Coforge: From NIIT's Software Arm to Global IT Services Powerhouse

I. Introduction & Episode Roadmap

Picture this: It's 2019, and a mid-tier Indian IT services company with a market cap of around ₹8,000 crore is about to undergo one of the most dramatic transformations in the industry. Private equity giant Baring swoops in, takes control, rebrands the entire company, orchestrates multiple acquisitions, and then exits completely—all within four years. The result? A company now worth ₹54,000 crore, with revenue touching $1.5 billion and ambitions to hit $2 billion by FY27.

This is the Coforge story—a narrative that begins not in a garage or dorm room, but in the classrooms of NIIT, India's pioneering computer education company. Today, Coforge stands as one of India's top-20 software exporters, serving clients like British Airways, ING Group, and Sabre with deep domain expertise in travel, banking, and insurance. But how did a training company's software division evolve into a global IT powerhouse?

The journey spans four decades of Indian IT history—from the pre-liberalization era when computers were curiosities, through the Y2K boom, the global financial crisis, multiple ownership changes, and now the AI revolution. It's a story of strategic pivots, calculated risks, and the power of specialization in an industry often obsessed with scale.

What makes Coforge particularly fascinating is its contrarian strategy. While TCS, Infosys, and Wipro built horizontal empires serving every industry under the sun, Coforge went deep rather than wide. They chose to master a few verticals completely rather than dabble in many. And while the giants grew organically, Coforge has used M&A as a strategic weapon, successfully integrating companies like SLK Global and Cigniti to accelerate growth.

Over the next few hours, we'll unpack this remarkable transformation. We'll explore how NIIT's franchising model revolutionized IT education in India, why the software services arm was spun off, how Baring Private Equity orchestrated a complete metamorphosis, and what the recent Cigniti acquisition means for the company's future. We'll also examine the financials—32% constant currency growth in FY25 is exceptional by any standard—and debate whether this momentum is sustainable.

For investors, the Coforge story offers lessons in value creation through focused execution, the role of private equity in transforming mid-market companies, and the ongoing consolidation in India's IT services sector. For operators, it's a masterclass in building domain expertise, managing ownership transitions, and using M&A to leapfrog competition.

Let's begin where all great business stories should—at the very beginning, in 1981, when two IIT Delhi graduates decided to solve India's computer education crisis.

II. The NIIT Origins & Educational Empire (1981–1992)

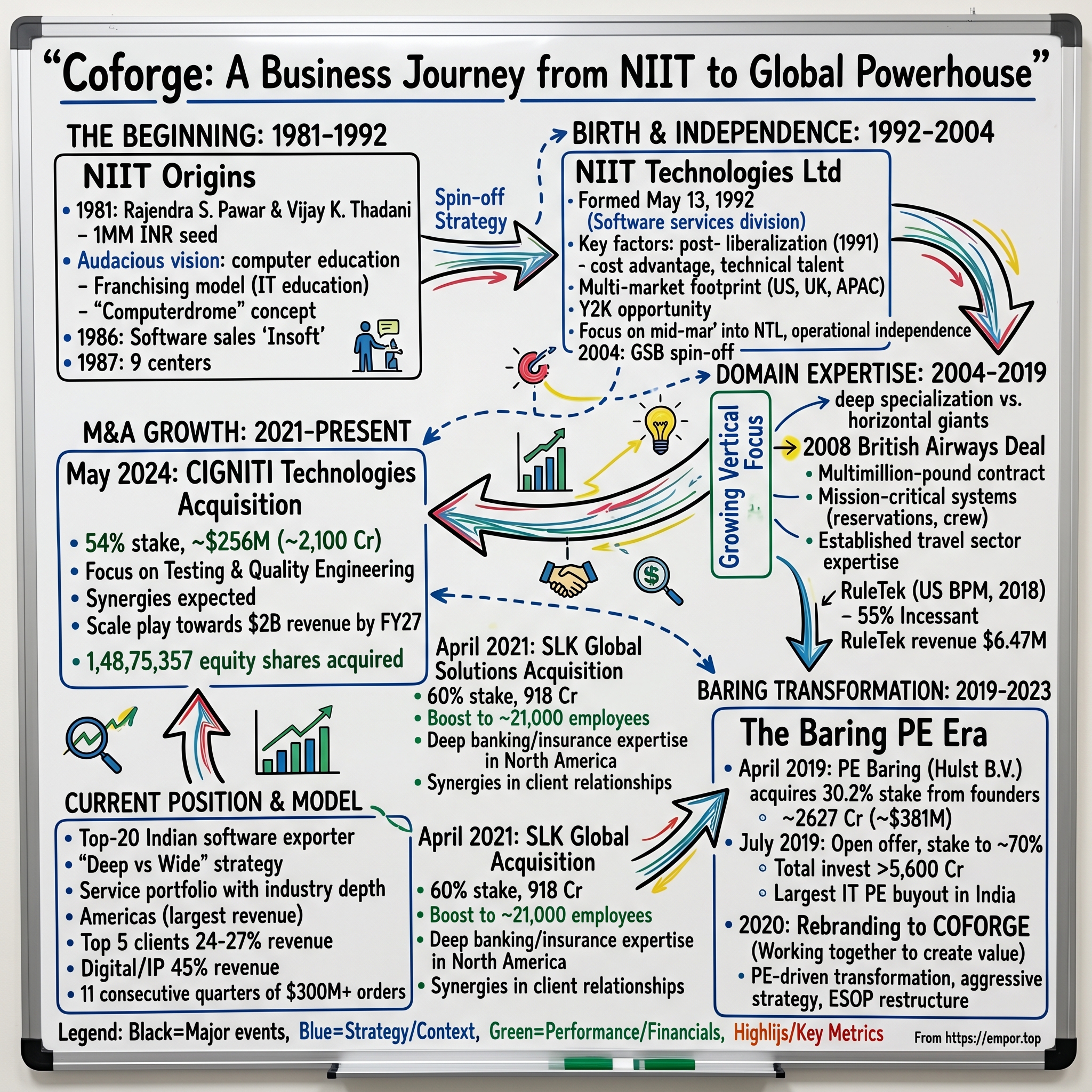

The year was 1981. Personal computers were still exotic machines in India, imported under strict license raj regulations. Most Indians had never seen a computer, let alone used one. Into this technology desert stepped two IIT Delhi alumni—Rajendra S. Pawar and Vijay K. Thadani—with one million rupees and an audacious vision: democratize computer education across India. Rajendra Singh Pawar, who would later receive the Padma Bhushan in 2011, wasn't your typical tech entrepreneur. Born in Jammu in 1951 and educated at the prestigious Scindia School in Gwalior before graduating from IIT Delhi in 1972, Pawar possessed a unique combination of technical expertise and educational vision. His partner, Vijay K. Thadani, brought complementary skills from his IIM Calcutta education and shared the belief that India's future depended on democratizing technology education. What they created was revolutionary. NIIT conceived a franchising model in IT education for the very first time, setting up nine centers by 1987. This wasn't just business expansion—it was a social movement. The franchising model allowed educated but unemployed youth to become entrepreneurs, spreading computer literacy across India's vast geography. The company earned the epithet, the 'McDonald's of the software business' by Far Eastern Economic Review in September, 2001.But 1986 marked a critical turning point. NIIT began selling software under its Insoft brand, expanding beyond education into software development and distribution. This wasn't just diversification—it was strategic positioning. While training students in IT skills, NIIT was simultaneously building its own software capabilities, creating a virtuous cycle where education fed into services and vice versa.

The context of 1980s India cannot be overstated. The country had just 150 computers in 1970. By 1980, this had grown to only 1,000. Personal computers were luxury items, imported under restrictive licenses. Most Indians viewed computers with a mixture of awe and suspicion. Into this environment, NIIT didn't just sell education—they sold a vision of India's digital future.

The franchising model was particularly ingenious. By allowing educated but unemployed youth to become NIIT franchisees, Pawar and Thadani created thousands of entrepreneurs overnight. Each franchise owner had skin in the game, ensuring quality and commitment. The model scaled rapidly because it aligned incentives perfectly—franchisees succeeded when students succeeded, and NIIT provided the curriculum, brand, and support systems.

What distinguished NIIT from government-run computer education initiatives was its market-driven approach. They constantly updated curricula based on industry needs, partnered with global technology companies, and focused on practical skills over theoretical knowledge. By 1990, they had created the "Computerdrome"—providing unlimited computer time to students, a revolutionary concept when computer access was measured in precious minutes.

The numbers tell the story of explosive growth. From one million rupees in capital and two founders in 1981, NIIT had expanded to multiple cities across India by the late 1980s. They weren't just riding the IT wave—they were creating it, training the very workforce that would power India's software revolution in the coming decades. The stage was set for the next chapter: spinning off their software services capabilities into what would eventually become Coforge.

III. Birth of NIIT Technologies: The Spin-off Story (1992–2004)

The year 1992 marked a watershed moment in NIIT's evolution. Rajendra Singh Pawar founded Coforge Ltd. in 1992, though it was then incorporated as NIIT Technologies Ltd., the dedicated software services division of the parent company. This wasn't merely an organizational restructuring—it was a strategic recognition that software services required a fundamentally different DNA from education services. The company was incorporated in 1992 as NIIT Technologies Ltd, the software services division of NIIT, formally registered on May 13, 1992, at the Registrar of Companies in Delhi. The timing was perfect—India had just begun its economic liberalization in 1991, opening up vast opportunities for software exports. Global companies were beginning to discover India's cost advantage and technical talent, but the market was still nascent enough for new entrants to carve out niches.

The early years of NIIT Technologies were about building credibility and capabilities. Unlike the parent company's education business, which served millions of students, the software services arm needed to compete for enterprise clients against established players. The strategy was clear: leverage NIIT's training expertise to ensure a steady pipeline of skilled developers while focusing on specific industry verticals where domain knowledge mattered as much as technical skills.

By the mid-1990s, NIIT Technologies had begun establishing its footprint in international markets. The company set up subsidiaries and offices in key markets—the United States, United Kingdom, and Asia-Pacific—not just as sales outposts but as delivery centers that could work closely with clients. This proximity to customers would become a key differentiator, allowing NIIT Technologies to understand business processes deeply rather than just execute coding projects.

The late 1990s brought the Y2K opportunity—a massive windfall for Indian IT companies. While larger players like Infosys and Wipro grabbed headlines with billion-dollar contracts, NIIT Technologies focused on building long-term relationships with mid-market clients. They weren't chasing the biggest deals but rather the stickiest ones—engagements where they could embed themselves deeply into client operations.

In 2004, a pivotal moment arrived: the Global Solutions Business was spun off into NIIT Technologies, marking its complete operational independence from the parent company. This wasn't just a corporate restructuring—it was a declaration of intent. NIIT Technologies would no longer be seen as merely the software arm of an education company but as a serious IT services player in its own right.

The spin-off came with both opportunities and challenges. On one hand, NIIT Technologies could now chart its own course, make independent strategic decisions, and attract investors specifically interested in IT services rather than education. On the other hand, it needed to establish its own identity in a crowded market dominated by much larger players.

What NIIT Technologies brought to the table was a unique combination: the discipline and process orientation inherited from its education heritage, deep domain knowledge in select verticals, and a culture of continuous learning. While competitors were building massive horizontal capabilities, NIIT Technologies was going deep into travel, insurance, and banking—industries where understanding the business was as important as understanding technology.

By 2004, the company had laid the foundation for what would become its core competitive advantage: the ability to combine technology expertise with deep domain knowledge. They weren't trying to be everything to everyone. Instead, they were positioning themselves as specialists who could solve complex, industry-specific problems. This focus would prove prescient as the IT services industry evolved from pure labor arbitrage to value-based partnerships.

IV. The Growth Years: Building Domain Expertise (2004–2019)

The period from 2004 to 2019 would define NIIT Technologies' identity as a domain specialist. While the Indian IT giants were expanding horizontally across every conceivable industry, NIIT Technologies made a contrarian bet: go deep, not wide.

In 2006, the company acquired UK Insurance Solutions Company and partnered with Adecco SA, marking its first major international acquisition. This wasn't just about adding revenue or headcount—it was about acquiring domain expertise that would take years to build organically. The UK Insurance Solutions Company brought deep knowledge of European insurance markets, regulatory frameworks, and established client relationships.

But the defining moment came in 2008 when the company signed a multi-million-pound deal with British Airways. This wasn't just another IT services contract—it was a transformational engagement that would shape NIIT Technologies' trajectory for the next decade. British Airways didn't just need a vendor; they needed a partner who understood the complexities of airline operations, from reservation systems to crew management, from revenue optimization to customer service.

The British Airways engagement became NIIT Technologies' calling card in the travel and transportation sector. It demonstrated their ability to handle mission-critical systems for one of the world's most demanding clients. The success with BA opened doors to other airlines and travel companies—suddenly, NIIT Technologies wasn't just another Indian IT vendor but a specialized travel technology partner.

In 2012, the company's capabilities caught the attention of the Indian government. They implemented the "Intranet Prahari" project for the Border Security Force and won a contract from the Indian Tobacco Board for implementing an e-auction system in Karnataka and Andhra Pradesh. These projects showcased NIIT Technologies' ability to execute complex, large-scale government projects—a capability that would become increasingly important as India digitized its governance infrastructure.

The company's growth strategy during this period was methodical. Rather than chasing every RFP that came their way, they focused on building Centers of Excellence in specific domains. The travel CoE, for instance, wasn't just a group of developers who worked on airline projects—it was a team that understood global distribution systems, airline revenue management, loyalty programs, and the intricate regulations governing international aviation.

Similarly, in banking and financial services, NIIT Technologies didn't try to compete with the likes of TCS or Infosys for core banking transformations. Instead, they focused on specific areas like wealth management, capital markets, and insurance. They built expertise in platforms like SEI Wealth Platform and became implementation partners for specialized financial software vendors. In 2018, a significant strategic move unfolded when the Company acquired controlling interest in RuleTek, a US-based BPM architecture services company. After the acquisition, Coforge's digital arm Incessant Technologies controls 55% of Ruletek. Headquartered in Meridian, Idaho, RuleTek is a fast-growing business serving customers in the US, with about 65 employees. The company reported revenues of $6.47 million for FY2017.

This acquisition wasn't about scale—RuleTek was tiny compared to NIIT Technologies' overall revenue. It was about capability. RuleTek brought deep expertise in business process management (BPM) architecture, particularly in implementing Pega and Appian platforms for Fortune 500 companies. More importantly, it gave NIIT Technologies near-shore capabilities in the United States, allowing them to offer a more complete delivery model to American clients.

The period from 2004 to 2019 saw NIIT Technologies perfect what would become its signature approach: the "deep and narrow" strategy. While TCS was becoming a $20 billion behemoth serving every industry imaginable, NIIT Technologies was content being a $1 billion specialist that knew travel, insurance, and banking inside out.

This focus paid dividends in client relationships. Companies like British Airways, Sabre, and SEI Investments didn't just use NIIT Technologies as a vendor—they relied on them as strategic partners who understood their business as well as they did. The company's Net Promoter Scores consistently ranked among the highest in the industry, a testament to the value of specialization.

By 2019, NIIT Technologies had revenues approaching $600 million and employed over 10,000 people globally. They weren't the biggest, but in their chosen domains, they were often the best. The company had built what Warren Buffett would call a "moat"—deep domain expertise that would take competitors years to replicate.

But the Indian IT services industry was evolving. Digital transformation was no longer a buzzword but an existential imperative for clients. Scale was becoming increasingly important to invest in new technologies and capabilities. NIIT Technologies needed to make a choice: remain a profitable niche player or find a way to achieve scale without sacrificing specialization. The answer would come from an unexpected source—private equity.

V. The Baring Private Equity Era & Transformation (2019–2023)

April 2019 marked the beginning of one of the most dramatic transformations in Indian IT services history. In 2019, NIIT and its founder's family sold their 30.2% stake to Hulst B.V., which subsequently acquired an additional ~40% through an open offer, reaching a 70% stake. Baring Private Equity Asia, through its entity Hulst B.V., didn't just buy into NIIT Technologies—they engineered a complete metamorphosis. The initial transaction was meticulously structured. BPEA signed definitive agreements to purchase approximately 18.85 million NIIT Technologies Limited shares (approximately 30% shareholding on a fully diluted basis in NIIT Technologies) from NIIT Limited and other promoter entities at a price of INR 1394 per share. The aggregate consideration for purchase of shares from promoter entities is estimated to be approximately INR 2627 crores (US$ 381 million).

But Baring wasn't content with a minority stake. In July 2019, Baring increased its shareholding by 35% via an open offer to public shareholders for ₹3,045 crore. This brought their total ownership to approximately 70%, giving them complete control of the company. The total investment exceeded ₹5,600 crore, making it one of the largest private equity buyouts in the Indian IT services sector.

What followed was a masterclass in PE-driven transformation. The first major move came in 2020 with a complete rebrand. In 2020, NIIT Technologies was re-branded as Coforge. This wasn't just cosmetic—it was a declaration of independence from the NIIT legacy and a signal that this was now a different company with bigger ambitions. The word 'Coforge' stands for working together to create lasting value. The name reflects the deep employee and client centricity ingrained within our firm's culture," explained CEO Sudhir Singh. This wasn't just marketing speak—it signaled a fundamental shift in how the company saw itself. No longer tied to the NIIT education legacy, Coforge could chart its own course.

But the real transformation came through aggressive M&A. In April 2021, Coforge acquired 60% stake in SLK Global Solutions for ₹918 crore. After this acquisition, the company's employee count rose to 21,000 having inherited SLK's employee strength of 10,000. This was transformational—nearly doubling the company's size overnight and adding significant capabilities in automation and digital services.SLK Global brought deep domain expertise in the banking and insurance businesses in North America. The firm has deep domain expertise in the banking and insurance businesses in North America. SLK Global reported consolidated revenue of 62 million dollars (about Rs 455 crore) during FY20 and is expected to report consolidated revenue of 73 million dollars (about Rs 536 crore) during FY21, representing a growth of about 15 per cent.

The integration of SLK was executed with surgical precision. Rather than forcing cultural assimilation, Coforge allowed SLK to maintain its identity while leveraging synergies in client relationships and delivery capabilities. The result was immediate—the acquisition was EBITDA margin accretive from day one.

Under Baring's ownership, Coforge underwent a cultural transformation as well. The company became more aggressive in pursuing large deals, more willing to invest in capabilities, and more focused on metrics that mattered to private equity—revenue growth, margin expansion, and cash generation. The employee stock ownership plans were restructured to align with PE-style value creation, creating significant wealth for senior management.

The financial performance during the Baring era was exceptional. Revenue grew from approximately $600 million when Baring entered to over $1 billion by 2023. More importantly, the company's positioning changed—it was no longer seen as just another mid-tier Indian IT company but as a specialist with unique capabilities in select verticals.

By August 2023, Baring Private Equity Asia divested its entire 70% stake in Coforge, selling it across multiple tranches beginning in October 2020. The exit was spectacularly successful—Baring made returns of over 3x on their investment in just four years, one of the best outcomes for a PE investment in the Indian IT services sector.

The Baring era demonstrated what focused PE ownership could achieve. They didn't try to make Coforge compete with TCS or Infosys on scale. Instead, they doubled down on what made Coforge unique—deep domain expertise, selective M&A, and a culture of specialization. The transformation from NIIT Technologies to Coforge wasn't just a name change—it was a complete reimagination of what a mid-tier IT services company could be.

VI. The Cigniti Acquisition & Scale Play (2024–Present)

The post-Baring era presented Coforge with a critical question: How do you sustain PE-style growth without PE ownership? The answer came in May 2024 with the announcement of a transformational deal: Coforge announced that it would acquire a 54% stake in Cigniti Technologies. The Cigniti acquisition represents Coforge's most ambitious move yet. Financial Terms: Coforge plans to utilise cash for the acquisition, with a per-share purchase price of ₹1,415. The total deal value approaches $256 million (approximately ₹2,100 crore) for the 54% stake. This isn't just about adding revenue—it's about transformation at scale. Founded in 1998 and headquartered in Telangana, India, Cigniti Technologies Limited is a publicly traded company listed on the Bombay Stock Exchange (BSE) and the National Stock Exchange. Cigniti Technologies Ltd is engaged in providing quality engineering & software testing services to clients across various industries. It was incorporated in 1998 in Hyderabad, Telangana.

What makes Cigniti particularly attractive to Coforge is its pure-play focus on testing and quality engineering. The company provides software testing and analysis services in the areas of Quality Assurance, Next Generation Testing, Digital Assurance, Quality Engineering, Advisory & Transformation, IP & Innovation, etc. With revenue approaching ₹2,080 crore and a client base that includes Fortune 500 companies, Cigniti brings immediate scale and specialized capabilities.

The strategic rationale for the acquisition is compelling. The acquisition of Cigniti will not only help Coforge grow into a $2 billion firm by FY27 but the ensuing synergies will help the latter improve its operating margins by 150 – 250 bps in this timeframe. More importantly, the acquisition will create three new scaled up verticals – retail, technology and healthcare.

This is classic Coforge strategy—using M&A not just for scale but for capability building. Cigniti's expertise in retail, technology, and healthcare complements Coforge's existing strengths in travel, BFSI, and insurance. The combined entity will have the scale to compete for larger deals while maintaining the specialization that has been Coforge's hallmark.

The integration appears to be progressing smoothly. the Company has completed the final tranche closing on December 20, 2024, through an off-market transaction pursuant to which the Company has purchased additional 59,54,626 equity shares amounting to 21.62% of the expanded voting share capital of Cigniti. Accordingly, the Company has acquired an aggregate of 1,48,75,357 equity shares amounting to 54% of the expanded voting share capital of Cigniti.

The Cigniti acquisition demonstrates that Coforge's M&A playbook, refined during the Baring era, remains intact. They're not trying to be a generalist IT services company. Instead, they're building depth in select verticals through targeted acquisitions that bring both scale and capability. With Cigniti, Coforge is well on its way to achieving its $2 billion revenue target by FY27—a remarkable achievement for a company that was generating less than $600 million just five years ago.

VII. Business Model & Competitive Positioning

Understanding Coforge's business model requires appreciating what makes it different from both the Indian IT giants and other mid-tier players. The company has carved out a unique position: large enough to handle complex, enterprise-wide engagements but specialized enough to offer deep domain expertise that generalists can't match.

Coforge is an IT services company providing end-to-end software solutions and services. It is among the top-20 Indian software exporters. Prominent global customers include British Airways, the ING group, SEI Investments, Sabre, and SITA. But these aren't just logos on a slide—they represent decades-long relationships where Coforge has become embedded in mission-critical operations.

The service portfolio spans the entire technology stack but with a twist. While competitors offer similar services—application development, infrastructure management, cloud, digital—Coforge delivers these through the lens of deep industry knowledge. A Coforge engineer working on an airline reservation system doesn't just understand code; they understand revenue management, global distribution systems, and IATA regulations.

Geographic diversification provides stability. Americas contributes the largest share of revenue, but the company maintains a significant presence in EMEA and APAC. This isn't just about following the sun for 24/7 delivery—it's about being close to clients, understanding local regulations, and building relationships that transcend vendor-client dynamics.

The "deep vs. wide" strategy is perhaps best illustrated through client metrics. While TCS might have 1,000+ clients, Coforge focuses on fewer but deeper relationships. Their top 5 clients contribute approximately 24-27% of revenue—a concentration that would worry some but reflects the stickiness of these relationships. When you're managing British Airways' crew scheduling or SEI's wealth management platform, switching costs are enormous.

The competitive landscape is nuanced. Coforge doesn't compete with TCS or Infosys for large, horizontal deals. Instead, they compete with specialized players in each vertical—companies like Hexaware in travel, Synechron in banking, or CitiusTech in healthcare. But unlike these single-vertical specialists, Coforge has the scale to invest in next-generation capabilities while maintaining focus.

Digital and IP-led services now contribute approximately 45% of revenue—a remarkable transformation from a company that was primarily about labor arbitrage a decade ago. Products like BlueSwan (Cigniti's testing platform) and proprietary solutions for specific industries create differentiation beyond just domain knowledge.

The delivery model has evolved significantly. While offshore delivery from India remains the backbone, near-shore centers in Eastern Europe and Latin America provide flexibility. The SLK acquisition brought significant onshore capabilities in the United States, allowing Coforge to offer the full spectrum of delivery models that large enterprises demand.

Partnerships amplify capabilities. Rather than trying to build everything in-house, Coforge partners with platform leaders—Pega for BPM, Salesforce for CRM, cloud providers for infrastructure. These aren't just implementation partnerships but deep collaborations where Coforge often co-develops industry-specific solutions.

What's particularly impressive is the company's ability to maintain culture through multiple ownership changes and acquisitions. The entrepreneurial spirit from the NIIT days, combined with PE-style execution discipline and a focus on specialization, creates a unique organizational DNA. Employees don't see themselves as generic IT workers but as domain experts who happen to use technology.

The business model is resilient by design. Long-term contracts provide revenue visibility. The focus on mission-critical systems creates switching costs. Deep domain expertise creates barriers to entry. And the combination of organic growth and strategic M&A provides multiple levers for expansion. This isn't the highest-margin business in IT services, but it's remarkably sticky and predictable—exactly what long-term investors value.

VIII. Financial Performance & Growth Story

The numbers tell a story of exceptional execution. Mkt Cap: 54,343 Crore (up 39.0% in 1 year) represents not just market appreciation but fundamental business transformation. From TTM revenue of $1.42 billion in 2024 to the current run rate approaching $1.5 billion, Coforge has delivered growth that would make even high-flying SaaS companies envious.

The FY25 performance deserves special attention. Delivering 32.0% constant currency growth in an environment where even industry leaders like TCS and Infosys are struggling to maintain double digits isn't just good—it's exceptional. This isn't financial engineering or one-time gains. It's broad-based growth across geographies, verticals, and service lines.

Margin expansion tells another story. Q4FY24 EBITDA improved 102 basis points quarter-on-quarter, demonstrating operational leverage kicking in. This is the beauty of the IT services model when executed well—incremental revenue drops almost directly to the bottom line once you've covered your fixed costs. The Cigniti acquisition promises another 150-200 basis points of margin improvement, taking Coforge into the territory of much larger players.

The order book provides visibility into future growth. With $1.02 billion in executable orders, up 17.3% year-on-year, the company has clear runway for continued expansion. More impressively, they've delivered 11 consecutive quarters of $300M+ order intake—a consistency that's rare in the feast-or-famine world of IT services.

Deal sizes are increasing. While Coforge doesn't win the $1 billion mega-deals that make headlines, they're increasingly winning $50-100 million engagements that provide multi-year revenue visibility. These aren't staff augmentation deals but transformational engagements where Coforge takes ownership of entire business processes or technology stacks.

Cash flow generation is robust. Unlike product companies that require constant R&D investment or asset-heavy businesses that consume capital, IT services is fundamentally a people business. Once you've invested in training and infrastructure, incremental growth requires minimal capital. This allows Coforge to fund acquisitions from cash flow while maintaining a strong balance sheet.

The capital allocation strategy reflects maturity. Rather than hoarding cash or paying excessive dividends, Coforge uses capital for strategic acquisitions that accelerate growth and capability building. The Cigniti acquisition, funded primarily through internal accruals, demonstrates the company's ability to self-fund transformation.

Employee metrics provide another lens. Revenue: 2,080 Cr for Cigniti alone, when combined with Coforge's existing business, creates a company with over 30,000 employees globally. But it's not just about headcount—utilization rates, bill rates, and the pyramid structure all indicate a well-managed services business.

What's particularly noteworthy is the growth quality. This isn't just rate increases or currency benefits. Volume growth, new client additions, and expansion within existing accounts all contribute. The "land and expand" strategy works—start with a small engagement, prove value, and gradually take over more of the client's IT landscape.

Geographic diversification continues to improve. While North America remains the largest market, growth in Europe and Asia-Pacific provides balance. The Cigniti acquisition strengthens presence in the US Southwest and Midwest, markets where Coforge was historically underrepresented.

The path to $2 billion by FY27 seems achievable. With the current run rate approaching $1.5 billion and the Cigniti acquisition adding scale, organic growth of 15-20% annually would get them there. Add selective tuck-in acquisitions and the target seems conservative rather than aggressive.

For investors, the financial story is compelling. A company growing at 30%+ with expanding margins, strong cash generation, and a clear path to continued expansion is rare in today's market. The valuation at 8.55 times book value might seem expensive compared to traditional value metrics, but for a high-growth, asset-light business with strong returns on capital, it represents reasonable value.

IX. Playbook: Business & Investing Lessons

The Coforge journey offers a masterclass in building value in the IT services industry—a sector often dismissed as commoditized and unexciting. Several key lessons emerge:

The Power of Domain Specialization vs. Scale: While everyone chased scale, Coforge chose depth. This isn't about being small—it's about being focused. By becoming indispensable in select verticals, they command premium pricing and enjoy client relationships that span decades. The lesson: in professional services, expertise beats scale until you achieve both.

Successful PE-Backed Transformation Playbook: Baring's involvement from 2019-2023 demonstrates how private equity can create value beyond financial engineering. They provided capital for acquisitions, sure, but more importantly, they brought discipline, ambition, and a value-creation mindset. The complete rebranding, aggressive M&A, and cultural transformation wouldn't have happened under the previous ownership structure.

M&A as a Growth Lever: Three major acquisitions—RuleTek, SLK Global, and Cigniti—each brought specific capabilities and scale. This isn't the scatter-gun approach of buying revenue. Each acquisition was strategic, focusing on capability building in core verticals or adding complementary strengths. The integration success, particularly maintaining talent and client relationships, shows operational excellence beyond just deal-making.

Managing Through Ownership Transitions: From NIIT subsidiary to independent company to PE-owned to now effectively sponsor-less—each transition could have been disruptive. Instead, Coforge used each change as an opportunity for reinvention. The lesson: ownership changes, handled well, can catalyze transformation rather than cause disruption.

Building Sticky Client Relationships: In B2B services, client acquisition is expensive but client retention is profitable. Coforge's multi-decade relationships with clients like British Airways demonstrate the value of becoming embedded in client operations. Once you're managing mission-critical systems, switching costs—both financial and operational—create a powerful moat.

The Mid-Tier IT Services Sweet Spot: Being mid-sized in IT services is usually a disadvantage—too small for large deals, too large to be nimble. Coforge turned this into an advantage by being large enough to invest in capabilities but small enough to provide senior management attention to every client. They found the sweet spot between boutique specialization and large-scale efficiency.

Lessons from Rebrand and Repositioning: The transformation from NIIT Technologies to Coforge wasn't just about changing the name. It was about shedding legacy perceptions, attracting new talent, and signaling transformation to the market. The lesson: sometimes a clean break from the past is necessary for future growth.

The Vertical Integration Strategy: Unlike horizontal expansion across industries, Coforge's vertical integration within chosen industries—from application development to testing to BPM—creates multiple touchpoints with clients and increases wallet share. This is harder to execute than horizontal expansion but creates stronger competitive advantages.

Cultural Transformation Without Losing Identity: Through all the changes, Coforge maintained its core identity as a domain specialist while adopting PE-style execution discipline. This balance between continuity and change is difficult but essential for successful transformation.

The Power of Patient Capital: While Baring exited in 2023, they held for four years—long enough to execute real operational improvements rather than just financial engineering. This patient approach to value creation generated superior returns compared to quick flips based on multiple arbitrage.

For founders, the lesson is about focus and the courage to say no to opportunities outside your sweet spot. For investors, it's about recognizing that in professional services, specialized expertise can be more valuable than scale. For operators, it's about using ownership changes and M&A as catalysts for transformation rather than disruption.

X. Analysis & Bear vs. Bull Case

Bull Case:

The growth momentum is undeniable. The acquisition of Cigniti will not only help Coforge grow into a $2 billion firm by FY27 but the ensuing synergies will help the latter improve its operating margins by 150 – 250 bps in this timeframe. With 32% constant currency growth in FY25, Coforge is growing faster than companies a fraction of its size.

The M&A integration track record inspires confidence. Unlike many serial acquirers who destroy value through poor integration, Coforge has successfully integrated RuleTek, SLK Global, and now Cigniti. Each acquisition has been accretive to margins and brought new capabilities that accelerated organic growth.

Deep domain expertise creates a moat that's difficult to replicate. You can't just hire a few people and claim expertise in airline operations or wealth management. Coforge's decades of experience in these verticals, combined with proprietary IP and long-standing client relationships, creates barriers to entry that protect margins and market share.

The market opportunity remains vast. Even in their core verticals, Coforge has a tiny share of the total IT spend. As digital transformation accelerates and companies increasingly rely on specialized partners rather than trying to do everything in-house, Coforge is well-positioned to capture a disproportionate share of this growth.

Low attrition rates of 11.7% LTM (including Cigniti) in an industry notorious for 20%+ attrition indicate strong culture and employee satisfaction. This translates to better project delivery, higher client satisfaction, and lower recruitment and training costs.

The balance sheet remains strong despite aggressive acquisitions. The ability to fund the Cigniti acquisition primarily through internal accruals demonstrates robust cash generation. This financial flexibility allows Coforge to continue pursuing strategic acquisitions while investing in organic growth.

Bear Case:

Mid-tier positioning could become increasingly challenging. As the IT services industry consolidates, mid-sized players might get squeezed between large players with scale advantages and small specialists with agility. Coforge needs to continue growing to remain relevant, but growth through acquisition has its limits.

Concentration risk in select verticals is a double-edged sword. While specialization creates competitive advantages, it also creates vulnerability. A downturn in travel or financial services would disproportionately impact Coforge compared to more diversified competitors. The COVID-19 impact on travel industry clients was a reminder of this risk.

Integration risks multiply with each acquisition. While Coforge has a good track record, integrating Cigniti—their largest acquisition to date—while maintaining growth momentum will be challenging. Cultural differences, system integration, and client retention all pose risks.

Macro headwinds in IT spending could impact growth. As enterprises tighten budgets and scrutinize IT spending, discretionary projects might get delayed or cancelled. Coforge's exposure to transformation projects rather than just maintenance makes them more vulnerable to spending cuts.

Competition from both Indian and global players is intensifying. Larger Indian players are building capabilities in Coforge's core verticals. Global players like Accenture and Capgemini have the scale to invest heavily in domain expertise. Boutique specialists can be more agile in emerging technologies.

The talent war in IT services continues to intensify. While Coforge has managed attrition well, the competition for specialized talent in areas like cloud, AI, and digital engineering is fierce. Rising wage costs could pressure margins even as billing rate increases face resistance from cost-conscious clients.

Technological disruption poses long-term risks. As AI and automation reduce the need for traditional IT services, companies that don't successfully transition to higher-value services risk margin compression and revenue decline. While Coforge is investing in digital and IP-led services, the transition is incomplete.

The Verdict:

The bull case appears stronger in the near to medium term. Coforge has momentum, a clear strategy, and execution capabilities proven through multiple successful transformations. The path to $2 billion revenue by FY27 seems achievable, and margin expansion provides additional upside.

However, the bear case raises valid long-term concerns. The IT services industry is undergoing fundamental changes, and mid-tier players face structural challenges. Coforge needs to continue evolving—perhaps through building product capabilities or expanding into new verticals—to maintain its growth trajectory beyond FY27.

For investors, the key question isn't whether Coforge can reach $2 billion in revenue—they probably can. It's whether they can build a sustainable competitive advantage that survives industry consolidation, technological disruption, and changing client needs. The next few years will be crucial in answering this question.

XI. Epilogue & "If We Were CEOs"

The Coforge story is far from over. As the company integrates Cigniti and marches toward its $2 billion revenue target, new chapters are being written. The post-Baring era will test whether the transformation was sustainable or merely PE-driven financial engineering.

If we were running Coforge, several strategic priorities would dominate our agenda:

First, we'd double down on product development. While services will remain the core, building proprietary products for specific verticals would create recurring revenue streams and improve margins. Imagine a SaaS platform for airline operations or a wealth management solution designed specifically for private banks. The domain expertise exists—it needs to be productized.

Second, geographic expansion into high-growth markets deserves attention. While North America and Europe provide stability, markets like the Middle East, Southeast Asia, and Latin America offer growth opportunities. The key would be following existing clients into these markets rather than trying to build from scratch.

Third, the AI and automation impact needs proactive management. Rather than viewing AI as a threat to the services business, we'd position Coforge as the partner that helps enterprises adopt AI responsibly. This means building AI Centers of Excellence, training employees in prompt engineering and AI implementation, and developing AI-powered solutions for specific industry use cases.

Further consolidation seems inevitable. With the successful integration of Cigniti demonstrating M&A capabilities, Coforge could pursue additional acquisitions. Targets might include specialized testing companies, domain-specific product companies, or regional players that provide geographic expansion. The key would be maintaining discipline—only acquiring companies that bring strategic value beyond just revenue.

The talent strategy needs evolution. As the war for talent intensifies, traditional approaches won't suffice. We'd explore innovative models like acqui-hiring startups, partnering with universities for specialized programs, and creating internal academies that turn generalists into domain specialists. The NIIT heritage provides a unique advantage here—few IT services companies understand education and training as deeply.

Client relationship deepening remains crucial. Moving from vendor to partner to strategic advisor requires continuous investment in understanding client businesses. We'd establish industry advisory boards, sponsor research into sector-specific challenges, and perhaps even take equity stakes in client digital transformation initiatives.

The sustainability agenda can't be ignored. As enterprises focus increasingly on ESG goals, IT services partners need to demonstrate their contribution. This means not just reducing Coforge's own carbon footprint but helping clients achieve their sustainability goals through technology.

Finally, the ownership question looms. While being sponsor-less provides flexibility, it also leaves Coforge vulnerable to acquisition. Strategic options might include finding a long-term anchor investor, pursuing a dual listing to access deeper capital markets, or even exploring a merger of equals with another mid-tier player to achieve scale.

The next five years will determine whether Coforge becomes a permanent fixture in the global IT services landscape or gets absorbed into a larger entity. The fundamentals are strong, the strategy is clear, and execution has been exceptional. But in the fast-moving world of technology services, past performance doesn't guarantee future success.

What's certain is that Coforge has already defied expectations. From a small software division of an education company to a $6.5 billion market cap IT services leader, the transformation has been remarkable. Whether the next chapter brings continued independence and growth or strategic combination with a larger player, the Coforge story demonstrates that with focus, execution, and a willingness to transform, even mid-tier players can create exceptional value.

For founders, investors, and operators watching this story unfold, the lessons are clear: specialization beats generalization until you can do both, cultural transformation is possible through multiple ownership changes, and in professional services, expertise and relationships matter more than scale—until you achieve all three.

The Coforge journey continues. And in an industry often criticized for commoditization and lack of differentiation, they've proven that there's still room for innovation, value creation, and exceptional growth. The question now isn't whether Coforge has succeeded—they clearly have. It's how much further they can go.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube