Crompton Greaves Consumer Electricals: From Industrial Legacy to Consumer Champion

I. Cold Open & Hook

Picture this paradox: A company commanding 26% market share in India's fans business—the clear market leader by volume—yet consistently ranking third in brand perception and second in distribution reach. How does the market leader become the perennial underdog in its own success story?

In 2015, Crompton Greaves stood at an inflection point that would define not just its future, but offer a masterclass in corporate transformation. Here was an 80-year-old industrial behemoth, built on the backbone of India's infrastructure—transformers humming in power plants, motors driving factories—suddenly betting everything on ceiling fans and LED bulbs. The audacity of the pivot was matched only by its improbability.

The numbers today tell a story of vindication: ₹20,436 crore market capitalization, ₹7,724 crore in revenue, ₹536 crore in profits. But these figures obscure the drama—a demerger that split an empire, private equity players who saw gold where others saw rust, a failed merger that shocked the street, and finally, a reinvention so complete they branded it "Crompton 2.0."

This is the story of how an industrial giant shed its skin to become a consumer champion. It's a tale of timing, transformation, and the peculiar dynamics of Indian consumer markets where brand heritage can be both your greatest asset and your heaviest burden. Along the way, we'll unpack the playbook that turned a neglected division into a standalone powerhouse, examine why a seemingly perfect acquisition went spectacularly wrong, and understand what it really takes to build a consumer business from industrial DNA.

The journey from Colonel Crompton's electrical experiments in 1878 to today's smart home aspirations spans three centuries, multiple continents, and countless reinventions. But the most dramatic transformation happened in just the last decade—a compressed timeline of corporate evolution that offers lessons for any company attempting to redefine itself in rapidly changing markets.

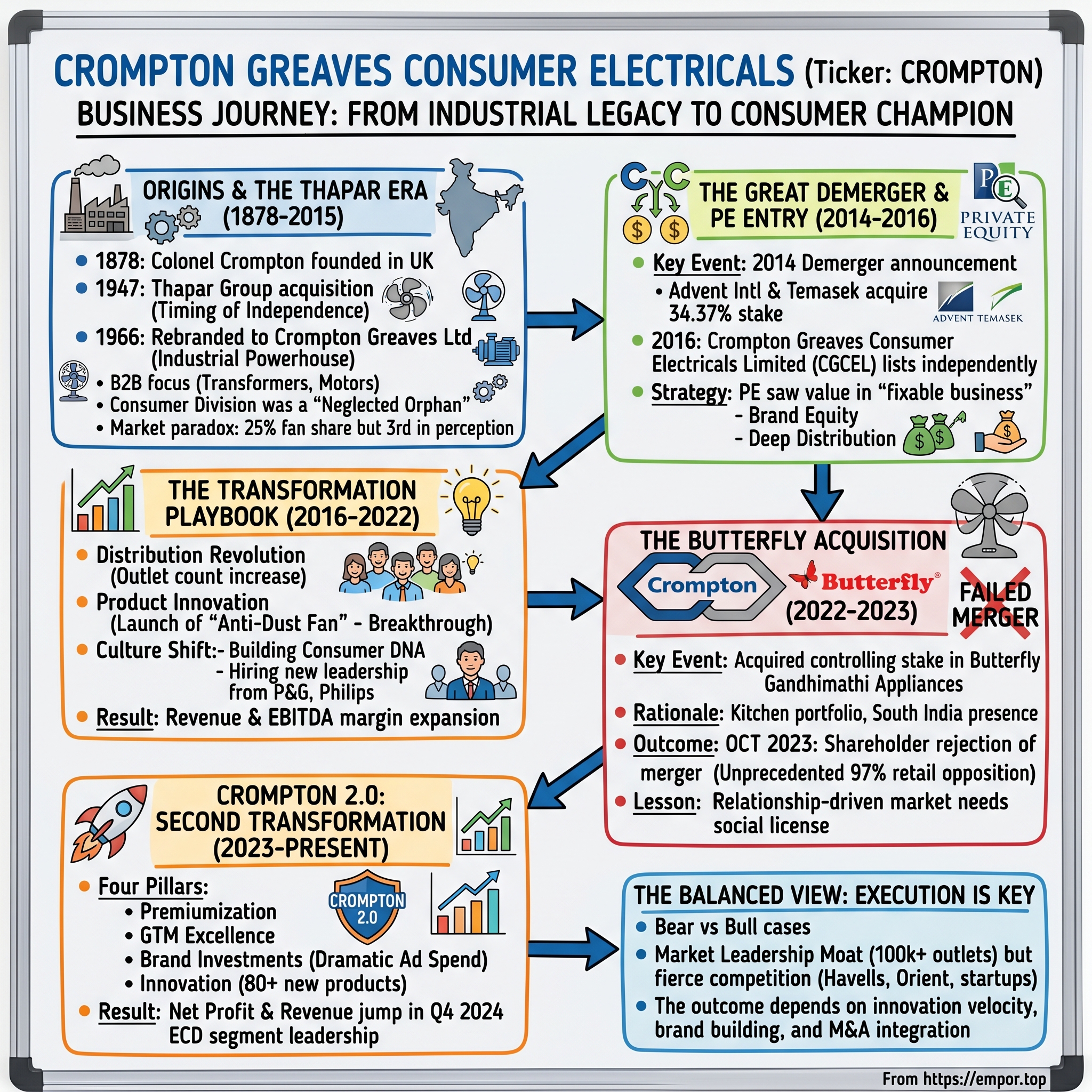

II. Origins & The Thapar Era (1878-2015)

The year is 1878. While Thomas Edison was still perfecting his incandescent bulb, Colonel R.E.B. Crompton—a British electrical engineer with a fascination for arc lighting—founded R.E.B. Crompton & Company. The Colonel wasn't just another Victorian inventor; he was an industrialist who understood that electricity's real revolution would come not from laboratory breakthroughs but from bringing power to the masses.

By 1927, Crompton's company merged with F.A. Parkinson to form Crompton Parkinson Ltd., creating one of Britain's electrical engineering powerhouses. But the real story for us begins in India, where Greaves Cotton and Company—established by James Greaves in 1859 as a trading firm dealing in cotton and engineering goods—was appointed as their concessionaire. This arrangement would eventually birth one of India's most enduring industrial brands.

The Indian entity, Crompton Parkinson Works Limited, was formally established in 1937, just as the subcontinent was stirring with independence movements and industrial ambitions. Ten years later, in 1947—the very year of India's independence—Karam Chand Thapar acquired the company. The timing was no coincidence. The Thapars, like the Birlas and Tatas, understood that political freedom would unleash economic opportunity.

Under Karam Chand Thapar's leadership, the company went public in 1960, riding the wave of Nehru's industrial policy that favored heavy engineering and infrastructure. By 1966, reflecting its evolved identity, the company changed its name to Crompton Greaves Limited. The rebranding signaled ambition—this wasn't just an Indian subsidiary anymore, but a standalone industrial force.

For the next four decades, Crompton Greaves built industrial India—literally. Their transformers powered the grid, their motors drove factories, their switchgears protected electrical systems. Walk into any major industrial facility built between 1960 and 2000, and you'd likely find Crompton equipment. The company became synonymous with electrical infrastructure, a B2B giant whose brand recognition came from engineers and procurement managers, not households.

But buried within this industrial empire was a consumer division—almost an afterthought. Fans, lights, and home appliances were side businesses, leveraging the Crompton brand but never receiving serious investment or attention. Why focus on ceiling fans when you're building transformers for nuclear power plants? This strategic neglect would prove both a curse and, paradoxically, an opportunity.

The Gautam Thapar years, beginning in the 2000s, marked a new chapter of empire building. Gautam, representing the third generation of Thapar leadership, had grand ambitions. The group expanded aggressively, particularly in paper and other businesses, funded by expensive debt. By 2010, the Avantha Group (the Thapar holding company) was stretched thin. High debt from costly acquisitions was weighing down the entire conglomerate.

Meanwhile, the consumer division languished in organizational purgatory. By 2014, insiders paint a picture of stunning neglect: the division functioned without a national sales head, had no dedicated innovation team, and operated without any meaningful R&D budget. Product development meant copying competitors six months late. Marketing meant printing the Crompton logo larger. This was not a business; it was an organizational orphan.

Yet despite this neglect—or perhaps because the brand's industrial reputation still carried weight—the consumer business maintained strong positions in certain categories. Fans, in particular, remained a stronghold with over 25% market share. The Crompton name, built over decades of industrial reliability, still commanded respect even if the products themselves were uninspiring.

By 2014, Gautam Thapar faced a stark reality: the debt-laden conglomerate needed capital, and the consumer business—despite its potential—didn't fit the industrial focus. The stage was set for one of Indian corporate history's most consequential demergers.

III. The Great Demerger & PE Entry (2014-2016)

July 2014 marked the beginning of the end—and a new beginning. Crompton Greaves Limited announced plans that would have seemed unthinkable just years earlier: splitting the company in two. The power and industrial systems would remain with the Thapars, while the consumer goods business would be spun off into a separate entity. For an 80-year-old conglomerate, this wasn't just restructuring; it was organizational surgery.

The consumer business crisis ran deeper than anyone publicly acknowledged. Internal assessments revealed an operation that barely functioned as a coherent business unit. There was no national sales head—regional managers operated as independent fiefdoms. Innovation was a foreign concept; the last major product development had been years ago. R&D budget? Essentially zero. Marketing strategy? Hope that the Crompton name still meant something to consumers.

One senior executive later described walking through the headquarters in 2014: "You could feel the neglect. Consumer products were treated like the poor cousin at a rich family's wedding—invited out of obligation but seated at the back table." The irony was palpable: here was a business with ₹2,000+ crore in revenue, market-leading positions in fans and pumps, yet operating like a mom-and-pop shop that happened to have national distribution.

But where the Thapars saw a distraction from their industrial focus, two sophisticated investors saw opportunity. Advent International and Temasek Holdings—private equity giants with deep pockets and proven playbooks—began circling. Their due diligence revealed what insiders already knew: beneath the dysfunction lay remarkable assets. The Crompton brand, despite years of neglect, still commanded respect. Distribution reached 100,000+ retail points across India. Market share in fans and pumps remained strong despite minimal investment. In April 2015, the deal was struck: Advent International and Temasek acquired Gautam Thapar's 34.37% stake for ₹2,000 crore, with the buyers also assuming ₹700 crore of Crompton Greaves's debt. The valuation—19.8 times FY16 estimates—disappointed street analysts who expected 10-12% higher. But for Advent and Temasek, this wasn't about current multiples; it was about transformation potential.

The ownership split was 65:35 between Advent and Temasek respectively, with Advent taking the lead role. This wasn't Temasek's typical sovereign wealth fund investment—they were betting on Advent's operational expertise to unlock value. For Advent's India head Shweta Jalan and her team, this represented their most ambitious consumer play in India.

The demerger mechanics were complex. Initially proposed as a partial split that would have left Crompton Greaves with residual ownership, minority investors and regulators pushed back, forcing a complete 100% demerger. The final structure mirrored shareholdings exactly—every Crompton Greaves shareholder would receive proportional shares in the new consumer entity.

Why did PE see gold where others saw rust? Three factors converged. First, the brand equity remained surprisingly robust despite neglect—Crompton still meant quality to millions of Indians, especially in tier-2 and tier-3 cities. Second, the distribution network, while underutilized, reached deep into India's hinterlands—a footprint that would take competitors decades and billions to replicate. Third, and most critically, the business was so obviously under-managed that basic blocking-and-tackling improvements could yield dramatic results.

The strengths were tangible: market leadership in fans with over 25% share, strong positions in pumps serving India's agricultural economy, and a lighting business with potential in the LED transition. These weren't sunset categories; they were essential products for India's growing middle class. Air conditioning might be aspirational, but every Indian home needed fans. Every farmer needed pumps. Every household was switching to LED.

The demerger was completed in early 2016, with Crompton Greaves Consumer Electricals Limited (CGCEL) listing as a standalone entity on the NSE and BSE. For the first time in eight decades, Crompton's consumer business would chart its own destiny, backed by patient capital and freed from the competing priorities of an industrial conglomerate.

IV. The Transformation Playbook (2016-2022)

The transformation began in earnest when new leadership arrived. Mathew Job joined the company in September 2015 and in his 5-year stint as the CEO, his role was instrumental in transforming the company into one of the top performers in the industry with industry-leading profitability. Shantanu Khosla, a P&G lifer with a stint of over three decades, joined CGCEL in June 2015 as its Managing Director. The contrast couldn't have been starker—Khosla brought consumer goods DNA from P&G's gold standard playbook, while Job brought operational excellence from stints at Philips, GROHE, and Racold.

Khosla later described the challenge memorably: "It seemed like we had to perform an open-heart surgery on a person running a marathon." The company couldn't stop operations for a complete overhaul; it had to transform while delivering quarterly results to newly public shareholders.

Job recalls how under-invested the consumer electricals business was at a time when the competition was agile and ambitious. The paradox was striking: In the fans category, it was the leader with a 27 per cent market share but "A study done by us showed we were third on perception and second when it came to distribution. It was very strange."

"The brand was losing sheen in the minds of the young." Khosla added there was no business problem but the question was how ready it was for the future. "Simply put, it was in need of a transformation."

The transformation playbook unfolded across multiple fronts simultaneously. First came the distribution revolution. Within eighteen months, the number of outlets selling fans increased by 20%, while lighting distribution expanded by 25%. But this wasn't just about adding points of sale—it was about upgrading the quality of distribution, training retailers, and creating pull through consumer demand rather than just push through trade loading.

Product innovation became the second pillar. For decades, Crompton had essentially been a fast follower—copying competitor products six months late with minor tweaks. In 2017, the company launched its breakthrough: an anti-dust fan based on actual consumer research. This wasn't revolutionary technology, but for Crompton it represented a seismic shift—listening to consumers, identifying unmet needs, and being first to market with solutions.

The anti-dust fan's success went beyond sales numbers. It signaled to retailers that Crompton was back in the innovation game. It gave the sales force confidence to push premium products. Most critically, it began changing internal culture—engineers started thinking like marketers, marketers started understanding technology, and everyone started obsessing over consumer insights.

Building a consumer company culture from industrial DNA proved the hardest transformation. The management decided there were five areas which were very important in the early days. They focused on stability first— Only three executives were recruited at the time of the demerger: Shantanu Khosla, Sandeep Batra, and Mathew Job. This helped because in the initial period, there was a lot of stability. They hardly lost any people.

The cultural transformation went deeper than org charts. The company launched initiatives like "Leadership Language," training managers on how words and communication styles impact team performance. This wasn't corporate fluff—research showed that high-performing teams within Crompton used distinctly different language patterns, emphasizing empowerment over control, possibilities over problems.

Advent's Shweta Jalan points to the fundamental strengths they saw: "The strengths were the Crompton brand and distribution. It had a leadership position in fans and pumps, while lighting and appliances was a big opportunity." The PE investors' faith was being vindicated—the business that functioned without a national sales head in 2014 was now executing coordinated national campaigns with precision.

By 2022, the transformation numbers spoke for themselves. Revenue had grown from ₹2,800 crore at demerger to over ₹5,000 crore. EBITDA margins expanded from single digits to mid-teens. Market share in fans held steady despite intense competition. The lighting business successfully navigated the LED transition. Return on capital employed consistently exceeded 30%.

But perhaps the biggest validation came from an unexpected source—talent. By 2020, Crompton was attracting executives from Hindustan Unilever, Asian Paints, and other consumer goods leaders. The company that couldn't fill a national sales head position in 2014 was now a desired destination for ambitious consumer goods professionals.

V. The Butterfly Acquisition Saga (2022-2023)

February 2022 brought what seemed like Crompton's boldest strategic move yet. The company signed definitive agreements to acquire up to a 55% stake in Butterfly Gandhimathi Appliances at Rs 1,403 per equity share, aggregating up to Rs 1,379.68 crore. Following mandatory open offer regulations, the total consideration reached Rs 2,076.63 crore for what would eventually become a 75% controlling stake.

The strategic rationale was compelling. Butterfly wasn't just another kitchen appliance company—it was a South Indian institution. Founded in 1986, the Chennai-based company had built an almost cult-like following for its wet grinders, pressure cookers, and mixer grinders. In Tamil Nadu and Karnataka, "Butterfly" was synonymous with quality kitchen equipment, much like how "Preethi" dominated in certain segments.

For Crompton, Butterfly represented three strategic prizes. First, geographical complementarity—while Crompton was stronger in North and West India, Butterfly derived more than 80% of its revenue from the southern region. Second, product portfolio expansion—Butterfly's expertise in kitchen appliances would instantly catapult Crompton into categories where it had minimal presence. Third, and perhaps most critically, Butterfly's exclusive distribution network in South India, with deep penetration in tier-2 and tier-3 towns, would take competitors decades to replicate.

The financials painted an attractive picture. Butterfly Gandhimathi commanded higher gross margins (36.3% in 9MFY23) than Crompton Greaves Consumer Electricals (31.1% in 9MFY23), but its Ebitda margins of 10.2% in 9MFY23 was depressed due to higher overhead and marketing costs—classic symptoms of subscale operations that could benefit from Crompton's larger platform.

Post-acquisition, Crompton changed the majority of the Board of Directors of Butterfly including the Managing Director. This wasn't a gentle integration—it was a takeover. The new management immediately began implementing Crompton's playbook: upgrading distribution, launching premium variants, and investing in brand building.

By March 2023, with integration progressing well, Crompton announced the logical next step: a complete merger. Public shareholders of Butterfly Gandhimathi as on the record date will receive 22 equity shares of Crompton Greaves Consumer Electricals for every five equity shares held by them in Butterfly. The exchange ratio implied a 7% premium for Butterfly shareholders—seemingly generous given Crompton's control position.

The merger made strategic sense. It would simplify corporate structure, eliminate duplicate costs, enable unified branding, and accelerate synergy realization. Investment bankers and analysts universally praised the move. Nomura called it "EPS accretive by FY25." Management painted a vision of a unified entity leveraging combined strengths to dominate kitchen appliances nationally.

Then came October 28, 2023—a date that would shock Crompton's boardroom and reverberate through Dalal Street. The shareholder voting results were devastating: a total of 28.82 lakh public investors voted regarding the proposal, with 20.93 lakh or 72.61 per cent voting against the merger. The breakdown was even more damning: Non-institutional public investors of Butterfly cast 17.12 lakh votes, with 16.62 lakh votes or 97.04 per cent against the merger.

The rejection was unprecedented. Here was a merger where the acquirer already owned 75%, offered a premium, had board control, and promised operational improvements—yet public shareholders overwhelmingly said no. The 97% opposition from retail investors suggested deep-seated concerns that went beyond financial metrics.

Why did Butterfly's shareholders revolt? Several theories emerged. Cultural resistance played a role—Butterfly was a Chennai institution, and shareholders feared its identity would be subsumed by Mumbai-based Crompton. Valuation concerns persisted despite the premium—some shareholders remembered Crompton had paid Rs 1,403 per share initially, and the merger valued shares at effectively Rs 1,294. There were also governance concerns about minority shareholder treatment in a company already 75% controlled by Crompton.

The failed merger became a cautionary tale about the limits of financial engineering in Indian markets. You could buy control, change management, and integrate operations—but winning hearts and minds of minority shareholders required something more. Crompton learned that in India's relationship-driven markets, strategic logic alone wasn't enough; you needed social license to operate.

VI. Crompton 2.0: The Second Transformation (2023-Present)

The failed Butterfly merger could have been a devastating blow to morale and strategy. Instead, it catalyzed what management branded "Crompton 2.0"—a comprehensive reinvention that began in June 2023. This wasn't just rebranding or incremental improvement; it was a fundamental rethinking of what Crompton could become. "Crompton 2.0 was launched in Jan 23 and we called out this new approach, I'm glad to say that our focus on revenue growth, translating also into profit growth, seems to be working," CEO Promeet Ghosh noted in the Q4 2024 earnings call. The strategy rested on four pillars: Premiumization, GTM (Go-To-Market) excellence, Brand Investments, and Innovation.

The company spent ~92 crores on advertising and promotion in Q2 & Q3 of FY24—a dramatic escalation from historical spending. This wasn't spray-and-pray marketing; it was targeted investment in building brand salience among younger consumers who had forgotten Crompton's heritage. High-impact campaigns were executed across categories, each designed to reposition Crompton from reliable-but-boring to innovative-yet-trustworthy.

Premiumization became the watchword. Instead of competing on price in commoditized segments, Crompton began introducing premium variants across categories. The anti-bacterial LED lamps commanded 30% price premiums. Designer fans with IoT connectivity sold at 2x the price of basic models. Water heaters with smart controls and energy-saving features justified 40% higher prices. The strategy wasn't just about higher prices—it was about giving consumers reasons to trade up.

Innovation accelerated dramatically. The company launched over 80 new products in 2023-24, entering entirely new segments like solar pumps and rooftop solar solutions. The Crompton Startup Innovation Challenge was launched, inviting external innovators to co-create solutions. This open innovation approach marked a cultural shift—from NIH (Not Invented Here) syndrome to embracing external ideas.

GTM excellence meant fixing basic blocking and tackling that had been neglected for years. Distribution quality improved with better retailer training and incentive alignment. E-commerce, which had been an afterthought, recorded 75% YoY growth in Q4 2024, becoming the fastest-growing channel. The company finally built capabilities in modern trade, working directly with large format retailers rather than through distributors.

The BEE (Bureau of Energy Efficiency) transition in fans—requiring higher energy efficiency standards—could have been a crisis. Crompton turned it into an opportunity, using the regulatory change to premiumize the entire category. While competitors scrambled to meet minimum standards, Crompton launched super-efficient models that exceeded requirements, commanding premium prices.

The transformation showed in the numbers. Revenue jumped 5.03% since last year same period to ₹2,076.57Cr in the Q4 2024-2025. More impressively, net profit jumped 22.49% since last year same period to ₹169.48Cr—margins were expanding even as the company invested heavily in brand building. The ECD segment grew 14.3% YoY with EBIT margins at 16.7%, industry-leading profitability.

Butterfly, despite the failed merger, wasn't abandoned. A transition was underway with new management appointments and policy alignments. The company continued investing in the brand, with advertising spend increased 2.4x year-over-year. The strategy shifted to operating Butterfly as a distinct brand targeting different consumer segments—Crompton for mass premium, Butterfly for regional strength in kitchen appliances.

VII. Business Model & Unit Economics

Crompton's business model rests on a seemingly simple two-segment structure that masks considerable complexity. The Electrical Consumer Durables (ECD) segment encompasses fans, appliances, and pumps—products with different seasonality, distribution requirements, and competitive dynamics. The Lighting segment includes both LED and legacy non-LED products, navigating a technological transition while maintaining profitability.

In fans, Crompton holds the #1 position with approximately 27% market share. But this leadership comes with challenges. Fans are highly seasonal—60% of annual sales occur in the four summer months. Manufacturing must ramp up months in advance, tying up working capital. Distribution partners need credit during lean seasons. Yet margins remain attractive at 15-17% EBIT because of Crompton's scale advantages in procurement and manufacturing efficiency.

The pumps business, often overlooked by analysts, represents a hidden gem. With strong positions in both residential and agricultural segments, pumps offer counter-cyclical balance to fans. When urban consumers aren't buying fans in winter, rural consumers need pumps for irrigation. The business also provides an entry point into the solar ecosystem—solar pumps for agriculture are becoming a significant growth driver with government subsidies making them affordable.

Lighting presents a different challenge. The LED transition decimated profits industry-wide as Chinese imports flooded markets and prices collapsed 70% over five years. Crompton navigated this by focusing on value-added segments—architectural lighting, smart lighting, and specialized applications where brand and service matter more than rock-bottom prices.

Butterfly Gandhimathi commands a higher gross margins (36.3 per cent in 9MFY23) than Crompton Greaves Consumer Electricals (31.1 per cent in 9MFY23), but its Ebitda margins of 10.2 per cent in 9MFY23 was depressed due to higher overhead and marketing costs. This margin differential reveals the integration opportunity—Butterfly's superior gross margins suggest strong product positioning and pricing power, while its weak EBITDA margins indicate subscale operations that could benefit from Crompton's infrastructure.

Distribution dynamics shape everything in Indian consumer durables. Crompton reaches consumers through multiple channels: 100,000+ retail points for general trade, 300+ distributors managing regional logistics, modern trade partnerships with organized retail, and rapidly growing e-commerce presence. Each channel requires different economics—general trade needs credit and margins, modern trade demands listing fees and promotions, e-commerce requires digital marketing and fulfillment capabilities.

The manufacturing strategy reflects pragmatic trade-offs. Fans and pumps are largely manufactured in-house across six facilities, providing quality control and cost advantages at scale. Appliances are primarily outsourced to OEMs, avoiding capital investment in rapidly evolving categories. Lighting uses a hybrid model—critical components manufactured internally, assembly often outsourced. This flexible approach optimizes capital efficiency while maintaining quality standards.

Brand architecture has evolved from monolithic to nuanced. "Crompton" remains the master brand, but sub-brands target specific segments. "Optimus" for premium fans, "Greaves" for industrial pumps, "Butterfly" for kitchen appliances. This portfolio approach allows price discrimination without brand dilution—a premium Optimus fan doesn't cheapen the perception of mass-market Crompton products.

Working capital management reveals operational excellence. Despite seasonal businesses and extended distributor credit, Crompton maintains negative working capital in several quarters—essentially using supplier credit to fund operations. Cash conversion cycles average 20-30 days, exceptional for consumer durables. This efficiency frees capital for growth investments rather than funding operations.

Channel economics vary dramatically. General trade offers 8-12% distributor margins plus 15-20% retailer margins, eating into manufacturer realizations. But it provides widest reach, especially in tier-3/4 towns where organized retail doesn't exist. Modern trade typically demands 25-30% margins plus promotional support, but offers volume and visibility. E-commerce margins are actually superior—15-20% platform fees but no distributor layer and better price realization from urban consumers.

The unit economics tell a story of operational leverage. A typical ceiling fan sells for ₹2,500 at MRP. After channel margins, Crompton realizes ₹1,750. Direct costs including materials and manufacturing total ₹1,200, yielding ₹550 gross profit. Allocating overheads and marketing brings EBITDA to ₹250-300 per unit—10-12% margins that become 15%+ at scale due to fixed cost absorption.

VIII. Competition & Market Dynamics

The Indian consumer electricals landscape has transformed from a cozy oligopoly to a battlefield where competition was agile and ambitious. Havells, Orient Electric, and Bajaj Electricals—once regional players or focused specialists—have emerged as formidable pan-India competitors, each with distinct strategies and deep pockets.

Havells represents the most direct threat. Lloyd Electric's transformation into Havells' consumer arm created a behemoth with ₹15,000+ crore revenue across categories. Their strategy? Aggressive brand building through cricket sponsorships and Bollywood endorsements, coupled with premium positioning. Where Crompton emphasizes reliability, Havells sells aspiration. Their "Havells Water Purifier" campaign featuring Dhoni reportedly cost more than Crompton's entire annual marketing budget.

Orient Electric, spun off from Orient Paper in 2018, brought fresh thinking unburdened by legacy. Their digital-first approach resonates with younger consumers—Instagram campaigns, influencer partnerships, and e-commerce focus that Crompton is only now matching. Orient's i-Series fans, with IoT controls and voice activation, launched two years before Crompton's smart products. They don't just compete; they set the innovation agenda.

Bajaj Electricals leverages a 75-year-old brand with deep consumer trust, particularly in western India. Their strategy mirrors Crompton's—broad portfolio, mass-market pricing, distribution strength—but with better execution in certain categories. Bajaj's mixer grinders and water heaters consistently rank higher in consumer surveys despite similar specifications and pricing.

Foreign competition takes different forms. In lighting, Philips remains the premium benchmark despite selling its domestic appliances business. Their Wiz smart lighting ecosystem makes Crompton's LED bulbs look commoditized. Panasonic and Samsung cherry-pick profitable niches—high-end ceiling fans, premium water heaters—without the burden of mass-market distribution.

But the real disruption comes from unexpected quarters. Atomberg, a startup founded in 2012, created the BLDC (Brushless DC) fan category from scratch. Their energy-efficient fans cost 3x regular fans but promise 65% electricity savings. Within a decade, they've captured 10% market share in premium fans, forcing established players to develop competing technologies. Crompton's BLDC response came three years late.

Regional dynamics add complexity. South India, contributing 35% of national consumer durables demand, shows distinct preferences. Butterfly's dominance in Tamil Nadu wet grinders reflects cultural factors—idli/dosa preparation requires specific grinding techniques that North Indian brands didn't understand. Similarly, Kerala's preference for Orient fans stems from decades of local manufacturing and service presence.

The rural-urban divide creates parallel markets. Urban India wants IoT-enabled, aesthetically designed, energy-efficient products. Rural India needs robust, repairable, value-for-money basics. Crompton must simultaneously premiumize for cities while defending market share in villages—a strategic split that fragments resources and focus.

Price points reveal market segmentation. The fans market spans ₹1,000 basic models to ₹15,000 designer pieces. Crompton plays across segments but excels in the ₹1,500-3,000 sweet spot—too premium for local assemblers, too mass for luxury brands. This positioning provides volume but limits margin expansion opportunities that pure premium players enjoy.

The EV and solar opportunity represents both promise and threat. As India pushes renewable energy, solar pumps and panels become mainstream. Crompton's early moves in solar pumps position it well, but specialized solar companies like Waaree and Vikram Solar bring technological expertise that traditional durables players lack. The question: Can Crompton leverage distribution to overcome technology gaps?

Distribution dynamics are shifting rapidly. Quick-commerce platforms like Blinkit and Zepto now deliver fans within 30 minutes in metro cities. D2C brands bypass traditional retail entirely. Social commerce through WhatsApp and Instagram challenges conventional marketing. Crompton's 100,000 retail points—once an unassailable moat—risk becoming a costly legacy if consumer behavior permanently shifts online.

Chinese competition looms despite government restrictions. Xiaomi's Mi brand expanded from phones to air purifiers and smart bulbs, leveraging their ecosystem advantage. If regulatory barriers ease, Chinese brands could replicate in durables what they achieved in smartphones—rapid share gain through aggressive pricing and decent quality.

IX. Playbook & Investment Lessons

The Crompton transformation offers a masterclass in value creation through corporate restructuring, but the lessons extend far beyond financial engineering. This is fundamentally a story about focus, timing, and execution—elements that separate successful transformations from the corporate graveyard of failed turnarounds.

Demerger as Value Creation

The 2015-16 demerger wasn't just splitting a company; it was unleashing trapped value. The consumer business within industrial Crompton Greaves was valued at perhaps 8-10x earnings, weighed down by conglomerate discount and capital allocation compromises. Post-demerger, the same business commands 35-40x multiples. The math is simple: same assets, different structure, 4x value creation.

But demergers often fail. What made this work? First, clean separation—no lingering cross-holdings, shared services, or complicated agreements. Second, immediate strategic clarity—PE owners knew exactly what they wanted to build. Third, management alignment—new leadership had no baggage from the industrial past. The lesson: structure must follow strategy, and both must be unambiguous.

PE Transformation Playbook

Advent and Temasek's approach deserves careful study. They didn't financial engineer their way to returns through leverage and cost-cutting. Instead, they invested—in people, brands, innovation, distribution. Advent International and Temasek for Rs 2,000 crore seems expensive for a neglected division, but PE saw what others missed: a fixable business with structural advantages.

The PE playbook had five elements: (1) Bring world-class management immediately—Khosla and Job arrived within months. (2) Fix basics before innovating—distribution, sales force, product quality. (3) Invest ahead of returns—marketing spend increased even as profits were pressured. (4) Maintain strategic patience—no flip in 3-5 years, building for long-term value. (5) Exit gradually—Advent's staggered exit from 2019-2021 avoided market overhang.

Failed M&A Lessons

The Butterfly merger rejection offers cautionary insights. Financial logic isn't enough—Non-institutional public investors of Butterfly cast 17.12 lakh votes, with 16.62 lakh votes against the merger, translating to 97.04 per cent against the merger plan. Institutional public investors cast 11.59 lakh votes, with 4.30 lakh votes against, translating to 37.15 per cent against the merger. In total, public investors cast 28.82 lakh votes, with 20.93 lakh votes against the merger, amounting to 72.61 per cent opposition. The 97% retail opposition suggests deep emotional and cultural factors that spreadsheets don't capture.

The failure teaches three lessons: (1) Minority shareholders in India have real power through regulatory protections—majority control doesn't guarantee merger success. (2) Regional brands carry emotional equity that transcends financial metrics—Butterfly wasn't just a company but a Tamil Nadu institution. (3) Integration before merger might be counterproductive—changing management and operations before shareholder approval created suspicion rather than confidence.

Building Consumer Brands from B2B Heritage

The transformation from industrial supplier to consumer champion required fundamental changes most B2B companies can't manage. Crompton succeeded by accepting that consumer businesses are fundamentally different—emotional rather than rational, push rather than pull, brand-driven rather than specification-driven.

The key was hiring consumer veterans who understood these differences. Mathew joined the company in September 2015 and in his 5-year stint as the CEO of CGCEL, his role has been instrumental in transforming the company into one of the top performers in the industry with industry-leading profitability while Shantanu Khosla, a P&G lifer with a stint of over three decades, who joined CGCEL in June 2015 as its Managing Director. They didn't try to convert industrial engineers into marketers; they hired marketers and taught them the category.

Capital Allocation in Consumer Durables

Crompton's capital allocation reveals sophisticated thinking. Instead of pursuing capital-intensive manufacturing across categories, they chose selective vertical integration. Fans and pumps—where they had scale and expertise—warranted manufacturing investment. Appliances—rapidly evolving with uncertain winners—remained outsourced. This hybrid model optimized returns while maintaining flexibility.

The working capital management deserves special mention. In a business with seasonal demand and extended channel credit, Crompton achieves negative working capital through supplier financing and efficient inventory management. This means growth actually generates cash rather than consuming it—the holy grail of consumer businesses.

The Importance of Distribution in India

Despite digital disruption, Crompton's 100,000+ retail points remain its moat. India isn't one market but thousands of micro-markets with distinct preferences, languages, and purchasing power. E-commerce might dominate metros, but 70% of India still buys from neighborhood stores. Crompton's distribution reach into tier-3/4 towns creates a barrier that new-age brands can't easily replicate.

But distribution must evolve. Crompton's investment in route-to-market technology, retailer apps, and digital ordering systems modernizes traditional trade without abandoning it. The lesson: in India, omnichannel isn't a buzzword but a necessity.

Managing Conglomerate Complexity Post-Demerger

Even after demerger, Crompton manages complexity across multiple categories, channels, and brands. The secret is organizational design that balances autonomy with synergy. Category heads run independent P&Ls but share manufacturing, distribution, and back-office infrastructure. Butterfly operates separately but leverages Crompton's procurement scale.

This federated model avoids both extremes—the inefficiency of complete independence and the sluggishness of centralized control. It's a difficult balance that requires sophisticated management systems and clear accountability frameworks.

X. Bear vs Bull Case & Analysis

Bull Case: The Convergence of Multiple Growth Vectors

The optimistic view sees Crompton at an inflection point where multiple positive factors converge. Market leadership in core categories provides a foundation for expansion rather than a summit to defend. The 27% share in fans and strong position in pumps create cash generation engines that fund growth investments without diluting returns.

The premiumization journey through Crompton 2.0 has just begun. Indian consumers are rapidly upgrading from functional to aspirational products. A ceiling fan is no longer just air circulation but a lifestyle statement. Crompton's pivot from price warrior to premium player aligns perfectly with this consumption upgrade. Early results validate the strategy—premium variants already contribute 30% of revenues versus 15% three years ago.

Butterfly synergies will eventually materialize, even without merger. Operating as sister companies allows cherry-picking synergies—combined procurement, shared R&D, cross-selling—without integration complexities. Butterfly's gross margins exceeding Crompton's suggest revenue synergies from premiumization. As operations scale and costs optimize, Butterfly could add 200-300 basis points to consolidated margins.

The distribution network, often dismissed as legacy infrastructure, becomes increasingly valuable as India develops. Quick-commerce serves metros, but Bharat needs traditional retail. Crompton's reach into 100,000+ outlets provides access to the next 500 million consumers entering the middle class. This distribution moat deepens as new brands find customer acquisition costs prohibitive.

revenue (10.3% per year) is forecast to grow suggests acceleration from the 11.7% over past five years. More importantly, margin expansion through premiumization means profit growth exceeding revenue growth. If Crompton achieves 12-15% revenue CAGR with 100-150 basis points margin expansion, earnings could compound at 18-20% annually.

The categories Crompton operates in have long runways. Fan penetration remains below 60% in rural India. LED transition is only 60% complete. Kitchen appliances penetration is sub-20% even in urban areas. Unlike saturated categories like televisions or refrigerators, Crompton's markets offer decades of growth.

Government initiatives turbocharge specific segments. PM-KUSUM scheme for solar pumps, rural electrification driving fan demand, energy efficiency mandates forcing appliance upgrades—policy tailwinds support structural growth beyond economic cycles.

Bear Case: Structural Challenges in a Commoditizing Market

The pessimistic view sees multiple headwinds that explain why The company has delivered a poor sales growth of 11.7% over past five years. This isn't just execution failure but structural challenges in commoditizing categories with limited differentiation.

The failed Butterfly merger signals deeper integration challenges. If Crompton couldn't convince minority shareholders of synergy benefits despite 75% control, what does that say about execution capabilities? The rejection might reflect broader market skepticism about management's ability to integrate acquisitions successfully. The significant management changes—CEO and MD transitions—during critical integration periods raise stability concerns.

Competition intensifies from every direction. Havells and Orient aren't just competing; they're out-innovating and out-marketing Crompton. Atomberg proved that startups can disrupt established players with superior technology. Chinese brands wait at the borders, ready to flood markets if regulations ease. D2C brands bypass Crompton's distribution advantage entirely. The competitive moat narrows daily.

Return on Equity is forecast to be low in 3 years time (19.4%) raises capital efficiency concerns. In capital-light consumer businesses, ROE should exceed 25%. Declining returns suggest either margin pressure from competition or inefficient capital allocation. Either interpretation questions the sustainability of current valuations.

Commodity cost pressures remain permanent headwinds. Copper for motors, steel for fans, plastics for appliances—input costs volatile and largely uncontrollable. While Crompton can pass through costs eventually, timing lags pressure margins. In competitive markets with Chinese imports providing price ceilings, cost inflation might not be fully recoverable.

The categories themselves face disruption. Air conditioning could obsolete ceiling fans in urban homes. Solar panels with battery storage might eliminate grid-connected pumps. LED commoditization destroyed lighting profits industry-wide—what if fans follow the same path? Category maturity limits growth potential regardless of execution excellence.

Distribution advantages erode as commerce digitizes. If 50% of purchases move online within five years—not unrealistic given smartphone penetration—Crompton's retail network becomes a liability rather than asset. Maintaining 100,000 touch points requires enormous fixed costs that digital-native competitors avoid.

Brand equity among youth remains questionable. Despite marketing investments, Crompton resonates more with 40+ consumers who remember its industrial heritage. Millennials and Gen-Z prefer new-age brands unburdened by legacy associations. Building relevance with younger cohorts requires more than advertising—it needs fundamental repositioning that risks alienating core customers.

The Balanced View: Execution Will Determine Outcome

Reality likely lies between extremes. Crompton possesses genuine strengths—market leadership, distribution reach, improving brand equity, and demonstrated transformation capability. But structural challenges are equally real—intense competition, category commoditization, and integration complexities.

The outcome depends on execution across three critical dimensions:

-

Innovation Velocity: Can Crompton match or exceed competitor innovation rates? Success requires not just R&D spending but cultural transformation from fast-follower to innovation leader.

-

Brand Building: Will increased marketing investments translate to preference among younger consumers? Money alone won't suffice—Crompton needs breakthrough creative and digital engagement that resonates with evolved consumer expectations.

-

M&A Integration: How effectively can Crompton extract Butterfly synergies without formal merger? This tests management's ability to coordinate independent entities while maintaining entrepreneurial energy.

Current valuations at 35-40x earnings price in significant success across all dimensions. Any execution slippage could trigger re-rating. Conversely, successful execution could drive multiple expansion as market recognizes transformation sustainability.

The investment case ultimately reduces to a bet on Indian consumption growth and management's ability to capture disproportionate share. Bulls see structural tailwinds overwhelming execution risks. Bears see competition and commoditization eroding returns regardless of market growth. Time will tell which narrative prevails.

XI. Epilogue: The Future of Indian Consumer Electricals

Crompton's journey from industrial conglomerate subsidiary to independent consumer champion mirrors India's own economic transformation. When Colonel Crompton founded his company in 1878, electricity itself was revolutionary. Today, as India becomes the world's most populous nation with ambitious economic aspirations, the question isn't whether households will have electricity, but what devices they'll plug in.

The Indian consumer electricals market stands at a fascinating inflection point. Per capita consumption remains a fraction of developed markets—Indians use one-fifth the appliances of Americans, one-third of Chinese. This gap represents not deprivation but opportunity. As 300 million Indians enter the middle class this decade, their first purchases won't be luxury cars or designer handbags but ceiling fans, mixer grinders, and water heaters—Crompton's sweet spot.

Yet the future won't simply extrapolate the past. Smart homes, once science fiction, become reality as Jio's 5G rollout enables IoT adoption at scale. Sustainability shifts from corporate buzzword to consumer demand as urban Indians experience climate change firsthand. Rural penetration accelerates as solar power and improved logistics overcome infrastructure constraints.

Can Crompton become India's Whirlpool or Electrolux? The ambition isn't unrealistic. Whirlpool built its empire through strategic acquisitions and brand portfolio management—exactly Crompton's playbook with Butterfly. Electrolux succeeded through innovation and premiumization—Crompton 2.0's core strategy. The template exists; execution determines success.

But India offers unique challenges that Western models don't address. Price sensitivity exceeds anywhere except Africa. Distribution complexity surpasses even China given linguistic and cultural diversity. Competition intensity—with both global giants and nimble startups—creates a cauldron that tests every strategy. Crompton must forge its own path rather than copying foreign playbooks.

The next battlegrounds are already visible. Smart home integration will separate winners from losers—consumers won't buy discrete devices but ecosystems. Sustainability becomes table stakes as energy costs rise and environmental consciousness grows. Rural penetration requires not just distribution but products designed for irregular power, extreme weather, and repair rather than replacement mindsets.

Crompton's transformation from industrial also-ran to consumer leader proves that corporate reinvention remains possible even for century-old companies. The demerger unlocked value, PE ownership provided capital and capability, and management executed a turnaround that skeptics deemed impossible. Whether the next chapter delivers similar success depends on navigating disruption while maintaining what made the transformation possible—consumer focus, execution excellence, and strategic courage.

The broader lesson transcends Crompton or even consumer electricals. India's consumption story has just begun. Companies that understand this opportunity, invest ahead of the curve, and execute with discipline will create enormous value. Those that don't will become case studies in business schools, examples of how market leaders became historical footnotes.

For Crompton, the journey from Colonel Crompton's arc lights to IoT-enabled smart fans spans 145 years and counting. The next decade will determine whether this remarkable transformation represents a new beginning or the final chapter of a storied legacy. Given the track record of reinvention, betting against Crompton seems premature. But in India's hypercompetitive consumer markets, past performance, as they say, guarantees nothing about future results.

The only certainty is that Indian consumers, armed with rising incomes and digital awareness, will demand more—more features, more value, more sustainability, more innovation. Companies that deliver will thrive. Those that don't will perish. Crompton has proven it can transform once. The question now is whether it can keep transforming, again and again, as markets evolve at digital speed.

In the end, Crompton's story isn't just about fans and lights. It's about industrial India becoming consumer India, about professional management creating value from neglected assets, about the power of focus in an age of conglomerate complexity. It's a story still being written, one quarterly result at a time, one innovation at a time, one consumer at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube