Delta Corp: The King of India's Casino Moat

I. Introduction & The "Vegas of the East" Hook

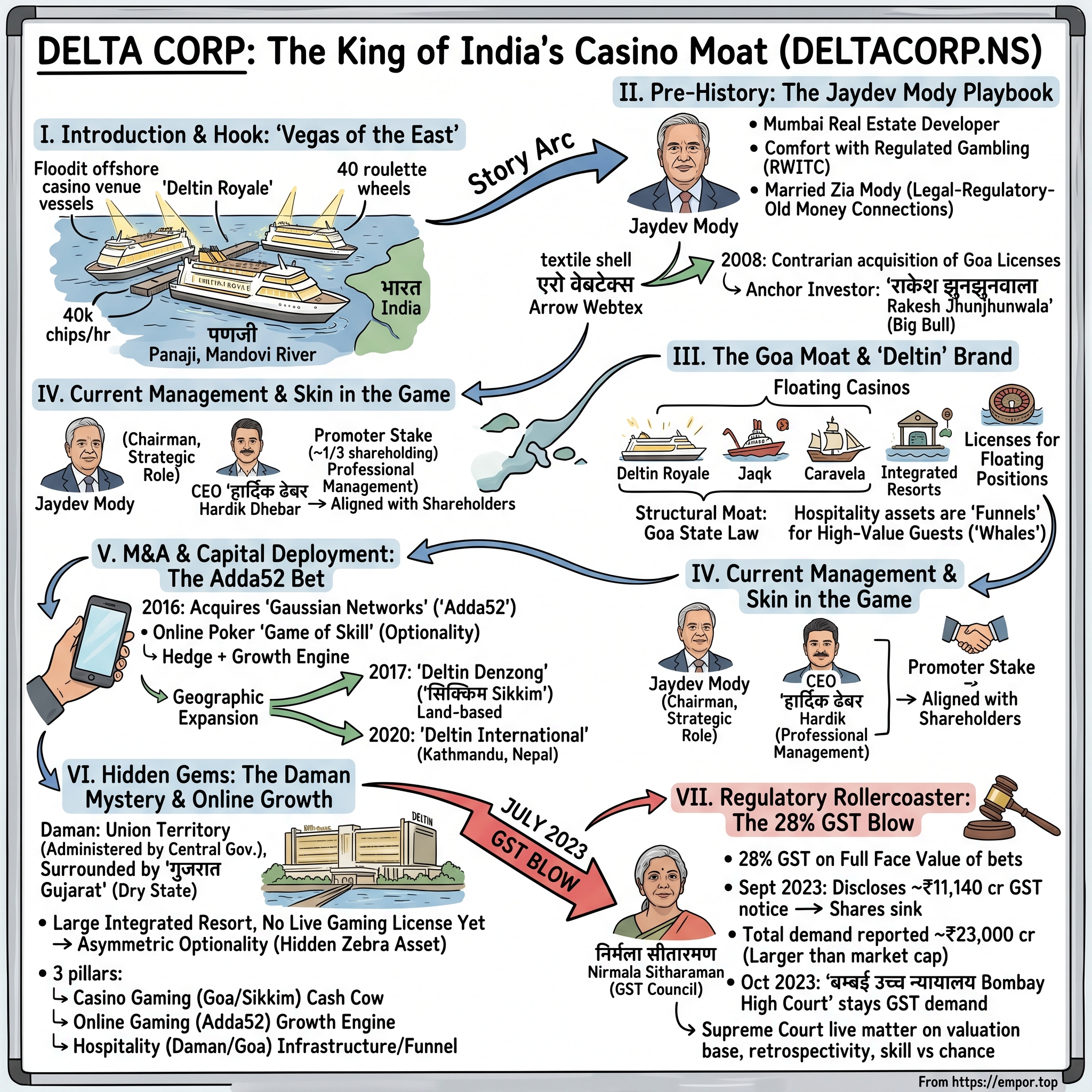

Picture this. It is a humid October evening in 2018 in पणजी Panaji, the small coastal capital of Goa. The Mandovi River runs slow and silty under a sodium-lit sky, fishing boats bobbing alongside a row of floodlit, multi-deck gambling palaces moored mid-stream. A high-roller in an open-collared shirt steps off a feeder jetty and onto the Deltin Royale. Inside, the air is thick with cologne, cigar smoke, and the unmistakable, low-frequency hum of forty thousand chips changing hands per hour. Forty roulette wheels spin in concert. A live cabaret act warms up on a stage two decks above the baccarat tables. Somewhere on the top deck, a private suite has been booked under a name that is not on any flight manifest.

This is भारत India's only legal, organized, exchange-listed slice of Las Vegas, and almost all of it belongs to one company.

डेल्टा कॉर्प Delta Corp Limited is the only listed pure-play gaming and hospitality operator in India. Its three offshore casino vessels in Goa, its land-based casino in Sikkim, its joint venture in Kathmandu, and its online poker franchise Adda52 together gave it well over half of the country's organized casino and online poker revenue pool through most of the 2017–2023 window.[^1] In a country of 1.4 billion people where every state legislates gambling differently and the central government regulates it nervously, Delta Corp built what is arguably the most regulatorily moated consumer business on the National Stock Exchange.

How did this happen? How does the only listed casino company in a country that has historically considered gambling spiritually questionable end up commanding a multibillion-rupee market cap, attracting one of India's most celebrated investors as an early backer, and surviving a tax notice larger than its entire equity value?

The short answer is जयदेव मोदी Jaydev Mody. The longer answer is a story about regulatory arbitrage, the slow conversion of a textiles shell company into a luxury entertainment empire, a contrarian acquisition of an online poker site that almost no one understood, and a once-in-a-decade collision with the Indian Goods and Services Tax Council. It is also a story about a particular kind of Indian capitalism: family-controlled, license-anchored, patient about cash flow, allergic to leverage, and willing to wait an entire decade for a single government file to move.

Over the next ten or so sections we will trace this arc. We will start with Mody himself, a real-estate man who married into the वाडिया Wadia family and parlayed proximity to Mumbai's horse-racing aristocracy into a foothold in a regulated vice industry. We will follow him into the मांडवी नदी Mandovi River, where the legal fiction of an "offshore" casino turned into one of the great cornered-resource stories of modern Indian business. We will watch the Adda52 acquisition reframe Delta from a single-asset story into something that looks more like a platform. We will examine the strangest item on the balance sheet, the half-finished integrated resort sitting in दमन Daman waiting on a gaming license that may or may not ever arrive. And we will end on the regulatory thunderclap of July 2023, when the GST Council voted to tax the full face value of every bet at 28%, and Delta Corp's stock collapsed by roughly a third in three sessions.

The themes will be familiar to listeners of any episode about a "sin stock" or a regulated monopoly. Cornered resources. Brand. Political risk. The strange paradox by which being un-investable for ESG-screened capital can sometimes create a valuation floor rather than a ceiling. The trickier theme, the one specific to India, is that none of this exists in a vacuum. It exists at the pleasure of the state government of Goa, the state government of Sikkim, the Ministry of Finance, and now the Supreme Court of India.

Let's start where every Delta Corp story has to start: with a man, a textile mill that nobody wanted, and a hunch about Goa.

II. Pre-History: The Jaydev Mody Playbook

In the late 1990s, Jaydev Mody was not a casino magnate. He was a Mumbai real-estate developer with a quiet reputation for being early. He had bought distressed properties in South Mumbai before the city's land prices broke into orbit. He sat on the committee of the Royal Western India Turf Club, the colonial-era horse-racing institution that defined a certain kind of Mumbai weekend, and through that world he had absorbed something most Indian businessmen of his generation actively avoided: a comfort with the legal, social, and operational mechanics of regulated gambling.1

He had also married Zia Mody, the daughter of former Attorney General of India Soli Sorabjee and herself one of the most powerful corporate lawyers in the country. The Mody household sat at the intersection of three power circles that almost no one else in Indian business could access simultaneously: real estate, legal-regulatory, and the turf club's quiet network of old-money families. To understand what happens next, hold that picture in your mind. He was not a gambler. He was a man who understood, in his bones, that in India the difference between a great business and a mediocre one is often the difference between holding a license and not holding one.

The vehicle that became Delta Corp started life as something completely unrelated. It was a small, listed narrow-fabrics and textile company called एरो वेबटेक्स Arrow Webtex, the kind of forgotten industrial shell that traded on the BSE on a couple of hundred shares a day. Mody and his associates accumulated control of it through the early 2000s, and over the next several years it served as the listed platform through which a sequence of real-estate, advertising, and hospitality assets were rolled in, renamed, and rationalized into what would eventually become Delta Corp Limited.

The inflection point came in 2008. The global financial crisis was tearing through balance sheets from New York to Mumbai. Indian real-estate developers, including some of Mody's competitors, were over-leveraged and frozen. Casino licenses in Goa, which the state government had been issuing in a slow, controlled trickle since the late 1990s, were suddenly available because the existing license-holders needed cash. Mody's read was contrarian and, in retrospect, definitional. He saw that the License Raj culture of Indian gaming was not the bug, it was the feature. If you could acquire licenses while everyone else was panicked about liquidity, you would own a position that no amount of capital, deployed later, could replicate.1

Through 2008 and 2009, Delta Corp acquired the operating company behind one of Goa's offshore casino vessels and progressively consolidated its position in the Mandovi. The numbers in those early transactions look almost quaint today. But every license and every vessel purchased during the panic translated, a few years later, into a slot in the river that the Goa government had effectively stopped reissuing.

To validate this strange, half-real-estate, half-gambling pivot on the public markets, Mody needed an anchor investor whose name carried the kind of weight that would override the obvious moral and ESG discomfort. He found it in राकेश झुनझुनवाला Rakesh Jhunjhunwala, the "Big Bull" of Indian equities, whose endorsement of any small-cap stock in that era was worth multiples of the actual capital he deployed.[^3] Jhunjhunwala's family office built a meaningful, long-duration position in Delta Corp. For a generation of Indian retail and HNI investors who watched his every move, that was the green light. A sin business, yes, but a sin business that the Big Bull was willing to be photographed owning.

The Mody playbook by the end of this period had crystallised. Use a listed shell to consolidate gaming assets while the asset class is mispriced. Bring in a credible anchor investor to neutralise the optics. Build slowly, organically, with promoter capital and operating cash flow rather than leverage. And above all, never, ever let go of the licenses.

It is here that the story moves out of the Mumbai boardrooms and onto a brown, slow river two hours south of Panaji.

III. The Goa Moat & The "Deltin" Brand

If you want to understand why Delta Corp exists as a listed entity at all, you need to understand a single peculiarity of Goa state law. Casinos are not permitted on Goan land in any meaningful sense. They are permitted on vessels moored in the Mandovi River, which is treated, for licensing purposes, as "offshore." This legal fiction, originally a compromise between a tourism-hungry state government and a culturally conservative electorate, has been the structural moat around the entire Goan casino industry for two decades.[^4]

The implication is enormous and frequently underappreciated by people who have never visited. Every gaming position in Goa, every roulette wheel, every baccarat shoe, every poker seat, has to exist on a floating platform. That means dredging rights, jetty rights, lighting rights, mooring rights, river-traffic clearances, environmental clearances, and the political tolerance of whichever coalition happens to be running the Goan state legislature in a given five-year window. None of those things scale linearly with capital. You cannot solve them by writing a bigger cheque. You can only solve them by being already inside.

Delta Corp's flagship vessel, the Deltin Royale, is the largest of these floating casinos. By the company's own description it carries forty live gaming tables across multiple decks, slot machine banks, three restaurants, a sky bar, and capacity for over a thousand guests at peak. It is, functionally, an integrated resort that happens to float. Around it, in the same stretch of the Mandovi, sit Deltin Jaqk and Deltin Caravela, the two smaller vessels in the fleet. Together this trio gave Delta Corp the dominant share of gaming positions in Goa through the entire 2015–2023 window.6

The economics of a floating casino, once you understand them, are extraordinary. Capital expenditure is high. A vessel of this scale, with the dredging and refurbishment cycle that goes with it, is a multi-hundred-crore commitment over its life. But the marginal cost of the next gaming hand, once the vessel is operational and the regulatory licences are paid for, is close to zero. The variable cost of a roulette spin is a croupier, the wear on a felt, and the discounted value of a complimentary drink. The revenue per spin, if you have built the right brand and curated the right customer base, is multiples of that.

This is why hospitality matters so much in Delta Corp's model, and why it is so easy to misread. The Deltin Suites hotel and the broader land-based footprint are not standalone businesses optimised for hotel-industry margins. They are funnels. Their job is to deliver high-value guests, the so-called "whales," from the runway at Dabolim Airport to a vessel in the Mandovi without ever exposing them to a competitor's marketing. A guest who flies into Goa, is met at the airport by a Deltin car, is checked into a Deltin Suite, dines at a Deltin restaurant, and is shuttled to the Deltin Royale, has touched the Delta Corp ecosystem at every node. The hospitality assets give the integrated resort thesis a continuous customer experience that no isolated boat operator can match.

The competitive landscape in Goa over the last decade has effectively settled into a duopoly between Delta Corp and the privately-held प्राइड Pride Group, with a long tail of smaller vessels. Delta's strategic choice within that duopoly was to go up-market. The Royale was deliberately positioned as the premium, high-stakes, integrated entertainment product, while volume-driven, lower-margin business was ceded to competitors. This choice has been consequential in two directions. On the upside, premium positioning means higher revenue per occupied gaming position and far better resilience through the GST shock we will get to shortly. On the downside, it makes the business sensitive to high-net-worth discretionary travel cycles and to any policy that nudges Indian wealth offshore to Macau, Singapore, or दुबई Dubai.

And then there is the question that hangs over every conversation about Goa: will the boats ever come ashore? Successive state governments have flirted with the idea of moving the casinos out of the Mandovi River entirely, citing environmental concerns and local political pressure, and have repeatedly extended the deadline.[^4] The "land-based-only" scenario, were it ever to actually arrive, would not necessarily destroy the business, but it would compress timelines and force a step-change in capital expenditure for whoever survives the transition. For now, the river holds.

What this section really tells you about the company is that the Goa moat is not a brand moat or a scale moat. It is a regulatory moat, and the brand is the customer-facing wrapper around it. Which raises the obvious question: who, exactly, is steering this thing?

IV. Current Management & Skin in the Game

Watch Jaydev Mody at an investor conference and the first thing you notice is what he does not do. He does not wave around hockey-stick projections. He does not promise to double EBITDA in three years. He does not talk about TAM. When asked about quarterly numbers, he tends to redirect the conversation to the underlying licence portfolio, the pipeline of integrated resort projects, and the structural cash-flow profile of the gaming positions the company already owns. He sounds, in other words, less like a tech founder and more like an old-school turf-club steward who happens to also chair a public company.

That tone reflects a deliberate evolution in his role. In the early years of Delta Corp's transformation, Mody was a hands-on operator, personally involved in licence negotiations, vessel acquisitions, and the structuring of the early capital raises. Over time, particularly through the mid-2010s, he transitioned to a strategic chairman role, leaving day-to-day operations to a professional management team while retaining final say on capital allocation and any decision that touched the licence portfolio.

The promoter stake is the single most important alignment signal in the entire equity story. The Mody promoter group has consistently held in the vicinity of a third of the company through the last several years of shareholding disclosures filed with the National Stock Exchange.2 That is meaningful in two ways. It means the family is firmly aligned with public shareholders on the upside, and it means they have the votes to resist any opportunistic takeover or short-term financial engineering, particularly during regulatory shocks when the share price is depressed. Mody has a long, documented pattern of buying more during panics rather than trimming, which is the kind of behaviour public-market investors notice and remember.

The professional management layer is built around CEO हार्दिक ढेबर Hardik Dhebar, who has spent the bulk of his career inside the Delta ecosystem and was promoted into the chief executive role after a long internal apprenticeship. The choice was deliberate. In a business where licence relationships, vessel operations, customer black books, and regulatory navigation all live in institutional muscle memory, an outside hire would have taken years to ramp. Continuity, in this kind of company, is itself a form of moat.

Compensation structure is the other tell. Delta Corp's management incentive design has historically leaned toward EBITDA margin preservation rather than topline growth or volume metrics, which is consistent with a business where the strategic answer to every "should we expand the customer base" question is "only if it doesn't dilute the margin profile of the existing seat." This is the opposite of how a typical Indian consumer-internet company is incentivised, and it is one of the reasons Delta's reported segment margins have stayed in a relatively narrow band even through cycles where competitors were chasing volume.

Succession is the awkward question. Mody is in his seventies. There is, as of the latest annual report, no publicly designated family successor with an operating role inside the company, which is unusual by the standards of Indian promoter families.[^1] The professional-management bench is deep, but the licence relationships, the political access, and the family's strategic patience are not easily institutionalised. This is a risk that does not show up on any income statement but that every long-term shareholder eventually has to think about.

The takeaway from the management layer is that Delta Corp is a promoter-led, licence-anchored compounder, run more like a family office's flagship operating asset than like a typical listed consumer company. That orientation explains a lot about the next chapter of the story, which is the one place where Mody's team deliberately stepped outside the comfort of the Goa moat and made a bet on a completely different surface.

V. M&A & Capital Deployment: The Adda52 Bet

In August 2016, Delta Corp announced that it would acquire गॉसियन नेटवर्क्स Gaussian Networks, the parent company of the online poker site Adda52, for an enterprise value of approximately ₹155 crore.[^6] The reaction in Mumbai's analyst community at the time was, to put it mildly, sceptical. Online poker in India was a legal grey zone. The market was small. The unit economics were unproven. And Delta Corp was, by every existing description, an offshore-casino company. Why was Mody writing a nine-figure rupee cheque for a website?

The answer is that he was not buying a website. He was buying optionality on a thesis that almost no one else in Indian business was willing to underwrite.

The thesis went like this. India's gaming demand was a function of two things: rising discretionary income and falling friction. The Goa casino business solved for both, but only for customers who could afford a flight, a hotel, and an offshore vessel ticket. There was a much larger pool of gaming demand, sitting in Tier-1 and Tier-2 Indian cities, that would never travel to a casino but would happily play a hand of poker on a phone in a living room. The question was whether anyone could legally deliver that product at scale, and whether the unit economics, once delivered, would justify the customer acquisition cost.

Adda52 had been the most credible answer to that question in the market. It was the dominant online poker brand in India by traffic and tournament volume, built on a "game of skill" legal interpretation that allowed it to operate in most Indian states (though not all, and that exclusion list has grown). For Delta Corp, owning Adda52 meant three things. It meant a hedge against any future tightening of physical casino regulation. It meant a faster, cheaper customer-acquisition surface for the high-margin physical product. And it meant a foothold in the segment of Indian gaming that was, even then, growing at a multiple of physical casino revenue.

Did Mody overpay? At the announcement multiple, plenty of analysts thought so. But by the time the Indian online real-money gaming sector hit its peak through the COVID-19 lockdowns of 2020 and 2021, when housebound urban Indians discovered online poker and rummy en masse, the Adda52 cheque looked closer to a steal. Online segment revenue for Delta Corp grew several-fold through that window, and the segment EBITDA became a material contributor at a moment when the physical casinos were largely shut.[^1]

Capital deployment around the same period extended geographically in a different direction. Delta Corp opened Deltin Denzong in सिक्किम Sikkim in early 2017, anchoring a land-based casino operation in one of the very few Indian states that explicitly permits onshore gambling.[^7] The Sikkim play was a hedge against the offshore-only ambiguity of Goa, but it was also a structural diversification. Different state, different regulator, different licensing regime, same management team and customer database.

Three years later, the company crossed an international border. Deltin International opened operations in a five-star property in Kathmandu in February 2020, marking Delta Corp's first overseas casino footprint and a deliberate attempt to access the broader South Asian high-roller circuit, including Indian customers who preferred to travel for their gaming rather than do it under the watchful eye of an Indian regulator.3 The timing, just weeks before COVID-19 shut down cross-border travel, was unfortunate, but the strategic logic, that Delta could franchise its operational template across a regulated South Asian network, remained intact.

What ties all of this together is a single capital-allocation discipline that runs through Mody's entire era. The cash flow generated by the Goa casinos was not paid out aggressively as dividends, not redeployed into unrelated diversification, and not levered up to chase growth. It was redeployed into adjacent gaming surfaces, each of which inherited the brand, the customer database, and the regulatory know-how of the parent. There is no easier way to lose money in a gaming business than to expand into something you do not understand. Delta Corp, to its credit, has spent twenty years expanding only into things it does.

Which brings us to the most peculiar item on the entire balance sheet.

VI. Hidden Gems: The Daman Mystery & Online Growth

Drive ninety minutes north of मुंबई Mumbai, through the industrial sprawl of Vasai and Virar, and you reach the small coastal enclave of दमन Daman. It is a former Portuguese territory, today a Union Territory administered directly by the central government rather than by a state. And on a stretch of land near the beach, surrounded by manicured lawns and a long, low-rise hotel complex, sits The Deltin, Delta Corp's largest integrated resort in India.4

The Deltin Daman is in some ways the most ambitious physical asset Delta Corp has ever built. It is a full integrated-resort campus: hundreds of hotel keys, conference space, restaurants, spa, banquet halls. By every visible measure, it should be the flagship of the entire portfolio. There is just one missing piece. After more than a decade of operation, the property still does not have a live gaming licence.

This is the Daman Mystery. The Government of गुजरात Gujarat, which surrounds the Daman enclave on three sides, is a dry state with strict prohibition laws and a culturally conservative electorate. The wealth concentrated in Gujarat, particularly the diaspora and family-business HNI base in Ahmedabad, Surat, and Vadodara, is enormous. If Daman were ever to be granted a casino licence, the gravitational pull on that wealth, into a tax-paying, Indian-resident gaming surface a short drive from Surat, would be transformative for Delta Corp. The economic case is so obvious that the licence question has been an active topic in regulatory circles for years. And yet, year after year, the licence has not come.

What this asset represents on Delta Corp's books is therefore a peculiar kind of optionality. The cost is already sunk. The hotel runs as a hotel, generating some revenue but well below what an integrated resort with a live floor would do. The upside, were the licence ever granted, is a step-change in segment EBITDA that would not require any incremental capex. The downside, if the licence never comes, is essentially zero relative to today's position, because the hotel itself continues to operate. Asymmetric. Long-dated. Unhedgeable. This is the kind of "zebra" asset that drives short-duration analysts to distraction and that long-duration family offices like Mody's are uniquely positioned to hold.

Step back and look at how the three operating pillars of Delta Corp fit together, and you see the architecture of the business clearly for the first time. The casino gaming segment, anchored in Goa and Sikkim, is the cash cow. It contributes the dominant share of group EBITDA in any normal year, with extraordinarily high incremental margins.[^1] The online gaming segment, built around Adda52 and the rummy adjacencies, is the growth engine, with structurally higher topline growth rates but lower margins. The hospitality segment, including the Deltin hotels in Daman, Goa, and elsewhere, is the infrastructure layer, both a standalone business and the funnel for the high-margin gaming products.

This three-pillar structure is what allows Delta Corp to be analysed simultaneously as a gaming company, a consumer-internet company, and a real-estate-and-hospitality company depending on which set of comparables you find most useful. It also creates a particular vulnerability, because the regulatory regime for each pillar is different, and changes in any one of them can shift the EBITDA mix.

That vulnerability turned into reality on a humid Tuesday in July 2023, when the GST Council walked into a press room in New Delhi and changed the tax treatment of gaming in India.

VII. The Regulatory Rollercoaster: The 28% GST Blow

On July 11, 2023, the 50th meeting of the Goods and Services Tax Council, chaired by Union Finance Minister निर्मला सीतारमण Nirmala Sitharaman, concluded with a press release that nobody in the Indian gaming industry had expected to read in quite those words. The Council had decided to levy a 28% GST on the "full face value" of bets placed in casinos, online gaming, and horse racing, ending years of industry argument that the appropriate base should be the much smaller "gross gaming revenue," that is, the operator's commission rather than the total wagered amount.5

To understand why this was an earthquake rather than a tremor, you have to understand what "full face value" means in mechanical terms. In a typical casino game, the player buys chips, plays multiple hands, recycles winnings into new wagers, and walks out with either more or less than they came in with. The total face value of bets placed over an evening can be several multiples of the amount the player actually risked, and many multiples of the gross margin the casino captured on those bets. Taxing the full face value at 28%, rather than the operator's commission, was not a small calibration. It was an order-of-magnitude change in the effective tax rate on every wager.

The fallout for Delta Corp arrived in installments. In September 2023, the company disclosed that it had received GST notices for an aggregate demand of approximately ₹11,140 crore, covering retrospective periods. That number then climbed to a reported aggregate of roughly ₹23,000 crore including subsidiaries and adjacent entities, a figure larger than the entire market capitalisation of the company at the time of disclosure. The stock fell sharply on the news.6

A month later, in October 2023, the बम्बई उच्च न्यायालय Bombay High Court granted a stay on a separate ₹16,000-plus crore GST demand notice issued against Delta Corp and certain subsidiaries, providing temporary relief and signalling that the courts were willing to engage seriously with the industry's argument that the retrospective application of the 28% rate was constitutionally suspect.7 The matter was subsequently consolidated into a broader set of petitions concerning the GST on online gaming, working its way up the judicial system to the Supreme Court of India, where the question of valuation base, retrospective application, and the very classification of "skill" versus "chance" games for tax purposes remains live.[^13]

This is the single most important regulatory event in the entire history of Delta Corp, and the way you frame it determines the way you frame the investment case. There are two competing narratives.

The first narrative is that this is an existential blow. If the full-face-value valuation is upheld and applied retrospectively, the cumulative tax liability across the industry exceeds the equity capital of every legal operator combined. The legal casino industry in India, on this reading, would not survive in its current form. Operators would either shut down, restructure offshore, or migrate to "grey market" platforms that ignore Indian tax law entirely.

The second narrative is that this is a one-time regulatory cleaning, painful but ultimately clarifying. On this reading, the 28% rate is now embedded in operator pricing, the retrospective component is likely to be diluted by the courts or by subsequent CBIC clarifications, and the long-term competitive position of a fully compliant, listed operator with deep political relationships actually improves as smaller, less-capitalised competitors are forced out of the market. A higher tax rate, on this view, becomes a moat for whoever can survive the transition.

Which narrative is correct is not, today, knowable. What is knowable is that the GST overhang has compressed Delta Corp's valuation multiples, deferred capital allocation decisions, and pushed the Adda52 segment into a structurally less profitable shape, because the full-face-value treatment falls particularly hard on high-frequency online formats where money is recycled across many hands per session.

There is a quieter, second-order risk that deserves naming. Taxing the legal operator at 28% of face value does not eliminate Indian demand for gaming. It simply changes the venue. Offshore, unregulated, app-based platforms that route payments through proxy structures pay no Indian GST at all. The price gap created by the new tax regime is an active subsidy to the grey market, and the legal industry's argument before the courts has consistently leaned on this point. Whether the policy ultimately gets refined in light of this dynamic is one of the open questions overhanging the entire sector.

VIII. Playbook: Business & Investing Lessons

Step back from the immediate noise of the GST case and look at Delta Corp through the lens of the standard strategy frameworks, and the structural picture becomes clearer than the headline volatility suggests.

Start with Hamilton Helmer's 7 Powers. The single most important power Delta Corp holds is Cornered Resource. The offshore casino licences in Goa are not theoretical. They are physically constrained by the geography of the Mandovi River, regulatorily constrained by a state government that has not issued new licences in years, and politically constrained by the slow-moving consensus required to alter the regime. Delta Corp owns the best mooring positions, the most established vessel operations, and the deepest customer database in that constrained set. This is the kind of resource that does not appear on a balance sheet but that defines the entire margin profile of the business.

The second power is Brand. "Deltin" has, over the last fifteen years, become functionally synonymous with the integrated luxury gaming experience in India. For the high-roller customer, the brand promise is a curated, premium, discretion-respecting experience that competitors have not consistently matched. Brand power matters less for the marginal slot-machine punter and more for the high-value table-game customer, which is exactly the segment Delta Corp has positioned itself toward.

Switching Costs are present but underpowered. A casino customer does not have the kind of contractual, integration-based lock-in that a software vendor enjoys. What Delta does have, in the form of its loyalty programme, its credit history with high-value players, and its hospitality wrap, is a softer form of friction that meaningfully tilts repeat behaviour in its favour without being a true lock-in.

Scale Economies are partial. The fixed-cost-per-gaming-position model of an integrated resort rewards scale within a specific location, which is why the Royale is structurally more profitable than smaller competing vessels. But Delta does not yet have the kind of cross-location scale that, say, a Macau-based operator enjoys.

Now apply Porter's Five Forces.

Bargaining power of suppliers is low. Gaming equipment, hospitality consumables, and labour are all available competitively. Bargaining power of buyers is similarly low; a single customer, even a whale, cannot meaningfully shift pricing. Threat of new entrants is near zero in Goa under the current regime, which is the single defining force in the entire analysis. Threat of substitutes is the real risk: international destinations such as मकाओ Macau, सिंगापुर Singapore, and Dubai, plus the rapidly evolving universe of offshore online platforms, compete for the same wallet and impose a hard ceiling on what Delta can charge per gaming position before customers vote with their feet. Industry rivalry within India, between Delta and Pride Group and the smaller operators, is real but contained, partly because the licence constraint limits the field.

There is one more lens that is worth applying here, which is what we might call the "Sin Stock Alpha" thesis. A meaningful fraction of global institutional capital, both ESG-screened mutual funds and pension funds with explicit gambling exclusions, is structurally not allowed to own Delta Corp. That permanent exclusion has two effects. It compresses the demand side of the stock, capping valuation upside in normal times. But it also creates a valuation floor, because the remaining buyer base, dominated by domestic retail, HNI, and opportunistic value investors, tends to step in aggressively at moments of regulatory or sentiment shock. This dynamic helps explain why the stock has, historically, traded with high amplitude around its own trend rather than around the broader Nifty.

The single most important playbook lesson from Delta Corp's history, for anyone studying regulated consumer businesses in emerging markets, is this: in a country where the state is a permanent counterparty to your business, the deepest moat is not technology, not brand, not scale. It is the licence portfolio, plus the institutional muscle memory required to maintain it. Mody's career has been a thirty-year extended demonstration of that single principle.

The question for the next five years is whether the licence-portfolio moat survives the GST war, and what that implies for the underlying earnings power of the business.

IX. Analysis & Bear vs. Bull Case

Let's lay the two cases on the table side by side, because the dispersion between them is unusually wide for a listed Indian consumer company.

The Bull Case. Start with the assumption that the Supreme Court ultimately reads the retrospective component of the GST notices narrowly, either remanding them to the executive for re-evaluation or striking down the most aggressive interpretations on constitutional grounds. The prospective 28% rate stays, but operators absorb part and pass part to consumers, and the industry settles into a new equilibrium in which the legal, compliant, listed players gain share against the grey market over time. In that world, Delta Corp's Goa cash cow is preserved, the Adda52 segment recalibrates to a smaller but profitable footprint focused on the genuinely skill-based formats, and the Daman licence, granted at any point in the next five years, delivers a step-function increase in segment EBITDA from a fully built-out asset with no incremental capex. Layer on top of that the secular tailwind of rising Indian discretionary income, the steady normalisation of luxury consumption in Tier-1 metros, and the gradual repatriation of gaming wallet from Macau and Singapore back into a more accessible Indian product, and you have a business that compounds intrinsic value at attractive rates from a depressed starting multiple.

The Bear Case. Start with the assumption that the Supreme Court upholds the GST framework broadly, including a meaningful portion of the retrospective demands. The industry's effective tax rate stays at the new elevated level, the unit economics of high-frequency online gaming break permanently, and a non-trivial share of demand migrates either offshore or into grey-market apps. Goa state politics, meanwhile, drifts toward a "land-based-only" regime, forcing Delta Corp into a multi-year, capital-intensive transition during which competitors and offshore venues capture share. The Daman licence remains in limbo. Discretionary travel within India faces a structural ceiling as the rupee depreciates and competing destinations such as सिंगापुर Singapore and Dubai become relatively cheaper. In that world, Delta Corp survives but it does not compound, and the licence moat that defined the bull case ends up being a moat around a smaller pond.

Benchmarking. It is worth situating Delta Corp briefly against the global gaming comparables. Genting Group, with assets in Malaysia, Singapore, and beyond, is the obvious Asian analogue: a family-controlled, licence-anchored, integrated-resort operator that has historically traded at low-to-mid teens earnings multiples and that has had to navigate exactly the kind of regulatory and tax-policy shocks that Delta now faces. Las Vegas-based operators such as Wynn Resorts and MGM operate at a much larger scale, with deeper capital markets behind them, but in a more mature, lower-growth domestic market. Delta Corp's market opportunity, on a population-adjusted basis, is closer to where the Macau operators were in the early 2000s, before the secular boom that turned them into mega-caps. The asymmetry of that comparison cuts both ways: enormous upside if Indian gaming follows even a fraction of the Macau path, meaningful downside if regulatory tightening permanently caps the trajectory.

KPIs for the long-term investor. Among the long list of metrics one could track for this business, three matter more than the rest combined.

First, revenue per gaming position on the Goa fleet. This is the cleanest measure of the underlying earning power of the cornered-resource moat, and it is the metric most insulated from accounting noise. Watch how it moves through the GST transition.

Second, online gaming segment EBITDA margin. Topline growth in Adda52 is far less important than the steady-state margin profile that emerges once the new tax regime has fully repriced the product. A segment that grows revenue but loses margin is a value-destruction signal.

Third, status of the Daman gaming licence. This is binary, long-dated optionality. Either it is granted at some point and the integrated resort there generates a step-change in EBITDA, or it is not, and the asset continues to operate as a profitable but sub-scale hotel. Any new disclosure on this front from the company's investor communications materially changes the intrinsic-value calculation.

A myth-versus-reality aside. The consensus retail narrative on Delta Corp swings between two extremes, both of which are wrong. The first myth is that the GST decision was a death sentence; the reality is that legal operators with licence moats and net cash balance sheets do not die quickly, and Delta's promoter conviction and absence of leverage have historically given it more runway through shocks than the headlines suggest. The second myth is that the moat is unassailable; the reality is that regulatory moats are the most powerful kind of moat right up until the moment they are not, and a single state-level policy reversal in Goa or a single Supreme Court ruling could materially reshape the entire industry. The honest position lives in the uncomfortable middle.

X. Epilogue & Final Reflections

Walk back along the Mandovi at the end of an evening on the Deltin Royale. The vessel has gone quiet. The last shuttle boat is ferrying a final group of guests back to the jetty. Somewhere above the deck, the cabaret crew is breaking down the stage. The river is dark and the lights of the Panaji waterfront are reflecting on the water like a long, broken ribbon of gold.

Delta Corp, in the end, is a bet on a very particular vision of India. It is a bet that the country's rising middle class and upper middle class will continue to want what every rising middle class in history has wanted: safe, regulated, premium spaces to spend their discretionary wealth on entertainment and aspiration. It is a bet that the regulatory architecture of Indian gaming, however turbulent in any given five-year window, will continue to permit a small number of well-licensed, well-capitalised, politically tolerated operators to capture that wallet. And it is a bet on Jaydev Mody, his family's promoter discipline, and the next generation of professional managers who inherit the licence portfolio he has spent two decades assembling.

Listen to Mody talk about Delta Corp long enough and you start to hear the horse-racing influence in his vocabulary. He talks about "positioning." He talks about "the field." He talks about "the long campaign." When pressed about quarterly volatility, he tends to bring the conversation back to the licences, the vessels, and the assets in the ground. There is an old saying around the Royal Western India Turf Club that captures his style better than any strategy framework: bet on the horse, not the jockey. In a country where management teams come and go, where regulatory rates change overnight, and where market sentiment can compress or expand a multiple by a factor of three in a single quarter, the horse is the licence portfolio. Everything else is the jockey.

For long-term investors trying to make sense of Delta Corp from outside India, the most useful frame is this. The company is not really comparable to a Las Vegas operator, because Las Vegas does not have the regulatory texture of Indian gaming. It is not really comparable to a Macau operator, because Macau is a single-jurisdiction concession regime. It is closest, perhaps, to a Genting in its earlier years: a family-controlled, multi-asset, multi-jurisdiction Asian gaming and hospitality group with deep regulatory entanglement and an unusually patient owner. The arc that Genting traced over four decades is one possible template for what Delta Corp could become over the next four. It is not the only template, and history rhymes rather than repeats, but it is a useful reference point.

The final image worth carrying away from this story is not of the vessels in the Mandovi or the half-built dream in Daman or the empty hearing rooms of the Supreme Court. It is of a quiet boardroom in South Mumbai, where a man who built his career around understanding the difference between a licence and a permit sits in front of a balance sheet he has spent twenty years constructing, and considers, in his own time, how to play the next decade. The horse is in the paddock. The river is still there. The licences are still on the books. And the long campaign continues.

References

References

-

Jaydev Mody, the king of casinos — Forbes India, 2017-11-20 ↩↩

-

Shareholding Pattern – Delta Corp — National Stock Exchange of India ↩

-

Delta Corp starts operations at its first international casino in Nepal — Business Standard, 2020-02-10 ↩

-

Delta Corp launches India's largest integrated resort in Daman — Financial Express, 2014-03-12 ↩

-

GST Council 50th Meeting Press Release — Ministry of Finance, Government of India, 2023-07-11 ↩

-

India's Delta Corp gets $1.34 billion GST notice, shares sink — Reuters, 2023-09-22 ↩↩

-

Delta Corp gets relief as HC stays Rs 16,000 crore GST demand notice — Moneycontrol, 2023-10-23 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube