Deccan Gold Mines Limited: Reclaiming the Lands of El Dorado

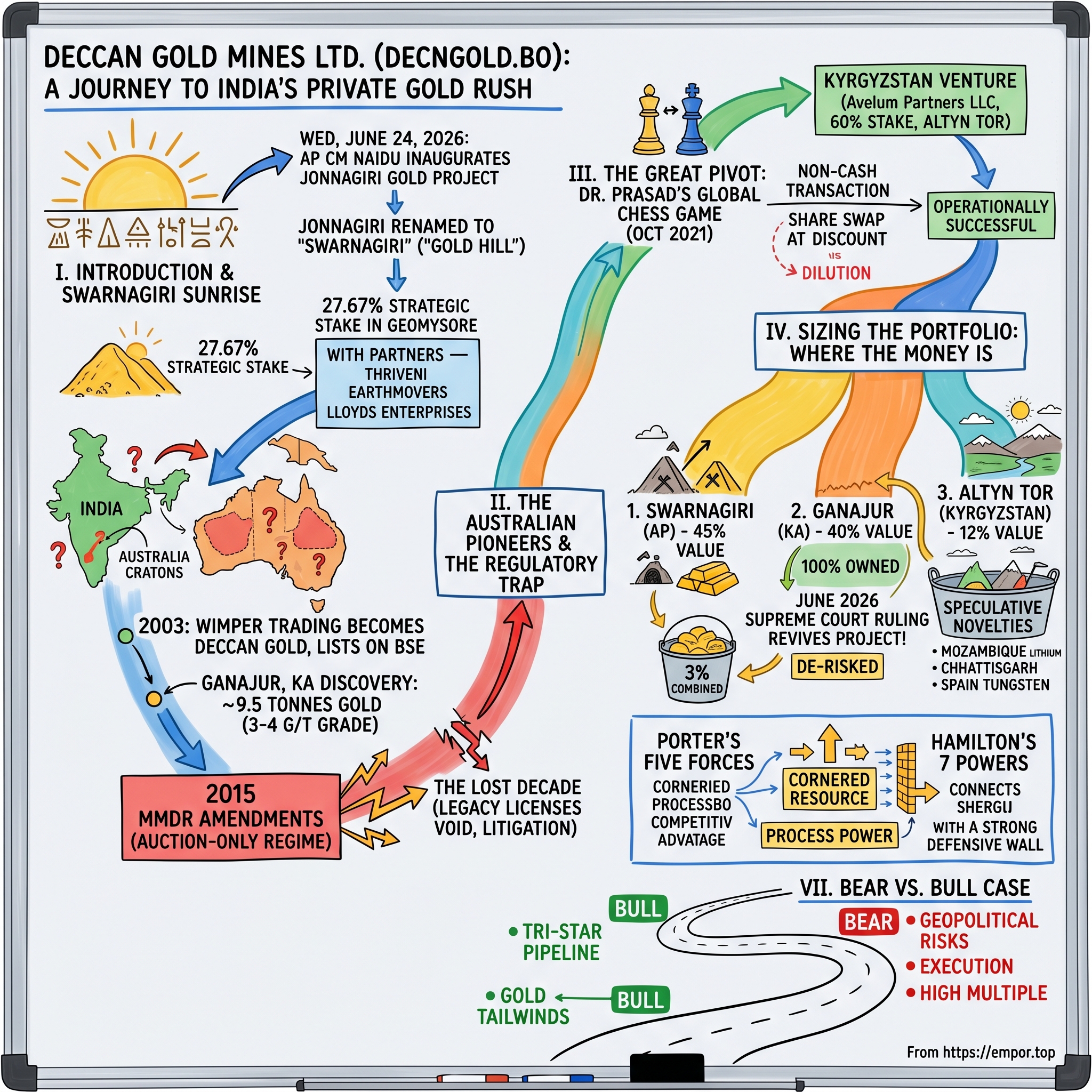

I. Introduction & The Swarnagiri Sunrise

Picture the scrubland of Tuggali Mandal in Kurnool District, Andhra Pradesh. This is the deep Rayalaseema interior—dry, rust-coloured, dotted with granite outcrops and the kind of thorny scrub that has watched empires rise and crumble. For thousands of years, people in these hills have known there was gold here. Ancient workings scar the rock; the old-timers panned the streams. The very name of the surrounding belt evokes it. And yet, in the seventy-nine years since Independence, not a single private company had ever been permitted to commercially pull gold out of this ground.

That changed on Wednesday, June 24, 2026. Andhra Pradesh Chief Minister N. Chandrababu Naidu arrived in the village of Jonnagiri to formally inaugurate the Jonnagiri Gold Project—and in a gesture freighted with symbolism, the state cabinet renamed the village itself to Swarnagiri, literally "Gold Hill."5 A village rechristened for the metal beneath it. It is the sort of thing that happens only when a government wants the world to remember a date. And the date worth remembering is this: the official commencement of commercial operations at the first private-sector gold mine India has seen since the British left.

The company holding the keys to that mine—or at least a decisive chunk of them—was not the operator on the ground. It was a micro-cap explorer that, for most of its life, has been better known to a handful of obsessive retail investors than to the broader market. Deccan Gold Mines owns a 27.67% strategic stake in Geomysore Services India Private Limited, the entity that controls the Jonnagiri concession, sitting alongside two heavyweight partners: the financier Lloyds Enterprises and the contract-mining muscle of Thriveni Earthmovers.[^2][^8] When Naidu cut the ribbon, Deccan's two-and-a-half decades of patience finally produced something it had never had before—a producing asset.

And here is the part that makes the timing almost suspicious in its neatness. Just days earlier, the Supreme Court of India had handed down a ruling in Karantharu Virama Foundation vs. State of Maharashtra that, on its face, had nothing to do with Andhra Pradesh gold. The judgment—delivered June 9 and widely reported around June 15, 2026—protected the validity of mineral lease applications filed before the great regulatory reset of 2015.[^4]4 For most observers it was a dry administrative-law decision. For Deccan Gold Mines it was a resurrection. The ruling effectively revived the company's wholly-owned Ganajur Gold Project in Karnataka—a 9.5-tonne deposit that had been frozen in legal amber for the better part of a decade.4

So in one week, two engines fired at once. A producing mine in Andhra Pradesh, and a long-dead crown jewel in Karnataka brought back to life by a court hundreds of kilometres away. The market noticed. Deccan's shares, which had spent most of their existence trading in the low double digits, surged roughly 20% to fresh lifetime highs on the news, eventually carrying the stock toward ₹217 and a market capitalisation around ₹4,330 crore—a little over half a billion US dollars.14

How does a company trading in pennies for most of its life survive twenty years in a regulatory desert, reinvent itself as a multinational acquirer with assets stretching from Central Asia to East Africa, and then suddenly find itself standing at the centre of India's first genuine private gold rush? To answer that, we have to go back to the beginning—and the beginning, fittingly for a story about ancient rock, involves a group of Australians who looked at a map of India and saw the ghost of their own continent.

II. The Australian Pioneers & The Regulatory Trap

Here is a geological fact that, once you understand it, makes the entire founding thesis of Deccan Gold Mines snap into focus. The Earth's oldest, most stable chunks of crust are called cratons. Australia's Yilgarn Craton, in the west of the continent, is one of the richest gold provinces on the planet—the rock that made Kalgoorlie and the Super Pit and a century of Aussie mining fortunes. The cratons of southern India—the Dharwar Craton, with its so-called greenstone belts threading through Karnataka and Andhra Pradesh—are geological cousins. Same age, same architecture, the same billion-year-old recipe that cooks up gold. If you trusted the geology, the conclusion was almost insulting in its obviousness: India should host enormous, barely-touched gold deposits, simply because the rock that hosts them is the same rock that made Australia rich.

A small band of Australian exploration veterans trusted exactly that. The corporate vehicle they would eventually use had an unglamorous origin—it began life as Wimper Trading Limited, incorporated back in 1984.[^2] In 2003, that shell was recast and renamed, and the geological dreamers, led by mining man Charles E. E. Devenish, poured their thesis into it.[^2] The renamed Deccan Gold Mines Limited listed on the Bombay Stock Exchange in 2003–04, and in doing so claimed a title it has held ever since: the only listed pure-play private gold explorer in the country.[^2]

What's worth dwelling on is how unusual a creature this was. India did not have a private gold-mining industry to speak of. Exploration is the riskiest, most capital-hungry stage of the entire mining value chain—you spend years and crores drilling holes, most of which find nothing, in the hope that one in a hundred turns into a mine. To do that in a country with no established private precedent, no peer group, and a thicket of state and central permitting, required either madness or genuine conviction. The Australians had conviction, and for a while it paid off.

Their headline discovery came at Ganajur, in Karnataka's Haveri district. Here the drill bits found a genuinely attractive deposit: roughly 308,000 ounces of gold—about 9.5 tonnes—at an open-pit grade of three to four grams per tonne.[^2]4 For the non-geologist, grade is everything in mining, and a simple analogy helps. Imagine two orchards. In one, you shake a tree and a single apple falls; in the other, a dozen come down. Both are apple trees, but only one is worth the cost of harvesting. Three-to-four grams per tonne is a generous shake of the tree for an open-pit operation—high enough that you can dig the ore from surface rather than tunnelling expensively underground, and rich enough that the economics genuinely work. Ganajur looked like a mine waiting to happen.

And then the ground shifted—not geologically, but legally.

In 2015, the Indian government enacted sweeping amendments to the Mines and Minerals (Development and Regulation) Act—the MMDR Act.3 The intent was honourable. For decades, the allocation of India's mineral wealth had run on a "first-come, first-served" basis, a system that had curdled into one of the great corruption swamps of Indian public life, immortalised by the coal-allocation scandals of the era. The 2015 reform swept all that away and replaced it with a clean, transparent auction-only regime: henceforth, mineral blocks would be awarded to the highest bidder at public auction.3

For new exploration it was a sensible, modernising fix. For companies like Deccan Gold Mines, which had spent years and capital discovering a deposit under the old rules, it was a trap with the jaws snapping shut. The Union Ministry of Mines interpreted the new law to mean that legacy exploration licences—the very permits that gave Deccan the right to convert its Ganajur discovery into a mining lease—were effectively null and void.34 The logic was brutal: you found the gold, but you cannot mine it; if you want it, bid for it at auction against everyone else, including against the value your own drilling created.

This is the moment the company's story curdles into something close to tragedy. Deccan had done the hard, risky, expensive part. It had found the apples. And just as it readied the harvest, the orchard was declared up for auction. The flagship asset froze. What followed was the lost decade—a grinding war of litigation, representations, and waiting, the company burning cash with no producing asset to offset it, while its Australian founders grew older waiting, in essence, for a single bureaucratic signature that never came.[^2]

A lesser company, or a more impatient set of owners, would have folded. Instead, the long stalemate set the stage for the most consequential decision in Deccan's history: the realisation that if you cannot win the game in front of you, you change the board entirely. That realisation arrived with a new man at the top.

III. The Great Pivot: Dr. Prasad's Global Chess Game

Every long corporate ordeal seems to produce, eventually, the person who decides the ordeal is optional. For Deccan Gold Mines, that person was Dr. Hanuma Prasad Modali, who stepped into the Managing Director's chair in October 2021.[^2]8

Dr. Prasad is worth lingering on, because he is not the founder-promoter archetype that dominates Indian corporate storytelling. He is a professional, an academic geologist with a doctorate and a career's worth of practical exploration behind him—a man who reads rock for a living and, crucially, who understood that the company's most dangerous adversary was not geology or markets but time itself.8 An exploration company with no production is a vessel that only loses water. Every year spent waiting for the Ministry of Mines to relent was a year of cash burned against the slim hope of a signature. Dr. Prasad's defining insight was almost coldly logical: waiting was not a strategy, it was a slow death sentence.

So he changed the board. The pivot he engineered was a wholesale reimagining of what Deccan Gold Mines was for. The old company was a passive domestic explorer, sitting on a frozen asset and petitioning the state. The new company would be an aggressive multinational producer. If the regulatory pipes in India were clogged, you did not stand under the dry tap and wait—you went and found taps that flowed, anywhere on Earth they happened to be. The destination he chose first surprised almost everyone: Kyrgyzstan.

The Kyrgyzstan Venture

In July 2023, Deccan Gold Mines acquired a 60% controlling interest in Avelum Partners LLC, the developer of the Алтын Тор Altyn Tor Gold Project, located in the Soltan Sary gold belt of the Tian Shan mountains in Kyrgyzstan.2 To a casual observer this looked like a tiny Indian micro-cap wandering improbably into post-Soviet Central Asia. To Dr. Prasad it was a textbook case of buying production capability that India's own rules would not let him build at home.

The deal structure is where the strategy gets genuinely interesting—and where it became briefly controversial. This was a non-cash transaction. Deccan did not have a war chest of dollars to spend; what it had was equity in a listed company. So it paid in shares, issuing 1.85 crore—18.5 million—new equity shares in a share swap valued at roughly $14.8 million, about ₹122 crore at the time.2 For a company with limited cash, paying in your own paper is the elegant move; you conserve liquidity and hand the seller upside in your story. The catch is dilution, and here the catch had teeth.

The shares were issued at a negotiated price of ₹53.47 each. The problem: the stock was trading around ₹77 at the time, meaning the new paper was handed over at roughly a 30% discount to market.2 Worse, the issuance expanded the company's share base by something like 58%—well over half again as many shares as existed before. Retail shareholders, who had endured the lost decade, did the arithmetic and were not amused: their ownership of the company was being meaningfully diluted, and at a discounted price to boot. The complaints were loud and, on the face of the numbers, understandable.

But step back and look at what was actually being bought, because the valuation tells a more flattering story. Altyn Tor holds roughly 180,000 ounces of gold resources.2 Put the share consideration together with assumed liabilities and the total implied project value lands around $24.7 million—which works out to roughly $137 per resource ounce in the ground. In the world of Central Asian development-stage gold assets, the going rate for an ounce of in-situ resource typically runs somewhere between $80 and $150. So Deccan paid toward the upper-middle of a normal range—not a steal, but not a fleecing either.

What justified the price was the type of deposit. Altyn Tor is an open-pit, "free-milling" gold project, and that phrase carries enormous economic weight. "Free-milling" means the gold can be liberated using simple, cheap physical methods—gravity separation and basic leaching—rather than the punishing chemistry and capital of "refractory" ore, where the gold is locked inside sulphide minerals and must be roasted or pressure-oxidised at great expense before it will give itself up. Think of it as the difference between cracking an egg and cracking a safe. On top of that, the project came with a large low-grade tailings stockpile—essentially a pile of already-mined material—sitting ready for immediate, low-cost processing. You could start making money almost the moment the plant switched on, without waiting years to develop a fresh pit.

History has been kind to the decision, which is the ultimate referee of any controversial deal. The shares Deccan issued at ₹53.47 were, by June 2026, worth more than ₹400 crore as the stock climbed past ₹200—meaning the sellers and the company alike rode the same wave, and the dilution that so angered shareholders bought an asset that appreciated alongside everything else.12 More importantly, the asset delivered operationally: the gravity plant was successfully commissioned in May 2026, with full-scale gold doré production—the rough gold-silver bars that mines ship to refiners—slated to begin in August 2026, targeting an annual output of 300 to 350 kilograms of gold.26 A company that had never produced an ounce in India was, within roughly two years of the pivot, about to pour gold bars in the Tian Shan.

The Kyrgyz gambit proved the thesis: Deccan could go anywhere, structure a deal creatively, and turn a frozen balance sheet into operating assets. But to understand whether the company is genuinely valuable or merely interesting, you have to do what every serious investor must—lay the assets side by side and ask, unsentimentally, where the money actually is.

IV. Sizing the Portfolio: Where the Money Actually Is

Mining stories are seductive precisely because every project sounds thrilling—every drill hole is "high-grade," every belt is "prospective," every press release glitters. The discipline of investing in them lies in ruthlessly weighting each asset by what it can actually contribute to cash flow and value, and refusing to let a shiny early-stage exploration play distract from the boring asset that actually pays the bills. So let us size Deccan's portfolio honestly, in rough order of what each piece is worth to the thesis.

1. The Swarnagiri (Jonnagiri) Gold Project — The Immediate Cash Engine

This is the heaviest weight in the portfolio, plausibly around 45% of the value case, for the simplest of reasons: it is producing now. Deccan's 27.67% stake in Geomysore gives it a meaningful slice of a genuinely good mine.[^2][^8] The structure here is the key to its appeal. Deccan does not have to fund the whole operation. The operational and capital muscle comes from Thriveni Earthmovers, one of India's largest contract miners, which handles the heavy lifting of actually moving and processing rock, while Lloyds Enterprises sits as a major equity holder with roughly 31.58% and brings financial heft.[^2][^8] Deccan keeps a substantial chunk of the upside while shielding its own modest balance sheet from the brutal capital intensity of mine construction.

The geology is the kind that makes the economics sing. The first 500 acres of the concession have confirmed roughly 13 tonnes of gold, with projections running as high as 50 tonnes across the full 1,500-acre concession.[^8] It is a high-grade open-pit operation, which means low-cost ounces. The production ramp targets 400 kilograms of gold in the first year, scaling toward one to two tonnes per annum as the operation matures.[^8] Now apply the price. With domestic gold fetching around ₹75 lakh per kilogram, even the modest Year-One target of 400 kilograms implies revenue measured in the hundreds of crores, against the low operating costs of a high-grade open pit.4[^8] This is not a speculative option; it is a near-term cash cow, and it is the reason the June 2026 ribbon-cutting mattered so much.

2. The Ganajur Gold Project — The Wholly-Owned Crown Jewel

If Swarnagiri is the engine, Ganajur is the sleeping giant—and arguably the most valuable single thing Deccan owns, perhaps 40% of the value case, because it owns 100% of it. There are no JV partners to share with, no minority stake to dilute the upside. The asset we met earlier—roughly 9.5 tonnes at three-to-four grams per tonne—had been the company's frozen heartbreak for a decade.[^2]4

The June 2026 Supreme Court ruling changed the math entirely. By protecting pre-2015 lease applications, the judgment removed the existential threat that had hung over Ganajur: the fear that Deccan would have to bid at auction, against all comers, for the right to mine a deposit it had discovered with its own capital.[^4]4 De-risked in a single stroke, Ganajur becomes an asset Deccan can develop on its own terms, capturing the full value of its grade without auction-forced dilution of the economics. The reason this matters so much to the thesis is ownership concentration: a wholly-owned, de-risked, high-grade open-pit deposit is worth far more per ounce to shareholders than the same ounces split three ways. The market's 20% leap on the ruling was, in essence, the value of Ganajur waking up.4

3. The Altyn Tor Project — Near-Term Global Diversification

We have already walked through the Kyrgyz deal, so here it earns its place in the portfolio as roughly 12% of the value case—real, near-term, but smaller in absolute terms than the two Indian assets. The project is underpinned by a $4.2 million loan from Beyond The Crowd Ventures, the gravity plant is running, and the leaching circuit was slated to go live in June 2026 to lift recovery rates further.26 Its strategic role is diversification: a producing asset in a different jurisdiction, denominated in a different risk profile, that proves the company can operate beyond India's borders. It is the smallest of the three producers but the one that turns "Indian explorer" into "multinational miner."

The Speculative Novelties

Everything else belongs in the optionality bucket—perhaps 3% of the value case combined—and the right way to hold these in your head is as cheap lottery tickets that cost little and might, someday, matter.

The most colourful is Mozambique lithium. In May 2024, through its Dubai subsidiary Deccan Gold FZCO, the company formed a 51% joint venture—Deccan Gold Mozambique Ltda, or DGMOZ—in the LCT-pegmatite-rich Moçambique Alto Ligonha belt, a region geologists prize for the lithium-caesium-tantalum mineralisation that feeds the battery economy.7 Deccan shipped a first 150-tonne pilot batch of lepidolite—a lithium-bearing mica—to China in September 2024.7 But the Mozambican state changed the rules underneath them: new 2026 mineral laws require a 15% state stake in projects and ban the export of unprocessed raw material, forcing Deccan to invest in local modular processing if it wants to continue.7 It is best understood as a long-dated option on the EV battery supply chain—genuinely interesting, genuinely uncertain, and emphatically not a reason to own the stock today. It does not crowd out the gold story; it sits quietly beside it.

Two other early-stage plays round out the collection: the Bhalukona nickel-chromium-PGE project in Chhattisgarh, where a nickel-copper-palladium discovery was reported in May 2026, and a tungsten agreement through España Logrosán Minera in Spain.[^2] Both are low-capital, high-optionality exploration bets—the kind of cheap ground that costs little to hold and occasionally turns into something. For now, they are footnotes to the gold thesis, and honest sizing keeps them there.

With the assets weighed, the obvious next question is why this little company gets to own any of this at all. Why is there no swarm of competitors? The answer lies in the strange, almost absurd structure of the Indian gold industry itself.

V. The Economics of Gold Mining & Competitive Moats

Here is a paradox worth savouring. India is arguably the most gold-obsessed society on Earth. Gold is woven into weddings, into festivals, into the household savings of hundreds of millions of families who trust a bangle over a bank. The country consumes well north of 800 tonnes a year. And it mines essentially none of it—India imports something on the order of 99.8% of its requirement, hauling the metal in from Switzerland, the UAE, and beyond, year after year, in one of the great structural trade deficits of the national accounts.[^2] A nation that adores gold has, for decades, been almost entirely unable to produce its own. That gap between obsession and production is the entire commercial opportunity, and it explains why a competitive analysis of Deccan reads so unusually.

Consider the incumbents, such as they are. The only meaningful domestic gold producer is the state-owned Hutti Gold Mines in Karnataka, which grinds out a modest 1.5 to 2 tonnes of gold a year using deep, ageing, high-cost underground methods—the mining equivalent of a steam engine still chugging in an age of electric trains.[^2] The legendary Kolar Gold Fields, the deep mines that once made the region world-famous, shut down in 2001, exhausted and uneconomic. There is no other private competitor of consequence anywhere in India. This is the rarest of situations in business: a vast, captive, growing demand pool served by a single sluggish state monopoly and almost nothing else.

To understand why that moat is so durable, two analytical frameworks earn their keep here.

Hamilton's 7 Powers

Of Hamilton Helmer's seven sources of durable competitive advantage, two apply to Deccan with unusual force.

The first, and the decisive one, is Cornered Resource. This is the power you have when you possess preferential access to a coveted asset that others simply cannot get. Deccan's mining leases at Swarnagiri and Ganajur are precisely that. Recall the trap of the 2015 MMDR Act: by abolishing the old licensing system and forcing everything through auctions, the reform made it virtually impossible for a private player to obtain a new gold lease without a ruinous, value-destroying bid.3 But Deccan's concessions are grandfathered—legacy assets, now explicitly protected by the June 2026 Supreme Court ruling.[^4]4 In other words, the same regulatory wall that imprisoned Deccan for a decade has, now that the company is on the right side of it, become the very thing that keeps everyone else out. The drawbridge that nearly trapped them inside is now raised behind them. There is a delicious irony in a moat that was, for ten years, a prison.

The second is Process Power, or what we might call regulatory navigation. Successfully threading the Indian Ministry of Mines, SEBI, multiple state mining departments, and—after the pivot—the foreign ministries and mining codes of Kyrgyzstan and Mozambique requires a specialised, almost generational institutional memory. This is not a capability you can buy off a shelf or hire in a quarter. The proof is in who failed: global giants of the calibre of Rio Tinto explored India and ultimately walked away in frustration at the permitting maze. Deccan did not have the option of walking away—it had only one country and one asset to fight for—and in being forced to master the maze, it built a competence that the giants never bothered to acquire. Survival, in this case, was itself the moat.

Porter's Five Forces

Run Deccan through Michael Porter's classic five-forces lens and the picture is almost comically favourable on two of the axes.

Start with the bargaining power of buyers, which is effectively zero. A gold miner does not have customers in any normal sense, does not run a sales force, does not negotiate contracts or worry about a concentrated client walking away. Gold is the ultimate commodity—you sell it instantly at the London Bullion Market Association spot price, the same price available to every seller on the planet. There is no customer concentration risk because there is, functionally, no customer relationship at all. You produce a bar; the world buys it at a published number.

Competitive rivalry, the force that grinds down margins in most industries, is similarly near-absent. A sluggish state monopoly producing a tonne or two a year, a structural national supply deficit, and no private peers add up to something close to a blue ocean. Deccan is not fighting for share in a crowded pool; it is one of the only swimmers in an enormous one.

The remaining forces are not zero—the threat of new entrants is precisely what the auction regime now suppresses, the power of suppliers like contract miners is real (which is why the Thriveni structure matters), and substitution is a macro question about gold itself rather than about Deccan. But the headline is unmistakable: this is a company operating in a market structure most businesses can only dream of.

A fortress is only as good as the people manning it, though, and the next question is whether Deccan's leadership has its own money on the line—or whether shareholders are funding someone else's experiment.

VI. The Playbook & Management Skin in the Game

The cynical read on any micro-cap with a soaring stock is that insiders are riding public money. So it is worth examining, with some care, exactly how Deccan's leadership is incentivised—because the structure here is unusual, and tells you something about how the company actually works.

Start with Dr. Prasad himself. He is, as noted, a professional executive rather than a legacy founder—he did not inherit the company or build it from a garage, he was brought in to fix it.8 His direct ownership is modest but genuinely material for a salaried manager: roughly 1.12 million shares, around 0.41% of the company's capital.8 That is not the commanding stake of a promoter, but it is real money tied to the same outcome as every other shareholder. The more telling signal came on May 4, 2026, when Dr. Prasad exercised 800,000 ESOP shares at an average exercise price of just ₹20 per share.8 With the stock trading at a large multiple of that price, the exercise converted a paper incentive into a sizeable personal position—and crucially, it bolted his net worth directly onto the public share price. When insiders exercise and hold rather than exercise and immediately dump, it is one of the cleaner alignment signals an outside investor can read.

The ownership structure as a whole is worth understanding because it shapes both the risk and the trading character of the stock. The institutional promoter group—comprising Rama Mines (Mauritius), Hira Infra Tek, and Australian Indian Resources—holds 20.62%.1 That is a relatively low promoter holding by Indian standards, where founding families routinely sit above 50%. The flip side is an unusually large and liquid 79.38% public float.1 For investors, this cuts both ways: a large float means the stock is genuinely tradable and less subject to promoter whim, but a modest promoter stake also means less of the concentrated, skin-in-the-game ownership that some investors prize. It is a more democratic cap table than most of corporate India, for better and worse.

The Playbook

The strategic playbook Dr. Prasad has run is best summarised as a deliberate shift from capital-heavy self-funding to a smart, asset-light, JV-partnered model. The old Deccan tried to do everything itself, and the result was a balance sheet that only bled. The new Deccan brings in partners who supply the capital and operational firepower while Deccan retains a meaningful equity slice of the upside.

Swarnagiri is the cleanest illustration. By bringing in Thriveni Earthmovers to shoulder the operational capital expenditure of building and running the mine, Deccan kept its own balance sheet largely shielded from the most dangerous, cash-devouring phase of mining—construction and ramp-up—while still holding 27.67% of a producing asset.[^2][^8] The Altyn Tor deal applied the same instinct in a different key: pay in equity rather than scarce cash, and fund operations partly through external loans rather than dilutive equity raises.2 It is the playbook of a company that learned, the hard way, that the fastest route to death in mining is to run out of money before you run into gold. Whether that discipline holds as the company scales is exactly the question the bull and bear cases turn on.

VII. The Bear vs. Bull Case

Every great story has a skeptic in the room, and a company that has risen this far this fast deserves a hard look from both directions. Let us war-game it honestly.

The Bear Case

The first and most obvious worry is geopolitical and jurisdictional risk. The pivot that saved Deccan also scattered its assets across some genuinely unpredictable corners of the world. Kyrgyzstan, through Avelum Partners, is a small Central Asian republic with a history of political volatility and a habit, common to resource-rich frontier states, of revisiting the terms of foreign mining deals when commodity prices rise. Mozambique has already demonstrated exactly this danger: the 2026 mineral laws that retroactively demanded a 15% state interest and banned raw exports are a textbook example of resource nationalism reaching into a project after the foreign partner has already committed capital.7 When you mine in frontier jurisdictions, the geology is the easy part; the government is the variable.

The second worry is execution. Mining is notoriously, almost proverbially, prone to delay—plants that do not commission on schedule, recovery rates that disappoint, ore that proves harder to process than the drill core promised. Deccan is attempting to ramp not one but two operations into steady commercial production simultaneously—Swarnagiri in Andhra Pradesh and Altyn Tor in Kyrgyzstan—while also gearing up to develop the newly-revived Ganajur. Each carries the risk of a processing bottleneck, a ramp slower than projected, or a costly technical surprise. A company that has never run a steady-state producing mine is, by definition, doing all of this for the first time.

The third, and for a valuation-minded investor the most sobering, is the multiple. With a market capitalisation around ₹4,330 crore—roughly $520 million—and effectively zero history of meaningful GAAP earnings, the stock trades almost entirely on future hope.14 The price embeds an assumption that the three-mine pipeline will deliver cleanly and on time. That is a heavy load for a future to carry. The brutal arithmetic of a hope-priced stock is that any operational stumble—a missed production target, a regulatory reversal, a softening in gold—can trigger severe multiple compression, and the fall from such heights is far quicker than the climb. Investors paying today's price are, in effect, underwriting near-flawless execution.

The Bull Case

Now turn the board around. The bull case rests first on the tri-star pipeline—the sheer speed of the transformation. Within roughly twelve months, Deccan moves from a company that had never produced a single ounce to one holding cash-flowing stakes in three separate gold mines across two countries: Swarnagiri in Andhra Pradesh, Altyn Tor in Kyrgyzstan, and the revived Ganajur in Karnataka.4[^8]6 Companies almost never re-rate on three independent catalysts firing in such close succession; the diversification across assets and jurisdictions also cushions the very execution risk the bears fear, because a stumble at one mine no longer sinks the whole story.

The second pillar is the macro tailwind. Global gold prices have been flirting with lifetime highs, around ₹75 lakh per kilogram in the domestic market.4[^8] Deccan is a pure, unhedged, leveraged play on the metal—as a producer with low-cost open-pit ounces, every rupee of gold-price appreciation flows toward the bottom line with operational leverage that a jewellery retailer or an importer simply does not enjoy. If your thesis is that gold stays strong, there are few cleaner ways to express it on the Indian market.

The third pillar is the moat we dissected earlier, and it bears restating only in its sharpest form: Deccan owns the only private gold mines in a country that is structurally, culturally, and almost spiritually obsessed with gold, protected by a regulatory wall that keeps competitors out. That is a genuinely rare position, and rare positions, when they finally start producing cash, tend to be valued generously.

So which KPIs actually matter for tracking whether the bull or the bear is right? Resist the temptation to drown in metrics. For this company, three numbers tell the story. First, gold production volumes—the kilograms and eventually tonnes actually poured at Swarnagiri and Altyn Tor against the stated targets, because production-versus-guidance is the single cleanest test of whether the execution bear is winning. Second, the development progress and lease status at Ganajur, because the wholly-owned crown jewel is where the largest unencumbered value sits, and its conversion from court victory to construction to production is the swing factor in the long-term thesis. Third, all-in sustaining cost per ounce as the operations mature, because in a commodity business you do not control your selling price—you only control your cost, and the gap between the two is the entire game. Track those three, and you will know far more about Deccan's trajectory than any quarterly headline can tell you.

VIII. Conclusion & The Acquired Carat Rating

Strip away the geology and the regulatory arcana and the cross-border deal structures, and Deccan Gold Mines is, at its core, a story about refusing to die. For twenty years this company sat on a discovery it was not allowed to mine, watched its founders age, burned cash in a regulatory desert, and was given every reasonable excuse to fold. It did not. Instead, under Dr. Prasad it changed the board it was playing on—going to Kyrgyzstan when India said no, paying in paper when it had no cash, partnering with operators when it could not fund mines alone—and then, in a single improbable week of June 2026, watched the Supreme Court and a Chief Minister with a pair of scissors deliver the two things it had waited two decades for.

It is the ultimate tale of corporate patience rewarded: a company that survived long enough for the world to come around to the thing it had believed all along—that the ancient greenstone of southern India hides real gold, and that someone, eventually, would be allowed to dig it.

As Ben and David might put it: this is not really a mining company at all. It is a twenty-year call option on Indian precious metals—an option that traded for pennies, that nearly expired worthless in the regulatory cold, and that just, finally, slipped into the money.

References

-

BSE India — Deccan Gold Mines Limited Stock Price, Corporate Announcements & Shareholding (532408) ↩↩↩↩↩

-

Deccan Gold Mines Limited — Official Investor Relations & Filings Portal ↩↩↩↩↩↩↩↩

-

Ministry of Mines, Government of India — Mines and Minerals (Development and Regulation) Act (MMDR) 2015 Amendments & Legacy Guidelines ↩↩↩↩

-

Deccan Gold Mines Shares Surge 20% to Fresh Lifetime Highs Following Supreme Court Ruling — The Economic Times, 2026-06-15 ↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Andhra Pradesh Cabinet Renames Jonnagiri to 'Swarnagiri' Ahead of Historic Private Gold Mine Launch — The Times of India, 2026-06-20 ↩

-

Deccan Gold Commences Milling and Gravity Trial Runs at Altyn Tor Project in Kyrgyzstan — Business Standard, 2025-12-11 ↩↩↩

-

Deccan Gold Acquires Majority Stake in Mozambique Lithium Blocks; Moves Into Critical Minerals — Rediff Business, 2024-05-18 ↩↩↩↩

-

Dr. Hanuma Prasad Modali Acquires Shares via ESOP Exercise; Aligns Skin In The Game — Trendlyne, 2026-05-04 ↩↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube