CSB Bank: From Century-Old Catholic Institution to Fairfax-Led Digital Transformation

I. Introduction & The Turnaround Story

Picture this: December 2019, Mumbai. The Bombay Stock Exchange buzzes with anticipation as CSB Bank's shares begin trading. The opening bell rings, and within minutes, the stock surges 41% above its IPO price. Traders scramble to get a piece of what seems impossible—a 99-year-old Kerala bank that was bleeding money just months ago, now commanding a market cap of over ₹5,000 crores. In the VIP gallery, representatives from Fairfax Financial Holdings watch quietly, knowing they've just pulled off one of Indian banking's most audacious turnarounds.

But rewind three years. The same institution—then called Catholic Syrian Bank—was on life support. NPAs had ballooned, losses mounted to ₹197 crores, and the Reserve Bank of India was breathing down its neck. Employees whispered about potential mergers or worse, closure. Customers queued to withdraw deposits. The bank that had survived two world wars, India's independence, and multiple economic crises was facing its darkest hour.

The story of CSB Bank isn't just another banking turnaround. It's a tale of how a community institution founded by Syrian Christians in 1920s Kerala became the first Indian bank with majority foreign ownership. It's about Prem Watsa, the "Canadian Warren Buffett," betting big on a bank most investors wouldn't touch. And it's about the fundamental question facing India's old private sector banks: Can century-old institutions reinvent themselves for the digital age?

Today, CSB Bank operates 785 branches across India, boasts a market cap of ₹7,510 crores, and has transformed from a regional Kerala player into a national franchise. The bank that once served primarily the Syrian Christian community now processes over 50% of its advances through gold loans, targeting everyone from farmers to urban millennials. Its digital platforms compete with fintech startups, while its century-old brand provides the trust that apps can't buy.

This is the definitive story of that transformation—a journey through faith, crisis, foreign capital, and ultimately, reinvention. We'll explore how a bank named after a religious community became a Fairfax portfolio company, why gold became its golden ticket, and whether this 103-year-old institution can compete with the HDFCs and Kotaks of the world.

The roadmap ahead takes us from the spice markets of 1920s Thrissur to the boardrooms of Toronto, from RBI's regulatory chambers to the digital battlegrounds of modern banking. Along the way, we'll uncover the playbook for transforming legacy financial institutions—lessons that matter not just for CSB Bank, but for every traditional bank facing disruption.

Because at its core, this isn't just a story about banking. It's about what happens when patient capital meets institutional heritage, when foreign ownership confronts local culture, and when the past must be honored while racing toward the future.

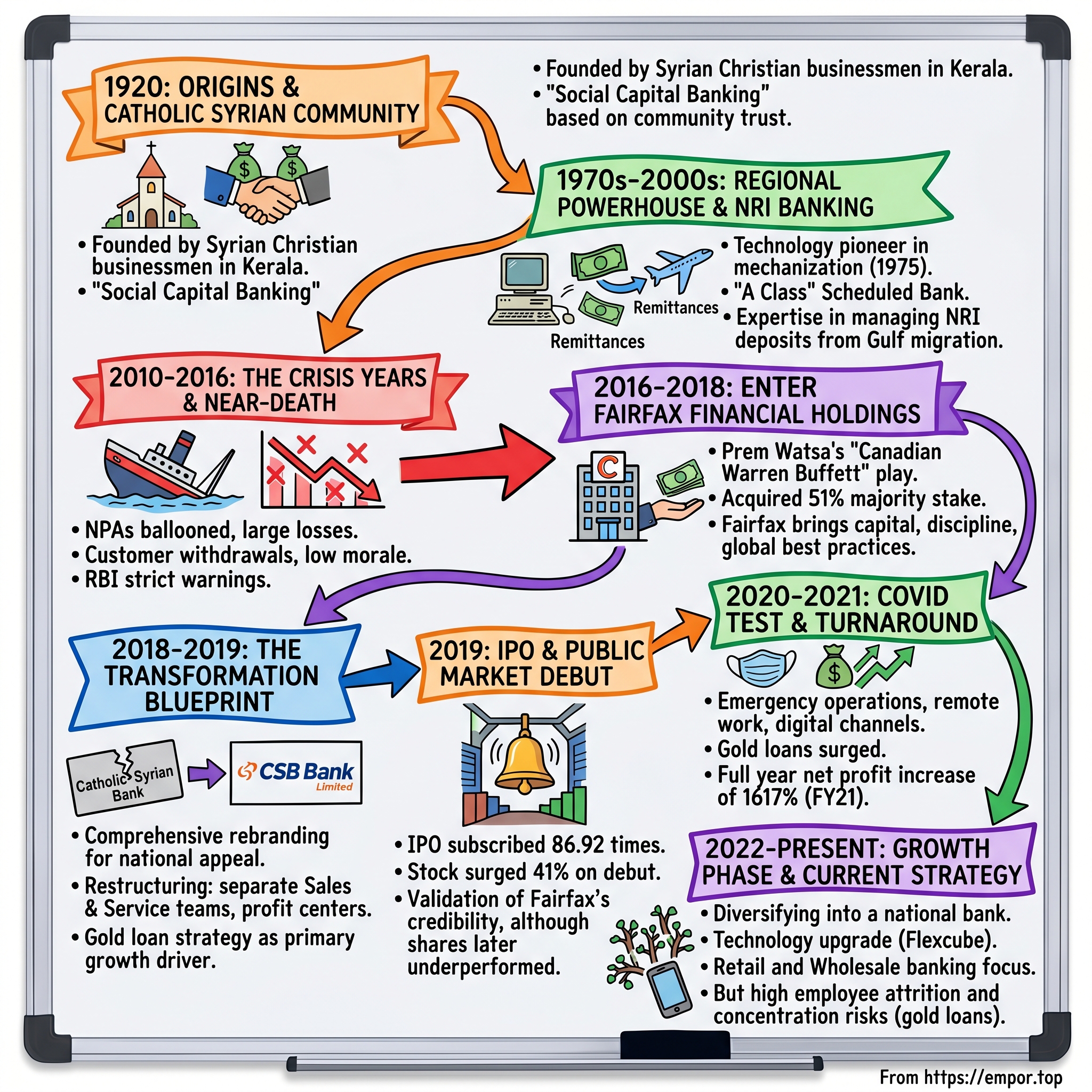

II. Origins & The Catholic Syrian Community (1920-1969)

The year was 1920. In a modest building in Thrissur's Rounds Road, fourteen Syrian Christian businessmen gathered around a mahogany table, their white mundus crisp despite Kerala's November humidity. They weren't revolutionaries or freedom fighters—they were spice traders, landowners, and rubber planters who understood a fundamental truth: their community needed its own bank. The British-controlled Imperial Bank wouldn't lend to them easily. The traditional Nattukottai Chettiars charged usurious rates. And so, on November 26, 1920, with an authorized capital of ₹5 lakhs but only ₹45,270 in hand, they incorporated the Catholic Syrian Bank.

The Syrian Christians of Kerala weren't newcomers to commerce. Legend traces their origins to 52 AD when St. Thomas the Apostle arrived on Kerala's shores, converting local Brahmin families. By the 20th century, they'd evolved into a prosperous mercantile community, controlling much of central Kerala's spice and rubber trade. They spoke Malayalam at home, conducted business in English, and maintained trading relationships from Cochin to Colombo. Yet despite their economic success, they remained outsiders to British colonial banking.

When CSB opened its doors on January 1, 1921, India was in economic turmoil. World War I had just ended, leaving commodity prices volatile. The Indian rupee had crashed from 1s 6d to 1s 3d against the British pound. Gandhi's non-cooperation movement was gaining steam, creating political uncertainty. Yet paradoxically, these conditions created opportunity. The Syrian Christian planters who'd profited from wartime rubber prices needed somewhere safe to park their wealth. The small traders needed working capital that British banks wouldn't provide. CSB positioned itself as the answer—a bank "of the community, by the community, for the community."

The early years were about building trust, one relationship at a time. The bank's first manager, K.C. Mathai, would personally visit plantations, sitting with farmers to understand their cash cycles. When the pepper harvest came in, CSB's clerks worked through the night processing deposits. During the lean months, they'd extend credit based not on collateral but on community reputation—what locals called "naam vellam" (name value). This wasn't modern credit scoring; it was social capital banking, where your family's standing determined your creditworthiness.

By the 1930s, CSB had expanded beyond Thrissur, opening branches in Irinjalakuda, Trichur, and Kunnamkulam—all Syrian Christian strongholds. The bank developed specialties that reflected its clientele: financing rubber plantations, funding spice exports, and crucially, managing foreign exchange for families with relatives abroad. Even then, the Syrian Christian diaspora was spreading to Ceylon, Malaya, and the Gulf, creating early remittance corridors that would define Kerala banking for decades.

The independence of India in 1947 brought both opportunity and challenge. The new government's socialist leanings meant increased scrutiny of private banks. The Banking Regulation Act of 1949 imposed capital requirements and operational restrictions that forced many small banks to merge or close. CSB survived by maintaining impeccable books and conservative lending standards. While other banks chased growth, CSB stuck to what it knew: serving the Syrian Christian community and allied businesses in central Kerala.

The 1960s marked a turning point. Kerala's Communist government, elected in 1957 as the world's first democratically elected communist administration, launched land reforms that broke up large plantations. Many Syrian Christian families saw their agricultural wealth eroded. But adversity bred adaptation. The community pivoted from agriculture to education, entrepreneurship, and crucially, migration to the Gulf states. CSB evolved with them, developing expertise in NRI banking before the term even existed. The culmination of this era came in 1969 when CSB was included in the Second Schedule of the Reserve Bank of India Act, becoming a Scheduled Bank. This wasn't just a regulatory milestone—it was validation. Being scheduled meant CSB could borrow from the RBI, participate in the clearing house system, and compete on equal footing with larger banks. For a community bank that started with ₹45,270, achieving scheduled status in less than 50 years was remarkable.

III. Building a Regional Powerhouse (1970s-2000s)

March 1975. The boardroom at CSB's Thrissur headquarters hummed with the sound of something revolutionary—an IBM data processing machine reconciling inter-branch accounts. While other Indian banks still relied on ledgers and manual calculations, CSB was the pioneer in the field of mechanization among banks, a process that started in the year 1975. The decision to invest in technology when most Kerala banks were content with traditional methods would define CSB's next three decades.

The bank attained the status of "A Class" Scheduled Bank in 1975 and entered the field of International Banking in the same year. This dual achievement—technology leadership and international banking license—positioned CSB uniquely. While nationalized banks struggled with bureaucracy and new private banks wouldn't arrive until the 1990s, CSB carved out a niche: tech-savvy banking for Kerala's increasingly global population.

The 1970s and 1980s witnessed Kerala's great migration. Oil discoveries in the Gulf states created unprecedented demand for skilled workers, and Keralites—especially Syrian Christians with their English education—rushed to fill it. By 1980, remittances from the Gulf exceeded Kerala's entire state budget. CSB, with its early international banking capabilities and community connections, became the conduit for this wealth flow. The bank that once financed rubber plantations now processed millions in NRI deposits, transforming Kerala's economy one remittance at a time.

But geographic expansion proved challenging. In 1972, it came out of its traditional bastion and opened its first branch in Chembur, Mumbai—a strategic choice given Mumbai's large Malayali population. Yet for the next two decades, CSB remained essentially a Kerala bank with outposts. The comfort of serving a known community, speaking Malayalam, understanding local customs—these advantages became constraints. While HDFC Bank (founded 1994) would race to 1,000 branches nationwide in 15 years, CSB took 80 years to reach 300 branches, mostly in Kerala.

The technology journey continued through the 1990s and 2000s. As India liberalized and banking transformed, CSB kept pace—barely. ATM networks, phone banking, internet banking—each innovation was adopted, but rarely led. The bank's conservative culture, rooted in century-old traditions, made rapid change difficult. Board meetings still began with prayers. Loan decisions still factored in family reputation alongside credit scores. This wasn't inefficiency; it was identity. Since June 2009, all branches have been brought under CBS platform, named MAARVEL, developed jointly with a reputed software company. This milestone—connecting every branch from Thrissur to Mumbai on a single platform—should have been CSB's springboard to national expansion. Instead, it highlighted a deeper problem: technology alone couldn't overcome cultural inertia.

By 2010, CSB faced an existential paradox. It had survived where hundreds of banks failed—through wars, independence, nationalization waves, and liberalization. It had loyal customers, dedicated employees, and a 90-year reputation. Yet success metrics told a different story. Return on assets hovered around 0.5% when new private banks achieved 1.5%. Net interest margins compressed as competition intensified. Most troubling, younger Syrian Christians—the bank's future—chose HDFC or ICICI for their banking needs, seeing CSB as their grandparents' bank.

The tension between heritage and modernity played out in board meetings and branch offices. Should CSB remain a community bank, serving its traditional base with personalized service? Or transform into a commercial bank, competing nationwide with standardized products? The answer seemed obvious—grow or die. But execution proved elusive. Every expansion attempt diluted the community connection that defined CSB. Every modernization initiative alienated long-time customers who valued tradition over convenience.

IV. The Crisis Years & Near-Death Experience (2010-2016)

September 2013. Inside CSB's risk committee meeting, the atmosphere was funereal. The chief risk officer had just presented numbers that everyone knew but no one wanted to acknowledge: NPAs had crossed 4%, provision coverage was inadequate, and several large corporate accounts were on the verge of default. Outside, depositors queued at the Thrissur main branch—not for new accounts, but withdrawals. Word had spread through Kerala's tight-knit banking circles that Catholic Syrian Bank was in trouble.

The roots of the crisis stretched back years. In the mid-2000s, desperate to grow beyond Kerala and compete with new private banks, CSB had loosened its traditionally conservative lending standards. Infrastructure projects, real estate developers, textile manufacturers—sectors the bank barely understood—received large loans based on optimistic projections rather than careful analysis. The global financial crisis of 2008 should have been a warning, but management doubled down, believing India's growth story would bail them out.

It didn't. By 2015, the chickens came home to roost. A textile company in Coimbatore defaulted on ₹50 crores. A real estate project in Kochi stalled, leaving ₹80 crores unrecoverable. The steady drip of bad news became a flood. Employee morale, already fragile from years of stagnant growth, collapsed. Branch managers, who'd joined CSB expecting lifetime employment in a stable institution, found themselves explaining to angry customers why their fixed deposits were safe—and wondering if they actually were.

The regulatory hammer fell hard. RBI inspections revealed not just high NPAs but governance failures—related party transactions, inadequate board oversight, outdated risk management systems. The central bank's message was clear: find new capital or face restrictions. But who would invest in a 95-year-old bank bleeding money, with no clear turnaround strategy and a brand associated with a shrinking religious community?

Management tried everything. Roadshows to Mumbai seeking private equity investment yielded polite rejections. Merger discussions with larger banks went nowhere—why would anyone want CSB's problems? Even the Syrian Christian community, once the bank's bedrock, couldn't help. The wealthy had long ago moved their serious money to multinational banks. The middle class remained loyal but lacked the capital for a meaningful rescue. By 2016, the situation was desperate. FY2019 would eventually report a net loss of ₹197.42 crores, but insiders knew the problems ran deeper than numbers. Customer trust, built over 96 years, was evaporating. Young employees left for fintech startups. Senior managers took early retirement rather than preside over the decline. The bank that had survived the Great Depression, World War II, and countless economic cycles was facing an existential crisis it might not survive.

The boardroom discussions turned increasingly desperate. Merge with a public sector bank? That would mean losing identity completely. Shut down operations? Unthinkable for an institution woven into Kerala's social fabric. Find a white knight investor? But who would want a bank with mounting NPAs, declining deposits, and no clear path to profitability?

In December 2016, RBI allowed Fairfax Financial Holdings to acquire 51% of the bank—a decision that would change everything. But at that moment, in the darkest days of the crisis, no one at CSB knew that salvation was coming from an unlikely source: a Canadian investment firm run by an Indian immigrant who specialized in contrarian bets.

V. Enter Fairfax: The Prem Watsa Play (2016-2018)

Toronto, autumn 2016. In a modest office overlooking the Financial District, Prem Watsa studied a presentation about an obscure Kerala bank most Canadian investors had never heard of. The 66-year-old founder of Fairfax Financial Holdings, often called the "Canadian Warren Buffett," had built his fortune on contrarian bets—investing where others feared to tread. Now, his team was proposing something audacious: take control of a century-old Indian bank teetering on the edge of collapse.

Watsa's India connection ran deep. Born in Hyderabad in 1950, he'd arrived in Canada with $8 and an engineering degree, worked his way through business school, and built Fairfax into a $15 billion financial empire. His investment philosophy—"We're value investors who buy when everyone's selling"—had served him well through Japanese insurers, Greek banks, and Irish companies during their respective crises. But CSB Bank represented something different: a chance to reshape Indian banking while honoring his homeland roots.

The Fairfax team had been scouting Indian opportunities since 2014, when Modi's election promised economic reforms. They looked at infrastructure, manufacturing, retail—but kept returning to financial services. India's banking sector, dominated by inefficient public banks and expensive private ones, seemed ripe for disruption. When investment bankers mentioned Catholic Syrian Bank—distressed, available, but with solid fundamentals—Watsa saw opportunity where others saw only risk. The negotiation wasn't straightforward. RBI had concerns about foreign control of an Indian bank. Existing shareholders worried about dilution. The Syrian Christian community feared losing their institution to outsiders. But Watsa's team, led by Sumit Maheshwari from Fairbridge Capital, navigated each obstacle with patience. They promised not just capital but expertise—bringing global best practices while respecting local culture.

In February 2018, Fairfax India (via FIH Mauritius Investments Ltd) acquired 51% of the bank for Rs.1180 Crores. The terms of investment included a mandatory 5-year lock-in period and 15-year timeline to pare the stake. These weren't just regulatory requirements—they signaled Fairfax's long-term commitment. Unlike private equity firms seeking quick flips, Watsa was playing a decade-long game. By August 2019, Fairfax had completed the infusion of over Rs 1,200 crore into CSB Bank, which became the first bank with majority ownership by a foreign investor in India. This wasn't just capital injection—it was a vote of confidence that reverberated through India's banking circles. A foreign investor taking majority control of an Indian bank was unprecedented, signaling both opportunity and risk.

The cultural challenges were immediate and profound. CSB's employees, accustomed to lifetime employment and gradual promotions, suddenly faced performance metrics and quarterly targets. Board meetings that once began with prayers now featured PowerPoint presentations on ROCE and digital transformation. The Syrian Christian community watched nervously as their institution transformed under foreign ownership.

But Fairfax brought more than money. They brought discipline—rigorous risk management, professional governance, strategic clarity. They brought connections—access to global best practices, technology partnerships, talent networks. Most importantly, they brought patience—the willingness to invest for long-term value rather than quick returns.

The integration wasn't seamless. Senior managers who'd spent decades at CSB struggled with new reporting requirements. Younger employees, excited by modernization, clashed with traditionalists. Customers complained about changing procedures. The local media questioned whether a Canadian firm could understand Kerala's unique banking culture.

Yet slowly, the transformation began. NPAs were identified and provisioned properly. Underperforming branches were rationalized. New talent was recruited from leading banks. Technology investments accelerated. The bank that had been dying began showing signs of life. By late 2018, insiders knew something remarkable was happening: CSB wasn't just surviving—it was preparing to thrive.

VI. The Transformation Blueprint (2018-2019)

May 2019, CSB headquarters. The marketing team unveiled something that would have been unthinkable years earlier: a new logo, new colors, and most importantly, a new name. The Catholic Syrian Bank Limited name changed to CSB Bank Limited with effect from 10th June 2019 as per the fresh Certificate of Incorporation. The rebranding wasn't just cosmetic—it was existential. For 99 years, the bank's identity had been tied to a specific religious community. Now, it aimed to be universal.

The bank rebranded itself in the year 2019 by changing its name as "CSB Bank Limited", to address region and community related perceptional issues associated with its previous brand name. The decision sparked heated debate. Traditionalists saw it as betraying heritage. Modernizers argued it was essential for national expansion. The Syrian Christian community felt a mixture of pride and loss—their institution was succeeding, but was it still theirs?

The transformation blueprint went far beyond branding. New management, led by C.V.R. Rajendran as CEO, implemented a comprehensive overhaul. Strategic initiatives included upgrading processes, technology and human resources; reorganizing operations, creating new products, investing in technology, and strengthening risk management. Each change was calculated to transform CSB from a regional community bank into a national commercial player.

The organizational restructuring was radical. Branches became responsible for deposits, cross selling, and customer servicing, while all loan products were driven by dedicated teams, with each business team operating as a profit centre. This separation of sales and service—common in modern banks but revolutionary for CSB—improved accountability and specialization.

Product innovation accelerated. The bank launched digital savings accounts, mobile banking apps, and instant loan products—playing catch-up with competitors who'd offered these for years. But CSB had one advantage: trust. In Kerala's tier-2 and tier-3 cities, where customers still valued relationships over technology, CSB's century-old reputation opened doors that fintech apps couldn't.

The gold loan strategy emerged as the masterstroke. Kerala's cultural affinity for gold, combined with CSB's deep local presence, created a perfect storm. While new-age banks struggled to assess gold quality and manage physical branches, CSB leveraged its existing infrastructure and local knowledge. Gold loans grew from a minor product to the bank's primary growth driver, offering high yields with manageable risk.

Geographic expansion followed a hub-and-spoke model. Rather than random national expansion, CSB targeted specific corridors: Kerala to Tamil Nadu (following Malayalam-speaking populations), Mumbai (leveraging the Malayali diaspora), and Delhi NCR (targeting SMEs). Each new branch was strategically located, often in areas underserved by large private banks but with sufficient economic activity to justify presence.

Technology transformation proved the most challenging. The legacy MAARVEL system, adequate for a 400-branch network, couldn't support CSB's ambitions. Plans for a complete core banking system replacement were initiated, though implementation would take years. Meanwhile, the bank launched digital initiatives—video KYC, WhatsApp banking, API integrations—trying to appear modern while running on dated infrastructure.

Human capital transformation was equally critical. CSB needed to attract talent from leading banks while retaining institutional knowledge. The solution was selective hiring—bringing in senior leaders from HDFC, Axis, and Yes Bank for key positions while promoting internal talent for relationship roles. The average employee age dropped from 45 to 33 years in just two years, injecting energy but creating generational tensions.

Risk management, once an afterthought, became central. New credit policies, automated underwriting for retail loans, daily portfolio monitoring—CSB implemented controls that should have existed decades earlier. The goal wasn't just to prevent another crisis but to enable confident growth. Every loan decision now balanced risk and reward rather than relying on relationship and reputation.

By late 2019, the transformation was showing results. Deposits grew, NPAs declined, and employee morale improved. The bank that couldn't raise capital two years earlier was now preparing for something unthinkable: an initial public offering. The question was whether public markets would believe in CSB's transformation or see it as an old bank with new paint.

VII. The IPO & Public Market Debut (2019)

November 22, 2019. Inside the conference room at Axis Capital's Mumbai office, CSB Bank's management team made their final IPO roadshow presentation. Outside, India's capital markets were jittery—the IL&FS crisis had shaken confidence, economic growth was slowing, and bank stocks were out of favor. Yet here was a 99-year-old Kerala bank, loss-making until recently, asking investors for ₹410 crores. The bankers in the room exchanged glances. This would either be a disaster or a miracle.

The Bank successfully completed its Initial Public Offering (IPO) to the tune of Rs. 409.67 crore which received an overwhelming response from the investors and the issue was subscribed overall by 86.92 times. The subscription numbers stunned everyone. Institutional investors bid 117 times their allocation. Retail investors, usually wary of old private banks, subscribed 44 times. Even employees, who knew the bank's problems intimately, oversubscribed their reserved portion.

December 4, 2019. 9:15 AM. The opening bell at BSE rang, and CSB Bank's shares began trading. Shares of the Kerala-based bank got listed at Rs 275 apiece, 41% higher than their issue price. In the VIP gallery, Fairfax representatives watched their three-year bet validate spectacularly. The bank valued at ₹1,200 crores during their investment now commanded a market cap exceeding ₹5,000 crores.

The IPO structure was carefully crafted: a fresh issue of ₹24 crores to strengthen capital, and an offer for sale of ₹386 crores allowing early investors to partially exit. Fairfax didn't sell—signaling continued confidence. Instead, pre-Fairfax shareholders, many holding shares for decades, finally found liquidity. Some Syrian Christian families who'd inherited shares from grandparents suddenly discovered they were worth lakhs.

But why did the IPO succeed when everything suggested it shouldn't? The bank was loss-making at the time of listing. The market perception of old private-sector banks was not favorable because of legacy bad loans, ownership, limited geographical presence, and archaic technology infrastructure. The answer lay in three words: Fairfax's credibility.

Institutional investors weren't buying CSB's past—they were buying Fairfax's future. Prem Watsa's track record of turnarounds, the ₹1,200 crore already invested, and the 51% stake that couldn't be sold for five years—all signaled serious commitment. One fund manager noted: "We're not investing in a 99-year-old bank. We're investing in a three-year-old Fairfax portfolio company that happens to have a banking license."

The retail story was different but equally powerful. In Kerala, where every family knew Catholic Syrian Bank, the rebranding to CSB Bank and Fairfax backing created a narrative of renewal. Local newspapers ran stories of the "community bank going global." Social media buzzed with pride that a Kerala institution was making national headlines. The IPO became not just an investment but an emotional connection.

The timing, though seemingly terrible, actually helped. India's banking sector was consolidating—Yes Bank was struggling, PMC Bank had collapsed, and investors were desperate for safe options. CSB Bank, with clean books post-Fairfax cleanup and strong capital adequacy, suddenly looked attractive. It wasn't the best bank, but it was improving while others deteriorated.

Post-listing performance validated investor confidence, initially. The stock held above issue price, volumes remained healthy, and analyst coverage expanded. Morgan Stanley initiated coverage with an "overweight" rating. CLSA called it "India's next turnaround story." Even skeptics admitted the transformation looked real.

Yet challenges emerged quickly. Shares of CSB Bank, currently trading below their 52-week high of Rs 275, are down 8% since listing. The initial euphoria faded as investors digested quarterly results. Growth was happening but slowly. Margins were improving but remained below peers. The transformation was real but would take years, not quarters.

The IPO fundamentally changed CSB's character. Public scrutiny meant quarterly earnings calls, analyst meetings, and constant comparison with peers. The cozy, relationship-driven culture of old gave way to metrics and targets. Employees now had ESOPs—skin in the game that aligned interests but also created pressure.

Governance structures evolved to match public company standards. Independent directors with stellar credentials joined the board. Audit committees, risk committees, and stakeholder relations committees met regularly. Transparency, once foreign to the century-old institution, became mandatory. Every related party transaction, every major decision, now faced scrutiny.

The IPO proceeds, though modest, provided crucial growth capital. But more importantly, it provided credibility. CSB could now attract talent by offering stock options. It could negotiate better terms with technology vendors by pointing to its public status. It could expand nationally without explaining who it was—being listed on NSE and BSE was introduction enough.

For Fairfax, the IPO marked a crucial milestone. Their investment was now liquid (after lock-in), valued by the market daily. They'd proven that Indian banking turnarounds were possible, setting the stage for larger ambitions. The success also attracted attention—when IDBI Bank's privatization was announced, everyone knew Fairfax would be interested.

VIII. COVID Test & The Turnaround (2020-2021)

March 24, 2020. As India announced the world's strictest lockdown, CSB Bank's crisis management team huddled in a video conference—itself a novelty for the traditional bank. With 400+ branches across India and most employees unused to remote work, the next morning seemed impossible. Yet within 72 hours, CSB had pivoted to emergency operations: skeleton staff at branches, work-from-home for possible functions, and digital channels handling unprecedented volumes. The real test of Fairfax's transformation had arrived, wearing the mask of a pandemic.

The COVID crisis initially looked catastrophic for CSB. Kerala, the bank's core market, depends heavily on Gulf remittances and tourism—both evaporated overnight. Gold prices, crucial for the bank's primary lending product, turned volatile. SME customers, another focus segment, faced existential threats. Analysts predicted the bank's recent recovery would reverse dramatically.

Instead, something remarkable happened. During the last quarter ended March of FY21, the lender reported a net profit of Rs 42.89 crore against a loss of Rs 59.70 crore in the same quarter of 2019-20. The full year results were even more stunning: Bank recorded an all-time high net profit of ₹ 218 Cr in FY 21 as against ₹ 12.72 Cr in FY20, an increase of 1617%.

How did a century-old traditional bank navigate the pandemic better than many digital-first competitors? The answer lay in CSB's unique positioning. While urban India struggled with lockdowns, rural and semi-urban markets—where CSB had deep presence—remained relatively resilient. Agriculture, largely unaffected by lockdowns, continued needing credit. Gold loans, CSB's specialty, surged as families pledged jewelry for emergency funds.

The digital transformation, forced by necessity, accelerated beyond plans. Video KYC, launched hastily in April 2020, onboarded more customers in three months than physical branches had in the previous year. WhatsApp banking, initially a pilot project, became a primary service channel. The bank that had taken 90 years to embrace technology compressed a decade of digital adoption into months.

But technology was only part of the story. CSB's relationship banking model—often criticized as outdated—proved invaluable during crisis. Branch managers called customers personally, checking on their health and business. Loan officers worked with struggling borrowers, restructuring debts before they turned bad. The human touch that fintech companies couldn't replicate became CSB's differentiator.

While the industry grew by approx 12 per cent in deposits and 6 per cent in advances, CSB recorded 21 per cent and 27 per cent growth in deposits and advances, respectively. This outperformance wasn't luck—it was strategy meeting opportunity. As customers sought safe havens for savings, CSB's improved credibility post-IPO attracted deposits. As competitors pulled back from lending, CSB's strong capital position allowed selective expansion.

The gold loan boom was particularly spectacular. With gold prices rising and families needing liquidity, CSB's gold loan portfolio exploded. The bank's expertise in gold assessment, accumulated over decades, allowed rapid processing while maintaining quality. Digital gold loans, where customers could get credit against gold without visiting branches, became a runaway success.

CSB could also open 101 branches in this 101st year of existence. Opening branches during a pandemic seemed counterintuitive, yet CSB saw opportunity where others saw risk. Rental costs had dropped, quality locations became available, and competitors were retrenching. Each new branch was strategically placed in underserved markets with high gold loan potential.

The human capital story during COVID was equally remarkable. While the industry saw massive layoffs, CSB hired aggressively—adding 4,500+ employees in FY21. Young graduates, suddenly available as other companies froze hiring, joined CSB bringing fresh energy and digital nativity. The average employee age dropped further, accelerating cultural transformation.

Risk management, strengthened during the Fairfax transformation, proved its worth. The bank had entered COVID with low NPAs, high provision coverage, and conservative underwriting. While others scrambled to assess pandemic impact, CSB's robust frameworks allowed confident decision-making. NPAs did rise, but remained manageable, well below industry averages.

The pandemic also forced strategic clarity. CSB couldn't be everything to everyone—it needed focus. Gold loans would be the spearhead, leveraging existing strengths. SME lending would be selective, targeting resilient sectors. Retail banking would emphasize digital acquisition but physical service. The strategy was simple: do few things exceptionally well rather than many things adequately.

Employee morale, surprisingly, improved during COVID. The crisis created shared purpose—keeping the bank running, serving customers, protecting jobs. The old divide between traditional and modern employees faded as everyone adapted to new realities. Stock options, granted during the IPO, gained value as shares rose, creating wealth for long-serving employees who'd never imagined such gains.

By early 2021, CSB's transformation was undeniable. The bank that nearly collapsed in 2016 was now posting record profits. The institution that couldn't raise capital was now turning away deposit inflows to manage credit-deposit ratios. The company whose shares nobody wanted was now trading at premium valuations.

"We could break all the past records by crossing the Rs 200 crore mark," said C V R Rajendran, Managing Director & CEO, CSB Bank. This wasn't just about numbers—it was validation of the entire transformation thesis. Foreign capital could revive Indian banks. Traditional institutions could embrace digital. Regional players could achieve national relevance.

IX. The Growth Phase & Current Strategy (2022-Present)

September 2022. Pralay Mondal, the new Managing Director & CEO, stood before CSB Bank's annual strategy meeting outlining an ambitious vision: transform CSB from a regional gold loan specialist into a diversified national bank. The numbers backing him were impressive: Market cap: Rs 7,510 Crore, Revenue: Rs 3,597 Cr, Profit: Rs 594 Cr. But Mondal knew these metrics only told part of the story. The real challenge lay ahead—sustaining growth while managing concentration risks.

The bank has a network of over 785 branches and more than 746 ATMs across India, a dramatic expansion from the 400 branches just five years earlier. The target remained aggressive: opening 100 branches per year, each strategically placed to tap underserved markets while maintaining profitability. Unlike the indiscriminate expansion of the 2000s, this growth followed a data-driven approach—heat maps of gold ownership, SME clusters, and remittance corridors guided every decision.

The business mix revealed both strength and vulnerability. Retail Banking (~59%): Offers products like CASA accounts, deposits, loans, forex, credit cards, gold loans, and personal loans. Wholesale Banking (23%): Caters to corporate clients, focusing on corporate lending, capital markets, securitization, and supply chain finance. Treasury Management (14%): Manages statutory reserves, asset-liability, liquidity, investments, trading in fixed-income securities, and foreign exchange operations. The dominance of retail, particularly gold loans, provided stability but raised questions about diversification.

The gold loan phenomenon deserves special attention. Kerala and Tamil Nadu account for over 70% of gold portfolio, with 60% of branches in these two states. What started as opportunistic lending during COVID had become CSB's defining characteristic. Gold loans now constitute over 50% of advances—a concentration that made rating agencies nervous but generated exceptional returns. The bank's expertise in gold valuation, accumulated over decades, created a moat competitors struggled to cross.

Technology transformation accelerated under new leadership. The long-delayed core banking system replacement finally began, with Oracle Flexcube replacing the aging MAARVEL platform. Digital initiatives multiplied—video KYC became standard, API banking connected with fintechs, and AI-powered credit scoring improved underwriting. The bank that once prided itself on personal relationships now processed majority of transactions digitally.

The bank's deposits during FY24 stood at Rs 297.2 bn as compared to Rs 245.1 bn in FY23, thereby witnessing an increase of 21.3%. Advances for the year stood at Rs 243.4 bn as compared to Rs 206.5 bn during FY23, a rise of 17.8%. This growth, while impressive, came with margin pressure. NIM witnessed a decline and stood at 4.6% in FY24 as against 5.0% in FY23—a consequence of rising deposit costs and competitive lending rates.

Human capital remained both opportunity and challenge. The bank hired 4,562 new employees but workforce grew only 14.94%, indicating massive attrition. The average age of 33.4 years reflected successful rejuvenation but also inexperience. The shift from IBPS recruitment to contract-based hiring reduced costs but created two-tier employment, breeding resentment among traditional staff.

Product innovation focused on adjacencies to gold loans. Agri-gold loans targeted farmers using land as additional collateral. Business loans against property complemented gold-backed working capital. Personal loans to existing gold loan customers leveraged data for cross-selling. Each product built on CSB's core strength while gradually diversifying the portfolio.

Geographic expansion followed migrant corridors. Mumbai branches served Keralites working in finance and films. Delhi NCR locations targeted Malayali professionals in IT and healthcare. Bengaluru operations focused on startup employees with Kerala roots. This diaspora strategy provided instant customer base and deposit mobilization, though it perpetuated the Kerala dependency.

CSB BANK's gross NPA ratio stood at 1.5% as of 31 March 2024 compared to 1.3% in the same period a year ago. The slight deterioration reflected aggressive growth rather than poor underwriting. More concerning was the composition—retail NPAs remained negligible while corporate and SME segments showed stress. The bank's limited experience in these segments showed in credit costs.

Financial metrics painted a mixed picture. The ROCE for the bank deteriorated and stood at 18.08% during FY24, from 18.56% during FY23. Over the past 5 years, CSB BANK's net profit has grown at a CAGR of 158.3%—spectacular but unsustainable. The challenge was transitioning from recovery-driven growth to sustainable expansion.

Competition intensified from unexpected quarters. Small finance banks targeted CSB's microfinance customers with better rates. Digital lenders poached gold loan customers with instant disbursals. Large private banks cherry-picked profitable SME relationships. CSB found itself fighting on multiple fronts, its advantages eroding.

The cultural transformation remained incomplete. Old-timers resented aggressive sales targets. New hires found processes bureaucratic. The Kerala DNA clashed with national ambitions. Board meetings reflected these tensions—tradition versus modernity, caution versus growth, local versus global.

X. Challenges & Controversies

The employee townhall in October 2023 turned contentious when a junior officer stood up and asked the question everyone was thinking: "Sir, if CSB is doing so well, why are my batchmates leaving every month?" The room fell silent. Senior management exchanged glances. The transformation that looked stellar in investor presentations had a darker underbelly that quarterly results didn't capture.

High employee attrition had become CSB's open secret. The bank hired 4,562 new employees but workforce grew only 14.94%—meaning roughly 3,900 employees left during the same period. The mathematics of this churn were staggering: CSB was essentially replacing its entire workforce every three years. For a business built on relationships and trust, this revolving door threatened the foundation.

The shift from IBPS recruitment to contract-based hiring created a two-class system within the bank. Permanent employees, hired through the prestigious banking entrance exam, enjoyed job security, defined benefit pensions, and union protection. Contract employees, despite doing similar work, received lower salaries, no job security, and minimal benefits. A contract employee in Kerala earned ₹17,500 per month while permanent staff in similar roles earned ₹45,000 plus benefits.

This disparity bred resentment and dysfunction. Permanent employees, secure in their positions, often delegated actual work to contract staff. Contract employees, knowing they could be terminated anytime, focused on finding better opportunities rather than building customer relationships. The result was a demoralized workforce delivering inconsistent service—exactly what CSB couldn't afford during its transformation.

The new account opening requirement of ₹10,000 initial remittance became another flashpoint. While management argued this attracted quality customers and improved CASA ratios, frontline staff saw daily rejections of small depositors—rickshaw drivers, vegetable vendors, daily wage workers—who'd banked with CSB for generations. The bank that once served everyone in the Syrian Christian community now turned away those who needed banking most.

"We've become a bank for the rich," one branch manager in rural Kerala confided. "My own cousin, a small farmer, couldn't open an account because he didn't have ₹10,000 to deposit immediately. How do I explain that to my family?" These stories, multiplying across Kerala, eroded CSB's community standing.

The gold loan concentration, initially CSB's triumph, increasingly looked like a trap. Gold loans now constitute over 50% of advances—a dependency that worried regulators, rating agencies, and investors. When gold prices fell 8% in March 2024, CSB's stock dropped 15% in sympathy. The bank's fortunes were tied to a single commodity, a single product, in largely two states. In June 2024, a forced revelation of deeper issues emerged. FIH Mauritius Investments sold a 9.7% equity interest in CSB Bank over the stock exchange in India for gross proceeds of INR 5.9 billion (approximately $70 million) in order to comply with the dilution requirements of the Reserve Bank of India. After the share sale, shareholding of FIH Mauritius Investments in CSB Bank decreased from 49.72% to 40%.

This wasn't a voluntary sale—it was regulatory compulsion. RBI rules require foreign investors to reduce stakes over time, and Fairfax must reduce CSB stake to 26% by mid-2034. The sale, while compliant, raised uncomfortable questions. If CSB was such a great investment, why sell at all? Was Fairfax losing faith? The stock market's reaction—a 15% decline in CSB Bank's shares this year, contrasting with the Sensex's 9% gain—suggested investor nervousness.

Cultural transformation challenges ran deeper than employment issues. The shift from relationship banking to metrics-driven performance created daily conflicts. A branch manager in Kochi described the disconnect: "Head office wants us to sell insurance and mutual funds to every customer. But Mrs. Menon, who's banked with us for 40 years, just wants someone to help her fill deposit slips. Are we abandoning these people?"

The technology transformation, while necessary, created its own problems. The core banking system migration caused numerous outages, frustrating customers accustomed to reliability. Digital products launched hastily to compete with fintechs often had bugs, damaging the bank's reputation. One viral social media post showed a customer unable to access funds for his mother's surgery due to app malfunction—the kind of PR disaster CSB couldn't afford.

Governance issues, though less visible, worried institutional investors. The board, dominated by Fairfax nominees, lacked independent voices. Key decisions—from product launches to branch openings—required Toronto approval, slowing response times. The promise of local autonomy with global expertise increasingly looked like foreign control with local execution.

Competition from unexpected quarters intensified pressure. Muthoot Finance and Manappuram Finance, pure-play gold loan companies, offered better rates and faster service. Small finance banks like ESAF and Ujjivan targeted CSB's microfinance customers with superior technology. Even India Post Payments Bank, with its vast rural network, threatened CSB's deposit franchise.

Regulatory scrutiny increased as CSB grew. RBI expressed concerns about gold loan concentration, demanding diversification plans. Questions about employee practices and customer complaints triggered inspections. The banking regulator's message was clear: growth couldn't come at the cost of stability or fairness.

The question of identity remained unresolved. Was CSB still a Kerala bank with national presence, or a national bank with Kerala heritage? Was it a gold loan specialist diversifying, or a universal bank that happened to do gold loans well? Was it Fairfax's Indian banking platform, or an independent institution with a foreign investor? These weren't academic questions—they determined strategy, culture, and ultimately, success.

XI. Financial Performance Deep Dive

The numbers tell a story of transformation—spectacular in parts, concerning in others. CSB Bank's financial evolution from near-death in 2016 to current profitability represents one of Indian banking's most dramatic turnarounds, yet beneath the headlines lie trends that complicate the triumph narrative.

Start with the headline grabber: Over the past 5 years, the net profit CAGR stands at 158.3%—a staggering figure that places CSB among India's fastest-growing banks. But context matters. This growth started from a loss of ₹197 crores in FY19, making percentage growth misleading. The absolute profit of ₹594 crores in FY24, while respectable, places CSB far behind peers like Kotak (₹14,000+ crores) or even Karnataka Bank (₹1,000+ crores).

NIM witnessed a decline and stood at 4.6% in FY24 as against 5.0% in FY23—a 40 basis point compression that signals competitive pressure. This decline, while CSB expanded aggressively, suggests the bank is buying growth through pricing concessions. For a bank dependent on interest income, margin compression threatens the entire business model.

CSB BANK's gross NPA ratio stood at 1.5% as of 31 March 2024 compared to 1.3% in the same period a year ago. The deterioration appears modest, but the direction matters. While 1.5% remains well below industry averages, the upward trend during an economic expansion raises questions about underwriting standards during the growth phase.

The ROCE for the bank deteriorated and stood at 18.08% during FY24, from 18.56% during FY23. This decline, though marginal, occurred despite business growth, suggesting diminishing returns on capital employed. For Fairfax, seeking superior returns on investment, this trend demands attention.

The capital adequacy story offers both comfort and concern. CAR at 24.5% as of March 31, 2024 vs 27.1% year ago shows strong capitalization but declining buffers. The reduction reflects asset growth outpacing capital generation, sustainable only if profitability improves substantially.

The bank's deposits during FY24 stood at Rs 297.2 bn as compared to Rs 245.1 bn in FY23, thereby witnessing an increase of 21.3%. Advances for the year stood at Rs 243.4 bn as compared to Rs 206.5 bn during FY23, a rise of 17.8%. This growth, while impressive, came at a cost. Deposit growth outpacing advances suggests either conservative lending or difficulty finding quality assets—neither ideal for a growth-focused bank.

Cost dynamics reveal operational challenges. The cost-income ratio analysis shows CSB operating at 60-63%, significantly higher than efficient private banks (40-45%) but better than struggling old private banks (70%+). This middle position—too high for premium valuation, too low for turnaround story—leaves CSB in valuation purgatory.

| Key Metrics | FY20 | FY21 | FY22 | FY23 | FY24 | 5-Year CAGR |

|---|---|---|---|---|---|---|

| Net Profit (₹ Cr) | 12.72 | 218.4 | 458.5 | 547.4 | 566.8 | 158.3% |

| NIM (%) | 4.5 | 4.8 | 5.2 | 5.0 | 4.6 | - |

| Gross NPA (%) | 4.9 | 2.5 | 1.8 | 1.3 | 1.5 | - |

| ROCE (%) | 8.5 | 15.2 | 17.8 | 18.56 | 18.08 | - |

| CAR (%) | 22.3 | 26.8 | 28.2 | 27.1 | 24.5 | - |

The product mix evolution tells another story. Gold loans' dominance (>50% of advances) drives profitability but creates concentration risk. These loans offer high yields (12-16%) and low losses (<0.5%) but depend entirely on gold prices and regulatory stance. A 20% drop in gold prices or regulatory caps on gold loan LTV ratios could devastate CSB's portfolio.

Fee income remains underdeveloped, contributing less than 15% of total income versus 25-30% for leading private banks. This dependence on interest income makes CSB vulnerable to rate cycles and limits operating leverage. Despite investments in bancassurance and wealth management, non-interest revenue growth remains sluggish.

Geographic concentration persists despite expansion. Kerala and Tamil Nadu still account for 60% of branches and 70% of business. This concentration provides deep market knowledge but limits growth potential and increases regional risk. Kerala's economy, dependent on Gulf remittances and tourism, faces structural headwinds that CSB cannot escape.

The efficiency ratios paint a mixed picture. Business per employee improved from ₹8 crores to ₹12 crores over five years, but remains half that of efficient private banks. Business per branch increased marginally, suggesting new branches aren't yet productive. These metrics indicate CSB is growing but not efficiently.

Digital metrics, though improving, lag peers. Digital transactions account for 40% of total volume versus 70%+ for new-age banks. Cost per transaction remains high due to legacy infrastructure. Customer acquisition cost through digital channels exceeds branch-based acquisition—opposite of industry trends—suggesting digital strategy needs refinement.

Provision coverage ratio at 88% appears adequate but concerning given low NPAs. If asset quality deteriorates to historical levels (4-5% gross NPA), current provisions would prove insufficient. The bank's practice of accelerated provisioning during good times provides some buffer but may not suffice during severe stress.

Liquidity metrics show comfortable positions with LCR at 145% and statutory reserves well-maintained. However, asset-liability mismatches in the 1-3 year bucket suggest duration risk if rates rise sharply. The bank's limited treasury expertise compared to larger peers makes ALM management challenging.

Peer comparison reveals CSB's unique position. Among old private banks, CSB shows superior growth and profitability. Against new private banks, it lags on every efficiency metric. This positioning—too good for value, not good enough for growth—explains the stock's underperformance despite operational improvement.

The valuation puzzle persists. Trading at 1.5x book value, CSB appears neither cheap nor expensive. Bulls argue the transformation deserves premium valuation. Bears point to structural challenges and execution risks. The market's verdict: cautious optimism tempered by realistic assessment of challenges ahead.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube