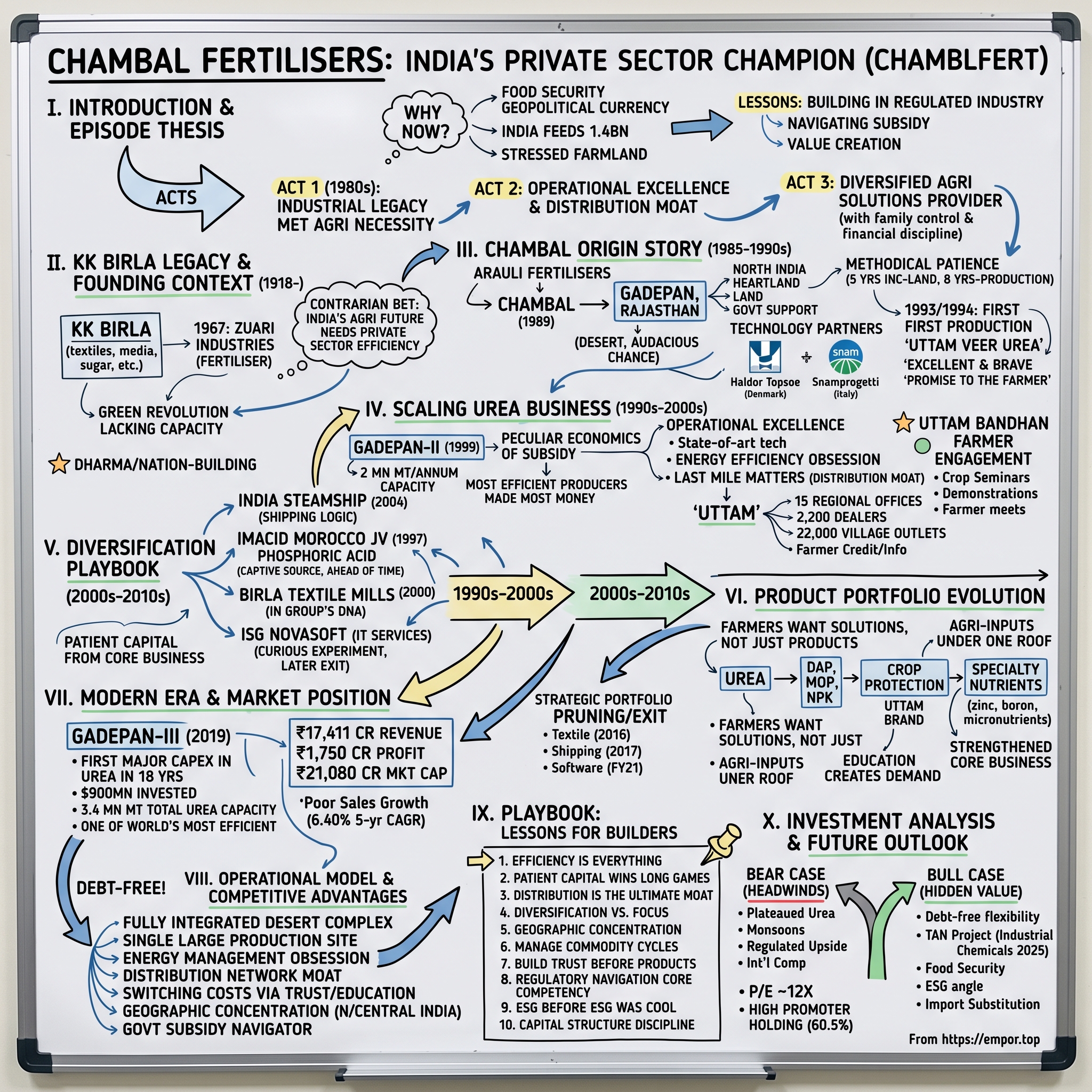

Chambal Fertilisers: India's Private Sector Fertilizer Champion

I. Introduction & Episode Thesis

Picture this: It's 1985, and while India's public sector fertilizer giants sprawl across the landscape with government backing and unlimited capital, a private player decides to enter the ring. Not just any player—but the KK Birla Group, armed with industrial heritage and a contrarian bet that India's agricultural future needed private sector efficiency. Today, that bet has materialized into Chambal Fertilisers and Chemicals Limited, a ₹21,000+ crore market cap behemoth that commands the title of India's largest private sector urea manufacturer with 1.5 million tonnes of annual capacity.

The central question isn't just how they did it—it's why this story matters now more than ever. In an era where food security has become geopolitical currency and where India feeds 1.4 billion people on increasingly stressed farmland, Chambal's journey from late entrant to market leader reveals profound lessons about building in regulated industries, navigating government subsidy frameworks, and creating value where others see only constraints.

This is a story of three distinct acts: First, how industrial legacy met agricultural necessity in the 1980s. Second, how operational excellence and distribution moats trump first-mover advantages. And third, how a commodity business transformed itself into a diversified agricultural solutions provider while maintaining family control and financial discipline. Along the way, we'll decode the playbook for building billion-dollar businesses in sectors where the government sets your prices, subsidizes your customers, and your product literally determines whether a nation eats or starves.

What makes Chambal particularly fascinating is its timing—entering fertilizers when the easy money had already been made, yet somehow emerging as the private sector champion. It's a masterclass in patient capital deployment, regulatory navigation, and the often-underappreciated art of being second.

II. The KK Birla Legacy & Founding Context

The year is 1918, and Ghanshyam Das Birla—already a legend in Indian business circles—welcomes his son Krishna Kumar into a family that would define Indian capitalism for the next century. But young KK, as he would come to be known, wasn't content merely inheriting wealth. He wanted to build industries that would feed, clothe, and employ a newly independent India.

By the 1960s, Dr. Krishna Kumar Birla had already established himself as more than just "GD Birla's son." His empire sprawled across textiles, media (The Hindustan Times), sugar, shipping, and engineering. But it was in 1967, two years after India's first Prime Minister Nehru's death and in the thick of India's food crisis, that KK Birla made his most prescient move—entering the fertilizer business through Zuari Industries. The context is crucial. The Group under his leadership made foray into Fertiliser Business in 1967 through Zuari Industries Limited, Goa, at a time when fertilizer sector was pre-dominantly controlled by Public Sector. This wasn't just any business decision—it was a direct challenge to the socialist planning model that dominated Nehru's India. The government controlled everything from steel to airlines, and fertilizers were considered too strategic to leave to private enterprise.

But KK Birla saw what others missed. India's Green Revolution, launched in 1965 under Prime Minister Lal Bahadur Shastri and continued by Indira Gandhi, desperately needed fertilizer capacity. The public sector companies—National Fertilizers Limited, Fertilizer Corporation of India—were bureaucratic behemoths, slow to expand and slower to innovate. Meanwhile, India's population was exploding, agricultural yields were stagnant, and the country was one bad monsoon away from famine.

He was born in Pilani (Rajasthan) to the legendary Late Shri G. D. Birla on November 11, 1918 – the holy day of Gopasthmi. He inherited a legacy in which the creation of wealth, philanthropy and political leadership were all regarded as part of nation-building. This wasn't just business—it was dharma, duty to the nation.

By the early 1980s, KK Birla had proven the private sector could deliver in fertilizers through Zuari. But he wanted something bigger, something that would outlast him. Enter Chambal Fertilisers and Chemicals Limited in 1985—not in the industrialized corridors of Gujarat or Tamil Nadu, but in the desert state of Rajasthan, his ancestral homeland. It was audacious, almost foolhardy. But as we'll see, sometimes the best opportunities lie where others fear to tread.

III. The Chambal Origin Story (1985-1990s)

The Chambal River flows through central India, notorious for its ravines that once harbored dacoits and outlaws. In 1985, KK Birla chose to name his newest venture after this untamed waterway—perhaps a metaphor for the challenge ahead. Chambal was promoted by Zuari Industries Limited (ZIL) and its two hi- tech nitrogenous Fertiliser Plants- Gadepan-I and Gadepan-II are located at Gadepan, Rajasthan, India. The location choice—Gadepan, 35 kilometers from Kota in Rajasthan—was either brilliant or insane. Here was a desert state with no natural gas pipelines, limited water resources, and far from major ports. But KK Birla saw what others didn't: proximity to the agricultural heartland of North India, availability of land at reasonable prices, and most importantly, a state government eager to industrialize.

In 1985, Aravali Fertilisers Limited was incorporated, renamed Chambal Fertilisers and Chemicals Limited in 1989. Land acquisition was completed at Gadepan (Kota) Rajasthan in 1990. The timeline reveals the methodical patience—five years from incorporation to land acquisition, eight years to first production. This wasn't a startup sprint; it was a marathon.

The technology partnerships were crucial. The Gadepan-I Ammonia Plant was designed by Haldor Topsoe (Denmark) and the Urea plant is based on Snamprogetti (Italy) Technology. The Ammonia Plant has a capability to produce 1,770 MT of Ammonia per day and the Urea plant has the capability to produce 3,100 MT of Urea per day. These weren't second-tier technology providers—Haldor Topsoe was the gold standard in ammonia synthesis, while Snamprogetti brought Italian engineering excellence to urea production.

The first plant was commissioned in October 1993 and started commercial production on 1st January 1994. The second plant was commissioned and started commercial production in 1999. The company went public in 1993, timing the IPO perfectly with the commissioning of the first plant—a masterclass in capital market execution.

But here's what made Chambal different from the start: the brand. In 1994, the company's flagship product was branded as 'Uttam Veer Urea'—"Uttam" meaning excellent, "Veer" meaning brave. This wasn't just fertilizer; it was a promise to the farmer, wrapped in cultural resonance.

The early years weren't without challenges. Building in the desert meant everything had to be imported or transported over long distances. Water had to be sourced and conserved meticulously. The workforce had to be attracted to what was essentially a greenfield location. The Herculean task of the greening the township area started even before the construction of the urea plants. Green avenues with rows of trees, rolling lawns and water bodies are now an integral part of the township.

By the late 1990s, Chambal had proven the model worked. The Gadepan complex wasn't just producing fertilizer; it was producing it efficiently, at scale, with quality that matched international standards. The stage was set for the next phase—massive expansion that would make Chambal not just a player, but the private sector champion.

IV. Scaling the Urea Business (1990s-2000s)

The turn of the millennium found Chambal at an inflection point. One plant was running, but to achieve real scale—to matter in a market dominated by government giants—they needed to double down. The second plant at Gadepan, commissioned in 1999, wasn't just an expansion; it was a statement of intent. With the two plants operational, Chambal's production capacity reached 2 million MT of urea per annum. But the real genius wasn't just in building capacity—it was in understanding the peculiar economics of Indian fertilizer subsidy.

Here's how the game worked: The government controlled urea prices to keep them affordable for farmers, but compensated manufacturers through a complex subsidy mechanism. The trick was to be efficient enough that your production cost stayed below the government's reimbursement rate. Every rupee saved in production was a rupee earned in profit. This created a perverse incentive structure where the most efficient producers made the most money, not necessarily those with the best products or customer relationships.

Chambal cracked this code through operational excellence. The plants used state-of-the-art technology from Denmark, Italy, United States and Japan. Energy efficiency became an obsession—in a business where natural gas accounts for 70-80% of production costs, even a 1% improvement in energy consumption could mean crores in additional profit.

But technology alone doesn't win markets. By 2000, Chambal had built a vast marketing network comprising 15 regional offices, 2,200 dealers and 22,000 village level outlets across 11 states. This wasn't just distribution—it was creating a moat. In fertilizers, the last mile matters. A farmer in rural Madhya Pradesh doesn't care about your Copenhagen technology; he cares whether your dealer will give him credit until harvest and whether your product reaches his village before sowing season.

The company launched "Uttam Bandhan" programme in 2000—a farmer engagement initiative that went beyond selling fertilizer. Under this programme, the company organizes crop seminars, product and field demonstrations and farmer meets. They launched "Chambal ki Chitthi" in 1997 with an initial print run of 20,000 copies—a farmer newsletter that became a trusted source of agricultural information. The website www.uttamkrishi.com launched in 2000, provided information on weather, suitable cropping techniques and markets in Hindi.

Competition during this period was intense but peculiar. Public sector giants like National Fertilizers Limited (NFL) and Rashtriya Chemicals and Fertilizers (RCF) had government backing but suffered from bureaucratic inefficiencies. Other private players like Coromandel International and FACT were regional powers but lacked Chambal's scale. The real competition wasn't for market share—in a supply-constrained market, everything sold. It was for operational efficiency and government favor.

By 2005, Chambal had achieved something remarkable: It had become the largest private sector urea manufacturer while maintaining operational metrics that matched global standards. The company was certified ISO 14001:2004 by Det Norske Veritas in 2000, OSHAS 18001:2007 in 2005, and ISO 9001:2008 in 2008. These weren't just certificates to hang on the wall—they represented a culture of continuous improvement that would become critical in the next phase.

V. The Diversification Playbook (2000s-2010s)

The year 2004 marked a curious pivot. While Chambal was printing money from urea, management made a bewildering decision: acquire India Steamship Company Limited, one of India's oldest shipping companies. On paper, this made no sense. What did a fertilizer company know about operating Aframax tankers on international waters? But dig deeper, and the logic emerges. In 2004, Chambal decided to enter the energy transportation sector and acquired India Steamship Company Limited, one of India's oldest shipping companies. India Steamship, founded in 1929, is one of the nation's oldest shipping lines. This wasn't just any shipping company—it was a storied name with heritage, albeit one that had seen better days.

The real insight was this: fertilizer imports require massive shipping capacity. India imports phosphatic fertilizers, potash, and increasingly, even urea when domestic production falls short. By owning ships, Chambal could hedge against freight rate volatility and potentially capture value in the supply chain. Today, India Steamship has a fleet capacity of over 4,00,000 DWT in the form of four Aframax tankers.

But the crown jewel of diversification came earlier, in 1997—a move so ahead of its time that it deserves special mention. Chambal also setup a Joint Venture – Indo Maroc Phosphore, SA in Morocco for manufacture of Phosphoric Acid way back in 1997 when overseas investment by Indian Companies was a rare phenomenon. Think about this: In 1997, when most Indian companies were still figuring out liberalization at home, Chambal was setting up manufacturing in Morocco.

The Morocco joint venture, IMACID (Indo Maroc Phosphore), was formed with OCP of Morocco and later Tata Chemicals joined as an equal partner. Phosphoric Acid is an important raw material in the manufacture of Phosphatic fertilisers. This vital ingredient is in short supply in India. With the country being the largest importer of Phosphoric Acid, there was a clear need to secure captive sources of this chemical.

Meanwhile, closer to home, Birla Textile Mills (BTM) was established in year 2000 as a division of Chambal. In less then a decade, BTM has emerged as leading name for textiles in India. The Baddi facility with 83,000 spindle capacity might seem random, but it made sense in the KK Birla ecosystem—textiles were in the group's DNA, and Chambal had the balance sheet to fund expansion.

The software business experiment was perhaps the most curious. Through subsidiaries like ISG Novasoft Technologies, Chambal entered IT services. The company was also engaged in Software business, However, in FY21, it sold assets and transferred certain liabilities of the business to cease the operations of the software business. This was the peak of India's IT boom, and every conglomerate wanted a piece of the action. For Chambal, it didn't work out, but the attempt showed management's willingness to experiment beyond traditional boundaries.

What's remarkable about this diversification phase is how it was financed. The fertilizer business, with its government-guaranteed returns, generated steady cash flows. This patient capital could be deployed in longer-gestation businesses like shipping or overseas ventures. It's the classic conglomerate playbook—use a stable, regulated business to fund growth experiments.

By 2010, Chambal wasn't just a fertilizer company anymore. It was a mini-conglomerate with interests spanning continents and industries. But as we'll see, not all diversifications are created equal, and the next decade would force some hard choices.

VI. Product Portfolio Evolution

Walk into any agricultural input dealer in North India circa 2010, and you'd notice something interesting. The Uttam brand wasn't just on urea bags anymore. It was on DAP, MOP, NPK fertilizers, pesticides, fungicides, herbicides—an entire arsenal of agricultural inputs under one trusted name.

Company is engaged in manufacturing Urea. It is also engaged in marketing of other fertilisers such as Di-Ammonium Phosphate ("DAP"), Muriate of Potash ("MOP"), NPK fertilisers, Speciality Plant Nutrients and Crop Protection Chemicals. Through JV it is engaged in the manufacture of phosphoric acid in Morocco.

This wasn't accidental. Chambal had recognized a fundamental truth about Indian agriculture: farmers don't think in products, they think in solutions. A farmer dealing with pest attack doesn't care whether you're a fertilizer company or a pesticide company—he wants something that works, from someone he trusts.

The expansion into crop protection chemicals was particularly strategic. Unlike fertilizers, where prices are controlled and margins are thin, crop protection offered better margins and less regulatory oversight. Chambal's established distribution network—those 22,000 village outlets—became the highway for these new products.

CFCL offers agri-inputs to farmers under one roof, thus, in addition to manufacturing urea, the Company markets other fertilisers and agri-inputs such as Di-Ammonium Phosphate (DAP), Muriate of Potash (MOP), Ammonium Phosphate Sulphate (APS), different grades of NPK fertilisers, Crop Protection Chemicals (CPC) and Speciality Nutrients (SN).

The specialty nutrients business deserves special attention. As Indian agriculture modernized, farmers began to understand that yield wasn't just about NPK (Nitrogen, Phosphorus, Potassium). Micronutrients—zinc, boron, molybdenum—could make the difference between an average harvest and a bumper crop. Chambal positioned itself at the forefront of this education, using its farmer engagement programs to create demand while simultaneously fulfilling it.

But here's what's brilliant about the strategy: every new product strengthened the core urea business. A dealer stocking Uttam urea was more likely to stock Uttam DAP. A farmer trusting Uttam for fertilizers would try Uttam pesticides. Digital media intervention and increasing awareness among the farmers about the importance of balanced nutrition in soil has resulted in growth of the CPC & SN business.

The company also recognized that different crops needed different solutions. Rice farmers in Punjab had different needs from cotton farmers in Gujarat or sugarcane growers in Maharashtra. Chambal developed targeted product portfolios for different crop-geography combinations, moving from a product-push to a solution-pull model.

Technology partnerships became crucial. For specialty products, Chambal tied up with global leaders, bringing international formulations to Indian fields. These weren't just trading arrangements—they involved technology transfer, local trials, and farmer education.

CPC & SN continued their growth momentum despite adverse market conditions and reduction in prices. The focused approach on marketing of CPC & SN by way of expansion of product basket, deeper penetration, farmer connect and demand generation have enabled the Company to achieve good performance in sales of these products.

By 2015, Chambal had transformed from a urea manufacturer to an agricultural solutions provider. The numbers tell the story: while urea remained the volume driver, the margins increasingly came from the value-added products. It's a playbook many have tried to copy, but few have executed as well. The key was patience—building trust over decades, then leveraging that trust to expand the relationship.

VII. Modern Era & Market Position (2015-Present)

January 2019 marked a watershed moment. After an 18-year hiatus in India's urea capacity additions, Chambal commissioned Gadepan-III, adding 1.34 million MT to its capacity. The three plants have an installed annual production capacity of about 3.4 million MT of Urea contributing to major chunk of Urea consumed in leading agri states in India. These plants were commissioned in 1994, 1999 and 2019 respectively. The timing was perfect and terrible simultaneously. No new urea production capacity came on stream in the country during last 18 years except revamp of few existing plants. This is the first major capex in Urea in 18 years. The government's New Investment Policy 2012 finally created incentives for capacity addition, but it came with a catch—the policy was only effective for 8 years from commencement.

The latest one, Gadepan III is one of the most efficient plants in the world, producing 1.34 million MT urea per annum and Gadepan is the only site in the country with the single largest production of urea at one place. The plant featured remarkable engineering—The Gadepan III Urea plant prill tower is the highest in world with total height of 141.5 meter.

The $900 million investment was a massive bet. The new Urea plant will increase the present Urea production capacity of the Company by about 1.34 million MT per annum. But the financials tell a different story from the triumphant capacity expansion narrative. Current financials reveal ₹17,411 crore revenue, ₹1,750 crore profit, and a market cap of ₹21,080 crore. The growth story, however, is more complex—the company has delivered a poor sales growth of 6.40% over past five years. Despite the capacity expansion triumph, the stock's journey has been volatile, though the 52 week high and low of Chambal Fertilisers & Chemicals Ltd is ₹333.4 and ₹742.2, indicating significant price swings.

The most significant development of the modern era is financial transformation. Company has reduced debt. Company is almost debt free. This is remarkable for a company that just invested $900 million in capacity expansion. The deleveraging story is as important as the growth story—it represents a fundamental shift from the leveraged conglomerate model to a focused, financially disciplined enterprise.

Meanwhile, strategic portfolio pruning continued. In fiscal 2016, Chambal had transferred its textile division to Sutlej Textiles and Industries Ltd on slump sale basis. During September 2017, Chambal sold off its all four remaining ships, thus exiting the shipping business. The company was also engaged in Software business, However, in FY21, it sold assets and transferred certain liabilities of the business to cease the operations of the software business.

Looking forward, Chambal isn't resting on its laurels. India's Chambal Fertilisers is building a greenfield 240,000 tonne/year technical ammonium nitrate (TAN) plant at its Gadepan complex in the northwestern Rajasthan state. The company plans to set up the TAN plant as well as a 210,000 tonne/year weak nitric acid (WNA) line at an estimated cost of Indian rupees (Rs) 16.45bn ($201m). The plants are expected to commence operations by October 2025.

The TAN project represents a strategic pivot into industrial chemicals, moving beyond agricultural applications. Technical ammonium nitrate is crucial for mining and infrastructure—sectors expected to boom as India builds out its infrastructure. It's a calculated bet on India's next growth phase.

VIII. Operating Model & Competitive Advantages

Stand at the gates of the Gadepan complex today, and you're looking at something unique in Indian industry—a fully integrated chemical complex in the middle of a desert, operating at global efficiency standards. The latest one, Gadepan III is one of the most efficient plants in the world, producing 1.34 million MT urea per annum and Gadepan is the only site in the country with the single largest production of urea at one place.

The operational excellence starts with energy management. In urea production, natural gas accounts for 70-80% of production costs. Every percentage point of efficiency improvement translates to crores in savings. Chambal's plants consistently operate at above 90% capacity utilization—remarkable in an industry where 75% is considered good.

But the real moat isn't the hardware—it's the distribution network built over three decades. The Company has a vast marketing network comprising 19 regional offices, 2800 dealers and 50,000 retailers. Think about what this means: in every tehsil, every major village across North India, there's someone who knows the Uttam brand, trusts it, and recommends it to farmers.

The farmer engagement model is particularly sophisticated. Under this programme, the company organizes crop seminars, product and field demonstrations and farmer meets. Soil and water analysis is also conducted for free at Chambal's laboratories and based on the results; Chambal experts emphasize on balance use of fertilisers. To encourage the new age farmer, a website, 'uttamkrishi.com', provides information on the weather, suitable cropping techniques and markets in Hindi language. 'Hello Uttam' toll-free telephonic helplines have been set up to answer the queries raised by farmers. Unemployed youth from villages are enrolled as 'Uttam Krishi Salhakars'. They are trained in the latest farming techniques and provide specialised services to farmers.

This isn't corporate social responsibility theater—it's building switching costs through trust and education. A farmer who's received free soil testing, attended Chambal's crop seminars, and relies on Hello Uttam for advice isn't just buying fertilizer; he's buying into an ecosystem.

The geographic focus strategy deserves attention. While competitors spread themselves thin trying to be pan-India, Chambal dominates specific regions. It caters to the needs of the farmers in approximately 10 states in northern, eastern, central and western regions of India and is the fertilizer supplier in the state of Rajasthan, Madhya Pradesh, Punjab and Haryana. In these markets, Chambal isn't just another fertilizer company—it's the fertilizer company.

Cost advantages come from multiple sources. Single-location manufacturing at Gadepan creates economies of scale. Backward integration into ammonia production provides raw material security. The Morocco JV for phosphoric acid hedges against import price volatility. Even the abandoned shipping venture wasn't a complete waste—it provided insights into global commodity flows that inform procurement strategies today.

The quality certifications tell their own story. The company has won the Sword of Honour from the British Safety Council for two consecutive years. It has been awarded ISO 14001 (Environment Management System Standard), ISO 9001 (Quality Management System Standard) and OHSAS 18001 (Occupational Health and Safety Management System Standard). In a commodity business, these differentiators matter—they signal operational discipline that translates to reliability.

Working with government subsidy frameworks requires a special skill. The government sets your selling price, determines your subsidy, and often delays payments. The company's capital structure, is constrained by large working capital borrowings following delay in subsidy disbursement by the government. Yet Chambal has mastered this game, maintaining profitability despite the constraints.

The corporate social responsibility isn't just good citizenship—it's strategic moat-building. The Company won the coveted Golden Peacock Award for Corporate Social Responsibility in the year 2009-10. In rural India, reputation matters. Being seen as a company that gives back to the community creates goodwill that no amount of advertising can buy.

IX. Playbook: Lessons for Builders

After four decades of navigating India's most regulated industry, Chambal's journey offers a masterclass in building within constraints. Here are the key lessons:

Lesson 1: In Regulated Industries, Efficiency Is Everything When the government controls your prices, the only lever for profitability is cost. Chambal's obsession with operational efficiency—from energy optimization to logistics management—shows how to thrive when pricing power doesn't exist. Every small improvement compounds over decades.

Lesson 2: Patient Capital Wins Long Games The 8-year gap between company formation (1985) and first production (1993), then another 26 years before the next major expansion (2019), reveals the power of patient capital. Family-controlled businesses can take views that quarterly-earnings-obsessed companies cannot. The KK Birla Group's ability to wait, to time the market, to strike when policy windows open—this is the conglomerate advantage in action.

Lesson 3: Distribution Is The Ultimate Moat Technology can be licensed, plants can be built, but distribution networks take decades to construct. Chambal's 50,000 retail touchpoints aren't just sales channels—they're relationships, trust networks, information gathering systems. In businesses selling to millions of small customers, distribution is destiny.

Lesson 4: Diversification vs. Focus—Know When to Pivot The 2000s diversification into shipping, textiles, and software, followed by the 2010s retreat to core fertilizers, offers a nuanced lesson. Diversification works when you have excess capital and management bandwidth. But when the core business needs investment (like Gadepan-III), focus becomes paramount. Knowing when to expand and when to contract is crucial.

Lesson 5: Geographic Concentration Can Beat National Presence Chambal chose to dominate North and Central India rather than spreading thin nationally. This concentration creates density advantages—in distribution, brand recall, and operational efficiency. Sometimes, being the big fish in selected ponds beats being a small fish in the ocean.

Lesson 6: Manage Commodity Cycles Through Integration Vertical integration into ammonia, the Morocco phosphoric acid JV, even the failed shipping venture—all represent attempts to control more of the value chain. In commodity businesses, controlling your input costs can be the difference between profit and loss during down cycles.

Lesson 7: Build Trust Before Products The Uttam Bandhan program, soil testing labs, farmer education initiatives—Chambal understood that in rural markets, trust precedes transactions. Investing in farmer education when you're selling to them might seem like a conflict of interest, but it creates loyalty that transcends price competition.

Lesson 8: Regulatory Navigation Is A Core Competency Operating in India's fertilizer sector means dealing with price controls, subsidy delays, import restrictions, and constantly changing policies. Companies that treat regulatory management as a necessary evil fail; those that make it a core competency thrive. Chambal's ability to remain profitable despite regulatory headwinds shows mastery of this art.

Lesson 9: ESG Before ESG Was Cool The Golden Peacock Award in 2009-10, the sustainable farming initiatives, the Uttam Nagar township—Chambal was doing ESG before it became a buzzword. In industries with environmental and social externalities, getting ahead of the curve on sustainability creates both defensive moats and offensive advantages.

Lesson 10: Capital Structure Discipline Matters Eventually The journey from leveraged conglomerate to near-debt-free focused player shows that capital structure isn't just about finance—it's about flexibility. Being debt-free when the next opportunity or crisis arrives is a massive strategic advantage.

X. Investment Analysis & Future Outlook

The investment case for Chambal presents a fascinating paradox: a company operating in one of India's most essential industries, with dominant market position and pristine balance sheet, yet trading at modest valuations and delivering pedestrian growth. Let's unpack this puzzle.

The Bear Case: Structural Headwinds The 6.4% five-year sales CAGR tells a sobering story. Urea consumption in India has plateaued as the government pushes nutrient-based subsidy schemes and promotes balanced fertilization. Climate change makes monsoons more erratic, affecting fertilizer demand unpredictably. The shift to direct benefit transfer (DBT) has made subsidy payments more transparent but also more complex.

The regulated nature of the business caps upside. When urea prices are controlled and subsidy rates are determined by bureaucrats, there's limited scope for pricing power or margin expansion. You're essentially running a utility with commodity risk.

International competition looms large. If India decides to liberalize fertilizer imports further or if global urea prices crash, Chambal's economics could deteriorate rapidly. The company is betting against trade liberalization—historically, not a winning bet in India.

The Bull Case: Hidden Value and Optionality But the bear case misses crucial nuances. First, the debt-free balance sheet provides enormous flexibility. In a rising rate environment, having zero financial leverage while competitors struggle with debt service is a massive advantage.

The TAN project opening in 2025 represents a pivot to industrial chemicals—higher margin, less regulated, growing market. If successful, this could be the beginning of Chambal 3.0: moving beyond agricultural inputs into industrial intermediates.

India's food security needs aren't going away. With 1.4 billion people to feed and limited arable land, fertilizer demand might plateau but won't collapse. Chambal's position as the largest private player gives it influence over policy that smaller players lack.

The ESG angle is underappreciated. As global investors focus on sustainable agriculture and food security, Chambal's role in enabling India's food production could attract ESG-focused capital. The company's track record on safety, environmental management, and farmer welfare positions it well for this trend.

Import substitution remains a powerful theme. India imports significant quantities of fertilizers and raw materials. Every geopolitical shock—whether Russia-Ukraine war or Red Sea shipping disruptions—reinforces the value of domestic production capacity.

Technology Disruption: Threat or Opportunity? Precision farming, nano-fertilizers, and biologicals represent both threats and opportunities. These technologies could reduce traditional fertilizer consumption, but they also open new product categories. Chambal's distribution network and farmer relationships position it well to distribute new-age agricultural inputs, regardless of who manufactures them.

The company's vast farmer database and engagement programs could be monetized through digital agriculture platforms, crop insurance distribution, or agricultural fintech products. The "Hello Uttam" helpline and website are primitive versions of what could become a comprehensive agtech platform.

The China +1 Opportunity Global fertilizer supply chains are reconsidering their China dependence. India, with its large domestic market and established manufacturing base, could become an alternative hub. Chambal's proven execution capabilities and financial strength position it to capture this opportunity through capacity expansion or contract manufacturing.

Valuation Perspective At ₹21,000 crore market cap for a company generating ₹1,750 crore in profits, we're looking at a P/E of 12x—modest for a market leader with pristine balance sheet. The 60.5% promoter holding provides stability but limits float, potentially suppressing valuations.

The key question: Is this a value trap or a hidden gem? The answer depends on your view of India's agricultural future, the pace of technology disruption, and the government's policy trajectory.

Forward-Looking Indicators to Watch

- Government's fertilizer subsidy allocation in annual budgets

- Progress on the TAN project and entry into industrial chemicals

- Global natural gas prices and their impact on production economics

- Policy changes around fertilizer pricing and import regulations

- Adoption rates of new agricultural technologies in core markets

- Success in value-added products (specialty nutrients, crop protection)

The investment case ultimately rests on whether you believe Chambal can transform from a regulated commodity producer into a diversified agricultural solutions provider while maintaining its operational excellence and financial discipline. The pieces are in place—execution will determine outcomes.

XI. Conclusion: The Chambal Paradox

Chambal Fertilisers presents a paradox that encapsulates broader truths about Indian business. Here's a company that succeeded not by disrupting or innovating, but by executing brilliantly within constraints. It built a ₹21,000 crore enterprise in an industry where the government sets prices, delays payments, and changes rules arbitrarily.

The journey from 1985 to today reveals that in India, patience pays, relationships matter, and operational excellence trumps financial engineering. Chambal didn't try to be everything to everyone—it chose to be essential to some. In focusing on North Indian farmers, mastering the subsidy game, and building trust over decades, it created a moat that no amount of capital can quickly replicate.

Yet the future remains uncertain. Can a company built for the India of subsidies and controls thrive in the India of digitization and markets? Can operational excellence in traditional manufacturing translate to success in new-age agriculture? These questions don't have easy answers.

What's clear is that Chambal represents a specific type of Indian success story—not the flashy unicorn or software services exporter, but the steady, industrial enterprise that feeds the nation. In a world obsessed with disruption, there's something reassuring about a company that just makes fertilizer really, really well.

For investors, Chambal offers a choice: bet on the exciting but uncertain future of agtech and precision agriculture, or invest in the boring but essential business of feeding 1.4 billion people. In typical Indian fashion, Chambal is trying to do both. Whether it succeeds will determine if this fertilizer giant can write its next chapter as brilliantly as it wrote its first.

The Chambal River, after which the company is named, flows through some of India's most fertile lands, nurturing crops that feed millions. Like its namesake, Chambal Fertilisers has been a quiet force of nourishment, enabling abundance where scarcity once reigned. In that sense, perhaps the company has already achieved something more valuable than market capitalization—it has earned its place in India's agricultural history.

As we look ahead, Chambal's story reminds us that in business, as in farming, success comes not from chasing every opportunity but from cultivating the right ones with patience, discipline, and deep roots in the soil you serve.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube