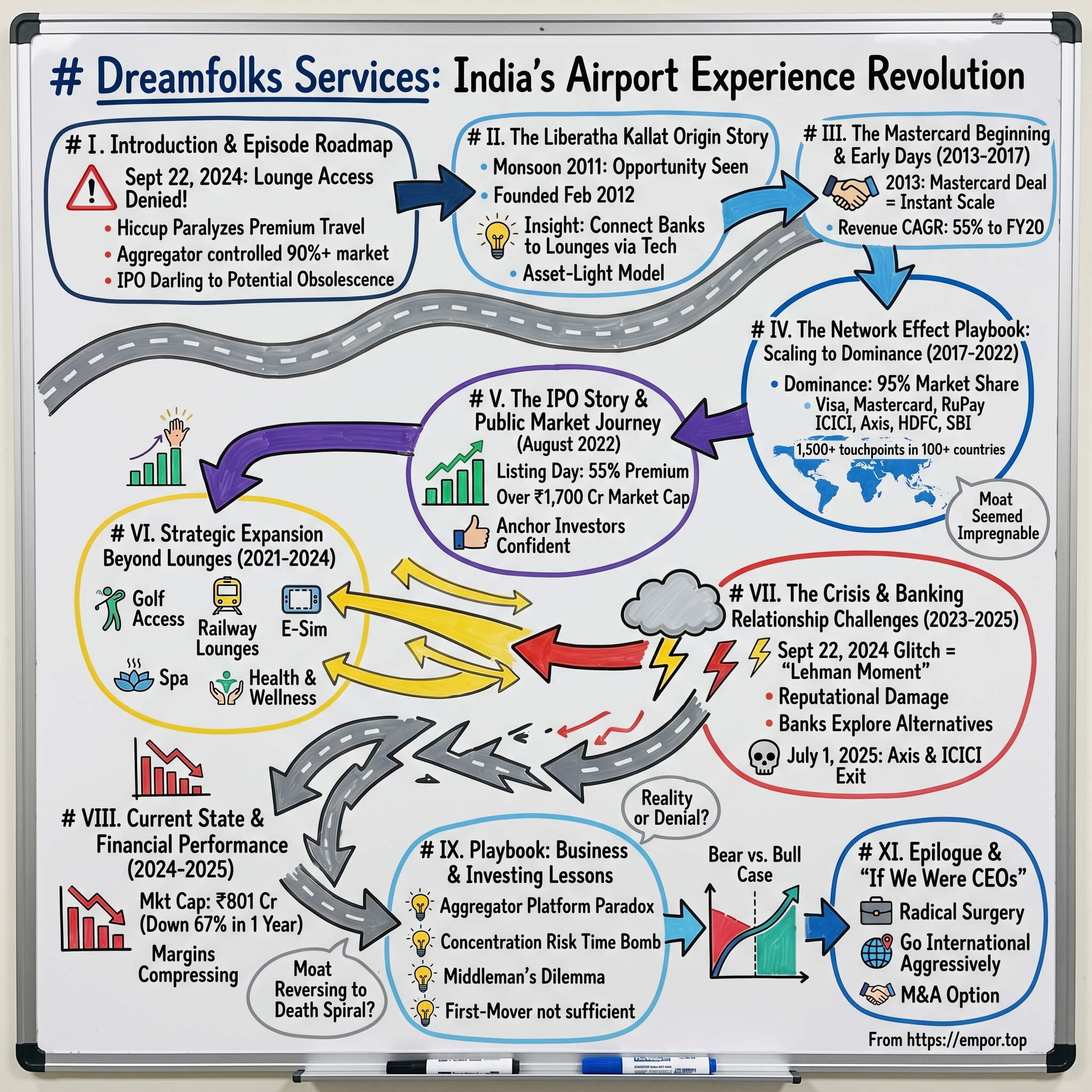

Dreamfolks Services: India's Airport Experience Revolution

I. Introduction & Episode Roadmap

Picture this: September 22, 2024. Thousands of premium credit card holders stand outside airport lounges across India, their access denied, their cards useless. The culprit? A "temporary disruption" at a company most travelers had never heard of—Dreamfolks Services. Yet this virtually invisible aggregator controlled over 90% of India's airport lounge access market, processing millions of visits annually. The disruption lasted just one day, but its aftershocks would ultimately reshape India's entire airport services ecosystem.

How does a simple technology middleman become so essential that its hiccup paralyzes premium travel experiences nationwide? And more importantly, how does that same company go from IPO darling to potential obsolescence in just three years?

This is the story of Dreamfolks Services—a company that democratized VIP airport experiences for millions of Indians, built a near-monopoly through network effects, and then watched its empire crumble as the very partners it served decided they no longer needed the middleman. It's a tale of visionary entrepreneurship, explosive growth, and the brutal reality that in platform businesses, your moat is only as strong as your relationships.

Despite posting 12% revenue growth in Q2 2025, the company faces existential threats. Major banks are cutting ties, airport operators are going direct, and the stock has crashed 67% from its peaks. Yet management insists relationships remain "strong and fully intact." Reality or denial? Let's dive into one of Indian capital markets' most dramatic rise-and-fall stories.

II. The Liberatha Kallat Origin Story

The monsoon of 2011 had just begun in Mumbai when Liberatha Peter Kallat made a decision that would transform India's airport experience. After spending nearly four years as General Manager at Plaza Premium Group—the global airport hospitality giant—she saw an opportunity that her employer couldn't, or wouldn't, pursue. India's burgeoning middle class was traveling more than ever, but airport lounges remained the exclusive domain of business and first-class passengers. The infrastructure existed, the demand was latent, but nobody had connected the dots.

Kallat founded Dreamfolks Services Ltd. in February 2012, and by March, she had already signed Mastercard as the company's first corporate client. This wasn't luck—it was the culmination of a career strategically built across hospitality's most prestigious corridors. Her journey through Pernod Ricard as Key Accounts Manager for Andhra Pradesh, stints at Novotel & HICC as Sales Manager, PepsiCo, and the Taj Group of Hotels had given her something invaluable: an understanding of both luxury service delivery and mass-market distribution.

But Kallat brought more than just experience. She held an MBA in Marketing and Computer Science from Andhra University (1995-1998), a combination that would prove prescient. While competitors saw airport lounges as a hospitality business, Kallat envisioned a technology platform—a digital bridge between banks hungry for customer perks and lounges with empty seats.

The founding insight was deceptively simple yet revolutionary: leverage an asset-light model by connecting the networks of card companies with airport service operators. No need to build lounges, hire staff, or manage food services. Just be the invisible orchestrator, the technology layer that makes everything work seamlessly. Dreamfolks would make airport services that were previously restricted to business or first-class travelers accessible to a large chunk of economy travelers.

As Kallat herself emphasizes, the company "kind of incubated the niche airport services industry". This wasn't hyperbole—before Dreamfolks, the very concept of mass-market lounge access barely existed in India. The company wasn't just entering a market; it was creating one.

III. The Mastercard Beginning & Early Days (2013-2017)

The company started its operations in 2013 by facilitating lounge access services for the consumers of Mastercard. That first Mastercard deal wasn't just a client win—it was a strategic masterstroke that would define Dreamfolks' entire playbook. Think about it: instead of pitching to dozens of banks individually, Kallat went straight to the network level. One deal, instant scale across every Mastercard-issuing bank in India.

The early days were about relentless execution and partnership building. Kallat began by negotiating and partnering with service operators like Premium Plaza, Oberoi, and other lounge companies, then took these services to banks and card companies to offer their customers. This two-sided marketplace approach created a virtuous cycle: more lounges attracted more banks, which brought more customers, which attracted more lounges.

By 2017, the foundation was set. The company's revenue had grown from Rs 98.7 crore in fiscal 2017 to eventually reaching Rs 367.04 crore by fiscal 2020—a compounded annual growth rate of 55%. But revenue was just one metric. What really mattered was market position. Dreamfolks had quietly become the essential infrastructure layer for India's airport lounge ecosystem.

The technology platform they built during these years was the real differentiator. While competitors saw lounge access as a manual, relationship-driven business, Dreamfolks automated everything: eligibility verification, real-time availability checking, payment processing, and reconciliation. The company evolved from an airport lounge aggregator to an end-to-end technology solutions provider.

The company focused on building strong tech capabilities that allowed clients to customize offerings and even design their own programs. Banks could set their own rules—which cards get access, how many visits per year, which lounges to include. Dreamfolks' platform handled all the complexity behind the scenes. For bank executives, it was magic: sign one contract, instantly offer nationwide lounge access.

IV. The Network Effect Playbook: Scaling to Dominance (2017-2022)

Between 2017 and 2022, Dreamfolks executed one of the most impressive platform scaling plays in Indian business history. The strategy was methodical: expand from Mastercard to every card network, then systematically lock up every major bank, while simultaneously achieving total coverage of India's lounge infrastructure.

The company provided services to all Card Networks operating in India including Visa, Mastercard, Diners/Discover and RuPay. Each network brought its own ecosystem of issuing banks, multiplying Dreamfolks' reach exponentially. But the real coup was the banking partnerships. Major issuers including ICICI Bank, Axis Bank, Kotak Mahindra, HDFC, and SBI Cards all came aboard, drawn by the simplicity of Dreamfolks' one-stop solution.

The numbers told the story of absolute dominance. By October 2022, the company had 100% coverage across 54 airport lounges in India and a market share of over 95% of all India-issued card-based access to domestic lounges. Let that sink in—95% market share. In most industries, 40% makes you a leader. Dreamfolks hadn't just won; it had essentially become the market.

In FY 2021-22, the company catered to 68% of overall lounge volume traffic across all lounges in Indian airports. The remaining 32%? International visitors, cash-paying customers, and airline-provided access. For Indian card-based access, Dreamfolks was essentially a monopoly.

The global expansion during this period was equally ambitious. The company established a global footprint extending to 1,500+ touchpoints in 100+ countries. This wasn't just about Indian travelers going abroad—it was about building relationships with international lounge operators that would prove valuable as India's aviation market exploded.

Platform effects were now in full swing. Lounges couldn't afford not to be on Dreamfolks because that's where all the bank customers were. Banks couldn't leave because Dreamfolks had all the lounges. New entrants faced an impossible challenge: how do you compete with someone who has 100% of supply and 95% of demand? The moat seemed impregnable.

V. The IPO Story & Public Market Journey (August 2022)

August 24, 2022. The Indian stock market was in a peculiar mood—global uncertainties loomed, but domestic consumption stories still commanded premiums. Into this environment, Dreamfolks launched its Initial Public Offering with a proposition that seemed irresistible: a profitable, asset-light, monopolistic platform riding India's aviation boom.

The IPO price band was set at ₹308-326 per share, with a lot size of 46 shares requiring a minimum retail investment of ₹14,996. The structure was telling—this was entirely an Offer for Sale (OFS), meaning no fresh capital was being raised. The company was 100% owned by promoters: Liberatha Peter Kallat and Dinesh Nagpal each held 33%, with Mukesh Yadav holding the remaining 34%.

The anchor book told a story of institutional confidence. Dreamfolks raised Rs 253 crore from anchor investors, allocating 7.76 crore shares at Rs 326 apiece to 18 investors including Societe Generale, BNP Paribas Arbitrage, Saint Capital Fund, Segantii India Mauritius, Kuber India Fund, Smallcap World Fund Inc, Aditya Birla Sun Life Mutual Fund, Sundaram Mutual Fund, Quant Mutual Fund, and PNB Metlife India Insurance Company. Smallcap World Fund emerged as the largest bidder with 28.46% of the anchor portion.

Public response was overwhelming. The IPO was subscribed 56.68 times, with QIBs bidding 70.53 times, retail investors 43.66 times, and NIIs 37.66 times. The grey market premium surged, indicating listing gains of 20-50%. Market guru Anil Singhvi predicted shares would list in the Rs 475-500 range against the issue price of Rs 326.

September 6, 2022: Listing day delivered on the hype. Shares debuted at a 55% premium, propelling the market capitalization to over ₹1,700 crore. The IPO diluted 33% of the promoters' stakes, but at these valuations, everyone was celebrating. Kallat's paper wealth alone exceeded ₹550 crore.

The market capitalization at IPO stood at ₹1,703.35 crore. Analysts were bullish—here was a company with 95% market share, an asset-light model, network effects, and exposure to India's booming aviation sector. What could possibly go wrong?

VI. Strategic Expansion Beyond Lounges (2021-2024)

Even before the IPO, Kallat understood a fundamental truth about platform businesses: dominance in one vertical creates opportunities in adjacent ones. If you control airport lounge access, why not airport transfers? If travelers trust you with one premium experience, why not others?

The expansion began strategically. June 2021 marked a significant pivot with the Go First partnership for departure lounge services, moving beyond just facilitating access to actually managing service delivery. September 2022 saw an ambitious move into railway lounges across eight stations—if Dreamfolks could democratize airport lounges, why not train stations?

December 2022 brought perhaps the most intriguing partnership: a strategic alliance with Vidsur Golf providing access to 250 golf courses. The logic was compelling—the same affluent customers using airport lounges were likely golf enthusiasts. One platform, multiple lifestyle services. March 2024's partnership with Healthians added health and wellness to the mix, further diversifying the platform's offerings.

Services expanded to include Visa Services, Airport Transfer, Meet and Assist, Lounge Access, E-Sim, F&B, Spa, Transit Hotels/Nap Rooms, and more. Each addition leveraged the same core asset: relationships with banks and their premium customers. The diversification strategy seemed to be working—by Q2FY25, services other than India airport lounges contributed 6.7% to revenue, up from 5.5% in Q2FY24.

But there was a hidden vulnerability in this expansion. While Dreamfolks was broadening its service portfolio, its core business—airport lounge aggregation—remained overwhelmingly dominant, contributing over 93% of revenues. The company was diversifying, but not fast enough. And storm clouds were gathering over that core business.

The operational metrics during this period painted a picture of robust growth. The startup reached about 10 million end users per annum through its B2B clients. Customer acquisition costs remained near zero—banks did all the marketing. It seemed like the perfect business model: grow horizontally into new services while the core vertical printed money.

VII. The Crisis & Banking Relationship Challenges (2023-2025)

September 22, 2024. What started as a technical glitch would become Dreamfolks' Lehman moment. A "temporary disruption in services" left thousands of bank customers unable to access lounges across India. For twenty-four hours, premium cardholders stood outside lounge doors like "rejected contestants on a reality show," as one observer put it. The technical issue was resolved the next day, but the reputational damage was irreversible.

Adani Airports issued a damning statement: "Passengers at airports across India have been experiencing disruptions in lounge access. This is due to the unexpected suspension of services by Dreamfolks Services Ltd, a lounge access provider partnered with several banks, in violation of its service agreements with the affected airports". The gloves were off. Travel Food Services, managing lounges in Kolkata and Chennai, reportedly threatened legal action.

The incident triggered a cascade of strategic reassessments. Though the issue was resolved the next day, it prompted banks and card networks to explore other alternatives. Why, they wondered, were they paying hefty commissions to a middleman who could bring their premium services to a grinding halt? American Express transitioned to Adani Digital for lounge access at Adani-operated airports. Others began similar discussions.

By early 2025, the exodus began. Reports emerged that ICICI Bank, Axis Bank, and Mastercard were considering direct partnerships with airport lounge operators, potentially bypassing Dreamfolks entirely. The fear was palpable—these weren't minor clients but the backbone of Dreamfolks' business model.

July 1, 2025 marked a watershed. Axis Bank credit cards no longer supported domestic airport lounge access via Dreamfolks, with certain programs of both Axis Bank and ICICI Bank closed effective July 01, 2025. The wildly popular Axis Bank Atlas Credit Card, one of India's largest travel cards by numbers, was among the products withdrawn. Dreamfolks acknowledged the impact would "likely be material in nature".

Management's response was a masterclass in corporate doublespeak. While programs were being terminated, they insisted "contracts with above clients are still valid". They announced plans to reduce airport revenue concentration from 93% while simultaneously claiming to have added 30 enterprise clients. But the market wasn't buying it. The stock fell 19.8% in just three sessions following the July announcements.

VIII. Current State & Financial Performance (2024-2025)

The Q2 2025 numbers tell a story of resilience undermined by profitability challenges. Revenue grew 12% year-over-year, reaching ₹3.18 billion for the quarter. For the half-year, H1FY25 showed revenue of Rs 6,377 million (up 16.2%), gross profit of Rs 768 million (up 21%), EBITDA of Rs 513 million (up 10.6%), and PAT of Rs 332 million (up 8.3%). On paper, still growing.

But dig deeper and cracks emerge. Net income for Q2 fell 9.8% to ₹161 million, with margins compressing to just 5.1%. Revenue missed analysts' projections by 6.7%, while EPS came in 19% below estimates. The market's verdict has been brutal: market capitalization stands at ₹801 crore, down 67.2% in one year. From IPO valuations of ₹1,703 crore to ₹801 crore—over ₹900 crore in market value evaporated.

The company maintains it's still the dominant player with no direct competition in India. Network expansion continues with lounges increasing from 70 to 74. But these incremental wins pale against the structural threats. When your biggest customers are actively planning to eliminate you from their value chain, adding four lounges won't save you.

As Liberatha Kallat stated in the H1FY25 results: "We achieved double-digit growth on Revenue and Gross Profit... This financial performance is the testament to the strategic initiatives we have undertaken over the past few quarters". Yet the strategic initiatives she references—diversification into golf, railways, and highways—still represent less than 7% of revenues. The core business that generates 93% of revenue faces existential threats.

Operational metrics paint a picture of a business model under siege. Customer acquisition costs remain low, but customer retention has become the challenge. The company's moat—its network effect—only works if both sides of the marketplace remain committed. Once banks start leaving, the virtuous cycle reverses into a death spiral.

IX. Playbook: Business & Investing Lessons

The Aggregator Platform Paradox

Dreamfolks exemplifies both the promise and peril of aggregator platforms in emerging markets. The promise: explosive growth, network effects, asset-light scaling, and winner-take-all dynamics. The peril: you're only as strong as your weakest relationship, and when those relationships are with powerful banks and airport operators, you're perpetually vulnerable.

The company's rise demonstrates that in fragmented markets with information asymmetry, aggregators can create immense value quickly. But its potential fall reveals an uncomfortable truth: when your entire business model depends on being a middleman, your customers will eventually wonder why they need the middle.

First-Mover Advantage: Necessary but Not Sufficient

Dreamfolks claims to be a dominant player with no direct competition, having essentially created the market. But first-mover advantage in platform businesses only matters if you can maintain switching costs. Once banks realized they could go direct to lounges—or that airport operators would gladly facilitate direct relationships—Dreamfolks' first-mover advantage evaporated.

The Concentration Risk Time Bomb

With major banks contributing the bulk of revenues and airport lounges representing 93% of the business, Dreamfolks violated the cardinal rule of platform businesses: diversify before you're forced to. The company's recent scramble into golf, railways, and highways feels reactive rather than strategic—too little, too late.

Technology Platform vs. Service Provider: The Identity Crisis

Dreamfolks positioned itself as a technology platform but was fundamentally a service intermediary. True technology platforms create tools others can't replicate easily. Dreamfolks' technology—while sophisticated—wasn't defensible. Any competent IT services company could build lounge access verification systems. The real value was in the relationships, and relationships can be disintermediated.

The Middleman's Dilemma

Perhaps the most important lesson: in critical infrastructure, being a middleman is inherently unstable. When your service becomes essential (as Dreamfolks' did), your partners start viewing your margin as their opportunity. The very success that made Dreamfolks dominant also made it a target for disintermediation.

X. Analysis & Bear vs. Bull Case

Bull Case: The Phoenix Scenario

Despite the challenges, bulls point to several factors suggesting Dreamfolks could emerge stronger:

Revenue is forecast to grow 15% annually over the next three years, above the 7.4% forecast for the broader Asia Infrastructure industry. India's aviation sector continues its explosive growth—passenger traffic is expected to double by 2030. Someone needs to manage the complexity of airport services, and Dreamfolks has the experience and infrastructure.

The diversification strategy, while nascent, shows promise. Golf course access, railway lounges, and highway rest stops all leverage the same core competency: aggregating lifestyle services for affluent Indians. If even two of these bets pay off, they could offset airport lounge losses.

International expansion remains underpenetrated. With operations in 121 countries but most revenue from India, there's significant room for geographic growth. The company's technology platform could be white-labeled to international banks or travel providers.

Most importantly, completely disintermediating Dreamfolks might prove harder than banks anticipate. Managing relationships with dozens of lounge operators, handling technology integration, processing payments, managing customer service—it's operationally complex. Banks might discover that Dreamfolks' commission is a bargain compared to building capabilities in-house.

Bear Case: The Disruption Scenario

Bears see a business model in terminal decline. Banks increasingly prefer dealing directly with lounge operators, cutting out middleman fees. Airport operators like Adani and GMR are launching their own platforms. The aggregator model that made Dreamfolks successful is becoming obsolete.

The July 2025 client losses aren't anomalies—they're the beginning of an avalanche. Once ICICI and Axis fully exit, other banks will follow. ICICI Bank and Axis Bank are among India's top 4 card issuers, and their departure creates a momentum shift that's hard to reverse.

Margin compression is accelerating. Even with revenue growth, profitability is declining. This suggests Dreamfolks is having to offer deeper discounts to retain clients—a classic sign of weakening bargaining power. In platform businesses, once margins start compressing, they rarely recover.

The diversification efforts are too small to matter. At less than 7% of revenue, non-airport services would need to grow 15x just to replace the airport lounge business if it disappears. That's not diversification; it's desperation.

Finally, trust, once broken, is hard to rebuild. The September 2024 service disruption didn't just inconvenience customers—it gave banks and airports the excuse they needed to pursue alternatives they were already considering. In enterprise relationships, reputation damage is often permanent.

XI. Epilogue & "If We Were CEOs"

If we were running Dreamfolks today, the playbook would be radical surgery, not incremental change.

First, accept reality: the domestic airport lounge aggregation business is dying. Instead of fighting to preserve it, use remaining cash flows to fund an aggressive pivot. The company has roughly 18-24 months before the core business becomes unviable.

Second, go international aggressively. India's model of bank-provided lounge access is increasingly common in Southeast Asia, Middle East, and Latin America. Dreamfolks should be the Stripe of airport services—the infrastructure layer that powers lounge access globally. License the technology, franchise the model, become the arms dealer rather than fighting in the war.

Third, embrace the platform identity fully. Stop being a service provider and become a true technology platform. Build APIs that any bank, fintech, or travel app can integrate. Charge for technology, not for transactions. Make switching costs real through deep technical integration.

Fourth, consider strategic M&A. With the stock down 67%, Dreamfolks is more acquisition target than acquirer. But sometimes being acquired is the best outcome. A global travel giant like Booking.com or Expedia, or even a payments player like Mastercard (coming full circle), might value Dreamfolks' infrastructure and relationships.

Finally, the nuclear option: shut down the airport business entirely and redeploy capital into the golf/lifestyle vertical where competition is minimal and margins are higher. It's better to be a living dog than a dead lion.

The Dreamfolks story isn't over, but it's at an inflection point. Founded with a vision to democratize premium travel experiences, the company succeeded beyond imagination—perhaps too well. In making airport lounges accessible to millions, Dreamfolks made itself so essential that partners decided they didn't need the orchestrator anymore.

Whether Dreamfolks survives this crisis will depend on management's ability to recognize that the business model that brought them to the dance won't take them home. The question isn't whether Dreamfolks can preserve its airport lounge dominance—it's whether it can reinvent itself before that dominance becomes worthless.

For investors, Dreamfolks represents a classic "fallen angel" situation. At ₹800 crore market cap with ₹332 million in half-yearly profits, it's either incredibly cheap or a value trap. The answer depends on whether you believe in management's ability to execute one of Indian corporate history's most challenging pivots.

The dream of democratizing premium travel experiences was noble and brilliantly executed. Whether that dream survives in its current form, or morphs into something entirely different, will be determined in the next 12-18 months. For Liberatha Kallat and her team, the real test of entrepreneurship isn't building a monopoly—it's surviving its dissolution.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube