Ethos Limited: Building India's Luxury Watch Empire

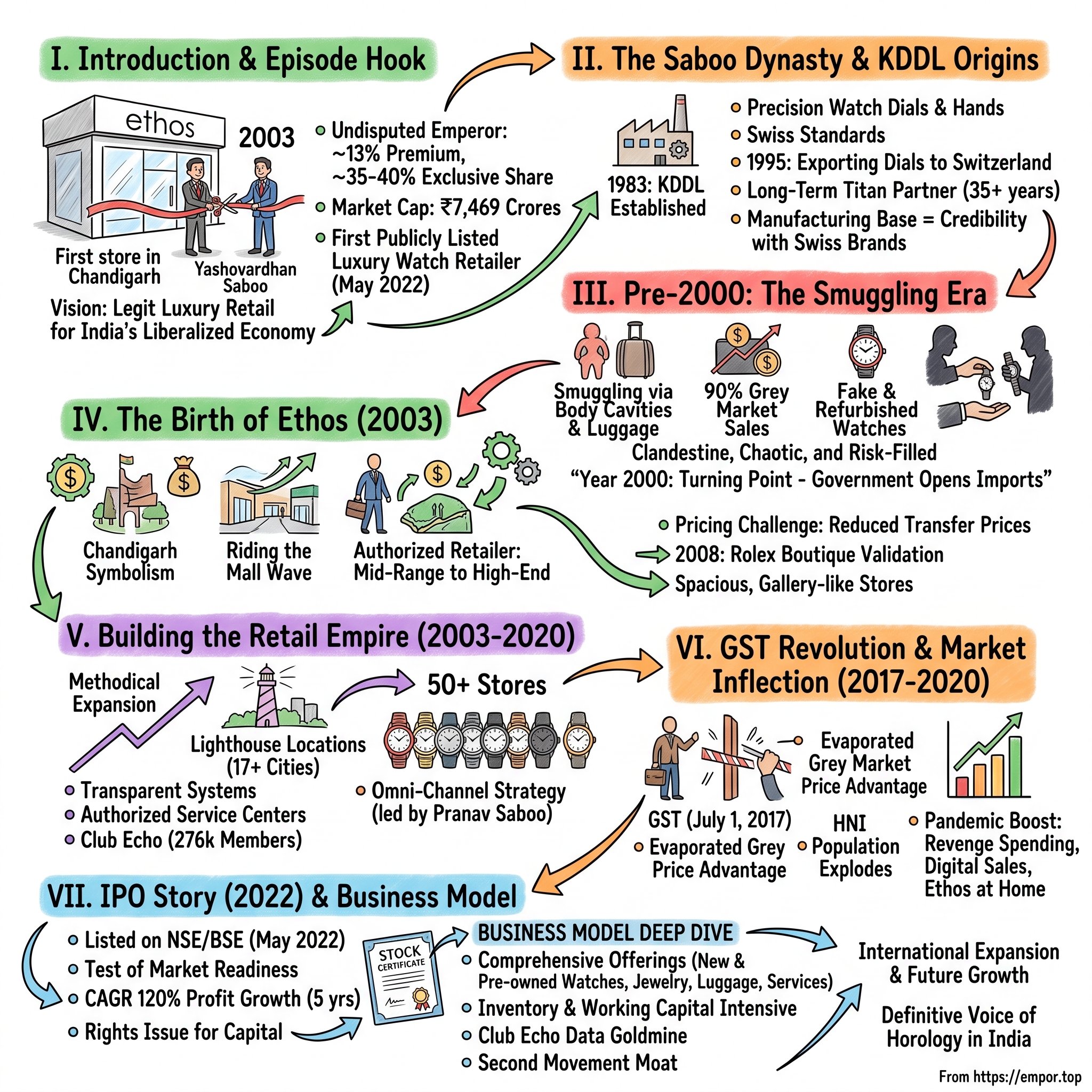

I. Introduction & Episode Hook

Picture this: It's 2003, and in the bustling streets of Chandigarh, a new kind of store is about to open its doors. Not another sari shop or electronics showroom, but something unprecedented in India's retail landscape—a legitimate luxury watch boutique. For decades, if you wanted a genuine Rolex or Omega in India, you had two choices: fly to Dubai or Singapore, or trust the shadowy networks of smugglers who controlled 90% of the premium watch market. That morning, as Yashovardhan Saboo cut the ribbon on the first Ethos store, he wasn't just opening a retail outlet. He was betting that India's newly liberalized economy would create a class of consumers who wouldn't just desire luxury—they'd demand it through legitimate channels.

Today, Ethos Limited stands as India's undisputed luxury watch emperor, commanding 13% of the entire premium and luxury segment and an astounding 35-40% share of the exclusive luxury tier. The company's journey from that single Chandigarh store to becoming India's first publicly listed luxury watch retailer in May 2022 reads like a masterclass in timing, trust-building, and transformation. With a market cap hovering around ₹7,469 crores, Ethos has become the bridge between Swiss craftsmanship and Indian aspiration.

But here's what makes this story remarkable: While Western luxury retailers were still debating whether India was "ready" for high-end retail, Saboo was already three moves ahead, building not just stores but an entire ecosystem. He understood something fundamental that others missed—India didn't need to be taught about luxury. The country that invented the concept of "shagun" (auspicious gifting) and where gold is stored by the kilogram in family vaults already understood value. What Indians needed was access, authenticity, and most importantly, respect.

The Ethos saga isn't just about selling expensive timepieces. It's about how a second-generation entrepreneur transformed his father's watch component manufacturing expertise into a retail empire that would redefine luxury consumption in the world's most populous nation. It's about navigating Byzantine import regulations, building trust in a market scarred by counterfeits, and convincing Swiss watchmakers that India deserved the same respect as Hong Kong or New York.

This episode traces the remarkable arc from KDDL's precision manufacturing roots through the smuggling era's wild west dynamics, to Ethos's current position as the gateway for over 70 luxury brands entering India. We'll explore how regulatory earthquakes like GST implementation and unexpected catalysts like COVID-19 accelerated a transformation that was decades in the making. Most intriguingly, we'll examine how a family business managed to go public while maintaining the personal touch that luxury demands—a balancing act that has eluded many global players.

II. The Saboo Dynasty & KDDL Origins

The year was 1980, and a fresh IIM Ahmedabad graduate named Yashovardhan Saboo faced the classic Indian middle-class dilemma: take a safe corporate job or venture into the uncertain world of entrepreneurship. Unlike the startup founders of today who chase unicorn valuations, Saboo was drawn to something almost quaint by modern standards—the intricate world of watch components. By 1983, he had established Kamla Dials and Devices Limited (KDDL), a name that would become synonymous with precision manufacturing in India's horological landscape.KDDL wasn't just another manufacturing venture—it was Saboo's calculated bet on India's nascent watch industry. The company started production of watch dials in 1983 in Parwanoo, India, and by 1990 had opened its second factory in Bengaluru. What set KDDL apart wasn't scale but precision. In an era when "Made in India" often meant compromise on quality, Saboo insisted on Swiss-level standards. The gamble paid off spectacularly when by 1995, KDDL expanded and began exporting dials to Switzerland—the horological equivalent of selling coal to Newcastle.

The relationship that would define KDDL's trajectory began in the mid-1980s when Titan, the Tata Group's ambitious watch venture, needed a reliable domestic supplier. For over 35 years, KDDL has been Titan's backbone, supplying the critical components that helped build India's first truly national watch brand. This wasn't just a vendor relationship; it was a symbiotic partnership that proved Indian manufacturing could meet global standards. Customers included major watch manufacturers like Titan, Allwyn, Timex, Bentex and HMT and exports to the European market.

But here's where Saboo's vision diverged from typical component manufacturers. While his peers were content being invisible suppliers, he saw KDDL as a stepping stone to something grander. The precision engineering expertise wasn't just about making watch hands and dials—it was about understanding the soul of horology. Every microscopic adjustment, every quality control process, every negotiation with Swiss suppliers taught Saboo what separated a timepiece from a luxury object.

KDDL Limited operates in India, Switzerland, and Hong Kong, manufacturing and trading watches and components. Their product range includes various types of watch dials and hands with intricate designs. They also provide precision stamping parts and tools for industries such as electrical, electronics, and automobile. This geographic spread wasn't accidental—it positioned KDDL at the intersection of Asian manufacturing efficiency and Swiss craftsmanship standards.

The financial architecture of KDDL reveals a company built for the long haul. With a market cap of ₹3,309 crores, the parent company has remained financially conservative, eschewing aggressive leverage for steady, self-funded growth. This prudence would prove crucial when Saboo decided to venture into retail—a capital-intensive business where many had failed spectacularly.

What's remarkable about the KDDL story is its timing. In the 1980s and 1990s, while India's software entrepreneurs were chasing the American dream through outsourcing, Saboo was quietly building manufacturing capabilities that would take decades to replicate. He understood that in luxury, provenance matters. Having a manufacturing base gave him credibility that pure retailers could never claim. When he walked into meetings with Rolex or Omega executives, he wasn't just another retailer asking for distribution rights—he was a fellow manufacturer who understood their language.

The transition from B2B component supplier to B2C luxury retailer might seem like a leap, but for Saboo, it was evolution. KDDL had given him two invaluable assets: deep relationships within the global watch industry and an intimate understanding of what makes a watch worth thousands of dollars. As the Indian economy liberalized and import restrictions began to ease, Saboo saw an opportunity that others missed. India didn't just need watch retailers—it needed trusted custodians of luxury. And who better to build that trust than someone who had spent two decades earning the respect of the Swiss watch establishment?

III. India's Watch Market Pre-2000: The Smuggling Era

The Dubai duty-free shop at midnight, circa 1995. Indian businessmen huddle around the Rolex counter, not browsing but negotiating bulk purchases. These weren't personal indulgences—they were inventory for India's vast grey market. Back home, these watches would pass through a byzantine network of dealers, each adding their margin and their own version of "authenticity." A genuine Omega might cost twice its Dubai price by the time it reached a customer in Delhi, assuming it was genuine at all. This was luxury retail in pre-liberalization India: clandestine, chaotic, and built entirely on personal relationships rather than brand guarantees.

Until about 2000, the Indian government's protectionist policies had created an absurd paradox. In a country where gold jewelry worth lakhs was routinely gifted at weddings, where maharajas had historically commissioned Cartier and Van Cleef & Arpels, importing a simple Swiss watch was illegal. The restriction wasn't just about luxury—even middle-tier brands like Tissot or Longines fell under the ban. Indian consumers who wanted to buy expensive watches had exactly two legal options: travel abroad or resign themselves to domestic brands like HMT or Allwyn.

But Indians, particularly the newly affluent class emerging from economic liberalization, weren't willing to settle. The result was a thriving smuggling economy that would make prohibition-era bootleggers proud. Conservative estimates suggest that 90% of luxury watches sold in India before 2000 came through illegal channels. Dubai and Singapore became the primary sourcing hubs, with watches hidden in everything from medicine bottles to television sets. The infamous "Dawood network" didn't just smuggle arms and drugs—they ran sophisticated watch smuggling operations that could deliver a Patek Philippe to your Mumbai doorstep within 48 hours of ordering.

The grey market wasn't just about availability; it had created its own twisted ecosystem. Mumbai's Heera Panna market became the epicenter, where "watch dealers" operated from tiny shops that looked like paan stalls but moved inventory worth crores. These weren't just smugglers—they were connoisseurs who could spot a fake Rolex from across the room and knew the serial numbers of every limited edition Audemars Piguet. Customers relied entirely on these dealers' reputation because there was no recourse if something went wrong. No warranties, no service centers, no returns. The counterfeit problem was perhaps even more insidious than smuggling. Refurbished watches were unregistered second hand watches which were polished and sold as new watches. Fake watches were replicas which look like the original watch especially when placed in a high end store, but will stop working within a few months or years. Compromised watches were genuine watches which have been tampered with replaced fake parts. A customer might pay ₹5 lakhs for what they believed was a genuine Cartier, only to discover years later when they tried to service it that half the movement was Chinese-made replacement parts.

The smuggling methods themselves became legendary in their creativity and occasional absurdity. Smuggled watches were brought into India through agents in terrible conditions—including methods of inserting them in plastic bags in bodily cavities. Such mistreatment reduced the life of the watch by damaging critical parts. Wedding parties returning from Dubai would distribute watches among family members, each wearing two or three timepieces to avoid suspicion. Business delegations would carry "sample" watches that somehow never made it back. The Heera Panna dealers developed relationships with customs officials, airline crew, and even diplomats who enjoyed immunity from searches.

What made this era particularly damaging wasn't just the illegality—it was how it warped the entire luxury ecosystem. Brands had no control over pricing, service, or even authenticity. A genuine Patek Philippe might sit next to a clever fake in the same dealer's safe, both offered with equal conviction. "The year 2000 was a turning point for the Indian watch market, as the government started to open the door to the import of luxury watches on a larger scale," says Yasho Saboo. "Before that, it was difficult to sell watches above 1,000 dollars without resorting to smuggling or the grey market."

The psychological impact was profound. For an entire generation of Indian luxury consumers, buying a high-end watch meant accepting risk as part of the transaction. You didn't just pay for the watch; you paid for the dealer's reputation, his connections, his ability to source "genuine" pieces. Trust became a currency more valuable than money itself. Stories circulated of prominent industrialists discovering their prized collections were entirely fake, or customs raids that destroyed millions in inventory overnight.

This environment created a unique Indian luxury consumer—skeptical, demanding, but also willing to pay premium prices for authenticity once trust was established. They became experts at spotting fakes, understanding serial numbers, and knowing which dealers had direct connections to Swiss suppliers versus those dealing in "Dubai specials." This hard-won expertise would become crucial when legitimate retail finally arrived. The Indian luxury consumer didn't need to be educated about watches—they needed to be convinced that legal channels were finally worth trusting.

IV. The Birth of Ethos (2003): Timing the Market Opening

The liberalization had begun, import restrictions were easing, but in 2003, the Indian luxury watch market was still a Wild West where legitimate players feared to tread. It was into this chaos that Yashovardhan Saboo launched Ethos, starting with a single store in Chandigarh—a city designed by Le Corbusier, the Swiss-French architect from La Chaux-de-Fonds, the heartland of Swiss watchmaking. The symbolism wasn't lost on Saboo. In 2003, Ethos opened its first luxury watch store in Chandigarh, where the company is based. Chandigarh is a "new city" with strong ties to Switzerland: it was planned by the famous architect Le Corbusier, who was born in La Chaux-de-Fonds. From the outset, Yasho Saboo made no secret of his ambition to go nationwide.

The timing seemed either brilliant or insane, depending on who you asked. Shopping malls—those air-conditioned temples of consumption that had transformed retail in the West—were just beginning to appear in India. The conventional wisdom among luxury brands was that Indians would never abandon their traditional bazaars for sterile Western-style retail environments. They were spectacularly wrong. The malls didn't just thrive; they became social destinations, places where the newly affluent could see and be seen. Ethos rode this wave, securing prime locations in these emerging retail cathedrals.

But location was just the beginning. The real challenge was convincing Swiss watchmakers that India deserved the same respect as established markets. While Ethos began by representing mid-range brands such as Rado, Longines, Tissot and TAG Heuer, it became a major beneficiary of this change. As a new player expanding through India's modern malls and airports, it offered the kind of prestigious presence the luxury Swiss brands were looking for. Gradually, the company started adding high-end watch companies to its portfolio, including Omega, Jaeger-LeCoultre, Hublot and Cartier.

The negotiation dynamics were fascinating. Brands were caught between opportunity and fear. On one hand, India represented a massive untapped market with a cultural affinity for luxury and gold. On the other, the grey market still controlled distribution, and brands worried about cannibalizing their duty-free sales in Dubai and Singapore, where Indians had traditionally shopped. Saboo's pitch was simple but powerful: give Indians the dignity of buying luxury in their own country, and they'll pay for it.

The brands' initial response was to treat India as a dumping ground for old inventory or to demand impossible minimum guarantees. But Saboo had an ace up his sleeve—his KDDL connection gave him credibility that pure retailers lacked. When he met with brand executives, he could discuss escapement wheels and hairspring assemblies with the fluency of someone who'd spent decades in manufacturing. This wasn't just another businessman trying to cash in on luxury; this was a fellow craftsman who understood the soul of horology.

The pricing challenge was particularly complex. Import duties and taxes meant that a watch could cost 40-50% more in India than in Dubai. To make matters worse, Indians were seasoned international travelers who knew exactly what these watches cost elsewhere. The solution came through creative negotiations with brands. Swiss manufacturers began accommodating the high import tariffs by exporting to India at reduced transfer prices, effectively subsidizing the duties to keep retail prices competitive. This wasn't charity—it was a calculated investment in building a legitimate market that could eventually rival China.

Another important turning point would come in 2008, through a partnership with Rolex. "We set up their first boutique in Bangalore," explains Yasho Saboo. Landing Rolex was more than just adding another brand; it was a validation of Ethos's entire model. Rolex, notorious for its selective distribution and exacting standards, didn't partner with just anyone. Their endorsement sent a signal to the entire Swiss watch industry: India was open for business, and Ethos was the gateway.

The early stores themselves were revelations. In an era when Indian retail meant cramped spaces with inventory stacked to the ceiling, Ethos stores were spacious, minimalist, almost gallery-like. Each watch had room to breathe, to be appreciated as an object of art rather than just merchandise. The staff weren't salespeople but "watch consultants" who could spend hours discussing complications and movements without pushing for a sale. This patient, educational approach was revolutionary in Indian retail.

But perhaps Saboo's most brilliant insight was understanding that in India, luxury purchase is rarely an individual decision. While Western brands focused on the individual consumer, Ethos designed its entire experience around the Indian reality of collective decision-making. Comfortable seating for family members, private viewing rooms for extended discussions, even tea and snacks for the entourage that inevitably accompanied major purchases. The stores became theaters where the drama of luxury acquisition could play out with proper dignity.

The first few years were brutal. Despite the buzz, actual sales were modest. The grey market dealers spread rumors that Ethos watches were overpriced, that warranties were worthless, that smart buyers still went to Dubai. Some brands grew impatient, threatening to revoke distribution rights if sales didn't improve. But Saboo persisted, understanding that he wasn't just building a retail chain—he was rewiring decades of consumer behavior.

V. Building the Retail Empire (2003-2020)

By 2010, seven years after opening its first store, Ethos had reached an inflection point. The company wasn't just surviving; it was defining what luxury retail meant in India. The expansion strategy was methodical, almost surgical in its precision. Rather than rushing to blanket the country with stores, Saboo focused on what he called "lighthouse locations"—flagship stores in key cities that would serve as beacons for the brand. Each new store opening was an event, often attended by Swiss brand ambassadors and local celebrities, creating buzz that no amount of advertising could buy.

The numbers tell only part of the story: from one store in 2003 to over 50 stores across 17 cities by 2020. But what's remarkable is how each expansion was calibrated to local market dynamics. The Mumbai stores catered to old money and Bollywood, with special emphasis on complicated pieces and limited editions. Bangalore, with its tech millionaires, saw more demand for sporty, contemporary designs. Delhi wanted visible luxury—the bigger, the bolder, the better. Each store became a reflection of its city while maintaining the Ethos standard of service.

Building trust in a market scarred by decades of grey market dealings required more than just nice stores and authentic products. With our strong transparent systems, we ensure that every watch sold at Ethos is legally brought into India, bought directly from the brand. Ethos launched an aggressive education campaign, not just about watches but about the dangers of the grey market. Ethos Watch Boutiques will never indulge in any malpractice and has launched a massive campaign against them. Ethos plans to educate 2,000,000 consumers by the end of 2016.

The brand portfolio expansion was equally strategic. Ethos became an authorized retailer for over 70 luxury watch brands, with over 30 brands available exclusively through their stores in India. This exclusivity wasn't just about market control—it was about creating destinations. If you wanted a Baume & Mercier or a Carl F. Bucherer in India, Ethos was your only option. This forced even skeptical luxury consumers to experience the Ethos difference.

The service infrastructure that Ethos built was perhaps its most underappreciated achievement. In a country where "warranty" often meant a piece of paper with no real backing, Ethos established authorized service centers that could handle everything from battery replacements to complicated movement repairs. They brought Swiss-trained technicians to India, invested in specialized equipment, and even created a system for sending complicated repairs directly to Switzerland with full tracking and insurance. This after-sales commitment converted skeptics into evangelists. The digital transformation, led by Pranav Saboo, second-generation entrepreneur and CEO, represented another critical evolution. Pranav started his entrepreneurial journey at the age of 22 by setting up Dream Digital Technology Limited, which now serves as a digital marketing and technology solutions provider to some of the largest MNCs in India. His passion for the digital world has led the digital initiative for Ethoswatches.com, which transformed Ethos into a truly omni-channel business. This wasn't just about launching a website—it was about creating India's first credible online luxury watch platform in a market where even buying a ₹10,000 product online was considered risky.

The omnichannel approach solved a uniquely Indian challenge. While stores in metros thrived, tier-2 and tier-3 cities presented a paradox: wealthy consumers existed, but not in sufficient density to justify physical stores. The digital platform allowed a businessman in Coimbatore or a doctor in Lucknow to access the same selection as someone in Mumbai. More importantly, it provided price transparency in a market long plagued by arbitrary markups.

By 2015, Ethos had become more than a retailer—it had become an institution. The company nurtures a vibrant watch community through frequent event hosting and facilitates the development of exclusive limited-edition watches, exclusively available at Ethos, for the Indian market. These weren't just sales events but cultural moments—Swiss watchmakers flying in for masterclasses, collectors gatherings that felt more like art exhibitions than retail promotions, limited editions created specifically for the Indian market.

The loyalty program, Club Echo, with 276,000 registered members, became a data goldmine that helped Ethos understand the evolving Indian luxury consumer. The insights were revealing: Indians didn't just buy watches for themselves but as gifts for business partners, wedding presents, and success markers. The average Ethos customer owned 3.7 luxury watches, higher than global averages, suggesting that once trust was established, Indians became serious collectors, not just occasional buyers.

The pre-owned segment launch through "Second Movement" was particularly bold. In a culture where "second-hand" carried stigma, Ethos reframed pre-owned watches as "vintage" and "collectible." Second Movement (powered by Ethos) is India's most trusted destination to buy and sell certified pre-owned luxury watches. This wasn't just about capturing another revenue stream—it was about creating liquidity in the luxury watch market, allowing customers to trade up, building a complete ecosystem rather than just a retail chain.

VI. The GST Revolution & Market Inflection (2017-2020)

July 1, 2017, midnight. As India launched its most ambitious tax reform since independence—the Goods and Services Tax (GST)—few understood its implications for the luxury market as clearly as the team at Ethos. For decades, India's byzantine tax structure had created massive arbitrage opportunities. A watch bought in Delhi faced different taxes than one bought in Mumbai. The grey market thrived on these differentials, moving inventory across state borders like bootleggers during Prohibition. GST changed everything overnight.

Demand for luxury watches in India started picking up pace about 7 years ago after a nationwide GST was introduced, per-capita income hit a new high, and the number of HNIs started to grow. The uniform tax structure didn't just level the playing field—it fundamentally altered the economics of luxury retail. Suddenly, the grey market's price advantage evaporated. Legal retailers could compete on price while offering something the grey market never could: authenticity, warranty, and dignity.

The numbers were staggering. In the first year post-GST, Ethos saw a 35% increase in walk-ins. More tellingly, the average transaction value increased by 40%. Customers who had previously bought entry-level pieces to "test" the legitimate market were now comfortable making significant purchases. The psychological barrier had been broken—buying luxury legally was no longer a tax on honesty.

But GST was just one piece of a larger transformation. India's high-net-worth individual (HNI) population was exploding. McKinsey estimated that the number of Indian households earning over $100,000 annually would triple between 2015 and 2025. These weren't just wealthy Indians—they were globally exposed, digitally savvy, and increasingly confident consumers who benchmarked their lifestyles against global standards, not local ones.

The more remarkable growth started after the pandemic due to an evolution in the luxury buying behaviour of Indian consumers. COVID-19 didn't just accelerate digital adoption—it fundamentally rewired luxury consumption patterns. Unable to travel internationally, wealthy Indians redirected their luxury spending domestically. The revenge spending phenomenon that followed lockdowns wasn't just about pent-up demand—it was about a new appreciation for tangible luxury in an increasingly uncertain world. The pandemic's impact on Ethos was counterintuitive. While initial lockdowns decimated retail, the recovery was spectacular. Pranav Saboo's digital investments paid off as online sales exploded. More importantly, the psychology of luxury consumption shifted. Unable to spend on international travel and experiences, wealthy Indians redirected budgets toward tangible luxury. Watches, being both investment and indulgence, became the perfect pandemic purchase.

Ethos's response was swift and strategic. They launched virtual consultations, where customers could explore collections via video calls with watch consultants. They created "private shopping experiences" where entire families could book stores for exclusive viewings. Most innovatively, they launched "Ethos at Home," bringing selections directly to customers' residences—a service that would have been unthinkable pre-pandemic but became a differentiator in the new normal.

The data tells a remarkable story: India's luxury market, currently valued at $17 billion, is set to more than triple by 2030, growing to upwards of $85 billion. The number of ultra-high-net-worth individuals—people with a net worth of at least $30 million—is anticipated to grow by 50 percent by 2028. There are over 850,000 HNIs, defined as individuals with investable assets of $1 million and above. The number is expected to rise further to 1.65 million by 2027.

What made this period transformative wasn't just the numbers but the nature of demand. Pre-GST, luxury watch purchases were often transactional—buying for occasions, gifting for business relationships. Post-GST and especially post-pandemic, Indians began collecting. They started understanding complications, appreciating craftsmanship, building themed collections. The average transaction value at Ethos stores increased not just because people were buying more expensive watches, but because they were buying multiple pieces in single transactions.

The regulatory environment continued to evolve favorably. While import duties remained high, the government's focus on ease of doing business meant fewer bureaucratic hurdles. Digital payments became ubiquitous, making large-value transactions smoother. Most importantly, the cultural perception of luxury shifted from indulgence to investment, especially as traditional investment avenues like real estate became less attractive.

VII. The IPO Story & Public Markets (2022)

May 30, 2022, 9:15 AM, National Stock Exchange, Mumbai. As the opening bell rang, Ethos Limited became the first luxury watch retailer in India to trade on public markets. The IPO, priced at ₹836-878 per share, was a test of whether Indian capital markets were ready to value a luxury retailer—a sector traditionally viewed as volatile and discretionary. The 3.93x subscription rate provided the answer: investors saw Ethos not just as a retailer but as a proxy for India's luxury consumption story.

The decision to go public wasn't driven by capital needs alone. With a debt-free balance sheet and positive cash flows, Ethos could have continued as a private company. The IPO was about institutionalizing excellence, creating liquidity for early investors, and most importantly, sending a signal to global luxury brands that Ethos was here for the long haul. Public listing meant quarterly scrutiny, sure, but it also meant transparency that luxury brands valued when choosing distribution partners.

The use of IPO proceeds revealed strategic thinking. Rather than aggressive store expansion, Ethos focused on inventory depth, technology infrastructure, and working capital optimization. The inherently working-capital intensive nature of the company's business requires maintaining adequate inventory across various watch segments to maintain brands' standard of displaying products. This wasn't just about having stock—it was about having the right stock, the limited editions, the complications that serious collectors sought.

Post-IPO performance validated the strategy. Company has delivered good profit growth of 120% CAGR over last 5 years. The stock's performance, while volatile like all luxury retail globally, showed resilience during market corrections, suggesting investors viewed it as a long-term structural play rather than a cyclical bet. The June 2025 rights issue announcement marked another inflection point. Board approved a rights issue of 22,77,250 fully paid-up equity shares at Rs 1,800 each, totaling up to Rs 409.90 crore. The entitlement ratio of 4:43 (4 rights shares for every 43 held) was designed to raise capital without excessive dilution. Importantly, promoters Yashovardhan Saboo, KDDL Ltd, and Mahen Distribution Ltd reaffirmed their commitment to exercise their rights entitlement fully, signaling confidence in the company's trajectory.

The capital allocation philosophy revealed through public market actions showed remarkable discipline. Rather than chasing growth at any cost—a temptation for newly listed companies—Ethos focused on sustainable expansion. The primary objective of the rights issue is to raise funds for the company's working capital requirements, in support of its expansion plans and diversification strategy. This wasn't growth for growth's sake but strategic capacity building.

ICRA has reaffirmed Ethos Ltd's long-term credit rating at A+ with stable outlook, providing external validation of the company's financial prudence. In an industry where competitors often leveraged aggressively during boom times, Ethos maintained a conservative balance sheet that could weather luxury market's inherent volatility.

The public market journey also forced operational improvements. Quarterly reporting meant inventory turns, same-store sales growth, and gross margins were scrutinized. This transparency, initially seen as a burden, became a competitive advantage. Brands appreciated the financial discipline, landlords valued the creditworthiness, and employees benefited from stock options that aligned their interests with shareholders.

What's particularly noteworthy is how Ethos managed investor expectations in a volatile sector. Luxury retail globally trades at discounts to broader retail due to cyclicality concerns. Yet Ethos has commanded premium valuations, suggesting investors view it less as a discretionary retailer and more as infrastructure for India's inevitable luxury market expansion.

VIII. Business Model Deep Dive

The elegance of Ethos's business model lies in its comprehensiveness. The company offers luxury and premium watches; pre-owned watches; jewellery and jewellery boxes; watch straps and winders; clocks; collector boxes; and luxury luggage. It also provides product repair and services. This isn't just product diversification—it's ecosystem building. A customer might enter for a battery replacement and leave with a limited edition timepiece.

The economics reveal both the opportunity and challenge of luxury retail in India. Gross margins typically range between 20-25%, lower than global luxury retail standards of 35-40%, compressed by India's high import duties and operational costs. Yet EBITDA margins of 8-10% compare favorably with international peers, achieved through operational efficiency and scale advantages. The key insight: in India, you make money on volume and velocity, not just margin.

Inventory management represents the most complex challenge. The inherently working-capital intensive nature of the company's business requires maintaining adequate inventory across various watch segments to maintain brands' standard of displaying products. A Rolex boutique must display the full range even if certain models take years to sell. A Patek Philippe corner requires millions in inventory that might turn just twice annually. This isn't inefficiency—it's the cost of credibility in luxury retail.

Second Movement (powered by Ethos) deserves special attention as a strategic masterstroke. In a market where pre-owned meant suspicious, Ethos reframed it as "certified pre-owned," borrowing from the automotive playbook. The business serves multiple purposes: it provides liquidity for customers wanting to upgrade, offers entry points for aspirational buyers, and most crucially, keeps customers within the Ethos ecosystem rather than losing them to grey market dealers when they want to sell.

The service center infrastructure represents hidden value. With state-of-the-art facilities and Swiss-trained technicians, Ethos doesn't just service watches—it builds lifetime relationships. A luxury watch requires servicing every 3-5 years, costing anywhere from ₹20,000 to ₹200,000. Each service visit is an opportunity for upgrade discussions, new purchases, or referrals. The service database becomes a goldmine of customer intelligence.

Club Echo, the loyalty program with 276,000 registered members, transcends traditional retail loyalty. Members don't just accumulate points—they gain access to exclusive launches, Swiss factory visits, horological masterclasses, and private sales. The program creates a community, not just a customer base. Data shows Club Echo members purchase 2.3x more frequently than non-members and have 40% higher average transaction values.

The omnichannel integration, spearheaded by Pranav Saboo, represents the future of luxury retail. Online contributes nearly 20% of sales, remarkable for a category where touch-and-feel traditionally dominated. But digital isn't just about transactions—it's about discovery, education, and community building. The website serves 10x more visitors than stores could ever accommodate, each interaction building brand equity even if immediate conversion doesn't occur.

Exclusive limited editions created specifically for the Indian market showcase sophisticated brand management. These aren't just special dial colors but thoughtfully crafted pieces that celebrate Indian occasions, partnerships, or milestones. A limited edition for Diwali, a special series for India's space achievements, collaborations with Indian artists—each creates scarcity, urgency, and most importantly, local relevance in a global luxury context.

The working capital cycle reveals both risk and moat. With 180-200 days of inventory and 30-45 day payment terms to brands, Ethos essentially finances the entire value chain. This capital intensity deters new entrants but also means that growth requires continuous capital infusion. The recent rights issue addresses this structural requirement while maintaining balance sheet strength.

What's underappreciated is the data advantage Ethos has accumulated. Two decades of transaction data across price points, brands, and customer segments provides insights no competitor can replicate. Which complications sell in Bangalore versus Delhi? What's the upgrade path from a ₹2 lakh watch to a ₹20 lakh piece? This intelligence drives everything from inventory planning to store locations to brand negotiations.

IX. International Expansion & Future Growth

The Dubai acquisition announced in 2025 marks Ethos's transformation from Indian retailer to regional player. Ethos Ltd has acquired 100% equity in Ficus Trading LLC, a newly incorporated subsidiary in Dubai, to strengthen its trading operations in the Middle East. This isn't just geographic expansion—it's strategic positioning in the global luxury supply chain. Dubai's free trade zones, zero corporate tax, and position as the grey market capital make it the perfect laboratory for Ethos's international ambitions.

The Middle East expansion serves multiple strategic objectives. First, it provides access to inventory at better prices, improving sourcing flexibility. Second, it positions Ethos to serve the massive Indian diaspora in the Gulf, who represent significant luxury consumption. Third, it offers learnings from a mature luxury market that can be applied back in India. International expansion in Dubai will continue to support the company's margin profile through better sourcing and the ability to participate in global inventory allocation.

Domestic expansion plans remain aggressive yet calculated. Ethos is set to unveil an additional 30 to 35 stores across new and existing cities as part of its expansion stride. But this isn't just about store count—it's about market deepening. Second stores in existing cities, smaller format boutiques for specific brands, airport locations for travel retail—each format serves distinct customer occasions and economics.

The India opportunity remains massive and underpenetrated. In India luxury watch market accounted for 24% of overall watch market whereas globally average stands to be 59%. This gap represents not just opportunity but inevitability. As India's per capita income crosses $3,000 and heads toward $5,000 by 2030, luxury consumption typically inflects. Ethos is positioned to capture this secular trend.

Competition is intensifying but in predictable ways. Reliance's luxury retail ambitions, Tata's expansion through Titan and acquisitions, and pure-play online competitors like Zimson and Kapoor Watch Company are all vying for share. Yet Ethos's first-mover advantage, brand relationships, and trust moat create significant barriers. The luxury watch market isn't winner-take-all—it's about carving out profitable niches and defending them with service and selection.

The technology integration roadmap reveals ambition beyond traditional retail. Augmented reality for virtual try-ons, blockchain for authentication, AI for personalization—Ethos is experimenting with all. But technology is viewed as an enabler, not a replacement for human touch. The future Ethos store might use AI to predict preferences, but a human consultant will still guide the purchase journey.

Market dynamics favor consolidation. Standalone watch retailers struggle with working capital, brand access, and scale economics. Ethos's war chest from the rights issue positions it for strategic acquisitions. Rolling up regional players, acquiring distressed competitors, or partnering with international retailers entering India—all paths remain open.

The demographic dividend is just beginning. India adds 10-12 million people to its workforce annually. The average luxury watch buyer is 35-45 years old. The cohort entering prime earning years over the next decade will be larger, wealthier, and more globally exposed than any before. This isn't speculation—it's demographic destiny.

Saboo expressed confidence in the unprecedented growth of India's watch market, while advocating a localised approach and cautioning against drawing comparisons to China's market dynamics. India's luxury evolution will follow its own path—less ostentatious than China, more value-conscious than the West, deeply rooted in occasions and relationships rather than pure status signaling.

X. Playbook: Building Luxury Retail in Emerging Markets

Trust emerges as the fundamental currency in Ethos's playbook. In developed markets, luxury retail competes on selection and service. In emerging markets, particularly those scarred by grey markets, authenticity becomes the primary differentiator. Every Ethos initiative—from Swiss service centers to certificate guarantees to brand partnerships—builds this trust architecture. The lesson: in markets transitioning from informal to formal luxury retail, reputation is everything and takes decades to build but moments to destroy.

Being first mover with credibility created compounding advantages. Ethos wasn't the first luxury watch retailer in India, but it was the first to operate at scale with international standards. This timing—late enough to avoid market education costs but early enough to shape consumer behavior—proves crucial. The playbook suggests entering emerging luxury markets just as regulatory frameworks formalize but before international competition arrives in force.

Brand relationship management in emerging markets requires delicate balancing. Global brands want growth but fear dilution. They demand minimum guarantees but won't provide exclusive territories. Ethos's solution: make yourself indispensable through market intelligence, operational excellence, and by becoming the brands' educator about local nuances. When Rolex executives want to understand Indian luxury consumers, they call Ethos. This advisory role transcends typical retailer-brand dynamics.

The exclusive limited edition strategy deserves emulation. Ethos nurtures a vibrant watch community through frequent event hosting and facilitates the development of exclusive limited-edition watches, exclusively available at Ethos, for the Indian market. These editions serve multiple purposes: they demonstrate market clout to brands, create urgency for customers, and most importantly, generate margin-accretive sales. The playbook: use exclusives to move from commodity retailer to curator.

Building for long-term value versus quarterly earnings pressure represents the central tension for public luxury retailers. Luxury requires patient capital—inventory builds slowly, brand relationships develop over years, customer trust accumulates over decades. Yet public markets demand quarterly progress. Ethos's solution: transparent communication about the business model's inherent characteristics while delivering consistent if not spectacular growth.

Family business dynamics intersected with professional management create unique advantages in luxury retail. The Saboo family's continued involvement signals long-term commitment to brands and customers. Yet professional management ensures operational discipline. This hybrid model—family vision with professional execution—resonates in emerging markets where relationships still matter but scale demands process.

The verticalization strategy—from retail to service to pre-owned to eventually perhaps manufacturing—creates competitive moats. Each additional vertical doesn't just add revenue but strengthens the core retail business. Service creates touchpoints, pre-owned provides liquidity, exclusive editions demonstrate market power. The playbook: view luxury retail as an ecosystem, not a transaction.

Localization without losing global appeal requires careful calibration. Ethos stores feel international yet Indian. Marketing speaks to local occasions while maintaining luxury aspiration. Pricing respects global standards while acknowledging local realities. This balance—global enough for brands, local enough for customers—defines successful emerging market luxury retail.

The community building approach transcends traditional marketing. Ethos doesn't just sell watches—it cultivates collectors. Events aren't sales promotions but cultural moments. The company positions itself as educator, curator, and convenor of India's horological community. In emerging markets where luxury knowledge is still developing, this educational role creates deep customer loyalty.

XI. Analysis: Bear vs. Bull Case

The Bull Case:

Ethos sits at the intersection of multiple structural tailwinds that could drive 15-20% compound growth for the next decade. The Market Cap of ₹7,469 Cr represents just 0.4% of India's projected 2030 luxury market, suggesting massive headroom. With ICRA's reaffirmation of an A+ rating with stable outlook, the balance sheet can support aggressive expansion without dilution beyond the current rights issue.

India's luxury penetration story has barely begun. At 24% of the overall watch market versus 59% globally, the category could double even without market growth. Add India's demographic dividend—500 million people entering middle class by 2030—and the runway appears endless. Ethos's 35-40% share of exclusive luxury segment creates winner-take-all dynamics in the most profitable tier.

The brand portfolio moat deepens annually. With over 30 exclusive brands and relationships spanning decades, replicating Ethos's position would require not just capital but time that competitors don't have. These aren't vendor relationships but partnerships where Ethos influences product development, pricing, and market strategy.

Operational leverage is just beginning to manifest. With fixed costs spread across 50+ stores, incremental sales drop disproportionately to bottom line. The rights issue funds working capital, not opex, suggesting margin expansion as inventory turns improve. Digital contributing 20% of sales at higher margins provides another profit lever.

The Dubai expansion opens new vectors for value creation. Beyond supporting margins through better sourcing, international operations position Ethos for the eventual Indian luxury market opening to foreign investment. When global luxury retailers inevitably enter India directly, Ethos could be an acquisition target at substantial premiums.

The Bear Case:

The company is exposed to forex fluctuation risk, as a substantial portion of its products is imported. A 10% rupee depreciation could wipe out annual profits unless passed to consumers, which might dampen demand. With luxury watches priced in Swiss francs and dollars, currency volatility represents unhedgeable risk.

Competition from domestic players and international markets in the retail segment intensifies quarterly. Reliance's luxury ambitions, Tata's expansion, and direct-to-consumer strategies from brands themselves threaten market share. As the market matures, brands might prefer owned boutiques over multi-brand retailers, potentially disintermediating Ethos.

High working capital requirements create a perpetual funding need. Despite profitable operations, cash generation remains weak due to inventory builds. The business model essentially requires shareholders to continuously fund growth, making returns on equity structurally challenged. This capital intensity might limit dividend potential and shareholder returns.

Discretionary spending vulnerability could manifest suddenly. Luxury watches are perhaps the most discretionary purchase possible. Any economic slowdown, market correction, or even sentiment shift could freeze demand instantly. Unlike essential retail that might see gradual decline, luxury can evaporate overnight as seen during 2008 and briefly during COVID.

Platform competition from online players operating asset-light models poses disruption risk. While Ethos has built omnichannel capabilities, pure-play digital competitors with lower cost structures might cherry-pick profitable segments. The younger generation's comfort with online luxury purchases could erode Ethos's physical store advantage.

Regulatory risks around luxury consumption remain. India's relationship with conspicuous consumption is complex. Populist policies targeting luxury goods through higher taxes, import restrictions, or even cultural campaigns against inequality could impact demand. The business operates at the intersection of aspiration and social sensitivity.

The Synthesis:

The truth likely lies between extremes. Ethos has built a formidable position in an attractive market, but structural challenges around capital intensity and competition remain. The company's success will depend on execution excellence rather than market tailwinds alone. The rights issue provides runway, but returns on that capital will determine whether the bull or bear case prevails.

XII. Epilogue: The Future of Luxury in India

As we stand in 2025, looking toward 2030 and beyond, Ethos's story becomes inseparable from India's luxury evolution. Saboo's vision of democratizing luxury access while maintaining exclusivity standards has largely succeeded. The company that started with a single store in Chandigarh now shapes how Indians perceive, purchase, and prize luxury timepieces.

The next generation of Indian luxury consumers presents both opportunity and challenge. Gen Z Indians, digitally native and globally conscious, view luxury differently than their parents. For them, sustainability matters as much as status. Experiences compete with products. Pre-owned isn't inferior but intelligent. Ethos's evolution must mirror these shifting sensibilities while serving existing collectors who value tradition.

Technology integration will accelerate but not dominate. The metaverse boutique, NFT authentication, AI-powered curation—all will emerge. Yet the fundamental human desire for recognition, achievement marking, and tangible beauty that drives luxury watch purchases remains unchanged. Ethos's challenge: embrace technology without losing the human touch that defines luxury service.

What success looks like in 2030: Ethos operating 100+ stores across India and the Middle East, with digital contributing 40% of sales. The company as a ₹3,000 crore revenue business with 12-15% EBITDA margins. More importantly, Ethos as the definitive voice of horology in India—not just retailer but cultural institution that shaped how the world's largest population appreciates mechanical artistry.

The broader implications extend beyond business metrics. Ethos's success validates that emerging markets can build world-class luxury retail without compromising standards. It proves that trust, patience, and respect for local nuances can triumph over pure capital deployment. Most significantly, it demonstrates that luxury in India isn't about westernization but about celebrating excellence in forms that resonate locally.

As Saboo noted, while advocating a localised approach and cautioning against drawing comparisons to China's market dynamics, India's luxury journey will be unique. Less ostentatious perhaps, more value-conscious certainly, but ultimately creating the world's largest luxury market by volume if not value. In that future, Ethos won't just be a participant but an architect of India's luxury landscape.

The watch industry itself faces existential questions. Smart watches threaten traditional timepieces. Younger consumers question the relevance of mechanical movements. Yet history suggests luxury evolves rather than evaporates. The quartz crisis of the 1970s nearly killed mechanical watches, yet they returned stronger, positioned as art rather than utility. Ethos's bet: mechanical watches will remain relevant as markers of achievement, appreciation of craft, and connections across generations.

The final insight returns to where we began—trust. In an increasingly digital, ephemeral world, luxury watches represent permanence. They mark moments, celebrate success, and transfer wealth across generations. Ethos's role transcends retail—it's the custodian of these moments for Indian consumers. Building that trust took two decades. Maintaining it will determine the next two.

For investors, entrepreneurs, and observers of India's economic transformation, Ethos offers lessons beyond luxury retail. It demonstrates that serving aspirational consumption in emerging markets requires more than importing Western models. Success demands patient capital, local insight, and most crucially, respect for customers navigating their own luxury journeys. In that sense, Ethos isn't just building India's luxury watch empire—it's writing the playbook for how emerging markets embrace and eventually define global luxury.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube