Exide Industries: The Lead-Acid King's Electric Pivot

I. Introduction & The "Battery" Hook

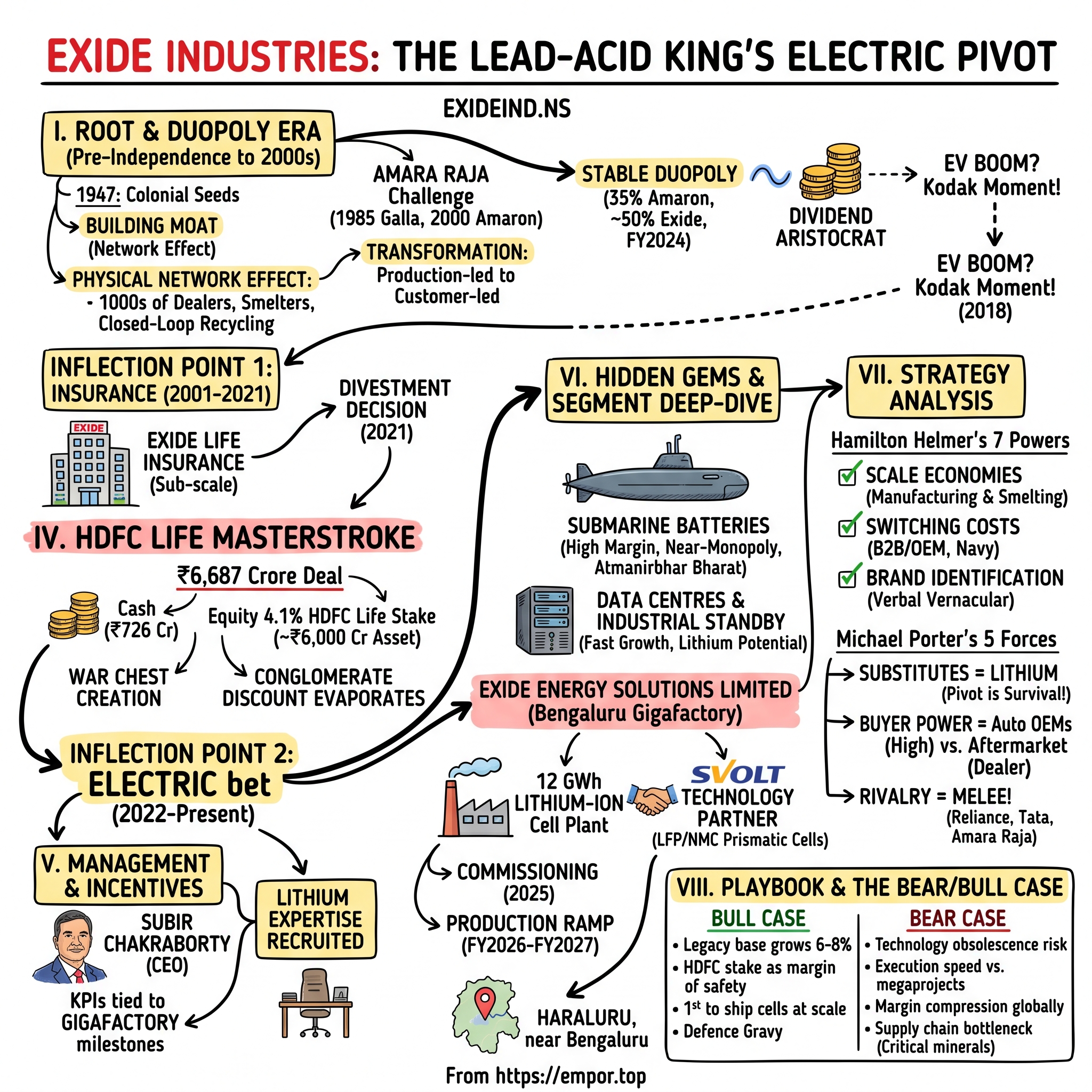

Picture a fluorescent-lit conference room in Kolkata in the autumn of 2021. The men around the table are not founders in hoodies. They are veterans of one of the oldest industrial companies in India, a firm that began life under British colonial rule before Independence, that powered the trucks of the Tata era, the Maruti hatchbacks of the Manmohan boom, and every Bajaj scooter your uncle ever owned. They are the custodians of एक्साइड Exide, a brand so culturally embedded in India that "Exide daalo" (put an Exide in it) is a verb in the country's auto-repair vernacular. And on this particular morning, they are signing a deal that would have seemed unthinkable to their predecessors. They are selling their entire life insurance subsidiary, a business they had nurtured for over two decades, to एचडीएफसी लाइफ HDFC Life Insurance for ₹6,687 crore — roughly $900 million in cash and stock.[^1][^2]

Why? Because the lunch was about to be eaten.

For more than a century, the lead-acid battery has been the unsexy, indispensable workhorse of every internal combustion vehicle on earth. It is the brick under your bonnet that fires the starter motor. It is also, increasingly, an endangered species. Every Tesla, every 比亚迪 BYD Dolphin, every Tata Nexon EV, every Ola electric scooter rolling off the assembly line replaces that lead-acid brick with a lithium-ion pack. And Exide, the dominant supplier of those lead-acid bricks to the Indian automotive industry, was staring at the slow-motion equivalent of a Kodak moment.

So they did something almost unheard of for an old-school Indian industrial. They bet the farm. They liquidated a non-core financial services subsidiary, set up a fully owned arm called Exide Energy Solutions Limited, broke ground on a 12 GWh lithium-ion cell manufacturing plant outside Bengaluru, and signed a technology licensing agreement with 蜂巢能源 SVOLT Energy Technology, the battery spin-off of 长城汽车 Great Wall Motor.1

That is the thesis of this story. Exide is not just another Indian industrial trading at a P/E of 30. Exide is a "Dividend Aristocrat" that looked in the mirror, recognised that its core product had a finite lifespan in the most important automotive market in the world, and pre-emptively decided to disrupt itself before someone else did. Whether they succeed or fail will determine whether this 100-year-old company survives the next 30.

Over the next three hours, we are going to trace that arc. We will start in colonial Calcutta with a British electrical storage company that became the seed of a national champion. We will visit the battery wars of the 1990s, when an upstart from Tirupati named अमरा राजा Amara Raja nearly upended Exide's monopoly with a brand called Amaron and a clever radio jingle. We will dissect the most consequential capital allocation decision in the company's modern history — the HDFC Life divestment — and we will walk the floor of the Bengaluru Gigafactory that this divestment funded. We will meet the engineer who runs the place, Subir Chakraborty, a man who joined Exide as a young salesman in 1985 and is now charged with reinventing it. And we will end with a hard look at the bull and bear cases, because the question of whether Exide can pivot from a lead chemistry it has mastered for a century to a lithium chemistry it has barely begun to ship is, to put it mildly, not yet settled.

This is the story of how a "boring" commodity business is executing one of the most sophisticated capital allocation pivots in Indian corporate history. Whether it works is the open question. Let us begin where every good Indian industrial story begins — with the British.

II. Roots & The Duopoly Era

The year is 1947. India is being born, painfully, in a cloud of partition violence and political compromise. In Calcutta, the commercial capital of the dying Raj, a quietly profitable subsidiary of the British firm Chloride Electrical Storage Company is going about its business — assembling lead-acid batteries imported from Manchester, distributing them through a network of agents serving the railways, the postal service, and the still-tiny Indian motor industry. Most British firms were preparing to leave. Chloride decided to stay, naturalise, and grow with the new republic. The Indian arm would become एक्साइड इंडस्ट्रीज़ लिमिटेड Exide Industries Limited, and over the next thirty years it would do what every monopolist does when it has time and political cover — it built distribution.2

By the early 1970s, Exide had the kind of moat that economists at Harvard Business School would later call a "physical network effect." Across India's sprawling geography — from the rust-belt of the Punjab to the truck routes of Bihar to the betel-leaf-stained workshops of Tamil Nadu — Exide had thousands of dealers, sub-dealers, mechanics, and किराना kirana shopkeepers who stocked their batteries. The product was identical from one brand to the next. What was not identical was the cost of getting it to a remote village in Madhya Pradesh on the day a tractor battery failed during harvest. Exide had figured that out. The Indian truck operator did not buy a battery; he bought availability. And nobody had availability like Exide.

This was the Hamilton Helmer 7 Powers framework playing out before Hamilton Helmer wrote the book. Scale economies in distribution, brand identification in a product category where the buyer cannot tell two batteries apart, and what we would now call a cornered resource — the lead recycling supply chain. Lead-acid batteries are one of the most recycled products on the planet, with closed-loop economics that approach 99% recovery of the lead.3 Exide ran its own smelters. It bought back dead batteries from its own dealers. It refined the lead and put it back into new batteries. A competitor entering the Indian market would have to build a battery factory, a smelter, a reverse-logistics network, and a dealer base — all simultaneously, all subject to India's notoriously difficult environmental permits for lead handling, and all while Exide cut prices to bleed them out.

For decades, no one tried. And then in 1985, a US-returned engineer from a small town in Andhra Pradesh named रामचंद्र नायडू Ramachandra Galla did. He set up Amara Raja Batteries Limited in तिरुपति Tirupati, initially with the modest ambition of supplying industrial standby batteries to telephone exchanges. The Indian government was just beginning to liberalise. Telecom was about to explode. And Amara Raja, in partnership with the American battery giant Johnson Controls, had a technical edge — they were making maintenance-free, valve-regulated lead-acid batteries (VRLA) when Exide was still selling the old "topping-up-with-distilled-water" variety.

Then in 2000, Amara Raja launched a consumer brand called Amaron, with a now-legendary tagline — "Last Lonnng. Really Lonnng." The radio jingles, the bright yellow casings, the warranty card claims of zero-maintenance batteries. For the first time in fifty years, an Indian consumer walking into a car battery shop had a real choice. Suddenly the mechanic was getting trade margin pitches from two suppliers, not one. By the late 2000s, Amara Raja had taken the number two position in Indian organised batteries, with market share estimates in the 30-35% range for the automotive aftermarket.[^6]

For Exide, this was a near-death experience disguised as a market share inconvenience. The Galla family had broken the monopoly. And in doing so, they forced Exide to do something painful and overdue — to transform itself from what insiders called a "production-led" company (we make what we make and dealers sell it) to a "customer-led" company. They had to invest in new R&D. They had to improve product quality. They had to launch sub-brands for two-wheelers, three-wheelers, inverters, and home UPS systems. They had to actually market the brand, which they had never really done. They had to professionalise.

The duopoly that emerged out of this decade-long war became one of the most stable competitive structures in Indian industrials. Exide retained around half of the organised lead-acid battery market by FY2024, Amara Raja held the other meaningful chunk, and a long tail of regional players competed for scraps in the unorganised aftermarket.4 The market itself was growing comfortably, propelled by Indian auto sales doubling roughly every decade and by the explosion of inverter batteries during years of power outages in tier-two cities. Margins were healthy. Capex needs were modest because both incumbents had already built their plants. Cash was returned to shareholders. Exide had become, by the mid-2010s, what investors call a "Dividend Aristocrat" — a slow-growing, cash-generative, fundamentally boring business that paid out reliably.

Boring is wonderful right up until the moment it is not. And by 2018, the rumblings of an existential threat — the electric vehicle — were no longer rumblings. They were a tsunami. The lead-acid king had to decide what kind of company it wanted to be when the cars no longer needed his product.

III. Inflection Point 1: The Insurance Diversification

To understand Exide's pivot in the 2020s, you have to first understand a decision they made in the early 2000s that looked, at the time, like an extremely fashionable mistake. They got into life insurance.

It was the year 2000. The Indian government had just opened the insurance sector to private players for the first time since nationalisation in 1956. The narrative of the moment in Mumbai's corner offices was simple — India was a vast, under-penetrated insurance market. Less than three percent of GDP was being saved through life insurance. The Indian middle class was about to mint itself. And whoever could combine an Indian distribution network with a foreign insurance partner's technical know-how would print money for a generation. ICICI Bank teamed up with Prudential. HDFC teamed up with Standard Life. SBI Life. Birla Sun Life. Tata AIG. Reliance. Every big Indian name with a balance sheet found themselves a foreign dance partner.

Exide, perhaps unwilling to be left at the wall, joined the dance. In 2001 they took a stake in what was then called ING Vysya Life Insurance. Over the subsequent decade and a half, Exide steadily increased its holding, and by 2014 they bought out their foreign partner entirely. The company was renamed Exide Life Insurance Company Limited. For the first time in its corporate history, Exide had become a conglomerate — a battery company that also sold endowment policies.5

The strategic rationale, on paper, was not insane. Exide was generating significant cash from its core lead-acid business. The Indian insurance industry was promising 15-20% compounded annual growth. The dealer network that sold batteries could theoretically cross-sell insurance to its customers. And insurance is a beautiful business when it works — the policyholder pays premiums today, the insurer invests the float for decades, and over time the compounding produces a financial juggernaut. Look at what Warren Buffett did with GEICO. Look at what the HDFC group was building.

The trouble was that Exide Life never became HDFC Life. It remained sub-scale, with embedded value growth in the single digits and a reputation for being neither a fast-growing private insurer nor a high-margin niche player. By the mid-2010s, the Indian listed-equity investor base — increasingly dominated by domestic mutual funds and foreign portfolio investors who liked clean, focused businesses — was openly frustrated. Why was a battery company, with a relatively easy-to-model auto-replacement cycle and a clean dividend stream, also running a complicated insurance balance sheet that required actuarial assumptions and embedded value calculations to value? The market did what markets do in such situations. It applied a conglomerate discount.

Analysts began publishing "sum of the parts" notes that valued the battery business at one multiple and the insurance subsidiary at a separate, often lower, multiple. The implicit message was that Exide's stock was worth more broken up than it was held together. Promoter family members and the board began to discuss whether the insurance subsidiary was a strategic asset or, in the polite language of capital markets, an "optionality" — a fancy word for "we are not sure what to do with this."

What changed everything was not insurance industry economics. It was what was happening under the bonnet, literally. The first electric two-wheelers were rolling out in India. The first electric buses were appearing in Delhi tenders. Tata Motors had announced the Nexon EV. The Indian government was signalling — through फेम India FAME India subsidies and aspirational targets — that the country was going to electrify, even if nobody was sure how quickly.

The Exide board, by 2020, had a question on its hands. Sit on the insurance subsidiary indefinitely and trade at a conglomerate discount? Or monetise it and redeploy the cash into the most expensive industrial bet the company had ever made — building a lithium-ion cell factory from scratch?

To their great credit, they chose the latter. And the buyer they found turned out to be exactly the company that the market had always wanted Exide Life to be — एचडीएफसी लाइफ HDFC Life Insurance. The narrative was about to undergo the most violent inversion in Exide's corporate history.

IV. Inflection Point 2: The HDFC Life Masterstroke

To appreciate just how clever the HDFC Life deal was, you have to understand what HDFC Life is. It is the crown jewel of Indian private life insurance — a joint venture originally between एचडीएफसी HDFC and the UK's Standard Life Aberdeen, listed on Indian stock exchanges since 2017, consistently the most profitable and best-managed of the private players, with the highest persistency ratios, the lowest claim repudiation rates, and the strongest VNB (Value of New Business) margins in the industry.6 In Indian financial services, HDFC Life is what 贵州茅台 Kweichow Moutai is in Chinese spirits — the gold standard.

What Exide Life was, in contrast, was a respectable but middle-of-the-pack private insurer with around 1% market share, modest growth, and the eternal challenge of distribution. The two companies were not equals. They were not even in the same weight class.

And yet, on the 18th of June 2021, Exide Industries announced a deal under which HDFC Life would acquire 100% of Exide Life Insurance Company for a total consideration of ₹6,687 crore — paid through a combination of cash (around ₹726 crore) and HDFC Life equity shares (8.7 crore newly issued shares).[^1] The transaction closed on the 1st of January 2022 after receiving the requisite regulatory approvals from IRDAI Insurance Regulatory and Development Authority of India, the सेबी SEBI Securities and Exchange Board of India, and the Competition Commission.[^2] As a result of the share-swap component of the deal, Exide Industries ended up owning approximately 4.1% of HDFC Life — a stake worth, at the time of closing, roughly ₹6,000 crore on the public market.

Let us sit with what just happened. Exide had taken a sub-scale, slow-growing insurance subsidiary that was depressing its own multiple, and traded it for a chunk of the best-in-class listed insurance company in the country. They had gone, in one transaction, from being a battery company with a problematic insurance arm to being a battery company with a passive, liquid, market-quoted financial asset worth roughly the equivalent of a billion dollars. The conglomerate discount evaporated. The insurance complexity was outsourced to HDFC Life's management. The cash and the listed-stock asset became, in effect, a war chest.

And here is the kicker — Exide Industries did not have to do anything with that stake. They could hold it forever. They could pledge it for debt. They could sell it down piece by piece over the next decade to fund the Gigafactory's expansion. They could distribute it as a special dividend to shareholders. Or they could simply mark it to market and let the value compound alongside HDFC Life's own growth. Whatever route they chose, the optionality was now sitting cleanly on the balance sheet as a liquid security, not as a stranded insurance subsidiary with restricted regulatory capital.

For long-time observers of Indian corporate history, this was the most elegantly executed corporate restructuring in the industrial sector since at least the demerger of Reliance Industries by the Ambani brothers. It was clean. It was tax-efficient (the share-swap structure deferred capital gains for shareholders). It was strategically congruent — HDFC Life got the agency distribution and rural reach of Exide Life, Exide Industries got a treasury asset. And critically, it created the financial capacity for what was coming next.

Because in May 2022, just months after the deal closed, Exide announced the formation of a wholly owned subsidiary called Exide Energy Solutions Limited, headquartered in Bengaluru, with a mandate to set up a 12 GWh lithium-ion cell manufacturing facility — the largest such facility, on paper at least, in India.17 The estimated capex was around ₹6,000 crore for the first phase, with potential further expansion phases that could bring the total investment north of ₹12,000 crore.

Coincidence on the dollar amounts? Not really. The financial planning was almost surgical. The HDFC Life stake gave Exide Industries the option to fund its lithium build-out either by drawing down the stake, by borrowing against it, or by simply using the implicit credit support it provided to the parent's balance sheet — without forcing the company to dilute its own shareholders or take on debt at unattractive levels. The insurance divestment was not a retreat from financial services. It was a war chest creation operation disguised as a strategic refocus. And the war it was funding was the existential one.

V. Current Management & Incentive Structures

Walk into Exide's corporate headquarters at 59E Chowringhee Road in Kolkata and you are struck by how unflashy it all is. The lobby has the same slightly worn marble floor and oversized portraits of past chairmen that you would find in any old Marwari or Bengali industrial house in eastern India. There is no Bezos-era open-floor plan. There are no glass-walled war rooms. The boardroom looks exactly like a 1990s law firm. This is the natural habitat of सुबीर चक्रवर्ती Subir Chakraborty, Exide's Managing Director and Chief Executive Officer.[^11]

Chakraborty is not the kind of CEO who appears on the cover of business magazines holding a battery cell aloft like a Wall Street trophy. He is a chemical engineer by training, an Exide lifer by tenure, and a man who has spent nearly four decades inside this company. He joined as a young sales engineer in the mid-1980s, when the duopoly with Amara Raja was still a decade away, when liberalisation was still seven years away, when Exide was a sleepy distribution machine. He worked his way through the industrial battery vertical, the after-market business, the automotive OEM business. He understood the dealer network, the smelting operations, the submarine contracts, the inverter market. He was made Managing Director in 2019 and CEO in 2022. By the time he was running the show, he had personally lived through nearly every major decision the company had made in the modern era.

This matters because the Exide pivot is not a Silicon Valley story. It is not a charismatic outsider hired by the board to disrupt the company from within. It is, instead, an institutional pivot — engineered by veterans who deeply understand the lead-acid base business and are now charged with adding a lithium-ion business on top of it without breaking the cash cow underneath. That is a fundamentally different and, in many ways, harder management challenge than just "burn the boats and become an EV company." Exide cannot afford to mismanage lead-acid while it builds lithium. The cash flows from lead are funding the lithium investment.

Chakraborty's style, according to people who have worked with him, is methodical to a fault. He runs operations reviews with the patience of an engineering manager, not the bravado of a celebrity CEO. He has been known to obsess over distribution metrics and warranty claim ratios at the same meeting where the team is discussing gigafactory equipment commissioning. This combination — patient incremental management of a legacy business plus capital-intensive moonshot management of a new business — is rare and quietly unfashionable. It is also exactly what Exide needs right now.

The other piece of the management puzzle is the promoter group. Exide is controlled by Chloride Eastern Industries Pte. Ltd. and related entities consolidated under the broader Chloride Strategic Systems family, which trace their lineage back to that original British colonial parent. Promoter holding has hovered in the high-40s percent range, with the balance held by domestic mutual funds, the Life Insurance Corporation of India, and foreign portfolio investors.8 LIC's holding has historically been substantial — Exide is one of those names that the institutional Indian buy-side treats as a proxy for the broader Indian mobility story. If you believe Indian auto sales will compound for the next twenty years, you tend to own Exide.

The interesting question for governance watchers is how performance incentives have been restructured around the Gigafactory milestones. Management's variable compensation, according to disclosures in the annual report, includes specific KPIs tied to Exide Energy Solutions' commissioning schedule, cell yield ramp, and customer order book.9 This is meaningful because it aligns the legacy lead-acid management team with the success of a business that, in the short term, will dilute consolidated margins, consume capex, and frustrate quarterly earnings expectations. Without that alignment, the natural temptation would be to milk lead-acid and starve lithium.

There has also been a deliberate effort to recruit lithium-ion expertise from outside. Exide Energy Solutions has hired engineers from Korean and Chinese cell makers, including individuals with deep experience at LG에너지솔루션 LG Energy Solution, Samsung SDI, and 宁德时代 CATL-adjacent operations. This is the part of the operation that does not look like 59E Chowringhee Road. Walk into the Bengaluru office of Exide Energy Solutions and you find a much younger, more international team — multiple nationalities, simulation software running on engineering workstations, prototype cells being cycled in environmental chambers. It is not Tesla. But it is also not your father's Exide.

The strategic question for the next five years is whether the Kolkata board and the Bengaluru engineers will speak the same language. Whether Chakraborty can keep both halves of the company moving in formation. And whether the institutional shareholder base — patient by Indian standards but not infinitely so — will tolerate the depressed near-term margins that any capex-heavy industrial transformation produces.

VI. Hidden Gems & Segment Deep-Dive

Most stock pitches on Exide focus on the obvious — automotive batteries, the EV pivot, the dealer network. But Exide is one of those Indian industrial conglomerates where the most interesting margin pockets are tucked away in segments that the sell-side cannot model cleanly. Three of these deserve their own treatment, because together they explain why Exide trades at a premium to a pure-play commodity peer and why the optionality on this name is more layered than it first appears.

The first is the submarine battery business. This is not a metaphor. Exide is, quite literally, the supplier of large-format lead-acid batteries to the Indian Navy's स्कॉर्पीन Scorpene-class submarines, the conventional diesel-electric attack submarines built at Mazagon Dock Shipbuilders Limited in Mumbai under licence from France's Naval Group.10 A modern conventional submarine runs on a massive bank of lead-acid cells when submerged — diesel engines charge the battery on the surface, and the boat then operates silently underwater on stored electrical energy. The batteries on a Scorpene weigh several hundred tonnes. They are bespoke, military-grade, with shock and vibration specifications that civilian batteries cannot meet. They require security clearances and supply chain audits that take years to acquire. And they are a near-monopoly business, because the Indian Navy is not going to qualify three suppliers when it has one trusted incumbent that has been making submarine batteries for decades.

The margins in this business are, by all accounts, several multiples of the standard automotive after-market. The volumes are small. But the contractual relationships are sticky in a way that no consumer business can match. And as India accelerates its naval modernisation under the indigenisation push — the so-called आत्मनिर्भर भारत Atmanirbhar Bharat Self-Reliant India initiative — the submarine programme is set to expand with additional Scorpene-class boats and potentially the larger Project 75I follow-on. Exide sits in the perfect position to capture every rupee of that battery spend. There is also a global angle. The submarine batteries that Exide makes are exportable to other navies in the Global South that operate similar conventional boats. It is the kind of business Buffett would call a "toll bridge" — small, beautiful, and almost impossible to compete away.

The second hidden segment is industrial standby and data centres. Every server rack in every data centre in India needs uninterruptible power supply, and behind every UPS sits a battery bank. Every telecom tower, every railway signalling station, every hospital emergency room, every airport ground operation — all of these run on industrial standby batteries. As India's digital economy explodes — the Reliance Jio-led mobile data revolution, the hyperscale data centres being built by Amazon Web Services, Microsoft Azure, Google Cloud, and the Indian players like Yotta and CtrlS — the demand for industrial-grade batteries is compounding at rates much faster than automotive. Exide has the established industrial dealer network and the manufacturing scale to capture this demand. And critically, the industrial customer is not as price-sensitive as the retail two-wheeler buyer; uptime is what they pay for, and Exide's track record on uptime is its principal competitive weapon.

This is also one of the segments where the lithium-ion transition is most interesting. For data centre applications, lithium-ion batteries are increasingly displacing lead-acid because of their smaller footprint, longer cycle life, and reduced cooling requirements. The same Exide Energy Solutions Gigafactory that makes EV cells can, with minimal modification, make stationary storage cells for industrial applications. The industrial vertical may turn out to be the bridge between the lead-acid past and the lithium-ion future — a place where Exide can deploy lithium product into existing customer relationships without needing to win new accounts.

The third, and most important, is the Lithium-ion Gigafactory itself — Exide Energy Solutions Limited. This is the bet that defines the next decade of the Exide story.

The plant is located at Haraluru, near Bengaluru, on a campus of around 80 acres.7 The first phase, with a designed capacity of 6 GWh, is intended to manufacture lithium iron phosphate (LFP) and nickel manganese cobalt (NMC) prismatic cells suitable for electric two-wheelers, electric three-wheelers, electric four-wheelers, and stationary storage. The eventual ambition, in phase two, is to take total capacity to 12 GWh.1 To put that in perspective, 12 GWh is roughly enough cell output to power one million electric cars or fifteen million electric two-wheelers per year, depending on pack sizes.

The technology partner is 蜂巢能源 SVOLT Energy Technology, a spin-off of 长城汽车 Great Wall Motor that was carved out as an independent cell manufacturer in 2018.[^15] SVOLT is best known for its work on cobalt-free NMx chemistry and its ambition to be one of the top-tier Chinese battery makers behind 宁德时代 CATL and 比亚迪 BYD. The partnership structure is a technology licensing arrangement — SVOLT provides the cell chemistry know-how, the process engineering, and the equipment specifications, while Exide builds, owns, and operates the plant in India. This is significant because it allows Exide to skip the multi-year cycle of in-house battery R&D and start with proven, already-commercialised chemistry. It also de-risks the technology bet, because SVOLT has skin in the game on making sure the Indian operation actually produces cells that work.

The benchmarking question is how this stacks up against the other Indian lithium-ion players. रिलायंस Reliance Industries has its own ambitious gigafactory plans under Reliance New Energy, targeting an even larger capacity at the Jamnagar complex.11 Amara Raja has announced its own gigafactory, in partnership with multiple technology providers, with a more modest initial capacity. Tata Group, through Agratas Energy Storage Solutions, has announced a 20 GWh plant in Sanand. And the Indian government's PLI Production-Linked Incentive scheme for advanced chemistry cells has earmarked subsidies for several of these players.12

Exide's strategic positioning is to be neither the largest nor the most diversified, but the first to actually ship cells at scale. The Bengaluru plant began commissioning activities in 2025, with commercial production ramping during the course of FY2026 and into FY2027 according to the company's investor updates.9 If Exide can be the first Indian manufacturer to deliver qualified automotive-grade lithium-ion cells to Indian OEMs at competitive cost, it will have the equivalent of a first-mover lock-in on a generation of EV programmes. If it cannot, Reliance and Tata's scale will likely overwhelm it.

The next two years are, in a very real sense, the most important two years in Exide's corporate history since Independence.

VII. The Strategy Analysis

Step back from the operational details and apply the frameworks that strategy professors love. Two are particularly useful for Exide — Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces. Together they explain why Exide has been a quietly dominant business for seventy-five years and why the next decade is going to be the hardest test of that dominance the company has ever faced.

Begin with Hamilton's 7 Powers. The first power, scale economies, is where Exide has historically been bulletproof. Lead-acid battery manufacturing has classic economies of scale — fixed costs in plant capacity, smelting, and distribution networks divided over high volume create a per-unit cost advantage that smaller competitors cannot match. Exide's manufacturing footprint across multiple plants in India is hard to replicate. Even Amara Raja, the only credible challenger of the modern era, took fifteen years and a strategic alliance with Johnson Controls to get to scale parity.

The second power, switching costs, applies most cleanly to Exide's B2B verticals. An automotive OEM that has qualified Exide as a Tier 1 supplier for original equipment batteries has invested years of vehicle testing, warranty calibration, and supply chain integration in that relationship. Swapping suppliers means re-validating the entire battery management interface on every vehicle programme. The Indian Navy is not going to switch its submarine battery supplier on a whim. A data centre operator is not going to risk uptime to save 5% on battery cost. Switching costs in Exide's industrial and OEM segments are genuinely high.

Brand identification is the third power, and this is where Exide enjoys what is arguably the strongest brand equity in any Indian industrial commodity category. Exide is to batteries what Xerox is to copiers — the generic name that the consumer reaches for. In tier-three Indian towns, a customer walks into a shop and asks for "an Exide" the same way they ask for "a Bisleri" instead of mineral water. This kind of cognitive monopoly is built over generations and is one of the most under-appreciated assets on Exide's balance sheet because it does not show up as an intangible.

The fourth power, cornered resource, is the lead recycling supply chain. India's regulatory regime around lead handling, smelting permits, and used-battery collection is notoriously difficult. Exide has decades of permits, environmental clearances, and physical recovery infrastructure that a new entrant simply cannot build in a reasonable time frame. Whoever owns the recycling loop owns the cost structure.

The remaining three powers — counter-positioning, network economies, and process power — apply less cleanly to the legacy business but become very interesting in the lithium-ion context. Counter-positioning is what the EV ecosystem is doing to Exide's lead-acid franchise. A new entrant building a lithium-only business does not have to worry about cannibalising a lead-acid book. Exide does. The classic incumbent's dilemma.

Now move to Porter's 5 Forces. The threat of new entrants in lead-acid is moderate but rising — capital requirements and regulatory hurdles keep it manageable, but Chinese imports and a few aggressive Indian regional players have nibbled at the unorganised aftermarket. In lithium-ion, the threat of new entrants is extreme. Reliance, Tata, Adani, Amara Raja, and a host of well-funded foreign players are all gunning for the same Indian EV demand pool. This is not an industry where Exide can rely on the historical moat.

The threat of substitutes is, candidly, the existential question for the lead-acid business. Lithium-ion is the substitute. Solid-state batteries and sodium-ion batteries, both in advanced R&D globally, could displace lithium-ion within a decade. The substitution risk is binary and historical — lead-acid will eventually be a niche chemistry confined to legacy ICE vehicles, industrial standby, and submarine applications. The pivot is not optional. It is survival.

The bargaining power of buyers varies dramatically by segment. Auto OEMs have enormous power — they squeeze battery suppliers on price annually, demand custom specifications, and play one supplier off another. Margins in the OEM segment are thin. In the after-market, where the consumer buys a replacement battery through a dealer, the power dynamic is reversed. The consumer has limited price information, brand inertia is high, and the dealer captures the relationship. Margins in the after-market are roughly double what they are in the OEM channel.

The bargaining power of suppliers is moderate. Lead prices on the London Metal Exchange create input cost volatility. Exide hedges this partially through its own recycling operations, but a significant share of lead requirement is still purchased externally. For lithium-ion, the supply situation is much more precarious — lithium carbonate, nickel sulphate, and the entire upstream chemistry chain are dominated by Chinese, Chilean, and Australian players, and the geopolitics of these supply chains are not friendly. India's lack of domestic mining for critical battery minerals is a structural vulnerability that Exide cannot solve on its own.

The intensity of competitive rivalry is the final force, and it is where the picture is most dynamic. Lead-acid competition in India is essentially a stable two-horse race between Exide and Amara Raja. Lithium-ion competition is going to be a multi-player melee, and the winner is not yet visible. What Exide has that the new entrants do not is the lead-acid cash flow to subsidise the lithium build-out. What it does not have is the financial firepower of Reliance or the global supply chain reach of LG에너지솔루션 LG Energy Solution.

The strategic conclusion is that Exide is making a calculated bet that brand, distribution, and customer relationships from the lead-acid era can be partially carried into the lithium era. Whether that bet pays off depends entirely on execution at the Bengaluru gigafactory.

VIII. Playbook & The Bear/Bull Case

Every Acquired episode arrives, eventually, at the central question — would you own this business for the next ten years? For Exide, the answer requires holding two very different scenarios in your head simultaneously.

The bull case is straightforward in outline but powerful in compounding. Start with the legacy lead-acid business. Indian automotive sales are projected to keep growing through the 2030s, driven by rural penetration, two-wheeler demand, and the slow replacement of an aging on-road fleet. Even as EVs penetrate, lead-acid battery demand will not vanish — every ICE car needs one, every electric car still uses a 12-volt lead-acid auxiliary battery, every inverter needs one, every diesel generator needs one. The base business will likely grow at 6-8% annually for the foreseeable future, generating predictable cash flow.

Layer on top of that the optionality of the HDFC Life stake, which acts as a roughly one-billion-dollar liquid asset on the balance sheet — a margin of safety that gives Exide capital flexibility no Indian competitor enjoys. That stake also grows alongside HDFC Life's own embedded value, providing a quiet compounding tailwind to consolidated net asset value.

Then layer on Exide Energy Solutions. If — and it is a meaningful if — the Gigafactory commissions on time, achieves yield benchmarks comparable to global cell makers, and wins meaningful order book share from Indian OEMs, Exide will have transformed itself from a single-chemistry commodity manufacturer to a multi-chemistry energy storage company at the moment when the addressable market is exploding. The market for Indian EV batteries alone, by 2030, could exceed $20 billion annually. Capturing even a mid-teens share of that opportunity, while maintaining the existing lead-acid franchise and the submarine and industrial verticals, would compound shareholder value at rates well above the company's historical CAGR.

The submarine and defence vertical is gravy. As India's naval programme expands and as the Atmanirbhar Bharat policy framework pushes domestic content requirements higher, Exide is one of the rare private-sector companies positioned to capture defence spend without being either a politically sensitive aerospace contractor or a low-margin general engineering firm. It is a niche the market does not price into the consolidated multiple.

Now the bear case, which is equally serious and demands respect. Technology obsolescence is the central risk. Lithium-ion is not the final battery chemistry. Solid-state batteries, sodium-ion batteries, and chemistries we have not yet conceived will displace lithium-ion within a window that is not absurdly long. Toyota and Samsung SDI are investing billions in solid-state R&D. 中科海钠 HiNa Battery and other Chinese players are bringing sodium-ion to commercial scale for stationary storage and entry-level EVs. If Exide commits ₹12,000 crore of capex to a 12 GWh lithium-ion plant just as the industry begins migrating to a next-generation chemistry, the asset becomes stranded long before its depreciation cycle completes.

A second bear concern is execution speed. The "speed of software" that defines the EV era is not Exide's natural habitat. Exide is a methodical, incremental, engineering-driven company. The competitors it now faces — Reliance, Tata, Adani — are not just larger; they are also more aggressive in capital deployment, more practiced at executing megaprojects on accelerated timelines, and more politically connected. If Exide is six months late, it loses an OEM programme. If it is two years late, it loses a generation.

A third bear concern is margins. Lithium-ion cell manufacturing is a brutal margin business globally. Even 宁德时代 CATL, the world's largest battery maker, has seen gross margins compress under Chinese domestic price wars. Cell prices have fallen from over $150 per kWh five years ago to under $90 per kWh today, and the trajectory continues downward.[^18] If Exide is competing on global price points but with sub-scale Indian volumes, the margin profile may never approach what the lead-acid franchise generated.

A fourth concern is supply chain. India has almost no domestic lithium mining, no nickel refining at meaningful scale, and limited cathode and anode material production. Every gigafactory in India is, to varying degrees, dependent on Chinese supply chains for critical inputs. The geopolitical risk is real. A Galwan-style border incident or a sharper US-China decoupling could create input bottlenecks that no amount of operational excellence can solve.

The Hamilton 7 Powers reading on the EV transition is mixed. The brand power and distribution power that Exide has in lead-acid does not automatically transfer to lithium-ion. OEM customers buying battery packs for electric vehicles are not going to choose Exide because their grandfathers bought Exide tractor batteries; they will choose based on cell quality, pack engineering, and warranty terms. Switching costs, for an EV programme, are at least partially reset.

The honest investor's posture is to acknowledge that this is a binary bet within a non-binary business. The lead-acid franchise provides a floor. The lithium-ion bet provides the upside. The question is how much capital is at risk in the bet and how much downside is protected by the floor.

The KPIs to actually track over the next three years are deliberately few. The first is automotive after-market revenue growth — this is the proxy for the health of the lead-acid franchise and the operating leverage of the legacy distribution network. The second is the commissioning timeline and capacity utilisation of Exide Energy Solutions — this is the proxy for whether the lithium bet is on track. The third is the size and quality of the Exide Energy Solutions customer order book — specifically, whether Exide is winning Tier 1 supply commitments from Indian OEMs like Maruti Suzuki, Tata Motors, Mahindra, Hero MotoCorp, and Ola Electric. Those three KPIs, taken together, will tell you in real time whether the playbook is working.

The myth versus reality assessment cuts both ways. The consensus narrative on the street is that Exide is a "value trap" — a slow-growing legacy industrial that is unlikely to ever earn the multiple of a true tech name. The reality, when you look at the HDFC Life stake plus the submarine business plus the Gigafactory option, is that Exide is significantly more financially flexible and strategically optioned than the consensus suggests. The opposite consensus error is the breathless EV narrative that treats every Indian battery name as a Tesla in waiting. The reality is that Exide's lithium-ion business will likely produce its first material revenue contribution only in FY2027 or FY2028, and the path from there to category leadership is highly uncertain.

IX. Conclusion

There is something genuinely remarkable about a hundred-year-old company that looks at its own product, its own customers, and its own future and concludes — quietly, methodically, without fanfare — that the time has come to bet everything on a chemistry it has never sold at scale.

Most legacy industrials, when faced with this kind of moment, hedge. They run pilot programmes. They form joint ventures that produce press releases but not products. They write strategy decks about "exploring" new technology while the executives who built the legacy business quietly ensure that the legacy business gets the lion's share of capital. Eventually a disruptor arrives, the legacy business gets cannibalised, and the company spends a decade in slow decline being acquired piece by piece.

Exide is trying to do something different. The HDFC Life divestment was the cleanest statement of intent that any Indian industrial has made in a generation. It said — in financial terms, with hard rupees on the table — that the company is willing to monetise a non-core asset to fund a core transformation. The Bengaluru Gigafactory, the SVOLT partnership, the engineering hires from Korea and China, the restructured incentive compensation tied to lithium milestones — every one of these signals is consistent with a company that has decided to be different in the second century than it was in the first.

Whether they pull it off is, as we have argued throughout, a genuinely open question. The technological risks are real. The competitive landscape is fierce. The execution challenges are enormous. And the timing is uncomfortably tight — by the time the Bengaluru plant ships its first commercial cell, Tata's Agratas and Reliance's New Energy will likely already have product in the field.

But there is a version of the next ten years where Exide quietly becomes one of the more important industrial stories in the broader आत्मनिर्भर भारत Atmanirbhar Bharat Self-Reliant India narrative. A company that supplied the British Empire's railways, the post-Independence republic's first car factories, the liberalisation-era automotive boom, the digital-era data centres, and now the electric era's transport revolution. Few corporate histories span that kind of arc. Most companies are lucky to navigate one such transition. Exide is attempting its fourth or fifth.

The lead-acid king is not, after all, content to be remembered as a king of the past. Whether it earns its place as a king of the future will depend on the cells that come out of Haraluru, the orders that come in from Mumbai and Pune and Chennai, the discipline with which the cash from Kolkata is deployed in Bengaluru, and the patience of an institutional shareholder base that has watched this management team execute for the better part of two decades.

The story is not yet written. It is being written. And for long-term fundamental investors, that is precisely what makes it interesting.

References

References

-

Why Exide is betting big on Lithium-ion Gigafactory — Business Standard, 2023-11-15 ↩↩↩

-

Investor Relations & Annual Reports — Exide Industries Limited ↩

-

Quarterly Earnings Presentation Q4 FY24 — Exide Industries Limited ↩

-

Investor Relations & Annual Reports — Exide Industries Limited ↩

-

Exide Energy Solutions Limited & SVOLT Partnership Announcement — Exide IR ↩↩

-

Quarterly Earnings Presentation Q4 FY24 — Exide Industries Limited ↩↩

-

Exide Industries: Deep Dive into Submarine Battery Business — Moneycontrol, 2023-05-20 ↩

-

Ministry of Corporate Affairs (MCA) Filings — Exide Energy Solutions Ltd ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube