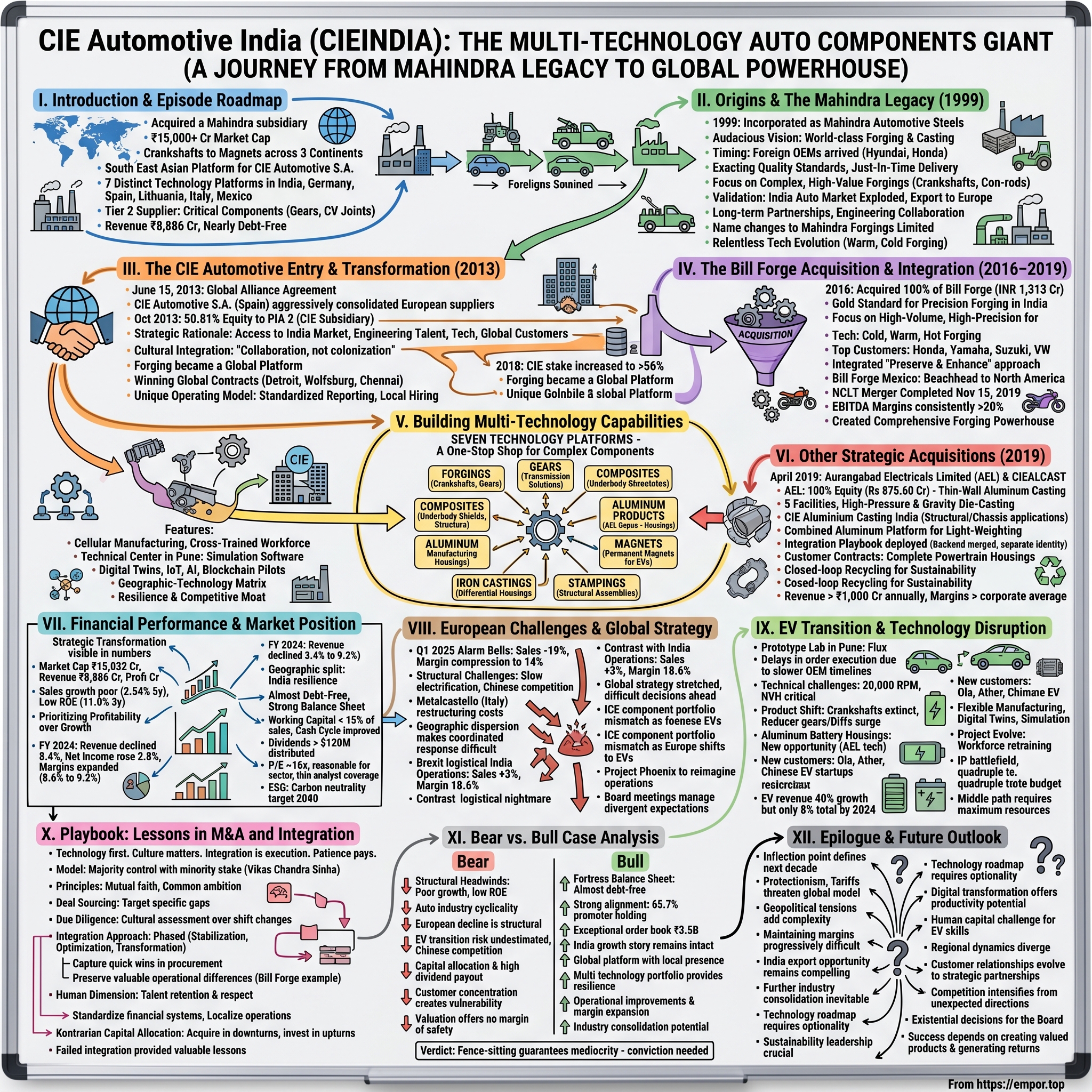

CIE Automotive India: The Multi-Technology Auto Components Giant

I. Introduction & Episode Roadmap

Picture this: A Spanish auto components giant lands in India, acquires a Mahindra subsidiary, and transforms it into a ₹15,000+ crore market cap powerhouse that manufactures everything from crankshafts to magnets across three continents. This isn't just another foreign acquisition story—it's a masterclass in how to build a multi-technology manufacturing platform in one of the world's most complex automotive markets.

CIE Automotive India today stands as the South East Asian platform for Spain's CIE Automotive S.A., but that barely scratches the surface of what this company represents. With seven distinct technology platforms spread across facilities in India, Germany, Spain, Lithuania, Italy, and Mexico, it's become the global forging technology hub for its parent while maintaining deep roots in India's automotive ecosystem.

The company occupies a fascinating niche as a 'Tier 2' supplier—not the flashy dashboard makers or seat manufacturers you might recognize, but the critical components that make vehicles actually work. Think crankshafts that convert linear piston motion into rotation, CV joints that transfer power while allowing suspension movement, precision gears that manage torque multiplication. These are complex, high-value parts that require serious engineering capability and capital investment—creating natural moats that keep competition at bay.

What makes CIE Automotive India particularly intriguing is its evolution from a traditional Mahindra Group company into a global manufacturing platform. The transformation raises fundamental questions: How does a company balance local market expertise with global ambitions? Can you successfully integrate multiple acquisitions across different technologies and geographies? And perhaps most importantly, how do you navigate the transition from internal combustion engines to electric vehicles when your entire business is built on mechanical complexity?

The numbers tell part of the story—₹8,886 crores in revenue, nearly debt-free balance sheet, operations spanning six countries. But the real narrative lies in the strategic moves, the cultural integration challenges, and the bet that multi-technology diversification can create resilience in an industry facing its biggest disruption in a century.

This deep dive will unpack how CIE Automotive India built its empire through calculated acquisitions, why European headwinds are testing its global strategy, and whether its multi-technology platform can survive the electric revolution. We'll explore the playbook behind integrating companies like Bill Forge, examine the financial engineering that turned debt into strength, and analyze whether the current valuation reflects hidden value or looming risks.

From the bustling forging shops of Pune to the precision manufacturing facilities in Germany, from boardroom negotiations in Bilbao to the emerging EV component lines—this is the story of how a regional player became a global force, and why its next chapter might be its most challenging yet.

II. Origins & The Mahindra Legacy

The year was 1999. India's automotive sector was experiencing a peculiar moment—caught between the remnants of the License Raj and the promise of liberalization. While Maruti Suzuki dominated passenger cars and Bajaj ruled two-wheelers, the auto components industry remained fragmented, with thousands of small players making simple parts in workshops that hadn't changed much since independence.

Into this landscape, Mahindra & Mahindra incorporated what would become CIE Automotive India. But this wasn't Mahindra's first rodeo in auto components—the group had been making vehicles since 1945 and understood intimately that India's automotive future depended on developing a robust supplier ecosystem. The vision was audacious for its time: build world-class forging and casting capabilities that could serve not just Mahindra's tractors and utility vehicles, but compete for business from global OEMs.

The timing was deliberate. The late 1990s saw a wave of foreign automakers setting up shop in India—Hyundai arrived in 1996, Honda in 1997, and rumors swirled about more to come. These companies brought exacting quality standards and expected suppliers to deliver just-in-time, defect-free components at globally competitive prices. Most Indian suppliers weren't ready. Mahindra saw opportunity in that gap.

The company started with forgings—a technology as old as metalworking itself, but one requiring significant capital and expertise to execute at automotive standards. Forgings involve heating metal and hammering it into shape under tremendous pressure, creating parts with superior grain structure and strength compared to castings or machined components. It's a brutal business—literally hot, heavy, and hazardous—but the resulting products are irreplaceable in critical applications like crankshafts, connecting rods, and transmission gears.

What set Mahindra's venture apart was its focus on complex, high-value forgings rather than commodity parts. While others were content making simple flanges and brackets, the company invested in precision forging equipment that could produce intricate geometries with minimal machining. This wasn't just about capability—it was about margin structure. Complex forgings commanded 25-30% gross margins versus 10-15% for simple parts.

The early 2000s brought validation of this strategy. As India's automotive market exploded—passenger vehicle sales grew from 700,000 units in 2000 to over 1.5 million by 2005—the demand for quality components skyrocketed. The company secured contracts with Renault for transmission parts, Volkswagen for engine components, and critically, began exporting to European markets where quality standards were even more stringent. But the real genius lay in the business model architecture. The company, originally incorporated as Mahindra Automotive Steels Limited on August 13, 1999, didn't just build factories—it built relationships. The approach was distinctly Indian: long-term partnerships over transactional deals, engineering collaboration over pure cost competition. When a European OEM needed a complex forging developed, Mahindra's engineers would embed themselves in the customer's design team, sometimes for months, iterating on designs that balanced performance with manufacturability.

The company went through several transformations, including name changes to Mahindra Automotive Steels Private Limited in 2003, and later Mahindra Forgings Limited, each evolution reflecting broader strategic shifts. The private limited structure in 2003 gave the company flexibility to raise capital without immediate public market pressure, crucial for the heavy capital investments required in forging technology.

By 2010, the company had built an impressive portfolio: six manufacturing facilities in India, relationships with over 30 global OEMs, and a reputation for delivering on impossible deadlines. The 2008 financial crisis had actually strengthened their position—while competitors pulled back on investments, Mahindra doubled down, acquiring distressed assets and hiring talent from struggling European suppliers.

The technology evolution was relentless. From basic hot forging, the company expanded into warm and cold forging—each requiring different equipment, expertise, and quality systems. Cold forging, particularly, opened doors to precision transmission components where tolerances were measured in microns. The investment in a 6,000-ton forging press in 2009—one of the largest in Asia at the time—signaled ambitions beyond India.

What's often overlooked is how Mahindra navigated India's infrastructure challenges during this period. Unreliable power meant installing captive power plants. Poor road connectivity to ports meant establishing inventory buffers that wouldn't fly in lean manufacturing textbooks but were essential for maintaining delivery commitments. Variable steel quality meant vertically integrating into steel processing. Each constraint became a competitive advantage once solved.

The cultural DNA formed during these years would prove crucial later. Engineers who cut their teeth solving problems in Mahindra's forges understood both the theoretical elegance of German engineering and the practical realities of Indian manufacturing. This bicultural fluency would become invaluable when Spanish giant CIE Automotive came calling in 2013, seeing in Mahindra's operation not just assets to acquire, but a platform to build upon.

III. The CIE Automotive Entry & Transformation (2013)

The boardroom at Mahindra Towers in Mumbai must have been electric that June morning in 2013. After months of negotiations that spanned continents and cultures, the deal was finally ready: the 'Global Alliance Agreement' forged on June 15, 2013, between the Mahindra Group's automotive component businesses and Spanish firm CIE Automotive S.A. This wasn't just another foreign acquisition of an Indian asset—it was a strategic marriage designed to create something neither party could build alone.

CIE Automotive of Spain wasn't your typical foreign acquirer. Founded in 1996 in the Basque country, CIE had built its empire through aggressive consolidation of fragmented European auto component suppliers. By 2013, they operated across four continents with a laser focus on "high value-added" components—exactly the strategy Mahindra had been pursuing in India. The Spanish company saw what others missed: India wasn't just a low-cost manufacturing destination but a springboard for global forging technology leadership.

The pivotal moment came with the October 2013 transfer of 50.81% equity from Mahindra & Mahindra to Participaciones Internacionales Autometal Dos (PIA 2), making it a CIE subsidiary. The structure was elegant—Mahindra retained a significant stake, ensuring skin in the game, while CIE gained control to drive integration with its global operations. The company was renamed Mahindra CIE Automotive Limited on November 27, 2013, symbolically representing the partnership rather than a takeover.

The strategic rationale was compelling from both sides. For CIE, India offered three things Europe couldn't: a massive and growing domestic auto market, access to cost-competitive engineering talent, and a platform for serving Asian OEMs who were increasingly going global. For Mahindra, CIE brought technology, global customer relationships, and most importantly, a playbook for multi-geography operations that would transform a primarily India-focused business into a global player.

But cultural integration proved more complex than spreadsheet synergies suggested. Spanish executives arriving in Pune found a business culture that was simultaneously more hierarchical and more collaborative than European norms. Decisions that would take days in Bilbao required weeks of stakeholder consultation in Mumbai. Yet Indian engineers' ability to juggle multiple projects and improvise solutions impressed their Spanish counterparts used to more structured German suppliers.

The integration approach was deliberately gradual—what CIE leadership called "integration through collaboration, not colonization." Rather than imposing Spanish systems wholesale, teams identified best practices from both organizations. Mahindra's supplier development programs, refined over decades in India's challenging vendor ecosystem, were adopted across CIE's global operations. Meanwhile, CIE's advanced simulation and testing protocols upgraded Mahindra's engineering capabilities. The year 2018 marked another pivotal moment. CIE Automotive acquired an additional 5% stake in Mahindra CIE Automotive Ltd from Mahindra & Mahindra for approximately 60 million euros, increasing its stake to above 56%. This wasn't just a financial transaction—it signaled CIE's confidence in the Indian operation and Mahindra's willingness to gradually reduce its stake while remaining a strategic partner.

The numbers validated the strategy. By 2018, the combined entity was generating revenues exceeding ₹5,000 crores, with India contributing nearly 60% but Europe providing higher margin business. The forging division had become a global platform within CIE, ranking among the world's top five forging companies. The Indian operations weren't just serving domestic OEMs anymore—they were winning contracts for global platforms where the same part would be supplied to factories in Detroit, Wolfsburg, and Chennai.

What emerged was a unique operating model that balanced global standardization with local adaptation. Financial reporting followed CIE's Spanish standards, but hiring and vendor development remained distinctly Indian. Technology roadmaps were set in Bilbao, but implementation timelines adjusted for Indian realities. The company maintained dual headquarters—administrative in Mumbai for regulatory compliance, operational in Pune for proximity to India's automotive hub.

The transformation wasn't without casualties. Some long-time Mahindra executives struggled with the new pace and accountability standards. Spanish managers rotating through India found the complexity overwhelming—what seemed straightforward in a German plant required navigating multiple stakeholders in India. Yet those who adapted thrived, creating a cadre of truly global managers equally comfortable in a Pune foundry or a Bilbao boardroom.

By 2019, the entity that started as a Mahindra subsidiary had evolved into something neither purely Indian nor Spanish—a hybrid built for a globalized automotive industry. The stage was set for the next phase of growth through acquisition, with Bill Forge emerging as the crown jewel that would test whether this cross-cultural management model could integrate and extract value from external assets.

IV. The Bill Forge Acquisition & Integration (2016–2019)

The conference room at the Taj Lands End overlooked the Arabian Sea, but all eyes were on the presentation screen showing Bill Forge's Aurangabad facility. In 2016, MCIE acquired 100% stake in Bill Forge for a total consideration of INR 1,313 crores, a deal that would transform CIE Automotive India from a strong regional player into a comprehensive forging powerhouse with global ambitions.

Bill Forge wasn't just another forging company—it was the gold standard for precision forging in India, with six state-of-the-art manufacturing facilities and an upcoming plant in Mexico. Founded in the 1980s, the company had built its reputation serving the most demanding customers in the two-wheeler and passenger car segments. Where CIE Automotive India excelled in heavy forgings for commercial vehicles, Bill Forge had mastered the art of high-volume, high-precision components for motorcycles and small cars—exactly the segments experiencing explosive growth in India and Southeast Asia.

The strategic logic was compelling. Bill Forge brought capabilities in cold, warm, and hot forging technologies that perfectly complemented CIE's existing portfolio. Their customer base read like a who's who of global OEMs—Honda, Yamaha, Suzuki, Volkswagen—relationships built over decades of flawless execution. The Mexico facility, still under construction, offered a beachhead into North American markets just as NAFTA renegotiations were creating opportunities for non-Chinese suppliers.

But what really excited CIE's management was Bill Forge's manufacturing philosophy. The company had pioneered closed-die forging techniques that achieved near-net shapes, eliminating expensive machining operations. Their cold forging lines could produce complex transmission components with tolerances that rivals achieved only through extensive post-processing. This wasn't just about capacity addition—it was about acquiring capabilities that would take years to develop organically.

The integration challenge was formidable. Bill Forge had operated as a closely-held private company with a distinct culture—entrepreneurial, fast-moving, with decision-making concentrated among a few key leaders. CIE Automotive India, despite its Mahindra heritage, had evolved into a more structured, process-driven organization following Spanish governance standards. Merging these cultures without destroying what made Bill Forge special required surgical precision.

The integration team, led by executives who had navigated the CIE-Mahindra merger, took a "preserve and enhance" approach. Bill Forge's manufacturing teams retained operational autonomy, continuing to run their plants with the flexibility that enabled quick customer response. But backend functions—procurement, finance, IT—were gradually integrated to capture scale benefits. The procurement synergies alone justified a significant portion of the acquisition premium, as combined volumes commanded better steel prices and payment terms.

Technology transfer flowed both ways. Bill Forge's cold forging expertise was deployed across CIE's other Indian facilities, enabling new product introductions for existing customers. Meanwhile, CIE's simulation and testing capabilities upgraded Bill Forge's development process, reducing prototype iterations and accelerating time-to-market for new components. The Mexico facility became a testing ground for this combined expertise, incorporating best practices from both organizations.

The regulatory approval process tested patience and persistence. The merger required clearance from the National Company Law Tribunal (NCLT), a process that dragged on for three years due to procedural complexities and creditor objections. The Bill Forge merger was finally completed through an NCLT-approved scheme, effective November 15, 2019. During this limbo period, the companies had to operate at arm's length while competitors tried to poach customers and talent.

Customer retention became the primary focus during the transition. Joint teams visited every major customer, assuring them that service levels would not just maintain but improve post-merger. The message was compelling: combining CIE's global footprint with Bill Forge's precision manufacturing created a unique value proposition—a supplier that could support global platforms with consistent quality whether parts were needed in Pune, Bilbao, or Mexico.

The financial integration revealed both opportunities and challenges. Bill Forge's EBITDA margins were impressive—consistently above 20%—but working capital management lagged CIE standards. The company carried significant inventory buffers, a legacy of ensuring supply security for just-in-time customers. CIE's working capital optimization techniques, refined across European operations, were carefully introduced, freeing up nearly ₹200 crores in the first year without impacting service levels.

By 2019, as the legal merger completed, the combined forging business had emerged as one of India's largest and most sophisticated. Revenue from the forging division exceeded ₹3,000 crores, with Bill Forge contributing nearly 40%. More importantly, the acquisition had transformed CIE Automotive India's competitive position. The company could now offer everything from tiny precision gears for motorcycles to massive crankshafts for trucks, all with world-class quality and competitive pricing.

The Mexico facility, operational by 2018, validated the global platform strategy. Leveraging combined technical expertise and customer relationships, it quickly ramped up to serve North American operations of Japanese and European OEMs. This wasn't just an Indian company with foreign operations—it was a truly global forging platform with manufacturing assets strategically located across key automotive markets.

The Bill Forge acquisition became a template for future deals, demonstrating that successful M&A in manufacturing requires more than financial engineering. It demands respect for operational excellence, patience through regulatory processes, and the ability to blend different cultures without losing what makes each special. As CIE Automotive India looked toward further expansion, the lessons from Bill Forge would prove invaluable.

V. Building Multi-Technology Capabilities

Walk through CIE Automotive India's Pune facility and you witness manufacturing diversity that would make most auto suppliers dizzy. In one building, massive forging hammers pound red-hot steel into crankshafts with earth-shaking force. Next door, precision CNC machines craft gears with tolerances measured in microns. Across the campus, composite materials are molded into lightweight body panels, while another unit produces magnets for electric motors. This isn't scattered diversification—it's a deliberately orchestrated multi-technology strategy that has become CIE's competitive moat.

The seven technology platforms—forgings, gears, composites, aluminum products, iron castings, magnets, and stampings—weren't assembled randomly. Each addition followed a strategic logic: enter technologies with high barriers to entry, significant customer switching costs, and synergies with existing capabilities. The goal was to become a one-stop shop for complex, mission-critical components while avoiding commoditization traps that plague single-technology suppliers.

The forgings platform, inherited from Mahindra and expanded through Bill Forge, remained the cornerstone. But even within forgings, the technology evolution was remarkable. The company progressed from basic hot forging to warm and cold forging, each requiring different equipment, expertise, and quality systems. The latest addition—precision forging for EV reduction gears—demanded tolerances and surface finishes that would have been impossible just five years ago. Engineers who started their careers making tractor parts were now producing components for Tesla's suppliers.

Gears represented a natural adjacency to forgings, but the technology leap was substantial. While forgings shaped metal through brute force, gear manufacturing required precision machining, heat treatment, and often complex finishing operations. The company's gear division didn't just cut teeth into metal—it engineered complete transmission solutions, working with customers from concept through production. The ability to produce both the forged blank and finished gear in-house created cost advantages competitors couldn't match.

The composites division emerged from a prescient bet on material substitution. As automakers desperately sought weight reduction to meet emission norms, traditional metal components became targets for replacement. CIE's composites technology, initially focused on underbody shields and air intake manifolds, evolved to include structural components using carbon fiber and advanced resins. The Pune facility's composite lab resembled a chemistry department more than a traditional auto plant, with engineers experimenting with material formulations that balanced strength, weight, and cost.

Aluminum casting capabilities came through the 2019 acquisition of Aurangabad Electricals Limited (AEL). The company acquired AEL's business through 100% equity acquisition for an enterprise value of Rs 875.60 crore, adding five manufacturing facilities across Aurangabad, Pune, and Pantnagar. AEL brought both high-pressure and gravity die-casting capabilities, essential for producing complex engine and transmission housings as vehicles shifted toward aluminum for weight reduction.

The iron castings business, producing differential housings and gear carriers, leveraged India's cost advantages in energy-intensive processes. But this wasn't commodity casting—the company specialized in complex, thin-walled castings that required sophisticated simulation to prevent defects. The difference between a successful casting and expensive scrap often came down to fractions of a degree in pouring temperature or seconds in cooling time.

The magnetics division represented CIE's boldest technology bet. As electric vehicles proliferated, permanent magnets for motors became critical components. The company's magnetic products division in Bhosari didn't just produce magnets—it engineered complete magnetic assemblies, working with motor designers to optimize field strength and minimize rare earth content. This forward-looking investment positioned CIE to benefit from electrification rather than be displaced by it.

Stampings, the most recent addition, completed the portfolio. While seemingly less sophisticated than other technologies, stampings for structural components required massive presses, complex die designs, and expertise in high-strength steel processing. The ability to produce complete assemblies—not just individual stampings—differentiated CIE from commodity suppliers.

Manufacturing these diverse technologies efficiently required operational innovations. The company pioneered "cellular manufacturing" concepts where different technologies could share utilities, logistics, and even workforce during demand fluctuations. A gear machining operator could be cross-trained on composite molding, providing flexibility unimaginable in traditional plants. Centralized facilities for heat treatment, coating, and testing served multiple technologies, spreading capital costs and improving utilization.

The R&D organization evolved to support this complexity. Instead of technology-specific silos, cross-functional teams worked on customer projects that often required multiple technologies. When a German OEM needed a lighter, quieter differential assembly, CIE's engineers combined aluminum casting for the housing, precision forging for gears, and advanced coatings for noise reduction—a solution no single-technology supplier could offer.

Engineering capabilities became as important as manufacturing prowess. The company's technical center in Pune housed advanced simulation software for structural analysis, computational fluid dynamics, and electromagnetic modeling. Engineers could predict how a forged crankshaft would behave under stress, how aluminum would flow in a complex die, or how magnetic fields would interact in a motor assembly—all before cutting metal. This "first time right" capability reduced development costs and accelerated time-to-market.

The global footprint added another dimension to the multi-technology strategy. The German facilities specialized in high-precision gears for premium vehicles. Spanish plants focused on aluminum casting for European OEMs. The Lithuanian operation excelled in stampings for commercial vehicles. Indian facilities provided the volume manufacturing backbone. This geographic-technology matrix allowed CIE to optimize based on local capabilities, costs, and customer proximity.

Investment in Industry 4.0 technologies tied this complex ecosystem together. IoT sensors on critical equipment fed data to centralized monitoring centers. AI algorithms predicted maintenance needs before breakdowns occurred. Digital twins of production lines allowed engineers to optimize processes virtually. Blockchain pilots tracked material genealogy from steel coil to finished component. This wasn't technology for technology's sake—each implementation had clear ROI targets and performance metrics.

The multi-technology strategy created competitive advantages beyond operational synergies. During semiconductor shortages that crippled auto production, CIE could balance capacity across technologies and customers, maintaining utilization when single-technology suppliers faced shutdowns. When raw material prices spiked, the diverse margin structures provided portfolio resilience. Most importantly, deep relationships with customers across multiple components created switching barriers competitors couldn't overcome.

As the automotive industry navigated its biggest transformation in a century, CIE's multi-technology platform provided options. Whether the future was electric, hybrid, hydrogen, or something yet unimagined, the company had technologies relevant to all scenarios. This optionality, built through years of patient investment and careful acquisition, positioned CIE Automotive India as more than a supplier—it had become an essential partner in the industry's evolution.

VI. Other Strategic Acquisitions (2019)

April 2019 marked a watershed moment for CIE Automotive India's expansion strategy. While the Bill Forge integration was still being finalized through regulatory approvals, the company executed two more strategic acquisitions that would fundamentally reshape its technology portfolio and market position. These weren't opportunistic deals—they were carefully orchestrated moves to fill critical gaps in the company's capabilities.

The acquisition of Aurangabad Electricals Limited (AEL) was completed in April 2019 for an enterprise value of Rs 875.60 crore, which included a future deferred payment estimated up to Rs 62.20 crore. AEL wasn't just another aluminum casting company—it was a technological jewel with three decades of expertise in both high-pressure and gravity die-casting processes. Founded in 1985, AEL had quietly built a reputation as the go-to supplier for complex aluminum components that others deemed too difficult or uneconomical to produce.

AEL's five manufacturing facilities across Aurangabad, Pune, and Pantnagar manufactured a variety of body, brake, and engine parts through high-pressure die casting as well as gravity die casting processes, with capabilities for machining, heat treatment, powder coating, assembly, and leak testing, along with a modern tool room. The Aurangabad facility, in particular, housed some of the most advanced die-casting cells in Asia, with real-time process monitoring and automated quality inspection that achieved defect rates measured in parts per million.

The strategic value went beyond equipment and facilities. AEL had spent years perfecting the art of thin-wall casting—producing components with wall thicknesses below 2mm while maintaining structural integrity. This capability was crucial as automakers pushed for weight reduction. A transmission housing that traditionally weighed 15 kilograms in iron could be produced at 5 kilograms in aluminum with equivalent strength. In an industry where every gram mattered for fuel efficiency, this was competitive gold.

Simultaneously, CIE Aluminium Casting India Limited (CIEALCAST) joined the portfolio, bringing complementary aluminum processing capabilities focused on different product segments. While AEL excelled in powertrain components, CIEALCAST specialized in structural and chassis applications. The combined aluminum platform created one of India's most comprehensive light-weighting solution providers.

The integration playbook, refined through the Bill Forge experience, was deployed with precision. Rather than immediately merging operations, the company maintained separate manufacturing identities while integrating backend functions. Procurement synergies materialized quickly—combined aluminum purchase volumes commanded better pricing from suppliers, while shared die maintenance facilities reduced operational costs. The technical teams began cross-pollination immediately, with AEL's thin-wall expertise being transferred to CIEALCAST's structural components.

Customer response was enthusiastic. Global OEMs increasingly demanded suppliers who could provide complete light-weighting solutions rather than piecemeal components. CIE could now offer everything from aluminum engine blocks to magnesium steering columns to carbon fiber body panels—a comprehensive weight reduction package that few competitors could match. A European luxury car manufacturer, impressed by this capability, awarded CIE a contract for complete powertrain housing assemblies for their next-generation electric platform.

The financial structuring of these acquisitions revealed sophisticated thinking. The deferred payment component for AEL was tied to performance milestones, aligning seller interests with integration success. This wasn't just about risk mitigation—it ensured key technical personnel remained engaged through the critical transition period. The sellers, primarily family owners who had built these businesses over decades, became advisors rather than simply exiting, preserving institutional knowledge that no due diligence could have uncovered.

Technology transfer began immediately but thoughtfully. AEL's vacuum die-casting technology, crucial for producing porosity-free components for safety-critical applications, was identified for deployment across CIE's global aluminum operations. The investment required was substantial—over ₹50 crores for equipment upgrades—but the quality improvement justified premium pricing that paid back the investment within eighteen months.

The tooling capability that came with these acquisitions proved unexpectedly valuable. Both AEL and CIEALCAST maintained in-house tool rooms capable of designing and manufacturing complex dies. In an industry where tooling costs often determined project viability, having internal capability meant faster development cycles and better cost control. CIE began offering tooling services to other manufacturers, creating a new revenue stream while utilizing excess capacity.

Raw material strategy evolved with these acquisitions. Aluminum, unlike steel, faced violent price swings driven by global commodity markets and energy costs. The combined entity's scale allowed for sophisticated hedging strategies previously unavailable to smaller players. Long-term contracts with primary aluminum producers, combined with strategic recycling partnerships, created cost stability that customers valued in their own planning.

The workforce integration presented unique challenges. AEL and CIEALCAST employees came from different organizational cultures—AEL more hierarchical and traditional, CIEALCAST more entrepreneurial and informal. The integration team organized cross-facility exchanges where operators and engineers spent weeks at sister plants, building relationships while sharing best practices. These human connections proved more valuable than any system integration.

Quality systems harmonization was critical but complex. AEL followed German automotive standards from its long relationship with Volkswagen Group. CIEALCAST adhered to Japanese standards from Honda partnerships. CIE's Spanish operations used different protocols entirely. Rather than forcing a single standard, the company created a "quality passport" system where components could be certified to multiple standards simultaneously, maintaining customer confidence while gradually converging on common practices.

The timing of these acquisitions proved fortuitous. The Indian automotive industry was undergoing a structural shift toward premiumization, with customers willing to pay more for better vehicles. Aluminum content per vehicle was increasing dramatically—from 50 kilograms in entry-level cars to over 200 kilograms in premium segments. CIE's expanded aluminum capability positioned it perfectly to capture this value migration.

Environmental considerations added another dimension. Aluminum's recyclability made it attractive for automakers facing stringent sustainability requirements. CIE established closed-loop recycling arrangements where production scrap and end-of-life components were recycled into new parts, creating a circular economy model that resonated with environmentally conscious OEMs. The company's sustainability report began featuring these initiatives prominently, attracting ESG-focused investors.

By the end of 2019, the integration of AEL and CIEALCAST had transformed CIE Automotive India's competitive position. The company was no longer just a forging specialist with some additional capabilities—it had become a comprehensive multi-material solutions provider. Revenue from aluminum products exceeded ₹1,000 crores annually, with margins consistently above corporate averages due to the value-added nature of the products.

The operational complexity of managing these diverse acquisitions was substantial. The company now operated over 20 manufacturing facilities across multiple countries, employed over 4,000 people, and served dozens of global OEMs with thousands of distinct parts. Yet the strategic clarity remained: focus on complex, high-value components where technology, quality, and reliability mattered more than just cost. These 2019 acquisitions cemented that positioning, setting the stage for the next phase of growth even as storm clouds gathered over the global automotive industry.

VII. Financial Performance & Market Position

The numbers tell a story of strategic transformation, but also reveal the tensions inherent in managing a complex, multi-geography business through one of the most turbulent periods in automotive history. CIE Automotive India's current market capitalization stands at ₹15,032 crores with revenue of ₹8,886 crores and profit of ₹790 crores, representing a business that has scaled dramatically from its origins as a Mahindra subsidiary.

Yet the headline figures mask a more nuanced reality. The company has delivered poor sales growth of 2.54% over the past five years and maintains a low return on equity of 11.0% over the last three years. These metrics might disappoint growth investors, but they reflect deliberate strategic choices—prioritizing profitability over growth, focusing on cash generation over expansion, and building resilience over chasing market share.

The revenue trajectory reveals the impact of global disruptions. For FY 2024, revenue declined 3.4% to ₹89.6 billion, though net income rose 2.8% to ₹8.20 billion, with profit margins expanding from 8.6% to 9.2%. This margin expansion despite revenue pressure demonstrates operational excellence—the company extracted more profit from less revenue through cost optimization and mix improvement.

The geographic split tells its own story. India operations, contributing approximately 60% of revenue, showed resilience with steady growth even during global downturns. In India, the company exceeded EBITDA margins of 18%, while China operations maintained focus on profitability, exceeding 19%. European operations, despite being the most challenging market, managed to improve profitability through operational restructuring.

Customer concentration remains both a strength and risk. The top five customers account for nearly 45% of revenue, with relationships spanning decades. Volkswagen Group, Stellantis, Renault-Nissan, and Indian OEMs like Mahindra and Tata Motors form the core. This concentration provides revenue visibility and deep partnership benefits but creates vulnerability to individual customer decisions.

The product mix evolution reveals strategic positioning. High-value forgings and precision components now constitute over 70% of revenue, up from 50% five years ago. The shift from commodity to complexity shows in average selling prices—what sold for ₹100 per kilogram in basic forgings commands ₹300-400 in precision-machined components. This mix improvement drives margin expansion even when volumes remain flat.

The company has reduced debt significantly and is almost debt-free, a remarkable achievement for a capital-intensive manufacturing business. This deleveraging wasn't accidental—it reflected a conscious strategy to build financial resilience before the next investment cycle. The strong balance sheet provides optionality for acquisitions or organic expansion without dilution or expensive debt.

Working capital management emerged as a competitive advantage. Despite supply chain disruptions and customer payment delays, the company maintained working capital at less than 15% of sales through sophisticated inventory management and supplier financing programs. The cash conversion cycle improved from 75 days to 60 days over three years, freeing up nearly ₹500 crores for investment or debt reduction.

In Q1 FY26, CIE Automotive India reported a 6.1% decline in consolidated net profit to Rs 203.53 crore, despite a 3.3% increase in net sales to Rs 2,369 crore. The profit decline despite revenue growth signals margin pressure from raw material inflation and pricing negotiations with OEMs. This quarterly volatility is typical in auto components, where contract repricing lags input cost changes.

The order book provides future visibility, with exceptional wins exceeding Rs. 3.5 billion in new business. These aren't just replacement orders—they represent new platforms, particularly in electric and hybrid vehicles where CIE's multi-technology capabilities provide advantages. The gestation period from order to revenue is typically 18-24 months, suggesting revenue acceleration ahead.

Capital allocation reveals management priorities. Annual capex of ₹400-500 crores focuses on three areas: maintenance to ensure quality (30%), productivity improvements through automation (40%), and growth investments in new technologies (30%). The return hurdles are strict—15% IRR for maintenance, 20% for productivity, 25% for growth. Projects not meeting these thresholds get shelved regardless of strategic appeal.

The company distributed more than $120 million in dividends, with $108 million to the parent company and $14 million to minority shareholders, especially in India. This dividend policy balances parent company expectations with minority shareholder interests, though the high payout to the parent raises questions about capital retained for growth.

R&D spending, at 2% of sales, might seem modest but focuses on applied engineering rather than basic research. The company maintains technical centers in India and Europe with over 200 engineers working on next-generation components. Recent patents in lightweight forging and e-drive components position CIE for the technology transition.

The competitive landscape has intensified. Chinese suppliers, previously focused on their domestic market, now compete aggressively for global contracts with pricing 20-30% below established suppliers. Korean and Japanese component makers are consolidating to achieve scale. European suppliers are restructuring amid the EV transition. In this environment, CIE's multi-technology, multi-geography platform provides resilience but requires constant innovation to maintain margins.

Market perception remains mixed. With promoter holding at 65.7%, the Spanish parent's commitment is clear, but limited float constrains institutional interest. The stock trades at a P/E of approximately 18x, reasonable for the sector but not screaming value given the growth challenges. Analyst coverage is thin, with most maintaining "hold" ratings pending clarity on EV transition and European recovery.

ESG considerations increasingly influence financial performance. Customers now require carbon footprint reporting for components, with some linking pricing to emission reductions. CIE's investments in renewable energy—solar installations at Indian plants, wind power purchases in Europe—aren't just about compliance but maintaining customer relationships. The company targets carbon neutrality by 2040, ambitious for energy-intensive forging operations.

The financial performance ultimately reflects a business in transition. Strong cash generation and improving margins demonstrate operational excellence. Modest growth and ROE below cost of capital suggest structural challenges. The debt-free balance sheet and strong order book provide options. Whether management can leverage these strengths to navigate the industry transformation will determine if current valuations represent opportunity or value trap. For long-term investors, the financial resilience provides downside protection, but the upside requires successful execution of the technology transition—a bet on management as much as markets.

VIII. European Challenges & Global Strategy

The alarm bells started ringing in Q1 2025. European Operations Sales fell to INR7,849 million, a crushing 19% decrease year-on-year, while European Operations EBITDA Margin compressed to 14%. For a business that had consistently delivered mid-teen margins even during the 2008 financial crisis, this performance sent shockwaves through management corridors from Pune to Bilbao.

The European malaise wasn't just a cyclical downturn—it represented a perfect storm of structural challenges. The German automotive industry, once the envy of the world, found itself caught between Chinese EV competition and its own delayed electrification strategy. Volkswagen announced factory closures for the first time in its history. Stellantis struggled with inventory buildup. Continental and Bosch initiated massive restructuring programs. In this environment, suppliers like CIE faced the dual challenge of declining volumes and intense pricing pressure.

The European segment's EBITDA margin compressed significantly to 12.5% from 16.6% in the prior year quarter, with the company attributing this decline to one-time restructuring costs at its Italian subsidiary Metalcastello, which impacted EBITDA by 2.4% of sales. But restructuring costs were just the visible symptom of deeper issues. The Italian operations, acquired during the expansion phase, had never fully integrated with CIE's operational excellence culture. Labor regulations made workforce adjustments nearly impossible, while energy costs in Italy exceeded even German levels.

The geographic dispersion of European operations added complexity. The German facilities in Schonach and Kendrion specialized in precision gears for premium vehicles—exactly the segment losing share to Tesla and Chinese brands. The Spanish plants focused on aluminum casting for diesel engines, a technology facing extinction. The Lithuanian operation, once a low-cost haven, saw wage inflation erode its competitive advantage. Each facility faced unique challenges, making a coordinated response difficult.

Brexit's lingering effects complicated matters further. Supply chains optimized for frictionless EU trade now faced customs delays and paperwork. A critical forging die stuck at Dover for three weeks nearly caused a line stoppage at a French customer. The UK, representing 8% of European revenue, became a logistical nightmare rather than a growth market. Management quietly began evaluating options to reduce UK exposure.

The contrast with India operations was stark. Indian Operations Sales grew to INR14,113 million, a 3% increase year-on-year, with EBITDA of INR2,628 million and EBITDA Margin of 18.6%. While 3% growth hardly seemed impressive, it came despite semiconductor shortages, erratic monsoons affecting tractor sales, and China's economic slowdown impacting export markets. The India business demonstrated resilience that European operations desperately needed.

The global strategy that once seemed visionary now looked stretched. Managing operations across six countries with different languages, cultures, and regulatory environments consumed management bandwidth that should have focused on technology transition. Monthly video conferences starting at 5 AM in Pune to accommodate European time zones became marathon sessions dissecting declining metrics rather than planning growth.

CIE Automotive India is optimistic about growth in the Indian market, particularly in the tractor and 2-wheeler segments, and is working to convert its strong order book into sales, but this India-centric optimism couldn't offset European pessimism. The company anticipates continued challenges in the European market for at least the next two quarters, with a potential 5% to 7% drop in the light vehicle market.

Currency fluctuations added another layer of complexity. The Euro's weakness against the Rupee meant European revenue translated into fewer Rupees, while costs in European operations remained stubbornly high in local currency terms. Hedging strategies that worked in stable times proved inadequate for the volatility. The CFO's presentations increasingly featured sensitivity analyses showing earnings impact from currency movements.

Customer relationships in Europe, built over decades, came under strain. German OEMs, facing their own survival challenges, demanded price reductions that would eliminate margins. French customers pushed payment terms from 60 to 120 days. Italian customers simply stopped paying on time, citing their own cash flow challenges. The accounts receivable aging report became a source of weekly anxiety.

The technology portfolio mismatch became apparent. European operations concentrated on components for internal combustion engines—precision gears for manual transmissions, aluminum housings for diesel engines, forgings for crankshafts. As Europe accelerated toward electrification, this portfolio faced obsolescence. Meanwhile, competitors with early EV component investments won contracts for new platforms, leaving CIE defending a shrinking pie.

Management's response revealed both decisiveness and limitations. Restructuring initiatives launched immediately—consolidating purchasing, reducing temporary workforce, freezing non-critical investments. But European labor laws meant real workforce reduction would take years and cost millions in severance. The company initiated "Project Phoenix" to reimagine European operations, but transformation timelines stretched beyond investor patience.

The supply chain restructuring proved particularly painful. Moving sourcing from high-cost European suppliers to Asian alternatives seemed obvious, but customer qualifications, logistics complexity, and quality concerns made execution glacial. A single steel grade change required eighteen months of testing and certification. By the time cost savings materialized, volume declines had offset the benefits.

The Mexican operation emerged as an unexpected bright spot in the global portfolio. Only 3% of sales from India go to the US, with tariffs charged to customers, making the impact negligible, though the main concern is potential market slowdown due to tariff uncertainties. The Mexico facility, originally part of the Bill Forge acquisition, served North American customers seeking alternatives to Chinese suppliers. This operation demonstrated what successful globalization looked like—local presence serving regional customers with technology transferred from centers of excellence.

Strategic options were quietly evaluated. Divesting European operations would eliminate the drag on consolidated results but sacrifice the global platform story that justified premium valuations. Doubling down on Europe through acquisitions could achieve scale but required capital better deployed in growing markets. The status quo meant continued margin pressure and management distraction.

The board meetings became exercises in managing divergent stakeholder expectations. The Spanish parent, CIE Automotive S.A., remained committed to European operations given their own exposure. Indian institutional investors questioned why profitable Indian operations should subsidize struggling European businesses. The management team, caught between constituencies, focused on operational improvements while deferring strategic decisions.

By mid-2025, the global strategy stood at a crossroads. The vision of a multi-geography platform serving global OEMs remained valid, but execution challenges mounted. India's growth couldn't indefinitely offset European decline. The technology transition to EVs required focus and investment that managing crisis consumed. Most critically, competitor actions—Chinese suppliers expanding globally, Korean companies consolidating, Japanese firms retreating to home markets—demanded strategic clarity that crisis management prevented.

The European challenges ultimately posed fundamental questions about CIE Automotive India's identity. Was it an Indian company with global operations, or a global company headquartered in India? Should it be a focused leader in specific technologies or a diversified supplier across multiple capabilities? Could it maintain premium margins while competing globally, or would commoditization prove inevitable? These questions, deferred during growth years, now demanded answers as the automotive industry's transformation accelerated and geographic disparities widened.

IX. EV Transition & Technology Disruption

The prototype lab at CIE's Pune facility tells the story of an industry in flux. On one bench sits a traditional crankshaft—2,000 years of metallurgical evolution refined to perfection, converting explosive combustion into rotational motion with 98% efficiency. Next to it lies an e-drive reducer gear—simpler in concept but demanding tolerances that make traditional forging look crude. One represents mastery of the past; the other, an uncertain future.

There are delays in order execution, particularly in electric vehicle projects, affecting the conversion of the order book into sales. These delays weren't just administrative hiccups—they reflected the industry's broader struggles with EV transition. OEMs announced bold electrification targets, then quietly pushed timelines as consumer adoption lagged projections. CIE found itself developing components for platforms that might launch in 2025, 2027, or never.

The technical challenges proved more complex than anticipated. EV powertrains operate at speeds up to 20,000 RPM, compared to 6,000 RPM for combustion engines. This meant gears faced unprecedented stress cycles, requiring new materials and heat treatment processes. The company's metallurgists worked with steel suppliers to develop alloys that maintained strength at high speeds while minimizing magnetic interference with electric motors—a consideration never relevant for traditional components.

Noise, vibration, and harshness (NVH) requirements transformed from important to critical. In combustion vehicles, engine noise masked gear whine. In EVs' near-silence, every mechanical sound became audible. CIE's engineers spent months perfecting gear tooth profiles that reduced noise below 50 decibels—quieter than normal conversation. The testing equipment alone cost ₹15 crores, measuring vibrations in nanometers and frequencies beyond human hearing.

The product portfolio transformation revealed winners and losers. Crankshafts, connecting rods, and pistons—60% of forging revenue—faced extinction in pure EVs. But reduction gears, differential assemblies, and precision shafts saw demand surge. The company's gear division, previously focused on manual transmissions, pivoted to e-drive components where gear precision directly impacted vehicle range—a key selling point for EVs.

Battery housing components emerged as an unexpected opportunity. While batteries themselves involved electrochemistry beyond CIE's expertise, the aluminum housings protecting them required sophisticated casting and machining. These components needed to be lightweight yet strong enough to protect batteries in crashes, conduct heat for thermal management, and provide electromagnetic shielding. CIE's aluminum casting expertise, acquired through AEL, positioned it well for this market.

The customer landscape shifted dramatically. Traditional OEM relationships remained important, but new entrants disrupted established hierarchies. A Chinese EV startup with no automotive heritage could specify components that established German brands would never consider. Indian companies like Ola Electric and Ather Energy brought software-industry speed to hardware development, expecting prototypes in weeks rather than months.

The investment dilemma proved particularly acute. Developing EV component capabilities required hundreds of crores in equipment, training, and certification. But with technology evolving rapidly, investments risked obsolescence before payback. The company adopted a "platform approach"—investing in flexible manufacturing systems that could adapt to changing specifications rather than dedicated lines for specific components.

Simulation capabilities became competitive differentiators. CIE's engineers used digital twins to predict how components would perform in vehicles that existed only in CAD files. Electromagnetic simulation ensured gears wouldn't interfere with motor controllers. Thermal modeling predicted heat dissipation in battery housings. Acoustic simulation identified potential noise sources before physical prototypes. This virtual development accelerated time-to-market while reducing development costs.

The supply chain required fundamental restructuring. Traditional steel suppliers struggled to meet the magnetic permeability requirements for EV components. Coating suppliers had to develop new formulations preventing electrical conductivity while maintaining corrosion resistance. Even packaging changed—components for EVs required anti-static materials to prevent damage to sensitive electronics.

Workforce transformation proved as challenging as technical evolution. Mechanical engineers who spent careers perfecting combustion-engine components had to learn electromagnetic compatibility, thermal dynamics, and high-speed mechanics. The company launched "Project Evolve"—a massive retraining initiative partnering with IITs and international universities. Senior engineers resistant to change were paired with young graduates fluent in simulation software, creating intergenerational learning teams.

The competitive landscape transformed beyond recognition. Chinese suppliers, backed by government subsidies and massive domestic EV market, offered components at prices that defied economic logic. Korean companies leveraged their battery expertise to bundle component supply with cell manufacturing. Traditional European suppliers retreated to niche premium segments. CIE found itself competing simultaneously with $100 billion multinationals and venture-funded startups.

Intellectual property became a battlefield. Every innovation in EV components triggered patent applications and potential litigation. The company quadrupled its IP budget, filing patents for everything from gear tooth profiles to heat treatment processes. Cross-licensing agreements with competitors became necessary evils, sharing technology to avoid litigation while maintaining competitive differentiation.

The business model evolution challenged fundamental assumptions. Traditional automotive contracts spanned 5-7 years with stable volumes and predictable pricing. EV contracts were shorter, volumes uncertain, and pricing under constant pressure. Some customers demanded risk-sharing agreements where component prices decreased with battery costs. Others wanted CIE to hold inventory for demand surges that might never materialize.

Government policy added complexity and opportunity. India's FAME subsidies made EVs temporarily competitive, driving demand for components. But subsidy changes could eliminate demand overnight. Europe's emissions regulations forced ICE improvements that ironically increased demand for sophisticated traditional components even as OEMs pivoted to EVs. China's dual-credit policy created artificial demand distorting global markets.

The financial metrics told a story of transition stress. EV-related revenue grew 40% annually but from a tiny base, reaching only 8% of total sales by 2024. Margins on EV components were initially negative as development costs exceeded revenue. The learning curve was steep—first-generation e-drive gears had 50% scrap rates before process optimization achieved automotive quality standards.

Management's cautious optimism reflected this reality. While publicly bullish on EV opportunities, internal discussions revealed anxiety about transition timing and competitive positioning. The board debated whether to accelerate EV investments risking stranded assets, or maintain ICE focus risking technological obsolescence. The middle path—balanced investment across technologies—satisfied no one while consuming maximum resources.

Partnerships and collaborations became essential. CIE joined consortiums developing next-generation EV technologies, sharing costs and risks with competitors. Joint development agreements with motor manufacturers ensured component compatibility. University collaborations provided access to cutting-edge research. Even customers became development partners, co-investing in technology that would differentiate their vehicles.

The hydrogen wildcard added another dimension. While battery EVs dominated headlines, hydrogen fuel cells offered alternative pathways requiring different components. CIE hedged by developing components compatible with both technologies—pressure vessels for hydrogen storage using composite expertise, heat exchangers leveraging aluminum casting capabilities.

By 2025, CIE Automotive India stood at technology crossroads. The company had successfully developed EV component capabilities, won significant contracts, and positioned itself for the transition. But execution challenges, competitive pressures, and uncertain timing meant the transition would be longer and more painful than anticipated. The next decade would determine whether CIE emerged as an EV component leader or became another casualty of the industry's greatest disruption. The only certainty was that standing still meant certain obsolescence—forward movement, however uncertain, remained the only option.

X. Playbook: Lessons in M&A and Integration

The conference room in Mumbai's Mahindra Towers has witnessed dozens of deal negotiations, but the principles written on the whiteboard have remained constant since 2013: "Technology first. Culture matters. Integration is execution. Patience pays." This deceptively simple framework guided CIE Automotive India through acquisitions totaling over ₹3,000 crores, transforming a single-technology regional player into a global multi-capability platform.

The CIE-Mahindra partnership model emerged from necessity rather than design. When CIE Automotive sought entry to India, outright acquisition would have triggered cultural antibodies. When Mahindra wanted global reach, going alone lacked technical depth. The solution—majority control with significant minority stake—aligned interests while preserving identity. Vikas Chandra Sinha, who has been with the company since its inception in 2013, was a key member on the project that led to CIE Automotive entering India by acquiring a majority stake in Mahindra & Mahindra Ltd's (M&M) auto component business.

The principle of "mutual faith and common ambition" sounds like corporate rhetoric but proved foundational. CIE brought technical expertise and global relationships but respected Mahindra's local knowledge and supplier networks. Mahindra provided market access and regulatory navigation while embracing CIE's operational disciplines. Neither party imposed their way wholesale—success came from synthesizing strengths.

Deal sourcing followed strategic logic rather than opportunistic availability. Each acquisition targeted specific capability gaps or market access. Bill Forge brought precision forging for two-wheelers. AEL added aluminum casting for lightweighting. The discipline to walk away from attractive but non-strategic assets—including a profitable stampings business that would have added complexity without synergy—demonstrated strategic clarity.

Due diligence evolved beyond financial analysis to cultural assessment. The Bill Forge evaluation spent as much time understanding family dynamics and employee relationships as analyzing machinery and contracts. Teams attended shift changes to observe worker-supervisor interactions. Engineers evaluated not just equipment capability but maintenance practices revealing organizational discipline. Customer interviews focused on relationship depth beyond contractual terms.

Valuation methodology balanced multiple perspectives. Discounted cash flow models satisfied financial analysts. Strategic value calculations justified premiums for unique capabilities. But the "integration complexity discount" often proved most accurate—deals requiring extensive restructuring rarely justified their cost, while well-run businesses needing only scale and systems delivered superior returns.

The integration approach rejected both rapid assimilation and permanent independence. Instead, a phased model emerged: stabilization (6 months), optimization (12 months), transformation (24 months). Stabilization focused on maintaining customer confidence and employee morale. Optimization captured quick wins in procurement and overhead. Transformation integrated systems and processes while preserving valuable differences.

Creating value through integration required surgical precision. Procurement synergies materialized quickly—combined steel purchases, shared logistics contracts, joint supplier negotiations. But operational integration proceeded carefully. Forcing Bill Forge's high-speed production methods onto CIE's heavy forging operations would have destroyed both. Instead, best practices were documented, adapted, and voluntarily adopted.

The human dimension often determined success. Key talent retention went beyond financial incentives to include career development and cultural respect. Bill Forge engineers were sent to European facilities not as subordinates but as experts teaching precision forging. AEL's founders became advisors, their decades of experience valued rather than dismissed. This respect for acquired company expertise reduced resistance and accelerated knowledge transfer.

System integration balanced standardization with flexibility. Financial reporting moved to CIE standards immediately—non-negotiable for public company compliance. But manufacturing execution systems remained local where they worked well. The principle: standardize what must be common, preserve what creates value. This pragmatic approach avoided the system implementation disasters that plagued many acquisitions.

Building resilience through diversification wasn't just about adding technologies—it required thoughtful portfolio construction. The combination of forgings, castings, and stampings created material flexibility. Gear machining and composite molding provided process diversity. Geographic spread across India, Europe, and Mexico reduced regional risks. Customer diversification across vehicle segments limited OEM-specific exposure. Each element reinforced others, creating resilience greater than individual components.

Capital allocation in a cyclical industry required contrarian thinking. Acquisitions happened during downturns when valuations were attractive and sellers motivated. Investments in capacity came during upturns when customer commitments were firm. This counter-cyclical approach required strong balance sheet and patient shareholders—both secured through consistent cash generation and transparent communication.

The multi-technology, multi-geography management model challenged traditional organizational structures. Instead of geographic silos, technology centers of excellence emerged. The forging expert in Pune could optimize operations in Mexico. The aluminum specialist in Germany could troubleshoot problems in India. This matrix structure complicated reporting but accelerated capability development.

Balancing autonomy with integration proved continually challenging. Too much autonomy led to sub-optimization and missed synergies. Too much integration destroyed entrepreneurial spirit and local responsiveness. The solution: central standards with local execution. Quality standards, safety protocols, and financial controls were non-negotiable. But production scheduling, supplier selection, and customer relationship management remained local.

Failed integration attempts provided valuable lessons. An early attempt to consolidate European purchasing failed when suppliers refused to serve multiple locations at single prices. A forced ERP implementation at an acquired facility caused three months of production disruption. These failures taught that integration must respect operational realities and proceed at sustainable pace.

Technology transfer mechanisms evolved through trial and error. Initial attempts at documentation and training proved insufficient. Success came through personnel rotation—engineers spending months at sister facilities, learning through immersion rather than instruction. The investment in travel and temporary productivity loss paid dividends in sustainable capability transfer.

Managing cultural differences required emotional intelligence rarely taught in business schools. German engineers' insistence on process documentation frustrated Indian colleagues who preferred flexible problem-solving. Spanish managers' long lunch breaks seemed inefficient to Indian teams working through meals. Mexican operators' family-first attitude conflicted with weekend overtime expectations. Success came from recognizing these differences as strengths to be leveraged rather than problems to be solved.

The role of advisors and intermediaries proved crucial but often overlooked. Investment bankers who understood both strategic rationale and cultural nuances added value beyond deal execution. Legal advisors who navigated regulatory complexity while maintaining business momentum earned their fees. Technical consultants who validated capabilities without destroying seller relationships enabled accurate valuation.

Communication strategies determined employee and customer confidence. Town halls where leadership explained strategic rationale reduced uncertainty. Customer visits where combined capabilities were demonstrated secured long-term contracts. Investor calls where integration milestones were transparently discussed maintained market confidence. Clear, consistent communication proved as important as operational execution.

The metrics for M&A success evolved beyond financial returns. Customer retention rates, employee satisfaction scores, and technology transfer effectiveness became key performance indicators. Deals that delivered target returns but lost key customers or talent were considered failures. This holistic view of success shaped future deal evaluation and integration planning.

By 2025, CIE Automotive India's M&A playbook had been tested across multiple deals, technologies, and geographies. The lessons—respect acquired capabilities, integrate gradually, preserve value-creating differences, communicate transparently—seemed obvious in hindsight but proved difficult in execution. The playbook's real value lay not in abstract principles but in institutional memory of what worked, what failed, and why. This accumulated wisdom, encoded in processes and embedded in culture, represented competitive advantage as valuable as any acquired technology or customer relationship.

XI. Bear vs. Bull Case Analysis

The investment case for CIE Automotive India splits seasoned analysts into two camps, each armed with compelling data supporting diametrically opposed conclusions. The bear-bull debate isn't academic—it reflects fundamental uncertainties about the automotive industry's future and CIE's position within it.

Bear Case: The Structural Headwinds

The bears begin with the obvious: The company has delivered a poor sales growth of 2.54% over past five years and maintains a low return on equity of 11.0% over last 3 years. These aren't temporary setbacks but structural realities. In an industry where technology leaders grow at 15-20% annually, CIE's anemic growth suggests market share loss or segment stagnation.

Auto industry cyclicality looms large in bearish arguments. The industry operates on 7-10 year cycles, and by most measures, we're late cycle. Global vehicle production has plateaued, inventory levels are rising, and consumer confidence is weakening. When the downturn arrives—not if, but when—component suppliers face immediate volume declines with limited pricing power. CIE's fixed cost structure means volume declines translate directly to margin compression.

The European operations experienced a 19% year-on-year sales drop due to a slowdown in all segments, impacting consolidated results. This isn't just a temporary European recession—it's structural decline. European auto production peaked in 2018 and won't recover as manufacturing shifts to Asia and Mexico. CIE's European assets, acquired at premium valuations, now generate returns below cost of capital. The restructuring costs are just beginning; true rightsizing will require write-downs and closures that management seems reluctant to acknowledge.

The EV transition represents existential risk that bulls underestimate. Yes, CIE is developing EV components, but so is everyone else. Chinese competitors with decades of electronics manufacturing experience have inherent advantages in EV components that mechanical forging expertise can't overcome. The company's EV revenue remains below 10% of total sales while ICE components face obsolescence. The transition period will be longer and more painful than management projections suggest.

Chinese competition intensifies daily. BYD, CATL, and dozens of lesser-known Chinese suppliers aren't just competing on price—they're innovating faster, investing more, and backed by government support that makes fair competition impossible. These companies are winning contracts for next-generation platforms while CIE defends legacy business. The competitive dynamics that allowed premium pricing for quality and reliability are eroding as Chinese quality improves and cost pressures intensify.

Management's capital allocation raises concerns. The dividend payout exceeding 50% of profits suggests either lack of growth opportunities or pressure from the Spanish parent to extract cash. Either interpretation is problematic. Growing companies reinvest profits; declining companies return cash. CIE seems caught between, satisfying neither growth nor value investors.

The technology investment requirements are staggering and accelerating. EV components, Industry 4.0 manufacturing, sustainability compliance—each requires hundreds of crores in investment with uncertain returns. The company's ₹400-500 crore annual capex seems insufficient for transformation while excessive for maintenance. This investment purgatory—too much for returns, too little for transformation—destroys value.

Customer concentration amplifies risks. The top five customers representing 45% of revenue creates vulnerability that diversification can't offset. Volkswagen's struggles, Stellantis' restructuring, Renault's strategic confusion—each customer crisis becomes CIE's problem. The long-term contracts that once provided stability now lock in pricing while customers demand cost reductions and volumes decline.

The valuation offers no margin of safety. At 18x P/E, the market prices CIE like a growth company despite evidence of stagnation. The EV/EBITDA multiple exceeds 8x, rich for a cyclical manufacturer. Any disappointment—a missed quarter, customer loss, restructuring announcement—could trigger multiple compression that devastates returns.

Bull Case: The Hidden Value

The bulls counter with equally compelling arguments, starting with the fortress balance sheet. Company has reduced debt. Company is almost debt free. In an industry where leveraged competitors face existential risks during downturns, CIE's financial strength provides strategic flexibility. The company can acquire distressed assets, invest counter-cyclically, or simply survive when others fail.

Promoter Holding: 65.7% signals alignment that public markets undervalue. CIE Automotive S.A. isn't a financial investor seeking quick returns—they're industry operators with multi-decade horizons. This patient capital enables long-term thinking that quarterly-focused public companies can't match. The Spanish parent's global relationships and technology access provide competitive advantages not reflected in standalone financials.

The exceptional order book of Rs. 3.5 billion represents future revenue visibility that current metrics ignore. These aren't replacement orders but new platform wins that will drive growth as they commercialize. The 18-24 month lag between order and revenue means today's bookings become tomorrow's growth. Patient investors buying at today's valuations will benefit from this revenue acceleration.

India's growth story remains intact despite near-term challenges. Vehicle penetration at 30 per 1,000 people compares to 600+ in developed markets. Rising incomes, improving infrastructure, and demographic tailwinds ensure multi-decade growth. CIE's 60% revenue exposure to India positions it perfectly for this structural growth. The 3% recent growth understates potential as semiconductor shortages and regulatory transitions create temporary headwinds.

The global platform with local presence creates competitive advantages bears overlook. When Volkswagen needs forgings for its India factory, CIE delivers locally while competitors import. When Indian OEMs expand internationally, CIE supports them globally. This unique positioning—global capability with local execution—becomes more valuable as supply chains regionalize.

The multi-technology portfolio provides resilience and optionality. While bears focus on ICE component obsolescence, they ignore growing segments. Precision gears for EV reduction drives command higher margins than traditional transmission gears. Aluminum castings for battery housings represent massive new market. Magnetics for electric motors leverage existing capabilities. The portfolio provides multiple paths to growth.

Operational improvements are bearing fruit despite revenue headwinds. Net income grew 2.8% despite revenue declining 3.4%, with profit margins expanding from 8.6% to 9.2%, driven by lower expenses. This margin expansion during volume decline demonstrates pricing power and operational excellence that bears underestimate.

The industry consolidation thesis remains compelling. Hundreds of sub-scale component suppliers face extinction as technology requirements and customer consolidation accelerate. CIE's balance sheet strength and operational excellence position it as consolidator rather than victim. Acquiring competitors at distressed valuations could double the business while improving margins through synergies.

Management quality, while difficult to quantify, differentiates CIE from peers. The team that navigated the CIE-Mahindra merger, integrated Bill Forge, and expanded into aluminum demonstrates execution capability. Their conservative guidance and consistent delivery build credibility that aggressive competitors lack. In cyclical industries, management quality matters more than growth rates.