Dr. Reddy's Laboratories: From Indian Generics Pioneer to Global Pharma Player

I. Introduction & Episode Setup

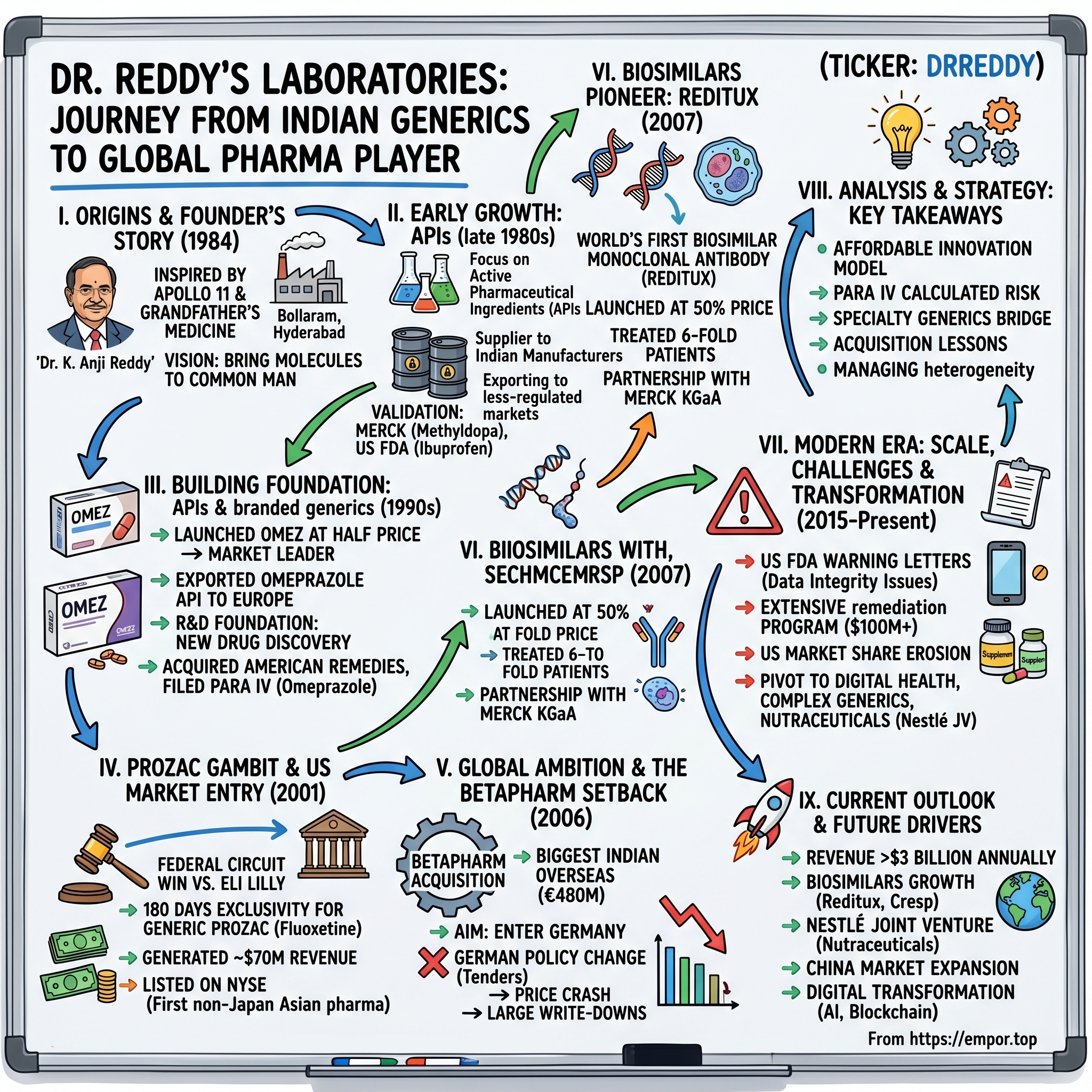

Picture this: It's August 2001, and inside a nondescript courtroom in Washington D.C., lawyers for Eli Lilly are making their final arguments to protect what might be the most valuable patent expiration in pharmaceutical history. Prozac, the little green-and-white capsule that had become synonymous with antidepressants, generated over $2 billion annually at its peak. Across from them sits a legal team representing a company most Americans had never heard of—Dr. Reddy's Laboratories from Hyderabad, India.

When the Federal Circuit Court ruled in Dr. Reddy's favor, it wasn't just a legal victory. It was a seismic shift in the global pharmaceutical landscape. For the first time, an Indian company had successfully challenged Big Pharma on its home turf and won the right to 180 days of generic exclusivity for one of the world's best-selling drugs. In those six months, Dr. Reddy's would generate nearly $70 million in revenue—more than many Indian pharma companies made in a year.

But how did a company founded just 17 years earlier by a chemical engineer from a farming village in Andhra Pradesh find itself toe-to-toe with one of America's pharmaceutical giants? How did Dr. Reddy's transform from a small API manufacturer serving the Indian market into a $10 billion global pharmaceutical powerhouse with operations spanning from New Jersey to Moscow?

The answer lies in a remarkable story of scientific ambition, calculated risk-taking, and an almost religious devotion to a simple principle: making expensive medicines affordable for the common man. It's a story that begins not in a boardroom or laboratory, but with a young boy watching his grandfather distribute herbal medicines for free to villagers who couldn't afford doctors. That boy, Kallam Anji Reddy, would grow up to challenge the entire economics of global healthcare.

Today, Dr. Reddy's operates across more than 40 countries, employs over 20,000 people, and manufactures everything from simple painkillers to complex biosimilar cancer treatments. Its American headquarters in East Brunswick, New Jersey, sits just miles from the offices of Johnson & Johnson and Bristol-Myers Squibb—a geographic proximity that would have seemed absurd when the company started in 1984.

This is the story of how one scientist's dream became India's pharmaceutical moonshot, how a company from Hyderabad rewrote the rules of generic drug development, and what happens when emerging market innovation collides with first-world regulatory systems. It's about patent battles and pricing wars, brilliant science and catastrophic acquisitions, biosimilar breakthroughs and FDA warning letters.

Most importantly, it's about a fundamental question that still drives pharmaceutical innovation today: Can you build a sustainable business model around making expensive drugs cheap? Dr. Reddy's thirty-year answer to that question has implications far beyond balance sheets and market caps—it's quite literally a matter of life and death for millions of patients worldwide.

II. The Founder's Story & Origins (1984-1990)

The date was July 20, 1969, and Kallam Anji Reddy couldn't sleep. Like millions around the world, the 28-year-old chemical engineer was glued to his radio, listening to the crackling broadcasts of Apollo 11's lunar landing. But while others marveled at Armstrong's first steps, Reddy's mind was racing in a different direction. "When Kennedy's seemingly impossible mission of landing a man on the moon was actually happening," he would later write, "I woke up from my sleep. Not just literally, but metaphorically. If America could put a man on the moon, why couldn't India create its own pharmaceutical industry? I started dreaming of creating my own pharmaceutical company."

It was an audacious dream for someone from Tadepalli, a farming village in Andhra Pradesh where his family was better known for growing rice than synthesizing molecules. Yet the seeds of this ambition had been planted much earlier. Reddy grew up watching his grandfather prepare and distribute herbal medicines to villagers who couldn't afford conventional treatment. This wasn't charity in the Western sense—it was dharma, duty, an understanding that healing shouldn't be limited by economics. The academic journey that followed was unconventional for a farmer's son in 1950s India. After excelling at A.C. College at Guntur in 1958, Reddy made his way to Mumbai—then Bombay—to study at the prestigious University Department of Chemical Technology. Here, in the bustling commercial capital of India, surrounded by textile mills and the beginnings of India's industrial revolution, he discovered his calling. He earned his B.Sc.(Tech) in Pharmaceuticals and Fine chemicals from the University Department of Chemical Technology of University of Mumbai, followed by a PhD in chemical engineering under L.K Doraiswamy from the National Chemical Laboratory, Pune in 1969.

But it was his first job that truly shaped his entrepreneurial vision. Dr Kallam Anji Reddy started his career in the state-owned Indian Drugs and Pharmaceuticals Limited, Hyderabad, in 1967. IDPL was Nehru's socialist dream made manifest—a government-owned pharmaceutical company meant to make India self-sufficient in essential medicines. For Reddy, it was both inspiring and frustrating. He saw firsthand how bureaucracy and lack of innovation kept drug prices high despite government ownership. The inefficiencies were maddening: it could take months to get approval for a simple process improvement, years to introduce a new product. In fact, as early as 1973, he had written down his vision: 'to bring new molecules into the country at a price the common man can afford'. This wasn't just corporate mission statement fodder—it was a deeply personal manifesto, written years before he would have the means to execute it.

The frustrations at IDPL eventually became unbearable. He worked for six years at the state owned Indian Drugs and Pharmaceuticals Limited, where his entrepreneurial ambitions were fired. In 1973, he left IDPL and over the next ten years was part of the founding team of two bulk drug manufacturing ventures. These ventures gave him invaluable experience in the pharmaceutical supply chain, but they weren't his companies. They didn't carry his vision.

In 1984, Reddy founded Dr. Reddy's Laboratories, using $40,000 of his own, backed by a bank loan for $120,000. The initial capital was laughably small by pharmaceutical standards—Pfizer probably spent more on office supplies that year. But Reddy had a strategy: start with what India did best—manufacturing active pharmaceutical ingredients (APIs) at a fraction of Western costs.

The location he chose was telling: Bollaram, on the outskirts of Hyderabad. In 1985, a small yet ambitious API factory opened its doors in Bollaram, Hyderabad. It was the beginning of Dr Reddy's journey in the field of pharmaceuticals. This wasn't Bangalore with its tech aspirations or Mumbai with its financial muscle. Hyderabad in 1985 was a sleepy city better known for biryani than biotechnology. But land was cheap, the state government was supportive, and most importantly, it was home.

The early strategy was brilliant in its simplicity. Rather than compete head-to-head with established Indian pharma companies in the domestic market, Dr. Reddy's began as a supplier to Indian drug manufacturers, but it soon started exporting to less-regulated markets that had the advantage of not having to spend time and money on a manufacturing plant that would gain approval from a drug licensing body such as the U.S. Food and Drug Administration (FDA).

The following year, 1986, marked a significant milestone as Dr Reddy's went public and became listed on the Bombay Stock Exchange. They proudly introduced APIs for the first time in India. Going public this early was unusual—most Indian companies waited decades before listing. But Reddy needed capital, and more importantly, he wanted transparency and accountability from day one.

The breakthrough came with methyldopa, a blood pressure medication. In one year, Dr. Reddy's Laboratories got listed on the Bombay Stock Exchange and entered the international market during this year with the export of the API Methyldopa. Western pharmaceutical companies were skeptical—could an Indian company really maintain the quality standards required for API exports? Despite doubts from big global companies like Merck, Dr. Reddy's became the largest supplier of Methyldopa to the US and Europe.

But the real validation came in 1987. The U.S. FDA, the gold standard of pharmaceutical regulation, approved Dr. Reddy's ibuprofen API manufacturing facility. This wasn't just a certificate on the wall—it was a passport to the global pharmaceutical market. In 1987, Reddy's started to transform itself from a supplier of pharmaceutical ingredients to other manufacturers into a manufacturer of pharmaceutical products.

As the 1980s drew to a close, Dr. Reddy's had established itself as a serious player in the API market. But Kallam Anji Reddy was already thinking bigger. APIs were commodities—important, profitable commodities, but commodities nonetheless. The real value, the real impact on patients' lives, came from finished formulations. And that's where Dr. Reddy's would go next, armed with the credibility of FDA approvals and the cash flow from API exports.

The moon landing that had inspired young Reddy twenty years earlier suddenly didn't seem like such an impossible analogy. If you could make medicines in Bollaram that met the standards of Washington, what else might be possible?

III. Building the Foundation: APIs & Early Growth (1990s)

The boardroom at Dr. Reddy's Hyderabad headquarters in early 1991 was tense. The marketing team had just presented their pricing strategy for Omez, the company's branded version of omeprazole, and the numbers seemed insane. They wanted to launch at 50% of the price of existing brands in India. The CFO was incredulous: "We'll be leaving money on the table. Doctors won't prescribe a cheaper drug—they'll think it's inferior."

Kallam Anji Reddy stood up and walked to the window overlooking the dusty streets of Hyderabad. "When I was young," he said, turning back to the room, "my neighbor had terrible stomach ulcers. The medicine cost more than his monthly salary. He chose to suffer instead. How many millions are making that same choice today?" The room fell silent. "We launch at half price. Let's see if we can't expand the market instead of fighting for the same small pie."

Soon, Dr. Reddy's obtained another success with Omez, its branded omeprazole – gastrointestinal ulcer and reflux oesophagitis medication – launched at half the price of other brands on the Indian market at that time. The gamble paid off spectacularly. In 1991, the company launched Omez (Omeprazole) for heartburn and gastro-related problems. It became a household name in India. Within two years, Omez wasn't just competing—it was dominating, becoming one of India's most prescribed gastrointestinal drugs.

But the real coup came from an unexpected direction. Within a year, Reddy's became the first Indian company to export the active ingredients for pharmaceuticals to Europe. European pharmaceutical companies, always looking to cut costs, discovered that Dr. Reddy's could deliver omeprazole API at a fraction of what their traditional suppliers charged. As Reddy told the Financial Times: "After Astra, I think I must be the largest producer in the world."

The success with Omez taught Dr. Reddy's a crucial lesson: in pharmaceuticals, pricing wasn't just about margins—it was about market creation. Millions of Indians needed these medicines but couldn't afford them at Western prices. By dramatically cutting costs through efficient manufacturing and accepting lower margins, Dr. Reddy's could tap into an enormous latent demand. This philosophy extended to international expansion. The company's first international move took it to Russia in 1992. There, Dr. Reddy's formed a joint venture with the country's biggest pharmaceuticals producer, Biomed. It was a bold move—post-Soviet Russia was chaotic, unpredictable, a Wild West of capitalism. But it was also a massive market starved of quality medicines.

The Russia venture started promisingly. In 1992, Dr Reddy's expanded its global footprint by establishing a branch in Russia. The joint venture gave Dr. Reddy's access to Biomed's distribution network across the former Soviet Union, while Biomed got access to quality generic formulations. In 1993, Reddy's entered into a joint venture in the Middle East and created two formulation units there and in Russia. Reddy's exported bulk drugs to these formulation units, which then converted them into finished products.

But by 1995, the Russian dream turned into a nightmare. They pulled out in 1995 amid accusations of scandal, involving "a significant material loss due to the activities of Moscow's branch of Reddy's Labs with the help of Biomed's chief executive". Reddy's sold the joint venture to the Kremlin-friendly Sistema group. The exact details remain murky—a combination of corruption, mismanagement, and the general chaos of 1990s Russia. It was Dr. Reddy's first major international setback, a harsh lesson in the risks of emerging market expansion.

Yet even as the Russia venture was unraveling, something remarkable was happening back in Hyderabad. Dr. Reddy's Research Foundation was established in 1992 and in order to do research in the area of new drug discovery. This was audacious—Indian companies didn't do drug discovery. They made copies, generics, maybe improved formulations. But creating entirely new molecules? That was the domain of Pfizer, Merck, and Glaxo.

In 1993, their commitment to innovation deepened with the initiation of new drug discovery through the Dr. Reddy's Research Foundation. The Research Foundation represented a fundamental shift in Indian pharmaceutical thinking. At first, the foundation's drug research strategy revolved around searching for analogues. Focus has since changed to innovative R&D, hiring new scientists, especially Indian students studying abroad on doctoral and post-doctoral courses.

The strategy was clever: focus on diseases prevalent in India but neglected by Western pharma—diabetes, cardiovascular disease, infections resistant to existing antibiotics. These were massive markets with unmet needs. If Dr. Reddy's could develop new molecules for these conditions, they wouldn't just be copying Western innovation—they'd be leading it.

By 1997, this bet began to pay off. The year 1997 marked another milestone as Dr. Reddy's became the first Indian pharma company to out-license a novel drug. The molecule was licensed to Novo Nordisk, the Danish diabetes giant. The financial terms were modest—a few million dollars upfront plus royalties—but the symbolic value was enormous. An Indian company had created something valuable enough for a Western pharmaceutical giant to license.

The 1990s also saw strategic acquisitions that strengthened Dr. Reddy's manufacturing base. In 1999, the company acquired American Remedies Ltd., adding significant formulation capacity and a strong domestic distribution network. The same year, they submitted their first Para IV application for omeprazole in the United States—a legal challenge asserting that the patent on Prilosec was either invalid or wouldn't be infringed by Dr. Reddy's generic version.

As the millennium approached, Dr. Reddy's had transformed from a small API manufacturer into a diversified pharmaceutical company with operations spanning from basic chemicals to cutting-edge drug discovery. Revenue had grown from a few million dollars in 1990 to over $100 million by 1999. The company employed over 2,000 people and operated six manufacturing facilities.

But Kallam Anji Reddy wasn't satisfied. In a 1999 interview, he laid out his vision for the next decade: "We want to be in the U.S. generic market in a big way. Not just participating, but shaping it." His executives thought he was dreaming. The U.S. generic market was brutal—razor-thin margins, fierce competition, and regulatory requirements that could bankrupt a company with one mistake.

What they didn't know was that Reddy had already identified the opportunity that would catapult Dr. Reddy's onto the global stage: Prozac was going off patent, and he intended to be first in line.

IV. The Prozac Gambit & US Market Entry (2000-2005)

The conference room on the 42nd floor of a Manhattan law firm was silent except for the shuffling of papers. It was August 9, 2001, and Dr. Reddy's legal team had just received word: the Federal Circuit Court had ruled in their favor. They had won the right to launch generic Prozac with 180 days of market exclusivity. Across the table, Eli Lilly's lawyers sat stone-faced. They had just lost control of a drug that generated $2.5 billion annually.

G.V. Prasad, Dr. Reddy's CEO and son-in-law of the founder, allowed himself a small smile. They had bet everything on this moment—$25 million in legal fees, untold hours of research, and the company's reputation. If they had lost, Dr. Reddy's would have been just another failed generic challenger. Instead, they were about to make history.

The Prozac story actually began in 1998, when Dr. Reddy's scientists in Hyderabad made a crucial discovery. While analyzing Eli Lilly's patents on fluoxetine (Prozac's active ingredient), they found what they believed was a weakness in the crystalline form patent that extended Lilly's monopoly. By 1997, Reddy's made the transition from being an API and bulk drug supplier to regulated markets like the US and the UK, and a branded formulations supplier in unregulated markets like India and Russia, into producing generics, by filing an Abbreviated New Drug Application (ANDA) in the USA. The same year, Reddy's out-licensed a molecule for clinical trials to Novo Nordisk, a Danish pharmaceutical company.

The Para IV certification—named after Paragraph IV of the Hatch-Waxman Act—was a high-stakes poker game. By challenging Lilly's patent, Dr. Reddy's was essentially saying: "We think your patent is invalid, and we're willing to bet millions in legal fees to prove it." If they won, they'd get 180 days of exclusive generic sales. If they lost, they'd face damages and would have to wait until the patent expired naturally. The litigation was complex and brutal. Lilly had numerous other patents surrounding the drug compound and had already enjoyed a long period of patent protection. The case to allow generic sales was heard twice by the Federal Circuit Court, and Reddy's won both hearings. When the appeals court finally ruled in Dr. Reddy's favor in August 2001, it triggered a gold rush.

In 2001 Reddy's became the first Indian company to launch the generic drug, fluoxetine (a generic version of Eli Lilly and Company's Prozac) with 180-day market exclusivity in the USA. Prozac had sales in excess of $1 billion per year in the late 1990s. Barr Laboratories of the U.S. obtained exclusivity for all of the approved dosage forms (10 mg, 20 mg) except one (40 mg), which was obtained by Reddy's.

The 40mg formulation might have seemed like the consolation prize, but Dr. Reddy's marketing team had done their homework. Many patients on long-term Prozac therapy took the 40mg dose. While Barr fought for the more common 20mg market, Dr. Reddy's quietly captured a lucrative niche. Reddy's generated nearly $70 million in revenue during the initial six-month exclusivity period. With such high returns at stake, Reddy's was gambling on the success of the litigation; failure to win the case could have cost them millions of dollars, depending on the length of the trial.

But the Prozac victory was about more than money. In 2001, Reddy's completed its US initial public offering of $132.8 million, secured by American Depositary Receipts. At that time the company also became listed on the New York Stock Exchange. Dr. Reddy's was the first Asian pharmaceutical company, excluding Japan, to list on the NYSE. For a company founded just 17 years earlier with $160,000, this was a stunning achievement.

The NYSE listing transformed Dr. Reddy's profile. Suddenly, American institutional investors were analyzing an Indian pharmaceutical company. The financial press was writing about Hyderabad alongside New Jersey. The listing raised Dr. Reddy's cost of capital expectations but also its governance standards. Funds raised from the initial public offering helped Reddy's move into international production and take over technology-based companies.

The years following Prozac saw Dr. Reddy's double down on the Para IV strategy. Reddy's entered into a venture investment agreement with ICICI Bank, an established Indian banking company. Under the terms of the agreement, ICICI Venture agreed to fund the development, registration and legal costs related to the commercialisation of ANDAs on a pre-determined basis. This was financial engineering at its finest—ICICI would share the risks and rewards of patent challenges, allowing Dr. Reddy's to pursue multiple targets simultaneously.

Meanwhile, the company continued its expansion through strategic acquisitions. In March 2002, Dr. Reddy's acquired BMS Laboratories, Beverley, and its wholly owned subsidiary Meridian Healthcare, for €14.81 million. These companies deal in oral solids, liquids and packaging, with manufacturing facilities in London and Beverley in the UK. This gave Dr. Reddy's a manufacturing footprint in Europe, crucial for serving that market directly.

The innovation engine also continued to hum. In 2003, Reddy's also invested $5.25 million (USD) in equity capital into Bio Sciences Ltd. Auriegene Discovery Technologies, a contract research company, was established as a fully owned subsidiary of Reddy's in 2002. Auriegene's objective was to gain experience in drug discovery through contract research for other pharmaceutical companies.

The period from 2000 to 2005 also saw a significant milestone in mergers. Reddy's merged Cheminor Drug Limited (CDL) with the primary aim of supplying active pharmaceutical ingredients to the technically demanding markets of North America and Europe. This merger also gave Reddy's an entry into the value-added generics business in the regulated markets of APIs. By 2005, Dr. Reddy's had become the third-largest pharmaceutical company in India.

The company also made a strategic move into Mexico, acquiring Roche's API business for $60 million in 2005. This gave Dr. Reddy's access to the Latin American market and additional API manufacturing capabilities. Each acquisition was carefully chosen to either expand geographic reach, add technical capabilities, or provide access to new product portfolios.

But as 2005 drew to a close, Kallam Anji Reddy was growing restless. The company had proven it could compete in generics, win patent battles, and execute targeted acquisitions. Revenue had crossed $500 million. But Reddy wanted more—he wanted Dr. Reddy's to be a truly global player, with a presence in every major pharmaceutical market.

His eyes turned to Europe, specifically Germany, where an opportunity had presented itself. Betapharm, Germany's fourth-largest generic company, was up for sale. At $560 million, it would be the largest acquisition in Indian pharmaceutical history. The board was nervous—it was more than the company's entire annual revenue. But Reddy was convinced: to play with the big boys, you had to make big bets. The question was whether this particular bet would pay off.

V. The Betapharm Acquisition: Ambition Meets Reality (2006-2014)

The boardroom at Dr. Reddy's Hyderabad headquarters was unusually quiet on February 16, 2006. The company had just agreed to acquire Betapharm, Germany's fourth largest generic pharmaceutical company, for €480 million ($560 million). It was a moment that should have been celebratory—the biggest overseas acquisition by an Indian pharmaceutical company. Yet G.V. Prasad, the CEO, noticed that several board members looked more worried than excited.

"This is ten times larger than any acquisition we've ever done," one director finally said. "What if something goes wrong?"

Kallam Anji Reddy, now 65, stood up slowly. "When I started this company, people said an Indian company could never get FDA approval. When we challenged Prozac, they said we'd be crushed by Eli Lilly's lawyers. Each time, we proved them wrong. Yes, this is big. But if we want to be a global company, we need to think globally. "The acquisition was hailed as the biggest overseas acquisition made by an Indian pharmaceutical company. The synergies from the acquisition were expected to benefit both DRL and Betapharm. The acquisition gave DRL access to the German generic drugs market, the second-largest generic drugs market in the world, as well as help DRL leverage the strong marketing and distribution channels of Betapharm in Germany.

What made the deal particularly interesting was how Dr. Reddy's won it. DRL's commitment to corporate social responsibility was also a factor that clinched the deal in its favor, despite not being the highest bidder. When the bidding process began, there were four Indian companies: Wockhardt, Zydus Cadila, Ranbaxy, and Dr. Reddy's. But 3i, the private equity firm selling Betapharm, wasn't just looking at price.

Betapharm had a unique culture. Beyond its portfolio of over 145 products and position as Germany's fourth-largest generic pharmaceutical company, Betapharm was known for its social initiatives. The sale deal also included the 'beta institut for sociomedical research GmbH' (beta Institut), a non-profit research institute founded and funded by betapharm to conduct research on issues related to social aspects of medicine and health management. This resonated deeply with Dr. Reddy's own philosophy of making medicines accessible.

The financing structure revealed both confidence and risk. The company already had $200 million in cash (about Rs 900 crore). The rest was raised through debt from domestic financial institutions. The debt-equity ratio rose to 1.39 times in March 2006. This was aggressive leveraging for an Indian pharmaceutical company, but the German generic market seemed worth the risk.

"We see our investment in Betapharm as a key strategic initiative towards becoming a mid-sized global pharmaceutical company with strong presence in all key pharmaceutical markets," Dr. K. Anji Reddy, Chairman, said in March 2006. "Betapharm has created a strong growth platform and is well positioned for the future and we are looking forward to partner with them in building a strategic presence in Europe."

Initially, the markets loved it. Dr. Reddy's stock closed a whopping 9.3% up on the news. Investment banks calculated the payback period at 6-7 years, with the deal seen as accretive to earnings. ICICI did a quick NPV valuation of Betapharm and arrived at a value of €550-560 million assuming WACC of 12% and a sustainable growth rate of 5%.

But within months, disaster struck. A few months after the acquisition, there were already early signs of trouble, as the Economic Optimisation of Pharmaceutical Care Act (AVWG) took effect in Germany on May 1, 2006. Within months of the acquisition, the German government changed its procurement policy, shifting to a tender-based system for a substantial number of drugs. This reduced drug reference prices.

The impact was catastrophic. Betapharm's contribution to sales has been falling consistently — from Rs 977 crore in 2008-09 to Rs 518 crore in 2011-12. In 2011-12, Betapharm posted losses of Rs 75 crore. Six years later, the valuation of Betapharm in the company's balance sheet is just $108 million (about Rs 590 crore), a 75 per cent fall.

The writedowns were painful and public. The carrying value (the fair value in accounting terms for the operations) of betapharm is down to €90 million from the acquisition cost of €480 million after four rounds of impairments in its books. Dr. Reddy's went into the red in 2008-09, thanks to huge write-downs because of betapharm.

The human cost was equally severe. To ensure it is viable, Dr Reddy's brass has been working on betapharm's cost structure—four years after the acquisition, 35 per cent of betapharm's products (by value) have been transferred to India, and the workforce downsized from 400 at the peak to around 80 today.

Managing Director and Chief Operating Officer Satish Reddy, who had taken over more operational responsibilities from his father, was remarkably candid about the failure: "Sufficient understanding of the market would have actually helped us, rather than making an acquisition of that nature, overpaying, and then trying to make the best out of it."

Executive Vice-President and Chief Financial Officer Umang Vohra reflected on the lessons learned: "We realised we should make acquisitions that improved the capabilities within the organisation, against buying a company in some market that merely increased the turnover."

The Betapharm experience fundamentally changed Dr. Reddy's acquisition strategy. The company decided not to take the bidding route in any acquisition. It also decided to concentrate on smaller acquisitions. As a result, all companies acquired by the company after Betapharm had ticket sizes of about $40 million and were chosen based on some product, research or manufacturing area that complemented capabilities within the company.

G.V. Prasad, looking back years later, was philosophical: "I don't think we have dealt with betapharm. What we have dealt with is writing down the value of betapharm, and we have cut costs. We have not grown but shrunk the business. It is still an unfinished task and will take another 2-3 years."

The Betapharm acquisition became a cautionary tale in Indian corporate history—a reminder that size alone doesn't guarantee success, that regulatory environments can change overnight, and that even the best-intentioned strategies can fail spectacularly. But for Dr. Reddy's, it also became a crucible that forged a more disciplined, focused approach to growth. The company that emerged from the Betapharm crisis was leaner, more careful, but also more determined to prove that the failure was an exception, not the rule.

VI. The Biosimilars Pioneer: Reditux & Beyond (2007-2015)

The cancer ward at Mumbai's Tata Memorial Hospital in early 2007 was a study in contrasts. In the private rooms, patients received Rituxan, Roche's blockbuster treatment for Non-Hodgkin's Lymphoma, at ₹1.5 lakh per dose. In the general ward, patients went without treatment entirely—the drug cost more than most Indians earned in a year. Dr. Suresh Advani, the hospital's chief oncologist, had watched this inequality for years. "We can diagnose the cancer," he would tell colleagues bitterly, "but we can't afford to cure it."

That March, everything changed. Dr. Reddy's launched Reditux, the world's first biosimilar monoclonal antibody, at ₹75,000 per dose—exactly half the price of the original. But this wasn't just another generic launch. Biosimilars are to traditional generics what Formula One racing is to go-karting—exponentially more complex, requiring living cell cultures, sophisticated manufacturing, and extensive clinical trials to prove similarity to the original biologic.

"People said we were crazy," recalls Dr. Krishna Prasad, who led the biosimilars division. "Even Big Pharma companies were hesitant to enter biosimilars. The investment required was enormous, the regulatory pathway unclear, and the science incredibly complex. But we saw it differently—if we could crack this, we could transform cancer care in India. "The development of Reditux had taken seven years and cost over $20 million—a fraction of what Western companies spent on biologics development, but enormous by Indian standards. The science was groundbreaking. Reditux was introduced in India in April 2007 at 50% of the original price in India, producing a 10-fold market expansion for the product. This wasn't just price elasticity at work—it was market creation.

The impact was immediate and profound. Within 3 years of launch of Reditux, the number of patients receiving this therapy increased more than six-fold in India. In 2010–11, domestic revenues from Reditux grew 75% making the product the fourth-largest brand in Dr Reddy's portfolio.

But what made Reditux truly revolutionary wasn't just the price. It was the proof of concept for biosimilars in emerging markets. Unlike small-molecule generics, which are chemically identical to their branded counterparts, biosimilars are produced in living cells and can only be "similar," never identical. The regulatory pathway was uncertain, the science complex, and the investment substantial.

Dr. Reddy's approach was pragmatic. The approval pathway for the rituximab product in India followed a single-arm clinical trial that populated a clinical trial database. The objective response rate of the trial was demonstrated among 67 patients in India. Comparisons were shown with the originator product using literature searches to show similar objective response rates for the same indication. Western regulators would have demanded much larger trials, but India's regulators understood the trade-off: perfect data versus accessible treatment.

The scientific validation came later. The pharmacokinetic profile and B-cell response to Reditux™ are comparable with those reported for MabThera™. Thus, MabThera™ can be substituted with Reditux™ for the treatment of B-cell lymphomas. Real-world studies confirmed what Dr. Reddy's had claimed: the biosimilar worked as well as the original.

The success with Reditux attracted international attention. In 2008, Dr. Reddy's entered the biosimilars market with Reditux, and by 2012 had three biosimilars on the market in India. The product portfolio expanded to include Cresp (darbepoetin alfa) for anemia and other biosimilar products. The real validation came in 2012 with an unexpected partnership. Partnership to co-develop a portfolio of biosimilar compounds in oncology, primarily focused on monoclonal antibodies (MAbs). The partnership between Dr Reddy's and German pharmaceutical firm Merck KGaA, covers co-development, manufacturing and commercialization of a portfolio of biosimilar compounds in oncology, primarily focused on monoclonal antibodies.

This wasn't just another licensing deal. According to the agreement, which is based on 'full R & D cost sharing', Dr Reddy's will lead early product development and complete Phase I development, after which the Merck Serono division will take over manufacturing of the compounds and will lead Phase III development. In the US, the parties will co-commercialize the products on a profit-sharing basis.

For Dr. Reddy's, this was recognition from one of Europe's oldest pharmaceutical companies that they were peers, not just contract manufacturers. Stefan Oschmann, Chief Executive Officer of Merck Serono, acknowledged as much: "Our expertise in developing, manufacturing, and commercializing biopharmaceuticals gives us a clear advantage in the biosimilars field, and the partnership with Dr. Reddy's will bring their first-in-market experience in biosimilars, as well as their expertise in generics and Emerging Markets, to the table."

The biosimilars business also helped Dr. Reddy's weather the Betapharm storm. By 2013, the company now has four biosimilars molecules on the market, with seven other biosimilars in various stages of development. These high-margin products provided crucial cash flow during the years of Betapharm writedowns.

But biosimilars also presented unique challenges. Unlike small-molecule generics, where the regulatory pathway was clear, biosimilars operated in a gray zone. The FDA had only recently established guidelines, Europe was still figuring out interchangeability, and emerging markets had wildly different standards. Dr. Reddy's had to essentially create different versions of the same product for different markets.

There were also ethical considerations. In 2013, at a conference in Mumbai, a Western journalist challenged G.V. Prasad about whether Dr. Reddy's biosimilars were truly equivalent to the originals. "You're asking the wrong question," Prasad replied. "The question isn't whether our biosimilar is identical to Roche's product. The question is whether a patient in India should get our biosimilar at half the price, or no treatment at all."

By 2015, Dr. Reddy's biosimilars division was generating over $200 million in revenue, with products approved in over 25 countries. The company had established dedicated biosimilar manufacturing facilities and was investing heavily in next-generation biologics. What had started as a moonshot project to make cancer drugs affordable had become a cornerstone of the company's growth strategy.

The biosimilars journey also marked a philosophical evolution for Dr. Reddy's. They were no longer just making copies of Western drugs—they were pioneering an entirely new category of medicines, creating the regulatory frameworks, educating doctors and patients, and proving that emerging market companies could innovate in the most complex areas of pharmaceutical science.

VII. Modern Era: Scale, Challenges & Transformation (2015-Present)

The morning of November 11, 2014, should have been routine at Dr. Reddy's manufacturing facility in Srikakulam, Andhra Pradesh. The plant was preparing a shipment of generic drugs bound for the United States when quality control flagged an anomaly. What they discovered would trigger one of the most challenging periods in the company's history.

FDA inspectors, arriving weeks later, found evidence of data integrity issues—laboratory results that had been selectively reported, stability tests that hadn't been properly documented. The Warning Letter that followed in November 2015 was devastating. Three of Dr. Reddy's most important manufacturing facilities were effectively banned from shipping new products to the United States, the company's largest market.

"It was a wake-up call," admits Satish Reddy, who had taken over as Chairman after his father's death in 2013. "We had grown so fast, acquired so many facilities, that our quality systems hadn't kept pace with our ambitions. We were operating like ten different companies instead of one."

The FDA issues came at the worst possible time. Dr. Reddy's had just crossed a major milestone—becoming the fastest Indian pharma company to surpass USD 1 billion in revenue in 2006, and by 2015, revenues had grown to over $2 billion. But with the U.S. market accounting for nearly 40% of sales, the FDA sanctions threatened to derail everything. The response was comprehensive and painful. An FDA warning letter found that for years, Dr. Reddy's Laboratories was testing drug batches in a laboratory that the FDA was never told existed and often shipped to the U.S. products that had repeatedly failed tests for impurities. The discovery of this "uncontrolled Custom QC laboratory" at the Srikakulam plant was particularly damaging to Dr. Reddy's credibility.

The company embarked on what G.V. Prasad called "the most extensive remediation program in our history." Over $100 million was invested in quality systems upgrades. External consultants from McKinsey were brought in to redesign processes. Every standard operating procedure was rewritten. More than 500 quality professionals were hired globally.

"We had to essentially rebuild our quality culture from the ground up," explains the head of quality who was brought in from Novartis in 2016. "It wasn't just about fixing specific observations. It was about changing how 20,000 employees thought about quality."

The remediation took five years. Based on our evaluation, it appears that you have addressed the violations and deviations contained in this Warning Letter, the FDA finally wrote in August 2020. But the damage was done. Dr. Reddy's U.S. market share had eroded, several product launches were delayed, and the company's reputation had taken a significant hit.

Yet even as Dr. Reddy's was dealing with quality issues, the company was quietly building capabilities in new areas. Digital therapeutics emerged as a surprising focus. In 2019, the company launched its first digital health initiative in India, combining medication with digital coaching for diabetes management. Most significantly, 2024 saw a major strategic shift. Nestlé India and Dr. Reddy's Laboratories Ltd today announced that they have entered into a definitive agreement to form a joint venture ("JV Company") to bring innovative nutraceutical brands to consumers in India and other agreed territories. The partnership will bring together the well-known global range of nutritional health solutions as well as vitamin, minerals, herbals and supplements of Nestlé Health Science (NHSc) with the strong and established commercial strengths of Dr. Reddy's in India.

This wasn't just another product extension—it represented a fundamental rethinking of what Dr. Reddy's could be. "We're moving beyond the traditional pharmaceutical model," explains M.V. Ramana, CEO of Branded Markets. "This joint venture is a novel approach by two companies that have a shared purpose of good health."

The venture, headquartered in Hyderabad, combines brands from both companies. Dr. Reddy's will license brands such as Rebalanz, Celevida, Antoxid, Kidrich-D3, Becozinc in the nutrition, and OTC segments. It's a $160 million bet on the future of healthcare being as much about prevention and wellness as treatment.

The modern Dr. Reddy's is a study in contrasts. The company produces over 190 medications, 60 active pharmaceutical ingredients (APIs) for drug manufacture, diagnostic kits, critical care, and biotechnology. Major therapeutic areas include gastrointestinal, cardiovascular, diabetology, oncology, pain management and dermatology. Major markets include USA, India, Russia & CIS, China, Brazil and Europe.

Digital transformation has become central to the company's strategy. In 2019, Dr. Reddy's expanded into digital therapeutics and e-commerce in India. By 2024, as they celebrated #40YearsOfDrReddys, the company was investing heavily in artificial intelligence for drug discovery, blockchain for supply chain management, and digital health platforms for patient engagement.

The Russia-Ukraine conflict presented unexpected challenges. While many Western companies withdrew from Russia after the 2022 invasion, Dr. Reddy's maintained operations, citing humanitarian obligations to patients. The decision was controversial but reflected the complex realities of operating in emerging markets.

Current financial performance reflects both the challenges and opportunities. Revenue has grown to over $3 billion annually, but margins remain under pressure from pricing competition in the U.S. generic market and continued investment in quality systems and new capabilities. The company's market capitalization hovers around $12 billion, making it one of India's most valuable pharmaceutical companies.

Yet challenges remain formidable. The U.S. generic market has become increasingly commoditized, with consolidation among buyers driving prices down. Biosimilar development requires massive investment with uncertain returns. Regulatory requirements continue to tighten globally. And new competitors from China are entering markets that Indian companies once dominated.

"We're at an inflection point," admits Satish Reddy. "The strategies that got us here won't get us to the next level. We need to innovate not just in products but in business models."

As 2024 draws to a close, Dr. Reddy's stands at a crossroads that mirrors the broader Indian pharmaceutical industry. The company that pioneered affordable generics and biosimilars must now navigate a world where those advantages are being eroded. The next chapter of Dr. Reddy's story will determine whether it can make the leap from emerging market champion to true global pharmaceutical leader.

VIII. Playbook: Business Strategy & Lessons

If you were to distill Dr. Reddy's forty-year journey into a business school case study, what would be the key lessons? The company's playbook—both its successes and failures—offers a masterclass in emerging market innovation, but also cautionary tales about the limits of ambition.

The Affordable Innovation Model

At its core, Dr. Reddy's business model has always been about arbitrage—not just price arbitrage, but innovation arbitrage. The company identified drugs that were essential but unaffordable and found ways to produce them at fractions of the original cost. This wasn't just about cheap labor or lax regulations. It required genuine innovation in chemistry, process engineering, and manufacturing.

Take the Reditux example. Creating a biosimilar wasn't simply copying a molecule—it required developing entirely new cell lines, perfecting fermentation processes, and proving clinical equivalence. Dr. Reddy's spent $20 million developing Reditux, while Western companies typically spent $100-200 million on biosimilars. The difference wasn't corner-cutting; it was frugal innovation—achieving the same outcome with radically different resource allocation.

The Para IV Strategy: Calculated Risk-Taking

Dr. Reddy's Para IV strategy—challenging pharmaceutical patents to win 180-day generic exclusivity—was essentially legalized gambling with enormous payoffs. The Prozac case alone generated $70 million in six months. But for every Prozac, there were multiple failures that cost millions in legal fees with zero return.

The key insight wasn't just to challenge patents randomly but to develop deep expertise in crystalline chemistry and formulation science. Dr. Reddy's scientists became experts at finding the weak points in pharmaceutical patents—alternative crystal forms, different salt formations, novel delivery mechanisms. This required investing in PhD-level scientists in India when most generic companies were focused on reverse engineering.

The Specialty Generics Bridge

One of Dr. Reddy's most sophisticated strategies was using specialty generics as a bridge between pure generics and innovative drugs. Complex generics—like long-acting injectables, controlled-release formulations, and combination products—commanded higher margins than simple generics but required less investment than new drug development.

This middle path allowed Dr. Reddy's to build sophisticated R&D capabilities while maintaining cash flow. The company could invest $10-20 million in a complex generic with relatively predictable returns, versus $100 million-plus for a new drug with a 90% failure rate.

Acquisition Lessons: The Betapharm Disaster

The Betapharm acquisition remains a defining moment—not for its success, but for its spectacular failure. The lessons are worth examining:

First, regulatory environments can change overnight, especially in socialized healthcare systems. Dr. Reddy's assumed German drug pricing would remain stable. When the government shifted to tender-based procurement, margins evaporated.

Second, cultural integration matters more than financial synergies. Betapharm's German employees never fully embraced Indian management styles. The productivity improvements Dr. Reddy's expected from applying Indian cost structures to German operations never materialized.

Third, size matters in acquisitions. As the CFO later admitted: "We realised we should make acquisitions that improved the capabilities within the organisation, against buying a company in some market that merely increased the turnover." Post-Betapharm, Dr. Reddy's never made an acquisition larger than $40 million.

Managing Complexity Across Markets

Dr. Reddy's operates in over 40 countries with vastly different regulatory requirements, pricing mechanisms, and competitive dynamics. Managing this complexity required developing what the company calls "profitable heterogeneity"—different strategies for different markets.

In the U.S., it's about Para IV challenges and complex generics. In India, it's about branded generics and market creation. In Russia, it's about relationships and local manufacturing. In emerging markets, it's about volume and distribution reach. Each market requires different capabilities, yet they must be managed under a single corporate umbrella.

The key has been developing strong local management while maintaining global standards, especially in quality and compliance. This tension—between local autonomy and global control—remains one of Dr. Reddy's biggest challenges.

The Biosimilars Bet: First-Mover Advantage

Dr. Reddy's bet on biosimilars in 2000—when the regulatory pathway didn't even exist—exemplifies the company's approach to strategic risk. By moving early, Dr. Reddy's established capabilities that would take competitors years to replicate.

But first-mover advantage in biosimilars came with costs. Dr. Reddy's had to educate regulators, doctors, and patients about biosimilars. They had to develop clinical trial protocols from scratch. They had to fight legal battles over interchangeability. Much of this investment benefited the entire industry, not just Dr. Reddy's.

The lesson: being first in a new category requires not just developing products but creating entire ecosystems. It's expensive, risky, and the benefits often accrue to fast followers. Yet for Dr. Reddy's, the biosimilars bet established them as innovation leaders, not just generic copycats.

Capital Allocation and Funding Innovation

Dr. Reddy's approach to funding innovation has been creative by necessity. The ICICI Venture partnership for Para IV challenges essentially created a venture capital model within pharmaceuticals—sharing risks and rewards with financial partners.

The company's R&D spending—typically 7-9% of revenues—is high for a generic company but low for an innovator. This forced Dr. Reddy's to be extremely selective about R&D investments, focusing on areas where they had unique advantages: diseases prevalent in India, complex generics with limited competition, and biosimilars for emerging markets.

Corporate Social Responsibility as Strategy

What's remarkable about Dr. Reddy's CSR approach is how integrated it is with business strategy. The Dr. Reddy's Foundation, established in 1996, doesn't just donate money—it runs schools, operates skill development centers, and provides healthcare in underserved areas.

This isn't just altruism. These programs create future employees, build government relationships, and establish brand loyalty in communities. When Dr. Reddy's won the Betapharm acquisition despite not being the highest bidder, it was their CSR commitment that tipped the scales.

The Unfinished Playbook

Perhaps the most important lesson from Dr. Reddy's is that the playbook is never complete. Strategies that worked in the 1990s—like entering Russia early—became liabilities in the 2000s. Capabilities that were differentiators—like low-cost manufacturing—became commodities.

The company's current challenges—commoditization of generics, biosimilar competition, regulatory scrutiny—require new strategies. The joint venture with Nestlé represents one attempt to move beyond traditional pharmaceuticals into nutrition and wellness. Digital therapeutics represent another.

The meta-lesson might be this: in rapidly evolving industries, the most important capability isn't executing a fixed strategy but continuously evolving the strategy itself. Dr. Reddy's has reinvented itself at least four times—from API supplier to generic manufacturer to biosimilar pioneer to integrated pharmaceutical company. The question is whether it can reinvent itself again for the digital health era.

IX. Analysis & Investment Case

Standing in 2024, how should an investor evaluate Dr. Reddy's? The company presents a fascinating study in contrasts—a emerging market champion with developed market ambitions, a generic company with innovation aspirations, a value player with premium pricing power in certain segments.

Market Position Analysis

Dr. Reddy's occupies an interesting position in the global pharmaceutical landscape. It's not among the top 20 global pharma companies by revenue, yet it's one of the most important players in generic drugs and biosimilars. In India, it competes with Sun Pharma (larger but more troubled), Cipla (similar size but different focus), and Lupin (smaller but more US-focused).

Globally, Dr. Reddy's competes with Israeli giant Teva (the world's largest generic company but heavily indebted), Mylan/Viatris (larger but struggling with integration), and increasingly with Chinese companies like Hengrui Medicine and Jiangsu Hansoh. Each competitor has different strengths—Teva's scale, Mylan's US presence, Chinese companies' cost advantages—but Dr. Reddy's combination of emerging market strength and developed market presence is relatively unique.

Financial Metrics Deep Dive

The numbers tell a complex story. Revenue has grown from $1 billion in 2006 to over $3 billion in 2024—impressive, but growth has slowed to single digits. Operating margins hover around 20%, healthy for a generic company but below the 25-30% Dr. Reddy's achieved in its best years.

R&D intensity at 7-9% of sales is a strategic choice—too high to be a pure generic player, too low to be a true innovator. This "stuck in the middle" position is both a weakness and potentially a strength if Dr. Reddy's can successfully bridge the generic-innovative divide.

Return on invested capital (ROIC) around 15% is respectable but not spectacular. The Betapharm write-down significantly impacted historical returns, and continued investment in biosimilars and complex generics requires patience from investors.

The Bull Case

The optimistic view starts with biosimilars. Dr. Reddy's early entry and established capabilities position it well for a market expected to reach $100 billion by 2030. With several biosimilars in late-stage development and partnerships with companies like Merck KGaA, Dr. Reddy's could capture significant value as biological drugs worth $200 billion lose patent protection.

Emerging markets represent another growth driver. Dr. Reddy's strong presence in India, Russia, and China positions it to benefit from growing healthcare spending in these markets. Unlike pure developed market players, Dr. Reddy's understands these markets' unique dynamics—price sensitivity, distribution challenges, regulatory quirks.

The integrated model—from APIs to finished dosages—provides competitive advantages in supply chain resilience and cost control. When COVID disrupted global supply chains, Dr. Reddy's vertical integration allowed it to maintain production when competitors couldn't source raw materials.

The Nestlé joint venture opens entirely new categories. Nutraceuticals and medical nutrition are growing faster than traditional pharmaceuticals, with better margins and less regulatory burden. If successful, this could be a template for future partnerships.

The Bear Case

Skeptics point to structural challenges in Dr. Reddy's core markets. US generic pricing continues to decline due to buyer consolidation. The top three buyers—CVS/Caremark, Express Scripts, and OptumRx—control over 80% of the market. Their purchasing power drives brutal price competition.

Regulatory risks remain elevated. Despite resolving the 2015 Warning Letter, Dr. Reddy's continues to receive FDA observations. Any major quality issue could shut down key facilities and destroy years of reputation building.

The biosimilar opportunity might be overhyped. As more companies enter biosimilars, including Big Pharma companies protecting their franchises, margins will compress. The 50% discounts Dr. Reddy's achieved with early biosimilars are unlikely to be repeated as markets mature.

Execution challenges persist. Dr. Reddy's has announced multiple strategic initiatives—digital health, specialty pharma, complex generics—but execution has been mixed. The company sometimes appears to be pursuing too many opportunities without sufficient focus.

The India Opportunity and Global Generic Dynamics

India's pharmaceutical market, growing at 10-12% annually, offers secular growth. Rising incomes, expanding insurance coverage, and increasing disease burden (especially diabetes and cardiovascular disease) create sustained demand. Dr. Reddy's strong brand and distribution network position it well to capture this growth.

But India also presents challenges. Price controls on essential medicines limit pricing power. The Jan Aushadhi scheme—government-run stores selling ultra-cheap generics—pressures margins. New digital pharmacies are disrupting traditional distribution models.

Globally, the generic drug market faces contradictory forces. Demand continues growing as populations age and more drugs lose patent protection. But supply has also expanded, with increased competition from China and continued pricing pressure in developed markets. The industry needs consolidation, but antitrust concerns limit major mergers.

Future Growth Drivers

Several factors could drive Dr. Reddy's next phase of growth:

Complex generics and 505(b)(2) products (improved versions of existing drugs) offer better margins than simple generics. Dr. Reddy's pipeline includes several such products that could generate significant value.

China represents a massive opportunity if Dr. Reddy's can navigate regulatory requirements and local competition. The company has been building presence slowly, learning from others' mistakes.

Digital therapeutics and AI-driven drug discovery could differentiate Dr. Reddy's from traditional generic competitors. Early investments in these areas are beginning to show promise.

Investment Verdict

Dr. Reddy's presents a complex investment case. It's neither a pure value play (too many uncertainties) nor a growth story (too many headwinds). Instead, it's a transformation story—a company trying to evolve from emerging market generic leader to global integrated pharmaceutical player.

For patient investors who believe in the biosimilars opportunity and emerging market healthcare growth, Dr. Reddy's offers exposure to powerful secular trends at reasonable valuations. The company trades at roughly 20x forward earnings—not cheap, but reasonable given its market positions and growth opportunities.

For skeptics worried about generic drug pricing, regulatory risks, and execution challenges, Dr. Reddy's might be a value trap—seemingly cheap but facing structural challenges that will compress returns.

The key question isn't whether Dr. Reddy's is a good company—it clearly is. The question is whether it can successfully navigate the transition from its historical model (affordable generics for emerging markets) to its aspired future (innovative products for global markets). That transformation is far from complete, making Dr. Reddy's either an opportunity or a risk, depending on your faith in management's ability to execute.

X. Epilogue & Reflections

Forty years after Kallam Anji Reddy mortgaged his house to start a small API factory in Bollaram, his company stands as one of India's pharmaceutical giants. The journey from that first $160,000 investment to today's $12 billion market capitalization is more than a business success story—it's a meditation on innovation, ambition, and the complex ethics of global healthcare.

Continuing the Innovation Legacy

As Dr. Reddy's celebrates #40YearsOfDrReddys in 2024, the company faces a paradox. It has achieved what seemed impossible in 1984—becoming a respected global pharmaceutical player—yet the original mission of making medicines affordable remains frustratingly incomplete. Drugs are still too expensive for billions of people. The diseases of poverty remain neglected. The innovation that could transform global health remains locked behind patents and profits.

Dr. Reddy's response has been to expand its definition of innovation. It's no longer just about making cheaper copies of Western drugs. It's about developing new delivery mechanisms that improve patient compliance. It's about creating digital tools that enhance treatment outcomes. It's about nutritional interventions that prevent disease rather than just treating it.

From Affordable Generics to Value Creation

The evolution from affordable generics to innovation-driven growth represents a fundamental shift in Dr. Reddy's identity. The company that once defined itself in opposition to Big Pharma—making their expensive drugs affordable—now partners with those same companies on biosimilar development and licensed products.

This isn't selling out; it's growing up. The pharmaceutical industry's economics are brutal. Developing a new drug costs over $1 billion and takes 10-15 years. Even biosimilars require $100-200 million investments. Dr. Reddy's has learned that to play at the highest levels, you need Big Pharma's resources, even if you don't share all their values.

Key Surprises and Counterintuitive Insights

Several aspects of Dr. Reddy's story defy conventional wisdom:

First, being from an emerging market was often an advantage, not a handicap. Dr. Reddy's understood price-sensitive markets, resource-constrained healthcare systems, and the needs of poor patients in ways Western companies never could.

Second, regulatory arbitrage—exploiting differences between Indian and Western regulations—was a temporary advantage at best. Long-term success required meeting the highest global standards, not circumventing them.

Third, corporate social responsibility wasn't charity—it was strategy. Dr. Reddy's CSR initiatives created capabilities, relationships, and reputation that translated into business advantages.

Fourth, failure (like Betapharm) could be more valuable than success if the lessons were properly absorbed. Dr. Reddy's post-Betapharm acquisition strategy has been far more successful precisely because of that expensive education.

What Would Success Look Like?

Looking ahead to the next decade, what would success look like for Dr. Reddy's? Financial metrics—reaching $5 billion in revenue, 25% operating margins, top 15 global pharma company—are important but insufficient.

True success would mean Dr. Reddy's becomes the bridge between innovation and access, proving that you can develop cutting-edge medicines while keeping them affordable. It would mean their biosimilars make cancer treatment accessible in Africa, their digital therapeutics transform diabetes management in India, their partnerships bring nutrition to malnourished children globally.

Success would also mean institutional transformation—becoming a company that attracts the world's best scientists to Hyderabad, that partners with leading universities on breakthrough research, that other emerging market companies study and emulate.

The Unfinished Mission

Perhaps the most profound aspect of Dr. Reddy's story is how it illuminates healthcare's fundamental contradictions. The same market forces that incentivize innovation also restrict access. The patents that reward research also prevent treatment. The regulations that ensure safety also delay availability.

Dr. Reddy's has spent forty years navigating these contradictions, sometimes successfully, sometimes not. The company has made medicines more affordable for millions, but billions still lack access. It has challenged Big Pharma's monopolies while becoming increasingly integrated into their ecosystem. It has pursued profit while maintaining social purpose.

As Satish Reddy said in a recent interview, "My father's vision was to bring new molecules into the country at a price the common man can afford. We've made progress, but the vision remains as relevant and challenging today as it was in 1973."

The story of Dr. Reddy's is ultimately about this unfinished mission—the gap between what is and what should be in global healthcare. It's about a company from the developing world that refused to accept that advanced medicines were only for the developed world. It's about scientists and entrepreneurs who believed that innovation and affordability weren't mutually exclusive.

Whether Dr. Reddy's succeeds in its transformation from generic challenger to innovative leader matters beyond shareholders and employees. It matters because the company represents a different model of pharmaceutical development—one rooted in emerging markets, focused on affordability, yet capable of world-class innovation.

The moon landing that inspired young Kallam Anji Reddy in 1969 proved that seemingly impossible goals could be achieved with sufficient will and resources. Fifty-five years later, his company continues pursuing its own moonshot: making quality healthcare accessible to all. The journey is far from over, but the trajectory—from a small factory in Bollaram to a global pharmaceutical force—suggests that impossible dreams sometimes do come true, just never quite as imagined.

The next chapter of Dr. Reddy's story will be written by a new generation of leaders facing new challenges—artificial intelligence, personalized medicine, gene therapy, global pandemics. But the core question remains unchanged: Can a company do well by doing good? Can profit and purpose coexist? Can medicines be both innovative and affordable?

Dr. Reddy's forty-year experiment in answering these questions continues. The results so far are mixed but meaningful, imperfect but important. And in a world where healthcare inequality continues to widen, where breakthrough treatments remain unaffordable for most, where the diseases of poverty remain neglected, Dr. Reddy's mission—bringing new molecules at prices the common man can afford—remains as audacious and necessary as ever.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube