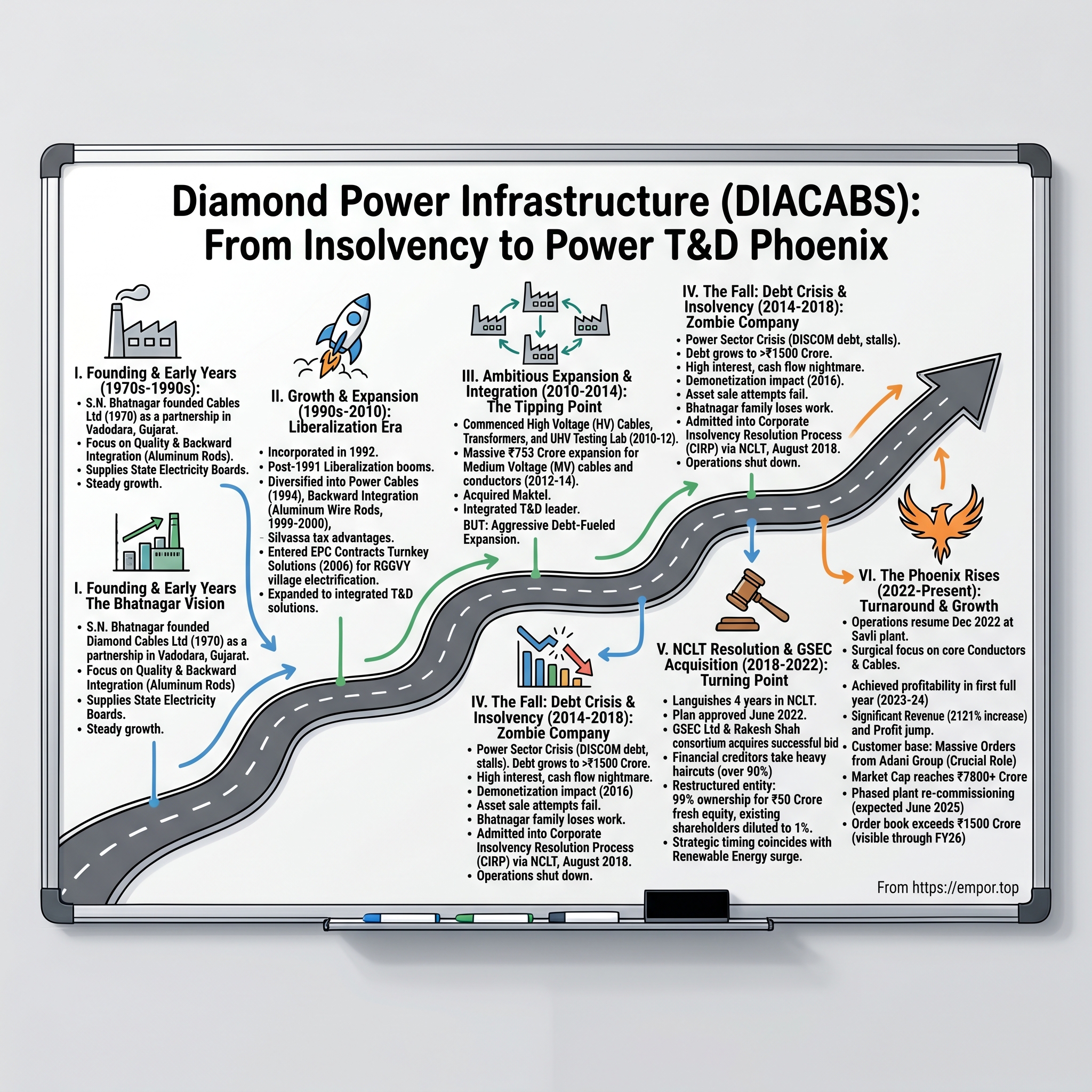

Diamond Power Infrastructure Limited: From Insolvency to India's Power T&D Phoenix

I. Introduction & Episode Roadmap

Picture this: A 50-year-old power equipment manufacturer, once the pride of Gujarat's industrial belt, lies dormant. Factory floors that once hummed with the production of conductors and cables stand silent. Creditors have given up hope. The company is deep in insolvency proceedings, its stock practically worthless. Most would write the obituary and move on.

But in June 2022, something extraordinary happens. The National Company Law Tribunal approves a resolution plan, and within two years, this same company—Diamond Power Infrastructure Limited—rockets from near-zero to a market capitalization exceeding ₹7,800 crore. The stock price multiplies over 100-fold. Orders pour in from India's renewable energy giants. The phoenix doesn't just rise; it soars.

How does a company go from manufacturing basic conductors in 1970 to bankruptcy in 2018, only to emerge as a critical supplier to India's renewable energy revolution? This is not just a turnaround story—it's a masterclass in timing, strategic positioning, and the hidden value in distressed assets.

Diamond Power Infrastructure Limited (NSE: DIACABS) operates in the unglamorous but essential business of power transmission and distribution equipment. They make the conductors that carry electricity across vast distances, the cables that connect power plants to cities, and the infrastructure that enables India's electrification dreams. It's picks-and-shovels for the energy transition—and as we'll see, sometimes the tool makers capture extraordinary value.

This story unfolds across five decades of Indian industrial history, touching on everything from post-independence manufacturing dreams to modern renewable energy ambitions. We'll explore how over-leverage killed a thriving business, how the NCLT process created an opportunity for value creation, and why the new promoters' connections might matter more than the company's balance sheet.

Along the way, we'll unpack crucial lessons: the danger of debt-fueled expansion, the importance of cycle timing in commodity businesses, and how corporate resurrections can create asymmetric investment opportunities. Whether you're an entrepreneur, investor, or student of business history, Diamond Power's journey offers insights into resilience, reinvention, and the brutal arithmetic of capital allocation.

II. Founding & Early Years: The Bhatnagar Vision (1970–1990s)

The year is 1964. A young mechanical engineer named S.N. Bhatnagar joins Jaipur Metals and Electrical Limited, part of the prestigious Kamani group. While his peers chase opportunities in consumer goods or textiles—the glamour industries of newly independent India—Bhatnagar obsesses over something decidedly unsexy: electrical conductors.

For seven years, Bhatnagar works his way through the ranks at Jaipur Metals. He becomes instrumental in developing groove contact wires—the specialized conductors that power electric trains and trams—for the first time in India. This wasn't just product development; it was import substitution at its most fundamental level. Every conductor manufactured domestically meant foreign exchange saved, industrial capability built.

But Bhatnagar sees a bigger opportunity. India's power grid is expanding rapidly, villages are being electrified, and industrial growth demands reliable power transmission. The country needs conductors—thousands of kilometers of them. In 1970, at an age when most engineers settle into comfortable corporate careers, Bhatnagar takes the leap. He resigns from his position heading the conductor and rod division to establish Diamond Cables Limited as a partnership firm. The choice of Vadodara (then Baroda) as the company's base was strategic. Gujarat in the 1970s was emerging as India's industrial powerhouse—a state where entrepreneurship was celebrated, where the government actively courted manufacturers, and where proximity to ports meant easier access to raw materials. For a capital-intensive business like conductor manufacturing, these advantages mattered.

Bhatnagar, a mechanical engineer by qualification, had joined Jaipur Metals and Electrical Limited (Kamani group companies) in 1964. During his tenure, he worked at many significant positions and was instrumental in developing groove contact wires, machineries and process, for the first time in the country. He was also heading the conductor and rod division. After rendering his outstanding services to the company for 7 years, he resigned and founded Diamond Cables Limited as a partnership company.

The early Diamond Cables was nothing like the integrated T&D giant it would become. The company started with basic aluminum conductors—the workhorses of power transmission. These aren't sophisticated products; they're essentially aluminum strands wound together to carry electricity over long distances. But in 1970s India, even manufacturing these reliably at scale was an achievement.

What set Bhatnagar apart was his technical obsession. While competitors focused on volume, he focused on quality and backward integration. He understood that in the conductor business, controlling your raw material—aluminum rods—was crucial. This insight would drive Diamond's strategy for the next two decades.

Through the 1970s and 1980s, Diamond Cables grew steadily but unremarkably. The company supplied to state electricity boards, benefited from India's expanding grid, and reinvested profits into capacity expansion. It was profitable, predictable, and entirely dependent on government contracts—a typical Indian industrial story of that era.

Diamond Power Infrastructure Limited, established on August 26, 1992, is an integrated solutions provider in Power T&D space in India. Primarily established as a conductor manufacturer in 1970 by Mr. S N Bhatnagar, a first generation technocrat, Diamond Power achieved greater integration post completion of its expansion projects during 2010-11.

The formal incorporation as Diamond Power Infrastructure Limited in 1992 marked a turning point. India was liberalizing, private power generation was being allowed, and the T&D sector was about to explode. Bhatnagar, now with over two decades of experience, sensed opportunity beyond just conductors.

By the early 1990s, Diamond had built a reputation for reliability. State electricity boards trusted them, payment cycles were manageable, and the business generated steady cash flows. But Bhatnagar wanted more—he envisioned Diamond as not just a conductor supplier but as an integrated T&D solutions provider. This ambition would drive the company's next phase of growth, setting the stage for both its spectacular rise and eventual fall.

III. Growth & Expansion Era (1990s–2010)

The liberalization of 1991 changed everything. Suddenly, private players could generate power, industries could set up captive plants, and India's chronic power shortage meant unlimited demand for T&D equipment. For Diamond Power, newly incorporated in 1992, the timing couldn't have been better.

In 1994, the company set up a small LT power cables manufacturing facility at Vadadala, Gujarat, in a bid to extend their Conductors Business. During the year 1999-2000, the company commenced commercial production of their backward integration cum expansion unit at Vadadala, Salvi, Gujarat to manufacture Aluminium and Alloy Wire rods.

The 1994 move into cables was strategic genius. Conductors and cables are complementary products—both essential for power transmission, often ordered together by utilities. By offering both, Diamond could bid for larger contracts, improve customer stickiness, and capture more value per project. The Vadadala facility started small but represented a crucial diversification.

But the real masterstroke came in 1999-2000 with backward integration into aluminum wire rods. This wasn't just about cost control—though that mattered. In the late 1990s, aluminum prices were volatile, and rod quality varied wildly. By manufacturing their own rods, Diamond could ensure consistent quality, manage inventory better, and critically, capture the margin that previously went to suppliers.

The Silvassa plant, also commissioned in 1999-2000, gave Diamond a tax advantage. Silvassa, a Union Territory, offered tax holidays for manufacturing units—a benefit that could significantly improve margins in a commodity business where every percentage point mattered.

During the year 2004-05, the company increased the production capacity of Aluminum Alloy & ACSR Conductors—a response to the massive infrastructure push under the National Democratic Alliance government. India was building highways, ports, and power plants at unprecedented scale. Every project needed power, and every power connection needed conductors and cables.

Then came 2006, and with it, a pivotal strategic shift. In August 2006 the company ventures in EPC Contracts Turnkey Contracts under Government of India sponsored RGGVY to reach free electricity to the people below poverty line. The Rajiv Gandhi Grameen Vidyutikaran Yojana (RGGVY) was ambitious—electrify every village, provide free connections to below-poverty-line families. For Diamond, this meant moving from being just an equipment supplier to becoming a turnkey solutions provider.

The EPC (Engineering, Procurement, Construction) business was fundamentally different from manufacturing. It required project management capabilities, working capital for long execution cycles, and the ability to handle multiple stakeholders. But it also offered higher margins and deeper customer relationships. Suddenly, Diamond wasn't just selling products; it was delivering outcomes.

Between 2006 and 2010, Diamond rode the infrastructure wave perfectly. Rural electrification projects, industrial expansion, and urban growth all drove demand. The company's integrated offering—we'll supply the conductors, cables, and execute the entire project—resonated with customers looking to minimize vendors.

The Company in 2010-11 commenced operations in Extra High Voltage (EHV) cables and power transformer units; commenced power transformer operations and in Oct 10, got into strategic JVs with Utkal Galvanizers, Skoda India and Schaltech Automation to increase their footprints in 220 KV and above EPC Projects.

The 2010-11 expansion into EHV cables and transformers was Diamond's boldest move yet. Extra High Voltage cables (220kV and above) are a different beast—they require sophisticated technology, rigorous testing, and command premium prices. The power transformer addition meant Diamond could now offer complete substation solutions. The strategic JVs brought technology and credibility in high-voltage projects.

By 2010, Diamond Power had transformed from a simple conductor manufacturer into an integrated T&D powerhouse. Nine manufacturing locations, all in Gujarat. Over 100 distributors across 16 states. A product portfolio spanning the entire T&D value chain. Revenue had grown multi-fold, and the company was profitable.

But this expansion came at a cost—debt. Each new facility, each backward integration, each capability addition required capital. And in the booming infrastructure market of the 2000s, banks were eager to lend. Diamond borrowed aggressively, confident that growth would continue, that margins would hold, that the infrastructure boom would never end.

As we entered 2011, Diamond Power looked unstoppable. But the seeds of its destruction were already sown. The company was about to embark on an even more ambitious expansion—one that would ultimately bring it to its knees.

IV. The Ambitious Expansion & Integration (2010–2014)

March 2012. Diamond Power's board meets to approve what seems like a minor diversification—₹50 crore investment in 6.3 MW windmills from Suzlon Energy at Jamanwada, Kutch. On paper, it makes sense: renewable energy is the future, power costs can be controlled, green credentials matter. But for a company already stretched thin by expansion, every crore matters.

During March 2012, the Company invested Rs. 50 crore to commission its 6.3 MW windmills, purchased from Suzlon Energy, at Jamanwada, Kutch. This wasn't core to the business—it was a distraction, capital deployed away from the main T&D operations at a time when working capital was already under pressure.

Seven months later, November 2012: another ambitious move. In November 2012, it commissioned Ultra High Voltage Cable Testing Laboratory having a capability to 500 KV capacity in Vadodara. This laboratory wasn't just equipment—it was a statement. Diamond wanted to play in the ultra-high voltage space, competing with multinationals like ABB and Siemens. The testing facility would give them credibility, allow them to certify their own products up to 500kV.

But the real bombshell drops quietly in company announcements: It embarked on Rs. 753 crore expansion programme for MV cables and conductors and acquired strategic stake in Maktel. Seven hundred and fifty-three crores. To put this in perspective, this was likely more than Diamond's entire net worth at the time. The company was betting everything on continued growth in India's power sector.

The expansion had multiple components. Medium voltage cables were seeing explosive demand from real estate and industrial projects. The conductor capacity expansion aimed to capture market share in the transmission segment. The Maktel acquisition brought additional manufacturing capabilities. On PowerPoint presentations to bankers, it all looked logical—vertical integration, economies of scale, market leadership.

In February 2014, it commissioned the Phase I of capacity expansion for 3000 kms in Medium Voltage (MV) cables and 50,000 MTPA in conductors businesses. Phase I alone added massive capacity. The company was now capable of producing 3,000 kilometers of MV cables annually—enough to wire a small state. The 50,000 metric tons per annum of conductor capacity put Diamond among India's largest manufacturers.

But here's what the expansion announcements didn't mention: the debt. Every new facility was funded primarily through borrowings. Banks were eager to lend—infrastructure was a "priority sector," Diamond had a track record, and the order book looked healthy. Interest rates were high—often 12-14%—but revenue growth was supposed to cover everything.

The strategic missteps were becoming clear even as they happened. Diamond was expanding capacity just as the power sector was entering a crisis. Distribution companies (DISCOMs) were bleeding money, delaying payments. Private power projects were stalling. The economy was slowing after the 2008 financial crisis aftershocks. Coal shortages meant power plants operated below capacity. Every link in the power chain was under stress.

Diamond's integrated model, once a strength, became a liability. They had facilities for conductors, cables, transformers, towers—each requiring separate working capital, separate management attention, separate technology upgrades. The company was trying to be everything to everyone in the T&D space, competing against focused specialists in each segment.

The EPC business, initially promising, turned into a cash flow nightmare. Government contracts meant dealing with bureaucracy, delayed payments, and constant renegotiation. The RGGVY projects that seemed like goldmines in 2006 were now bleeding money as execution stretched beyond timelines and costs escalated.

By early 2014, warning signs were flashing red. Receivables were mounting—customers owed Diamond hundreds of crores. Inventory was piling up as orders slowed. The company was borrowing short-term money at high rates just to meet working capital needs. The magnificent 110-acre Savli facility, built for the future, was operating well below capacity.

Diamond Power had built capabilities to serve an infrastructure boom that was already ending. They had leveraged up precisely at the wrong point in the cycle. The ₹753 crore expansion would never generate the returns projected. The company had essentially signed its own death warrant, though it would take another four years for the inevitable to unfold.

V. The Fall: Debt Crisis & Insolvency (2014–2018)

By 2014, the cracks in Diamond Power's foundation were widening into chasms. The company's debt had ballooned to over ₹1,500 crore. Interest payments alone were consuming most of the operating profits. Working capital had become a daily crisis—suppliers demanded cash upfront while customers delayed payments for months.

The power sector's systemic crisis made everything worse. Distribution companies across India owed over ₹3 lakh crore to generators, who in turn couldn't pay equipment suppliers. Diamond Power, positioned squarely in this value chain, felt every tremor. Orders dried up. Existing projects faced endless delays. Receivables aged from months to years.

Inside Diamond's Vadodara headquarters, the mood had shifted from expansion euphoria to survival mode. Cost-cutting measures were implemented—travel budgets slashed, hiring frozen, non-essential projects shelved. But these were bandages on a hemorrhaging wound. The fundamental problem was structural: Diamond had built capacity for a boom that had turned to bust.

The banks, initially patient, began tightening the screws. Quarterly reviews turned hostile. Restructuring proposals were floated—convert debt to equity, extend tenures, reduce interest rates. But with the entire power sector in crisis, lenders had little appetite for accommodation. They wanted their money back.

2016 brought a new crisis: demonetization. The sudden withdrawal of high-denomination notes froze the economy. Construction projects stopped. Payment cycles, already stretched, broke entirely. For a company already gasping for oxygen, this was suffocation.

The management tried everything. Asset sales were explored but found few takers—who wanted to buy power equipment manufacturing facilities when the sector was in crisis? Strategic investors were courted but balked at the debt burden. The Bhatnagar family, which had built Diamond over four decades, watched helplessly as their life's work crumbled.

By 2017, Diamond Power was essentially a zombie company—technically operational but financially dead. Production had slowed to a trickle. Key employees were leaving. Suppliers had cut credit lines. The magnificent Savli facility, built for annual revenues of thousands of crores, was generating barely enough to cover electricity bills.

The insolvency petition against Diamond Power Infrastructure Ltd, the Vadodara-based manufacturer of power transmission equipment and turnkey services provider, was moved by public sector lender Bank of India (BoI) for a default on payment of Rs 485 crore due to the bank. The end came on August 24, 2018, when The Ahmedabad bench of the NCLT had admitted the insolvency petition.

The company was admitted in Corporate Insolvency Resolution Process (CIRP) on 24th August, 2018. The CoC had appointed Prashant Jain as the insolvency resolution professional. For the Bhatnagar family, it was a devastating blow. The company they had nurtured from a small conductor manufacturer to an integrated T&D giant was now in the hands of creditors and courts.

Diamond Power had turned insolvent and was admitted on the Corporate Insolvency Resolution Process (CIRP) of National Company Law Tribunal (NCLT) in August 2018. Operations shut down completely. The 110-acre Savli facility fell silent. Hundreds of workers lost their jobs. Creditors—including banks, operational creditors, and employees—faced massive haircuts on their dues.

The fall was complete. From a market capitalization of hundreds of crores to practically zero. From industry leader to insolvency case. From employer of thousands to abandoned factories. It was a cautionary tale written in debt and ambition, a reminder that in capital-intensive businesses, leverage is a double-edged sword that cuts deepest when the cycle turns.

VI. The NCLT Resolution & GSEC-Monarch Acquisition (2018–2022)

Four years. That's how long Diamond Power Infrastructure languished in insolvency purgatory. From August 2018 to June 2022, the company existed in a peculiar state—legally alive but operationally comatose. The factories stood silent, gathering dust. The order books emptied. The brand, once synonymous with quality T&D equipment, faded from memory.

The Corporate Insolvency Resolution Process (CIRP) is supposed to be time-bound—270 days maximum under the Insolvency and Bankruptcy Code. But Diamond's case, like many complex insolvencies, stretched far beyond. Extensions were sought and granted. Resolution applicants came and went. The Committee of Creditors (CoC) rejected multiple bids, holding out for better terms.

Behind the scenes, a different story was unfolding. NCLT, in an order delivered on June 20, 2022, approved the resolution plan submitted by "GSEC Ltd in consortium with one Mr Rakesh Shah." (Full name: Rakesh Ramanlal Shah) But who exactly were these saviors?

GSEC Limited, which has emerged as the successful resolution applicant, was once owned by Gujarat government. It was earlier known as the Gujarat State Export Corporation Ltd, a sleepy state PSU that had been privatized. But the interesting part wasn't GSEC—it was the man behind it.

Rakesh Ramanlal Shah is the CMD of GSEC Ltd — an erstwhile Gujarat state government entity (then known as Gujarat State Export Corporation Ltd), now privatized. Shah wasn't a power sector veteran or a turnaround specialist. His background was in trading and logistics. But he had something perhaps more valuable: connections and timing.

[Some unconfirmed media reports indicate that Rakesh Ramanlal Shah is a close relative of Gautam Adani, Chairman of the Adani Group.] Whether true or not, the speculation alone would later drive market enthusiasm when Diamond's operations resumed.

The resolution plan itself was remarkable for what it revealed about distressed asset investing. Creditors, owed over ₹2,000 crore, would recover a fraction. Operational creditors got almost nothing. Financial creditors took massive haircuts—in some cases over 90%. The existing shareholders saw their holdings decimated.

In terms of the NCLT order dated 20 thJune, 2022 and approved resolution plan, the Board of Directors of the Company in its meeting held on September 17, 2022 has approved the reduction of share capital to the extent of 99% of the existing paid-up share capital and issue and allotment of 5,00,00,000 Equity Shares of Rs 10/- each at par, aggregating to Rs 50 Crores, to GSEC & its affiliates. Further, there is a reduction of existing share capital of the Company as per the approved resolution plan, to the extent of 99% of the existing Paid-up Share Capital of the Company w.e.f. September 17, 2022. After reduction, the reduced share Capital Stands to 26,97,106 Equity Shares of Rs 10/- each.

The numbers were brutal but illuminating. Existing shareholders, who once owned a company valued at hundreds of crores, now held just 1% of the restructured entity. The new promoters—GSEC and Rakesh Shah's consortium including Monarch Infraparks Pvt Ltd—acquired 99% ownership for ₹50 crore in fresh equity, plus whatever they paid to creditors under the resolution plan.

The promoters of DPIL, as of March 31, 2024, are Rakesh Ramanlal Shah and his HUF relatives; GSEC Ltd and Monarch Infraparks Pvt Ltd. The ownership structure was carefully crafted—family and close associates ensuring complete control of the resurrected entity.

But acquiring a dead company is one thing; reviving it is another. The Savli facility had been shuttered for four years. Machinery needed refurbishment. The workforce had dispersed. Customer relationships had evaporated. Supplier confidence was zero. The Diamond Power brand, once respected, now carried the stigma of insolvency.

The new management's first moves were cautious but strategic. Rather than attempting to restart everything at once, they focused on the core—conductors and cables. These required less working capital than EPC projects and could generate quick cash flows. The sprawling ambitions of the previous era were replaced with surgical focus.

The Company received the trading approvals from BSE Limited and National Stock Exchange of India Limited on September 13, 2023. When Diamond Power shares resumed trading after a five-year suspension, the market's reaction was explosive. From practically worthless, the stock began its remarkable ascent.

The timing of the acquisition would prove prescient. India's renewable energy sector was about to explode. The government had announced ambitious targets—500 GW of renewable capacity by 2030. Every solar park, wind farm, and green hydrogen project would need transmission infrastructure. And Diamond Power, with its 110-acre facility and established capabilities, was perfectly positioned to capture this demand.

The NCLT resolution had achieved what seemed impossible—transforming ₹2,000 crore of debt into ₹50 crore of equity, giving new promoters a debt-free company with valuable assets. For creditors, it was a disaster. For the new owners, it was the deal of a lifetime. The stage was set for one of Indian capital markets' most dramatic resurrections.

VII. The Phoenix Rises: Turnaround & Revival (2022–Present)

December 2022. The Savli factory gates open for the first time in over four years. It's a skeleton crew—just essential staff to assess equipment condition, check inventory, and begin the slow process of resurrection. The Company started operations under the new management since December, 2022 with part utilization of the infrastructure. Since then, it has progressed significantly under the new management. In first full year of operations i.e. 2023-24 itself, the Company has achieved robust turnover and attained profitability also despite not operating at full capacity.

The transformation was methodical. Rather than trying to restart all product lines simultaneously, the new management focused on what could generate immediate cash: basic conductors and low-voltage cables. These products had ready demand, required minimal working capital, and could leverage the existing machinery with minor refurbishment.

The numbers tell a remarkable story. For the full year, net profit reported to Rs 17.03 crore in the year ended March 2024 as against net loss of Rs 42.88 crore during the previous year ended March 2023. Sales rose 2121.02% to Rs 343.37 crore in the year ended March 2024 as against Rs 15.46 crore during the previous year ended March 2023. From near-zero revenue to ₹343 crore in the first full year—a 2,121% increase that defied all expectations.

But revenue alone doesn't explain the stock market's explosive reaction. When trading resumed in September 2023, Diamond Power's market capitalization quickly surged past ₹1,000 crore, then ₹2,000 crore, eventually reaching Mkt Cap: 7,831 Crore. What drove this revaluation wasn't just the operational turnaround—it was the customer base.

"The firm had zero business in 2022, but by 2023-24, it had revenue of Rs 344 crore -- largely from orders placed by the Adani Group businesses. Thanks to Mr Adani's business, Diamond Power Infra Ltd is now valued at Rs 7,626 crore, a seven-fold increase in valuation", noted media reports, highlighting the crucial role of strategic customers in the revival.

The Adani connection, whether through family ties or business relationships, transformed Diamond Power's prospects. India's renewable energy boom was being led by companies like Adani Green Energy, which needed massive quantities of conductors and cables for their solar and wind projects. Diamond Power, with its revived manufacturing capabilities and strategic ownership, was perfectly positioned to capture these orders.

The financial performance in 2024 validated the turnaround strategy. Net profit of Diamond Power Infrastructure rose 200.00% to Rs 16.56 crore in the quarter ended June 2024 as against Rs 5.52 crore during the previous quarter ended June 2023. Sales rose 200.69% to Rs 223.86 crore in the quarter ended June 2024 as against Rs 74.45 crore during the previous quarter ended June 2023.

By Q3 of FY25, the momentum had become undeniable. The company reported a net profit of Rs 6.42 crore in the quarter ended December 2024, compared to a net loss of Rs 5.28 crore in the quarter ended December 2023. Sales rose 412.71% to Rs 307.42 crore in Q3 FY25 from Rs 59.96 crore in Q3 FY24.

The operational metrics revealed disciplined execution. Instead of the sprawling ambitions of the previous era, the new Diamond Power focused on: - Core products with immediate demand - Cash generation over market share - Strategic customer relationships over volume - Phased capacity utilization rather than aggressive expansion

The company wasn't just selling products; it was selling into the right ecosystem at the right time. India's renewable energy capacity additions were accelerating. Every megawatt of solar or wind capacity needed transmission infrastructure. And Diamond Power, risen from the ashes, was there to supply it.

For investors who bought during the resumption of trading, the returns were spectacular. The stock that traded at virtually nothing in 2022 was now a multi-bagger. But this wasn't speculation—it was backed by real orders, real revenues, and real profits. The phoenix hadn't just risen; it was soaring on the winds of India's energy transition.

VIII. Current Operations & Market Position

Today, Diamond Power Infrastructure operates from a strategic position few could have imagined during its darkest days. Diamond Power Infrastructure Limited is engaged in the business of manufacturing of Transmission & distribution of power products & services in India. Diamond Power Infrastructure Ltd owns a cable and conductor plant, spread over 110 acres, at Savli in Gujarat.

The scale of operations has returned to impressive levels. The Savli plant has annual conductor manufacturing capacity of around 2.5 lakh tonnes. To put this in perspective, that's enough conductor capacity to wire transmission lines from Mumbai to Delhi multiple times over. The plant is equipped with five CCV (catenary continuous vulcanization) lines for producing cables—sophisticated equipment that allows Diamond to manufacture high-quality cables meeting international standards.

The product portfolio spans the entire T&D value chain. It designs and manufactures a range of power transmission equipment that includes conductors, power cables (HV, LV, and UHV), and transmission towers. We have evolved among the top manufacturers with an installed capacity of over 2,50,000 MT. Our product range comprises conductors of 7 strands to 90 strands and from 11 kV to 765 kV HVDC lines. Our product range includes highly reliable LV/HV cables from 1.1 kV to 132 kV and EHV cables from 220 kV to 550 kV.

But what truly sets the current Diamond Power apart is its order book visibility. Thanks to major orders received in the recent past, the outstanding order book position of Diamond Power Infrastructure Ltd (DPIL) has crossed Rs.1,500 crore. More recently, According to the company's exchange filing, these new orders contribute to a robust outstanding order book of Rs 1,554.08 crore, which is scheduled to be executed by 31 March 2026.

The customer concentration that might worry traditional investors has become Diamond's competitive moat. The company's revival coincided perfectly with India's renewable energy boom, particularly the massive capacity additions by players like Adani Green Energy. Every solar park needs evacuation infrastructure—the transmission lines that carry generated power to the grid. Diamond Power, with its strategic ownership and operational capabilities, positioned itself as a key supplier.

DPIL is currently in the process of re-commissioning its plant and is expected to complete the activity by June 2025. This phased approach to capacity utilization reflects the new management's disciplined capital allocation. Rather than rushing to full capacity and burning cash, they're scaling up in line with confirmed orders.

The financial metrics reflect this operational discipline. Revenue: 1,193 Cr · Profit: 38.0 Cr shows a business that has not just recovered but is generating healthy profits. The operating margins, while lower than the pre-crisis peak, are sustainable and improving with scale.

The market positioning is particularly interesting. Diamond Power isn't trying to be everything to everyone anymore. They've focused on specific segments where they have competitive advantages:

- Conductors for renewable energy evacuation

- Cables for distribution infrastructure upgrades

- Specialized products for high-voltage applications

The company's renewed focus on its EHV testing laboratory, capable of testing up to 500kV, gives it credibility in the high-margin, high-voltage segment. This isn't just manufacturing capacity—it's technical capability that differentiates Diamond from commodity cable manufacturers.

Competition remains intense. Established players like KEI Industries, Polycab, and KEC International have stronger balance sheets and broader customer bases. International giants like Prysmian and Nexans bring global technology. But Diamond's advantage lies in its focused approach, strategic relationships, and most importantly, its timing.

India's power T&D sector is at an inflection point. The government has announced investments of over ₹9 lakh crore in power infrastructure by 2030. Renewable capacity is expected to reach 500 GW, each requiring transmission infrastructure. Grid modernization, including smart grids and HVDC lines, demands sophisticated equipment. Diamond Power, risen from insolvency with a clean balance sheet and proven execution capability, is positioned to capture this opportunity.

The transformation from a debt-laden, operationally challenged company to a profitable, growing enterprise with a ₹7,800+ crore market cap is complete. But as we'll explore, the strategic relationships that enabled this resurrection bring both opportunities and questions about the company's future trajectory.

IX. Strategic Relationships & The Adani Connection

The elephant in the room can no longer be ignored. Both these orders were placed by the Adani Group. When Diamond Power announces major orders, increasingly they carry one name: Adani. Diamond Power Infrastructure secures ₹899.75 crore LOI from Adani Energy for AL 59 Conductors. Diamond Power Infrastructure announced on Monday that it has received an order worth Rs 409 crore from Adani Green Energy for the supply of various LV/MV cables.

The relationship isn't subtle. Diamond Power Infrastructure Limited announced that the Company has received the Letter of Intent dated 19th January, 2024, in its ordinary course of business aggregating to INR 2,220.8 million (with GST) from Adani Green Energy Limited for supply of various Cables & Conductors for its various projects. Order after order, the pattern is unmistakable.

The connection runs deeper than just customer-supplier dynamics. [Some unconfirmed media reports indicate that Rakesh Ramanlal Shah is a close relative of Gautam Adani, Chairman of the Adani Group.] Whether confirmed or not, the market certainly believes in the relationship, and in capital markets, perception often becomes reality.

Consider the strategic timing. Adani Green Energy is developing what will be AGEL's world's largest renewable energy plant at Khavda, Gujarat begins wind energy generation with initial 250 MW, enhancing Khavda's operational capacity to 2,250 MW including solar. This single project in Khavda, Gujarat, requires massive quantities of conductors and cables for power evacuation. Diamond Power, with its 110-acre facility just hours away in Vadodara, is perfectly positioned geographically and operationally.

The numbers are staggering. In just one year, Diamond Power has secured orders worth over ₹2,000 crore from various Adani entities. On July 9, 2024, DPIL reported the winning of a Rs.899.75-crore order for the supply of AL-59 conductors. Earlier, on July 8, 2024, the company won an order, valued at Rs.409 crore, for the supply of LV/MV cables.

But this isn't just about nepotism or favoritism—there's industrial logic here. Adani Green Energy Ltd (AGEL) is developing a renewable portfolio of 25 GW by 2025 which includes wind power, solar power, and hybrid power projects. Every gigawatt of renewable capacity needs approximately 5-7 kilometers of transmission lines per MW. That's potentially 175,000 kilometers of conductors—an astronomical requirement that needs reliable, proximate suppliers.

Diamond Power's capabilities align perfectly with Adani's needs. The AL-59 conductors Diamond supplies are high-efficiency aluminum alloy conductors specifically designed for long-distance power transmission with minimal losses—exactly what's needed for evacuating power from remote renewable sites to consumption centers.

The symbiotic relationship extends beyond simple procurement. Diamond Power's revival timeline mysteriously aligns with Adani Green's expansion plans. As Adani accelerates renewable capacity addition, Diamond ramps up production. As Adani wins new projects, Diamond's order book swells. It's industrial choreography at its finest.

Critics point to concentration risk. What happens if Adani orders dry up? The company addresses this obliquely in its filings: The company stated that none of the promoters or promoter group companies had any interest in the entities that awarded the orders. Technically true, perhaps, but the market isn't convinced.

Yet from another perspective, this relationship represents brilliant strategic positioning. India's renewable energy ambitions are national priority. "Our vision is to have a portfolio of 50 GW of RE capacity by 2030." says Adani Green. If even half of this materializes, the conductor and cable requirements would keep Diamond busy for years.

The broader ecosystem play is equally important. Adani isn't just Diamond's customer—it's Diamond's gateway to the entire renewable energy ecosystem. Other renewable developers, seeing Adani's supplier choices, often follow suit. Banks financing renewable projects gain comfort from established supplier relationships. It's network effects in action.

The stock market has certainly bought into this narrative. Diamond Power Infrastructure was locked in 5% upper circuit at Rs 99.09 after the company announced that it has received a letter of intent (LoI) from Adani Green Energy for a project worth Rs 214.65 crore. Every Adani order announcement triggers buying frenzy, upper circuits, and valuation expansion.

But there's a flip side to this cozy relationship. Diamond Power's valuation now trades at a significant premium to peers, entirely based on this strategic relationship. The company's fortune is inexorably tied to Adani's renewable ambitions, regulatory approvals, and financial health. It's concentration risk of the highest order, dressed up as strategic partnership.

The ultimate question isn't whether the Adani connection exists—it clearly does. The question is whether Diamond Power can leverage this relationship to build capabilities, credibility, and customer base beyond Adani. Can they use Adani orders as a launching pad rather than a crutch? The answer will determine whether Diamond Power's resurrection is sustainable or merely borrowed time.

X. Playbook: Business & Investing Lessons

The Diamond Power story isn't just a corporate turnaround—it's a masterclass in financial engineering, cycle timing, and strategic positioning. For investors and entrepreneurs, the lessons are profound and sometimes counterintuitive.

Lesson 1: The Resurrection Playbook

How do you revive a dead company? Diamond Power's resurrection reveals a precise formula. First, you need patient capital with a long-term view. The GSEC-Monarch consortium didn't rush to restart operations; they took months to assess, plan, and execute. Second, you focus ruthlessly. The old Diamond Power tried to be everything—conductors, cables, transformers, EPC. The new Diamond Power started with just conductors and cables, their core competence. Third, you need an anchor customer. The Adani relationship, whatever its nature, provided the demand certainty needed to restart operations.

Lesson 2: Asset Quality vs. Debt Burden

Diamond Power in 2018 had ₹2,000+ crore in debt but also had a 110-acre manufacturing facility, established production lines, technical capabilities, and industry certifications. The debt was a point-in-time problem; the assets were enduring. Distressed investors who could see past the balance sheet to the replacement value of assets made fortunes. The lesson: in capital-intensive industries, asset quality matters more than debt quantum—debt can be restructured, but rebuilding industrial capabilities takes decades.

Lesson 3: The NCLT Arbitrage

The NCLT process is brutal for existing stakeholders but creates extraordinary opportunities for new capital. Diamond Power's creditors recovered perhaps 10-15% of their dues. Existing shareholders saw 99% dilution. But new investors acquired a debt-free company with valuable assets for ₹50 crore in equity. It's financial alchemy—converting ₹2,000 crore of liabilities into ₹50 crore of equity. For sophisticated investors, NCLT resolutions represent one of the last sources of true value investing.

Lesson 4: Timing the Cycle

Diamond Power's resurrection coincided perfectly with India's renewable energy boom. This wasn't luck—it was strategic timing. The new promoters could have acquired the company earlier in the NCLT process but waited until the renewable cycle was clearly turning. They understood that in commodity businesses, timing matters more than execution. You can be the best operator, but if you're fighting the cycle, you'll lose.

Lesson 5: Capital Allocation Post-Bankruptcy

The new Diamond Power's capital allocation is radically different from the old. No grand expansion plans. No diversification dreams. No EPC adventures. Just steady, profitable growth in core products. They're using the order book to determine capacity addition, not the other way around. This discipline—born from witnessing the previous management's downfall—is perhaps the most valuable lesson.

Lesson 6: Network Effects in Infrastructure

Diamond Power's Adani relationship illustrates how infrastructure businesses are ultimately about networks. One anchor customer leads to credibility, which leads to more customers, which leads to better terms from suppliers, which improves margins, which attracts more customers. It's a virtuous cycle, but it starts with that first strategic relationship. In infrastructure, who you know matters as much as what you know.

Lesson 7: The Stigma Discount Opportunity

Companies emerging from bankruptcy carry stigma. Customers worry about reliability. Suppliers demand cash upfront. Investors remain skeptical. This creates opportunity. Diamond Power traded at massive discount to replacement value for months after resuming operations. Those who could look past the stigma to the fundamentals made multiples. The lesson: the market's emotional biases create rational opportunities.

Lesson 8: Operational Leverage in Recovery

When you're restarting from zero, every incremental sale drops almost entirely to the bottom line. Diamond Power's fixed costs were largely covered by initial orders; subsequent orders drove extraordinary margin expansion. This operational leverage is unique to recovery situations—it's why seemingly small order wins drive explosive profit growth.

Lesson 9: The Importance of Regional Champions

Diamond Power isn't competing with global giants like Prysmian or Nexans. They're not even trying to be pan-Indian like KEI or Polycab. They're content being the regional champion in Gujarat, serving the renewable energy cluster developing there. This focused approach—choosing your battlefield carefully—is crucial in commodity industries where transport costs and relationships matter.

Lesson 10: Debt Capacity vs. Debt Usage

The old Diamond Power borrowed because it could—banks were eager to lend to an infrastructure company. The new Diamond Power can borrow but doesn't—they've learned that in cyclical businesses, debt is dynamite. Having debt capacity and using it are very different things. The unused balance sheet capacity becomes competitive advantage during downturns.

Lesson 11: The Platform Value of Distressed Assets

Diamond Power's 110-acre facility, testing laboratories, and certifications would cost thousands of crores and take years to replicate. For the new promoters, acquiring this platform through NCLT was like buying a house in foreclosure—you get the infrastructure at a fraction of replacement cost. The lesson: in distressed investing, think platform value, not book value.

Lesson 12: Customer Concentration as Strategy

Conventional wisdom says customer concentration is risk. But for Diamond Power, focusing on Adani was strategic genius. One sophisticated customer is easier to serve than hundreds of small ones. Payment certainty is higher. Technical requirements push capability development. It's concentration by design, not default.

The Diamond Power playbook ultimately teaches that in business, as in life, failure isn't final. What matters is how you restructure, who backs the restructuring, and when you choose to restart. For those who understand these dynamics, distressed situations offer not just recovery potential but transformation opportunities. The company that nearly died at ₹2,000 crore of debt is now worth ₹7,800 crore—a 100x+ return for those who saw the phoenix in the ashes.

XI. Analysis & Bear vs. Bull Case

The Bull Case: Riding India's Infrastructure Supercycle

India's power transmission sector is entering what could be a multi-decade supercycle. The government has announced ₹9.15 lakh crore investment in power infrastructure by 2030. Renewable capacity addition of 50 GW annually requires approximately 250,000 kilometers of new transmission lines. Grid modernization, interstate transmission systems, and last-mile connectivity programs are all accelerating simultaneously.

Diamond Power sits at the sweet spot of this expansion. With manufacturing capacity of 250,000 MT of conductors and cables, they can capture even a small market share and see revenues multiply. The current order book of ₹1,554 crore provides visibility through FY26, but this could be just the beginning. If India achieves even 70% of its renewable targets, conductor demand would exceed current national manufacturing capacity.

The balance sheet transformation is remarkable. From ₹2,000 crore debt to virtually debt-free operations. This gives Diamond Power the flexibility to bid aggressively for orders, offer better payment terms, and invest in capacity without financial stress. In a capital-intensive industry, a clean balance sheet is a competitive weapon.

The Adani relationship, controversial as it may be, provides unmatched order visibility. Adani Green's 50 GW target by 2030 alone could generate ₹10,000+ crore in conductor and cable orders. Even at 20% share of Adani's requirements, Diamond Power has a multi-year growth runway. And success with Adani opens doors with other renewable developers who often follow Adani's supplier choices.

Valuation remains attractive despite the recent run-up. At ₹7,800 crore market cap generating ₹1,200 crore revenue, Diamond trades at 6.5x sales. Peers like Polycab trade at 3-4x sales but don't have Diamond's growth trajectory or strategic positioning. As margins normalize with capacity utilization, the earnings multiple will compress dramatically.

The technical capabilities—especially the 500kV testing laboratory—position Diamond for high-margin, high-voltage products where competition is limited. As India builds more 765kV and HVDC lines for long-distance renewable power transmission, Diamond's capabilities become increasingly valuable.

The Bear Case: A House of Cards?

The customer concentration is terrifying. If Adani orders constitute 60-70% of revenues, Diamond Power is essentially an Adani subsidiary without the formal structure. Any stress in the Adani ecosystem—regulatory challenges, financing issues, project delays—directly impacts Diamond. This isn't a business; it's a derivative bet on one conglomerate.

The industry dynamics remain challenging. Conductor and cable manufacturing is fundamentally a commodity business. Raw material (aluminum and copper) costs constitute 70-80% of revenues. Diamond has no pricing power—they're price takers in competitive tenders. One bad quarter of raw material volatility can wipe out years of profits.

Competition is intensifying. Every major electrical equipment manufacturer is expanding conductor and cable capacity seeing the same opportunity. KEI Industries, Polycab, Sterlite Power, KEC International—all have stronger balance sheets, broader customer bases, and longer operating histories. Why would customers choose Diamond except for the Adani connection?

The working capital requirements are brutal. The power sector means dealing with state utilities, renewable developers, and EPC contractors—none known for prompt payments. As Diamond scales, working capital needs will balloon. Without the balance sheet strength to support 150-180 day working capital cycles, growth itself becomes a liquidity trap.

The execution risk is real. Diamond is essentially a startup in a 50-year-old company's body. Most of the experienced workforce left during insolvency. The new team has limited experience in large-scale manufacturing. Ramping from ₹1,200 crore to ₹5,000 crore revenue requires operational excellence that's yet to be proven.

The regulatory overhang persists. The NCLT resolution gave Diamond a fresh start, but questions remain. Related party transactions with Adani entities will attract scrutiny. The dramatic market cap appreciation might trigger SEBI examination. Any regulatory action would crater the stock.

The technology risk looms large. The power transmission industry is evolving—HVDC, gas-insulated lines, superconductors. Diamond's current capabilities are conventional. Without R&D investment and technology partnerships, they risk being left behind as the industry modernizes.

The Verdict: Calculated Speculation

Diamond Power represents a unique investment proposition—part recovery play, part infrastructure bet, part Adani proxy. The bull case is compelling if you believe in India's renewable energy transition and Adani's execution capability. The bear case is equally valid if you worry about concentration risk and commodity dynamics.

The truth likely lies in between. Diamond Power will probably succeed in growing revenues and profits over the next 2-3 years, riding the renewable wave and Adani relationship. But sustainable, long-term value creation requires diversifying customers, improving operational efficiency, and building technological capabilities—none guaranteed.

For investors, Diamond Power is not a buy-and-forget proposition. It's a tactical position requiring constant monitoring of order flows, Adani's health, and industry dynamics. The risk-reward is asymmetric—potential for another 2-3x appreciation if everything goes right, but 50-70% downside if the Adani relationship sours or execution falters.

The stock is ultimately a bet on timing. Those who bought during the resurrection have already won. New investors must decide if the infrastructure supercycle has enough room to run, and whether Diamond Power's strategic positioning outweighs its structural vulnerabilities. In a market that loves story stocks, Diamond Power has one of the best stories. Whether that story translates to sustainable returns remains the billion-rupee question.

XII. Epilogue & "If We Were CEOs"

The transformation is complete. From bankruptcy to ₹7,800 crore market cap. From shuttered factories to ₹1,500 crore order book. From corporate graveyard to stock market darling. Diamond Power Infrastructure's resurrection ranks among the most dramatic in Indian corporate history.

But what makes this story truly remarkable isn't the financial engineering or the stock price multiplication—it's the lesson about corporate mortality and rebirth. Companies, like organisms, can die and be reborn in entirely different forms. The Diamond Power of 2024 shares little with its 2014 predecessor except the physical assets and the name. Different owners, different strategy, different culture, different destiny.

If We Were CEOs: The Path Forward

Standing in the corner office at Vadodara, looking out at 110 acres of manufacturing capability, what would we do? The temptation would be to chase growth—announce grand expansion plans, diversify into adjacent products, perhaps even venture into EPC again. But that's exactly what killed the previous Diamond Power.

Instead, we'd focus on three strategic imperatives:

First, customer diversification with surgical precision. Not abandoning Adani—that would be suicidal—but systematically adding 2-3 large renewable developers each year. Target Tata Power Renewables, JSW Energy, ReNew Power. Offer them the same reliability and proximity that Adani enjoys. The goal: no single customer above 30% of revenues by 2027.

Second, technology partnerships over ownership. Rather than trying to develop cutting-edge technology internally, partner with global leaders. License HVDC conductor technology from General Cable. Joint venture for gas-insulated lines with a Japanese manufacturer. Let others bear the R&D cost while Diamond provides local manufacturing and market access.

Third, working capital optimization through supply chain finance. The biggest risk to Diamond's growth isn't demand—it's cash flow. Implement vendor financing programs, receivable factoring, and channel financing to reduce working capital from 180 days to 90 days. Every day of working capital saved is profit margin earned in a commodity business.

The Broader Implications

Diamond Power's resurrection signals something profound about India's corporate landscape. The IBC (Insolvency and Bankruptcy Code) is working. Assets are being recycled from weak hands to strong. Productive capacity is being preserved and revived. What was once a lengthy, value-destructive process has become a mechanism for corporate renewal.

For India's power sector, Diamond's revival couldn't be better timed. The country needs every bit of manufacturing capacity to support its energy transition. Having Diamond's 250,000 MT capacity back online meaningfully adds to national capability. It's industrial policy through market mechanisms.

The story also highlights the changing nature of Indian capitalism. The new promoters aren't industrialists in the traditional sense—they're financial engineers who saw value where others saw wreckage. This financialization of industry brings efficiency but also raises questions about long-term commitment to manufacturing excellence.

Lessons for Entrepreneurs

For entrepreneurs, Diamond Power offers sobering lessons about leverage and growth. The Bhatnagar family built for 40 years and lost everything in 4. The culprit wasn't competition or technology disruption—it was debt. In capital-intensive businesses, the balance sheet is destiny.

The resurrection also shows that failure isn't final if the underlying assets have value. The Bhatnagars lost ownership but the company survived, jobs returned, and industrial capability was preserved. There's dignity in building something that outlasts the builder, even if the builder doesn't reap the ultimate rewards.

What the Future Holds

Can Diamond Power become a T&D major again? The ingredients are there—manufacturing capability, market opportunity, and strategic backing. But history suggests the path from ₹1,000 crore to ₹10,000 crore revenue is littered with failures. Scale brings complexity that often overwhelms companies that grew too fast.

More likely, Diamond Power finds its niche as a regional champion—the preferred conductor and cable supplier for renewable projects in Western India. There's no shame in that. In a ₹50,000 crore market growing at 15% annually, even a 5% share means a ₹2,500 crore business.

The ultimate test will come during the next downturn. Every infrastructure business eventually faces a cycle turn. When order books dry up, working capital stretches, and margins compress, will the new Diamond Power show the discipline to survive? Or will they repeat their predecessors' mistakes?

Final Reflections

Corporate resurrections are rare because they require a unique confluence of factors—good assets in bad balance sheets, patient capital with vision, market timing, and execution capability. Diamond Power had all four, plus the catalyst of India's renewable energy boom.

For investors who bought at the bottom, Diamond Power delivered life-changing returns. For those buying today, the story is more complex. The easy money has been made. What remains is a bet on execution, relationship stability, and market growth—a very different risk-reward proposition.

The Diamond Power story ultimately reminds us that in business, as in nature, death and rebirth are part of the cycle. Companies that seem invincible can collapse overnight. Companies given up for dead can roar back to life. The key is recognizing which phase of the cycle you're in and positioning accordingly.

As the sun sets over the Savli factory, machines humming with renewed life, one can't help but wonder: Is this resurrection sustainable, or just another chapter in an ongoing cycle of boom and bust? Only time will tell. But for now, the phoenix flies.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube