Craftsman Automation: The Engineering DNA of the Indian Growth Story

I. Introduction & The Coimbatore Context

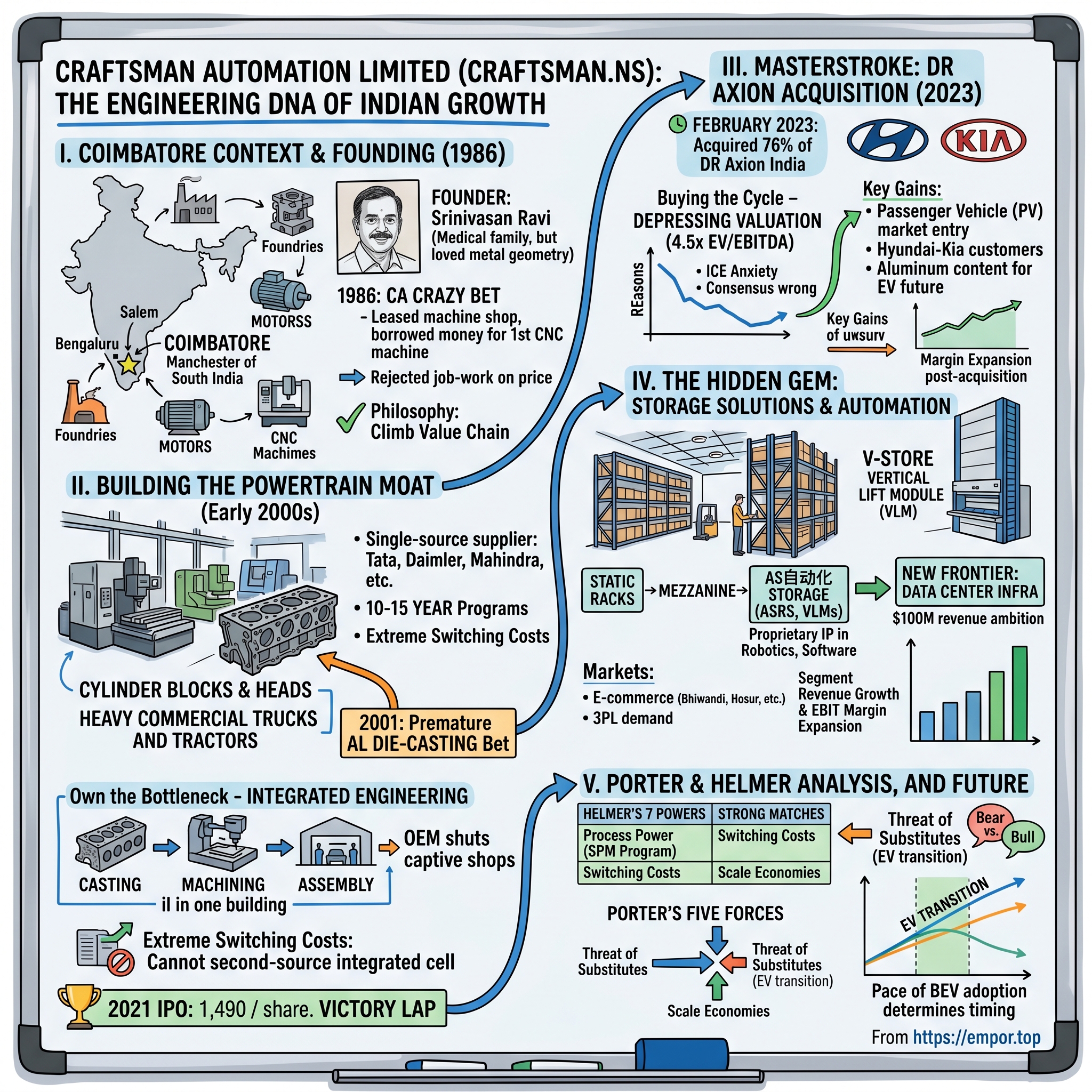

Drive south from Bengaluru, past the granite ridges of Salem, and you eventually descend into a valley where the air smells of cotton, cutting oil, and red earth. This is कोयंबटूर Coimbatore — the city that locals proudly call the "Manchester of South India," and which a German metallurgist once described, with grudging admiration, as the place where Indian heavy industry actually keeps its promises.

It is a strange town to stand in if you have been brought up on the consumer-tech version of the Indian growth story. There are no glass office parks named after fintech unicorns. There are no Lulu malls oozing café chains. Instead, the city is a quietly humming grid of foundries, motor-winding shops, textile mills, and CNC machining houses, many of them family-owned for three generations. Coimbatore exports pump motors to Africa, wet grinders to Sri Lanka, and — increasingly — cylinder heads, axle housings, and aluminum sub-assemblies to global automakers whose logos are nowhere on the building.

Out of this very specific ecosystem grew Craftsman Automation Limited, a company most retail investors in Mumbai still mispronounce. By May 2026, Craftsman commands a market capitalization of roughly ₹120 billion, give or take a trading session,1 and its parts ride inside almost every commercial truck and tractor sold in India. If you have eaten a meal in a Chennai apartment building delivered by a Tata Ace, you have, in some indirect way, been a customer.

The episode you are about to read is not a story about hyper-growth. It is a story about an engineer's obsession with precision, an entrepreneur's willingness to buy expensive German machines before he had the orders to feed them, and — in the most recent and most controversial chapter — a contrarian acquisition of a Korean-controlled aluminum business at the very bottom of an auto cycle, when the consensus said the world was about to abandon the internal combustion engine forever.

The roadmap is straightforward. We start in a leased machine shop in 1986, when a 25-year-old named श्रीनिवासन रवि Srinivasan Ravi walked away from a family of doctors and bought his first CNC machine on borrowed money. We then trace the slow construction of an integrated powertrain moat — castings, machining, assembly, all under one roof — that gradually made Craftsman the single-source supplier for the heaviest, hardest, ugliest parts inside a heavy-truck engine. We pivot to the 2023 acquisition of 디알액시온 DR Axion India,[^2] possibly the cleanest example of "buying the cycle" in Indian auto-component history. We dig into the company's least-understood limb — a storage and warehouse automation business that sells robotic vertical lift modules into the booming Indian e-commerce supply chain. And finally we walk through the bull-bear debate every Indian auto-ancillary holder has been having since 2020: does the EV transition kill this company, or does it quietly turn Craftsman into something larger?

It is, in short, the story of a founder who chose grease over glamour, and an investment thesis that depends on whether you believe vertical integration in heavy engineering still constitutes a moat in 2026. Let's start with the man.

II. The Genesis: Srinivasan Ravi's 1986 "Crazy Bet"

Picture a young man in 1985, standing in the foyer of a south-Indian medical college, watching his cousins receive their MBBS hoods. He is the son and nephew and grandson of physicians. He has been told, kindly but firmly, since childhood that the family lineage runs through stethoscopes and operating theatres. He nods politely at the ceremony. Then he goes home and tells his father he wants to start a machine shop.

That young man was श्रीनिवासन रवि Srinivasan Ravi. According to a long-form profile The Economic Times ran on him after the 2021 IPO, Ravi had grown up around Coimbatore's small-engineering district and become quietly obsessed with the geometry of metal — the way a single thousandth-of-an-inch error in a bored cylinder could mean the difference between a truck engine that hummed and one that seized at 80 km/h on the Western Ghats.[^3] His family was deeply skeptical. In a culture where a doctor's prestige still outweighs an engineer's, choosing CNC machines over consulting rooms was treated as a quiet act of rebellion.

In 1986, with capital cobbled together from a small family loan and a bank line collateralized against his father's house, Ravi set up Craftsman Automation as a job-work outfit with a handful of imported CNC machines.[^4] The very first orders were unglamorous: small batches of machined components for Coimbatore's own pump and textile-machinery industry. Margins were thin, deliveries were brutal, and the workshop floor doubled as Ravi's de facto office.

What separated Craftsman from the dozens of similar shops that sprouted across Tamil Nadu in those years was a refusal — almost a religious one — to compete on price alone. Ravi noticed early that the job-work model in Indian engineering had a structural defect: as soon as you proved you could machine a part well, your customer would source a second supplier and slowly grind your price down. The only way out was to climb the value chain, to do not just one process but the entire chain of processes that surrounded it.

So by the early 1990s, Craftsman began absorbing adjacent operations. If the customer needed a casting, machined, then sub-assembled, Ravi would invest in the casting line. If the part needed heat treatment, he would buy the furnace rather than send it out. The phrase the company later adopted to describe this was "integrated engineering," but inside the shop floor, the operating philosophy was simpler: own the bottleneck. Whatever process most often delayed a delivery, most often confused a customer, or most often forced a margin negotiation — bring it inside the gate.

This had a second, less obvious effect. Once Craftsman did the casting and the machining and the sub-assembly under one roof, the original equipment manufacturer no longer had a clean way to second-source. You can second-source a machined block; you cannot easily second-source an entire integrated cell that the OEM's own engineers had spent two years validating. Without ever using the word, Ravi had begun engineering switching costs.

The 1990s also taught Ravi the rhythm of the Indian commercial-vehicle cycle — the multi-year boom-bust pattern in heavy-truck sales tied to infrastructure spending and freight rates. He internalized a rule that would re-emerge thirty years later in the DR Axion deal: the best time to buy capacity is when no one else wants it. By the end of the decade, Craftsman had positioned itself, modestly but firmly, as a preferred supplier to a handful of Tier-1 truck-makers, with a reputation for taking on parts no one else wanted to machine.

It is tempting, in hindsight, to call this strategic genius. The truer reading is that Ravi was a stubborn engineer who hated being commoditized and built a company designed to be impossible to commoditize. That stubbornness sets the stage for the company's first major leap.

III. Building the Powertrain Moat: The Heavy Lifters

Walk through Craftsman's main Coimbatore plant today and the first thing that hits you is not the noise but the size. The cylinder blocks for heavy commercial trucks are roughly the dimensions of a microwave oven and weigh upwards of 100 kilograms apiece. They move through the line on automated rollers, get bored, milled, drilled, washed, leak-tested, and stamped, while overhead a Special Purpose Machine — built in-house, painted Craftsman green — clamps and torques fasteners with a repeatability that the German-made equivalent next to it cannot quite match.

This is the heart of the powertrain business, and it is the business that made Craftsman a real company. Cylinder blocks and heads are the most expensive single-piece machined components inside a diesel engine. They tolerate almost no rework. A single mis-bored block can stop an entire engine line, and an OEM that has to halt its engine plant in Chennai or Jamshedpur for an avoidable supplier defect remembers the experience for a decade. Suppliers who can deliver these parts consistently, in volume, with single-source reliability, are rare; suppliers who can also cast them in-house are rarer still.

By the early 2000s, Craftsman had been selected as a single-source machining partner for cylinder blocks and heads across several of India's largest commercial-vehicle and tractor programs — Tata Motors, Daimler India Commercial Vehicles, and महिंद्रा Mahindra & Mahindra prominent among them.2 These were not promotional flings. Commercial-vehicle engine programs run for ten to fifteen years, and supplier validation cycles take eighteen to twenty-four months. Once you are in, you tend to stay in — provided you do not blow up the line.

The strategic chess move came in 2001, when Ravi committed Craftsman to an aluminum die-casting and machining facility. At the time, India's automotive lightweighting story was still a slide in McKinsey decks; passenger-vehicle penetration was low, fuel-economy regulations were lax, and the heavy commercial-vehicle market was happily married to cast iron. Building an aluminum foundry was, by the standards of the day, premature. Ravi's view, articulated to investors years later, was that the lightweighting trend was inevitable, and that aluminum machining was a fundamentally different and higher-margin skill set than ferrous machining. The "right time" to learn it was before the customers were demanding it.3

That bet looked silly through most of the 2000s and brilliant by the mid-2010s. As CAFE-style fuel-economy norms began pressing on Indian passenger-vehicle OEMs, aluminum content per vehicle quietly compounded, and Craftsman's foundry — by then operating at scale — picked up program after program. The second-order effect was even more important. The same OEM customers who knew Craftsman for cylinder blocks now had a second reason to keep the relationship: aluminum housings, brackets, and structural parts.

Inside the company, the cultural breakthrough of this era was the doctrine that one floor manager described, with a straight face, as "the customer should not do their own machining." Across Indian industry, OEMs had historically run captive machining lines because they did not trust outsiders with engine-critical tolerances. Craftsman set out to make that calculus unworkable. The pitch was unsubtle: you, the OEM, are good at designing engines and assembling vehicles; we are better than you at machining the blocks and casting the housings; let us do this for you and you can shut down your captive shop. Several customers, over the better part of a decade, did exactly that.2

The financial consequence is that revenue concentration in the powertrain segment, while real, is mirrored by customer concentration that runs in the opposite direction: the OEM cannot easily walk away either. Switching to a new cylinder-head supplier mid-engine-program is, for practical purposes, impossible without redesigning the engine. This is the "extreme switching cost" that the Hamilton Helmer framework prizes, hidden inside the dullest-looking parts of an industrial bill of materials.

The IPO in March 2021 — at an issue price of ₹1,490 per share[^7] — was, in many ways, a victory lap for this entire arc. It also gave Ravi the war chest for the next move, which was unlike anything Craftsman had attempted before.

IV. The Masterstroke: The DR Axion Acquisition & Benchmarking

In February 2023, Indian auto-component analysts opened their inboxes to a disclosure they had to read twice. Craftsman Automation, the heavy-truck cylinder-block specialist from Coimbatore, had agreed to acquire 76% of 디알액시온 DR Axion India Private Limited for an enterprise consideration of ₹375 crore.[^2] DR Axion was the Indian arm of a South Korean aluminum die-casting group, and its main business in India was supplying aluminum cylinder heads and structural parts to 현대자동차 Hyundai Motor India and 기아 Kia India. It was, on paper, exactly the asset Craftsman had been missing.

To understand why this deal matters out of proportion to its size, you have to understand both the strategic gap it filled and the price at which it filled it.

The strategic gap was simple. For all its dominance in heavy commercial vehicles and tractors, Craftsman had historically been a marginal player in the Indian passenger-vehicle aluminum value chain. The Hyundai-Kia complex in southern India — one of the largest, fastest-growing PV ecosystems in the country, with a heavy bias toward SUVs that consume disproportionate amounts of aluminum — was almost a closed shop, threaded together by Korean-origin Tier-1 suppliers like 디알액시온 DR Axion. Cracking it organically would have taken Craftsman a decade. DR Axion, in one transaction, gave them the customer relationship, the program approvals, and the validated supplier code.

The price tells the second half of the story. According to research published by Motilal Oswal at the time of the announcement, the acquisition multiple worked out to roughly 4.5x EV/EBITDA on DR Axion's then-current earnings.[^8] To put that in context, listed Indian auto-component peers with comparable margin profiles — Uno Minda, Endurance Technologies, Sundram Fasteners — were trading at trailing EV/EBITDA multiples in the high teens to high twenties through 2022 and 2023. The implied discount was extraordinary, and it existed for a reason. DR Axion's Korean parent was working through a capital reorganization and wanted an exit from the Indian subsidiary; the Indian commercial-vehicle cycle was widely viewed as toppy; and EV-transition anxiety was hammering valuations across the ICE-exposed Tier-1 universe. In other words, the asset was on sale because the consensus did not want it.

Ravi's view, articulated in subsequent earnings calls and reiterated by management in the FY2024 annual report, was that the consensus was misreading three things at once. First, DR Axion's customer relationships and aluminum-machining know-how would not become less valuable in an EV world — they would become more valuable, because EV vehicle architectures require even more high-precision aluminum content per vehicle than ICE platforms do. Second, the synergy between Craftsman's heavy-machining capabilities and DR Axion's PV-focused die-casting operations was real and unhedged anywhere in the listed peer set. Third, DR Axion's operating margins, then sitting in the low teens, were structurally depressed by sub-scale plant utilization and procurement inefficiencies that Craftsman knew how to fix.4

What followed in the eighteen months after the close was, by the company's own disclosures, exactly the operational improvement program the deal thesis required. Craftsman consolidated procurement, re-engineered the casting cells around its in-house Special Purpose Machine know-how, and worked through DR Axion's vendor base with the same playbook that had compounded margins in the legacy aluminum business. By the time the FY2025 numbers landed, DR Axion's contribution to consolidated EBITDA was visibly higher than the run-rate at acquisition, and the company described the unit as broadly EPS-accretive within the first full year of consolidation.4

There is a second, subtler lesson buried in this transaction. The conventional Indian auto-component M&A pattern through the 2010s — most visibly in the playbooks of मदरसन Motherson Sumi and भारत फोर्ज Bharat Forge — involved buying distressed assets in Europe or North America at low multiples and trying to fix them at a continental distance. Craftsman did the same thing inside its own home market. The asset was a few hundred kilometers from Coimbatore, the workforce spoke the same languages as Craftsman's own engineers, and the customers were the same Indian PV OEMs that Craftsman already aspired to serve. The integration risk was a fraction of what a cross-border deal would have carried.

It is, in short, a case study in buying a high-quality asset at a commodity-cycle price, in your own backyard, when the consensus is looking the other way. Which makes the next chapter of the story — the one investors still under-appreciate — even more interesting.

V. The "Hidden" Gem: Storage Solutions & Warehouse Automation

Most investors who have spent an afternoon reading Craftsman's annual report come away thinking of it as an auto-component company with a small storage business attached, in roughly the same way one might think of a steel company that also owns a captive port. That mental model is rapidly becoming wrong, and the gap between perception and reality is, in some senses, the most interesting optionality embedded in the equity.

The storage solutions business sits inside the company's "Industrial & Engineering" segment, and on the surface it does what the name suggests: it designs and manufactures pallet racks, mezzanine flooring, and other industrial storage hardware for warehouses across India.5 Boring enough. But over the last several years, the segment has been quietly metamorphosing into something rather different — a vertically integrated material-handling automation business, designed and built in Coimbatore, with proprietary intellectual property in robotics, control systems, and warehouse-management software.

The flagship product is something called V-Store, a family of automated vertical lift modules — what the global trade press calls VLMs — designed and assembled domestically.5 If you have ever watched a pharmaceutical warehouse pick orders, you have probably seen the foreign equivalents: tall enclosed cabinets, often two stories high, with trays that shuttle up and down on command, presenting the right SKU to a picker at waist height in under ten seconds. They are the workhorses of modern e-commerce fulfillment, particularly for high-SKU, low-cube items: spare parts, electronics, beauty, pharmaceuticals.

The macro tailwind here is not subtle. Indian e-commerce gross merchandise value compounded through the 2020s at rates that consistently surprised consensus forecasts, and the corresponding build-out of तीसरा पक्ष लॉजिस्टिक्स third-party logistics warehouse capacity in clusters like Bhiwandi, Farukhnagar, and Hosur produced relentless demand for both basic racking and increasingly sophisticated automation. The Ken, in its 2024 deep dive on the segment, described Craftsman as one of the rare Indian players capable of supplying both ends of the spectrum to the same customer — racking today, ASRS and VLMs tomorrow — without forcing the customer to integrate two different vendors.[^11]

The financial signature of this transformation is interesting. The storage segment as a whole grew at high-teens to twenty-percent-plus rates through FY2024 and FY2025, and the EBIT margin profile expanded as the product mix shifted from static racks (a commoditizing product where Chinese competition is real) to automation (a specialty product where the customer is buying engineering, software, and after-sales service, not just folded steel).4 The same dynamic that played out in the powertrain business in the 2000s — climbing the value chain from cut metal to integrated systems — is now playing out in storage, on roughly a decade-compressed timeline.

The new frontier the management team has flagged is data center infrastructure. As India's hyperscale and colocation data center market exploded through the mid-2020s, every operator needed something boring but critical: high-density, seismic-rated server racks; in-row power distribution units; cable management; precision-cooled cabinet systems. These are products that look, structurally, very much like what Craftsman has been bending and welding for warehouses for years, but the customer is paying a premium for spec compliance, certifications, and lead times. Craftsman has set out a publicly stated ambition of building its data center-adjacent product line into a roughly $100 million revenue contributor by the end of the decade.4

There is a second-order consideration worth noting here on the diligence checklist. Storage automation is a segment where credit underwriting on the customer side actually matters: 3PLs that take large racking orders can be lumpy payers, and aggressive working capital can flatter margins in the short run while building receivables risk. The fact that Craftsman has historically run conservative working-capital metrics on its industrial segment, and has not chased volume by financing customers, is the kind of operating discipline that does not show up in headline numbers but does show up in the absence of write-offs five years later.

The investor question, in any case, is no longer whether storage solutions is a "real" business. It is. The question is how quickly its share of consolidated EBITDA crosses thresholds — twenty percent, thirty percent — that force the market to re-rate the entire company as something other than a pure-play auto-component supplier.

VI. Current Management: The Ravi Playbook

There is an industry-wide habit of describing every Indian promoter-led mid-cap as a "founder-driven success story." It is the safe phrase to use, the one that lets analysts gesture at corporate-governance virtue without saying anything specific. Craftsman, on closer inspection, deserves slightly more precise language.

Srinivasan Ravi, four decades after founding the company, still walks the shop floor most days he is in Coimbatore. His direct shareholding sits at approximately 44% of the company, with the broader Promoter Group holding accounting for roughly 55% of the equity in aggregate, a structure disclosed in the company's quarterly shareholding pattern filings.6 In an Indian mid-cap landscape where post-IPO promoter dilution to the high twenties or low thirties is now common, this is an unusually high level of insider economic alignment.

The more interesting governance disclosure is on the compensation side. Ravi's commission as Chairman and Managing Director is contractually capped at a percentage of net profits — most recently disclosed at 7.5% — rather than tied to revenue, market capitalization, or operating cash flow.7 That structural choice is itself a statement. Net profit is the most-manipulable headline number in heavy engineering only in the very short run; over five-year and ten-year stretches, it tracks fairly closely with actual capital-allocation skill. Tying executive compensation to net profits rather than to top-line growth or to capex deployed is a quiet bet against empire-building, and it has shaped the company's behavior in ways that are easy to miss.

The most visible expression of this culture is the in-house Special Purpose Machine (SPM) program. Across most of the global heavy-machining industry, the dominant pattern is to buy multi-axis CNC machining centers from a Japanese, German, or Italian supplier — Mazak, DMG Mori, Heller, GROB — at sticker prices that frequently run into seven-figure dollar amounts per machine, and then to operate and maintain them through long, expensive service contracts with the OEM. Craftsman, almost from the beginning, treated this as a violation of the "own the bottleneck" doctrine. Where standard CNC machines were genuinely better than anything an in-house team could build, they bought standard machines. Where a process was specific enough that a Coimbatore engineer could design something tailored — a custom transfer line for a specific cylinder block, say, or a leak-test station for a particular aluminum housing — they built it in-house, often for a meaningful fraction of the imported cost.

Cumulatively, that has done two things. It has compressed the capital-intensity of every major capacity expansion, because a non-trivial share of the equipment cost in any new Craftsman plant is internal labor and engineering rather than imported capex. And it has built a knowledge stock that competitors cannot easily replicate, because the SPM designs live inside Craftsman's own design office and shop-floor tribal knowledge, not on any vendor's blueprint shelves.

Around Ravi, the second-tier leadership has matured in a recognizable pattern. The senior team is heavy on engineers with two decades of internal tenure, light on outside hires from McKinsey or Bain, and almost devoid of the "professional-CEO" archetype that institutional investors sometimes demand as a sign of governance modernity. Whether this is a strength or a weakness depends on how much you trust the founder. As succession looms in the second half of the decade, the absence of an obvious external heir-apparent is the kind of risk that thoughtful long-term holders will want to track without panicking about.

The qualitative signal worth holding onto is this: in earnings calls and at site visits, Ravi sounds like an operator describing a machine, not a CEO selling a story. He talks about hit rates on quotations, line-rejection percentages, and the lead time on imported Korean alloy. He very rarely talks about share price. For a long-term holder, that is the right way around.

VII. Porter's Five Forces and Hamilton's Seven Powers

Strip away the narrative for a moment, and look at Craftsman through the two analytical lenses that long-term industrial investors actually use: Michael Porter's structural-industry framework, and Hamilton Helmer's specific-firm one. The picture that emerges is consistent across both, which is itself a useful signal.

Begin with the Hamilton Helmer Seven Powers, because they are sharper. Three of the seven map onto Craftsman with unusual clarity.

The first is Process Power. The in-house Special Purpose Machine program described in the previous section is a textbook example. It is an accumulated, tacit, organization-specific body of know-how that cannot be replicated by writing a check, hiring a consultant, or buying a competitor's blueprints. A new entrant who wants to compete with Craftsman in heavy-truck cylinder-head machining does not just need capital — they need ten years of doing the same thing badly before they start doing it well. This is the most underrated source of moat in heavy engineering, and it tends to get stronger with scale, not weaker.

The second is Switching Costs, and they are in some ways even more extreme than the conventional Tier-1 narrative suggests. A heavy commercial-vehicle engine program runs for roughly a decade and a half between major redesigns. The validation cycle for a new cylinder-block or cylinder-head supplier inside that program is typically eighteen to twenty-four months, and involves dozens of physical engine builds, durability tests, and regulatory recertifications. Once Craftsman is in the bill of materials for a given engine, displacing them mid-program is, in pure cost-benefit terms, almost never worth it for the OEM. The customer is effectively locked in until the engine itself is replaced — and even then, the incumbent supplier starts the next negotiation with structural advantages.

The third is Scale Economies, both at the plant level and at the engineering-resource level. Craftsman operates what is, by Indian standards, the largest aggregated cylinder-block and cylinder-head machining capacity for heavy commercial vehicles — a position that is reinforced every time a customer consolidates their supplier base.8 The scale advantage compounds because the fixed cost of carrying a deep engineering bench — application engineers, metallurgists, control-systems designers — is amortized across more programs than any smaller competitor can manage.

The remaining four Helmer powers — Counter-Positioning, Branding, Cornered Resource, and Network Economies — apply less obviously. There is no real brand power in B2B heavy machining; customers care about quality and lead time, not about logos. There is no network effect; this is not a marketplace. Counter-positioning is plausible only in a limited sense, in that the company's vertical-integration model is genuinely difficult for a pure-play machinist to copy without burning down their own light-asset playbook. Cornered Resource is similarly limited, although the relationship with Hyundai-Kia secured through DR Axion now functions as a partial cornered resource within the southern Indian PV ecosystem.

Switch to Porter, and the most striking force is Buyer Power. The OEM customer base in Indian commercial vehicles and tractors is consolidated into a small number of very large buyers. Each one of them has, in theory, immense leverage over a single-product supplier. Craftsman has spent thirty years systematically dulling that leverage by making itself a single-source partner across multiple part families, by being deeply embedded in program design from a stage at which switching becomes nearly impossible, and by adding new customer relationships (DR Axion's PV exposure, the entire industrial-engineering segment) that are uncorrelated to its legacy CV concentration.

Threat of new entrants is moderated by capital intensity, validation cycles, and the SPM-driven process moat. Threat of substitution is the interesting one, and it shades into the EV-transition debate that we turn to next. Internal rivalry — among Indian auto-component peers — exists but is mitigated by the fact that the powertrain machining specialty within which Craftsman is dominant has relatively few credible domestic competitors.

The honest summary is that Craftsman's structural advantages are real, multiple, and reinforcing, but they are concentrated in a part of the automotive value chain that the consensus believes is about to shrink. That is the bear case, and it deserves to be taken seriously.

VIII. Bear vs. Bull Case & The EV Threat

The bear case begins with a single number that anyone who has read an EV-transition report has internalized: a battery-electric vehicle has roughly twenty moving parts in its powertrain, against several hundred in an internal combustion engine. No cylinder block. No cylinder head. No camshaft, no crankshaft, no engine cooling jacket. If the world transitions to electric mobility on the timelines that Bloomberg New Energy Finance, IEA, and India's own NITI Aayog projections have at various points sketched, a meaningful share of Craftsman's powertrain bill of materials simply vanishes from the global vehicle.

That is the steel-manning version of the bear case. Add in the cyclical layer — the Indian commercial-vehicle market is mature, has compounded at low- to mid-single-digit volume rates over the long run, and is exposed to interest rates, infrastructure spending, and freight pricing — and you have a portfolio manager's nightmare: a stock that looks cheap today but might be in structural decline.

The bull case responds in three layers.

The first is timing and segment mix. India's heavy commercial-vehicle and tractor segments are the latest, slowest, and most economically resistant to BEV transition of any major mobility segment globally. The energy density requirements of long-haul trucking, the cost-sensitivity of agricultural equipment, and the underdeveloped state of high-power charging infrastructure outside metropolitan corridors mean that diesel powertrains in commercial vehicles and tractors will remain dominant well into the 2030s, possibly the 2040s. Hydrogen internal-combustion solutions in trucking, where they emerge, will still need cylinder blocks and heads — just made of slightly different alloys. The customers Craftsman serves most deeply are precisely the customers least exposed to the BEV transition timeline.

The second layer is the aluminum hedge. BEV vehicle architectures, contrary to the simplistic "fewer parts" narrative, actually require more aluminum content per vehicle than ICE platforms — for battery enclosures, structural battery-to-body integration parts, e-motor housings, thermal management plates, and lightweighting of body-in-white components. Every kilogram of cast iron and machined steel that exits the Craftsman bill of materials in a hypothetical BEV future has, in many cases, an aluminum analogue entering it elsewhere on the same vehicle. The DR Axion acquisition, viewed through this lens, is not just a Hyundai-Kia customer-access play. It is a deliberate inventory of aluminum-machining capability bought at the bottom of an ICE-correlated valuation cycle, in anticipation of an EV-driven aluminum-content cycle.

The third layer is diversification. The storage solutions and industrial engineering segment is, definitionally, uncorrelated to automotive end markets. As that segment compounds at rates well above the consolidated company average, the share of group EBITDA tied to powertrain ICE products will mechanically decline regardless of what happens at the parent company. If the data center adjacency materializes at anything close to management's publicly stated ambition, that uncorrelated share of the business gets larger still.

On Porter, the EV transition does represent a credible threat-of-substitution event for the legacy product line, but Craftsman's response — moving toward higher aluminum content, building out non-automotive industrial engineering, and hedging into EV-relevant components — directly addresses it. On Helmer, the process power, switching costs, and scale economies built up over thirty years are arguably more durable than the specific product chemistry of any one engine architecture.

The honest version of the bear-bull debate is that this is not a binary question. It is a question about pace. If BEV adoption in Indian commercial vehicles arrives faster than the bull case anticipates, the legacy powertrain segment will compress before the new growth segments scale, and the equity will go through an unpleasant intermediate period. If BEV adoption in commercial vehicles arrives more slowly than the bear case fears, Craftsman will compound calmly through the transition while quietly remaking its product mix.

Among Indian auto-ancillary peers, the most useful comparators on this debate are मदरसन Motherson Sumi, भारत फोर्ज Bharat Forge, and Sundram Fasteners — companies that have each made their own deliberate bets on how to position through the transition. Craftsman's bet is the most concentrated on heavy commercial vehicle ICE persistence, paired with the most aggressive non-auto industrial pivot. Whether that turns out to be the smart positioning will not be clear for several years.

The single most useful key performance indicator to track on this debate is the share of consolidated EBITDA contributed by the Industrial & Engineering segment, supplemented by the powertrain segment's aluminum-content mix. A secondary KPI worth tracking is consolidated free cash flow conversion, because the test of "buying the cycle" is ultimately whether the deployed capital comes back as cash. Beyond those two, most other metrics — quarterly revenue prints, segment-level operating margins on any given quarter — are noise.

IX. Playbook & Conclusion

Step back from the segment commentary and the cycle analysis, and three durable lessons emerge from the Craftsman story — lessons that travel far beyond Indian auto components.

The first is that vertical integration is only a moat if you have the engineering talent to maintain it. The standard MBA critique of vertical integration is that it is capital-inefficient, slow, and prone to internal complacency. That critique is correct, until you meet a company where the engineering bench is deep enough to run every integrated process at or above the standard of an external specialist. Craftsman is one of the few mid-cap Indian industrials where the in-house engineering culture has consistently been good enough to make integration accretive rather than dilutive. It is not a model that travels well to companies whose talent base does not match. The lesson for investors is to be skeptical of "integrated" pitches that are not backed by visible engineering depth.

The second is the discipline of buying the cycle. The DR Axion transaction, taken in isolation, is one of the cleaner examples in recent Indian industrial M&A history of acquiring a structurally strong asset at a cyclically depressed valuation, from a seller who needs to exit, in a moment when the consensus narrative is bearish on the entire end market. The four-and-a-half-times EV/EBITDA multiple was not an accident — it was an active choice to act when others were paralyzed.[^8] Replicating that discipline is hard because it requires both a balance sheet that can act when sentiment is poor and a board that will let management do so. Most Indian mid-caps fail one or both of those tests.

The third is the value of staying in the boring parts. There is a recurring temptation in Indian capital markets to chase the year's narrative — fintech in 2019, EV in 2021, AI infrastructure in 2024 — and to penalize companies that refuse to participate in the rotation. Craftsman has, with notable consistency, stayed in the dullest, greasiest, most capital-intensive parts of Indian engineering, and quietly compounded inside them. The lesson is not that boring is always better; it is that boring done excellently is frequently undervalued by markets that prefer interesting done averagely.

The "Acquired" question that lingers is whether Craftsman is the next Motherson Sumi — a south-Indian auto-component company that compounds itself across multiple decades into a genuine global story — or whether it is something different and smaller: a regional specialist that builds a high-quality franchise inside a defined ecosystem and never fully escapes it. The honest answer is that the storage-solutions segment, more than any other variable, will determine which of those stories ends up being true. If that business scales to the ambitions management has articulated, Craftsman becomes a diversified industrial engineering company with auto-component roots. If it does not, the company remains an excellent — but more bounded — auto-component franchise.

What is unambiguous is the founder story underneath it all. Forty years after Ravi turned down medical school in favor of a leased CNC machine in Coimbatore, the company he built is one of the few Indian industrials whose moat has visibly deepened, rather than eroded, through every major market transition of the last two decades — globalization, the dot-com bust, the 2008 crisis, demonetization, COVID, the EV transition scare. Whether one is bullish or bearish on the next chapter, the underlying record is the kind of record that long-term fundamental investors are supposed to pay attention to: a founder who does the work, an organization that internalizes the work, and a moat that is the residue of decades of that work, accumulated in a Coimbatore machine shop while the rest of the country was busy chasing the next thing.

References

-

Craftsman Automation Stock Price & Historical Filings — NSE India ↩

-

Engineering Excellence in Coimbatore: The Craftsman Story — Business Standard, 2022-11-15 ↩↩

-

Storage Solutions Segment — V-Store & ASRS, Craftsman Automation Official Site ↩↩

-

Management Compensation and Incentive Policy — Craftsman Automation IR Portal ↩

-

Investor Presentation Q4 FY26 / FY26 Results — Craftsman Automation ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube