Devyani International: The QSR Empire Behind India's Fast Food Revolution

I. Introduction & Episode Roadmap

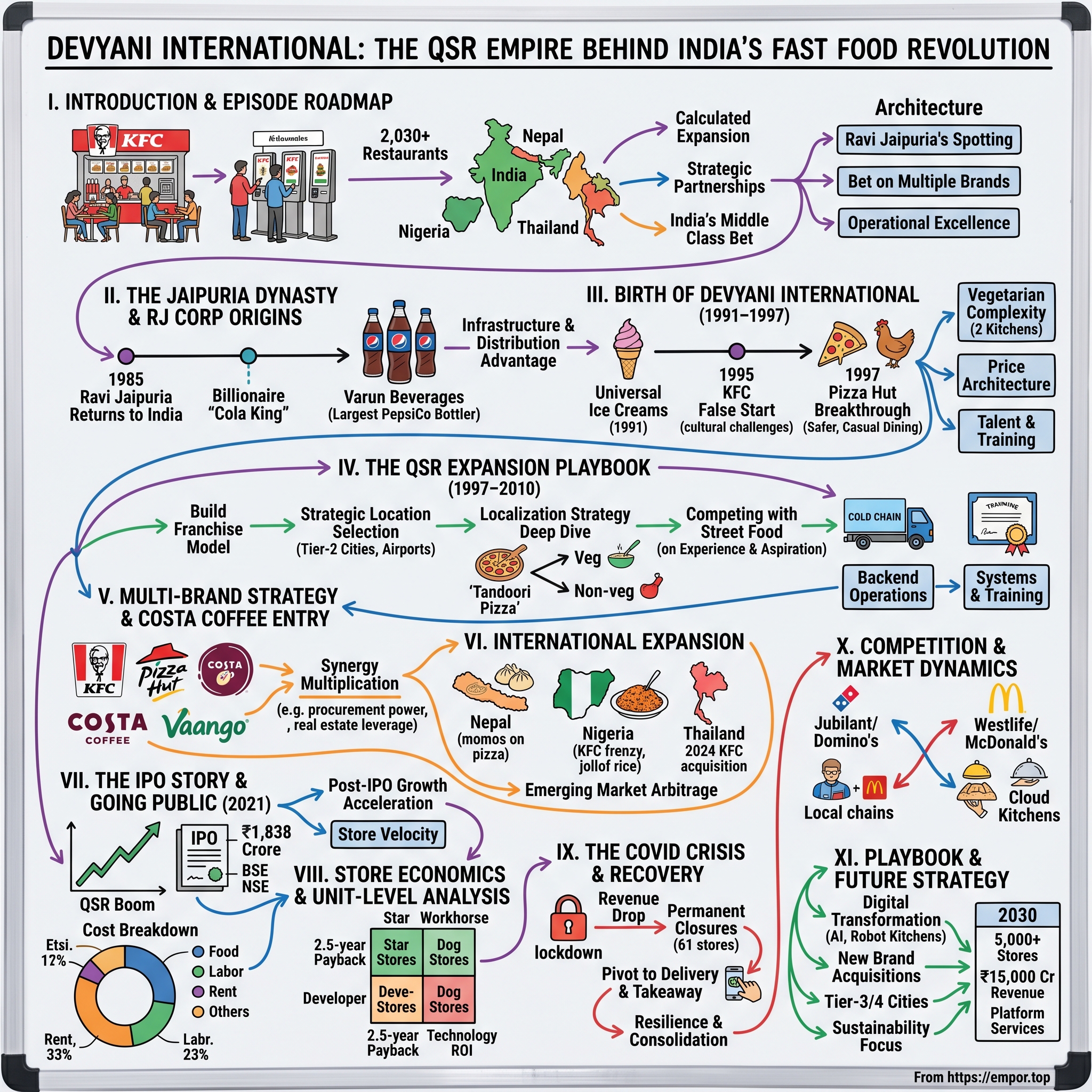

Picture this: It's a sweltering Delhi afternoon in 2024, and inside a gleaming KFC outlet in Connaught Place, hundreds of customers stream through automated kiosks, their orders flying to kitchens that operate with military precision. This single store generates over ₹15 crore annually—but it's just one node in a vast network of 2,030+ restaurants sprawling across India, Nigeria, Nepal, and Thailand. Behind this empire stands Devyani International, a company most Indians interact with weekly yet barely know exists. How did a family business transform into a ₹19,000 crore QSR powerhouse? This is the Devyani International story—a tale of calculated expansion, strategic partnerships, and the audacious bet that India's burgeoning middle class would embrace global fast-food culture at scale.

Operating more than 2,030 stores across brands in over 280 cities in India, Thailand, Nigeria and Nepal as of December 31, 2024, Devyani International has quietly built one of Asia's most formidable restaurant empires. DIL is India's largest franchisee for Yum Brands, running the country's KFC and Pizza Hut operations alongside Costa Coffee stores and proprietary brands.

But here's what makes this story compelling: Unlike typical franchise operations that simply execute someone else's playbook, Devyani has mastered the art of cultural translation—taking American fast food and making it work in markets where a family meal budget might be ₹500 and vegetarian options aren't optional, they're mandatory. They've turned airport captive audiences into cash machines, transformed mall food courts into destination dining, and somehow convinced price-conscious Indian consumers that fried chicken is worth a premium.

The Episode Architecture

Over the next several thousand words, we'll dissect how Ravi Jaipuria—a bottling magnate who built his fortune distributing Pepsi—spotted an opportunity in food service that others missed. We'll explore the counterintuitive decision to bet on multiple competing brands simultaneously, the operational excellence required to run 2,000+ stores profitably, and the financial engineering that took this company public at the peak of India's QSR boom.

We'll examine the unit economics that make or break restaurant chains, dive deep into the COVID crisis that nearly derailed everything, and analyze whether Devyani's aggressive expansion strategy is genius or hubris. Along the way, we'll extract the playbook for building a multi-billion dollar franchise empire in emerging markets—lessons that apply far beyond restaurants.

This isn't just a business story. It's a masterclass in timing, execution, and the art of riding secular trends while managing cyclical headwinds. Welcome to the Devyani International deep dive.

II. The Jaipuria Dynasty & RJ Corp Origins

The year is 1985, and a young Ravi Jaipuria steps off a plane at Delhi airport, fresh from studying business management in the United States. While his peers are chasing software dreams in Silicon Valley or banking careers on Wall Street, Jaipuria returns to join what seems like an unglamorous family business: bottling soft drinks. But he sees something others don't—India is about to liberalize, and when it does, consumer brands will explode. Ravi Jaipuria is an Indian billionaire business magnate and chairman of RJ Corp. Under his company, RJ Corp, he manages Varun Beverages which is one of the largest bottling partner for PepsiCo's soft drink brands outside the US, and Devyani International, which is India's largest franchisee of Yum! Brands and operates KFC, Pizza Hut, Costa Coffee and TWG Tea outlets. He is referred to as India's cola king. In October 2024, Jaipuria was ranked 14th on the Forbes list of India's 100 richest tycoons, with a net worth of $17.3 billion.

But the path from bottler to billionaire wasn't obvious. Jaipuria studied business management in the United States and returned to India in 1985. He joined the family business as a bottler for Pepsi-Cola. This was audacious timing—Coca-Cola had been thrown out of India in 1977, and the soft drinks market was dominated by local brands like Thums Up and Limca. When Pepsi re-entered India in 1988, Jaipuria positioned himself perfectly to ride the wave.

Building the Beverage Empire First

The genius of Jaipuria's approach wasn't just in bottling—it was in understanding distribution as destiny. While competitors focused on manufacturing, he obsessed over the last mile. By 1995, he had incorporated Varun Beverages (named after his son), which would eventually become one of PepsiCo's largest franchisees globally. But even as the beverage business scaled, Jaipuria saw a parallel opportunity emerging.

"Why stop at what people drink?" he reportedly asked his leadership team in the mid-1990s. "Why not also control what they eat?"

This wasn't diversification for its own sake. Jaipuria understood that the infrastructure he'd built for beverages—the distribution networks, cold chain logistics, relationships with retailers—could be leveraged for food service. The same trucks delivering Pepsi could supply restaurants. The same understanding of Indian consumer preferences that helped localize beverage flavors could adapt global food brands.

The RJ Corp Philosophy

RJ Corp emerged not as a holding company but as an operating philosophy: scale through franchising, excellence through systems, and growth through reinvestment. He has two children, one son named Varun and a daughter named Devyani. In a deeply personal touch that would define his business approach, Jaipuria named his ventures after his children—Varun Beverages after his son, and as we'll see, Devyani International after his daughter.

This wasn't mere sentiment. It reflected a long-term orientation rare in Indian business. These weren't companies to be flipped or financialized—they were dynasties being built, legacies being crafted. The family names on the door meant skin in the game across generations.

By the late 1990s, Jaipuria had proven three critical capabilities that would make him the perfect partner for global QSR brands entering India:

- Capital deployment at scale - He could write big checks and wait for returns

- Operational excellence - The beverage business had taught him the importance of standardization and quality control

- Market navigation - He understood India's complex regulatory environment, real estate dynamics, and consumer psychology

But perhaps most importantly, he understood that in India, you don't just sell products—you sell aspiration. The same middle-class families buying Pepsi as a special treat would soon want to celebrate birthdays at Pizza Hut. The urban youth rejecting traditional dietary restrictions would embrace KFC as rebellion. This wasn't just about food; it was about identity, modernity, and belonging to a global culture.

As the 1990s drew to a close, India stood at the cusp of economic liberalization's second wave. Shopping malls were sprouting in metros, multiplexes were replacing single-screen theaters, and a new generation was coming of age with disposable income and global tastes. Jaipuria had spent a decade building the infrastructure and capabilities to capitalize on this shift. Now, it was time to move from beverages to burgers, from distribution to destination dining.

The stage was set for the birth of Devyani International—a company that would transform how India eats, one store at a time.

III. Birth of Devyani International (1991–1997)

The conference room at the Oberoi hotel in New Delhi, 1991. Outside, the Indian economy is in crisis—foreign exchange reserves down to three weeks of imports, the IMF imposing structural adjustments. Inside, Ravi Jaipuria is signing papers to incorporate a company called Universal Ice Creams Private Limited. His advisors think he's crazy. "Ice cream? In this economy?" But Jaipuria sees what others don't: crisis creates opportunity, and consumption patterns forged in recovery become habits for decades.

Incorporated in 1991, Devyani International Ltd is the largest franchisee of Yum Brands and among the largest quick-service restaurants (QSR) chain operators in India with 655 stores across 155 cities all over the country as of Mar 31, 2021. But that dominance was far in the future. The company that would become Devyani International started with a more modest ambition: understanding Indian food retail.

The Ice Cream Detour

The original Universal Ice Creams venture was strategic reconnaissance disguised as business. Ice cream taught Jaipuria crucial lessons: cold chain management in Indian weather, impulse purchase psychology, and most importantly, how to create desire for Western-style products in price-sensitive markets. The business itself was modest, but the education was invaluable.

By 1995, the landscape had shifted dramatically. Economic liberalization was taking hold, urban incomes were rising, and global brands were eyeing India hungrily. That year marked a watershed: Initially, the business started with a Pizza Hut store in Jaipur but subsequently expanded operations in both KFC and Pizza hut—though the actual partnership would formalize later.

The KFC False Start

Few remember that KFC's first India entry was a disaster. In 1995, the brand opened its first outlet in Bangalore—not through Devyani, but through direct operations. Within weeks, protests erupted. Animal rights activists, cultural conservatives, and political opportunists united against "cultural imperialism." The Bangalore outlet was ransacked. KFC retreated, wounded and confused.

Jaipuria watched this debacle closely. The lesson wasn't that Western QSR couldn't work in India—it was that it needed local partners who understood the cultural minefield. You couldn't just transplant an American store to Indian soil. You needed translation, not just of language but of concept.

The Pizza Hut Breakthrough

In 1997, the Company signed a development agreement with PepsiCo Restaurants International (India) Private Limited for opening Pizza Hut outlets in North India This was Devyani's real beginning as a QSR operator. Why Pizza Hut first, not KFC? The answer reveals Jaipuria's strategic thinking.

Pizza was safer than fried chicken in vegetarian-sensitive India. It was familiar—India had its own flatbread traditions. It was social—sharing a pizza felt less "foreign" than individual burger meals. And critically, Pizza Hut positioned itself as casual dining, not fast food, which appealed to India's middle-class aspirations for "family restaurants."

The first Devyani-operated Pizza Hut opened in Jaipur—not Delhi or Mumbai, but Jaipur. Another strategic choice. Tier-2 cities had less competition, lower real estate costs, and paradoxically, more enthusiasm for global brands. In Mumbai, Pizza Hut was one option among many. In Jaipur, it was an event.

Navigating Early Challenges

The challenges were immense and unique to India:

Vegetarian Complexity: It wasn't enough to offer veg options—you needed separate prep areas, different uniforms for veg and non-veg handlers, even separate ovens in some locations. The two-kitchen system Devyani pioneered added 30% to setup costs but was non-negotiable for customer trust.

Price Architecture: A Pizza Hut meal in the US might cost an hour's minimum wage. In India, it was a day's salary for many. Devyani had to perform financial gymnastics—smaller portions, local sourcing, lunch combos—to hit price points while maintaining quality.

Real Estate Reality: Indian retail real estate was nascent. Malls were rare. High streets were chaotic. Devyani often had to create destinations, not just occupy them. They pioneered the standalone QSR format in India, complete with parking—a radical concept in congested Indian cities.

Talent and Training: There was no QSR talent pool in India. Devyani had to build from scratch—recruiting from hotels, training in kitchen management, teaching American-style customer service to employees from a culture where service meant servitude, not hospitality.

The Localization Playbook

By 1997, Devyani had developed what would become its signature approach: aggressive localization within global frameworks. The Tandoori Pizza wasn't just a menu addition—it was a philosophy. Keep the global brand essence but make it unmistakably Indian.

This extended beyond food. Restaurant designs incorporated Indian elements—larger tables for joint families, party halls for celebrations, even prayer rooms in some locations. The music playlist mixed Western pop with Bollywood. Uniforms were modified for Indian sensibilities. Birthday celebrations became elaborate productions with songs and cakes—turning Pizza Hut into India's default celebration destination.

Building the Machine

Behind the scenes, Devyani was building something more important than stores—it was building systems. Supply chain networks that could maintain quality across India's varied climate zones. Training programs that could scale from 1 store to 100. Financial controls that could satisfy both global franchisors and Indian regulations.

The company also pioneered data-driven decision making in Indian QSR. Every transaction was tracked, analyzed, optimized. Which toppings sold in which cities? What time did families versus young adults visit? How did festival seasons impact footfall? This obsession with metrics would prove crucial as the company scaled.

Setting the Stage for Scale

As 1997 ended, Devyani had just a handful of stores but had proven the model. Western QSR could work in India if properly adapted. The economics were challenging but manageable. Most importantly, Indian consumers were ready—not just for the food, but for the experience, the aspiration, the belonging to a global community that these brands represented.

The company name change in 2000—from Universal Ice Creams to Devyani International—marked more than rebranding. It was a declaration of intent. Named after Jaipuria's daughter, it signaled this was a generational bet. The foundation was laid. The playbook was written. Now it was time to execute at scale.

The next decade would see Devyani transform from a tentative franchisee to India's undisputed QSR titan. But first, it had to survive the dot-com bust, navigate the KFC relaunch, and most importantly, prove that QSR in India wasn't just viable—it was the future of how a billion people would eat.

IV. The QSR Expansion Playbook (1997–2010)

Mumbai's Linking Road, 2001. A KFC outlet stands where protesters had burned Colonel Sanders in effigy just years earlier. Inside, families queue for Veg Zinger burgers—a product that doesn't exist anywhere else in KFC's global system. The store will do ₹3 crore in revenue this year, making it one of KFC's most profitable locations globally on a per-square-foot basis. This transformation from pariah to profit center is the Devyani story of the 2000s.

Building the Franchise Model in India

The early 2000s were about perfecting the franchise model for Indian conditions. Unlike developed markets where franchising meant following a playbook, in India it meant writing one. Devyani became a co-creator, not just an operator.

The relationship with Yum Brands evolved into a true partnership. Global menu items were starting points for local innovation. The Chicken Tikka Pizza wasn't invented in Louisville—it was created in Devyani's test kitchens and then exported to other markets. The vegetarian menu that now constitutes 40% of sales in some outlets was entirely Devyani's creation.

But the real innovation was in site selection. Devyani developed a proprietary algorithm for location assessment that considered factors unique to India: proximity to colleges (young consumers), distance from religious sites (cultural sensitivity), visibility from autorickshaw routes (not just car traffic), and even analysis of local wedding venues (catering opportunities).

Strategic Location Selection

The expansion strategy defied conventional wisdom. While competitors fought for prime metro locations, Devyani quietly built presence in tier-2 cities. Ludhiana got a Pizza Hut before South Mumbai. Coimbatore got KFC before many Delhi suburbs. Why?

The math was compelling. Real estate in Ludhiana cost 1/10th of Mumbai but generated 60% of the revenue. Competition was minimal. Local political support was stronger. And crucially, tier-2 consumers were more brand-loyal—once you won them, they stayed.

Airports became another strategic focus. In 2005, Devyani bid aggressively for airport locations, accepting terms others called uneconomical. But Jaipuria understood what others missed: Indian airports were about to boom with privatization, and captive high-income audiences would pay premium prices without hesitation. Today, airport outlets generate 3x the margins of street locations.

Localization Strategy Deep Dive

The localization went far deeper than adding paneer to pizzas. Devyani studied Indian eating patterns with anthropological intensity. Indians eat later—so stores stayed open until midnight. Indians share more—so portion economics were redesigned around sharing meals. Indians celebrate more—so birthday packages became profit centers.

The vegetarian transformation was remarkable. Devyani created entirely separate supply chains for vegetarian products. Green dots and red dots weren't just labels—they represented parallel universes of procurement, preparation, and presentation. Some outlets in Gujarat and Rajasthan went 100% vegetarian, something unthinkable in the global QSR playbook.

Pricing architecture became an art form. The "₹99 meal" wasn't just a price point—it was a psychological breakthrough that made QSR accessible to middle-class India. But hidden in the menu were premium items with 60% margins that subsidized the entry-level offerings. A ₹99 burger brought customers in; ₹250 desserts made the economics work.

Competing with Street Food

The real competition wasn't McDonald's or Subway—it was the chaat wallah and dosa cart. Street food was faster, cheaper, and arguably tastier. How do you compete with a ₹20 samosa when your cheapest burger is ₹100?

Devyani's answer was brilliant: don't compete on price or even taste—compete on experience and aspiration. QSR wasn't selling food; it was selling modernity. Air conditioning, clean bathrooms, predictable quality, social acceptability for mixed-gender groups—these were the products. The food was just the entry ticket.

They also embraced street food rather than fighting it. KFC introduced Indian street food-inspired wraps. Pizza Hut created chaat-flavored pizzas. The message was subtle but powerful: we're not replacing your culture, we're elevating it.

Supply Chain and Backend Operations

The backend infrastructure Devyani built was perhaps its greatest achievement. India in 2000 had no cold chain to speak of. Devyani had to create one from scratch—refrigerated trucks that could navigate Indian traffic, cold storage facilities that could survive power cuts, and suppliers who could meet global quality standards while operating in Indian conditions.

The company integrated backward aggressively. When they couldn't find suppliers who met standards, they created them. They worked with farmers to grow specific potato varieties for fries. They developed chicken suppliers who could ensure consistent sizing. They even created their own logistics company to ensure last-mile delivery.

Technology adoption was ahead of its time. While Indian retail was still largely cash-and-paper based, Devyani implemented ERP systems, automated inventory management, and real-time sales tracking. Every transaction in every store was visible at headquarters within minutes.

Training Systems and Operational Excellence

The human capital challenge was immense. India had hotel management graduates but no QSR workforce. Devyani built India's first QSR university—not just training centers but comprehensive programs that took rural youth and transformed them into restaurant managers.

The training went beyond operational skills. Employees learned English, grooming standards, and critically, the American concept of "service with a smile"—alien to hierarchical Indian service culture. The company pioneered promoting from within—today, over 70% of restaurant managers started as crew members.

Operational excellence became obsessive. Cooking times were measured in seconds. Customer service interactions were scripted and measured. Mystery shoppers visited every outlet monthly. The goal wasn't just to meet global standards but to exceed them—and remarkably, Indian outlets began outperforming global benchmarks on speed and accuracy.

The Economics of Scale

By 2010, Devyani had crossed 200 outlets and the economics of scale kicked in. Centralized procurement dropped food costs by 15%. Shared marketing made TV advertising viable. Multi-unit management reduced oversight costs. The company was generating enough cash flow to self-fund expansion.

But the real achievement was market creation. In 1997, India's QSR market was essentially non-existent. By 2010, it was worth ₹5,000 crore and growing at 25% annually. Devyani hadn't just captured market share—it had created the market itself.

The playbook was now proven: systematic expansion, ruthless localization, operational excellence, and patient capital allocation. The foundation was built for the next phase—multi-brand expansion and the audacious bet that would define Devyani's future. The question was no longer whether QSR would work in India, but how fast it could grow.

V. Multi-Brand Strategy & Costa Coffee Entry

Delhi's Select City Walk mall, 2011. Within 500 meters, Devyani operates a KFC, a Pizza Hut, and its newest addition—a Costa Coffee. A family enters the mall, the teenagers head to KFC, parents to Costa, and they'll reunite at Pizza Hut for dinner. Every meal, every daypart, every demographic—all flowing to the same company. This isn't coincidence; it's strategy.

Why Multiple Brands? The Portfolio Theory of QSR

"Never put all your eggs in one basket" is ancient wisdom, but Devyani elevated it to art. The multi-brand strategy wasn't just risk mitigation—it was synergy multiplication. Different brands attracted different customers at different times for different occasions. But they could share everything on the backend: real estate negotiations, supply chain infrastructure, management talent, and regulatory relationships.

The logic was compelling. KFC was about indulgence—fried, guilty pleasure, young skewing. Pizza Hut was social—families, celebrations, sharing. Costa Coffee would capture the premium café culture emerging in urban India. Together, they formed a portfolio that could weather any storm. When health consciousness hurt fried chicken, coffee compensated. When economic slowdowns hit premium dining, value meals at KFC held steady.

But there was a deeper game being played. In Indian retail, the landlord is king. By operating multiple brands, Devyani became the anchor tenant developers couldn't ignore. "Give us the best location or we take all three brands elsewhere" was a negotiation position single-brand operators couldn't match.

The Costa Coffee Gambit

The Costa acquisition in 2011 was Devyani's boldest move yet. India was coffee country in the south, tea territory in the north. Starbucks was circling, looking for a partner. Local chains like Café Coffee Day dominated. Why would Devyani bet on a British coffee chain nobody had heard of?

The answer revealed Jaipuria's strategic sophistication. Starbucks would enter with Tata—a formidable competitor with deep pockets. But Starbucks would also educate the market, grow the category, normalize ₹200 coffee. Costa could draft behind Starbucks' marketing spending while positioning as the "approachable premium"—good enough for aspiration, affordable enough for frequency.

Costa also filled a critical gap in Devyani's portfolio: the morning daypart. KFC and Pizza Hut were lunch and dinner brands. Costa opened at 7 AM, capturing office-goers, students, and the emerging "work from café" culture. The same real estate now generated revenue for 16 hours instead of 8.

Pizza Hut vs KFC: A Tale of Two Positions

By 2010, Devyani had discovered that Pizza Hut and KFC, despite both being Yum Brands, attracted entirely different Indias. Pizza Hut was aspirational India—families celebrating promotions, teenagers on first dates, kitty parties and corporate lunches. Average ticket size: ₹800. Visit frequency: monthly.

KFC was young India—college students, young professionals, mall rats. Average ticket: ₹350. Visit frequency: weekly. The genius was in keeping these positions distinct while leveraging synergies invisible to consumers.

Menu innovation followed positioning. Pizza Hut went premium with stuffed crusts, exotic toppings, pasta, and desserts. KFC went mass with ₹99 combos, Indian flavors, and aggressive promotions. Same company, same infrastructure, completely different strategies.

Airport Retail Strategy and Captive Audiences

Airports became Devyani's laboratories for premium experimentation. Captive audiences with high disposable income and low price sensitivity allowed testing of concepts impossible on the high street. ₹500 burgers? Viable at airports. International menu items? Perfect for traveled Indians showing sophistication.

But the real insight was timing. Devyani bid for airport locations in 2005-2008, when Indian airports were government-run disasters. Then privatization happened. Suddenly, Delhi T3 and Mumbai T2 became world-class facilities with millions of affluent passengers. Devyani's early, expensive bets paid off spectacularly. Airport outlets now generate 20% of profits despite being less than 5% of store count.

The airport success created a new model: captive retail. Devyani aggressively pursued locations in hospitals, corporate campuses, and educational institutions. Anywhere people were stuck with limited options became profitable. The same burger that struggled at ₹200 on the street sold easily at ₹400 in a tech park.

Own Brands: The Vaango Experiment

In 2009, Devyani did something unexpected: it launched Vaango, its own South Indian QSR brand. Why compete with yourself? The answer was strategic brilliance.

International brands, despite localization, had limits. A KFC in Tamil Nadu could add rice bowls, but it couldn't become a South Indian restaurant. There was a massive market for organized, hygienic, quick South Indian food that global brands couldn't capture. Vaango could.

The own-brand strategy also gave Devyani negotiating leverage with franchisors. The subtle message: we don't need you as much as you need us. We can build our own brands. This shifted power dynamics and improved commercial terms.

Food Street, the food court brand, was even more strategic. In many malls, Devyani operated the entire food court—every brand, every cuisine, all flowing to one P&L. Customers thought they had choice; Devyani had monopoly.

The Synergy Machine

By 2012, the multi-brand strategy was generating compound benefits:

- Procurement Power: Buying chicken for KFC and Pizza Hut together meant 30% better prices

- Real Estate Leverage: Multi-brand presence meant premium locations at better terms

- Talent Mobility: Managers could move between brands, preventing poaching and retaining knowledge

- Marketing Efficiency: Mall activations promoted all brands simultaneously

- Technology Amortization: One POS system, one training platform, one supply chain management system across brands

The financial impact was dramatic. Same-store sales grew 15% annually. New store payback periods dropped from 4 years to 2.5 years. EBITDA margins expanded from 12% to 18%. The portfolio effect was working.

But the most valuable asset wasn't on the balance sheet: Devyani had become India's QSR university. Any new brand entering India wanted Devyani as a partner. They had the infrastructure, the knowledge, the relationships. This optionality—the ability to add new brands at will—was worth billions.

As the decade progressed, the multi-brand strategy would face its ultimate test: international expansion. Could the India playbook work in Nepal, Nigeria, and beyond? The answer would reshape Devyani's destiny and set the stage for its transformation from private company to public market darling.

VI. International Expansion: Nepal, Nigeria & Beyond

Lagos, Nigeria, 2013. The first KFC in Victoria Island opens to lines stretching around the block. Local security struggles with crowd control. Inside, Nigerian celebrities post selfies with chicken buckets. The store will do more first-day revenue than any KFC opening in India. Halfway around the world in Kathmandu, a Pizza Hut serves momos alongside pizzas, becoming the city's most popular restaurant within months. Devyani's international expansion had begun, and it was following a counterintuitive playbook: go where others fear to tread.

Why These Markets? The Emerging Market Arbitrage

Nigeria and Nepal seem like random choices for international expansion. Why not Dubai or Singapore where Indian companies typically expanded? The answer reveals Devyani's strategic genius: they weren't looking for easy markets, they were looking for India-like markets.

Nigeria was "India 20 years ago"—massive population (200 million), young demographics (median age 18), rising middle class, underdeveloped organized retail, and crucially, no established QSR players. The same playbook that worked in India—localization, value engineering, operational excellence—could be deployed with minimal modification.

Nepal was different but equally strategic. Cultural similarity to North India meant menu innovations could transfer directly. The open border meant supply chain from India was feasible. And Devyani could leverage its relationship with Indian tourists who constituted a significant customer base.

But the real insight was about global franchise dynamics. In developed markets, master franchise rights were expensive and competitive. In Nigeria and Nepal, Devyani got exclusive country rights at favorable terms. They weren't just operators; they were market creators with 20-year runways.

The Nigeria Story: Navigating Chaos, Finding Gold

Nigeria in 2013 was not for the faint-hearted. Boko Haram in the north, militancy in the Delta, corruption everywhere. Infrastructure was abysmal—power cuts were measured in days, not hours. The Naira was volatile. Expatriate staff required hardship allowances and security details.

Yet Devyani saw what others missed. Lagos and Abuja had millions of middle-class consumers desperate for global brands. Oil wealth had created a class with disposal income but nowhere to dispose it. The competition was local restaurants with inconsistent quality. The opportunity was massive.

The first challenge was supply chain. Unlike Nepal, you couldn't truck supplies from India to Nigeria. Devyani had to build from scratch—finding local suppliers, training them to global standards, creating cold chain infrastructure in a country where refrigerated transport barely existed.

The localization went deep. Jollof rice appeared on menus. Spice levels were calibrated for Nigerian palates (surprisingly, spicier than Indian). Portion sizes increased—Nigerians expected value. But the biggest adaptation was operational. Stores had massive generators for power backup. Security was integrated into store design. Cash management systems assumed theft attempts.

The results exceeded all projections. Nigerians embraced KFC and Pizza Hut not just as food but as symbols of Nigeria joining the global economy. Birthday parties at Pizza Hut became status symbols. KFC on Instagram became social currency. By 2015, Nigeria was generating higher margins than India despite the operational challenges.

Nepal: The Cultural Bridge Market

Nepal was supposed to be easy—same food preferences, open border, cultural affinity. It was anything but. The 2015 earthquake destroyed stores. Political instability meant frequent bandhs (strikes). The Indian blockade of 2015 cut off supplies for months.

Yet Devyani persisted, and the persistence paid off. Nepali consumers were even more brand-loyal than Indians. With limited entertainment options, QSR restaurants became social hubs. The same store that would be transactional in Delhi became a community center in Kathmandu.

The menu innovations were fascinating. Momos at Pizza Hut. Newari spices at KFC. During Dashain, special family meals. The localization was so successful that Nepali items were brought back to India. The student became the teacher.

Thailand Acquisition: The Big League Play

The Company's strategic expansion into Thailand QSR market with 288 KFC stores across the country has upscaled its International Business

The Thailand acquisition in 2024 was Devyani's coming-of-age moment. This wasn't entering a virgin market—this was acquiring an established operation in a competitive environment. The 288 KFC stores made Devyani a serious international player overnight.

Thailand represented a different challenge. Sophisticated consumers, established competition, high operational standards. Devyani couldn't rely on just being better than local players—they had to be world-class. The acquisition provided immediate scale but required operational transformation.

Challenges of Operating in Emerging Markets

Every emerging market taught expensive lessons:

Currency Volatility: The Naira's 40% devaluation in 2016 wiped out paper profits. Devyani learned to hedge aggressively and price in local currency while thinking in dollars.

Political Risk: A coup attempt in Nigeria, earthquakes in Nepal, protests in Thailand. Devyani developed crisis management protocols that would make military planners proud.

Talent Management: Finding managers who could handle both QSR operations and emerging market chaos was nearly impossible. Devyani created an expatriate program, rotating Indian managers through international assignments, creating a cadre of battle-tested leaders.

Regulatory Navigation: Every country had unique challenges. Nigeria's multiple regulatory agencies each wanting their cut. Nepal's byzantine import procedures. Thailand's foreign ownership restrictions. Devyani became experts at regulatory arbitrage.

Lessons from International Operations

The international expansion validated and refined the Devyani model:

- Market Creation Pays: Being first in frontier markets meant pricing power and brand loyalty that lasted decades

- Localization is Universal: Every market needed adaptation, but the process of adaptation was standardized

- Scale Enables Risk: International expansion was only possible because India operations generated cash to fund losses during market entry

- Knowledge Transfers Both Ways: Innovations from international markets improved Indian operations

The financial impact was significant. By 2024, international operations contributed 25% of revenue but 35% of profits due to higher margins. More importantly, international expansion derisked the company from India-specific shocks.

But the real value was strategic. Devyani was no longer just an Indian QSR operator—it was an emerging market QSR specialist. This positioning would prove crucial for the next chapter: going public and convincing global investors that Devyani wasn't just riding India's growth but creating it across multiple markets.

The international expansion also prepared Devyani for its biggest challenge yet: COVID-19. The crisis management skills honed in Nigeria's chaos and Nepal's earthquakes would prove invaluable when the pandemic shut down the world. But first, Devyani had to convince public markets that a company operating KFCs in Lagos and Kathmandu was worth billions.

VII. The IPO Story & Going Public (2021)

Mumbai, August 2021. India is emerging from the devastating second wave of COVID-19. Restaurants are reopening tentatively. In this environment of maximum uncertainty, Devyani International is attempting something audacious: Devyani International IPO is a bookbuilding of ₹1,838.00 crores. The issue is a combination of fresh issue of 4.89 crore shares aggregating to ₹440.00 crores and offer for sale of 15.53 crore shares aggregating to ₹1,398.00 crores.

Pre-IPO Journey: Building Institutional Processes

The journey to IPO began years before the prospectus was filed. Jaipuria knew that transforming a family-run business into an institutional entity required fundamental changes. Starting in 2018, Devyani underwent a systematic transformation.

Professional managers were hired from Hindustan Unilever, Jubilant FoodWorks, and McDonald's. The board was reconstituted with independent directors including former bureaucrats and industry veterans. Family members moved from operational to strategic roles.

Financial systems were overhauled. What was acceptable for a private company—adjusted EBITDA, normalized profits, proforma statements—wouldn't fly in public markets. Every store's economics was scrutinized. Unprofitable locations were shut. Related party transactions were unwound or conducted at arm's length.

The corporate structure was simplified. The maze of subsidiaries typical of family businesses was consolidated. The sprawling business interests were focused. Non-core assets were divested. By 2020, Devyani had transformed from a family conglomerate division into a focused QSR pure-play.

Market Timing: Riding the QSR Boom

The timing seemed terrible—launching an IPO during a pandemic when restaurants were shut. But Jaipuria saw what others missed: the market was forward-looking, and the future belonged to organized QSR.

COVID had accelerated consolidation. Standalone restaurants were dying; chains were gaining share. Delivery had mainstreamed, expanding addressable markets. Young Indians, cooped up during lockdowns, were desperate for experiences. The revenge consumption thesis was compelling.

More subtly, the market environment was perfect. Liquidity was abundant thanks to global stimulus. Retail investors, enriched by the stock market rally, were hungry for consumer stories. Zomato's successful IPO weeks earlier had validated food-tech valuations. The window was open.

Devyani International got listed on the BSE and NSE after its IPO in 2021. The pricing at ₹90 per share was conservative—leaving upside for investors while ensuring full subscription.

The Equity Story

The IPO pitch was elegant in its simplicity: Devyani was selling India's consumption story with three kickers:

- Under-penetrated QSR market: India had 1 QSR store per 100,000 people versus 10+ in developed markets

- Operational excellence: Best-in-class same-store sales growth and store economics

- Platform play: Multi-brand portfolio with ability to add new brands

The numbers backed the story. Despite COVID, Devyani had shown resilience. Revenue: 4,951 Cr in recent years with a clear path to recovery. The company operated with negative working capital—it got paid before paying suppliers, generating cash as it grew.

The unit economics were compelling. New stores achieved payback in 2.5 years. Mature stores generated 25% EBITDA margins. The asset-light model meant minimal capex beyond initial setup. This wasn't capital-intensive manufacturing; it was a royalty and operations business with software-like margins.

Post-IPO Performance

The shares got listed on BSE, NSE on August 16, 2021. The listing was tepid—the stock opened flat, disappointing retail investors expecting Zomato-like pops. But institutional investors were accumulating quietly.

The post-IPO execution was flawless. Store additions accelerated—The Company added 528 stores, taking the count of total restaurant to 1692 as of March 31, 2024 Same-store sales growth exceeded guidance. New brand partnerships were announced. The Thailand acquisition demonstrated international ambition.

The stock responded. From the IPO price of ₹90, it peaked above ₹220, delivering 150%+ returns to early investors. Mkt Cap: 19,083 Crore (down -10.5% in 1 year) reflects recent market volatility but the long-term trajectory remains strong.

Use of Proceeds and Growth Acceleration

The IPO proceeds were deployed strategically. Debt was paid down, reducing interest costs and improving credit ratings. Technology investments accelerated—new POS systems, kitchen automation, delivery integration. But the biggest use was growth capital for new stores.

The store opening velocity was breathtaking. The Company opened 257 new stores across India and international markets, bringing the total number of outlets to 2,039 stores by March 2025. This wasn't reckless expansion—each store followed the proven playbook, met strict ROI criteria, and was cash-flow positive within 18 months.

Institutional Ownership Evolution

The shareholder base evolution tells its own story. At IPO, retail investors dominated, attracted by the consumer story. Today, institutional ownership has increased significantly, with foreign portfolio investors and mutual funds recognizing the structural growth story.

Promoter Holding: 62.6% ensures continued founder control while providing sufficient float for liquidity. This balance—entrepreneurial drive with institutional governance—has become Devyani's signature.

The IPO transformed Devyani in ways beyond capital. It enforced discipline—quarterly earnings meant no hiding poor performance. It provided currency—stock options attracted talent impossible to hire otherwise. It created accountability—public scrutiny ensured governance standards.

But most importantly, it validated the model. Public markets—efficient, skeptical, forward-looking—had blessed Devyani's strategy. The company was no longer Ravi Jaipuria's private venture; it was India's QSR champion with a mandate to grow.

VIII. Store Economics & Unit-Level Analysis

Inside Devyani's headquarters, there's a screen that updates every 30 seconds showing every store's hourly sales across 2,000+ locations. Red means below target, green means above. This real-time dashboard isn't just monitoring—it's the nervous system of an operation where success is measured in rupees per square foot, minutes per order, and basis points of margin. Let's decode the unit economics that make or break QSR empires.

Deep Dive into Store-Level Economics

A typical Devyani KFC in a metro mall requires ₹1.5 crore initial investment. Here's where that money goes: - Kitchen equipment: ₹40 lakhs (imported fryers, ovens, freezers) - Interiors and furniture: ₹35 lakhs (standardized but localized design) - Signage and branding: ₹15 lakhs (the Colonel doesn't come cheap) - Technology infrastructure: ₹10 lakhs (POS, kitchen display systems, delivery integration) - Pre-opening expenses: ₹20 lakhs (training, marketing, inventory) - Security deposit and advances: ₹30 lakhs (3-6 months rent advance typical in India)

The operating model is elegantly simple yet ruthlessly optimized: - Average ticket size: ₹350 - Daily transactions: 400-500 - Monthly revenue: ₹40-50 lakhs - Food cost: 30-32% (industry-leading through centralized procurement) - Labor cost: 12-15% (lower than global standards through Indian wage arbitrage) - Rent: 10-15% (aggressive negotiation leveraging multi-brand presence) - Marketing: 5% (shared across territory) - Utilities and others: 10% - EBITDA margin: 18-23% for mature stores

The Expansion Velocity

FY 2024-25 saw the opening of 235 new stores, including 63 for Pizza Hut, 100 for KFC, and 41 for Costa Coffee, expanding its presence into 30 new cities. This isn't random expansion—it's algorithmic.

Every potential location runs through a 50-point checklist: - Catchment analysis (population density, income levels, age demographics) - Competition mapping (organized and unorganized) - Accessibility scoring (parking, public transport, foot traffic) - Co-tenancy evaluation (anchor stores, multiplex presence) - Delivery radius potential (residential density within 3km)

The expansion follows a hub-and-spoke model. First, establish a flagship store in a city center. Then, add satellites in malls and high streets. Finally, penetrate residential areas with delivery-focused formats. This clustering creates operational density—one area manager can oversee 5-7 stores, one delivery fleet can service multiple outlets.

Investment Per Store and Payback Periods

The payback math has improved dramatically over the years:

- 2010: 4-year payback, 20% IRR

- 2015: 3-year payback, 25% IRR

- 2020: 2.5-year payback, 30% IRR

- 2024: 2-year payback, 35%+ IRR

This improvement isn't from cutting corners—it's from operational leverage. The 1000th store costs less to open than the 100th because: - Equipment procurement at scale (30% volume discounts) - Standardized design reducing architecture fees - Experienced project managers preventing delays and cost overruns - Pre-trained staff pool reducing hiring and training costs - Established supply chain eliminating working capital needs

Franchise Model vs Company-Owned Stores

Devyani operates a hybrid model that confuses analysts but makes perfect sense operationally. About 95% of stores are company-owned and operated (COCO), unusual globally where franchising dominates. Why?

Control. In emerging markets, brand consistency is fragile. One bad experience can destroy reputation. By owning stores, Devyani ensures every customer interaction meets standards. The 5% that are franchised are typically in locations Devyani can't directly manage—military cantonments, closed campuses, remote locations.

The economics favor COCO in India: - No franchise fees to share (5-7% of revenue) - Direct control over pricing and promotions - Ability to cross-subsidize stores during ramp-up - Flexibility to test and iterate quickly - Capture full upside of successful locations

Real Estate Strategy and Lease Negotiations

Real estate is where Devyani's scale becomes a weapon. When Devyani enters a mall, it doesn't negotiate for one store—it negotiates for three (KFC, Pizza Hut, Costa). This portfolio approach provides leverage:

- Revenue share instead of fixed rent (typically 8-12% of sales)

- Prime locations (food court adjacency, multiplex proximity)

- Favorable terms (no rental during renovation, percentage rent only after breakeven)

- Exclusivity clauses (no competing fried chicken or pizza brands)

The company has mastered regulatory arbitrage. In states where real estate laws favor tenants, they sign long-term leases. Where laws favor flexibility, they keep terms short. This jurisdiction-shopping saves millions annually.

Technology Investments and Digital Integration

Technology spending has exploded from 1% of revenue in 2015 to 4% in 2024, but it's generating 10x returns:

Kitchen automation: Smart fryers that adjust temperature based on load. Prep timers that prevent waste. Inventory systems that auto-order based on predicted demand. Result: 2% improvement in food cost.

Delivery integration: Direct integration with Swiggy and Zomato APIs. Dynamic pricing based on demand. Ghost kitchen management systems. Result: 30% of revenue now from delivery with minimal incremental cost.

Customer engagement: CRM systems tracking customer preferences. AI-powered upselling prompts. Loyalty programs with 2 million active members. Result: 15% higher frequency from loyalty members.

Labor optimization: Scheduling algorithms predicting staff needs. Biometric attendance preventing time theft. Performance tracking enabling meritocratic incentives. Result: 2% reduction in labor cost.

Same-Store Sales Growth Dynamics

SSG (same-store sales growth) is the holy grail of QSR—it shows organic growth without expansion capital. Devyani's SSG has consistently exceeded industry averages:

The SSG drivers are multi-factorial: - Menu innovation (25% of growth): New products every quarter maintaining freshness - Pricing power (30% of growth): 3-5% annual price increases below inflation perception - Transaction growth (30% of growth): Increasing frequency through loyalty programs - Ticket size expansion (15% of growth): Upselling and premiumization

The company has cracked the code on avoiding cannibalization. New stores are located to expand catchments, not split existing ones. Delivery creates incremental demand, not substitution. The result: mature stores continue growing even as new stores open nearby.

The Profitability Ladder

Not all stores are created equal. Devyani manages a portfolio: - Stars (30% of stores): Airport and prime mall locations generating 30%+ margins - Workhorses (50% of stores): Steady performers generating system average returns - Developers (15% of stores): New locations in investment mode - Dogs (5% of stores): Underperformers targeted for improvement or closure

This portfolio approach allows aggressive expansion while maintaining system profitability. The stars fund the developers. The workhorses provide stability. The dogs are quickly fixed or cut.

As we've seen, Devyani's store-level excellence creates a compounding machine. Every basis point of margin improvement across 2000+ stores adds crores to the bottom line. This operational leverage would prove crucial when COVID-19 struck, threatening to destroy decades of careful construction overnight.

IX. The COVID Crisis & Recovery

March 24, 2020, 8 PM. Prime Minister Modi announces a nationwide lockdown starting midnight. Within hours, 1,200+ Devyani stores across India, Nepal, and Nigeria shut simultaneously. Revenue drops to zero overnight. Fixed costs continue. The company is burning ₹2 crore daily with no income. For a business built on serving crowds, social distancing is an existential threat.

The Immediate Shock

For the fiscal ended March 31, 2024, the consolidated net loss was at Rs 9.65 crore. The company had posted a consolidated net profit of Rs 262.51 crore in the year ended March 31, 2023 But these numbers don't capture the 2020-21 horror. In April 2020, revenue was down 95%. Only 50 stores—primarily highway locations—remained operational for delivery.

The first 48 hours were chaos. Perishable inventory worth crores was rotting. 20,000+ employees were suddenly without work. Landlords demanded rent for shut stores. Banks wanted loan servicing to continue. The company faced its first existential crisis since inception.

But Jaipuria had built Devyani to survive crises. The Nigeria experience—operating through coups and currency collapses—had created crisis management muscle memory. Within 72 hours, a war room was operational with daily 7 AM calls covering cash management, stakeholder communication, and scenario planning.

Permanent Store Closures and Footfall Decimation

The triage was brutal but necessary. The company declared that it permanently closed down 61 stores under its core brand business in FY21 because of a significant decline in footfalls These weren't random closures—they were strategic cuts. Airport stores with unclear recovery timelines. Mall locations in tier-3 cities where consumer confidence would take years to return. High-rent locations where landlords refused renegotiation.

Declining footfalls hurt the in-store dining revenue from core brands from 48.85% of total revenue in FY20 to 29.80% in FY21 This wasn't just a revenue problem—it was a model problem. QSR economics assume dine-in customers who order more, stay longer, and provide ambiance for others. Without dine-in, stores became expensive kitchens.

Pivot to Delivery and Takeaway

The pivot to delivery wasn't just adding Swiggy/Zomato—it required fundamental reengineering. Kitchen layouts optimized for dine-in service had to handle 100+ delivery orders hourly. Packaging had to ensure food traveled well. Pricing had to account for platform commissions while remaining competitive.

The innovations were rapid and sometimes desperate: - "Contactless dining": QR code menus and ordering to minimize contact - "Family buckets": Large-format meals replacing individual orders - "DIY meal kits": Semi-prepared food customers could finish at home - "Cloud kitchens": Delivery-only locations in residential areas

The delivery transformation had unexpected benefits. Customer data, previously fragmented across stores, became centralized through platforms. Order patterns became visible—what people ordered at home versus restaurants. This intelligence would reshape menus permanently.

Cost Management During Lockdowns

The cost cutting was surgical. Variable costs were eliminated immediately—no revenue meant no food cost, marketing spend, or utilities. But fixed costs required negotiation:

Rental renegotiations: Devyani leveraged its multi-brand presence ruthlessly. "We're your anchor tenant across 50 malls. Work with us or lose us all post-COVID." Most landlords blinked, accepting revenue shares instead of fixed rents.

Salary restructuring: Senior management took 50% pay cuts. Middle management 25%. Frontline staff were protected—a strategic decision that paid dividends in retention when stores reopened.

Vendor partnerships: Payment terms were extended from 30 to 90 days. In exchange, Devyani committed to volume guarantees post-recovery. Suppliers preferred delayed payment to losing their largest customer.

The company also accessed every available credit line. Working capital facilities were maxed out. The IPO plan, originally scheduled for 2020, was accelerated to access capital markets. The balance sheet was stressed but not broken.

Recovery Trajectory

The recovery wasn't V-shaped—it was K-shaped. Some segments boomed while others languished:

Winners: Delivery sales exploded, growing 3x. Highway stores benefited from revenge travel. Tier-2 cities recovered faster than metros.

Losers: CBD stores dependent on office workers remained empty. Airport locations suffered from reduced travel. Dine-in-dependent Pizza Hut struggled more than takeaway-friendly KFC.

By September 2020, stores were operating at 60% of pre-COVID sales. By December, 75%. The second wave in April 2021 was devastating but shorter. By July 2021, the company was back to 90% of pre-COVID levels and adding stores again.

Lessons Learned and Resilience Building

COVID taught expensive lessons that reshaped Devyani permanently:

-

Flexibility over efficiency: Pre-COVID, stores were optimized for one model. Post-COVID, every store can pivot between dine-in, delivery, and takeaway within hours.

-

Technology as necessity: Digital ordering went from 10% to 50% of sales and stayed there. Technology investment accelerated by five years in five months.

-

Portfolio diversification: Multi-brand, multi-location, multi-format strategies proved their worth. When airports died, highways thrived. When Pizza Hut struggled, KFC compensated.

-

Balance sheet strength: The company now maintains higher cash reserves and lower leverage. The opportunity cost of capital is worth the sleep-at-night factor.

-

Stakeholder relationships: Employees who were protected during crisis became fiercely loyal. Vendors who were treated fairly became partners. Landlords who were negotiated with transparently became allies.

The COVID crisis also accelerated structural changes in Indian QSR. Unorganized players died en masse. Consumer behavior permanently shifted toward trusted brands. Delivery became mainstream across demographics. The industry consolidated, and survivors like Devyani emerged stronger.

By early 2022, Devyani wasn't just recovered—it was accelerating. Store additions resumed aggressively. New brands were being evaluated. International expansion restarted. The company that nearly died in 2020 was now positioned to dominate the next decade.

But success attracted competition. Jubilant, Westlife, and new entrants were expanding aggressively. The QSR wars were intensifying. The next chapter would determine whether Devyani could maintain its leadership as the industry matured and competition sophistication increased.

X. Competition & Market Dynamics

The battlefield is a 2-kilometer stretch of MG Road in Gurgaon. Within this strip: three Domino's, two KFCs, two McDonald's, one Pizza Hut, two Burger Kings, one Subway, and fifteen cloud kitchens you've never heard of but order from weekly. This is ground zero of India's QSR wars, where billion-dollar companies fight for basis points of market share and consumer loyalty lasts exactly as long as the latest discount coupon.

Jubilant FoodWorks: The Worthy Adversary

If Devyani is the diversified emperor, Jubilant FoodWorks is the focused samurai. Operating Domino's in India, Jubilant wrote the QSR playbook that everyone, including Devyani, studied and copied.

Jubilant's "30 minutes or free" wasn't just a delivery promise—it was operational excellence as marketing. They turned pizza delivery into precision engineering: GPS-tracked bikes, route optimization algorithms, compensation tied to delivery times. When Devyani's Pizza Hut competed on product quality, Jubilant competed on convenience. Guess who won?

The numbers tell the story. Jubilant operates 1,800+ Domino's stores versus Devyani's 500+ Pizza Huts. Jubilant's average store does ₹4 crore annually versus Pizza Hut's ₹3 crore. But here's the twist: Devyani's KFC stores outperform both, averaging ₹5 crore. The lesson: execution beats strategy, but portfolio beats focus.

The rivalry drove innovation. Jubilant's technology forced Devyani to digitize. Devyani's multi-brand presence forced Jubilant to diversify (they now operate Popeyes and Dunkin'). Both companies are better because of the other.

Westlife (McDonald's): The Premium Challenger

Westlife Development operates McDonald's in West and South India—and they've played a different game entirely. While Devyani and Jubilant fought on value, Westlife went premium. McCafé competing with Costa. Gourmet burgers competing with casual dining. McDonald's, the global symbol of cheap fast food, became aspirational in India.

Westlife's real innovation was real estate. They pioneered the drive-through format in India when everyone said Indians don't eat in cars. Today, drive-throughs generate 30% of Westlife's revenue with 50% margins. Devyani watched, learned, and is now rolling out drive-through KFCs aggressively.

The McDonald's bifurcation (Westlife in West/South, Hardcastle in North/East) created an interesting dynamic. Devyani could play different strategies against different operators. Against Westlife's premium positioning, KFC positioned as value. Against Hardcastle's operational struggles, KFC positioned as quality.

Local and Regional Chains: Death by a Thousand Cuts

The real competition isn't global brands—it's the thousand local chains serving better food at lower prices. Burger Singh's "Indian burgers." Fassos's wraps delivered in 20 minutes. Chaayos's tea cafés. Each takes a small piece, but collectively they're formidable.

These chains have advantages Devyani can't match: - Founder intensity versus professional management - Local taste understanding versus global standardization - Nimble decision-making versus franchise approvals - Lower costs through informal operations

But they also have disadvantages Devyani exploits: - Limited capital for expansion - Weak supply chain infrastructure - Inconsistent quality across locations - No brand moat against competition

Devyani's response has been selective acquisition and inspiration. Can't beat Biryani By Kilo? Consider acquiring it. Impressed by Burger Singh's Indian flavors? Launch Zinger Tandoori. The giant learns from the pygmies.

Cloud Kitchens: The Invisible Threat

The biggest threat to Devyani might be brands you've never heard of—Faasos, Behrouz Biryani, Oven Story—operating from dark kitchens in Versova and Koramangala. No real estate costs. No service staff. Just food, delivered fast.

Cloud kitchens have unit economics that make traditional QSR look bloated: - Setup cost: ₹10 lakhs versus ₹1.5 crore - Breakeven: 6 months versus 2 years - Margins: 25% EBITDA achievable from day one

Devyani's response has been measured. They've launched cloud kitchen experiments—KFC and Pizza Hut delivery-only locations. But they understand their moat isn't just food—it's experience. A first date happens at Pizza Hut, not from a cloud kitchen. Birthday celebrations need physical spaces. The brand equity built over decades can't be replicated by Instagram marketing.

Financial Performance Comparison

The numbers reveal different strategies yielding similar outcomes:

Devyani International: Consolidated revenue for the second quarter of FY25 rose by 49% to ₹1,220 crore

The margin profiles differ based on model choices: - Jubilant: Higher margins (25% EBITDA) through single-brand focus and operational excellence - Westlife: Lower margins (15% EBITDA) but higher revenue per store through premiumization - Devyani: Moderate margins (18% EBITDA) but diversified revenue streams reducing volatility

Market Share Dynamics

The Indian QSR market, worth ₹35,000 crore, is fragmenting and consolidating simultaneously. The top 5 chains control 40% share, but the long tail of 10,000+ brands controls 40% too. The middle is disappearing.

Devyani's multi-brand strategy positions it uniquely. While Jubilant dominates pizza and Westlife dominates burgers, Devyani has meaningful presence across categories. This portfolio approach means Devyani captures more occasions, dayparts, and demographics than focused competitors.

Growth Opportunities in White Spaces

The real competition isn't for existing customers—it's for the 95% of Indians who've never eaten at a QSR. The opportunity is massive: - 600 million Indians have never eaten branded QSR - 8,000 cities have no organized QSR presence - Breakfast and snacking dayparts are underpenetrated - Corporate catering is unorganized

Devyani's aggressive expansion into tier-3/4 cities targets these white spaces. A KFC in Bikaner isn't competing with McDonald's—it's competing with local restaurants and creating category awareness. First-mover advantage in these markets creates mini-monopolies that last decades.

The competitive landscape is intensifying but also expanding. As the pie grows, there's room for multiple winners. The question isn't whether Devyani can beat Jubilant or Westlife—it's whether organized QSR can collectively capture the massive opportunity before new models disrupt the industry entirely.

XI. Playbook: Business & Investing Lessons

Let's step back from the operational trenches and examine the meta-lessons from Devyani's journey. These aren't just QSR insights—they're frameworks for building and evaluating businesses in any emerging market consumer sector.

The Power of Franchise Models in Emerging Markets

Franchising in emerging markets is fundamentally different from developed markets. In the US, franchising is about capital efficiency—let others invest while you collect royalties. In India, franchising is about knowledge transfer and risk mitigation.

Devyani's franchise model mastery reveals several insights:

Franchise arbitrage: Global brands undervalue emerging market rights because they apply developed market multiples. Devyani bought India rights for KFC and Pizza Hut at fractions of intrinsic value. The same rights today would cost 50x more.

Reverse innovation: Emerging market franchisees aren't just executors—they're innovators. The Tandoori Pizza, veggie KFC menu, breakfast offerings—all created by Devyani and licensed back to global brands. The student becomes the teacher, and gets paid for it.

Regulatory shield: Foreign brands face regulatory scrutiny that local operators avoid. Devyani provides the shield. When activists protest Western cultural invasion, they target KFC corporate, not Devyani. This political insurance is invaluable.

Scale economics: A single-brand franchisee has limited leverage. A multi-brand operator has massive leverage—with suppliers, landlords, regulators, even franchisors. Devyani negotiates as equals with Yum Brands because Yum needs Devyani more than vice versa.

Multi-Brand Strategy as Risk Mitigation

Portfolio theory applied to operations. Different brands have different: - Customer demographics (young vs family) - Occasion timing (breakfast vs dinner) - Economic sensitivity (premium vs value) - Cultural acceptance (vegetarian-friendly vs meat-forward) - Real estate requirements (mall vs street)

This diversification creates resilience. When demonetization hit cash-dependent KFC, card-friendly Costa compensated. When health trends hurt fried chicken, coffee and pizza grew. When COVID killed dine-in Pizza Hut, delivery-friendly KFC thrived.

But multi-brand isn't just defense—it's offense. Customer acquisition costs are amortized across brands. A Pizza Hut customer becomes a KFC customer becomes a Costa customer. The lifetime value multiplies while acquisition cost remains constant.

Importance of Local Adaptation

The Tandoori Pizza is worth a Harvard case study. It seems obvious now—of course Indians want Indian flavors on pizza. But it represents profound insight: global brands provide structure, local adaptation provides soul.

Devyani's localization goes beyond menu: - Service adaptation: Indian customers expect more service than Americans. Devyani added table service to counter formats. - Pricing adaptation: ₹99 price points that seem arbitrary are psychologically optimized for Indian wallets - Format adaptation: Party halls for Indian celebrations, prayer rooms for religious customers - Marketing adaptation: Bollywood tie-ins, cricket promotions, festival specials

The lesson: Don't choose between global and local. Global provides systems, brand equity, and best practices. Local provides relevance, acceptance, and growth. The magic is in the blend.

Capital Allocation: When to Expand vs Consolidate

Devyani's capital allocation reveals masterful timing:

2000-2010: Build the base. Focus on same-store growth, operational excellence, and capability building. Expansion was measured—50 stores per year, each profitable before the next.

2010-2015: Accelerate selectively. With proven economics, expansion accelerated but remained focused on tier-1/2 cities where brand awareness existed.

2015-2020: Blitzscale. With capital access and operational maturity, add 200+ stores annually. Enter tier-3/4 cities accepting lower initial returns for market creation.

2020-2022: Consolidate and strengthen. COVID forced pause. Close weak stores, strengthen balance sheet, improve unit economics.

2022-present: Intelligent expansion. The Company opened 257 new stores across India and international markets, bringing the total number of outlets to 2,039 stores by March 2025. But now with AI-driven site selection, proven formats, and profitable growth.

The lesson: Expansion and consolidation aren't strategies—they're tactics deployed based on market conditions, competitive dynamics, and internal capabilities.

Building Operational Excellence at Scale

Scale creates complexity that kills most consumer businesses. Devyani manages 2,000+ stores across 4 countries, 5 brands, and 280+ cities. The operational complexity is staggering. How do they maintain quality?

Standardization with flexibility: 80% of processes are standardized globally. 20% are localized. This 80/20 rule allows efficiency without rigidity.

Technology as backbone: Every transaction, every inventory movement, every employee action is digitized and analyzed. Exceptions are flagged in real-time. Problems are solved before customers notice.

Culture as control: Beyond systems, Devyani has built a culture of operational excellence. Store managers compete on metrics. Best practices are shared religiously. Excellence is celebrated publicly.

Vertical integration where it matters: Devyani doesn't manufacture food, but controls critical elements—logistics, training, technology. This selective integration ensures quality without capital intensity.

Family Business to Professional Management Transition

The Jaipuria family's evolution from operators to strategists is a masterclass in transition:

Stage 1 (1991-2000): Family members in every function. Decisions based on intuition and relationships.

Stage 2 (2000-2010): Professional managers in execution roles, family in strategy. Decisions based on data but approved by family.

Stage 3 (2010-2020): Professional CEO and management team. Family on board providing vision and capital allocation guidance.

Stage 4 (2020-present): Institutional governance with family as strategic shareholders. Decisions based on shareholder value creation.

This evolution wasn't forced—it was planned. Each stage built capabilities for the next. The family retained what mattered (vision, values, capital allocation) while delegating what didn't (operations, execution, administration).

Long-term Thinking in Cyclical Businesses

QSR is brutally cyclical. Economic downturns destroy demand. Food inflation crushes margins. Competition intensifies constantly. Yet Devyani has compounded at 25% CAGR for two decades. How?

Counter-cyclical investment: Expand aggressively during downturns when real estate is cheap and competition is weak. The stores opened during COVID at distressed rents are now the most profitable.

Margin of safety in unit economics: Target 35% IRR when 20% would be acceptable. This buffer absorbs shocks without destroying value.

Patient capital structure: Promoter Holding: 62.6% provides stability. No pressure for quarterly earnings management or short-term optimization.

Secular trend conviction: Short-term cycles matter less when you're riding a 20-year wave of urbanization, rising incomes, and lifestyle changes.

The meta-lesson: In cyclical businesses, time horizon is competitive advantage. Those who can think in decades while others think in quarters win by default.

XII. Analysis & Bear vs. Bull Case

The investment community is split on Devyani. Bulls see India's Starbucks—a consumption story with decades of growth ahead. Bears see an overvalued restaurant chain facing margin pressure and competition. Both are right, and both are wrong. Let's examine the arguments with clinical precision.

Bull Case: The India QSR Penetration Story

The bulls start with an undeniable fact: India has 1 QSR store per 150,000 people. China has 1 per 15,000. The US has 1 per 5,000. If India reaches even half of China's penetration, that's a 5x growth opportunity. At US levels, it's 15x. The runway isn't years—it's decades.

But penetration statistics hide nuance. The addressable market isn't India's 1.4 billion people—it's the 200 million with disposable income for ₹350 chicken buckets. Still, this cohort is growing 10% annually. By 2030, it'll be 400 million. The TAM expansion alone drives 15% annual growth.

Earnings are forecast to grow 41.15% per year This isn't analyst optimism—it's mathematical inevitability given store addition plans and same-store sales growth trends.

The Consumption Megatrend

India's per capita income crosses $3,000 in 2025—the inflection point where consumption historically explodes. Young demographics (65% under 35) with Western aspirations and Indian wallets create perfect conditions for QSR adoption.

Urbanization accelerates the trend. Every year, 10 million Indians move from villages to cities. Rural diets of dal-roti transform into urban habits of burgers and pizza. This isn't just dietary change—it's identity transformation, and QSR brands are identity markers.

The nuclear family revolution multiplies impact. Joint families cooking elaborate meals are fragmenting into nuclear units ordering in. Cooking is becoming optional, not mandatory. QSR isn't competing with home food—it's replacing it.

Execution Track Record

Bulls point to management's execution: As on December 31, 2024, DIL operates more than 2,030 stores across brands in over 280 cities in India, Thailand, Nigeria and Nepal. This isn't lucky growth—it's systematic execution across multiple markets, brands, and formats.

The Thailand acquisition proves international capability. Nigeria demonstrates frontier market success. The multi-brand portfolio shows strategic sophistication. This isn't a one-trick pony—it's a platform that can add brands, geographies, and formats at will.

Bear Case: Structural Challenges

Bears start with brutal facts: Company has low interest coverage ratio. Company has a low return on equity of 3.76% over last 3 years These aren't temporary issues—they're structural problems.

The ROE problem is particularly concerning. Restaurant businesses are capital-intensive. Every new store requires ₹1.5 crore investment. With 3.76% ROE, that capital could generate better returns in fixed deposits. Bulls argue this is temporary, reflecting COVID impacts and expansion investments. Bears see fundamental business model challenges.

Margin Pressure Intensifying

For the quarter under review, consolidated reported EBITDA was ₹200 crore, with a margin of 16.3%, down from 18.3% in the previous quarter. This margin compression isn't seasonal—it's structural.

Food inflation runs at 8-10% annually, but menu prices can only increase 3-5% without demand destruction. Labor costs are rising 12% annually as India formalizes. Real estate costs in prime locations are increasing 15% yearly. The margin squeeze is mathematical—costs rising faster than pricing power.

Competition makes it worse. Every player is fighting for the same customer with discounts, promotions, and loyalty programs. The industry is in a race to the bottom on pricing while costs race to the top.

Competition Intensifying

The bear case sees competition destroying economics. Jubilant's Domino's dominance in pizza limits Pizza Hut's growth. Westlife's McDonald's premium positioning caps KFC's pricing power. New entrants like Popeyes and Taco Bell fragment the market further.

But the real threat is structural change. Cloud kitchens operate at 1/10th the capital intensity. D2C brands build following on Instagram without store investments. Grocery delivery platforms are adding ready-to-eat options. The QSR model itself might be obsolete.

Execution Risks with Rapid Expansion

The Company opened 257 new stores across India and international markets, bringing the total number of outlets to 2,039 stores by March 2025. Bears see reckless expansion that will destroy returns.

Quality suffers at scale. The 2000th store can't maintain the standards of the 200th. Management bandwidth is stretched. Site selection becomes less rigorous. New markets lack brand awareness requiring heavy marketing investment. International expansion adds currency risk, political risk, and execution complexity.

The store addition target implies opening one store every 1.5 days. This breakneck pace inevitably leads to mistakes—wrong locations, poor execution, underperforming units that drag system economics.

Valuation Analysis

At current valuations, Devyani trades at premium multiples: - P/E ratio: Not meaningful given volatile earnings - EV/EBITDA: ~25x, expensive for a restaurant business - Stock is trading at 17.1 times its book value

Bulls argue these multiples reflect growth potential. Bears see priced-for-perfection valuations with no margin of safety. Any execution stumble, margin compression, or competitive loss will trigger multiple compression alongside fundamental deterioration.

The Balanced View

The truth, as always, lies between extremes. Devyani is neither the next Starbucks nor the next restaurant bankruptcy. It's a well-executed QSR platform riding secular trends but facing structural challenges.

The bull case is stronger long-term. India's consumption story is real, and Devyani is positioned to capture it. But the path won't be linear. Margins will compress before expanding. Competition will intensify before consolidating. Some stores will fail. Some markets will disappoint.

The bear case has validity short-term. Current valuations assume flawless execution. Any stumble will punish the stock. Margin pressure is real and will persist. Competition is intensifying and will take share.

For investors, the question isn't whether Devyani will grow—it will. The question is whether growth will create value after accounting for capital intensity, competitive dynamics, and execution risks. At current valuations, the market is betting yes. History suggests the answer is more nuanced.

XIII. Future Strategy & Growth Vectors

The war room at Devyani's Gurgaon headquarters, 2025. On the wall, a map of India with 2,030 green dots representing current stores. But it's the 10,000 grey dots that matter—potential locations identified by machine learning algorithms analyzing satellite imagery, mobile phone data, and consumption patterns. This is Devyani's next decade: using technology to capture the white space before competitors even know it exists.

Digital Transformation and Tech Investments

The digital transformation at Devyani isn't about apps and websites—it's about rebuilding the business as a technology company that happens to sell chicken. The investments are staggering but the returns are already visible.

AI-Powered Site Selection: Gone are the days of intuition-based location selection. Devyani's proprietary AI model ingests 200+ variables—from Google Maps foot traffic to Instagram geo-tags to credit card spending patterns—to predict store performance within 10% accuracy. The model has identified 5,000 high-probability locations that traditional analysis would miss.

Autonomous Kitchen Operations: The next generation of Devyani kitchens will be semi-autonomous. Robotic fryers that adjust temperature based on computer vision analysis of browning. Automated inventory systems that predict demand 72 hours ahead. The goal: reduce labor cost from 15% to 8% while improving consistency.