EID Parry: The Sugar Empire That Sweetened India's Independence

I. Introduction & Episode Roadmap

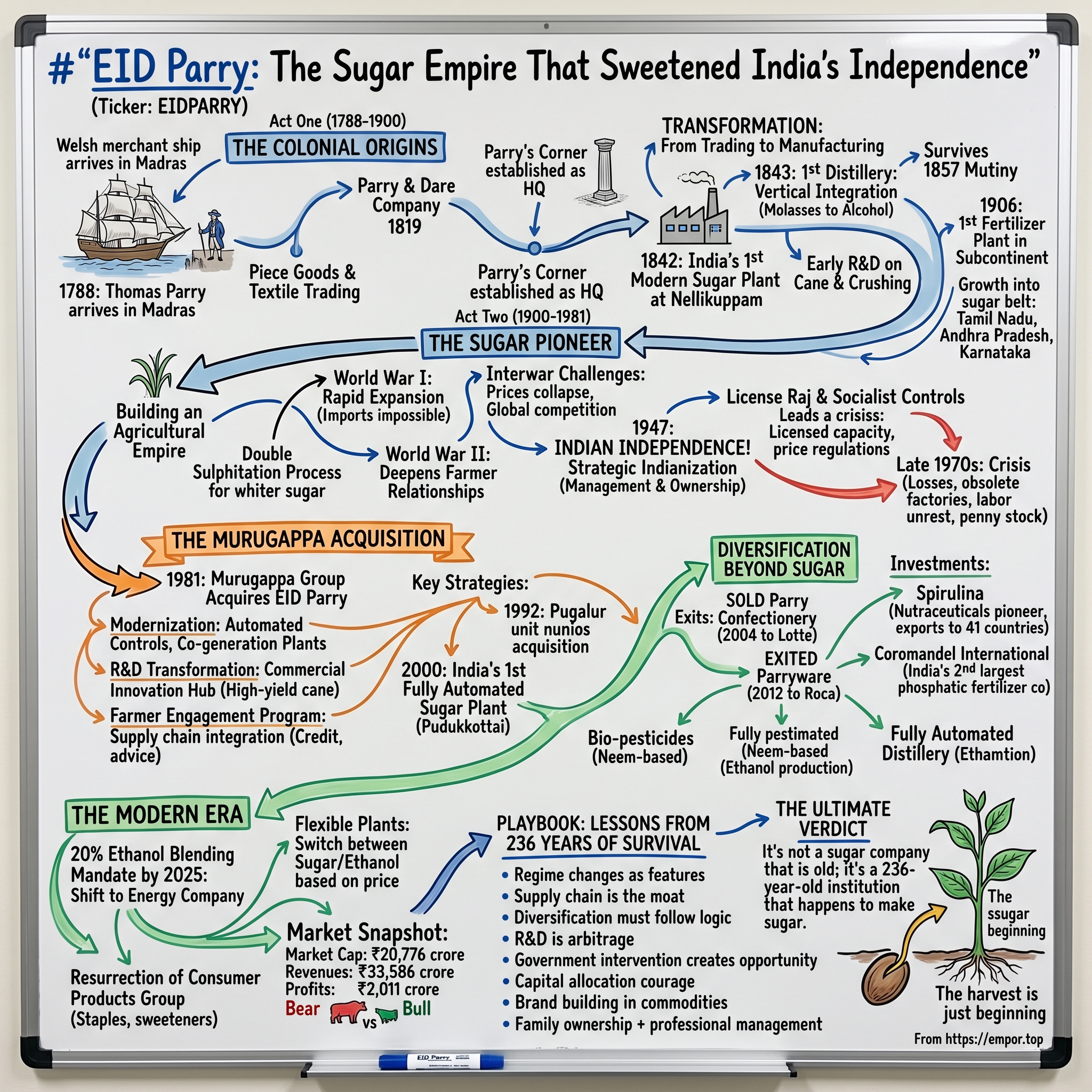

Picture this: A Welsh merchant steps off a ship in Madras harbor in 1788, the monsoon air thick with humidity and opportunity. Thomas Parry had no idea that the trading firm he was about to establish would outlive the British Empire itself, survive two world wars, witness India's independence, and emerge 236 years later as a ₹20,776 crore agricultural powerhouse. This isn't just another colonial trading house story—it's the improbable tale of how a piece goods business became India's sugar czar, pioneered the country's fertilizer industry, and somehow managed to thrive through every economic upheaval from the East India Company to economic liberalization.

Most investors today know EID Parry as the sugar and nutraceuticals arm of the Murugappa Group, generating ₹33,586 crores in revenue. But here's what they miss: this company literally invented modern sugar manufacturing in India. Before Parry set up that first plant in Nellikuppam in 1842, India—the land that gave sugar to the world—was importing refined sugar from Java and Mauritius. The irony is delicious.

The central question driving this story isn't just how a company survives 236 years—plenty of European firms have done that. It's how a colonial-era enterprise successfully transformed itself into an Indian company, survived the License Raj that killed countless businesses, and emerged stronger under family ownership. Most colonial firms either packed up after 1947 or slowly withered away. EID Parry did neither.

Today's snapshot reveals a company straddling multiple identities: It's India's second-largest sugar producer with 40,800 TCD crushing capacity. It's a global leader in spirulina, exporting to 41 countries. It's an ethanol producer riding the biofuel wave. And through its subsidiary Coromandel International, it's one of India's largest fertilizer companies. The market values all this at ₹20,776 crores—but is that the right price for 236 years of accumulated advantages?

What makes this story particularly fascinating is the three-act structure: Act One features Welsh and British entrepreneurs building an agricultural empire in colonial India. Act Two shows the traumatic transition through independence, nationalization threats, and the License Raj. Act Three unveils the Murugappa Group's 1981 acquisition and transformation of a creaking colonial relic into a modern agribusiness conglomerate. Each transition could have killed the company. Instead, each made it stronger.

We'll explore how a company founded when George Washington was president managed to reinvent itself for the age of ESG and ethanol blending mandates. We'll dissect the decisions to exit businesses like Parryware (remember those sanitaryware products in every Indian bathroom?) and Parry Confectionery (sold to Lotte in 2004). We'll understand why a sugar company became a spirulina pioneer and how government intervention—usually a business killer—became EID Parry's moat.

But most importantly, we'll answer the investor's question: In an era of tech unicorns and digital disruption, what's the value of 236 years of agricultural expertise, government relationships, and farmer networks? As we'll see, in India's agricultural sector, history isn't just context—it's competitive advantage.

II. The Colonial Origins: Thomas Parry's Indian Adventure (1788–1900)

Thomas Parry's arrival in Madras wasn't glamorous. In 1788, the Welsh trader stepped into a sweltering, chaotic port city where fortunes were made in indigo, textiles, and spices—but mostly lost to disease, competition, and the capricious whims of the East India Company. Parry had something most European adventurers lacked: patience and an eye for the mundane businesses others ignored. While contemporaries chased quick fortunes in opium and indigo, Parry started with banking and "piece goods"—essentially, textile trading. On July 17, 1788, he established what would become EID Parry, though nobody called it that yet.

The early years were about survival, not empire-building. Parry operated in the shadow of the East India Company, which controlled most legitimate trade. His genius was recognizing that the Company, focused on extracting maximum value for London shareholders, left gaps in the local market. Indian merchants needed banking services. British officials wanted European goods. The growing Anglo-Indian community required everything from wine to wagon wheels. Parry became the middleman's middleman, too small to threaten the Company, too useful to eliminate.

By 1819, Parry had accumulated enough capital and credibility to formalize operations. He partnered with John William Dare to establish "Parry and Dare Company." This wasn't just a rebrand—it marked the shift from individual trader to institutional presence. The partnership brought capital, connections, and most critically, continuity beyond a single person's mortality. In the disease-ridden tropics where European mortality rates exceeded 50% in the first year, this mattered. The Welsh trader's prescience was remarkable. The area where he established his headquarters would become known as Parry's Corner, with the corporate headquarters of EID Parry Company still standing there today—a testament to permanence in a city that has reinvented itself from Madras to Chennai. One of the original thirteen pillars erected by the British in 1773 to separate Black Town from White Town still stands in the Parry's building compound, a physical reminder of the colonial structures Parry navigated.

The real transformation came in 1842. While the East India Company was busy fighting the First Afghan War and annexing Sindh, Parry's successors made a bet that would define the company for the next two centuries: they established India's first modern sugar manufacturing plant at Nellikuppam, about 200 kilometers south of Madras. Think about the audacity of this move. India had been cultivating sugarcane for millennia—the word "sugar" itself comes from the Sanskrit "sharkara." Yet by the 1840s, the subcontinent was importing refined sugar from its own colonies' competitors. Parry's plant wasn't just about manufacturing; it was about reclaiming an industry that India had birthed.

The following year, 1843, the company doubled down, becoming the first sugar manufacturer in India to start a distillery. This wasn't diversification for its own sake—it was vertical integration before anyone called it that. Sugar production generates molasses as a byproduct; distilleries turn molasses into alcohol and industrial spirits. What others saw as waste, Parry saw as revenue.

By the 1850s, Parry & Co. had become the trading firm every British official and Indian merchant needed to know. They financed indigo cultivation, traded in textiles, imported machinery for the nascent railway boom, and exported everything from groundnuts to leather. The company operated like a proto-investment bank, providing credit to planters, advances to weavers, and working capital to smaller traders. In an economy starved of formal financial institutions, Parry filled the void.

The company's survival through the 1857 Sepoy Mutiny—when many British businesses saw their Indian operations destroyed—speaks to something deeper than luck. While other firms maintained an arms-length relationship with local populations, Parry had embedded itself into the agricultural economy. The company's agents spoke Tamil, its advances kept farmers afloat during bad monsoons, and its trading networks provided markets for crops that would otherwise rot in villages. This wasn't corporate social responsibility; it was enlightened self-interest executed brilliantly.

As the 19th century waned, Parry & Co. faced a choice that would define its next century: remain a trading house or become a manufacturer. The answer came in stages. First, more sugar plants. Then, in a move that presaged the Green Revolution by half a century, the company began manufacturing fertilizers in 1906—the first such operation in the Indian subcontinent. While the Swadeshi movement urged Indians to boycott British goods, Parry was quietly building the industrial infrastructure that would eventually make imports unnecessary.

III. The Sugar Pioneer: Building an Agricultural Empire (1842–1950)

The Nellikuppam sugar plant of 1842 wasn't just India's first—it was a declaration that India could industrialize its own agricultural wealth. Picture the scene: massive crushing wheels powered by bullocks, juice flowing through primitive filters, crystallization pans bubbling over wood fires. By today's standards, laughably inefficient. By 1840s standards, revolutionary. The plant could process 100 tons of cane per day, producing sugar that was finally competitive with imports from Java.

But here's what made Parry different from other colonial enterprises: they didn't just extract value, they created it. The company established what would become India's first private sector R&D facility, experimenting with cane varieties, crushing techniques, and crystallization methods. While the British Raj was content to export raw materials and import finished goods, Parry was proving that value addition could happen in India itself.

The 1906 decision to manufacture fertilizers reveals strategic thinking decades ahead of its time. The company's managers had noticed a troubling pattern: Indian soil was depleting, yields were falling, and farmers were trapped in cycles of debt. Fertilizers weren't just another product line—they were an investment in the sustainability of the supply chain. A sugar company needs sugarcane; sugarcane needs fertile soil; fertile soil needs fertilizers. The logic was circular and brilliant.

World War I transformed everything. Suddenly, imports were impossible, prices skyrocketed, and domestic production became a matter of survival, not choice. Parry's factories ran round the clock. The company expanded from Tamil Nadu into Andhra Pradesh and Karnataka, following the sugar belt of South India. By 1920, Parry operated six sugar plants and had become the largest sugar producer in the Madras Presidency.

The interwar period brought new challenges. Global sugar prices collapsed in the 1920s. Cuban and Javanese sugar flooded world markets. Many Indian sugar mills shut down. Parry survived through a combination of technological innovation and political maneuvering. The company pioneered the "double sulphitation" process that produced whiter sugar preferred by Indian consumers. More importantly, they lobbied successfully for protective tariffs, arguing that Indian sugar was essential for food security—an argument that would resonate through independence.

World War II marked another inflection point. The British government imposed price controls, requisitioned output for the war effort, and restricted expansion. Yet Parry emerged from the war stronger than ever. How? They had used the war years to deepen relationships with cane farmers, establishing cooperative agreements that guaranteed supply. They had invested in worker training, creating a generation of Indian engineers and chemists who could run complex industrial operations. Most presciently, they had begun preparing for a post-colonial future.

The run-up to independence in 1947 was treacherous for British businesses. Nationalist sentiment ran high. Calls for nationalization grew louder. Many British firms sold out cheap or simply abandoned their Indian operations. Parry did something remarkable: they Indianized. By 1947, most senior management positions were held by Indians. The company's shares were increasingly owned by Indian investors. When the Union Jack came down on August 15, 1947, Parry was already more Indian than British.

The early years of independent India tested every assumption. The new government, influenced by Fabian socialism, viewed private enterprise with suspicion. The sugar industry, deemed essential, faced strict controls: licensed capacity, regulated prices, mandatory levy for public distribution. Many companies crumbled under the regulatory burden. Parry adapted. They positioned themselves as partners in nation-building, not remnants of colonialism.

The 1953 decision to promote the fertilizer industry wasn't just prescient—it was existential. Prime Minister Nehru's government was obsessed with food security. The memories of the Bengal Famine of 1943 were fresh. Any company that could help India feed itself would receive government support. Parry's fertilizer operations became their ticket to survival in the License Raj. While sugar remained controlled, fertilizers received subsidies, allocated natural gas, and priority in Five Year Plans.

IV. The Murugappa Acquisition: Transformation Under New Ownership (1981–2000)

By 1981, EID Parry was a company in crisis. The grand old firm that had survived colonialism and independence was hemorrhaging money. Years of government price controls had destroyed margins. Underinvestment had left factories obsolete. Labor unrest was chronic. The company's shares, once blue-chip, had become penny stocks. Financial institutions like LIC, United India Assurance, and Unit Trust of India, who had accumulated stakes through loan conversions, wanted out. Enter the Murugappa Group.

The Murugappas were an unlikely savior. The family business, founded in 1900 by A.M. Murugappa Chettiar, had built its fortune in Burma before being forced to return to India during World War II. By 1981, they ran a successful but relatively small conglomerate: Tube Investments (bicycles), Carborundum Universal (abrasives), and Cholamandalam Finance. Taking over a 193-year-old sugar giant with 8,000 employees and massive legacy issues was either brilliantly ambitious or monumentally foolish.

M.V. Subbiah, the Murugappa patriarch who led the acquisition, saw something others missed. "Everyone looked at EID Parry's past problems," he later recalled. "We saw future potential." The Murugappas understood that India's sugar consumption, at 7 kg per capita, was a fraction of the global average. Economic liberalization was inevitable. When controls lifted, when Indians got richer, when soft drinks and confectionery markets exploded—sugar demand would soar. The question wasn't if, but when.

The first challenge was cultural. EID Parry's British-era management culture—hierarchical, formal, ossified—clashed with the Murugappa style: entrepreneurial, informal, family-driven. Senior managers who had spent decades in a controlled economy couldn't grasp concepts like market share or customer focus. The Murugappas didn't fire them en masse; instead, they brought in younger managers, created parallel structures, and let generational change do the work.

The November 1992 acquisition of the Pugalur sugar unit marked a turning point. This wasn't just capacity addition—it was a statement of intent. While other groups were diversifying away from commodities, the Murugappas were doubling down on sugar. But they were doing it differently. Pugalur became a laboratory for modernization: automated controls, co-generation power plants, zero-discharge effluent treatment. The message was clear: EID Parry would compete on efficiency, not government favor.

The R&D transformation was even more dramatic. The old Parry research station, once pioneering, had devolved into a sleepy outpost where scientists published papers nobody read. The Murugappas transformed it into a commercial innovation hub. The focus shifted from theoretical research to practical solutions: developing high-yield cane varieties, optimizing fertilizer formulations, creating value-added products from molasses. Within a decade, EID Parry's cane breeding program was setting industry benchmarks, with varieties that yielded 20% more sugar per acre.

The real masterstroke was the farmer engagement program. The Murugappas understood that in commodities, competitive advantage comes from supply chain control. EID Parry began providing farmers with credit, seeds, fertilizers, pesticides, and most importantly, agronomy advice. Field officers—many recruited from agricultural universities—worked directly with farmers, teaching everything from drip irrigation to optimal harvest timing. By 2000, over one lakh farmers had been trained. This wasn't corporate social responsibility; it was supply chain integration disguised as social service.

The year 2000 brought the crown jewel: India's first fully automated sugar plant at Pudukkottai. In an industry where most plants still used technology from the 1960s, Pudukkottai was a spaceship. Programmable logic controllers managed every process. A plant that would typically need 300 workers operated with 50. Sugar recovery rates hit 11.5%—when the industry average was 9.5%. The message to competitors was unmistakable: the future had arrived, and EID Parry owned it.

Yet the Murugappa transformation wasn't without casualties. The family's attempt to modernize labor relations triggered strikes in 1994 that shut plants for months. The push for efficiency led to VRS (Voluntary Retirement Schemes) that, while financially necessary, destroyed communities built around factory townships. The aggressive expansion strained balance sheets, forcing asset sales and restructuring. By 2000, EID Parry was profitable and growing, but the scars of transformation were visible.

V. The Diversification Play: Beyond Sugar (1990s–2010s)

The 1990s began with a question that would define EID Parry's next two decades: What business are we really in? Sugar? Agriculture? Nutrition? The answer, it turned out, was all of the above—and more. The company's diversification strategy reads like a textbook case of corporate ADD, yet hidden within the chaos was brilliant strategic logic.

The spirulina story began almost by accident. In 1993, a young scientist in EID Parry's R&D division was researching effluent treatment when he noticed blue-green algae thriving in wastewater ponds. Instead of seeing waste, he saw opportunity. Spirulina, it turned out, was a superfood before anyone used that term: 60% protein, packed with vitamins, growing in conditions where nothing else would. By 1997, EID Parry had built the world's largest spirulina production facility in Tamil Nadu. Today, they export to 41 countries, from Japanese health food stores to American supplement manufacturers. A sugar company had become a pioneer in nutraceuticals.

The Parryware saga was more complex. The sanitary ware division, inherited from colonial times, had once dominated Indian bathrooms. Every middle-class home aspired to Parryware toilets and washbasins. But by the 1990s, the business was bleeding. Competition from cheaper Chinese imports, changing consumer preferences, and massive capital requirements for modernization made it a millstone. In 2008, EID Parry formed a joint venture with Roca, the Spanish sanitaryware giant. By 2012, they had exited completely, selling their stake for ₹185 crores. The lesson: knowing when to quit is as important as knowing when to double down.

The Parry Confectionery sale to Lotte in 2004 was even more painful. The confectionery business, built over decades, included iconic brands like Parry's Coffee Bite and Lacto King. But competing with global giants like Cadbury and Nestle required marketing spending that EID Parry couldn't justify. Lotte paid ₹240 crores—good money, but the emotional cost was higher. Employees who had spent careers building these brands watched them disappear into a Korean conglomerate.

Yet while EID Parry was exiting consumer businesses, it was doubling down on industrial agriculture. The Coromandel International story is instructive. Originally Coromandel Fertilizers, acquired in stages through the 1990s, it was transformed from a sick public sector unit into India's second-largest phosphatic fertilizer company. The synergies were obvious: Coromandel provided fertilizers that EID Parry's contracted farmers needed, creating a captive market. By 2010, Coromandel contributed more to group profits than sugar itself.

The bio-pesticides venture revealed another dimension of EID Parry's strategy. Neem-based pesticides weren't just environmentally friendly—they were strategically brilliant. As Western markets demanded pesticide-free sugar, having an integrated organic solution became a competitive advantage. EID Parry could guarantee customers that their sugar was produced using only biological pest control. In commodity markets where differentiation is nearly impossible, this mattered.

The 2009 commissioning of a fully automated distillery in Sivaganga with zero emission and zero effluent wasn't just about environmental compliance—it was about seeing around corners. The Murugappas had realized that ethanol would become central to India's energy security strategy. While competitors saw distilleries as ways to monetize molasses, EID Parry saw them as future energy companies. The Sivaganga plant could switch between producing industrial alcohol, ethanol for fuel blending, and extra neutral alcohol for liquor—depending on which paid more.

The pattern that emerges from this diversification decade is clear: exit B2C, enter B2B; exit commodities without control, enter value-added products with moats; exit businesses requiring marketing genius, enter businesses rewarding operational excellence. It wasn't always pretty—the Parryware exit left thousands unemployed, the confectionery sale killed beloved brands—but it was strategically coherent.

VI. The Sugar Wars: Market Dynamics & Competition (2000–2020)

To understand EID Parry's journey through the 2000s and 2010s, you need to understand the bizarre economics of Indian sugar. It's an industry where the government sets the price of inputs (sugarcane), controls the price of outputs (sugar), mandates how much you must sell to it (levy sugar), decides how much you can export, and occasionally bans exports altogether. It's capitalism with socialist characteristics, and navigating it requires political skill as much as business acumen.

The competition landscape was equally complex. On one side stood the cooperatives, particularly in Maharashtra and Uttar Pradesh, with deep political connections and access to cheap credit. These weren't really businesses—they were political vehicles that happened to make sugar. On the other side were private players like Bajaj Hindusthan (India's largest), Balrampur Chini, Shree Renuka, and EID Parry. Each had different strategies: Bajaj went for scale, Balrampur for efficiency, Shree Renuka for global integration. EID Parry chose differentiation through integration.

The 2012 acquisition of GMR Group's sugar plants in Karnataka and Andhra Pradesh was a masterclass in opportunistic expansion. GMR, the infrastructure giant, had entered sugar during the 2006-2008 boom when sugar prices hit historic highs. By 2011, prices had collapsed, GMR was overextended in airports and power, and the sugar plants were bleeding cash. EID Parry paid roughly ₹450 crores for assets that had cost GMR over ₹1,000 crores to build. More importantly, the acquisition took EID Parry's crushing capacity to 40,800 TCD, making it India's second-largest private sugar producer.

But scale meant nothing without efficiency. The sugar industry is cyclical—viciously so. In good years, when production falls short of consumption, prices soar and mills mint money. In bad years, when bumper crops create gluts, prices crash below production costs. Most companies simply ride these cycles, making hay when the sun shines and bleeding when it doesn't. EID Parry decided to break the cycle—or at least dampen it.

The strategy was three-pronged. First, maximize recovery. If you're getting 11.5% sugar from cane when competitors get 9.5%, you're effectively getting 20% more revenue from the same input. Second, integrate power generation. Every sugar mill generates bagasse (cane waste); bagasse can generate power; power can be sold to the grid. EID Parry's 140 MW of co-generation capacity meant that even when sugar prices crashed, electricity revenues provided cushion. Third, and most importantly, build a brand in a commodity.

"Parrys Pure" becoming India's only sugar brand with 'Super Brand' status sounds like marketing fluff, but it represents something profound. In a market where sugar is sugar is sugar, EID Parry convinced consumers to pay a premium for their product. How? By guaranteeing purity (no sulfur), consistency (uniform crystal size), and traceability (you could track your sugar back to the farm). In retail markets, Parrys Pure commanded a 5-10% premium. In industrial markets—soft drinks, confectionery, pharmaceuticals—where consistency matters, the premium was even higher.

The farmer engagement program, now covering over one lakh farmers, became EID Parry's real moat. While competitors struggled with cane availability during droughts, EID Parry's farmers, using drip irrigation and drought-resistant varieties developed by the company, maintained supply. The company's field officers became trusted advisors, helping farmers with everything from loan applications to children's education. This wasn't captured in any financial statement, but it was worth billions.

The government's schizophrenic sugar policies created opportunities for those agile enough to exploit them. When the government mandated 5% ethanol blending in petrol in 2003, EID Parry was ready with distillery capacity. When blending was increased to 10% in 2011, they had already expanded. When the government allowed mills to convert B-heavy molasses to ethanol in 2018, EID Parry's plants could switch within weeks. Each policy change that bankrupted inflexible players enriched the adaptable ones.

VII. The Modern Era: Ethanol, ESG & Future Bets (2020–Present)

The 2020s began with a convergence of forces that would reshape EID Parry fundamentally. The government's announcement of a 20% ethanol blending mandate by 2025 wasn't just another policy tweak—it was a paradigm shift. Suddenly, sugar mills weren't food processors; they were energy companies. A mill that could produce 100,000 tons of sugar worth ₹3,500 crores could instead produce ethanol worth ₹4,000 crores. The math was simple, the implications profound.

EID Parry's response was swift and decisive. The company's distillery capacity of 582 KLPD (kiloliters per day) positioned it among India's top five ethanol producers. But capacity was just the beginning. The real innovation was flexibility—plants that could switch between sugar and ethanol production based on price signals. When sugar prices are high, make sugar. When ethanol prices are better, make ethanol. When both are low, make specialty chemicals from molasses. It's optionality as strategy.

The financial performance tells only part of the story. Yes, market capitalization reached ₹20,776 crores. Yes, revenues hit ₹33,586 crores with profits of ₹2,011 crores. But the more interesting metrics are hidden in the details. The company's farmer network now extends to over 100,000 farmers across three states. The R&D division has developed 15 high-yield cane varieties now planted across 40% of the company's catchment area. The nutraceuticals division, anchored by spirulina, generates 18% of profits while using less than 5% of capital.

The ESG transformation goes beyond compliance. The zero-emission plants aren't just good for the environment—they're good for business. European customers buying spirulina pay premiums for products with carbon-negative footprints. The farmer training programs on scientific methodologies aren't charity—they're supply chain investments that improve cane quality and yield. The water conservation initiatives that save 2 billion liters annually aren't just about sustainability—they're about ensuring operations can continue during increasingly frequent droughts.

Yet challenges lurk beneath the surface. The 12.8% ROE over three years is concerning in an era when the cost of capital exceeds 12%. The dividend payout of 8.56% suggests either capital allocation discipline or growth constraints—interpretation depends on your perspective. The stock's 48.28% rise over the past year has taken valuations to levels that assume perfect execution of the ethanol opportunity. The recent Q2 2024 results tell a more nuanced story. Sugar segment profits declined due to lower cane volumes (5.61 lakh MT vs 8.54 lakh MT in Q2 2023), reduced recovery rates, and higher distillery input costs. Yet distillery revenues surged 48% to ₹281 crores, driven by the new 120 KLPD Haliyal and 45 KLPD Nellikuppam capacity running at full utilization. This dichotomy—struggling sugar, soaring ethanol—captures EID Parry's transformation in real-time.

The most intriguing development is the Consumer Products Group's resurrection. CPG turnover reached ₹236 crores, up 76% year-over-year, driven by branded staples. The branded sweetener range grew 21%. After years of exiting consumer businesses, EID Parry is tiptoeing back, but with a twist—leveraging their agricultural supply chain to sell branded commodities, not manufactured products.

The future bets are becoming clearer. Ethanol isn't just about blending mandates—it's about energy independence. Nutraceuticals isn't just about spirulina—it's about protein security for a vegetarian nation. The farmer engagement isn't just about CSR—it's about climate resilience. Each bet addresses a national priority, ensuring government support regardless of which party rules.

VIII. Playbook: Lessons from 236 Years of Survival

If you had to distill EID Parry's 236-year journey into actionable lessons, what would they be? The playbook that emerges isn't about sugar or even agriculture—it's about institutional longevity in volatile environments.

Lesson 1: Regime changes are features, not bugs. EID Parry survived the transition from East India Company to Crown rule, from British Raj to independent India, from socialism to liberalization. Each transition that killed competitors created opportunities for the adaptable. The key wasn't predicting change but building organizational flexibility to exploit it. When the government mandated ethanol blending, EID Parry already had distilleries. When ESG became mandatory, they already had zero-emission plants. Luck? No—preparedness meeting opportunity.

Lesson 2: In commodities, the supply chain is the moat. Sugar is sugar. Anyone can build a mill. But can you guarantee cane supply during droughts? Can you ensure quality when farmers use random pesticides? Can you maintain relationships through price cycles? EID Parry's network of 100,000 farmers, built over decades, isn't replicable by capital alone. It requires trust, earned season by season, crisis by crisis.

Lesson 3: Diversification must follow logic, not fashion. EID Parry's failed ventures—sanitaryware, confectionery—had no synergy with their core. Their successful ones—fertilizers, ethanol, nutraceuticals—leveraged existing capabilities. The difference between conglomerate bloat and strategic expansion is whether new businesses strengthen or distract from the core.

Lesson 4: R&D in traditional industries is arbitrage. Most sugar companies view R&D as cost. EID Parry, India's first private sector R&D company, views it as investment. Developing cane varieties that yield 20% more sugar provides returns no financial engineering can match. In industries where everyone uses similar technology, marginal improvements compound into insurmountable advantages.

Lesson 5: Government intervention creates opportunity for the prepared. While competitors complained about sugar price controls, EID Parry built ethanol capacity. While others fought fertilizer subsidy policies, EID Parry through Coromandel became a beneficiary. The lesson: in regulated industries, policy isn't constraint—it's the playing field. Master the rules, and you master the game.

Lesson 6: Capital allocation in cyclical businesses requires courage and discipline. EID Parry's pattern—aggressive expansion during downturns, conservative financing during booms—seems obvious in hindsight. In practice, it requires resisting both euphoria and despair. The GMR acquisition in 2012, when sugar was in crisis, exemplifies this. They paid 45% of replacement cost for modern assets. That's not luck—that's discipline.

Lesson 7: Brand building in commodities is possible but different. Parrys Pure doesn't compete on advertising like consumer brands. It competes on consistency, traceability, and trust. In B2B markets, brand means reliability. In B2C commodity markets, brand means safety. EID Parry understood this distinction and built accordingly.

Lesson 8: Family ownership provides patient capital but requires professional management. The Murugappa Group's stewardship since 1981 provided stability that public markets couldn't. But they also professionalized operations, bringing in outside talent and modern management practices. The balance—family ownership, professional management—might be the optimal structure for long-term value creation.

IX. Bear vs. Bull Case: Investment Analysis

The Bear Case: Why EID Parry Might Disappoint

The numbers tell an uncomfortable truth: 12.8% ROE over three years in an era when the risk-free rate approaches 7% and equity risk premiums demand another 5-6%. This isn't value creation—it's value stagnation. For a company with such storied history and strategic positioning, this mediocrity is damning.

The commodity trap remains real. Sugar prices are controlled, ethanol prices are regulated, fertilizer prices are subsidized. Where exactly is the pricing power? The government giveth (ethanol mandates) and taketh away (export bans, stock limits, monthly release quotas). Operating in India's agricultural sector means accepting the government as your silent partner—one with veto power over your profits.

Climate change poses existential risk that no amount of R&D can fully mitigate. Sugarcane requires massive water inputs precisely where water is becoming scarce. Tamil Nadu and Karnataka face increasing droughts. Maharashtra's sugarcane cultivation is already economically unviable, surviving only through political support. What happens when water becomes too expensive or simply unavailable?

The competitive landscape is treacherous. Cooperatives, particularly in Maharashtra and Uttar Pradesh, operate with soft budget constraints—losses are covered by state governments, loans are regularly waived. Competing against entities that can't go bankrupt is a fool's game. Meanwhile, new-age companies are developing alternative sweeteners, from stevia to synthetic biology solutions. Is EID Parry investing billions in an industry that might not exist in 20 years?

The capital intensity is crushing. Interest costs increased 12.35% quarter-on-quarter, hitting five-quarter highs. Every expansion requires hundreds of crores. Every modernization demands fresh capital. In a business where dividend payouts average just 8.56% of profits, shareholders fund growth but rarely see returns.

The Bull Case: Why EID Parry Could Surprise

But step back and see the forest, not the trees. EID Parry isn't a sugar company—it's an agricultural transformation platform. The ₹20,776 crore market cap values the company at less than 1x sales, despite controlling critical agricultural infrastructure across South India. The replacement cost of their assets—40,800 TCD crushing capacity, 140 MW power plants, 582 KLPD distilleries—exceeds ₹15,000 crores. You're buying productive assets at a discount to construction cost.

The ethanol opportunity is generational. India imports 85% of its crude oil, spending $100+ billion annually. The 20% ethanol blending mandate could reduce this by $15 billion. The government needs companies like EID Parry to succeed. This isn't hope—it's policy imperative. With distillery revenues growing 48% and new capacity coming online, EID Parry is perfectly positioned for this secular shift.

The nutraceuticals business is a hidden gem. Global spirulina markets are growing at 15% CAGR. Plant-based protein markets could reach $50 billion by 2030. EID Parry's position—among the world's largest spirulina producers, exporting to 41 countries—provides exposure to global wellness trends while leveraging Indian cost advantages. This isn't commodity agriculture—it's specialty chemicals with 40%+ gross margins.

The Murugappa backing provides unquantifiable value. The group's ₹778 billion revenue, nine listed companies, and century-long reputation means EID Parry will never face a liquidity crisis. In commodity businesses where survival through cycles matters more than peak performance, this safety net is invaluable. Patient capital allows long-term thinking that public markets rarely tolerate.

The ESG tailwinds are real and monetizable. European customers pay premiums for carbon-neutral sugar. Indian corporations need sustainable supply chains for their net-zero commitments. EID Parry's zero-emission plants and farmer engagement programs aren't greenwashing—they're competitive advantages that translate to pricing power in premium markets.

The Verdict

The investment case for EID Parry hinges on your view of India's agricultural transformation. Bears see a commodity business trapped by government intervention and climate change. Bulls see an infrastructure play on India's food and energy security. Both are right—the question is which matters more over your investment horizon.

For traders and momentum investors, EID Parry offers little. The stock will track sugar cycles, government policy announcements, and monsoon patterns—essentially noise. For long-term investors seeking exposure to India's agricultural modernization, EID Parry provides a rare combination: 236 years of accumulated advantages, strategic positions in growing markets, and the backing to survive inevitable downturns.

X. Power & Conclusion: The Sweet Spot of Indian Agriculture

Stand at Parry's Corner in Chennai today, and you'll see controlled chaos: wholesale traders hawking everything from textiles to electronics, buses disgorging passengers, the High Court looming across the street. The Dare House building, Art Deco facade weathered but dignified, seems an anachronism. Yet this corner, named after a Welsh trader who arrived when America was twelve years old, represents something profound about business longevity.

EID Parry's 236-year journey offers a masterclass in institutional evolution. This isn't the company Thomas Parry founded—that was a trading house. It's not the company that built India's first sugar mill—that was a colonial enterprise. It's not even the company the Murugappas acquired—that was a failing industrial relic. Today's EID Parry is something unprecedented: a colonial foundation supporting an Indian superstructure, addressing 21st-century challenges.

The biggest surprise in researching this story isn't that EID Parry survived—plenty of old companies exist as shadows of themselves. It's that EID Parry thrived through each transformation, emerging stronger from crises that killed comparable firms. The company that started selling "piece goods" to homesick British officers now exports nutraceuticals to health-conscious Americans. That's not just adaptation—that's metamorphosis.

What makes EID Parry special in Indian agriculture? Three things stand out:

First, temporal arbitrage. In an industry where most players think season to season, EID Parry thinks in decades. Their R&D investments, farmer relationships, and infrastructure builds make no sense on quarterly timescales. But compound them over years, and they become unassailable moats.

Second, regulatory symbiosis. Rather than fighting government intervention, EID Parry evolved to benefit from it. Ethanol mandates, fertilizer subsidies, MSP (Minimum Support Price) for sugarcane—each policy that constrains also protects. EID Parry has mastered the art of turning regulatory constraints into competitive advantages.

Third, network effects in physical markets. Every farmer who plants EID Parry's cane varieties becomes locked into their ecosystem—the varieties are optimized for their mills, the agronomy support assumes their processes, the credit ties them financially. This isn't software-style lock-in, but it's equally powerful and harder to disrupt.

Comparing EID Parry to global sugar giants reveals striking differences. Brazil's Cosan became an energy company, buying gas stations and lubricant businesses. Thailand's Mitr Phol expanded across Southeast Asia through acquisitions. European beet sugar producers like Südzucker diversified into frozen foods. EID Parry's strategy—vertical integration within agriculture—seems narrower but might prove more resilient.

The future of sugar is uncertain. Climate change threatens cultivation. Health consciousness reduces consumption. Alternative sweeteners proliferate. Yet EID Parry's evolution suggests these threats are also opportunities. Climate change makes their drought-resistant varieties valuable. Health consciousness drives demand for organic sugar and nutraceuticals. Alternative sweeteners require industrial ethanol for processing. The company has survived bigger disruptions.

For entrepreneurs, EID Parry offers timeless lessons. Building for centuries requires different thinking than building for exits. It means creating institutions, not just companies. It means embedding into economic infrastructure, not just serving markets. It means accepting lower returns in exchange for higher resilience. In an era obsessed with disruption, EID Parry reminds us that duration has value too.

For investors, EID Parry presents a philosophical choice. Do you value the certainty of 236 years of survival over the possibility of 10x returns? Do you see government intervention as bug or feature? Do you believe India's agricultural transformation will accelerate or stagnate? Your answers determine whether EID Parry is value trap or hidden gem.

The ultimate verdict? EID Parry isn't a sugar company that happens to be old. It's a 236-year-old institution that happens to make sugar. The distinction matters. Sugar is the product; agricultural transformation is the business; institutional longevity is the true asset. In India's volatile, government-influenced, climate-threatened agricultural sector, that longevity might be the only sustainable competitive advantage.

As Thomas Parry stepped off that ship in 1788, he couldn't have imagined his trading firm would outlive the British Empire, survive Indian independence, and thrive in the digital age. He couldn't have known that the corner where he built his warehouse would bear his name two centuries hence. But perhaps he understood something fundamental: in business, as in agriculture, the seeds you plant matter less than the soil you cultivate. EID Parry has spent 236 years cultivating that soil. The harvest, it seems, is just beginning.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube