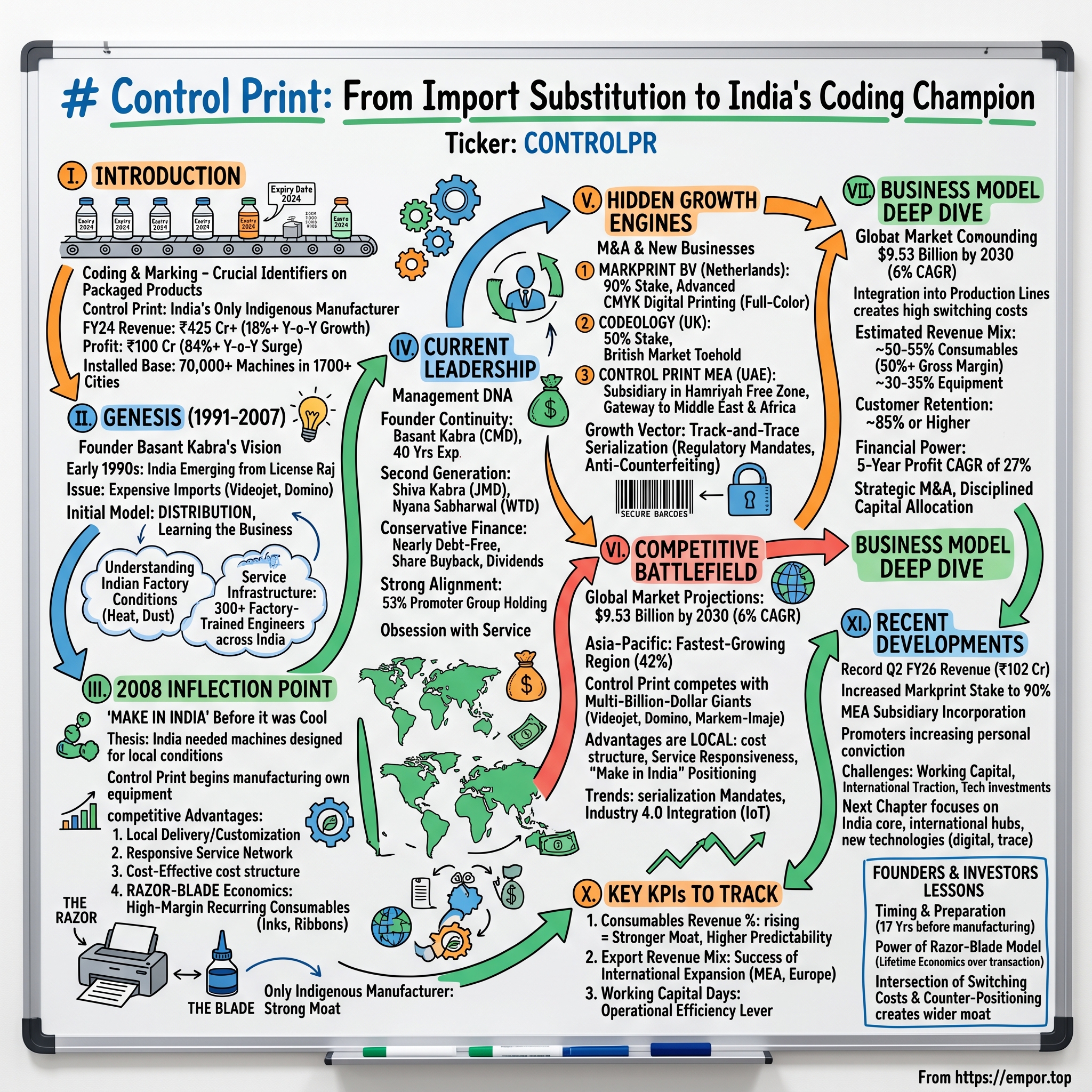

Control Print: From Import Substitution to India's Coding Champion

I. Introduction

Picture a bottle of cough syrup sitting on a pharmacy shelf in Lucknow. Flip it over. On the base, or perhaps along the neck, there is a tiny string of characters—a batch number, an expiry date, maybe a barcode. Most people never think about how those markings got there. But behind that seemingly trivial act of printing a few lines of text onto a moving bottle sits a multi-billion-dollar global industry, a fierce competitive war between American and European giants, and one unlikely Indian challenger that decided the game could be played differently.

Control Print Limited, headquartered in Mumbai, is India's only indigenous manufacturer of coding and marking equipment—the machines that stamp, spray, etch, and print those critical identifiers onto virtually every packaged product that moves through an Indian factory. From pharmaceutical vials to cement bags, from agrochemical containers to pipe lengths, if a product needs a date code, a batch number, or a regulatory barcode, chances are a coding machine put it there. And in India, there is a growing probability that the machine was made by Control Print.

The numbers tell a compelling story. Revenue crossed four hundred and twenty-five crores in fiscal year 2024, growing at over eighteen percent year-on-year. Net profit surged eighty-four percent to one hundred crores. Over the preceding five years, profit compounded at roughly twenty-seven percent annually. The balance sheet carries almost no debt. And the company sits on an installed base of over seventy thousand machines spread across more than seventeen hundred cities.

But the real story is not in the financials alone. It is in how a Mumbai entrepreneur named Basant Kabra spent seventeen years learning the coding business from the inside—importing and servicing foreign machines—before making a calculated bet in 2008 to build his own. It is in the razor-blade economics that generate recurring consumables revenue from every machine sold. It is in the three-hundred-plus factory-trained service engineers stationed across India, a boots-on-the-ground army that no multinational has been willing to match. And it is in the quiet moves—an acquisition in the Netherlands, a subsidiary in the UAE, a bet on track-and-trace serialization—that hint at ambitions far beyond the current scale.

This is the story of import substitution done right, a local champion taking on global Goliaths, and what happens when deep domain expertise meets patient capital and India's manufacturing awakening.

II. The Genesis: Founder Basant Kabra's Vision (1991–2007)

To understand Control Print, one must first understand what coding and marking actually is, and why it matters far more than its unglamorous reputation suggests. Every time a pharmaceutical company prints a batch number on a blister pack, every time a beverage company stamps an expiry date on a can, every time a pipe manufacturer etches a grade code along a length of PVC—that is coding and marking. The machines that perform this task sit directly on production lines, firing tiny droplets of ink or applying thermal transfers at high speed while products race past on conveyors. If the coding machine goes down, the production line goes down. Full stop. There is no workaround, no manual alternative at industrial scale. This makes coding equipment mission-critical infrastructure for any manufacturer, which in turn makes the service relationship between the equipment provider and the factory floor profoundly sticky.

Basant Kabra understood this before most people in India even knew the industry existed. In the early nineteen-nineties, India was emerging from decades of the License Raj. Economic liberalization under Prime Minister Narasimha Rao was cracking open markets. Manufacturing was beginning to stir. Kabra, who had exposure to coding technology during travels abroad, recognized a yawning gap: Indian factories needed coding machines, but the only options were expensive imports from companies like Videojet, Domino, and Markem-Imaje—global giants headquartered in the United States, the United Kingdom, and France respectively.

In 1991, Kabra partnered with Anirudh Joshi to incorporate Control Print Limited. The initial model was not manufacturing—it was distribution. Control Print began by importing coding equipment from international brands and selling it into the Indian market. This was a deliberate choice. Kabra wanted to learn the business from the ground up before attempting to build his own machines. He wanted to understand Indian factory conditions, customer pain points, the specific ways in which heat, dust, humidity, and unreliable power supply destroyed equipment designed for the climate-controlled factories of Stuttgart and Chicago.

For the next seventeen years, Control Print built something that would prove even more valuable than any machine: a service infrastructure. By the mid-two-thousands, the company had assembled a network of over three hundred factory-trained engineers spread across India. These were not salespeople—they were technicians who could diagnose and fix a malfunctioning continuous inkjet printer on a cement factory floor in Rajasthan or a pharmaceutical line in Hyderabad. This network became the bedrock of everything that followed.

The market context made the opportunity clear. Globally, coding and marking was dominated by three players. Videojet, a subsidiary of the American conglomerate Danaher, commanded roughly twenty-three percent of the global market. Domino, later acquired by Brother Industries of Japan, held about seventeen percent. Markem-Imaje, a French company, rounded out the top tier. Together, these three controlled over a third of the global market. But India was an afterthought for them. Prices were set in dollars and euros. Service response times could stretch into days. Spare parts had to be shipped internationally. And consumables—the inks, ribbons, and fluids that these machines consumed continuously—were priced at what Indian manufacturers considered ransom levels. Kabra saw all of this. He catalogued every complaint, every service failure, every price objection. He was building a playbook for the day he would need it. That day came in 2008.

III. The 2008 Inflection Point: Make in India Before It Was Cool

By 2008, Basant Kabra had spent nearly two decades inside the coding industry. He knew which components failed most often in Indian conditions. He knew that the dust in a cement plant could clog a printhead designed for a European pharmaceutical cleanroom. He knew that voltage fluctuations in a small-town factory could fry control boards engineered for stable European power grids. He knew that when a coding machine broke down on a production line running twenty-four hours a day, seven days a week, waiting three days for a foreign technician was not an inconvenience—it was a catastrophe that cost lakhs in lost output.

The realization crystallized into a simple but audacious thesis: India did not need better versions of foreign machines. India needed machines designed from the ground up for Indian conditions.

Control Print began developing its own coding equipment in 2008, drawing on some core German technology but engineering the machines specifically for the realities of Indian manufacturing. The decision was a massive bet. Here was a mid-size Indian company, with no brand recognition in equipment manufacturing, proposing to compete against billion-dollar multinationals with decades of R&D and global scale. The initial customer reaction was predictable skepticism. Indian factory managers, conditioned to equate foreign brands with quality, asked the obvious question: why would we buy Indian when we can buy German or American?

The answer came in four parts, and together they formed Control Print's competitive advantage thesis.

First, local manufacturing meant dramatically faster delivery and easier customization. A factory in Gujarat did not have to wait weeks for a machine shipped from Illinois. Control Print could deliver from its two manufacturing facilities in Mumbai, and if a customer needed a modification for a specific production line configuration, the engineering team was a phone call away, not an ocean away.

Second, the service network. Those three hundred-plus engineers that Kabra had patiently assembled over seventeen years were now the most potent weapon in his arsenal. When a Videojet machine broke down, the customer called a helpline and waited. When a Control Print machine had an issue, a trained technician could be on-site within hours in most of urban and semi-urban India. In an industry where downtime is measured in lost production, this was not a nice-to-have—it was the difference between winning and losing a customer.

Third, the cost structure. By manufacturing in India, Control Print could offer machines at prices dramatically lower than imports—industry estimates suggest thirty to forty percent lower—while still maintaining healthy margins thanks to lower labor and overhead costs.

Fourth, and perhaps most importantly, the consumables strategy. This is where the razor-blade model comes alive. Coding machines are the razors; inks, ribbons, and fluids are the blades. Every machine sold creates a captive customer for consumables over the machine's lifetime, which typically stretches five to ten years or more. Control Print formulated its own inks, designed specifically for Indian conditions—inks that performed in high humidity, that dried properly on the substrates common in Indian manufacturing, that resisted the temperature extremes of a factory in Nagpur in May. By controlling both the machine and the consumables, Control Print could offer the lowest total cost of ownership in the market while generating high-margin recurring revenue.

The strategy worked. Over the following decade, Control Print built an installed base of over seventy thousand machines, reaching into twenty-seven hundred pin codes across India. The company became—and remains—the only Indian manufacturer of coding and marking equipment. No other domestic company has attempted to replicate what Kabra built, which says something about both the difficulty of the undertaking and the strength of the moat once established.

The product range expanded to cover virtually every coding technology in use: Continuous Inkjet, Thermal Inkjet, Thermal Transfer Overprinting, Drop-on-Demand, Laser, and Large Character printing. Each technology serves different applications, substrates, and speed requirements, and by offering the full portfolio, Control Print could be a one-stop shop for factories that needed multiple coding solutions across different production lines.

The razor-blade economics deserve special emphasis because they are the engine of the business model. Machines are sold at competitive prices—sometimes at thin margins—because every installation becomes an annuity. The customer needs ink, ribbons, cleaning fluids, and maintenance for as long as the machine runs. These consumables carry estimated gross margins north of fifty percent. And once a coding machine is integrated into a production line, the switching costs are enormous. Ripping out an installed coder means production downtime, retraining operators, recalibrating the line, and risking quality issues during the transition. Very few factory managers take that risk unless they absolutely must.

IV. Current Leadership and Management DNA

The Kabra family's fingerprints remain firmly on Control Print's steering wheel, and that continuity has been both a strength and a source of legitimate questions for outside investors.

Basant Kabra continues to serve as Chairman and Managing Director, the same role he has held since founding the company in 1991. His four decades of experience in the coding industry are virtually unmatched in India. In September 2025, his direct shareholding increased significantly—from about four and a half percent to over thirteen percent—through a share transmission within the promoter group. The promoter family collectively holds approximately fifty-three percent of the company, a level of ownership that ensures deep alignment between management decisions and long-term value creation, but also concentrates control in a way that limits minority shareholder influence.

The second generation is already in the driver's seat for key operational areas. Shiva Kabra serves as Joint Managing Director, overseeing marketing, business development, and corporate strategy. His involvement signals that succession planning is underway, though the company has not publicly detailed a formal transition timeline. Nyana Sabharwal, a Whole-time Director, handles corporate social responsibility and branding initiatives.

The management style reflects a distinctly conservative financial philosophy. The balance sheet is almost entirely debt-free—a rarity among mid-cap Indian industrials and a choice that sacrifices potential leverage-driven growth for resilience. In 2023, the company executed a buyback of roughly three hundred and thirty-seven thousand shares for two hundred and seventy million rupees, returning capital to shareholders rather than hoarding cash or making speculative investments. Dividend payouts have been consistent, with a payout ratio around twenty-three percent.

The cultural DNA of the organization centers on a few principles that are worth noting for their strategic implications. The obsession with service—maintaining three hundred-plus engineers in the field—is expensive. It compresses margins relative to a leaner operation. But it is the single most important competitive asset the company owns, because it creates a level of customer intimacy and switching cost that no amount of advertising or price-cutting can replicate. The willingness to invest in this network over decades, even when it hurt short-term profitability, reveals a management team that thinks in years and decades, not quarters.

The question investors should watch is whether this family-run, professionally managed hybrid model can scale into the next phase of growth—particularly as the company pushes into international markets and more complex technology domains like digital printing and track-and-trace software.

V. The Hidden Growth Engines: M&A and New Businesses

If Control Print's core Indian coding business is the foundation, then a series of recent strategic moves represent the scaffolding for what could be a materially larger company. These moves have received relatively little attention from the market, partly because Control Print is a small-cap stock with limited analyst coverage, and partly because the initiatives are still in early stages. But they deserve close examination.

The most significant bet is Markprint BV, a Netherlands-based company specializing in advanced CMYK digital printing technology. Control Print acquired a seventy-five to eighty-five percent stake in 2022 for one and a half million euros—a remarkably modest price tag. By 2025, the company had increased its stake to ninety percent with an additional two hundred thousand euro investment, signaling growing confidence in the acquisition.

What did they buy? Markprint develops single-pass digital printing systems for packaging and industrial applications. Think of it this way: traditional coding machines print simple text—batch numbers, dates, barcodes—typically in a single color. Markprint's technology prints full-color, high-resolution images at industrial speeds. The applications span flexible packaging, labels, textiles, and other surfaces where brands increasingly demand high-quality printed packaging. In India, where the packaging industry alone represents a massive addressable market, the ability to offer digital printing solutions alongside traditional coding could significantly expand Control Print's revenue per customer and total addressable market.

Markprint generated approximately one point three million euros in revenue in fiscal year 2025—modest, but the acquisition was priced at roughly one point one five times revenue, which is reasonable for a technology acquisition that comes with intellectual property and a European market foothold. The strategic logic is to transfer Markprint's technology to India, localize it for Indian cost structures and customer requirements, and sell into the massive Indian packaging and textile markets. If this works, it represents a step-change in the value proposition Control Print can offer.

The second international move was acquiring a fifty percent stake in Codeology Group Limited, a UK-based coding company, for one million pounds in 2023. This is a more modest play—a toehold in the British market that provides additional technical capabilities and product portfolio breadth, structured as a joint venture to facilitate knowledge transfer.

The third move came in January 2025 with the incorporation of Control Print MEA FZE, a wholly-owned subsidiary in the Hamriyah Free Zone in the United Arab Emirates. This is the company's gateway to the Middle East and Africa—regions where Indian manufacturing companies have historically found success by offering cost-competitive alternatives to Western equipment. Control Print already exports to Kenya, Saudi Arabia, Indonesia, Germany, and the UK, but export revenue currently represents only about two point eight five percent of total revenue. That number is strikingly low and represents enormous headroom if the MEA subsidiary gains traction.

Perhaps the most intriguing growth vector is track-and-trace serialization, where regulatory mandates are creating forced demand. India's Drug Amendment Act of 2022 mandated serialization for the top three hundred pharmaceutical formulations. GS1-based QR codes became mandatory for active pharmaceutical ingredients and pharma packaging in 2023. Pharmaceutical exports require serialization to the government's iVEDA platform. And similar anti-counterfeiting regulations are emerging in the FMCG sector.

For Control Print, this regulatory wave is a gift. Track-and-trace requires high-resolution printers capable of producing GS1-compliant data matrix codes and barcodes—exactly the kind of equipment the company manufactures. The existing installed base of seventy thousand machines may need upgrades. New installations will be required at factories that previously used simpler coding solutions. And there is a potential software and services layer—compliance management, serialization platforms, per-unit transaction fees—that could introduce high-margin recurring revenue streams beyond hardware and consumables.

Though Control Print does not publicly break out detailed segment-level data, the revenue mix can be estimated roughly. Equipment sales likely represent thirty to thirty-five percent of revenue at lower margins. Consumables—inks, ribbons, fluids—probably account for fifty to fifty-five percent at margins north of fifty percent. Service contracts make up the remainder. The digital printing and track-and-trace businesses are in early innings but represent the highest-potential growth avenues. For investors, the key question is not whether these initiatives exist, but whether management can execute on them at scale. The acquisitions have been disciplined—small checks, strategic rationale, no empire-building. But international expansion and technology integration are genuinely hard, and the next three to five years will reveal whether these seeds bear fruit.

VI. The Competitive Battlefield and Industry Dynamics

The global coding and marking equipment market was valued at approximately six point six six billion dollars in 2024 and is projected to reach nine point five three billion by 2030, growing at a compound annual rate of about six percent. Asia-Pacific accounts for roughly forty-two percent of global demand and is the fastest-growing region, driven by manufacturing expansion, regulatory tightening, and the relentless growth of packaged consumer goods.

Within this arena, Control Print faces formidable opponents. Videojet, operating under the Danaher umbrella, deployed over one hundred and five thousand systems globally in 2023 alone. Danaher is a two-hundred-billion-dollar conglomerate with deep pockets, advanced R&D capabilities, and a reputation for operational excellence through its famed Danaher Business System. Domino, now part of Brother Industries, placed over ninety-two thousand CIJ and TIJ printers globally and has particular strength in pharmaceutical applications. Markem-Imaje remains a formidable European competitor. Chinese players like SUNINE are emerging as low-cost challengers, particularly in less-regulated markets. Laser-focused companies like Han's Laser and Trumpf compete in the growing laser coding segment.

Against this lineup, Control Print's advantages are distinctly local. It is the only Indian manufacturer, which gives it a monopoly on the "Make in India" positioning that resonates strongly with government procurement, public sector undertakings, and nationalist industrial policy. Its cost structure—Indian labor costs, Indian real estate, Indian raw materials—allows it to be profitable at price points where Videojet or Domino would be losing money or would refuse to compete. And its service network remains the most comprehensive of any coding equipment provider in the Indian market.

Several industry trends play directly into Control Print's hands. The regulatory tsunami around track-and-trace is perhaps the most powerful tailwind. Industry research suggests that nearly forty-six percent of coding equipment growth between 2025 and 2030 will be driven by pharmaceutical serialization mandates. By 2024, an estimated sixty-eight percent of enterprises had adopted traceable coding systems. This is not a discretionary purchase—it is compliance-driven demand that creates a floor under industry growth regardless of economic cycles.

Industry 4.0 integration is reshaping customer expectations. Roughly thirty-nine percent of new installations in 2024 were IoT-enabled, featuring remote monitoring, predictive maintenance, and cloud connectivity. Control Print offers modular coders with remote monitoring capabilities, but this is an area where the global giants have deeper technology stacks. The sustainability push is creating demand for eco-friendly inks and recyclable cartridges. And the e-commerce explosion is driving labeling requirements for last-mile logistics.

Control Print's positioning can be summarized in a single observation: in a market dominated by expensive foreign equipment and serviced by skeleton crews, it offers the lowest total cost of ownership backed by the most responsive service network. Its installed base of seventy thousand machines is a captive market for high-margin consumables. And its status as the sole Indian manufacturer provides a structural advantage that would take any new entrant a decade and hundreds of crores to replicate.

VII. Business Model Deep Dive: Why This Works

The elegance of Control Print's business model lies in the compounding nature of its revenue streams. Every machine sold is not a one-time transaction—it is the beginning of a multi-year relationship that generates consumables revenue, service contract revenue, and eventually replacement or upgrade revenue. This is the razor-blade model, and Control Print executes it with unusual discipline.

On the "razor" side, coding machines are priced competitively—often with financing options for small and medium enterprises—and include installation and training. The margins on equipment sales are modest by design. The strategy is to get machines into factories and onto production lines, because once installed, the switching costs become the moat.

Those switching costs are worth dwelling on, because they explain why the business is far stickier than it might appear. A coding machine is not a standalone device—it is integrated into a production line. It interfaces with conveyor systems, product sensors, factory automation software. Operators are trained on its specific interface. Quality control processes are calibrated around its output characteristics. Replacing it means production downtime during the swap, retraining, recalibration, and a period of quality risk while the new system stabilizes. For a factory running twenty-four hours a day where every hour of downtime costs lakhs, this is a risk that most managers will not take unless forced to. The result is customer retention that industry participants estimate at eighty-five percent or higher.

The financial performance reflects this model's power. Revenue reached four hundred and twenty-five crores in fiscal year 2024. The five-year profit compound growth rate of twenty-seven percent is exceptional for an industrial company. The second quarter of fiscal year 2026 set a record with revenue of one hundred and two crores and profit of nearly nineteen crores. And the debt-free balance sheet provides both resilience and optionality.

However, the model is not without friction. Working capital management has been a persistent drag on return ratios. The nature of the business—selling equipment to industrial customers who expect credit terms, carrying inventory of machines and consumables, managing receivables across thousands of accounts—ties up cash. Improving working capital efficiency is perhaps the single most impactful lever management could pull to improve return on capital employed and return on equity without requiring any top-line growth.

Capital allocation has been disciplined. The M&A strategy involves small, targeted acquisitions—one and a half million euros for Markprint, one million pounds for Codeology—rather than transformative deals that could strain the balance sheet or create integration nightmares. The buyback in 2023 returned cash when management saw no better use for it. Dividends have been consistent. This is not a management team chasing growth at any cost; it is one that compounds value through steady reinvestment, strategic positioning, and patience.

VIII. Frameworks for Analysis: Forces, Powers, and Moats

Applying Michael Porter's Five Forces to Control Print reveals a business environment that is more favorable than it might initially appear.

The threat of new entrants is low. Building a coding equipment manufacturing capability requires significant capital investment in facilities, R&D, and testing infrastructure. But more importantly, it requires the kind of deep domain expertise that only comes from decades of operating in the industry—understanding which inks work on which substrates, how different printing technologies perform in different environmental conditions, what failure modes occur in specific industries. And replicating a three-hundred-plus engineer service network across India would take years and enormous capital. Control Print's thirty-year head start is a formidable barrier.

Supplier bargaining power is low to moderate. Core components like printheads and specialized electronics are sourced from a limited number of global suppliers, which creates some dependency. But inks and consumables—the highest-margin products—are manufactured in-house, and non-critical components come from a diversified supplier base.

Buyer bargaining power is moderate. Industrial buyers are sophisticated and price-sensitive, and they can choose from multiple coding technologies and suppliers. But once a machine is installed, the switching costs described earlier shift the balance back toward Control Print. The total cost of ownership argument—lower upfront price, cheaper consumables, faster service—is a powerful tool in negotiations.

The threat of substitutes is low to moderate. Different coding technologies compete with each other—laser versus inkjet versus thermal transfer—but they serve somewhat different applications, and coding itself is not optional. Products must be marked. There is no viable alternative to automated coding at industrial scale.

Competitive rivalry is high but manageable. Global giants compete aggressively, and Chinese entrants are adding price pressure. But Control Print's local manufacturing, service network, and cost structure create insulation that pure price competition cannot easily breach.

Hamilton Helmer's Seven Powers framework points to two dominant sources of competitive advantage. The first is counter-positioning. This is arguably Control Print's most important strategic asset. Global multinationals like Videojet and Domino have built their businesses around premium pricing and global standardization. To match Control Print's low-cost, high-service, India-specific approach, they would have to fundamentally restructure their Indian operations in ways that would cannibalize their premium positioning and compress their global margins. It is the classic innovator's dilemma: the incumbents can see what Control Print is doing, but responding effectively would hurt their existing business model.

The second power is switching costs. The integration of coding machines into production lines, the consumables lock-in, the training investment, the multi-year service relationships—these create a customer base that is remarkably difficult for competitors to poach. Combined, counter-positioning and switching costs create a sustainable moat against larger, better-resourced competitors.

IX. The Bull Case and the Bear Case

Every investment thesis must reckon with what could go wrong. For Control Print, the bear case centers on several legitimate risks.

Technology disruption is the most existential concern. Laser coding is getting cheaper and eliminates the consumables revenue stream entirely—no ink, no ribbons, just a laser beam. If laser technology advances to the point where it can replace inkjet and thermal transfer across a wide range of applications and substrates, Control Print's razor-blade model loses its blade. Digital codes like QR and RFID could theoretically reduce the need for traditional marking in some applications. And global players could introduce low-cost, India-specific product lines designed to compete directly with Control Print on price—something they have not yet done but certainly have the resources to attempt.

Competitive pressure from Chinese manufacturers like SUNINE, who can undercut even Control Print's pricing, is a growing concern, particularly in less brand-sensitive market segments. Execution risk on the international expansion and M&A integration front is real—transferring Markprint's technology to India, building a customer base through the MEA subsidiary, and extracting value from the Codeology joint venture are all genuinely difficult tasks that many companies fail at.

The financial picture has some blemishes. First-quarter fiscal year 2026 profit dropped over twenty-six percent year-on-year, raising questions about whether the eighty-four percent profit growth of the prior year was sustainable or a peak. Working capital management remains a drag on return ratios. And limited public disclosure of segment-level data makes it harder for outside investors to assess the true profitability and trajectory of individual business lines.

The bull case, however, rests on powerful structural tailwinds and a competitive position that would be extraordinarily difficult to replicate.

India's manufacturing sector is in the early innings of a multi-decade expansion driven by production-linked incentive schemes, the China-plus-one diversification trend, and growing domestic consumption. Every new factory needs coding equipment. Every new production line needs marking machines. Every tightening regulation creates forced demand. The pharmaceutical serialization mandates alone could drive a meaningful upgrade cycle across Control Print's installed base and create net new installations at factories that previously used basic solutions.

The company's position as the sole Indian manufacturer is a structural moat that would take any challenger a decade and hundreds of crores to breach. The installed base of seventy thousand machines is a consumables annuity that generates revenue regardless of whether the company sells a single new machine in any given quarter. The service network provides a level of customer lock-in that transcends the product itself.

And then there are the hidden options—growth vectors that are not yet priced into the current valuation because they are too early-stage to model with confidence. If Markprint's digital printing technology can be successfully adapted for the Indian packaging and textile markets, it opens an entirely new revenue stream with higher average selling prices than traditional coding equipment. If the MEA subsidiary gains traction, exports could grow from under three percent to ten or fifteen percent of revenue. If track-and-trace evolves into a software and services platform with per-unit transaction fees, it introduces a high-margin recurring revenue stream that transforms the company's economic profile.

The company trades at a market capitalization of roughly one thousand crores against four hundred and twenty-five crores in revenue and one hundred crores in profit—multiples that are modest by the standards of Indian small-cap industrial companies with this kind of growth profile and balance sheet strength.

X. The KPIs That Matter

For investors tracking Control Print's ongoing performance, three metrics deserve primary attention above all others.

The first is consumables revenue as a percentage of total revenue. This is the single most important indicator of business quality. A rising consumables mix means the installed base is generating more recurring, high-margin revenue—strengthening the moat, improving margins, and increasing the predictability of cash flows. If this ratio declines, it could signal that the installed base is aging out, that competitors are winning consumables share, or that the shift to laser coding is eroding the blade business. This number should trend upward over time for the thesis to hold.

The second is the export revenue mix. Currently at two point eight five percent, this metric will reveal whether the international expansion strategy—the MEA subsidiary, the Markprint integration, the Codeology partnership—is producing real commercial results or remaining aspirational. A move from under three percent to ten or fifteen percent over the next three to five years would validate the strategy and meaningfully diversify revenue sources and growth drivers.

The third is working capital days. This is the operational efficiency lever that management has the most direct control over, and improvement here would flow directly to return on capital employed and return on equity without requiring any top-line acceleration. A declining trend in working capital days would signal that management is executing on the operational discipline needed to compound value more efficiently.

XI. Recent Developments and What Comes Next

The most recent data points paint a picture of a company at an inflection point. The second quarter of fiscal year 2026 delivered record revenue of one hundred and two crores with healthy profit growth, suggesting that the first-quarter dip was more likely a seasonal or one-time phenomenon than a structural deterioration. The increase in Markprint's stake to ninety percent signals that management is more, not less, confident in the digital printing bet after a year of operating the business. The MEA subsidiary incorporation in January 2025 is a tangible step toward geographic diversification. And Basant Kabra's personal shareholding increase reinforces the family's conviction in the long-term trajectory.

The challenges ahead are real but manageable. Working capital efficiency needs to improve. The international businesses need to demonstrate commercial traction beyond their first few customers. Technology investments in laser coding and IoT integration need to keep pace with global competitors who have larger R&D budgets. And the company needs to begin providing more granular segment-level disclosures to allow investors to properly assess the growth and profitability of individual business lines.

The next chapter of the Control Print story will be written across three theaters simultaneously. In India, the core business will be driven by manufacturing expansion, regulatory mandates, and the steady drumbeat of consumables revenue from a growing installed base. Internationally, the MEA hub and European footholds through Markprint and Codeology will test whether the localization playbook that worked in India can be adapted for other emerging and developed markets. And in new technology domains, the digital printing and track-and-trace bets will either validate or undermine the thesis that Control Print can evolve from a coding equipment company into a broader industrial printing and compliance platform.

XII. Lessons for Founders and Investors

The Control Print story contains several lessons that are worth extracting, not because they are novel, but because they are so rarely executed with this kind of patience and discipline.

For founders, the most striking lesson is about timing and preparation. Basant Kabra did not rush to manufacture his own equipment. He spent seventeen years—an entire generation in startup terms—importing, distributing, and servicing other companies' machines. He used that time to build a service network, understand customer pain points, study failure modes, and develop the domain expertise needed to design equipment specifically for Indian conditions. When he finally made the move in 2008, he was not guessing about what the market needed. He knew. The lesson is not that founders should wait seventeen years before making their big bet. The lesson is that deep domain expertise, patiently accumulated, creates a quality of insight that no amount of market research or consulting can replicate.

The razor-blade model, when executed properly, creates a business that is far more valuable than its revenue line suggests. Every machine sold is not revenue—it is a customer acquired for a multi-year consumables relationship. The upfront economics of the machine sale matter far less than the lifetime economics of the relationship. Companies that understand this will invest in customer acquisition—lower machine prices, better service, easier financing—even when it compresses near-term margins, because they are playing a different game than competitors focused on maximizing margin per transaction.

For investors, Control Print illustrates the power of looking for businesses where switching costs and counter-positioning intersect. The consumables lock-in provides predictable recurring revenue. The local manufacturing and service advantage creates a cost and service position that global competitors cannot match without restructuring their entire business model. Together, these two forces create a moat that is wider than either would be alone.

The question that hangs over the story—can Control Print become the Videojet of Asia, or will global giants eventually find a way to crush the local champion?—will not be answered tomorrow. But the structural position, the management alignment, the balance sheet strength, and the multiple growth vectors suggest that the answer, whatever it turns out to be, will be worth watching closely.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube