Cummins India: Engineering India's Power Revolution

I. Cold Open & Episode Roadmap

The lights went out again in Gurugram. It was July 2012, and India's millennium city—home to Fortune 500 companies and gleaming tech parks—was experiencing its third power cut of the day. Across the subcontinent, 670 million people had just lost electricity in what would become the largest blackout in human history. In the basement of a Cyber City office tower, a diesel generator roared to life, its distinctive Cummins badge barely visible through the exhaust haze. Within seconds, computers flickered back on, air conditioners resumed their hum, and business continued as if nothing had happened.

This is the paradox of modern India: a nuclear power with a space program that still relies on diesel generators to keep the lights on. And at the center of this paradox sits a company that most Indians have never heard of, despite its products literally powering their economy. Cummins India Limited—a ₹1,06,565 crore market cap giant that generates ₹10,982 crores in revenue and ₹2,141 crores in profit—has spent six decades quietly becoming the circulatory system of Indian infrastructure.

The company serves everyone from construction sites to data centers, from naval vessels to railway engines, from hospitals to hotels. When a metro tunnel is being bored beneath Mumbai, Cummins powers the drilling equipment. When a new IT park rises in Hyderabad, Cummins generators provide backup power. When the Indian Navy patrols the Arabian Sea, Cummins engines drive their vessels. This ubiquity isn't accidental—it's the result of one of the most successful technology transfers in emerging market history.

Our story today isn't just about diesel engines and power generators. It's about how American engineering excellence met Indian industrial ambition at the perfect moment in history. It's about navigating the labyrinth of Indian regulation, from the License Raj to modern emission standards. It's about building an industrial moat so deep that even after sixty years, competitors struggle to cross it. Most importantly, it's about how a joint venture between a Midwestern engine manufacturer and an Indian industrial house became the template for how global companies can build lasting franchises in emerging markets.

What makes this story particularly relevant now is that Cummins India just pulled off something remarkable: implementing the world's most stringent emission standards while posting record revenues. As the world debates the future of fossil fuels and the pace of energy transition, this company offers a masterclass in turning regulatory disruption into competitive advantage. They didn't just survive India's CPCB IV+ emission norms—which reduced particulate matter and nitrogen oxide emissions by 90%—they used them to strengthen their market position.

Over the next several hours, we'll unpack how a company from Columbus, Indiana, population 47,000, came to dominate power generation in a nation of 1.4 billion people. We'll explore the delicate dance of joint ventures in post-independence India, the art of technology localization, and the strategic patience required to build industrial empires. We'll examine how Cummins navigated the transition from Indian partner to American subsidiary while maintaining local trust. And we'll analyze what their success tells us about the future of industrial development in emerging markets.

But to truly understand Cummins India, we need to travel back to 1962, to a newly independent nation desperate for industrial capability, and to two men who saw opportunity where others saw only obstacles.

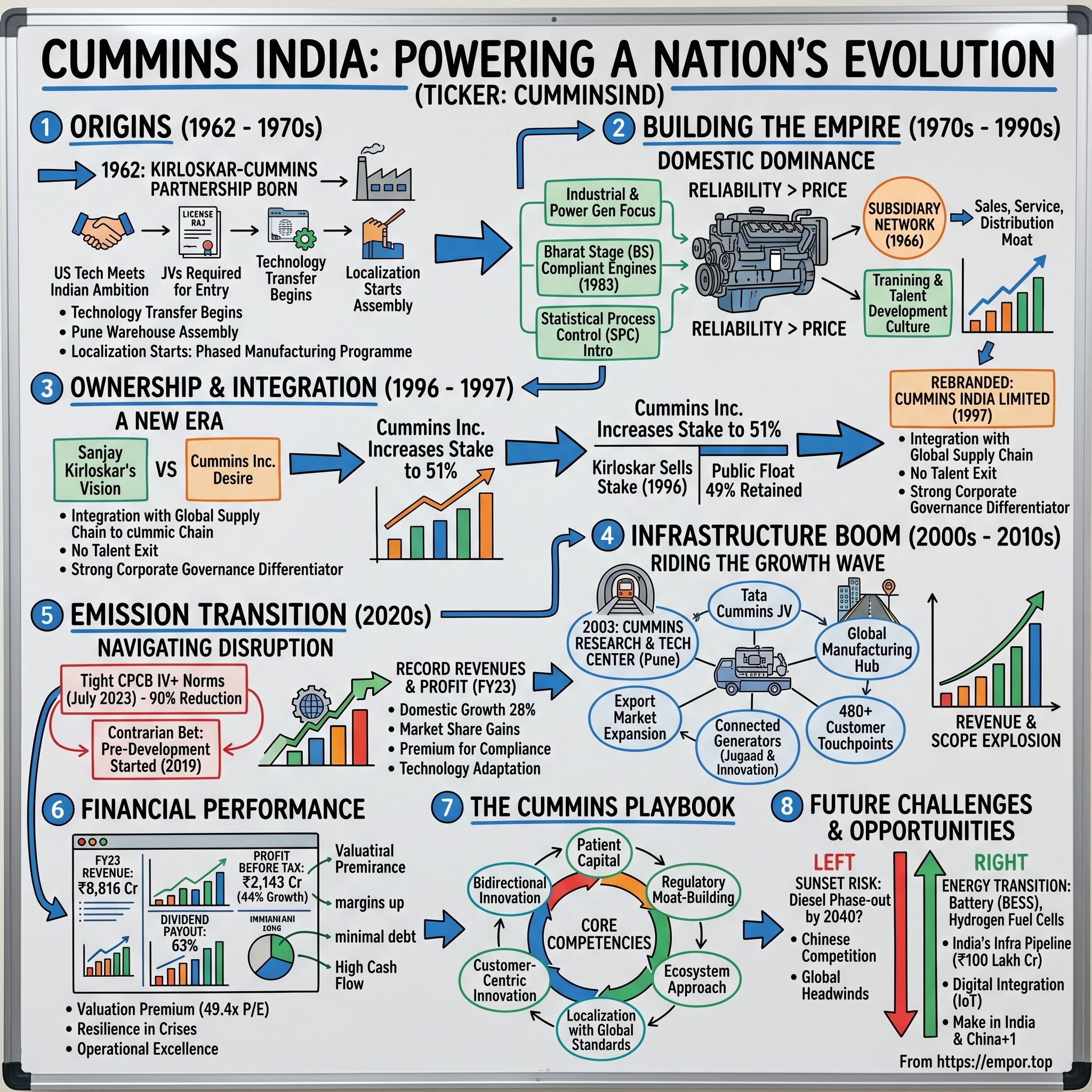

II. Origins: The Kirloskar-Cummins Partnership

Laxmanrao Kirloskar was furious. The year was 1961, and the founder of Kirloskar Oil Engines had just returned from his third trip to Columbus, Indiana, where he'd been courting Cummins Engine Company for a potential joint venture. The Americans were interested but cautious—India's License Raj made foreign investment a bureaucratic nightmare, and the country's industrial base was still nascent. But Kirloskar saw what others didn't: India's agricultural revolution would need mechanization, its infrastructure would need power, and both would need diesel engines.

The Kirloskar Group wasn't just any Indian company. Founded in 1888, it had survived British colonialism, two world wars, and the chaos of partition. Laxmanrao's father had started by making ploughs; now the son was building engines. The family understood something fundamental about India: progress here happened in steps, not leaps. You couldn't jump straight to sophisticated technology; you had to build the capability to absorb it first.

Meanwhile, in Columbus, J. Irwin Miller was having his own moment of vision. The nephew of Cummins's founder and the company's leader since 1947, Miller was that rare breed of American executive who thought in decades, not quarters. He'd already expanded Cummins across Europe and was eyeing Asia. But India was different. This wasn't about selling engines to a developing market; it was about creating an industrial ecosystem from scratch.

The timing was extraordinary. Jawaharlal Nehru's government had just launched the Third Five-Year Plan, emphasizing heavy industry and import substitution. Foreign companies could enter India, but only through joint ventures with local partners, and only if they transferred technology. The government wanted Indian companies to learn, not just assemble. For most American corporations, these conditions were deal-breakers. For Miller, they were exactly right.

On February 17, 1962, Kirloskar Cummins Limited was born. The shareholding structure told the whole story: 38,250 shares to Kirloskar Oil Engines, 75,000 shares to Cummins Engine Company, and crucially, 36,750 shares offered to the Indian public. This wasn't just a business arrangement; it was a three-way marriage between American technology, Indian entrepreneurship, and public participation.

The early days were brutal. The first engines were essentially knocked-down kits imported from Columbus and assembled in a converted Kirloskar warehouse in Pune. Indian engineers would carefully study each component, understanding not just how to put them together, but why they were designed that way. Cummins sent its best engineers to Pune—not for weeks, but for years. They lived in company quarters, learned Marathi, and trained a generation of Indian engineers who would become the backbone of the country's diesel engine industry.

The product-market fit was immediate but challenging. India needed engines for irrigation pumps, generators for factories, and power for a grid that barely existed outside major cities. But Indian conditions were unlike anything Cummins had encountered. Dust levels that would destroy American engines in weeks. Maintenance intervals measured in years, not months, because skilled technicians were scarce. Fuel quality that varied wildly depending on the source. Every assumption had to be reengineered.

By 1973, the joint venture had built its first dedicated manufacturing facility in Pune, a 25-acre complex that would eventually become one of Cummins's largest factories outside America. But this wasn't just about scale—it was about localization. The Indian government's Phased Manufacturing Programme demanded that foreign companies progressively increase local content. What started as simple assembly evolved into forging, casting, and precision machining. Kirloskar Cummins wasn't just making engines; it was creating an entire supply chain.

The subsidiary network began expanding almost immediately. In 1966, they established Cummins Diesel Sales and Services India Limited, which would later become a wholly-owned subsidiary. This wasn't corporate bureaucracy—it was strategic architecture. Different entities for manufacturing, sales, and service allowed the company to navigate India's complex regulatory environment while building specialized capabilities in each area.

The cultural fusion was remarkable. Kirloskar brought deep understanding of Indian business practices—the importance of relationships, the need for flexible payment terms, the art of working with government. Cummins brought rigorous quality standards, systematic training programs, and a long-term view that matched Indian patience. Together, they created something unique: world-class engineering wrapped in Indian pragmatism.

What's often missed in corporate histories is how personal these ventures were. Laxmanrao Kirloskar and Irwin Miller developed a genuine friendship, exchanging letters about philosophy and business ethics. Both were deeply religious men who saw business as a form of service. This wasn't just convenient corporate PR—it shaped how the company operated. When disputes arose, as they inevitably did in any joint venture, they were resolved through dialogue, not litigation.

The foundation laid in these early years would prove remarkably durable. The technology transfer wasn't just about blueprints and specifications; it was about transferring a way of thinking about quality, about customer service, about the role of business in society. As we'll see, this cultural DNA would survive multiple ownership changes and market upheavals, but first, the company had to build its empire during India's most challenging economic decades.

III. Building the Engine Empire (1970s–1990s)

The phone rang at 3 AM in the Pune factory manager's bedroom. It was 1978, and a textile mill in Coimbatore had just lost power—their Kirloskar Cummins generator, installed five years earlier, had failed for the first time. Within an hour, two engineers were on a overnight train with replacement parts. By noon the next day, the generator was running again. The mill owner, stunned by the response time, would become a customer for life and tell this story to every industrialist he knew. This was how empires were built in pre-liberalization India—one emergency response, one reputation, one relationship at a time.

The 1970s and 80s were India's industrial adolescence—awkward, inefficient, but absolutely critical for what came next. The License Raj meant that everything required permission: importing a component, expanding production, even changing a product design. Most foreign joint ventures foundered in this bureaucratic maze. Kirloskar Cummins thrived by becoming more Indian than the Indians while maintaining American engineering standards.

The product strategy during this period was brilliantly counterintuitive. While competitors chased volume in the agricultural pump-set market, Kirloskar Cummins focused on industrial and power generation applications where reliability mattered more than price. A farmer might tolerate a pump breaking down; a hospital losing power during surgery could not. This focus on mission-critical applications created a quality premium that exists to this day.

The 1983 launch of BS (Bharat Stage) compliant engines marked a crucial inflection point. India was beginning to care about emissions—not because of environmental consciousness, but because urban air quality had become a political issue. Kirloskar Cummins was ready with engines that met these standards before they were mandatory. This pattern—anticipating regulation rather than reacting to it—would become a core competitive advantage.

Technology transfer during this period went far beyond engines. Cummins introduced Statistical Process Control to Indian manufacturing when most factories still relied on end-of-line inspection. They implemented preventive maintenance schedules in a country where "run it until it breaks" was standard practice. They created training programs that turned diploma holders into world-class technicians. The Pune facility became a university disguised as a factory.

The subsidiary network that started in 1966 with Cummins Diesel Sales and Services evolved into a sophisticated distribution system. But this wasn't just about coverage—it was about capability. Each dealer needed to stock parts, train technicians, and provide emergency support. In a country where roads turned to mud during monsoons and spare parts could take weeks to arrive, this distributed inventory and expertise network became an unassailable moat.

The late 1980s brought an unexpected challenge: success. Kirloskar Cummins engines had become so reliable that replacement cycles stretched longer than projected. The company responded by expanding into generator sets and specialized components, transforming from an engine company into a power solutions provider. This wasn't diversification for its own sake—it was about owning the entire value chain of power generation.

Localization reached remarkable levels during this period. By 1990, engines that had started as 100% imported kits were now 85% Indian-made. But this wasn't just about replacing American parts with cheaper Indian alternatives. Local suppliers were developed, trained, and often funded to meet Cummins's global quality standards. Many of these suppliers would later become successful exporters themselves, creating an ecosystem that benefited the entire Indian engineering sector.

The human story of this period is particularly compelling. Engineers who joined in the 1970s talk about a culture unlike anything in Indian industry. Performance reviews were based on metrics, not relationships. Promotion paths were clear and merit-based. Training wasn't a one-time event but a continuous process. Workers were sent to Columbus for months-long assignments, returning with not just technical knowledge but a different way of thinking about manufacturing excellence.

One veteran engineer recalls the first time they achieved Six Sigma quality levels in the mid-1990s—defect rates so low they were measuring in parts per million. The entire factory celebrated, but the American technical advisor reminded them that Cummins's global standard was even higher. This combination of recognition and aspiration, of celebrating progress while demanding more, created a performance culture that attracted India's best engineering talent.

The relationship between the Indian and American partners evolved significantly during these decades. What started as teacher-student became a partnership of equals. Indian engineers began contributing innovations that were adopted globally—solutions for high-dust environments, extended maintenance intervals, multi-fuel capability. The Pune Technical Center, established in the late 1980s, wasn't just implementing American designs; it was creating new ones.

Market dynamics during this period were fascinating. The License Raj that frustrated so many businesses actually protected Kirloskar Cummins's market position. New entrants faced the same bureaucratic hurdles but without the established relationships and local knowledge. The company's early investment in distribution and service created switching costs that price competition couldn't overcome. By the time India began liberalizing in 1991, Kirloskar Cummins had built a fortress that would prove remarkably defensible.

The numbers tell only part of the story. Revenue grew from tens of crores in the 1970s to hundreds by the 1990s. But the real achievement was institutional: creating an industrial capability that could compete globally while serving local needs. As India stood on the brink of economic liberalization, Kirloskar Cummins was perfectly positioned for what came next—though first, it would undergo its own transformation that would test everything built over three decades.

IV. The Ownership Transition & Independence (1996–1997)

The boardroom at Kirloskar Oil Engines' Pune headquarters was silent. It was March 1996, and Sanjay Kirloskar had just proposed something unthinkable: selling the family's stake in Kirloskar Cummins to the Americans. For a family that had spent a century building industrial India, this felt like betrayal. But Sanjay saw what others didn't—the joint venture had outgrown its original structure. What India needed now wasn't protection but integration with global supply chains, and that required a different ownership model.

The negotiation that followed was unlike any typical acquisition. This wasn't a hostile takeover or a distressed sale. Both partners were profitable, both were satisfied with the partnership, yet both recognized that India's post-liberalization economy demanded a new structure. Cummins wanted greater control to integrate Indian operations into its global strategy. Kirloskar wanted capital to pursue opportunities in other sectors. The public shareholders—that crucial third leg of the original structure—needed protection.

The deal structure was elegant in its simplicity: Cummins Inc. would purchase Kirloskar's shares, taking its stake to 51%. The remaining 49% would continue trading on the Bombay Stock Exchange, ensuring public participation and transparency. This wasn't just financial engineering—it was a template for how foreign companies could deepen their Indian presence while maintaining local stakeholder trust.

September 10, 1997, marked more than a name change from Kirloskar Cummins Limited to Cummins India Limited. It was a declaration of intent. The company was no longer an Indian-American joint venture; it was now the Indian subsidiary of a global corporation. But unlike many foreign acquisitions that led to headquarters in Singapore or Dubai, Cummins doubled down on India. The Pune facility wouldn't just serve Indian markets—it would become a global manufacturing hub.

The transition revealed the strength of the institutional culture built over 35 years. When companies change ownership, key talent often leaves. At Cummins India, virtually no one did. The Indian managers who had grown up in the joint venture now found themselves with greater responsibilities and global exposure. The American expats who had made India their home stayed on, providing continuity. The workers, many second-generation Cummins employees, saw opportunity rather than threat.

Corporate governance became a differentiator during this period. While Cummins had majority control, they operated as if they didn't. Independent directors were given real power. Minority shareholders' interests were actively protected. Financial reporting exceeded regulatory requirements. This wasn't altruism—it was strategic. In a market where foreign companies were viewed with suspicion, Cummins India's governance standards became a competitive advantage.

The timing of the ownership transition was remarkable. India's infrastructure boom was just beginning. The Golden Quadrilateral highway project was on the drawing board. Power sector reforms were creating demand for distributed generation. The IT boom was driving demand for reliable backup power. Cummins India, with its new structure and global backing, was perfectly positioned to capture this growth.

But the transition wasn't without challenges. Suppliers who had worked with "Kirloskar Cummins" for decades suddenly wondered if contracts would be honored. Government officials questioned whether an American subsidiary would maintain the same commitment to local manufacturing. Competitors spread rumors that Cummins would now import everything from America. Each concern had to be addressed through action, not words.

The response was decisive. Instead of reducing local manufacturing, Cummins announced major capacity expansions. Rather than replacing Indian suppliers, they invested in upgrading supplier capabilities. The Pune Technical Center was expanded, eventually housing over 2,500 engineers. This wasn't just maintaining the status quo—it was accelerating the localization strategy that had begun in 1962.

The cultural integration was handled with unusual sensitivity. Cummins didn't impose American management practices wholesale. Instead, they created a hybrid model that combined Cummins's global processes with Indian relationship-based business practices. Performance metrics were standardized globally, but implementation was localized. Technical standards were non-negotiable, but commercial terms were flexible.

One senior manager from this period describes the transition as "changing the engine while the car was running at full speed." Orders couldn't be delayed, quality couldn't slip, and relationships couldn't be disrupted. The fact that the transition was essentially seamless—customers noticed no service disruption, suppliers saw no payment delays—was a testament to the planning and execution.

The financial markets' response was telling. Rather than selling after the ownership change, public shareholders held on. The stock price, which had been range-bound during the joint venture years, began a steady climb. Institutional investors, both domestic and foreign, started taking positions. The company that had been a steady but unexciting industrial stock was transforming into a growth story.

What made this transition unique in the annals of emerging market acquisitions was its success in maintaining local identity while gaining global scale. Cummins India wasn't just a sales office or assembly plant for an American company—it was a full-fledged business with its own R&D, manufacturing, and market strategy. This model would inspire numerous other multinationals entering India, though few would execute it as successfully.

The ownership transition also coincided with a generational change in leadership. The engineers who had joined as fresh graduates in the 1960s and 70s were now in senior positions. They brought institutional memory but weren't wedded to old ways. This combination of experience and adaptability would prove crucial as Cummins India entered its most dramatic growth phase, riding India's infrastructure boom while building capabilities that would serve global markets.

V. Infrastructure Boom & Market Leadership (2000s–2010s)

The call came at midnight. It was May 2003, and Delhi Metro's tunnel boring machine had just broken through into Connaught Place station, three months ahead of schedule. The project director's first call wasn't to the Transport Minister or the media—it was to Cummins India's emergency response team. The generators powering the ventilation systems had run continuously for 72 hours straight without a single failure. In the brutal Delhi summer, with temperatures hitting 45°C, this wasn't just reliability—it was a miracle of engineering.

India in the 2000s was a country transforming at breakneck speed. The Golden Quadrilateral connected the four metros with world-class highways. Every tier-2 city wanted an airport. IT parks sprouted from Bangalore to Bhubaneswar. The power deficit, which had touched 13% in the late 1990s, meant every commercial building needed backup generation. Cummins India wasn't just participating in this boom—they were enabling it.

The masterstroke of this period was the 2003 establishment of the Cummins Research and Technology Center in Pune. This wasn't a token R&D facility to satisfy government requirements. It was a serious engineering center that would eventually employ over 2,500 engineers, making it one of Cummins's largest technical centers globally. The mandate was audacious: don't just adapt global products for India, create solutions that the world could use.

The technical center's first breakthrough came from an unexpected source—Indian jugaad. Engineers noticed that customers were modifying generators to run on multiple fuels, switching between diesel, natural gas, and even biogas depending on availability and price. Instead of stopping this practice, Cummins formalized it, creating flex-fuel generators that became a global product line. Innovation wasn't always about advanced technology; sometimes it was about understanding how customers actually used products.

The joint venture with Tata Motors, forming Tata Cummins as a 50:50 partnership, showed how much Cummins had learned about the Indian market. Despite being a subsidiary of an American corporation, they understood that certain markets required local partnerships. The medium and heavy commercial vehicle segment was dominated by Tata, and trying to compete would have been futile. Instead, they created a structure that gave both partners what they wanted—Tata got world-class engines, Cummins got market access.

The export hub strategy that emerged during this period was particularly clever. India's cost advantages were obvious, but Cummins went beyond labor arbitrage. They used India's challenging operating conditions as a testing ground. Engines that survived Indian dust, heat, and maintenance practices could work anywhere. Products developed for price-sensitive Indian customers found markets across Asia, Africa, and Latin America. By 2008, exports had become a significant revenue stream.

The human capital story of this period deserves special attention. The Cummins Technical Centre India (CTCI) became a talent magnet, recruiting from IITs and NITs. But recruitment was just the beginning. Engineers were rotated through global assignments, working on projects from Brazilian mining equipment to North American locomotives. This wasn't just about individual development—it was about creating a globally integrated workforce where an engineer in Pune could seamlessly collaborate with teams in Columbus or Beijing.

The numbers from this period are staggering. Revenue touched ₹5,700 crores in 2008, a tenfold increase from a decade earlier. But the real transformation was in scope. Cummins India was no longer just selling engines and generators. They were providing complete power solutions—design, installation, maintenance, financing. When a data center needed 100% uptime, when a hospital required seamless power transition, when a construction site needed mobile power solutions, Cummins had an answer.

The infrastructure boom also revealed the importance of the distribution network built over decades. While competitors struggled to provide service in remote locations, Cummins had touchpoints everywhere. A hydroelectric project in Arunachal Pradesh, a port in Gujarat, a steel plant in Odisha—wherever India was building, Cummins was present. The company now had over 480 customer touchpoints, each capable of not just selling but servicing products.

The 2008 financial crisis provided an unexpected validation of the India strategy. While developed markets collapsed, India's infrastructure spending continued. The government's stimulus package focused on roads, power, and urban development—all sectors where Cummins was dominant. The company's India revenues actually grew during the crisis, offsetting weakness in other markets and proving the value of emerging market exposure.

Manufacturing capabilities expanded dramatically during this period. The five state-of-the-art plants weren't just assembly facilities—they included sophisticated testing centers, training institutes, and innovation labs. The Pune plant could conduct high-altitude testing, simulating conditions from sea level to the Himalayas. The Phaltan facility specialized in high-horsepower engines for marine and rail applications. Each plant developed unique capabilities while maintaining global quality standards.

The ecosystem play extended beyond direct operations. Cummins created vendor development programs that upgraded hundreds of small suppliers. They established training institutes that certified thousands of technicians annually. They partnered with engineering colleges to develop curriculum. This wasn't corporate social responsibility—it was building the infrastructure for long-term growth.

What's remarkable about this period is how Cummins India maintained its culture despite explosive growth. The company grew from hundreds to thousands of employees, yet retained its performance-driven, customer-focused DNA. New hires were immersed in the "Cummins Way"—a set of values and practices that transcended national boundaries. The company that emerged from the infrastructure boom wasn't just bigger; it was fundamentally more capable.

As the 2010s drew to a close, Cummins India faced a new challenge. Environmental regulations were tightening globally, and India was following suit. The diesel engines that had powered India's growth were increasingly seen as polluters. The company that had built its fortune on fossil fuels would need to reinvent itself for a cleaner future. This transition would test everything Cummins India had built over five decades, requiring not just technical innovation but a fundamental reimagining of what it meant to power progress.

VI. The Great Emission Transition (2020s)

The conference room at the Central Pollution Control Board fell silent as the new emission norms were unveiled. It was January 2022, and the CPCB IV+ standards just announced were more stringent than anyone had anticipated—a 90% reduction in particulate matter and nitrogen oxides compared to existing CPCB II standards, effective July 1, 2023. For most manufacturers, this was a death sentence. For Anant Talaulicar, Managing Director of Cummins India, it was the moment he'd been preparing for since 2019.

Three years earlier, when competitors were lobbying for delayed implementation, Cummins had made a contrarian bet. They began developing CPCB IV+ compliant products before the standards were finalized, using global emissions technology adapted for Indian conditions. This wasn't just about installing catalytic converters or particulate filters—it required fundamental reengineering of combustion systems, cooling circuits, and control software. The investment was massive, the risk substantial, but the strategic logic was clear: regulatory compliance could become a competitive moat.

The technical challenge was staggering. Indian operating conditions made achieving these emission levels particularly difficult. Dust levels that clogged filters designed for cleaner environments. Fuel quality that varied dramatically across regions. Maintenance practices that assumed robust, simple systems rather than sophisticated emission controls. Each problem required innovation, not just adaptation of global solutions.

The Ashwasan IV+ program launched in early 2023 was a masterclass in change management. Rather than just selling new products, Cummins created an entire ecosystem to support the transition. Customer education sessions explained not just what was changing but why it mattered. Service technicians were retrained on new technologies. Financing programs helped customers upgrade equipment. The message was clear: Cummins wasn't just complying with regulations; they were partners in their customers' transition.

The Automotive Research Association of India (ARAI) certifications obtained months before the deadline vindicated the early investment strategy. While competitors scrambled for approvals, Cummins was already shipping compliant products. Orders that might have gone to cheaper alternatives flowed to Cummins simply because they were ready. The premium for certainty in uncertain times proved far more valuable than any price advantage.

What made this transition remarkable was its financial impact. Conventional wisdom suggested that tighter emission norms would hurt sales as customers delayed purchases or switched to alternatives. Instead, Cummins India posted record revenues. Total sales reached ₹8,816 crores, up 16% year-over-year. Profit before tax hit ₹2,143 crores, a stunning 44% increase. The market was willing to pay for compliance, reliability, and the peace of mind that came with choosing the industry leader.

The domestic market response was particularly strong, with sales growing 28% to ₹7,143 crores. This wasn't just replacement demand—it was market share gain. Customers who might have previously chosen cheaper alternatives now prioritized compliance certainty. The reputational risk of being caught with non-compliant equipment outweighed any cost savings. Cummins's decades-long investment in brand trust paid dividends when trust mattered most.

The export story was more complex, with sales declining 18% to ₹1,673 crores. But this wasn't a failure of strategy—it reflected global market dynamics and currency fluctuations. More importantly, the technology developed for Indian CPCB IV+ standards was finding applications globally. Countries across Asia and Africa were adopting similar emission norms, and Cummins India's solutions were often more cost-effective than those developed in higher-cost markets.

The product portfolio transformation went beyond just meeting emission standards. Engineers used the regulatory transition as an opportunity to improve overall performance. The new engines were not just cleaner but more fuel-efficient, quieter, and more reliable. Digital integration allowed remote monitoring and predictive maintenance. What started as regulatory compliance became product innovation.

The manufacturing transformation was equally impressive. Plants that had produced relatively simple mechanical engines now assembled sophisticated systems with electronic controls, after-treatment systems, and sensor arrays. Workers trained on welding and machining learned programming and diagnostics. The factory floor looked more like a tech company than a traditional manufacturing plant.

The financial metrics from this period tell a story of operational excellence. Despite the massive investment in new technology, the company maintained a healthy dividend payout of 63%, signaling confidence in sustained profitability. The balance sheet remained strong, with minimal debt despite significant capital expenditure. This wasn't financial engineering—it was the result of decades of prudent management and reinvestment.

The competitive dynamics during the transition were fascinating. Several competitors, particularly smaller Indian manufacturers, couldn't make the technological leap. Some exited the market entirely; others became assemblers of Cummins components. Chinese manufacturers, who had been gaining share in price-sensitive segments, struggled with the certification process and local support requirements. The regulatory transition that many feared would level the playing field actually reinforced Cummins's dominance.

Customer relationships deepened during this period. The transition wasn't just transactional—it required trust. Customers needed to believe that Cummins's solutions would work, that support would be available, that the company would stand behind its products. The thousands of customer touchpoints, the decades of service history, the reputation for reliability—all of this intangible capital became tangible value during the transition.

The human story of this transformation deserves recognition. Engineers who had spent careers optimizing mechanical systems had to learn chemistry and electronics. Service technicians comfortable with wrenches and grease now worked with laptops and diagnostic software. Yet employee satisfaction remained high, driven by pride in meeting a challenge many thought impossible and being part of a company that was defining industry standards rather than just meeting them.

As 2024 progressed, with complete transition to CPCB IV+ norms for applicable products, Cummins India stood stronger than ever. They hadn't just survived the most significant regulatory disruption in their history—they had used it to widen their competitive moat. But even as they celebrated this success, new challenges loomed. The energy transition was accelerating globally, and questions about the long-term future of diesel engines, even clean ones, were becoming impossible to ignore.

VII. Financial Performance & Market Position

The spreadsheet on the analyst's screen didn't make sense. It was late 2023, and she was modeling Cummins India's financials for her Mumbai-based fund. Companies implementing expensive emission standards should show margin compression, market share loss, working capital stress. Instead, she was looking at profit before tax up 44%, margins expanding, and cash generation at record levels. Either the numbers were wrong, or Cummins had pulled off something extraordinary.

The headline revenue figure of ₹8,816 crores for fiscal 2023 told only part of the story. The real insight was in the composition. Domestic sales at ₹7,143 crores reflected not just market growth but pricing power—customers were paying premiums for CPCB IV+ compliant products. The 28% domestic growth rate was nearly double the industry average, indicating significant market share gains. This wasn't riding a rising tide; this was taking share in a transforming market.

The export decline to ₹1,673 crores initially seemed concerning until you understood the context. Global supply chains were still recovering from pandemic disruptions. More importantly, Cummins India was being selective about export orders, prioritizing high-margin products and strategic relationships over volume. The company was choosing profitability over growth, a luxury only market leaders can afford.

The profitability metrics were where Cummins India truly distinguished itself. Profit before tax of ₹2,143 crores represented a 24.3% margin—exceptional for an industrial manufacturer. This wasn't financial engineering or one-time gains. It was operational excellence compounded over decades: superior product mix, pricing discipline, and cost management that bordered on art. While competitors struggled to pass on increased costs, Cummins's brand strength allowed them to maintain margins.

The dividend payout ratio of 63% sent a powerful signal to the market. Despite massive investments in emission technology, despite global uncertainty, despite energy transition questions, management was confident enough to return significant cash to shareholders. This wasn't recklessness—the company maintained a fortress balance sheet with minimal debt. It was confidence born from competitive position and cash generation capability.

The capital allocation strategy revealed sophisticated financial management. Rather than hoarding cash or pursuing aggressive acquisitions, Cummins India invested in high-return projects while maintaining financial flexibility. Capital expenditure focused on technology upgrades and capacity expansion in high-margin segments. Working capital management was exemplary, with days sales outstanding actually improving despite rapid growth.

The ownership structure—51% held by Cummins Inc. with 49% public float—created interesting dynamics. The parent company provided technology and global market access but allowed local management significant autonomy. This wasn't the typical subsidiary relationship where profits were upstreamed to headquarters. Cummins India retained earnings for local growth while maintaining healthy dividends for all shareholders.

Market valuation told its own story. Trading at 49.4 times price-to-earnings, Cummins India commanded a premium valuation unusual for industrial companies. The market was pricing in not just current performance but sustained competitive advantages. This wasn't speculation—it was recognition that regulatory compliance, distribution networks, and customer relationships created barriers to entry that justified premium multiples.

The comparison with global peers was instructive. Cummins India's margins exceeded those of the parent company and most international engine manufacturers. This wasn't because India was an easy market—quite the opposite. It was because decades of localization had created a cost structure optimized for emerging market realities while maintaining developed market quality standards. The company had achieved the holy grail of global business: world-class quality at competitive costs.

Segment analysis revealed strategic focus. While power generation remained the core business, industrial applications were growing faster. Data centers, construction equipment, mining operations—sectors driving India's growth—were also Cummins's sweet spots. The company wasn't just benefiting from macro trends; they had positioned themselves at the intersection of India's development needs and their core capabilities.

The return metrics were particularly impressive. Return on equity consistently exceeded 25%, return on capital employed topped 30%. These weren't leverage-driven returns—the company operated with minimal debt. It was pure operational efficiency: asset utilization that extracted maximum value from every rupee invested. For a capital-intensive manufacturing business, these returns were exceptional.

Cash flow generation deserved special attention. Operating cash flow consistently exceeded reported profits, indicating high-quality earnings. Capital expenditure was self-funded, eliminating dependence on external financing. Free cash flow generation allowed simultaneous investment in growth and shareholder returns. This financial flexibility became a competitive weapon, allowing quick response to opportunities or challenges.

The resilience of the business model was tested during various crises—the 2008 financial crisis, 2016 demonetization, COVID-19 pandemic, and the emission transition. Each time, Cummins India not only survived but emerged stronger. Revenue might dip temporarily, but profitability remained robust, market share increased, and competitive position strengthened. This wasn't luck—it was the result of conservative financial management and operational excellence.

Working capital management told a story of market power. Despite being in a manufacturing business with significant inventory requirements, Cummins maintained negative working capital cycles in several segments. Customers paid advances for generators, suppliers extended credit, and efficient operations minimized inventory. This cash generation machine funded growth without external capital.

The geographic revenue split revealed untapped potential. While domestic sales dominated, the export percentage had room to grow. As emission standards tightened globally, Cummins India's proven solutions could find larger international markets. The technology developed for Indian conditions was increasingly relevant for other emerging markets facing similar transitions.

What made these financial achievements remarkable was their sustainability. This wasn't a cyclical upturn or temporary regulatory windfall. The competitive advantages—technology leadership, distribution network, customer relationships, operational excellence—were structural and strengthening. The financial performance was the scoreboard, but the real game was building capabilities that would endure regardless of market conditions. As impressive as the current numbers were, they might just be the foundation for what was to come.

VIII. The Cummins India Playbook

Every Monday morning at 7 AM, before the Pune factory floor stirred to life, Ashwant Dwivedi would walk the production line. The Head of Manufacturing wasn't checking for defects or efficiency—those metrics were monitored continuously. He was looking for something subtler: signs of innovation, evidence that workers were thinking beyond their immediate tasks. This ritual, inherited from his predecessors going back decades, embodied the Cummins India playbook—global standards delivered through local wisdom.

Technology transfer, the foundation of Cummins India's success, had evolved far beyond its original conception. In the 1960s, it meant teaching Indian workers to assemble American designs. By the 2020s, it had become a bidirectional flow of innovation. The multi-fuel engines developed for Indian power cuts became global products. Cooling systems designed for Indian dust found applications in Australian mines. The teacher-student relationship had become a partnership of equals, with Pune engineers leading global projects.

The power of patient capital was perhaps Cummins's greatest strategic advantage. While competitors optimized for quarterly earnings, Cummins thought in decades. The investment in emission technology began years before regulations were announced. The distribution network was built settlement by settlement over sixty years. Training programs educated engineers who wouldn't contribute meaningfully for years. This temporal arbitrage—investing on ten-year horizons while competitors focused on ten quarters—created advantages that compound couldn't replicate.

Regulatory compliance as moat-building was counterintuitive but brilliant. Most companies viewed regulations as costs to minimize. Cummins saw them as competitive opportunities. Every new emission standard, safety requirement, or quality mandate was a chance to widen the gap with competitors. The CPCB IV+ transition wasn't a burden—it was a gift that eliminated weaker players and reinforced Cummins's position. By making compliance a core competency rather than a necessary evil, they turned government policy into competitive advantage.

Distribution excellence went beyond mere presence. With over 480 customer touchpoints, Cummins had India covered geographically. But coverage was just the beginning. Each touchpoint was a full-service operation: sales, service, parts, training. A customer in remote Arunachal Pradesh received the same response time as one in Mumbai. This wasn't economically rational for individual transactions, but it built trust that translated into decades-long relationships and premium pricing power.

The manufacturing backbone of five state-of-the-art plants represented more than production capacity. Each facility was a center of excellence: Pune for mid-range engines, Phaltan for high-horsepower applications, others specializing in generators, components, or specific technologies. This specialization allowed world-class capabilities in each domain while maintaining economies of scale. The plants weren't just factories—they were universities, innovation centers, and customer experience centers.

Human capital development at Cummins India transcended traditional corporate training. With over 3,000 employees, the company had created one of India's deepest pools of engine technology expertise. But this wasn't just about quantity. Engineers regularly rotated through global assignments. Technicians were certified to international standards. Even shop-floor workers understood statistical process control and lean manufacturing. This investment in people created capabilities that competitors couldn't poach—the knowledge was too embedded in Cummins's systems and culture.

The partnership philosophy extended beyond the Tata joint venture. Relationships with suppliers weren't transactional but developmental. Cummins invested in supplier capabilities, provided training, sometimes even funded equipment upgrades. This created a dedicated supply base that prioritized Cummins during shortages and collaborated on innovations. The ecosystem approach meant that Cummins's competitive advantage extended beyond its factory walls.

Localization with global standards was a delicate balance mastered over decades. Products were adapted for Indian conditions—extended maintenance intervals, multi-fuel capability, dust resistance—without compromising core performance. Manufacturing processes accommodated local practices while maintaining quality standards. Management styles blended American metrics-driven approaches with Indian relationship-based business. This wasn't choosing between global and local—it was achieving both simultaneously.

Customer education had become a strategic differentiator. Cummins didn't just sell products; they taught customers how to maximize value from them. Training programs for customer technicians, efficiency optimization consultations, total cost of ownership analyses—these services created switching costs beyond the physical product. A customer buying a Cummins generator wasn't just buying hardware but accessing decades of accumulated knowledge.

The innovation model balanced global R&D with local insight. The 2,500 engineers at the Pune technical center weren't just implementing designs from Columbus—they were creating solutions for global markets. But innovation wasn't limited to R&D labs. Shop-floor suggestions were systematically captured and implemented. Customer feedback loops were shortened to weeks, not months. This democratized innovation model meant insights came from everywhere.

Financial discipline underpinned everything. Despite market leadership, Cummins never became complacent about costs. Every expense was scrutinized, every investment required rigorous justification. This wasn't penny-pinching—strategic investments were made boldly. But operational efficiency was a religion. The result was industry-leading margins that funded both growth and shareholder returns.

The brand strategy was subtle but powerful. Cummins never advertised to consumers—few Indians knew the company name. But every facilities manager, every construction executive, every industrial purchaser knew that Cummins meant reliability. The brand was built through millions of hours of uptime, thousands of emergency responses, decades of kept promises. This B2B brand power translated into pricing premiums that consumer brands would envy.

Risk management was embedded in the business model. Multiple manufacturing sites provided redundancy. Diverse end markets—construction, industrial, marine, power generation—reduced concentration risk. The domestic-export balance provided currency hedging. Conservative financial management maintained flexibility for unexpected shocks. This wasn't risk aversion—it was intelligent risk-taking backed by robust mitigation strategies.

The cultural elements of the playbook were hardest to replicate. The performance culture that demanded excellence. The customer focus that prioritized long-term relationships over short-term profits. The integrity that meant honoring commitments even when costly. The humility that kept learning despite market leadership. These soft factors, built over sixty years, were perhaps the strongest competitive advantages.

What made the Cummins India playbook remarkable was its reproducibility with irreproducibility. The principles—patient capital, regulatory excellence, distribution depth, ecosystem building—could be understood and copied. But the execution—the thousands of small decisions, the accumulated relationships, the embedded knowledge—couldn't be replicated quickly. Competitors could follow the playbook, but they were sixty years behind. This time advantage, in a world obsessed with speed, was Cummins India's ultimate moat.

IX. Future Challenges & Opportunities

The PowerPoint slide was stark: "Diesel Dead by 2040?" It was January 2024, and Cummins India's strategy team was presenting to the board. Outside, in the parking lot, electric buses hummed past diesel generators—a daily reminder that the energy transition wasn't a distant threat but a present reality. Yet Managing Director Ashish Bhandari seemed remarkably calm. "Every transformation," he said, "creates more opportunity than it destroys. The question isn't whether diesel has a future, but what role Cummins will play in whatever future emerges."

The energy transition represented both existential threat and generational opportunity. Globally, governments were setting net-zero targets. India had committed to 500 GW of renewable energy by 2030. Electric vehicles were gaining market share. Yet the reality was more nuanced than headlines suggested. India's power grid remained unreliable. Renewable energy needed backup. Industrial applications required power density that batteries couldn't yet provide. The transition wouldn't be a cliff but a curve, and Cummins intended to profit from every point along it.

Battery energy storage systems (BESS) entry marked Cummins's first major diversification beyond combustion engines. This wasn't a desperate pivot but a logical extension. The customers were the same—data centers, industrial facilities, commercial buildings. The need was the same—reliable backup power. Only the technology changed. Cummins's advantages—distribution network, service capability, customer relationships—transferred seamlessly. Early projects showed promising returns, with customers valuing Cummins's reliability reputation even in new technologies.

Chinese competition was intensifying in ways that transcended traditional rivalry. Companies like Weichai and Yuchai weren't just offering cheaper products—they were bringing integrated solutions backed by state support. Their strategy was classic: enter with low prices, accept losses to gain share, then raise prices once established. But Cummins had seen this playbook before. The response wasn't to match prices but to emphasize total cost of ownership, where Chinese products' lower reliability and service network gaps became expensive liabilities.

Infrastructure growth potential remained massive despite India's development. The government's ₹100 lakh crore National Infrastructure Pipeline wasn't just about building—it was about modernizing. Smart cities needed intelligent power systems. Ports required cleaner equipment. Railways were electrifying but needed diesel backup. Each transformation created demand for Cummins's evolving product portfolio. The company that had powered India's first infrastructure boom was positioning for the second.

Export market recovery prospects were improving as global emission standards tightened. Countries across Southeast Asia, Africa, and Latin America were adopting regulations similar to India's CPCB IV+. Cummins India's cost-effective solutions, proven in challenging conditions, were increasingly competitive globally. The technology developed for Indian dust worked in Saudi Arabia. Engines designed for Indian fuel quality thrived in Nigeria. The emerging market to emerging market corridor was Cummins India's to dominate.

Digital and IoT integration was transforming power systems from dumb machines to intelligent assets. Cummins's connected generators could predict failures before they occurred, optimize fuel consumption in real-time, and integrate with smart grids. This wasn't just about adding sensors—it was about changing the business model from selling products to providing outcomes. Customers didn't want generators; they wanted guaranteed uptime. Digital capabilities allowed Cummins to sell reliability as a service.

The hydrogen opportunity was particularly intriguing. While battery electric vehicles dominated passenger car discussions, hydrogen fuel cells showed promise for heavy-duty applications. Trucks, trains, ships, and stationary power generation—Cummins's core markets—were potential hydrogen adopters. The company's engine expertise translated naturally to fuel cells, which required similar thermal management, control systems, and integration capabilities. Early investments were already yielding patents and pilot projects.

Renewable energy integration created unexpected opportunities. Solar and wind farms needed backup power for critical systems. Microgrids required sophisticated controllers to balance multiple power sources. Hybrid systems combining diesel, battery, and renewable sources demanded complex integration—exactly the kind of engineering challenge Cummins excelled at solving. The transition to clean energy didn't eliminate the need for Cummins; it made their expertise more valuable.

The regulatory landscape was becoming more complex but also more favorable. India's focus on manufacturing self-reliance through "Make in India" benefited established local manufacturers. Emission standards were tightening but also harmonizing globally, reducing the cost of compliance. Carbon pricing mechanisms, while challenging for fossil fuel products, also created markets for cleaner alternatives where Cummins was investing.

Supply chain resilience had become a strategic imperative after COVID-19 and geopolitical tensions. Cummins India's localized supply base, developed over decades, provided unusual stability. While competitors struggled with semiconductor shortages and shipping delays, Cummins maintained production through local alternatives and strategic inventory. This resilience was becoming a selling point, with customers willing to pay premiums for supply certainty.

The talent challenge was evolving from quantity to quality. India produced plenty of engineers, but the skills needed were changing. Mechanical engineers needed to understand software. Service technicians required data analysis capabilities. Sales teams had to articulate total cost of ownership, not just product features. Cummins's training infrastructure, built over decades, was adapting to develop these hybrid skills.

Market segmentation was revealing new opportunities. The data center boom, driven by India's digital transformation, created demand for ultra-reliable, efficient power systems. The healthcare sector's growth meant hospitals needed uninterrupted power supply. Cold chain expansion for agriculture and pharmaceuticals required mobile refrigeration powered by clean engines. Each segment had unique needs that Cummins could address with specialized solutions.

Technology partnerships were becoming crucial for accessing capabilities beyond Cummins's core competencies. Collaborations with battery companies, hydrogen developers, and digital platform providers accelerated innovation while sharing risk. The company that had succeeded through self-reliance was learning that the future required ecosystems, not just individual excellence.

Geopolitical dynamics favored Cummins India in unexpected ways. As global supply chains restructured away from China, India became an alternative manufacturing hub. Cummins's established presence, proven quality, and export capabilities positioned them to capture this "China plus one" opportunity. Western companies seeking to diversify supply chains found in Cummins India a partner that combined Eastern costs with Western standards.

The sustainability narrative was shifting from burden to opportunity. ESG-focused investors were pushing companies toward cleaner technologies. Customers were demanding carbon footprint reductions. Regulations were tightening globally. But Cummins India, having navigated the CPCB IV+ transition successfully, was ahead of the curve. Their experience turning environmental compliance into competitive advantage would be valuable as sustainability became central to business strategy.

Despite these opportunities, challenges remained formidable. The core diesel business would eventually decline. New technologies required capabilities Cummins didn't fully possess. Competition was intensifying from both traditional players and new entrants. The capital required for transformation was substantial. Success wasn't guaranteed. But as Cummins India had proven repeatedly over six decades, challenges often became the foundations for the next phase of growth.

X. Bear vs. Bull Case

The debate had been raging for three hours. In one corner of Morgan Stanley's Mumbai conference room sat the bear case advocate, a veteran industrials analyst who'd seen too many incumbents disrupted. In the other, a growth investor who believed Cummins India was just beginning its journey. The moderator, a pension fund manager with ₹500 crores to allocate, needed to make a decision. Both cases were compelling, both were backed by data, but only one could be right.

The bull case started with the fundamentals: Cummins India was virtually debt-free with a cash-generating machine that had delivered 22.4% profit CAGR over five years. This wasn't leveraged financial engineering or accounting creativity—it was operational excellence converting into cash. The balance sheet strength provided flexibility to invest in new technologies, acquire capabilities, or weather downturns without dilution or distress. In a world where capital was increasingly expensive, being self-funded was a superpower.

The parent company technology pipeline was a gift that kept giving. Cummins Inc. invested billions in R&D globally, developing everything from hydrogen fuel cells to battery management systems. Cummins India accessed this innovation at a fraction of the cost, adapting global technologies for local markets. The upcoming X15 engine platform, Destination Zero strategy for carbon neutrality, and HELM hydrogen systems would all flow to India. This technology transfer was worth multiples of the current market cap but wasn't reflected in valuations.

India's infrastructure spending trajectory was barely beginning. The ₹100 lakh crore National Infrastructure Pipeline was just the headline number. State governments were adding their own programs. Private capital was flowing into logistics, warehousing, and industrial capacity. Each project needed power—primary or backup, temporary or permanent. Even with grid improvements, the reliability gap meant backup power would remain essential for decades. Cummins wasn't betting on India staying underdeveloped; they were betting on growth creating complexity that required sophisticated power solutions.

The CPCB IV+ compliance creating barriers to entry was perhaps the strongest moat. Competitors faced a brutal reality: matching Cummins's emission technology required years of development and hundreds of crores in investment. Even if they succeeded technically, they needed ARAI certification, customer trust, and service networks. The regulatory transition that was supposed to level the playing field had actually raised the walls around Cummins's castle. Future tightening of standards would only reinforce this advantage.

The bear case was equally forceful, starting with the elephant in the room: diesel engine sunset risk. Governments worldwide were setting phase-out dates for internal combustion engines. Even if industrial applications lasted longer than automotive, the direction was clear. Cummins might execute a perfect transition to new technologies, but transitions were messy, expensive, and uncertain. The company generating record profits from diesel might not be the winner in batteries or hydrogen.

Export market weakness was concerning beyond the recent 18% decline. Global manufacturing was reshoring, reducing trade. Protectionism was rising. Currency volatility made pricing difficult. Chinese competitors were aggressively expanding internationally with state support. The export story that diversified Cummins India's revenue might not recover to previous levels. Dependence on domestic markets increased concentration risk.

Valuation concerns were hard to dismiss. Trading at 49.4 times earnings, Cummins India was priced for perfection. Any disappointment—a delayed transition to new technologies, market share loss, margin compression—would trigger multiple compression. The stock had risen so far, so fast, that even good news might not be good enough. The risk-reward was skewed unfavorably, with more downside than upside from current levels.

Geopolitical and supply chain risks had multiplied since COVID-19. A Taiwan conflict could disrupt semiconductor supplies. Russia-Ukraine war had shown how quickly energy markets could shift. India-China border tensions could escalate. Each risk individually was manageable, but collectively they created uncertainty that markets hated. Cummins's global integration, previously a strength, became vulnerability in a fragmenting world.

The bull rebuttal was swift: transformation capabilities were proven. Cummins had successfully navigated transitions before—from mechanical to electronic engines, from CPCB II to CPCB IV+, from products to solutions. The company culture embraced change rather than resisting it. Early investments in batteries and hydrogen showed management was ahead of the curve, not behind it. The same capabilities that dominated diesel would dominate whatever came next.

Market structure favored incumbents in industrial markets. Unlike consumer products where brands could shift overnight, industrial customers valued relationships, service, and reliability over decades. Switching costs were high—not just equipment but training, parts inventory, and operational integration. Cummins's installed base created annuity-like service revenues that would continue even if new equipment sales slowed. The transition would be gradual, giving Cummins time to adapt.

The bear's counter was philosophical: every dominant company thought they were different until they weren't. Kodak dominated photography, Nokia owned mobile phones, General Electric defined industrial conglomerates. Each had resources, relationships, and track records. Yet they failed to navigate disruption. Why would Cummins be different? The very success in diesel engines might create organizational antibodies to change.

Technology risk cut both ways. Yes, Cummins was investing in new technologies, but so was everyone else. Tesla's energy division, Chinese battery manufacturers, hydrogen startups—all were targeting the same opportunities with different approaches. Some were unencumbered by legacy businesses. Others had deeper pockets or government support. Cummins might be fighting tomorrow's war with yesterday's advantages.

The bull's closing argument was about asymmetry. The market was pricing in significant disruption risk, but what if the transition was slower than expected? What if hybrid solutions dominated for decades? What if Cummins successfully pivoted to new technologies? The upside from multiple expansion and continued growth could be multiples of current valuations. The downside was protected by the balance sheet, cash generation, and gradual nature of industrial transitions.

The bear's final point was about opportunity cost. Even if Cummins India survived and thrived, were there better opportunities? Younger companies attacking new markets with modern technologies? Global leaders trading at lower multiples? The question wasn't whether Cummins India was a good company—it clearly was. The question was whether it was a good investment at current prices.

The pension fund manager had heard enough. Both cases had merit, both had flaws. The decision would come down to time horizon and risk tolerance. For long-term investors who believed in India's growth and Cummins's execution, the bull case was compelling. For those worried about disruption and valuation, the bear case warranted caution. Like most investment decisions, the answer wasn't black or white but shades of gray, and success would depend as much on position sizing and timing as on which case ultimately proved correct.

XI. Epilogue: Lessons for Global Business

The last flight from Columbus to Mumbai had just taken off, carrying three young Cummins engineers to their new assignments in Pune. It was December 2024, and this journey—once rare and remarkable—had become routine. The westward flow of Indian talent to American headquarters was now matched by Americans seeking experience in the world's most dynamic market. This bidirectional exchange embodied the larger lesson of Cummins India: success in emerging markets requires not just investment but integration, not just presence but partnership.

The joint venture to subsidiary playbook that Cummins pioneered had become a template for multinationals entering emerging markets. Start with a local partner who provides market knowledge and government relationships. Transfer technology gradually, building local capabilities rather than just assembly operations. Maintain public shareholding to ensure transparency and local participation. Eventually transition to majority control, but operate with the humility of a guest, not the arrogance of a conqueror. This model—patient, respectful, mutually beneficial—had proven more durable than aggressive acquisition or organic entry strategies.

The emerging market industrial development pattern that Cummins India exemplified challenged conventional wisdom. Traditional theory suggested countries moved linearly from agriculture to manufacturing to services. But India was doing all three simultaneously, creating unique demands that required novel solutions. Power generation for IT services, engines for agricultural mechanization, infrastructure for manufacturing—all happening in parallel. Companies that understood this complexity and provided integrated solutions thrived; those seeking simple markets failed.

Environmental regulation as innovation catalyst was perhaps the most counterintuitive lesson. Conventional business wisdom treats regulation as a cost to minimize. Cummins India proved it could be a strategic weapon. By embracing standards early, investing ahead of requirements, and helping shape regulations, they turned compliance into competitive advantage. The CPCB IV+ transition that competitors feared became Cummins's opportunity to widen its moat. In an era of increasing environmental consciousness, this approach—making regulation an ally, not an enemy—would become essential for industrial companies globally.

Building engineering capabilities in developing economies required more than technology transfer—it demanded human capital development. Cummins didn't just train workers; they created engineers. The Pune technical center's 2,500 engineers weren't just implementing designs but creating them. This investment in local talent created capabilities that served global markets while being rooted in local realities. The lesson for multinationals was clear: treat emerging markets as sources of innovation, not just consumption.

The power of localization with global standards resolved a false dichotomy that plagued many multinationals. Companies often felt forced to choose between global standardization (efficient but inflexible) and local adaptation (responsive but chaotic). Cummins India achieved both—products optimized for local conditions manufactured to global quality standards. This wasn't compromise but synthesis, creating solutions that worked locally but could compete globally.

The patient capital advantage in volatile markets was demonstrated repeatedly throughout Cummins India's history. While competitors optimized for quarterly earnings, Cummins invested for decades. This temporal arbitrage—thinking in different time horizons than competitors—created sustainable advantages. In emerging markets where volatility was high but growth was certain over time, patient capital wasn't just virtuous but profitable.

The ecosystem approach to industrial development went beyond traditional supply chain management. Cummins didn't just source from suppliers; they developed them. They didn't just sell to customers; they educated them. They didn't just operate factories; they created industrial clusters. This ecosystem approach created network effects that reinforced Cummins's position while developing entire industries. The lesson was that in emerging markets, companies couldn't assume infrastructure—they had to build it.

Cultural integration without cultural imperialism was a delicate balance Cummins mastered. American management practices around metrics and processes were adopted, but Indian relationship-based business wasn't abandoned. Technical standards were non-negotiable, but implementation was flexible. English was the business language, but local languages were respected. This cultural synthesis created an organization that was neither American nor Indian but uniquely Cummins India.

The distribution as competitive advantage lesson challenged the digital age assumption that physical presence was obsolete. Cummins's 480 customer touchpoints weren't just sales outlets but service centers, training facilities, and trust-building mechanisms. In markets where infrastructure was unreliable and distances were vast, physical presence provided assurance that no algorithm could match. The future might be digital, but in emerging markets, the last mile remained stubbornly physical.

Risk management through diversification was built into Cummins India's model from inception. Multiple manufacturing sites, diverse end markets, balanced domestic-export mix, varied product portfolio—each decision reduced concentration risk. This wasn't risk aversion but intelligent risk distribution. In volatile emerging markets, survival required not avoiding risk but managing it through diversification.

The technology transition template that Cummins was now executing—from diesel to batteries and hydrogen—offered lessons for all industries facing disruption. Don't abandon the core business prematurely, but invest in alternatives early. Use existing advantages (distribution, relationships, brand) as bridges to new technologies. Partner where you lack capabilities rather than trying to build everything internally. Most importantly, bring customers along the journey rather than forcing sudden transitions.

The governance model that balanced subsidiary control with local autonomy deserved special attention. Cummins Inc.'s 51% ownership provided control, but the 49% public float ensured accountability. Local management had significant autonomy, but global standards were maintained. This structure—neither fully independent nor completely controlled—created alignment while maintaining flexibility. For multinationals struggling with subsidiary management, this model offered a proven template.

The sustainability narrative that Cummins India was writing—transitioning from diesel engines to clean energy solutions—would become the defining challenge for industrial companies globally. The lesson wasn't that fossil fuel companies were doomed but that those who adapted early and authentically would survive. Cummins's approach—acknowledging diesel's limitations while leveraging existing capabilities for cleaner solutions—showed pragmatic evolution beat revolutionary rhetoric.

The human capital development model where engineers became business leaders, technicians became engineers, and workers became technicians, created not just a company but a institution. This commitment to development created loyalty that no compensation could buy and capabilities that no competitor could poach. In an era where talent was increasingly mobile, Cummins India showed that investment in people created sustainable competitive advantage.

As our three engineers landed in Mumbai, beginning their Indian assignment, they carried with them six decades of accumulated wisdom about building industrial capabilities in emerging markets. They would learn that success required not just good products but deep relationships, not just efficiency but resilience, not just global standards but local adaptation. Most importantly, they would discover what every generation of Cummins leaders had learned: emerging markets weren't just places to sell products but laboratories for innovation, not just sources of growth but teachers of adaptability.

The Cummins India story ultimately transcended business strategy to offer a model for how global companies could contribute to emerging market development while building sustainable competitive advantages. In an era of rising protectionism and fragmenting supply chains, this model—respectful, patient, mutually beneficial—offered hope that globalization could evolve rather than retreat. The company that began as a joint venture to bring diesel engines to India had become something far more significant: proof that Western technology and Eastern ambition could create value that neither could achieve alone.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube