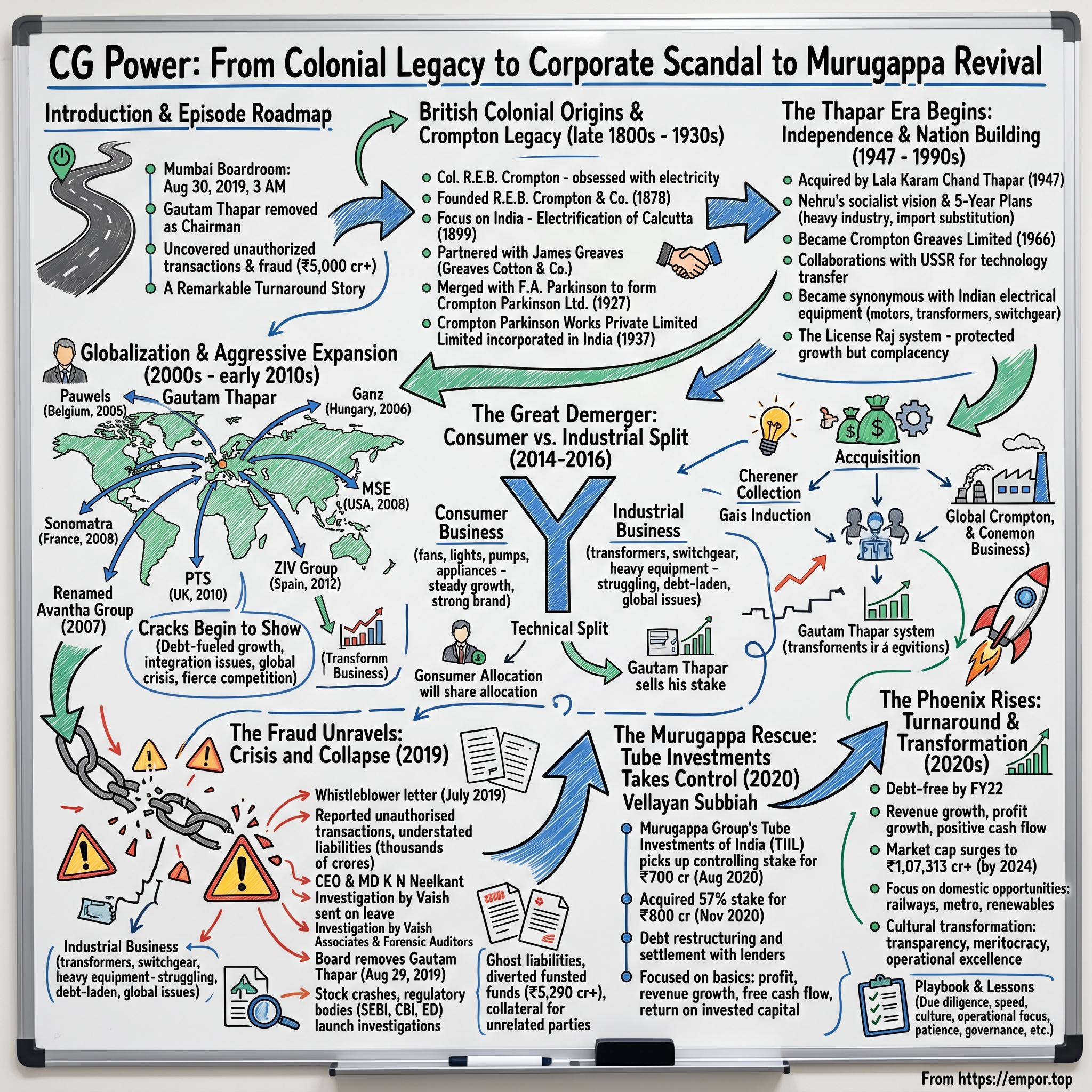

CG Power: From Colonial Legacy to Corporate Scandal to Murugappa Revival

Introduction & Episode Roadmap

The boardroom at CG Power's Mumbai headquarters fell silent at 3:00 AM on August 30, 2019. After hours of heated deliberation, the directors had just voted to remove Gautam Thapar—the man whose family had controlled the company for seven decades—as chairman. Outside, the monsoon rain pounded against the windows, a fitting soundtrack to the end of an era. What the board had uncovered in the preceding weeks would shock India's corporate establishment: a web of unauthorized transactions, fictitious sales, and diverted funds totaling over ₹5,000 crore.

This is the story of CG Power and Industrial Solutions—a company that began in the gaslit workshops of Victorian England, helped electrify independent India, expanded globally with imperial ambitions, collapsed in spectacular fraud, and then rose from the ashes under new ownership to become one of the most remarkable turnaround stories in Indian corporate history.

Today, CG Power stands as a ₹1,07,313 crore market cap powerhouse, generating ₹10,559 crore in revenue and ₹999 crore in profit. But these numbers only hint at the dramatic journey—one that mirrors India's own evolution from colonial outpost to industrial power, complete with all the triumphs, excesses, and painful reckonings along the way.

How does an 87-year-old electrical giant go from being a crown jewel of Indian industry to a cautionary tale of corporate malfeasance, only to emerge stronger under entirely new management? The answer lies in understanding not just business strategy but the interplay of ambition, governance, and the peculiar dynamics of Indian capitalism. This is a story about technology transfer and nation-building, about the perils of debt-fueled growth, about how good companies can go catastrophically wrong, and ultimately, about redemption through operational excellence.

The British Colonial Origins & Crompton Legacy

Colonel Rookes Evelyn Bell Crompton was not your typical Victorian entrepreneur. A military engineer who had served in the Crimean War, Crompton returned to England in 1875 with an obsession: electricity. While gas lamps still illuminated London's streets and candles flickered in most homes, Crompton saw a different future. In a converted stable in Chelmsford, Essex, he began tinkering with arc lamps and dynamos, convinced that electric light would transform civilization.

By 1878, Crompton had founded R.E.B. Crompton & Company, initially focusing on importing and distributing electrical equipment. But Crompton was no mere trader—he was an innovator. His company pioneered the development of DC generators and was among the first to light public spaces electrically in Britain. When the Vienna Opera House needed electric lighting in 1883, they called Crompton. When the King of Burma wanted to illuminate his palace in Mandalay, Crompton's engineers made the journey east. It was India that would prove to be Crompton's most consequential market. In 1896 the Indian government invited him back to assist in the preparation of electric lighting legislation and he was heavily involved in the electrification of Calcutta and many other places. The connection was more than commercial—Crompton had served in India as a young officer and understood the subcontinent's vast potential. In 1899, a Crompton dynamo produced the first unit of electricity generated in Calcutta.

The British empire needed a local partner to manage this growing Indian business, and they found one in James Greaves, who had established Greaves Cotton and Company in 1859. Greaves Cotton and Company, established by James Greaves in 1859, was appointed as their concessionaire in India. This arrangement worked well until 1927, when corporate consolidation fever swept through the British electrical industry. The company was merged with F.A. Parkinson in 1927 to form Crompton Parkinson Ltd.

The newly formed Crompton Parkinson Limited didn't waste time establishing its Indian presence. The company was incorporated on 28 April 1937 as Crompton Parkinson Work Private Limited. This wasn't just another colonial trading post—it was a full-fledged manufacturing operation, bringing industrial-scale electrical production to the subcontinent. The timing was prescient. Within a decade, India would be independent, and the new nation would need every kilowatt of power it could generate.

The Bombay factory that opened in 1937 was more than a manufacturing facility; it was a statement of intent. While other British companies treated India as a market for finished goods, Crompton Parkinson was transferring technology, training engineers, and building an industrial ecosystem. They produced switchgear for Bombay's textile mills, motors for Delhi's water pumps, and transformers for the railways that bound the vast country together.

The company's early Indian engineers tell stories of British foremen who insisted on precision to the thousandth of an inch, of testing protocols that seemed excessive for a "colonial market," and of a culture that refused to compromise on quality even when cheaper alternatives would have sufficed. This obsession with engineering excellence would become part of the company's DNA—a trait that would serve it well through the tumultuous decades ahead.

By 1947, as the Union Jack was lowered for the last time at the Red Fort, Crompton Parkinson Works had become indispensable to India's electrical infrastructure. The question was: what would happen to this very British company in a newly independent India that was eager to shed its colonial past?

The Thapar Era Begins: Independence & Nation Building

Lala Karam Chand Thapar stood at the gates of the Crompton Parkinson factory in Bombay on a humid August morning in 1947. Independence had come just days earlier, and the British managers were packing their bags, uncertain about their future in Nehru's India. Thapar, a Punjabi industrialist who had built his fortune in paper and sugar mills, saw opportunity where others saw chaos. "The British are leaving," he told his son, "but electricity is staying."

In 1947, it was acquired by Karam Chand Thapar of Thapar Group. The acquisition wasn't just a business transaction—it was a bet on India's industrial future. Thapar understood that newly independent India would need massive amounts of electrical equipment for its ambitious development plans. Dams were being planned, factories were being built, and cities were expanding. Every project needed transformers, switchgear, and motors.

The early years under Thapar ownership coincided with Nehru's socialist vision for India. The government's Five-Year Plans emphasized heavy industry and import substitution. Foreign companies were restricted, imports were controlled, and Indian manufacturers were protected. For Crompton Greaves—as the company would soon be known—this was a golden cage. Competition was limited, but so was access to foreign technology and capital.

The company went public in 1960 and changed its name to Crompton Greaves Limited in 1966. The public listing was strategic—it gave the Thapars access to capital while maintaining control, and it positioned the company as a truly Indian enterprise at a time when economic nationalism was at its peak.

But the most fascinating chapter of this era was Crompton Greaves' unlikely partnership with the Soviet Union. The company in Cold War era collaborated with the USSR and the Eastern Bloc for technology transfer of new electrical technologies. While American and European companies were restricted by Cold War politics and India's non-aligned stance, the Soviets were eager to share technology with the world's largest democracy. Russian engineers arrived in Bombay to transfer designs for high-voltage equipment. Indian engineers traveled to Moscow and Leningrad to learn about power generation systems that could withstand extreme conditions.

The collaboration produced some remarkable innovations. The company developed transformers that could handle India's notoriously unstable grid conditions. They created motors that could function in temperatures ranging from the freezing Himalayas to the scorching Rajasthan desert. The Soviet connection also gave Crompton Greaves access to markets in Eastern Europe and Central Asia that Western companies couldn't touch.

By the 1970s, Crompton Greaves had become synonymous with Indian electrical equipment. Their motors powered the pumps that irrigated the Green Revolution. Their transformers stepped down power from the massive Bhakra Nangal Dam. Their switchgear protected the steel plants of Bhilai and Rourkela. The company's advertisements from this era show proud Indian workers standing next to massive transformers with the tagline: "Powering the Nation's Progress."

The License Raj system, for all its inefficiencies, created a protected environment where Crompton Greaves could grow steadily without facing serious competition. The company expanded from its Bombay base to establish factories in Nashik, Goa, and Ahmednagar. Each facility specialized in different products, creating an integrated manufacturing ecosystem that could produce everything from tiny fractional horsepower motors to massive power transformers.

But protection bred complacency. While Japanese and Korean companies were revolutionizing manufacturing with lean production and quality circles, Crompton Greaves operated much as it had in the 1960s. Labor relations were fraught—strikes were common, and productivity lagged behind global standards. The company's engineers were excellent, but its management systems were outdated.

The 1980s brought the first hints of change. Rajiv Gandhi's government began loosening some controls, allowing limited technology imports and joint ventures. Crompton Greaves responded by establishing partnerships with companies like Hitachi and Siemens for specific product lines. But these were tentative steps, constrained by regulations and the Thapar family's reluctance to dilute control.

As the 1990s dawned and India stood on the brink of economic liberalization, Crompton Greaves faced a critical question: Could a company that had thrived in a protected market survive and grow in a globalized economy? The answer would depend on the next generation of leadership—specifically, on a young man named Gautam Thapar, who had very different ideas about what Crompton Greaves could become.

Globalization & Aggressive Expansion

Gautam Thapar landed at Brussels Airport in May 2005 with a team of investment bankers and a audacious plan. The 45-year-old scion of the Thapar family had taken control of Crompton Greaves just a few years earlier, and he was determined to transform the steady but stodgy Indian manufacturer into a global electrical equipment powerhouse. His target: Pauwels Group, a 90-year-old Belgian transformer manufacturer with operations across four continents. Its overseas acquisitions began in 2005 with Crompton Greaves taking over Belgium-based power transformer maker Pauwels. The Pauwels acquisition wasn't just another deal—it was a statement of intent. For ₹180 crore, Crompton Greaves gained not just factories in Belgium, Ireland, USA, Canada, and Indonesia, but also access to cutting-edge transformer technology and, crucially, a global customer base that included utilities in Europe and North America.

The negotiations in Brussels stretched for weeks. Pauwels' management was skeptical—what did an Indian company know about serving sophisticated European utilities? Gautam Thapar, who became the Chairman of Crompton Greaves on 22 July 2004, personally led the discussions, bringing in McKinsey consultants and international lawyers to structure a deal that would preserve Pauwels' operational independence while integrating it into Crompton Greaves' global vision.

Today, he is the undisputed head of the US$3 billion group, which he renamed Avantha in 2007. The Avantha name itself was carefully chosen: 'Avan' comes from the French 'avant,' meaning forward, vanguard, advancing; and the Sanskrit 'stha' stands for stability. The rebranding signaled a break from the conservative Thapar past and an embrace of aggressive global expansion.

The Pauwels deal opened the floodgates. This was followed with a series of successful acquisitions - Ganz, Hungary in 2006; Microsol, Ireland in 2007; Sonomatra, France; MSE, USA in 2008 and PTS, UK in 2010. Each acquisition had its own strategic logic. Ganz brought expertise in extra high-voltage transformers crucial for long-distance power transmission. Microsol provided switchgear technology for renewable energy applications. Sonomatra added capabilities in specialized transformers for the rail sector. MSE gave access to the North American utility market.

The acquisition spree was breathtaking in its ambition. Between 2005 and 2010, Crompton Greaves spent over ₹2,000 crore on acquisitions, transforming from an India-centric manufacturer to a company with manufacturing facilities across four continents. CG, claims Thapar, is one of the country's most globalised companies, with half of its assets and more than 50 per cent of sales coming from abroad.

But this wasn't just financial engineering. Gautam Thapar had a vision of creating an integrated global electrical equipment powerhouse that could compete with ABB, Siemens, and General Electric. He spoke of achieving revenues of $8 billion by 2015—a target that would require growing at over 30% annually.

The strategy seemed to be working. Crompton Greaves could now offer end-to-end solutions for power projects anywhere in the world. A utility in Canada could buy transformers made in Belgium, switchgear from Ireland, and get them serviced by engineers from India. The company won major contracts in Europe, Africa, and the Americas. Its engineers worked on prestigious projects like the London Underground upgradation and power infrastructure for the Beijing Olympics.

Yet beneath the surface, cracks were beginning to show. Each acquisition came with its own culture, systems, and legacy issues. The Hungarian operations struggled with outdated factories and militant unions. The Belgian business faced intense competition from Chinese manufacturers. Integration proved far more difficult than anticipated. IT systems didn't talk to each other. Manufacturing standards varied wildly. European engineers resisted taking direction from Mumbai.

More fundamentally, the acquisitions were funded primarily through debt. By 2010, Crompton Greaves' debt had ballooned to over ₹3,000 crore. The company was betting that rapid growth and synergies would generate enough cash to service this debt. But the 2008 financial crisis changed everything. Orders dried up, working capital requirements spiked, and suddenly the debt burden looked unsustainable.

Gautam Thapar's response was characteristic—double down. He continued acquiring, adding three businesses from Nelco India in 2011, Emotron Sweden in 2011, and ZIV Group Spain in 2012. The logic was that scale would eventually deliver profitability. But the global electrical equipment industry was entering a period of overcapacity and intense price competition. Chinese manufacturers, backed by state funding, were undercutting prices by 30-40%.

By 2013, the strain was showing. Crompton Greaves reported its first loss in decades. International operations were bleeding cash. The stock price, which had touched ₹400 in 2007, crashed to below ₹100. Investors began asking uncomfortable questions about the sustainability of the global expansion strategy. Something had to give.

The Great Demerger: Consumer vs. Industrial Split

The boardroom at Crompton Greaves' Worli headquarters was unusually quiet on a July morning in 2014. Gautam Thapar had just finished presenting what he called "Project Gemini"—a radical restructuring that would split the 77-year-old company in two. On one side would be the consumer business: fans, lights, pumps, and appliances that adorned millions of Indian homes. On the other, the industrial business: transformers, switchgear, and heavy electrical equipment that powered factories and cities. In July 2014, Crompton Greaves Limited announced plans to demerge the company in order to separate its consumer goods business from the power and industrial systems segment. The decision wasn't made lightly. The two businesses had fundamentally different dynamics, customer bases, and capital requirements. The consumer business was growing steadily, with strong brand recognition and predictable cash flows. The industrial business, weighed down by global acquisitions and debt, was struggling with overcapacity and intense competition.

"The demerger will achieve the objective of creation of two industry leading independent entities and unlocking shareholder value," announced Laurent Demortier, the CEO Gautam Thapar had brought in to execute the split. The Board believes that such a demerger will create better growth opportunities for its two large but significantly different businesses - power, industrial and automation which is a B2B business, and the consumer products business which is B2C.

The mechanics of the split were complex. The shareholders holding one equity share of Crompton Greaves on the record date will receive one equity share of Crompton Greaves Consumer Electricals. But behind this simple 1:1 ratio lay months of negotiations, valuations, and strategic decisions. Which assets would go where? How would the debt be allocated? Who would keep the Crompton name that had such strong brand value?

The consumer business had always been the crown jewel. Crompton fans whirred in millions of Indian homes. Their pumps irrigated countless farms. Their lights illuminated everything from wedding halls to corner shops. This was a business with 70% market share in certain categories, operating in a growing domestic market with rising disposable incomes. Private equity firms circled like hawks.

Meanwhile, the industrial business told a different story. The ambitious global expansion had created a sprawling, difficult-to-manage empire. The Belgian transformer business was losing money. The Hungarian operations needed massive capital investment. Integration costs had spiraled out of control. Worse, the global market for power equipment had entered a severe downturn, with Chinese competitors offering products at prices that barely covered material costs.

The demerger was completed in 2016 with the listing of Crompton Greaves Consumer Electricals Limited (CGCEL) and Gautam Thapar selling his 34% stake in CGCEL to Advent International and Temasek Holdings for ₹ 2,000 crore. The sale was revealing. Here was Gautam Thapar, the man who had spent a decade building a global electrical empire, essentially admitting defeat by selling the profitable consumer business to fund the struggling industrial operations.

The market reaction was brutal but telling. Shares of Crompton Greaves tanked by over 70% as the company de-merged its consumer business from Tuesday. The shares of Crompton fell Rs 110.20, or 71.10% at Rs.44.80. While this reflected the technical adjustment for the demerger, it also showed what investors really thought: the value was in the consumer business, not the debt-laden industrial operations.

For employees, the demerger created two distinct cultures. The consumer business, now free from the industrial division's problems, could focus on innovation and marketing. They launched anti-dust fans and antibacterial LED lamps, expanded distribution, and increased advertising spend. From 2015 to 2020, CGCEL has moved beyond its traditional imagery to a contemporary and innovative organisation. After the demerger in 2015, Crompton followed a five-dimensional strategy, which according to Mathew helped the brand to not only perform well, but become one of the leading companies in the immensely competitive electricals industry.

The industrial business, meanwhile, faced a grimmer reality. In January 2017, Crompton Greaves changed its name from Crompton Greaves Limited to CG Power and Industrial Solutions Limited. The name change was symbolic—dropping the historic Crompton name that the consumer business retained, signaling a break from the past. But changing the name wouldn't change the fundamental challenges.

CG Power, as it was now known, embarked on a painful restructuring. International businesses were sold to First Reserve International for €115 million—a fraction of what had been paid to acquire them. Factories were shuttered. Thousands of employees were let go. The company that had once dreamed of competing with ABB and Siemens was now fighting for survival.

Yet even as CG Power struggled to restructure, a more sinister problem was brewing beneath the surface. The demerger had separated the businesses, but it hadn't addressed the fundamental governance issues that had allowed such reckless expansion in the first place. The complex web of related-party transactions, the aggressive accounting, the culture of saying yes to the promoter's every whim—all of this remained. And soon, it would all come crashing down in a scandal that would shock corporate India.

The Fraud Unravels: Crisis and Collapse

The anonymous letter arrived at the Securities and Exchange Board of India's headquarters in Mumbai on a humid July morning in 2019. Three pages, single-spaced, detailing transactions that didn't add up, sales that seemed fictitious, and money that had mysteriously disappeared. The whistleblower claimed to be a senior finance executive at CG Power who could no longer stay silent. By the time SEBI investigators finished their preliminary review, they knew they were looking at something explosive. In August 2019, CG Power and Industrial Solutions reported that its employees had carried out unauthorised transactions resulting in an "understatement of the company's liabilities" by thousands of crores in the previous financial year. The carefully worded statement masked an explosive reality. What the board had discovered was far worse than mere accounting errors.

The unraveling began innocuously. In March 2019, the Board of Directors of CG Power constituted Operations Committee ("Ops Committee") with aim of improving stakeholders' value. However, while working on one of its priority tasks of seeking refinancing, of certain facilities and as part of conducting financial analysis, the Ops Committee was made aware of some unauthorised transactions. A simple refinancing exercise had opened a Pandora's box.

The Operations Committee's discovery was like pulling a thread on a sweater—the more they pulled, the more it unraveled. In a separate case, CG Power's managing director received a request from a bank to replace a cheque whose validity was about to expire. And here, too, the operations committee could not track the said liability in the company's financials. Ghost liabilities were floating around that didn't appear in any books.

By May 2019, the situation had become untenable. As a result of this, on 10th May 2019 the CEO and Managing Directors K N Neelkant, sent on leave by board to enable proper investigation into financial irregularities. The board hired Vaish Associates, a law firm, to conduct an independent investigation. What they found would shock even seasoned corporate watchers.

The company in August disclosed the findings of its risk and audit committee (RAC), which revealed that the firm and the group together could have under-reported liabilities to the extent of over Rs 3,600 crore in the financial years 2017 and 2018. As per the company, they also understated the loans advanced to related and unrelated parties to the tune of about Rs 7,600 crore during the two financial years.

The numbers were staggering, but the methods were even more disturbing. The industrial land of the company in Nashik and Kanjurmarg was purportedly provided as collateral for enabling unrelated parties to get loans without due authorisation. The Aditya Birla Finance gave a loan of Rs 150 crore to Blue Garden Estates Ltd on May 12, 2015, which had an advance of the same amount to CG Power and Industrial Solutions on the same day. In the next six days, CG Power and Industrial Solutions Ltd advanced Rs 145 crore to Avantha Holdings of Thapar, which then advanced Rs 150 crore to BILT Graphics (a group company of CG Power) between May 13 to May 30, 2016.

The forensic auditors called these "colorable transactions"—deals that appeared legitimate on paper but were designed to move money out of CG Power into Gautam Thapar's other struggling companies. The complaint said the forensic audit suspected the diversion of Rs 5,290 crore of company funds.

The board meeting on August 29, 2019, began at 2 PM and stretched deep into the night. Directors who had served for years listened in disbelief as the full extent of the fraud was laid out. Some had suspected something was wrong but had been assured by management that all was well. Others were completely blindsided. By the time the meeting ended at 3 AM on August 30, they had made their decision.

Late last month, the board of CG Power and Industrial Solutions removed its founder Gautam Thapar as chairman following an investigation unearthing a multi-crore financial fraud in the company. The man whose family had controlled the company for 72 years was unceremoniously removed. The board also fired CFO V.R. Venkatesh and other senior executives implicated in the fraud.

The market reaction was swift and brutal. The company's stock crashed close to 20 per cent to Rs 14.80 soon after the revelations. From a peak of over ₹200, the stock eventually fell to below ₹10, wiping out thousands of crores in market value. Small investors who had trusted the Thapar name saw their life savings evaporate.

SEBI moved quickly. Gautam Thapar, V. R. Venkatesh, Madhav Acharya and B. Hariharan are restrained from accessing the securities market and are further prohibited from buying, selling or otherwise dealing in securities in any manner whatsoever, either directly or indirectly, till further orders. The regulator's order detailed how Thapar along with the other noticees had perpetrated several irregularities, ranging from using CG Power's assets as collateral to help third parties bag loans without due authorisation from the board of directors to "inappropriate netting-off the liabilities with the receivables from different entities". Furthermore, they allegedly used different accounting heads to conceal payments made by CG Power and entered into dubious transactions aimed at reducing the liability of the promoter-affiliated companies towards CG Power.

The CBI and Enforcement Directorate launched their own investigations. Besides Thapar, the CBI has also booked CG Power and Industrial Solutions, erstwhile Crompton Greaves Ltd, and the then executives, including chief executive officer and managing director K N Neelkanth, executive director and chief financial officer (CFO) Madhav Acharya, director B Hariharan, non-executive director Omkar Goswami and CFO Venkatesh Rammoorthy. "It was alleged that the said accused had cheated SBI and other consortium member banks, including Bank of Maharashtra, Axis bank, Yes Bank, Corporation Bank, Barclays Bank, IndusInd Bank etc..."

KKR, which had invested ₹562 crore in CG Power in 2015, found itself in a precarious position. Their board nominee had apparently been kept in the dark about the fraudulent transactions. The private equity giant now faced the prospect of a total write-off of its investment. They began exploring legal options, including invoking drag-along rights to force a sale of the company.

Banks were in an even worse position. With loans of over ₹2,400 crore outstanding, they faced massive write-offs. The company's factories still functioned, orders were still being executed, but without working capital and with its reputation in tatters, CG Power was essentially a zombie—alive but unable to function normally.

By late 2019, CG Power had become a cautionary tale of everything wrong with Indian corporate governance. A company with an 82-year legacy, built by generations of engineers and workers, had been brought to its knees by financial engineering and fraud. The question now was whether anything could be salvaged from the wreckage.

The Murugappa Rescue: Tube Investments Takes Control

Vellayan Subbiah sat in his corner office at Tube Investments' Chennai headquarters, studying the CG Power financials for the third time that October morning in 2020. His CFO had just walked him through the numbers again, and they were sobering: ₹2,400 crore in debt, negative net worth, factories operating at 40% capacity, and a reputation so damaged that customers were actively seeking alternative suppliers. "Everyone thinks we're crazy," his CFO said. Vellayan smiled. "That's exactly why this might work. "The Murugappa Group was an unlikely savior. One of South India's oldest business houses, founded in 1900, they were known for their conservative approach, strong governance, and aversion to controversy. Their businesses—from bicycles to sugar, fertilizers to financial services—were built on steady growth rather than spectacular deals. Yet here was Vellayan, the fourth-generation Murugappa Group scion, seriously considering acquiring India's most scandal-tainted company.

Murugappa Group's Tube Investments of India taking control of the company, in a Rs 700-crore deal agreed to on Friday. The announcement on August 7, 2020, sent shockwaves through the market. Murugappa group's engineering firm Tube Investments of India Ltd (TIIL) is picking up a controlling stake in the fraud-hit CG Power & Industrial Solutions for a consideration of Rs700 crore. As per a regulatory filing by CG Power (erstwhile Crompton Greaves, the electrical equipment maker), TIIL will be issued 64.25 crore shares at Rs8.56 apiece aggregating to Rs550 crore. Besides, the Murugappa group company will also invest Rs150 crore in the company (that counts private equity firm KKR as a minority investor) over the next 18 months in the form of buying warrants that can be converted into equity shares.

The price—₹8.56 per share—seemed almost insulting for a company that had once traded above ₹200. But for existing shareholders watching their holdings evaporate, it was a lifeline. CG Power has gained 27 per cent while TII shares are up 15.8 per cent since the announcement as the Street sees it as a win-win deal for the two companies. CG Power gets a stronger parent, while TII gets a larger business and growth opportunity, albeit with its share of risk.

What the market didn't know was the intense due diligence that preceded the deal. Vellayan had dispatched teams of engineers, accountants, and lawyers to every CG Power facility. They interviewed customers, suppliers, and employees. They examined every contract, every liability, every piece of machinery. But the IIT Madras alumnus admits the decision to acquire the company "wasn't so scientific or so well thought through." Instinctively, it felt like a very good company.

The real challenge wasn't the acquisition—it was the restructuring that followed. CG Power and Murugappa Group firm Tube Investments of India Ltd, said lenders have accepted one-time settlement and restructuring of debt. Now, CG Power, TIIL and the lenders have "executed the requisite binding agreements dated November 20, 2020 for one-time settlement and restructuring of funded facilities and guaranteed debt of CG Power." The pact provides for lenders being paid an upfront amount of Rs 650 crore. Also, Rs 200 crore of debt would be converted into non-convertible debentures having a five-year tenure. Besides, lenders would be paid "out of the proceeds from sale of CG House property on best efforts and as is where is basis, within a period of five years," the filings said.

The negotiations with banks were brutal. They had already written off most of their exposure and were skeptical that even Murugappa could salvage the situation. But Vellayan had a different approach. Instead of haggling over every rupee, he focused on speed and certainty. Banks would take haircuts, but they would get immediate cash and a clear path to recovery.

In November 2020, TII acquired a 57% stake in CG Power for Rs 800 crore and set a five-year target to turn it debt-free and generate an annual revenue of Rs 5,000 crore. Under Vellayan's chairmanship, it accomplished this by March 2022. (It turned net debt-free by FY22).

The transformation began immediately. Vellayan didn't bring in an army of consultants or announce grandiose strategies. Instead, he focused on basics. Vellayan attributes the successful turnaround to the emphasis on four key metrics: profit, revenue growth, free cash flow, and return on invested capital. Every expense was scrutinized. Every customer relationship was rebuilt. Every process was simplified.

Sources say that the business performance of CG Power has adversely been affected due to a severe crunch in working capital and bringing in an investor like Murugappa Group would help tide over that. Capital restructuring of the business is critical as the working capital gap is wide and while the businesses are intrinsically strong, this starvation has led to lower revenue, even as the company has a robust order book of Rs3,000 crore.

The cultural change was perhaps the most dramatic. Under Thapar, CG Power had operated like a feudal kingdom with complex hierarchies and opaque decision-making. Under Murugappa, it became a meritocracy. Young engineers who had been sidelined were given responsibility. Performance metrics were made transparent. The company that had hidden billions in liabilities now published detailed monthly updates.

Customers who had blacklisted CG Power after the fraud slowly began returning. The products hadn't changed—the transformers were still well-engineered, the motors still reliable. What had changed was trust. With Murugappa's name behind it, CG Power was bankable again. Orders from railways, power utilities, and industrial customers began flowing back.

Inspired by leading auto parts manufacturers globally and domestically, such as American diversified conglomerates Danaher Corporation and ITW, Motherson Sumi, and Sundram Fasteners (from the erstwhile TVS Group where Vellayan has worked), a three-engine growth plan was drawn up—TI-1 or core business; TI-2 or frontier businesses; and TI-3 for inorganic growth through acquisitions. Danaher, a firm he has tracked since 1995 and one that safeguarded itself from cyclical loops to grow through acquisitions, offered a solid playbook. In the past, Danaher would acquire firms that were not considered top performers and then work to improve their performance. To its credit, TII too has acquired and turned around a debt-ridden and fraud-hit company—CG Power and Industrial Solutions.

By early 2021, the impossible was becoming possible. CG Power was generating positive cash flow. Debt was being paid down ahead of schedule. The stock, which had touched ₹7, was climbing steadily. The phoenix was beginning to rise.

The Phoenix Rises: Turnaround & Transformation

The number flashing on the screen at the Bombay Stock Exchange on November 21, 2023, seemed almost unbelievable: ₹455. CG Power's stock had just hit a new 52-week high, completing a journey from ₹7 to over ₹450 in just three years. In the executive dining room at Tube Investments' Chennai headquarters, Vellayan Subbiah allowed himself a rare smile. "The market is just catching up to what we've known all along," he told his team. "This company was never broken—it was just badly managed. "The stock has leaped and given a whopping return of 1,268 per cent during the period. From the nadir of ₹7 in March 2020 to over ₹650 by 2024, CG Power's resurrection wasn't just impressive—it was unprecedented in Indian corporate history. But numbers only tell part of the story.

Today, CG Power stands as a ₹1,07,313 crore market cap powerhouse, generating ₹10,559 crore in revenue and ₹999 crore in profit. The transformation from a company with negative net worth to one trading at 27.1 times its book value happened through relentless focus on operational excellence.

The turnaround began in the factories. At the Kanjurmarg transformer plant, which had been operating at 35% capacity during the crisis, production lines were reorganized using lean manufacturing principles. Inventory that had been gathering dust for years was liquidated. Procurement processes were centralized, cutting material costs by 15%. Most importantly, worker morale—shattered by the fraud scandal—was rebuilt through transparent communication and performance-linked incentives.

Operating income during the year rose 27.2% on a year-on-year (YoY) basis. The company's operating profit increased by 18.2% YoY during the fiscal. Net profit for the year grew by 26.5% YoY. These weren't just recovery numbers—they represented genuine operational improvement.

The order book told an even more compelling story. The unexecuted order book as of December 31, 2023, was Rs 5,556 crores, showing a 34% increase YoY. Customers who had abandoned CG Power during the crisis were returning. Indian Railways, which had blacklisted the company, reinstated it as a supplier. Power utilities that had insisted on bank guarantees began accepting normal payment terms again.

But perhaps the most dramatic change was in the company's approach to new opportunities. Under Thapar, CG Power had chased glamorous international deals. Under Murugappa, it focused on bread-and-butter domestic opportunities where it had competitive advantages. The company began winning contracts for metro rail projects, renewable energy installations, and transmission infrastructure upgrades—all areas benefiting from India's infrastructure push.

The railways business became a particular bright spot. CG Power's traction motors and power equipment were critical for Indian Railways' electrification drive. With the government pushing to electrify 100% of broad-gauge routes by 2024, orders poured in. The company's Bhopal factory, which manufactured railway equipment, went from single-shift to round-the-clock operations.

Financial discipline was equally impressive. Free cash flow generated for the year was Rs 784 crore. This wasn't financial engineering—it was cash generated from operations, collected from customers, and carefully managed through the working capital cycle. The company that had once hidden billions in liabilities now published detailed cash flow statements every quarter.

ROCE for FY24 was at 37%. For a capital-intensive manufacturing business, this was exceptional. It meant that every rupee invested in the business was generating 37 paise in returns—a level that matched the best global electrical equipment companies.

The cultural transformation was equally remarkable. The company instituted a "Voice of Customer" program where senior managers personally visited clients to understand their needs. Quality circles were established in every factory. A suggestion scheme generated over 1,000 improvement ideas from workers in the first year alone. The company that had once been synonymous with fraud was becoming known for operational excellence.

International operations, which had been a millstone around CG Power's neck, were restructured or sold. The focus shifted entirely to India and select export markets where the company had clear competitive advantages. The dream of becoming a global giant was replaced by the discipline of being a profitable, well-run Indian company.

By 2023, institutional investors who had fled during the scandal began returning. Promoter holding has decreased over last quarter: -1.68%, but this was by design—Murugappa was gradually reducing its stake as the company's governance improved and it could stand on its own feet. Foreign institutional investors, who had completely exited during the fraud, began accumulating shares again.

The Q3 FY25 results released in January 2025 showed the sustainability of the turnaround. Aggregate sales for the quarter was Rs 2,389 crore with a growth of 28% YoY and 5% up v/s Q2FY25. PBT (before other income) was higher at Rs 306 crore as against Rs 227 crore in Q3FY24 with a growth of 35%. Order intake for Q3FY25 was Rs 3,636 crore (61% growth YoY) and Unexecuted Order backlog as at 31 Dec 2024 was Rs 8,952 crore (61% higher YoY).

The numbers were staggering, but what they represented was even more impressive: a company that had been left for dead was now growing faster than most of its peers, with better margins and stronger cash generation. The phoenix hadn't just risen—it was soaring.

Playbook: Crisis Management & Value Creation Lessons

The conference room at the Indian Institute of Management Ahmedabad was packed with MBA students, executives, and professors. Vellayan Subbiah had been invited to deliver a case study on the CG Power turnaround, and the audience leaned forward as he began with an unexpected statement: "The biggest mistake in a turnaround is trying to be a hero. The real work is boring, systematic, and requires more patience than brilliance."

The CG Power turnaround offers a masterclass in crisis management and value creation that goes far beyond financial engineering. The playbook that emerged from this transformation has become required reading for distressed asset investors and turnaround specialists across India.

Lesson 1: Due Diligence Beyond the Numbers

When Tube Investments evaluated CG Power, they didn't just examine financial statements—they understood those were compromised. Instead, they focused on operational reality. Engineers visited factories at different times to observe actual capacity utilization. They interviewed customers to understand product quality and service levels. They studied employee attendance records to gauge morale. The insight: in a fraud situation, traditional due diligence fails. You need to understand the business's fundamental health beyond what appears in spreadsheets.

Lesson 2: Speed Matters More Than Perfection

The restructuring with lenders was completed in record time—just four months from initial approach to signed agreements. Vellayan's team didn't negotiate for the last rupee; they negotiated for certainty and speed. This allowed them to move quickly to operational improvements while competitors were still analyzing the opportunity. As one banker involved noted: "They came with a take-it-or-leave-it offer that was fair to everyone. No games, no drama, just business."

Lesson 3: Culture Eats Strategy for Breakfast

The first 100 days focused entirely on cultural transformation. Before any strategic plans or restructuring, Murugappa established trust. Town halls were held at every location. A whistleblower hotline was established. Financial reporting was made transparent down to the factory level. Employees who had been demoralized by the fraud saw that new management meant what it said. This cultural foundation enabled everything that followed.

Lesson 4: Operational Excellence as Competitive Advantage

Rather than pursuing new markets or products, CG Power focused on doing existing things better. Delivery times improved from 12 weeks to 8 weeks. Defect rates fell by 60%. Customer complaints were resolved in days rather than months. These improvements required no capital investment—just focus and discipline. The company's Net Promoter Score, which had been negative during the crisis, reached 67 by 2023.

Lesson 5: The Power of Patient Capital

Murugappa Group's approach differed fundamentally from typical private equity turnarounds. They didn't load the company with debt to juice returns. They didn't strip assets or cut R&D. They invested for the long term, understanding that sustainable value creation takes time. The target wasn't a quick flip but building a business that could thrive for decades.

Lesson 6: Governance as Value Creator

Post-crisis, CG Power implemented governance standards that exceeded most Indian companies. Board meetings were webcast to all employees. Detailed minutes were published. Related-party transactions were eliminated entirely. This transparency didn't just prevent future fraud—it became a competitive advantage. Customers and lenders trusted CG Power precisely because it had learned from its mistakes.

Lesson 7: Focus Beats Diversification

Under Thapar, CG Power had tried to be everything—consumer products, industrial equipment, global player. Under Murugappa, it became focused: industrial and power systems for the Indian market. This clarity allowed for better resource allocation, clearer accountability, and stronger competitive positioning. Revenue per employee increased by 40% simply through better focus.

Lesson 8: The Value of Incremental Improvements

The turnaround didn't involve any breakthrough innovations or dramatic pivots. It was built on hundreds of small improvements: better inventory management, faster collection of receivables, reduced machine downtime, improved vendor negotiations. Collectively, these incremental gains transformed the company's economics. EBITDA margins improved from 8% to 15% through operational improvements alone.

Lesson 9: Building Trust Takes Time

Rebuilding relationships with stakeholders—customers, suppliers, employees, investors—was the longest part of the journey. Trust lost in moments takes years to rebuild. CG Power instituted a "Promises Kept" metric, tracking every commitment made to any stakeholder. By 2023, the company had a 98% promise fulfillment rate—remarkable for any organization, extraordinary for one recovering from fraud.

Lesson 10: Crisis Creates Opportunity

The fraud crisis, devastating as it was, created the conditions for transformation. It broke the old power structures, cleared out complacent management, and created urgency for change. Sacred cows could be slaughtered. Difficult decisions could be made. The company that emerged was stronger not despite the crisis but because of how it responded to it.

The playbook's most important lesson might be its simplest: turnarounds succeed not through financial engineering or strategic brilliance, but through disciplined execution of basics. As Vellayan concluded his IIM-A lecture: "We didn't save CG Power. CG Power saved itself. We just created the conditions for that to happen."

Analysis & Investment Case

The equity research report from a leading Mumbai brokerage in late 2024 opened with an unusual disclaimer: "We initially rated CG Power a 'Sell' at ₹15 in 2020, then 'Hold' at ₹150 in 2022, and 'Buy' at ₹300 in 2023. We were wrong each time—too bearish initially, too cautious later. This company has consistently defied conventional valuation metrics." This honest admission captured the challenge of analyzing CG Power: how do you value a company that has transformed so fundamentally?

The Bull Case: Multiple Growth Engines

CG Power's investment thesis rests on several powerful tailwinds. India's power demand is expected to grow at 7% annually through 2030, driven by industrialization, urbanization, and electrification. The railway electrification program, metro rail expansion, and renewable energy boom all play directly to CG Power's strengths. With an order backlog exceeding ₹8,900 crore and strong execution capabilities, revenue visibility extends well into 2026.

The company's competitive position has actually strengthened post-crisis. While competitors grew complacent, CG Power rebuilt with modern manufacturing practices and lean operations. Its cost structure is now among the best in the industry. The Bhopal factory for railway equipment operates at efficiency levels matching global benchmarks. The transformer facilities in Nashik and Kanjurmarg have reduced manufacturing cycle times by 30%.

Margins have expansion potential. Current EBITDA margins of 15% remain below the 18-20% achieved by global peers like ABB and Siemens. As product mix improves toward higher-margin segments like railway signaling and automation, profitability should increase. The company's renewed focus on exports, particularly to Africa and Southeast Asia, offers better pricing than competitive domestic markets.

Management quality under Murugappa ownership provides comfort. The group's track record across multiple businesses—from Cholamandalam Finance to Coromandel International—demonstrates an ability to create long-term value. Corporate governance, once CG Power's greatest weakness, has become a strength. The company now scores in the top quartile of BSE 500 companies on governance metrics.

The balance sheet provides optionality. With net cash position and generating ₹700+ crore in annual free cash flow, CG Power can pursue growth organically or through acquisitions. The company has been conservative post-crisis, but management has indicated openness to strategic acquisitions in adjacent segments like energy storage or grid automation.

The Bear Case: Valuation and Cyclicality Concerns

Critics point to demanding valuations. Trading at 27 times book value and 65+ times trailing earnings, CG Power is priced for perfection. Any disappointment in execution or market conditions could trigger a sharp correction. The stock's spectacular rise from ₹7 to ₹650+ has been driven partly by re-rating rather than just fundamentals—this re-rating may have run its course.

The electrical equipment industry remains highly cyclical. Government capital expenditure drives demand, and any fiscal consolidation could impact orders. Private sector investment, while recovering, remains below previous peaks. China's economic slowdown could lead to dumping of electrical equipment at predatory prices, pressuring margins.

Competition is intensifying. Large conglomerates like Larsen & Toubro and global giants like Schneider Electric are expanding in CG Power's core markets. New players, particularly in renewable energy equipment, are emerging with aggressive pricing. Technology shifts toward smart grids and digital substations require continuous investment with uncertain returns.

Execution risks persist. Rapid order book growth strains manufacturing capacity and working capital. The company is investing heavily in new facilities, but project execution delays could impact profitability. Supply chain disruptions, while managed well so far, remain a constant threat. The global semiconductor shortage has already impacted some product lines.

Key person dependency is a concern. While Murugappa has built a strong professional team, the turnaround has been closely associated with Vellayan Subbiah's leadership. Any change in management or Murugappa's commitment could unsettle investors. The group has reduced its stake from 58% to 56%, raising questions about long-term commitment.

The Balanced View: Quality at a Price

The investment case ultimately comes down to whether CG Power's quality transformation justifies premium valuations. The company has moved from the "too hard" pile to institutional portfolios, but the easy money has been made. Future returns will likely track business performance rather than multiple expansion.

For long-term investors, CG Power offers exposure to India's infrastructure story with proven execution capabilities and strong governance. The company's focus on railways, renewable energy, and transmission infrastructure aligns with national priorities unlikely to change regardless of political shifts.

For value investors, the stock appears expensive on traditional metrics. Waiting for a correction might mean missing further upside, but discipline suggests patience. The company's history reminds us that governance failures can destroy value rapidly—while the new management has performed admirably, the institutional memory of fraud will take years to fully fade.

For growth investors, CG Power presents an interesting proposition. The order backlog provides visibility, new segments offer expansion potential, and management has demonstrated an ability to exceed expectations. The risk-reward may still be favorable for those with conviction in India's infrastructure build-out.

The technical picture remains constructive, with the stock consistently making higher highs and higher lows. Institutional ownership has increased from virtually zero during the crisis to over 25%, providing support. However, retail investors who bought during the penny stock phase may book profits at regular intervals, creating volatility.

Consensus estimates suggest 20-25% earnings growth over the next three years, implying forward valuations becoming more reasonable. But consensus has consistently underestimated CG Power's recovery—actual results could surprise positively. Conversely, any disappointment could trigger a sharp de-rating given elevated expectations.

Epilogue & Reflections

As 2025 dawns, CG Power's headquarters in Mumbai's Kanjurmarg bears little resemblance to the crisis-ridden offices of 2019. The executive floor, once marked by paranoia and secrecy, now features open workspaces and glass-walled meeting rooms. The company that once symbolized everything wrong with Indian corporate governance has become a case study in redemption.

But the larger story of CG Power transcends one company's turnaround. It's a reflection of Indian capitalism's evolution—messy, sometimes painful, but ultimately progressive. The fraud that destroyed value also created opportunity for reform. The crisis that seemed catastrophic catalyzed transformation that might never have occurred otherwise.

The role of institutional investors deserves recognition. When KKR invoked their rights and forced transparency, when mutual funds demanded governance changes, when proxy advisors recommended against resolutions—these actions, though painful for management, protected minority shareholders. The system worked, albeit imperfectly and belatedly.

The contrast between the Thapar and Murugappa approaches offers lessons in business philosophy. Thapar built an empire through debt-funded acquisitions and financial engineering. Murugappa created value through operational excellence and governance. Both approaches can work in different contexts, but when crisis strikes, substance matters more than style.

For employees who survived the transition, the journey has been transformational. Engineers who joined CG Power in the 1990s, watched it expand globally in the 2000s, survived the 2019 crisis, and participated in the recovery, have lived through multiple lifetimes of corporate experience. Their resilience—staying with a company through fraud allegations, stock price collapse, and ownership change—speaks to something deeper than just employment.

The human cost shouldn't be forgotten. Thousands of employees lost jobs during the crisis. Small shareholders saw life savings evaporate. Suppliers went unpaid for months. While the spectacular recovery makes for a compelling narrative, these losses remain real and largely uncompensated. Corporate fraud has victims whose stories rarely make it into business case studies.

What the story teaches about Indian corporate governance is both encouraging and sobering. Encouraging because the system ultimately worked—fraud was detected, perpetrators were removed, and the company was rescued. Sobering because it took so long, the red flags were ignored for years, and the fraud's magnitude suggests widespread complicity or negligence.

The role of culture in corporate success emerges as paramount. CG Power under Thapar had the same factories, products, and market opportunities as under Murugappa. What changed was culture—from opacity to transparency, from feudalism to meritocracy, from financial engineering to operational excellence. Culture, nebulous as it seems, drove concrete financial results.

Looking forward, CG Power faces new challenges. Success has raised expectations. The stock price assumes continued excellence. Competition is intensifying. Technology is evolving rapidly. The company that survived existential crisis must now manage success—often a harder challenge. Complacency, the enemy that contributed to the original crisis, remains a constant threat.

The international ambitions that drove the ill-fated expansion may resurface. As India's manufacturing ambitions grow and companies seek global scale, CG Power will face pressure to expand internationally. Whether it can do so while maintaining the discipline learned through crisis will test institutional memory.

For India Inc., CG Power offers both warning and hope. The warning: governance failures can destroy decades of value creation in months. The hope: with right leadership and commitment to reform, even the most damaged companies can recover. The spectacular recovery shouldn't obscure the importance of prevention—strong governance isn't just about crisis management but crisis avoidance.

The investment community's relationship with CG Power has evolved from skepticism to enthusiasm, perhaps too much of the latter. The same analysts who couldn't imagine recovery at ₹10 now project continued outperformance at ₹650. This cycle of despair and euphoria suggests markets still struggle to price fundamental transformation.

As Vellayan Subbiah noted in a recent interview, "The CG Power story isn't finished—it's just beginning a new chapter." The company born in colonial workshops, built through protected markets, expanded with global ambitions, brought down by fraud, and rescued through operational excellence, now faces its next evolution. Whether it becomes a sustainable industrial champion or another cautionary tale remains to be written.

The ultimate lesson might be that corporate mortality and immortality are closer than we think. Companies that seem invincible can collapse suddenly. Companies given up for dead can resurrect spectacularly. In business, as in life, the only constant is change—and the opportunity for redemption always exists for those willing to do the hard work of transformation.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube