DOMS Industries: From Pencils to Portfolios - The Story of India's Stationery Giant

I. Introduction & Episode Roadmap

Picture this: It's December 2023, and the Indian stock market is witnessing something extraordinary. A stationery company—yes, a company that makes pencils and erasers—is seeing its IPO oversubscribed 92 times. Retail investors are frantically refreshing their screens, trying to grab a piece of DOMS Industries. The grey market premium has soared to 63% above the issue price. For a business selling products that cost less than a cup of chai, the frenzy seems almost surreal.

But here's what makes this story fascinating: DOMS Industries Limited isn't just another stationery company. It's the second-largest player in India's branded stationery and art products market, commanding a 29% market share in pencils and 30% in mathematical instrument boxes as of FY23. The company, primarily engaged in designing, developing, manufacturing, and selling these everyday products under its flagship DOMS brand, has somehow transformed from a small partnership firm founded in the 1970s into a ₹14,000+ crore enterprise.

How does a company selling 50-paise pencils build such massive value? How did two Gujarati entrepreneurs, starting with basic manufacturing in the license raj era, create a brand that competes with global giants? And perhaps most intriguingly, why did an Italian multinational pay millions to partner with them?

This is a story about more than just pencils and profits. It's about timing markets perfectly, building distribution moats in a fragmented industry, navigating family business dynamics, and understanding when to bring in global partners versus going it alone. We'll explore how DOMS rode India's education boom, why they chose to consolidate multiple partnership firms, how they convinced FILA—the Italian giant behind Giotto and Canson—to not just partner but take a majority stake, and what their recent IPO success tells us about Indian consumer brands.

Over the next few hours, we'll dissect the business model evolution from contract manufacturing to brand building, examine the strategic pivots that mattered, and understand why institutional investors are willing to pay 70+ times earnings for a stationery company. We'll also explore the bear case—because at these valuations, there's plenty to worry about.

This isn't just a business story; it's a masterclass in building brands in emerging markets, a case study in strategic partnerships, and a window into India's consumption story through the unlikely lens of pencils and erasers. Whether you're a founder thinking about distribution strategy, an investor evaluating consumer brands, or simply curious about how everyday products become empire-builders, there are lessons here that extend far beyond stationery.

Buckle up as we trace the journey from humble beginnings in 1970s Gujarat to today's public market darling, uncovering the decisions, partnerships, and market forces that transformed DOMS from a local manufacturer into India's stationery giant.

II. The Origins: Partnership Firms and Family Foundations (1970s–2005)

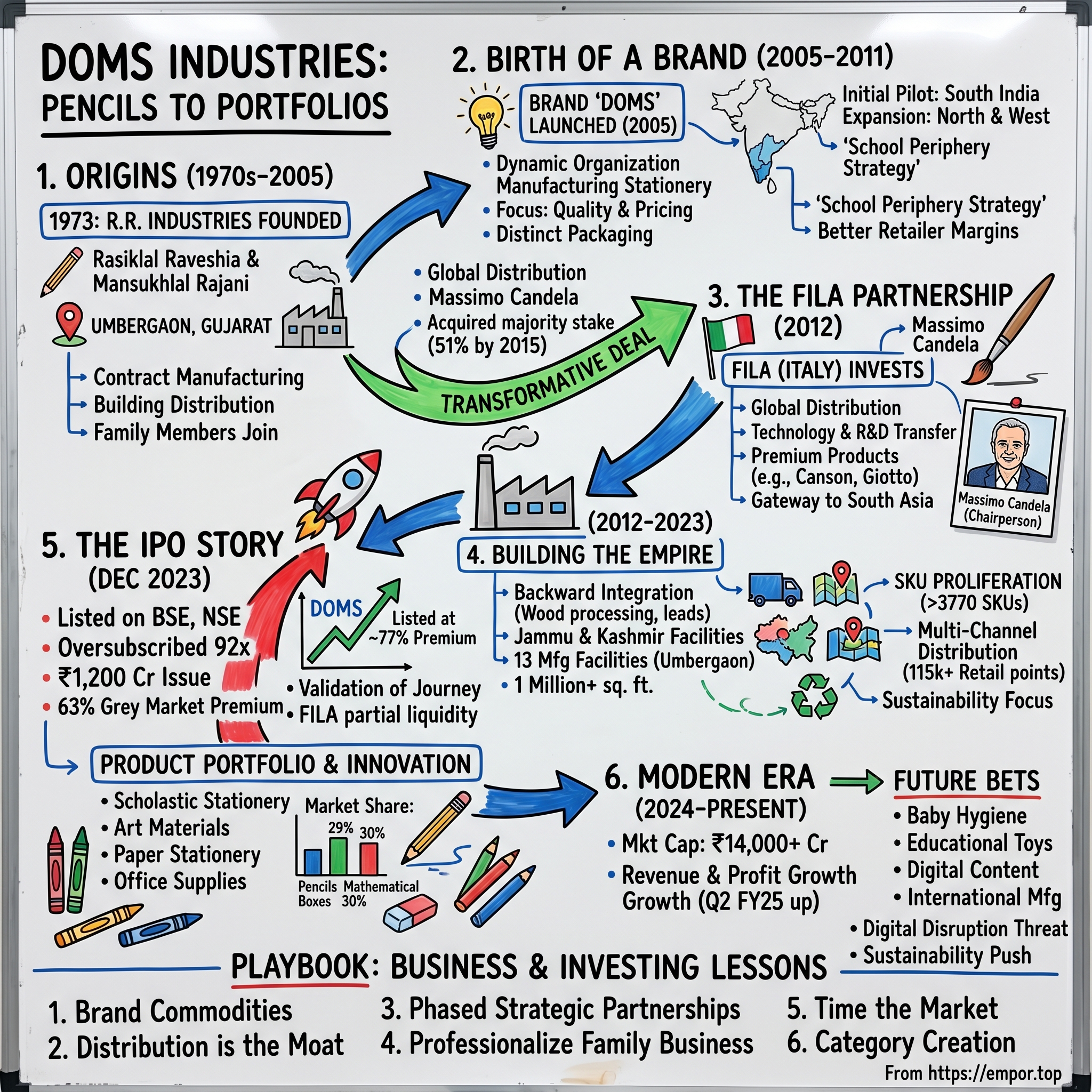

The year is 1973. India is still finding its economic feet, barely two years after the Bangladesh Liberation War and in the midst of Indira Gandhi's socialist policies. In this environment of licenses, permits, and controlled capitalism, two Gujarati entrepreneurs—Rasiklal Amritlal Raveshia and Mansukhlal Jamnadas Rajani—see an opportunity that others have overlooked: pencils.

Why pencils? The answer lay in post-independence India's most ambitious project—universal education. The government was building schools at breakneck speed, literacy campaigns were spreading across villages, and millions of children were entering classrooms for the first time in their families' histories. Each child needed basic tools: a slate, chalk, and eventually, pencils. The demand was astronomical, but the supply was dominated by imports and a handful of large players. The market was ripe for disruption.

Rasikbhai and Mansukhlal weren't industrialists with deep pockets. They were traders who understood distribution, knew the pulse of small retailers, and most importantly, recognized that in a price-sensitive market like India, even saving a few paise per pencil could mean the difference between a child getting education supplies or not. They founded R.R. Industries as a partnership firm, setting up basic manufacturing for pencils and crayons. The initial years were brutal. Operating from a small shed in Umbergaon—a nondescript town in Gujarat that would later become famous as the filming location for TV serials Ramayana and Mahabharat—the partners faced every conceivable challenge. Rasiklal had chosen to relocate from Mumbai to the then little-known town of Umbergaon, which became famous after two mythological serials, Ramayana and Mahabharat, were filmed nearby. The Gujarat State Finance Corporation provided 100% financing under a special scheme for budding entrepreneurs, but money was just the beginning of their problems.

The license raj meant navigating a byzantine system of permissions. Raw materials were controlled, distribution was restricted, and every expansion required government approval. But Rasikbhai and Mansukhlal had an advantage—they understood the pulse of small retailers and the economics of tier-2 and tier-3 India. Raveshia got his friend Mansukhlal Rajani who had a small engineering workshop, to provide material to a leading stationery company.

What's fascinating about this period is how the founders approached the business. They weren't trying to build a brand—brands were luxury in 1970s India. They were contract manufacturers, supplying to bigger companies, learning the trade, understanding quality standards, and most importantly, building relationships across the supply chain. R.R. Industries, RR Group's flagship company was formed in the year 1973 for manufacturing and sale of pencils and crayons by Late Shri Rasikbhai A. Raveshia and Late Shri Mansukhlal Rajani.

As the business grew through the 1980s and 1990s, family dynamics became central to the story. Raveshia's younger sibling Harshad and Rajani's younger brother, Suresh Rajani were roped in soon after the project took off. This wasn't just about adding manpower—it was about building a succession pipeline, ensuring that the next generation would be ready when their time came.

The children of the founders began joining the business in the late 1990s and early 2000s. Santosh Raveshia joined R.R. Industries in 2000 and has been its partner since 2002, while Sanjay Rajani joined R.R. Industries in 1985 and has been its partner since 2011. Each family member took on specific responsibilities—one focused on production, another on procurement, someone else on distribution. This wasn't nepotism; it was strategic positioning of trusted lieutenants who had grown up breathing the business.

By 2005, the partnership had evolved into something more complex. Subsequently, in 2005, another Partnership Firm S. Tech Industries was founded by certain members of the Promoter Group, to undertake the business of manufacturing and sale of polymer based scholastic stationery. This second partnership firm represented a strategic pivot—moving beyond wood-based products into polymer-based stationery, anticipating where the market was heading.

The proliferation of partnership firms—R.R. Industries, S-Tech Industries, and others—might seem chaotic, but it served multiple purposes. It allowed different family branches to have ownership stakes, distributed risk across entities, and perhaps most importantly, kept the business nimble in an era when corporate structures were heavily regulated.

What's remarkable about this three-decade journey from 1973 to 2005 is what didn't happen. There were no venture capital rounds, no professional CEOs brought in, no grand strategic pivots. Just steady, patient building of manufacturing capabilities, distribution relationships, and family consensus. The foundations being laid would prove crucial for what came next—the birth of a brand that would change everything.

III. Birth of a Brand: The DOMS Launch (2005–2011)

The conference room in Umbergaon was tense. It was 2005, and the second generation of the Raveshia and Rajani families faced a decision that would define their future. For over three decades, they had been successful contract manufacturers, but the writing was on the wall—literally. Chinese imports were flooding the market, margins in contract manufacturing were shrinking, and retailers were increasingly asking for branded products. The choice was stark: remain invisible manufacturers or take the leap into brand building.

The consolidation began with incorporating Writefine Products Private Limited in October 2006. The company was originally incorporated as Writefine Products Private Limited as a Private Limited Company, dated October 24, 2006, and the name was later changed to DOMS Industries Private Limited on April 21, 2017. This wasn't just a legal restructuring—it was about bringing multiple partnership firms under one umbrella, creating operational synergies, and preparing for a brand launch that would require significant investment.

The name DOMS itself tells a story. DOMS originally stood for "Dynamic Organization Manufacturing Stationery". In a market dominated by foreign-sounding brands and century-old legacies, DOMS was deliberately modern, aspirational, yet accessible. The founders understood something crucial: Indian parents, especially in tier-2 and tier-3 cities, wanted quality products for their children but at prices that didn't break the bank.

Santosh Raveshia, who had joined the family business in 2000, emerged as the driving force behind the brand strategy. Santosh says: "I have been running DOMS more like a start-up–barring the negatives often associated with them. Our focus has been getting the product and its pricing right. Owing to limited finances, we never spent too much money on marketing or advertising. We just wanted to create a product that always had something different than its peers."

The initial brand launch strategy was counterintuitive. Instead of starting in their home market of Gujarat or the massive markets of North India, DOMS was launched in the South with just pencils, erasers and sharpeners. This was tried on a pilot basis in South India. The success of these products saw expansion across categories under the DOMS brand. Why South India? The market was more organized, consumers were willing to pay for quality, and crucially, it was far from the strongholds of established competitors.

Building a brand in the stationery market presented unique challenges. Unlike FMCG products with high advertising budgets, stationery purchases were largely impulse-driven, made by children influencing parents at small shops near schools. The company couldn't afford TV commercials or celebrity endorsements. Instead, they focused on three things: distinctive packaging, consistent quality, and aggressive pricing.

The packaging innovation was subtle but effective. While competitors used standard designs that hadn't changed in decades, DOMS introduced vibrant colors, cartoon characters, and child-friendly graphics. Products were designed to stand out on crowded shelves, to catch a child's eye from across a cluttered stationery shop. Every SKU was thought through—from the grip on pencils to the smell of erasers.

But the real innovation was in distribution. After gaining acceptance in the South, DOMS expanded its presence in Northern and Western India, its biggest markets today. While 35% of its sales come from the North, 25% comes from the West, while the South and the East contribute 20% each. Today, with over 4,500 channel partners and over 10,000 retail points, the brand has established its grip firmly.

The company developed what they called the "school periphery strategy"—ensuring presence in every small shop within 500 meters of schools. They offered better margins to retailers than established players, faster replenishment, and crucially, sale-or-return policies that reduced retailer risk. This wasn't sustainable long-term, but it was necessary to break the inertia of retailers who had been selling the same brands for decades.

The competition wasn't sleeping. Hindustan Pencils (makers of Nataraj and Apsara) had been around since 1958. Camlin had history dating back to 1931. These companies had brand recall that DOMS couldn't match. But DOMS had advantages too—no legacy infrastructure to maintain, no unionized workforce to manage, and most importantly, hunger that established players had perhaps lost.

By 2011, just six years after the brand launch, DOMS was clocking revenues that caught the industry's attention. The Umbergaon-based brand grew at over 20 percent CAGR since 2013, and with demand for school stationery going up, the company achieved Rs 1,000 crore revenues in FY 2023. The brand had moved from obscurity to becoming a serious player, but the founders knew they needed something more to break into the big league—they needed a global partner.

The consolidation of partnership firms, the brand building exercise, and the distribution expansion had prepared DOMS for its next chapter. In order to streamline operations and achieve integration of businesses, the Company acquired the business of these partnership firms. The stage was set for what would become the most transformative decision in the company's history—a partnership that would bring Italian style to Indian classrooms.

IV. The FILA Partnership: Going Global (2012)

The email from Italy landed in Santosh Raveshia's inbox in late 2011. F.I.L.A.—Fabbrica Italiana Lapis ed Affini S.p.A—wanted to meet. For a company that had been making pencils in Florence since 1920, makers of the legendary Giotto brand, to reach out to a six-year-old Indian brand was unexpected. What Santosh didn't know was that Massimo Candela, CEO of FILA since 1992, had been studying the Indian market for years, and DOMS had caught his attention for a very specific reason.

FILA wasn't just any stationery company. F.I.L.A., founded in Florence in 1920 and managed since 1956 by the Candela family, is a highly consolidated, dynamic and innovative Italian industrial enterprise. The company, with revenue of Euro 653.5 million in 2021, had achieved a series of strategic acquisitions, including the Italian Adica Pongo, the US Dixon Ticonderoga Company and Pacon Group, the German LYRA, the Mexican Lapiceria Mexicana, the English Daler-Rowney Lukas and the French Canson.

The Italian company had been on an acquisition spree, building a global portfolio of heritage brands. But India presented a unique challenge. Unlike developed markets where FILA could simply acquire and integrate established brands, India's stationery market was fragmented, price-sensitive, and required deep distribution capabilities that no foreign company could build quickly. FILA needed a partner, not an acquisition target.

From DOMS's perspective, the timing was perfect and precarious. Perfect because they had proven their execution capabilities and built a recognized brand. Precarious because breaking through to the next level—competing with MNCs, expanding internationally, developing premium products—required capital and technology they didn't have.

The initial negotiations were fascinating in their cultural complexity. The Italians, with their emphasis on design and heritage, meeting the Gujarati entrepreneurs who had built their business on value and efficiency. Massimo Candela flew to Umbergaon, touring the facilities that, while impressive by Indian standards, were a far cry from FILA's European operations. What impressed him wasn't the infrastructure but the hunger, the systematic approach to market development, and surprisingly, the quality standards DOMS had achieved with limited resources. The deal structure was elegant in its simplicity yet revolutionary for the Indian stationery industry. Fila, renowned for producing Giotto coloring pencils and Canson papers, initially acquired an 18.5% stake in DOMS for €5.4 million in 2012. In 2015, Fila increased its holding to 51%, becoming the majority shareholder. This wasn't a typical acquisition where the acquirer takes full control immediately. It was a phased approach that allowed both parties to test the partnership before deepening commitment.

The year 2011-2012 was a transformative year in the journey of DOMS. The Group entered into a strategic partnership with F.I.L.A. – Fabbrica Italiana Lapis ed Affini S.p.A, Italy (F.I.L.A.) – a worldwide leader in stationery industry to partner. The strategic rationale was compelling for both sides. For FILA, DOMS offered instant access to one of the world's fastest-growing stationery markets, a manufacturing base with significant cost advantages, and most importantly, a distribution network that reached into the deepest corners of India—something no amount of money could quickly replicate.

For DOMS, the benefits were transformative. The partnership with FILA enabled to gain access to international markets for distribution of products, augmentation of R&D and technological capabilities, which resulted in expansion of international footprint in key American and European markets and has helped in the global distribution of DOMS brand. Suddenly, a company that had never exported seriously was talking about entering European and American markets. Technology that would have taken years to develop was available immediately. And perhaps most importantly, the FILA association gave DOMS credibility with premium retailers and institutional buyers who had previously ignored them.

The technology transfer aspect was particularly fascinating. FILA brought expertise in areas DOMS had never ventured into—professional art materials, specialized papers, high-end coloring products. The Italians introduced quality control processes that were almost obsessive by Indian standards. Every batch of colored pencils had to match precise Pantone colors. Erasers were tested for residue levels that Indian manufacturers had never bothered measuring. The learning curve was steep, but the Raveshia and Rajani families absorbed it all with characteristic Gujarati business acumen.

But the partnership wasn't without friction. The Italian emphasis on aesthetics and premium positioning clashed with DOMS's value-for-money DNA. Massimo Candela wanted to launch premium products immediately; Santosh Raveshia worried about alienating their core customer base. The solution was brilliant—maintain DOMS as the mass-market brand while using FILA's other brands for premium segments. This dual-brand strategy allowed them to play across price points without confusion.

The cultural integration was equally complex. Italian executives visiting Umbergaon were bewildered by the informal, family-style management. Board meetings that started with prayers and ended with homemade Gujarati snacks. Decision-making that involved consulting multiple family members rather than following corporate hierarchies. Yet somehow, it worked. The Italians brought process and global perspective; the Indians brought market understanding and execution capability.

The Company has an exclusive tie-up with certain entities of the FILA Group, for distribution and marketing for all categories of their respective products, under their name and trademark, in India, Nepal, Bhutan, Sri Lanka, Bangladesh, Myanmar, and Maldives. This wasn't just about DOMS selling in Italy—it was about DOMS becoming FILA's gateway to South Asia, a market of nearly 2 billion people.

The financial engineering of the partnership was equally sophisticated. FILA's investment wasn't just equity—it came with guaranteed technology transfer agreements, export purchase commitments, and importantly, management bandwidth. FILA executives joined DOMS's board, bringing global governance standards to what had been a closely-held family business. Massimo Candela, aged 59 years, is the Chairperson and Non-Executive Director of our Company. He holds a degree in Business Administration with major in corporate finance from Bocconi University, Milan. He has been associated with FILA since 1992 as chief executive officer.

By 2015, when FILA increased its stake to 51%, the partnership had proven its worth. DOMS was no longer just an Indian stationery company—it was part of a global network, with products being developed in Italy, manufactured in India, and sold worldwide. The company that had started in a small shed in Umbergaon was now discussing strategy with executives who managed brands founded before America was discovered.

What makes this partnership particularly instructive is what it tells us about globalization in emerging markets. This wasn't the typical story of a multinational acquiring and gutting a local company. It was a true partnership where both sides brought unique strengths, where the local company retained its identity and management, and where value creation happened through capability building rather than cost cutting. As we'll see in the next section, this partnership would become the foundation for unprecedented scaling of manufacturing and distribution capabilities.

V. Building the Empire: Manufacturing Scale & Distribution Mastery (2012–2023)

The morning shift at Umbergaon begins at 6 AM. By 6:15, over 3,000 workers are at their stations across what has become one of Asia's largest integrated stationery manufacturing complexes. The transformation from the modest facilities of 2012 to today's sprawling campus tells a story of ambitious capital allocation, operational excellence, and the courage to build ahead of demand.

When FILA's money started flowing in 2012, the temptation might have been to go slow, test the waters, build incrementally. Instead, DOMS did something audacious—they decided to build for the future they envisioned, not the present they inhabited. The company operates a network of 13 manufacturing facilities in Umbergaon, Gujarat, covering around 34 acres of land, making it one of the largest stationery manufacturing facilities in India. But this wasn't just about scale—it was about integration.

The backward integration strategy reads like a masterclass in supply chain control. Wood processing units in Jammu & Kashmir, where Kashmir Poplar trees provide the soft wood ideal for pencils. Lead and graphite manufacturing in-house, eliminating dependency on Chinese suppliers. Polymer processing units for plastic products. Even the wooden pallets for shipping were manufactured internally. By 2023, DOMS controlled nearly 70% of its raw material requirements—remarkable in an industry where most players remained assemblers. The Jammu operations deserve special attention. In Jammu, current production facilities are spread across 100,000 square feet of build-up area focused on producing high quality pencils, sourcing one of the best quality wood available in India. Ketan Rajani, who had joined R.R. Industries in 1985 and has been its partner since 2011, took charge of this critical operation. The Kashmir Poplar tree provided soft wood ideal for pencils, and by controlling the source, DOMS eliminated a major supply chain vulnerability. DOMS's manufacturing facilities are sprawled in Umbergaon, Gujarat and Jammu & Kashmir in India, spreading across 1 million square feet of built-up area.

But manufacturing was only half the equation. The real moat DOMS built was in distribution—a network so extensive that competitors found it almost impossible to replicate. As of September 30, 2023, the company has a strong, global multi-channel distribution network in over 45 countries in the USA, Africa, Asia Pacific, Europe, and the Middle East. The domestic distribution network for general trade comprises of over 100 super-stockists, and 3,750 distributors along with a dedicated sales team of over 450 personnel covering more than 115,000 retail touch points over 3,500 cities and towns.

The numbers are staggering but don't tell the full story. What DOMS created wasn't just reach—it was intimacy with the market. Their sales team didn't just take orders; they understood which products moved in which seasons, which colors sold in which regions, how exam schedules affected demand. This granular market intelligence, fed back into product development and manufacturing planning, created a virtuous cycle of better products leading to better distribution leading to better market understanding.

The SKU proliferation strategy was counterintuitive in a low-margin business. Apart from this, it has a wide and differentiated product category, which includes over 3,770 SKUs as of March 31, 2023. Most competitors kept SKUs limited to manage complexity. DOMS went the opposite direction—if a child wanted a specific cartoon character on their eraser, DOMS would make it. If a region preferred triangular pencils over round ones, DOMS would manufacture them. This wasn't inefficiency; it was customer obsession at scale.

The multi-channel strategy evolved organically. Traditional trade remained the backbone—those thousands of small shops near schools. But as modern retail grew, DOMS was ready. They understood that Big Bazaar needed different packaging than the corner store. E-commerce required individual product listings optimized for search. Each channel had different economics, different customer behaviors, different competitive dynamics. DOMS built separate teams for each, avoiding the mistake of force-fitting one model across channels.

International expansion accelerated post-FILA partnership. The Company has an exclusive tie-up with certain entities of the FILA Group, for distribution and marketing for all categories of their respective products, under their name and trademark, in India, Nepal, Bhutan, Sri Lanka, Bangladesh, Myanmar, and Maldives. But more importantly, DOMS products started appearing in American and European stores—not as cheap imports but as quality products from FILA's global network.

The acquisition strategy during this period was surgical. Later, we acquired Pioneer Stationery Private Limited, expanding our existing product range to include paper stationery products for school, office, and professional artist use. Pioneer Stationery brought paper products expertise. The ClapJoy stake (30% acquisition) gave them entry into educational toys. Each acquisition filled a gap, either in product portfolio or distribution capability.

What's remarkable about this period is how DOMS managed to scale without losing agility. Large companies typically become slow, bureaucratic. DOMS remained entrepreneurial. Santosh Raveshia still personally reviewed new product designs. Family members stationed themselves at different plants, ensuring quality standards. The company culture remained that of a startup, even as revenues crossed ₹1,000 crores.

The investment in sustainability wasn't just compliance—it was strategic. Besides touching millions of hearts, our manufacturing facility is aware of its responsibilities towards the environment, making use of solar energy and water conservation systems in the plants. DOMS is actively working towards reducing its carbon footprint & adapting sustainability practices. Solar panels covered factory roofs. Water recycling systems were installed. These investments, while expensive upfront, reduced operating costs and more importantly, resonated with increasingly environment-conscious consumers and institutional buyers.

By 2023, DOMS had built something unique—manufacturing scale with flexibility, distribution reach with market intimacy, global partnerships with local identity. The company that had started as a contract manufacturer was now setting industry standards. The infrastructure was in place for the next big leap—going public and using capital markets to accelerate growth even further.

VI. The IPO Story: Going Public at Peak (December 2023)

The boardroom at the Trident Hotel in Mumbai was electric. It was September 2023, and the DOMS leadership team was making final presentations to investment bankers competing to manage their IPO. The timing seemed perfect—Indian markets were hitting new highs, the IPO pipeline was active, and most importantly, DOMS had delivered three consecutive years of exceptional growth. But beneath the optimism was a crucial question: Was this the right time, or were they selling at the peak?

DOMS Industries IPO is a bookbuilding of ₹1,200.00 crores. The issue is a combination of fresh issue of 0.44 crore shares aggregating to ₹350.37 crores and offer for sale of 1.08 crore shares aggregating to ₹849.63 crores. The structure itself told a story—this wasn't just about raising growth capital. FILA wanted partial liquidity after an 11-year journey, and the Indian promoters were ready to crystallize some value while retaining control.

The backstory to the IPO decision was complex. FILA, despite the success of the partnership, needed to reduce leverage at the parent level. The effects of the Indian listing will allow FILA to significantly reduce its leverage ratio to support future growth objectives. The Italian company had been on its own acquisition spree globally and needed capital. Selling a stake in DOMS, which had grown spectacularly, was the obvious solution.

For the Indian promoters, the IPO represented validation of a five-decade journey. From partnership firms to a company that could command premium valuations in public markets—it was the ultimate entrepreneurial dream. But they were also pragmatic. The Indian education market was evolving, digital disruption was a real threat, and having public market currency would help in future acquisitions.

DOMS Industries IPO bidding started from December 13, 2023 and ended on December 15, 2023. The allotment for DOMS Industries IPO was finalized on Monday, December 18, 2023. The shares got listed on BSE, NSE on December 20, 2023. DOMS Industries IPO price band is set at ₹790 per share.

The roadshow revealed fascinating investor dynamics. Institutional investors were initially skeptical—how could a pencil company justify such valuations? The DOMS team's response was masterful. They didn't sell themselves as a stationery company; they positioned themselves as a play on India's education boom, as a creative economy enabler, as a consumption story with international growth potential. They showed how their 30% EBITDA margins in certain categories matched FMCG companies, not traditional manufacturing.

The retail investor response was phenomenal. The IPO of DOMS Industries was fully subscribed within just an hour of its launch. As of Wednesday, the IPO saw a subscription rate of 5.12 times, fuelled by significant interest from retail investors. The section allocated for retail individual investors was particularly popular, being subscribed 18 times over. Every middle-class parent who had bought DOMS products for their children wanted to own a piece of the company. It was emotional investing at its finest—a brand they trusted, products they used daily, and a growth story they could understand.

According to market observers, DOMS IPO commanded a grey market premium of Rs 495 (a premium of 63% over IPO price). This wasn't just speculation—it reflected genuine demand from investors who had missed the allocation. The grey market premium sustained even as other IPOs in the pipeline struggled, indicating strong fundamental interest rather than momentum trading.

Shares of Doms Industries were listed on the bourses on 20 December 2023. The scrip was listed at Rs 1,400, exhibiting a premium of 77.22% to the issue price of Rs 790. The listing day was spectacular. The extraordinary performance of the company's first trading day, which closed registering a 69 percent advance, shows the strength and potential of the Indian market.

The use of proceeds was carefully structured to signal growth intent while maintaining financial prudence. Proposing to partly finance the cost of establishing a new manufacturing facility to expand its production capabilities for a wide range of writing instruments, watercolour pens, markers, and highlighters. This wasn't just capacity expansion—it was category expansion into higher-margin products where DOMS had been underrepresented.

FILA's approach to the IPO was particularly sophisticated. As part of the listing, FILA, as the selling shareholder, disposed of 10.1 million shares of DOMS for a total consideration of INR800 million, corresponding to approximately EUR88.0 million, while still remaining the company's largest single shareholder post-listing, as it owns 18.6 million shares of DOMS, representing 30.6 percent of the latter's share capital.

The post-IPO shareholding structure was carefully balanced. FILA retained 30.6%, enough to maintain strategic influence but not enough to control unilaterally. The Indian promoters collectively held about 44%, ensuring continued family control. The public float of 25% was just enough to ensure liquidity while maintaining pricing power.

What's fascinating about the DOMS IPO is what it represented for the broader Indian market. Here was a company in a seemingly commoditized sector commanding software-like valuations. It validated the India consumption story, proved that brands could be built in traditional sectors, and most importantly, showed that patient capital combined with execution excellence could create extraordinary value.

The IPO also marked a transition in governance. Upon the conversion of the Company into a Public Limited Company, the name was changed to DOMS Industries Limited and a fresh Certificate of Incorporation was issued to Company by the RoC on August 3, 2023. Independent directors were inducted, quarterly reporting discipline was instituted, and the informal family-style management had to adapt to public market scrutiny.

For investment bankers, the DOMS IPO became a template for positioning traditional businesses to modern investors. For the promoters, it was vindication of their strategy to partner with FILA rather than sell out completely. And for FILA, it was proof that emerging market investments, done right, could deliver spectacular returns—they had invested about €5.4 million in 2012 and were sitting on holdings worth over €88 million just from the IPO sale, with substantial holdings still retained.

VII. Product Portfolio & Innovation Engine

Walk into any stationery store in India today, and the DOMS shelf tells a story of calculated category expansion. From a single product line of pencils in the 1970s to over 3,770 SKUs by 2023, the journey represents one of the most comprehensive product portfolio buildouts in Indian consumer goods history. But this wasn't random proliferation—each category entry was strategic, each SKU justified by data.

The company offers stationery and art materials to consumers, which are classified into seven categories: (i) scholastic stationery; (ii) scholastic art materials; (iii) paper stationery; (iv) kits and combos; (v) office supplies; (vi) hobby and craft; and (vii) fine art products. This seven-category framework wasn't just organizational—it represented seven different consumer occasions, seven different competitive dynamics, seven different margin profiles.

The scholastic stationery category remained the cash cow. Core products 'pencils' and 'mathematical instrument boxes' enjoy high market shares; 29% and 30% market share by value in FY 2022-23 respectively. But within pencils alone, the innovation was remarkable. Triangular pencils for better grip. Extra-dark pencils for Indian examination requirements. Pencils with multiplication tables printed on them. Each innovation seemed minor, but collectively they created a moat.

The mathematical instruments category showcased DOMS's ability to disrupt through design. The traditional geometry box hadn't changed in decades—a tin box with basic instruments. DOMS introduced themed boxes with cartoon characters, transparent boxes to prevent theft in shops, boxes with built-in sharpeners and erasers. They turned a commodity into a lifestyle product, commanding 30% market share in the process.

The art materials expansion leveraged the FILA partnership brilliantly. Professional-grade oil pastels that could compete with imported brands. Water colors with Italian formulation but Indian pricing. Sketch pens that didn't dry out in Indian heat. The company moved from serving just students to serving art professionals, opening up entirely new distribution channels—art galleries, professional suppliers, online specialized retailers.

What's particularly impressive is the innovation in seemingly mundane products. Take erasers—a product most companies treated as an afterthought. DOMS introduced dust-free erasers that didn't leave residue, scented erasers that made studying pleasant, erasers shaped like cartoon characters that doubled as toys. They understood that in low-involvement categories, small delights could drive brand preference.

The company offers products under the flagship brand, DOMS along with other brand/sub-brands including C3, Amariz, and Fixyfix. The multi-brand strategy allowed them to play at different price points without diluting the core DOMS brand. C3 targeted the ultra-premium segment, Amariz focused on art professionals, Fixyfix captured the adhesives market. Each brand had its own identity, distribution strategy, and margin profile.

The R&D investment, while modest by global standards, was significant for Indian stationery. The company didn't just copy products—they adapted them for Indian conditions. Pencils that could write on rough paper common in government schools. Markers that worked despite dust and humidity. Geometry instruments calibrated for Indian examination patterns. This wasn't glamorous innovation, but it was innovation that mattered.

The kits and combos category represented brilliant revenue management. By bundling products, DOMS increased average transaction values, reduced distribution costs, and most importantly, introduced children to their full range. A geometry box wasn't just instruments—it included a DOMS eraser, sharpener, and pencil. A art kit introduced kids to products they might never have tried individually.

The office supplies expansion was strategic—moving beyond children to capture lifetime value. As students became professionals, DOMS wanted to remain relevant. Permanent markers for offices. Highlighters for professionals. Whiteboard markers for corporate training rooms. The margins were better, the volumes steadier, and importantly, it reduced seasonality tied to academic calendars.

The company derived a significant portion amounting to 59.54% of the Gross Product Sales in FY 2022-23 from the sale of key products and a significant portion amounting to 31.66% in FY 2022-23 from the sale of wooden pencils. Any decline in the Gross Product Sales of key products in general or specifically 'wooden pencils' could harm the business. This concentration risk drove continuous innovation—ensuring the core remained strong while new categories grew.

The hobby and craft segment targeted a different consumer entirely—parents looking for creative activities for children. DIY kits, craft materials, modeling clay. This wasn't about school requirements but about enrichment, allowing DOMS to command premium pricing and access modern retail channels that prioritized such products.

Fine art products represented the apex of the portfolio pyramid. Professional-grade materials that competed with international brands, leveraging FILA's technical expertise. The volumes were small, but the brand halo was significant. When art students used DOMS professional products, it elevated the entire brand perception.

The private label opportunity was particularly interesting. As organized retail grew in India, chains needed stationery suppliers who could deliver quality at scale with consistency. DOMS became the partner of choice, manufacturing under retailer brands while maintaining their own brand sales. This dual strategy—building their brand while being the backbone for others—provided both stability and growth.

What made DOMS's product strategy successful wasn't just the range but the speed of innovation. In an industry where product lifecycles were measured in decades, DOMS launched new products every quarter. They borrowed from FMCG playbooks—limited edition products, seasonal variations, collaborative designs. They made stationery exciting in a way competitors hadn't imagined possible.

The portfolio strategy also reflected sophisticated margin management. High-volume, low-margin pencils drove distribution reach. Higher-margin art materials improved profitability. Premium products enhanced brand perception. Private label provided volume stability. Each piece of the portfolio puzzle had a role, creating a system that was resilient to competition in any single category.

VIII. Modern Era: Post-IPO Performance & Future Bets (2024–Present)

Eight months after the spectacular listing, DOMS's conference room screens showed a different picture. The stock that had listed at ₹1,400, a 77% premium to the IPO price, was trading volatile. The initial euphoria had settled into the hard reality of meeting quarterly expectations, and the market was discovering what it really meant to own a stationery company valued at software multiples. The financial performance post-IPO has been robust, validating the premium valuations to some extent. Mkt Cap: 14,424 Crore (up 4.15% in 1 year) · Revenue: 2,030 Cr · Profit: 218 Cr. The company reported 42.54% surge in consolidated net profit to Rs 51.33 crore in Q2 FY25 as against 36.01 crore posted in Q2 FY24. Revenue from operations jumped by 19.71% YoY to Rs 457.77 crore in the quarter ended 30 September 2024.

But the real story isn't in the numbers—it's in the strategic pivots DOMS is making to justify its valuation. The company is no longer content being just a stationery manufacturer. They're repositioning as a "creative products company," expanding into adjacent categories that leverage their distribution but offer better margins and growth potential.

The most surprising move has been the entry into baby hygiene products. This seems random until you understand the logic—the same parents buying stationery for school-going children have younger kids needing diapers. The distribution infrastructure is identical, the retailer relationships exist, and the brand trust transfers. It's category expansion that looks unrelated but is deeply synergistic.

DOMS Industries posted its Q1 results on 8th August 2025. The company posted robust numbers, with Q1 PAT standing at ₹57.28 crores against revenue of ₹562.28 crores. During Q1 FY26, the profit increase of the company was recorded at 10.49% YoY, and the revenue increase for the same period was 26.35%. These numbers suggest the growth momentum continues, but the market remains skeptical about sustainability.

The competitive landscape has intensified post-IPO. The success and visibility have attracted attention. Chinese manufacturers are targeting the Indian market more aggressively. Digital-native brands are emerging, selling directly to consumers online. Even FMCG companies are eyeing the stationery space as a natural extension. The moat that seemed impregnable is being tested.

FILA's stake reduction adds another dimension to the story. Italian multinational FILA Group, a promoter of DOMS Industries, recently sold a 4.6% stake for Rs 798 crore in an open market deal. FILA's shares were sold between Rs 2,879.12 and Rs 2,879.47 each, totalling Rs 798.54 crore. This sale reduced FILA's holding in DOMS Industries from 30.58% to 25.98%. While FILA maintains it remains committed to the partnership, the stake sale raises questions about long-term alignment.

The international expansion strategy is evolving. Rather than just exporting, DOMS is exploring manufacturing partnerships in Africa and Southeast Asia. The logic is compelling—these markets are where India was 20 years ago, with growing education access and rising incomes. But execution in new geographies is always harder than anticipated.

Digital disruption remains the elephant in the room. Tablets in schools, digital note-taking, online examinations—each trend chips away at traditional stationery demand. DOMS's response has been to emphasize the cognitive benefits of handwriting, partner with schools on "writing improvement" programs, and ironically, launch digital education content that complements physical products.

The sustainability push has accelerated post-IPO. Recycled paper products, plantable pencils (pencils with seeds that can be planted after use), plastic-free packaging—these initiatives resonate with environmentally conscious consumers and increasingly, with institutional buyers who have ESG mandates. The margins are lower, but the brand value and customer loyalty gains are significant.

In the second quarter of FY2025, DOMS Industries Limited reported strong growth. Revenue from operations rose by 19.7% to ₹457.8 crore, up from ₹382.4 crore in the same period last year. The company's EBITDA increased by 31.7%, reaching ₹85.9 crore, which improved the EBITDA margin to 18.8% compared to 17.1% in Q2 FY2024. Profit after tax (PAT) also surged, growing by 42.8% to ₹53.7 crore, with the PAT margin rising from 9.8% to 11.7%.

The acquisition pipeline remains active. EdTech companies with complementary products, regional stationery brands with strong local presence, even toy companies that fit the "creative play" positioning. The IPO proceeds and strong cash generation provide the war chest, but the challenge is finding targets at reasonable valuations in a frothy market.

What's particularly interesting is how DOMS is managing the public market pressure. Quarterly earnings calls have become education sessions about the industry. Management provides guidance but emphasizes long-term value creation over quarterly beats. They're trying to train the market to think of them as a consumer brand company, not a commodity manufacturer.

The employee stock options granted during IPO are creating interesting dynamics. Young professionals who joined for the startup culture are now seeing real wealth creation. This is attracting talent from FMCG and tech companies, bringing fresh perspectives to a traditional industry. The third generation of the founding families, armed with international education and modern management ideas, is taking larger roles.

Looking at stock performance, the volatility is notable. The stock that listed at a 77% premium has seen days of 10% moves in both directions. Institutional investors who missed the IPO are waiting for corrections to enter. Retail investors who got allocation are torn between booking profits and holding for long-term. On the opening bell of 11th August 2025, the shares of DOMS Industries opened at ₹2,359.70 per share. However, the initial gains are sustained as of now, and DOMS Industries shares are trading at ₹2,513.80 per share, higher than their opening price. Considering the long-term performance, DOMS Industries shares have yielded close to 2.96% returns in the past 1 year.

The future bets DOMS is making—baby care, educational toys, digital content, international manufacturing—represent a transformation from a stationery company to something broader. Whether the market will continue to award premium valuations for this transformation remains the key question. The next few quarters will be crucial in establishing whether DOMS can sustain its growth trajectory while managing the expectations that come with being a high-profile public company.

IX. Playbook: Business & Investing Lessons

After spending hours dissecting DOMS's journey, certain patterns emerge that transcend stationery and speak to fundamental business principles. These aren't theoretical frameworks from business schools but hard-won insights from five decades of building in one of India's most challenging sectors.

Building Brands in Commodity Markets

The first lesson is perhaps the most counterintuitive: brands can be built in any category, even one as commoditized as pencils. DOMS didn't accept that a pencil is just a pencil. They understood that parents buying pencils aren't just buying writing instruments—they're investing in their children's education, expressing care, hoping for better futures. By tapping into these emotions through packaging, quality consistency, and thoughtful innovations, DOMS transformed a commodity into a brand.

The key was segmentation within seeming homogeneity. While competitors saw "pencils," DOMS saw exam pencils, art pencils, beginner pencils, professional pencils. Each micro-segment had different needs, different price sensitivities, different purchase occasions. This granular understanding allowed them to build a portfolio that seemed broad to consumers but was actually precisely targeted.

The Power of Distribution in Emerging Markets

Distribution, not manufacturing, is the real moat in emerging markets. Anyone can set up a pencil factory. But building relationships with 3,750 distributors, ensuring product availability in 115,000 retail points, managing credit across thousands of small retailers—this is the hard work that creates lasting competitive advantage.

DOMS understood that in India, distribution isn't just logistics—it's relationships. Their sales team didn't just deliver products; they helped retailers manage inventory, provided credit during tough times, even helped with store displays. This high-touch model seems inefficient compared to modern retail, but in markets where trust matters more than contracts, it's irreplaceable.

The multi-tier distribution structure—super-stockists to distributors to retailers—seems archaic but serves crucial functions. It distributes working capital requirements, provides market intelligence from every tier, and creates multiple points of resilience. When COVID hit and modern retail shut down, this traditional network kept DOMS products flowing.

Strategic Partnerships vs Going Alone: The FILA Model

The FILA partnership offers a masterclass in structuring international collaborations. Rather than selling out completely or struggling alone, DOMS found a middle path—bring in a strategic investor who provides technology and market access while maintaining operational control and cultural identity.

The phased investment approach was brilliant. FILA's initial 18.5% stake in 2012 was a dating period. The increase to 51% in 2015 was marriage. The IPO partial exit was conscious uncoupling while remaining friends. Each phase served its purpose, and both parties benefited enormously.

What made it work was aligned incentives without complete convergence. FILA wanted returns and Asian market access. DOMS wanted technology and global reach. Neither tried to impose their complete vision on the other. The Italians didn't try to make DOMS a European company; the Indians didn't resist global best practices. This balance is rare and valuable.

Family Business Professionalization

DOMS's evolution from partnership firm to public company demonstrates how family businesses can professionalize without losing their essence. The key was gradual transition, not dramatic disruption. Family members were given real responsibilities, not ceremonial titles. Performance mattered, even for founders' children.

The decision to bring in independent directors before the IPO, to separate ownership from management gradually, to create formal processes while maintaining entrepreneurial agility—these choices positioned DOMS for public market success. Many family businesses either remain too insular or overcorrect by bringing in outside professionals too quickly. DOMS found the balance.

Timing the Public Markets

The December 2023 IPO timing was masterful. The Indian market was buoyant but not bubbling. The company had delivered three years of strong growth but still had runway ahead. FILA needed liquidity but wasn't desperate. This combination of favorable conditions, strong performance, and aligned stakeholder needs created the perfect IPO window.

But timing wasn't just about market conditions. DOMS had spent years preparing—strengthening governance, building sophisticated financial reporting, creating a compelling equity story. When the window opened, they were ready to jump through it. This preparation-meets-opportunity framework is crucial for any IPO aspirant.

Category Creation and Expansion Strategies

DOMS didn't just enter categories; they created new ones. "Mathematical instruments" wasn't a category before DOMS made it one. "School kits" became a distinct purchase occasion. "Art materials for beginners" carved out space between toys and professional supplies. This category creation allowed them to define the rules rather than follow them.

The expansion sequence was strategic. Start with adjacent products that use similar raw materials (pencils to color pencils). Then move to complementary products sold to the same customer (pencils to erasers). Then leverage distribution for entirely new categories (stationery to toys). Each step built on previous capabilities while adding new ones.

Manufacturing Excellence in Low-Margin Products

In a business where products sell for rupees, not hundreds of rupees, every paisa matters. DOMS's manufacturing excellence wasn't about automation or cutting-edge technology—it was about relentless focus on efficiency. Reducing wood wastage by 1% meant lakhs in savings. Optimizing packaging to fit one more unit per box reduced transportation costs significantly.

The backward integration strategy was about control, not just cost. By manufacturing their own graphite, processing their own wood, producing their own packaging, DOMS controlled quality and supply. This control became crucial during supply chain disruptions when competitors struggled to source materials.

The India Consumption Story Through Stationery Lens

DOMS's growth mirrors India's economic development. Rising education enrollment drove volume growth. Increasing income levels enabled premiumization. Urbanization created organized retail opportunities. Digital adoption opened e-commerce channels. Understanding these macro trends and positioning accordingly was crucial to DOMS's success.

But DOMS didn't just ride trends—they shaped consumption patterns. They taught Indian parents that better stationery could improve academic performance. They convinced children that stationery could be self-expression. They showed retailers that stationery could be a profit center, not just a necessity. This market-making, not just market-serving, created additional growth beyond economic trends.

The Capital Allocation Framework

Throughout its history, DOMS demonstrated disciplined capital allocation. In the early years, every rupee went back into the business. During the growth phase, they balanced expansion with profitability. Post-FILA, they leveraged partner capital without overdependence. Post-IPO, they're balancing growth investments with shareholder returns.

The decision to maintain asset-light operations where possible while investing heavily in core manufacturing shows sophisticated thinking. Own what provides competitive advantage (manufacturing facilities), partner for what doesn't (logistics), outsource commoditized activities (basic packaging). This selective ownership model optimizes capital efficiency.

Building for Resilience, Not Just Growth

DOMS built redundancies that seemed inefficient but proved crucial during crises. Multiple manufacturing locations provided backup during local disruptions. Diverse product portfolio reduced dependence on any single category. Multi-channel distribution ensured market access even when some channels closed. This resilience-first thinking enabled them to survive multiple economic cycles and emerge stronger.

The lessons from DOMS extend far beyond stationery. They show how patient capital, operational excellence, strategic partnerships, and deep market understanding can create extraordinary value even in ordinary industries. For entrepreneurs, it's inspiration that unicorns can be built with pencils, not just pixels. For investors, it's a reminder that boring businesses with strong execution can deliver exciting returns.

X. Bear vs Bull Case & Valuation Analysis

Bull Case: The Optimist's Perspective

The bulls see DOMS as a rare combination—a company with proven execution capabilities, operating in a market with massive headroom, trading at valuations that, while high, are justified by growth potential and quality metrics.

Start with market leadership. DOMS's 29% share in pencils and 30% in mathematical instruments provides pricing power and economies of scale. In fragmented markets, leaders tend to consolidate share over time. As smaller players struggle with compliance costs, GST implementation, and working capital requirements, DOMS is positioned to capture their market share. The shift from unorganized to organized alone could double DOMS's addressable market.

The distribution moat is perhaps the strongest bull argument. Building a network reaching 115,000 retail outlets took decades. The relationships, credit arrangements, and market intelligence embedded in this network cannot be replicated quickly even with unlimited capital. This distribution infrastructure can be leveraged for new categories—as proven by the baby care entry—making each additional product launch increasingly profitable.

International expansion remains nascent. With presence in 40+ countries but minimal market share, the growth potential is enormous. The FILA partnership provides access without heavy investment. As these markets develop their education infrastructure, DOMS is positioned to capture growth similar to what they achieved in India.

The premiumization opportunity is compelling. As Indian parents increasingly view education as investment, they're willing to pay more for quality stationery. DOMS's ability to offer products across price points—from value to premium—allows them to capture this entire spending upgrade cycle. The gross margins in premium products are 2-3x that of basic products, so even small mix shifts drive significant profit growth.

Education sector tailwinds remain strong. Despite digital disruption fears, physical writing remains fundamental to learning, especially in early education. India's push toward universal education, reduction in dropout rates, and growth in private schools all drive stationery demand. The New Education Policy's emphasis on activity-based learning actually increases demand for art and craft materials.

The management quality deserves premium valuation. The successful navigation from family partnership to public company, the FILA partnership structuring, the consistent execution through multiple cycles—this track record suggests management can handle future challenges. The presence of next-generation family members with modern education provides succession clarity.

ESG considerations increasingly matter. DOMS's sustainability initiatives, local manufacturing focus, and employment generation in smaller cities resonate with ESG-focused funds. As global capital increasingly considers ESG factors, DOMS could see valuation re-rating purely from index inclusion and ESG fund buying.

Bear Case: The Skeptic's Concerns

The bears see a traditional manufacturing business trading at tech valuations, facing structural headwinds, with execution risks that markets are ignoring.

The valuation concern is paramount. At 70+ times trailing earnings and 14+ times book value, DOMS trades at multiples typically reserved for high-growth tech companies. For context, global stationery leaders trade at 15-20 times earnings. Even assuming significant India premium, current valuations embed extremely optimistic assumptions about growth and margins.

Digital disruption is real and accelerating. Tablets in schools aren't widespread today but could be tomorrow. Government digital education initiatives, while nascent, aim to provide digital devices to students. Each tablet distributed is potentially one less customer for traditional stationery. The trend is irreversible, and DOMS's core market could shrink structurally.

The dependence on FILA for exports (over 20% of revenues) creates vulnerability. FILA's recent stake sale, while maintaining strategic partnership, suggests reduced commitment. If FILA decides to source from other partners or develop internal capabilities, DOMS's international growth story could unravel quickly. The company lacks independent international distribution capabilities.

Competition from Chinese imports remains a threat. While DOMS has competed successfully so far, Chinese manufacturers continue to improve quality while maintaining cost advantages. Any reduction in import duties or free trade agreements could flood the market with cheaper alternatives. The anti-China sentiment provides temporary protection but isn't a permanent moat.

Working capital intensity is a structural issue. In a business selling low-value products through traditional distribution, cash conversion cycles are long. As DOMS grows, working capital requirements grow proportionally. This limits free cash flow generation despite healthy profit margins. The company's negative cash flows from investing activity of Rs (not disclosed) for FY 2022-23 highlights this challenge.

Category expansion risks are underappreciated. Moving into baby care, toys, and other categories seems logical but execution is complex. Each category has entrenched competitors, different consumer behavior, distinct regulatory requirements. The distraction from core business and investment required might not generate adequate returns.

The high promoter holding (70.4%) limits float and creates overhang risk. Any significant stake sale by promoters or FILA could pressure stock price. The limited float also means institutional investors seeking significant positions might struggle to build stakes, potentially limiting demand.

Input cost volatility remains a concern. Wood prices, polymer costs, graphite prices—all fluctuate based on global commodities. While DOMS has managed this historically, any sustained input cost inflation without ability to pass on costs could pressure margins significantly.

Peer Comparison and Relative Valuation

Comparing DOMS with listed peers provides context:

- Navneet Education trades at ~25x earnings with similar growth but stronger publishing business

- Linc Pen trades at ~30x earnings with focus on writing instruments

- Flair Writing trades at ~15x earnings with lower growth and margins

- Global peers like Newell Brands (owner of Paper Mate, Sharpie) trade at ~10x earnings

DOMS's premium to peers is justified partially by superior growth and margins but the magnitude of premium seems excessive. The company argues it deserves consumer goods multiples, not manufacturing multiples, but even FMCG companies in India rarely sustain 70x earnings multiples.

Growth vs Profitability Trade-offs

DOMS faces classic growth-profitability tension. Maintaining 20%+ revenue growth requires: - Increasing marketing spend (currently minimal) - Expanding distribution (dilutes margins initially) - Category expansion (requires investment) - Price competition (pressures margins)

The company has managed this balance well historically, but as base grows, maintaining both growth and margins becomes increasingly difficult. Markets pricing in continued margin expansion alongside rapid growth might be disappointed.

Capital Allocation Priorities

Post-IPO capital allocation will be crucial: 1. Growth capex for new categories and capacity 2. Working capital for revenue growth 3. Acquisitions in adjacent spaces 4. Dividend distribution to shareholders 5. Technology investments for digital initiatives

Balancing these competing priorities while maintaining ROCE above cost of capital will determine whether premium valuations are sustained. Any mis-allocation could trigger re-rating.

The Verdict

DOMS represents a fascinating valuation puzzle. The business quality is undeniable—strong brand, excellent distribution, proven execution, favorable industry position. But at current valuations, much of this quality is priced in. The stock is priced for perfection—continued rapid growth, margin expansion, successful category expansion, and no major disruption.

For long-term investors believing in the India consumption story and management's execution capabilities, DOMS could still deliver returns, though unlikely to match the spectacular past performance. For value investors, waiting for a meaningful correction might be prudent. For growth investors, other opportunities might offer better risk-reward.

The key monitorables are: - Quarterly revenue growth momentum (needs to stay above 20%) - Margin trajectory (any compression would be concerning) - Success of new category launches - FILA relationship stability - Market share trends in core categories

XI. Epilogue: The Future of Creative Industries

As we reach the end of DOMS's story—though really, it's just the beginning of a new chapter—it's worth stepping back to consider what this journey tells us about Indian manufacturing, consumer brands, and the future of creative industries.

DOMS's transformation from a small partnership firm to a ₹14,000+ crore public company isn't just a business success story. It's a meditation on how value gets created in emerging markets, how traditional industries can be reimagined, and what happens when patient capital meets persistent execution.

What DOMS Tells Us About Indian Manufacturing

The DOMS story challenges conventional wisdom about Indian manufacturing. We're often told that India can't compete with China on cost, can't match Western quality, lacks the ecosystem for manufacturing excellence. Yet here's a company that built world-class facilities in Umbergaon and Jammu, competed successfully against Chinese imports, and convinced an Italian luxury goods company to not just partner but hand over majority control.

The key insight is that manufacturing success in India isn't about replicating Chinese scale or German precision. It's about finding the sweet spot between automation and employment, between global standards and local adaptation, between efficiency and flexibility. DOMS's factories employ thousands but also use modern equipment. They follow international quality standards but adapt products for Indian consumers. They achieved scale but maintained agility.

This model—globally competitive but locally rooted—might be the template for Indian manufacturing renaissance. Not trying to out-China China, but creating a distinctly Indian manufacturing paradigm that leverages our strengths: understanding of diverse, price-conscious markets; ability to manage complexity; innovation within constraints.

The Next Decade: AI, Sustainability, and New Categories

The next decade will test DOMS in ways the last five decades haven't. Artificial intelligence isn't just threatening jobs—it's changing how children learn, create, and express themselves. When AI can generate art instantly, what happens to art materials demand? When homework can be completed digitally, what happens to writing instruments?

DOMS's response will need to be more sophisticated than just hoping these trends reverse. They'll need to position physical creation as complementary to digital, not competitive with it. The tactile experience of drawing, the cognitive benefits of handwriting, the emotional satisfaction of physical creation—these become selling points, not assumed benefits.

Sustainability will shift from nice-to-have to business imperative. The European Union's regulations on single-use plastics, India's own environmental consciousness, institutional buyers' ESG mandates—all push toward fundamental product redesign. DOMS's experiments with plantable pencils and recycled materials need to scale from marketing gimmicks to core product lines.

New categories will emerge at the intersection of physical and digital. Smart notebooks that digitize handwritten notes. Augmented reality coloring books. Educational toys that combine physical manipulation with digital feedback. DOMS's ability to navigate these hybrid categories will determine whether they remain relevant or become nostalgic.

International Expansion Possibilities

The real international opportunity for DOMS isn't in competing with established players in developed markets but in becoming the champion of emerging markets. Africa's education boom, Southeast Asia's rising middle class, Latin America's infrastructure development—these mirror India's journey with a lag.

DOMS understands the constraints and opportunities of these markets better than Western multinationals. They know how to build distribution without modern retail. They understand price-conscious consumers who still aspire to quality. They can manage complexity that would frustrate developed market companies.

The playbook would be different from simple export. Local manufacturing partnerships, regional brand adaptation, distribution joint ventures—the FILA model reversed, with DOMS as the senior partner bringing emerging market expertise. This isn't far-fetched; it's the natural evolution of successful emerging market companies.

Lessons for Founders and Investors

For founders, DOMS offers several crucial lessons:

First, boring is beautiful. You don't need to build the next unicorn app to create massive value. Sometimes, executing better in existing categories creates more sustainable value than inventing new ones.

Second, patience pays. DOMS took 47 years from founding to IPO. The founders who started in 1973 didn't live to see the public listing. Yet their patience in building capabilities, waiting for the right partner, choosing the right moment to go public—this patience created extraordinary value.

Third, partnerships can accelerate without surrendering. The FILA partnership shows that bringing in strategic investors doesn't mean losing control or identity. Structured correctly, partnerships multiply capabilities rather than divide ownership.

For investors, DOMS illustrates the importance of looking beyond obvious metrics:

Distribution networks don't show up on balance sheets but represent real moats. Brand value in seemingly commoditized categories can be enormous. Execution consistency over decades matters more than quarterly innovations. Understanding these intangibles separates great investors from good ones.

The timing lesson is crucial. DOMS was a great investment at any point in its journey, but the returns varied dramatically based on entry point. Recognizing inflection points—the brand launch in 2005, the FILA partnership in 2012, the IPO in 2023—and having conviction to invest before these become obvious, that's where exceptional returns originate.

The Role of Patient Capital in Building Consumer Brands

DOMS's journey illustrates a crucial tension in modern capitalism—the time required to build lasting value versus the pressure for quick returns. The founders spent decades building capabilities before attempting to build a brand. They spent years building a brand before seeking institutional capital. They waited for the perfect partner rather than accepting the first offer.

This patience seems anachronistic in an era of blitzscaling and growth-at-all-costs. Yet the value created—sustainable, defensible, compounding—suggests patience might be the ultimate competitive advantage. In categories where trust matters, where distribution creates moats, where brand-building takes time, patient capital isn't just helpful—it's essential.

The FILA partnership worked because both parties understood this. FILA didn't demand immediate returns or radical pivots. They provided capital and capabilities, then waited for compound growth. The 10x+ return they achieved validates this patience.

What It All Means

As we close this deep dive into DOMS, what emerges isn't just the story of a successful company but a template for value creation in emerging markets. It shows that:

- Traditional industries can be transformed through better execution

- Local companies can successfully partner with global players while maintaining identity

- Patient capital combined with persistent execution creates extraordinary value

- Distribution and brand, not just manufacturing, create sustainable moats

- Family businesses can professionalize without losing their essence

- Public markets will reward quality, even in seemingly mundane sectors

DOMS today stands at an inflection point. The easy growth from organizing an unorganized market is behind them. The challenges ahead—digital disruption, international expansion, category evolution—are more complex. Whether they navigate these successfully will determine if DOMS becomes a century-old institution or remains a impressive but time-bound success story.

For India, DOMS represents possibility. If a pencil company can create such value, what about the thousands of other traditional industries waiting for transformation? The DOMS playbook—brand building, distribution mastery, strategic partnerships, patient execution—can be applied across sectors.

The pencil that started this journey still costs less than a cup of tea. But the value created around that pencil—in manufacturing capabilities, distribution networks, brand equity, human capital—runs into thousands of crores. That transformation, from commodity to value creation engine, is ultimately what the DOMS story is about.

Whether you're an entrepreneur looking for inspiration, an investor seeking patterns, or simply someone curious about how businesses really get built, DOMS offers lessons. Not flashy lessons about disruption and innovation, but grounded lessons about execution, patience, and the extraordinary value that can be created from ordinary products.

The story continues. Every child picking up a DOMS pencil for the first time, every retailer stocking their shelves, every investor analyzing quarterly results—they're all part of the next chapter. What that chapter holds depends on how well DOMS navigates the challenges ahead while staying true to what got them here: understanding customers, executing relentlessly, and never forgetting that at the heart of every big business is a simple product solving a real need.

In a world obsessed with the next big thing, DOMS reminds us that sometimes the current small thing, done exceptionally well over time, becomes bigger than anyone imagined.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube