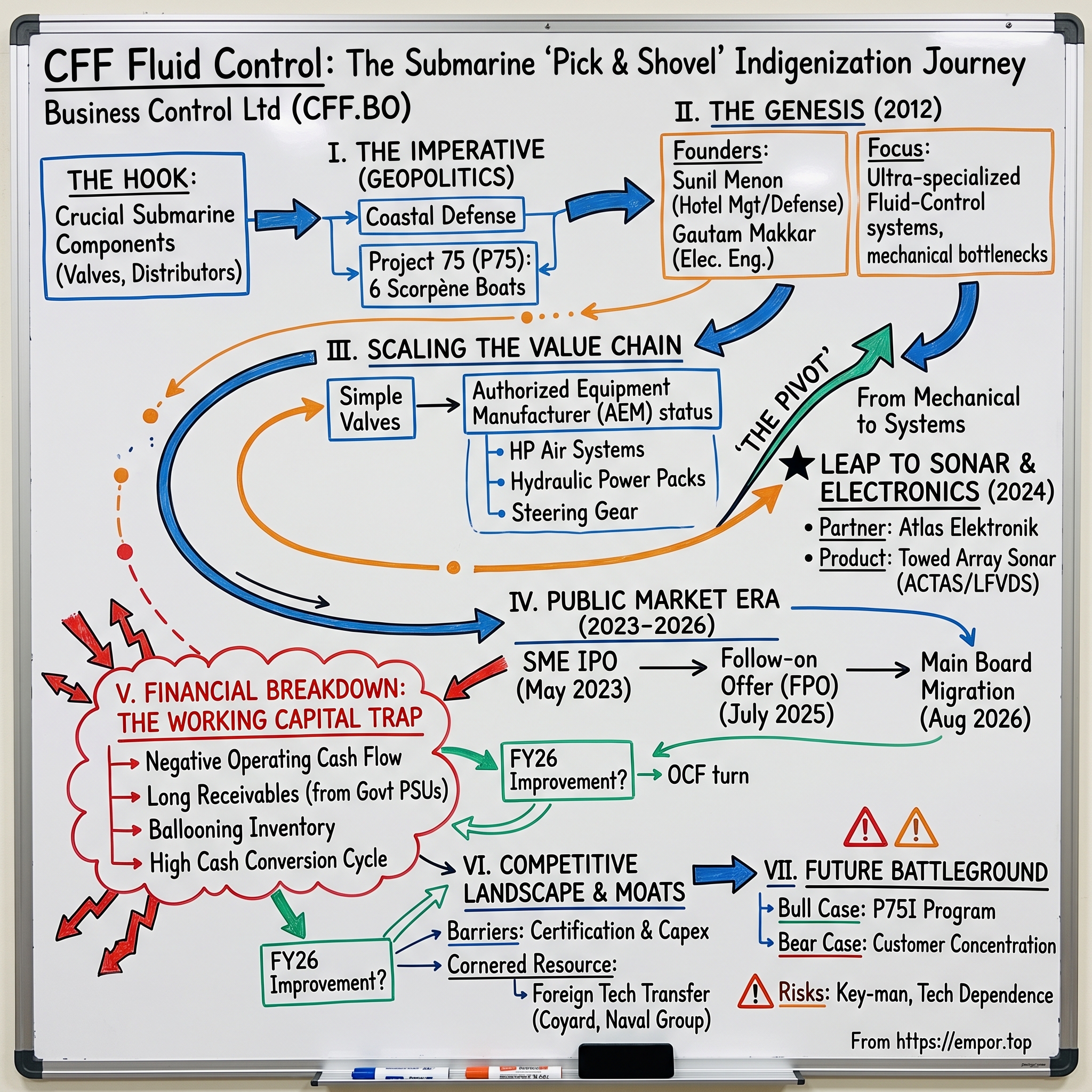

CFF Fluid Control: The Submarine Defense "Pick & Shovel" Indigenization Play

I. Episode Roadmap & The Hook

Somewhere off the coast of Mumbai, three hundred meters beneath the surface of the Arabian Sea, a Scorpène-class submarine sits in silence. The hull is under crushing pressure—roughly thirty times the weight of the atmosphere at sea level, pressing in from every direction. Inside, a lattice of valves, distributors, and high-pressure air panels holds the boat's breath, its buoyancy, and its ability to surface. If any one of those components fails—if a valve seat corrodes, if a seal weeps, if a distributor chatters and betrays the boat's position to a listening enemy—the submarine's entire reason for existing collapses. It is no longer invisible. It is no longer safe.

The company that makes many of those valves is not a sprawling defense prime with a marble lobby and a lobbying budget. It is a firm of a few dozen engineers working out of a 6,000-square-meter shed in Khopoli, a dusty industrial town in Raigad district, Maharashtra, roughly two hours inland from the docks where the submarines are actually built.1 That firm is CFF Fluid Control Ltd, and its story is one of the more improbable in India's defense-industrial awakening.

Founded in 2012 by two brothers-in-law—one a former hotel-management graduate turned defense entrepreneur, the other an electrical engineer from Pune—CFF spent its first decade as an anonymous private company.2 By July 2026, it had become an Authorized Equipment Manufacturer for the Indian Navy, holding single-source supplier status on critical submarine mechanical systems, partnered with French and German defense giants, and on the cusp of migrating from the BSE's junior SME platform to the main board—the stock exchange equivalent of graduating from the minor leagues.3

This is a story about a specific, unglamorous investment thesis: the pick-and-shovel play. During the California gold rush, the people who reliably got rich were not the prospectors panning for nuggets but the merchants selling them picks, shovels, and blue jeans. The modern equivalent in Indian defense is not the multi-billion-dollar shipyard—Mazagon Dock, which actually assembles the submarines and carries the political weight and the execution risk. It is the specialized tier-2 subsystem supplier who quietly controls a critical engineering bottleneck that nobody else in the country can replicate. That is the seat CFF has tried to occupy.

The rest of this episode walks the full arc: the geopolitics of India's submarine deficit and the Project 75 mandate that created CFF's entire addressable market; the founding, the French technology transfer, and the deliberate construction of a regulatory-and-capex moat; the strategic climb from simple valves to sonar electronics; the capital-markets journey through an IPO, a follow-on offer, and a main-board migration; the financial paradox of blistering growth alongside a working-capital trap that swallowed cash for years; the competitive map against MTAR, Paras, and Sika Interplant; a hard look at management and governance; and finally the bull-versus-bear spine—why this business could compound for a decade, and what could break the case. Throughout, the posture is neutral. Management's claim that it will win is a hypothesis to be tested, not a conclusion to be repeated.

Let's start where CFF's opportunity started: not in a boardroom, but on a map.

II. India's Maritime Imperative & The Birth of Project 75

Look at a map of the Indian Ocean and the strategic problem announces itself. India has a coastline of roughly 7,500 kilometers, a peninsula thrusting into one of the busiest and most contested waterways on earth. Through the sea lanes to its west flows the bulk of the world's oil; to its east lie the Malacca chokepoints and an increasingly assertive Chinese navy that has spent two decades building blue-water reach. For a nation with hostile land borders to its north and west, the ocean is not a moat—it is the flank most easily turned, and the one where deterrence is most valuable precisely because it is hardest to see.

The crown jewel of that undersea deterrence is the conventional submarine: diesel-electric boats that can lurk quietly on batteries, wait, and strike. By the late 2000s, India's submarine arm had a demographic crisis. Its fleet leaned heavily on aging Russian Kilo-class and German Type 209 boats, many of them decades old, with retirements looming faster than replacements were arriving. A fighting arm designed around a certain number of hulls was quietly shrinking below the line at which planners could sleep comfortably.

The answer was Project 75 (P75)—a program to license-build six advanced Scorpène-class submarines with France's Naval Group (then known as DCNS) as technology partner, assembled at the state-owned Mazagon Dock Shipbuilders Limited (MDL) in Mumbai.[^4] The Scorpène is a compact, quiet, conventionally powered hunter-killer, roughly seventy meters of steel designed to disappear. The deal, signed in the mid-2000s and stretching across two decades of construction, was as much about industrial transfer as about the boats themselves. India did not merely want six submarines; it wanted the capability—the tooling, the know-how, the qualified supply chain—to build submarines again and again. The first of class, INS Kalvari, was commissioned in December 2017; the sixth, INS Vagsheer, in January 2025, closing out the original P75 line and rolling into follow-on orders for additional hulls.[^4]

That timeline itself tells a story. A program conceived in the 2000s took until 2025 to deliver its sixth boat—the sort of grinding, milestone-gated schedule that is normal in submarine construction and abnormal almost everywhere else. Submarines are among the most complex machines humans build; a single boat integrates tens of thousands of parts, each of which must work flawlessly under conditions that would destroy ordinary industrial equipment. That slowness is not incidental to CFF's story. It is the reason the working-capital problem examined later is so severe, and it is the reason a qualified supplier, once embedded, is so hard to replace: nobody wants to re-run a five-year qualification on a program that is already behind schedule.

Here is where the story turns from geopolitics to industrial reality, and where CFF's window opened. Foreign OEMs like Naval Group operate under India's "Make in India" indigenization mandate, embedded in successive iterations of the Defence Acquisition Procedure, which contractually pushes them to localize an ever-rising share of component sourcing. The stated national ambition is dramatic: to move defense procurement from something like ten percent domestic content toward seventy percent and beyond, converting India from the world's largest arms importer into a maker of its own weapons. But mandating local sourcing and achieving it are very different things. In the late 2000s and early 2010s, Indian industry simply did not possess the metallurgy or the process discipline to fabricate components that could survive a submarine's operating environment—seawater corrosion that eats ordinary steel, extreme pressure cycling that fatigues metal with every dive and surface, and the acoustic-silence requirement that means a part cannot even be allowed to vibrate audibly, because a chattering valve is a beacon to enemy sonar.

Consider what that last requirement alone implies. On a warship, a valve that works is good enough. On a submarine, a valve that works but hums is a liability that could get the crew killed. The tolerances, the materials, the balancing, the testing—all of it operates a full order of magnitude beyond civilian or even surface-naval standards. There was no Indian firm in 2012 that could simply pick up this work; the capability had to be imported, absorbed, and certified essentially from scratch.

That gap was the whole opportunity. Somebody had to step forward and learn to build ultra-specialized fluid-control systems, air panels, steering gear, and breathing systems to French naval standards, on Indian soil, at a price and quality the program could accept. The shipyards could weld hulls and integrate systems; they could not, overnight, become precision valve houses—and it made little sense for a shipyard the size of MDL to try. This is the structural reason the pick-and-shovel layer exists at all: the primes are integrators, and integrators need specialists to feed them. Into that specific, unsexy bottleneck walked a brand-new company with no track record and an audacious plan—which is exactly where the founding story begins.

III. The Genesis: Flash Forge, Coyard SAS, and Khopoli

Every origin myth needs a founder with an unlikely résumé, and CFF has two. Sunil Menon, the managing director and driving force, did not train as a naval architect or a metallurgist. His formal qualification is a diploma in hotel management, catering, and nutrition from the Board of Technical Education in Delhi—a detail so incongruous it is almost a punchline.4 What he actually had was thirty years operating in and around the defense and engineering trade, a family business steeped in sourcing hard-to-make industrial equipment, and, evidently, an instinct for where the puck was heading. His brother-in-law and co-founder, Gautam Makkar, brought the technical spine: a bachelor's in electrical engineering from Pune University in 1991 and more than two decades supplying solutions to the defense, power, and marine industries.4

What Menon lacked in formal engineering credentials he apparently made up for in a trader's nose for where demand was heading and a builder's willingness to bet the house on it. Over the years that followed he would take the company, in his own filings' framing, "from being a small components manufacturer to a strong company whose product and services portfolio includes turnkey projects, integrating various platform systems."4 That is founder-speak, and it should be read with the usual skepticism—but the trajectory of the business over the decade broadly bears out the claim of a deliberate climb from parts to systems. Makkar, for his part, has served since 2022 as non-executive chairman, the technical and sourcing counterweight to Menon's executive drive.4

The family's original vehicle was Flash Forge Private Limited, incorporated back in 1991—the entity through which the promoters had spent more than two decades in the defense, power, and marine supply trade before CFF existed.5 That prior history matters: CFF was not two novices stumbling into defense, but experienced defense-sourcing hands spinning up a dedicated manufacturing arm at exactly the moment the indigenization mandate turned their existing relationships into a manufacturing opportunity. In 2012, they carved out a dedicated new company aimed squarely at one target: the Scorpène program's appetite for localized mechanical equipment. It was incorporated on February 16, 2012, as Flash Forge Fluid Control Private Limited, and renamed CFF Fluid Control within months, in September 2012.6 The name change is a small tell—the founders were building not a forge but a fluid control specialist, betting the whole enterprise on a narrow, deep competency rather than a broad engineering shop. In an industry where breadth is a temptation and focus is a discipline, that early choice to specialize is one of the more revealing decisions in the company's history.

The pivotal move came in 2015. A company with ambition and a shed is not a submarine supplier; a company with a technology transfer agreement is. CFF signed a Transfer of Technology (ToT) with Coyard SAS of France, a high-pressure fluid-control specialist for the French Navy, covering the design, manufacture, and supply of mechanical components for the Scorpène program.7 The same year, CFF landed its first government order connected to Naval Group.7 The ToT is the hinge of the entire business: it gave CFF the European design blueprints, the material specifications—including the specialized copper-nickel and aluminum-bronze alloys that resist seawater without going brittle—and the high-tolerance testing protocols. Crucially, the transfer only converted into a license to produce after the relevant authorities approved it and inspectors physically walked the factory floor. The technology was necessary but not sufficient; the qualification was the real prize.

That distinction explains the physical fort at Khopoli. CFF's facility spans roughly 6,000 square meters and is approved not only for ISO 9001:2015 quality management but, far more importantly, by the Indian Navy, MDL, and Naval Group itself.1 The property was acquired in December 2015 from the family's own Flash Forge Private Limited—a related-party transaction worth noting for the governance file, though a common enough arrangement for a founder-financed startup.8 What matters strategically is what sits inside: the test setups. To qualify as a submarine supplier, a firm must demonstrate that its components survive conditions that mimic the deep sea—pressure testing, endurance cycling, the works. These rigs cost millions and take years to build and certify. Tellingly, CFF's own business description lists "test facilities" as a product line in its own right, alongside the machinery: the company sells not just the parts but the ability to prove the parts work.1

CFF's filings put a number on the qualification barrier that is worth pausing over. By the company's own account, a horizon of roughly three years is required to empanel and get on board with a customer in defense—three years of technical scrutiny, prototyping, security clearance, and inspection before you are approved as the vendor for a specific piece of equipment, and only then do the supplies flow for the life of the platform.9 Think about what that means as an economic barrier. A would-be competitor must fund three years of engineering, testing, and compliance work with no revenue at the end of it—a negative-cash-flow tunnel with no guarantee of emerging. Venture-style capital will not fund it; the timelines are wrong. Bank debt will not fund it; there are no cash flows to service. It must be funded by an owner willing to wait, which is precisely why this industry is populated by family firms and state entities rather than by fast-moving challengers.

This is the moat, and it is worth naming precisely. It is not a patent or a brand; it is a capex-plus-certification barrier. A generic engineering workshop cannot bid for this work no matter how skilled its machinists, because it lacks the approved test infrastructure and the multi-year vendor qualification. And the numbers show how slowly even a successful climb up that barrier compounds. CFF crossed ₹20 crore of turnover only in 2018—six years after incorporation—reached ₹35 crore in 2019, and was still only crossing the ₹45 crore mark in 2022, a full decade in.7 Along the way it picked up recognition from the Society of Indian Defence Manufacturers, participating in the 2020 SIDM Champion Awards under the category of creating niche technological capability for design, manufacturing, or testing—in the start-up sub-category, a decade after founding.7 That is the honest shape of this business: it is not a rocket ship, it is a slow, expensive climb up a wall that most competitors will not attempt.

Which produces the paradox at the heart of the company. The barrier keeps competitors out—but that same barrier is expensive to erect and finance, and it is precisely what chains CFF to a punishing working-capital cycle. Long qualification, long inventory, long payment terms; the very frictions that protect the franchise also starve it of cash. The moat and the trap are built from the same bricks. First, though, CFF had to prove it could climb from loose valves to something far more valuable.

IV. Scaling the Value Chain: From Valves to Sonar & Systems

There is a well-worn path in industrial supply that separates the merely competent from the genuinely defensible: you start by selling a part, and you try to end by selling a system. Selling a valve makes you a vendor, interchangeable in principle with anyone who can meet the spec. Selling an integrated steering-and-propulsion system, tested and certified as a unit, makes you something closer to a partner—harder to displace, higher in value, and stickier across the life of the platform.

CFF walked that path deliberately. Its Khopoli lines grew from fluid-control valves, distributors, and air panels into a wider catalogue: high-pressure air systems, hydraulic power packs, steering gear, propulsion components, weapons and control systems, breathing and diving-air systems, and integrated platform-management systems for both submarines and surface ships.1 Each rung up the ladder raised the average order value and, more importantly, embedded CFF more deeply into the boat's design.

It is worth translating what some of those systems actually do, because the jargon hides how existential they are. The high-pressure air system is, in plain terms, the submarine's lungs and its life insurance: banks of air stored at enormous pressure that get blown into the ballast tanks to force water out and drive the boat to the surface. If it fails at the wrong moment, the boat does not surface. Steering gear is the hydraulic muscle that moves the control surfaces—the boat's rudder and diving planes—translating a helmsman's small input into the force needed to turn thousands of tonnes of steel. The breathing and diving-air systems keep the crew alive in a sealed metal tube for weeks. None of these are peripheral conveniences; each is a single point of failure for the platform and the people inside it. That is exactly why the Navy is so paranoid about who is allowed to make them—and why, once someone is allowed, the Navy is so reluctant to switch.

CFF's own reach across the fleet reflects an accumulating installed base. Its filings cite involvement in the supply and servicing of equipment across SSK-class, Kalvari-class, and Kilo-class submarines—which is to say, across both the new French-derived boats and the legacy Russian and German fleet.1 That breadth matters more than it first appears: legacy boats need spares and refits now, independent of whether new construction programs slip, which gives the business a partial hedge against the notorious lumpiness of fresh procurement.

The mechanism that turns that embedding into durable economics is the Authorized Equipment Manufacturer (AEM) status. In Indian naval procurement, when a specific item's AEM is allocated to a vendor, the Navy must source that item—and its spares and repairs—from that vendor for the operational life of the platform.9 CFF holds AEM status for mechanical equipment on Scorpène submarines and for underwater communication equipment on the same class.9 Put in Hamilton Helmer's language of the 7 Powers, this is switching costs in their purest form: a submarine's systems cannot be casually re-engineered mid-life to accommodate a cheaper supplier. Once your part is written into the technical manual, you own not just the initial sale but the thirty-year tail of maintenance, overhaul, and replacement.

That tail is the analytically interesting part. Low-margin, one-time manufacturing becomes high-margin, recurring, single-source annuity revenue—the kind of cash flow that compounds quietly for decades. It is the same economic logic that makes aircraft aftermarket parts more profitable than the jets themselves: the razor is sold on a competitive tender, the blades are sold to a captive customer for thirty years. The claim is credible on its mechanics; the caveat is that the annuity only grows as the installed base of CFF-equipped platforms grows, which keeps CFF hostage to the pace of India's shipbuilding. Reinforcing the lock-in, CFF holds a framework agreement with Naval Group and France's Issartel explicitly structured to let it support additional equipment and systems across the thirty-year lifecycle of the Scorpène fleet—the contractual scaffolding that turns AEM status from a single-item privilege into a platform-wide franchise.9

Underneath the AEM headline sits an equally important and less glamorous asset: registrations. CFF's customer set runs through MDL and the naval dockyards at Mumbai, Visakhapatnam, and Karwar, and the company worked through the registration process with the other major yards—GRSE, Hindustan Shipyard, and Cochin Shipyard—to widen its permitted customer base.9 Vendor registration is not a formality in defense; it is the gate. Each new yard registered is a genuine expansion of addressable market that costs years to obtain and cannot be shortcut with a sales pitch.

The company has also hedged, modestly, against pure naval dependence. Alongside its defense work, CFF designs and services mechanical equipment for the nuclear and clean-energy sectors—an adjacency that leverages the same precision-and-certification competency in a different regulated market.1 At the time of the IPO, however, the split was starkly lopsided: roughly 89 percent of business came from the defense sector against about 11 percent non-defense.1 The diversification is real but small, and investors should treat it as optionality rather than as a meaningful counterweight to the concentration risk examined later.

The most ambitious move up-market came in 2024, and it changed the character of the business. CFF partnered with Atlas Elektronik GmbH—the naval-electronics arm of Germany's Thyssenkrupp Marine Systems—to indigenize sonar for the Indian Navy, including Low-Frequency Variable Depth Sonar (LFVDS) and Active Towed Array Sonar (ACTAS) systems.10 The specific opportunity: producing a batch of LFVDS units for the Navy's Anti-Submarine Warfare Shallow Water Craft program, with the sonars destined for vessels built by Garden Reach Shipbuilders (GRSE) and Cochin Shipyard.11 Notably, Atlas Elektronik had supplied towed-array sonar to the Indian Navy before, so the technology itself was not alien to Indian waters—what was new was the plan to build it locally.11

A word on why variable-depth sonar is such a prized capability, since the physics is genuinely counterintuitive. The ocean is not a uniform medium; it is layered, with bands of differing temperature and salinity that bend sound waves the way a lens bends light. A submarine that tucks itself beneath a thermal layer can become effectively invisible to a sonar mounted on a surface ship's hull, because the sound simply refracts away and never reaches it. The answer is to stop listening from the surface and instead lower the sensor on a cable through the layer, down to where the submarine is hiding—and to do it at low frequencies, which travel farther through water. That is what an LFVDS does: it is a microphone on a long leash, dropped past the ocean's blind spot. For a navy whose principal worry is other people's submarines, it is close to the definition of a critical capability.

Why does this matter more than another valve contract? Two reasons. First, it is a leap from mechanical hardware into high-value defense electronics, a category with a richer margin profile and substantially higher order values—a sonar suite is worth many multiples of a valve package. Second, and more strategically, sonar for surface ships expands CFF's addressable market beyond submarines to the far larger fleet of destroyers, frigates, and ASW craft. The submarine business is deep but narrow; surface combatants are the broad market. The Atlas tie-up, in effect, doubles the number of platform types CFF can sell into.

A parallel bet runs through Nereides of France, which specializes in towed-wire antennas—the trailing wire that lets a submerged submarine receive communications across VLF, LF, and HF bands without surfacing and exposing itself.10 CFF committed real money here, spending roughly ₹8.5 crore of its IPO proceeds acquiring the technology.14 It is the same playbook run a third time: find a niche European specialist with a technology India needs, transfer it, indigenize it, and own the resulting AEM franchise.

The honest analytical caveat is that this playbook is now being asked to work in a domain where CFF has no track record. Machining a submarine valve to French naval tolerances and integrating a low-frequency sonar array are genuinely different disciplines—one is precision metallurgy and mechanical assembly, the other is signal processing, electronics, and software. Management's claim is that the transferable asset is not the specific technology but the capability to absorb, qualify, and indigenize foreign technology, which is domain-agnostic. That is a plausible thesis and a common one among successful industrial firms, but it remains a thesis. The evidence that will settle it is delivery: whether the sonar programs convert into executed, inspected, paid-for revenue on schedule. Until then, investors should treat the electronics pivot as promising optionality rather than as proven competence. To fund all of this ambition, CFF needed outside capital, and in 2023 it went public.

V. The Public Market Era: SME IPO, FPO, and Main Board Migration

For most of its life, CFF was invisible to public investors—a promoter-funded company leaning on unsecured loans from the family's Flash Forge entity to bridge its cash needs.12 That changed on May 30, 2023, when CFF opened its initial public offering on the BSE's SME platform: 52 lakh fresh shares at ₹165 apiece, raising ₹85.80 crore.13 The use of proceeds tells you exactly what kind of business this was even then—not a growth-capital story so much as a plumbing exercise. Roughly ₹29.4 crore went to working capital, ₹21 crore to repaying the high-cost promoter and other loans, ₹8.9 crore to machinery, and ₹8.5 crore to acquiring towed-wire-antenna technology from France's Nereides.14 In other words, a large chunk of the very first equity raise went simply to plug the working-capital hole and refinance expensive debt—a foreshadowing that any careful reader should have filed away.

The structure of the IPO is itself revealing. It was a fixed-price issue on the SME platform, priced at 16.5 times the ₹10 face value, with Aryaman Financial Services as lead manager, and it was entirely a fresh issue—no offer for sale.13 That last detail deserves credit: the founders took nothing off the table. Every rupee raised went into the company rather than into promoter pockets, which is not always the case in SME listings and is a genuine signal of intent, whatever one makes of the uses to which the money was put.

There is a second detail in the offer documents worth flagging for the governance file. Among the objects was repaying ₹21 crore of unsecured loans owed to Flash Forge Private Limited—the promoters' own group entity—which had been lent at 12 percent per annum and used partly for working capital and partly to acquire the company's Powai property.12 Read charitably, this is a founder financing his own company when no one else would, and then using public money to clean up the arrangement and remove a related-party overhang. Read skeptically, public shareholders funded the retirement of a promoter's high-interest loan to his own business. Both readings are defensible; the transaction was disclosed, which is what matters most.

The market did not care about the plumbing. It cared about the story: a certified, single-source submarine supplier riding the indigenization wave, listing at a moment when Indian defense stocks were the hottest theme on the exchange. The stock was bid up hard in the years that followed, and CFF became a classic SME "sleeper"—an obscure name that HNI and retail investors discovered and re-rated aggressively. It is worth being clear-eyed about what drove that re-rating. Some of it was genuine business progress. A great deal of it was thematic: between 2023 and 2025, Indian defense manufacturing became one of the most crowded trades on the exchange, and a small-float SME stock with "defense" and "submarine" in its description was always going to catch a bid regardless of its cash-flow statement. Small floats amplify moves in both directions—a fact that matters when considering what a main-board migration and a broader shareholder base might do to the stock's behavior.

Two years later, in July 2025, CFF returned to the well with a follow-on public offer. It issued 15 lakh fresh shares at ₹585—3.5 times the original IPO price—raising ₹87.75 crore.15 The offer was subscribed 8.45 times and the shares listed at ₹621, a modest premium.16 Note the discipline in how the money was to be spent: essentially all of it, ₹72.6 crore, was earmarked for working capital, with the small remainder for general corporate purposes.17 There were no acquisitions, no diversification into unrelated hot sectors, no empire-building. This is a genuine and creditable contrast with Western aerospace roll-ups that grow by serial, dilutive M&A. But it is also worth reframing bluntly: CFF was not raising equity to seize a bold new opportunity. It was raising equity to fund its own receivables. The FPO was, in large part, a working-capital rescue dressed in the language of expansion—a reading the financials in the next section make unavoidable.

Interestingly, the migration was not an opportunistic afterthought—it was in the plan from the beginning. CFF's 2023 IPO prospectus laid out an explicit three-stage vision: Stage 1, the IPO, to strengthen deliverables under the technology transfers, build infrastructure capable of executing orders up to ₹500 crore, and ensure "smooth flow of working capital"; Stage 2, two to three years while on the SME platform, bidding and executing large defense orders and creating a presence in missiles, main battle tanks, aircraft, and drones; Stage 3, migration to the main board.1 Judged against that roadmap, management has done roughly what it said it would do, on roughly the schedule it said it would do it—the ₹500 crore order-book capability arrived, and the migration followed. That is a meaningful data point on execution credibility, and it is the kind of multi-year promise-versus-delivery test that deserves more analytical weight than any single quarter's commentary. The one leg conspicuously not delivered is the diversification into missiles, tanks, aircraft, and drones; CFF remains a naval-systems company. Whether that is prudent focus or a quietly abandoned ambition is a fair question—and management has not, in public materials, explained the shift.

The third act arrived in July 2026. On the recommendation of its audit committee, CFF's board approved a plan to migrate from the BSE SME segment to the main boards of both BSE and NSE, subject to shareholder approval at the 14th Annual General Meeting scheduled for August 7, 2026.3 The same board meeting reappointed statutory auditor V.N. Purohit & Co.—the firm that has audited CFF since well before the IPO—for a further five-year term running through the 19th AGM, and the agenda included a resolution to increase the company's borrowing limits.3 That last item is not incidental, and an attentive reader should file it alongside the cash-flow analysis that follows: a company seeking headroom to borrow more is a company that anticipates needing more funding.

The migration is not a cosmetic upgrade. Large domestic mutual funds, foreign institutional investors, and pension funds are frequently mandate-blocked from holding SME-platform stocks; the main board removes that barrier and opens CFF to a far deeper pool of institutional capital. As of March 2026, institutional ownership was still negligible—foreign institutions held a rounding error at 0.01 percent and domestic institutions well under one percent—so the runway for institutional accumulation is essentially untouched.26 It is a real catalyst—though, as always, one that cuts both ways, because a broader and more sophisticated shareholder base also brings sharper scrutiny of exactly the cash-flow problem we turn to now.

VI. Financial Breakdown: The Working Capital Trap

Start with the headline numbers, because they are genuinely impressive, and then watch what happens when you follow the cash. In FY24, CFF reported revenue of roughly ₹107 crore and net profit of about ₹17.1 crore—a net margin near sixteen percent, extraordinary for a component manufacturer.18 In FY25, revenue climbed about 36 percent to roughly ₹145.6 crore and net profit jumped near forty percent to about ₹23.9 crore.19 Then, in the results reported in May 2026, the trajectory steepened again: FY26 revenue of roughly ₹208.7 crore—up about 43 percent—and net profit of about ₹39.2 crore, with fourth-quarter EBITDA margins expanding to 28.5 percent.20 A three-year revenue path of roughly ₹107 crore to ₹146 crore to ₹209 crore is a compound rate north of 35 percent, and the order book that underwrites it stood around ₹551 crore at the end of December 2024 and roughly ₹514 crore by May 2025—well over three times trailing revenue, giving multi-year visibility.21

Pause on those margins, because they are the first thing a skeptic should interrogate. A sixteen percent net margin—and EBITDA margins running in the high twenties—is not what component manufacturing normally looks like. Contract machining businesses typically earn single-digit net margins, because they compete on price against anyone with a similar machine. CFF's margin structure is therefore evidence, not just assertion, that something is protecting it from price competition. That something is the certification-and-single-source position described earlier. When a supplier earns three times the normal margin for its industry, either it has a moat or it has an accounting problem. The margin profile is consistent with the moat thesis—which makes it all the more important to check whether the earnings are real.

So far, this reads like a flawless growth story. It is not, and the reason is the single most important thing to understand about CFF.

For years, CFF's profits were largely paper. Despite record reported earnings, operating cash flow was persistently, deeply negative: roughly negative ₹9.3 crore in FY23 and a striking negative ₹26.8 crore in FY24—a year in which the company reported profit before tax of about ₹24 crore while consuming ₹26.8 crore of cash from operations.22 Sit with that inversion for a moment. The gap between reported profit and cash generated in a single year exceeded ₹50 crore, against a company whose entire revenue that year was ₹107 crore. The disconnect is not an accounting trick, and there is no suggestion of impropriety; it is the physical reality of the business written into the balance sheet. Every rupee of "profit" was being swallowed by a ballooning pile of inventory and receivables.

The balance sheet makes the point without commentary. Current assets—inventories, trade receivables, short-term advances, and other current assets—constituted between roughly 65 and 78 percent of CFF's total assets across FY22 through the September 2024 half-year.23 This is a manufacturer whose factory and machinery are a minority of what it owns; the majority of the company is, quite literally, unsold stock and unpaid invoices. Inventories alone rose from about ₹21 crore in FY22 to roughly ₹58 crore by September 2024, while trade receivables exploded from about ₹8.8 crore at the end of FY24 to ₹52.1 crore just six months later.23 Growth, in this business, is not something you harvest. It is something you fund.

The mechanism is worth slowing down on, because it is the crux of the entire investment case. Defense PSUs like Mazagon Dock pay on a milestone model. CFF must first buy expensive, specialized raw material—those imported copper-nickel alloys and precision castings—and pay for it upfront. It then spends many months, often more than a year, machining, assembling, and testing a bespoke system. Only after delivery, and after multiple tiers of government inspection and sign-off, does payment get released. The company's own prospectus lays the cycle bare: inventory alone was held for 162, 193, and 180 days across FY22 through FY24, and receivable days swung violently—from around 30 days in FY24 to 118 days by the September 2024 half-year and up toward 150 days in FY25, with the full cash-conversion cycle sitting well above 400 days.23 Read that again: money goes out the door and comes back more than a year later. In the interim, someone has to finance the gap.

That someone was, first, the promoter's loans; then the IPO; then bank lines—a modest ₹15 crore working-capital facility from Axis Bank as of the FPO filing; and then the FPO itself.23 This reframes the July 2025 equity raise entirely. It was not a luxury or an offensive move—it was a necessity to fund the working-capital gap of a rapidly expanding half-a-billion-rupee order book without spiraling into high-interest debt.17 A skeptic's version of the same sentence is sharper: shareholders were being asked to supply the interest-free float that the Indian government's payment terms refuse to provide. That is the working-capital trap in one line, and it is the question a serious investor must keep returning to.

The company's own FPO arithmetic is unusually candid about this, and it rewards a close read. CFF's auditor-certified working-capital projections showed a total working-capital gap of ₹165.8 crore in FY25 rising to ₹220.6 crore in FY26—against a company whose FY25 revenue was ₹146 crore.23 Read that comparison again: the working capital required to run the business was projected to exceed the company's annual revenue, and by FY26 to exceed it by half again. Most businesses turn their working capital over several times a year. CFF turns it over less than once. The funding plan for that gap was explicit—owned funds, a ₹15 crore bank line, and ₹72.6 crore from the FPO.23 The equity raise was not a strategic choice layered on top of the business model. It was the business model's financing plan, written down and certified by the auditors.

There is one more disclosure here that functions as a live test of management's forecasting discipline, and it is not flattering. In the FPO documents certified in November 2024, management projected debtor days of 91 for FY25 and 90 for FY26, complete with a detailed breakdown of the government's payment pipeline—invoice submission, document verification, store receipts, internal approvals, payment authorization, processing—summing neatly to about ninety days.23 The actual FY25 outcome was roughly 150 days.19 Management missed its own auditor-certified receivables forecast by roughly two-thirds, within months of publishing it. That is worth stating plainly, because it cuts to the heart of the credibility question: either management does not have visibility into when its single customer will pay, or its projections were optimistic in a document being used to raise equity. Neither interpretation is comfortable, and the company has not, in public materials, explained the miss. When assessing any future guidance from CFF on working-capital normalization, this episode is the relevant precedent.

Here, though, is where the story earns a genuine update, and where neutrality demands we credit the evidence as well as the risk. The FY26 numbers suggest the trap may be loosening. The company reported that its ₹87.75 crore FPO proceeds were fully deployed—₹72.6 crore into working capital exactly as promised, with a minor reallocation of about ₹27 lakh of unspent issue expenses into general corporate purposes—by March 31, 2026.24 Two things follow. The first is reassuring: the money went precisely where management said it would go, with a deviation so small it borders on rounding. Against a market where SME issuers have been known to redirect proceeds creatively, that is clean execution. The second is sobering: an ₹87.75 crore raise was entirely consumed in roughly eight months. Whatever else the FPO was, it was not a war chest. It was fuel, and the engine burned it fast.

And yet the same year, for the first time in its listed life, the board recommended a dividend—a modest ₹0.75 per share on a ₹10 face value, against earnings per share of ₹19.08.2024 The payout is token, well under five percent of earnings, and no one should mistake it for a capital-return program. But it is a signal, and signals from a company in a cash trap are worth reading carefully. A board does not initiate a dividend, however small, while fighting for liquidity; it does so when it believes the worst of the cash drain is behind it. Combined with FY26's 43 percent revenue growth and expanding EBITDA margins, the FY26 evidence points toward a business that may finally be outgrowing its working-capital cycle rather than being consumed by it.

The honest conclusion is a suspended judgment, and investors should resist the urge to resolve it prematurely in either direction. One improved year does not break a structural pattern rooted in how the Indian government pays its suppliers—a pattern CFF does not control and has so far shown no ability to renegotiate. But the FY26 data is genuinely the most important operational evidence in the whole file, and dismissing it would be as lazy as celebrating it. The reason the trap matters so much is that it defines who can even survive in this business—which brings us to the competition.

VII. Competitive Landscape & Strategic Moats

Imagine you are a rival Indian engineering firm looking at CFF's margins and thinking, "I'd like some of that." Now war-game what it would actually take to steal a single AEM line item from CFF. You would need a foreign technology partner willing to transfer submarine-grade design and metallurgy—partners who are few, jealously guarded, and often already spoken for. You would need to build hyperbaric and endurance test rigs costing millions. You would need to survive a multi-year vendor-qualification process with the Navy and the shipyards, during which you earn nothing. And at the end of all that, you would be bidding to replace a part that the Navy is contractually bound to keep buying from CFF for the life of the boat. The exercise usually ends before it begins. That is the shape of CFF's competitive protection.

It helps to place CFF among India's specialized defense-engineering peers, because the comparison sharpens what CFF is and is not. MTAR Technologies is a larger, Hyderabad-based precision-manufacturing house serving nuclear, space, and clean-energy customers as well as defense—broader, more diversified, and exposed to different end-market cycles. Its diversification is a genuine strength when one end-market stalls, but it also means MTAR competes on several fronts at once rather than owning a single bottleneck outright; its history of margin pressure when a key customer's order pattern shifts is instructive about the limits of the specialist-supplier model. Paras Defence and Space Technologies plays in optics and defense electronics, a high-technology but intensely competitive arena where the moats are built more on R&D pace than on single-source lock-in—you must keep out-innovating rivals rather than simply holding a certification. Sika Interplant Systems is perhaps the closest analog in spirit—a small, high-barrier aerospace-and-defense engineering niche player operating below the radar of most institutional investors.

Against this set, CFF's distinguishing feature is not scale (it is meaningfully smaller than MTAR) or technological breadth (it is narrower than Paras); it is the depth of lock-in on the specific platforms it serves. It is a deep, narrow moat rather than a wide, shallow one. The trade-off is symmetrical and should not be glossed over: a narrow moat concentrates risk exactly as much as it concentrates advantage. MTAR can lose a nuclear customer and lean on space; Paras can lose an optics tender and lean on electronics. If India's submarine program stalls, CFF has no second leg to stand on. Investors are not choosing between a good business and a bad one here—they are choosing between diversified mediocrity of moat and concentrated depth of it. Reasonable people land differently on that trade.

One further competitive nuance deserves mention, because it is the most plausible route by which CFF's advantage could erode. The threat is not a domestic upstart out-machining CFF; that is close to impossible for the reasons already given. The realistic threat is disintermediation from above: a foreign OEM deciding to set up its own wholly owned Indian subsidiary to capture the indigenization mandate directly, or a PSU shipyard vertically integrating component manufacture in-house to capture the margin. Both have precedent in global defense. CFF's protection against the first is that OEMs generally prefer the capital-light route of licensing to a local partner over building Indian factories themselves; its protection against the second is that PSU shipyards have historically been poor at precision component work and have little appetite to try. These are real protections, but they are commercial preferences rather than legal barriers—and preferences can change.

Run it through the two frameworks investors reach for. In Helmer's 7 Powers, CFF's strongest claims are switching costs—the thirty-year single-source lifecycle already described—and a form of cornered resource, in the shape of the exclusive technology-transfer agreements with Coyard, Naval Group, Atlas Elektronik, and Nereides that domestic rivals simply cannot copy.710 Through Porter's Five Forces, the threat of new entrants is very weak, throttled by the certification timeline and test-rig capex; rivalry among qualified suppliers is limited by how few clear the bar. The genuinely double-edged force is buyer power. On paper, CFF sells into a near-monopsony: the Indian Navy and its PSU shipyards are effectively the only customer, and a monopsony buyer normally crushes supplier margins. In practice, CFF's single-source AEM status inverts the relationship for the specific items it owns—the Navy needs those parts and cannot shop elsewhere, giving CFF real pricing power on spares and repairs. But make no mistake: that inversion holds only item by item, and the buyer's structural leverage reappears with a vengeance in the one place it hurts most—payment terms. CFF can, apparently, name its price; what it cannot do is get paid on time. The moat protects the margin but not the cash. That tension—strong on paper, strained in the bank account—runs straight through to the people responsible for managing it.

VIII. Management Spotlight & Corporate Governance

A company this dependent on relationships—with the Navy's procurement bureaucracy, with French and German OEMs, with the shipyards—is, in the end, a bet on the people holding those relationships. At CFF, that means a tightly held, family-run structure, with all the strengths and all the flags that implies.

Sunil Menon and Gautam Makkar are not just co-founders; they are brothers-in-law, and their alignment is written into the cap table.25 After the July 2025 FPO diluted their stake, the promoter group still held about 68 percent of the company, down from roughly 73 percent before the FPO and 80.5 percent at the time of the IPO.26 That is a heavy insider ownership—the classic "skin in the game" that aligns founders with minority holders, since the vast majority of any value created accrues to the same two families that built the firm.

Menon's own profile is worth dwelling on, because in a relationship-driven business the man is part of the moat—and part of the risk. His authority inside the company is near-total: founding promoter since 2012, redesignated managing director in September 2022, individually the single largest shareholder, and by the company's own telling "the guiding force behind the growth and business strategy."425 The unconventional hotel-management background, far from being a liability, seems almost fitting for a business whose hardest problems are not engineering but orchestration—managing French and German technology partners, satisfying Navy inspectors, shepherding orders through a Byzantine PSU payment bureaucracy. Those are fundamentally relationship problems, and they reward a temperament for people and process over pure technical brilliance. But the flip side is unavoidable: a company this dependent on one person's relationships and judgment carries a key-man risk that no organizational chart can fully mitigate.

On capital allocation, the behavioral track record over time is genuinely consistent, and consistency is the trait most worth rewarding in management assessment. Across three years of filings, offer documents, and disclosures, the founders have said the same thing and done the same thing: stick to naval defense engineering, deepen technology tie-ups, expand Khopoli, and refuse the temptation to diversify into unrelated hot sectors when the stock was flying. There is no diworsification here, no vanity acquisition, no sudden pivot into whatever theme the market was rewarding that quarter. The one gap between word and deed—the un-pursued ambition to enter missiles, tanks, aircraft, and drones sketched in the IPO roadmap—errs on the side of too little diversification rather than too much, which for a small-cap promoter is the safer sin. Narrative and action match. For a small-cap promoter in a frothy sector, that discipline is not nothing, and it is the strongest single argument in management's favor.

The fair critique is equally clear, and it lives in the working-capital story. Management has, so far, been unable—or unwilling—to negotiate meaningfully better payment milestones with its PSU customers, and the consequence has been repeated equity raises that dilute the very minority holders whose interests are supposedly aligned. An activist would put the question directly: is this a company that funds growth, or a company that funds government float and calls it growth? The FY26 improvement in cash generation is the first real evidence for the defense; a single year is not yet a rebuttal.

Then there is the governance file that comes with any closely held family firm, and it will only draw more scrutiny as CFF moves to the main board. The promoter group extends into family members holding equity, related-party history is present in the company's DNA—the Khopoli property itself was bought from the promoters' own Flash Forge entity, and the pre-IPO working capital was financed by promoter-group loans at 12 percent.812 None of this is unusual for a founder-built company, and none of it is presented here as wrongdoing. But main-board listing brings stricter independent-board expectations, and the watch items are obvious: independence of the board relative to a dominant promoter duo, the pricing and disclosure of any future related-party dealings, and whether governance formalizes as the shareholder base institutionalizes. These are matters to monitor, not to indict. And they feed directly into a broader risk radar.

IX. Active Risk Radar & Skeptical Stress Test

Every bull thesis deserves to be stress-tested by an imagined short-seller, and CFF offers a short three genuine pressure points—not vague macro hand-waving, but specific mechanisms that could actually break the business.

The first is customer concentration, and it is severe. By the company's own disclosure, its top five customers accounted for between 91 and 100 percent of revenue across recent years, and its top ten for essentially all of it—overwhelmingly Indian defense PSU shipyards and their associates.27 Over 90 percent of the order book traces to that same government-linked demand.21 This is not a diversified customer base with one big client; it is, functionally, one customer—the Indian state—wearing several uniforms. If the submarine budget slips, if a program is delayed, if defense procurement priorities shift, CFF's order book does not soften gradually. It can freeze. The company has no commercial market to fall back on; there is no civilian buyer for a submarine's high-pressure air distribution panel.

The second is the working-capital / cash-flow exhaustion risk already dissected. If debtor days drift back above 180 and stay there, cash consumption can outrun even a freshly topped-up balance sheet, forcing CFF into high-interest working-capital debt that would compress the return on equity the whole story depends on. The bear's sharpest framing is the "leaky bucket": a business that must raise equity every few years just to finance receivables from a government that pays late is, in effect, asking shareholders to permanently subsidize the state's float, with dilution as the recurring cost. Each equity raise resets the clock but does not fix the mechanism.

The third is geopolitical technology dependence. CFF's cornered-resource advantage rests on transfer agreements with French and German partners. That is a strength in normal times and a vulnerability in abnormal ones. Any serious rupture in Indo-French or Indo-German defense relations, any export-control tightening, or any commercial breakdown with Coyard, Naval Group, Atlas Elektronik, or Nereides could choke off the technical documentation and specialized machinery upgrades on which future qualification depends. Indigenization reduces this dependence over time, but it does not yet eliminate it. There is a subtler version of this risk worth naming: the ToT partners are not charities. Each transfer is negotiated, and CFF's bargaining position with a Naval Group or a TKMS-owned Atlas Elektronik is that of a small Indian firm negotiating with a global prime. The terms of those agreements—royalties, exclusivity, renewal—are not fully public, and they sit upstream of everything CFF does.

A fourth, quieter risk sits in the execution disclosures themselves. CFF's own IPO document acknowledged that most of its contracts carry liquidated-damages or penalty clauses for delayed delivery, that it provides performance guarantees, and that it had in the past failed to complete some projects on schedule—though it had not, to that point, paid material penalties.28 In a business where the customer inspects at every stage and the schedules are already tight, delay risk is not hypothetical; it is a standing feature. A single major slippage on a flagship program could trigger penalties, guarantee invocations, or withheld payments that would compound the working-capital strain precisely when the company could least absorb it.

Now the skeptic's central question, put plainly: is CFF capitalizing what are really normalized, recurring working-capital needs? If receivables at these levels are a permanent feature of selling to Indian defense PSUs rather than a temporary growth artifact, then the equity raised to fund them is not building durable capacity—it is filling a bucket that leaks by design. The bull's honest counter is not a denial but a bet on scale: as programs like the follow-on Scorpène orders and the looming P75I enter high-volume procurement, CFF's growing importance to the supply chain should, in theory, give it the leverage to demand better milestone advances from MDL and to spread fixed costs over more revenue. The FY26 cash-generation improvement is the first flicker of evidence for that thesis. Whether it becomes a trend is the question the entire investment case now turns on—and it leads straight into the bull-and-bear ledger.

X. The Investment Spine: Bull vs. Bear Case

Strip away the narrative and the case reduces to a single tension: an exceptional competitive position stapled to a difficult cash-conversion model. Here is each side, argued at its strongest.

The Bull Case

The demand runway is the headline. India's submarine program is not winding down; it is accelerating. Beyond the follow-on Scorpène hulls, the enormous Project 75I (P75I) program looms—six advanced conventional submarines with air-independent propulsion, for which Germany's TKMS entered contract negotiations with Mazagon Dock in September 2025 after India's finance ministry cleared a program reportedly worth on the order of ₹70,000 crore.[^29] That figure dwarfs anything in CFF's current order book, and while the prime contract will go to MDL and TKMS, the indigenization mandate ensures that a lattice of qualified Indian suppliers will feed it. For a certified, single-source supplier of submarine mechanical and communication systems, a new multi-boat program is not just an order—it is a new thirty-year annuity waiting to be seeded. CFF's AEM status and existing MDL relationship position it to capture a premium slice, though it is worth noting the crucial caveat that P75I uses a different submarine design from a different OEM, so CFF's Scorpène-specific qualifications do not transfer automatically; it would have to re-qualify on the new platform.

The near-term order flow lends the demand thesis concrete support rather than leaving it as speculation. Through late 2025 and into 2026, CFF continued to book Navy work: a purchase order of roughly ₹78.74 crore from the Directorate of Procurement for equipment across various Navy programs, announced in April 2026, alongside a string of smaller P75-related awards.29 A single order worth more than half of the prior year's entire revenue is a meaningful vote of confidence from the customer, and the steady drumbeat of smaller wins is consistent with an installed base that keeps generating follow-on demand. This is the kind of operating evidence—actual contracts, actually signed—that separates a demand thesis from a hope.

The second pillar is the high-margin MRO shift. As the original six Scorpène boats accumulate operating years, they enter medium-refit and life-certification cycles, and refit-and-overhaul work on already-installed, single-source equipment is structurally more profitable than first-fit manufacturing—and less exposed to the multi-year build-and-inspect cash drag. Over time, a rising mix of recurring aftermarket revenue could decouple CFF's margins from the punishing manufacturing cycle. The FY26 EBITDA-margin expansion toward the high twenties is at least consistent with that direction.20

The third is the main-board catalyst: institutional access, potential index inclusion over time, and a deeper, more stable shareholder base once the SME-platform barrier is removed in the 2026 migration.3

The Bear Case

The bear needs only to keep pointing at the cash. For most of its listed life, CFF's record profits did not convert into operating cash, and the business could not simultaneously self-fund growth and reward shareholders—hence the serial dilution.22 One improved year does not retire a structural pattern rooted in how the Indian government pays. Second, execution risk is real and lumpy: defense manufacturing is slow, inspection-gated, and prone to slippage, so any procurement lag by the Navy flows straight into quarterly earnings volatility—especially uncomfortable on a freshly migrated main board where more investors are watching each print. Third is key-man risk: the business leans heavily on Sunil Menon's personal relationships inside the Navy's procurement machinery and the French and German defense channels. Those relationships are an asset that does not appear on the balance sheet and cannot easily be transferred.

Weighed together, neither side is a knockout. The competitive moat is real and well-evidenced; the cash-conversion weakness is also real and only tentatively improving. That is precisely why the case cannot be settled by assertion—it has to be tracked through a small number of hard metrics.

Key KPIs for Long-Term Investors to Track

Three numbers carry most of the signal, and the reader should track them over time rather than trust any single snapshot:

-

Operating cash flow versus reported profit (or OCF/EBITDA). This is the master gauge. It answers the only question that ultimately matters for this company: are the profits real cash, or accounting artifacts? Sustained positive operating cash flow would validate the FY26 turn; a relapse into deep negative territory would confirm the leaky-bucket thesis.

-

Debtor days (and the broader cash-conversion cycle). The direct measure of the working-capital trap. Watch for a durable contraction toward and below 120 days as evidence that CFF is winning better terms or executing faster; watch for a drift back above 180 as the warning sign.

-

Order-book execution (book-to-bill and backlog conversion). A ₹500-crore-plus backlog is only worth what CFF can actually build and invoice. The question is whether execution is fast enough to convert the backlog into revenue and cash before the next raise—turning visibility into value rather than into more inventory.

XI. Epilogue & Playbook Lessons

The enduring lesson of CFF Fluid Control is almost counterintuitive: in a business as vast and capital-hungry as building warships, the most defensible economics may belong not to the shipbuilder but to the maker of a valve. By targeting tiny, unglamorous, high-precision components—the parts nobody writes headlines about—and welding them to a certification-and-single-source moat, CFF built a position that is, in its narrow way, harder to dislodge than the shipyard's. Owning the bottleneck can beat owning the platform. That is the pick-and-shovel principle, translated from the gold rush to the deep sea.

There is a broader market lesson embedded here too, and it explains why Indian defense names have traded at premium multiples to Western defense primes. The premium is not really about growth in the usual sense; it is about a one-time structural transition—the indigenization gap—as India drags domestic content in defense procurement from a low base toward a mandated majority. Companies positioned in that gap enjoy a tailwind that is policy-driven, multi-year, and largely insensitive to the ordinary business cycle. The risk, of course, is that premiums price in the transition long before it fully arrives, and that the gap between the story and the cash flow—so vivid in CFF's own accounts—gets glossed over in the enthusiasm.

Which returns us to where the analysis keeps landing. CFF Fluid Control is a genuine engineering success: a company that started as a small forge and became a mission-critical technology partner to the Indian Navy, absorbing European submarine know-how and turning it into a durable, single-source franchise. The competitive case is well-evidenced and, on its own terms, credible. But a franchise that cannot reliably convert its profits into cash is a franchise with an asterisk, and for most of CFF's history that asterisk has been large. The FY26 results hint that the company may finally be growing into its own working-capital demands rather than being consumed by them. Whether that hint hardens into a trend—whether the maker of the submarine's valves can master the plumbing of its own balance sheet—remains the multi-billion-rupee question this business has yet to answer.

References

-

CFF Fluid Control Limited — Prospectus (Business Overview, Khopoli facility, product portfolio) — BSE / Company, 2023-05-23 ↩↩↩↩↩↩↩↩

-

CFF Fluid Control plans migration to main board of BSE and NSE; reappoints auditor — ScanX, 2026 ↩↩↩↩

-

CFF Fluid Control Limited — Prospectus (Brief Biographies of Directors: Sunil Menon, Gautam Makkar) — 2023-05-23 ↩↩↩↩↩

-

CFF Fluid Control Limited — Prospectus (Group Company: Flash Forge Private Limited, incorporated 1991) — 2023-05-23 ↩

-

CFF Fluid Control Limited — Prospectus (Incorporation as Flash Forge Fluid Control Pvt Ltd, Feb 16 2012; name change Sep 2012) — 2023-05-23 ↩

-

CFF Fluid Control Limited — Prospectus (Major events: 2015 Naval Group order and Coyard SAS ToT for Scorpène) — 2023-05-23 ↩↩↩↩↩

-

CFF Fluid Control Limited — Prospectus (Khopoli property acquired Dec 22, 2015 from Flash Forge Private Limited) — 2023-05-23 ↩↩

-

CFF Fluid Control Limited — Prospectus (Authorized Equipment Manufacturer status and 30-year lifecycle concept) — 2023-05-23 ↩↩↩↩↩

-

Partners — CFF Fluid Control Ltd (Naval Group, Atlas Elektronik, Nereides technology tie-ups) ↩↩↩

-

Indian firm ties up with German major Atlas Elektronik for indigenous sonar project — ANI News, 2024-06-13 ↩↩

-

CFF Fluid Control Limited — Prospectus (Unsecured promoter-group loans of ₹2,158.20 lakh at 12% p.a.; repayment object) — 2023-05-23 ↩↩↩

-

CFF Fluid Control Limited — Prospectus (IPO: 52,00,000 shares at ₹165, ₹8,580 lakh; issue opens May 30 2023) — 2023-05-23 ↩↩

-

CFF Fluid Control Limited — Prospectus (Objects of the Issue: working capital, loan repayment, machinery, Towed Wire Antenna technology) — 2023-05-23 ↩↩

-

CFF Fluid Control FPO — Date, Price, Subscription, Listing — Chittorgarh.com, 2025 ↩

-

CFF Fluid Control FPO — Objects of the Issue (₹72.60 cr working capital, GCP) — InvestorGain.com, 2025 ↩↩

-

CFF Fluid Control Ltd — FY24 revenue and net profit — Screener.in ↩

-

CFF Fluid Control Limited — FY26 board release (FY25 comparatives: revenue ₹14,556.05 lakh, PAT ₹2,385.03 lakh) — ScanX, 2026-05-05 ↩↩

-

CFF Fluid Control Reports Strong FY26 Results; Q4 EBITDA Margin Expands to 28.47% — ScanX, 2026-05-05 ↩↩↩

-

CFF Fluid Control Limited — FPO Draft Prospectus (Order book ₹55,160.19 lakh as of Dec 31 2024; >90% from Indian Navy/PSUs) — BSE, 2025-01-13 ↩↩

-

CFF Fluid Control Limited — FPO Draft Prospectus (Net cash from operating activities: FY24 −₹2,675.37 lakh, FY23 −₹927.20 lakh) — BSE, 2025-01-13 ↩↩

-

CFF Fluid Control Limited — FPO Draft Prospectus (Inventory and trade-receivable holding days; working-capital justification) — BSE, 2025-01-13 ↩↩↩↩↩↩↩

-

CFF Fluid Control Discloses Deviation in Fund Utilisation for Quarter Ended March 31, 2026 (FPO ₹8,775 lakh fully deployed; maiden dividend) — ScanX, 2026-05-05 ↩↩

-

CFF Fluid Control Limited — Prospectus (Promoters Sunil Menon and Gautam Makkar; brothers-in-law) — 2023-05-23 ↩↩

-

CFF Fluid Control Ltd — Shareholding pattern (promoter holding 68.06%, Mar 2026; prior 73.30%) — Screener.in ↩↩

-

CFF Fluid Control Limited — FPO Draft Prospectus (Top-5 customers 91–100% of revenue) — BSE, 2025-01-13 ↩

-

CFF Fluid Control Limited — Prospectus (Risk factors: liquidated-damages / penalty clauses and past project delays) — 2023-05-23 ↩

-

CFF Fluid Control Ltd receives contract worth Rs. 78.74 crores from Indian Navy — EquityBulls, 2026-04 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube