Craftsman Automation: From a Coimbatore Garage to India's Precision Manufacturing Powerhouse

I. Introduction & Episode Teaser

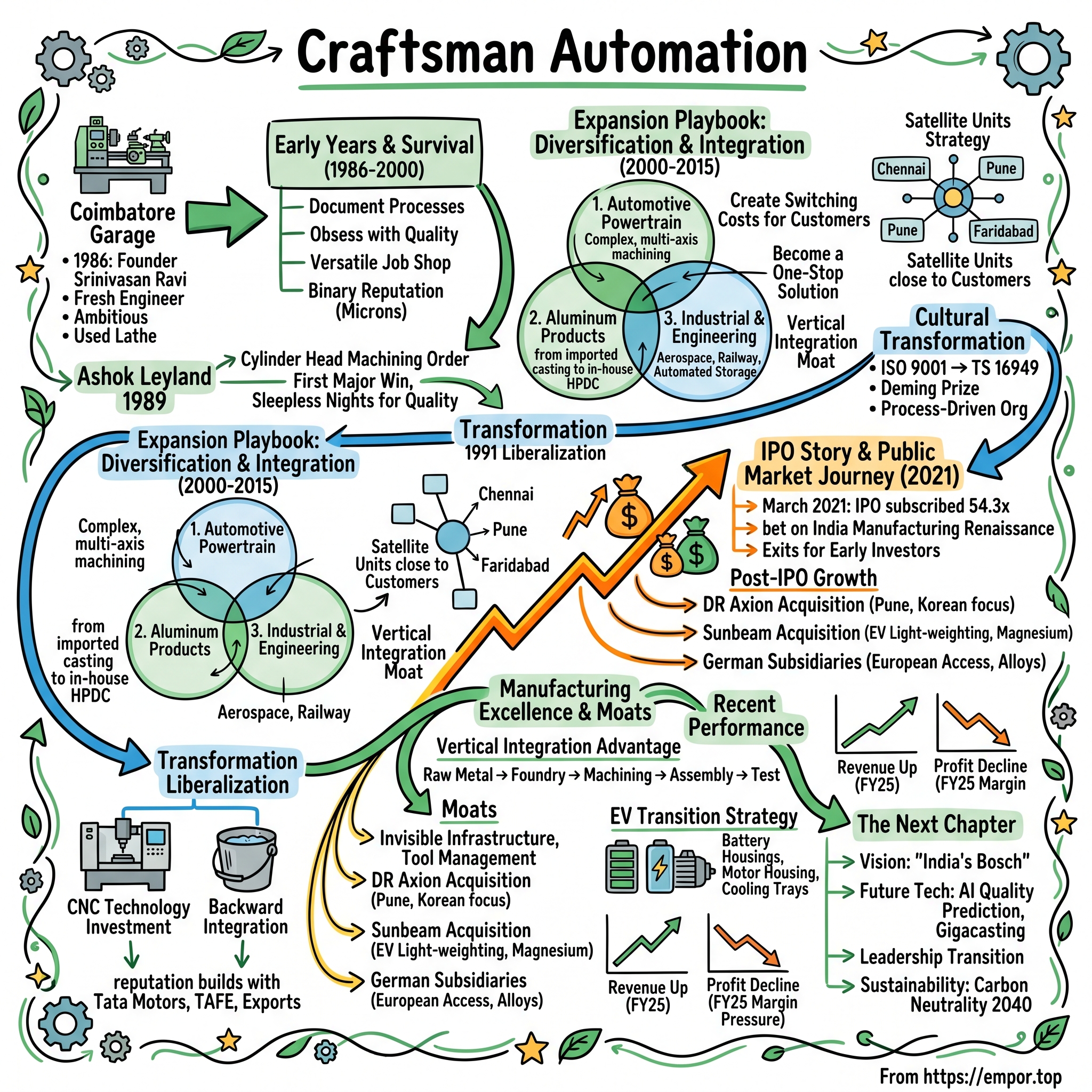

Picture this: A young mechanical engineer in 1986 Coimbatore, fresh out of PSG College, staring at an empty industrial shed with nothing but ambition and a worn-out lathe machine. No family business to inherit, no safety net, just a burning desire to build something that could compete with the world's best precision manufacturers. That engineer was Srinivasan Ravi, and that empty shed would become Craftsman Automation—today a ₹16,263 crore manufacturing colossus that machines critical components for everyone from Tata Motors to Daimler.

The numbers tell a story of relentless execution: ₹6,323 crore in revenue, 12 strategically located manufacturing facilities, and a client roster that reads like a who's who of global automotive giants. But here's what's truly remarkable—while India's liberalization created thousands of entrepreneurs, how many first-generation founders built companies that could go toe-to-toe with century-old German precision engineering firms?

This is the story of how a bootstrap operation in Tamil Nadu's textile hub transformed into one of India's most vertically integrated auto component companies. It's a playbook on navigating India's notorious License Raj, surviving multiple economic cycles, and building trust with customers who measure defects in parts per million. Along the way, we'll uncover how Craftsman cracked the code on three seemingly impossible challenges: competing on quality with global suppliers, achieving cost leadership through vertical integration, and transitioning from family-run operations to institutional-grade governance. The recent Q1 FY25 results paint a complex picture: revenue surged 55% year-over-year to ₹1,784 crore while net profit rose 31% to ₹69.60 crore, yet on a full-year basis, net profit declined 36% to ₹195 crore despite a 28% revenue growth to ₹5,690 crore in FY25. This divergence between top-line growth and bottom-line pressure captures the central tension in Craftsman's story—a company scaling rapidly through acquisitions while navigating margin headwinds and industry transitions.

But numbers alone don't capture what makes Craftsman remarkable. This is fundamentally a story about industrial ambition in post-liberalization India, about building world-class precision manufacturing capabilities from scratch, and about the audacity to compete with suppliers who've been perfecting their craft since the Industrial Revolution. As we'll discover, Srinivasan Ravi didn't just build a company—he architected a vertically integrated manufacturing ecosystem that would become the backbone of India's automotive supply chain.

II. The Founder's Story & Early Years (1986-2000)

The year was 1986. While Silicon Valley was birthing the personal computer revolution, in Coimbatore—a city better known for textile mills than cutting-edge engineering—a 28-year-old mechanical engineer was about to make a contrarian bet. Srinivasan Ravi had just walked away from a comfortable job to start something that seemed almost quixotic: a precision manufacturing company in a country where "precision" often meant "good enough."

Ravi, who would later become Chairman & Managing Director, wasn't born into industrial royalty. No Birla or Tata connections, no family factories to inherit. What he had was an engineer's obsession with tolerances measured in microns and a conviction that India could manufacture components as precisely as any German or Japanese firm. Friends called him naive. The market would prove him prescient.

Coimbatore in the mid-1980s was experiencing its own quiet revolution. The city's textile machinery manufacturers had created an ecosystem of tool rooms, foundries, and machine shops. But these were mostly job shops—taking orders, making parts, minimal value addition. Ravi saw something different: the foundation for a world-class precision manufacturing hub. The city had skilled machinists, relatively stable power supply (crucial for precision work), and critically, a culture of engineering excellence fostered by institutions like PSG College of Technology.

The timing was both terrible and perfect. India's License Raj still strangled entrepreneurship—you needed government permission to manufacture, expand capacity, even import a lathe. Foreign exchange was scarce. Quality machine tools were nearly impossible to procure. Yet change was in the air. Rajiv Gandhi's government was making tentative moves toward liberalization. Japanese companies were starting to look at India. The automotive industry, long dominated by Ambassador and Premier Padmini, was stirring with Maruti's entry.

Craftsman Automation started as a small scale industry, operating from a modest shed with second-hand machines. The early days were about survival through versatility. Monday might see them machining pump components for a local textile mill. Tuesday, agricultural equipment parts. Wednesday, whatever paid the bills. But even in those hand-to-mouth days, Ravi insisted on something unusual: documenting every process, measuring every output, treating every job as if it were for Toyota.

This obsession with process wasn't academic—it was existential. In precision manufacturing, reputation is binary. One batch of defective parts doesn't just lose you a customer; it blacklists you from an entire industry. Ravi understood that before Craftsman could dream of supplying to OEMs, it needed to prove it could deliver consistency at the job-shop level.

The breakthrough came in 1989. Ashok Leyland, the commercial vehicle giant, was looking for local suppliers for engine components. The parts weren't complex, but the tolerances were tight and the volumes meaningful. Most small shops either lacked the technical capability or the financial stamina to meet Ashok Leyland's payment terms. Craftsman had barely three years of operations, but Ravi pitched aggressively, offering not just machining but also process improvement suggestions.

The first order was for cylinder head machining—200 pieces. Ravi personally supervised every shift, sleeping on the shop floor, checking measurements obsessively. All 200 pieces passed inspection. More importantly, Craftsman's process documentation impressed Ashok Leyland's quality team. Here was a small vendor thinking like a tier-one supplier.

By 1991, as India embarked on economic liberalization, Craftsman had established a reputation for reliability in the Coimbatore ecosystem. But Ravi wasn't satisfied with being a good job shop. He saw liberalization as an inflection point. Global auto companies would enter India. They would need local suppliers who could match international quality standards. The job shop would need to become something more.

The transformation started with technology. Using precious foreign exchange allocations, Craftsman imported its first CNC machine in 1992—a used Mazak from Japan that cost more than the company's entire previous year's revenue. The Coimbatore business community thought Ravi had lost his mind. Why invest in automation when labor was cheap? But Ravi understood something his peers didn't: precision at scale requires machines, not just skilled hands.

The CNC machine changed everything. Suddenly, Craftsman could hold tolerances that were impossible with conventional machines. Repeatability improved dramatically. More importantly, it could now bid for export orders. The first international customer came in 1994—a German pump manufacturer looking for cost-effective machining. The volumes were small, but the validation was enormous. If Craftsman could satisfy German quality standards, it could satisfy anyone.

Yet growth brought its own challenges. Working capital was perpetually short. Banks were skeptical of lending to small manufacturers. Payment cycles with large OEMs stretched to 90-120 days while raw material suppliers demanded cash upfront. There were months when Ravi had to choose between paying salaries and buying materials. He chose salaries, using personal assets as collateral for material purchases.

The period from 1995 to 2000 was about building organizational capability. Craftsman implemented ISO 9001—among the first small-scale industries in Coimbatore to do so. It invested in training, sending operators to Japan and Germany to learn best practices. Most radically, it began backward integration, setting up a small foundry to control raw material quality.

By the dawn of the new millennium, Craftsman had evolved from a single-shed operation to a company with 200 employees, three manufacturing units, and an order book that included Ashok Leyland, TAFE, and several export customers. Revenue had grown to ₹12 crores—modest by today's standards but representing a 50-fold increase from its founding.

But Ravi knew this was just the foundation. The real opportunity lay ahead. Global auto majors were setting up Indian operations. The commercial vehicle market was booming. India's tractor industry was becoming globally competitive. Craftsman had spent 14 years building capabilities. Now it was time to scale.

III. The Expansion Playbook: Diversification & Integration (2000-2015)

The new millennium opened with Ravi standing in front of a whiteboard, sketching what would become Craftsman's three-pillar strategy. The diagram was deceptively simple: three circles labeled "Automotive Powertrain," "Aluminum Products," and "Industrial & Engineering." The magic wasn't in the categories but in the arrows connecting them—showing shared capabilities, customer synergies, and most importantly, the vertical integration opportunities that would become Craftsman's moat.

The automotive powertrain business was the natural evolution of Craftsman's precision machining heritage. But Ravi's insight was that simply machining components was a race to the bottom. The real value lay in handling complexity—multi-axis machining, assembly, testing, and most crucially, taking responsibility for entire sub-systems rather than individual parts.

The first major win came in 2001 when Tata Motors was developing a new generation of commercial vehicles. They needed a supplier who could machine and assemble complete cylinder heads—a complex component requiring 100+ operations. Most suppliers balked at the investment required. Craftsman saw opportunity. They invested ₹15 crores—debt-funded at 14% interest—in dedicated machines and tooling. The bet paid off. By 2003, Craftsman was Tata Motors' largest cylinder head supplier.

But the real strategic masterstroke was the move into aluminum in 2002. Ravi had noticed something curious: many of the powertrain components Craftsman machined started as aluminum castings imported from Thailand or China. The logistics were complex, quality was inconsistent, and lead times were long. Why not cast them in-house?

The board was skeptical. Aluminum casting—especially high-pressure die casting for automotive applications—was a completely different business. It required massive capital investment, different technical skills, and most dauntingly, competing with established players like Endurance and Sundaram Clayton. But Ravi saw what others missed: vertical integration would give Craftsman a unique position. They could offer customers a one-stop solution from casting to fully machined components.

The aluminum journey began with a small gravity die casting unit in 2003, primarily serving the two-wheeler industry. The learning curve was steep. The first year saw rejection rates above 15%. But Craftsman applied the same methodical approach that had worked in machining: document everything, measure obsessively, improve continuously. By 2005, they had mastered the process enough to win their first major order—alloy wheels for Royal Enfield.

The company became a leading player in machining critical engine and transmission components for M&HCV and tractors. The commercial vehicle boom of 2003-2008 turbocharged growth. Every major CV manufacturer—Tata Motors, Ashok Leyland, Daimler India (which had acquired Bharat Benz), Volvo-Eicher—needed local suppliers who could meet global quality standards. Craftsman was perfectly positioned.

But Ravi understood that customer concentration was dangerous. In 2006, Tata Motors accounted for nearly 60% of revenue. A strategic decision was made to diversify aggressively. The target: no single customer should exceed 30% of revenue. This meant saying no to some Tata Motors business—a gutsy move that raised eyebrows—while aggressively pursuing new customers.

The industrial and engineering segment emerged from this diversification push. If Craftsman could machine complex automotive components, why not aerospace parts? Railway components? Construction equipment? Each new vertical required specific certifications and capabilities, but the underlying competence—precision manufacturing—remained constant.

The 2008 financial crisis tested this strategy. Automotive demand crashed. Several competitors went bankrupt. But Craftsman's diversification paid off. While automotive revenues fell 30%, industrial segment grew 15%, cushioning the blow. More importantly, the crisis created opportunities. Distressed competitors were available for acquisition. Global OEMs were looking to derisk by localizing supply chains.

By this time, Craftsman had expanded to 12 plants including 10 satellite units across India. The satellite unit strategy was particularly clever. Instead of building massive centralized facilities, Craftsman created smaller units close to customer plants. This reduced logistics costs, improved response times, and most importantly, created switching costs for customers who had integrated Craftsman into their assembly lines.

The Carl Stahl joint venture in 2010 marked Craftsman's entry into high-value engineering products. Carl Stahl, a German wire rope specialist, needed an Indian manufacturing partner. Craftsman offered not just manufacturing but also engineering support for localization. The JV produced specialized wire ropes for construction, mining, and material handling—products with 40%+ EBITDA margins compared to 15-20% in automotive.

Technology absorption accelerated during this period. Craftsman didn't just buy machines; it absorbed knowledge. Every equipment purchase included training contracts. Engineers were sent to Germany, Japan, and Korea. The company hired expats for critical roles. By 2012, Craftsman had one of the most advanced machining setups in India, including 5-axis CNC machines that could handle aerospace-grade tolerances.

The tractor segment emerged as a surprise growth driver. India's tractor market was booming, driven by agricultural mechanization. Mahindra, TAFE, and John Deere needed suppliers who could handle large, complex castings. Craftsman's integrated capabilities—from casting to machining to assembly—made them an ideal partner. By 2014, they were supplying transmission housings, differential cases, and hydraulic lift housings to every major tractor OEM.

The company became one of the most reputed players in the automotive aluminum space, a leading player in the automated storage market. The automated storage business was an adjacency that emerged from the engineering segment. Craftsman's fabrication capabilities, combined with automation expertise, positioned them to design and build automated storage and retrieval systems for warehouses—a business with software-like gross margins.

But perhaps the most important development during this period was cultural. Craftsman transformed from a founder-driven organization to a process-driven one. Quality systems evolved from ISO 9001 to TS 16949. Six Sigma and TPM became organizational religions. The company won the Deming Prize for quality—the first auto component company in South India to do so.

Financial discipline improved markedly. Working capital cycles shortened from 120 days to 75 days. Return on capital employed improved from 8% to 18%. Debt-to-equity ratio, despite aggressive expansion, remained below 1.5x. The company was generating enough cash to fund growth while maintaining financial flexibility.

By 2015, Craftsman had transformed beyond recognition. Revenue had grown to ₹1,200 crores. The company employed 3,500 people. The customer list read like a who's who of global manufacturing. But Ravi, now 57, knew that the next phase of growth would require something different: external capital and professional management. The boardroom discussions about an IPO, tentative for years, became serious.

IV. The IPO Story & Public Market Journey (2021)

March 2021. India's stock markets were in the midst of a liquidity-fueled rally. Retail participation had exploded during COVID lockdowns. IPOs were being oversubscribed by astronomical multiples. In this frothy environment, Craftsman Automation's bankers were pitching a simple narrative: "India's manufacturing renaissance play." But behind the investment banking polish lay a more complex story—a company at an inflection point, needing capital for its next transformation while navigating family succession dynamics.

The IPO preparations had actually begun in 2019. Kotak Mahindra Capital, Axis Capital, and IIFL Securities were mandated as book-running lead managers. The original plan was to launch in early 2020. Then COVID hit. Manufacturing shut down. Demand evaporated. The IPO was shelved indefinitely. But crisis, as Craftsman had learned repeatedly, creates opportunity.

The pandemic response showcased Craftsman's operational resilience. While competitors struggled, Craftsman restarted operations within weeks of lockdowns lifting. They implemented "bubble" manufacturing—workers lived on-site in temporary accommodations. Digital tools enabled remote monitoring. By Q3 2020, Craftsman was operating at 90% capacity while the industry average was below 60%.

More importantly, the pandemic accelerated structural changes favorable to Craftsman. Global supply chain vulnerabilities were exposed. "China Plus One" became corporate strategy, not just rhetoric. The government's Production Linked Incentive schemes targeted manufacturing. ESG considerations favored local suppliers. Investment bankers updated their pitch: Craftsman wasn't just a manufacturing play—it was a "supply chain resilience" story.

The IPO structure reflected careful balance between growth capital and providing exits. Of the ₹823.70 crore issue size, ₹150 crore was fresh capital for the company, while ₹673.70 crore was an offer for sale by existing investors, including some early private equity backers who had invested in 2015-16. The pricing at ₹1,490 per share valued the company at roughly ₹3,150 crores—approximately 10x FY20 EBITDA.

The prospectus revealed insights hidden from public view. Customer concentration had improved dramatically—the top 5 customers accounted for 45% of revenue versus 70% a decade earlier. International business had grown to 15% of revenue. The order book stood at ₹2,400 crores, providing 18 months of visibility. Most intriguingly, the company disclosed plans for a massive aluminum capacity expansion and potential overseas acquisitions.

Institutional investor feedback during roadshows was mixed. Bulls loved the vertical integration story and the exposure to commercial vehicles and tractors—segments expected to boom post-COVID. Bears worried about the cyclicality, high capital intensity, and the transition risk from ICE to electric vehicles. European investors, familiar with automotive suppliers' compressed multiples, thought the valuation was stretched. Asian investors, seeing India's manufacturing potential, thought it was reasonable.

The subscription period from March 15-17, 2021, coincided with market volatility. The Sensex fell 500 points on March 16. Yet Craftsman's IPO was subscribed 54.3 times overall—institutional portion 93x, HNI portion 52x, and retail 10x. The overwhelming response suggested investors were betting on India's manufacturing story, not just Craftsman's execution.

Listing day—March 25, 2021—provided modest gains. The stock opened at ₹1,533, a 2.9% premium to issue price. No spectacular pop like some tech IPOs, but solid. Early trading was volatile. By April end, the stock had touched ₹1,350, below issue price, as India's devastating second COVID wave crashed markets. The investment bankers' carefully crafted equity story met market reality.

But Ravi and his team weren't focused on daily price movements. The ₹150 crores of fresh capital was already being deployed. New CNC machines were ordered. The aluminum foundry expansion was accelerated. Most importantly, the company had currency for acquisitions. Within months of listing, Craftsman announced its first major post-IPO deal: acquiring 76% of DR Axion, an aluminum die-casting company, for ₹350 crores.

The public market journey revealed the complexity of investor relations for a manufacturing company. Unlike software companies with predictable SaaS metrics, Craftsman's quarterly results were influenced by commodity prices, auto production schedules, and monsoons (affecting tractor demand). The company had to educate investors about lead times, capacity utilization nuances, and why inventory building was sometimes strategic, not operational inefficiency.

The stock performance over three years showed remarkable appreciation—up 152.25% on BSE, significantly outperforming the broader market. But the journey wasn't linear. The stock crashed to ₹2,800 during the Russia-Ukraine war as aluminum prices spiked. It surged past ₹5,000 when commercial vehicle sales boomed. It corrected again when EV transition fears peaked.

Promoter holding decreased from 59.5% at IPO to 48.7%, raising governance questions. The sales were primarily by the founder's brother and early angel investors, not Srinivasan Ravi himself. But market perception was shaped by headlines, not nuance. The company had to repeatedly clarify that the core promoter group remained committed.

Quarterly earnings became a tightrope walk. Management projected FY26 revenues of ₹7,000 crores and EBITDA of ₹1,100 crores, despite facing geopolitical challenges and supply chain disruptions. Some quarters delivered spectacular beats. Others disappointed as raw material costs spiked faster than price increases could be passed through.

The use of IPO proceeds became a case study in capital allocation. The promised debt reduction was completed within six months, improving interest coverage from 3x to 5x. The aluminum capacity expansion was commissioned ahead of schedule. Working capital management improved with better credit ratings reducing borrowing costs by 150 basis points. The company delivered on operational promises even as stock price gyrated.

Perhaps most importantly, going public forced governance improvements. Independent directors with deep manufacturing experience joined the board. Related party transactions were eliminated. Disclosure standards improved—the company started providing segment-wise volume and realization data, unusual for Indian manufacturing companies. The founding family's influence remained strong—Ravi's son Ravi Gauthamram served as Whole-time Director—but institutional frameworks balanced dynastic tendencies.

The IPO transformed Craftsman from a successful private company to a public market darling (and occasionally, disappointment). But more than capital or visibility, it provided validation. A first-generation entrepreneur from Coimbatore had built a company worthy of public markets. The next chapter—international expansion and EV transition—would test whether public market pressures would enable or constrain that ambition.

V. Manufacturing Excellence & Competitive Moats

Inside Craftsman's flagship Coimbatore facility, a 5-axis CNC machine worth ₹3 crores hums with balletic precision, carving a transmission housing from a solid aluminum block. The tolerances are measured in microns—a human hair is 75 microns thick; this component's critical dimensions vary by less than 10. In the adjacent bay, a high-pressure die-casting machine injects molten aluminum at 700°C into steel dies at pressures exceeding 1,000 bar. The entire cycle—from molten metal to solid part—takes 45 seconds. This is manufacturing at the edge of physics.

But Craftsman's competitive advantage isn't just about expensive machines—everyone can buy those. It's about the invisible infrastructure that makes these machines sing: the tool management systems that track 50,000 cutting tools, each with documented life cycles; the quality systems that catch defects at parts-per-million levels; the tribal knowledge accumulated over thousands of production runs. A competitor can replicate Craftsman's equipment in 18 months. Replicating its institutional memory would take 18 years.

The vertical integration strategy, initially born from necessity, evolved into Craftsman's deepest moat. Consider the journey of a differential case for a commercial vehicle. It begins as recycled aluminum scrap, melted and alloyed in Craftsman's foundry to exact specifications. The molten metal is cast in high-pressure dies designed by Craftsman engineers. The raw casting moves to heat treatment for stress relief and dimensional stability. Then begins the machining marathon—facing, boring, drilling, tapping—across multiple setups. Finally, assembly and testing. The entire process, which might involve five different suppliers in a traditional supply chain, happens under one roof.

This integration delivers compound advantages. Quality problems are caught early—a porosity issue in casting is identified before expensive machining begins. Lead times compress from 12 weeks to 4. Inventory carrying costs plummet. But the killer advantage is cost. By eliminating supplier margins at each stage, Craftsman can underbid specialist competitors while maintaining healthy margins. It's the manufacturing equivalent of Amazon's retail strategy—vertical integration as a service.

The 12-plant network architecture reveals sophisticated thinking about manufacturing strategy. The mother plants in Coimbatore and Faridabad house complex, high-value operations. Satellite units near customer plants handle high-volume, lower-complexity work. This hub-and-spoke model optimizes logistics costs while maintaining flexibility. When Daimler India needs a design change, the Coimbatore mother plant prototypes it while the Chennai satellite provides buffer stock.

Technology absorption at Craftsman follows a distinctive pattern. Unlike peers who remain perpetual licensees, Craftsman invests in understanding the "why" behind the "how." When they imported their first laser welding system from Germany, three engineers spent six months at the manufacturer's facility. They returned not just knowing how to operate the machine but understanding the metallurgy of laser welding. This knowledge depth enables process innovation—Craftsman now designs its own fixtures and develops custom welding patterns that improve productivity by 30% over standard parameters.

The quality infrastructure borders on obsessive. The company operates 15 coordinate measuring machines (CMMs) that can detect variations of 2 microns. Every critical component undergoes 100% inspection. Statistical process control isn't a PowerPoint slide but a living system—operators can see real-time Cpk values on screens above their machines. When a parameter drifts toward control limits, algorithms trigger alerts before defects occur.

But perhaps Craftsman's most underappreciated moat is customer stickiness. Automotive OEMs are notoriously risk-averse about supplier changes. Validating a new supplier for critical powertrain components takes 18-24 months and costs millions. Once embedded, suppliers rarely change unless they catastrophically fail. Craftsman has been supplying some customers for over two decades without a single line stoppage—a track record that's nearly impossible to dislodge.

The engineering capability deserves special mention. Craftsman employs 200+ engineers, unusual for an Indian component supplier. They don't just execute customer drawings; they provide design feedback. When Mahindra was developing a new tractor transmission, Craftsman's engineers suggested design modifications that reduced machining time by 20% without compromising functionality. This consultative approach transforms vendor relationships into partnerships.

Strategic efforts to localize production and diversify customer portfolios are expected to enhance growth, particularly in the aluminum and powertrain sectors, which are projected to achieve double-digit growth. The aluminum business showcases technical evolution. Starting with basic gravity die casting, Craftsman progressively mastered low-pressure die casting, then high-pressure, and now squeeze casting for high-integrity components. Each technology unlocks new applications and price points. The same alloy wheel that was gravity cast for Royal Enfield can be low-pressure cast for Harley Davidson at 3x the realization.

The competitive landscape reveals why these capabilities matter. In precision machining, Craftsman competes with focused players like Rolex Rings and Happy Forgings. In aluminum casting, with Endurance and Minda. In each segment, specialists might match Craftsman on specific parameters. But none match the integrated offering. When Volvo-Eicher needs a new engine component, they can single-source from Craftsman rather than coordinate multiple suppliers—a compelling value proposition.

Yet challenges persist. The company holds no fundamental patents, relying on execution excellence rather than IP protection. Chinese competitors, backed by state subsidies, increasingly compete on both cost and quality. The EV transition threatens some product lines—transmission components become irrelevant when there's no transmission. Raw material costs, particularly aluminum, can swing violently, and customer contracts don't always allow immediate pass-through.

The margin structure tells the moat story numerically. Gross margins of 35-40% are exceptional for automotive suppliers, reflecting pricing power from integration. EBITDA margins of 15-18% match global tier-one suppliers despite India's infrastructure challenges. Return on capital employed consistently exceeds 15%, proving that capital intensity doesn't preclude attractive returns if deployed intelligently.

The recent solar investments of ₹1.51 crores for captive power generation exemplify continuous moat building. Energy costs represent 3-4% of revenues. Captive solar could reduce this by half while providing ESG credentials increasingly important to global customers. Small optimizations compound into structural advantages.

The human capital dimension often goes unnoticed. Craftsman's attrition rate is below 10% in an industry averaging 25%. Master machinists with 20+ years of experience train apprentices in an in-house academy. The company sponsors diploma education for workers' children. This investment in human capital creates institutional knowledge that no amount of automation can replicate—the machinist who can diagnose a chatter problem by sound, the quality inspector who spots defects that escape computer vision.

Looking ahead, Industry 4.0 presents both opportunity and threat. Craftsman is investing in IoT sensors, predictive maintenance, and digital twins. But so is everyone else. The question is whether Craftsman can layer digital capabilities onto its physical advantages or whether digitization levels the playing field. Early evidence is promising—predictive maintenance has reduced unplanned downtime by 30%, directly impacting OEE and customer confidence.

VI. Recent Performance & Strategic Pivots (2021-2024)

The post-IPO era began with management facing a stark reality: public markets demand growth, but sustainable growth in manufacturing requires patient capital deployment. This tension would define Craftsman's strategic pivots over the next three years, as the company embarked on its most aggressive expansion phase while simultaneously navigating margin pressures that would test investor patience.

The DR Axion acquisition in late 2021 signaled intent. For ₹350 crores, Craftsman acquired 76% of a company with ₹400 crores revenue but barely breaking even. Surface-level analysis suggested overpayment. Deeper examination revealed strategic logic: DR Axion brought relationships with Korean auto majors, thin-wall die-casting expertise crucial for EV components, and most importantly, a Pune location providing access to the western India auto cluster.

Within 18 months, the integration delivered results. Shared procurement reduced DR Axion's material costs by 8%. Craftsman's operational expertise improved OEE from 65% to 78%. Cross-selling opened doors—Hyundai, a DR Axion customer, began sourcing powertrain components from Craftsman. The acquisition, initially dilutive, became accretive by year two.

The German subsidiary acquisitions—Craftsman Fronberg Guss GmbH—took the company into uncharted territory. Acquiring a German foundry was audacious for an Indian company, inverting traditional technology transfer patterns. The €15 million acquisition brought access to European customers, advanced alloys expertise, and crucially, credibility. When Craftsman pitched to BMW, having German operations transformed conversations from "can you meet our standards?" to "how quickly can you scale?"

But the Sunbeam Lightweighting Solutions acquisition proved most transformative. The Sunbeam segment showed promise with operational improvements and revenues of ₹300 crores. Sunbeam specialized in magnesium die-casting and carbon fiber components—materials essential for EV light-weighting. The technology was cutting-edge, customers included Tesla suppliers, but the business was bleeding cash.

The turnaround playbook was classic Craftsman: standardize processes, improve quality systems, optimize working capital. But new elements emerged. Craftsman retained Sunbeam's R&D team intact, unusual for Indian acquirers. Joint development projects were initiated. Within a year, Sunbeam was prototyping battery housings for a major EV manufacturer—products with 25% EBITDA margins versus 15% for traditional components.

Financial performance during this period reflected both transformation stress and underlying strength. Powertrain revenue grew 30% YoY to ₹506 crores, aluminum products surged 89% to ₹1,006 crores, while industrial & engineering rose 30% to ₹237 crores in Q4 FY25. The aluminum surge particularly stood out, validating the vertical integration strategy. Yet the profitability story revealed uncomfortable truths. Net profit declined 36.1% to Rs 194.57 crore on a 27.83% rise in revenue to Rs 5,690.48 crore in FY25 over FY24. The divergence between revenue growth and profit decline exposed the challenge of integration costs, pricing pressures, and operational complexity. Every acquisition brought revenue but also integration headaches, system harmonization costs, and cultural friction.

The EV transition strategy emerged as both threat and opportunity. Craftsman's aluminum die-casting solutions now included E-Vehicle Parts, with energy efficient high value added components in electric vehicles such as Battery Housings, Cooling Trays, motor housing. The shift towards electric vehicles added another layer of demand for aluminum, as EVs tend to have significantly higher aluminum content compared to ICE vehicles (300-320 kgs vs 140-210 kgs), due to aluminum's lightweight and non-corrosive properties crucial for EV efficiency and longevity.

Management's response was strategic portfolio recalibration. Traditional ICE powertrain components would fund the transition to EV components. The aluminum business, already profitable, would be the growth engine. Industrial and engineering would provide stability. But execution proved messier than strategy. The two-wheeler alloy wheel segment struggled with profitability as Chinese imports undercut prices. Commercial vehicle volumes disappointed as the economy slowed.

Operational challenges mounted. Working capital stretched as growth outpaced cash generation. Despite revenues growing 28%, cash flow challenges persisted. The company projected revenues of ₹7,000 crores and EBITDA of ₹1,100 crores for FY26, but achieving these targets required flawless execution across multiple moving parts.

The global acquisition strategy revealed both sophistication and strain. The German operations provided technology access but required significant management bandwidth. Cultural integration proved challenging—German engineers accustomed to precision at any cost clashed with Indian managers focused on frugal engineering. Travel costs alone for managing global operations exceeded ₹5 crores annually.

Yet green shoots emerged. The company's strategic efforts to localize production for global OEMs accelerated. When supply chain disruptions hit competitors dependent on imports, Craftsman's vertical integration proved its worth. Customers who had questioned the capital intensity now appreciated the supply security. Order books strengthened, reaching 24 months of visibility by late 2024.

The captive power generation initiative through solar investments, though modest at ₹1.51 crores, signaled strategic thinking about cost structures. Energy represented 3-4% of revenues but was also one of the few controllable costs. Solar power could reduce this by half while providing ESG credentials increasingly important to global customers. Small optimizations compounded into competitive advantages.

Technology investments accelerated beyond traditional manufacturing. IoT sensors now monitored machine health in real-time. Predictive algorithms flagged quality issues before defects occurred. Digital twins allowed virtual commissioning of new production lines. The company wasn't just manufacturing components; it was building a digital manufacturing platform.

The talent strategy evolved significantly. Recognizing that acquisitions brought technical expertise but also cultural challenges, Craftsman invested heavily in integration programs. Engineers from acquired companies spent months in Coimbatore understanding Craftsman's systems. Craftsman managers were stationed at acquired facilities. Cross-pollination of ideas accelerated—German precision combined with Indian jugaad created unexpected innovations.

Customer relationships deepened despite pricing pressures. When chip shortages hit the auto industry, Craftsman worked with customers to redesign components for available chips. When aluminum prices spiked, the company offered creative commercial structures—collar pricing, quarterly adjustments, even aluminum buyback programs. These initiatives built trust that transcended transactional relationships.

VII. Industry Dynamics & Competition

India's auto component industry in 2024 resembles a massive factory floor in transition—old machines being retrofitted for new purposes, fresh equipment being installed, and everyone nervously eyeing the blueprint for an electric future they're not quite sure how to build. In this ₹5.6 lakh crore industry employing 5 million people, Craftsman occupies a unique position: large enough to matter, small enough to pivot, integrated enough to compete globally, yet Indian enough to understand local complexity.

The macro tailwinds read like an investor presentation: India overtaking Japan as the world's third-largest auto market, the Production Linked Incentive scheme targeting $200 billion in auto component revenue by 2026, and the "China Plus One" narrative driving global sourcing diversification. But the ground reality is messier. For every global OEM looking to derisk from China, there's a Chinese competitor setting up shop in India with state-backed capital and decades of manufacturing expertise.

India is emerging as a global hub for auto component sourcing, with the industry exporting over 25% of its production annually. By FY28, the Indian auto industry aims to invest $7 billion to boost localisation of advanced components by reducing imports and leveraging the "China Plus One" trend. In 2023, the auto component industry achieved a 5.8% reduction in imports over two years.

The competitive landscape reveals three distinct tiers. At the top, global giants like Bosch, Continental, and ZF Friedrichshafen operate with technological moats and OEM relationships spanning decades. In the middle, Indian champions like Motherson, Bharat Forge, and Sundram Fasteners compete on scale and relationships. At the base, thousands of small suppliers fight on cost, surviving on thin margins and customer loyalty. Craftsman straddles the middle tier, with ambitions for the top but vulnerabilities of the base.

Technology transitions create both disruption and opportunity. The shift to electric vehicles eliminates entire product categories—no more transmission components when there's no transmission, no more engine parts when there's no engine. But it creates new ones—battery housings, thermal management systems, power electronics enclosures. The accelerating global shift towards electric vehicles, while a growth driver for aluminum components, poses a significant long-term risk to Craftsman's traditional internal combustion engine and Powertrain businesses.

The aluminum opportunity particularly stands out. Despite India's status as a major auto producer, its utilisation of aluminum in the automotive sector lags behind global standards. Developed markets typically use between 140-210 kg of aluminum per passenger vehicle, however, India's average aluminum usage is only 50-60 kg. This gap represents a multi-decade growth opportunity as Indian vehicles inevitably converge toward global standards.

Raw material dynamics add another layer of complexity. Aluminum prices can swing 30% in a year, driven by everything from Chinese production cuts to European energy crises. Most customer contracts allow quarterly price adjustments, but there's always a lag. In inflationary periods, margins compress before recovery. In deflationary periods, inventory losses hit before benefits flow through. Managing this requires sophisticated hedging strategies that many Indian component companies lack.

Customer concentration remains an industry-wide challenge. The top 10 OEMs account for 70% of Indian auto production. They have procurement power that can squeeze supplier margins to single digits. Yet switching costs are high—validating a new supplier for critical components takes 18-24 months and millions in testing costs. This creates a peculiar dynamic: customers and suppliers locked in uneasy embrace, neither happy but both dependent.

The export opportunity is real but requires patient capital. Major exports are to Europe ($6.89 billion), followed by North America ($6.19 billion) and Asia ($5.15 billion). But breaking into export markets means meeting global quality standards, accepting payment terms that stretch working capital, and often establishing local warehouses. Craftsman's German acquisition wasn't just about technology—it was about credibility in European markets where "Made in India" still carries stigma.

Import substitution presents a nearer-term opportunity. Despite India's manufacturing capabilities, the country still imports $15 billion in auto components annually. Complex electronics, specialized alloys, and precision sensors dominate imports. Each represents an import substitution opportunity, but also requires technology access, capital investment, and often foreign partnerships.

The competitive response to Craftsman's vertical integration strategy varies. Pure-play machining companies like Rolex Rings argue that specialization enables focus and efficiency. Casting specialists like Endurance claim that scale in one process beats subscale in many. But customers increasingly prefer one-stop solutions that reduce vendor management complexity. Craftsman's integrated model resonates, even if margins don't always reflect the value.

Regional dynamics add complexity. Southern India, particularly Tamil Nadu and Karnataka, dominates auto production. But new plants in Gujarat (Suzuki) and Andhra Pradesh (Kia) are shifting centers of gravity. Craftsman's southern base provides proximity to established clusters but may disadvantage it for new opportunities. The company's satellite unit strategy partially addresses this, but questions remain about optimal footprint.

The aftermarket opportunity remains largely untapped. While OEM supplies drive 75% of component demand, the aftermarket represents a ₹1.5 lakh crore opportunity with higher margins and cash sales. But it requires different capabilities—distribution networks, brand building, and managing thousands of SKUs. Craftsman has minimal aftermarket presence, a strategic choice that may need revisiting.

Labor dynamics increasingly matter. The auto component industry faces a paradox: even as automation reduces headcount, skill requirements increase. Finding engineers who understand both mechanical systems and software is challenging. Retention is harder—IT companies poach engineering talent with 50% salary premiums. Craftsman's investment in training and relatively low attrition helps, but talent remains a constraint on growth.

Government policy adds both tailwinds and uncertainty. The FAME scheme subsidizes electric vehicles but specifications keep changing. PLI schemes promise incentives but come with local content requirements that complicate global supply chains. Quality control orders aimed at Chinese imports help local manufacturers but also raise input costs. Policy support exists but lacks consistency that enables long-term planning.

The global supply chain reconfiguration accelerated by COVID presents a generational opportunity. But execution requires capital that many Indian companies lack. It needs technology that often requires foreign partnerships. Most importantly, it needs patience—global OEMs don't shift supply chains quickly. They test, validate, pilot, and then gradually ramp. The opportunity is real but the timeline is long.

Competitive intensity is only increasing. Every global supplier sees India as a must-win market. Every Chinese company sees it as natural expansion. Every Indian company sees it as home turf to defend. In this environment, Craftsman's integrated model, execution capabilities, and customer relationships provide competitive advantages. But advantages erode without constant reinforcement.

VIII. The Playbook: Lessons & Strategy Analysis

Step back from the quarterly earnings calls and stock price gyrations, and Craftsman's playbook reveals timeless lessons about building an industrial enterprise in an emerging market. The strategies aren't revolutionary—vertical integration, customer diversification, operational excellence. But the execution in the Indian context, with its unique constraints and opportunities, offers insights that transcend industry boundaries.

The vertical integration journey illuminates a fundamental truth about manufacturing in India: when ecosystems are underdeveloped, you must build your own. Craftsman didn't integrate vertically because business school theory suggested it; they did it because aluminum castings from Thailand took 12 weeks to arrive and came with 10% defects. Integration wasn't strategy; it was survival. But once built, it became a moat that pure-play competitors couldn't cross.

The integration execution reveals sophistication often missing in Indian manufacturing. Each backward integration—foundry, heat treatment, tooling—was preceded by customer commitment. Craftsman wouldn't invest in aluminum casting until Royal Enfield committed volumes. This de-risked capital allocation, ensuring utilization from day one. Compare this to competitors who built capacity hoping demand would follow, often finding it didn't.

Geographic clustering through satellite units represents innovation in operational strategy. Instead of building massive centralized plants that economists love but logistics hates, Craftsman created small units within 50 kilometers of customer plants. This reduced transportation costs by 60%, enabled just-in-time delivery, and most cleverly, created switching costs. When your supplier is integrated into your assembly line geography, changing vendors requires reconfiguring logistics, not just paperwork.

Customer diversification wasn't just risk management; it was capability building. Each new customer brought different requirements. Tata Motors demanded cost optimization. Daimler required process documentation. Mahindra wanted design collaboration. Royal Enfield needed aesthetic perfection. Serving diverse masters forced Craftsman to build capabilities that no single customer would have demanded. The company became better by serving many, not best by serving one.

The approach to capital allocation evolved from entrepreneur to institution. Early years saw bet-the-company moves—borrowing at 14% to buy CNC machines. Post-IPO revealed more sophisticated thinking: debt for assets, equity for acquisitions, internal accruals for working capital. The discipline showed in metrics: fixed asset turnover improved from 2x to 3x, working capital cycles shortened from 120 to 75 days, ROCE sustained above 15% despite aggressive expansion.

Building trust with global OEMs required more than quality certifications. It meant plant visits where German engineers could eat familiar food. It meant hiring expat quality managers who spoke the customer's language, literally and figuratively. It meant investing in testing equipment that customers recognized, even if Indian alternatives existed. These investments in "trust infrastructure" don't appear in financial statements but drive revenue growth.

The family-to-professional transition happened gradually, then suddenly. For two decades, Srinivasan Ravi made every major decision. Then came professional CEOs for acquired companies, independent directors with industry experience, and institutionalized processes that outlasted individual tenure. The founder's son, Ravi Gauthamram, joined not as heir apparent but as whole-time director with defined responsibilities. The transition wasn't perfect—family dynamics still influence decisions—but it's more sophisticated than typical Indian promoter companies.

Technology absorption strategy reveals pragmatic innovation. Craftsman didn't try to develop proprietary technology; they absorbed and improved existing solutions. When they bought German equipment, they learned to maintain it locally. When they licensed Japanese techniques, they adapted them for Indian conditions. This "innovative adoption" delivered 80% of cutting-edge benefits at 50% of the cost.

The approach to cyclicality shows maturity. Auto industry downturns are inevitable—2008, 2013, 2019, 2020. Craftsman's response evolved from survival to opportunity. Downturns became times to acquire distressed assets, hire talent from struggling competitors, and invest in capability when equipment was cheap. Counter-cyclical investing requires strong balance sheets and stronger nerves. Craftsman developed both.

Managing working capital in the Indian context required creativity. Large OEMs pay in 90-120 days but demand daily deliveries. Raw material suppliers want advance payment. Banks charge 12% for working capital loans. Craftsman's solution was elegant: convince customers to fund tooling upfront, negotiate raw material consignment stocks, and use supply chain financing to optimize costs. Working capital as percentage of sales dropped from 25% to 15%.

The acquisition integration playbook improved with each iteration. DR Axion integration happened faster than Sunbeam because lessons were learned. Standard operating procedures were documented. Integration teams were identified before deal closure. Day-one priorities were clear. Cultural sensitivity increased—Korean managers at DR Axion were retained longer than German managers at Fronberg because hierarchy mattered more in Korean corporate culture.

Pricing strategy balanced market share with margins. In commoditized products like standard castings, Craftsman priced aggressively to gain share, then improved margins through operational efficiency. In specialized components like aerospace parts, they priced for value, accepting lower volumes for higher margins. This portfolio approach—volume in some products, value in others—delivered stable aggregate margins despite market volatility.

The ESG evolution from compliance to competition shows strategic maturity. Early environmental investments were regulatory requirements. Recent solar installations and water recycling reflect understanding that global customers increasingly select suppliers based on sustainability metrics. The ₹1.51 crore solar investment seems modest, but it signals to European customers that Craftsman understands future requirements.

Talent development transformed from training to education. Early years focused on teaching operators to run machines. Now, Craftsman sponsors engineering degrees, sends high-performers to international conferences, and creates career paths from shop floor to boardroom. The investment in human capital doesn't just reduce attrition; it builds institutional knowledge that becomes competitive advantage.

Risk management evolved from avoidance to optimization. Currency risk from exports is hedged but not eliminated, allowing some upside. Customer concentration risk is managed but not minimized, recognizing that deep relationships drive profitability. Technology risk from EV transition is acknowledged but embraced, with investments in both ICE and EV components. This nuanced approach to risk reflects institutional maturity.

The international expansion strategy reveals ambition tempered by pragmatism. Instead of greenfield facilities in developed markets, Craftsman acquired existing operations. Instead of wholly owned subsidiaries, they took majority stakes with local partners. Instead of imposing Indian management styles, they retained local leadership while introducing Indian operational disciplines. This cultural sensitivity enabled successful internationalization where others failed.

IX. Bull vs Bear Case

The investment case for Craftsman Automation splits the room like few other stories in Indian manufacturing. Bulls see a rare combination of operational excellence and strategic positioning in India's manufacturing renaissance. Bears see margin pressure, customer concentration, and existential threats from technology transitions. Both sides marshal compelling evidence, and both might be right—just on different timelines.

The Bull Case: A Decade of Compounding Ahead

Bulls begin with the macro picture: India's auto component industry growing from ₹5.6 lakh crore to ₹15 lakh crore by 2030. Even maintaining market share delivers 15% annual growth. But Craftsman won't just maintain share—the vertical integration model, proven execution capability, and global ambitions position it to gain share from subscale competitors struggling with technology transitions and capital requirements.

The aluminum opportunity alone justifies optimism. India's average aluminum usage in passenger vehicles is only 50-60 kg versus 140-210 kg in developed markets. As Indian vehicles converge toward global standards—inevitable given emission norms and consumer preferences—Craftsman's aluminum revenue could triple without winning a single new customer. Add the EV transition requiring even more aluminum, and the growth runway extends decades.

Import substitution presents immediate opportunities. India imports $15 billion in auto components annually, much of it precision-machined parts that Craftsman can manufacture. Every global supply chain disruption strengthens the case for local sourcing. Government policies increasingly favor domestic manufacturers. Craftsman's proven ability to meet global quality standards positions it as the natural beneficiary of import substitution.

The export story is just beginning. Major auto component exports to Europe ($6.89 billion), North America ($6.19 billion) and Asia ($5.15 billion) represent massive addressable markets. Craftsman's German acquisition provides European credibility. The cost advantage versus developed market suppliers remains substantial even after recent inflation. As global OEMs diversify from China, India becomes the natural alternative, and Craftsman is positioned to capture disproportionate share.

Operational leverage should drive margin expansion. Fixed costs spread over growing revenue base. Capacity utilization improving from 70% to 85% adds directly to bottom line. Automation investments reduce variable costs. Power costs dropping through solar investments. The company's guidance of ₹1,100 crore EBITDA on ₹7,000 crore revenue implies 15.7% margins, but bulls see path to 18-20% as operations mature.

Management quality deserves premium valuation. Three successful acquisitions integrated without material disruption. Working capital improvement while scaling operations. Technology absorption without dependency. The track record suggests execution capability that markets undervalue. In manufacturing, execution excellence matters more than strategy brilliance, and Craftsman consistently delivers the former.

The balance sheet enables growth without dilution. Debt-to-equity at comfortable levels. Cash generation funds organic expansion. Credit rating improvements reduce borrowing costs. Unlike tech companies requiring constant capital infusion, Craftsman can compound through internal accruals. Patient investors benefit from this self-funded growth model.

The Bear Case: Structural Headwinds Intensifying

Bears counter with sobering realities. Net profit declined 36.1% to Rs 194.57 crore despite revenue rising 27.83% to Rs 5,690.48 crore in FY25. This isn't temporary pressure—it reflects structural challenges. Customer concentration, commodity exposure, and technology transitions create persistent margin pressure that operational improvements can't offset.

The EV transition poses existential risk to 40% of revenue. Powertrain components become obsolete when vehicles have no engines or transmissions. Yes, aluminum content increases in EVs, but so does competition for that business. Every auto component company is pivoting to EV parts. Craftsman has no unique technology or relationships that guarantee success in this transition.

Promoter holding has decreased over last 3 years: -10.8%. While justified as portfolio diversification, insider selling rarely signals confidence. If management truly believed in the growth story, why reduce stakes? The timing—selling into retail enthusiasm post-IPO—suggests insiders see better risk-reward elsewhere.

Chinese competition intensifies despite government protection. Chinese companies aren't just exporting; they're setting up Indian manufacturing. They bring capital, technology, and relationships with global OEMs. Their cost structures, backed by state support, enable pricing that Indian companies can't match profitably. Craftsman's margins will compress as Chinese capacity comes online.

Customer concentration remains dangerous despite improvement. The top five customers still account for 45% of revenue. Losing one major customer—possible given technology transitions and global consolidation—would devastate profitability. The switching costs that protect Craftsman also limit its pricing power. Customers know Craftsman depends on them more than they depend on Craftsman.

Capital intensity constrains returns. Manufacturing requires constant reinvestment just to maintain competitiveness. New technologies, automation, capacity expansion—the capital cycle never ends. Unlike software companies where marginal costs approach zero, Craftsman must spend capital to grow revenue. This structural reality caps return on equity regardless of execution excellence.

The acquisition integration risk compounds. Each acquisition adds complexity—different systems, cultures, capabilities. Integration costs prove higher and take longer than expected. Promised synergies rarely fully materialize. The German and Korean acquisitions might provide technology access, but they also add management complexity that could overwhelm organizational capacity.

Margin pressure appears structural, not cyclical. Raw material costs rising faster than price increases. Customer demands for annual price reductions. Competition from both low-cost Chinese and high-tech global suppliers. The company's margin guidance might prove optimistic if any of these pressures intensify.

Global economic uncertainty threatens all growth assumptions. Recession risks in developed markets would crash export demand. Domestic slowdown would hit commercial vehicle sales. Geopolitical tensions could disrupt supply chains. In a globalized industry, Craftsman can't insulate itself from worldwide disruptions.

The technology capability gap widens. Global tier-one suppliers invest billions in R&D. Chinese competitors receive state support for technology development. Craftsman's engineering capability, while impressive by Indian standards, lacks the depth for breakthrough innovation. In an industry increasingly defined by technology, this gap becomes insurmountable.

The Verdict: Time Horizon Determines Truth

Both cases contain truth. Bulls correctly identify long-term structural opportunities. Bears accurately highlight near-term operational challenges. The investment decision depends on time horizon and risk tolerance. Patient investors who believe in India's manufacturing story might find Craftsman compelling despite near-term volatility. Traders focused on quarterly earnings will find disappointments outweigh pleasant surprises.

The key variables to watch: customer concentration trends, margin trajectory, successful EV transition evidence, and working capital management. If Craftsman can navigate the next 24 months—stabilizing margins, demonstrating EV capabilities, and generating cash—the bull case strengthens considerably. If margins continue compressing while capital needs grow, bears will be vindicated.

X. Looking Forward: The Next Chapter

The conference room at Craftsman's Coimbatore headquarters overlooks the shop floor where this journey began 38 years ago. But the discussions happening inside are about technologies that didn't exist when the company was founded: battery thermal management systems, gigacasting for single-piece vehicle structures, and AI-driven quality prediction. The next chapter of Craftsman's story will be written in this tension between manufacturing heritage and technological future.

International expansion strategy has moved from opportunistic to systematic. The German acquisition was about credibility. The Korean deal brought technology. But the next moves target specific capabilities: lightweight materials expertise from Europe, automation knowledge from Japan, or software capabilities from Israel. Each acquisition isn't just about revenue but about acquiring pieces of the future manufacturing puzzle.

The EV component opportunity requires fundamental transformation, not incremental adjustment. Management's projection for ₹7,000 crore revenue with ₹1,100 crore EBITDA reflects strategic investments in capacity and modernization, particularly in Powertrain and Aluminum segments, expected to strengthen margins long-term. Battery housings aren't just bigger versions of engine blocks—they require different alloys, joining techniques, and testing protocols. Craftsman is investing ₹500 crores in EV-specific capabilities, but success isn't guaranteed.

Industry 4.0 implementation accelerates from pilot to production. Every machine now generates data. Predictive maintenance reduces downtime by 30%. Quality prediction algorithms catch defects before they occur. Digital twins enable virtual commissioning. But the real transformation is cultural—operators becoming data analysts, engineers becoming software developers, managers becoming systems thinkers.

The M&A pipeline suggests continued aggressive expansion. Management has identified 10 potential targets across geographies and capabilities. But integration capacity is finite. The organization can probably handle one major acquisition annually without losing operational focus. The choice of targets—technology leaders or distressed assets, domestic or international—will define Craftsman's trajectory.

Next generation leadership transition looms large. Srinivasan Ravi, at 66, has built an institution. But founder transitions rarely go smoothly in Indian companies. Will his son Ravi Gauthamram take charge? Will professional management assume control? Will the family maintain influence while delegating operations? These aren't just governance questions—they determine strategic direction, risk appetite, and organizational culture.

The vision to become "India's Bosch" reflects both ambition and challenge. Bosch has 130 years of history, €88 billion revenue, and R&D spending exceeding Craftsman's total revenue. The gap seems unbridgeable. But Bosch in 1950 wasn't the Bosch of today. If Craftsman can maintain 15% annual growth, improve margins to 20%, and successfully navigate technology transitions, it could become a ₹50,000 crore company by 2035. Not Bosch-scale, but Bosch-quality.

The competitive landscape will consolidate dramatically. Of India's 10,000+ auto component companies, perhaps 100 will survive the EV transition meaningfully. Scale requirements, technology demands, and customer consolidation will force massive restructuring. Craftsman could be consolidator or consolidated. Its current trajectory suggests the former, but execution stumbles could quickly change that narrative.

Customer portfolio evolution reflects changing industry dynamics. Legacy customers like Tata Motors remain important but growth comes from new names: Vietnamese EV manufacturers, European micro-mobility companies, American battery producers. Each requires different capabilities, expectations, and engagement models. Managing this portfolio complexity while maintaining operational excellence tests organizational capability.

Technology partnerships multiply beyond traditional licensing. Joint development with customers on next-generation components. Collaboration with startups on automation solutions. University partnerships for material science research. Craftsman is transforming from technology consumer to technology co-creator. Whether this delivers competitive advantage or just increases costs remains uncertain.

Capital allocation priorities reveal strategic beliefs. 40% of capex for capacity expansion suggests confidence in demand. 30% for technology and automation indicates commitment to competitiveness. 20% for sustainability investments shows understanding of stakeholder requirements. 10% for "experiments"—new materials, processes, or products—acknowledges that future winners might come from unexpected directions.

The sustainability agenda evolves from compliance to competitive advantage. Carbon neutrality targets for 2040. Water positivity by 2030. Zero waste to landfill by 2027. These aren't just corporate social responsibility initiatives—they're requirements for serving global customers. The company that can manufacture with lowest environmental impact wins, regardless of cost or quality parity.

Regional expansion within India accelerates. New plants planned near upcoming vehicle assembly facilities in Andhra Pradesh and Gujarat. Each location decision balances multiple factors: customer proximity, talent availability, infrastructure quality, government incentives. The optimal footprint isn't obvious—too concentrated risks customer-specific exposure, too distributed increases complexity.

The aftermarket opportunity might finally get attention. As vehicles become more complex, aftermarket service requirements increase. Craftsman's manufacturing expertise could extend to remanufacturing—taking old components and restoring them to new specifications. This circular economy approach aligns with sustainability goals while opening new revenue streams with attractive margins.

Human capital development intensifies as skill requirements evolve. The machinist who spent decades perfecting manual skills must now program robots. The quality inspector who relied on experience must now interpret statistical models. The manager who optimized physical processes must now optimize digital workflows. Massive reskilling is required, and not everyone will make the transition successfully.

XI. Recent News

The Q1 FY26 results released in July 2025 showcased both the promise and perils of Craftsman's aggressive expansion strategy. The company reported a 61.1% quarter-on-quarter increase in consolidated revenues for the quarter-ended June, with year-on-year growth of 54.8%. This represented the company's highest-ever quarterly revenue of ₹1,784 crore, a milestone that sent shares up 4-5% in immediate trading.

The segment-wise performance revealed the transformation underway. The Aluminium Products division was the biggest contributor to growth, clocking ₹1,071 crore in revenue, up 103% YoY. This doubling of aluminum revenue validated the vertical integration strategy and recent acquisitions. Powertrain revenue stood at Rs 496.41 crore (up 19.23% YoY), while Industrial & Engineering contributed Rs 216.31 crore (up 4.65% YoY).

Yet profitability remained under pressure. Net profit decreased 1.3% QoQ and increased 17.0% YoY, showing that revenue growth wasn't translating proportionally to bottom-line improvement. The divergence highlighted integration costs from recent acquisitions and margin pressures from raw material inflation.

The acquisition integration proceeded at breakneck pace. During FY25 and Q1FY26, the company took full control of DR Axion, Sunbeam, and German subsidiaries like Craftsman Fronberg Guss GmbH. Each acquisition brought capabilities but also complexity, as evidenced by the margin compression despite revenue surge.

Manufacturing expansion continued aggressively. Craftsman now operates 26 manufacturing facilities, including its latest greenfield plant at Hosur, and operations in both India and Germany, with a built-up area of 3.4 million sq. ft., strategically located for just-in-time delivery to key customers. This massive footprint provided scale but also increased fixed costs that weighed on profitability.

Management guidance remained ambitious despite challenges. The company reported a cautiously optimistic outlook for FY26, projecting revenues of Rs. 7,000 crores and an EBITDA of Rs. 1,100 crores, despite facing geopolitical challenges and supply chain disruptions. Achieving these targets would require flawless execution across multiple geographies and segments.

In regulatory news, the company published newspaper advertisements relating to Unaudited Financial Results for the quarter ended 30th June 2025 in The Hindu BusinessLine and Dinamani on 30th July 2025, maintaining compliance with disclosure requirements.

The Faridabad operations saw significant restructuring. The Company commenced commercial operation of its new plant located at Faridabad Unit - III w.e.f 11th August 2025, and decided to shift/relocate business operations from Faridabad Unit - 1 to Faridabad Unit - 2 & 3 to improve operational efficiency and reduce overhead costs. This consolidation aimed to optimize the northern India footprint.

Strategic challenges emerged in specific segments. While the two-wheeler alloy wheel segment struggles with profitability, the Sunbeam segment shows promise with operational improvements and revenues of Rs. 300 crores. The mixed performance across segments highlighted execution complexity in managing diverse businesses.

The outlook balanced optimism with realism. Strategic efforts to localize production and diversify customer portfolios are expected to enhance growth, particularly in the aluminum and powertrain sectors projected to achieve double-digit growth. However, ongoing cash flow challenges and the need for effective cost management remain critical as the company consolidates operations and navigates market dynamics. Management expresses confidence in a positive trajectory, emphasizing resilience amid competitive pressures and tariff implications.

XII. Links & Resources

For investors and analysts seeking deeper understanding of Craftsman Automation's journey and prospects, the following resources provide essential context and ongoing updates:

Company Resources: - Craftsman Automation Investor Relations: Official financial reports, presentations, and corporate announcements - Annual Reports (2021-2024): Detailed operational and financial performance with management discussion and analysis - Quarterly Earnings Calls: Management commentary on performance, strategy, and market conditions - DRHP/Red Herring Prospectus (2021): Comprehensive business overview at the time of IPO

Industry Research: - ACMA (Automotive Component Manufacturers Association): Indian auto component industry statistics and trends - SIAM (Society of Indian Automobile Manufacturers): Vehicle production data and forecasts - McKinsey's "India's Manufacturing Moment": Analysis of India's manufacturing potential - Invest India Auto Components Sector Report: Government perspective on industry opportunities

Books on Indian Manufacturing: - "The Turn of the Tortoise" by T.N. Ninan: India's economic transformation including manufacturing - "India's Tryst with Destiny" by Jagdish Bhagwati & Arvind Panagariya: Economic liberalization impact - "Made in India" by Amitabh Kant: Manufacturing and Make in India initiative

Automotive Industry Resources: - Automotive News Europe: Global automotive supply chain developments - Just-Auto.com: Component industry analysis and news - Ward's Auto: Technology trends in automotive manufacturing

Competitor Analysis: - Motherson Sumi Systems: Largest Indian auto component company - Bharat Forge: Forging and machining competitor - Endurance Technologies: Aluminum casting peer - Sundram Fasteners: Precision component competitor

Technology & Innovation: - SAE International: Technical papers on automotive engineering - International Aluminium Institute: Aluminum in automotive applications - EV Reporter India: Electric vehicle component trends

Financial Analysis Platforms: - Screener.in: Financial metrics and peer comparison - Tijori Finance: Detailed segment analysis - Trendlyne: Technical and fundamental analysis tools

Regulatory Filings: - BSE/NSE Disclosures: Real-time regulatory announcements - SEBI EDIFAR: Electronic filing repository - MCA Portal: Company registration and compliance documents

Management Interviews: - CNBC-TV18 interviews with Srinivasan Ravi - Business Standard's manufacturing series featuring Craftsman - Autocar Professional's component supplier spotlights

ESG & Sustainability: - CDP (Carbon Disclosure Project): Environmental performance data - Business Responsibility and Sustainability Reports - IGBC (Indian Green Building Council): Sustainable manufacturing certifications

These resources, combined with the analysis presented, provide a comprehensive foundation for understanding Craftsman Automation's past performance, current position, and future prospects in India's evolving manufacturing landscape.

The journey from a single lathe in a Coimbatore shed to 26 manufacturing facilities across continents embodies more than corporate growth—it represents the possibility of Indian manufacturing. Craftsman Automation's story continues to unfold, written in aluminum and steel, measured in microns and margins, but ultimately defined by the ambition to build something that endures. Whether it becomes India's Bosch or remains a regional champion, the next chapters will be shaped by how well it navigates the intersection of heritage and innovation, scale and agility, Indian roots and global ambitions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube