Easy Home Finance Limited: Coding the Mortgage for the Missing Middle

I. Introduction & Episode Roadmap (00:00 - 05:00)

There is a particular kind of Indian borrower that the banking system has spent decades looking straight through. She runs a two-chair tailoring shop in a Tier III town, or drives a contract truck between mandis, or sells vegetables from a cart that turns over real cash every day. Her income is genuine, her creditworthiness is arguably better than many salaried professionals', and she wants nothing more exotic than a ₹10 lakh loan to buy or finish a small house. But she has no Form 16, no three years of tidy tax returns, no salary slip an underwriting algorithm can parse. To a tier-one commercial bank running a standardised, document-first mortgage model, she is not a risk to be priced — she is simply invisible.

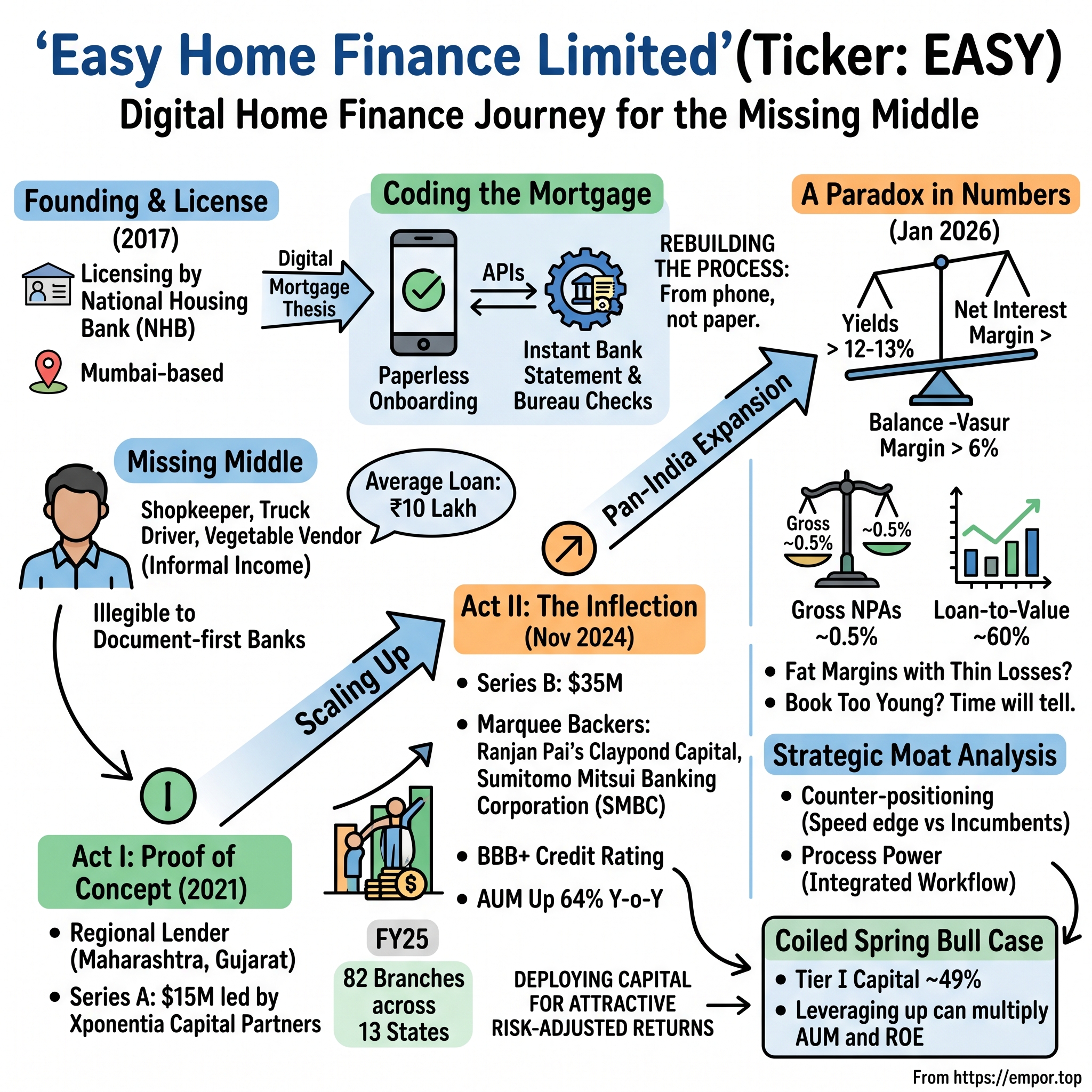

Easy Home Finance Limited (EHFL) was built to see her. Founded in 2017 and licensed as a housing finance company shortly after, the Mumbai-based lender has assembled an unusual coalition of backers around a simple wager: that the "missing middle" of Indian housing credit can be underwritten profitably if you rebuild the mortgage process to run on a phone rather than a stack of paper.12 By the end of FY25 (year ended March 2025), the company reported roughly ₹830 crore of assets under management (AUM), up about 64% year on year, spread across a granular book of small-ticket loans originated through a paperless onboarding process.1 It has drawn equity from Ranjan Pai's Claypond Capital, from Japan's Sumitomo Mitsui Banking Corporation through its Asia Rising Fund, and, most recently, from Bahrain-based Investcorp — a roster of institutional names that most companies of EHFL's tiny size never get near.34

The paradox that makes the company worth an episode is stated in its own numbers. EHFL lends to informal, self-employed borrowers — precisely the segment conventional risk models flag as dangerous — yet it reports a net interest margin above 6% and gross non-performing assets of around half a percent.1 High yield and pristine asset quality are supposed to be a contradiction; earning one usually means surrendering the other. Understanding how an affordable housing finance company squares that circle, and whether EHFL specifically has actually squared it or has merely not yet been tested, is the whole underwriting question.

It is worth naming the risk-reward paradox precisely, because it is the hinge the whole story turns on. A net interest margin above 6% (and 8%-plus in the most recent nine months) is extraordinary for a secured lender — prime mortgage lenders would be delighted with half that — and it is being earned, on the reported evidence, alongside gross NPAs of around half a percent and a conservative ~60% loan-to-value.1 Fat margins are supposed to be compensation for fat risk; earning fat margins with thin losses is either evidence of a genuinely superior model or evidence of a book too young to have shown its true losses yet. Both readings fit the current data, and distinguishing between them is not a matter of opinion but of time — specifically, of watching the 2024–2025 vintages age through their riskiest years and, eventually, through a downturn. A public-market underwriter cannot resolve that today; what it can do is refuse to treat the benign present as proof of a benign future, and hold the margin-quality question open as the single most important thing the coming years will answer.

This is not an investor-relations story, and EHFL has filed no prospectus — there is no DRHP or RHP, and the "Startup" tag denotes its lifecycle stage, not an imminent listing. What follows is an independent reading of the public record: the structure of India's bifurcated mortgage market and the segment EHFL targets; the founder and the family capital behind him; the technology thesis and where it bumps into physical reality; the three funding rounds and the extraordinary capital cushion they left behind; the operating economics of a small, high-margin, under-leveraged lender; a structural read through Porter and Helmer; and the bull and bear cases with the metrics that would confirm or falsify either.

A note on method before the story, because for a lender it matters more than usual. None of EHFL's funding rounds came with a disclosed valuation, so there is no headline "mark" to carry forward, and that is clarifying rather than limiting — it forces the analysis onto the operating evidence where value actually lives. A lender is not valued the way a software company is: enterprise-value multiples are meaningless here, because debt is not a financing choice to be netted out but the company's raw material, the very thing it borrows in order to lend. The right lenses are book value and the return earned on it — price-to-book calibrated to return on equity — plus asset quality, margin durability and the cost and diversity of funding. Where the evidence to compute something an investor would want does not exist, we will say so rather than invent it. And throughout, we will hold apart two questions that a private round's glamour tends to fuse: what someone was willing to pay for a slice of preferred stock, and what the underlying lending business is actually worth.

II. The Affordable Housing Finance Landscape & The "Missing Middle" (05:00 - 20:00)

To understand EHFL you first have to understand the shape of the market it sits inside, because that shape is the entire opportunity and the entire risk. India's residential mortgage market is sharply bifurcated. At the top sit the large commercial banks and prime housing financiers, competing ferociously for salaried professionals buying homes above roughly ₹30 lakh in metros and large cities. These borrowers have documented incomes, clean tax records and credit bureau histories, so they can be underwritten cheaply and at scale by standardised models — and because the risk is legible and the competition fierce, the yields are thin. This is a low-margin, high-volume, commoditised business, and it is not the one EHFL is in.

Below that prime tier lies the segment the industry has come to call the "missing middle": the self-employed and informally-employed households whose incomes are real but undocumented. The annual report frames its customers explicitly as the Low-Income Group (LIG) and Middle-Income Group (MIG) categories defined by National Housing Bank guidelines — shopkeepers, micro-entrepreneurs, small contractors and service providers in Tier II, Tier III and peri-urban locations.1 They are not poor, and they are not bad credits; they are simply illegible to a document-first bank. A vegetable vendor may bring in ₹40,000 a month reliably, but she cannot prove it on paper, and so the mainstream system either declines her or pushes her toward informal moneylenders at usurious rates. The gap between her genuine creditworthiness and her documentary legibility is the arbitrage that the entire affordable housing finance company (AHFC) sector exists to capture.

The sector did not invent itself yesterday. A first generation of specialist AHFCs — Aavas Financiers, Aptus Value Housing, Home First Finance, India Shelter — spent the 2010s proving that this segment could be lent to profitably, and several have since listed publicly and built AUMs in the tens of thousands of crores.567 Their method was not primarily technological; it was human and laborious. Rather than reading tax returns, their loan officers reconstruct a borrower's cash flow by hand — visiting the shop, counting the daily till, interviewing suppliers and neighbours, assessing the property in person. This "feet-on-the-street" underwriting is expensive per loan, which is exactly why it is defensible: it cannot be done from a call centre in another city, and it prices out lenders unwilling to build local presence. The high origination cost is the moat.

The economics that result are genuinely attractive when executed well, and they explain the paradox from the introduction. AHFCs charge yields of roughly 12–13% — far above prime mortgages — because the segment has no cheaper alternative and because serving it costs more. Crucially, though, the loans are secured by the borrower's own home, and in India homeownership carries an emotional weight that translates into unusually disciplined repayment: a borrower will default on almost anything before the roof over the family. That behaviour produces very low loss-given-default and, historically, sector gross NPAs comfortably below 1.5%.8 The result is a business that earns prime-plus yields on collateral-backed loans to borrowers who repay like their home depends on it — because it does. High margin and low losses are not a contradiction in this segment; they are the segment's defining feature. The catch, and it is the one a public-market investor must never forget, is that this pristine performance has largely been earned during a long benign macro stretch for Indian housing, and the model's behaviour through a genuine property or employment downturn in these geographies remains substantially untested for the newer entrants.

There is a powerful policy tailwind behind all of this that a fair account cannot ignore, and that a skeptical one must size correctly. The Indian state has made housing for the lower and middle income a formal priority — the Pradhan Mantri Awas Yojana (PMAY) and its interest-subsidy schemes channel real subsidy toward exactly the borrowers AHFCs serve, and the National Housing Bank provides refinance lines that lower these lenders' cost of funds. This is why the affordable-housing segment has compounded faster than the overall mortgage market: the annual report's own sector data, drawn from CRISIL and CareEdge, shows AHFC AUM growing at a materially higher rate than the broader HFC industry over recent years, propelled by rising formalisation of informal incomes, digitised onboarding and these policy supports.18 The tailwind is genuine and durable. But two cautions apply. First, subsidy-linked demand is also subsidy-dependent demand — a change in PMAY's terms or budget would remove a real prop under origination volumes. Second, a rising tide of this kind lifts every AHFC, which is precisely why the segment is crowded and why sector-wide growth is not, by itself, evidence that any particular lender is winning.

EHFL's positioning within this landscape is orthodox in its target and heterodox in its method. It aims at the same missing-middle borrower that Aavas and Home First proved could be served, with an average loan ticket around ₹10 lakh and a loan-to-value at sanction of about 60% — conservative enough that even a meaningful fall in property prices would leave the loan well-covered.1 What it proposes to change is not who gets the loan but how the loan gets made: to replace as much of the expensive paper-and-footwork process as possible with software, and to keep only the parts — valuation, collection — that genuinely require a human in the town. Whether that substitution actually lowers cost, or merely relocates it, is the question Section V returns to.

It is worth being precise about market size before going further, because a category this large invites lazy extrapolation. The sector EHFL competes in is enormous — India's mortgage-penetration-to-GDP ratio remains low by the standards of developed and even many emerging economies, and the affordable-housing sub-segment alone runs into the trillions of rupees. But the reachable market for a lender of EHFL's size is not that whole category, and conflating the two is the single most common error in bull cases for small lenders. EHFL can only lend where it has branches, valuers and collectors physically present, because in this business the underwriting and the recovery are irreducibly local — you cannot inspect a house or repossess it from a server. Its reachable market today is therefore the specific towns across its 13-state footprint where it has planted that infrastructure, a tiny fraction of the category. The broad total addressable market is a real tailwind; the reachable market is a function of how fast, how cheaply and how well EHFL can lay down local physical presence, and every rupee of that expansion carries the opex that Section V shows is the company's central problem. Market share, in other words, is not there for the taking — it must be built branch by branch against incumbents who are building too.

III. The Founding and Promoter Legacy: Capital Meets Technology (20:00 - 35:00)

Every lending startup is, at its origin, a bet that a particular founder can hold two contradictory disciplines in one head: the growth instinct that raises capital and opens branches, and the credit conservatism that says no to most of the loans that growth instinct wants to make. EHFL was founded in 2017 by Rohit Chokhani, an entrepreneur whose background sits closer to real estate and capital markets than to retail credit — with education spanning economics at the London School of Economics and construction management at the University of Reading, and a prior career as an investor and advisor.12 That pedigree is double-edged, and worth naming honestly. Real-estate and capital-markets fluency is genuinely useful for a mortgage lender — it helps in understanding collateral, structuring funding and courting institutional money. But it is not the same thing as a decade spent inside the collections and underwriting engine of a retail lender, which is where affordable-housing credit is actually won or lost. The relevant diligence question is whether EHFL has built deep credit-and-collections leadership beneath the founder, and that is exactly the kind of organisational detail a future prospectus would need to make legible.

The regulatory dimension of that founding is more important than it first appears, and it is a genuine barrier that protects EHFL as much as it once constrained it. A housing finance company in India is not a thing one simply decides to become: it requires a licence from the National Housing Bank, minimum net-owned-funds, fit-and-proper promoter vetting, and ongoing compliance with capital-adequacy, provisioning and asset-classification norms overseen by the NHB under the RBI's regulatory umbrella. EHFL secured that licence in its early years, and the licence is itself an asset — it is the reason the "software-only" fintechs that covet secured lending cannot simply flip a switch and compete, and it is why a diligent reader should treat the regulatory relationship as core infrastructure rather than back-office overhead.1 The annual report's account of clean regulatory standing — no penalties levied by the RBI or NHB during the year under review, compliance with capital and principal-business-criteria requirements — is, as far as a single year's disclosure goes, a positive signal about the company's compliance culture, though it is a point-in-time attestation and not a permanent guarantee.1

What the founder did bring was access to capital and credibility, and here the promoter backing matters. EHFL's early equity and standing drew on the Chokhani and Halwasiya family networks — established groups with long histories in corporate finance, real estate and infrastructure.1 For a housing finance company, which must satisfy a regulator (the National Housing Bank, under the RBI's umbrella) before it can take a single deposit or draw a single refinance line, day-one credibility with regulators and lenders is not a soft asset; it is the difference between getting a licence and funding lines or not. Family capital and reputation gave EHFL a running start that a founder without those networks would have spent years assembling. It also, however, raises the standard governance flag for any promoter-backed financial company: related-party exposures, the independence of the board relative to the founding families, and any transactions between the lender and promoter-affiliated real-estate interests are precisely the items a public-market investor would want mapped in detail before a listing — not because anything is known to be amiss, but because the structure is one where such conflicts can arise, and their absence has to be demonstrated rather than assumed.

The strategic thesis that distinguishes EHFL from the first-generation AHFCs is the digital-first build. Where Aavas and Home First scaled primarily by adding loan officers and branches, Chokhani's wager was to construct a native digital mortgage platform first and hang the physical network off it. The company's proprietary "EASY" software suite is pitched as covering the whole loan lifecycle: customer sourcing and sales onboarding, instant bank-statement verification through APIs, digital property and technical evaluation, and collections — all delivered through what the company describes as a 100% paperless process.1 The intended payoff is twofold: faster turnaround time, which is a real competitive weapon in a market where a borrower who needs money quickly will take the first lender who says yes; and, in theory, lower cost per loan as the software absorbs work that rivals pay humans to do.

It helps to be concrete about what the software actually replaces, because the parts of a mortgage that digitise well and the parts that do not are the whole story. The front end — sourcing a lead, capturing a customer's details, pulling and parsing bank statements through account-aggregator APIs, running bureau checks, generating a sanction letter — is genuinely amenable to automation, and this is where EHFL's turnaround-time advantage lives. A borrower who would wait days or weeks for a traditional lender's paperwork can be sanctioned far faster, and in a segment where a shopkeeper often needs money on a specific timeline, speed converts. That is a real, defensible product advantage, and it is the strongest thing the "tech-first" claim has going for it.

The honest framing, though, is that the technology is a credible operational advantage and an unproven cost advantage. The back end of the mortgage runs into a hard physical floor that no amount of software removes: someone still has to physically value the property before the loan is made, and someone still has to knock on the door when a borrower stops paying. Those two functions — valuation and collection — are irreducibly local and human, and they are also where the cost and, crucially, the credit risk concentrate. Automating the application while still staffing a branch network for valuation and recovery can shorten the sales cycle without necessarily lowering the total cost per loan, because the expensive half of the process is the half that resists automation. The company's own cost structure, examined next, is the clearest test of whether the digital thesis has actually bent the cost curve or has merely digitised the easy front end while the back end stays stubbornly manual. It is a claim to be judged by the opex ratio over time, not by the branding — and one further caution belongs here: lending against informally-documented income, where alternative data substitutes for tax returns, also raises the ceiling on fraud and misrepresentation risk, which is exactly the kind of exposure that a fast, digital front end can amplify if the human verification behind it is thin. That, too, is something only a seasoned book will reveal.

IV. The Capital Blitz and Institutional Backing (35:00 - 01:05:00)

EHFL's capital history is a three-act escalation, and the striking thing is how the quality of its backers improved faster than the size of its balance sheet. The first act was a $15 million Series A in July 2021, led by the Indian private-equity firm Xponentia Capital Partners, with participation from Harbourfront Capital, Finsight Ventures and a cluster of smaller investors.2 At that point the company was a regional lender operating mainly in Maharashtra and Gujarat, and the round's job was to fund the technology build and prove the concept could travel beyond its home geography.

The second act was the inflection. In November 2024 EHFL raised $35 million in a Series B led by Claypond Capital — the family office of Ranjan Pai, chairman of the Manipal group — and the Asia Rising Fund of Sumitomo Mitsui Banking Corporation, one of Japan's largest banks, with existing backers including Xponentia, Finsight, Harbourfront and Pegasus following on.3 It is worth pausing on why a global banking group and a marquee Indian family office would write cheques into a company with under ₹1,000 crore of AUM. Part of the answer is strategic rather than purely financial: for SMBC, a small equity position in an Indian affordable-housing lender is a cheap, informative option on a market it wants exposure to, and a strategic investor's motives — market access, learning, optionality — are not the same as a pure financial investor's, which means the price it will pay is not a clean read on standalone value. The Series B roughly doubled EHFL's net worth, which jumped from about ₹175 crore at the end of FY24 to about ₹384 crore at the end of FY25 as the fresh equity landed within the fiscal year.1 That single fact — a balance sheet whose equity more than doubled in twelve months — is the origin of both the company's greatest strength and its most awkward near-term problem, as we will see.

The third act, in late January 2026, was a $30 million Series C led by Investcorp's Growth Equity and Growth Opportunity funds, with existing investors participating, which the company said took its cumulative equity raised past $80 million.4 By this point EHFL had expanded to a materially larger operating footprint — reported at 82 branches across 13 states, with AUM of about ₹920 crore as of mid-2025 and climbing toward the ₹1,000 crore threshold.9 Managing director Rohit Chokhani framed the proceeds as funding pan-India expansion, faster distribution, and deeper investment in product and talent.4

Two features of this progression deserve a closer look before drawing conclusions from it. The first is that the equity is only half of a lender's capital story: EHFL has separately raised debt — reporting, around the time of the Series B, cumulative equity-plus-debt financing exceeding $100 million — because a housing finance company funds its loan book primarily by borrowing, not by equity.3 The equity is the loss-absorbing cushion that lets it borrow safely; the debt is the fuel. That distinction matters for how one reads the "over $80 million raised" headline: it is the cushion, not the lending capacity, and the lending capacity is a multiple of it. The second feature is the cadence of dilution. Three primary rounds in under five years means the founder and early holders have been diluted repeatedly, and each new preferred investor has taken a slice of the company at terms that are not public. Without the cap table, one cannot say how much of EHFL the founding families still control, how much sits with Xponentia, Claypond, SMBC and Investcorp, or what an employee option pool looks like — all of which are first-order questions for a public-market investor and all of which remain, for now, undisclosed.

Now the capital-structure analysis, and here the discipline of separating price from value does most of its work. Not one of these three rounds carried a publicly disclosed valuation. That means any "implied market capitalisation" for EHFL is genuinely unknown — it cannot be reverse-engineered from public data, and no reader should accept a figure that claims otherwise. What can be said is grounded and useful: across three rounds the company raised roughly $80 million of primary equity, and it ended FY25 with about ₹384 crore of net worth against roughly 5.2 crore shares outstanding, implying a book value of very approximately ₹74 per share before the Series C further changed the count.1 Those are the anchors a lender is actually valued from. The rounds were primary — fresh capital into the company to fund the loan book — rather than secondary sales in which founders cash out, which is the healthier signal, because the money went to build the business rather than to enrich early holders. But the terms attached to that preferred stock are entirely undisclosed: liquidation preferences, any participation or anti-dilution rights, board seats and information rights held by Claypond, SMBC and Investcorp are not public, and every one of them would sit ahead of the common stock a future IPO would sell. A public common share and a Series C preferred share are not the same instrument, and treating the private rounds as if they priced the common equity would be a category error. The fully diluted share count — including any employee option pool and the conversion terms of the preferred — is likewise not public, so even a book-value-per-share figure is an approximation pending a real filing.

The rounds also give a way to judge management against its own stated targets, which is more informative than any pitch. At the Series B in November 2024, the company said it intended to grow AUM to roughly $300 million — on the order of ₹2,500 crore — within 24 months and to build presence across about 150 locations.3 That is a concrete, dated, falsifiable promise, and it is exactly the kind of commitment a public-market investor should file and later check. As of mid-2025, roughly seven months in, AUM stood near ₹920 crore against a ₹504.75 crore FY24 base — real progress, but implying a very steep remaining climb to hit ₹2,500 crore by late 2026.19 Whether EHFL lands that target, misses it modestly, or falls well short will be an early and honest read on management's forecasting discipline and execution — and, just as importantly, on whether it can grow that fast without letting credit quality slip, which is the temptation every AUM target creates. Growth promises in lending are cheap; growth promises kept at constant asset quality are the ones that matter.

The most consequential fact in this section is not the money raised but the money not yet deployed. The Series B and C left EHFL almost comically over-capitalised for its size: a capital adequacy ratio of about 85% at the end of FY25 against a regulatory minimum of 15%, and a reported Tier I ratio near 49% and debt-to-tangible-equity of only about 1.8x in the first nine months of FY26.19 For a lender, that is extreme under-leverage. A housing finance company is a machine for turning equity into a multiple of loans by borrowing against it; a well-run, seasoned AHFC typically runs leverage of 4–6x. EHFL is running under 2x, which means it is sitting on a mountain of equity earning very little. This is the direct cause of the company's depressed return on equity — about 3.75% in FY25 — and it reframes the entire investment question.1 The under-leverage is simultaneously a coiled spring and an indictment: a spring, because the room to lever up means AUM and ROE can rise sharply without raising another rupee of equity; an indictment, because it also means the company has raised far more capital than it has yet demonstrated it can profitably deploy, and the burden is now squarely on management to prove it can grow the book fast enough, and cleanly enough, to earn a real return on all that equity. Raising capital is a skill EHFL has clearly demonstrated; deploying it at attractive risk-adjusted returns is the skill still on trial.

V. The Operational Mechanics & The Economics of a Tech HFC (01:05:00 - 01:25:00)

Start with the growth curve, because it is genuinely impressive and genuinely small at the same time. EHFL's AUM rose from about ₹255 crore in FY23 to ₹504.75 crore in FY24 and ₹830.09 crore in FY25 — a 64% jump in the most recent year — before reaching roughly ₹920 crore by mid-2025.19 Disbursements crossed ₹425 crore in FY25, up about 29% year on year.1 Those growth rates are high, but the absolute base is tiny: this is a lender with total income of about ₹105 crore and a book that would be a rounding error on Aavas's or Home First's balance sheet.1 The correct way to hold this is that EHFL has proven it can grow quickly from a small base in a benign environment; it has not yet proven it can grow to scale, and the two are very different tests.

Before the margin, a word on revenue quality, because it is one of the genuinely attractive features of a lending business and is easy to take for granted. EHFL's income is overwhelmingly recurring interest on a secured, amortising loan book: a mortgage disbursed today produces contractual interest income every month for years, and because these are home loans the contractual tenors run long. That is a far higher-quality revenue base than the transactional, campaign-driven income of many consumer-internet startups — it does not have to be re-won each quarter, it is contracted, and it is secured by collateral. The reported figures bear this out: revenue from operations rose from about ₹63.7 crore in FY24 to ₹92.8 crore in FY25, tracking the AUM growth, with total income near ₹105 crore.1 The durability question for this kind of revenue is not churn in the software sense but prepayment and balance-transfer attrition — how many borrowers refinance away once seasoned — and credit losses, both of which are addressed below.

The margin story is the heart of the bull case, and the numbers are real. EHFL reported a net interest margin of about 6.57% in FY25 (up from 6.18% in FY24), widening to a striking 8.17% in the first nine months of FY26 as its cost of borrowing fell toward 10.23%.19 That NIM expansion has a clear and creditable mechanism behind it: as the company scaled and its credit rating improved — the annual report reflects an India Ratings profile at BBB+ — it gained access to cheaper and more diversified funding, and the gap between what it earns on loans (12–13% yields) and what it pays for money widened.1 It is worth understanding why the rating is the fulcrum here. A lender's cost of funds is set largely by its credit rating, and ratings improve with scale, track record and capital strength; EHFL's enormous capital cushion and clean asset quality are exactly what pull a rating up, which lowers borrowing cost, which widens NIM — a virtuous loop that is real but also self-limiting, because the biggest gains come early and the path from BBB+ to the A-band and beyond is slow and earned over years.

The funding diversification is worth crediting specifically, because concentrated funding is what kills small lenders in a crisis — the Indian NBFC sector's 2018–2019 liquidity squeeze, triggered by the IL&FS default, wiped out or crippled several lenders whose funding was too concentrated and too short-dated against long-dated loans. EHFL reports borrowing relationships spanning the National Housing Bank's refinance lines, commercial banks and various NBFCs/HFCs, and it operates co-lending arrangements with partners including ICICI, DCB Bank and Bajaj Housing Finance.1 Co-lending — where a larger, cheaper-funded institution puts up the bulk of a loan alongside EHFL's smaller share — is doubly useful: it lowers the blended cost of funds, and it moves part of the book off EHFL's own balance sheet, generating fee income and stretching the equity further. This diversified, partly NHB-backed funding base is one of the more mature aspects of EHFL's operation and a genuine mitigant to the classic small-lender fragility. It does not, however, eliminate asset-liability management risk — the structural danger of funding long-dated fixed-rate mortgages with shorter-dated or floating-rate borrowings — which is an inherent exposure of the model and another item a full filing would need to lay out.

The asset quality is, on the reported evidence, excellent. Gross NPAs stood at about 0.50% of AUM in FY25 — a gross NPA figure of roughly ₹4.16 crore against the ₹830 crore book — and around 0.62% in early FY26, comfortably inside the sector's historically clean range and consistent with the conservative ~60% loan-to-value at origination.19 The bull reading is that EHFL's data-led underwriting is genuinely selecting good borrowers. The necessary skeptical caveat is that a book growing at 30–60% a year is, by construction, dominated by young loans that have not had time to go bad — a portfolio this unseasoned will almost always flatter its NPA ratio, because the denominator is swollen with fresh disbursements and the numerator has not caught up. Low NPAs on a rapidly growing, young, never-recession-tested book are encouraging but are emphatically not proof that the credit model works through a cycle. That proof takes years and at least one downturn to earn, and EHFL has had neither.

Now the problem the tech thesis was supposed to solve, and largely has not — yet. Despite the "tech-first" branding, EHFL's operating expenses run at roughly 9% of average assets, and its cost-to-income ratio was about 46.7% in FY25.1 That opex ratio is high — the very thing a software-driven model was meant to compress — and it is the single biggest drag on the company's returns. The explanation is the physical floor described earlier: with 65 branches at the end of FY25 (and 82 by mid-2025), a real estate of loan officers, valuers and collectors, EHFL carries the cost base of a "phygital" lender, not a pure software platform.19 There is a benign reading and a bearish one, and both are alive. The benign reading is that opex-to-assets is high because the book is young and each new branch runs below capacity — as branches season and AUM per branch rises, the fixed cost spreads over more loans and the ratio should fall. The bearish reading is that the ratio is structural, that valuation and collection simply cost what they cost in this segment, and that the "tech" saving was always going to be marginal. The FY19–FY25 trend is encouraging on this point — opex-to-assets has fallen steeply from over 24% in FY20 as the company scaled — but it has plateaued near 9%, and whether it breaks meaningfully lower is the crux operational question.1

There is also a concentration question hiding inside the growth, and the state-level data makes it concrete. Of the ₹830 crore FY25 book, Maharashtra alone accounted for about ₹355 crore — over 40% — with Gujarat, Rajasthan and Madhya Pradesh adding most of the rest, so that four western and central states carry the overwhelming majority of the portfolio.1 The newer states — Delhi, Uttar Pradesh, Karnataka, Telangana, Andhra Pradesh — are real but small, together a modest slice of AUM. This matters two ways. On the upside, geographic density is efficient: clustering branches lets valuers and collectors cover more ground per rupee of cost, and deep local knowledge sharpens underwriting. On the downside, a book this concentrated is exposed to a regional shock — a property-price correction, a local economic downturn, a state-specific regulatory or political event affecting western India — that would strike a disproportionate share of the loans at once. Diversification across 13 states reads well in a pitch, but the economic reality is a western-India book with a national veneer, and the veneer will only become substance if the newer geographies scale into meaningful weight.

Put the pieces together and the profitability arithmetic becomes clear, and clarifying. EHFL earned a profit after tax of about ₹7.02 crore in FY25 (up from ₹5.23 crore in FY24), for a return on assets of roughly 1.22% and that depressed ROE of about 3.75%.1 The low ROE is not primarily an operating failure — a 6.5%+ NIM and sub-1% NPAs are good operating outcomes — it is an arithmetic consequence of running under 2x leverage on a huge equity base while carrying a 9% opex load. The path to durable, attractive profitability therefore runs through two specific, measurable improvements: lever the balance sheet up from ~1.8x toward the 4–5x that a seasoned AHFC sustains, which mechanically multiplies the assets each rupee of equity supports; and drive the opex ratio down as AUM per branch matures and the fixed costs of the network amortise across a larger book. If both happen, ROE could plausibly climb toward the mid-teens without any change in the fundamental margin or credit profile. If neither happens fast enough, EHFL remains what it is today — a well-capitalised, high-margin, low-return curiosity. Nothing about the model guarantees which outcome arrives, and the reader should notice that the entire bull thesis is a bet on financial engineering (leverage) plus operating maturity (opex), not on any change to the underlying loan.

The co-lending and off-book strategy deserves a closer look here, because it is the one lever that could improve returns without simply taking on more balance-sheet leverage. In a co-lending or direct-assignment arrangement, EHFL originates and services the loan but holds only a fraction of it on its own books, with a bank partner holding the rest; EHFL earns a spread on its share plus a servicing fee on the whole, while consuming far less of its own capital per rupee of loan originated. If EHFL can push a meaningful portion of its AUM — the sector norm for such strategies runs toward a quarter or a third of the book — off-balance-sheet this way, it earns fee income on originations its equity could not otherwise support, lifting return on equity through capital efficiency rather than leverage. The catch is that off-book economics are thinner per rupee than on-book lending (you keep the fee, not the full spread), and the strategy makes EHFL more dependent on the willingness of partners like ICICI to keep buying its loans — a willingness that can evaporate exactly when it is most needed, in a stressed market. Co-lending is a genuine capital-efficiency tool and a real part of the maturation path; it is not a free lunch, and its contribution should be judged by realised fee income, not by the aspiration.

VI. Playbook: Technology vs. "Feet-on-the-Street" (01:25:00 - 01:40:00)

Hamilton Helmer's 7 Powers framework asks which specific, durable advantage lets a business hold returns above its cost of capital against competent rivals. Applied honestly to EHFL, most of the powers are early-stage or weak, and one or two are plausible — which is exactly what one should expect of a sub-₹1,000-crore lender.

Scale economies are the power EHFL most needs and least has today. Lending is a scale business — fixed costs of technology, compliance and branch overhead spread across a larger book lower the cost per loan, and larger balance sheets earn better credit ratings and cheaper funding. EHFL's NIM expansion as it scaled is scale economics beginning to work, but at its current size the power is nascent, not established. Network effects are essentially absent, as they are in almost all lending: one more borrower does not make the product better for the next. Counter-positioning is the company's most genuine claim — the digital, fast-turnaround model is a real repositioning against slow, paper-based incumbents, and incumbents cannot trivially copy it without disrupting their existing processes. But counter-positioning is only durable if the incumbent genuinely cannot or will not respond, and here the larger AHFCs are themselves digitising quickly, which erodes the edge over time rather than entrenching it.

Switching costs are low, and this is a real vulnerability worth stating plainly: once a mortgage is disbursed, a borrower can refinance to a cheaper lender through a balance transfer, and in a segment where every basis point matters to a stretched household, a larger rival with cheaper funding can poach EHFL's best-seasoned, lowest-risk customers precisely when they have proven their creditworthiness. This is the cruel dynamic of high-yield lending: your best borrowers are the ones most able to leave, because they are the ones a cheaper lender most wants to take, and the moment they season into obvious quality is the moment they become a balance-transfer target. The friction and cost of refinancing provide some stickiness, but not a moat. Brand is growing but immature — "the paperless mortgage" is a positioning, not yet a household name with pricing power, and in affordable housing the brand that ultimately matters is trust built through a local presence and word of mouth, which EHFL is still accumulating town by town.

The two powers with the most promise are cornered resource and process power. If EHFL's proprietary underwriting models and alternative-data credit algorithms prove genuinely predictive through a full cycle — if they can price the informal borrower's risk better than a rival's — that would be a cornered resource of real value, because credit models that actually work are rare and hard to copy. But note the tense: that is a hypothesis awaiting a downturn to confirm, not an established fact, and a model that looks brilliant on a book originated entirely in good times has proven nothing yet. Process power — the integrated onboarding-valuation-collection workflow refined into an efficient, repeatable system — is more tangible and is where EHFL's tech investment could compound, but it is also replicable by well-funded incumbents digitising in parallel. The honest verdict is that EHFL's moat today is thin and mostly prospective: its defensibility rests on execution and scale it has not yet achieved, not on a structural power it already possesses. That is not a criticism so much as a description of an early-stage lender — moats in this business are earned over a decade of seasoned performance, and EHFL is a few years into that decade.

Step back to the section's animating question — technology versus feet-on-the-street — and the resolution is that the two are not really rivals but layers, and EHFL's bet is best understood as a layering bet rather than a replacement bet. The first-generation AHFCs proved that feet-on-the-street underwriting works; nobody has yet proven that software can replace it in this segment, and EHFL's own 9% opex ratio is the strongest evidence that it has not tried to. What EHFL is actually attempting is subtler and more defensible than the "we digitised the mortgage" headline: to keep the feet-on-the-street where it is indispensable — valuation, collection, relationship — and to strip cost and time out of everything around it. If that works, EHFL ends up with a modest structural cost edge and a real speed edge over an equally-sized traditional AHFC, which at scale compounds into better growth and slightly better margins. If it does not — if the software saves days but not rupees — EHFL is simply a well-funded traditional AHFC with a nicer app, competing on the same terms as everyone else. The honest state of the evidence is that the speed edge is proven and the cost edge is not, and the whole "tech HFC" valuation premium rides on the unproven half.

Porter's Five Forces sharpens the competitive picture. The threat of new entrants is high in spirit but moderated in practice: many fintechs covet secured lending, but the RBI/NHB licensing regime, the capital requirements, and above all the need for a local recovery and valuation network are real barriers that keep the "software-only" entrants out — you cannot collect a defaulted mortgage in a Tier III town over an API. Buyer (borrower) power is moderate: borrowers want the lowest rate, but their lack of documentation limits how many lenders will serve them, which blunts their leverage. Supplier power — here the "suppliers" are EHFL's own lenders — is the classic vulnerability of a small HFC, since it depends entirely on wholesale funding it does not control; EHFL mitigates this meaningfully through its diversified funding base and co-lending relationships, which is one of the more mature aspects of its operation.1 The threat of substitutes is genuinely low — there is no substitute for a mortgage when buying a home. And competitive rivalry is intense and intensifying, from listed AHFC giants like Aavas, Home First, Aptus and India Shelter to Aadhar Housing and the banks themselves as they push down-market. The structural read is that EHFL operates in an attractive segment with real regulatory barriers, but as a small player among well-capitalised, increasingly digital incumbents — its edge has to be earned continuously, not banked.

VII. The Investment-Story Spine: Bull vs. Bear Case & Risk Radar (01:40:00 - 01:55:00)

The bull case is coherent and rests on a specific, quantifiable lever rather than on hope, and it is worth making the arithmetic concrete because the mechanism is unusually clean. Return on equity is, at its simplest, return on assets multiplied by leverage. EHFL's return on assets is a respectable ~1.2%, which is roughly in line with what good AHFCs earn; the reason its ROE is a poor ~3.75% rather than a healthy mid-teens number is almost entirely that it multiplies that ROA by leverage of only ~2x, where a seasoned peer multiplies a similar ROA by 4–5x.1 So even holding ROA flat, moving leverage from ~2x to ~4x would roughly double ROE toward the 6–8% range, and a simultaneous rise in ROA as opex falls with scale would push it further, plausibly into the low-to-mid teens. The elegance of this is that it requires no heroic assumption about the loan itself — no wider margin, no lower loss rate, no new product — only that EHFL borrows against the equity it already holds and grows into it. That is why the under-leverage is genuinely a coiled spring rather than mere weakness. The catch, restated, is that the same act of levering up and growing the book fast is what tends to import credit risk, so the spring only pays off if it is released with underwriting discipline intact.

EHFL is a high-margin lender with pristine reported asset quality that happens to be sitting on an enormous, under-used equity cushion. Its Tier I capital near 49% and leverage below 2x mean it can roughly triple its balance sheet — funding the growth with debt it is already rated to raise — without diluting a single existing shareholder.19 In a lending business, that is the most valuable position to be in: growth capital already in hand. If EHFL moves from ~1.8x toward 3x leverage over the next couple of years while holding its 6.5%+ NIM and sub-1% NPAs, AUM could climb well past ₹2,000 crore and ROE could rise from today's ~3.75% toward the 15–18% that the market rewards in seasoned AHFCs — a re-rating driven purely by putting existing capital to work.1 The co-lending strategy, targeting a meaningful share of AUM held off-book through partners like ICICI, adds fee income and capital efficiency on top. In this reading, EHFL is a coiled spring: the operating model already works, and it simply needs to scale into its own balance sheet.

The bear case is equally grounded, and a skeptical public-market investor should weight it heavily, because every pillar of the bull case is an assumption not yet demonstrated. First, the opex trap: if the tech-first model never actually delivers a lower cost per loan — if 9% opex-to-assets proves structural rather than transitional — then scaling the book scales the cost base alongside it, and the profitability re-rating never arrives.1 Second, the unseasoned portfolio: EHFL's proprietary underwriting has never been tested through a real credit cycle or a property downturn in western India, and a young, fast-growing book's low NPAs are exactly what you would see whether the model is brilliant or merely lucky — the truth only emerges when the loans age into a worse environment. Third, geographic concentration: despite the 13-state footprint, the book remains heavily anchored in Maharashtra (about ₹355 crore of the ₹830 crore FY25 AUM, over 40%) plus Gujarat, Rajasthan and Madhya Pradesh, so a regional shock in western India would hit the portfolio disproportionately.1 Fourth, yield compression: EHFL's fat NIM depends on charging 12–13% to borrowers with no cheaper option, and as larger banks and HFCs with structurally lower funding costs push into the affordable segment, they can undercut EHFL on rate and skim its best customers via balance transfer, squeezing the very margin the bull case relies on.

There is a subtler bear point that sits underneath all four, and it is the one most easily missed: the huge capital cushion that anchors the bull case is also what makes the returns look bad today, and management now faces a genuine tension between two goods. To fix the low ROE quickly, it must lever up and grow the book fast; but growing a lending book fast is precisely how credit mistakes get made, because the loans that are easiest to write in a hurry are the ones most likely to sour. The company is therefore being asked, in effect, to press the accelerator and the brake at once — to deploy its capital aggressively enough to earn a return on it while underwriting conservatively enough to keep the 0.5% NPA intact through a book that triples. Those two imperatives pull against each other, and the history of Indian NBFC lending is littered with companies that resolved the tension in favour of growth and paid for it two years later. Watching how EHFL grows — whether NPAs stay flat as leverage and AUM rise — is the single most revealing thing an observer can do.

The risk radar for a future filing extends beyond the operating debate. Governance items sit near the top: the independence of the board relative to the founding families, the mapping of any related-party transactions between the lender and promoter-affiliated real-estate interests, and the founder's own equity and control after three rounds of preferred issuance are all diligence items that a prospectus must make legible and that are currently opaque.1 Interest-rate and asset-liability risk is inherent and technical but real: an HFC that funds long-dated mortgages with shorter or floating-rate borrowings is exposed if rates move against it, and with 60–70% of HFC portfolios industry-wide linked to floating rates, a falling-rate environment can compress yields faster than funding costs adjust.1 Fraud and misrepresentation risk is elevated in any lender underwriting informal, undocumented income, and a fast digital front end can amplify it if verification is thin. And key-person risk is acute in a founder-driven financial company of this size — much of the strategy, the investor relationships and the credit culture runs through one person. Regulatory exposure is inherent to the model — an HFC lives or dies by NHB and RBI compliance, and any tightening of norms on co-lending, or on lending against informally-documented income, would strike at the core method; the company reports no regulatory penalties in the year under review, which is reassuring as far as it goes but is a point-in-time fact, not a guarantee.1 Funding dependence remains the structural fragility of any small lender: EHFL's improving rating and diversified base mitigate it, but a wholesale-funding freeze of the kind that periodically hits Indian NBFCs would test it. None of these is evidence of a problem today; all of them are reasons that the absence of a filing should be read as "not yet disclosed," never as "safe."

VIII. Epilogue & Key Takeaways (01:55:00 - 02:00:00)

The valuation question, held to the end, is best answered in the currency a lender is actually priced in: book value and the return earned on it. Because no round disclosed a valuation, there is no market price to anchor to, so the honest exercise is a scenario frame built from operating evidence rather than a reverse-engineered mark. EHFL ended FY25 with about ₹384 crore of net worth, and the Series C added roughly another ₹250 crore of fresh equity, so the company's post-money book value sits in the rough vicinity of ₹600–650 crore.14 What a public market would eventually pay for that book depends almost entirely on the return it earns on it, and this is where a transparent scenario frame is more honest than any single number. The logic that governs a lender's valuation is straightforward: a bank or HFC earning a return on equity equal to its cost of equity is worth roughly one times book; one earning well above its cost of equity is worth a multiple of book, scaled by how far above and for how long; one earning below it is worth a discount to book. Cost of equity for an Indian HFC sits somewhere in the low-to-mid teens. So the entire valuation turns on where EHFL's ROE settles and how durably.

Trace the scenarios. In a bear-to-base outcome — leverage stays stuck near 2x, opex remains sticky around 9%, and ROE lingers in the mid-single digits — EHFL earns well below its cost of equity, and a lender in that state does not command a premium to book; it is worth roughly its net worth, perhaps a modest discount or premium depending on growth optionality, because the market will not pay up for returns beneath its own hurdle. In a base-to-bull outcome — leverage climbs toward 3–4x, opex drifts down toward the 4–6% of efficient scaled AHFCs, and ROE reaches the low-to-mid teens with asset quality holding — EHFL earns around or modestly above its cost of equity and could justify something in the range of one-and-a-half to two-and-a-half times book. In a full-bull outcome — leverage at 4–5x, opex compressed, mid-to-high-teens ROE sustained across a seasoned, geographically diversified book — EHFL would begin to resemble the early-stage version of an Aavas or a Home First, and those companies have at various points commanded price-to-book multiples of roughly 3–4x on the strength of high-teens ROE and long growth runways.56 The sensitivities that move the answer most are, in order: the ROE (which is itself mostly a function of leverage and opex), the credit cost as the book seasons, and the durability of the NIM against competitive compression. The output is a wide range anchored to book value, not a point estimate — and emphatically not a target price — and the width of that range is itself the finding: EHFL's value is unusually undetermined because its defining variable, through-cycle ROE, has not yet been observed.

That peer comparison must be handled with care, because it is where an unwary underwriting goes wrong. Aavas, Home First and India Shelter are the right directional comparables — same segment, same collateral, same borrower — but they are aspirational, not direct, peers today: each is many times EHFL's size, each has a seasoned book tested across more of a cycle, and each already earns the mid-teens-plus ROE that EHFL only aspires to.567 Applying their price-to-book multiple to EHFL's book would be borrowing their proven returns for a company that has not yet earned them — precisely the error of paying a seasoned-franchise multiple for an unseasoned one. Two more cautions apply before importing any peer number: those multiples must be read on a like-for-like basis (same metric, same period, same currency, and — for a lender — always an equity-value basis such as price-to-book or price-to-earnings, never an enterprise-value multiple, which is meaningless when debt is the raw material); and the specific current trading multiples of those peers are not independently verified here and would need to be pulled fresh before use. The correct reconciliation is that EHFL's eventual multiple is not a given to be imported from peers but an output of its own future ROE, and that ROE is exactly what remains unproven. The prospective value, in other words, embeds a specific and demanding belief: that management executes the leverage-up and the opex-down without the credit quality cracking as the book seasons. If that belief proves out, the peer multiples become relevant and the equity is worth a real premium to book; if it does not, EHFL is a well-capitalised lender worth approximately its net worth.

One more force will shape any eventual listing price independent of the fundamentals, and it should be named so it is not mistaken for value. A first-of-its-kind "digital affordable-HFC" listing would carry scarcity appeal; a marquee cap table (SMBC, Investcorp, Claypond) lends narrative credibility; and a thin free float, given how much equity sits with the founders and a handful of institutions, could mechanically amplify price moves in either direction after listing. Those forces are real and can push a price well above or below any intrinsic range for extended periods, but they are pricing phenomena, not business value, and conflating them is the specific mistake this analysis is built to avoid.

Three KPIs will confirm or falsify the thesis faster than anything else, and each maps directly to a fork above. First, and most important, the leverage ratio and the ROE it produces: watch debt-to-equity climb from ~1.8x and ROE climb from ~3.75%, because that single pair of numbers is the entire re-rating thesis made measurable — if leverage rises and ROE follows without NPAs deteriorating, the bull case is being proven in real time.1 Second, the opex-to-assets ratio: a durable decline from ~9% toward the lower cost ratios of efficient scaled AHFCs would validate the tech-first claim; a stubborn plateau would confirm the bear's suspicion that the "tech" premium was never real.1 Third, gross NPAs as the book seasons: the meaningful test is not today's 0.5%, which a young book flatters, but whether asset quality holds as loans originated in 2024–2025 age into their third and fourth years and through whatever macro arrives — the first genuine read on whether the underwriting model actually works.19

The surprise lesson of Easy Home Finance is one the sector keeps re-teaching: technology alone is not a silver bullet in Indian mortgage lending. Software can shrink the turnaround time and delight the borrower at onboarding, but it cannot value a house from a server or collect a delinquent loan over an API, and so the winning model is not "digital" but "phygital" — digital where it scales, human where it must be. EHFL has built a credible version of that hybrid and raised more capital than almost any peer of its size, which buys it the rarest commodity in lending: time and room to grow without dilution. What it has not yet done is the harder thing — turn that capital into a seasoned, scaled, through-the-cycle return. The catalysts that will decide it are identifiable: the pace of leveraging up, the crossing of the ₹1,000 crore and then ₹2,000 crore AUM thresholds, the trajectory of NPAs as the book ages, and, eventually, a filing that finally discloses the governance, ownership and terms that today remain dark. Until those arrive, EHFL is best understood as a well-capitalised option on a proven segment, executed by an operator not yet tested at scale — a genuinely interesting business whose value, as opposed to its price, still waits on evidence it has not yet had the years to produce.

References

-

EHFL Annual Report FY 2024-25 — Easy Home Finance Limited, 2025 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Mortgage firm Easy raises $15 mn in Series A, focus on affordable housing — Business Standard, 2021-07-29 ↩↩↩

-

Easy Home Finance raises $35 Mn from Ranjan Pai's Claypond Capital, others — Entrackr, 2024-11 ↩↩↩↩

-

Easy Home Finance raises $30 million in Series C led by Investcorp — Business Standard, 2026-01-28 ↩↩↩↩

-

Home First Finance Company — Competitor Financial Profile ↩↩↩

-

India Shelter Finance Corporation — Competitor Financial Profile ↩↩

-

India Affordable Housing Sector Credit Overview — CRISIL Ratings ↩↩

-

Credit Rating Report on Easy Home Finance Limited — Acuité Ratings & Research, 2025-11-21 ↩↩↩↩↩↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube