Endurance Technologies: The Aluminum King's Global Auto Components Empire

I. Introduction & Episode Setup

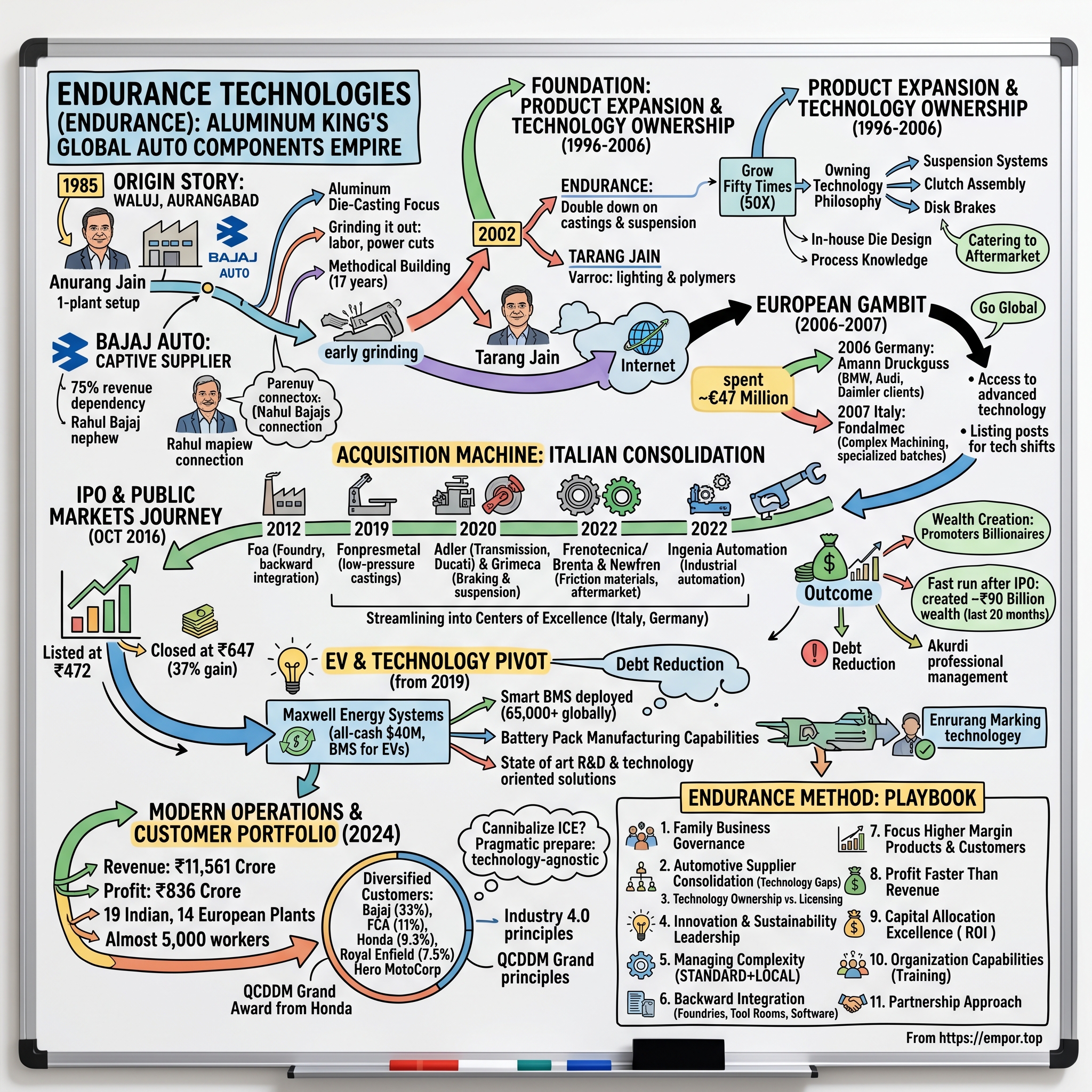

Picture this: A sprawling 200-acre manufacturing complex in Aurangabad, Maharashtra. The year is 2024. Inside one of the massive warehouses, a 2,700-ton die-casting press—the size of a small building—thunders to life, injecting molten aluminum into precision molds at temperatures exceeding 700°C. In seconds, what emerges is a critical engine component that will find its way into a BMW motorcycle cruising the Autobahn, or perhaps a Royal Enfield thundering through the Himalayas. This is Endurance Technologies at work—a company that has quietly become the aluminum die-casting powerhouse of India while building a formidable European empire through calculated acquisitions.

The numbers tell a remarkable story: ₹35,409 Crore market capitalization, 19 plants scattered across India, 14 more dotting the European landscape from Germany to Italy. Annual revenues touching ₹11,561 Crore with profits of ₹836 Crore. But these figures only hint at the deeper narrative—how a company that began as a captive supplier to Bajaj Auto transformed itself into India's largest aluminum die-casting company and a global Tier-1 automotive supplier serving everyone from Porsche to Hero MotoCorp.

The central question that drives our exploration today isn't just how Endurance achieved this scale—it's how a family business, born from the complex dynamics of India's most prominent automotive clan, managed to break free from its origins while maintaining the very relationships that birthed it. This is a story of strategic focus meeting family politics, of European acquisitions meeting Indian manufacturing prowess, and ultimately, of how aluminum castings became the foundation for a global automotive components empire.

What makes Endurance particularly fascinating is its timing. The company's evolution mirrors India's own automotive journey—from license raj to liberalization, from Bajaj scooters to BMW motorcycles, from mechanical components to battery management systems for electric vehicles. Each phase of Endurance's growth reveals not just corporate strategy but the changing face of Indian manufacturing itself.

Over the next several hours, we'll dissect how Anurang Jain, starting with family connections and a single plant in Aurangabad, built what is today one of India's most successful auto component companies. We'll explore the strategic decisions that turned a regional supplier into a global player: the bold European acquisitions starting in 2006, the technology ownership philosophy that drove margin expansion, the calculated IPO that created billions in wealth, and the current pivot toward electrification that may define its next chapter.

Three themes will emerge repeatedly in our analysis. First, the delicate dance of family business dynamics in Indian corporate culture—how being Rahul Bajaj's nephew opened doors but also created dependencies that had to be carefully unwound. Second, the relentless focus on aluminum die-casting and suspension systems that gave Endurance its competitive moat while others chased diversification. And third, the art of automotive supplier consolidation—how Endurance became an acquisition machine in Europe, rolling up capabilities from Italy to Germany in a way few Indian companies have successfully executed.

This isn't just a business story—it's a playbook for how Indian manufacturing companies can compete globally, how family businesses can professionalize without losing their entrepreneurial edge, and how strategic patience in building capabilities can trump financial engineering. As we'll see, Endurance's journey from Waluj to the world stage offers lessons that extend far beyond the auto components sector.

II. The Origin Story: Family, Bajaj, and Breaking Away

The conference room at Bajaj Auto's Akurdi plant in November 1985 must have been thick with familial tension. On one side sat Rahul Bajaj, the legendary industrialist who had turned his grandfather's company into India's scooter king. On the other, his nephew Anurang Jain, barely 32 years old, presenting plans for a new aluminum die-casting venture. Between them—unspoken but palpable—was the weight of family expectations, the promise of guaranteed orders, and the complex dynamics that define Indian business dynasties.

Anurang wasn't arriving empty-handed or without pedigree. His father, Naresh Chandra Jain, had already proven himself in the auto components space by founding Varroc. His mother, Suman, was Rahul Bajaj's sister—a connection that meant everything in the relationship-driven world of 1980s Indian manufacturing. But what made this moment particularly intriguing was that Anurang wasn't alone in his ambitions. His identical twin brother Tarang sat beside him, both brothers united in their vision to build something of their own.

The company they founded was initially called Anurang Engineering—a straightforward name that reflected both ownership and ambition. The first plant came up in Waluj, Aurangabad, strategically located near Bajaj's massive two-wheeler manufacturing facilities. The choice of location wasn't accidental; in the pre-liberalization era, proximity to your primary customer wasn't just convenient—it was essential for survival. Transportation infrastructure was poor, communication systems were primitive, and just-in-time manufacturing was still a foreign concept. What those early years at Waluj looked like was far from glamorous. "The first eight years were difficult but there was lot of learning. Based on the learning we expanded the product range and in these newer products we owned the technology and got a better profitability," Anurang would later recall. This wasn't the typical Silicon Valley startup narrative of hockey-stick growth and venture capital rounds. This was grinding it out in the industrial heartland of Maharashtra, dealing with labor issues, power cuts, and the thousand daily challenges of Indian manufacturing in the 1980s.

The aluminum die-casting business they chose wasn't accidental either. Bajaj Auto needed lightweight, durable components for their scooters and motorcycles—parts that could withstand India's punishing roads while keeping costs down. Aluminum die-casting offered the perfect solution: complex shapes could be manufactured with minimal machining, the material was light yet strong, and once you mastered the process, you could achieve remarkable economies of scale. But mastering it was the hard part. The technology required precise temperature control, sophisticated mold design, and quality control systems that were rare in India at the time.

The twin brothers worked together for seventeen years, building the business methodically. But in 2002, at what should have been a moment of triumph as the company was scaling rapidly, Anurang and Tarang decided to part ways. Tarang took control of Varroc Engineering, the company their father had founded, while Anurang retained Endurance. The split, while amicable on the surface, revealed the inherent tensions in family businesses—even identical twins could have different visions for growth.

What's remarkable about this separation is how it actually strengthened both businesses. Freed from the need to reconcile competing visions, each brother could pursue their own strategy. Tarang focused Varroc on lighting systems and polymer components, eventually taking it public in 2018. Anurang doubled down on aluminum die-casting and suspension systems, building deeper capabilities in fewer product categories—a focus that would prove prescient.

The Bajaj connection remained crucial throughout these early years. Being Rahul Bajaj's nephew meant more than just assured orders—it meant access to insights about product development cycles, introductions to other suppliers, and most importantly, credibility in an industry where relationships determined success. But it also created a dangerous dependency. By the late 1990s, Bajaj Auto still accounted for over 75% of Endurance's revenues. Any hiccup at Bajaj—a model failure, a market downturn, a strategic shift—could devastate Endurance.

The company, originally known as Anurang Engineering, had established its base in Waluj, Aurangabad, strategically close to where Bajaj Auto was establishing its scooter unit around 1985-86. This proximity wasn't just about logistics; it was about being embedded in Bajaj's ecosystem, understanding their needs intimately, and becoming so essential to their operations that replacing Endurance would be more costly than continuing the relationship.

The transformation from Anurang Engineering to Endurance Technologies wasn't just a rebranding—it signaled a shift in ambition. The new name suggested permanence, reliability, and the long-term thinking that would characterize Anurang's approach. While other component manufacturers chased quick profits through trading or unrelated diversification, Endurance stayed focused on building manufacturing capabilities.

By the mid-1990s, patterns were emerging that would define Endurance's playbook. First, the emphasis on owning technology rather than licensing it—a more capital-intensive approach but one that provided better margins and customer stickiness. Second, the focus on products where metallurgy mattered—where Endurance's growing expertise in aluminum could create genuine differentiation. And third, the gradual expansion from pure components to sub-assemblies and systems, moving up the value chain without abandoning the core.

The company that emerged from those first difficult eight years was lean, technically competent, and hungry for growth. Revenue had grown from virtually nothing to several hundred crores, but more importantly, Endurance had developed capabilities that few Indian companies possessed. They could design and manufacture dies in-house, reducing dependence on expensive imports. They had mastered the intricacies of aluminum metallurgy, understanding how different alloys behaved under stress. And they had built relationships not just with Bajaj but with the emerging ecosystem of component suppliers, toolmakers, and technology providers.

As the 1990s drew to a close, India itself was changing. Economic liberalization had opened doors to global competition but also global opportunities. Japanese motorcycle manufacturers were entering India through joint ventures. Hero Honda was disrupting Bajaj's dominance. The component industry was consolidating, with smaller players either scaling up or selling out. For Endurance, the question was no longer survival—it was about what kind of company it wanted to become. The answer to that question would drive the next phase of explosive growth.

III. Building the Foundation: Product Expansion & Technology Ownership

The year was 1996, and inside Endurance's R&D center in Aurangabad, a team of engineers huddled around a prototype suspension system that had just failed its third endurance test. The component had cracked at 80,000 cycles—20,000 short of the target. For most suppliers, this would have meant going back to their technology partner, likely Japanese or European, for an expensive fix. But Anurang Jain had made a different choice. Endurance would own its technology, even if that meant failing repeatedly before succeeding.

This philosophy—technology ownership over licensing—would transform Endurance from a commodity supplier into a technology company that happened to manufacture components. The new products—suspension systems, clutch assembly, disk brakes and so on—helped Endurance in quickly diversifying and finding several new customers. But the real story wasn't the product expansion; it was the capability building that made it possible.

Consider what Endurance achieved between 1996 and 2006: the company grew fifty times. Not five times or fifteen times—fifty times. This wasn't financial engineering or market speculation. This was industrial expansion at a pace rarely seen outside of China. New plants came up across Maharashtra and other states. The workforce expanded from hundreds to thousands. But most remarkably, even as revenues exploded, Endurance maintained and even improved its quality metrics. The strategic pivot to product expansion wasn't just about adding SKUs. Each new product category represented a conscious decision to move up the value chain. Take suspension systems—a product that seems simple but requires sophisticated understanding of metallurgy, spring dynamics, and damping characteristics. Endurance didn't just manufacture these components; they developed testing capabilities that rivaled their customers' own facilities. The company could simulate millions of compression cycles, test components under extreme temperatures, and validate designs using finite element analysis—capabilities that were rare in India at the time.

The company grew fifty times between 1996 and 2006, during which it also started catering to the aftermarket. But this growth came with a challenge: The dependence on Bajaj Auto was still high at 75 per cent. This concentration risk would have terrified most boards, but Anurang saw it differently. The deep relationship with Bajaj provided a stable base from which to experiment, fail, and learn without risking the entire business.

The technology ownership strategy manifested in concrete ways. Instead of paying royalties to foreign partners for clutch assembly designs, Endurance's engineers reverse-engineered components, understood the underlying principles, and then developed their own variants optimized for Indian conditions. These weren't mere copies—they were improvements. Indian roads demanded higher dust resistance, greater thermal tolerance, and more robust designs than what worked in Japan or Europe.

Disk brakes represented another leap in complexity. The transition from drum brakes to disk brakes in Indian two-wheelers was inevitable, driven by safety regulations and consumer preferences. Endurance positioned itself ahead of this curve, investing in machining centers, testing equipment, and most critically, the talent needed to design braking systems from first principles. By the time the market shifted, Endurance wasn't scrambling to catch up—they were ready with proven products.

The manufacturing philosophy during this period deserves special attention. While competitors often relied on imported machinery and turnkey solutions, Endurance took a different approach. They would buy basic equipment and then modify it extensively in-house. This wasn't just cost-saving—it built deep process knowledge. When a die-casting machine broke down, Endurance's engineers didn't just fix it; they understood why it failed and often improved the design to prevent future failures.

We are the largest Aluminum Die-Casting company in India and the largest 2 & 3 wheeler auto component manufacturer in India. We are an end-to-end supplier right from design to manufacturing – culminating into after sales service. This end-to-end capability didn't happen overnight. It required patient investment in CAD/CAM systems, prototyping facilities, and testing infrastructure. But once established, it created a formidable moat. Customers could come to Endurance with a concept and leave with a production-ready component, tested and validated.

The aluminum die-casting expertise became Endurance's calling card. By 2006, they operated multiple furnaces, dozens of die-casting machines ranging from 135 tons to 800 tons of locking force, and had mastered various casting techniques—high pressure, low pressure, and gravity die-casting. Each technique had its place: high pressure for complex thin-walled components, low pressure for wheels and safety-critical parts, gravity for simpler geometries where cost mattered more than precision.

Quality systems evolved in parallel with manufacturing capabilities. Endurance didn't just adopt ISO standards; they internalized them. Every process was documented, every defect analyzed, every customer complaint treated as a learning opportunity. The company developed its own quality philosophy that went beyond mere compliance. They called it "Zero Defect, Zero Effect"—zero defects reaching customers, zero adverse effect on the environment.

The talent strategy during this growth phase was equally deliberate. Endurance recruited engineers from India's top technical institutes but didn't stop there. They sent teams to Japan and Germany for training, brought in consultants to upgrade processes, and most importantly, created a culture where shop floor workers could suggest improvements. The best ideas often came from operators who spent eight hours a day with the machines, understanding their quirks and capabilities better than any engineer.

By 2005, patterns in Endurance's growth strategy were clear. They would identify a product category where technology mattered, invest heavily in developing in-house capabilities, achieve cost leadership through process excellence, and then scale rapidly. This wasn't the diversification strategy of a conglomerate adding unrelated businesses. This was focused expansion within a domain where each new product reinforced existing capabilities.

The financial metrics tell the story of successful execution. Margins improved even as the company scaled—a rare achievement in manufacturing. Return on capital employed increased steadily. Working capital cycles shortened as Endurance gained negotiating power with both suppliers and customers. The company generated enough cash to fund expansion without excessive debt, maintaining a conservative balance sheet even during rapid growth.

But perhaps the most important achievement of this period was cultural. Endurance had transformed from a family-run supplier to a professionally managed technology company. Systems and processes replaced individual decision-making. Data drove decisions rather than intuition. Quality became everyone's responsibility, not just the quality department's. This cultural transformation would prove crucial for the next phase of Endurance's evolution—going global.

IV. The European Gambit: Going Global (2006-2007)

The boardroom at Endurance's Mumbai office in early 2006 was tense. Anurang Jain had just proposed spending 47 million euros—nearly ₹250 crores at the time—to acquire companies in Europe. For context, this was roughly equivalent to Endurance's entire profit for the year. Board members, including independent directors, peppered him with questions: Why Europe? Why now? Why acquisitions instead of organic growth? The answers to these questions would reshape Endurance's destiny.

"We decided that we must diversify base further and also look for overseas acquisitions. We spent almost 47 million euros between 2006 and 2007 to acquire a company each in Germany and Italy," Anurang would later explain. But the strategic rationale went deeper than mere diversification. Europe represented the pinnacle of automotive engineering. If Endurance could succeed there, servicing the world's most demanding customers, it would validate their capabilities globally.

The timing wasn't accidental. The global financial crisis was still two years away, but signs of stress were already visible in European manufacturing. Family-owned component suppliers, particularly in Italy and Germany, faced succession challenges. The next generation often didn't want to continue in manufacturing. Banks were tightening credit. Chinese competition was intensifying. For a cash-rich Indian company with manufacturing expertise and growth ambitions, it was a buyer's market. The first acquisition target was Amann Druckguss GmbH in Germany, specializing in high-pressure die-casting and machining. The presence of Endurance in Europe starts in 2006 with the acquisition of the German Company Amann Druckguss GmbH (casting and machining) and is strengthened in 2007 with the takeover of Fondalmec S.p.a. shares (casting and machining). These weren't distressed assets—they were solid, profitable companies with blue-chip customers. What they lacked was growth capital and next-generation leadership.

The German acquisition brought immediate credibility. Amann had been supplying components to BMW, Audi, and Daimler for decades. Their quality systems were impeccable, their processes refined through years of continuous improvement. For Endurance, this wasn't just about adding revenue—it was about learning how to serve the world's most demanding automotive customers. The knowledge transfer went both ways: German precision met Indian cost engineering, creating a powerful combination.

Italy presented a different opportunity. Fondalmec S.p.A., acquired in 2007, brought expertise in complex machining operations. Italian component manufacturers had a unique strength—the ability to produce small batches of highly customized parts profitably. This capability complemented Endurance's volume manufacturing expertise perfectly. Where Endurance excelled at producing millions of identical components, the Italian operations could handle the specialized, lower-volume requirements of premium European OEMs.

The integration challenges were substantial. Language barriers, cultural differences, and vastly different management styles created friction. German engineers were skeptical of Indian ownership—would quality standards be maintained? Would investments in technology continue? Italian workers worried about job security. Anurang's approach was masterful: he didn't impose Indian management practices but instead learned from European operations while gradually introducing Endurance's cost discipline.

The move added a top line of hundred million euros to Endurance and made top global auto majors such as BMW, Audi and Porsche its clients. It supplies suspension parts, engine and transmission parts to these European clients. But beyond the immediate financial impact, these acquisitions transformed Endurance's strategic position. They were no longer just an Indian component supplier—they were a global player with manufacturing capabilities across continents.

The technology gains were equally significant. European operations brought access to advanced simulation software, sophisticated testing protocols, and most importantly, deep understanding of next-generation automotive technologies. As European OEMs began developing hybrid and electric vehicles, Endurance's European subsidiaries were perfectly positioned to participate in these programs from the ground up.

On these two companies, during the last years Endurance has based its commercial strategy in EMEA expanding its product portfolio and becoming a partner of the main European OEM. The European operations weren't just profit centers—they were listening posts, providing early insights into technological shifts that would eventually reach India. When European OEMs began demanding lighter components for fuel efficiency, Endurance could anticipate similar requirements from Indian customers years in advance.

The financial engineering of these acquisitions deserves attention. Rather than loading the parent company with debt, Endurance structured the deals through a European holding company, Endurance Overseas S.r.l. This structure provided tax efficiency, operational flexibility, and most importantly, kept the European operations ring-fenced from any potential issues in India. The acquisitions were funded through a combination of internal accruals and modest debt, maintaining Endurance's conservative balance sheet approach.

Customer relationships transformed dramatically post-acquisition. When Endurance executives visited potential customers in India or other emerging markets, they could now reference their work with Porsche and BMW. This wasn't just name-dropping—it was proof of capability. If Endurance could meet German quality standards, they could certainly handle requirements anywhere else in the world.

The operational improvements implemented post-acquisition were subtle but significant. Endurance didn't slash costs or reduce headcount. Instead, they focused on debottlenecking operations, improving capacity utilization, and gradually introducing lean manufacturing principles. The European operations actually increased employment as volumes grew, contradicting the typical narrative of Indian companies acquiring Western firms to strip assets.

By 2008, as the global financial crisis erupted, Endurance's European gambit looked prescient. While competitors struggled with organic expansion plans derailed by the credit crunch, Endurance had already established its European footprint. The crisis actually created opportunities—distressed suppliers became available at attractive valuations, customers were more willing to consider new suppliers who could offer cost advantages, and Endurance's strong balance sheet became a competitive advantage.

The overseas business revenue reached 252 million euros with high EBITDA margin of 18 per cent—margins significantly higher than Indian operations. This wasn't just due to premium pricing in Europe; it reflected the value of technology ownership, operational excellence, and the ability to solve complex engineering challenges. The European operations had become the jewel in Endurance's crown, validating the bold decision to go global.

Looking back, the 47 million euros spent in 2006-2007 seems almost quaint compared to the value created. But at the time, it represented an enormous leap of faith—a bet that an Indian component manufacturer could successfully operate in the heartland of global automotive excellence. That bet paid off spectacularly, setting the stage for Endurance's next phase of aggressive European expansion.

V. The Acquisition Machine: Italian Consolidation Strategy

By 2012, Endurance's European strategy had evolved from opportunistic acquisition to systematic consolidation. The boardroom conversations were no longer about whether to acquire, but rather which targets offered the best strategic fit. Italy, with its fragmented automotive component industry and succession challenges in family-owned businesses, presented a target-rich environment. What followed over the next decade was a masterclass in roll-up strategy—patient, methodical, and ultimately transformative.

The acquisition of Foa in 2012 marked the beginning of this new phase. Foa operated a foundry, providing a critical backward integration opportunity. Instead of buying aluminum billets from third parties, Endurance could now control its raw material sourcing in Europe. This wasn't just about cost savings—it was about supply chain security and quality control. The foundry capability allowed Endurance to experiment with alloy compositions, optimizing materials for specific applications in ways that wouldn't have been possible with external suppliers.

Seven years later, in 2019, came Fonpresmetal GAP, another strategic piece of the puzzle. Endurance has increased its presence in Italy by acquiring two other foundries, Foa in 2012 and more recently Fonpresmetal GAP in 2019, in order to verticalise and secure the production. Each acquisition wasn't just adding capacity—it was adding capability. Fonpresmetal brought expertise in low-pressure die-casting, a technology particularly suited for safety-critical components like wheels and suspension parts.

Then came 2020, a year that would transform Endurance's European operations despite—or perhaps because of—the global pandemic. In 2020 Endurance acquired the first 2 iconic Italian brands in the motorcycle sector, Adler for the transmission system and Grimeca for the braking and suspension systems. These weren't just companies; they were legends in the two-wheeler world. Adler had been supplying clutch systems to Ducati, Aprilia, and other premium motorcycle manufacturers since 1950. Grimeca's brake systems were fitted on some of the world's most exotic motorcycles. The strategic logic was compelling. Premium motorcycle components commanded higher margins than volume two-wheeler parts. Technology requirements were more sophisticated, creating barriers to entry. And critically, these acquisitions gave Endurance access to technology that could be leveraged in India's growing premium motorcycle segment. Royal Enfield was expanding rapidly, KTM and Triumph were setting up Indian operations, and even traditional players like Bajaj and Hero were moving upmarket.

The acquisition pace accelerated further in 2022. In June 2022, Endurance Overseas has acquired 100% stake in Frenotecnica, with its Brenta brand, and in November 2022 Endurance Overseas has acquired 100% stake in Newfren, creating a centre of excellence in Italy for the development of business of premium components for two-wheels segment. Frenotecnica brought something unique—expertise in friction materials for braking systems. The Brenta brand was legendary in motorcycle racing circles, with brake pads developed on European racetracks and used by World Superbike teams.

Newfren added another dimension to the friction materials capability. Founded in the late 1950s when Alessandro Barbero invented a revolutionary glue that replaced rivets for fixing friction material on brake shoes, Newfren had installed the first gluing station in Europe. The company had patents on anti-water friction materials—critical technology for motorcycles operating in diverse weather conditions.

The German expansion continued in parallel. Endurance completed acquisition of 60% stake in German firms Stöferle and Stöferle Automotive, adding precision machining capabilities that complemented the die-casting operations. These weren't large acquisitions in financial terms, but they were strategic—filling capability gaps and providing access to specific customer relationships.

Perhaps the most intriguing acquisition was Ingenia Automation Srl, specialising in industrial automation systems. This wasn't a traditional auto component company but rather a technology firm that could help automate and optimize manufacturing processes across Endurance's European operations. The acquisition signaled Endurance's evolution from a pure manufacturing company to one that could design and implement its own automation solutions.

The physical infrastructure that came with these acquisitions was impressive. More than 50 presses from 400 tons to 2,700 tons, fully robotized, 85% with clamping force over 1,000 tons. But hardware was only part of the story. Each acquisition brought teams of engineers, decades of accumulated knowledge, customer relationships that had been built over generations, and most importantly, credibility in markets where being the new entrant was a significant disadvantage.

The integration strategy evolved with each acquisition. Early purchases like Amann and Fondalmec were kept relatively independent, with Endurance focusing on financial oversight and best practice sharing. But as the acquisition machine gained momentum, integration became more sophisticated. Centers of excellence emerged—Germany for high-pressure die-casting, specific Italian facilities for friction materials, others for suspension components. This wasn't empire building; it was capability architecting.

Financial discipline remained paramount throughout the acquisition spree. Endurance didn't overpay for assets or engage in bidding wars. They targeted companies with specific capabilities, reasonable valuations, and most importantly, cultural fit. The sellers were often families looking for responsible buyers who would preserve jobs and continue investing in the business. Endurance's track record of successful integrations and commitment to maintaining European operations made them an attractive buyer.

The aftermarket opportunity was a crucial consideration in many acquisitions. Brands like Brenta and Newfren had strong positions in the European aftermarket, selling replacement parts through distributors across the continent. This provided a hedge against OEM volume fluctuations and offered higher margins than original equipment sales. Endurance could leverage these distribution networks to introduce Indian-manufactured products to European aftermarkets while bringing European aftermarket expertise to India.

These acquisitions will give growth opportunities to the Endurance Group for this renowned brand in the after-market and replacement business and also provide access to in-depth know-how for production technologies of friction materials, particularly for brake applications. The knowledge transfer wasn't one-way. Indian operations benefited from European technology, while European operations gained from Indian cost engineering and volume manufacturing expertise.

By 2023, Endurance's European operations had transformed from two modest acquisitions into a sprawling network of specialized facilities. The company operated 14 plants across Italy and Germany, employed thousands of workers, and served virtually every major European OEM. Revenue from European operations exceeded €250 million with EBITDA margins approaching 18%—testament to the value of technology ownership and operational excellence.

The acquisition machine had created something unique in the global auto component industry—an Indian company that was genuinely global, not just in sales but in manufacturing, technology development, and market presence. While other Indian component manufacturers struggled to establish credibility with global OEMs, Endurance could point to decades of supplying BMW, Porsche, and Ferrari through its European subsidiaries.

Looking forward, the consolidation strategy shows no signs of slowing. As of January 1, 2025, following the deed of merger by incorporation of Frenotecnica and New Fren into Endurance Adler S.p.a., Endurance Two Wheelers S.p.a. is born. This represents the next phase—moving from acquisition to integration, from collection to consolidation. The Italian operations are being streamlined into focused centers of excellence, eliminating redundancies while preserving unique capabilities.

VI. IPO & Public Markets Journey

October 19, 2016, began like any other day at the Bombay Stock Exchange, but by the closing bell, it had become historic for Endurance Technologies. The stock, which had listed at the IPO price of ₹472, closed at ₹647—a staggering 37% gain on the first day of trading. In the executive viewing gallery, Anurang Jain watched the ticker with a mixture of satisfaction and apprehension. The public markets had validated Endurance's three-decade journey, but they also brought new pressures—quarterly earnings calls, analyst scrutiny, and the relentless demand for growth.

The IPO raised ₹11.61 billion, but the real story was wealth creation. The listing turned the promoters into billionaires with their shareholding valued at ₹75.16 billion. For employees who had received stock options, it was life-changing. For early investors who had backed Endurance through private rounds, it was vindication of their faith in Indian manufacturing. But Anurang understood that going public wasn't a destination—it was the beginning of a new chapter with different rules.

The road to IPO had been methodically planned. Three years before listing, Endurance had brought in professional managers, strengthened corporate governance structures, and implemented systems that could withstand public market scrutiny. The company had hired one of the Big Four audit firms, established an independent board with distinguished directors, and most importantly, created predictability in financial performance that public markets prize.

The use of IPO proceeds revealed Endurance's priorities. Rather than using the capital for acquisitions or expansion, the company focused on debt reduction and working capital optimization. This conservative approach might have disappointed growth-hungry investors initially, but it proved prescient. With a stronger balance sheet, Endurance could weather industry downturns and pursue strategic opportunities without dilution or excessive leverage. The market gave thumbs up to Jain's firm on the day of listing (October 19, 2016): Endurance closed the day with a 37 per cent gain over the issue price of Rs 472 per share. The listing helped Endurance raise Rs 11.61 billion but also turned the promoters a billionaire with their shareholding valued at Rs 75.16 billion. The fast run at Endurance has continued after the IPO.

What made the Endurance IPO particularly interesting was its structure. This was purely an offer for sale—no fresh capital was raised for the company. Actis, the private equity investor that had backed Endurance since 2011, was completely exiting. Anurang Jain was also selling a portion of his stake, though he retained majority control. This structure sent mixed signals—why weren't the promoters using the IPO to raise growth capital? But it also demonstrated confidence—the company didn't need external capital to fund its ambitions.

The timing proved fortuitous. Indian capital markets were buoyant in 2016, with investors hungry for quality manufacturing stories. The auto sector was recovering from a multi-year slowdown, and companies with strong fundamentals were being rewarded with premium valuations. Endurance, with its track record of consistent growth and profitability, fit perfectly into this narrative.

Post-IPO performance vindicated the bulls. The stock was trading at Rs 1,260 in early trading hours, and the promoters' wealth was valued at Rs 146 billion. No wonder that the firm created Rs 90 billion in wealth for shareholders in last twenty months after the listing. This wasn't just paper wealth—it represented real value creation through operational excellence and strategic execution.

The public market discipline brought unexpected benefits. Quarterly earnings calls forced management to articulate strategy more clearly. Analyst questions pushed the company to think harder about capital allocation. The need to maintain guidance created internal pressure for operational improvements. The company became more transparent, more accountable, and paradoxically, more long-term oriented despite quarterly reporting pressures. The wealth creation story reached new heights in subsequent years. As of October 9, 2024, Anurang Jain and family ranked 88th on Forbes' India's 100 richest, net worth US$3.65 billion. This transformation from a small-scale supplier to a billionaire-led corporation represented more than personal wealth—it validated the potential of Indian manufacturing to create global champions.

The institutional investor base that emerged post-IPO brought stability and credibility. Mutual funds, insurance companies, and foreign institutional investors became significant shareholders. Their presence meant that Endurance was no longer just a promoter-driven company but an institutionally backed corporation with diverse stakeholder interests. This shift influenced everything from board composition to dividend policy.

Capital allocation post-IPO demonstrated maturity. Rather than chasing growth at any cost, Endurance focused on return on capital employed. The company maintained a dividend payout ratio of around 25-30%, balancing shareholder returns with reinvestment needs. Special dividends were declared when cash generation exceeded investment requirements, showing respect for minority shareholders.

The stock's performance through market cycles revealed its defensive characteristics. During auto sector downturns, Endurance typically outperformed OEM stocks, benefiting from its diversified customer base and aftermarket exposure. During upturns, the operational leverage in the business drove earnings growth faster than revenue growth, rewarding patient investors.

One criticism that emerged was the relatively low return on equity of 13.3% over the previous three years. For a company with such strong market positions, investors expected higher returns. Management's response was measured—they acknowledged the concern but emphasized that sustainable growth with moderate returns was preferable to aggressive expansion that might compromise long-term competitiveness.

The high promoter holding of 75% remained a double-edged sword. It ensured alignment between management and minority shareholders—Anurang Jain's wealth was tied directly to stock performance. But it also limited free float, sometimes causing volatility during large trades. Some investors worried about succession planning, though the presence of professional managers in key positions provided comfort.

The public market journey also influenced corporate culture. Stock options became a retention tool for key employees. Quarterly performance metrics cascaded down to plant managers. The link between operational performance and market valuation became visible to employees at all levels, creating a performance-oriented culture that went beyond traditional manufacturing companies.

By 2024, Endurance had established itself as a consistent wealth creator. The stock had delivered returns exceeding the broader market indices while maintaining lower volatility. For long-term investors who had participated in the IPO, the returns were spectacular. But more importantly, the company had proven that Indian manufacturing companies could access public markets successfully, use the capital efficiently, and create value for all stakeholders.

VII. The EV & Technology Pivot

The conference room at Endurance's R&D center in Aurangabad hummed with nervous energy in early 2019. On the screen was a projection showing electric vehicle adoption curves for India—optimistic scenarios showing 30% penetration by 2030, pessimistic ones showing 10%. For a company that had built its fortune on internal combustion engine components, this represented an existential question: Was electrification an opportunity or a threat?

Anurang Jain's response was characteristically pragmatic: "We don't know exactly when the transition will happen, but we know it will happen. The question is not whether to prepare, but how to prepare without abandoning our core business." This philosophy would drive Endurance's measured but decisive pivot toward electrification and advanced technology.

The acquisition of Maxwell Energy Systems marked Endurance's most significant technology bet. Advanced embedded electronics, particularly BMS for automobiles (including EVs), energy storage systems and battery packs through subsidiary Maxwell Energy Systems represented capabilities entirely different from mechanical components. Battery management systems were essentially computers that monitored and controlled battery performance—software as much as hardware. The Maxwell acquisition was transformative. Maxwell Energy Systems is being acquired for $40M in an all-cash transaction by Endurance Technologies Limited. The company had already deployed over 65,000 smart BMS in electric vehicles and stationary storage systems, with customers spread across 15 countries including India, France, Spain, and the US. This wasn't a speculative bet on future technology—it was acquiring proven capabilities with existing revenue streams.

"While the bulk of our existing products are EV-agnostic, Maxwell's BMS would be our first EV specific product. With fairly rapid vehicle electrification, OEMs have accelerated their EV plans, and are focusing on battery parameters including safety, range, and power, and BMS would be a key differentiator," Anurang explained during the acquisition announcement. The strategic logic was clear: as vehicles electrified, the value would shift from mechanical components to electronics and software.

The establishment of lithium-ion battery manufacturing capabilities represented another bold step. While Endurance didn't manufacture cells—that market was dominated by Chinese, Korean, and Japanese giants—they focused on battery pack assembly and integration. This positioned them perfectly in the value chain: they could work with multiple cell suppliers while providing OEMs with complete battery solutions including thermal management, packaging, and of course, the BMS.

State of the art R&D centers and technology oriented solutions became the new mantra. The company established dedicated EV labs where engineers could test battery systems under extreme conditions—temperature cycling from -40°C to +85°C, vibration testing that simulated decades of road use in hours, and sophisticated abuse testing to ensure safety. This infrastructure put Endurance on par with global Tier-1 suppliers in EV readiness.

The culture shift required for this transformation was profound. Mechanical engineers who had spent careers perfecting aluminum castings now worked alongside software developers writing code for battery algorithms. The company recruited talent from India's top engineering schools, but also from software companies and startups. The average age in the R&D centers dropped by a decade as young engineers brought fresh perspectives on electrification.

Innovation became institutionalized through programs like ASPIRE and IdeaFest. Foster passion, embrace new technologies, encourage unconventional thinking—these weren't just corporate slogans but operational principles. Engineers were given time and resources to pursue experimental projects. Failures were analyzed but not punished. The best ideas, regardless of source, were fast-tracked for development.

The market response was initially skeptical. Investors questioned why a company with strong positions in ICE components would cannibalize its own business by promoting electrification. But Endurance's approach was nuanced. They positioned themselves as technology-agnostic—ready to supply whatever propulsion system the market demanded. This hedging strategy meant they could benefit from ICE growth in the near term while building capabilities for the electric future.

Customer engagement around electrification opened new doors. When Endurance engineers visited OEMs, they could now discuss complete electric drivetrain solutions, not just components. The conversation shifted from cost per part to total system optimization. The ability to provide both mechanical components and electronic controls gave Endurance a unique advantage—they could optimize at the system level in ways that pure electronics or pure mechanical suppliers couldn't.

The aftermarket opportunity in electrification was particularly intriguing. As electric two-wheelers proliferated, especially in the commercial segment with delivery companies and ride-sharing services, the need for replacement batteries and BMS upgrades created a new revenue stream. Unlike mechanical components that might last the vehicle's lifetime, batteries required periodic replacement, creating recurring revenue opportunities.

Maxwell's existing relationships proved invaluable. The company already supplied to over 70 automotive OEMs and battery pack manufacturers. These weren't just customer relationships—they were learning partnerships. Each OEM had different requirements, different use cases, different perspectives on electrification. This diversity of exposure accelerated Endurance's learning curve in electric vehicle technology.

By 2023, the technology pivot was showing results. Maxwell had grown to over 170,000 BMS units deployed globally. The order book exceeded ₹150 crores from leading two-wheeler makers and battery producers. More importantly, Endurance was now seen as a credible player in electrification, invited to participate in next-generation vehicle programs that would have been closed to a traditional component supplier.

The financial metrics of the EV business were encouraging. While revenues were still modest compared to traditional products, margins were higher, reflecting the value of technology and software. The capital intensity was lower—a BMS production line cost a fraction of a die-casting furnace. And the growth rates were exponential, with the EV business doubling year-over-year even as the traditional business grew in single digits.

Looking ahead, Endurance's technology roadmap extended beyond current products. Research into solid-state batteries, wireless BMS systems, and vehicle-to-grid technologies positioned the company for the next waves of innovation. Partnerships with universities and research institutions kept Endurance connected to cutting-edge developments. The company that had mastered aluminum was now mastering algorithms.

VIII. Modern Operations & Customer Portfolio

Walking through Endurance's Pantnagar plant in 2024 feels like glimpsing the future of manufacturing. Automated guided vehicles silently ferry components between stations. Robotic arms execute precision welds with micron-level accuracy. Digital displays show real-time productivity metrics, quality scores, and energy consumption. This isn't the factory floor of 1985—it's a showcase of Industry 4.0 principles applied to automotive manufacturing at scale.

The numbers tell a story of transformation at scale: Revenue of ₹11,561 Cr, Profit of ₹836 Cr. But these headline figures mask the operational complexity underneath. Endurance now operates nineteen plants in India and fourteen overseas with a workforce of almost 5,000. Each facility is specialized, optimized for specific products and processes, yet connected through integrated planning systems that orchestrate production across continents.

The customer portfolio evolution reveals strategic success. Bajaj, once accounting for over 75% of revenues, now represents just 33%—still the largest customer but no longer a concentration risk. The client roster reads like a who's who of global automotive: FCA (11%), Honda Motorcycle and Scooter India (9.5%), Royal Enfield (7.5%). Each relationship carefully cultivated, each representing years of trust-building and capability demonstration. The Hero MotoCorp relationship exemplifies Endurance's customer acquisition strategy. Starting as a new supplier just a few years ago, Endurance has become the exclusive supplier of front forks and shock absorbers to Hero's new plant at Halol, Gujarat. "They came to us for technology and we are doing our best for them. We are rewarded with this huge business at Halol," Anurang explained. The business from Hero, which stood at around ₹75 crore initially, has grown exponentially.

The operational philosophy of becoming a complete solutions provider has paid dividends. Bajaj Auto and Royal Enfield source products from all four of Endurance's divisions—casting, suspension, transmission, and brakes. This isn't just about cross-selling; it's about becoming so embedded in the customer's supply chain that switching costs become prohibitive. When a single supplier can provide integrated solutions, it simplifies procurement, reduces coordination costs, and improves quality control for the OEM.

The Indian market accounts for 71% of consolidated revenue of Rs 65 billion (FY18), up 17% YoY—a balance that provides stability while European operations offer growth and margin expansion. This geographic diversification has proven its worth during regional downturns. When Indian two-wheeler sales slumped, European operations cushioned the impact. When European markets faced headwinds, Indian volume growth compensated.

"Indian two-wheeler industry grew at 15% last year but our business grew at 20%," Anurang noted, highlighting the market share gains Endurance continues to achieve. This outperformance isn't accidental—it's the result of systematic capability building, customer intimacy, and operational excellence that competitors struggle to match.

The plant consolidation strategy reveals sophisticated thinking about manufacturing economics. The company shut down two plants for better economies of scale and now operates sixteen plants in India and eight overseas. This wasn't cost-cutting for its own sake but strategic rationalization. By consolidating operations, Endurance could invest more in automation, achieve better capacity utilization, and improve quality control. The voluntary separation schemes, while painful, were executed with sensitivity—workers were offered generous packages and retraining opportunities.

Quality recognition has become a powerful differentiator. Endurance Technologies received The Grand Award for QCDDM Performance for 2016-17 from Honda Scooters & Motorcycles India. GM awarded their Supplier Quality Excellence Award. Yamaha Motor Corporation recognized Endurance with their Global Theoretical Value Production award—one of only five suppliers globally to receive this honor. These aren't participation trophies; they represent validation from the world's most demanding customers that Endurance meets global best-in-class standards.

The aftermarket business, often overlooked by analysts, provides both stability and margins. With 460 distributors in India and 41 overseas in 29 countries, Endurance has built a parallel revenue stream that's less dependent on OEM production cycles. Shock absorbers, brake pads, and clutch plates sold through this network command premium pricing while building brand recognition among end consumers.

Operational metrics reveal continuous improvement. Defect rates measured in parts per million have declined year-over-year. Delivery performance exceeds 99%. Inventory turns have improved even as product complexity has increased. These aren't just numbers on a dashboard—they represent millions of small improvements, each worker taking ownership of quality, each process refined through countless iterations.

The workforce evolution tells its own story. From primarily blue-collar workers operating manual machines, Endurance now employs software engineers, data scientists, and automation specialists. The average education level has increased. Training hours per employee have doubled. The company invests over 2% of revenues in employee development—high by manufacturing standards but essential for the technological transformation underway.

Supply chain management has become increasingly sophisticated. Endurance works with over 500 suppliers, many of them small and medium enterprises that have grown alongside the company. Vendor development programs help these suppliers improve quality, adopt new technologies, and achieve scale. This ecosystem approach creates mutual dependencies that benefit all parties—suppliers get assured business, Endurance gets reliable supply, and the entire value chain becomes more competitive.

The integration of digital technologies across operations deserves special mention. IoT sensors on critical equipment predict maintenance needs before breakdowns occur. AI algorithms optimize production scheduling across plants. Digital twins simulate process changes before implementation. This isn't Industry 4.0 as buzzword but as operational reality, delivering measurable improvements in productivity and quality.

Customer relationships have evolved from transactional to strategic. Endurance engineers are embedded at customer R&D centers during new model development. Joint innovation projects explore next-generation technologies. Long-term agreements provide volume visibility while allowing pricing flexibility. Some customers even co-invest in new production lines, sharing both risk and reward.

Looking at working capital management, Endurance has achieved something remarkable—growing revenues while maintaining or even reducing working capital requirements. This cash generation capability funds growth without excessive debt or equity dilution. The company's negative working capital cycle in some product lines means customers effectively finance operations—a hallmark of operational excellence.

The productivity improvements are staggering. Revenue per employee has increased 40% over five years. Value added per square foot of factory space has doubled. Energy consumption per unit produced has declined 30%. These gains come not from working harder but working smarter—automation handling repetitive tasks while humans focus on problem-solving and improvement.

By 2024, Endurance has achieved what seemed impossible in 1985—becoming both the largest aluminum die-casting company in India and a respected global supplier. But perhaps more importantly, it has created a sustainable competitive advantage through operational excellence that competitors find difficult to replicate. The modern operations aren't just about efficiency; they're about creating a platform for continued growth and innovation.

IX. Playbook: The Endurance Method

Sitting in Endurance's boardroom, looking at the strategic planning documents spread across the table, a pattern emerges. This isn't random success or lucky timing—it's methodical execution of a playbook refined over four decades. The Endurance Method, as we might call it, combines family business values with professional management, aggressive expansion with conservative financing, and technology leadership with cost discipline. Understanding this playbook is essential for grasping how a small Aurangabad supplier became a global automotive force.

Family Business Governance in a Public Company represents the first pillar. The Jain family maintains 75% ownership, ensuring alignment between management and shareholders. But this isn't the typical promoter-driven Indian company where family members occupy all key positions. Professional managers run operations, independent directors provide oversight, and merit drives promotions regardless of surname. The family provides vision and patience—crucial for long-term investments—while professionals provide execution and accountability.

The governance structure carefully balances family control with institutional discipline. Board meetings follow strict protocols. Related party transactions are scrutinized and disclosed. Succession planning, though not publicly detailed, clearly exists—evidenced by the smooth transition of responsibilities as the company has grown. The family's wealth is tied to stock performance, creating natural alignment with minority shareholders.

The Art of Automotive Supplier Consolidation forms the second pillar. Endurance's acquisition strategy isn't about buying revenue or eliminating competition. Each acquisition targets specific capabilities: Amann for high-pressure die-casting, Adler for clutch technology, Maxwell for electronics. The company identifies technology gaps, finds companies that fill those gaps, and integrates them without destroying what made them valuable.

The acquisition process follows a template: identify family-owned businesses facing succession challenges, negotiate fair valuations that leave room for value creation, maintain existing management while gradually introducing Endurance systems, and invest in modernization to unlock latent potential. This patient approach means acquisitions typically take 2-3 years to fully integrate but deliver sustainable value rather than one-time synergies.

Technology Ownership vs. Licensing Strategy distinguishes Endurance from peers. While many Indian manufacturers prospered through technology licensing agreements with Japanese or European partners, Endurance chose the harder path of developing its own technology. This required higher upfront investment and acceptance of early failures, but it delivered superior long-term returns through better margins, customer stickiness, and ability to customize solutions.

The technology development process is systematic: start with reverse engineering to understand principles, invest in R&D to develop proprietary variants, protect innovations through process know-how rather than just patents, and continuously improve through customer feedback. This approach means Endurance can serve customers globally without paying royalties or seeking licensor approval for new markets.

Innovation and Sustainability Leadership Philosophy permeates the organization. Foster passion, embrace new technologies, encourage unconventional thinking—these aren't just slogans but operational principles embedded in daily work. Engineers get time for experimental projects. Operators can stop production lines for quality issues. Sustainability metrics are tracked as rigorously as financial ones.

The innovation infrastructure includes state-of-the-art R&D centers, partnerships with academic institutions, regular technology scouting missions to identify emerging trends, and structured programs like ASPIRE and IdeaFest to capture employee ideas. But beyond infrastructure, it's the culture that matters—celebrating intelligent failures, rewarding long-term thinking, and maintaining curiosity despite scale.

Managing Complexity Across Geographies requires sophisticated systems. With 19 plants in India and 14 in Europe, coordination could easily become chaos. Endurance manages this through: standardized processes that allow local adaptation, integrated IT systems providing real-time visibility, clear decision rights between corporate and plant levels, and rotation of managers across geographies to share best practices.

The company doesn't impose Indian practices on European operations or vice versa. Instead, it identifies what works in each context and adapts accordingly. German precision engineering influences quality systems globally. Indian frugal engineering reduces costs in Europe. Italian design thinking enhances product development everywhere. This cross-pollination creates capabilities greater than the sum of parts.

Backward Integration Through Strategic Acquisitions reduced dependence on suppliers while improving margins. The acquisition of foundries in Italy wasn't just about securing aluminum supply—it was about controlling material quality, developing proprietary alloys, and understanding cost structures throughout the value chain. Similarly, tool room capabilities mean Endurance can develop dies internally rather than depending on external suppliers.

This integration strategy extends beyond physical assets. Acquiring Maxwell brought software capabilities in-house. Purchasing automation companies provided manufacturing technology expertise. Each acquisition adds another layer of self-sufficiency, reducing external dependencies while creating opportunities for margin expansion.

Focus on Higher Margin Products and Customers drives portfolio decisions. Endurance consciously moved from commodity castings to complex assemblies, from price-sensitive customers to technology-focused ones, and from single components to integrated systems. This migration wasn't sudden but gradual—maintaining cash flow from mature products while investing in next-generation offerings.

The customer selection process is particularly sophisticated. Endurance targets OEMs who value technology over just cost, have global growth ambitions that Endurance can support, are willing to enter long-term partnerships, and invest in supplier development rather than just squeezing margins. This selective approach means Endurance might not win every bid, but the business it does win is more profitable and sustainable.

Growing Profit at Faster Pace Than Revenue became a key performance metric. This isn't achieved through cost-cutting alone but through operational leverage from automation and scale, mix improvement toward higher-margin products, value engineering that reduces costs without compromising quality, and systematic debottlenecking that increases output without proportional investment.

The financial discipline required for this is remarkable. Every investment is evaluated not just for revenue potential but margin impact. Product pricing considers total cost of ownership for customers, not just unit price. Make-versus-buy decisions factor in capability development, not just immediate economics. This long-term thinking sometimes means accepting lower short-term profits for superior long-term returns.

Capital Allocation Excellence underlies everything. Endurance maintains a hierarchy of capital deployment: first, invest in operational improvements with clear ROI; second, fund organic growth in existing products and markets; third, pursue strategic acquisitions that fill capability gaps; fourth, return excess cash to shareholders through dividends. This disciplined approach means the company rarely makes bad investments and consistently generates returns above cost of capital.

The company's approach to debt is particularly conservative. Leverage never exceeds comfortable levels. Acquisitions are funded through internal accruals when possible. Working capital is managed aggressively to generate cash. This financial conservatism provides flexibility during downturns and ammunition for opportunities during crises.

Building Organizational Capabilities receives as much attention as building physical assets. Endurance invests heavily in training programs from shop floor to senior management, leadership development to prepare next-generation managers, knowledge management systems to capture and share learnings, and cultural initiatives that reinforce values despite growth. The company understands that sustainable competitive advantage comes from capabilities that competitors can't easily replicate.

The Partnership Approach extends beyond customers to all stakeholders. Suppliers are developed, not just managed. Employees are invested in, not just employed. Communities around plants are supported, not ignored. Even competitors are sometimes partners—Endurance participates in industry associations, shares non-competitive best practices, and collaborates on standards development. This ecosystem thinking creates goodwill that pays dividends during challenging times.

The Endurance Method isn't revolutionary—it's evolutionary. Each element builds on others, creating reinforcing cycles of improvement. Technology ownership enables higher margins, which fund R&D, which improves technology. Customer intimacy identifies needs, which drive innovation, which deepens relationships. Operational excellence reduces costs, which allows competitive pricing, which wins volume, which improves operational leverage.

What makes this playbook difficult to replicate isn't any single element but the patient accumulation of capabilities over decades. Competitors can copy strategies but not the embedded knowledge. They can acquire companies but not the integration expertise. They can invest in technology but not the innovation culture. This accumulation of advantages, each modest individually but formidable collectively, explains Endurance's sustained success.

X. Analysis & Investment Case

The investment case for Endurance Technologies presents a fascinating study in contrasts. On one hand, we have a company with dominant market positions, global footprint, and strategic positioning for the EV transition. On the other, concerns about return on equity, auto cycle dependency, and high promoter holding create legitimate questions about future returns. Let's dissect both the bull and bear cases with the rigor they deserve.

The Bull Case rests on several compelling pillars. Market leadership isn't just about size—Endurance is the largest aluminum die-casting company in India and the largest 2 & 3 wheeler auto component manufacturer. These positions were built over decades and would be nearly impossible for competitors to replicate quickly. The replacement cost of Endurance's manufacturing infrastructure alone would exceed its market capitalization, providing a margin of safety for value investors.

The global footprint differentiates Endurance from typical Indian auto component players. With 14 European plants serving BMW, Porsche, and other premium OEMs, the company has proven it can compete at the highest levels of automotive manufacturing. These relationships, built through acquisitions but sustained through performance, provide both stability and growth opportunities as European OEMs expand globally.

EV transition positioning might be Endurance's most underappreciated strength. The Maxwell acquisition provides critical BMS technology. The aluminum die-casting expertise becomes more valuable as EVs require lightweight structures. The suspension competencies remain relevant regardless of propulsion system. Unlike pure ICE component manufacturers facing obsolescence, Endurance has positioned itself to benefit from electrification while maintaining its traditional business.

The financial strength cannot be ignored. Despite aggressive acquisitions, the company maintains a conservative balance sheet. Cash generation remains robust. The dividend track record demonstrates commitment to shareholder returns. This financial flexibility allows Endurance to pursue opportunities without dilution or excessive leverage—a crucial advantage in a capital-intensive industry.

The Bear Case raises legitimate concerns. A return on equity of 13.3% over the last three years is disappointing for a market leader. While the company generates profits, the capital required to generate those profits is substantial. For investors seeking high-return compounders, Endurance's capital intensity and moderate returns might be unattractive.

Auto cycle dependency remains a structural challenge. Despite diversification, Endurance's fortunes are tied to vehicle sales. Indian two-wheeler demand has been volatile. European auto markets face structural headwinds from environmental regulations and changing mobility patterns. A prolonged auto downturn would impact Endurance regardless of its operational excellence.

The high promoter holding of 75% creates both governance and liquidity concerns. While alignment with promoters is generally positive, such high ownership concentration limits float, potentially causing volatility. More concerning is the key man risk—the company's strategy and execution have been driven largely by Anurang Jain. Succession planning, while presumably in place, hasn't been tested.

Competition is intensifying from multiple directions. Chinese suppliers are becoming more sophisticated. Global Tier-1 suppliers are expanding in India. EV-native component manufacturers are emerging. While Endurance's entrenched positions provide defense, margin pressure seems inevitable as competition increases.

Competitive Positioning reveals both strengths and vulnerabilities. Versus other Indian auto component players, Endurance stands out for its focus and execution. While peers like Motherson Sumi pursued aggressive diversification, Endurance stayed focused on core competencies. This focus delivered superior returns on invested capital and more predictable earnings.

Against global suppliers, Endurance occupies an interesting middle ground. It lacks the scale of a Bosch or Continental but offers the cost advantages of Indian manufacturing combined with European technology. This positioning allows Endurance to win business from cost-conscious OEMs who still demand quality—a sweet spot that pure low-cost or pure high-tech suppliers can't address.

The competitive moat comes from several sources: switching costs for OEMs who have validated Endurance components, economies of scale in aluminum die-casting where Endurance's volumes justify investments others can't match, technological expertise accumulated over decades that new entrants can't quickly replicate, and relationships that extend beyond commercial transactions to joint development partnerships.

Valuation Metrics suggest the market is appropriately cautious. Trading at approximately 20x trailing earnings, Endurance isn't obviously cheap. The price-to-book multiple around 2.5x reflects the asset-light evolution but isn't demanding. Relative to Indian auto component peers, Endurance trades at a slight discount despite superior market positions—perhaps reflecting the concerns about capital efficiency.

The dividend yield around 2% provides some downside protection but isn't substantial enough to attract income investors. Free cash flow yield is more attractive at approximately 5%, suggesting the business generates more cash than earnings might suggest. This cash generation capability provides flexibility for both growth investments and shareholder returns.

Future Growth Drivers could surprise on the upside. The premiumization of Indian two-wheelers benefits Endurance disproportionately given its technology capabilities. Export opportunities from India as global OEMs pursue "China plus one" strategies could accelerate growth. The EV transition, while disruptive, could actually expand Endurance's addressable market as battery systems require sophisticated thermal management using aluminum components.

The aftermarket opportunity remains underpenetrated. As vehicle parcs age and customers become more quality-conscious, demand for branded replacement parts should grow. Endurance's distribution network and brand recognition position it well to capture this higher-margin business.

European operations could see margin expansion as recent acquisitions are integrated and optimized. The creation of centers of excellence should drive efficiency improvements. Cross-selling opportunities between European subsidiaries remain substantial.

Risks extend beyond the obvious. Technology disruption could come from unexpected directions—3D printing could disrupt traditional casting, new materials could replace aluminum, or autonomous vehicles could reduce overall vehicle demand. While Endurance monitors these trends, disruptive change often comes faster than incumbents expect.

Regulatory changes present both opportunities and threats. Stricter emission norms benefit Endurance's lightweight components but could also reduce overall vehicle affordability. Safety regulations drive content per vehicle but also increase costs. Trade policies could disrupt carefully constructed global supply chains.

The capital allocation record, while generally good, shows some concerning signs. Recent acquisitions have been made at higher multiples than earlier deals. The push into electronics and batteries requires capabilities quite different from mechanical components. Integration risks increase with each acquisition, and culture dilution is a real concern as the company globalizes.

The Investment Verdict depends on one's investment philosophy and time horizon. For patient, long-term investors who believe in India's consumption story and the gradual premiumization of mobility, Endurance offers a relatively safe way to participate with a company that has proven execution capabilities and sustainable competitive advantages.

For growth investors seeking multibaggers, Endurance might disappoint. The company's size and maturity limit explosive growth potential. Returns are likely to be steady rather than spectacular. The high promoter holding limits the potential for significant re-rating even if fundamentals improve.

For value investors, the question is whether current valuation adequately reflects both the quality of the business and its growth prospects. The answer isn't obvious—Endurance isn't statistically cheap, but neither is it egregiously expensive given its market positions and capabilities.

Perhaps the most balanced view is that Endurance represents a high-quality company at a fair price. Not every investment needs to be a contrarian bet or a momentum play. Sometimes, owning good businesses run by capable managers at reasonable valuations is enough. Endurance might not make anyone rich quickly, but it's unlikely to destroy wealth either—and in the volatile world of auto components, that stability has value.

XI. Reflections & Future Outlook

As we reach the conclusion of our deep dive into Endurance Technologies, it's worth stepping back to appreciate the broader narrative. This isn't just a story about aluminum castings or suspension systems—it's a case study in how Indian manufacturing can compete globally, how family businesses can professionalize without losing their entrepreneurial edge, and how patient capital allocation can create enduring value.

The Transformation Journey from single-customer supplier to global Tier-1 is remarkable when viewed in its entirety. In 1985, Endurance was entirely dependent on Bajaj Auto, operating from a single plant, with technology licensed from others. Today, it serves dozens of global OEMs from 33 plants across continents with proprietary technology. This transformation didn't happen through a single bold move but through thousands of incremental improvements, each building on the last.

The journey teaches us that industrial development isn't about leapfrogging stages but progressing through them. Endurance had to master basic manufacturing before attempting complex assemblies. It had to succeed in India before venturing abroad. It had to prove itself with two-wheelers before entering four-wheeler markets. Each stage provided learnings that enabled the next.

Lessons on Family Business Succession and Separation are particularly relevant for Indian business. The 2002 separation of the twin brothers could have been acrimonious and value-destructive. Instead, it was handled with maturity, allowing both Endurance and Varroc to flourish independently. This shows that family business splits, often seen as negative, can actually unlock value when handled properly.

The governance evolution is equally instructive. The Jain family maintained control while progressively professionalizing management. They brought in independent directors before going public. They separated ownership from operation. They created systems that could function without daily family involvement. This balance between family values and professional management is something many Indian businesses struggle with.

India's Auto Component Industry Evolution is perfectly captured in Endurance's story. From import substitution in the 1980s to global competitiveness in the 2020s, the industry has transformed remarkably. Endurance both benefited from and contributed to this evolution. Its success encouraged suppliers to upgrade capabilities. Its global acquisitions showed that Indian companies could compete internationally. Its IPO demonstrated that manufacturing companies could create significant wealth.

The industry's future looks even more interesting. As global supply chains reconfigure post-COVID, India has an opportunity to capture a larger share of global auto component sourcing. Companies like Endurance, with proven capabilities and global footprints, are ideally positioned to benefit. The shift to EVs, while disruptive, could actually accelerate this trend as new supply chains are established.

The Next Decade presents both enormous opportunities and existential challenges. EVs will definitely gain share, though the pace remains uncertain. For Endurance, this means managing two businesses simultaneously—maximizing cash flows from ICE components while investing in EV technologies. This dual challenge requires careful capital allocation and organizational ambiguity tolerance.