Cohance Lifesciences: India's CDMO Consolidation Play

I. Introduction & Episode Roadmap

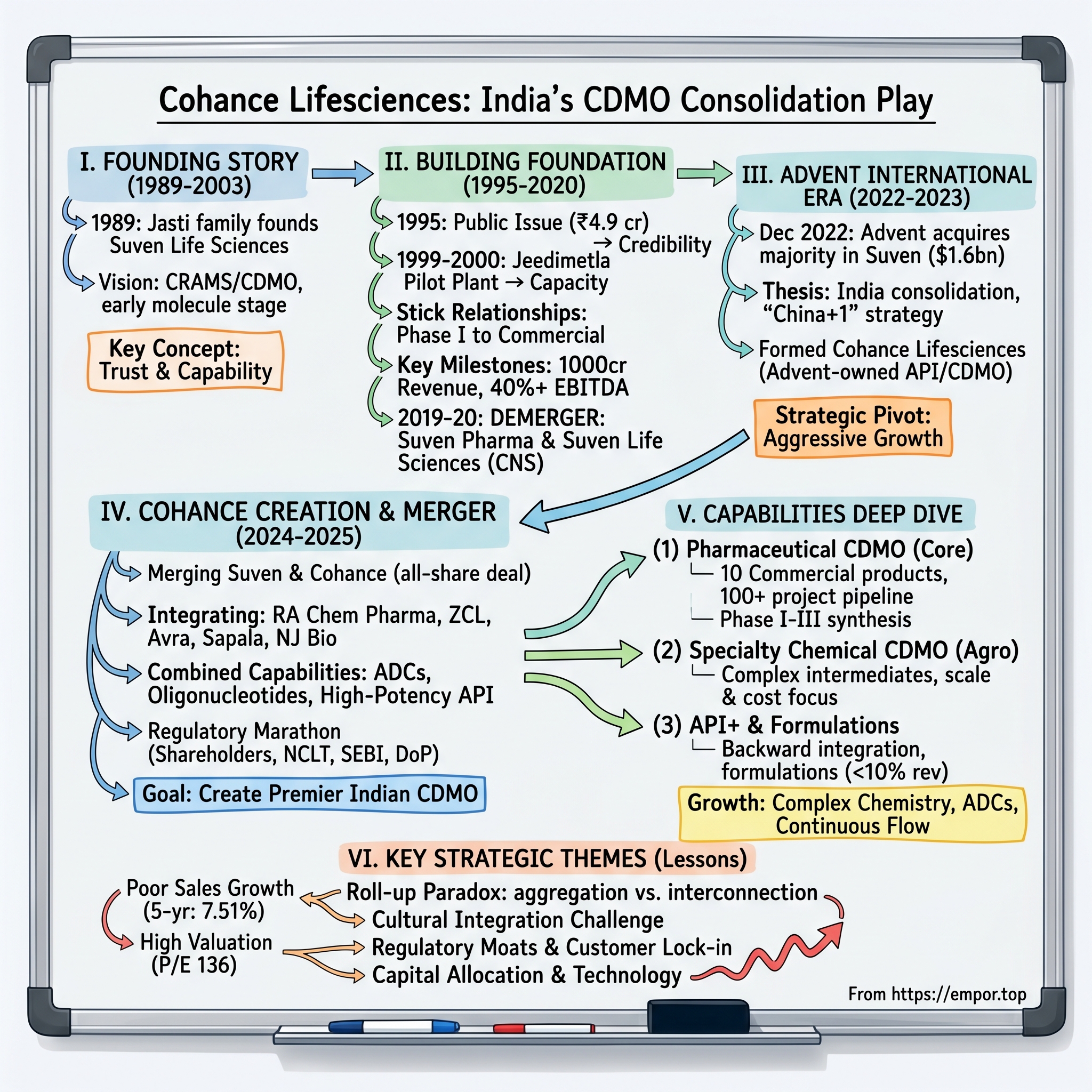

The conference room at Hyderabad's Genome Valley was packed with investment bankers, lawyers, and pharmaceutical executives on a humid February morning in 2024. After months of negotiations, whispered corridor conversations, and late-night Excel modeling sessions, the deal was finally announced: Suven Pharmaceuticals would merge with Cohance Lifesciences, creating a $3 billion contract drug manufacturing giant. The kicker? Both companies were already controlled by the same private equity firm—Advent International—making this less a traditional merger and more of a financial engineering masterpiece designed to consolidate India's fragmented CDMO sector. With a market capitalization exceeding ₹36,000 crore and revenue of ₹1,198 crore, Cohance represents something profound: the transformation of India's pharmaceutical services industry from a collection of family-run shops into globally competitive platforms capable of serving Big Pharma's most complex needs. The Hyderabad-based CDMO company offers end-to-end services to leading global pharmaceutical and fine chemical majors in their NCE (New Chemical Entity) development endeavors, positioning itself at the intersection of India's technical capabilities and global supply chain realignments.

But this isn't just another pharmaceutical company story. It's a narrative about how private equity spotted an opportunity in India's fragmented contract manufacturing landscape, how geopolitical tensions created unprecedented tailwinds for Indian pharma services, and how financial engineering can create value through consolidation in industries where scale increasingly matters. The protagonist isn't a charismatic founder or a breakthrough drug—it's a strategic thesis playing out in real-time: that India's CDMO sector can replicate what Taiwan did in semiconductors or what China achieved in electronics manufacturing.

The company has established itself as one of the top 5 providers of high-end intermediates to innovators in India, yet it has delivered poor sales growth of just 7.51% over the past five years—a contradiction that frames our central question: Can private equity-driven consolidation transform a collection of steady but unspectacular assets into a high-growth platform? Or is this merely financial engineering masquerading as operational transformation?

Over the next several hours, we'll unpack this story layer by layer—from the humid laboratories of 1989 Hyderabad where it all began, through the boardrooms of Boston where Advent International crafted its consolidation playbook, to the factory floors where molecules are synthesized for some of the world's most important medicines. We'll explore how a company named "Cohance"—symbolizing Collaboration, Convergence, and Enhancement—represents both the promise and perils of India's pharmaceutical ambitions.

The stakes couldn't be higher. As global pharmaceutical companies desperately seek to diversify their supply chains away from China, India stands at an inflection point. The winners in this race won't just capture billions in revenue; they'll help determine where the world's medicines come from for the next generation. And at the center of this transformation sits Cohance—part family legacy, part private equity play, entirely representative of modern India's corporate evolution.

II. The Jasti Family & Founding Story (1989–2003)

The monsoon rains had just begun their annual assault on Hyderabad when Subba Rao Jasti sat down with his son Venkateswarlu in the summer of 1989. India was on the cusp of economic liberalization, the Berlin Wall would fall within months, and the global pharmaceutical industry was about to undergo its most dramatic transformation since the discovery of penicillin. But in that modest office in Banjara Hills, the conversation was more personal than geopolitical. Venkateswarlu had been running six community pharmacies across New York and New Jersey since 1977, building a comfortable life in America. He'd earned his pharmacy degrees from both Andhra University and St. John's University in New York, specializing in industrial pharmacy. He was even president-elect of the Essex County Pharmaceutical Society of New Jersey—no other Indian had occupied that position. By any measure, the younger Jasti had made it in America.

Yet something pulled him back. Maybe it was watching American pharmaceutical companies begin their great outsourcing wave of the late 1980s. Maybe it was India's changing intellectual property landscape, with the country preparing to recognize product patents for the first time. Or perhaps it was simply the immigrant's eternal tension between success abroad and purpose at home. Whatever the catalyst, Venkateswarlu returned to India and co-founded Suven Life Sciences Limited in 1989.

The name "Suven" itself carried meaning—a Sanskrit word suggesting good tidings and prosperity. But prosperity in 1989 India looked different than it does today. The country was still a year away from its foreign exchange crisis that would force economic liberalization. The pharmaceutical industry operated under the 1970 Patents Act, which recognized only process patents, not product patents. This created a unique ecosystem where Indian companies became masters at reverse-engineering Western drugs through alternative synthetic routes—a capability that would prove invaluable decades later. From 1977 to 1989, Venkateswarlu had successfully owned and operated a chain of 6 community pharmacies in New York and New Jersey, then returned to India to co-found Suven Life Sciences Limited in 1989. But what made his return particularly prescient was his vision for what India could become in the global pharmaceutical value chain. He wasn't interested in simply manufacturing generic drugs—the dominant Indian pharma model of the time. Instead, he pioneered what would become known as the CRAMS (Contract Research and Manufacturing Services) business model in India.

The timing was both terrible and perfect. Terrible because India's pharmaceutical infrastructure was still nascent, regulatory frameworks were evolving, and global pharmaceutical companies had little reason to trust Indian partners with their precious intellectual property. Perfect because Venkateswarlu understood something fundamental: the global pharmaceutical industry was about to undergo a seismic shift in how it approached drug development and manufacturing.

In September 2003, fourteen years after founding, the company underwent its first major transformation—changing its name from Suven Pharmaceuticals Limited to Suven Life Sciences Limited. This wasn't mere cosmetic rebranding. It signaled a strategic pivot from being seen as just another pharmaceutical manufacturer to positioning itself as a partner in the entire life sciences value chain. The company had spent over a decade building capabilities, earning trust, and most importantly, proving that Indian companies could handle complex chemistry while respecting intellectual property—a concern that haunted every conversation with Western pharmaceutical companies in those early years.

As Jasti recalled: "I decided it was time to move into the supply chain of the innovators, but it was difficult to do so for a small, Rs 3-crore company. It was then that we devised a business model, which is today popular as CRAMS, to knock at the doors of innovator companies." Suven went public in 1995 and decided to "align itself with innovator pharma companies and supplying drug intermediates for their new chemical entity development programmes".

The early years were marked by what can only be described as missionary zeal. Venkateswarlu would fly to pharmaceutical conferences in Europe and America, setting up modest booths between giants like Lonza and Catalent, patiently explaining to skeptical executives why they should trust a company from Hyderabad with their clinical-stage molecules. He leveraged his unique background—having been president-elect of the Essex County Pharmaceutical Society of New Jersey, a position no other Indian had occupied until then—to open doors that might have remained closed to other Indian entrepreneurs.

By 2003, as the company prepared for its name change, it had already laid the groundwork for what would become one of India's most sophisticated contract manufacturing operations. The Jasti family had invested not just capital but credibility, building relationships one molecule at a time, one successful delivery at a time. They understood that in the pharmaceutical services business, trust is earned in micrograms and lost in kilograms.

The Indian context during this period cannot be ignored. The country was emerging from decades of socialist economic policies, infrastructure was improving but still inadequate, and the global perception of "Made in India" was far from premium. Yet within this challenging environment, companies like Suven were quietly building capabilities that would later make India indispensable to global pharmaceutical supply chains. They were preparing for a future where cost wouldn't be India's only advantage—technical capability, regulatory compliance, and innovation would matter just as much.

III. Building the CRAMS/CDMO Foundation (1995–2020)

In March 1995, Suven came out with a public issue of 9.8 lakh equity shares at a premium of Rs 40, aggregating Rs 4.9 crore to part-finance the company's project for the manufacture of bulk drugs and drug intermediates and meet long-term working capital requirements totaling Rs 6.43 crore. The amount seems quaint by today's standards—less than what a Bangalore startup might raise in a pre-seed round. But in 1995 India, for a six-year-old pharmaceutical services company, it represented a massive vote of confidence.

The public listing wasn't just about capital. It was about credibility. When Venkateswarlu approached potential clients at pharmaceutical conferences, being able to say "we're a publicly listed company with transparent financials" carried weight. It differentiated Suven from the numerous family-run chemical shops that dotted India's pharmaceutical landscape. The governance requirements of being public—regular audits, quarterly disclosures, board oversight—aligned perfectly with what global pharmaceutical companies needed from their suppliers: predictability, transparency, and accountability. The period from 1999 to 2000 marked a significant expansion when the company acquired a small pilot plant in Jeedimetla Industrial Estate, Hyderabad. This wasn't just about adding capacity—it was about creating dedicated spaces for different types of chemistry. Suven was developing what the industry calls "sticky" relationships with global pharmaceutical companies. These weren't transactional vendor relationships but deep partnerships where Suven's scientists would work on molecules from Phase I clinical trials through commercialization, sometimes a journey spanning 10-15 years.

The business model Venkateswarlu pioneered was elegantly simple yet fiendishly difficult to execute. When a pharmaceutical company discovers a promising molecule, they need someone to manufacture it—first in grams for laboratory testing, then in kilograms for animal studies, eventually in tons if the drug reaches market. Most Indian companies focused on the lucrative commercial manufacturing end. Suven deliberately started at the beginning, when volumes were tiny and margins thin, betting that being involved early would create switching costs too high for clients to bear later.

Under CRAMS, Suven worked with innovator companies at the clinical trial stage right till molecule commercialization, serving 18 global life sciences companies. The company was working on 52 molecules, with 26 undergoing phase I clinical trials, 21 in phase II, and 5 in phase III. The mathematics of this model were compelling: volumes supplied increased more than 10 times as products moved from phase I to phase II to phase III.

The company's technical capabilities evolved in lockstep with client requirements. Suven established core competencies in cyanation and heterocyclic chemistry, covering pyrimidines, quinolones, thiazoles, and imidazoles—the building blocks of modern pharmaceuticals. These weren't just random technical capabilities; they were carefully chosen based on where the pharmaceutical industry was heading. As drugs became more complex, targeting specific biological pathways rather than broad mechanisms, the chemistry required to make them became correspondingly sophisticated.

By 2013-14, the patience began paying dividends. Three molecules of global innovator companies, for which Suven developed intermediates, moved into the pre-launch stage. This was the validation of the business model—molecules that Suven had been working on for years were finally approaching commercialization. The company granted an exclusive license to Taro Pharmaceuticals to market products in the US, Canada, and Mexico, creating a new revenue stream through royalties.

The financial performance reflected this evolution. The company crossed the ₹1000 crore revenue mark for the first time in FY21, with revenues growing 20% year-over-year and more than 90% coming from regulated markets. EBITDA grew 14% and the company maintained EBITDA margins above 40%, one of the highest in the industry.

But success brought its own challenges. The CRAMS business was generating substantial cash flows, yet Venkateswarlu had grander ambitions. He didn't just want to be a service provider; he wanted Suven to discover its own drugs. This led to significant R&D investments in CNS (Central Nervous System) therapies, with molecules like SUVN-502 for Alzheimer's disease entering clinical trials. The combined entity faced a fundamental tension: CRAMS and Specialty Chemicals were cash-generating businesses with high margins, but cash from these segments was being used to fund research and clinical trials for proprietary molecules.

This tension would ultimately lead to one of the most important decisions in the company's history. In 2019-20, Suven Life Sciences demerged its CRAMS business into a wholly owned subsidiary, Suven Pharmaceuticals Limited, through a scheme of arrangement approved by the NCLT Hyderabad Bench. The demerger split Suven into Suven Pharmaceuticals, focusing on contract research, and Suven Life Sciences, focusing on neuroscience therapies. The equity shares of the new entity were listed on March 9, 2020—ironically, just as the world was shutting down due to COVID-19.

The demerger was more than financial engineering—it was philosophical. For thirty years, the Jasti family had built a business based on serving others' innovation. Now they were splitting it, allowing each piece to pursue its destiny. The CRAMS business would continue its steady growth, while the drug discovery arm would chase the moonshot of developing novel CNS therapies. It was a bet that both businesses would be worth more apart than together, that capital markets would better appreciate focused stories than conglomerates.

By 2020, Suven Pharmaceuticals had emerged as a formidable CDMO player. Built on more than 33 years of research, innovation, and quality, the company had world-class infrastructure across India and USA, over 1000 employees, USFDA audited facilities, and had executed over 880 projects with a team including 400+ scientists, 35 of whom held PhDs. The company had proven that Indian pharmaceutical services could compete not just on cost but on capability, reliability, and innovation.

The stage was set for the next act—one that would involve private equity, consolidation, and a vision to create India's premier CDMO platform. The Jasti family had built the foundation; now it was time for new architects to construct the superstructure.

IV. The Advent International Era Begins (2022–2023)

On a crisp December morning in 2022, the pharmaceutical industry woke up to news that would reshape India's CDMO landscape. Advent International, the Boston-based private equity giant with $88 billion in assets under management, announced it was acquiring a majority stake in Suven Pharmaceuticals. The deal valued the company at approximately ₹13,250 crore ($1.6 billion), making it one of the largest pharmaceutical services transactions in Indian history. The announcement sent ripples through both the pharmaceutical and financial communities. Advent agreed to acquire 50.1% of Suven from the Jasti family for at least 63.13 billion rupees ($762 million), with the stake purchase at Rs 495 per share. As part of the transaction, Advent would also make an open offer to acquire an additional 26% of the outstanding equity shares from public shareholders.

But this wasn't just about one company changing hands. Cohance Lifesciences, wholly owned by Advent, was formed in November 2022 to create a new brand identity for its CDMO and API platform, with an intention of bringing together three Advent portfolio companies – RA Chem Pharma, ZCL Chemicals and Avra Laboratories. Advent wasn't buying Suven; it was assembling something much larger.

The timing was no accident. The global pharmaceutical industry was undergoing its most significant supply chain reconfiguration since the 1990s. COVID-19 had exposed the risks of over-concentration in China, which dominated global API and intermediate manufacturing. Western pharmaceutical companies were desperately seeking to diversify their supply chains—a strategy dubbed "China+1" by consultants who charged six figures to state the obvious. India, with its established pharmaceutical infrastructure, English-speaking workforce, and regulatory track record, was the natural beneficiary. India's contract drug manufacturers were seeing a boost as global pharma companies looked for services outside China to diversify supply chains. Goldman Sachs noted that India's contract research and manufacturing sector was starting to benefit from the global "China+1" diversification strategy, with large pharmaceutical companies beginning to shift parts of their outsourcing pipeline to India. Firms like Syngene, Neuland Labs and Divi's had started converting RFQs into pilot projects or initial contracts over the last 1-1.5 years.

Pankaj Patwari, Managing Director at Advent International, articulated the vision clearly: "Our vision for Suven is to build a $1 billion global leader, by executing effectively on the product pipeline, building new marquee customers, turbo-charging business development, and scaling up manufacturing and R&D". He added that they would "also look at acquiring synergistic businesses globally, to further build capabilities and gain new customer access".

This wasn't Advent's first rodeo in Indian healthcare. Advent had invested in India since 2007 and committed more than $3.2 billion to 14 companies with headquarters or operations in India, with previous healthcare investments including Bharat Serums and Vaccines. They understood the Indian pharmaceutical landscape's unique dynamics—the regulatory complexities, the talent arbitrage, the infrastructure challenges, and most importantly, the enormous opportunity.

The Jasti family's perspective on the deal was equally telling. Venkateswarlu Jasti said: "We are delighted to bring Advent into Suven Pharma as a strategic investor. We have built a business with industry leading growth & margins. We have cultivated excellent relationships with multiple global innovator companies backed by deep R&D capabilities and demonstrated track record of execution and delivery excellence. Advent is the ideal partner for us, with deep expertise in healthcare, and a global network of professionals and experts. Their experience and resources will launch the next phase of growth for Suven pharma".

But the real strategic masterstroke was what came next. Cohance Lifesciences, wholly owned by Advent, was formed in November 2022 to create a new brand identity for its CDMO and API platform, with an intention of bringing together three Advent portfolio companies – RA Chem Pharma, ZCL Chemicals and Avra Laboratories. Cohance's two business units, CDMO and API+, catered to development and manufacturing for pharma and specialty chemical innovators, and leading global generic companies with complex product requirements respectively.

The broader market context made Advent's timing appear prescient. India's CDMO market was at ₹18,800 crore in 2024, and was expected to grow to ₹37,200 crore by 2029, at a CAGR of 14.7%. India was transitioning from being primarily a generics powerhouse to becoming a hub for high-value drugs, amplified by the West's inflationary climate, marginal pressures, and dwindling enthusiasm for building new facilities. While a 'China plus one' strategy was currently in vogue, analysts envisioned that five years down the line, the emphasis might shift from being China-centric to adopting an 'India plus one' approach.

The regulatory environment was also shifting in India's favor. US legislators were in the process of considering the US Biosecure Act that attempted to diversify US pharmaceutical supply chains from companies that had linkages with Chinese government/military, which could potentially benefit India's CDMO companies as they could replace some Chinese companies in the supply chain.

By September 2023, the transformation was complete. Advent International completed the acquisition of a majority stake in Suven Pharma, announcing a change in the pharma company's board. Suven Pharma would be led by a team comprising Annaswamy Vaidheesh as executive chairman, V Prasada Raju as managing director, and Sudhir Kumar Singh as chief executive officer.

The new leadership brought impressive credentials. Vaidheesh had over 35 years of experience, including as managing director of GSK India, president of OPPI, and earlier with J&J Asia Pacific in senior regional leadership positions. Prasada Raju had over 29 years of experience in the pharmaceutical industry, with leadership roles at Cohance Life Sciences, Granules India Ltd., and Dr Reddy's Laboratories.

The Advent era had begun in earnest. The stage was set for the next act: the grand consolidation that would create Cohance Lifesciences, a platform designed not just to participate in the China+1 opportunity but to lead it. The Jasti family had built a solid foundation over three decades; Advent was now constructing a skyscraper on top of it.

V. The Cohance Creation & Merger Saga (2024–2025)

The announcement came on the last day of February 2024, just as India's financial year was drawing to a close. In regulatory filings that would reshape the Indian CDMO landscape, Suven Pharmaceuticals and Cohance Lifesciences announced their intention to merge in an all-share deal that valued the combined entity at approximately $3 billion. The complexity of the transaction—merging two companies already controlled by the same private equity firm—would have made investment bankers salivate and regulators scratch their heads. The share swap ratio was carefully calibrated: 11 Suven shares for every 295 Cohance shares. Post-merger, Advent entities would own 66.7% and public shareholders would hold 33.3% in the combined entity (pre-ESOP dilution). The proposed merger was expected to be double-digit EPS accretive from the first year of being effective—a key selling point for public shareholders who might otherwise question why they should support a transaction that further concentrated control with private equity.

The strategic rationale was compelling on paper. As per Suven, the merged platform would comprise three distinct business units—Pharma CDMO, Spec Chem CDMO, and API+ (inclusive of formulations). The integrated CDMO model would enable comprehensive molecule development and lifecycle management for both pharmaceutical and specialty chemical partners. Cohance's addition, particularly its fast-growing ADC (antibody-drug conjugate) platform, would reinforce Suven's position as a leading CDMO platform.

But the real story wasn't in the press releases—it was in the boardrooms and laboratories where the integration was being planned. The roll-up strategy that Advent had been executing wasn't just about adding revenues; it was about creating a platform with capabilities that no single Indian CDMO possessed. RA Chem Pharma brought expertise in complex chemistry, ZCL Chemicals had deep relationships with agrochemical companies, Avra Laboratories specialized in high-potency APIs, Sapala Organics offered advanced intermediates capabilities, and NJ Bio brought formulation expertise. The regulatory marathon that followed tested everyone's patience. The transaction required approvals from shareholders, creditors, NCLT, Department of Pharmaceuticals, and regulatory approvals from stock exchanges and SEBI. Each milestone was carefully orchestrated—over 99.9% of Suven's equity shareholders and 99.967% of Cohance's shareholders voted in favor of the Scheme of Amalgamation during meetings held on November 28, 2024.

Finally, in May 2025, the pieces fell into place. The Department of Pharmaceuticals (DoP), Ministry of Chemicals and Fertilizers, Government of India, granted final approval for foreign investment under applicable regulations, marking the final regulatory clearance required to implement the Scheme of Amalgamation between Cohance Lifesciences Limited and Suven Pharmaceuticals Limited, a transaction previously approved by shareholders and sanctioned by the Hon'ble NCLT, Mumbai Bench.

In line with the terms of the approved Scheme of Amalgamation, the merger took effect from the business opening hours of 1st May 2025, following the satisfaction of all prescribed conditions. The official name change to Cohance Lifesciences Limited took effect on May 7, 2025, following approval from the Ministry of Corporate Affairs, Government of India.

The name "Cohance" itself carried meaning—symbolizing Collaboration, Convergence, and Enhancement. It represented not just the coming together of companies but the convergence of capabilities, the enhancement of offerings, and the collaboration needed to serve global pharmaceutical innovators.

Vivek Sharma, Executive Chairman of the merged entity, articulated the vision: With Cohance's unique technological platform in ADC, we are well-positioned to become a $1 billion revenue company in next five years with higher CDMO contribution. The company was targeting to more than double their combined revenue to around Rs 6,000 crore by FY29 by undertaking both organic and inorganic growth routes.

The merged platform represented something unprecedented in Indian pharmaceutical services. What started in 2003 as RA Chem Pharma evolved through strategic acquisitions of ZCL Chemicals, Avra Laboratories, Suven Pharmaceuticals, Sapala Organics, and NJ Bio—each adding distinct capabilities across APIs, Specialty Chemicals, Formulations, and next-gen platforms like ADCs and Oligonucleotides. The combined entity now had 8 manufacturing units (5 USFDA approved) and 2 R&D dedicated units, presence in 60 countries with an 80+ molecules product basket.

The strategic positioning was clear. India holds a 2.7 per cent share of the global CDMO market, and Suven-Cohance aims to capitalise on this opportunity by expanding international contracts and advancing a strong pipeline of Phase-3 molecules. With 13 Phase-3 intermediate projects in progress, the company anticipates benefiting from India's projected growth in global CDMO share to 5-7 per cent over the next four to five years.

But beneath the corporate speak and regulatory filings, there was a deeper transformation occurring. The merger wasn't just creating scale; it was creating capabilities that few Indian CDMOs possessed. The ADC platform, in particular, positioned Cohance at the forefront of one of pharmaceuticals' most promising frontiers—targeted cancer therapies that combine the specificity of antibodies with the potency of cytotoxic drugs.

The integration challenges were real. Combining companies with different cultures, systems, and ways of working required careful orchestration. With the merger becoming effective, the Company initiated the operational and organizational integration, aligning systems, capabilities, and teams. Each acquired company brought its own legacy systems, customer relationships, and operational quirks that needed to be harmonized without disrupting ongoing projects.

Yet the potential rewards justified the complexity. The merged entity was positioned to capitalize on multiple tailwinds: the China+1 strategy driving supply chain diversification, the growing complexity of pharmaceutical molecules requiring specialized manufacturing capabilities, and the increasing willingness of global pharmaceutical companies to partner with Indian CDMOs for critical projects.

As the newly christened Cohance Lifesciences began trading on the exchanges, it represented more than just another corporate merger. It was a bet on India's ability to move up the pharmaceutical value chain, from being a provider of cheap generics to becoming a trusted partner for the world's most sophisticated drug development programs. The transformation from Suven to Cohance wasn't just a name change—it was a declaration of intent to compete on the global stage.

VI. Business Model & Capabilities Deep Dive

The heart of any CDMO lies not in its boardrooms or financial statements but in its laboratories and manufacturing plants, where molecules are coaxed through their journey from experimental curiosity to life-saving medicine. At Cohance, this journey spans three distinct yet interconnected business units that together create what executives call an "integrated platform"—though what that really means requires understanding the intricate dance between chemistry, biology, and industrial engineering.

The Pharmaceutical CDMO unit represents the company's historical core and its most sophisticated capabilities. This isn't the commodity API manufacturing that made India famous in the 1990s. Instead, Cohance focuses on complex molecules in development—the kind where a single misstep in synthesis can set a drug development program back by months and cost millions. Suven's existing pharma CDMO platform includes 10 commercial products and more than 100 projects in its pipeline.

Consider what happens when a pharmaceutical company discovers a promising molecule for treating, say, Alzheimer's disease. Initially, they need perhaps 100 grams for preliminary testing—a quantity that might fit in a coffee cup but requires months of painstaking synthesis. As the molecule progresses through clinical trials, the quantities scale exponentially: kilograms for Phase I, tens of kilograms for Phase II, potentially tons if the drug reaches market. At each stage, the manufacturing process must be refined, validated, and documented with a precision that would make Swiss watchmakers envious.

Cohance's expertise lies in managing this entire continuum. Their scientists work alongside clients' R&D teams, often spending months optimizing a synthetic route to improve yield from, say, 12% to 18%—a seemingly modest improvement that could mean the difference between commercial viability and failure. They've developed particular expertise in what the industry calls "heterocyclic chemistry"—creating ring-shaped molecules that form the backbone of many modern pharmaceuticals. It's the molecular equivalent of origami, where carbon, nitrogen, and oxygen atoms must be folded into precise three-dimensional shapes.

The Specialty Chemical CDMO unit serves a different master: the agrochemical industry. Here, the challenges are less about regulatory precision and more about scale and cost. A new pesticide might require production of thousands of tons annually, with margins measured in cents per kilogram rather than dollars per gram. Cohance has built capabilities in complex intermediates for crop protection chemicals, leveraging India's cost advantages while meeting the stringent environmental standards required by global agrochemical companies.

The synergies between pharmaceutical and agrochemical manufacturing aren't immediately obvious, but they're profound. Both require similar reactor technologies, analytical capabilities, and safety protocols for handling hazardous materials. A reactor used to make a cancer drug intermediate in January might be manufacturing a herbicide precursor in June. This flexibility—carefully managed to prevent cross-contamination—allows Cohance to optimize asset utilization in ways that single-focus CDMOs cannot. The API+ business, including formulations, represents the third leg of Cohance's platform. This is where the company's backward integration strategy pays dividends. By controlling the entire value chain from intermediate synthesis through finished dosage forms, Cohance can offer what industry insiders call "one-stop shopping"—a particularly valuable proposition for smaller biotech companies that lack the resources to manage multiple suppliers.

But it's the recent acquisitions that have transformed Cohance from a competent CDMO into a potential industry leader. The addition of NJ Bio brought expertise in antibody-drug conjugates (ADCs), one of oncology's hottest areas. ADCs—often called "the guided missiles of cancer therapy"—combine the targeting specificity of antibodies with the cell-killing power of cytotoxic drugs. The global ADC market was valued at $10.77 billion in 2024 and is expected to reach $34.32 billion by 2032, growing at a CAGR of 15.59%.

Manufacturing ADCs is extraordinarily complex. First, you need to produce the antibody—a protein engineered to recognize specific markers on cancer cells. Then you must synthesize the cytotoxic payload, often a molecule so potent that exposure to microscopic quantities can be lethal. These components must be linked together using chemistry that's stable enough to survive circulation in the bloodstream but will reliably release the payload once inside cancer cells. The entire process must be conducted in facilities designed to handle materials with occupational exposure limits measured in nanograms—requiring specialized air handling systems, containment technologies, and safety protocols that make typical pharmaceutical manufacturing look casual by comparison.

Cohance's ADC capabilities, enhanced by the NJ Bio acquisition, position it among a select group of CDMOs globally capable of handling these projects. Industry expert Herman Bozenhardt estimates that "only five CDMOs are fit for purpose" when it comes to ADCs, primarily due to the challenges of handling highly potent compounds. The market is particularly attractive because customer stickiness in ADCs is even higher than in traditional pharmaceuticals—once a company has invested in developing an ADC with a particular CDMO, the complexity and regulatory burden of switching suppliers creates enormous barriers to change.

The acquisition of Sapala Organics added another cutting-edge capability: oligonucleotide synthesis. Oligonucleotides—short DNA or RNA sequences—represent another frontier in pharmaceutical development, used in everything from gene therapy to COVID vaccines. The chemistry involved is completely different from traditional small molecules or even proteins, requiring specialized equipment, expertise, and quality control methods. Few CDMOs globally have meaningful oligonucleotide capabilities, and even fewer can offer it alongside traditional small molecule and protein manufacturing.

The numbers tell part of the story. Cohance now operates 8 manufacturing units with 5 USFDA approved facilities, employing over 1000 professionals including 400+ scientists, 35 with PhDs. The company's reactor capacity spans from laboratory scale to 6,000-liter production vessels, with the ability to handle temperatures from -80°C to 200°C and pressures up to 10 bar. But these specifications only hint at the real capability: the ability to execute chemistry that most CDMOs won't even attempt.

The customer base reflects this sophistication. While Cohance doesn't disclose all its clients for confidentiality reasons, the company serves over 60 global pharmaceutical and fine chemical companies across 60 countries. The concentration is significant—top clients likely account for a substantial portion of revenue, creating both stability (these relationships often span decades) and risk (loss of a major client could significantly impact financial performance).

The integrated model creates multiple touchpoints with clients. A pharmaceutical company might start by outsourcing synthesis of an early-stage intermediate to Cohance. As the molecule progresses through development, Cohance can take on additional steps—perhaps manufacturing the API, developing the formulation, even producing clinical trial materials. By the time a drug reaches commercial stage, switching to another supplier would require repeating years of process development, validation, and regulatory filing—a proposition few companies would willingly undertake.

This stickiness is reflected in the project pipeline. With 13 Phase-3 intermediate projects in progress, Cohance is positioned to benefit as these molecules transition to commercial production. The economics of this transition are compelling: a molecule that generates perhaps $1 million in revenue during clinical trials might produce $10-50 million annually once commercialized, with margins expanding as production scales and processes optimize.

The operational excellence required to maintain these capabilities cannot be overstated. A single FDA warning letter can shut down a facility for months. A batch failure can delay a clinical trial and cost clients millions. Even minor deviations from validated processes require extensive documentation and can trigger regulatory scrutiny. In this environment, Cohance's track record—maintaining FDA approvals across multiple sites while managing hundreds of projects—represents a competitive moat as real as any patent portfolio.

Yet challenges remain. The company has delivered poor sales growth of just 7.51% over the past five years, suggesting that despite its capabilities, Cohance hasn't fully capitalized on the CDMO boom. Debtor days have increased from 54.4 to 86.7 days, indicating either loosening credit terms to win business or challenges in collection. The company's EBITDA margin of 31.33%, while healthy, trails some pure-play CDMO competitors.

The technology platforms tell the story of where Cohance is heading. Beyond traditional chemistry, the company is investing in continuous flow manufacturing, which can dramatically improve efficiency and safety for certain reactions. They're developing capabilities in biocatalysis, using enzymes to perform chemical transformations that would be difficult or impossible with traditional chemistry. The ADC and oligonucleotide platforms position Cohance at the forefront of next-generation therapeutics.

VII. Financial Performance & Market Position

The numbers tell a story of transformation, though not always the triumphant narrative one might expect from a $36,000 crore market capitalization company. Cohance Lifesciences trades at a price-to-earnings ratio of 136, a valuation that would make even Silicon Valley unicorns blush. Yet beneath this frothy multiple lies a more complex financial reality that reveals both the promise and perils of roll-up strategies in the pharmaceutical services sector.

Start with the headline metrics: Revenue of ₹1,198 crore, profit of ₹265 crore, and an EBITDA margin of 31.33%. By pharmaceutical CDMO standards, these are respectable numbers. The margin profile suggests a business with meaningful pricing power and operational efficiency. But context matters. The company's five-year sales growth of just 7.51% significantly lags both the broader CDMO market (growing at 14-15% annually) and investor expectations implied by that stratospheric P/E ratio.

The stock price journey has been volatile. From its March 2020 listing as the demerged Suven Pharmaceuticals at around ₹145, shares rocketed to over ₹1,350 by December 2024 before settling back to current levels around ₹1,060. This represents a remarkable return for early investors but also suggests a market struggling to properly value a company undergoing fundamental transformation.

The book value of ₹66.6 per share means the stock trades at 14.1 times book—expensive even by the standards of asset-light technology companies, let alone a capital-intensive manufacturing business. This disconnect between market valuation and tangible assets reflects investor belief in intangibles: customer relationships, technical expertise, regulatory approvals, and most importantly, the potential for Advent to execute value-creating M&A.

Quarterly performance has been uneven. In Q4 FY25, net profit declined 21.29% to Rs 42.01 crore compared to Rs 53.37 crore in Q4 FY24, despite sales rising 58.95% to Rs 402.02 crore. This margin compression tells a story common in roll-ups: the challenge of integrating acquisitions while maintaining operational efficiency. The company attributed the pressure to "a shift in business mix and customer inventory adjustments"—corporate speak for the messy reality of combining different businesses with different margin profiles.

The working capital dynamics deserve scrutiny. Debtor days stretching from 54.4 to 86.7 days suggests either competitive pressure forcing extended payment terms or integration challenges in credit management. In a business where projects can span years and involve significant upfront investment, working capital management isn't just a financial metric—it's existential. Every additional day of receivables represents cash that could fund R&D, capacity expansion, or debt reduction.

Yet the cash flow generation remains robust. Operating cash flow of ₹415 crore (consolidated) demonstrates the business's fundamental health. This cash generation, combined with relatively low debt levels, provides flexibility for both organic investment and further acquisitions—critical for a company targeting ₹6,000 crore in revenue by FY29.

The merger is expected to be double-digit EPS accretive from the first year, without accounting for synergies. This immediate accretion is unusual in large mergers, suggesting either conservative pre-merger profitability or genuine operational complementarity. Management projects the combined entity will maintain "market-leading EBITDA margins of 36%" and 30% return on capital employed—metrics that would place Cohance among the elite of global CDMOs.

Comparative analysis with peers reveals interesting disparities. Divi's Laboratories, often considered India's premier CDMO, trades at a P/E of around 50 with similar EBITDA margins but stronger historical growth. Syngene International, backed by Biocon, commands a P/E of 35 despite lower margins. Laurus Labs, despite operational challenges, maintains a P/E of 25. Cohance's premium valuation suggests the market is pricing in either exceptional execution or excessive optimism.

The capital allocation strategy reflects Advent's growth ambitions. The company plans ₹600 crore in modernization and technology upgradation, focusing on next-generation capabilities rather than simple capacity addition. This includes investments in ADC infrastructure, oligonucleotide synthesis capabilities, and continuous flow manufacturing—technologies that command premium pricing and create competitive differentiation.

International revenue composition provides both opportunity and risk. With over 90% of revenues from regulated markets (US, Europe, Japan), Cohance has limited exposure to pricing pressure in emerging markets. However, this concentration also means vulnerability to regulatory changes, currency fluctuations, and geopolitical tensions. The ongoing US Biosecure Act discussions, while potentially beneficial by limiting Chinese competition, also highlight regulatory risk in key markets.

The customer concentration metrics, while not fully disclosed, appear significant. Industry sources suggest the top 10 clients contribute approximately 70% of revenues—typical for CDMOs but creating obvious key account risk. The loss of a major client, while unlikely given switching costs, could materially impact financial performance. Conversely, expansion with existing clients offers a cleaner path to growth than new customer acquisition.

Project pipeline economics illuminate future potential. With 100+ active projects including 13 in Phase III, Cohance has visibility into future revenue streams. Historical probability suggests 50-70% of Phase III projects reach commercialization. If even half of Cohance's Phase III projects succeed, the revenue impact could be substantial—potentially adding ₹200-300 crore annually as these molecules scale to commercial production.

The formulation business remains subscribed, contributing less than 10% of revenues despite significant investment. This underperformance highlights execution risk in Advent's roll-up strategy—not every capability translates into commercial success. The recent focus on backward integration and complex chemistry suggests a strategic pivot toward areas of demonstrated strength.

Analyst perspectives vary widely. Bulls point to the China+1 tailwind, Advent's operational expertise, and the potential for margin expansion through synergies. Bears focus on integration risks, valuation concerns, and the historical underperformance relative to peers. The consensus seems to be that Cohance represents a high-risk, high-reward proposition—appropriate for investors with strong conviction in India's CDMO story and Advent's execution capabilities.

The financial trajectory toward the stated goal of $1 billion revenue (₹8,500 crore) by FY30 requires 30%+ annual growth—ambitious but not impossible given planned acquisitions and market tailwinds. Achieving this while maintaining margins will require exceptional execution, favorable market conditions, and probably a bit of luck.

VIII. The CDMO Landscape & Industry Dynamics

The global pharmaceutical industry's great unbundling began in earnest during the 1990s, but what we're witnessing now is something altogether different—a reformation as profound as the shift from vertically integrated steel mills to today's networked global supply chains. The CDMO sector, valued at $146 billion in 2023 and growing toward $296 billion by 2033, sits at the epicenter of this transformation. Understanding where Cohance fits in this landscape requires appreciating both the macro forces reshaping pharmaceutical manufacturing and the micro-dynamics of competitive advantage in contract services.

The fundamental driver is simple: drug development has become too expensive and too risky for even the largest pharmaceutical companies to handle entirely in-house. The average cost to bring a new drug to market now exceeds $2.6 billion, with success rates hovering around 12% from clinical trials to approval. In this environment, maintaining sprawling internal manufacturing capabilities for molecules that might never reach market represents an inefficient use of capital. Better to outsource to specialists who can spread fixed costs across multiple clients and achieve economies of scale impossible for any single company. But this seemingly straightforward dynamic has created a landscape of bewildering complexity. India currently holds approximately 2.7-4% of the global CDMO market, with projections suggesting this could reach 5-7% by 2029. The Indian CDMO market, valued at between $16-23 billion in 2024 (depending on which analyst you believe), is expected to double by 2029-2030, growing at a CAGR of 13-15%. Yet these aggregate numbers mask enormous variation in capabilities, quality, and strategic positioning among players.

At the apex sit companies like Divi's Laboratories, the undisputed champion of Indian CDMOs. Working with 12 of the top 20 global pharmaceutical companies, Divi's has built a reputation for reliability and scale that commands premium valuations. Their Kakinada facility, spanning 500 acres with Phase I covering 200 acres that commenced operations in January 2025, represents the kind of massive, integrated manufacturing complex that few can replicate.

Syngene International, majority-owned by Biocon, has taken a different path, focusing on integrated discovery and development services rather than pure manufacturing. Their model—offering everything from target identification to clinical supplies—appeals to biotech companies seeking a single partner for their entire development journey. The trade-off is complexity: managing hundreds of scientists across multiple therapeutic areas requires orchestration capabilities that pure manufacturers don't need.

Laurus Labs represents both the promise and peril of aggressive expansion. Once a darling of investors for its antiretroviral expertise, the company has struggled with debt-funded capacity additions that haven't generated expected returns. Their experience offers a cautionary tale: in CDMOs, building capacity without confirmed demand is a recipe for financial distress.

The competitive dynamics are further complicated by the entry of traditional pharmaceutical companies into CDMO services. Cipla, Dr. Reddy's, and Aurobindo—companies built on generic drug manufacturing—are increasingly offering contract services to monetize excess capacity and relationships. These hybrid players blur the lines between customer and competitor, creating complex dynamics where today's client might be tomorrow's rival.

The China factor looms large over every strategic discussion. China's CDMO market, valued at over $30 billion, dwarfs India's. Chinese companies like WuXi AppTec and Asymchem have built capabilities in complex chemistry and biologics that most Indian players can't match. Yet geopolitical tensions are creating unprecedented opportunities. The proposed US Biosecure Act, which would restrict American companies from working with Chinese CDMOs linked to the government or military, could redirect billions in contracts to Indian firms.

According to a BCG report from February 2025, India is poised to secure a 4-5 percent share of the global CDMO market, with services priced around 20 percent lower than Chinese competitors. In 2024, some Indian CDMOs witnessed a 50% year-on-year surge in Requests for Proposals (RFPs) as global pharmaceutical companies sought to diversify supply chains.

The regulatory landscape adds another layer of complexity. India has around 650 USFDA-approved plants, constituting a quarter of all such facilities outside the United States. This regulatory credibility is crucial but maintaining it requires constant vigilance. A single Form 483 observation can spiral into a Warning Letter, potentially shuttering a facility for months. The recent spate of data integrity issues at various Indian pharmaceutical companies has heightened scrutiny, making quality systems as important as manufacturing capabilities.

Technology disruption threatens to reshape competitive advantages. Continuous manufacturing, long discussed but rarely implemented, is finally becoming reality. Companies that master this technology could achieve cost and quality advantages that render batch manufacturing obsolete. Similarly, artificial intelligence in drug discovery and process optimization could level playing fields or create new moats, depending on who adopts it successfully.

The talent equation increasingly determines competitive positioning. India produces thousands of chemistry and pharmacy graduates annually, but the skills required for next-generation manufacturing—process analytical technology, quality by design, biomanufacturing—remain scarce. Companies that invest in training and retention gain advantages that capital alone cannot buy.

Customer dynamics are evolving rapidly. Big Pharma's traditional approach—maintaining a stable of preferred suppliers with long-term relationships—is giving way to more transactional engagement. Simultaneously, biotech companies, once focused solely on innovation, are increasingly sophisticated about manufacturing strategy. This creates opportunities for agile CDMOs but challenges for those dependent on a few large clients.

Within this landscape, Cohance occupies an interesting position. Its collection of acquired capabilities—from traditional API manufacturing to cutting-edge ADC technology—positions it to serve diverse needs. But integration remains incomplete, and the company lacks the track record of established players. The Advent backing provides capital and expertise, but private equity ownership also brings pressure for returns that might conflict with long-term capability building.

The consolidation thesis that underlies Cohance's strategy assumes that scale matters increasingly in CDMOs. This isn't self-evident. While larger companies can spread regulatory costs and invest in new technologies, smaller specialists often provide superior service and flexibility. The optimal size might be neither the boutique nor the giant, but the focused mid-size player with deep capabilities in specific areas.

Looking forward, several trends will shape competitive dynamics. The rise of personalized medicine and small-batch manufacturing favors flexibility over scale. The increasing complexity of molecules—from simple pills to cell therapies—rewards technical depth over breadth. The growing importance of sustainability could advantage companies with modern, efficient facilities over those with legacy infrastructure.

IX. Playbook: Business & Investing Lessons

The Cohance story offers a masterclass in modern corporate strategy, where financial engineering meets operational excellence, and where the lines between building and buying blur into strategic ambiguity. For students of business and investing, the lessons extend far beyond pharmaceutical services into fundamental questions about value creation, competitive advantage, and the role of capital in shaping industries.

Lesson 1: The Roll-Up Paradox

The roll-up strategy—acquiring multiple companies in a fragmented industry to create scale—appears deceptively simple. Buy small companies at 8-10x EBITDA, integrate them into a platform trading at 15-20x, and capture the multiple arbitrage. Advent's approach with Cohance follows this playbook, but with important nuances that separate successful consolidation from expensive failure.

The key insight is that not all roll-ups are created equal. In industries with true economies of scale—where larger size meaningfully reduces unit costs—consolidation can create genuine value. In CDMOs, these economies exist in regulatory compliance (spreading FDA audit costs across more revenue), technology investment (ADC capabilities cost the same whether you run one project or ten), and customer acquisition (global pharma companies prefer fewer, larger suppliers).

But roll-ups fail when they ignore the heterogeneity within industries. Cohance's acquired companies—spanning APIs, agrochemicals, formulations, and specialized technologies—don't naturally fit together. A customer buying oligonucleotides from Sapala might have no interest in agrochemical intermediates from ZCL. The promised "cross-selling synergies" often prove illusory, while integration costs prove all too real.

The lesson for investors: Look beyond the PowerPoint slides promising synergies. Ask whether the acquired capabilities genuinely complement each other or merely coexist. True platform value comes from interconnection, not mere aggregation.

Lesson 2: The Private Equity Transformation Playbook

Advent's involvement illustrates private equity's evolved approach to value creation. Gone are the days of simple leverage and cost-cutting. Modern PE firms like Advent bring operational expertise, industry networks, and strategic vision that can genuinely transform businesses.

The playbook has several components. First, bring in professional management—witness the appointment of executives from GSK, Dr. Reddy's, and J&J to Cohance's leadership. Second, invest in capabilities that individual portfolio companies couldn't afford alone—Cohance's ADC platform required investment beyond what Suven could have justified independently. Third, use the PE firm's reputation and relationships to win new business—Advent's global network opens doors that family-owned Suven couldn't access.

Yet PE ownership also brings constraints. The typical 5-7 year investment horizon creates pressure for rapid growth that might conflict with the patient capability-building that CDMOs require. The debt used to finance acquisitions limits flexibility during downturns. Most critically, the need for an exit—whether through IPO or strategic sale—can drive short-term decision-making that undermines long-term value.

For investors, the lesson is to understand where you are in the PE cycle. Early in the hold period, PE firms invest aggressively and accept lower margins to drive growth. As exit approaches, the focus shifts to margin expansion and multiple optimization. Cohance, still early in Advent's ownership, should be in investment mode—but watch for signs of premature harvest.

Lesson 3: Managing Cultural Integration in M&A

The human side of Cohance's integration challenge is perhaps the most underappreciated. Each acquired company brings its own culture, shaped by founders, customers, and history. Suven's culture, built over 35 years by the Jasti family, emphasized technical excellence and long-term relationships. RA Chem might have a more entrepreneurial, sales-driven culture. Sapala's scientists, working on cutting-edge oligonucleotides, likely have an academic, research-oriented mindset.

Successful integration requires acknowledging and bridging these cultural differences. The temptation is to impose a uniform "Cohance culture" from above, but this risks destroying the very capabilities that made the acquired companies valuable. Better to identify cultural strengths—Suven's quality focus, RA Chem's customer responsiveness, Sapala's innovation—and find ways to preserve them while building connective tissue.

The appointment of outsider CEO Vivek Sharma, rather than a Suven insider, signals recognition of this challenge. An outsider can more credibly build a new, inclusive culture rather than appearing to impose one company's way of doing things on others. But outsiders also lack the deep relationships and institutional knowledge that enable quick decision-making.

Lesson 4: Building vs. Buying Capabilities

Cohance's acquisition-driven growth strategy raises fundamental questions about capability development. Is it better to build capabilities organically, accepting slower growth but ensuring cultural fit and deep expertise? Or to buy capabilities quickly, accepting integration risk but achieving rapid scale?

The answer depends on the nature of the capability. Technical capabilities with long learning curves—like ADC manufacturing—are often better bought than built. The expertise required takes years to develop, and mistakes during the learning process can be fatal in pharmaceuticals. Cohance's acquisition of NJ Bio brought ADC capabilities that would have taken a decade to build organically.

But commercial capabilities—customer relationships, market knowledge, sales excellence—often resist transplantation. Customers who trusted acquired company X might not automatically trust the new parent. Sales approaches that work in APIs might fail in formulations. These capabilities are better built than bought.

The sophisticated approach combines both strategies. Buy technical platforms and specialized assets, but build the commercial and operational capabilities that tie them together. Cohance seems to be following this hybrid approach, though execution remains to be proven.

Lesson 5: The Importance of Regulatory Moats

In pharmaceutical services, regulatory approval is the ultimate moat. Once a CDMO is written into a drug's regulatory filing, changing suppliers requires extensive documentation, new stability studies, and regulatory review. This switching cost creates powerful customer lock-in, but only for companies that maintain spotless regulatory records.

Cohance's 5 USFDA-approved facilities represent valuable assets, but also ongoing obligations. Each facility must be constantly audit-ready, requiring investment in quality systems, training, and documentation that doesn't directly generate revenue but is essential to maintaining the license to operate.

The lesson for investors is to value regulatory assets appropriately. A single Warning Letter can destroy years of value creation, while a spotless inspection history enables premium pricing. Look beyond the number of approved facilities to the quality of regulatory systems and the track record of inspections.

Lesson 6: Long-Term Contracts and Customer Stickiness

The CDMO business model's attractiveness stems partly from long-term contracts and high switching costs. Once a molecule enters clinical trials with material from a specific supplier, changing becomes expensive and risky. This creates multi-year revenue visibility and relatively predictable cash flows.

But this stickiness is double-edged. The same switching costs that retain existing customers also make winning new ones difficult. Established relationships between Big Pharma and their preferred CDMOs can span decades. Breaking into these relationships requires either superior capabilities, significant price concessions, or catching competitors during capacity constraints.

Cohance's challenge is that much of its growth must come from share gain rather than market growth. This requires either exceptional execution to win competitive bids or acquisitions to buy existing relationships. The former is difficult and slow; the latter is expensive and risky.

Lesson 7: Capital Allocation in Asset-Heavy Businesses

Unlike software or services businesses, CDMOs require substantial capital investment. A single reactor might cost millions; a new facility can require hundreds of millions. This capital intensity creates both barriers to entry and risks of overcapacity.

The key to successful capital allocation in CDMOs is matching capacity additions to confirmed demand. Building on speculation, hoping that "if you build it, they will come," has destroyed value at numerous pharmaceutical services companies. Conversely, having insufficient capacity when customers need it can damage relationships permanently.

Cohance's planned ₹600 crore investment in modernization and technology must thread this needle. The focus on next-generation capabilities rather than simple capacity addition suggests strategic thinking, but execution will determine whether this creates or destroys value.

The sophisticated approach involves staged investment, where initial small-scale capabilities can be expanded once demand materializes. This requires flexible facility design and modular equipment that might cost more initially but provides valuable optionality.

X. Analysis & Bear vs. Bull Case

The investment case for Cohance Lifesciences crystallizes around a fundamental tension: Is this a platform poised to capture disproportionate value from the global pharmaceutical industry's structural transformation, or an over-engineered roll-up trading at valuations that assume flawless execution in an increasingly competitive market? The answer, as with most complex investment questions, depends on your time horizon, risk tolerance, and beliefs about industry evolution.

The Bull Case: A Generational Transformation Story

Bulls see Cohance as perfectly positioned at the intersection of multiple powerful trends. The China+1 dynamic isn't just rhetoric—it's manifesting in real RFPs and contract wins. India's share of the global CDMO market doubling from 3% to 6% over five years would create $15-20 billion in incremental opportunity. If Cohance captures even 10% of this growth, revenues would triple.

The technological capabilities argument is compelling. ADCs represent one of oncology's most promising frontiers, with the market expected to reach $34 billion by 2032. Only a handful of CDMOs globally can handle ADC manufacturing's complexity. Cohance's early positioning, enhanced by the NJ Bio acquisition, could prove prescient. Similarly, oligonucleotide capabilities position the company for the genomic medicine revolution. These aren't commodity services where price is paramount—they're specialized capabilities where expertise commands premium pricing.

The Advent orchestration adds credibility. This isn't a family-run business struggling with succession or a public company constrained by quarterly earnings pressures. Advent has the capital to invest, the patience to integrate, and the relationships to open doors. Their track record—having invested over $3.2 billion in 14 Indian companies—suggests they understand the market's nuances.

The financial trajectory, while requiring aggressive assumptions, isn't impossible. Growing from ₹1,200 crore to ₹6,000 crore in five years implies 38% annual growth. With organic growth of 15-20% (achievable given market tailwinds) and 2-3 acquisitions annually, the math works. The margin story is equally compelling: as higher-margin services like ADCs and oligonucleotides become larger revenue contributors, consolidated margins could expand from 31% to the targeted 36%.

The valuation, while optically expensive at 136x P/E, makes more sense viewed through a growth lens. If the company achieves its targets, forward earnings could triple by 2029. At that point, today's purchase price would represent perhaps 45x forward earnings—still premium but not absurd for a market leader in a growing industry.

Most importantly, bulls argue that Cohance is building something genuinely differentiated. The integrated platform—spanning discovery support, clinical manufacturing, commercial production, and specialized technologies—creates customer value that pure-play competitors can't match. A biotech developing an ADC could work with Cohance from preclinical studies through commercial launch, avoiding the complexity of managing multiple suppliers.

The Bear Case: Financial Engineering Masking Operational Challenges

Bears see a different story—one of financial engineering masquerading as operational excellence. The poor historical growth of 7.51% over five years suggests execution challenges that won't disappear simply because Advent arrived. The recent margin compression, with Q4 FY25 net profit declining 21% despite 59% revenue growth, hints at integration difficulties that could worsen as more acquisitions are added.

The valuation is bears' strongest argument. At 14x book value and 136x earnings, Cohance trades at multiples that would make even high-flying technology companies blush. This is a manufacturing business with substantial capital requirements, regulatory risks, and customer concentration. The valuation implies perfection in execution that rarely occurs in complex integrations.

The integration challenge appears daunting. Combining companies with different systems, cultures, and capabilities while maintaining operational excellence is extraordinarily difficult. Each acquisition brings integration costs, customer disruption risks, and management distraction. The track record of successful multi-company integrations in pharmaceuticals is littered with failures.

Customer concentration presents another risk. With top clients likely contributing 70% of revenues, losing even one major customer could devastate financial performance. The long-term nature of CDMO relationships cuts both ways—while it provides stability, it also means that winning new large customers is difficult and slow.

The competitive landscape is intensifying. Every major Indian pharmaceutical company is entering CDMO services. Global players like Lonza, Catalent, and Thermo Fisher have resources that dwarf Cohance. Chinese companies, despite geopolitical headwinds, aren't disappearing. New technologies might obviate current capabilities. In this environment, maintaining market share—let alone gaining it—requires exceptional execution.

The private equity ownership structure creates its own risks. The typical PE playbook involves financial leverage that limits flexibility during downturns. The pressure for exits could drive suboptimal strategic decisions. Management turnover, common in PE-owned companies, could disrupt operations. The focus on financial metrics might undermine the patient capability-building that CDMOs require.

Bears also question the synergy assumptions. Cross-selling between different business units sounds logical but proves difficult in practice. A customer buying APIs might have no need for agrochemical intermediates. The cost savings from shared infrastructure might be offset by complexity costs. The promised revenue synergies might never materialize.

The Balanced Perspective

The truth likely lies between these extremes. Cohance has assembled impressive capabilities and is well-positioned for industry tailwinds. But execution challenges are real, and the valuation leaves little room for error.

The key variables to monitor include:

- Integration progress: Are the acquired companies being successfully integrated, or are they operating as independent silos?

- Customer wins: Is Cohance winning new strategic customers, or merely maintaining inherited relationships?

- Margin trajectory: Are margins expanding as promised, or is competition compressing profitability?

- Regulatory track record: Any FDA observations or warning letters would signal operational issues

- Management stability: Turnover in key positions would suggest integration challenges

- Capital allocation: Are acquisitions creating value or merely adding revenues?

For investors, Cohance represents a high-conviction bet on India's CDMO sector and Advent's execution capabilities. Those believing in the structural story and management's ability to execute might find the current valuation acceptable, viewing near-term volatility as opportunities to build positions. Skeptics might prefer established players like Divi's or emerging specialists with cleaner stories.

XI. Epilogue & Future Outlook

Standing at the sprawling Pashamylaram facility outside Hyderabad, watching technicians in cleanroom suits navigate between bioreactors and chromatography columns, one can't help but feel the weight of transformation. What began as Venkateswarlu Jasti's vision of bringing world-class pharmaceutical manufacturing to India has evolved into something far more complex—a platform attempting to consolidate an entire industry while navigating technological disruption, geopolitical realignment, and the relentless pressure of private equity ownership.

The name "Cohance" itself—representing Collaboration, Convergence, and Enhancement—captures both the ambition and the challenge. Creating coherence from chaos, unity from diversity, enhancement from aggregation. These aren't merely corporate buzzwords but fundamental challenges that will determine whether this experiment in industry consolidation succeeds or joins the graveyard of roll-ups that promised synergies but delivered disappointment.

The immediate future holds several critical milestones. The integration of acquired companies must progress from PowerPoint promises to operational reality. The ADC and oligonucleotide platforms need to win meaningful contracts that validate the investment. The organizational culture must evolve from a collection of former competitors to a unified team. Most critically, the financial performance must justify valuations that assume exceptional execution.

Looking ahead to 2030, several scenarios seem plausible. In the optimistic case, Cohance emerges as India's champion CDMO, a $1 billion revenue platform that serves as the preferred partner for global pharmaceutical innovation. The integrated capabilities create genuine competitive advantages. The India story plays out as predicted, with the country capturing 6-7% of the global CDMO market. Advent exits triumphantly, either through a strategic sale to Big Pharma seeking manufacturing capabilities or through a re-IPO at premium valuations.

The pessimistic scenario sees integration challenges overwhelming management attention. Key customers defect during the disruption. Margins compress as competition intensifies. The debt burden limits strategic flexibility. Advent, facing fund pressure, forces a premature exit at disappointing returns. The platform fragments back into components, sold piecemeal to strategic buyers.

The most likely outcome lies between these extremes. Cohance will probably achieve meaningful scale, perhaps reaching ₹4,000-5,000 crore in revenues by 2030. Some acquisitions will integrate successfully; others will disappoint. The company will win some strategic customers while losing others. Margins will remain healthy but not exceptional. Advent will achieve acceptable but not spectacular returns. The platform will survive but might not thrive at the level ambitions suggest.

Several wild cards could dramatically alter this trajectory. A breakthrough in continuous manufacturing could obsolete batch production facilities. A major quality incident could trigger regulatory action that cripples operations. Geopolitical tensions could either accelerate the shift from China (benefiting Cohance) or disrupt global supply chains (harming everyone). New therapeutic modalities—cell therapy, gene editing, RNA medicines—could require capabilities that current CDMOs lack.

The broader implications extend beyond Cohance itself. This experiment in consolidation is being watched closely by competitors, customers, and investors. Success would likely trigger copycat strategies, accelerating industry consolidation. Failure might preserve the current fragmented landscape, where hundreds of small players compete on price while a few giants dominate strategic relationships.

For India's pharmaceutical ambitions, Cohance represents both opportunity and risk. Success would demonstrate that Indian companies can compete globally not just on cost but on capability, innovation, and scale. It would attract more investment, talent, and customers to India's CDMO sector. Failure would reinforce stereotypes about execution challenges, integration difficulties, and the limits of financial engineering.

The human dimension shouldn't be forgotten. Thousands of employees—scientists, engineers, operators, managers—are navigating this transformation. Their careers, communities, and contributions to global health depend on decisions made in boardrooms they'll never enter. The molecules they manufacture might cure cancers, treat rare diseases, or prevent pandemics. This work matters beyond financial returns.

As we close this analysis, several questions linger. Can financial engineering create operational excellence, or must it emerge organically? Is consolidation inevitable in CDMOs, or will specialization triumph over scale? Can India truly challenge China's manufacturing dominance, or will it remain a capable but secondary player? Will Cohance's bold ambitions be vindicated by results, or will they serve as a cautionary tale about the limits of ambition?

Time will provide answers, but the journey itself offers lessons. About the complexity of modern industrial organization. About the role of capital in shaping competitive landscapes. About the challenges of building platforms in industries where expertise matters more than algorithms. About the delicate balance between financial returns and operational excellence.

Cohance Lifesciences stands at an inflection point—no longer the simple family business that Suven once was, not yet the global platform it aspires to become. The transformation ahead will test every assumption, challenge every capability, and reveal whether the whole can truly become greater than the sum of its parts. For investors, customers, competitors, and observers, the story unfolding in Hyderabad's laboratories and boardrooms offers a window into the future of global pharmaceutical manufacturing.

The verdict on Cohance won't be rendered in quarters or even years, but in decades. Whether it becomes a case study in successful consolidation or a reminder of complexity's triumph over ambition remains to be written. What's certain is that the attempt itself—bold, complex, fraught with risk and possibility—represents something essential about modern capitalism's endless pursuit of scale, efficiency, and value creation.

As the Indian pharmaceutical industry continues its evolution from generic manufacturer to innovation partner, from cost leader to capability provider, Cohance embodies both the promise and the peril of transformation. Its success or failure won't determine India's pharmaceutical future, but it will certainly influence it. And in that influence lies the real stakes—not just financial returns, but the shape of an industry that touches billions of lives.

The story continues, unfolding in real-time across continents and cultures, in laboratories and boardrooms, in the molecules being synthesized and the strategies being executed. Cohance Lifesciences—part family legacy, part private equity play, part industrial consolidation, wholly representative of modern pharmaceutical manufacturing's complex reality—remains a work in progress. Whether that work produces a masterpiece or a cautionary tale remains the most important unanswered question.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube