Cholamandalam Financial Holdings: The Evolution of India's Financial Services Pioneer

I. Introduction & Episode Roadmap

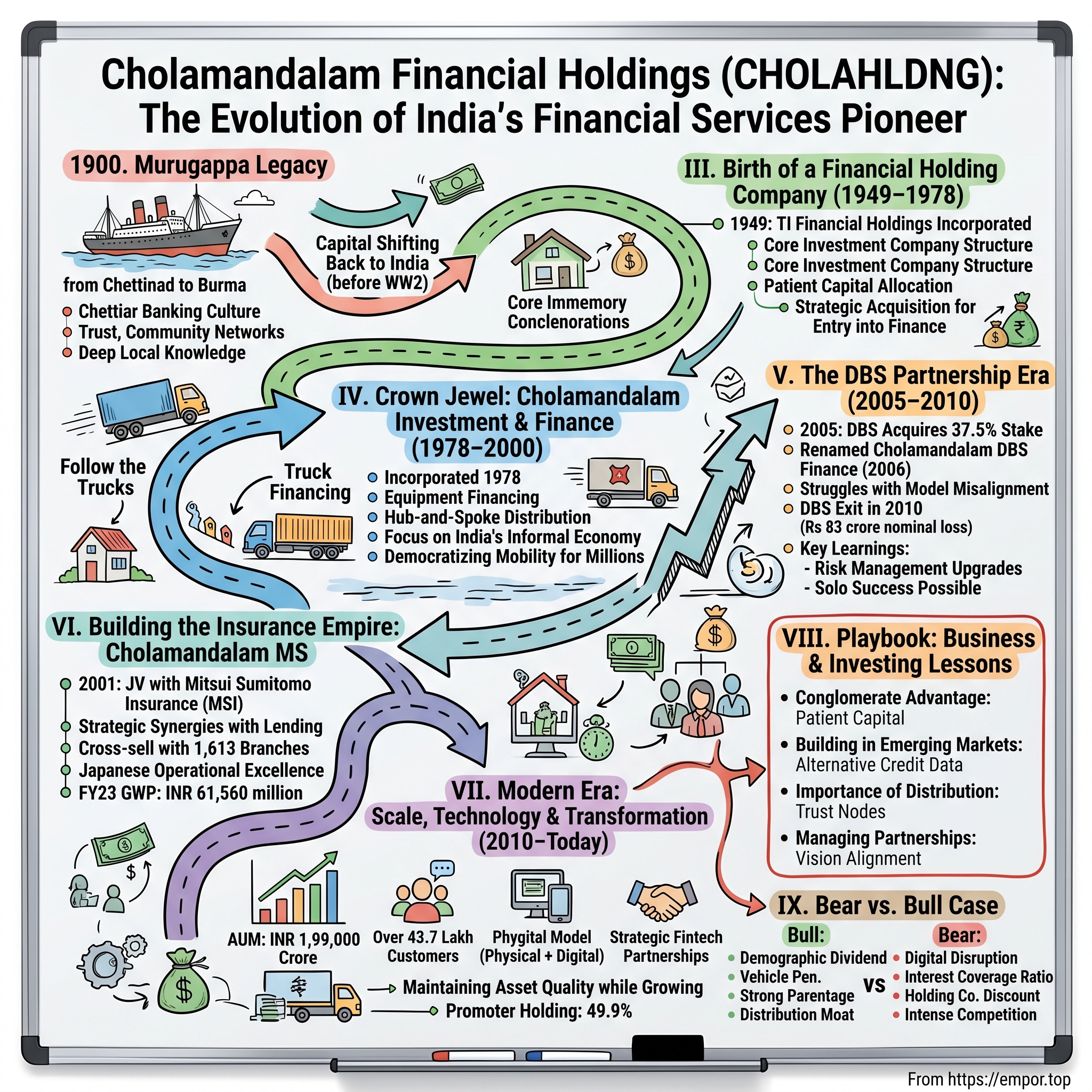

Picture this: Chennai, 1949. India has just gained independence, the economy is finding its feet, and a group of visionary businessmen from the Murugappa family are sitting in a modest office, incorporating what would become one of India's most enduring financial institutions. They called it TI Financial Holdings then—a name that would stick for seven decades before transforming into Cholamandalam Financial Holdings in 2019.

Today, this company commands a market capitalization of ₹34,820 crore, generates annual revenues of ₹34,789 crore, and delivers profits of ₹4,840 crore. But numbers only tell part of the story. The real narrative is how a post-colonial financial holding company, born from the ashes of World War II and the partition of Burma, evolved into one of India's most respected non-banking financial companies (NBFCs).

The question that drives our exploration: How did a traditional South Indian business family, whose roots trace back to colonial-era money lending, build a financial services empire that today serves over 43 lakh customers across 1,613 branches? And more intriguingly, how did they manage to maintain family control while partnering with global giants like DBS Bank and Mitsui Sumitomo?

This is a story of patience—the kind of multi-generational patience that only family-owned conglomerates seem to possess. It's about building financial services not in Mumbai's gleaming towers or Bangalore's tech parks, but in the dusty roads of rural Tamil Nadu, the busy markets of tier-2 cities, and the industrial belts where small businesses desperately need capital but banks won't venture.

We'll journey through the Murugappa legacy that began in 1900, explore the strategic pivot to financial services in 1978, dissect the fascinating DBS partnership that lasted exactly five years, and understand how this holding company structure—often viewed as inefficient by modern standards—actually became its greatest strategic advantage.

Along the way, we'll uncover lessons about building in emerging markets, managing international partnerships, and why sometimes the old ways of doing business still work in the digital age.

II. The Murugappa Legacy & Group Origins

The year was 1900. Dewan Bahadur A.M. Murugappa Chettiar, a young entrepreneur from the Chettinad region of Tamil Nadu, was boarding a steamer to Moulmein, Burma. He wasn't alone—hundreds of Chettiars were making similar journeys, carrying with them an ancient banking tradition that would reshape finance across Southeast Asia.

The Chettiars weren't just moneylenders; they were India's original investment bankers. Operating from Burma to British Malaya, Ceylon to the Dutch East Indies, and even French Indo-China, they financed everything from rice mills to rubber plantations. Their system was remarkably sophisticated: they maintained detailed palm-leaf manuscripts tracking loans, used hundis (traditional bills of exchange) that worked across borders, and built trust networks that made modern credit bureaus look primitive.

Murugappa Chettiar's genius wasn't just in lending money—it was in sensing opportunity. By the 1930s, as war clouds gathered over Asia, he made a prescient decision. While other Chettiar families stayed put, believing the British would protect their interests, Murugappa began moving assets back to India. When the Japanese invaded Burma in 1942, those who stayed lost everything. The Murugappa family's early repatriation of capital became the foundation of what is today a ₹85,000 crore (US$9.8 billion) conglomerate. The story of the Chettiar banking culture deserves more attention than it typically receives. These families operated sophisticated financial networks that stretched from Moulmein in Burma to British Malaya, Ceylon, Dutch East Indies, and French Indo-China. They weren't merely lenders but architects of regional commerce, financing everything from agricultural ventures to industrial enterprises. The prescient decision to shift assets to India before the Japanese invasion of Burma proved pivotal—while other Chettiar families lost everything, the Murugappas preserved their capital.

Today's Murugappa Group stands as a ₹85,000 crore (US$9.8 billion) conglomerate, an INR 778 billion enterprise by revenue, testament to this early foresight. The empire now encompasses 29 businesses including 10 companies listed on NSE and BSE—names like Carborundum Universal, Cholamandalam Investment and Finance, Cholamandalam MS General Insurance, Coromandel International, EID Parry, Shanthi Gears, Tube Investments of India, and Wendt India.

What's fascinating is how the Chettiar culture of relationship banking—built on trust, community networks, and deep local knowledge—still permeates Cholamandalam's modern operations. Visit any of their branches in rural Tamil Nadu today, and you'll find relationship managers who know their customers' families, businesses, and cash flows intimately. This isn't just corporate rhetoric; it's DNA inherited from a century of community banking.

The transition from colonial-era money lending to modern financial services wasn't merely evolution—it was transformation through crisis, opportunity, and remarkable prescience about India's future.

III. Birth of a Financial Holding Company (1949–1978)

The monsoons had just ended in Chennai when the Murugappa family gathered to sign the incorporation papers in 1949. India was barely two years into independence, Nehru's industrial policy was taking shape, and the family sensed opportunity in the chaos. They named it TI Financial Holdings Limited—a deliberately understated name that would remain unchanged for seven decades. The company, formally incorporated on September 9, 1949 as TI Financial Holdings Limited, was fundamentally a Core Investment Company—a structure that would define its strategy for the next seven decades. This wasn't accidental. The Murugappa family understood something crucial: in a capital-starved economy, a holding company structure would provide flexibility to deploy capital across opportunities without the constraints of operating company regulations.

The initial relationship with Tube Investments UK wasn't just about capital—it was about legitimacy. In post-independence India, foreign partnerships conferred instant credibility. The Group established TI Cycles of India Limited (present day Tube Investments of India Limited) in association with Tube Investments Limited, UK in 1949, creating what would become one of India's most successful industrial ventures.

But here's where the story gets interesting. While TI Cycles manufactured bicycles and Tube Products made steel tubes, the holding company quietly accumulated stakes in financial services ventures. The family was playing a long game—industrial businesses generated cash, but financial services would multiply it.

The 1950s and 1960s saw careful expansion. Each acquisition was strategic: companies that either generated consistent cash flows or provided entry into new sectors. The holding company structure allowed them to maintain control while bringing in partners for specific ventures. They weren't empire builders in the traditional sense—they were patient capital allocators.

By the 1970s, as India's economy lurched through the License Raj, the Murugappas made a crucial observation: while industrial licenses were hard to come by, financial services licenses were becoming available. Banks were nationalized in 1969, creating a vacuum in private sector finance. Small businesses, traders, and individuals needed credit that public sector banks couldn't or wouldn't provide.

The stage was set for their most important acquisition—one that would transform a sleepy holding company into a financial services powerhouse.

IV. Cholamandalam Investment & Finance: The Crown Jewel (1978–2000)

In 1978, while India was still recovering from the Emergency and economic stagnation gripped the nation, a small team gathered in a modest office on Mount Road, Chennai. Cholamandalam Investment and Finance Company Limited was incorporated as the financial services arm of the Murugappa Group. The name itself was a statement—Cholamandalam, derived from the Chola dynasty that once ruled South India, signaled both heritage and ambition. Cholamandalam was incorporated in 1978 as the financial services arm of the Murugappa Group. But the genius wasn't in the timing—it was in the positioning. The company commenced business as an equipment financing company, focusing on a segment that banks considered too risky and too operationally intensive.

The early strategy was brilliantly simple: follow the trucks. While banks sat in their air-conditioned offices waiting for customers, Cholamandalam's executives spent their days at transport nagars, industrial estates, and construction sites. They understood that a truck wasn't just a vehicle—it was a small business on wheels, a family's entire livelihood. A used truck buyer in Tirupur didn't need a 50-page loan application; he needed someone who understood seasonal cash flows and could structure repayments around harvest cycles.

By 1985, Cholamandalam had pioneered what would become its signature model: the hub-and-spoke distribution system. Major branches in district headquarters served as hubs, while smaller collection centers reached into rural areas. This wasn't just about physical presence—it was about building trust in communities where a handshake still meant more than a contract.

The 1990s brought liberalization and competition, but also validation. The company evolved from equipment financing into a comprehensive financial services provider offering vehicle finance, home loans, loan against property, SME loans, and various other financial services. Each new product line followed the same playbook: identify an underserved segment, build deep distribution, and create customized products.

What set Cholamandalam apart was its understanding of India's informal economy. They developed innovative credit assessment models that looked beyond traditional metrics. A vegetable vendor's daily cash collection patterns, a trucker's route profitability, a small manufacturer's order book—these became the data points for lending decisions. They were doing "alternative data" lending decades before fintech made it fashionable.

The vehicle finance revolution was particularly transformative. Cholamandalam didn't just finance vehicles; they democratized mobility for millions of Indians. A farmer could buy a tractor with just 10% down payment, a young entrepreneur could start a transport business with a single truck, families could upgrade from two-wheelers to cars. The company's tagline—"Enabling customers to enter a better life"—wasn't marketing fluff; it was lived reality for millions.

By 2000, Cholamandalam had built something remarkable: a financial services company that understood India's economic complexity better than most banks. They had cracked the code of serving the underserved profitably. But the company was about to enter its most intriguing chapter—a partnership with one of Asia's most sophisticated banks.

V. The DBS Partnership Era (2005–2010)

The boardroom at Dare House was unusually crowded in June 2005. On one side sat the Murugappa family members and senior executives; on the other, a team from DBS Bank, Singapore's largest financial institution. After months of negotiations, they were about to sign one of Indian financial services' most ambitious partnerships.DBS Bank acquired a 37.5% stake in Cholamandalam Investment and Finance Company in 2005, with the Murugappa Group lowering its stake to 37.5%. The board had approved the issue of 30 lakh equity shares to DBS at a premium of Rs 140 per share in June 2005. The company was subsequently renamed as Cholamandalam DBS Finance in 2006.

The strategic rationale was compelling on paper. DBS brought international expertise in risk management, technology, and product innovation. Cholamandalam offered deep local knowledge, extensive distribution, and understanding of India's complex credit markets. Together, they would create a financial services powerhouse combining global standards with local insights.

DBS had spent Rs 213 crore in June 2006 for its 37.5% stake—a significant investment that signaled confidence in India's growth story. DBS partnered with Cholamandalam to grow the personal finance business, asset management business and also the banking business for which it launched 10 branches. The foreign partner was expected to grow the financial services business by using its expertise in retail loans.

But partnerships between equals are always complex, especially when those equals come from different worlds. DBS executives, accustomed to Singapore's orderly markets and sophisticated credit bureaus, struggled to understand why a borrower with no credit history could be a better risk than one with a blemished record. Cholamandalam's managers, who had built their careers on relationship banking and intuitive risk assessment, found DBS's quantitative models overly rigid.

The cultural differences went deeper. DBS wanted to move upmarket, focusing on salaried professionals and urban consumers—segments with better data availability and lower operational costs. Cholamandalam's DNA was in serving small businesses, transporters, and rural customers—messier but more profitable segments. The tension wasn't about right or wrong; it was about fundamentally different visions of what the company should become.

The personal loan portfolio developed major delinquencies—a painful lesson in the dangers of applying developed market playbooks to emerging market realities. The global financial crisis of 2008 only amplified these challenges, as risk aversion gripped international banks.

By 2010, both parties recognized the inevitable. The purchase by Murugappa Group was made at INR91 per share, representing a 1.2% premium to the closing price. The transaction was completed on or before 12 April 2010. DBS said the decision to sell was in line with its strategy to grow in India by focusing on corporate clients as well as high net worth and emerging affluent segments.

The numbers told a sobering story: DBS had invested Rs 213 crore and exited at approximately Rs 130 crore—a loss of Rs 83 crore in nominal terms, not accounting for the opportunity cost. But for Cholamandalam, the partnership, despite its challenges, had been transformative. They had absorbed best practices in risk management, upgraded technology systems, and learned valuable lessons about scaling operations.

Most importantly, the Murugappa Group had demonstrated something crucial to the market: they could partner with global institutions as equals, and when necessary, they could stand alone. The exit wasn't a failure—it was a graduation.

VI. Building the Insurance Empire: Cholamandalam MS

While the DBS partnership was playing out, another strategic move was quietly taking shape. In 2001, four years before the DBS deal, Cholamandalam had entered the insurance sector through a joint venture with Mitsui Sumitomo Insurance Group of Japan. This wasn't opportunistic diversification—it was strategic brilliance. Cholamandalam MS General Insurance Company Limited was established in 2001 as a joint venture between the Murugappa Group and Mitsui Sumitomo Insurance Company Limited, Japan. Unlike the DBS partnership in lending, this collaboration had a different dynamic—the Japanese partner understood emerging markets and took a genuinely long-term view.

The strategic importance of insurance in the portfolio cannot be overstated. Insurance companies generate float—premiums collected today that won't be paid out as claims until later. This float can be invested, creating a powerful compounding machine when managed well. For a holding company with patient capital, insurance was the perfect business.

But more importantly, the synergies with the lending business were extraordinary. Cholamandalam Investment and Finance operates from 1,613 branches across India, and each branch became a potential distribution point for insurance products. A customer financing a vehicle needed insurance; a home loan borrower required property insurance. The cross-sell opportunities were enormous.

The Murugappa Group holds a 60% stake in Cholamandalam MS General Insurance, with Mitsui Sumitomo holding the remaining 40%. They also established Cholamandalam MS Risk Services Limited as a risk management joint venture where the Group holds 49.5%. This wasn't just about selling policies—it was about building a comprehensive risk management ecosystem.

In FY 2022-23, the company achieved a Gross Written Premium (GWP) of INR 61,560 million. Chola MS has 189 branches and over 30,000 intermediaries across the country. The growth has been remarkable, but what's more impressive is the quality of growth. Chola MS champions a brand philosophy called T3, which stands for Trust, Transparency, and Technology.

The Japanese influence is evident in the company's operational excellence. Claims processing times are among the best in the industry, underwriting discipline is rigorous, and customer service standards reflect Japanese attention to detail combined with Indian warmth. This cultural fusion created something unique in Indian insurance—a company that could compete with global players on efficiency while maintaining the local touch essential for success in India.

The insurance business also provided portfolio diversification. While lending is cyclical and sensitive to interest rates, insurance premiums provide steady, recurring revenue. During economic downturns when loan growth slows, insurance often performs better as people become more risk-conscious. This countercyclical nature made the holding company structure more resilient.

VII. Modern Era: Scale, Technology & Transformation (2010–Today)

The conference room was packed with analysts in Mumbai when Vellayan Subbiah, then Managing Director, stood up to present Cholamandalam's post-DBS strategy in 2010. "We're not going backward," he declared. "We're going forward—on our own terms. "What followed was one of the most impressive growth stories in Indian financial services. Chola operates from 1613 branches across India with assets under management above INR 1,99,000 Crore. Chola has a growing clientele of over 43.7 lakh happy customers across the nation. As of 2024, the company has 1,387 branches across the country and more than 54,000 employees, with the majority being in smaller towns.

The transformation wasn't just about scale—it was about reimagining what an NBFC could be in the digital age. While fintech startups were burning venture capital to acquire customers in metros, Cholamandalam was quietly building a hybrid model that combined digital efficiency with physical presence. They understood something the fintechs missed: in India, trust is built face-to-face, especially when lending to first-time borrowers.

The numbers tell a remarkable story. Total AUM: INR1,77,426 crores, up 33% year on year as of Q2 FY2025. The company's recent performance shows the strength of this model: Q1 FY26 consolidated PAT of Rs.1,260 Cr, with income of Rs.9,383 Cr.

Digital transformation at Cholamandalam wasn't about replacing branches—it was about empowering them. Field executives use tablets for instant credit decisions, customers can track loan applications on mobile apps, but the final disbursement often happens with a handshake at a local branch. This phygital model—physical plus digital—became their competitive moat.

The company also made strategic technology investments. They partnered with fintech companies for specific capabilities rather than trying to build everything in-house. Strategic partnerships with companies like BankBazaar, Kreditbee, and Paytail for the Consumer & Small Enterprises Loans (CSEL) division showed pragmatic thinking—collaborate where you're weak, compete where you're strong.

But perhaps the most impressive achievement has been maintaining asset quality while growing rapidly. Asset Quality - Stage 3 Levels: Increased to 2.83% as of September '24. GNPA: Increased to 3.78% as of September '24. While NPAs have risen slightly, they remain manageable given the customer segments served.

The holding company structure continues to provide advantages. Cholamandalam Financial Holdings maintains a Promoter Holding: 49.9% stake in CIFCL, ensuring family control while allowing public participation. This balance has enabled patient capital allocation, long-term thinking, and the ability to invest through cycles rather than chasing quarterly targets.

VIII. Playbook: Business & Investing Lessons

The Cholamandalam story offers a masterclass in building financial services in emerging markets. The lessons aren't just about finance—they're about understanding the interplay between culture, capital, and patience in building enduring businesses.

The Conglomerate Advantage: Patient Capital and Long-term Thinking

The holding company structure, often criticized by modern portfolio theorists as inefficient, proved to be Cholamandalam's greatest strength. Unlike standalone NBFCs that face constant pressure to show quarterly growth, the Murugappa Group's diversified cash flows from industrial businesses provided cushion during tough times. When the 2008 crisis hit and credit markets froze, Cholamandalam could rely on group support rather than fire-selling assets or diluting equity at distressed valuations.

This patience manifests in peculiar ways. While competitors chase the latest lending fad—personal loans one year, buy-now-pay-later the next—Cholamandalam stuck to its core competencies for decades. Vehicle finance still represents 65% of their book because they understand it better than anyone else. This isn't stubbornness; it's the confidence that comes from deep domain expertise.

Building Financial Services in Emerging Markets

The company's approach to emerging market finance deserves its own business school case study. They recognized early that formal credit scoring models developed for Western markets don't work when 80% of your customers have no credit history. Instead, they built proprietary assessment models based on cash flow patterns, community references, and asset ownership.

Consider their approach to truck financing. They don't just evaluate the borrower; they assess the route profitability, seasonal variations, and even the reliability of the truck model. Branch managers know which routes see freight rate spikes during harvest season, which trucking companies have the best payment records, and which second-hand truck dealers can be trusted. This hyperlocal intelligence, accumulated over decades, cannot be replicated by algorithms alone.

The Importance of Distribution and Local Presence

In an era obsessed with digital customer acquisition, Cholamandalam's investment in physical branches seems anachronistic. Yet their 1,613 branches aren't just collection points—they're trust nodes in a low-trust society. A farmer in rural Karnataka might download a loan app, but he'll only believe the money is real when he can walk into a branch and shake someone's hand.

The distribution strategy follows a hub-and-spoke model perfected over decades. Major branches in district headquarters handle underwriting and disbursement, while smaller collection centers maintain customer relationships. This allows them to achieve the reach of a bank with the agility of an NBFC.

Managing Partnerships and Joint Ventures

The DBS experience taught valuable lessons about international partnerships. The failure wasn't in execution—it was in vision alignment. DBS wanted to import a developed market playbook; Cholamandalam knew India needed something different. The amicable exit and subsequent solo success proved that sometimes the best partnership is knowing when to walk alone.

Contrast this with the Mitsui Sumitomo partnership in insurance, now over two decades old. The Japanese partner understood that insurance in India wasn't just about risk transfer—it was about providing security in a society where social safety nets are weak. This philosophical alignment, more than capital or technology, made the partnership work.

Capital Allocation in a Holding Company Structure

The holding company's capital allocation decisions reveal sophisticated thinking. They maintain high stakes in operating companies (45.41% in CIFCL, 60% in Cholamandalam MS General Insurance) to ensure control while leaving room for external investors. This structure allows them to raise growth capital at the operating company level without diluting holding company ownership.

The pyramid structure—family → holding company → operating companies—might seem complex, but it serves multiple purposes: tax efficiency, regulatory compliance (different businesses have different regulatory requirements), and flexibility in capital raising. Each level of the structure serves a specific purpose, optimized over decades of experience.

IX. Analysis & Bear vs. Bull Case

Bull Case: The Demographic Dividend Play

The optimists see Cholamandalam as perfectly positioned for India's next growth phase. With credit penetration at just 35% of GDP compared to 150%+ in developed markets, the runway for growth seems infinite. The company's presence in semi-urban and rural markets—where 65% of India's population resides but formal credit penetration is below 20%—provides massive untapped opportunity.

The vehicle finance business alone has enormous potential. India has 22 vehicles per 1,000 people compared to 850 in the US. As infrastructure improves and incomes rise, vehicle ownership will explode. Cholamandalam's 40+ year relationships with automobile manufacturers and dealers give them pole position in this race.

The insurance business provides additional optionality. Insurance penetration in India is 4% of GDP versus a global average of 7%. As awareness grows and regulations mandate insurance coverage, Cholamandalam MS is positioned to capture disproportionate share. The synergies with the lending business—every vehicle financed needs insurance—create a powerful flywheel effect.

Strong parentage cannot be understated. The Murugappa Group's century-old reputation opens doors that remain closed to standalone players. In a market where trust is currency, this reputational capital is invaluable. The group's AAA rating and banking relationships ensure access to low-cost funding even during credit crunches.

The distribution moat appears unassailable. Building 1,600+ branches took four decades and billions in investment. Fintech competitors might offer better apps, but they can't replicate the trust and relationships built over generations. In rural India, where a branch manager might have financed three generations of the same family, switching costs are emotional, not just financial.

Bear Case: The Disruption Thesis

Skeptics worry that Cholamandalam is fighting yesterday's war. Digital-first lenders like Bajaj Finance have shown that you can build massive loan books without extensive branch networks. As smartphone penetration crosses 60% and digital payments become ubiquitous, the value of physical distribution diminishes daily.

The low interest coverage ratio raises red flags. While manageable now, any spike in funding costs or credit losses could pressure profitability. NBFCs face structural disadvantages versus banks—higher funding costs, no CASA deposits, limited access to RBI's liquidity window. These disadvantages amplify during crises.

The holding company discount is real and persistent. Cholamandalam Financial Holdings trades at a 30-40% discount to its sum-of-parts value. This discount reflects genuine concerns: opacity in capital allocation, potential for value-destructive related party transactions, and the complexity that makes the structure difficult for investors to analyze.

Competition is intensifying from unexpected quarters. Banks, flush with deposits post-demonetization, are aggressively entering vehicle finance and SME lending. Fintech players backed by billions in venture capital are willing to lose money for years to gain market share. Even manufacturers like Bajaj and TVS are expanding their captive finance arms.

Regulatory risks loom large. The RBI has been tightening NBFC regulations, increasing capital requirements, and restricting certain lending practices. Any major regulatory change could disproportionately impact NBFCs versus banks. The recent warnings about excessive growth and increasing NPAs suggest regulatory scrutiny is intensifying.

The quality of growth raises questions. We have moderated our disbursement growth to 13% for the quarter, reflecting a conscious decision to align with regulatory expectations and internal discussions. This moderation will continue as base effects wear off. This forced moderation suggests the company might be growing faster than its risk management capabilities.

X. Epilogue & "If We Were CEOs"

Standing at the crossroads of tradition and transformation, Cholamandalam faces choices that will define its next century. If we were sitting in the CEO's chair at Dare House, looking out at Chennai's bustling streets, what strategic priorities would guide us?

Digital vs Physical Distribution Balance

The temptation to go fully digital must be resisted. The future isn't digital or physical—it's both, seamlessly integrated. We'd invest in making branches smarter, not fewer. Imagine branches that use AI to predict which customers will visit, what they'll need, and pre-approve loans before they walk in. The branch of 2030 should feel like visiting an Apple Store—high-tech, high-touch, and highly efficient.

We'd also create a "Chola Stack"—an open API platform that allows partners to embed Cholamandalam's lending capabilities into their applications. Why compete with every fintech when you can power them all? Let others handle customer acquisition while we focus on what we do best: risk assessment and capital deployment.

Potential New Business Lines

The logical expansion isn't into new products but deeper into existing ecosystems. Vehicle finance naturally extends into fleet management, logistics financing, and mobility-as-a-service. Why just finance trucks when you can finance entire logistics operations?

In insurance, the opportunity lies in parametric products—insurance that pays out automatically based on predefined triggers. Imagine crop insurance that pays out immediately when rainfall drops below threshold, or business interruption insurance triggered by mobility data. These products would leverage Cholamandalam's data advantage while serving underserved segments.

Supply chain financing represents enormous potential. Every SME customer has suppliers and buyers who need credit. By financing entire supply chains rather than individual companies, Cholamandalam could create sticky ecosystems while reducing risk through diversification.

Capital Allocation Between Subsidiaries

The holding company structure needs modernization without losing its advantages. We'd create an internal venture capital fund, allowing subsidiaries to invest in startups that could disrupt them. Better to cannibalize yourself than let others do it.

The insurance business deserves more capital. While lending faces increasing competition, insurance offers better returns on capital with less competition. We'd explore taking Cholamandalam MS public separately, crystallizing value while maintaining control.

Most importantly, we'd establish clear capital allocation metrics visible to all stakeholders. Each subsidiary would have defined return hurdles, growth targets, and capital budgets. Transparency would reduce the holding company discount while maintaining strategic flexibility.

Final Reflections and Biggest Surprises

The biggest surprise in studying Cholamandalam isn't what changed—it's what didn't. In an era of blitzscaling and growth-at-all-costs, here's a company that grew methodically for 75 years. While startups celebrate customer acquisition, Cholamandalam celebrates customer retention—some families have been customers for three generations.

The DBS partnership failure, initially seen as a setback, emerges as a defining moment. It proved that Indian financial services require Indian solutions. The confidence to chart an independent path after the partnership ended marked Cholamandalam's coming of age.

Perhaps most surprising is how a company founded in 1949, named after a medieval dynasty, managed by a family conglomerate, has remained relevant in 2025. In a world obsessed with disruption, Cholamandalam proves that sometimes the most radical thing you can do is stay the course.

The story of Cholamandalam isn't just about finance—it's about how businesses adapt across generations while maintaining their core identity. It's about the patient accumulation of advantages that compound over decades. It's about understanding that in emerging markets, trust is the ultimate currency, and trust, unlike technology, cannot be acquired—it must be earned, one customer, one village, one generation at a time.

As India stands on the cusp of potentially explosive growth, Cholamandalam's next chapter is being written. Whether it becomes a case study in successful adaptation or institutional inertia remains to be seen. But one thing is certain: any company that survived the journey from colonial Burma to digital India has resilience coded in its DNA.

The Murugappa family motto—"Progress through righteousness"—might sound quaint in an era of unicorns and decacorns. But for long-term fundamental investors, there's something deeply reassuring about a company that measures success not in quarters or years, but in generations.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube