Valor Estate Limited: Mumbai's Brownfield Developer

I. Introduction & Episode Roadmap

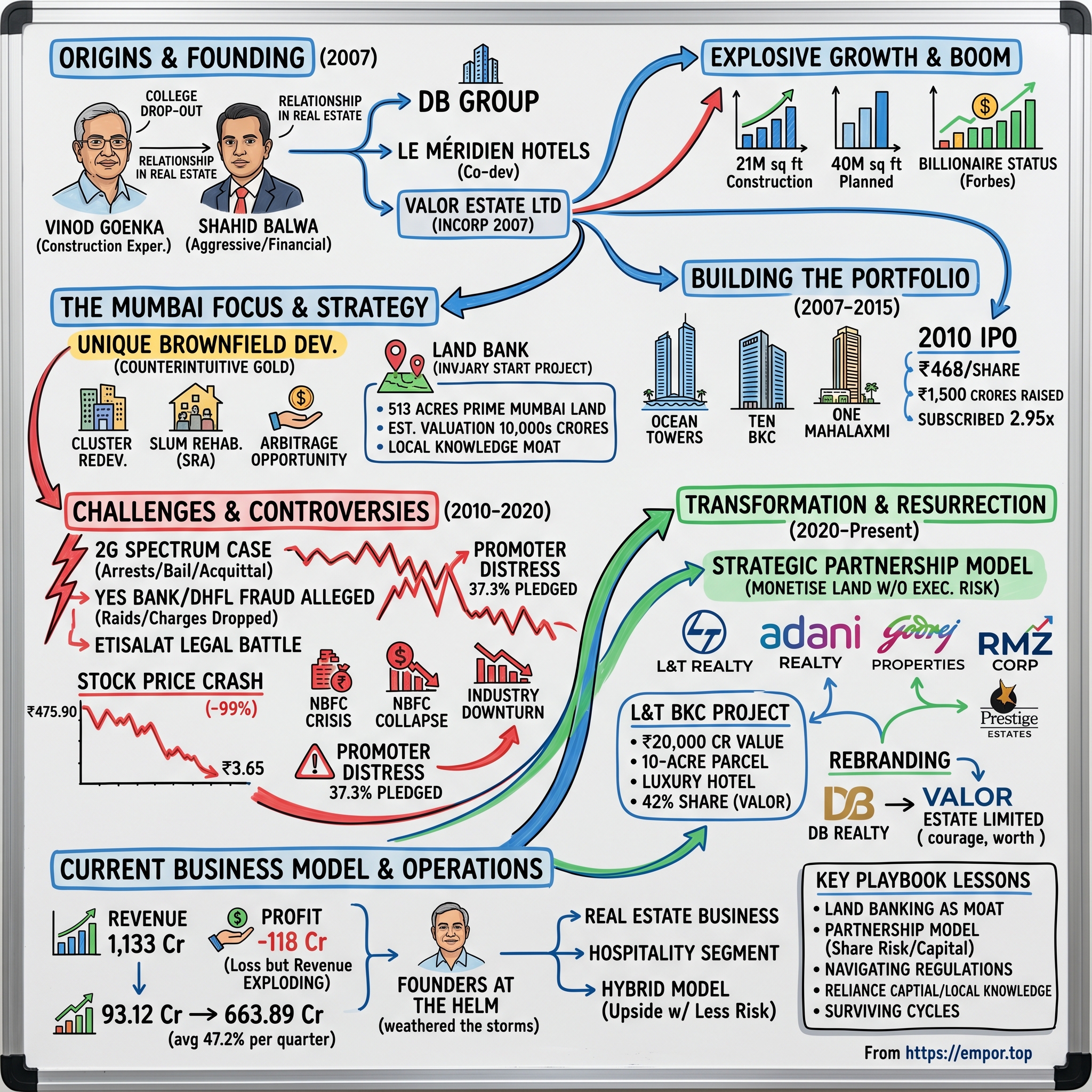

Picture this: It's March 2024, and a Mumbai real estate company with a tumultuous past quietly changes its name from DB Realty to Valor Estate Limited. The rebranding isn't just cosmetic—it's a declaration that this company, which once touched ₹475 per share before crashing to ₹3.65, believes its best days lie ahead. With a market cap hovering around ₹9,892 crore and 513 acres of prime Mumbai land in its portfolio, Valor Estate represents one of the most fascinating transformation stories in Indian real estate.

The question that drives this entire narrative is deceptively simple: How did a company founded in 2007, right before the global financial crisis, navigate through controversies, market crashes, and regulatory nightmares to emerge as a major player in Mumbai's most expensive real estate market? The answer involves a unique brownfield development strategy, controversial figures, high-stakes partnerships, and a bet that Mumbai's slums and old mill lands represent the city's greatest untapped opportunity.

This is a story about relationships—not just the kind you build with customers, but the deep, sometimes murky connections that make Indian real estate tick. It's about Vinod Goenka, who started working in his father's business at 19 and built a billion-dollar empire by age 51. It's about Shahid Balwa, his partner whose name would later appear in headlines for all the wrong reasons. And it's about how a company can shed its skin, partner with giants like L&T and Adani, and attempt to rewrite its narrative in real-time.

The themes we'll explore cut to the heart of Indian capitalism: the value of land banking in a country where real estate is religion, the art of navigating byzantine regulations, the delicate dance between developers and politicians, and how partnerships can transform risk into opportunity. We'll examine how Valor Estate's exclusive focus on Mumbai—specifically brownfield sites and slum rehabilitation—became both its greatest strength and its Achilles' heel.

What makes this company particularly intriguing for investors is its contradictions. Here's a firm sitting on some of Mumbai's most valuable land parcels, including prime Bandra-Kurla Complex (BKC) properties, yet it posted losses of ₹118 crore. Promoters have pledged 37.3% of their holdings, suggesting financial stress, yet major developers are lining up to partner with them on projects worth tens of thousands of crores. The stock trades at a fraction of its historical highs, but the land bank alone might justify a much higher valuation—if they can execute.

This episode roadmap will take us from the company's origins in 2007 through its current transformation phase. We'll dissect the brownfield strategy that sets Valor apart from typical developers who chase greenfield sites on city outskirts. We'll explore the portfolio they built, the controversies that nearly destroyed them, and the partnership model they've embraced as their path to redemption. Along the way, we'll extract lessons about surviving in one of the world's most complex real estate markets and examine whether Valor Estate represents a deep value opportunity or a value trap.

The Mumbai real estate market itself becomes a character in this story—a city where a square foot can cost more than most Indians earn in a year, where slums sit adjacent to billionaire towers, and where the ability to navigate local politics and regulations matters more than architectural excellence. In this context, Valor Estate's strategy of urban regeneration isn't just business; it's an attempt to reshape India's commercial capital, one brownfield site at a time.

II. Origins & Founding Story (2007)

The year is 1978. A 19-year-old Vinod Goenka walks into his father's modest business office in Mumbai, ready to learn the ropes of commerce. Born on July 2, 1959, Goenka wasn't destined for the Ivy League education or foreign MBAs that would later become de rigueur for Indian business scions. Instead, he chose the old-fashioned route: learning by doing, deal by deal, relationship by relationship. This early immersion in Mumbai's business ecosystem would prove invaluable three decades later when he'd navigate the city's labyrinthine real estate market.

By the early 1980s, Goenka had caught the real estate bug. Mumbai was transforming—mills were closing, creating vast swaths of underutilized land in the heart of the city. The Bombay of textile mills was dying; the Mumbai of glass towers was being born. Goenka saw opportunity where others saw decay. He founded Conwood Constructions, initially focusing on small residential projects. But small wasn't in Goenka's vocabulary for long. Each project taught him something new: how to manage contractors, how to navigate municipal approvals, how to read the subtle signals of Mumbai's property market. The Conwood years taught Goenka a fundamental truth about Mumbai real estate: it wasn't just about construction—it was about creating communities. Through innovative projects like Gokuldham and Yashodham in Goregaon, he introduced a new paradigm of neighborhood development, where community, convenience, and quality converged to create holistic living spaces. These weren't just buildings; they were self-contained ecosystems where residents could find schools, healthcare, and places of worship without venturing far. This philosophy—building neighborhoods, not just structures—would later become central to DB Realty's approach.

What's fascinating about Goenka's early career is how diverse his business interests were. In the late 90s, he joined forces with his father, K.M. Goenka, in Conwood Group, which later rebranded as the Dynamix Group. He contributed to Conwood Furnitures Co. Pvt. Ltd., Conwood Interior Decorators Pvt. Ltd., and later Crystal Granite & Marbles Pvt. Ltd., an Export Oriented Unit in Bangalore that specialized in cutting and polishing slabs for international markets. This exposure to different facets of the construction value chain—from interiors to materials—gave him an integrated view of real estate development that most pure-play developers lacked.

Then came 2006, a year that would change everything. Goenka had been watching Shahid Balwa, another Mumbai-based realtor who shared his appetite for ambitious projects. The two men recognized something in each other—complementary skills, shared vision, and most importantly, the ability to navigate Mumbai's complex web of permissions, politics, and partnerships. By 2006, he partnered with Shahid Balwa in a 50:50 collaboration to develop Le Méridien Mumbai (now Hilton International Airport Hotel). This partnership resulted in the creation of the DB group.

The hotel project was more than just their first major collaboration—it was a statement of intent. Here were two developers saying they could play in the hospitality space, manage international brands, and deliver world-class infrastructure. The success of Le Méridien validated their partnership model and gave them the confidence to think bigger. Much bigger. On January 8, 2007, Valor Estate Ltd (then DB Realty Limited) was officially incorporated, with the company being registered at the Registrar of Companies, Mumbai. The timing was audacious—global markets were frothy, Indian real estate was booming, and Mumbai property prices seemed to have no ceiling. The company was founded by Jayvardhan Vinod Goenka and Shahid Balwa, though the younger Goenka's role would evolve over time.

What made the DB partnership unique wasn't just the 50:50 split between the Goenka and Balwa families—it was the complementary nature of their skills and networks. Both founders were college drop-outs and came from families that, directly or indirectly, dealt in real estate. Goenka brought decades of construction experience, relationships with contractors, and deep knowledge of Mumbai's western suburbs. Balwa, younger and more aggressive, understood the new economy, had connections in emerging sectors, and possessed an appetite for complex financial engineering that would later prove both beneficial and problematic.

The company hit the ground running with an ambitious vision. In a few years, the company reported 21 million sq ft under construction and 40 million sq ft in planned projects. This wasn't gradual growth—it was an explosion. The founders weren't interested in being another mid-sized Mumbai developer. They wanted to be titans.

Interestingly, In 2010, Balwa was the youngest Indian to feature on the Forbes List and is amongst the 10 youngest billionaires in the world. He was ranked by Forbes as India's 50th richest man in 2010. For Goenka, his net worth was estimated at US$1.18 billion the same year. These weren't paper fortunes built on startup valuations—this was wealth created from bricks, mortar, and Mumbai land.

The founding philosophy was clear from day one: focus exclusively on Mumbai, specifically on brownfield sites—old mills, dilapidated buildings, slums—that could be transformed into modern developments. While other developers were chasing greenfield projects in Pune, Nashik, or Gurgaon, DB Realty doubled down on the belief that Mumbai's future lay not in expansion but in regeneration. This contrarian bet would define everything that followed.

III. The Mumbai Focus & Brownfield Strategy

Stand at the corner of Senapati Bapat Marg and Tulsi Pipe Road in Lower Parel, and you're witnessing Mumbai's greatest transformation. Where textile mills once employed hundreds of thousands, glass towers now house multinational corporations. This metamorphosis—from Manchester of the East to Manhattan of India—is precisely the opportunity that DB Realty was founded to capture. But while others saw opportunity in Mumbai's periphery, DB saw gold in its decaying core.

DB Realty is a full service development company focusing on large scale, urban regeneration projects in the Mumbai Metropolitan Region. Our exclusive focus on brownfield development and on this region helps us understand the nuances of market trends and timing. Our relationships and technical knowledge give us an edge in developing iconic properties in challenging land and regulatory regimes. This wasn't marketing speak—it was a fundamental strategic choice that would shape every decision the company made.

The brownfield strategy is worth unpacking because it's so counterintuitive. Most developers prefer greenfield sites—virgin land on city outskirts where you can build from scratch, avoid messy tenant issues, and scale quickly. Brownfield development is the opposite: you're dealing with existing structures, multiple stakeholders, complex legal titles, environmental remediation, and often, political sensitivities. So why choose the hard path?

The answer lies in Mumbai's unique geography and economics. Bounded by the Arabian Sea on three sides, Mumbai can only grow northward, making land in the island city exponentially valuable. A brownfield site in Worli or Lower Parel, even with all its complications, is worth multiples of pristine land in Thane or Navi Mumbai. DB Realty understood this arbitrage opportunity better than most. The company has 513 acres of land and focuses on residential and commercial developments. To put that in perspective, in Mumbai's context where land is measured in square feet, not acres, this represents approximately 22.3 million square feet of developable area. At current Mumbai prices, even conservatively valued, this land bank could be worth tens of thousands of crores.

But the genius wasn't just in accumulating land—it was in the type of land DB Realty targeted. The strategy of cluster redevelopment and slum rehabilitation represented a unique approach to value creation. Instead of competing for clean, titled land that everyone wanted, DB went after the messy stuff: slums under the Slum Rehabilitation Authority (SRA) scheme, old cessed buildings falling apart, mill lands with unclear titles, and clusters of old societies ready for redevelopment.

Consider the economics of slum rehabilitation in Mumbai. Under the SRA scheme, a developer who rehabilitates slum dwellers gets compensatory FSI (Floor Space Index) to build commercial projects on the same land. The math is compelling: provide free housing to slum dwellers in vertical towers, freeing up valuable horizontal land for premium development. The slum dwellers get pucca houses with running water and proper sanitation; the developer gets to build luxury towers on some of the most valuable real estate in the world. It's capitalism with a social conscience—or at least that's how it's marketed.

DB Realty took this model and scaled it. They didn't just do one-off SRA projects; they identified entire clusters where multiple projects could be combined for greater efficiency. This clustering approach had multiple advantages: better negotiating power with authorities, economies of scale in construction, and the ability to create entire neighborhoods rather than standalone buildings.

The technical knowledge required for brownfield development is vastly different from greenfield projects. You need to understand environmental regulations for remediation of industrial land. You need lawyers who can untangle decades-old title disputes. You need liaisons who can navigate the byzantine world of Mumbai's municipal permissions. You need the patience to wait years, sometimes decades, for projects to clear regulatory hurdles. DB Realty built all these capabilities in-house, creating what they described as their "edge in developing iconic properties in challenging land and regulatory regimes."

The exclusive Mumbai focus was another strategic masterstroke. While competitors like DLF built across India, DB Realty bet everything on one city. This concentration had risks—any downturn in Mumbai real estate would hit them hard—but it also created deep local knowledge. They understood which areas would gentrify, where the new metro lines would create value, which old mill lands would get rezoned. They knew every municipal councilor, every SRA official, every important bureaucrat in Mantralaya. In Mumbai real estate, these relationships are currency.

This focused approach also meant they could respond quickly to opportunities. When a distressed mill owner needed to sell quickly, DB Realty could move fast because they already understood the land, its challenges, and its potential. When a cluster of societies wanted to redevelop, DB Realty already had relationships with key decision-makers. Speed and local knowledge became competitive advantages.

The portfolio they built reflected this strategy. Our expanding portfolio consists of over 100 million sq. ft of prime property - carefully crafted by 15,000 experts and managed by over 500 internationally and nationally acclaimed executives- across 35 exclusive projects that have served close to 20,000 satisfied customers till date. These weren't random projects scattered across India—each was carefully chosen for its location in Mumbai's transformation story.

IV. Building the Portfolio (2007–2015)

The period from 2007 to 2015 was DB Realty's golden age—a time when ambition met opportunity, when Mumbai's skyline was being rewritten, and when two college dropouts from Mumbai were on their way to becoming billionaires. The global financial crisis that devastated real estate markets worldwide somehow spared India initially, and DB Realty rode this wave with remarkable timing.

DB Realty emerged as a full service development company focusing on large scale, urban regeneration projects in the Mumbai Metropolitan Region. Its residential projects became landmarks that would define neighborhoods for generations. The portfolio was eclectic yet focused: Ocean Towers reaching toward the Arabian Sea, One Mahalaxmi bringing luxury to the racecourse district, Rustomjee Crown adding density to suburban Mumbai, Ten BKC establishing a presence in the city's new financial district, DB SkyPark, DB Ozone, DB Woods, and Orchid Suburbia spreading across the western suburbs. Each project told a story about Mumbai's evolution. Orchid Suburbia in Kandivali represented the suburbanization of the middle class. Ten BKC symbolized Mumbai's ambition to create a new financial district to rival Nariman Point. One Mahalaxmi brought luxury to old money neighborhoods. The diversity wasn't accidental—it was a portfolio approach to risk management, ensuring that a downturn in one segment or location wouldn't sink the entire company.

The 2010 IPO marked DB Realty's coming of age. DB Realty IPO bidding started from January 29, 2010 and ended on February 2, 2010. The shares got listed on BSE, NSE on February 24, 2010. DB Realty IPO price band is set at ₹468 per share. The timing was audacious—global markets were still recovering from the 2008 crisis, but Indian real estate was experiencing a V-shaped recovery.

The issue was a main-board IPO of 32051282 equity shares of the face value of ₹10 aggregating up to ₹1,500.00 Crores. For a company founded just three years earlier, raising ₹1,500 crores from public markets was a remarkable achievement. DB Realty IPO subscribed 2.95 times. The public issue subscribed 0.37 times in the retail category, 4.47 times in QIB, and 4.25 times in the NII category by February 2, 2010 (Day 3).

The retail subscription of just 0.37 times was telling—ordinary investors were skeptical. But institutional investors, who presumably understood the land bank value better, oversubscribed their portion 4.47 times. This divergence between retail and institutional interest would become a recurring theme in DB Realty's public market journey.

Post-IPO, DB Realty had the war chest to accelerate its land banking strategy. The company went on an acquisition spree, targeting distressed assets from other developers who couldn't survive the 2008-2009 slowdown. Mill lands in Lower Parel, old textile compounds in Worli, slum pockets in Dahisar—if it was brownfield and in Mumbai, DB Realty was interested.

By 2010, Vinod Goenka's net worth was estimated at US$1.18 billion. Shahid Balwa, the younger partner, became one of the youngest Indians to feature on the Forbes List and was amongst the 10 youngest billionaires in the world, ranked as India's 50th richest man in 2010. These weren't just paper fortunes—they represented real assets, real land, in one of the world's most expensive cities.

The portfolio expansion wasn't just about quantity; it was about strategic positioning. DB Realty understood that Mumbai's growth would follow predictable patterns: wherever the metro went, property values would spike. Where old industries died, new commercial districts would emerge. Where slums could be rehabilitated, luxury towers would rise. By positioning themselves ahead of these trends, they could capture enormous value appreciation.

The company also diversified beyond pure residential development. DB Realty Ltd. founded in 2007 has been redefining the Mumbai skyline by transforming spaces into landmarks. Emerging as one of India's preferred real estate developers, at DB Realty they focus on designing and creating aesthetically pleasing and functionally brilliant residential and commercial spaces, keeping in mind the evolving needs and lifestyles of our customers and stakeholders.

This period also saw DB Realty perfecting its execution model. With over 500 internationally and nationally acclaimed executives, the company built capabilities that few Indian developers possessed. They could handle everything from slum negotiations to environmental clearances, from architectural design to project financing. This vertical integration gave them control over timelines and quality—crucial in a market where delays and cost overruns were endemic.

V. Challenges & Controversies (2010–2020)

If 2007-2015 was DB Realty's golden age, then 2010-2020 was its trial by fire. The company that had seemed unstoppable suddenly found itself in the eye of multiple storms—regulatory, legal, and financial. The story of this decade is how a high-flying real estate company nearly crashed and burned, taking its stock price from ₹475.90 to ₹3.65, a decline of over 99%.

The first signs of trouble emerged in 2011, not from the real estate business but from an unexpected quarter—telecommunications. Goenka was arrested on 20 April 2011 for his alleged involvement in the 2G spectrum case. During his imprisonment, he temporarily stepped down from his roles in the companies he was associated with. After spending over seven months in custody, Goenka was granted bail by the Supreme Court of India on 23 November 2011.

The 2G scandal connection wasn't direct—DB Realty had ventured into telecom through Swan Telecom, which sold a stake to UAE's Etisalat. The allegation was that DB Group had facilitated questionable transactions, including transferring funds to companies connected to political figures. The arrests of both Goenka and Balwa sent shockwaves through the market. Here were two of India's youngest billionaires, behind bars, their empire suddenly rudderless.

In 2013, UAE telecommunications operator Etisalat initiated legal proceedings against its Indian partners, Goenka and Shahid Balwa, after the Supreme Court canceled the latter's 2G licenses. The telecom misadventure, which was supposed to diversify DB Realty's revenue streams, had become an existential threat.

But there was redemption, eventually. On 21 December 2017, Goenka and all 18 other accused persons in the 2G spectrum case were acquitted of all charges levied against them. Six years of legal battles, reputational damage, and business disruption—all for an acquittal. But the damage was done. The DB Realty brand had been tarnished, institutional investors had fled, and the stock price had cratered.

The controversies didn't end there. Goenka was linked to a Yes Bank-Dewan Housing Finance Corporation fraud case over a ₹350 crore loan his firm, Neelkamal Realtors, received from Yes Bank between 2013 and 2016, which the Central Bureau of Investigation alleged was diverted as part of a ₹4,733 crore siphoning scheme involving DHFL. Despite raids in 2022 and a chargesheet in 2024, a CBI court in March 2025 dropped the charges against Goenka, finding that the loan had been settled with Piramal Capital and Housing Finance Limited, which had acquired DHFL, before the chargesheet was filed and that there was no evidence of fraud, thereby clearing him of liability. This repayment was a key factor in the court's decision to dismiss the allegations against him.

Beyond the legal troubles, DB Realty faced severe industry headwinds. The Indian real estate sector entered a prolonged downturn post-2013. Demonetization in 2016 sucked liquidity out of the market. The Real Estate Regulatory Authority (RERA) implementation in 2017 increased compliance costs and delayed projects. The IL&FS crisis in 2018 froze lending to real estate developers. Then came the NBFC crisis, with major lenders to real estate like DHFL and Yes Bank collapsing.

The company's financials reflected these challenges. Company has low interest coverage ratio. Company has a low return on equity of 4.65% over last 3 years. These metrics painted a picture of a company struggling to service its debt, generate returns for shareholders, and maintain operational efficiency.

The stock price told the most brutal story. Stock price volatility: DBREALTY reached its all-time high on Mar 10, 2010 with the price of 475.90 INR, and its all-time low was 3.65 INR and was reached on Apr 22, 2020. From hero to zero in a decade—a 99.2% decline that wiped out nearly all shareholder value. Investors who bought at the IPO price of ₹468 saw their investment shrink to less than 1% of its original value.

The promoter distress was evident in their actions. Promoters have pledged or encumbered 37.3% of their holding, suggesting they were using their shares as collateral for loans, a sign of financial stress. When promoters pledge shares, it creates a vicious cycle—if share prices fall, lenders demand more collateral or sell the pledged shares, causing prices to fall further.

Mumbai's real estate market itself was undergoing a painful adjustment. Prices had gotten ahead of affordability. Inventory was piling up—thousands of unsold flats across the city. Buyers were waiting for prices to correct. Developers were stuck with unsold inventory, mounting interest costs, and no cash flow. It was a perfect storm.

For DB Realty, with its focus on brownfield development and slum rehabilitation, the challenges were even more acute. These projects had long gestation periods—sometimes 7-10 years from acquisition to completion. In a rising market, the wait was worth it. In a falling market, it was death by a thousand cuts. Interest costs accumulated, approvals got delayed, and sales dried up.

The company's reputation took hit after hit. Every few months, there seemed to be a new controversy, a new investigation, a new crisis. Banks became reluctant to lend. Customers became wary of booking flats in DB Realty projects, fearing they might never get delivered. Partners started reconsidering joint ventures. It was a downward spiral that seemed impossible to arrest.

By early 2020, just before COVID hit, DB Realty looked like a company on life support. The stock was trading at ₹3.65, the company was posting losses, multiple projects were stuck, and the promoters were fighting legal battles on multiple fronts. The question wasn't whether DB Realty would recover—it was whether it would survive.

VI. The Partnership Strategy & Transformation (2020–Present)

March 2020. COVID-19 lockdowns paralyzed Mumbai. Construction sites shut down. Sales offices closed. For a company already on the brink, this should have been the final blow. Instead, it became the catalyst for one of the most dramatic transformations in Indian real estate. DB Realty's resurrection strategy was audacious in its simplicity: if you can't develop alone, partner with those who can.

The pivot to joint ventures and partnerships wasn't born from strength but from necessity. DB Realty had the land—513 acres of prime Mumbai real estate. What it lacked was capital, credibility, and execution capability. The solution? Find partners who had all three. Over the past few years, Valor Estate has pursued strategic alliances to monetise key land parcels, partnering with realty developers like Prestige Estates Projects, Adani Realty, Godrej Properties, and RMZ Corp.

The partnership model was elegant. DB Realty would contribute land, partners would bring capital and development expertise, and both would share the profits. For partners, it was access to Mumbai land that would otherwise be impossible to acquire. For DB Realty, it was a lifeline—a way to monetize land without the execution risk. The crown jewel of this partnership strategy emerged in July 2024. L&T Realty has signed a binding agreement with Valor Estate to co-develop a major project worth over Rs 20,000 crore on a 10-acre land parcel in Mumbai's Bandra-Kurla Complex (BKC). The project will feature a mix of premium housing, commercial spaces, and five-star luxury hotel which boasts 1,000 rooms. This mixed-use development has a total development potential of over 7.5 million square feet. L&T Realty and Valor Estate will share the developed area in a 58:42 ratio, respectively, with Valor Estate fully owning the luxury hotel.

Think about the mathematics here. A ₹20,000 crore project where Valor Estate contributes land and gets 42% of the developed area plus a luxury hotel. Even at that split, Valor's share could be worth ₹8,000-10,000 crores. For a company with a market cap of under ₹10,000 crores, this single project could theoretically justify the entire valuation.

The BKC project wasn't just about the numbers—it was about credibility. L&T Realty, backed by the $23 billion Larsen & Toubro conglomerate, was essentially validating Valor Estate's land bank. If L&T was willing to partner on such a massive project, it sent a signal to the market that Valor's assets were real, valuable, and developable. But L&T wasn't the only partner. Prestige (BKC) Realtors is developing a project with a potential gross leasable area of 2.79 million sq ft Grade A office space in Mumbai's Bandra Kurla Complex. This partnership with Prestige Estates, one of India's largest developers, was another validation of Valor's assets. The BKC location is Mumbai's most prestigious business district, where office rents rival Manhattan and London.

The partnership strategy extended beyond the marquee BKC projects. Over the past few years, Valor Estate has pursued strategic alliances to monetise key land parcels, partnering with realty developers like Prestige Estates Projects, Adani Realty, Godrej Properties, and RMZ Corp. Each partnership was carefully structured—Valor brought land, partners brought everything else, and both shared the upside.

This model solved multiple problems simultaneously. First, it addressed the capital constraint—Valor didn't need to raise billions for construction. Second, it solved the execution problem—experienced developers like L&T and Godrej had the project management capabilities Valor lacked. Third, it restored credibility—if blue-chip developers were willing to partner, it signaled that Valor's assets were real and valuable.

The transformation wasn't just operational—it was corporate. In March 2024, the company shed its controversial past by rebranding from DB Realty to Valor Estate Limited. The name change was more than cosmetic. "Valor" suggested courage, value, worth—a company rising from the ashes. It was a signal to the market that this wasn't the same company that had been mired in controversies for a decade.

The financial impact of this partnership strategy has been dramatic. Revenue is up for the last 4 quarters, 93.12 Cr → 663.89 Cr (in ₹), with an average increase of 47.2% per quarter. While the company still posts losses, the trajectory is clear—revenues are exploding as partnership projects begin to monetize.

The stock market has taken notice. From the COVID low of ₹3.65 in April 2020, the stock has recovered dramatically, though it still trades well below its historical highs. The market seems to be pricing in the potential of these partnerships while remaining cautious about execution risks.

What's remarkable about this transformation is how it turned weakness into strength. Unable to develop alone, Valor became the land partner of choice for India's best developers. Unable to raise capital, they structured deals where partners brought the money. Unable to execute complex projects, they partnered with those who could. It's a masterclass in strategic pivoting—when you can't win the game you're playing, change the game.

The partnerships also revealed the true value of Valor's land bank. When L&T values a 10-acre BKC parcel at ₹20,000 crores, it implies a land value of ₹2,000 crores per acre. Extrapolate that to even a fraction of Valor's 513-acre land bank, and you get valuations that dwarf the current market cap. Of course, not all land is in BKC, but even at much lower valuations for suburban land, the numbers are compelling.

VII. Current Business Model & Operations

Today's Valor Estate is a fundamentally different company from the debt-laden, controversy-plagued entity of the 2010s. The business model has evolved from a traditional developer taking development risk to a land-rich partner monetizing assets through joint ventures. It operates in two segments: Real Estate Business and Hospitality Business. The company develops and sells residential, commercial, retail, and other projects, such as mass housing and cluster redevelopment, as well as hospitality projects.

The financial snapshot tells a story of a company in transition. Revenue: 1,133 Cr, Profit: -118 Cr. Yes, the company is still loss-making, but the revenue trajectory is explosive. Revenue is up for the last 4 quarters, 93.12 Cr → 663.89 Cr (in ₹), with an average increase of 47.2% per quarter. This isn't organic growth—it's the partnership projects beginning to contribute.

The management structure remains unchanged at the top. Mr. Vinod Kumar Goenka is the Chairman & Managing Director. Mr. Shahid Usman Balwa is the Vice Chairman and Managing Director. Despite all the controversies, both founders remain at the helm, suggesting they've weathered the storms and are committed to the turnaround.

The operational model has become more sophisticated. Instead of taking on entire projects alone, Valor now operates through multiple structures. In some cases, they contribute land for a revenue share. In others, they maintain equity participation in the development. The L&T BKC project, for instance, sees Valor retaining 42% of the developed area plus full ownership of a luxury hotel. This hybrid model allows them to capture upside while limiting downside risk.

The company's approach to slum rehabilitation has also evolved. The land, part of a 13-acre plot, currently houses around 5,500 families living in slums who will be relocated as part of the project. Valor Estate will handle the relocation and get the necessary approvals, aiming to complete these tasks in 12-18 months. This expertise in managing rehabilitation—a complex process involving negotiations with thousands of families—has become a core competency that partners value.

The hospitality segment represents an interesting diversification. While relatively small compared to real estate, it provides recurring income and adds prestige to the portfolio. The conversion of hospitality assets into operational hotels, often in partnership with international brands, creates long-term value beyond just property development.

What's particularly interesting is how Valor has positioned itself in the value chain. They're no longer trying to be everything—architect, builder, marketer, financier. Instead, they focus on what they do best: navigating Mumbai's complex land and regulatory environment, managing rehabilitation processes, and maintaining relationships with authorities. Partners handle construction, marketing, and financing.

The company's relationships remain its most valuable intangible asset. In Mumbai real estate, relationships with municipal authorities, state government officials, and local stakeholders can make or break projects. Valor's ability to get approvals, manage local sensitivities, and navigate bureaucracy is what makes their land developable. Without these relationships, the land bank would be just expensive dirt.

The current strategy also reflects a deep understanding of market cycles. By partnering rather than developing solo, Valor reduces its exposure to market downturns. If property prices fall, the impact is shared with partners. If construction costs rise, partners bear much of the burden. It's a more resilient model for a cyclical industry.

Looking at the portfolio today, it's a mix of legacy projects being completed, new partnership projects being launched, and future projects being planned. The focus remains firmly on Mumbai, with particular emphasis on locations that will benefit from infrastructure development—areas near new metro lines, the upcoming coastal road, and the trans-harbor link.

The financial metrics, while still showing losses, hint at the potential ahead. The company is essentially in investment mode, with costs front-loaded and revenues back-loaded. As partnership projects complete over the next 3-5 years, the revenue and profit profile should transform dramatically. The question for investors is whether the current market cap adequately reflects this future value creation.

VIII. Playbook: Business & Investing Lessons

The Valor Estate story offers a masterclass in surviving and potentially thriving in one of the world's most complex real estate markets. The lessons extend far beyond real estate, touching on themes of resilience, strategic pivoting, and value creation through partnerships.

Land banking in prime Mumbai locations as a moat stands out as perhaps the most important lesson. While others chased quick profits in peripheral locations, Valor accumulated land in Mumbai's core. This wasn't just about betting on appreciation—it was about creating an irreplaceable asset. You can always raise capital, hire talent, or license technology. You cannot create more land in South Mumbai. The 513-acre land bank, accumulated when the company had access to capital, has become the foundation for its resurrection. The lesson for investors: in businesses with finite resources (land, spectrum, licenses), accumulation during good times creates optionality during bad times.

The partnership model: Sharing risk and capital requirements represents a profound shift in how real estate development can work. Traditional developers try to capture the entire value chain—land, construction, sales. Valor's evolution shows that sometimes the best strategy is to focus on your unique strengths and partner for everything else. By contributing land and getting 40-50% of developed value, Valor captures significant upside without construction risk, working capital requirements, or execution challenges. For other capital-intensive businesses, this model suggests that asset-light variations might exist even in traditionally asset-heavy industries.

Navigating India's complex real estate regulations has become a core competency that's difficult to replicate. Every major Mumbai project requires navigating multiple authorities: BMC for building permissions, SRA for slum rehabilitation, environment ministry for coastal zone clearances, aviation authority for height restrictions, state government for various NOCs. Valor's ability to manage this complexity, built over decades, is what makes their land developable. The lesson: in highly regulated industries, regulatory navigation capability can be as valuable as operational excellence.

Urban regeneration and slum rehabilitation as opportunity reflects a deeper understanding of urban economics. While most developers see slums as obstacles, Valor saw opportunity. The SRA scheme essentially allows developers to create value by solving a social problem—rehousing slum dwellers in vertical structures frees up horizontal land for commercial development. It's capitalism with a social conscience, or at least that's the narrative. The broader lesson: the biggest business opportunities often lie in solving the hardest social problems.

Surviving cycles: From boom to bust to recovery is perhaps the most relevant lesson for current markets. Valor's journey from ₹475 to ₹3.65 to recovery shows that survival is the first priority in cyclical industries. The company survived by not overleveraging during good times, by having patient promoters who didn't sell during distress, and by finding creative solutions (partnerships) when traditional methods (bank financing) weren't available. For investors, it's a reminder that cyclical industries require different analytical frameworks than growth industries.

The importance of relationships in Indian real estate cannot be overstated. Vinod Goenka and Shahid Balwa's relationships, built over decades, are what enabled the partnership strategy. L&T, Prestige, and Godrej partnered with Valor not just for land but for the relationships and local knowledge that make projects possible. In many emerging markets, relationship capital is real capital—it determines what's possible and what's not.

The playbook also reveals mistakes to avoid. Diversifying into unrelated areas (telecom) nearly destroyed the company. Overleveraging during boom times left them vulnerable during downturns. Getting too close to political figures created regulatory risks. These negative lessons are as valuable as the positive ones.

For real estate investors globally, the Valor playbook suggests that land banking in supply-constrained markets, combined with patient capital and creative structuring, can create enormous value. The key is surviving long enough to realize that value. Valor's near-death experience and potential resurrection is a reminder that in real estate, he who survives, thrives.

The partnership model also has implications for how we think about competitive advantage. Traditional strategy suggests you should control your value chain. Valor's evolution suggests that in capital-intensive industries with long cycles, partnership models that share risk and reward might be more resilient. It's not about capturing all the value—it's about capturing enough value with less risk.

Finally, the transformation from DB Realty to Valor Estate demonstrates that corporate rehabilitation is possible, even after severe reputational damage. It requires time, strategic changes, and most importantly, delivering results. The market may be slow to forget, but it eventually rewards performance.

IX. Analysis & Bear vs. Bull Case

The investment case for Valor Estate is perhaps one of the most polarizing in Indian real estate. Bulls see a land bank worth multiples of the current market cap. Bears see a history of controversies and current losses. The truth, as always, lies somewhere in between.

Bull Case:

The arithmetic of the bull case is compelling. Start with the crown jewel: Prime Mumbai land bank of 513 acres. At current Mumbai prices, where land in prime locations trades at ₹500-1000 crores per acre, the theoretical value could be ₹25,000-50,000 crores. Even if we haircut this by 80% for less prime locations, regulatory challenges, and development costs, we get values that dwarf the current market cap of under ₹10,000 crores.

The Strong partnership pipeline with major developers changes everything. L&T, Prestige, Godrej, and Adani aren't charitable organizations—they've done their diligence and see value. The L&T BKC project alone, worth ₹20,000 crores, could contribute ₹8,000-10,000 crores to Valor. Add the Prestige BKC office project, and other partnerships, and the development pipeline could be worth ₹15,000-20,000 crores to Valor.

Mumbai real estate recovery potential provides the macro tailwind. Mumbai property prices have been stagnant for nearly a decade. With infrastructure projects like the coastal road, trans-harbor link, and metro expansion, the city is set for a transformation. Rising incomes, limited supply, and pent-up demand could drive a multi-year upcycle. Valor, with its Mumbai-centric land bank, is perfectly positioned to benefit.

BKC developments could be transformational. BKC is becoming Mumbai's premier business district, with rents rivaling global cities. Valor's significant BKC presence, including the L&T partnership and Prestige office project, positions them in the highest value-creation zone in India. As BKC matures, land values could surprise on the upside.

The partnership model de-risks execution. By partnering with experienced developers, Valor has solved its execution challenges. Partners bring capital, construction expertise, and marketing capabilities. Valor brings land and regulatory navigation. It's a win-win that should accelerate value realization.

Bear Case:

The bears have equally compelling arguments. Start with the current reality: Profit: -118 Cr - Currently loss-making. Despite all the partnerships and potential, the company continues to burn cash. Revenues are growing, but when will profits follow? The market has seen too many promise-heavy, delivery-light stories in Indian real estate.

The capital structure concerns are significant. Promoters have pledged or encumbered 37.3% of their holding. This creates a sword of Damocles—if share prices fall significantly, margin calls could force promoter selling, creating a downward spiral. Debtor days have increased from 67.2 to 81.2 days, suggesting working capital stress.

The corporate governance overhang persists. Promoter holding has decreased over last 3 years: -17.9%. Why are promoters selling if the future is so bright? The history of controversies, while legally resolved, creates a trust deficit. International institutional investors remain wary.

Execution risk on large projects is real. The partnership projects are massive in scale—₹20,000 crores for L&T BKC alone. Delays are common in Indian real estate. Cost overruns are endemic. What if partnerships sour? What if approvals get delayed? The bigger the project, the bigger the potential problems.

Regulatory and market risks loom large. Mumbai real estate is heavily regulated and politically sensitive. SRA rules could change. FSI norms could be modified. Political changes could affect project approvals. A broader economic slowdown could defer the Mumbai recovery indefinitely.

The competition is intensifying. Every major developer wants a piece of Mumbai. International funds are buying land. Local developers are consolidating. Valor's land bank advantage could erode as others accumulate land through distressed sales.

The Balanced View:

The truth is that Valor Estate is a complex bet on multiple variables: Mumbai real estate recovery, successful execution of partnerships, regulatory stability, and management credibility. It's not a simple value play or a growth story—it's a transformation bet.

For value investors, the land bank provides a margin of safety. Even in distress, the land has value. The partnerships validate this value. But value traps exist when assets can't be monetized, and Indian real estate has many examples of valuable land that remains undeveloped for decades.

For growth investors, the revenue trajectory is exciting, but the path to profitability remains unclear. The partnership model could drive explosive growth as projects complete, but the timing and magnitude are uncertain.

For income investors, this isn't the stock—no dividends, no visibility on when they might resume.

The risk-reward seems asymmetric. If Mumbai real estate recovers and partnerships execute successfully, the stock could be a multi-bagger. If challenges persist, the land bank provides downside protection, though perhaps not at current levels.

X. Epilogue & "If We Were CEOs"

As we stand in 2025, looking at Valor Estate's journey from near-death to potential rebirth, the bigger question emerges: what does this tell us about The future of Mumbai real estate and urban development? Mumbai, with its 20 million inhabitants squeezed into 603 square kilometers, represents the extreme edge of urban density. Every square foot matters. Every development decision reshapes thousands of lives. Valor's focus on brownfield development and slum rehabilitation isn't just a business strategy—it's a bet on how megacities must evolve.

Can Valor Estate capitalize on its land bank? This is the trillion-rupee question. Land is only valuable if it can be developed, and development requires more than just ownership papers. It requires capital, which Valor has accessed through partnerships. It requires execution, which partners provide. It requires regulatory approvals, which Valor's relationships facilitate. Most importantly, it requires market demand, which Mumbai's demographics suggest will persist. The pieces are in place, but assembly is everything.

The Partnership model vs. solo development debate extends beyond Valor. Should developers try to capture the entire value chain, or focus on their comparative advantages? Valor's evolution suggests that in capital-intensive, long-cycle businesses, partnerships might be superior. You capture less of the pie, but the pie is more likely to be baked. For an industry littered with half-completed projects and bankrupt developers, this might be the sustainable model.

ESG considerations in slum rehabilitation add another dimension. Valor's projects will relocate thousands of families from horizontal slums to vertical towers. Is this social progress or social engineering? The residents get pucca houses with running water and legal titles. But they also get moved from community structures built over generations to anonymous towers. The environmental impact of densification versus sprawl, the social impact of relocation versus rehabilitation in place—these aren't just CSR talking points but fundamental questions about urban development.

If We Were CEOs:

First, we'd double down on transparency. The market still doesn't fully understand the partnership economics. Detailed project-by-project disclosure of economics, timelines, and milestones would help investors understand value creation. Regular investor calls, site visits, and progress updates would rebuild credibility.

Second, we'd accelerate the partnership strategy. With validation from L&T and Prestige, we'd approach international developers and funds. The land bank is large enough to support multiple partnerships. Why wait for sequential development when parallel development could accelerate value realization?

Third, we'd consider a REIT structure for completed commercial assets. As office and retail projects complete, moving them into a REIT would provide regular income, improve valuations, and separate development risk from income generation.

Fourth, we'd strengthen the balance sheet. The current debt levels and pledged shares create fragility. A rights issue or strategic stake sale, while dilutive, would provide the financial strength to weather any storms and negotiate from a position of strength.

Fifth, we'd invest in institutional capability. The company needs professional management beyond the promoters. Hiring senior executives from successful developers, strengthening project management, and building institutional processes would prepare the company for its next phase.

Final Reflections:

The Valor Estate story is far from over. It could end as a spectacular turnaround—the land bank monetized, partnerships successful, stock price recovering to historic highs. Or it could remain a perpetual value trap—always promising, never delivering, the land bank providing theoretical comfort while operational challenges persist.

What makes this story particularly relevant is its broader implications. India needs to build homes for hundreds of millions as it urbanizes. The traditional model of government-led development has failed. The pure private sector model creates affordability challenges. Valor's hybrid model—private development with social rehabilitation—might be a template, despite its challenges.

For investors, Valor represents a fascinating risk-reward proposition. It's not for the faint-hearted—the volatility will continue, the controversies might resurface, the execution could disappoint. But for those who believe in Mumbai's future, who understand the value of irreplaceable assets, and who have the patience for long-term value realization, it might be one of the most interesting stories in Indian real estate.

The transformation from DB Realty to Valor Estate is more than a name change—it's an attempt to rewrite a corporate story. Whether this new chapter ends in triumph or disappointment will depend on execution, market conditions, and perhaps a bit of luck. But the very attempt—to rise from the ashes, to transform through partnerships, to create value from challenged assets—makes this a story worth watching.

In the end, Valor Estate embodies the contradictions of Indian capitalism: enormous opportunity shadowed by regulatory complexity, spectacular wealth creation alongside social challenges, professional management mixed with promoter control. It's messy, it's complex, and it's very, very real. Just like Mumbai itself.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube