DCM Shriram: From Colonial Mills to Chemical Conglomerate

I. Introduction & Cold Open

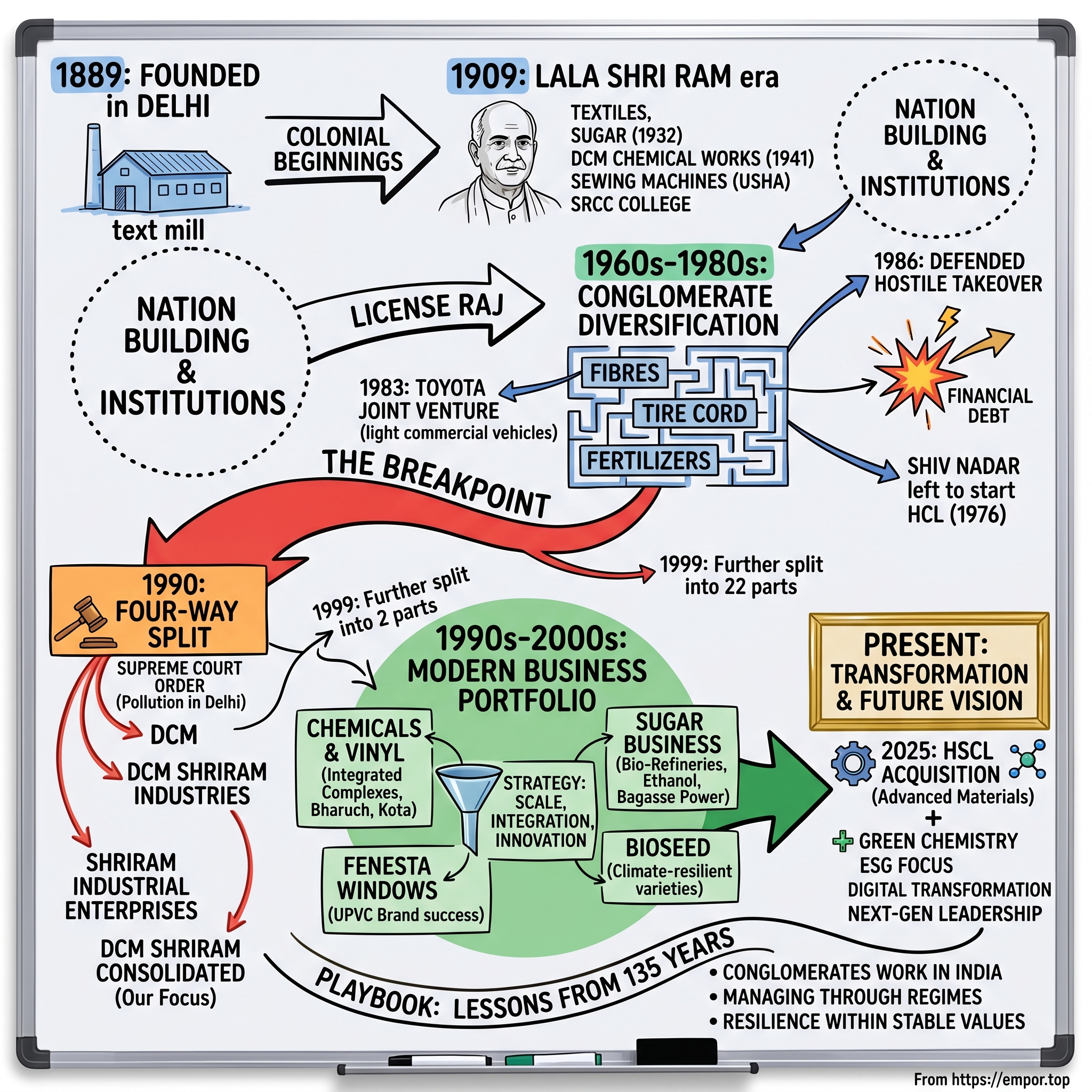

The year is 1889. Delhi's old city hums with the sounds of horse-drawn carriages and street vendors. In a modest office near Chandni Chowk, three men—Lala Chunnamal, Master Shiv Pershad, and Rai Bahadur Ram Kishen Das Gurwale—sign papers that will outlive the British Raj itself. They're incorporating Delhi Cloth & General Mills under Act VI of 1882, betting that India's ancient textile tradition can be mechanized, modernized, and scaled. None of them could have imagined that 135 years later, their creation would transform into a ₹20,779 crore market cap conglomerate generating ₹12,741 crore in annual revenue—not from textiles, but from chemicals, sugar, and seeds.

This is the improbable story of DCM Shriram, a company that survived colonial rule, thrived through partition's chaos, navigated the License Raj's bureaucratic maze, and emerged from the 1991 liberalization as something entirely different from its origins. Today, it operates chlor-alkali plants in Gujarat, sugar mills across Uttar Pradesh, fertilizer facilities in Rajasthan, and even manufactures the UPVC windows in modern Indian homes through its Fenesta brand.

The central question isn't just how a textile mill became a chemical powerhouse—it's how any company survives 135 years of such radical transformation. The answer lies in a peculiarly Indian form of corporate evolution: the ability to shed skins like a snake, to rebuild from first principles when the environment demands it, and to find opportunity in the very constraints that destroy others.

What follows is a journey through colonial beginnings, the vision of Lala Shri Ram who would become Sir Shri Ram, the partition that nearly destroyed everything, the License Raj years that forced bizarre diversifications, the 1990 Supreme Court judgment that literally expelled factories from Delhi, and the modern transformation under the Shriram brothers. It's a story about how conglomerates actually work in emerging markets—not as unfocused behemoths, but as adaptive organisms that survive by being everything to everyone when the market won't let you be one thing perfectly.

We'll examine how DCM Shriram built integrated chemical complexes that turn salt into caustic soda and chlorine, how it runs sugar mills that generate their own power and produce ethanol, how it survived hostile takeover attempts from UK investors, and why Shiv Nadar left in 1976 to start HCL. We'll decode the 1990 split that created four separate companies, the family dynamics that determined who got what, and the strategic logic behind staying diversified when every MBA textbook says to focus.

This isn't just corporate history—it's a masterclass in institutional resilience, a blueprint for managing through multiple economic systems, and a case study in how family businesses can professionalize without losing their entrepreneurial soul. From its founding three years before Gandhi arrived in India to its recent acquisition of Hindusthan Speciality Chemicals in 2025, DCM Shriram has been both a witness to and participant in the creation of modern India.

II. The Lala Shri Ram Era & Nation Building (1889–1960s)

The transformation began in 1909 when a 25-year-old named Lala Shri Ram walked through the gates of Delhi Cloth Mills. His family had made their fortune in banking and trading, but young Shri Ram saw something different in those mechanical looms—not just profit, but the possibility of industrial nation-building decades before independence was even imaginable. Within years, he had acquired controlling interest, and by 1920, he was running what would become one of pre-independence India's most ambitious industrial experiments.

The 1889 founding by Lala Chunnamal and his partners had established the foundation—Delhi Cloth & General Mills was among India's earliest mechanized textile operations, competing directly with Manchester imports that had decimated traditional Indian weavers. But under Lala Shri Ram's leadership, it became something far more ambitious. He didn't just want to make cloth; he wanted to prove that Indians could build and run modern industrial enterprises at any scale.

By the 1930s, Shri Ram was diversifying with an almost manic energy. Sugar seemed logical—India imported massive quantities despite having ideal growing conditions. In 1932, he established sugar operations, integrating backward to work directly with farmers. The Lyallpur Textile Mills expanded the textile footprint. Then came the 1938 acquisition of Jay Engineering Works, which would later become Usha—yes, the sewing machine and fan company that still exists today. Each move wasn't random; it was about capturing more of the value chain and reducing dependence on imports.

The 1941 establishment of DCM Chemical Works marked a crucial pivot. While others saw chemicals as too complex for Indian companies, Shri Ram saw it as essential infrastructure for an industrial economy. The British colonial government, recognizing his contributions to the war effort and industrial development, knighted him in 1943—he became Sir Shri Ram, one of the few Indian industrialists to receive such recognition during the Raj.

But Sir Shri Ram's most significant contribution wasn't building factories—it was building institutions. He was one of seven architects of the Bombay Plan, the 1944 blueprint for India's post-war economic development created by leading industrialists including J.R.D. Tata and G.D. Birla. The plan, radical for its time, called for a mixed economy with significant state intervention—essentially designing the economic framework that independent India would adopt. When the Reserve Bank of India was established in 1935, Sir Shri Ram served on its first Board of Directors, helping design the monetary infrastructure for a nation that didn't yet exist. The post-independence period saw even more aggressive expansion. In 1948, the company launched the Swatantra Bharat Mills, and by 1956, it had established the DCM Silk Mills. The name "Swatantra Bharat" (Free India) wasn't accidental—it represented Sir Shri Ram's belief that industrial self-reliance was the truest form of independence. Each new facility wasn't just capacity addition; it was nation-building infrastructure.

Sir Shri Ram's institution-building went beyond factories. In 1920, Shri Ram conducted the first experiment in vocation-oriented education by founding the Commercial Education Trust (CET). The first school promoted by CET was the commercial high school, which was raised in 1926 to the standard of an intermediate college, in 1930 to a degree college, and in 1934 to a post-graduate college. This became the Shri Ram College of Commerce, today one of India's most prestigious institutions. Lady Shri Ram College for Women was established in 1956, in New Delhi, by Ram in memory of his wife Phoolan Devi.

The philosophy driving all this wasn't mere profit maximization. Sir Shri Ram believed that business had a duty to society—that industrialists were trustees of national wealth. The Shriram Institute for Industrial Research, founded in 1947 by Shri Ram, started functioning in 1950. Shri Ram believed that if India was to catch up with the rest of the world, it was necessary to understand existing technology and innovate it through research. This wasn't corporate social responsibility as we understand it today—it was something deeper, an almost spiritual belief that business success without social progress was meaningless.

By Sir Shri Ram's death in 1963, DCM had become an industrial empire spanning textiles, sugar, chemicals, vanaspati, pottery, fans, sewing machines, electric motors, and capacitors. But more importantly, it had created a template for how Indian business could operate—technically competent, socially conscious, and institutionally robust. The company he built would soon face its greatest test: surviving without its founding genius.

III. Building the Conglomerate: License Raj Navigation (1960s–1980s)

The 1960s opened with DCM facing an existential question: Could an institution built around one man's vision survive without him? Sir Shri Ram's death in 1963 left a sprawling conglomerate that manufactured everything from textiles to chemicals, but also left a leadership vacuum that lesser companies might not have survived. What followed was a masterclass in navigating India's License Raj—that byzantine system of permits, quotas, and government approvals that could make or break industrial ambitions.

The company's response was counterintuitive: instead of consolidating, it diversified even further. Under the License Raj, you couldn't simply expand existing capacity—you needed government permission for everything from importing machinery to increasing production. But you could get licenses for new industries, especially if they aligned with government priorities. DCM's leaders understood this game perfectly. They expanded into rayon when the government wanted import substitution, into tire cord when the automotive industry needed supplies, into fertilizers when the Green Revolution demanded agricultural inputs. In 1983, the company formally changed its name from Delhi Cloth & General Mills to DCM Limited, symbolically acknowledging that it had evolved far beyond textiles. That same year, they entered into a partnership with Toyota to manufacture light commercial vehicles—a coup in an era when foreign collaborations were rare and heavily regulated. The Toyota partnership represented something deeper: DCM had the political capital and bureaucratic expertise to navigate approvals that would have stymied lesser companies.

But the most dramatic moment came in the mid-1980s. Lord Swraj Paul, the UK-based businessman, made a hostile bid for takeover of DCM. The promoter shareholding had gradually declined over the years, making the company vulnerable. It was this reduced holding that encouraged Paul to make a hostile bid for the company in 1986. Ironically, DCM was going through a resurgence at the time, after years of internecine battles, thanks to a tieup with Japanese auto major Toyota. Staving off the takeover - which it succeeded at - proved, however, financially damaging for the company, leaving it heavily indebted.

The hostile takeover defense revealed both the strength and weakness of the conglomerate model. On one hand, DCM's diversified revenue streams and political connections helped it resist the raid. On the other, the complex holding structure and family disputes had left it vulnerable in the first place. The successful defense came at a terrible cost—the company emerged victorious but financially crippled, setting the stage for the dramatic restructuring that would follow. One of the most intriguing subplots of this era involves Shiv Nadar, who would later found HCL Technologies. Nadar started his career as part of the elite DCM management trainee system. It was at DCM that he met the people with whom he later started HCL in a Delhi Barsati "akin to a garage startup" with a compelling vision that the microprocessor would change the world. His interest in computers began when he was working at Delhi Cloth Mills (DCM) in the calculator division as an engineer. Along with six other colleagues, he quit DCM in 1976 and founded Microcomp Limited. The departure of Nadar and his colleagues to start what would become one of India's largest IT companies represents both DCM's strength as a talent incubator and its weakness in retaining entrepreneurial minds constrained by conglomerate bureaucracy.

The 1970s brought financial troubles that tested the conglomerate's resilience. The oil crisis, labor unrest, and increasing competition from both domestic players and imports (when allowed) squeezed margins across all divisions. The complex holding structure that had enabled diversification now became a liability—capital was trapped in underperforming units, cross-subsidization masked individual business performance, and family disagreements about strategic direction created paralysis.

The Toyota partnership of 1983 seemed like salvation—a world-class manufacturer choosing DCM as its Indian partner for light commercial vehicles. But this too revealed the challenges of the era. The partnership would end in 1995, unable to navigate the conflicting demands of Japanese manufacturing excellence, Indian regulatory requirements, and DCM's own complex decision-making structure. The subsequent partnership with Daewoo Motors would meet an even worse fate, ending in 2001 when Daewoo went bankrupt.

Through it all, DCM survived by mastering the art of regulatory arbitrage. When you couldn't expand textiles, you expanded chemicals. When chemicals faced restrictions, you moved into fertilizers. When urban manufacturing became difficult, you established rural plants. It was industrial strategy as jazz improvisation—responding to each regulatory chord change with a new business melody. This approach created enormous complexity but also remarkable resilience. By the late 1980s, DCM was generating revenues across dozens of business lines, employed tens of thousands, and had become too big to fail. But it was also too complex to manage effectively, setting the stage for the dramatic restructuring ahead.

IV. The Great Restructuring: Birth of DCM Shriram (1989–1990)

The restructuring that created DCM Shriram began not in boardrooms but in India's highest court. The razing was the result of a 1989 Supreme Court decision which drove factories out of the city of Delhi. The judgment, aimed at reducing Delhi's pollution, ordered all polluting industries to relocate outside city limits. For DCM, whose original textile mill had operated in Delhi for exactly a century, this wasn't just an operational challenge—it was an existential crisis that would trigger the most dramatic corporate restructuring in Indian business history.

The court order coincided with mounting family tensions that had been simmering since the 1970s. The third generation of the founding family now included multiple branches, each with different visions for the conglomerate's future. Some wanted to modernize and focus on high-growth sectors, others preferred the stability of traditional businesses, and still others questioned whether the conglomerate structure itself made sense in a liberalizing economy. The Supreme Court judgment became the catalyst that forced a resolution.

As the eventual result of the failed takeover, DCM was split into four distinct companies in 1990. The four companies were: DCM, DCM Shriram Industries, Shriram Industrial Enterprises and DCM Shriram Consolidated. This wasn't a simple division—it was a surgical separation of a century-old organism into four viable entities, each with its own strategic logic and family leadership.

DCM Shriram emerged from this split with a specific mandate: take the chemical and agri-business operations and build them into a focused industrial enterprise. The company inherited Shriram Fertilizer & Chemicals, Shriram Cement Works, Swatantra Bharat Mills, and DCM Silk Mills. On paper, it looked like a random collection of assets. In reality, there was a strategic thread: these were businesses that could benefit from integration, where chemicals fed into fertilizers, where agricultural operations created captive markets, where industrial infrastructure could be shared.

The mechanics of the split were Byzantine. Assets had to be valued, liabilities allocated, employees reassigned, and contracts renegotiated. Some businesses were literally split—the sugar operations went to different entities based on plant location. The brand itself was divided, with each entity getting rights to use "DCM" or "Shriram" in specific contexts. Shareholders received proportional stakes in all four entities, creating a complex web of cross-holdings that would take years to unwind.

In 1999 there was further splintering of the company into two additional parts. The initial four-way split hadn't fully resolved the underlying tensions. Different family branches still had overlapping interests, and the partial separation created new conflicts over shared resources and market territories. The 1999 restructuring was an attempt to create cleaner boundaries, with each family branch getting clearer control over specific businesses.

What emerged from this chaos was remarkable: instead of destroying value, the restructuring unlocked it. Each entity, freed from the bureaucracy of the mega-conglomerate, could move faster, make clearer strategic choices, and access capital markets independently. DCM Shriram, in particular, benefited from this focus. No longer needing to subsidize struggling textile operations or negotiate with multiple family stakeholders, it could invest aggressively in its core chemical and agri-business operations.

The human dimension of this restructuring often gets overlooked. Thousands of employees who had joined "DCM" suddenly found themselves working for new entities with uncertain futures. Many senior managers had to choose sides in family disputes. Entire departments were dismantled and reformed. Yet remarkably, there were no major labor disputes, no significant operational disruptions. The restructuring was managed with a combination of generous separation packages, careful communication, and the credibility built over a century of operations.

For Ajay Shriram and his brothers, who would lead DCM Shriram, the restructuring was both liberation and burden. They inherited strong industrial assets but also the challenge of creating a new corporate identity. They had the Shriram name and its century of goodwill, but they had to prove they could build something worthy of that legacy. The stage was set for the next phase: building a focused chemical and agri-business conglomerate that could compete in a liberalizing Indian economy about to integrate with global markets.

V. The Shriram Brothers Take Charge (1990s–2000s)

September 1991 marked a double transformation—India opened its economy to the world, and Ajay Shriram took charge as Chairman & Senior Managing Director of the newly independent DCM Shriram. The timing was either perfect or terrible, depending on your perspective. License Raj was ending, meaning DCM Shriram would face global competition for the first time. But it also meant freedom from the suffocating regulations that had constrained growth for decades. Ajay Shriram, armed with a PMD from Harvard Business School, understood that the company needed more than restructuring—it needed reimagination.

The leadership structure that emerged was uniquely Indian: three brothers sharing power but with clear domains. Ajay as Chairman provided strategic vision and external leadership, Vikram as Vice Chairman focused on operations and technology, and Ajit as Joint Managing Director handled finance and new ventures. This wasn't the professional management structure that business schools recommend, but it worked because each brother brought complementary skills and, crucially, they trusted each other completely.

Ajay Shriram's leadership philosophy was shaped by an interesting duality. As Past President of the Confederation of Indian Industry (CII), he was deeply embedded in India's business establishment, understanding the importance of policy influence and industry collaboration. But his Harvard education and international exposure convinced him that DCM Shriram needed to think globally, benchmark against international standards, and build capabilities that could compete anywhere.

The first major strategic move was expanding the Shriram Alkali & Chemicals plant in Bharuch, Gujarat. This wasn't just capacity addition—it was a statement of intent. The Bharuch complex would become one of India's largest integrated chlor-alkali facilities, using membrane cell technology that was both more efficient and environmentally cleaner than older mercury cell processes. The location in Gujarat provided access to salt (the primary raw material), proximity to chemical consuming industries, and state government support for industrial development.

But the real innovation was in backward and forward integration. The chlor-alkali plant didn't just produce caustic soda and chlorine—it became the anchor for an entire chemical complex. Chlorine went into PVC production, caustic soda supplied to paper and textile industries, and hydrogen (a byproduct) was used for power generation. Every waste stream became someone else's raw material. This circular economy approach, before the term became fashionable, created cost advantages that standalone producers couldn't match.

The sugar business transformation was equally ambitious but followed a different logic. The Shriram brothers recognized that Indian sugar wasn't just about crushing cane—it was about managing relationships with millions of small farmers. They acquired the Rupapur sugar mill and established new plants at Hariawan and Loni, but the real innovation was in farmer engagement. DCM Shriram introduced scientific farming practices, provided quality seeds, guaranteed procurement, and most importantly, ensured timely payment when most sugar mills delayed farmer payments by months.

The decision to integrate distilleries with sugar mills was prescient. Every ton of sugar produces molasses, which can be converted to ethanol. With India beginning to mandate ethanol blending in petrol, DCM Shriram was positioning itself for a regulatory shift that would fully materialize only in the 2010s. The three distilleries with 560 KLD capacity weren't just about alcohol production—they were about seeing waste as resource and regulation as opportunity.

Building professional management culture in a family-dominated company required delicate balance. The Shriram brothers brought in external talent for key positions—CFOs from multinationals, technology heads from global chemical companies, marketing professionals from FMCG firms. But they ensured these professionals understood that DCM Shriram wasn't trying to become a faceless corporation. The family values of trust, long-term thinking, and stakeholder welfare weren't obstacles to professionalization—they were its foundation.

The 2000s brought new challenges as India integrated more deeply with the global economy. Chinese chemical imports flooded the market, global sugar prices became more volatile, and environmental regulations tightened. DCM Shriram's response was to double down on integration and innovation. Instead of competing on price alone, they focused on reliability, quality, and solutions. When customers needed caustic soda, DCM Shriram didn't just supply the chemical—they provided application expertise, logistics support, and technical services.

The leadership team also recognized that scale alone wouldn't ensure survival. They needed technological capability, which led to partnerships with global technology leaders. But unlike the failed Toyota partnership of the 1980s, these were focused technology transfers in specific areas—membrane cell technology for chlor-alkali, co-generation technology for power, biotechnology for seeds. The Shriram brothers had learned that successful partnerships required clear boundaries, aligned incentives, and mutual respect.

By the end of the 2000s, DCM Shriram had transformed from a collection of inherited assets into a coherent industrial enterprise. Revenue had grown from hundreds of crores to thousands, but more importantly, the company had built capabilities—in technology, management, and stakeholder relations—that would enable the next phase of growth. The three brothers had proven they could work together, professional managers had been integrated successfully, and the company had navigated India's economic liberalization without losing its essential character. The foundation was set for DCM Shriram to become one of India's leading chemical and agri-business conglomerates.

VI. Modern Business Portfolio & Transformation (2000s–Present)

The modern DCM Shriram represents a masterclass in conglomerate management—not the unfocused diversification of the past, but a carefully orchestrated portfolio where each business strengthens the others. On June 12, 2025, DCM Shriram Ltd. announced a transformative step in its growth journey, approving a definitive agreement to acquire 100% equity share capital of Hindusthan Specialty Chemicals Ltd. (HSCL) for ₹375 crore. This acquisition marks DCM Shriram's bold entry into the advanced materials segment, positioning the company to capitalize on India's burgeoning demand for high-performance materials in sectors like renewables, aerospace, and electric vehicles.

The HSCL acquisition exemplifies the modern DCM Shriram strategy. HSCL, an unlisted subsidiary of Hindusthan Urban Infrastructure Ltd., operates a cutting-edge production facility in Jhagadia, Gujarat, just 3.5 km from DCM Shriram's existing chemicals complex. This proximity unlocks significant operational synergies, enabling seamless integration with DCM Shriram's chlor-alkali platform. HSCL specializes in epoxy and advanced materials, a segment that aligns perfectly with India's push toward innovation in sunrise industries like electronics, defense, and composites.

Today's business structure reflects decades of strategic evolution. The Chemicals & Vinyl division anchors the portfolio with fertilizer facilities in Kota (Rajasthan) producing 379,500 TPA of urea, and the Bharuch (Gujarat) chlor-alkali complex with 1845 TPD combined capacity. These aren't standalone plants but integrated complexes where every molecule finds value—chlorine becomes PVC, hydrogen generates power, and waste heat drives other processes. The 263 MW coal-based captive power plants at Kota and Bharuch aren't just about energy security; they're profit centers that sell surplus power to the grid.

The Sugar Business represents a complete reimagination of what was once simple cane crushing. Four integrated complexes in Uttar Pradesh with 42,400 TCD crushing capacity don't just produce sugar—they're bio-refineries. The 166 MW of power generation from bagasse (sugarcane waste) makes each mill energy-positive. Three distilleries with 560 KLD capacity produce ethanol for fuel blending, industrial alcohol, and even hand sanitizer (a rapid pivot during COVID-19). Every byproduct becomes a product: molasses to ethanol, press mud to bio-compost, excess power to the grid.

The 2013-2014 entry into PVC compounding through Shriram Axiall Pvt. Ltd. demonstrated the ability to form strategic partnerships even after decades of failed collaborations. Unlike the Toyota debacle, this was a focused technology partnership with clear boundaries and aligned incentives. The venture gave DCM Shriram access to global PVC compounding technology while providing Axiall (now Westlake) an entry into the Indian market.

Fenesta Building Systems emerged as an unexpected success story. What began as an attempt to add value to PVC production became one of India's leading UPVC window and door brands. By targeting the premium residential and commercial segments with European technology and Indian manufacturing costs, Fenesta created a new category in Indian construction. The business generates higher margins than commodity chemicals and provides a consumer-facing brand that enhances corporate visibility.

Bioseed represents the most forward-looking element of the portfolio. With hybrid seed development centers in Hyderabad and operations in the Philippines, it's not just selling seeds but developing climate-resilient varieties for a warming world. The R&D intensity—over 15% of Bioseed revenues go to research—reflects a bet that agricultural innovation will be as important as industrial capacity in the coming decades.

The integration across these businesses creates competitive advantages that financial analysts often miss. Sugar mills provide assured feedstock for distilleries. Chemical plants supply fertilizers to contracted farmers who grow sugarcane. Power plants balance load across facilities. Bioseed develops varieties optimized for DCM Shriram's catchment areas. Fenesta uses PVC from the chemical division. It's not diversification for its own sake but a web of reinforcing activities that create value greater than the sum of parts.

Digital transformation, often an afterthought in traditional manufacturing, has become central to operations. IoT sensors monitor chemical processes in real-time, AI algorithms optimize power generation, blockchain tracks sugar from farm to refinery, and mobile apps connect directly with farmers. The company isn't trying to become a tech company but using technology to amplify industrial capabilities built over decades.

The ESG (Environmental, Social, Governance) focus isn't corporate greenwashing but operational necessity. Chemical manufacturing faces increasing environmental scrutiny, sugar mills must manage water resources carefully, and farmer relations determine raw material security. DCM Shriram's circular economy approach—where every waste stream becomes an input elsewhere—predates ESG terminology but perfectly aligns with modern sustainability demands.

Financial discipline underlies everything. Despite operating in capital-intensive industries with volatile commodity cycles, the company maintains conservative leverage, funds expansion primarily through internal accruals, and focuses on return on capital employed rather than just revenue growth. This discipline, inherited from the founding generation's experience with financial crises, provides resilience during downturns and flexibility during upturns.

The modern DCM Shriram has answered the fundamental question of conglomerate strategy: why should these businesses exist under one roof? The answer isn't financial engineering or management capability but operational synergy, shared infrastructure, and deep market knowledge that enables each business to perform better within the group than it would standalone. It's conglomerate strategy not as portfolio management but as ecosystem orchestration.

VII. Strategy & Business Model Evolution

The evolution of DCM Shriram's strategy reads like a business school case study in how conglomerates can create value in emerging markets—not through financial engineering or aggressive acquisition, but through patient capital allocation, operational excellence, and deep market understanding. The company's approach challenges Western orthodoxy about focused strategies while embracing global best practices in execution.

The fundamental insight driving DCM Shriram's strategy is that in India, complexity can be a competitive advantage if managed correctly. While focused competitors struggle with infrastructure gaps, regulatory changes, and market volatility, DCM Shriram's diversified portfolio provides multiple options for capital deployment, natural hedges against commodity cycles, and the scale to build shared infrastructure that no single business could justify.

The Strategic Business Unit (SBU) structure implemented in the 2000s was crucial. Each SBU—Fertilizers, Chloro-Vinyl, Shriram Farm Solutions, Sugar, and Bioseed—operates with its own P&L responsibility, capital allocation authority, and performance metrics. This isn't mere divisional organization but true strategic autonomy. The fertilizer head doesn't need to understand UPVC windows, and the sugar chief doesn't interfere in chlor-alkali operations. Yet they share critical resources: treasury management, government relations, IT infrastructure, and most importantly, accumulated organizational knowledge about operating in India.

The growth philosophy follows four pillars that sound simple but require sophisticated execution. First, scale: DCM Shriram doesn't enter businesses to be marginal players. Whether it's chlor-alkali or sugar, the company builds to be among the top five nationally. Second, integration: every business must have clear backward or forward linkages. Third, adjacent opportunities: new ventures emerge from existing capabilities, like Fenesta emerging from PVC production. Fourth, innovation: not blue-sky research but practical innovation that solves real customer problems.

Capital allocation follows a disciplined framework that would impress any private equity firm. Every investment must meet hurdle rates adjusted for business risk—15% for stable chemicals, 20% for volatile sugar, 25% for new ventures. But unlike financial investors, DCM Shriram thinks in decades, not quarters. The Bharuch chemical complex took ten years to reach optimal capacity, the sugar modernization program spanned fifteen years, and Bioseed required twenty years of patient investment before becoming profitable.

The circular economy approach predates the term but exemplifies it perfectly. At the Kota complex, natural gas feeds the fertilizer plant, but process heat generates power, CO2 goes to soda ash production, and ammonia supplies to other chemical processes. At sugar mills, nothing is waste: bagasse generates power, molasses produces ethanol, press mud becomes fertilizer, and even wastewater, after treatment, irrigates fields. This isn't environmental virtue signaling but hard economics—every recovered molecule improves margins.

Risk management in commodity businesses requires particular sophistication. DCM Shriram doesn't try to predict sugar prices or caustic soda demand. Instead, it builds structural advantages: long-term contracts with customers, integrated operations that capture margins across the value chain, and financial hedging for extreme scenarios. The company learned from the 1970s crisis that commodity businesses can destroy value rapidly, so every business must be able to survive a two-year downturn without group support.

The innovation framework focuses on practical applications rather than breakthrough research. The R&D budget—over ₹100 crore annually—goes toward process optimization, product customization, and application development. When textile customers needed specialized caustic soda grades, DCM Shriram developed them. When farmers wanted drought-resistant seeds, Bioseed created them. When builders needed tropical-adapted window systems, Fenesta designed them. Innovation serves customer needs, not corporate ego.

Digital transformation accelerated post-2015, but with a distinctly practical approach. Instead of hiring Silicon Valley consultants to reimagine the business, DCM Shriram identified specific pain points and deployed targeted solutions. Predictive maintenance in chemical plants reduced downtime by 30%. Digital farmer engagement platforms increased sugar recovery by ensuring optimal harvesting times. IoT-based quality monitoring eliminated customer complaints about product consistency. Each digital initiative had clear ROI targets and operational owners.

The stakeholder management philosophy reflects Indian business reality. Unlike Western corporations focused primarily on shareholders, DCM Shriram explicitly balances six stakeholder groups: shareholders, employees, customers, suppliers (especially farmers), communities, and regulators. This isn't altruism but pragmatism. A chemical plant needs community support to operate, a sugar mill needs farmer loyalty for cane supply, and every business needs regulatory comfort for expansion.

Partnerships strategy evolved from the failed mega-collaborations of the past (Toyota, Daewoo) to focused technical tie-ups. Modern partnerships are narrow in scope, limited in duration, and clear in value exchange. Technology for chlor-alkali membranes, enzymes for ethanol production, genetics for seed development—each partnership solves a specific capability gap without creating strategic dependence.

The resilience framework, tested through multiple crises, ensures survival during black swan events. Every business maintains minimum cash reserves, multiple raw material sources, and scenario plans for various disruptions. During COVID-19, this framework enabled rapid pivots: chemical plants produced sanitizers, sugar mills operated with skeleton crews, and Fenesta shifted to contactless sales. The company didn't just survive but gained market share from less-prepared competitors.

Competitive positioning varies by business but follows consistent principles. In commodities (caustic soda, fertilizer), compete on reliability and service, not price. In differentiated products (seeds, Fenesta), build brand and innovation advantages. In regulated industries (sugar, ethanol), excel at compliance and government relations. In all businesses, leverage the DCM Shriram reputation for quality and integrity built over 135 years.

The strategic questions facing DCM Shriram today aren't about survival but optimization. Should the company demerge into focused entities as markets mature? How aggressively should it pursue international expansion? What's the optimal balance between commodity and specialty chemicals? How does it participate in India's renewable energy transition? These are good problems—the questions of a successful company planning for the next century, not struggling through the current quarter.

VIII. Financial Performance & Market Position

The financial numbers tell a story of steady execution rather than explosive growth—exactly what you'd expect from a 135-year-old conglomerate managing commodity cycles. DCM Shriram's market capitalization stands at ₹20,779 crore, with revenue of ₹12,463 crore and profit of ₹618 crore. These aren't tech unicorn numbers, but they represent real industrial value creation in sectors where many competitors have failed.

The most recent quarterly performance demonstrates operational momentum. For Q1 FY26, the company reported consolidated revenues of ₹3,455 crore, a 12% year-on-year increase, and PBDIT of ₹326 crore, up 19% from the same period last year. Profit After Tax stood at ₹114 crore, reflecting a 13% rise. The improvement in PBDIT margins despite commodity volatility shows pricing power and operational efficiency gains.

Promoter holding at 66.5% provides stability but also raises questions about float and liquidity. The Shriram family's continued majority stake signals confidence but potentially limits institutional participation. This concentrated ownership has pros and cons—it enables long-term thinking but may contribute to the conglomerate discount.

The valuation metrics reveal market skepticism about conglomerates. The stock trades at 2.95 times book value, which seems reasonable for an industrial company but doesn't reflect any premium for the integrated business model or century-old franchise. The P/E ratio of 33.7 appears elevated but needs context—it includes cyclical businesses at different points in their cycles.

Growth metrics highlight the challenge of scale. The company has delivered sales growth of 9.23% over the past five years and has a return on equity of 9.97% over the last 3 years. These aren't spectacular numbers, but they're consistent with a mature industrial conglomerate prioritizing stability over growth. The question is whether this conservative approach creates or destroys shareholder value in a rapidly growing economy.

Segment performance varies significantly, reflecting the portfolio nature of the business. Sugar contributed 35% of revenue in 9M FY25 versus 26% in FY23, showing the impact of favorable sugar cycles and ethanol blending mandates. But this increased dependence on sugar also increases earnings volatility, as sugar remains one of the most cyclical businesses in the portfolio.

The capital allocation track record deserves scrutiny. The recent ₹375 crore acquisition of Hindusthan Speciality Chemicals represents about 1.8% of market cap—meaningful but not transformative. The company's approach of measured, strategic acquisitions contrasts with the aggressive M&A strategies of newer conglomerates. Whether this conservatism is prudence or missed opportunity depends on your investment philosophy.

Working capital management in commodity businesses requires particular attention. Sugar operations tie up significant capital in inventory and farmer payments, chemical businesses need raw material buffers, and the overall cash conversion cycle can stretch during commodity upcycles. DCM Shriram manages this through careful inventory planning and strong banker relationships, but it remains a structural challenge.

Dividend policy reflects the balance between growth investment and shareholder returns. The company maintains consistent dividend payments, understanding that many shareholders (including promoter families) depend on dividend income. But this also limits capital available for aggressive expansion, potentially explaining the modest growth rates.

Peer comparison is complicated because few companies match DCM Shriram's exact portfolio. In chemicals, it competes with focused players like Aarti Industries or Gujarat Alkalies who often show better margins. In sugar, companies like Balrampur Chini or Dhampur Sugar may demonstrate higher returns during upcycles. But none match the diversification and integration that DCM Shriram offers.

The debt position remains conservative, with the company preferring internal accruals to fund growth. This limits financial leverage but provides resilience during downturns. The 2008 financial crisis and 2020 pandemic validated this approach—DCM Shriram continued operations and investments when leveraged competitors struggled.

International revenue remains minimal, representing a missed opportunity or deliberate strategy depending on perspective. While Indian chemical companies like UPL or PI Industries generate significant export revenues, DCM Shriram focuses on domestic markets. This limits currency risk but also growth potential as Indian markets mature.

Environmental and regulatory costs increasingly impact financial performance. Stricter pollution norms require continuous capex for upgrades, carbon taxes may impact energy-intensive operations, and sugar pricing remains government-influenced. These aren't captured in traditional financial metrics but significantly affect long-term value creation.

The investment case ultimately depends on your view of Indian conglomerates. Bulls see a well-managed portfolio trading at reasonable valuations with multiple growth drivers. Bears see a complex structure with modest returns in commodity businesses. The truth, as often, lies somewhere between—DCM Shriram offers stability and integration benefits but unlikely to deliver venture-style returns.

IX. Playbook: Lessons from 135 Years

The DCM Shriram story offers a masterclass in institutional resilience—not the Silicon Valley version of "move fast and break things," but the deeper resilience that comes from surviving colonial rule, partition, socialism, and liberalization while continuously reinventing yourself. The playbook that emerges isn't about quarterly earnings beats but century-long survival strategies.

The first lesson is that in emerging markets, conglomerate structures aren't inefficient—they're adaptive. When infrastructure is unreliable, you build your own power plants. When supply chains are fragile, you integrate vertically. When capital markets are underdeveloped, you cross-subsidize between businesses. When regulations change arbitrarily, you have multiple options for capital deployment. Western MBA programs teach focus, but Indian reality rewards flexibility.

Managing through regime changes requires a particular skill: being essential without being partisan. DCM navigated British colonial rule by becoming industrial infrastructure, survived independence by aligning with nation-building goals, thrived under socialism by mastering the License Raj, and adapted to liberalization by professionalizing management. The company never bet everything on one political outcome—it positioned itself as necessary regardless of who governed.

The successful restructuring blueprint from 1990 offers lessons for any complex separation. First, create clean boundaries—trying to maintain shared services or overlapping markets creates endless conflicts. Second, be generous in separation—the cost of litigation and bad blood far exceeds any short-term financial gain. Third, move quickly—prolonged uncertainty destroys more value than imperfect division. Fourth, respect history but don't be enslaved by it—the DCM name was divided because holding onto it entirely would have prevented necessary change.

Family business succession remains one of the most difficult challenges, and DCM Shriram's approach offers insights. The three Shriram brothers work because each has clear domain and mutual respect—Ajay's strategic vision, Vikram's operational excellence, and Ajit's financial acumen complement rather than compete. But this also required earlier generations to make hard choices—other family branches had to exit or accept passive roles. Professional management was brought in for execution, but family retained strategic control. It's not a perfect model, but it has survived multiple generations.

Trust and innovation might seem contradictory—one backward-looking, one forward-looking—but DCM Shriram shows they're complementary. Trust with farmers enables sugar operations, trust with customers justifies premium pricing, trust with regulators facilitates approvals, and trust with employees enables transformation. But trust without innovation leads to stagnation. The company continuously innovates within its chosen domains—new seed varieties, chemical applications, window designs—without abandoning core relationships.

The sustainable growth framework isn't about ESG reports but operational reality. Every waste stream becomes a product, every byproduct finds value, every resource gets optimized. This wasn't driven by environmental consciousness initially but by economic necessity—when capital is scarce and regulations tight, you can't afford waste. Today's circular economy buzzwords describe what DCM Shriram has practiced for decades.

Capital allocation in cyclical businesses requires different thinking than growth investing. You invest during downturns when assets are cheap and competition weak. You maintain conservative leverage to survive the inevitable crashes. You focus on through-cycle returns rather than peak profitability. You build structural advantages—integration, scale, relationships—that matter more than temporary cost advantages. Most importantly, you remember that in commodities, the survivors inherit the earth.

Building institutional capabilities while maintaining entrepreneurial spirit seems paradoxical but is essential for long-term success. DCM Shriram built systems and processes that ensure consistency—quality standards, financial controls, governance structures. But it also maintains entrepreneurial energy through autonomous business units, performance-based incentives, and tolerance for calculated risks. It's not the freewheeling entrepreneurship of startups but the disciplined entrepreneurship of institutions.

The approach to technology deserves special mention. DCM Shriram was never a technology leader—it didn't pioneer chemical processes or develop breakthrough seeds. Instead, it became excellent at adapting and implementing proven technologies. When membrane cell technology matured, DCM Shriram adopted it. When biotechnology enabled better seeds, they licensed it. When digital tools improved operations, they deployed them. Technology as tool, not religion.

Stakeholder management in the Indian context requires understanding that businesses exist in society, not apart from it. DCM Shriram's survival through multiple crises came from having deep reservoirs of goodwill—farmers who continued supplying sugarcane during cash crunches, workers who accepted temporary hardships, communities that supported expansion plans, and governments that provided policy support. This social capital, built over decades, matters more than financial capital during crises.

The lesson on partnerships is to learn from failures. The Toyota partnership failed because of misaligned expectations, the Daewoo partnership because of partner weakness. Modern partnerships work because they're narrow, specific, and temporary. Don't seek transformative partnerships—seek targeted capability enhancement. Don't depend on partners—use them to build internal capabilities.

Crisis management becomes institutional muscle memory after 135 years. The company survived partition by quickly rebuilding supply chains. It survived the 1970s financial crisis through asset sales and restructuring. It survived the 1980s hostile takeover through stakeholder mobilization. It survived 1990s liberalization through professionalization. It survived 2020's pandemic through operational flexibility. Each crisis created antibodies for the next.

The ultimate lesson is that longevity requires constant reinvention within stable values. DCM Shriram of 2025 would be unrecognizable to its 1889 founders in terms of products, technologies, and scale. But the core values—trust, quality, stakeholder welfare—remain unchanged. It's this combination of strategic flexibility and value stability that enables century-long survival.

X. Bear vs. Bull Case Analysis

The investment case for DCM Shriram splits thoughtful analysts into two camps, each with compelling arguments grounded in fundamental realities rather than market sentiment.

The Bull Case: Integration, Infrastructure, and India

Bulls see DCM Shriram as a rare integrated play on India's industrial transformation. The chlor-alkali business benefits from the Make in India push as domestic manufacturing expands. Every new paper mill, textile unit, or aluminum smelter increases caustic soda demand. With Chinese imports facing quality concerns and trade tensions creating supply uncertainty, domestic integrated producers like DCM Shriram capture both volume and pricing power.

The sugar-to-ethanol transformation represents a multi-decade opportunity. India's ethanol blending mandate—20% by 2030—creates assured demand for ethanol producers. DCM Shriram's integrated sugar complexes with attached distilleries are perfectly positioned. They're not just sugar mills but bio-refineries generating power, ethanol, and organic fertilizers. When sugar prices fall, ethanol provides cushion. When ethanol policies change, sugar provides stability.

Management quality and governance standards surpass most mid-cap industrials. The Shriram brothers have demonstrated strategic vision, operational excellence, and stakeholder fairness over three decades. Professional managers run day-to-day operations while family provides strategic direction. Related-party transactions are minimal, independent directors are genuinely independent, and disclosure standards exceed regulatory requirements.

The ESG transformation isn't greenwashing but operational advantage. Circular economy practices reduce costs, farmer engagement ensures raw material security, and environmental compliance avoids regulatory surprises. As global customers increasingly demand sustainable supply chains, DCM Shriram's century-old community relationships and environmental practices become competitive advantages.

Infrastructure and chemical sector tailwinds provide multi-year growth visibility. India needs to triple chemical production to meet 2030 demand. Sugar production must modernize to remain globally competitive. Renewable energy mandates create opportunities across the portfolio. DCM Shriram doesn't need to gain market share—it just needs to participate in sector growth.

Valuation remains undemanding despite quality operations. Trading at less than 3x book value for a company with integrated operations, strategic assets, and consistent profitability seems conservative. If the market ever re-rates quality mid-cap industrials or conglomerate discounts narrow, significant upside exists.

The Bear Case: Complexity, Commodities, and Competition

Bears see unnecessary complexity in a world demanding focus. Why should one company produce caustic soda, sugar, seeds, and windows? Each business faces different dynamics, requires different capabilities, and attracts different valuations. The supposed synergies—shared infrastructure, integrated operations—don't justify the complexity costs: management attention dilution, capital allocation challenges, and investor confusion.

Commodity exposure across chemicals and sugar creates permanent earnings volatility. Caustic soda prices depend on global supply-demand beyond company control. Sugar economics swing wildly with monsoons, government policies, and global surpluses. Even with integration and diversification, DCM Shriram can't escape commodity cycles. Investors seeking predictable earnings should look elsewhere.

Growth and returns remain pedestrian despite India's economic boom. Five-year revenue CAGR under 10% during India's fastest growth phase raises questions. ROE below 10% suggests either operational challenges or structural disadvantages. If DCM Shriram can't generate teens returns during good times, what happens during downturns?

Regulatory risks loom large across the portfolio. Sugar remains politically sensitive with government-mandated prices, export restrictions, and stock limits. Fertilizer pricing faces subsidy uncertainties. Chemical manufacturing confronts tightening environmental regulations. Ethanol policies could change with one government notification. Multiple regulatory exposures create binary risks that fundamental analysis can't predict.

Competition intensifies from focused specialists. In chemicals, companies like Aarti Industries or Bodal Chemicals show better growth and margins. In sugar, pure-plays like Balrampur Chini operate more efficiently. In seeds, multinationals like Bayer or Corteva have superior R&D. Fenesta faces organized players like Saint-Gobain and unorganized local manufacturers. Fighting multi-front wars against focused competitors seems unsustainable.

The conglomerate discount appears permanent. Markets consistently value diversified companies below sum-of-parts, and nothing suggests this will change for DCM Shriram. Even if individual businesses perform well, the holding company structure, complexity, and limited float ensure persistent undervaluation. Why suffer this discount when focused alternatives exist?

Family control limits strategic flexibility. The 66.5% promoter holding provides stability but prevents transformative M&A requiring equity dilution. It also reduces float, limiting institutional interest. The three-brother structure works today, but what about next-generation succession? Family businesses face unique transition risks that professional companies avoid.

The Verdict: A Question of Investment Philosophy

The bull-bear debate ultimately reflects different investment philosophies. Bulls see a stable, dividend-paying, asset-rich company trading at reasonable valuations with multiple growth options. Bears see a complex, commodity-exposed, modestly growing conglomerate with structural disadvantages.

Both are right within their frameworks. DCM Shriram won't deliver venture capital returns, but it also won't go bankrupt. It won't become a focused global champion, but it will remain a significant Indian industrial player. The investment decision depends on whether you value stability over growth, integration over focus, and track record over potential.

XI. Future Vision & Strategic Questions

The strategic choices facing DCM Shriram over the next decade will determine whether it remains a respectable industrial conglomerate or transforms into something more ambitious. These aren't academic questions but existential ones that will shape the company's next century.

The chemical sector consolidation opportunity looms large. India's chemical industry remains fragmented with thousands of small players lacking scale, technology, or environmental compliance capabilities. Tighter environmental regulations will force closures and consolidation. DCM Shriram could emerge as a consolidator, acquiring distressed assets at attractive valuations and integrating them into its existing complexes. The Hindusthan Speciality Chemicals acquisition provides a template—adjacent technologies, regional proximity, operational synergies. But this requires moving faster and thinking bigger than historical comfort zones.

The sugar-to-ethanol transition represents both opportunity and threat. If ethanol blending mandates accelerate and pricing remains favorable, sugar mills become energy companies. DCM Shriram's integrated complexes are well-positioned, but success requires continuous investment in distillery capacity and technology. The threat is that pure ethanol players using agricultural waste or other feedstocks might prove more efficient than molasses-based production. The strategic question: double down on integrated sugar-ethanol complexes or separate them to pursue focused strategies?

Green chemistry and sustainability initiatives move from nice-to-have to must-have. Global customers increasingly demand carbon-neutral supply chains, renewable feedstocks, and zero-discharge manufacturing. DCM Shriram's century of operations creates legacy environmental issues but also provides time-tested sustainable practices. The company must decide whether to lead India's green chemistry transition—requiring significant R&D investment—or remain a fast follower adopting proven technologies.

Next-generation leadership transition cannot be deferred indefinitely. The three Shriram brothers have provided stable leadership for three decades, but succession planning requires clarity. Will the next generation continue family leadership? If so, how will roles be divided among multiple potential successors? If professional management takes over, how will family shareholders maintain strategic influence? These aren't just family matters—they affect institutional confidence and long-term strategy.

Portfolio optimization remains an perpetual question. Should Bioseed be scaled aggressively or divested to focus on industrial businesses? Does Fenesta belong in a chemical conglomerate or would it thrive independently? Should the company double down on its strongest businesses—chemicals and sugar—or maintain diversification? Each choice involves trade-offs between growth and stability, focus and flexibility.

International expansion potential deserves serious consideration. Unlike Indian IT or pharmaceutical companies, DCM Shriram remains domestically focused. But Indian chemical companies increasingly compete globally, and agricultural businesses naturally cross borders. Should DCM Shriram acquire international assets, build export capabilities, or remain India-focused? The answer depends on risk appetite and capability assessment.

Technology disruption poses different threats across businesses. In chemicals, continuous process improvements incrementally advantage competitors. In agriculture, precision farming and biotechnology could revolutionize traditional approaches. In building materials, new composites might obsolete current products. DCM Shriram must decide whether to lead, follow, or selectively participate in technological change.

The renewable energy transition creates complex choices. Chemical manufacturing remains energy-intensive, but carbon taxes and renewable mandates increase costs. Should DCM Shriram invest in solar/wind generation, explore green hydrogen, or focus on energy efficiency? The sugar business generates renewable power, but should this become a standalone business? Energy strategy increasingly determines competitive positioning.

Capital allocation frameworks need evolution. The historical approach—steady investment across all businesses, conservative leverage, consistent dividends—served well during volatile times. But with deeper capital markets, sophisticated investors, and competitive pressures, more dynamic allocation might create superior value. Should the company increase leverage for growth, buy back shares, or pursue transformative acquisitions?

Stakeholder capitalism versus shareholder primacy remains unresolved. DCM Shriram's multi-stakeholder approach—balancing employee, farmer, community, and shareholder interests—reflects Indian business tradition and ensures social license. But global investors increasingly demand shareholder value maximization. Can the company satisfy both philosophies, or must it choose?

The Make in India and Atmanirbhar Bharat (self-reliant India) initiatives create policy tailwinds but also expectations. Should DCM Shriram position itself as a national champion in chemicals, accepting the responsibilities and regulations that entails? Or maintain strategic flexibility as a private enterprise? The choice affects everything from government relations to capital allocation.

Digital transformation acceleration requires strategic clarity. Should DCM Shriram build internal digital capabilities, partner with technology companies, or acquire digital-native businesses? The answer varies by business—B2B chemicals need different digital strategies than consumer-facing Fenesta or farmer-engaging sugar operations.

These questions don't have obvious answers, and that's precisely the point. DCM Shriram stands at an inflection point where multiple futures remain possible. The choices made in the next five years will determine whether the company's bicentennial in 2089 celebrates continued relevance or mere survival. Given the track record of navigating previous transitions, betting against DCM Shriram seems unwise. But betting on it requires understanding which future the company chooses to build.

XII. Epilogue & Reflections

Standing at the 135-year mark of DCM Shriram's journey, we see not just a company but a mirror reflecting India's own economic transformation. From colonial enterprise to independence-era institution to modern conglomerate, DCM Shriram has been both witness and participant in creating the India we know today.

The textile mill that opened in 1889 Delhi embodied colonial India's industrial awakening—Indian capital, British technology, and hybrid management creating something neither purely foreign nor entirely indigenous. That DNA of synthesis, of taking global knowledge and making it work in Indian conditions, remains embedded in today's DCM Shriram. The chlor-alkali plants use international technology but operate with Indian ingenuity. The sugar mills follow global best practices but maintain distinctly Indian farmer relationships.

The institution-building philosophy of Sir Shri Ram deserves special reflection. While contemporaries focused on accumulating wealth, he built colleges, research institutes, and industry associations. This wasn't altruism but enlightened self-interest—understanding that businesses thrive only in thriving societies. Today's DCM Shriram continues this tradition, not through charity but through creating sustainable livelihoods for farmers, employment in tier-2 cities, and industrial infrastructure for national development.

What modern founders can learn from 135 years of adaptation isn't about specific strategies but meta-principles. First, longevity requires constant reinvention within stable values. The products, technologies, and structures continuously evolve, but core values—trust, quality, stakeholder welfare—remain unchanged. Second, in volatile environments, resilience matters more than efficiency. DCM Shriram's conservative leverage, diversified portfolio, and deep relationships seem suboptimal in spreadsheets but prove invaluable during crises.

The conglomerate structure itself offers lessons for emerging market entrepreneurs. In developed markets with robust infrastructure, deep capital markets, and stable regulations, focus makes sense. But in markets where everything from power supply to policy can change overnight, diversification provides options. DCM Shriram's ability to shift capital between chemicals, sugar, and seeds based on opportunities and threats has enabled survival when focused competitors failed.

The family business evolution provides a template for one of capitalism's hardest transitions. Most family businesses fail by third generation—founder builds, children consolidate, grandchildren dissipate. DCM Shriram's fourth and fifth generations remain engaged because the family created structures—professional management, independent boards, clear succession rules—that preserve institutional strength while maintaining family values. It's not perfect, but it has endured.

The relationship between business and nation-building deserves consideration as India aspires to developed status. DCM Shriram's story shows that private enterprise can serve national goals without sacrificing commercial viability. Building fertilizer capacity serves farmers and generates profits. Creating rural employment supports social stability and ensures raw material supply. Environmental investments meet regulations and reduce costs. Alignment, not sacrifice, drives sustainable business.

Looking forward, DCM Shriram faces the challenge confronting all century-old institutions: remaining relevant in accelerating change. The next 50 years will see more transformation than the previous 135—artificial intelligence, biotechnology, climate change, demographic shifts. Can a company rooted in 19th-century manufacturing thrive in 21st-century disruption? The answer depends on whether DCM Shriram can maintain its historical adaptability while increasing its pace of change.

The investment implications extend beyond DCM Shriram to Indian industry broadly. As India's economy matures, will conglomerates disaggregate into focused entities, following the Western pattern? Or will Indian conditions—infrastructure gaps, regulatory complexity, relationship-based business—continue favoring diversified structures? DCM Shriram's evolution will provide clues to this larger question.

The sustainability transformation represents both culmination and new beginning. DCM Shriram's circular economy practices, developed from economic necessity, now position it for a carbon-constrained future. But moving from incremental efficiency to transformative sustainability requires different thinking. Can a chemicals and sugar company become genuinely sustainable, or will these industries face existential challenges? The answer will determine not just DCM Shriram's future but industrial capitalism's viability.

For investors, DCM Shriram embodies a fundamental choice about what we value. Is it better to own a stable, dividend-paying, asset-rich company with modest growth? Or chase high-growth stories with existential risks? In a world of zero interest rates and speculative excess, DCM Shriram seems anachronistic. But in a world of inflation, deglobalization, and uncertainty, industrial assets with pricing power and essential products regain relevance.

The human dimension ultimately matters most. Behind financial statements and strategic analyses are 20,000 employees, 100,000 farmers, and millions of customers whose lives intertwine with DCM Shriram. The security guard at the Kota plant, the farmer delivering sugarcane in Hariawan, the family installing Fenesta windows—these stakeholders, not shareholders alone, determine institutional longevity.

As we conclude this 135-year journey, from Lala Chunnamal's textile mill to today's chemical conglomerate, the overwhelming impression is continuity within change. Technologies transformed, products evolved, structures restructured, but something essential persisted—call it culture, values, or institutional memory. This intangible asset, built over centuries and irreplaceable by capital, may be DCM Shriram's truest competitive advantage.

The story continues, of course. Someday, someone will write about DCM Shriram's second century, examining choices being made today with hindsight's clarity. Will they describe bold transformation or steady evolution? Global expansion or domestic focus? Continued conglomerate structure or focused disaggregation? The answers remain unwritten, awaiting decisions by current leaders and future circumstances.

What remains certain is that DCM Shriram will continue adapting, as it has through colonialism, independence, socialism, and liberalization. The company that began when Queen Victoria ruled India and the Qing Dynasty governed China has survived into the age of artificial intelligence and space commercialization. That alone deserves respect, study, and perhaps, for patient investors, participation in the journey ahead.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube