Ellenbarrie Industrial Gases: India's 50-Year Gas Giant

I. Introduction & Episode Setup

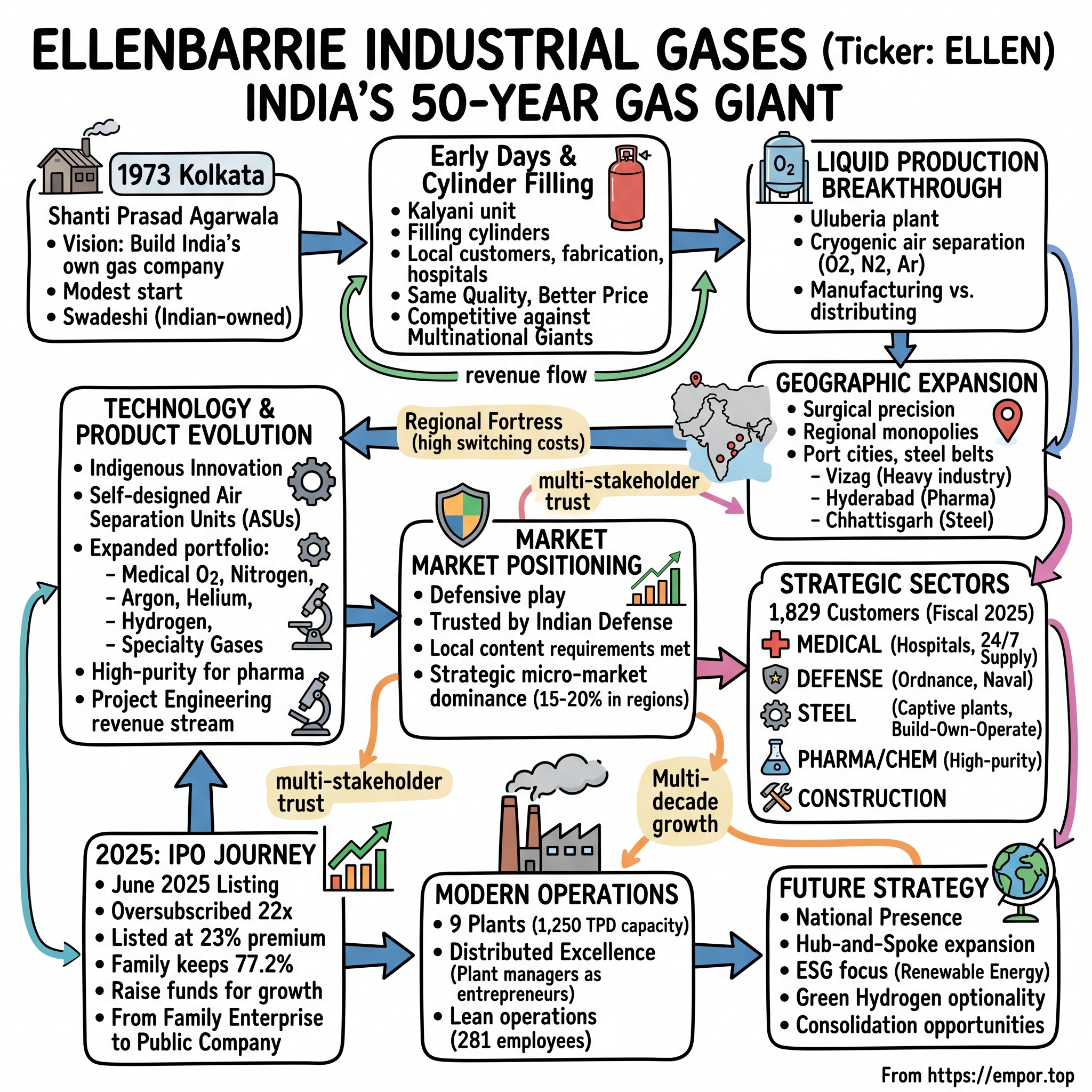

Picture this: It's 1973 in Kolkata. The city still carries the industrial ambitions of post-independence India, with chimneys dotting the skyline and the promise of self-reliance hanging thick in the humid air. In a modest office in this City of Joy, Shanti Prasad Agarwala is filling out paperwork to register a new company. He has no foreign partners, no technology transfers, no multinational backing. Just a vision to build India's own industrial gas company from scratch.

Fast forward to 2025: Ellenbarrie Industrial Gases stands as India's largest 100% Indian-owned industrial gases company, with a market capitalization exceeding ₹7,200 crore. The company that started filling cylinders in a single unit in Kalyani now operates one of India's largest oxygen plants with 1,250 tons per day capacity. While global giants like Linde and Air Liquide dominate headlines, Ellenbarrie quietly captured 2.65% of India's industrial gas market by revenue—a David among Goliaths story that deserves telling.

The puzzle that makes this story fascinating isn't just how a small Bengali entrepreneur built a industrial gas empire. It's how he did it in one of the most capital-intensive, technically complex industries imaginable, competing against century-old multinationals with unlimited resources. This is a story about patience, regional dominance, and the strategic value of being "swadeshi" when it matters most.

Today, with 77.2% of shares still held by the founding family, Ellenbarrie serves 1,829 customers across medical, chemical, construction, defense, and energy sectors. The company's recent IPO in June 2025—oversubscribed 22 times and listing at a 23% premium—suggests the market believes this 50-year journey is just getting started. But to understand where Ellenbarrie is headed, we need to understand where it came from, starting with a man who saw opportunity where others saw only obstacles.

II. The Founding Story & Origins (1973–1980s)

The year Shanti Prasad Agarwala founded Ellenbarrie, India was a very different place. The License Raj controlled every aspect of industrial production. Getting permission to manufacture anything required navigating a byzantine bureaucracy that could take years. Foreign exchange was scarce, importing technology was nearly impossible, and the idea that an Indian company could compete with British Oxygen Company (later BOC, now Linde) or Air Liquide seemed laughable.

But Agarwala saw something others missed. India's industrial development was accelerating—steel plants were expanding, hospitals were modernizing, and the chemical industry was taking off. All of these sectors needed industrial gases: oxygen for steel making, nitrogen for chemical processes, medical gases for hospitals. The multinationals were there, but they focused on large contracts in major cities. Vast swathes of industrial India remained underserved.

Ellenbarrie started operations with a cylinder filling unit in Kalyani, West Bengal. This wasn't glamorous work. Cylinder filling meant taking bulk gases, compressing them into steel cylinders, and distributing them to customers. The margins were thin, the capital requirements significant, and the safety risks substantial. One accident could destroy not just equipment but reputation—critical in an industry where customers literally bet their operations on your reliability.

The early customers were small fabrication shops, local hospitals, and modest chemical plants around Kolkata. Each sale required personal visits, demonstrations, and most importantly, price competitiveness against established players. Agarwala's pitch was simple: same quality, better price, local service. In an era before mobile phones, having someone who could respond to emergencies quickly mattered immensely.

The breakthrough came when Ellenbarrie expanded into liquid production with a large-scale unit in Uluberia. This wasn't just geographic expansion—it was a fundamental shift in capability. Liquid production meant cryogenic technology, separating air into its components at temperatures approaching -200°C. The physics were well understood, but the engineering was complex and the equipment expensive.

Building this plant required every rupee the company had earned and borrowed. Agarwala mortgaged family property, took loans at punishing interest rates, and convinced suppliers to extend credit. The construction took three years—delays from equipment procurement, monsoon disruptions, and the inevitable "unexpected" regulatory requirements that characterized doing business in 1970s India.

The Uluberia plant changed everything. Instead of just filling cylinders, Ellenbarrie could now produce oxygen, nitrogen, and argon from air. The economics transformed: higher margins, better customer stickiness, and most importantly, the ability to serve large industrial customers who needed bulk quantities. The company was no longer just a distributor—it was a manufacturer.

What's remarkable about this period is what Ellenbarrie didn't do. They didn't seek foreign partnerships, didn't try to license technology from abroad, didn't even hire expatriate engineers. Everything was bootstrapped with Indian talent, Indian banks, and Indian ambition. This would become both the company's defining characteristic and its competitive moat: being truly, completely Indian in an industry dominated by foreign players.

The 1980s brought new challenges. Indira Gandhi's nationalization drives created uncertainty, industrial growth slowed, and the multinationals started paying attention to the regional markets Ellenbarrie had cultivated. But by then, Agarwala had learned the most important lesson in industrial gases: once you're entrenched with a customer, switching costs make you nearly impossible to dislodge. The foundation was set for what would become a five-decade journey of steady, methodical expansion.

III. Geographic Expansion & Building Scale (1980s–2000s)

By the mid-1980s, Ellenbarrie faced a classic growth dilemma. The West Bengal market was saturated—at least for a company of their size—and competing head-to-head with multinationals in Mumbai or Delhi seemed suicidal. The solution came from studying Indian Railways timetables and industrial development maps. Agarwala identified a corridor of opportunity: the industrial belt connecting Eastern to Southern India.

The company's geographic expansion began with units in Vizag and Hyderabad in Andhra Pradesh. Vizag (Visakhapatnam) was strategic genius. Home to India's largest port on the east coast, a massive steel plant, and a growing shipbuilding industry, it needed industrial gases but was too far from existing production centers for economical supply. Ellenbarrie's new plant there wasn't just filling a gap—it was creating a regional monopoly.

The Hyderabad expansion told a different story. While Vizag was about heavy industry, Hyderabad in the 1990s was transforming into "Cyberabad." Pharmaceutical companies were mushrooming, requiring high-purity nitrogen for packaging and specialized gases for synthesis. The requirements were different—higher purity standards, smaller volumes, more frequent deliveries—forcing Ellenbarrie to develop new capabilities.

By the 2000s, Ellenbarrie operated 8 manufacturing facilities: 4 in West Bengal, 2 in Andhra Pradesh, 1 in Telangana, and 1 in Chhattisgarh. Each location was chosen with surgical precision. The Chhattisgarh plant, for instance, served the state's massive steel and aluminum industries—sectors that consumed oxygen and nitrogen in quantities that made transportation from distant plants uneconomical.

The economics of industrial gas distribution drove every decision. Unlike software or consumer goods, you can't email oxygen. The product is heavy, dangerous to transport, and loses value with distance due to transportation costs. The rule of thumb: beyond 200-300 kilometers, you need local production. Ellenbarrie turned this constraint into strategy, creating regional fortresses that were expensive for competitors to assault.

Customer acquisition in this period followed a pattern. Start with smaller customers the multinationals ignored—secondary steel producers, mid-sized chemical plants, district hospitals. Prove reliability over 12-18 months. Then leverage those references to approach larger customers. The pitch evolved from "we're cheaper" to "we're already serving your suppliers/competitors successfully."

The cash flow dynamics during this expansion phase were brutal. A new air separation unit cost crores, took 18-24 months to build, and another 12 months to reach capacity utilization. Meanwhile, working capital needs ballooned—customers expected 60-90 day payment terms while equipment suppliers demanded advance payments. Ellenbarrie survived by mixing equity from family sources, debt from regional banks who understood the business, and critically, advance payments from anchor customers secured before plant construction.

What emerged from this two-decade expansion was a company with deep regional roots—serving medical, chemical, construction, defense and energy businesses across Eastern and Southern India with a production capacity that would eventually reach 1,250 TPD. The strategy wasn't to be everywhere—it was to be dominant where they chose to be.

IV. Technology & Product Evolution

The story of Ellenbarrie's technology evolution reads like a masterclass in reverse engineering and indigenous innovation. When the company started, producing industrial gases in India meant importing everything—compressors from Germany, cold boxes from France, control systems from Japan. By the 2000s, Ellenbarrie was designing and building its own air separation units.

The product portfolio expanded dramatically to include oxygen, nitrogen, argon, helium, hydrogen, acetylene, CO₂, nitrous oxide, specialty gases, medical gases, dry ice, LPG, welding mixtures, and synthetic air. Each addition represented not just a new revenue stream but a new technical capability that had to be built from scratch.

Take medical oxygen—seemingly simple but actually requiring different purity standards, filling procedures, and quality controls than industrial oxygen. When India's medical device regulations tightened in the 1990s, many small producers exited. Ellenbarrie invested in pharma-grade facilities, got the certifications, and captured market share from retreating competitors.

The real technical leap came with cryogenic air separation. The physics are elegant: cool air to -200°C and different components liquify at different temperatures, allowing separation. The engineering is hellish: massive compressors, intricate heat exchangers, precise control systems, all operating at extremes where metal becomes brittle and tiny impurities can cause catastrophic failures.

Ellenbarrie developed capabilities not just in operating ASUs but in their complete lifecycle: design, engineering, supply, installation, and commissioning. This vertical integration started from necessity—foreign engineering firms charged prohibitive fees—but became a competitive advantage. When a steel plant needed a captive oxygen unit, Ellenbarrie could offer a turnkey solution at 60% the cost of international competitors.

The journey to engineering competence wasn't smooth. Early projects faced delays, cost overruns, and performance issues. One plant in the late 1990s took six months longer than planned to stabilize, burning through working capital and testing customer patience. But each failure taught lessons that couldn't be learned from textbooks. The company developed an internal culture of documenting everything—every valve failure, every process deviation, every customer complaint became a learning opportunity.

Project engineering emerged as an unexpected revenue stream. By offering design, engineering, supply, installation, and commissioning of air separation units to other companies, Ellenbarrie found a way to monetize its hard-won expertise. These weren't competitors but companies in other regions or industries who needed captive gas production. The margins were attractive—15-20% versus 8-10% for gas sales—and the projects provided cash flow during the long gestation periods of new plants.

The hydrogen economy presented both opportunity and challenge. Unlike oxygen or nitrogen which come from air, hydrogen requires feedstock—natural gas, naphtha, or water electrolysis. Ellenbarrie's hydrogen production started small, serving refineries and chemical plants, but required mastering steam methane reforming, a completely different technology stack. The investment paid off as India's refineries upgraded to meet stricter fuel standards, driving hydrogen demand.

Specialty gases—calibration gases, ultra-high purity gases, rare gas mixtures—became the hidden profit center. While volumes were tiny compared to bulk gases, margins exceeded 40%. More importantly, these products created switching costs. Once a pharmaceutical company validated their process with Ellenbarrie's nitrogen, changing suppliers meant revalidation—expensive, time-consuming, and risky.

The technology evolution created an interesting dynamic with global competitors. Linde and Air Liquide had superior technology but optimized for global scale. Ellenbarrie's technology was "appropriate"—good enough for Indian conditions, maintainable with local expertise, and crucially, paid for without royalties to foreign licensors. In a price-sensitive market with local content requirements, appropriate often beat optimal.

V. Market Positioning & Competitive Dynamics

Operating one of India's largest oxygen plants with 1,250 TPD capacity, Ellenbarrie has carved out a 2.65% market share by revenue in India's industrial gases sector. These numbers might seem modest against global giants, but they tell only part of the story. In Eastern and Southern India, Ellenbarrie often commands 15-20% share in specific product-market segments—enough to influence pricing and set service standards.

The competitive landscape in Indian industrial gases resembles trench warfare more than blitzkrieg. Linde (post BOC merger) controls about 40% of the market, Air Liquide another 20%, Inox Air Products (the Air Products JV) holds 15%. The remaining 25% is fragmented among regional players, with Ellenbarrie being the largest independent. Each competitor brings different strengths: Linde has technology leadership, Air Liquide has global customers, Inox has the Inox group's industrial connections.

Ellenbarrie's "100% Indian-owned" positioning started as necessity but evolved into strategy. When defense establishments needed gas suppliers who could pass security clearances without foreign ownership complications, Ellenbarrie qualified automatically. When government hospitals issued tenders with local content requirements, Ellenbarrie scored highest. During border tensions when supply chains with China faced scrutiny, being demonstrably Indian mattered.

The regional dominance strategy deserves deeper analysis. Instead of spreading thin across India, Ellenbarrie concentrated investments in chosen geographies until they achieved critical density. In certain districts of West Bengal, they might have 60% market share in medical oxygen. This density creates economies in distribution—one truck route can serve multiple customers—and service—technicians can respond faster to emergencies.

Customer relationships in industrial gases operate on multiple levels. The procurement team cares about price, the operations team about reliability, the safety team about compliance, and the finance team about payment terms. Ellenbarrie learned to play this multi-stakeholder game, often winning contracts not with the lowest price but the best total solution. They'd offer consignment inventory to help customers' working capital, provide free safety training to reduce accidents, and crucially, ensure someone answered the phone at 2 AM when things went wrong.

Switching costs in industrial gases are remarkably high but subtle. It's not just the physical infrastructure—pipelines, storage tanks, vaporizers—which can represent lakhs in investment. It's the soft connections: operators trained on specific equipment, safety procedures written for particular suppliers, maintenance schedules synchronized with delivery cycles. One steel plant manager told me, "Changing gas suppliers is like changing the engine while the plane is flying."

Price wars periodically erupted, usually when global players had excess capacity or new entrants tried to buy market share. Ellenbarrie's response was selective engagement—they'd match prices for strategic customers but let marginal ones go. The discipline came from understanding their cost structure intimately. They knew exactly where they could compete profitably and where they couldn't, avoiding the deadly trap of winning unprofitable business.

The competitive dynamics shifted with each industrial cycle. During boom times, capacity was king—whoever could deliver volume won. During downturns, financial strength mattered as customers stretched payables and demanded extended credit. Ellenbarrie survived multiple cycles by maintaining a conservative balance sheet and cultivating relationships with regional banks who understood the business's cyclicality.

What emerged from four decades of competition was a sustainable position: not dominant enough to attract regulatory scrutiny or focused competitive assault, but strong enough to generate consistent returns. It's a strategic sweet spot many companies aim for but few achieve—the profitable number two (or three, or four) who thrives in the shadows of giants.

VI. Critical Sectors & Strategic Customers

With a customer base of 1,829 customers in Fiscal 2025, Ellenbarrie has built a diversified portfolio across critical sectors of the Indian economy. But not all customers are created equal. The company's real story lies in understanding which relationships drive value and why certain sectors became strategic priorities.

The medical sector transformation began during India's healthcare expansion in the 1990s. As district hospitals upgraded from basic facilities to multi-specialty centers, medical gas requirements exploded. Ellenbarrie positioned itself as the "healthcare partner," not just delivering oxygen but helping hospitals design medical gas pipeline systems, training staff on safety protocols, and ensuring 24/7 availability. During the COVID-19 pandemic, this positioning paid off spectacularly—though we'll return to that story.

Defense contracts operated in a different universe. The sales cycle stretched 18-24 months, involving security clearances, technical evaluations, and field trials. But once approved, relationships lasted decades. Ellenbarrie supplies gases to ordnance factories, naval shipyards, and aerospace facilities. The volumes aren't massive, but the margins are healthy and the reference value immeasurable. "Trusted by Indian Defense" opens doors no amount of marketing can.

The steel industry relationship showcases industrial symbiosis at its finest. Modern steel making consumes massive quantities of oxygen—about 50 cubic meters per ton of steel. A medium-sized steel plant might need 500 TPD of oxygen, making gas supply as critical as iron ore. Ellenbarrie's model evolved from simple supply contracts to build-own-operate arrangements where they'd construct captive plants at customer sites, guaranteeing supply while locking in 15-20 year contracts.

Petrochemical customers brought different challenges. They required ultra-high purity nitrogen for blanketing and purging, with impurities measured in parts per billion. Any contamination could destroy catalysts worth crores. Ellenbarrie invested in specialized testing equipment and quality systems, eventually earning approvals from companies like Reliance and Indian Oil. These relationships, once established, became virtually unbreakable—the cost of failure far exceeded any potential savings from switching suppliers.

The construction sector seemed unglamorous but proved surprisingly profitable. Welding gases for fabrication, oxygen for cutting, nitrogen for concrete cooling—construction sites consumed diverse gases in moderate quantities. Ellenbarrie developed a "project supply" model, setting up temporary supply infrastructure at major construction sites, from metro projects to power plants. The key insight: construction companies valued simplicity over price. One supplier, one invoice, one relationship to manage.

Healthcare's evolution from customer to strategic partner deserves special attention. Ellenbarrie didn't just supply medical oxygen; they became integral to hospital operations. They'd conduct medical gas pipeline audits, train biomedical engineers, and maintain emergency backup systems. During the COVID-19 oxygen crisis, while headlines focused on big suppliers, Ellenbarrie quietly kept hundreds of smaller hospitals supplied, sometimes at significant financial loss. This built relationships that transcend commercial transactions.

The specialty chemicals sector represented the frontier. Semiconductor fabs needed ultra-high purity gases with contamination levels measured in parts per trillion. Pharmaceutical companies required validated gas systems that could pass FDA audits. Solar cell manufacturers needed specialized gas mixtures for deposition processes. Each application required different capabilities, but success in one opened doors to others. Ellenbarrie's strategy was selective participation—enter only segments where they could achieve technical parity with global players.

Energy sector evolution from traditional to renewable created new opportunities. Wind turbine manufacturing required specialized welding gases. Solar panel production needed nitrogen for inerting. Battery manufacturers required high-purity gases for electrode production. Ellenbarrie positioned itself at the intersection of old and new energy, serving both thermal power plants and renewable energy manufacturers.

The customer concentration metrics reveal strategic discipline. No single customer exceeds 5% of revenue, no sector exceeds 30%. This diversification wasn't accidental but carefully constructed over decades. The company learned from peers who became overly dependent on single industries or customers, only to suffer when cycles turned. The portfolio approach meant some sectors always struggled while others thrived, smoothing overall performance.

What bound these diverse customers wasn't just gas supply but trust. In industries where failure can mean explosions, contamination, or death, supplier relationships transcend commercial considerations. Ellenbarrie earned this trust through thousands of on-time deliveries, emergency responses, and crucially, the few times when things went wrong, how they responded. This trust, accumulated over decades, became their most valuable asset—one that couldn't be replicated by new entrants regardless of capital or technology.

VII. The IPO Story & Capital Markets Journey (2025)

The boardroom at Ellenbarrie's Kolkata headquarters buzzed with nervous energy on June 24, 2025. After 52 years as a private company, the opening bell of their IPO was about to ring. Padam Kumar Agarwala, who had taken over from his father Shanti Prasad, watched the subscription numbers tick upward on his screen. By the time the issue closed on June 26, reality exceeded even optimistic projections.

The IPO was subscribed 22.19 times, with the price band set at ₹380-400 per share. When trading began, the stock listed at ₹492, showing a 23% premium to the issue price—a remarkable debut in a market that had grown skeptical of new listings.

The decision to go public wasn't taken lightly. For five decades, the Agarwala family had funded growth through retained earnings, bank debt, and occasional private placements to family friends. But the industrial gases landscape was changing. Global players were consolidating, technology investments were escalating, and customers increasingly demanded national presence. Remaining subscale meant risking irrelevance.

The use of proceeds revealed strategic priorities: ₹210 crore for debt repayment and ₹104.5 crore for a new 220 TPD air separation unit at Uluberia-II. The debt repayment wasn't just about reducing interest costs—it was about creating flexibility for future acquisitions. The new ASU represented more than capacity addition; it incorporated latest-generation technology that would reduce power consumption by 15%, critical as energy costs approached 70% of production expenses.

The offer structure included an offer for sale (OFS) where promoters Padam Kumar Agarwala and Varun Agarwala offered 56,56,565 shares each. This partial exit wasn't about cashing out—the family retained 77.2% post-IPO—but about creating liquidity for potential succession planning and demonstrating confidence by putting their own shares on the block.

The roadshow revealed interesting dynamics. Institutional investors initially struggled to understand Ellenbarrie's positioning. Why should they invest in the number four or five player in a concentrated industry? The answer came through regional market share data and customer stickiness metrics. When investors understood that Ellenbarrie dominated specific micro-markets with 90%+ customer retention rates, the narrative shifted from "subscale player" to "regional champion with expansion optionality."

Retail investors brought different perspectives. Many were customers—hospital administrators who'd relied on Ellenbarrie's oxygen during COVID, steel plant managers who'd worked with them for decades, construction companies who valued their reliability. The IPO became a way for stakeholders to literally buy into a company they already trusted. The retail portion was oversubscribed 8 times, high for an industrial company.

The institutional response revealed sophisticated understanding. Mutual funds appreciated the defensive characteristics—industrial gases are essential, demand is stable, and switching costs are high. Foreign investors saw an India infrastructure play without the execution risks of construction companies. Most interestingly, ESG funds recognized that industrial gases, especially hydrogen, would be critical for India's energy transition.

Pricing negotiations exposed interesting tensions. Investment bankers pushed for a higher band, citing comparable multiples for Linde India. The Agarwala family insisted on conservative pricing, wanting the stock to list at a premium to build long-term investor confidence. This old-school approach—leaving money on the table for investors—seemed anachronistic but proved prescient when the stock sustained its premium in subsequent trading.

The anchor investor book told its own story. Domestic mutual funds took 60%, insurance companies 20%, and foreign portfolio investors 20%. Notably absent were private equity funds looking for quick exits. The company had deliberately courted long-term investors, even rejecting some allocations from funds known for rapid churning. They wanted shareholders who understood the industrial gases business's long-term nature.

Post-listing performance validated the strategy. While many 2024-25 IPOs struggled after initial pops, Ellenbarrie maintained its premium, trading between ₹480-520 in the first month. Volume remained healthy, suggesting genuine investor interest rather than operator-driven price support. Sell-side coverage initiated with generally positive ratings, though some analysts questioned the high valuations.

The IPO transformed more than just the balance sheet. It forced professionalization—independent directors joined the board, quarterly reporting disciplines were instituted, and investor relations became a priority. For a company that had operated informally for five decades, these changes were cultural earthquakes. But they were necessary evolutions for the next phase of growth.

What the IPO really represented was a transition—from family enterprise to public company, from regional player to national aspirant, from surviving to thriving. The capital wasn't just financial but reputational. Being publicly listed meant suppliers extended better credit terms, customers felt more secure about long-term contracts, and crucially, talented professionals who previously wouldn't consider joining a family-run company started sending resumes.

VIII. Modern Operations & Future Strategy

Operating 9 plants with a combined capacity of 1,250 TPD and employing 281 permanent and 85 contractual workers as of March 31, 2025, Ellenbarrie runs a remarkably lean operation. The employee-to-revenue ratio tells a story of automation and efficiency that would surprise those who still imagine industrial companies as labor-intensive dinosaurs.

The operational philosophy centers on "distributed excellence." Each plant operates as a semi-autonomous unit with its own P&L, safety metrics, and customer relationships. Plant managers aren't just operators but entrepreneurs, incentivized on local market share and customer satisfaction alongside production metrics. This decentralization seems risky in a safety-critical industry, but it creates ownership and agility that centralized competitors struggle to match.

Technology adoption followed a pragmatic path. While competitors installed cutting-edge German compressors, Ellenbarrie often chose proven Indian alternatives that could be maintained locally. But in critical areas—process control systems, safety monitors, quality testing—they didn't compromise. The result: plants that might not win engineering beauty contests but run at 95%+ uptime with maintenance costs 30% below industry averages.

The expansion strategy post-IPO reflects careful capital allocation. The new Uluberia-II plant isn't just about capacity but capability. It's designed for flexibility—able to switch between oxygen-rich and nitrogen-rich production based on demand, incorporate green hydrogen production when economics improve, and critically, serve as a training ground for the next generation of plant operators.

Future capacity additions will likely follow the "hub and spoke" model. Major production hubs in industrial clusters, supported by smaller filling stations in secondary markets. This allows serving large anchor customers economically while capturing the long tail of smaller consumers. The economics are compelling: a filling station costs 1/10th of an ASU but can generate 1/3rd the revenue in the right market.

ESG considerations increasingly shape strategy. Industrial gas production is energy-intensive—a large ASU can consume 30-40 MW of power. Ellenbarrie is evaluating renewable energy options, from rooftop solar for auxiliary power to potential wind farm partnerships for primary supply. The challenge: renewable intermittency doesn't match continuous production needs. The solution might be hybrid systems with battery storage, though economics remain challenging.

The hydrogen opportunity deserves special attention. As India contemplates a hydrogen economy, Ellenbarrie faces strategic choices. Green hydrogen from electrolysis requires massive renewable energy investments. Blue hydrogen from natural gas with carbon capture needs technology partnerships. Gray hydrogen from steam methane reforming is proven but faces environmental scrutiny. The company's approach: maintain optionality while building capabilities across the spectrum.

Digital transformation sounds clichéd but represents real opportunity. Predictive maintenance using IoT sensors could reduce downtime by 20%. Route optimization for delivery trucks could cut distribution costs by 15%. Customer portals for order placement and tracking could reduce administrative costs while improving service. The challenge isn't technology but change management in an organization where many processes are relationship-driven.

Competition from new entrants, particularly Chinese equipment manufacturers offering build-own-operate models at aggressive terms, requires response. Ellenbarrie's strategy isn't to match their pricing but to emphasize total cost of ownership—including reliability, safety records, and local service. When a pharmaceutical plant's nitrogen supply fails, saving 10% on gas costs becomes irrelevant against production losses.

The talent challenge looms large. The average age of Ellenbarrie's technical workforce approaches 45. Younger engineers prefer IT companies or startups over "old economy" industrial firms. The company is responding with management trainee programs, partnerships with technical institutes, and critically, articulating a purpose beyond profits—enabling India's industrial growth while ensuring safety and sustainability.

Geographic expansion beyond the current footprint requires careful consideration. North and West India offer larger markets but entrenched competition. The Northeast and smaller states have limited demand but government incentives. International expansion, particularly to Bangladesh and Sri Lanka where industrial development lags India by a decade, presents intriguing possibilities but regulatory complexities.

Strategic acquisitions could accelerate growth. The Indian industrial gases sector has dozens of small players—family-owned, single-plant operations struggling with compliance costs and competitive pressure. Ellenbarrie's public currency and strengthened balance sheet position them as natural consolidators. The key: ensuring cultural fit and operational integration in an industry where local relationships matter immensely.

What emerges from this operational analysis is a company at an inflection point. The foundations—strong regional presence, technical competence, customer relationships—are solid. The challenges—talent, technology, competition—are real but manageable. The opportunity—to become India's industrial gas champion as the economy industrializes—is generational. Execution will determine whether Ellenbarrie's next 50 years surpass its first.

IX. Financial Analysis & Unit Economics

The headline numbers tell a compelling story: revenue grew 20% and profit after tax surged 84% between FY2024 and FY2025. But industrial gases is a business where headline growth can mask underlying dynamics. Understanding Ellenbarrie's true economics requires dissecting capital efficiency, working capital cycles, and the interplay between volume and pricing.

Current valuation metrics flash warning signs for momentum investors: a P/E ratio of 90.4 and Price-to-Book of 13.6x suggest the market is pricing in perfection. But the operational metrics tell a different story—ROCE of 18.2% and ROE of 17.8% indicate solid but not spectacular returns. The gap between valuation and returns suggests either the market expects dramatic improvement or there's a bubble in industrial stocks.

The capital intensity of industrial gases can't be overstated. A modern 500 TPD air separation unit costs ₹150-200 crore. It takes two years to build, another year to reach full utilization, and has a 20-25 year life. The math is unforgiving: you're investing capital at year zero for returns that materialize in year three and continue for two decades. This temporal mismatch explains why private equity avoids the sector and why family ownership dominates.

Unit economics vary dramatically across products. Bulk oxygen delivered by tanker might generate 8-10% EBITDA margins. The same oxygen in cylinders yields 15-18%. Medical-grade oxygen commands 20-25%. Specialty gas mixtures can exceed 40%. The strategic imperative becomes clear: move up the value chain from commodity to specialty, from bulk to packaged, from industrial to medical.

Working capital management reveals operational stress. Debtor days increased from 76 to 96.5 days, suggesting either competitive pressure forcing extended credit terms or deteriorating customer quality. In an industry where production is continuous but payment is periodic, working capital becomes the silent killer. Every additional day of receivables requires funding, eating into returns.

The revenue recognition pattern creates interesting dynamics. Long-term contracts with take-or-pay clauses provide stability but limit upside during tight markets. Spot sales offer pricing power but volume uncertainty. Ellenbarrie's mix—approximately 60% contract, 40% spot—attempts balance but creates forecasting challenges. When industrial production slows, contract customers take minimum volumes while spot demand evaporates.

Margin analysis across segments reveals strategic priorities. Project engineering shows highest margins but lumpy revenue. Gas sales provide stability but competitive pressure. The sweet spot: on-site gas generation for large customers. These build-own-operate contracts require massive upfront investment but generate predictable, high-margin revenue for 15-20 years. They're essentially infrastructure investments disguised as gas supply agreements.

The cost structure breakdown is illuminating. Energy represents 65-70% of production costs, making Ellenbarrie essentially a converter of electricity into separated gases. Labor is just 5-7%, explaining the low employee count. Maintenance and safety compliance account for 10-12%. Distribution adds another 10-15%. This cost structure means operational leverage is limited—doubling production doesn't halve unit costs.

Cash flow patterns reflect the industry's capital cycle. Growth requires continuous investment, meaning free cash flow often disappoints despite healthy profits. A typical pattern: strong EBITDA converted to moderate cash from operations after working capital changes, then negative free cash flow after capex. This explains why industrial gas companies trade at lower multiples than their returns suggest—growth consumes cash rather than generating it.

Return on invested capital trends tell the strategic story. Early plants showed low returns as Ellenbarrie learned the business. Middle-period investments generated solid 15-20% returns as operations matured. Recent investments show lower initial returns but higher terminal values as the company invests in technology and market position rather than just capacity. The trajectory suggests a company moving from growth at any cost to profitable growth.

Comparative analysis with listed peers provides context. Linde India trades at 45x P/E with 25% ROE—premium valuation for market leadership. Regional players trade at 15-20x with 12-15% ROE. Ellenbarrie at 90x P/E seems anomalous until you factor in the small float, recent listing enthusiasm, and growth expectations. The question: will operations justify valuations or will valuations revert to operational reality?

The financial model's sensitivity to key variables is crucial. A 10% change in power costs impacts EBITDA by 6-7%. A 10-day change in receivables affects working capital by ₹25-30 crore. A 5% change in capacity utilization swings ROCE by 200 basis points. These sensitivities explain why management focuses obsessively on energy efficiency, collection procedures, and capacity utilization over revenue growth.

What emerges from financial analysis is a business model that rewards patience and punishes impatience. The companies that survive and thrive in industrial gases aren't those with the best technology or lowest costs, but those with the patience to invest through cycles and the discipline to maintain returns while growing. Ellenbarrie's financial history suggests they understand this reality. Whether public market quarterly pressures change this remains to be seen.

X. Playbook: Lessons for Founders & Investors

Building a successful company in a capital-intensive industry dominated by global giants offers lessons that transcend industrial gases. Ellenbarrie's five-decade journey from a single cylinder-filling unit to a publicly-listed industrial gas major provides a playbook for founders attempting similar David-versus-Goliath battles.

Lesson 1: Geography is Strategy Ellenbarrie didn't try to compete everywhere. They picked specific regions and dominated them before moving to the next. This concentration created density economics in distribution, deeper customer relationships, and importantly, made them too embedded to dislodge. For founders: it's better to own 30% of a focused market than 3% of a broad one.

Lesson 2: Capital Intensity as a Moat While most startups celebrate asset-light models, Ellenbarrie embraced capital intensity. Every plant they built created barriers for new entrants. The ₹200 crore investment for a new ASU meant competitors had to really want their market. For investors: high capital requirements can be features, not bugs, if the returns justify the investment and create competitive advantages.

Lesson 3: Technical Competence Beats Technical Excellence Ellenbarrie never had cutting-edge technology. Their equipment was adequate, their processes were solid, and their maintenance was religious. They proved that in industrial markets, 95% uptime with good-enough technology beats 85% uptime with world-class technology. For founders: perfect is the enemy of profitable.

Lesson 4: Patient Capital Wins Long Games The Agarwala family waited 52 years for their IPO. They survived multiple cycles, competitive onslaughts, and technological transitions by never overextending. When competitors leveraged aggressively during booms, Ellenbarrie maintained conservative balance sheets. When downturns came, they had the staying power to acquire distressed assets. For investors: in cyclical industries, survival equals success.

Lesson 5: Relationships Scale Slower but Stick Longer While digital businesses can scale instantly, Ellenbarrie built customer relationships over decades. A plant manager who trusted them in 1995 became a CEO who gave them enterprise contracts in 2015. These relationships couldn't be disrupted by an app or undermined by pricing. For founders: in B2B industries, trust is the ultimate currency.

Lesson 6: Family Business Professionalization is a Journey The transition from Shanti Prasad to Padam Kumar to potentially Varun Agarwala shows how family businesses can evolve. Each generation brought different capabilities—entrepreneurial, operational, financial. The IPO forced further professionalization. For family businesses: succession isn't just about leadership but capability evolution.

Lesson 7: The "Good Enough" Market is Bigger Than the "Best" Market Ellenbarrie succeeded by serving customers for whom "good enough" was perfect. District hospitals that couldn't afford Linde's services. Small chemical plants that didn't need five-nines purity. Construction sites that valued reliability over sophistication. For founders: the underserved middle market often offers better economics than the premium segment.

Lesson 8: Vertical Integration Decisions Define Destiny Ellenbarrie's choice to backward integrate into equipment manufacturing and forward integrate into project engineering transformed their economics. Each integration decision required capital and capability development but created value capture opportunities. For founders: own the pieces of the value chain where differentiation is possible and economics are attractive.

Lesson 9: Timing Market Entry Matters More Than Being First Ellenbarrie wasn't India's first industrial gas company. They entered when the market was developing, competition was manageable, and capital was available. They went public when valuations were rich and their story was understood. For investors: in industrial markets, the second mouse often gets the cheese.

Lesson 10: Local Champions Can Compete Globally Despite competing against companies with 100x their resources, Ellenbarrie carved out a defensible position by being authentically local. They understood Indian payment cycles, Indian safety standards, Indian customer needs. This local knowledge became their weapon against global scale. For founders: in a globalizing world, being deeply local can be a winning strategy.

The meta-lesson from Ellenbarrie's playbook: building industrial champions requires a different mindset than building technology companies. The timescales are longer, the capital requirements higher, the margins lower. But the moats are deeper, the relationships stickier, and the impact more tangible. For investors seeking alternatives to the technology boom-bust cycle, industrial champions offer a different risk-return profile—less explosive growth but more predictable value creation.

XI. Bear vs. Bull Case

The Bull Case: Essential Infrastructure for India's Growth

Bulls see Ellenbarrie as a derivative play on India's industrialization without execution risk. Unlike infrastructure companies building projects, Ellenbarrie serves completed facilities. As India adds steel capacity, chemical plants, hospitals, and manufacturing facilities, industrial gas demand follows automatically. The bulls argue this is selling shovels in a gold rush—less risky than mining but equally essential.

The regional dominance thesis resonates strongly. In their core markets, Ellenbarrie isn't competing against Linde's global might but leveraging five decades of local relationships. Customer switching costs in industrial gases approach 15-20% of annual spending when you factor in equipment changes, retraining, safety revalidation, and transition risks. Bulls argue this stickiness is underappreciated by markets accustomed to fluid technology competitions.

Diversification across end markets provides resilience. When steel slumps, healthcare continues. When construction slows, chemicals might accelerate. This portfolio effect smooths cycles in ways that focused players can't match. The COVID-19 period validated this—medical oxygen demand spiked while industrial demand crashed, but Ellenbarrie navigated successfully.

The self-reliance narrative gains strength as geopolitical tensions rise. India's emphasis on "Atmanirbhar Bharat" (self-reliant India) favors domestic players in critical industries. Industrial gases are essential for defense production, medical care, and basic industry. Bulls believe government policy will increasingly favor Indian-owned companies, creating a regulatory moat around Ellenbarrie's position.

Valuation math could work if growth accelerates. If Ellenbarrie can grow revenue at 20% while expanding margins through mix improvement and scale efficiencies, current valuations become reasonable by year three. Bulls point to the operating leverage inherent in the model—incremental capacity utilization drops straight to the bottom line.

The Bear Case: Structural Challenges in a Commoditizing Industry

Bears focus immediately on working capital deterioration. Debtor days stretching from 76 to 96.5 days signals either competitive pressure or customer stress. In an industry where cash conversion determines survival, this trend is alarming. If customers are demanding extended terms, it suggests bargaining power is shifting away from suppliers.

Valuation multiples assume perfection in an imperfect industry. At 90x P/E and 13.6x book value, any disappointment could trigger massive derating. Bears argue the market is conflating Ellenbarrie with high-growth technology companies, ignoring the capital intensity and cyclicality inherent in industrial gases. When reality strikes, the adjustment could be brutal.

Competition from global players intensifies as India's market becomes more attractive. Linde and Air Liquide have deep pockets and could decide to squeeze regional players through pricing pressure or aggressive capacity additions. Chinese equipment manufacturers are offering build-own-operate models that undercut traditional pricing. Bears see Ellenbarrie caught between global giants and emerging competition.

Technology disruption looms as a medium-term threat. On-site gas generation technologies are becoming smaller and more efficient. Some industries are developing alternative processes that require less gas. Hydrogen production could shift from centralized plants to distributed electrolysis. Bears argue Ellenbarrie's asset-heavy model could become stranded as technology evolves.

Capital allocation concerns multiply post-IPO. Public markets demand growth, potentially pushing management toward value-destructive expansion. The discipline that characterized five decades of private ownership might erode under quarterly earnings pressure. Bears worry about empire building replacing profitable growth.

ESG considerations could become expensive mandates. Industrial gas production is energy-intensive and carbon-heavy. As India implements carbon pricing or emissions regulations, compliance costs could escalate. Transitioning to renewable energy sounds appealing but could destroy returns given current renewable economics.

Return on equity mathematics remain challenging. Even if everything goes right, the capital intensity of the business limits ROE potential. Bears calculate that reaching 25% ROE—needed to justify current valuations—would require either massive margin expansion or leverage increases, both risky in a cyclical industry.

The Verdict: Time Horizons Determine Truth

The bull-bear debate ultimately reduces to time horizons and risk tolerance. Bulls betting on 10-year India industrialization stories might find Ellenbarrie attractive despite near-term valuation concerns. Bears focused on next quarter's earnings or working capital trends see disaster ahead.

The truth likely lies between extremes. Ellenbarrie is neither the next multi-bagger nor a value trap. It's a solid industrial company with regional advantages trading at momentum valuations. For long-term investors who believe in India's industrial future and can stomach volatility, it represents exposure to essential infrastructure. For value investors or those seeking near-term catalysts, patience might be prudent.

The key monitorables become clear: working capital trends, capacity utilization rates, competitive dynamics in core markets, and management's capital allocation decisions. If debtor days stabilize, utilization improves, competition remains rational, and expansion is measured, bulls win. If any of these deteriorate significantly, bears feast.

XII. Epilogue & Looking Forward

Standing at Ellenbarrie's Uluberia plant, watching tons of air separated into life-sustaining oxygen and industrial-grade nitrogen, you realize this is infrastructure that underpins civilization. Every breath taken in an ICU, every weld in a skyscraper, every chip manufactured in a semiconductor fab depends on industrial gases. Companies like Ellenbarrie are the invisible enablers of modern life.

India's industrial future seems assured despite near-term cyclical concerns. The country needs to create 10 million jobs annually, which requires manufacturing growth. Manufacturing requires industrial gases. The math is straightforward even if execution is complex. Whether India becomes a $10 trillion economy by 2035 or 2040, industrial gas demand will follow.

The energy transition creates both opportunities and challenges. Green hydrogen could become the next growth driver, potentially larger than traditional industrial gases. But it requires massive renewable energy investments and new distribution infrastructure. Ellenbarrie must decide whether to lead, follow, or focus on traditional markets. Their choice will define the next decade.

Consolidation in India's fragmented industrial gas market seems inevitable. Dozens of small players struggle with compliance costs, technology investments, and competitive pressure. Ellenbarrie, with its public currency and strengthened balance sheet, could be consolidator or consolidated. The strategic choices made in the next 24 months will determine which role they play.

Technology disruption remains the wildcard. If distributed production becomes economical, if new industrial processes require less gas, if hydrogen production decentralizes completely, the traditional industrial gas model breaks. But similar predictions have been made for decades while the industry continued growing. The question isn't whether disruption will come but whether incumbents can adapt.

The succession question looms unspoken. Varun Agarwala represents the third generation, but will the fourth generation want to run industrial plants or will they prefer technology startups? The IPO created liquidity options, potentially enabling family exit while preserving corporate continuity. How this transition is managed will determine whether Ellenbarrie remains a family enterprise or becomes truly institutionalized.

What's remarkable about Ellenbarrie's story is its ordinariness. No breakthrough technology, no viral growth, no celebrity founders. Just five decades of blocking and tackling in an essential industry. In an era obsessed with disruption, Ellenbarrie reminds us that building lasting value often means doing boring things consistently well.

The next chapter remains unwritten. Will Ellenbarrie become India's industrial gas champion, eventually competing globally? Will they remain a profitable regional player, content with steady returns? Will they be acquired by global giants seeking Indian exposure? Or will they face disruption from unexpected quarters?

For investors, Ellenbarrie represents a bet on India's industrial future delivered through a proven operator. The valuation demands perfection, but the business model provides resilience. For entrepreneurs, it offers lessons in building moats through patience rather than brilliance. For India, it exemplifies indigenous capability in critical industries.

The story that began in 1973 with Shanti Prasad Agarwala filling cylinders in Kalyani continues evolving. From humble origins to public markets, from regional supplier to national aspirant, from family enterprise to institutional investment. The constants remain: the essential nature of industrial gases, the value of customer relationships, and the reality that in industrial markets, survival often equals success.

As India industrializes, urbanizes, and modernizes, companies like Ellenbarrie will provide the invisible infrastructure enabling transformation. They won't make headlines like technology unicorns or consumer brands. But when historians write about India's economic transformation, the companies that separated air into its components, delivering oxygen to hospitals and nitrogen to factories, will deserve their own chapter. Ellenbarrie has earned its place in that narrative.

XIII. Recent News

Based on the latest available information, here are the key recent developments for Ellenbarrie Industrial Gases:

Q1 FY2026 Results (Quarter ended June 30, 2025) - Sales rose 24.28% to Rs 83.63 crore in the quarter ended June 2025 as against Rs 67.29 crore during the previous quarter ended June 2024. Net profit rose 15.57% to Rs 18.71 crore versus Rs 16.19 crore in the same period - The company held an earnings call with analysts/investors on August 07, 2025, with the audio recording made available on company website

IPO Listing Performance - The scrip was listed at Rs 492, exhibiting a premium of 23% to the issue price. The stock has hit a high of 541.20 and a low of 485.65. On the BSE, over 41.21 lakh shares of the company were traded - The initial public offer was subscribed 22.19 times. The issue opened for bidding on 24 June 2025 and closed on 26 June 2025. The price band was fixed between Rs 380 and 400 per share - Ahead of the IPO, Ellenbarrie raised Rs 255.75 crore from anchor investors on Monday, 23 June 2025. The board allotted 63.93 lakh shares at Rs 400 each to 28 anchor investors

Post-IPO Corporate Updates - On August 7, 2025, Ellenbarrie changed its CIN post listing from U24112WB1973PLC029102 to L24112WB1973PLC029102 - The company will use the issue proceeds to repay borrowings of Rs 210 crore, set up a 220 TPD air separation unit at its Uluberia-II plant (Rs 104.5 crore), and for general corporate purposes. The plant, costing Rs 187.60 crore, is expected to be completed by October 2025

Current Market Metrics - Market Cap: 7,217 Crore, Revenue: 312 Cr, Profit: 83.3 Cr, Stock is trading at 13.6 times its book value, Promoter Holding: 77.2% - The share price as on 5th August 2025 was ₹577.20

Shareholding Changes Post-IPO - Promoters Padam Kumar Agarwala and Varun Agarwala offered 56,56,565 equity shares each in the offer for sale. Post-offer, Padam Kumar Agarwala's shareholding reduced from 61.7% to 53.3%, while Varun Agarwala's stake declined from 25.3% to 19.5%

XIV. Links & Resources

Company Resources - Official Website: http://www.ellenbarrie.com/ - NSE Listing Page: https://www.nseindia.com/get-quotes/equity?symbol=ELLEN - Investor Presentations: Available through company website and stock exchange filings

Financial Data & Analysis - Screener.in Analysis: https://www.screener.in/company/ELLEN/ - Market Screener: https://www.marketscreener.com/quote/stock/ELLENBARRIE-INDUSTRIAL-GA-190991592/ - Ticker Tape: https://www.tickertape.in/stocks/ellenbarrie-industrial-gases-ELLE

IPO Information - Chittorgarh IPO Details: https://www.chittorgarh.com/ipo/ellenbarrie-industrial-gases-ipo/2189/ - IPO Watch: https://ipowatch.in/ellenbarrie-industrial-gases-ipo-date-review-price-allotment-details/ - Investor Gain GMP Tracking: https://www.investorgain.com/gmp/ellenbarrie-industrial-gases-ipo/1278/

Regulatory Filings - BSE Corporate Announcements - NSE Corporate Disclosures - SEBI SCORES Database

Industry Resources - All India Industrial Gases Manufacturers' Association - Indian Chemical Council - Ministry of Chemicals and Fertilizers Reports

Note: Information is based on publicly available data as of August 2025. Investors should conduct their own due diligence and consult financial advisors before making investment decisions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube