Eureka Forbes: How India's Door-to-Door Salesmen Built a ₹10,000 Crore Water Empire

I. Cold Open & Episode Setup

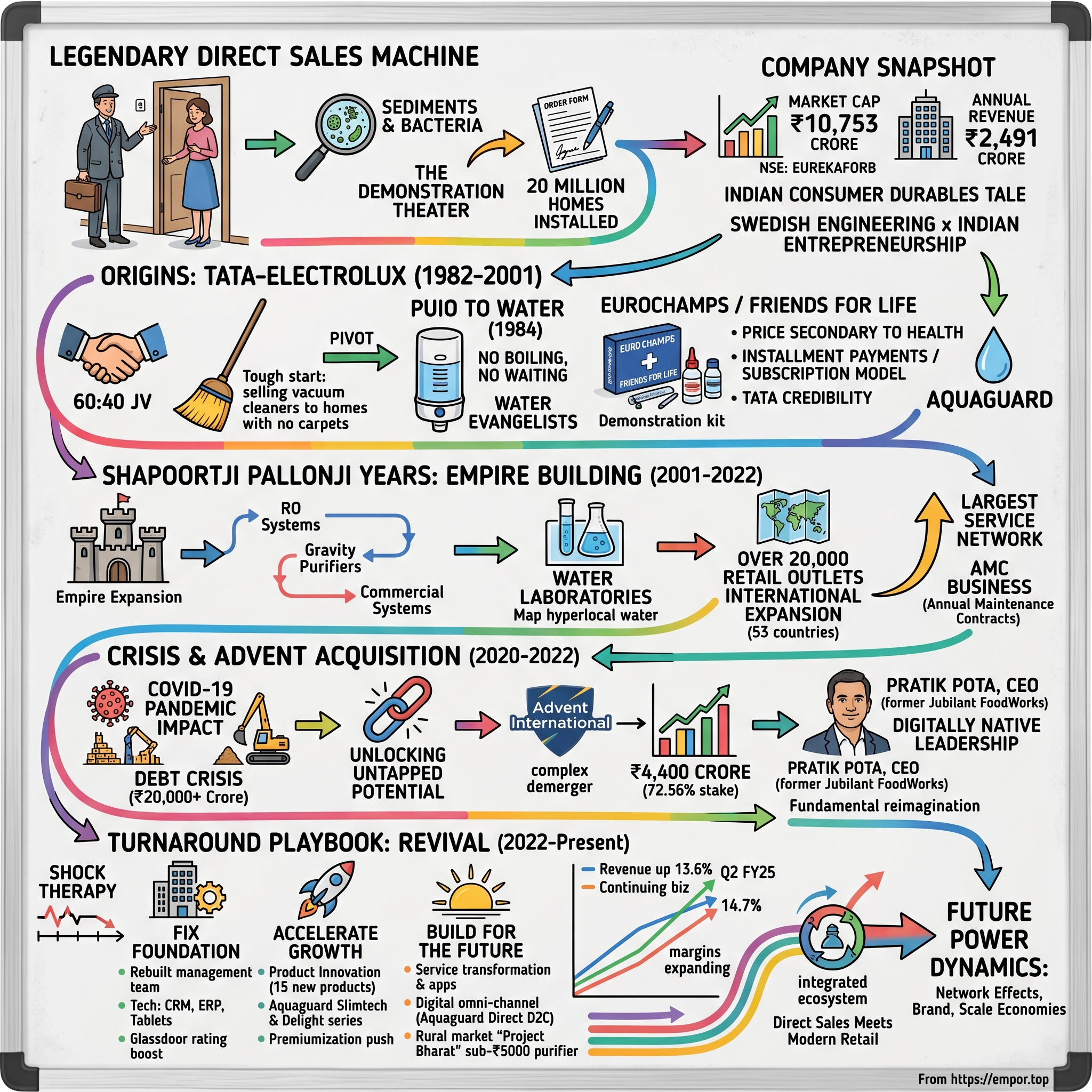

Picture this: It's 6 PM in a middle-class apartment complex in Pune, 1995. The doorbell rings. A man in a crisp white shirt and tie stands outside, carrying a briefcase that seems too heavy for its size. "Madam, may I have just five minutes of your time? I want to show you how your family is drinking poison every day." Within the hour, he's dismantled the kitchen tap, demonstrated a terrifying array of sediments and bacteria under a portable microscope, and walked away with a signed order for ₹15,000—three months of the household's income. This wasn't a scam. This was Eureka Forbes' legendary direct sales machine at work, a force that would go on to install water purifiers in 20 million Indian homes.

Today, Eureka Forbes commands a market capitalization of ₹10,753 crores on the NSE, with annual revenues touching ₹2,491 crores. But those numbers barely scratch the surface of what might be India's most fascinating consumer durables story—a tale of Swedish engineering meeting Indian entrepreneurship, of door-to-door salesmen becoming household consultants, and of how a simple water filter became synonymous with safe drinking water for an entire nation.

The company's journey reads like a business school case study in contradictions. Founded in 1982 as a 60:40 joint venture between the Tata Group's Forbes & Company and Sweden's Electrolux, it started by selling vacuum cleaners to Indians who mostly didn't have carpets. It built its empire through direct sales when everyone said retail was the future. It dominated a market for decades, then nearly collapsed under debt and mismanagement, only to be rescued by private equity. And perhaps most remarkably, it created a product category—water purification—that didn't exist in Indian homes before they showed up at the door.

This is the story of how Eureka Forbes didn't just sell products; they sold peace of mind in a country where clean water remains a luxury for millions. It's about how they built a sales force that became as trusted as family doctors, how they survived multiple ownership changes that would have killed most companies, and how they're now attempting to transform from a door-to-door relic into a digital-first, professional-management-driven growth machine under Advent International's ownership and former Jubilant FoodWorks CEO Pratik Pota's leadership.

What makes this story particularly relevant now? India's water purifier market has exploded from $890 million in 2020 to $4 billion in 2024, yet household penetration remains below 10%. The question isn't whether this market will grow—it's who will capture the value, and whether Eureka Forbes can defend the empire it built, one doorbell at a time.

II. Origins: The Tata-Electrolux Partnership Era (1982-2001)

The year was 1982, and India was a fundamentally different country. Indira Gandhi was Prime Minister, the economy was shackled by the License Raj, and foreign companies needed Indian partners just to sell a bar of soap. It was into this environment that Electrolux, the Swedish home appliances giant, decided to venture—not with refrigerators or washing machines, but with vacuum cleaners. Their chosen partner was Forbes & Company, part of the Tata Group's sprawling empire, run by the Forbes family who had been Tata associates since the 1920s.

The joint venture seemed logical on paper. Electrolux brought technology and global expertise; Forbes brought local knowledge and the Tata name's credibility. The 60:40 split (Forbes holding majority) reflected India's foreign investment restrictions. But there was one small problem: Indians in 1982 didn't really need vacuum cleaners. Most homes had marble or mosaic floors, cleaned daily by domestic help with traditional brooms. Carpets were luxury items found in five-star hotels and the occasional industrialist's drawing room.

The early days were tough. The EuroClean vacuum cleaner was a solution looking for a problem. Sales crawled along, and by 1984, just two years into operations, the venture needed a pivot. That pivot came from an unexpected source: water.

India's water crisis in the 1980s was both invisible and omnipresent. Municipal water supply in major cities was unreliable and often contaminated. Middle-class families boiled water religiously, a time-consuming ritual that offered imperfect protection. Waterborne diseases like cholera, typhoid, and dysentery were common enough that every family had horror stories. The wealthy installed overhead tanks and hoped for the best. Everyone else made do.

The launch of Aquaguard in 1984 wasn't just a product introduction—it was a revelation. Here was a device that could purify water instantly, using ultraviolet technology to kill bacteria and viruses. No boiling, no waiting, no guesswork. Just turn the tap and drink. The technology wasn't revolutionary globally, but in India, it might as well have been magic.

But how do you sell magic to skeptics? This is where Eureka Forbes wrote the playbook that would define direct sales in India for the next four decades. They didn't just hire salespeople; they recruited and trained an army of "EuroChamps"—later rebranded as "Friends for Life." These weren't your typical door-to-door salesmen hawking encyclopedias or insurance. They were water evangelists, armed with demonstration kits that would make a chemistry professor jealous.

The sales demonstration was theater at its finest. The EuroChamp would arrive at your home, often through a reference from a neighbor or relative. He'd test your tap water with various reagents, turning it alarming shades of yellow and brown. He'd show you the sediment under magnification—a horror show of particles and possible pathogens. Then came the pièce de résistance: water from the same tap, passed through an Aquaguard, emerging crystal clear and testing pure. The before-and-after was so dramatic that resistance crumbled.

By the late 1980s, Eureka Forbes had discovered something profound about Indian consumer psychology. Indians might haggle over the price of vegetables, but when it came to their children's health, price became secondary. The Aquaguard wasn't sold as an appliance; it was positioned as a guardian of family health. The marketing tagline—"We thought of it first, so you can drink it first"—emphasized innovation and trust.

The direct sales model had another genius element: installment payments. A ₹15,000 Aquaguard could be paid over 12 months, making it accessible to families who couldn't afford the upfront cost. The EuroChamp would personally collect the monthly installments, using each visit to check the machine, replace filters, and deepen the relationship. This wasn't just sales; it was customer service as a subscription model, decades before SaaS became fashionable.

Cultural context is crucial here. In 1980s and 1990s India, organized retail was virtually non-existent outside major metros. There were no big-box stores, no mall culture, and certainly no e-commerce. For a middle-class family in Nagpur or Coimbatore, the EuroChamp might be the only branded product salesperson who ever entered their home. This exclusivity created a powerful dynamic. The salesperson became a trusted advisor, someone who understood water quality, could fix problems, and represented a large, respectable company.

The Tata connection provided critical credibility. In an era before consumer courts and online reviews, the Tata name was insurance against fraud. If Tata was involved, it had to be legitimate. This association opened doors—literally—that might have remained closed to an unknown brand.

By the mid-1990s, Eureka Forbes had achieved something remarkable. "Aquaguard" had become genericized—the Xerox of water purifiers. People didn't buy water purifiers; they bought Aquaguards, even if the actual product was from another brand. The company claimed over 70% market share in UV purifiers. Their database of customers grew into the millions, each one personally recruited through that theatrical door-to-door demonstration.

The numbers told the story of dominance. From near-zero revenues in 1984, the company crossed ₹100 crores by 1995 and kept climbing. More importantly, they had created a category. Before Aquaguard, water purification was something industrial plants did. After Aquaguard, it was something every aspirational Indian family wanted in their kitchen.

Yet as the 1990s drew to a close, storm clouds gathered. The Indian economy was liberalizing, foreign brands were entering directly, and organized retail was finally beginning to emerge. The very factors that had made door-to-door sales successful—limited retail infrastructure, restricted competition, information asymmetry—were beginning to erode. The question was whether Eureka Forbes could evolve beyond its original model, or whether it would remain trapped in the amber of its early success.

III. The Shapoorji Pallonji Years: Empire Building (2001-2022)

The year 2001 marked a seismic shift in Eureka Forbes' trajectory, though few recognized it at the time. The Tata Group, under increasing pressure to focus on core businesses, decided to divest Forbes & Company. The buyer was unexpected: the Shapoorji Pallonji Group, the construction-to-engineering conglomerate run by the reclusive Pallonji Mistry family. Ironically, the Mistry family was already Tata Group's largest shareholder, owning 18.4% of Tata Sons. This transaction meant Eureka Forbes was moving from one room of the Bombay House to another, though the management philosophy would prove vastly different.

The Shapoorji Pallonji Group's acquisition strategy was classic financial engineering. They saw in Forbes & Company a cash-generating machine with stable revenues and a dominant market position. The construction moguls, who had built landmarks from the Reserve Bank of India building to the Taj Mahal Hotel, understood the value of strong brands and recurring revenue streams. Water purification, unlike construction, wasn't cyclical. People needed clean water in booms and busts alike.

The first major move came in 2005 when Electrolux, facing its own strategic realignment globally, decided to exit the venture. The Swedish company's 40% stake was acquired by Forbes & Company, making Eureka Forbes a wholly-owned Indian entity for the first time. The purchase price wasn't disclosed, but industry insiders suggested Electrolux was happy to exit what had become a non-core investment in a complex market. For Shapoorji Pallonji, it was a chance to own a crown jewel outright.

Under Shapoorji Pallonji's ownership, Eureka Forbes embarked on an aggressive expansion that would define the next decade. The strategy was multi-pronged: dominate water purification, expand the product portfolio, build multiple distribution channels, and go international. Each element revealed both the ambition and, ultimately, the limitations of the approach.

The water purification dominance play was ruthless in its execution. Eureka Forbes didn't just want to lead the market; they wanted to own every segment of it. They launched RO (Reverse Osmosis) systems for areas with high TDS (Total Dissolved Solids) water, gravity-based non-electric purifiers for rural markets, and commercial systems for offices and institutions. The product range exploded from a handful of models to over 50 SKUs, each targeted at specific water conditions, price points, and consumer segments.

The innovation wasn't just in products but in understanding India's water complexity. India doesn't have one water problem; it has thousands. Bangalore's borewell water is different from Chennai's, which is different from Delhi's. Eureka Forbes built what they called "Water Laboratories" across cities, mapping water quality down to the neighborhood level. Sales teams were armed with this hyperlocal data, allowing them to recommend specific solutions for specific areas. A customer in Mumbai's Andheri might need a different purifier than one in Bandra, just a few kilometers away.

The multi-channel expansion was recognition that the direct sales model, while still powerful, couldn't be the only growth engine. By 2010, Eureka Forbes products were available in over 20,000 retail outlets, from large-format stores like Croma and Reliance Digital to neighborhood electronics shops. The company launched exclusive "Aquaguard Galleries" in major cities—experience centers where customers could see the entire range, get water tested, and make informed purchases. E-commerce, initially resisted as channel conflict, was eventually embraced, with the company launching its own online store alongside presence on Amazon and Flipkart.

But the real testament to Shapoorji Pallonji's ambition was the international expansion. In 2010, Eureka Forbes acquired a 25% stake in Swiss Lux International AG, a water treatment company with operations across Europe and Asia. By 2013, they had become the controlling shareholder. The vision was audacious: could an Indian company take its water purification expertise global? The results were mixed. While Eureka Forbes did establish a presence in 53 countries, from Sri Lanka to Saudi Arabia, the international operations never achieved the dominance enjoyed in India.

The product portfolio expansion beyond water was both logical and problematic. Eureka Forbes launched air purifiers (Forbes brand), vacuum cleaners (a return to origins), and even security solutions. The logic was clear: leverage the direct sales force and customer relationships to cross-sell. The execution was harder. Air purifiers faced a chicken-and-egg problem—Indians didn't think they needed them until Delhi's air quality crisis made global headlines, by which time numerous competitors had entered. The new vacuum cleaner range, despite superior technology, couldn't overcome the market's association of Eureka Forbes with water.

The service business evolution during this period deserves special attention. Eureka Forbes realized that selling a water purifier was just the beginning of a customer relationship. These machines needed regular maintenance—filter changes, UV lamp replacements, general servicing. The company built India's largest water purifier service network: 8,000+ trained technicians, 400+ service centers, and a CRM system tracking millions of customers. The Annual Maintenance Contract (AMC) business became a gold mine—high-margin, recurring revenue with upfront cash collection. By 2015, service revenues contributed nearly 30% of total turnover with margins significantly higher than product sales.

Yet for all this expansion, something was going wrong. Revenues plateaued around ₹2,000 crores and refused to budge. Profitability eroded as competition intensified. Kent RO, founded in 1999 by Mahesh Gupta, emerged as a formidable competitor, using celebrity endorsements (Hema Malini as brand ambassador) and aggressive pricing. Hindustan Unilever launched Pureit with a massive marketing budget. Countless regional players offered Chinese-manufactured purifiers at half the price.

The direct sales force, once Eureka Forbes' greatest asset, was becoming a liability. The cost of maintaining thousands of sales personnel in an era of e-commerce and digital marketing was crushing margins. Younger consumers, comfortable researching online, found the door-to-door model intrusive and outdated. The demonstration that once dazzled now seemed like pressure tactics.

Internal challenges compounded external pressures. The Shapoorji Pallonji Group's management style—centralized, family-driven, conservative—clashed with market realities demanding agility and innovation. Decision-making slowed. Digital transformation lagged. Marketing remained stuck in the 1990s while competitors embraced social media and influencer partnerships.

By 2019, the cracks were becoming chasms. Shapoorji Pallonji Group itself was facing a severe liquidity crisis, triggered by the IL&FS collapse and tightening credit markets. The construction giant's debt had ballooned to over ₹20,000 crores. Asset sales became inevitable. Eureka Forbes, one of the few crown jewels generating steady cash, was put on the block.

The irony was palpable. A company that had pioneered selling water purifiers to protect families from unseen dangers was itself drowning in unseen debt and strategic confusion. The empire built over four decades was magnificent in scale but fragile in foundation. What Eureka Forbes needed wasn't just capital but transformation—a complete reimagining of what a 40-year-old direct sales company could become in the digital age.

IV. Crisis & The Advent Acquisition (2020-2022)

The Shapoorji Pallonji Group's boardroom in 2020 resembled a triage unit more than a corporate headquarters. The COVID-19 pandemic had delivered a knockout blow to an already staggering conglomerate. Construction sites were frozen, real estate projects stalled, and cash flows evaporated. The group's debt burden—exceeding ₹20,000 crores—was becoming unsustainable. Chairman Shapoor Mistry, son of the late Pallonji Mistry, faced an existential choice: sell the crown jewels or risk losing everything.

Eureka Forbes, generating steady cash even during lockdowns, was the obvious candidate for divestment. But finding a buyer for a ₹4,000+ crore asset during a pandemic was like selling an umbrella in a hurricane—everyone needed one, but few could afford it. The initial auction in late 2020 attracted unusual suspects. Private equity firms circled like hawks: Advent International, Bain Capital, Blackstone, and Warburg Pincus all submitted preliminary bids. Strategic buyers showed interest too—Haier from China, A.O. Smith from the US, even some Indian conglomerates kicked the tires.

What followed was a masterclass in distressed M&A. Advent International, the Boston-based private equity giant with $75 billion in assets under management, saw something others missed. While competitors focused on Eureka Forbes' problems—stagnant growth, intense competition, outdated distribution model—Advent saw untapped potential. Their due diligence team, led by partners who had previously transformed consumer businesses across Asia, identified three key insights that would drive their investment thesis.

First, India's water purifier penetration at less than 10% was not a saturated market but an enormous opportunity. China, with similar water quality issues, had 30% penetration. The addressable market wasn't 20 million households but potentially 200 million. Second, the direct sales force everyone saw as a liability could be transformed into an asset with the right technology and training. These weren't just salespeople; they were 10,000+ data points on Indian consumers, walking databases of customer preferences and pain points. Third, the service business was a hidden gem—sticky, profitable, and scalable with minimal capital investment.

The September 2021 announcement of Advent's winning bid sent shockwaves through the industry. At ₹4,400 crores for a 72.56% stake, it was one of the largest private equity deals in India's consumer sector. The valuation—roughly 2x revenues—seemed rich for a company with declining profitability. But Advent wasn't buying Eureka Forbes' past; they were betting on its future.

The transaction structure revealed sophisticated financial engineering. The deal involved a complex demerger of Eureka Forbes from Forbes & Company Limited, creating a standalone entity. This wasn't just paperwork; it was surgery, separating four decades of intertwined operations, shared services, and cross-holdings. The process took over a year, with armies of lawyers, accountants, and consultants working to untangle the corporate web.

The regulatory approvals were equally complex. The Competition Commission of India scrutinized the deal for anti-competitive implications. SEBI examined the restructuring for minority shareholder protection. The Foreign Investment Promotion Board reviewed the foreign ownership structure. Each approval came with conditions, modifications, and extensive documentation. The final structure saw Advent holding 72.56% through a Singapore-based vehicle, with Shapoorji Pallonji retaining a minority stake—a face-saving exit that allowed them to participate in any upside.

But the real drama was happening inside Eureka Forbes. Employees, particularly the vast direct sales force, were terrified. Private equity ownership typically meant cost cuts, layoffs, and "optimization"—corporate speak for pain. The senior management, many of whom had spent decades with the company, wondered if they'd survive the transition. Competitors smelled blood, poaching top performers and spreading rumors about impending collapse.

Advent's first move was unexpected and brilliant. Instead of bringing in McKinsey consultants and Excel-wielding cost-cutters, they went shopping for leadership. Their target was Pratik Pota, the former CEO of Jubilant FoodWorks, who had transformed Domino's Pizza in India from a fast-food chain into a technology-driven delivery powerhouse. Pota was everything Eureka Forbes wasn't: young (early 40s), digitally native, and experienced in building consumer brands in competitive markets.

The courtship of Pota revealed Advent's sophistication. They didn't just offer him a CEO role; they presented a transformation mandate with full board backing, significant equity upside, and freedom to rebuild the management team. Pota's appointment in August 2022 was a signal to the market: this wasn't going to be a typical private equity flip. This was going to be a fundamental reimagination.

The formal listing on the BSE in late 2022 completed the transition. Eureka Forbes was now a public company, with quarterly earnings calls, analyst scrutiny, and stock price pressure. Advent subsequently sold 10% of its stake in the open market, partially recovering its investment while maintaining control. The stock's initial performance was volatile, reflecting market uncertainty about whether a 40-year-old direct sales company could transform into a modern consumer brand.

Behind the financial engineering and ownership changes, a deeper transformation was beginning. Advent brought more than capital; they brought global best practices, technological expertise, and a network of advisors who had transformed similar businesses worldwide. They introduced sophisticated data analytics to optimize the sales force, deployed CRM systems to better track customer lifetime value, and began the painful but necessary process of modernizing IT infrastructure that hadn't been updated since the early 2000s.

The pandemic, ironically, had accelerated certain trends that favored Eureka Forbes. Health consciousness had skyrocketed. Work-from-home meant people were consuming more water at home. The middle class, despite economic pressures, was prioritizing health spending. Online purchasing of high-ticket items had become normalized. These tailwinds created a window of opportunity, but capitalizing on them would require execution excellence.

The bear case was equally compelling. Kent RO had used the pandemic to strengthen its position, claiming market leadership in certain segments. New D2C brands like DrinkPrime were offering water purifiers on subscription models—no upfront cost, just monthly rentals. Chinese manufacturers were flooding the market with sub-₹5,000 purifiers that performed adequately for most users. The competitive intensity was higher than ever.

As 2022 drew to a close, Eureka Forbes stood at an inflection point. The old model was clearly broken—door-to-door sales couldn't be the primary growth driver in the age of Amazon. But the new model was still being written. The company had the three things needed for transformation: a crisis that demanded change, capital to fund that change, and leadership with the vision to execute it. Whether they could pull off one of Indian consumer sector's great turnarounds remained to be seen.

V. The Turnaround Playbook: Pratik Pota's Revival (2022-Present)

Pratik Pota walked into Eureka Forbes' Gurgaon headquarters on August 16, 2022, carrying the weight of enormous expectations. His appointment as Managing Director and Chief Executive Officer came with a five-year mandate, but the real timeline was much shorter—Advent needed to see tangible results within 18 months to justify their investment thesis. The 30-year veteran who had previously transformed Domino's Pizza India at Jubilant FoodWorks, with stints at PepsiCo, Airtel, and Hindustan Unilever, understood that incremental change wouldn't cut it. This required shock therapy.

Pota's first hundred days revealed the depth of the challenge. The company was generating revenues of around ₹2,000 crores but bleeding talent, losing market share, and operating with systems that belonged in a museum. The ERP was from 2003. Customer data was scattered across dozens of Excel sheets. The direct sales force still carried paper forms. The e-commerce presence was an afterthought, generating less than 2% of revenues. Most damning, employee morale had collapsed—the company's Glassdoor rating was a dismal 2.8 out of 5.

The new CEO's transformation playbook had three pillars: fix the foundation, accelerate growth, and build for the future. Each pillar required surgical precision and speed of execution that would test even seasoned operators. But Pota had an advantage—he'd seen this movie before at Jubilant FoodWorks, where he'd transformed a pizza chain into a technology company that happened to sell pizzas.

The foundation-fixing began with people. Within six months, Pota rebuilt the entire senior management team. He brought in a new CFO from the FMCG sector who understood both consumer businesses and capital markets. The Chief Marketing Officer came from Samsung, bringing digital-first thinking to a company stuck in print advertising. The head of sales was poached from Asian Paints, another company that had mastered direct-to-consumer distribution. The technology chief came from Flipkart, tasked with building a digital backbone from scratch.

The management team was mandated to continue scaling the business, solidifying Eureka Forbes' market leadership position, and delivering innovative products for a growing customer base. But the real change was cultural. Pota instituted weekly business reviews, something unheard of in the previous regime where decisions could take months. He launched "Project Phoenix"—a 100-day sprint to identify and fix the top 50 operational bottlenecks. Sales teams got tablets with real-time inventory and pricing data. Service technicians received smartphones with route optimization apps. The headquarters moved from a Shapoorji Pallonji building to a modern office in Gurgaon, signaling both independence and modernization.

The growth acceleration strategy was built on a simple insight: Eureka Forbes had been playing defense for a decade when it should have been attacking. Revenue from operations increased 13.6% year-over-year to ₹672.9 crores in Q2 FY25, with continuing business growing even higher at 14.7%. But this wasn't just about pushing harder on existing levers; it was about finding new ones.

Product innovation became the spearhead. Under the previous management, new product development had atrophied—the same Aquaguard models from 2015 were still being sold in 2022. Pota launched "Innovation Fridays" where teams presented new product concepts directly to him, bypassing layers of bureaucracy. Within 18 months, Eureka Forbes launched 15 new products, more than in the previous five years combined. The Aquaguard Slimtech series targeted urban millennials with sleek designs that looked like art installations rather than appliances. The Aquaguard Delight series brought RO+UV technology to the ₹10,000 price point, previously dominated by Chinese imports.

The service business transformation was equally dramatic. Adjusted EBITDA increased 25.1% year-over-year to ₹77.5 crores, with margins improving 106 basis points to 11.5%. The Annual Maintenance Contract (AMC) business, which had been declining at 5% annually, was reimagined. Instead of selling one-year contracts, Eureka Forbes introduced three-year and five-year plans with significant discounts. Service technicians were incentivized not just on contract sales but on customer satisfaction scores. A new app allowed customers to schedule service visits, track technician arrival, and rate service quality—bringing Uber-like transparency to appliance servicing.

The digital transformation wasn't just about e-commerce; it was about reimagining every customer touchpoint. The company launched "Aquaguard Direct," a D2C platform that offered virtual demonstrations, EMI options, and installation within 24 hours in major cities. Social media spending increased 10x, with influencer partnerships and targeted Facebook campaigns replacing newspaper ads. The traditional door-to-door sales force wasn't abandoned but augmented—sales representatives now carried tablets that could show product videos, calculate water quality based on pin code, and process digital payments instantly.

By Q4 FY25, continuing business revenue grew by 10.9% year-over-year, marking the sixth successive quarter of double-digit growth, with EBITDA margins touching 13% for the first time. The numbers told a story of momentum building quarter by quarter.

The focus on premiumization was counterintuitive but brilliant. While competitors raced to the bottom with ₹5,000 purifiers, Pota pushed upmarket. The Aquaguard Glory series, priced above ₹30,000, offered features like hot water dispensing, fruit and vegetable purification, and IoT connectivity. These premium products contributed over 30% of revenues despite being less than 10% of unit sales. The logic was simple: middle-class Indians would pay for health and convenience if you gave them a reason to upgrade.

International expansion, long neglected, got renewed focus. Instead of trying to compete globally with the Aquaguard brand, Eureka Forbes positioned itself as a white-label manufacturer for international brands. Contracts with Middle Eastern retailers and Southeast Asian distributors brought in high-margin export revenues without massive marketing investments.

But perhaps the most radical change was in corporate governance and communication. In Q2 FY25, the company reported revenue growth of 13.6% to ₹672.9 crores, with continuing revenues growing 14.7% year-over-year—the fourth successive quarter of double-digit growth, underpinned by product business growing in excess of 20%. Quarterly earnings calls became events where Pota personally addressed analyst concerns, something previous CEOs had delegated to CFOs. The company started publishing monthly business updates, unprecedented transparency for an Indian consumer company.

The transformation metrics by end of FY25 were staggering. Growth stepped up from 2.2% in FY23 to 7.9% in FY24 and to 12.0% in FY25, while margins expanded from 6.3% in FY23 to 10.3% in FY24 and to 11.7% in FY25. The company had gone from stagnation to double-digit growth, from losses to expanding margins, from organizational paralysis to entrepreneurial energy.

Yet challenges remained formidable. The direct sales force, while modernized, still represented a massive fixed cost. Competition had intensified, with Kent RO matching every innovation within months. The promoter pledge of 53.7% of holdings created an overhang on the stock. Most critically, the core water purifier market was maturing in urban areas while rural penetration remained stubbornly low.

Pota's response was to think beyond the current business model. In late 2024, he launched "Project Bharat"—an initiative to create a sub-₹5,000 water purifier specifically for rural India, distributed through self-help groups and microfinance institutions. He piloted water purifier vending machines in Mumbai local train stations. He even explored subscription models where customers paid ₹300 monthly for purified water rather than buying machines.

The cultural transformation was perhaps the most profound. As Pota explained in earnings calls, they were "rebuilding the business for the next 40 years, building on the foundations laid in the last 40". The company that had been notorious for bureaucracy and slow decision-making was becoming agile and entrepreneurial. Employee satisfaction scores jumped from 2.8 to 4.1 on Glassdoor. Attrition in critical roles dropped from 30% to 12%. Young talent from IIMs and IITs, who wouldn't have considered Eureka Forbes earlier, were now joining in droves.

The Advent partnership brought more than capital and leadership. They introduced sophisticated pricing analytics that optimized SKU-level profitability. They brought in supply chain experts who reduced working capital by 20%. They even facilitated partnerships with other Advent portfolio companies globally, opening new technology and market access opportunities. This wasn't passive private equity ownership; it was active value creation.

As 2024 drew to a close, Eureka Forbes looked like a different company from the one Advent had acquired just three years earlier. The transformation wasn't complete—cultural change takes time, and competitive pressures remained intense. But the trajectory was clear. From a tired legacy player, Eureka Forbes was becoming a modern consumer company—digital-first, innovation-driven, professionally managed, but still rooted in the direct customer relationships that had built its empire. The question was no longer whether the transformation would succeed, but how far it could go.

VI. The Business Model: Direct Sales Meets Modern Retail

The heart of Eureka Forbes still beats in the living rooms of middle India, where 8,000 company-trained technicians make over 50,000 service calls daily. This vast human network—part salesman, part technician, part family health advisor—represents both the company's greatest moat and its most complex operational challenge. Understanding how this machine works, and how it's evolving, is key to understanding Eureka Forbes' future.

Consider a typical service technician, Rajesh Kumar, operating in Pune's Kothrud area. His day begins at 8 AM at a local service center, one of 400+ across India. He checks his smartphone app, which has already optimized his route for the day—12 service calls covering 30 kilometers, algorithmically sequenced to minimize travel time and maximize customer availability. His bike carries spare parts worth ₹50,000, tracked via RFID, automatically replenished based on consumption patterns. He's not just fixing machines; he's a walking data point in a massive customer intelligence system.

The first call is routine maintenance for a five-year-old Aquaguard. While replacing filters, Rajesh notices the customer's water TDS has increased—monsoon runoff affecting the municipal supply. His tablet automatically recommends an upgrade to an RO+UV model. He shows the customer a video demonstration, offers an exchange discount, and processes the order digitally. Commission credited instantly. The old unit will be refurbished and sold in the second-hand market, another revenue stream most investors miss.

This interaction reveals the genius of the service-led business model. Unlike product sales, which are episodic and competitive, service creates recurring touchpoints. Each technician meets 4,000+ customers annually, generating real-time intelligence on product performance, customer satisfaction, and upgrade potential. This data feeds into product development, pricing strategy, and competitive intelligence. No competitor has this ground-level visibility.

The Annual Maintenance Contract (AMC) business is the crown jewel within services. At ₹3,000-5,000 per year, AMCs generate ₹500+ crores in revenue with 40%+ EBITDA margins—double that of product sales. The beauty lies in the economics: upfront cash collection, predictable revenue streams, and negative working capital. Customers prepay for services they'll consume over 12 months, effectively funding Eureka Forbes' operations interest-free.

But the real magic is customer stickiness. AMC customers have 85% renewal rates, creating lifetime values exceeding ₹25,000 per household. They upgrade products 3x more frequently than non-AMC customers. They recommend Eureka Forbes 2x more often. In a world obsessed with customer acquisition costs, Eureka Forbes has 2 million households paying them annually to maintain the relationship.

The product portfolio strategy reflects decades of market learning. The 50+ SKU range isn't random proliferation; it's careful segmentation across three vectors: water quality (TDS levels, contamination types), price sensitivity (₹5,000 to ₹50,000), and lifestyle needs (family size, kitchen space, usage patterns). Each product addresses specific customer segments identified through service interactions.

Take the Aquaguard Glory, priced at ₹35,000. It's not competing with Kent RO's ₹15,000 models; it's targeting the 30-something IT professional who wants hot water for green tea, chilled water for post-workout hydration, and an app that tracks consumption patterns. The margins on Glory exceed 30%, compared to 15% on entry-level models. One Glory sale equals five basic units in profitability.

The gravity-based purifier range, dismissed by many as low-tech, generates ₹200 crores annually with minimal marketing spend. These ₹2,000-3,000 units target households without reliable electricity or running water—30% of India. The distribution happens through rural self-help groups and microfinance institutions, channels competitors haven't cracked. The simplicity is deceptive; these products required extensive R&D to achieve effective purification without power.

The Forbes vacuum cleaner revival deserves special mention. Written off as a failed diversification, the category has been reimagined under Pota's leadership. The Forbes Trendy Wet & Dry series targets small businesses—salons, clinics, small offices—with commercial-grade performance at consumer prices. The Robo Vac series, priced at ₹25,000+, captures the premium home segment. Vacuum cleaners now contribute 15% of revenues with higher margins than water purifiers.

Global operations across 53 countries generated ₹300 crores in FY24, mostly through white-labeling and private-label manufacturing. The Middle East is the largest market, where Indian expatriates trust the Aquaguard brand. But the real opportunity lies in Southeast Asia and Africa, where water challenges mirror India's. The company's ability to design products for extreme conditions—inconsistent power, varying water quality, harsh usage—gives them an edge over European and American competitors.

The channel strategy has evolved from direct sales dominance to true omni-channel presence. Direct sales still contributes 40% of revenues but now works synergistically with other channels. The 20,000+ retail outlets aren't just points of sale; they're experience centers where customers can test water quality and see demonstrations. E-commerce, growing at 50% annually, contributes 15% of revenues. The company's own D2C platform accounts for 30% of online sales, offering better margins and customer data ownership.

The unit economics reveal why water purifiers remain attractive despite competition. Customer acquisition cost averages ₹2,000 through direct sales, ₹1,000 through retail, and ₹500 online. Gross margins range from 35% on basic units to 50% on premium models. The payback period on customer acquisition is 14 months, after which the service revenue stream becomes pure profit. With average product life of seven years and AMC attachment rates of 40%, lifetime values exceed ₹30,000 per customer.

The working capital management has improved dramatically under professional management. Inventory turns have increased from 4x to 6x annually. Receivables days have dropped from 60 to 45. The company now operates with negative working capital in the service business, using customer advances to fund operations. This efficiency has released ₹200 crores in cash, funding growth without additional debt.

Supply chain sophistication often goes unnoticed but drives competitive advantage. Eureka Forbes sources from 200+ vendors, many exclusive partners for decades. Critical components like UV lamps and RO membranes are dual-sourced to ensure supply security. The company maintains strategic inventory of 45 days, balancing service levels with carrying costs. Regional warehouses use AI-driven demand forecasting, reducing stockouts by 30% while cutting inventory costs by 15%.

The after-sales service infrastructure is unmatched in India's consumer durables sector. The 400+ service centers are company-owned, ensuring quality control. The 8,000+ technicians undergo 40 hours of annual training, certified on new products and service protocols. The call center handles 50,000 queries daily, with 80% first-call resolution. This infrastructure represents ₹500 crores in invested capital, a barrier no new entrant can easily replicate.

Digital integration is transforming traditional strengths. The EuroSmart app has 1 million+ downloads, allowing customers to schedule services, track water consumption, and order consumables. IoT-enabled purifiers, currently 5% of sales, provide real-time water quality data and predictive maintenance alerts. The company's CRM system tracks 20 million customer records, enabling personalized marketing and service delivery.

The franchise model, launched in 2023, opens new growth avenues. Entrepreneurs can open Aquaguard-exclusive stores with ₹10 lakh investment, receiving territorial exclusivity, marketing support, and product training. With 200 franchises operational and 500 targeted by 2025, this asset-light expansion accelerates market penetration without capital intensity.

Sustainability initiatives, while generating limited revenue currently, position the company for future regulations. The "Blue Gold" recycling program collects old purifiers, recovering precious metals and plastics. The company has reduced plastic usage by 30% through design optimization. Water-saving features in new models address increasing environmental consciousness among urban consumers.

Looking at the model holistically, Eureka Forbes has built something rare in Indian consumer businesses: a fully integrated ecosystem. They don't just sell products; they manage the entire customer lifecycle from education to purchase to service to upgrade. This model generates multiple revenue streams, creates switching costs, and provides competitive intelligence. While execution challenges remain and competition intensifies, the fundamental business model architecture remains robust and differentiated.

VII. Market Dynamics & Competition

The morning of March 15, 2024, should have been celebratory at Eureka Forbes' headquarters. Revenue from operations had increased 13.6% year-over-year to ₹672.9 crores, with continuing business growing even higher at 14.7%. But the mood was tense. Down the road in Noida, Kent RO Systems was preparing its IPO roadshow, claiming market leadership with around 40% share in the RO purifiers market. The water wars of India had entered a new, more brutal phase.

India's water purifier market, valued at USD 3,350.1 million in 2024 and projected to reach USD 7,119.1 million by 2033 at a CAGR of 8.7%, represents one of the world's most dynamic consumer durables battlegrounds. Yet this impressive growth masks a Darwinian struggle where technology commoditization, price wars, and new business models threaten to upend four decades of carefully constructed competitive advantages.

The market's fundamental driver remains unchanged: India's water crisis. In 2024, gastroenteritis, diarrhea, and jaundice cases rose significantly, with 3,991 cases and 15 deaths reported, the highest number in four years. The explosive population growth and varied geographic challenges further complicate clean water availability, with polluted sources causing outbreaks of cholera and typhoid. This health emergency creates non-discretionary demand—families will sacrifice other expenses before compromising on water safety.

Yet penetration remains stubbornly low. Less than 50% of India's population has access to safe drinking water, but household water purifier penetration hovers around 8-10%. The paradox is striking: those who need purifiers most can't afford them, while those who can afford them often have alternative solutions like bottled water or bore wells. Breaking this paradox requires not just products but ecosystem transformation.

Eureka Forbes' Aquaguard brand and Forbes vacuum cleaners maintain market leadership positions, but the competitive landscape has transformed beyond recognition from the duopoly days of Aquaguard versus Pureit. Kent RO, founded by IIT graduate Mahesh Gupta in 1999, exemplifies the new challenger archetype—aggressive, marketing-savvy, and unencumbered by legacy infrastructure.

Kent's rise deserves deeper examination. With legendary actress Hema Malini as brand ambassador since 2005, their message of "Kent RO hi lena" struck a chord with families. Their ad campaign paid off, with revenue soaring to ₹250 crore by 2010 and a 45% annual growth rate. By 2017, revenue had crossed ₹950 crore. The company's claims to serve over 5.50 million consumers as of September 2024 and has the highest number of SKUs in both overall and premium water purifier categories.

The Hema Malini factor cannot be underestimated. Her endorsement—anchored by the memorable line "Kent RO hi lena"—has conveyed trust, purity, and class since 2005, helping Kent capture roughly 40% market share in the ₹4,000 crore RO segment. This single celebrity endorsement achieved what Eureka Forbes' thousands of door-to-door salesmen struggled with: instant brand recognition and trust.

But Kent represents just one threat vector. Hindustan Unilever's Pureit, backed by massive marketing budgets and distribution reach, targets the mass market with sub-₹10,000 purifiers. In July 2024, HUL launched the new Pureit Revito Series powered by DURAViva™ filtration technology to remove heavy metals while providing maximum purified water up to 8000L. Their strategy: make water purification accessible to the next 100 million households.

The technology proliferation adds another dimension. Reverse Osmosis (RO) technology currently dominates with the largest market share, owing to its capabilities to kill micro-organisms, heavy metals, pesticides, and other dissolved solids. But RO's dominance faces challenges. UV technology offers lower costs and no water wastage. Gravity-based purifiers work without electricity. Each technology serves different water conditions and consumer segments, fragmenting the market further.

New-age disruptors are rewriting the rules entirely. In October 2024, Urban Company launched smart RO water purifiers under the "Native" brand—India's first range needing no servicing for two years and capable of 12,000 liters output without filter changes. Lustral Water announced the world's first IoT and AI-enabled water purifier, equipped to remove harmful bacteria while preserving vitamins and minerals. These aren't just products; they're platforms challenging the entire service-dependent business model.

The subscription revolution poses an existential threat to traditional players. Companies like DrinkPrime offer zero upfront cost, just ₹300-500 monthly rentals. For young urban consumers wary of large capital expenses, this model is compelling. It transforms water purification from a product purchase to a utility payment, similar to electricity or internet. Eureka Forbes' response—testing subscription models in select cities—acknowledges this threat but lacks the aggressive execution of pure-play subscription companies.

Chinese manufacturers add pricing pressure from below. Brands like Xiaomi's Mi Smart purifiers, priced under ₹10,000, offer 80% of premium features at 40% of the cost. The market is led by players including Eureka Forbes, Havells, Whirlpool, Kent RO Systems, Panasonic, Hindustan Unilever, Mi (Xiaomi), Godrej, Tata Swach, Aquasure, Blue Star, LG, Nasaka, Livpure and A.O. Smith. The technology democratization means anyone can source components from China, assemble in India, and undercut established players by 50%.

Distribution dynamics are evolving rapidly. Offline retail channels, including brick-and-mortar stores and specialty stores, traditionally dominated distribution, as consumers prefer to physically see and buy water purifiers. But online retail is experiencing rapid growth due to increasing online shopping trends, with e-commerce platforms allowing for a wide range of choices. This shift advantages digital-native brands while forcing traditional players to cannibalize their offline channels.

Government initiatives create both opportunities and disruptions. The Har Ghar Jal Programme under Jal Jeevan Mission aims to ensure every rural household has safe drinking water through tap connections. As of February 2024, 74.58% of targeted 19.27 crore households received functional tap connections, with budgetary allocation reaching ₹70,162.9 crore in FY2025. If successful, this could reduce demand for household purifiers while creating opportunities for community-level purification systems.

Regional variations add complexity. Western and Central India capture the largest revenue share due to high urbanization, heightened consumer awareness, and extensive retail networks. But growth increasingly comes from Tier 2 and 3 cities where competition is less intense but consumer education costs are higher. Each region requires different products (RO for high TDS areas, UV for low TDS), pricing strategies, and distribution models.

The technology convergence trend sees purifiers becoming smart home appliances. LG's PuriCare Self-Service Tankless Water Purifier delivers purified water through an advanced 4-Stage All Puri Filter System, removing nine types of heavy metals and 99.99% of norovirus. Features like app connectivity, water quality monitoring, and predictive maintenance are becoming table stakes. Companies slow to adopt smart features risk being perceived as outdated.

Environmental concerns create new battlegrounds. RO technology wastes 3 liters for every liter purified—increasingly unacceptable in water-scarce India. Brands promoting water conservation and plastic reduction gain consumer goodwill. Kent's "Zero Water Wastage" technology and Eureka Forbes' recycling programs respond to these concerns, but younger brands build sustainability into their core proposition from day one.

The competitive intensity shows in margin compression across the industry. Where Eureka Forbes once enjoyed 40%+ gross margins, intense competition has pushed industry averages below 30%. Price wars during festivals and online sales events further erode profitability. Only scale players and niche premium brands maintain healthy margins.

Looking forward, the market structure suggests consolidation is inevitable. Small regional players lack the scale for technology investments. Mid-sized players struggle with national distribution costs. Even large players like Eureka Forbes face pressure to merge or acquire to maintain competitiveness. The next five years could see the current 15+ major brands consolidate to 5-7 national players.

For Eureka Forbes, the competitive dynamics present a clear strategic imperative: leverage existing strengths while rapidly building new capabilities. The 8,000+ service network remains unmatched. The Aquaguard brand, despite competition, retains tremendous equity. The customer database of 20 million households provides unparalleled market intelligence. But these advantages erode daily without aggressive innovation and execution.

The market's evolution from product sales to ecosystem play favors integrated players who can offer products, services, and solutions. Pure product players will struggle against subscription models. Pure service players will lose to technology automation. Only companies that successfully blend physical and digital, product and service, traditional and modern, will thrive in India's water purification market of tomorrow.

VIII. Financial Analysis & Stock Performance

The trading floor at the NSE on September 11, 2024, buzzed with anticipation. After years of private ownership and corporate restructuring, Eureka Forbes was returning to public markets. The opening bell rang at ₹500, and within minutes, the stock gyrated wildly—touching ₹550 before settling at ₹482. For a company with four decades of history, this was both a homecoming and a reality check.

Today's numbers tell a story of contrasts: ₹10,764 crore market capitalization, up 22.0% over one year, with revenues of ₹2,491 crores and profit of ₹171 crores. Yet beneath these seemingly healthy metrics lies a more complex narrative. The company has a low return on equity of 2.31% over the last three years, suggesting capital isn't being deployed efficiently despite the turnaround efforts.

The valuation puzzle confronts every investor examining Eureka Forbes. The stock trades at a P/E ratio of 64.4—eye-watering for a consumer durables company, especially one with single-digit ROE. This multiple implies either massive growth expectations or market mispricing. The bull case argues the former: transformation under Pratik Pota, underpenetrated market, and improving margins justify premium valuations. The bear case sees a value trap: intense competition, commoditizing products, and execution risks don't support 60x earnings.

The financial trajectory under Advent's ownership reveals dramatic improvement. In Q4 FY25, continuing business revenue grew by 10.9% year-over-year, marking the sixth successive quarter of double-digit growth, with EBITDA margins touching 13% for the first time. The momentum in product business sustained with innovations and growth investments helping products grow in high teens. Looking at the full year, growth stepped up from 2.2% in FY23 to 7.9% in FY24 and to 12.0% in FY25, while margins expanded from 6.3% in FY23 to 10.3% in FY24 and to 11.7% in FY25.

The profit turnaround deserves scrutiny. The company delivered good profit growth of 183% CAGR over the last five years—impressive until you realize this growth came from a near-zero base during the Shapoorji Pallonji era's final years. Absolute profit levels remain modest for a company of this scale. Net margins at approximately 7% lag best-in-class consumer companies achieving 15%+.

The balance sheet transformation stands out as Advent's clearest success. The company has reduced debt and is almost debt free. This deleveraging freed up cash for growth investments and removed financial risk from the equation. Working capital improvements generated additional liquidity, funding the transformation without external capital.

But the elephant in the room remains promoter pledging. Promoters have pledged or encumbered 53.7% of their holding—a massive red flag for governance-conscious investors. This pledge, likely related to Advent's acquisition financing, creates asymmetric risk. If the stock price falls significantly, forced selling could trigger a downward spiral. The pledge also signals that Advent might be more financially stretched than their public positioning suggests.

Stock performance since listing tells its own story. The 52-week high is ₹655.90 and 52-week low is ₹439.90—a 49% range indicating extreme volatility. The stock has fallen by 0.10% compared to the previous week, but shown a 9.32% rise over the month, with a 1.71% increase over the year. This volatility reflects market uncertainty about the transformation's sustainability and competitive positioning.

Institutional interest remains lukewarm. Promoter holding stands at 62.6%, leaving limited free float for institutions. Mutual fund holdings remain below 2%, suggesting domestic institutions aren't convinced. Foreign institutional investors show marginally more interest, but their holdings remain in single digits. This lack of institutional backing creates liquidity challenges and amplifies volatility.

The dividend policy—or lack thereof—raises questions. Though the company is reporting repeated profits, it is not paying out dividend. For a mature consumer company generating cash, zero dividends seems puzzling. The likely explanation: Advent needs every rupee for transformation investments and eventual debt servicing. But this also means minority shareholders aren't seeing tangible returns despite profitability improvements.

Analyst coverage remains thin, with most brokerages maintaining "Hold" ratings. According to analysts, EUREKAFORB price has a max estimate of 750.00 INR and a min estimate of 586.00 INR. This wide range—nearly 30% spread—reflects fundamental uncertainty about the company's trajectory. Bulls see a turnaround story with massive runway; bears see a legacy player in a commoditizing market.

The quarterly momentum provides encouragement. In Q2 FY25, revenue from operations increased 13.6% year-over-year to ₹672.9 crores, with continuing business growing higher at 14.7%. Adjusted EBITDA increased 25.1% to ₹77.5 crores from ₹62.0 crores in Q2FY24, with margins improving 106 basis points to 11.5%. Profit after tax increased 83.2% to ₹46.7 crores from ₹25.5 crores. These aren't just growth numbers; they show operational leverage kicking in.

Peer comparison reveals relative underperformance. Eureka Forbes' top 5 peers in the Consumer sector include Crompton Greaves and other electrical consumer durables companies. Most peers trade at 30-40x P/E with similar or higher ROEs. Eureka Forbes' premium valuation despite inferior returns suggests either market inefficiency or faith in future improvement.

The capital allocation priorities under Pota show clear strategic thinking. Growth investments in product development and digital infrastructure take precedence. Marketing spending has increased but remains disciplined. M&A appears off the table for now—organic growth is the focus. This conservative approach makes sense given the execution challenges but might limit growth potential.

Working capital metrics show continued improvement. Inventory turns have reached 6x annually, matching best-in-class consumer companies. Receivables management has tightened with DSO (Days Sales Outstanding) below 45 days. The company operates with negative working capital in services—a powerful cash generation mechanism. These operational improvements don't make headlines but fundamentally strengthen the business.

The ESOP (Employee Stock Option Plan) implementation signals long-term thinking. Eureka Forbes has allotted 5,659 equity shares under ESOP on June 24, 2025, increasing paid-up capital from ₹193,48,61,570 divided into 19,34,86,157 shares to ₹193,49,18,160 divided into 19,34,91,816 shares. While dilutive, this aligns management interests with shareholders and helps retain talent in a competitive market.

The currency of transformation remains time. Financial metrics are improving but from a low base. Competitive intensity isn't abating. Market penetration remains frustratingly low. The question for investors isn't whether Eureka Forbes is improving—it clearly is—but whether improvements are happening fast enough to justify current valuations and overcome structural challenges.

Risk-adjusted returns present a mixed picture. The stock's beta exceeds 1.5, indicating higher volatility than the broader market. Sharp ratios remain negative over most timeframes. For risk-averse investors, the volatility and governance concerns (promoter pledge) make this unsuitable. For risk-tolerant investors seeking turnaround plays, the improving fundamentals might justify measured exposure.

The rating agency perspective adds another dimension. CARE upgraded credit rating for long term bank facilities and issuer rating from CARE A+; Stable to CARE AA-; Stable. This upgrade reflects improving financial health and reduced balance sheet risk. For debt investors, this signals safety. For equity investors, it removes one worry but doesn't address growth and profitability concerns.

Looking ahead, several catalysts could re-rate the stock. Successful IPOs of competitors like Kent RO would provide valuation benchmarks. Resolution of the promoter pledge would remove a major overhang. Sustained margin expansion beyond 15% would validate the transformation thesis. Conversely, market share losses, margin compression, or governance issues could trigger significant downside.

The financial analysis ultimately reveals a company in transition. The numbers are moving in the right direction—revenue growth accelerating, margins expanding, debt reducing. But the pace of improvement, while impressive relative to recent history, might not be sufficient given the competitive dynamics and market expectations embedded in current valuations. For fundamental investors, Eureka Forbes presents a classic risk-reward dilemma: undeniable improvement but uncertain ultimate destination.

IX. Power Dynamics & Lessons

The conference room at Advent International's Boston headquarters, December 2023. The quarterly review of portfolio companies was underway, and Eureka Forbes was up next. The presentation showed hockey-stick growth projections, margin expansion targets, and market share gains. But the senior partner's question cut through the optimism: "What power does Eureka Forbes actually have in its market?" The ensuing discussion would reveal fundamental truths about building and maintaining competitive advantage in India's consumer markets.

Power in business, as Hamilton Helmer defines it in "7 Powers," is the ability to generate persistent differential returns. Examining Eureka Forbes through this lens reveals both why the company dominated for decades and why that dominance is now under threat. The analysis also surfaces lessons for founders, operators, and investors navigating similar transitions.

The original power dynamic was elegant in its simplicity: switching costs plus process power. Once a family bought an Aquaguard, they were locked in. The machine required specific filters, regular servicing, and familiarity with operation. Switching to another brand meant learning new systems, finding new service providers, and risking water quality during transition. The direct sales process—theatrical demonstrations creating fear then providing salvation—was nearly impossible to replicate at scale. Competitors could copy products but not the thousands of trained salespeople and millions of customer relationships.

This power structure worked brilliantly in an analog world. Information asymmetry was absolute—consumers couldn't Google water purifier reviews or compare prices across brands. Distribution was physical—without retail presence or direct sales force, you couldn't reach customers. Service was local—the neighborhood Eureka Forbes technician was often the only person who understood these machines. Trust was personal—families bought from salespeople they knew, serviced by technicians they recognized.

The digital revolution didn't just erode these advantages; it inverted them. Information asymmetry collapsed—every customer now has access to reviews, comparisons, and technical specifications. Distribution democratized—any brand can reach customers through e-commerce. Service commoditized—YouTube videos teach filter replacement, and gig economy platforms provide on-demand technicians. Trust transferred—from personal relationships to online ratings and influencer endorsements.

Consider the Kent RO phenomenon through the power lens. Mahesh Gupta didn't try to out-execute Eureka Forbes at their own game. Instead, he identified where Eureka Forbes' power was weakest—brand marketing and celebrity endorsement—and concentrated resources there. With Hema Malini as brand ambassador, their message of "Kent RO hi lena" struck a chord with families, with revenue soaring to ₹250 crore by 2010 and a 45% annual growth rate. Kent's power wasn't in distribution or service but in brand—a form of power Eureka Forbes had never truly developed.

The private equity playbook, as executed by Advent, represents an attempt to build new forms of power while preserving existing ones. The digital transformation creates network effects—the more customers use the app, the better the service algorithms become. The data analytics build information advantages—understanding customer behavior and predicting maintenance needs better than competitors. The professional management introduces process power—systematic approaches to innovation, marketing, and operations that amateur competitors can't match.

But herein lies a crucial lesson: power transitions are extraordinarily difficult. Eureka Forbes is attempting to move from one form of power (switching costs + process) to another (network effects + brand + scale economies) while under competitive attack. It's like rebuilding a plane while flying it through a storm. The old advantages erode faster than new ones develop, creating a dangerous transition period where the company is vulnerable.

The distribution paradox illustrates this challenge perfectly. The direct sales force was Eureka Forbes' greatest strength but became an albatross—expensive, difficult to manage, and increasingly ineffective with younger consumers. Yet abandoning it entirely would mean losing millions of customer relationships and service touchpoints. The solution—gradual transition to omnichannel while maintaining but modernizing direct sales—is logical but expensive and complex to execute.

The innovation imperative reveals another dimension of power dynamics. In the 1990s, Eureka Forbes could launch a product and milk it for years. Today, product lifecycles have compressed from years to months. The Aquaguard Slimtech might be innovative today, but within six months, three competitors will have similar products at lower prices. This forces continuous innovation—exhausting and expensive—just to maintain position. It's the Red Queen effect: running faster and faster just to stay in place.

Brand power remains Eureka Forbes' most underutilized asset. "Aquaguard" has become generic for water purifiers—extraordinary brand equity that the company has failed to fully monetize. Compare this to how Bisleri leveraged similar genericide in packaged water, or how Xerox fought to maintain brand distinctiveness. Eureka Forbes allowed the brand to become commoditized rather than premiumized, missing opportunities to create true brand power.

The service moat deserves special attention. While products are easily copied, service networks are not. Eureka Forbes' 8,000+ technicians and 400+ service centers represent decades of investment and relationship building. This physical infrastructure creates local scale economies—the more customers in an area, the more efficient service delivery becomes. Competitors must either build similar networks (capital intensive) or outsource service (quality risk). This remains Eureka Forbes' most defensible advantage.

The lesson from Eureka Forbes' journey is that market position without power is ultimately unsustainable. For decades, the company confused market share with market power. High share made them complacent, assuming customers would always choose Aquaguard. But market share without switching costs, network effects, or brand power is just a number—vulnerable to any competitor willing to spend aggressively to acquire customers.

The private equity dimension adds another layer to power dynamics. Advent's power comes from capital, connections, and capability. Capital allows transformation investments the Shapoorji Pallonji Group couldn't afford. Connections bring in world-class management and advisors. Capability transfers best practices from global portfolio companies. But private equity also brings constraints—time pressure, return requirements, and eventual exit needs that might conflict with long-term power building.

For founders, the Eureka Forbes story offers crucial insights. First, build power from day one—don't assume market share equals defensibility. Second, recognize when your source of power is eroding and begin building new forms before the old ones fail. Third, understand that different life stages require different power structures—what works in startup phase won't work at scale.

For operators, the lessons are equally valuable. Power transitions require complete commitment—half-measures fail. Cultural change must accompany strategic change—you can't build digital-age power with analog-age thinking. Most importantly, preserve existing advantages while building new ones—throwing away hard-won positions rarely makes sense.

For investors, Eureka Forbes illustrates the importance of distinguishing between temporary advantages and sustainable power. High returns on capital might reflect historical power that's eroding. Transformation stories sound compelling but execution is extraordinarily difficult. The key question isn't "does this company have advantages?" but "will these advantages persist and strengthen?"

The competitive dynamics in India's consumer markets are evolving from relationship-based to technology-enabled, from information asymmetry to radical transparency, from physical to digital distribution. Companies that recognize and adapt to these shifts can build new forms of power. Those that don't, regardless of historical dominance, face inevitable decline.

Eureka Forbes' power reconstruction remains incomplete. The company has stabilized and begun growing, but hasn't yet established sustainable differential advantages. The next few years will determine whether Pratik Pota and team can complete the power transition or whether Eureka Forbes becomes another case study in how market leaders lose their way. The jury's still out, but the clock is ticking.

X. Bear vs. Bull Case

The investment committee meeting at a major Mumbai mutual fund, January 2025. The topic: whether to initiate a position in Eureka Forbes. The analyst presenting the bull case was passionate, armed with charts showing improving metrics and TAM expansion. The senior portfolio manager playing devil's advocate was equally prepared, with competitive analysis and margin pressure scenarios. The debate that followed encapsulated the profound uncertainty surrounding Eureka Forbes' future.

The Bull Case: A Transformation Story Just Beginning

The optimists see Eureka Forbes as India's next great consumer turnaround story, comparable to Asian Paints in the 1990s or Titan in the 2000s. The core argument rests on five pillars, each compelling in isolation, potentially transformative in combination.

First, the market opportunity is staggering. India's water purifier market, valued at USD 3,350.1 million in 2024, is projected to reach USD 7,119.1 Million by 2033, exhibiting a CAGR of 8.7%. With household penetration below 10%, compared to 30% in China, the runway for growth extends decades. Every percentage point of penetration gain represents ₹500 crores in market opportunity. Eureka Forbes, with its brand recognition and distribution, is best positioned to capture this growth.

Second, the brand equity remains extraordinarily powerful despite recent challenges. "Aquaguard" is to water purifiers what "Xerox" was to photocopying—generic shorthand for the category. This mindshare, built over 40 years, would cost billions to replicate. Under professional management, this dormant asset is being activated through premium products, digital engagement, and service excellence. The brand's trust quotient with middle India remains unmatched.

Third, the distribution and service moat is wider than perceived. While e-commerce and D2C brands make noise, 70% of water purifier sales still happen offline where Eureka Forbes dominates. The service network—8,000 technicians, 400 centers—creates customer stickiness competitors can't match. As the market shifts toward smart, IoT-enabled purifiers requiring regular service, this infrastructure becomes more valuable, not less.

Fourth, the financial transformation under Pratik Pota validates the bull thesis. Six consecutive quarters of double-digit growth, EBITDA margins expanding from 6.3% to 11.7%, and a debt-free balance sheet demonstrate execution capability. The company has delivered good profit growth of 183% CAGR over the last five years. This isn't financial engineering; it's operational improvement with room to run.

Fifth, the Advent partnership provides resources and expertise to accelerate transformation. Unlike family promoters who might resist change, private equity ownership ensures professional management, capital for growth, and urgency in execution. Advent's global network brings technology partnerships, operational best practices, and eventual strategic buyers when exit time comes.

The bulls also point to strategic initiatives showing early success. The premium push with products like Aquaguard Glory is working—average selling prices up 20% year-over-year. The service business transformation from cost center to profit center is ahead of schedule. Digital sales growing at 50% annually from a small base suggest momentum in modern channels. Even the old direct sales force, retrained and digitally enabled, is showing productivity improvements.

Valuation, while optically expensive at 64x P/E, makes sense in context. Consumer companies with similar growth profiles and market opportunities trade at comparable or higher multiples. If Eureka Forbes achieves 15% revenue CAGR and 15% EBITDA margins—both achievable given market growth and operational leverage—the stock could double in three years. The risk-reward favors believers.

The Bear Case: Structural Challenges in a Commoditizing Market

The skeptics see a legacy player struggling to remain relevant in a fundamentally changed market. Their argument, equally compelling, rests on structural challenges that no amount of operational improvement can overcome.

First, the competition isn't just intense; it's coming from every direction with different business models. Kent RO attacks from above with superior marketing. Chinese brands attack from below with aggressive pricing. D2C brands like DrinkPrime attack with subscription models. Tech giants like Xiaomi attack with ecosystem plays. Urban Company attacks with service-led models. Each competitor exploits a different Eureka Forbes weakness.

The commoditization trajectory seems irreversible. Water purifiers are becoming like televisions or refrigerators—necessary appliances where brand matters less than price and features. Technology diffusion means every competitor has access to similar components. Chinese manufacturing ensures price points keep dropping. In commoditized markets, incumbents with high cost structures inevitably lose.

The customer acquisition cost mathematics don't work. Direct sales CAC exceeds ₹2,000 per customer in urban markets where competition is fiercest. Online CAC is rising as digital marketing costs inflate. Meanwhile, customer lifetime values are dropping as switching becomes easier and competition intensifies. The unit economics that sustained Eureka Forbes for decades are breaking down.

Promoters have pledged or encumbered 53.7% of their holding—a massive governance red flag. This pledge suggests Advent is financially stretched, potentially forcing premature exit or asset stripping. The zero dividend policy despite profitability confirms cash is being extracted through other means. Minority shareholders face asymmetric risk with limited upside participation.

The transformation execution risk is substantial. Cultural change in a 40-year-old organization takes years, not quarters. The sales force disruption could backfire—alienating traditional customers while failing to attract young ones. Technology investments might not generate returns in commoditizing markets. Management might be good but faces structural headwinds beyond their control.

Market penetration limits might be closer than bulls assume. Urban markets are saturating with multiple solutions—RO purifiers, packaged water, community RO plants. Rural markets lack purchasing power and infrastructure for traditional purifiers. The TAM might be large theoretically but addressable market for Eureka Forbes' products could be much smaller.

The bears also highlight warning signs in recent results. Revenue growth of 12% sounds impressive until you realize it's barely beating inflation plus market growth. Market share continues eroding despite all efforts. Margin expansion comes partly from cost cuts that might not be sustainable. The stock's volatility suggests institutional investors remain unconvinced.

The regulatory wildcard looms large. Government's Har Ghar Jal mission providing piped water could reduce purifier demand. Standards changes might obsolete existing inventory. Environmental regulations on water wastage could hurt RO technology. Any regulatory shift could devastate the investment thesis.

The Synthesis: A Calculated Bet on Execution

The truth, as often happens, lies between extremes. Eureka Forbes is neither the next Asian Paints nor the next Kodak. It's a company with real assets—brand, distribution, service network—facing real challenges—competition, commoditization, technological disruption. The outcome depends on execution quality, competitive dynamics, and some luck.

For growth investors comfortable with risk, Eureka Forbes offers an interesting speculation. The upside if transformation succeeds could be substantial—a double or triple in five years isn't impossible. But this requires everything going right: market growth continuing, competition remaining rational, execution remaining flawless, and exits happening at optimal valuations.

For value investors seeking safety, Eureka Forbes remains problematic. The promoter pledge, rich valuations, and competitive threats create multiple ways to lose money. Even if the business improves operationally, the stock might not follow if multiples compress or governance issues emerge.

For strategic buyers, Eureka Forbes might be attractive. The distribution network, service infrastructure, and customer base have value to adjacent players. A Whirlpool, Samsung, or even Reliance could extract synergies unavailable to financial buyers. But until Advent's exit timeline clarifies, strategic interest remains hypothetical.