented FACT at its best—a public institution stepping up during crisis, leveraging its industrial capabilities for social good.

The COVID-19 oxygen crisis of 2021 saw FACT play an unexpected but crucial role. While the company wasn't a medical oxygen producer, its industrial oxygen infrastructure and technical expertise became invaluable. FACT's engineers helped establish oxygen generation facilities, its supply chain networks facilitated distribution, and its CSR funds supported medical infrastructure. The irony wasn't lost: a fertilizer company helping people breathe during a respiratory pandemic.

But FACT's social impact extends far beyond crisis response. Presently FACT is the lead fertilizer supplier of Kerala. This position carries enormous responsibility. Kerala's agricultural economy—from rubber plantations in Wayanad to spice gardens in Idukki—depends on consistent, affordable fertilizer supply. When global prices spike or supply chains disrupts, FACT acts as a buffer, maintaining supplies even at financial loss.

The dealer network tells a story of inclusive growth. FACT is having 5935 dealers for distribution of fertilizers. FACT is encouraging SC/ST category dealers to apply for the dealership. SC/ST dealers are exempted from payment of Security Deposit and there is no prerequisite of furnishing Fixed Deposits as in general category dealers. This isn't tokenism but substantive economic empowerment, creating entrepreneurship opportunities in marginalized communities.

The farmer education programs represent FACT's most enduring legacy. Since the 1960s, company agronomists have conducted village-level training on scientific fertilizer use. These aren't mere product promotions but genuine agricultural extension services: soil testing, crop-specific nutrient management, integrated pest management. Generations of Kerala farmers learned modern agriculture through FACT's programs.

Company continued to give priority to various Social Responsibility measures. The theme for 2021-22 was 'Health & Nutrition' with special focus on COVID related measures. Company's CSR activities inter alia focussed on supply of drinking water to nearby areas of Udyogamandal, farmer education programs such as Soil testing services and marketing of organic manures.

The environmental rehabilitation efforts around FACT's plants tell a complex story. Udyogamandal, once pristine, bore the environmental cost of India's industrial ambitions. Today, FACT spends crores on effluent treatment, air purification, and green belt development. The company that once polluted is now trying to heal—a metaphor for India's broader environmental awakening.

The employment generation impact is substantial but complicated. FACT directly employs about 2,500 people, but the ecosystem—dealers, transporters, contract workers—supports tens of thousands of livelihoods. Yet these aren't always quality jobs. Contract workers lack job security, transporters face payment delays, and dealer margins are thin. The social impact is real but uneven.

The gender dimension deserves attention. Buildings are allotted to FACT Women's Welfare Organisation at concessional rate for running Women's hostel/Creche. A Complaints Committee is functioning to look into complaints of sexual harassment to women employees at work place under the Sexual Harassment of Women at Workplace (Prevention, Prohibition & Redressal) Act, 2013. Not less than half of the members are women including an external member who is a lady Professor of a reputed Social Work College. These initiatives, while important, highlight how far industrial India still has to go on gender equity.

The relationship with local communities is multifaceted. FACT township in Udyogamandal created a middle-class ecosystem—schools, hospitals, cultural centers—that elevated the region's social infrastructure. FACT English Medium School educated generations of children. FACT hospital provided healthcare when private options were scarce. These institutions created social capital beyond economic value.

Yet there's also resentment. Local communities bear the environmental burden of industrial operations while benefits often flow elsewhere. Job opportunities increasingly require technical skills that local youth lack. The prosperity FACT brought is visible but not always accessible to original inhabitants. This tension between industrial development and community welfare remains unresolved.

The knowledge transfer impact is perhaps most significant. FACT Engineering & Design Organisation (FEDO) and FACT Engineering Works (FEW) trained hundreds of engineers who went on to build India's chemical industry. The technical expertise developed at FACT seeded fertilizer plants across India. This human capital development—hard to quantify but enormously valuable—might be FACT's greatest contribution to nation-building.

During recent disasters—floods, cyclones, pandemic—FACT has consistently stepped up. Beyond mandatory CSR spending, there's genuine institutional commitment to Kerala's welfare. Employees voluntarily contribute to relief funds, company infrastructure supports disaster response, and technical expertise assists recovery efforts. This reciprocal relationship between FACT and Kerala transcends commercial transactions.

The organic farming initiatives represent an interesting evolution. PDM is suitable for all crops, all soils and all seasons. It is also good for drought resistant crops. PDM is the best suitable manure for Organic farming. The company that epitomized chemical agriculture is now promoting organic alternatives—responding to changing consumer preferences and environmental consciousness.

Yet contradictions remain. FACT's core business—chemical fertilizers—contributes to soil degradation, water pollution, and greenhouse gas emissions. The CSR initiatives, however well-intentioned, can't fully offset these environmental impacts. The company faces an existential question: Can a chemical fertilizer company ever be truly sustainable?

The social license to operate, earned over eight decades, provides FACT with resilience that financial metrics don't capture. When privatization is proposed, communities resist. When plants face closure, political pressure ensures continuation. This social capital—intangible but real—might be FACT's most valuable asset.

Looking ahead, FACT's social role will likely evolve. Climate change demands agricultural transformation. Food security requires sustainable intensification. Rural development needs inclusive growth. Whether FACT can adapt its social mission to these challenges while maintaining commercial viability remains an open question. The company that helped feed independent India must now help create sustainable food systems for the climate era.

XI. Playbook: Lessons from a PSU Success Story

The FACT story offers a masterclass in navigating the unique challenges of building and sustaining industrial capacity in a developing economy. Eight decades of operations, spanning colonial ambition to socialist planning to market liberalization, provide insights relevant beyond fertilizers or even PSUs.

Building Industrial Capacity in a Developing Economy

The first lesson is about timing and vision. The Maharajah of Travancore didn't wait for independence or industrial infrastructure or technical expertise. He started with what he had—wood from Kerala's forests—and figured out the rest. This "start before you're ready" approach, antithetical to modern planning paradigms, enabled India to have fertilizer production capacity precisely when the new nation needed it most.

The progression from wood gasification to naphtha reforming to RLNG illustrates adaptive evolution. FACT didn't leap directly to global best practices but climbed the technology ladder rung by rung. Each transition—painful and expensive—built capabilities for the next. This gradualism, often criticized as inefficient, created indigenous expertise that technology transfer alone couldn't provide.

Managing Political and Commercial Objectives

FACT's perpetual balancing act between public service and profitability offers lessons in stakeholder management. The company learned to speak multiple languages fluently: socialist planning to secure capital, commercial metrics to justify operations, social development to maintain legitimacy. This multilingual capability—articulating value in terms each stakeholder understands—is crucial for institutions serving multiple masters.

The M.K.K. Nair era demonstrated that PSU leadership requires different skills than private sector management. Success came not from fighting the system but from working within it—using Five-Year Plan vocabulary to secure expansions, leveraging socialist ideals to motivate workers, deploying bureaucratic processes to achieve commercial ends. The best PSU leaders are translators, converting political mandates into operational reality.

Surviving Economic Liberalization as a PSU

FACT's survival through 1991's economic liberalization, when many PSUs collapsed, reveals important strategies. First, the company had diversified beyond pure commodity production—FEDO's consultancy services and specialized fertilizer grades provided differentiation. Second, regional dominance in Kerala created a political constituency for continuation. Third, operational improvements—even if insufficient by private sector standards—demonstrated viability.

The caprolactam venture, while financially challenging, provided unexpected benefits. It forced FACT to develop marketing capabilities, quality systems, and customer orientation—skills absent in the allocation economy. Failed diversification became capability building. This suggests that strategic mistakes, if survived, can strengthen organizations in unexpected ways.

Technology Absorption and Indigenous Capability Building

FACT's approach to technology provides a template for industrial development. Rather than remaining dependent on technology suppliers, the company systematically built indigenous capabilities. FEDO didn't just implement technologies but understood, adapted, and improved them. FEW didn't just operate imported equipment but learned to fabricate it.

This absorption model—starting with operations, moving to maintenance, then modification, and finally innovation—created genuine technological sovereignty. The engineers who cut their teeth at FACT went on to design plants across India. Knowledge spillovers from PSUs, often ignored in privatization debates, represent enormous social returns on public investment.

Diversification vs. Focus in Commodity Businesses

FACT's diversification journey offers nuanced lessons. The move into engineering services (FEDO) leveraged existing capabilities and created value. The petrochemical venture stretched capabilities too far and destroyed value. The difference? Adjacency. FEDO was a natural extension of engineering expertise; caprolactam was a leap into unfamiliar territory.

For commodity businesses facing margin pressure, the temptation to diversify is strong. FACT's experience suggests a framework: Diversify into services that leverage operational expertise (like FEDO), be cautious about upstream/downstream integration (like caprolactam), and maintain focus on core operations even while exploring adjacencies.

The Role of Patient Capital in Nation-Building

FACT's history vindicates patient capital. The company took 15 years from incorporation to profitability, another decade to achieve scale, and several more to become strategically important. Private capital, demanding quicker returns, might have abandoned the venture. Government ownership, despite its inefficiencies, provided runway for capability building.

This has implications for contemporary industrial policy. Complex industries—semiconductors, renewable energy, biotechnology—require patient capital that can survive J-curves. While private equity and venture capital serve important roles, strategic industries might need public investment willing to accept longer gestation periods and lower returns for strategic benefits.

Creating Ecosystem Effects

FACT's impact extended far beyond fertilizer production. The company created Kerala's chemical engineering ecosystem—training engineers, developing suppliers, establishing quality standards. The township model, while paternalistic, created social infrastructure that attracted talent and enabled industrial development.

Modern industrial policy often focuses on individual firm competitiveness, missing ecosystem effects. FACT's experience suggests that public investment should be evaluated not just on direct returns but on spillovers—human capital development, supplier capability building, infrastructure creation—that enable broader industrial development.

Navigating Subsidy Regimes

FACT's relationship with fertilizer subsidies illustrates both opportunities and challenges of operating in regulated markets. The company learned to optimize within constraints—timing production to subsidy cycles, managing working capital despite payment delays, maintaining supply despite commercial pressures.

The key insight: In heavily regulated industries, operational excellence matters less than regulatory navigation. FACT survived not by being the most efficient producer but by being the most reliable supplier to government programs. This suggests that firms in regulated industries need different capabilities than those in free markets.

Balancing Efficiency and Employment

FACT's overstaffing, relative to private competitors, represents a conscious choice: trading efficiency for employment. This isn't necessarily irrational. In developing economies with surplus labor and scarce capital, labor-intensive production might be socially optimal even if privately inefficient.

The lesson isn't that overstaffing is good but that evaluation metrics matter. If PSUs are judged solely on commercial returns, they'll always appear inefficient. If evaluated on employment generation, skill development, and regional development, the calculus changes. The challenge is developing metrics that capture total social returns, not just financial returns.

Managing Technological Transitions

FACT's multiple technological transitions—wood to naphtha, naphtha to RLNG—provide a template for managing disruption. Each transition was preceded by parallel running (maintaining old technology while building new), followed by gradual switchover, with careful attention to workforce retraining. The company never attempted dramatic overnight transformations but evolved incrementally.

This evolutionary approach, while slower, proved more sustainable. Workers had time to adapt, operations continued during transitions, and learning from each phase informed the next. In an era of rapid technological change, FACT's measured approach to transformation offers an alternative to Silicon Valley's "move fast and break things" philosophy.

Building Social License

FACT's deep roots in Kerala society—through employment, CSR, and regional identity—created resilience beyond financial metrics. When privatization threatened, communities mobilized. When competition intensified, regional preference provided protection. This social license, earned over decades, proved more valuable than physical assets.

The playbook lesson: Industrial enterprises, especially in democratic societies, need social legitimacy beyond legal compliance. This requires genuine community engagement, consistent social investment, and alignment with regional development goals. Social license can't be bought through CSR spending alone but must be earned through sustained commitment.

The FACT playbook ultimately teaches that industrial development in emerging economies requires different strategies than textbook capitalism suggests. Patient capital, capability building, ecosystem development, and social legitimacy matter as much as operational efficiency. The company that began as a princely experiment became a template for industrial development in democratic, developing nations—imperfect but instructive, challenged but resilient.

XII. Bear vs. Bull Case Analysis

Bull Case: The Hidden Value Thesis

Agricultural Importance and Food Security Imperative

India's food security challenge isn't diminishing—it's intensifying. With population expected to peak at 1.7 billion by 2050 and climate change threatening agricultural productivity, fertilizer demand will only grow. FACT, as India's first fertilizer company with deep agricultural relationships, occupies a strategic position that transcends quarterly earnings. The government cannot allow FACT to fail; it's not just a company but infrastructure for food security.

The global fertilizer market context strengthens this thesis. The volume of the fertilizer market is estimated at $381.7 billion in 2024. It is projected to reach $541.2 billion by 2030, with an average annual growth rate of 5.99% in 2024-2030. Between 2024 and 2028, potash consumption is projected to increase by 10%, compared with 8% for phosphorus and 6% for nitrogen. FACT's integrated production capabilities across nitrogen and phosphorus position it well for this growth.

Government Backing and Strategic Sector Status

The 90% government ownership, often seen as a liability, provides unparalleled stability. Unlike private players who might exit during downturns, FACT has an implicit sovereign guarantee. The recent operational turnaround demonstrates that when government focus aligns with management execution, PSUs can deliver. The new capacity additions and RLNG conversion show continued government commitment to FACT's modernization.

The fertilizer subsidy regime, while complex, provides predictable revenue streams. Private players face margin volatility; FACT has government backstop. In any crisis—financial, supply chain, geopolitical—FACT will receive preferential treatment. This "too strategic to fail" status has option value not reflected in current valuations.

Asset Base and Replacement Value

FACT's physical assets—land in prime Kerala locations, production facilities, distribution infrastructure—have replacement values far exceeding book value. The Udyogamandal and Cochin Division plots alone, in today's real estate market, could be worth thousands of crores. The production facilities, if built today, would cost multiples of their carrying value.

The intangible assets are equally valuable. FACT's brand, built over 80 years, has immense recall value among farmers. The dealer network of 5,935 outlets would take decades to replicate. The technical expertise in tropical agriculture and customized fertilizer formulations represents irreplaceable intellectual property. These assets don't appear on balance sheets but have substantial strategic value.

Regional Monopoly in Kerala

FACT's dominance in Kerala—supplying majority of the state's fertilizer needs—creates a moat that new entrants can't easily breach. Kerala's unique geography, with its fragmented land holdings and diverse cropping patterns, requires localized knowledge that FACT has accumulated over decades. The logistics of serving Kerala's remote areas, the relationships with thousands of small dealers, the understanding of local soil conditions—these create barriers beyond mere production capacity.

The political economy reinforces this monopoly. Any attempt to displace FACT would face fierce resistance from farmers, dealers, employees, and politicians. The social license FACT has earned provides protection that regulatory licenses alone cannot. This regional fortress, while limiting growth, ensures survival and steady returns.

Potential for Operational Improvements

FACT's current inefficiencies paradoxically represent opportunity. With employee productivity at 50-60% of private sector benchmarks, even modest improvements would dramatically impact profitability. The ongoing capacity expansion, when complete, will improve fixed cost absorption. Modern digital tools could optimize distribution, reduce working capital, and improve customer service.

The RLNG conversion has already demonstrated operational improvement potential. Similar upgrades across the production chain—energy efficiency, waste reduction, automation—could transform economics. FACT doesn't need to match private sector efficiency; even reaching 70-80% would justify significantly higher valuations.

Bear Case: The Structural Decline Thesis

Subsidy Dependence and Policy Risk

FACT's fundamental business model depends entirely on government subsidies. Without subsidies, the company would be deeply unprofitable. This isn't a temporary support but structural dependence. Any change in subsidy policy—reduction in rates, delays in payments, shift to direct benefit transfers—could devastate FACT's economics.

The policy risk is real and growing. India's fiscal situation, with high debt-to-GDP ratios and competing development priorities, makes fertilizer subsidies increasingly unsustainable. International pressure on agricultural subsidies, WTO obligations, and environmental concerns about chemical fertilizer overuse all point toward policy shifts that would hurt FACT disproportionately.

Import Parity Pricing Pressures

Global fertilizer markets have structural advantages FACT can't match. Middle Eastern producers have access to cheap natural gas, Chinese producers benefit from scale and subsidies, Russian producers have integrated raw material access. FACT, importing RLNG at international prices and operating subscale plants, faces permanent cost disadvantages.

Import liberalization is gradually eroding FACT's protection. As India signs more trade agreements and reduces import duties, cheaper international fertilizers will flood the market. FACT's high-cost production will become increasingly unviable. The company is essentially a high-cost producer in a commodity market—a recipe for value destruction.

Competition from Efficient Private Players

Private sector competitors are widening the efficiency gap. Companies like Coromandel International operate with half the employees, newer technology, and market-driven decision-making. They're expanding aggressively, building world-scale plants, and capturing market share. FACT's PSU constraints—inability to close inefficient units, reduce workforce, or exit unprofitable segments—make it uncompetitive.

The talent drain accelerates this divergence. FACT struggles to attract quality engineers and managers who prefer private sector opportunities. The aging workforce, averaging 45+ years, lacks skills for modern manufacturing. Meanwhile, competitors hire the best talent, deploy cutting-edge technology, and continuously improve operations. This capability gap will only widen.

High Valuations and Limited Growth Prospects

Current valuations imply growth and margins FACT cannot deliver. With a PB ratio of 46x, the market is pricing in either hidden assets or explosive growth—neither of which exists. The capacity expansion, while significant, only adds 5.45 lakh MT to a base of over 8 lakh MT—less than 70% growth that won't transform economics.

The growth constraints are structural. Kerala's fertilizer market is mature with limited expansion potential. Expanding beyond Kerala means competing with entrenched players in their home markets. International expansion is impossible given cost disadvantages. FACT is essentially a single-state player in a slow-growth market—hardly justifying premium valuations.

Environmental and Regulatory Challenges

Chemical fertilizers face increasing environmental scrutiny. Soil degradation, water pollution, greenhouse gas emissions—fertilizers contribute to multiple environmental crises. Regulations are tightening globally, with Europe considering fertilizer taxes and China restricting production. India will inevitably follow, impacting FACT's core business.

The transition to sustainable agriculture threatens FACT's existence. Organic farming, precision agriculture, and biological inputs reduce chemical fertilizer dependence. While FACT has token organic initiatives, its core competence and assets are in chemical production. The company faces potential stranded assets as agriculture transforms.

The location challenges compound environmental issues. FACT's plants, surrounded by urban development, face constant pollution complaints. Expansion is impossible, efficiency improvements are constrained by layout, and any incident could trigger closure demands. The plants are essentially industrial anachronisms in increasingly residential areas.

The Verdict: A Speculation, Not an Investment

The bull and bear cases reveal a fundamental truth: FACT is no longer trading on fundamentals but on momentum and narrative. The bull case requires faith in government support, belief in hidden asset values, and hope for operational transformation. The bear case sees structural decline masked by temporary subsidies and irrational exuberance.

For fundamental investors, FACT at current valuations is uninvestable. The risks—policy changes, competition, environmental regulations—far outweigh potential returns. The company might survive, even thrive operationally, but shareholders could still lose money from multiple compression as reality reasserts itself.

For traders, FACT remains interesting. The tiny float, retail enthusiasm, and narrative power create volatility that traders can exploit. But this is speculation on crowd psychology, not investment in business value.

The tragedy is that FACT could be a decent investment at reasonable valuations. The operational improvements are real, the strategic position has value, and the regional dominance provides stability. At ₹200-300 per share, reflecting realistic earnings potential and asset values, FACT might offer acceptable risk-adjusted returns.

But at current levels, FACT embodies the excesses of retail speculation in Indian markets. It's become a symbol—of PSU resurgence, of Kerala pride, of retail investor empowerment—rather than a business. Symbols can be powerful, but they make poor investments.

XIII. Epilogue & Looking Forward