Avenue Supermarts: How DMART Cracked India's Retail Code

I. Opening & Episode Thesis

Picture this paradox: In 2017, a company selling rice and soap at razor-thin 6-7% discounts became India's 65th most valuable firm on its very first day of trading. On its listing date 22 March 2017, it became the 65th most valuable Indian firm. The stock opened at ₹604.40 against an issue price of ₹299—a staggering 102% premium that had institutional investors scrambling for allocations and retail investors celebrating lottery-like returns.

This isn't a story about technology disruption or venture capital moonshots. It's about something far more counterintuitive: how a stock market wizard named Radhakishan Damani built India's most successful retail chain by obsessing over mundane details like vendor payment cycles and inventory turnover ratios.

The numbers tell an extraordinary tale. Market Cap ₹ 3,09,879 Cr. Company's median sales growth is 26.4% of last 10 years From a single store in Mumbai's Powai suburb in 2002 to 415 Stores across India by 2025, Avenue Supermarts has achieved what Big Bazaar, Reliance Retail, and even Walmart couldn't: consistent profitability in Indian retail while maintaining the lowest prices in the market.

But here's what makes this story truly fascinating for students of business: DMart succeeded by doing exactly the opposite of what conventional wisdom dictated. While competitors rushed to prime locations in glitzy malls, DMart bought land in unfashionable suburbs. While others delayed vendor payments to manage cash flow, DMart paid suppliers in 7-9 days. While the industry chased variety with 30,000+ SKUs, DMart focused on just 5,000 fast-moving items.

The core question we're exploring today isn't just how a dropout commerce student became one of India's richest men. It's this: How did someone who made his fortune predicting market irrationality build a retail empire on the most rational principles imaginable? And perhaps more urgently—can this model survive the age of 10-minute grocery delivery?

We'll trace Damani's journey from a single room apartment in Mumbai to creating a retail juggernaut worth over ₹3 lakh crore. We'll decode the operational playbook that turns 3.7% net margins into market-beating returns. And we'll examine whether DMart's legendary discipline can withstand the venture-funded assault of Blinkit, Zepto, and Instamart.

Because ultimately, this is a story about the power of compound excellence—how doing simple things extraordinarily well, year after year, can create one of the most valuable companies in India. Let's begin where all great business stories begin: with an unlikely founder who saw opportunity where others saw only constraints.

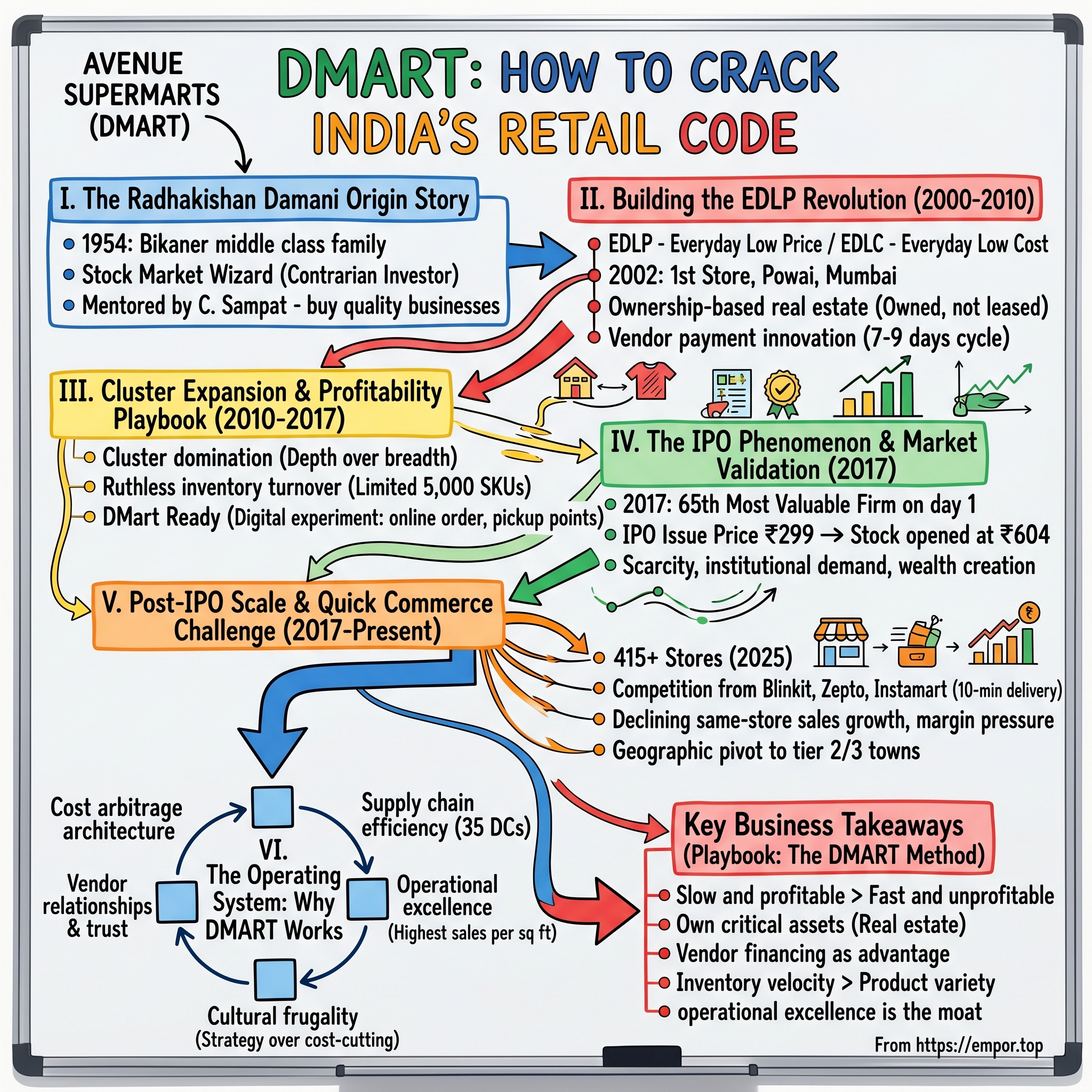

II. The Radhakishan Damani Origin Story

The Mumbai monsoons of 1954 brought more than just rain to the Damani household. Radhakishan Shivkishan Damani was born on October 15, 1954, into a modest Maheshwari Marwari Hindu middle-class family in Bikaner, Rajasthan, India. The family would later move to Mumbai, where young Radhakishan would grow up in conditions that would shape his legendary frugality—in a single room apartment in Mumbai.

The trajectory of Damani's early life seemed predetermined: commerce student, family business, middle-class respectability. He studied commerce at the University of Mumbai but dropped out after one year. Instead of pursuing academics, he started a small ball-bearing trading business—unglamorous, practical, profitable. This was Damani in his twenties: methodical, risk-averse, content with steady returns.

Then, at 32, everything changed. After the death of his father who worked on Dalal Street, Damani left his ball bearing business and became a stock market broker and investor. It wasn't ambition that drew him to the markets—it was necessity. The family needed someone to take over the stockbroking business, and Damani, despite having no interest or experience in trading, stepped up.

What happened next would become legend on Dalal Street. The quiet ball-bearing trader transformed into one of India's most astute market operators. His nickname? "Mr. White and White"—because he wore the same white shirt and white trousers every day to save time on decision-making. This obsession with eliminating unnecessary choices would later define DMart's entire operating philosophy.

The early 1990s brought Damani his first fortune, but not through conventional investing. In the early 1990s, he made big profits by short-selling stocks that had been artificially inflated by Harshad Mehta. While Mehta pumped stocks to astronomical heights, Damani and his associates—including a young Rakesh Jhunjhunwala—bet against the bubble. When the scam unraveled in 1992, Damani's contrarian positions paid off spectacularly.

But here's what separated Damani from other traders who profited from the crash: he didn't see it as vindication of his trading genius. Instead, he saw the fragility of paper wealth. While others celebrated their winnings, Damani was already thinking about real businesses, tangible assets, sustainable competitive advantages.

The mid-1990s marked Damani's evolution from trader to investor. Damani was reportedly the largest individual shareholder of HDFC Bank after it went public in 1995. This wasn't a trade—it was a twenty-year position that would multiply his wealth several hundred fold. He was learning what his mentor Chandrakant Sampat had taught him: wealth isn't built by predicting quarterly earnings, but by identifying quality businesses and holding them through cycles.

By 1999, Damani had accumulated enough capital to retire comfortably. Instead, he did something peculiar: In 1999, he operated a franchise of Apna Bazaar, a cooperative department store, in Nerul, but was "unconvinced" by its business model. The experiment lasted less than a year, but it planted a seed. Damani spent hours in the store, observing customer behavior, analyzing purchase patterns, understanding the economics of retail.

What he saw troubled him. Indian retail was dominated by two extremes: traditional kiranas with their personalized service but limited selection, and modern retailers hemorrhaging money in their quest for scale. There had to be a third way—a model that combined the kirana's cost discipline with modern retail's efficiency.

This led to multiple study trips to the United States, where Damani became obsessed with one company: Walmart. He would spend days in Walmart stores, studying everything from shelf heights to checkout procedures. Sam Walton's biography became his business bible. The Everyday Low Price philosophy resonated with something deep in Damani's trader psyche: the best arbitrage is between wholesale and retail prices.

The decision to quit stock markets at their peak in 2000 baffled everyone. Damani exited the stock market in 2000 and began building a retail business by buying cheap land in Navi Mumbai. Here was someone who had mastered the art of making money from money, walking away to sell groceries. His friends thought it was a midlife crisis. His broker peers called it retirement.

But Damani saw what they didn't: India was at an inflection point. Organized retail penetration was less than 2%. The middle class was growing. Consumer brands were proliferating. And most importantly, every existing retailer was trying to be everything to everyone. There was space for someone who could do just one thing—offer genuine value—better than anyone else.

Incorporated in 2000 by Radhakishan Damani, DMart opened its first store in Powai, Mumbai, in 2002. The store was deliberately unglamorous: warehouse-like interiors, steel racks instead of fancy fixtures, merchandise stacked high rather than artfully displayed. Opening day saw modest crowds. The press ignored it. Competitors dismissed it.

Twenty-three years later, that first store's DNA would be replicated across 400+ locations, creating India's most valuable retail company. But in 2002, it was just a stock market veteran's expensive experiment in selling soap at a discount. The real revolution was about to begin.

III. The EDLP Revolution: Building the Foundation (2000-2010)

The first DMart store in Powai was an exercise in calculated minimalism. No grand opening, no celebrity endorsements, no advertising blitz. DMart opened its first store in Powai, Mumbai, in 2002. Damani stood at the entrance on day one, personally greeting customers and observing their shopping patterns. What he saw confirmed his hypothesis: Indian consumers would trade ambiance for value, every single time.

The foundational principle was deceptively simple: Everyday Low Price, Everyday Low Cost. But while competitors understood the first part, they completely missed the second. It follows the "Everyday Low Cost - Everyday Low Price" strategy, focusing on competitive procurement, operational efficiency, and cost-effective distribution to offer value-for-money pricing to customers. DMart's innovation wasn't in selling cheap—it was in being structurally designed to sell cheap profitably.

Consider the real estate strategy, which would become DMart's first major competitive moat. Unlike other Indian supermarkets which typically leased 4,000 sq ft properties, DMart operated much larger stores, ranging up to 30,000 sq ft, most of which it owned. While Future Group and others rushed to secure prime mall locations at ₹150-200 per square foot, Damani bought land in residential neighborhoods at a fraction of the cost.

The numbers were compelling: A typical mall retailer paid ₹6-8 crore annually in rent for a 40,000 sq ft store. DMart would buy land and construct a similar-sized store for ₹15-20 crore total. The breakeven: just 2-3 years. After that, pure operational advantage forever. By 2010, while competitors struggled with lease escalations, DMart owned 21 of its 29 stores outright.

But ownership meant more than just cost savings. It meant complete control over store layout, operating hours, and crucially, the ability to stack inventory vertically. Those 30-foot high ceilings weren't architectural excess—they were working capital optimization. Every square foot of height meant less money tied up in back-end warehouses.

The vendor payment innovation would become DMart's second transformative advantage. While the industry standard was 30-45 days credit period, DMart paid suppliers in 7-11 days—sometimes even cash on delivery. The logic was counterintuitive but brilliant: the 2-3% additional discount for prompt payment more than offset the working capital cost. More importantly, it made DMart the preferred customer for vendors, ensuring first access to inventory during shortages.

By 2007, this had created a virtuous cycle. Suppliers would offer DMart exclusive pack sizes, special promotions, and most importantly, their best prices. A Hindustan Unilever executive would later admit: "When we launch a new product, DMart is among the first three calls we make. They pay fast, they move volume, and they never return stock."

The inventory turnover obsession bordered on religious. While Big Bazaar carried 30,000+ SKUs to offer "everything under one roof," DMart deliberately limited itself to 5,000-6,000 items. Every product had to earn its shelf space through velocity. If an item didn't sell 6 times a year, it was eliminated. This meant cheese might only come in two brands instead of ten, but those two brands were always in stock and always cheapest.

In its early years, the company adopted everyday low price strategy and pursued "slow expansion", growing to 29 stores across Maharashtra and Gujarat in 2010. This glacial pace frustrated investors who watched Pantaloon Retail open 100+ stores in the same period. But Damani's rule was iron-clad: no new store until the previous one was profitable. No geographic expansion until the cluster was dominant. No category addition until the supply chain was optimized.

The discipline extended to human resources. DMart store managers weren't MBAs from premier institutes but often promoted from within—people who started as checkout clerks and understood ground realities. They were given significant autonomy but measured on just three metrics: sales per square foot, inventory turns, and shrinkage (theft/damage). Everything else was noise.

Technology adoption was pragmatic, not aspirational. While competitors invested millions in ERP systems and customer analytics, DMart's IT spending focused on basics: billing accuracy, inventory tracking, and vendor payments. The point-of-sale system was deliberately simple—if a high school graduate couldn't master it in three days, it was too complex.

Marketing spend was essentially zero. No television commercials, no newspaper advertisements, no loyalty programs. The marketing budget went into one thing: lower prices on the shelf. Damani believed that every rupee spent on advertising was a rupee stolen from customer savings. Word-of-mouth from satisfied customers was the only marketing that mattered.

The private label strategy emerged gradually. DMart began introducing its own brands in categories like pulses, grains, and home care—products where brand loyalty was low but quality consistency mattered. These weren't inferior alternatives but identical quality at 15-20% lower prices. By 2010, private labels contributed 8% of revenues but 12% of gross margins.

The organizational culture was deliberately unglamorous. The corporate office in Mumbai was functional, not fancy. Damani himself drove a modest car and flew economy class. Store employees wore simple uniforms. The message was clear: every rupee saved on corporate overhead was a rupee invested in customer value.

Financial discipline was paramount. Despite opportunities for debt-funded expansion, DMart maintained conservative leverage ratios. The company would rather grow slowly with internal accruals than rapidly with borrowed money. This meant missing some opportunities, but it also meant surviving downturns that destroyed leveraged competitors.

By 2010, the model was proven but still regional. Twenty-nine stores, ₹1,800 crore revenue, and most importantly, consistent profitability. While Kishore Biyani was being celebrated as India's retail king, Damani was quietly building the foundation for something far more durable. The next phase would test whether the DMart model could scale beyond Maharashtra and Gujarat. The answer would exceed everyone's expectations—except perhaps Damani's own.

IV. The Cluster Expansion & Profitability Playbook (2010-2017)

The year 2010 marked an inflection point. Pantaloon Retail was negotiating desperate debt restructuring. Subhiksha had collapsed spectacularly. Vishal Mega Mart was struggling. The consensus was clear: Indian retail was where capital went to die. Into this graveyard of ambitions, DMart began its measured march toward national presence.

In 2013, DMart reported having 65 stores across Maharashtra and Gujarat, along with one store each in Hyderabad and Bangalore as it began expanding to other states. But the expansion blueprint was unlike anything the industry had seen. While others pursued a "flag-planting" strategy—opening marquee stores in major cities for visibility—DMart followed what internally came to be known as the "cluster domination" playbook.

Here's how it worked: Enter a new micro-market with one store. Achieve 20% market share in the catchment area. Open the second store within 5-kilometer radius. Build local supply chain infrastructure. Negotiate city-specific vendor contracts. Only then move to the adjacent micro-market. It was retail expansion as ground warfare—inch by inch, street by street, neighborhood by neighborhood.

Take the Bangalore entry in 2012. While competitors rushed to Indiranagar and Koramangala—high-income areas with expensive real estate—DMart opened in Hegde Nagar, a emerging residential suburb where land was cheap and middle-class families abundant. Within eighteen months, that store was generating ₹2 crore monthly revenue. The second store came up just 4 kilometers away. By 2015, DMart had six stores in Bangalore, all profitable, all in unfashionable locations, all packed with customers.

The immediate supplier payment system had evolved into an art form by 2013. DMart's procurement team would negotiate annual contracts with vendors, guaranteeing volume in exchange for the lowest possible price. But here's the twist: payment happened within 7-12 days of delivery, sometimes even same-day for certain categories. For vendors struggling with 60-90 day payment cycles from other retailers, DMart became the account that funded their working capital.

A Procter & Gamble distributor in Pune explained the impact: "When DMart opens in an area, we assign our best delivery boys to their account. They get priority during stock shortages. Why? Simple math—DMart pays in 10 days, others pay in 45. That 35-day difference is worth 3-4% to us. We pass half of that to DMart as additional discount."

The store economics had been refined to a science. A typical DMart store in 2014: - Size: 30,000-40,000 sq ft - Investment: ₹18-25 crore (including land) - Inventory: ₹3-4 crore - Monthly revenue: ₹1.5-2.5 crore - Breakeven: Month 8-12 - Store-level EBITDA margin: 8-9% - Payback period: 3-4 years

Compare this to a Big Bazaar hypermarket: 2x the investment, 60% of the revenue per square foot, and many never achieving store-level profitability. The difference? DMart's model was optimized for one thing—moving products fast at the lowest possible cost structure.

The December 2016 launch of DMart Ready marked the company's cautious digital experiment. While Big Basket and Grofers were burning cash acquiring customers, DMart Ready started with just one fulfillment center in Mumbai. The model was deliberately different: order online, but pick up from designated collection points. No expensive last-mile delivery. No venture capital subsidies. Just the same DMart prices with digital convenience.

The approach to store design had become iconically anti-iconic. Concrete floors instead of tiles (₹50 per sq ft saved). Steel racks instead of wooden displays (40% cheaper, 100% more durable). Minimal air conditioning in non-perishable sections (₹3-4 lakh monthly electricity saved). Box packaging left intact on shelves (labor cost reduced by 30%). Every decision optimized for function over form.

Product curation remained ruthlessly disciplined. In 2015, when Greek yogurt became trendy, DMart didn't stock it—too slow-moving, too niche. When quinoa emerged as a superfood, DMart waited two years until volumes justified shelf space. The buying team's mandate was clear: we're not educators or trend-setters. We stock what Indian families buy every week, and we sell it cheaper than anyone else.

The human capital strategy had matured into a unique model. In March 2024, the company had a total of 13,971 permanent employees and 59,961 employees hired on contractual basis. This 80% contractual workforce provided flexibility during seasonal demand while keeping fixed costs low. But unlike others who treated contract workers as disposable, DMart invested in training and often promoted high performers to permanent roles.

Private label penetration reached new sophistication. DMart's "D-Mart" branded products weren't just cheaper alternatives—they were engineered for value. The D-Mart wheat flour, for instance, was milled to exact specifications that balanced quality and cost. The 1kg pack was priced at ₹27 when branded alternatives sold for ₹35-40. The margin difference: 8 percentage points higher than branded equivalents.

Financial performance during this period validated every strategic choice. Revenue grew from ₹2,222 crore in FY2012 to ₹8,606 crore in FY2016—a 40% CAGR. More impressively, this growth came with expanding margins. Net profit increased from ₹65 crore to ₹320 crore in the same period. While the retail industry collectively lost thousands of crores, DMart was generating 15%+ return on equity.

The competitive dynamics had shifted dramatically. Big Bazaar, once the undisputed leader, was now struggling with debt and closing stores. Reliance Retail had pivoted to fashion and electronics. Spencer's was perpetually on the block. International players like Carrefour and Tesco had retreated. DMart wasn't just winning—it was increasingly the only profitable food and grocery retailer at scale.

By October 2016, the company operated 112 stores across Maharashtra, Gujarat, Telangana, Karnataka, Madhya Pradesh, and Tamil Nadu. Each store was a carbon copy of the original Powai outlet—same layout, same principles, same price advantage. The model hadn't just scaled—it had proven remarkably resilient across different geographies, demographics, and competitive environments.

The decision to go public wasn't about capital needs—DMart had ₹300+ crore in cash reserves. It was about providing exits to early investors and employees while creating currency for future expansion. The IPO preparation revealed something remarkable: in 15 years of operations, DMart had never had a loss-making year. In retail, that wasn't just unusual—it was unprecedented.

As investment bankers prepared the IPO prospectus in late 2016, they struggled to find appropriate comparables. DMart's numbers looked more like a FMCG company than a retailer: consistent growth, expanding margins, positive cash flows, and minimal debt. The street was about to discover what Damani had known all along: in Indian retail, boring discipline beats exciting innovation every time. The IPO would prove this thesis spectacularly.

V. The IPO Phenomenon & Market Validation (2017)

March 8, 2017, 10:00 AM. The Avenue Supermarts IPO opened for subscription. Within hours, the retail portion was oversubscribed. By day three, the issue was subscribed 104.48 times overall—institutional investors bid for 144 times their allocation, high net worth individuals 277 times. Avenue Supermarts IPO is a main-board IPO of 6,25,41,806 equity shares of the face value of ₹10 aggregating up to ₹1,870.00 Crores. The issue is priced at ₹299 per share.

The grey market told its own story. Premium surged from ₹150 in February to ₹250 by mid-March. Unofficial trades suggested a listing around ₹550—nearly double the issue price. Wealth managers who had dismissed retail as "uninvestable" were suddenly scrambling for allocations. The narrative had flipped: DMart wasn't just a retailer, it was India's answer to Walmart.

But here's what made this IPO unique: There is no offer for sale by existing shareholders. The entire ₹1,870 crore was fresh capital going to the company, not promoters cashing out. This sent a powerful signal—Damani and his family, who owned 82% post-IPO, weren't selling a single share. They were raising growth capital while maintaining skin in the game.

The valuation metrics sparked heated debates. The company is being valued at an FY-17 P/E of 40.13 and an FY-18 P/E of 26.67. The valuation on EV/EBITDA basis (assuming 200–300 crore debt post issue) is 20.37 times for FY-17 and 16 times for FY-18. For context, Walmart traded at 25x P/E, Costco at 30x. But those were mature businesses growing at 3-5% annually. DMart was growing at 40% with massive runway ahead.

The investment thesis was compelling in its simplicity. India's organized retail penetration was just 9%—compared to 85% in the US, 40% in China. The grocery market alone was worth $500 billion, growing at 10% annually. DMart had cracked the code on profitable growth in this massive market. The TAM (Total Addressable Market) wasn't just large—it was civilization-scale.

March 21, 2017, 9:15 AM. The stock opened for trading at ₹604.40—a 102% premium to issue price. Within minutes, it hit ₹650. The market capitalization crossed ₹40,000 crore, making it India's most valuable retail company on day one. On its listing date 22 March 2017, it became the 65th most valuable Indian firm. Damani's 82% stake was worth ₹33,000 crore. The ball-bearing trader had become one of India's richest men.

The institutional response was extraordinary. Foreign funds that had avoided Indian retail for a decade suddenly wanted exposure. The logic was intuitive: if India's consumption story was real, DMart was the purest play on it. No fashion risk, no technology obsolescence, no brand fickleness—just Indian families buying rice, dal, and shampoo at the best prices.

Retail investors had their own celebration. Those lucky enough to get allotment saw immediate doubling of capital. Social media was flooded with screenshots of profits. DMart became the dinner table conversation—everyone knew someone who had applied, few had gotten shares. The scarcity amplified the frenzy.

But beyond the price action, the IPO revealed DMart's financial exceptionalism through detailed disclosures. Revenue per square foot: ₹33,000 versus industry average of ₹15,000. Inventory turns: 12 times versus 6 times for competitors. Working capital days: Negative 8 days—DMart collected cash from customers before paying suppliers. These weren't just good numbers—they were best-in-class globally.

The use of IPO proceeds was characteristically conservative. ₹1,080 crore for debt repayment, bringing leverage to near-zero. ₹366 crore for new stores. ₹217 crore for working capital. No acquisitions, no digital ventures, no diversification. Just more of what worked—more stores in more neighborhoods selling groceries at unbeatable prices.

Analyst reports post-listing revealed fascinating insights. Morgan Stanley's deep dive showed DMart's prices were 8-12% below organized competition, 3-5% below even kiranas for branded products. CLSA's mystery shopping exercise across 10 stores found 97% product availability versus 85% for Big Bazaar. Credit Suisse calculated that DMart needed just ₹6 of working capital to generate ₹100 of sales—a capital efficiency unmatched in global retail.

The competition's response was telling. Future Group announced "Big Bazaar Direct" to match DMart's prices. Reliance Retail refocused on grocery. Spencer's promised store renovations. Everyone suddenly discovered religion on costs and prices. But copying DMart's prices without its cost structure was a recipe for larger losses.

The stock trajectory post-listing defied gravity. From ₹604 on day one, it reached ₹800 by May, ₹1,000 by September, ₹1,400 by December. Every dip was bought aggressively. The narrative was unstoppable: secular growth story, execution excellence, and a promoter with skin in the game. Mutual funds that had missed the IPO allocation were forced to buy in open market at ever-higher prices.

International investors drew parallels with Walmart's early days. Same founder-led culture, same obsession with costs, same focus on everyday essentials. Some went further—DMart was better positioned than Walmart had been. India's GDP per capita was growing faster than 1960s America. The unorganized market was larger. The competitive moat from owned real estate was stronger.

The financial media transformation was complete. Damani, who had shunned publicity for decades, was now on every magazine cover. "Retail King," "India's Sam Walton," "The ₹100 Billion Man"—headlines competed for superlatives. Business schools scrambled to create case studies. The same establishment that had ignored DMart's first decade was now desperate to claim discovery.

Employee wealth creation added another dimension. DMart had allocated shares to 9,600 employees pre-IPO. Checkout clerks who had joined in 2010 with ₹8,000 monthly salaries suddenly held stock worth ₹5-10 lakhs. Store managers became crorepatis overnight. It was India's most democratic wealth creation event outside of IT services.

The vendor ecosystem benefited too. Suppliers who had supported DMart through early years by accepting quick payments at lower margins now serviced India's most valuable retailer. Transport contractors who had offered credit during expansion saw volumes multiply. The entire value chain participated in the success.

By December 2017, the stock had delivered 150% returns from listing price. The market cap crossed ₹85,000 crore. Skeptics who called it overvalued at ₹299 were silenced by results—Q3 FY18 showed 43% revenue growth, 50% profit growth. The company added 24 stores during the year while maintaining 8% EBITDA margins. Every quarter validated the premium valuation.

The IPO's success had broader implications. It proved that Indian consumers would pay a premium for value retailers. It demonstrated that profitable growth was possible in Indian retail. Most importantly, it showed that patient capital and operational excellence could create extraordinary wealth. The boring grocery business had become India's most exciting growth story.

As 2017 ended, DMart wasn't just a successful IPO—it was a cultural phenomenon. The company that had spent nothing on marketing had become the most discussed brand in India. But Damani, true to character, was already focused on the next challenge: could DMart maintain its edge as it scaled from 100 to 500 stores? The answer would determine whether this was a great IPO story or the beginning of India's greatest retail empire.

VI. Post-IPO Scale & Quick Commerce Challenge (2017-Present)

The post-IPO era began with a land-buying spree that would make real estate developers envious. Armed with ₹1,870 crore in fresh capital and zero debt, DMart went shopping—not for companies or technology, but for acres of unglamorous land in tier-2 suburbs. Between 2017 and 2020, the company acquired over 200 acres across 50 locations, often paying cash upfront, sometimes buying land for stores planned three years hence.

From FY24 to FY25 store count has increased from 365 Stores to 415 Stores, with the majority of stores situated in West, South, and Central India, which fits the Dmart's cluster-based expansion strategy. But this wasn't random expansion. Each new store followed the same template: 45,000-60,000 square feet (nearly double the earlier format), located in residential catchments, built to last 30 years. The economics remained consistent—₹30-40 crore investment, 12-month breakeven, 20%+ store-level ROI.

The numbers told a story of relentless execution. In 2024, Avenue Supermarts's revenue was 593.58 billion, an increase of 16.87% compared to the previous year's 507.89 billion. Earnings were 27.08 billion, an increase of 6.78%. But beneath these headlines, a more complex narrative was emerging. Same-store sales growth, the holy grail of retail, was decelerating. Stores older than 24 months were growing at 8-9% versus 15% historically.

The culprit had a name: Quick Commerce.

By 2019, a new breed of competitors had emerged. Grofers (later Blinkit), BigBasket, and Swiggy Instamart weren't just delivering groceries—they were delivering them in 10-30 minutes. Quick commerce platforms like Blinkit, Zepto, and Instamart are redefining what it means to shop quickly. These platforms match D-Mart's low prices and add the convenience of speedy delivery, appealing to the tech-savvy, convenience-seeking consumer of 2024.

The threat was existential. DMart's entire model was predicated on customers traveling to stores, loading monthly groceries into cars, trading convenience for price. But what if you could get DMart prices delivered to your doorstep in 15 minutes? The venture capital community certainly believed in this future—pumping $3 billion into quick commerce between 2020-2023.

DMart's response was characteristically measured. While competitors burned cash acquiring customers, DMart quietly expanded DMart Ready, its online platform. DMart Ready, Noronha said it grew by 21.5 per cent in the first nine months of FY 2025. But true to form, the model was different—order online, pick up from stores or designated points. No 10-minute delivery promises, no venture subsidies, just the same DMart prices with digital convenience.

The pandemic years of 2020-21 became an unexpected validation. While pure-play online grocers struggled with unit economics, DMart's stores became fulfillment centers. Customers ordered online, and DMart used its existing infrastructure to fulfill efficiently. The company added just 31 stores in FY21—the slowest expansion year—but revenue still grew 12% as existing stores saw utilization spike.

Management's communication about quick commerce evolved tellingly. In 2019: "Online is complementary to our physical stores." In 2021: "We're monitoring the space closely." By 2023: Management noted that stores and operations in metro cities, including the online offering DMart Ready, were impacted by online grocery format players, including quick commerce players.

The impact was measurable. Stores in Mumbai and Bangalore—DMart's most productive locations—saw growth rates halve. The shares of DMart have plunged by more than 30% since the September peak took a further hit by Q2 FY25 results. The retail major's net profit for the Q2FY25 rose by 5.8% YoY, reaching ₹659.6 crore, compared to ₹623.6 crore in the same period last year. Avenue Supermarts revenue rose by 14.4% YoY to ₹14,444.5 crore, up from ₹12,624.4 crore YoY. The biggest miss for Avenue Supermarts was revenue growth, which was the slowest in four years. The like-for-like growth was the slowest in three years.

But here's what the bears missed: DMart was simultaneously executing a geographic pivot that would define its next decade. While quick commerce fought over 20 metro cities, DMart quietly entered 150 tier-2 and tier-3 towns where 10-minute delivery was economically unviable. Places like Solapur, Bhiwandi, Hosur—unsexy names with solid demographics and zero quick commerce competition.

They opened 10 new stores this quarter, bringing their total store count to 387. Each new store was larger, more automated, and crucially, designed for a hybrid future. Wide aisles for in-store shopping, dedicated zones for online order pickup, loading bays for home delivery. DMart wasn't choosing between offline and online—it was building infrastructure for both.

The margin story became the critical battleground. The EBITDA Margin stood at 6.40 percent for the Q4FY25 quarter compared to 7.40 percent for Q4FY24, and the PAT Margin stood at 3.70 percent as compared to 4.40 percent for the same period. The company commented about 3 things that happened during Q4FY25: Competition intensity increased in the FMCG space, which impacted their gross margins, there was a surge in wages of entry-level positions, and the company made continued investments in improving their service levels.

The quick commerce players, flush with venture capital, were selling products at losses to gain market share. DMart faced a choice: match the subsidized prices and destroy margins, or maintain discipline and lose share. Characteristically, they chose a middle path—selective matching on high-frequency items while maintaining overall basket profitability.

The organizational response revealed DMart's hidden strength: patient capital. While listed peers faced quarterly earnings pressure, Damani's 52% ownership meant long-term thinking prevailed. The message to management was clear: we're not going to win the next quarter, we're going to win the next decade. Don't chase unprofitable growth.

Technology investments accelerated, but with DMart's signature pragmatism. While others built AI-powered recommendation engines, DMart focused on basics: inventory accuracy, billing speed, and supply chain visibility. The company spent ₹200 crore on technology in FY23—significant for DMart, but a rounding error compared to what Amazon spent in a week.

Private label evolution showed sophisticated thinking. DMart Minimax (household items), DMart Premia (premium groceries), and Dmart Garden (fresh produce) weren't just cheaper alternatives—they were strategic weapons. With 25% private label penetration generating 35% of gross profits, DMart could afford to match quick commerce prices on branded products while maintaining overall profitability.

The human capital transformation was profound yet understated. In March 2024, the company had a total of 13,971 permanent employees and 59,961 employees hired on contractual basis. This 80% contractual workforce provided flexibility, but DMart invested heavily in training. Every employee, permanent or contract, underwent 40 hours of annual training. The focus: customer service, inventory management, and increasingly, digital literacy.

Financial performance reflected these crosscurrents. Avenue Supermarts Ltd, which owns and operates retail chain DMart, has reported 17.5 per cent increase in standalone revenue from operations at Rs 15,565.23 crore for the third quarter ended December 31, 2024. The company had posted a revenue of Rs 13,247.33 crore in December quarter a year ago. Growth continued, but at a moderating pace. The stock price, which had touched ₹5,900 in 2021, corrected to ₹3,500 levels by 2024.

The strategic response crystallized around three pillars. First, dominate tier-2/3 markets where quick commerce couldn't reach. Second, build omnichannel capabilities for metros where digital was inevitable. Third, leverage private labels and supply chain efficiency to maintain price leadership even against subsidized competition.

Recent quarters showed green shoots. Q3 FY25 results: For Q3 FY25, DMart reported revenue growth of 17.5% year-on-year, reaching ₹15,973 crore. Their net profit stood at ₹724 crore, reflecting a year-on-year growth of about 5%. Same-store sales growth stabilized at 8-9%. New stores in smaller towns exceeded projections. DMart Ready contributed 3% of sales, small but growing at 20% annually.

The bull case remained intact despite quick commerce headwinds. India's grocery market would grow from $600 billion to $1 trillion by 2030. Organized retail penetration would double from 12% to 25%. DMart, with its proven model and fortress balance sheet, would capture disproportionate share. The math suggested potential for 1,000 stores generating ₹2 lakh crore revenue by 2035.

But the bear case had merit too. Quick commerce was improving unit economics. Blinkit achieved EBITDA breakeven in select cities. Zepto raised $1 billion at a $5 billion valuation. The narrative shifted from "unsustainable cash burn" to "future of retail." If 10-minute delivery became profitable at scale, DMart's model faced existential questions.

As 2025 unfolds, DMart stands at a crossroads. The company that disrupted Indian retail by doing less—fewer SKUs, no frills, simple operations—now faces disruption from those doing more—faster delivery, wider selection, digital convenience. The next chapter will determine whether Damani's boring discipline can withstand Silicon Valley's exciting innovation. The battle for India's grocery basket has just begun.

VII. The Operating System: Why DMART Works

To understand DMart's resilience, you need to understand its operating system—not software, but the interconnected processes that create sustainable competitive advantage. Think of it as a flywheel where each element reinforces the others, creating momentum that's nearly impossible to replicate.

Start with the cost arbitrage architecture. They buy in bulk and pay their suppliers quickly. This gives them the upper hand in negotiations, allowing them to get better deals—lower prices, bigger discounts, and faster deliveries. Unlike many other retailers that delay payments to vendors, DMart has built strong trust with its suppliers. In return, they get favorable terms.

The math is elegant. A typical FMCG company offers 2-3% cash discount for payments within 10 days. DMart pays in 7-9 days, earning the full discount. Competitors pay in 45-60 days, earning nothing. On ₹50,000 crore annual procurement, that's ₹1,500 crore advantage—roughly equal to DMart's entire annual profit. The suppliers win too—faster cash conversion, reduced credit risk, simplified collections.

But the payment advantage compounds. During Diwali 2023, when Hindustan Unilever faced production constraints on premium detergents, guess who got first allocation? When Nestle launched limited-edition Maggi flavors, which retailer got exclusive two-week window? When Pepsi offered special price promotions, who got the deepest discounts? Trust, built over decades of prompt payment, became currency more valuable than money itself.

The supply chain architecture reveals another layer of sophistication. DMart operates just 35 distribution centers for 400+ stores—compared to 100+ for similar-sized competitors. How? The hub-and-spoke model with clustered stores means one DC can efficiently serve 15-20 stores within 50-kilometer radius. Trucks leave at 4 AM, reach stores by 6 AM, return by noon for second run. Asset utilization: 2x industry standard.

Inventory velocity becomes religious doctrine. Their stores consistently generate some of the highest sales per square foot in the retail industry because they focus on stocking fast-moving, high-demand items. Every inch of store space is optimized to move products quickly and efficiently, which is critical for their low-margin, high-volume model. The average product stays on DMart shelves for 8 days versus 18 days for competitors. This isn't just working capital efficiency—it's freshness, reduced damage, lower storage costs.

The lean operations philosophy permeates everything. Marketing spend: 0.1% of revenue versus 2-3% for competitors. How? ~Operational efficiency: Streamlined processes and cost control. ~Vendor relationships: 7-day payment vs. the industry standard of 30+ days Word-of-mouth marketing: Great prices drive customer loyalty and free promotion. Every customer becomes a brand ambassador when they save ₹500 on monthly groceries. That's more powerful than any celebrity endorsement.

Store labor productivity showcases operational excellence. DMart generates ₹3.5 lakh revenue per employee monthly versus ₹1.8 lakh industry average. The secret: simplified operations. Fixed planograms mean shelf stacking requires no decision-making. Clear pricing eliminates customer queries. Limited SKUs reduce training complexity. Self-service model minimizes assistance needs. Result: same revenue with half the workforce.

The product curation strategy deserves deeper examination. DMart's 5,000 SKU limit isn't arbitrary—it's scientifically optimized. Analysis shows 80% of Indian household grocery spending concentrates in 3,000 items. DMart stocks these plus 2,000 location-specific products. No long-tail items, no experimental categories, no vanity SKUs. If it doesn't turn 12 times annually, it's eliminated.

Another part of their strategy is selling their own products, known as private labels. These private labels offer better margins because DMart controls the manufacturing process and cuts out the middlemen. Private labels now transcend mere cost advantage. DMart contracts directly with manufacturers, specifying everything from wheat grain quality to detergent enzyme concentration. Products match branded quality at 20-30% lower prices. The margin differential—8-10 percentage points—funds price aggression on branded products.

Real estate strategy creates structural advantage. DMart owns 85% of stores versus 20% for competitors. Beyond eliminating rent, ownership enables customization impossible in leased properties. Those 35-foot ceilings for vertical storage? Custom loading docks for rapid truck turnaround? Mezzanine floors for back-office operations? Only possible with ownership. The replacement cost of DMart's real estate portfolio: ₹15,000+ crore, carried at ₹6,000 crore on books.

Another key part of DMart's strategy is its cluster-based expansion. Instead of opening stores randomly across the country, they focus on growing in specific regions, one cluster at a time. This approach helps them streamline operations, improve supply chain efficiency, and build brand loyalty in each area. It's a deliberate, slow-and-steady strategy that ensures they grow sustainably without overstretching.

Technology deployment follows characteristic pragmatism. While competitors chase AI and IoT, DMart focuses on foundational systems. Automated billing reduces checkout time by 40%. RFID tracking eliminates inventory discrepancies. Vendor portals streamline ordering. Simple, proven, effective. The entire IT budget equals what Reliance Retail spends on one failed experiment.

The workforce model balances flexibility with expertise. The 80% contractual structure isn't about cost-cutting—it's about matching capacity to demand. Diwali sees 30% traffic spike? Add temporary staff. Monsoon reduces footfall? Scale back. But critical roles—buyers, store managers, DC heads—remain permanent, accumulating institutional knowledge. Average store manager tenure: 8 years versus 2 years industry standard.

Data utilization reveals hidden sophistication. DMart doesn't need customer data because it has product data. Which soap sells fastest? Stock more. Which biscuit has highest velocity? Better placement. Which oil has lowest margin? Negotiate harder. Product-level gross margin analysis drives every decision. Customer surveys are unnecessary when checkout data reveals preferences.

The vendor ecosystem operates like an extended enterprise. Transport partners dedicate trucks exclusively to DMart routes. Packaging suppliers customize carton sizes for DMart shelves. Local wholesalers act as emergency backup inventory. Security agencies assign best personnel to DMart accounts. Everyone succeeds when DMart succeeds—alignment without equity.

Quality control happens through systematic simplicity. No quality inspectors needed when you stock only established brands. No complex return policies when customers trust your curation. No elaborate customer service when prices speak for themselves. Problems are prevented, not solved. Complexity is eliminated, not managed.

Cash flow dynamics reveal the model's elegance. Customers pay immediately (cash or UPI). Suppliers paid within 10 days. Inventory turns in 8 days. Result: negative working capital cycle. DMart uses customer money to pay suppliers, earning interest on the float. The business generates cash while growing—the holy grail of retail.

The cultural elements bind everything together. Frugality isn't policy—it's identity. When Neville Noronha became CEO, his first decision: keep the same small office. When stores exceed targets, celebration means team lunch, not bonuses. When competitors offer employees better salaries, DMart offers better stability. The message: we're building something permanent, not chasing quarters.

Risk management happens through diversification within focus. No single supplier exceeds 5% of procurement. No single store exceeds 2% of revenue. No single category dominates. Geographic concentration in clusters provides efficiency while reducing single-point failure risk. The business is resilient because it's distributed yet coordinated.

The innovation philosophy: continuous improvement, not disruption. Every year, checkout time reduces by 5%. Inventory accuracy improves by 2%. Energy consumption per square foot decreases by 3%. Compound these marginal gains over decades, and you get revolutionary results through evolutionary methods.

This operating system isn't replicable through capital or technology. It's the accumulation of thousands of small decisions, refined processes, and cultural elements built over 25 years. When competitors try copying DMart, they copy the visible—prices, products, store formats. They miss the invisible—supplier trust, employee loyalty, operational discipline. That's why DMart works. That's why it endures.

VIII. Competitive Dynamics & Market Position

The Indian retail battlefield in 2025 resembles a three-way chess match: traditional retail fighting for relevance, organized retail battling for profitability, and quick commerce burning capital for dominance. DMart occupies a unique position—profitable enough to concern investors, traditional enough to seem vulnerable, yet resilient enough to keep growing.

Start with the market opportunity that makes everyone salivate. India's retail market: $900 billion growing to $2 trillion by 2032. Organized retail penetration: 12% heading to 25%. The prize for winning: potential to build multiple $100 billion companies. No wonder every conglomerate, from Reliance to Tata to Adani, wants a piece.

Reliance Retail represents the most formidable threat. With 18,000+ stores and ₹2.6 lakh crore revenue, it dwarfs DMart's ₹60,000 crore scale. JioMart promises integration with telecom, creating an ecosystem DMart can't match. The strategy: lose money on groceries, profit from fashion and electronics, subsidize from oil refining. Deep pockets, patient capital, ecosystem play—everything DMart isn't.

Yet Reliance's grocery ambitions keep stumbling. Smart Point stores, launched to compete with DMart, achieve barely 50% of targeted revenue. JioMart's quick commerce pivot burned ₹2,000 crore before scaling back. The problem: Reliance's DNA is scale and complexity. DMart's is simplicity and efficiency. Culture eats strategy, even Ambani's strategy.

The Big Bazaar cautionary tale haunts every retailer. Once valued at ₹40,000 crore, sold for ₹25,000 crore in distress. Kishore Biyani's empire collapsed not from poor execution but excessive ambition. The lesson DMart internalized: growth without profitability is suicide. Every competitor rushing to scale should remember Big Bazaar's 145 stores couldn't save it from bankruptcy.

Regional players present a different challenge. In Tamil Nadu, Saravana Stores offers similar prices with local touch. In Andhra, Ratnadeep knows local tastes better. In Punjab, Vishal Mega Mart has first-mover advantage. But none have DMart's scale economies or operational discipline. They win neighborhoods; DMart wins cities.

International players' struggles validate DMart's approach. Walmart's wholesale model serves businesses, not families. Metro Cash & Carry retreated to wholesale. Carrefour exited entirely. Tesco sold to Trent. The lesson: transplanting Western retail to India fails. You need Indian frugality, not American abundance. DMart understood this intuitively.

The quick commerce segment is growing at breakneck speed, driven by convenience and ultra-fast delivery. According to a Morgan Stanley report, this market could balloon to $25 billion–$55 billion by 2030. High-frequency users—about a third of the customer base—are expected to drive nearly 75–80% of the total market value. This sector is even projected to surpass food delivery in gross order value by 2026, making it a critical battleground for e-commerce players.

The quick commerce disruption deserves deeper analysis. Blinkit, Zepto, and Instamart aren't just competing—they're changing consumer behavior. The 10-minute delivery promise rewires expectations. Convenience trumps price for urban millennials. The monthly shopping trip becomes daily micro-purchases. DMart's bulk-buying model faces existential questions.

But quick commerce economics remain problematic. Quick commerce struggles with the "distribution" or "last mile" problem—getting products to customers' doors involves significant costs: fuel, labor, delivery logistics, and tech infrastructure. Dark stores in expensive urban locations. Delivery costs of ₹40-50 per order. Customer acquisition costs of ₹500-1000. Path to profitability requires either massive scale or higher prices—neither guaranteed.

The competitive response reveals strategic choices. Trent (Tata's retail arm) focuses on fashion with Zudio, avoiding grocery wars. Future Retail's remnants sold to Reliance. Spencer's perpetually seeking buyers. Godrej Nature's Basket targets premium, avoiding mass market. Everyone's zigging while DMart zags—staying focused on middle-class value retail.

Market segmentation shows DMart's sweet spot. Premium retail (3% of market): dominated by Nature's Basket, Foodhall. Urban convenience (8%): quick commerce territory. Traditional retail (77%): kiranas' stronghold. Value-conscious organized (12%): DMart's dominance. This 12% segment, worth ₹100,000 crore, offers decades of growth.

The moat analysis reveals three layers of protection. First, owned real estate creates 15-20% cost advantage—unreplicable at scale. Second, supplier relationships built over decades can't be bought. Third, operational culture takes generations to build. Competitors can copy stores, not systems.

Digital transformation strategies diverge sharply. Reliance bets billions on technology. Quick commerce players are digital-native. DMart's approach: selective digitization. Self-checkout counters reduce labor. Inventory management systems improve accuracy. But no algorithmic pricing, no AI-powered recommendations, no metaverse experiments. Technology as tool, not theology.

Geographic strategies reveal different philosophies. Quick commerce concentrates on 20 metro cities. Reliance spreads everywhere simultaneously. Regional players protect home territories. DMart's cluster approach: dominate 150 cities thoroughly rather than presence in 500 cities superficially. Depth over breadth.

The partnership dynamics show ecosystem evolution. Amazon partners with More Retail. Flipkart partners with local stores. Swiggy partners with all formats. DMart partners with nobody. The independence has costs—no marketplace access, no delivery network leverage. But also benefits—no margin sharing, no strategic dependence.

Price competition intensifies but within bounds. Quick commerce can't sustain 50% discounts forever. Reliance won't subsidize groceries indefinitely. Kiranas can't match organized retail efficiency. DMart's 8-12% price advantage remains sustainable because it's structurally embedded, not promotion-driven.

Customer segmentation reveals DMart's resilience. The ₹30,000-80,000 monthly household income segment—DMart's core—is least penetrated by quick commerce. Too price-conscious for premium retail. Too quality-conscious for kiranas. Too bulk-buying for quick commerce. This 200 million person segment ensures DMart's relevance.

Innovation horizons suggest different futures. Quick commerce experiments with 10-minute medicine delivery. Reliance builds digital ecosystems. Amazon tests drone delivery. DMart's innovation: opening stores profitably in Tier-3 towns. Not sexy, but effective.

The regulatory environment could reshape competition. Proposed e-commerce rules limiting discounts help DMart. Data localization requirements add costs for digital players. FDI restrictions prevent global retailers' entry. The regulatory moat, accidentally created, protects domestic physical retailers.

Competitive advantages compound over time. DMart's 25-year head start in operational excellence can't be bridged with capital. Quick commerce's venture funding will eventually demand returns. Reliance's patience isn't infinite. Time, the scarcest resource, favors the incumbent who's profitable.

The end game appears increasingly clear. India will have 3-4 large grocery retailers: DMart dominating value segment, Reliance leveraging ecosystem, quick commerce owning convenience, and kiranas retaining personal touch. The ₹2 trillion market can sustain all models. Competition intensifies margins but doesn't eliminate players.

As Warren Buffett observed: "The key to investing is not assessing how much an industry is going to affect society, or how much it will grow, but rather determining the competitive advantage of any given company and, above all, the durability of that advantage." DMart's advantage isn't technology or capital—it's the accumulated wisdom of selling groceries profitably for 25 years. That's harder to disrupt than Silicon Valley imagines.

IX. Playbook: The DMART Method

After analyzing DMart's quarter-century journey, distinct lessons emerge that transcend retail. These aren't just tactics but philosophical approaches to building enduring businesses in emerging markets. Each lesson challenges conventional wisdom while offering actionable insights for founders and investors.

Lesson 1: Slow and profitable beats fast and unprofitable

The venture capital playbook says grow fast, figure out profits later. DMart inverted this: profit from day one, then grow. The company adopted everyday low price strategy and pursued "slow expansion", growing to 29 stores across Maharashtra and Gujarat in 2010. While Big Bazaar opened 100 stores in five years, DMart opened 29. But DMart's stores were profitable; Big Bazaar's weren't.

The discipline seems anachronistic in today's blitzscaling era. But consider the outcome: DMart worth ₹3 lakh crore, Big Bazaar sold in distress. The tortoise and hare isn't just a fable—it's a business model. Growth that doesn't generate cash isn't growth; it's disguised destruction of capital.

For founders, this means resisting the siren song of "growth at all costs." Every unicorn that died—from Foodpanda to Shopclues—forgot this principle. Sustainable growth comes from serving customers profitably, not from subsidizing them with venture money. Ask not how fast you can grow, but how fast you can grow profitably.

Lesson 2: Own your real estate in emerging markets

Conventional wisdom says asset-light is superior. DMart proved exactly opposite in Indian context. Owning stores meant higher initial capital but lower operating costs forever. The math: ₹40 crore to build and own versus ₹4 crore annual rent. Breakeven: year 10. Advantage thereafter: permanent.

But ownership transcends economics. It enables customization—those 35-foot ceilings, specialized loading docks, mezzanine storage. It provides stability—no lease renegotiations, no forced relocations. It creates optionality—stores can be modified, expanded, or repurposed. In volatile emerging markets, real estate ownership is insurance against uncertainty.

The broader principle: own your critical assets. For software companies, it might be proprietary data. For manufacturers, specialized equipment. For platforms, network effects. Whatever drives your competitive advantage, own it, don't rent it. Control creates compound advantages over time.

Lesson 3: Vendor financing as competitive advantage

DMart transformed a liability (paying suppliers) into an asset (earning discounts). By paying in 7-9 days versus industry's 45 days, they earned 2-3% additional margin. On ₹50,000 crore procurement, that's ₹1,500 crore annual advantage—roughly equal to total profits.

The insight: in B2B relationships, payment terms matter more than payment amounts. Suppliers will sacrifice margin for certainty. They'll offer discounts for speed. They'll provide preferential treatment for reliability. DMart weaponized promptness into competitive advantage.

For any business, examine your payment cycles. Where can faster payment earn discounts? Which relationships would strengthen with prompt settlement? How can financial discipline become strategic differentiation? Your CFO's efficiency might be your CEO's best strategy.

Lesson 4: Inventory velocity over product variety

Competitors stocked 30,000+ SKUs to offer choice. DMart stocked 5,000 to ensure availability. The insight: customers don't want infinite choice; they want reliable access to what they need. Better to never run out of daily essentials than occasionally stock exotic items.

Every inch of store space is optimized to move products quickly and efficiently, which is critical for their low-margin, high-volume model. This velocity focus compounds. Faster inventory turns mean less working capital, fresher products, lower storage costs, reduced shrinkage. The entire business accelerates when inventory velocity increases.

The principle extends beyond retail. In software, focus on core features users engage with daily rather than edge cases. In services, excel at frequent interactions rather than rare scenarios. Velocity in core activities beats variety in peripheral ones.

Lesson 5: Cultural frugality as strategy

DMart's frugality isn't cost-cutting—it's cost consciousness embedded in DNA. When the CEO flies economy while running a ₹60,000 crore company, it sends a message. When stores use steel racks instead of wooden displays, it reinforces priorities. When the company spends nothing on advertising, it demonstrates confidence.

This cultural frugality becomes self-reinforcing. Employees who waste resources self-select out. Vendors who expect lavish entertainment don't engage. Customers who value ambiance over prices shop elsewhere. The culture acts as an automatic filter, attracting aligned stakeholders.

For founders, the lesson is clear: culture isn't what you say but what you consistently do. If you preach frugality but fly business class, the message is clear. If you talk customer focus but obsess over competitors, employees notice. Authentic culture comes from lived values, not posted values.

Lesson 6: The power of patient capital and long-term thinking

Damani's 52% ownership enables decision-making in decades, not quarters. When quick commerce threatened, DMart didn't panic-pivot. When margins compressed, they didn't slash quality. When growth slowed, they didn't chase fads. Patient capital permits patient strategies.

The contrast with venture-backed competitors is stark. They optimize for next funding round, not next decade. They prioritize growth metrics over unit economics. They pivot strategies with management changes. Impatient capital produces impatient decisions.

For investors, this suggests backing founders who think in decades. For founders, it means choosing investors who share your time horizon. For employees, it means joining companies playing long games. Time horizon might be the most important strategic decision that nobody discusses.

Lesson 7: Systems thinking over point solutions

DMart doesn't excel at any single element—prices aren't lowest, stores aren't fanciest, technology isn't cutting-edge. But the system—how elements interconnect and reinforce—is superior. Owned stores enable bulk storage enabling inventory velocity enabling supplier discounts enabling low prices enabling volume growth enabling economies of scale. It's a virtuous cycle, not isolated advantages.

Competitors copy elements but miss connections. They match prices without cost structure. They build stores without cluster density. They negotiate with suppliers without payment credibility. Copying parts without understanding whole guarantees failure.

The lesson: build systems, not features. Design reinforcing loops, not standalone advantages. Think ecosystem, not product. Amazon isn't great at any single thing but exceptional at how everything connects. DMart proves this principle works in physical retail too.

Lesson 8: Operational excellence as the only moat

DMart has no technology moat, brand moat, or regulatory moat. Its only defense: doing basic things better than anyone else. This operational excellence—built over 25 years—can't be acquired, funded, or disrupted. It must be earned through repetition.

In an era obsessed with disruption, DMart proves the power of execution. While everyone seeks the next big thing, DMart perfects the current small things. While competitors chase transformation, DMart pursues incremental improvement. Revolution is exciting; evolution is profitable.

Lesson 9: Focus as competitive advantage

DMart sells groceries and household items. Period. No fashion adventures. No electronics experiments. No financial services. This focus seems limiting but creates advantages: deeper expertise, simpler operations, clearer positioning.

When Reliance Retail sells everything from apples to smartphones, complexity explodes. When Amazon spans books to cloud computing, management attention divides. DMart's narrow focus enables excellence within chosen domain. Constraints create creativity.

Lesson 10: Respect the incumbent

Every year, consultants predict DMart's disruption. Physical retail is dead. Quick commerce changes everything. Technology transforms shopping. Yet DMart keeps growing, keeps profiting, keeps expanding. The incumbent has advantages disruptors underestimate: customer relationships, operational knowledge, and most importantly, profitable unit economics.

The broader lesson: disruption is harder than Silicon Valley pretends. Incumbents who adapt survive. Experience matters. Domain expertise compounds. The boring company doing boring things boringly might outlast the exciting startup doing exciting things excitingly.

These lessons from DMart's playbook aren't rules but principles. They won't guarantee success but improve odds. They're particularly relevant for emerging markets where infrastructure is developing, consumers are value-conscious, and patience gets rewarded. DMart didn't just build a retail chain—it demonstrated how to build enduring value in chaotic markets. That playbook is worth more than any technology.

X. Bear vs Bull: The Investment Case

The investment community remains sharply divided on Avenue Supermarts. At ₹4,100 per share and ₹2.66 lakh crore market cap, DMart trades at 95x trailing P/E and 47x EV/EBITDA—valuations that make value investors queasy and growth investors excited. Let's examine both sides with the rigor this decision demands.

The Bull Case: Structural Winner in Massive Market

India's grocery market math is compelling: $600 billion today, $1 trillion by 2030. Organized retail penetration doubling from 12% to 25% means $150 billion opportunity. If DMart maintains just 15% share of organized retail, that's ₹2 lakh crore revenue—3x current levels. The runway isn't just long; it's generational.

Store economics remain best-in-class despite quick commerce pressure. For Q3 FY25, DMart reported revenue growth of 17.5% year-on-year, reaching ₹15,973 crore. Their net profit stood at ₹724 crore, reflecting a year-on-year growth of about 5%. New stores achieve profitability in 8-12 months versus 24-36 months for competitors. Return on capital employed consistently exceeds 20%—rare in retail globally, unprecedented in India.

The cluster dominance strategy creates local monopolies. In established clusters like Thane-Mumbai, DMart commands 35%+ market share in organized retail. New entrants face the chicken-egg problem: need scale for economics, need economics for scale. DMart's first-mover advantage in 150+ cities is effectively permanent.

Management quality remains exceptional. Neville Noronha, CEO since 2017, worked with Damani since 2002. The leadership transition was seamless—no strategy pivots, no culture dilution. With promoters holding 52%, alignment is absolute. This isn't hired management optimizing stock options; it's owners building legacy.

The balance sheet provides warfare capability. Near-zero debt, ₹5,000 crore annual cash generation, no dividend pressure. DMart can fund 50+ stores annually from internal accruals while competitors depend on external capital. In any recession, DMart emerges stronger as leveraged competitors collapse.

Quick commerce threat is overstated. DMart's Advantage? DMart skips the last mile entirely. Customers come to them for unbeatable prices. The 10-minute delivery model works for impulse purchases, not monthly grocery shopping. DMart's average ticket size (₹1,800) and basket size (25 items) indicate planned purchases that quick commerce can't replicate economically.

Geographic expansion into tier-2/3 cities opens massive opportunity. These 300+ cities with 1-10 lakh population are unviable for quick commerce but perfect for DMart. Limited competition, lower real estate costs, and value-conscious consumers create ideal conditions. DMart could add 500 stores in these markets alone.

The Bear Case: Valuation Ignores Reality

Start with valuation absurdity. At 95x P/E, DMart is priced like a software company, not a retailer. Walmart trades at 35x, Costco at 45x—and they're growing at 5% versus DMart's 15%. Even assuming 20% growth for five years, the terminal multiple needs to be 40x to justify current price. That's betting on perfection.

Margin compression is structural, not cyclical. DMart's net profit margin dropped to 4.53%, down from 5.09% a year ago and 4.57% in the previous quarter. The management pointed to "increased discounting in the FMCG category" as one of the main reasons for this margin squeeze. Quick commerce players, funded by patient venture capital, will continue subsidizing prices. DMart faces the innovator's dilemma: match prices and destroy margins, or maintain margins and lose share.

Same-store sales growth deceleration signals saturation. Stores older than 24 months growing at 8% versus 15% historically suggests market share loss. In metros, the impact is worse—Mumbai stores' growth halved. If DMart can't grow same-store sales in India's most prosperous cities, what happens when consumption slows?

Quick commerce economics are improving rapidly. Blinkit achieved EBITDA profitability in select cities. Zepto's valuation at $5 billion suggests investors see path to profitability. Once 10-minute delivery becomes profitable, DMart's value proposition—travel to store for marginal savings—weakens significantly.

Competition intensification from Reliance Retail can't be ignored. With ₹2.6 lakh crore revenue and Ambani's unlimited capital, Reliance can subsidize grocery losses indefinitely. JioMart's integration with telecom creates ecosystem lock-in DMart can't match. When India's richest man decides to win, betting against him is dangerous.

Digital transformation costs will pressure margins. DMart must invest in technology, logistics, and talent to remain relevant. These investments won't generate returns for years but are necessary for survival. The capital allocation discipline that created DMart's success becomes liability in digital age.

Store expansion economics deteriorate with scale. The best locations are already captured. New stores in tier-3 cities will generate lower revenue per square foot. The real estate arbitrage that powered early growth disappears as land prices appreciate. Growth becomes more expensive precisely when it's most needed.

The Balanced View: Quality Company, Questionable Price

DMart remains India's best-managed retailer with sustainable competitive advantages. The business model works, management executes brilliantly, and runway exists for decades. No rational analysis suggests DMart will fail or stagnate. The question isn't quality but price.

At current valuations, DMart needs everything to go right: sustained 15%+ growth, margin maintenance despite competition, successful digital transformation, and continued execution excellence. Possible? Yes. Probable? Debatable. The margin of safety that Benjamin Graham advocated is absent.

The intelligent approach might be patience. Wait for quick commerce shakeout—not all will survive. Monitor same-store sales growth—stabilization above 10% would signal resilience. Watch margins—maintenance above 7% EBITDA would confirm moat durability. Great companies at great prices create wealth; great companies at any price destroy it.

For existing shareholders, the calculus differs. With 500% gains from IPO, taking partial profits seems prudent. The next 500% return requires DMart to become a ₹13 lakh crore company—possible but improbable in any reasonable timeframe. Risk-reward has shifted unfavorably.

The investment decision ultimately depends on time horizon and risk tolerance. For 10+ year holders believing in India's consumption story, DMart offers exposure to structural growth. For value-conscious investors seeking margin of safety, current prices offer none. For momentum traders, the stock's consolidation suggests wait for breakout.

DMart exemplifies the eternal investment tension: wonderful company versus wonderful stock. The former is undeniable; the latter is questionable at current prices. As Buffett reminds us, "Price is what you pay, value is what you get." At ₹4,100, you're paying premium price for premium company. Whether you get commensurate value depends on India's next decade unfolding exactly as bulls expect. That's a big bet on many variables beyond anyone's control.

XI. Epilogue: What Would the Founders Do?

If Radhakishan Damani were starting DMart today, facing quick commerce giants and digital-native consumers, what would he do differently? The question isn't hypothetical—it reveals timeless principles versus temporal tactics, helping us separate DMart's essential DNA from era-specific adaptations.

First, the real estate strategy would invert. Instead of buying land in suburbs for future stores, Damani might buy warehouses in city centers for rapid fulfillment. The arbitrage opportunity has shifted: suburban land is expensive, but urban warehouse space—unfashionable industrial properties—offers value. Same principle (buy undervalued assets), different application.

The technology stack would be foundational, not incremental. But knowing Damani's pragmatism, it wouldn't be cutting-edge AI or blockchain experiments. More likely: robust inventory management, efficient routing algorithms, and seamless payment systems. Technology as enabler, not differentiator. The competitive advantage would still be operations, just digitally enhanced.

The vendor payment innovation would evolve into real-time settlement. Imagine DMart paying suppliers instantly upon delivery verification through automated systems. The 7-day payment advantage becomes 7-second advantage. In a world of digital payments, speed of settlement becomes even more powerful as competitive weapon.

Store formats would be hybrid from day one. Not the current DMart Ready pickup model, but stores designed as fulfillment centers with shopping areas. Customers could browse physically while pickers fulfill online orders from the same inventory. The economics: shared real estate, inventory, and staff across channels. Omnichannel not as strategy but as default architecture.

The SKU philosophy would remain constrained but dynamic. Instead of fixed 5,000 items, perhaps 3,000 core products plus 2,000 rotating based on local preferences and seasonal patterns. Machine learning would identify fast-moving items, but human judgment would curate selection. Data-informed, not data-driven.

Geographic expansion would follow different logic. Instead of adjacent clusters, Damani might create distributed networks—one store per micro-market, connected digitally. The density comes from delivery coverage, not physical proximity. Think nodes in a network rather than clusters on a map.

The employment model would blend permanent expertise with gig flexibility. Core operations managed by full-time employees ensuring quality. Delivery and peak-hour support through gig workers providing scalability. The cultural challenge: maintaining DMart's service standards with transient workforce.

Private labels would launch earlier and broader. With digital channels enabling direct consumer feedback, DMart could iterate products faster. Imagine DMart-branded products achieving 40% share versus current 25%. The margin advantage would fund price competition against venture-subsidized players.

Marketing might actually exist—but characteristically different. Not brand advertising but education: teaching consumers unit price comparison, bulk buying benefits, quality indicators. Content marketing that adds value rather than interrupts. DMart as consumer advocate, not just retailer.

The capital structure would be fascinating. Damani might stay private longer, building fortress balance sheet before facing public market scrutiny. Or perhaps go public earlier but with dual-class shares preserving founder control. The principle—patient capital enabling long-term thinking—would remain sacrosanct.

Partnerships would be selective but strategic. Perhaps exclusive arrangements with local producers bypassing FMCG giants. Maybe collaboration with housing societies for group buying. Possibly white-label services for small retailers. Partnerships that strengthen ecosystem, not dilute focus.

The competitive response to quick commerce would be judo-like. Instead of matching 10-minute delivery, promise 10-hour delivery but 10% cheaper. Let competitors burn capital on speed while DMart owns value. Different games, different rules, peaceful coexistence.

Data strategy would focus on products, not people. Track every item's journey from supplier to customer. Understand velocity, seasonality, price elasticity. But resist temptation to become data broker or advertising platform. The customer relationship remains transactional—fair price for good products.

Sustainability would be embedded, not retrofitted. Solar panels on store roofs (reducing electricity costs). Reusable packaging systems (eliminating plastic while saving money). Local sourcing when economical (reducing transport costs and emissions). Green as side effect of efficiency, not separate initiative.

The financial metrics would evolve. Instead of just store-level profitability, track customer lifetime value across channels. Instead of inventory turns, measure cash conversion cycles. Instead of revenue per square foot, calculate revenue per customer. Same discipline, evolved scorecards.

Innovation would remain incremental but relentless. Each year, checkout time reduces 5%. Delivery cost decreases 3%. Product availability improves 2%. Compound these marginal gains over decades—revolutionary results through evolutionary methods. The DMart way, digitally enhanced.

Risk management would anticipate different threats. Not just competition but regulation—data privacy, gig worker rights, antitrust scrutiny. Not just market risk but climate risk—supply chain disruption from extreme weather. Not just financial risk but cyber risk—protecting payment systems and customer data. New world, new risks, same conservative approach.

The succession planning would start earlier. Identifying and grooming leaders who understand both physical retail and digital commerce. Creating institution that outlasts founder. Building culture that survives generational transition. DMart as century-long enterprise, not one-generation wonder.

Looking ahead, the next decade's winners won't be pure-play physical or digital retailers but those who blend both seamlessly. DMart's operational excellence provides foundation. Digital capabilities provide growth vector. The combination—operational excellence plus digital reach—creates next-generation retail.