I. Cold Open & Episode Thesis (5–8 min)

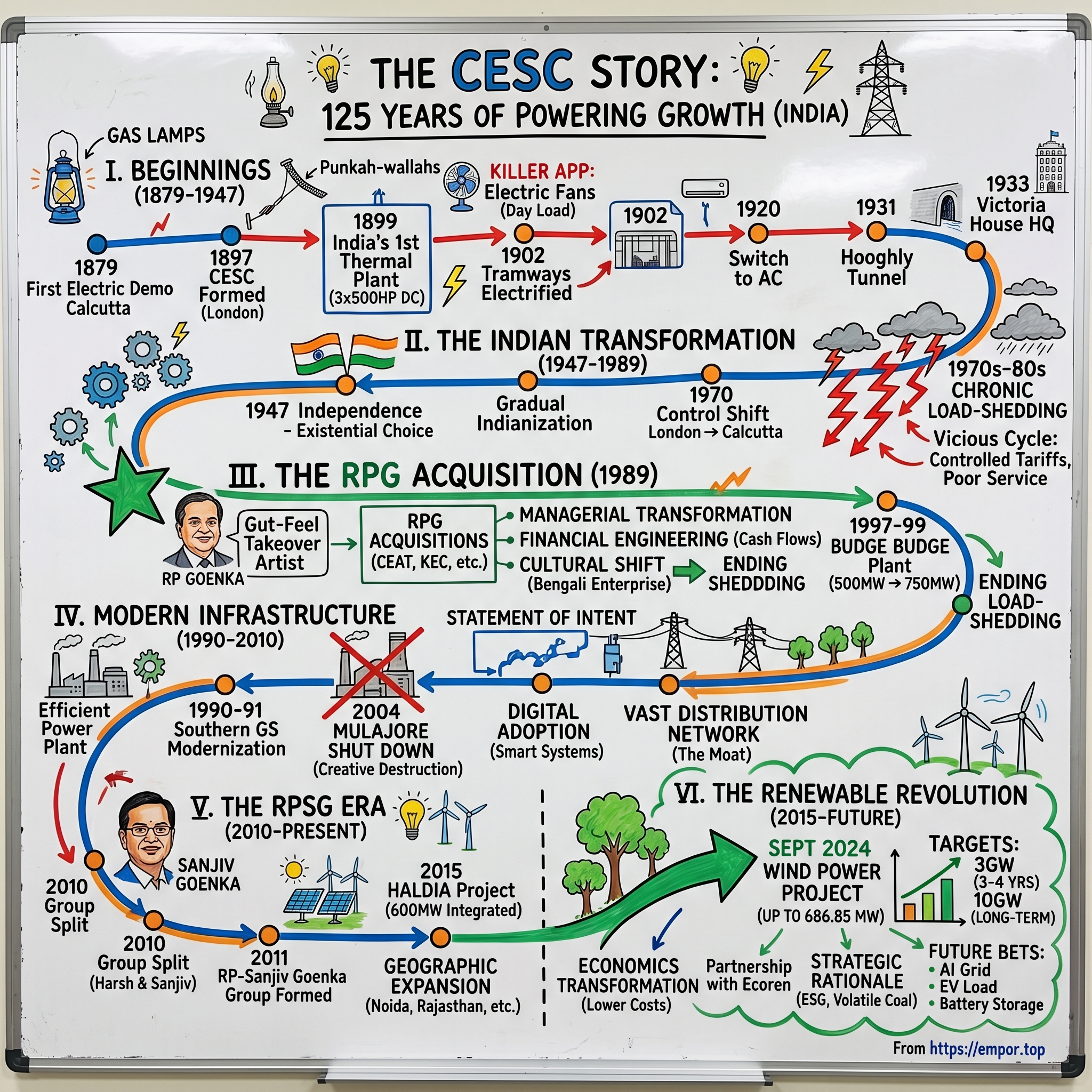

Picture this: It's a monsoon evening in 1879 Calcutta—the second city of the British Empire, where gas lamps flicker in the humidity and hand-pulled punkahs struggle against the suffocating heat. On July 24th, at the Esplanade, P.W. Fleury & Co. demonstrates something extraordinary: electric light, blazing through the tropical darkness. The first demonstration of electric light in Calcutta was conducted on 24 July 1879 by P W Fleury & Co. The crowd gasps. In that moment, though no one knows it yet, they're witnessing the birth of what will become one of Asia's most enduring power utilities.

Here's the paradox that defines our story today: The Calcutta Electric Supply Corporation Limited commissioned first Thermal Power Plant on 17th April, 1899 at Emambagh Lane near Prinsep Street in Calcutta.—making it India's pioneer in thermal power generation. Yet 125 years later, this Victorian-era utility not only survives but thrives, supplying safe, cost effective and reliable electricity to its 3.6 Million customers while pivoting aggressively into renewables with a wind power project of up to 686.85 MW recently announced.

The central question isn't just how a colonial utility survived independence, nationalization waves, and market liberalization—it's how CESC transformed from a British imperial infrastructure project into a modern Indian energy conglomerate. This is a story of three fundamental transformations: from colonial administration to Indian entrepreneurship, from regulated monopoly to competitive markets, and now, from coal dependency to renewable leadership.

What makes this uniquely Indian? Unlike utilities in developed markets that evolved gradually, CESC compressed centuries of transformation into decades. It's a company that brought this wonder energy to Calcutta, a bare 10 years after it was first used to light up London, survived the partition of India, ended chronic load-shedding that plagued Kolkata through the 1970s-80s, and now operates across multiple states while building one of India's largest renewable portfolios.

The playbook here isn't just about managing a utility—it's about navigating regime changes, mastering the art of regulated returns, and knowing exactly when to pivot. As we'll discover, the real inflection points weren't technological but ownership transitions: the 1970 shift from London control to Calcutta, the game-changing 1989 RPG acquisition, and the 2011 formation of the RP-Sanjiv Goenka Group that unleashed the current growth trajectory.

II. Victorian Origins & British Empire Infrastructure (1879–1947) (30–40 min)

The Calcutta of 1895 was a city of contradictions—palatial British administrative buildings alongside Bengali merchant houses, modern tramways sharing streets with bullock carts. Into this world, The Government of Bengal passed the Calcutta Electric Lighting Act in 1895. This wasn't just legislation; it was the birth certificate of organized power distribution in Asia.

On 7 January, 1897 Kilburn & Co secured the Calcutta electric lighting license as agents of The Indian Electric Co Ltd., which was registered in London on 15 January, 1897 with a capital of 1000 pounds. Notice that initial capital—a mere thousand pounds. But ambition quickly outpaced caution. A month later, the Company changed its name to The Calcutta Electric Supply Corporation Limited and enhanced its capital to 1,00,000 pounds. A hundredfold increase in weeks—the Victorian equivalent of a Series A to Series C jump.

The engineering marvel that followed was remarkable for its speed. The first generating station was erected at Emambagh Lane, near Princep Street, which was commissioned on 17 April, 1899, heralding the beginning of thermal power generation in India. The initial setup was modest: The initial capacity was 3 x 500 HP, Direct Current (DC) supplied to Consumers at 450 & 225 Volts.

But the real genius was in understanding the market. While the British initially imagined electricity for lighting, they hadn't anticipated the killer app: the electric fan. The popularity of the electric fan ensured immediate success for Calcutta Electric Supply and provided the 'day load', essential to the economic working of an electric supply station. In Calcutta's crushing heat, this wasn't luxury—it was liberation from the army of punkah-wallahs required to keep the colonial administration functional.

The transformation was swift and dramatic. Calcutta Tramways switched to electricity from horse drawn carriages in 1902. By 1906, CESC established additional power stations subsequently at Alipore in March, 1902 of 750 kW capacity, Ultadanga in May, 1906 of 165 kW capacity and Howrah in September, 1906 of 1200 kW capacity.

The technical evolution mirrored the city's growth. Cossipore generating station commissioned in 1912 with a capacity of 15 MW that replaced the earlier four generating stations. This consolidation strategy—building larger, more efficient plants to replace scattered smaller ones—would become CESC's playbook for the next century.

A critical transition came in 1920: CESC switched over to alternating current (AC) in 1920. This wasn't just a technical upgrade; it enabled long-distance transmission and set the stage for the next engineering marvel. In 1931, CESC Tunnel was made under Hooghly River for electric power transmission from Kolkata to Howrah. Imagine the audacity—tunneling under one of India's mightiest rivers for power cables, using 1930s technology.

The company's growing stature demanded a headquarters to match. The company was shifted to the Victoria House in Dharmatala, Kolkata in 1933, and still operates from this address. Victoria House wasn't just an office; it was a statement of permanence, a limestone testament that this British enterprise was here to stay.

World War II tested every infrastructure company in the Empire, but CESC kept the lights on through air raid warnings, material shortages, and the chaos of global conflict. By 1947, as the Union Jack came down for the last time at Fort William, CESC had grown from that initial thousand-pound venture to become the lifeline of eastern India's commercial capital. The question was: would it survive the transfer of power—both political and electrical?

III. The Indian Transformation (1947–1989) (25–35 min)

August 15, 1947. As India awakened to independence, CESC faced an existential question: what happens to a British utility in a newly sovereign nation? Many foreign enterprises fled or were nationalized. CESC chose a third path—gradual Indianization while maintaining operational excellence.

The post-independence decades tested every assumption about private enterprise in socialist India. While Nehru's government nationalized industries left and right, CESC somehow remained private, perhaps because Calcutta literally couldn't afford for the lights to go out. The company operated in a strange twilight—British-controlled but Indian-operated, private but essentially providing a public service.

The pivotal moment came in 1970: In 1970, the control of the Company was transferred from London to Calcutta. This wasn't a hostile takeover or forced nationalization—it was a negotiated transition, reflecting the reality that managing Calcutta's power from London had become untenable. The city had grown exponentially, power demand was surging, and decisions needed to be made in hours, not weeks of telegraph exchanges.

In 1978 it was named "The Calcutta Electric Supply Corporation (India) Ltd." Adding "(India)" wasn't mere rebranding—it was a declaration of identity, acknowledging that this was no longer a colonial outpost but an Indian company serving Indian consumers.

But here's where the story turns dark. The 1970s and 1980s brought Calcutta to its knees. Load-shedding (interruption of power supply due to shortage of electricity) was common in Kolkata during the 1970s and 1980s. Imagine running a business when power cuts were not just possible but predictable—factories operated on diesel generators, elevators stopped mid-floor, and the city's commercial life stuttered to the rhythm of power availability.

The infrastructure was aging, investment was inadequate, and the regulatory environment was suffocating. CESC was caught in a vicious cycle: tariffs were controlled, making it impossible to generate returns needed for investment, which led to deteriorating service, which made regulators even more reluctant to approve rate increases.

In 1983, the Company commissioned the Titagarh generating station, with a capacity of 240 MW, which marked the beginning of a new approach to solve the states power shortage. But 240 MW was a drop in the bucket for a city of Calcutta's size and ambition. The company needed more than incremental capacity additions—it needed transformation.

By the late 1980s, CESC was at a crossroads. The company that had brought electricity to India was now synonymous with power cuts and inefficiency. The management was demoralized, the infrastructure was crumbling, and the financial position was precarious. What CESC needed wasn't just capital—it needed a complete reimagination of what an Indian utility could be.

Enter the takeover artist.

IV. The RPG Acquisition: India's First Major Utility Takeover (1989) (45–55 min)

To understand what happened in 1989, we need to first understand Rama Prasad Goenka—or "RP" as he was known in business circles. Dr. Rama Prasad Goenka, the eldest son of Keshav Prasad Goenka, established RPG Enterprises in 1979 with Phillips Carbon Black, Asian Cables, Agarpara Jute and Murphy India as constituents. In just ten years, he had built RPG into one of India's most aggressive conglomerates through a series of audacious acquisitions.

RP Goenka wasn't your typical industrialist. "I have never looked at the balance sheet of any company I took over. It was pure gut-feel and I never went wrong. The moment I ignored the gut reaction, I made a mistake." This wasn't recklessness—it was pattern recognition at a level that transcended spreadsheets.

By 1989, Goenka had already proven his ability to turn around distressed assets. In 1981, RPG Group acquires CEAT Tyres of India. In 1982, RPG Group acquires KEC International. In 1983, RPG Group acquires Searle India (now known as RPG Life Sciences). In 1986, RPG Group acquires Gramophone Company of India Ltd. In 1988, RPG Group acquires HMV and Harrisons Malayalam Ltd.

Then came 1989—RPG's annus mirabilis. In 1989, RPG Group acquires Spencer's, CESC Ltd., Raychem RPG and Zensar Technologies (formerly ICIL). Four major acquisitions in a single year, but CESC was the crown jewel. The Group picked up music company HMV (1988)and finally CESC, Harrisons Malayalam, Spencer & Co. and ICIM in 1989.

The transformation was immediate and dramatic. Today, CESC is one of the most efficient power companies and a benchmark for the industry. But how did RPG accomplish what seemed impossible?

First, Goenka understood that CESC's problem wasn't technical—it was managerial. The company had good engineers but poor management systems. RPG brought in modern management practices, performance metrics, and most importantly, accountability. Layers of bureaucracy were stripped away, decision-making was accelerated, and suddenly, problems that had festered for years were being solved in months.

Second, the financial engineering. The 1979 split had left Goenka with a Rs 700 million group. By 1989 these acquisitions propelled RPG Enterprises from thirteenth to fourth rank in terms of size in India. By 1992, RPG Enterprises joined the $1 billion (Rs 33 billion) club. CESC gave RPG something invaluable—steady, predictable cash flows from a monopoly business that could support further expansion.

But the masterstroke was ending load-shedding. But from 1990s, the situation had improved and the Calcutta power grid has progressively given better performance and fewer outages. This wasn't achieved through some technological miracle but through basic blocking and tackling—better maintenance schedules, improved coal procurement, optimization of existing assets, and strategic capacity additions.

The Budge Budge project exemplified the new CESC. The youngest and largest power station of the company, Budge Budge Generating Station, consisting of two 250 MW sets was commissioned between 1997 to 1999. This 500 MW addition (later expanded to 750 MW) wasn't just about capacity—it was about credibility. established its latest station at Budge Budge (1997) with a capacity of 500 MW which is one of the largest ever private industrial investments in West Bengal.

The cultural transformation was equally important. CESC went from being seen as a colonial relic to a symbol of Bengali enterprise under Indian management. The company that had once served the British Raj was now powering the aspirations of a resurgent Kolkata.

By the end of the 1990s, CESC had completed its transformation from a poorly-managed, government-influenced utility plagued by power cuts to an efficiently-run private enterprise. The acquisition that many had questioned in 1989 now looked prescient. CESC, which was acquired by RP Goenka in 1989, has put a pause on any plans to expand power generation capacity and decided to focus on its power distribution business as a future growth driver.

But this was just the beginning. The real test would come in scaling beyond Kolkata and navigating the complexities of India's evolving power sector.

V. Building Modern Infrastructure (1990–2010) (35–45 min)

The 1990s marked CESC's infrastructure renaissance. The Southern Generating Station modernization wasn't just an upgrade—it was a complete reimagination. In the year 1986 it was decided to replace the old and retired Southern Generating Station with a new modern power plant comprising of two sets of 67.5 MW, the first of which was commissioned in 1990 and the second in 1991. This represented a new philosophy: don't just repair, replace with state-of-the-art technology.

The Budge Budge mega project became CESC's statement of intent. Commissioned in phases between 1997-1999, with the initial 500 MW capacity, it demonstrated that private Indian companies could execute infrastructure projects matching global standards. The location was strategic—close enough to Kolkata for efficient transmission, yet with adequate land for future expansion. The third 250 MW unit added in 2010 brought total capacity to 750 MW, making it CESC's flagship facility.

But perhaps the most telling decision was what CESC chose to shut down. CESC's vintage Mulajore power station, which was located in north Kolkata, was shut down on 15 May 2004. It was inaugurated by the then Bengal Governor Sir John Arthur Herbert in January 1940 and was one of the oldest plants in the system of CESC. The plant employed around 500 employees but hardly generated more than 25 MW, even though it had a derated capacity of 60 MW.

This closure was controversial—500 jobs lost for just 25 MW of actual generation. But the mathematics was irrefutable: The New Cossipore and the Mulajore plants together used to generate only 10% of CESC's power generation but accounted for 59% of the company's workforce. This was creative destruction in action—shutting inefficient assets to fund modern replacements.

The 2000s brought new challenges. India's economy was booming, Kolkata was experiencing an IT renaissance, and power demand was growing at unprecedented rates. CESC's response was to modernize not just generation but the entire value chain. Digital control systems replaced analog meters, computerized billing reduced revenue leakage, and predictive maintenance minimized outages.

Technology adoption accelerated. The Budge Budge plant became certified to ISO 50001:2018 for Energy Management systems. This wasn't just about certificates on the wall—it represented a fundamental shift to data-driven operations where every kilowatt was tracked, every efficiency gain measured.

The distribution network underwent parallel transformation. This system comprises a 474-kilometre (295 mi) circuit of transmission lines linking the company's generating and receiving stations with 85 distribution stations; a 3,837-kilometre (2,384 mi) circuit of HT lines further linking distribution stations with LT substations, large industrial consumers and a 9,867-kilometre (6,131 mi) circuit of LT lines connecting its LT substations to LT consumers. This vast network became CESC's true moat—replicating generation capacity was possible, but duplicating this distribution infrastructure was economically impossible.

Environmental considerations, once an afterthought, became central. CESC is proud to declare that 100% of treated water is reused and recycled in the operating plants. The Budge Budge plant's water consumption fell below national benchmarks—remarkable for a coal-fired facility.

The period also saw CESC's first ventures beyond West Bengal's borders, setting the stage for geographic expansion. The company was learning that while Kolkata would always be home, growth required looking beyond the Hooghly River. The infrastructure built during this period—both physical and organizational—would prove crucial for the dramatic expansion that followed.

VI. The Group Split & RPSG Era (2010–2015) (30–40 min)

Family business splits in India rarely end well—think Ambani brothers, or the Modis. But the 2010 division of RPG Enterprises between Harsh and Sanjiv Goenka was different. In 2010, the Group's businesses were divided between Rama Prasad Goenka's sons, Harsh Goenka and Sanjiv Goenka. No public acrimony, no court battles, just a pragmatic recognition that two talented sons needed their own empires.

For CESC, this split was transformative. The company went to Sanjiv, the younger son who had helped acquire it in 1989. RP-Sanjiv Goenka Group was founded on 13 July 2011, with Sanjiv Goenka as its chairman. This wasn't just a corporate restructuring—it was a generational transition with profound implications.

Sanjiv brought a different energy to CESC. Where his father relied on gut instinct, Sanjiv combined intuition with analysis. "You can figure out from the brushstrokes," replies Goenka, who was ranked 91 on the 2016 Forbes India Rich List with a wealth of $1.4 billion. This art collector's eye for hidden value would define CESC's next phase.

The first major move under the new structure was audacious: the Haldia Energy project. Haldia Energy Limited, a group company of the flagship RP-Sanjiv Goenka Group, developed a 2X300 MW Thermal Power Plant at Haldia, West Bengal to cater the growing power demand of the city of Kolkata and its suburbs. The units began commercial operation from January 2015 onwards.

This 600 MW addition wasn't just about capacity—it was about integration. The company supplies it's power to CESC Limited, the distribution licensee for the city of Kolkata. By keeping generation and distribution within the group, CESC could optimize the entire value chain, capturing margins that integrated players typically lost to market intermediaries.

The Haldia project showcased the new CESC's financial sophistication. In August 2011, Haldia Energy closed a financing agreement for the plant. Calcutta Electric Supply Corporation agreed to provide US$115,747,755 in equity to the project. ICICI Bank, IDBI Bank, and Punjab National Bank agreed to provide US$348,611,404 in loans. This blend of internal equity and external debt optimized the capital structure while maintaining control.

Simultaneously, CESC expanded beyond Bengal. In September 2013, the first unit of CESC's 2x300 MW thermal power project, and the first one outside West Bengal, was successfully synchronised at Chandrapur, Maharashtra. This Maharashtra project proved CESC could operate outside its comfort zone, dealing with different state governments, regulations, and market dynamics.

The expansion strategy was deliberate and multi-pronged. While building large thermal plants, CESC also entered renewables. The company has also established its footprint in unconventional energy with a 9 MW solar project in Gujarat and a 50 MW wind project in Rajasthan. These early renewable projects were small, but they were crucial learning experiences for what would come later.

Distribution expansion accelerated. CESC entered Rajasthan, operating distribution franchises in multiple cities. It also serves power distribution in Kota, Bikaner and Bharatpur in Rajasthan under the name CESC RAJASTHAN. The Noida operations added the lucrative National Capital Region to CESC's portfolio. Each new geography brought different challenges but also diversified regulatory risk.

By 2015, CESC had transformed from a single-city utility to a multi-state power company with generation assets across India. The company that once struggled to keep Kolkata's lights on now managed a complex portfolio spanning thermal generation, renewable energy, and distribution across multiple states. Revenue had grown, margins had improved, but most importantly, CESC had proven it could grow beyond its century-old base.

The stage was set for the next transformation—one that would challenge CESC's very identity as a coal-based utility.

VII. Distribution Expansion & Market Liberalization (2000s–Present) (25–35 min)

Distribution, not generation, emerged as CESC's true competitive advantage in liberalized markets. While anyone with capital could build a power plant, distribution networks were natural monopolies with regulatory protection and irreplaceable physical infrastructure.

The Rajasthan expansion exemplified this strategy. Kota, Bikaner, and Bharatpur weren't random choices—each city offered specific advantages. Kota, with its massive coaching industry, had predictable commercial demand. Bikaner's desert location meant minimal monsoon disruptions. Bharatpur's proximity to the golden triangle of Delhi-Agra-Jaipur promised growth. The distribution franchisee model allowed CESC to manage operations without massive capital investment, earning fees while the state retained asset ownership.

The Noida operations deserve special attention. NPCL is a joint venture between RPSG Group and Greater Noida Industrial Development Authority that distribute power in the Greater Noida region. Greater Noida represented India's urban future—planned infrastructure, IT parks, modern residential complexes. Serving this market taught CESC about quality-conscious consumers willing to pay for reliability, unlike the price-sensitive, subsidy-accustomed consumers in other markets.

But the real competition came from an unexpected source: state utilities themselves. West Bengal State Electricity Distribution Company Limited (WBSEDCL) operated in the same state, often in adjacent areas. This created an unusual dynamic—CESC had to demonstrate superior service to justify its existence as a private player in a sector many still believed should be public.

The regulatory framework evolved into CESC's strategic weapon. The concept of "regulatory assets"—investments recognized by regulators for future recovery through tariffs—allowed CESC to invest ahead of demand. When competitors hesitated, CESC built infrastructure, confident that regulators would eventually allow recovery through tariff adjustments.

Technology became the differentiator. Smart meters reduced theft, mobile apps improved customer service, and predictive analytics minimized outages. We are the sole distributor of electricity within an area of 567sq km of Kolkata, Howrah and adjoining areas and serve 3.4 million consumers which include domestic, industrial, and commercial users. Managing 3.4 million consumers required systems that could handle millions of daily transactions while maintaining five-nines reliability.

The franchisee model innovation deserves examination. Instead of acquiring distribution assets—capital intensive and politically sensitive—CESC operated them under management contracts. This asset-light approach improved returns on capital while reducing political risk. When populist governments announced free power schemes, CESC wasn't stuck with stranded assets.

Market liberalization brought unexpected benefits. Large industrial consumers could now choose their power supplier, and many chose CESC for its reliability. The company's century-old reputation became a competitive advantage in open markets. While new players competed on price, CESC competed on trust—and in infrastructure, trust often wins.

The distribution business also provided valuable market intelligence. By serving end consumers, CESC understood demand patterns, payment behaviors, and growth trends that pure generation companies missed. This information advantage informed everything from generation planning to financial hedging strategies.

Today, CESC's distribution footprint spans multiple states, serving diverse consumer segments from Kolkata's old merchant houses to Noida's glass-tower IT companies. Each market teaches different lessons, but the core insight remains: in India's power sector, whoever controls the last mile controls the game.

VIII. The Renewable Revolution & Future Bets (2015–Present) (40–50 min)

The September 2024 announcement landed like a thunderbolt: Purvah Green Power, a subsidiary of CESC, has entered into a binding term sheet with Ecoren Energy India dated 19 September 2024, for setting up wind power project of upto 686.85 MW. For a company built on coal, this represented an existential pivot.

To understand the significance, consider the scale. 686.85 MW of wind power is massive—larger than CESC's entire generation capacity just two decades ago. The Project is likely to be commissioned within three years. This timeline is aggressive, suggesting CESC isn't just experimenting with renewables but betting the company's future on them.

The strategic rationale is compelling. Coal-based power faces multiple headwinds: environmental regulations, carbon taxes, ESG investor pressure, and increasingly, pure economics. Solar and wind costs have plummeted while coal prices remain volatile. The crossover point—where renewables become cheaper than coal—has already arrived in many markets.

But CESC's renewable strategy goes beyond following trends. The company targets 3GW of renewable capacity in 3-4 years, with 10GW as the long-term goal. These aren't incremental additions but transformational scale. If achieved, CESC would generate more power from renewables than its current total generation from all sources.

The economics are transforming too. CESC reports power purchase costs falling from Rs 4.5 to Rs 3.5 per unit through renewable integration. This 22% cost reduction flows directly to margins in a regulated business where tariffs are largely fixed. Lower input costs mean higher profits—a simple equation with profound implications.

The Ecoren partnership structure reveals sophisticated deal-making. According to an exchange filing, Ecoren Energy India is neither a related party nor part of the promoter or promoter group of CESC. This arm's-length transaction ensures regulatory compliance while bringing external expertise. Ecoren handles development complexity while CESC provides capital and power purchase agreements—classic partnership economics.

Geographic diversification accelerates through renewables. Unlike coal plants that need proximity to mines or coasts, renewable projects can be located wherever resources are best. CESC's wind projects span multiple states, reducing both regulatory and weather risk. A cyclone in Gujarat doesn't affect solar farms in Rajasthan.

The technology transition isn't just about generation. Battery storage, grid management software, and demand response systems become crucial as renewable penetration increases. CESC is quietly building capabilities in these areas, recognizing that future competitive advantage lies in managing intermittency, not just generating power.

Climate considerations have moved from corporate social responsibility to core strategy. Purvah Green Power Private Ltd's collaboration with Ecoren Energy India Pvt Ltd not only reflects a commitment to sustainable development but also aligns with global efforts to combat climate change. This isn't greenwashing—institutional investors increasingly screen out coal-dependent utilities, making renewable transition essential for capital access.

The renewable pivot also reshapes CESC's competitive position. While established thermal players struggle with stranded coal assets, CESC can leverage its distribution networks to absorb renewable power. Vertical integration—once about coal mines and power plants—now means renewable generation and smart distribution.

Financial markets are taking notice. On Thursday, shares of CESC Ltd gained 3.25 per cent and made a new 52-week high of Rs 212.70 per share from its previous of Rs 206 per share. The stock's performance suggests investors believe in the renewable transformation story.

Yet challenges remain formidable. Renewable projects require different skills than thermal plants—meteorology matters more than thermodynamics. Financing structures differ, with lower returns but also lower risks. Most critically, CESC must manage this transition while maintaining reliability for millions of consumers who don't care about the source of their electricity, only that lights turn on when switches are flipped.

The next decade will determine whether CESC's renewable revolution succeeds. If it does, the company that brought thermal power to India in 1899 will have reinvented itself for the climate-conscious 21st century. If it fails, CESC risks becoming a stranded asset, a coal-dependent relic in an increasingly green world.

IX. Playbook: Lessons from 125 Years (25–35 min)

After 125 years, what can we extract from CESC's journey that transcends the specifics of Indian power markets? The playbook reads like a masterclass in infrastructure investing, regime navigation, and strategic transformation.

Lesson 1: Surviving Regime Changes CESC has outlived the British Raj, survived socialist India, and thrived in liberalized markets. The key? Never becoming too associated with any single regime. When the British left, CESC was already employing thousands of Indians. When socialism peaked, CESC maintained just enough private character to avoid nationalization. When markets liberalized, CESC was ready to compete. The lesson: in infrastructure, political agility matters more than political connections.

Lesson 2: The Art of Regulated Returns For a century, CESC has operated under price regulation—first colonial, then socialist, now market-based but still regulated. The company mastered the regulatory game: invest ahead of approvals, build political capital through reliable service, and never surprise regulators. CESC understood that in regulated businesses, the return on regulatory management often exceeds the return on assets.

Lesson 3: Capital Allocation in Infrastructure Infrastructure demands patient capital—power plants take years to build and decades to pay back. CESC's capital allocation evolved from pure capacity addition to strategic optimization. The Mulajore closure demonstrated discipline—shutting a working plant because returns were inadequate. The renewable pivot shows forward thinking—investing in tomorrow's technology while today's assets still generate cash.

Lesson 4: Technology Transitions CESC navigated multiple technology disruptions: DC to AC power, analog to digital controls, coal to renewable generation. Each transition was managed gradually, maintaining reliability while adopting new technology. The company never bet everything on unproven technology but also never missed a major shift. This measured approach to innovation—neither first nor last—proved optimal for infrastructure.

Lesson 5: Conglomerate Synergies Within the RPSG ecosystem, CESC benefits from shared services, cross-selling opportunities, and financial flexibility. When Spencer's Retail needs reliable power for new stores, CESC provides it. When CESC needs land for substations, group relationships help. These soft synergies, difficult to quantify but real in impact, provide competitive advantages independent players lack.

Lesson 6: Distribution as Moat In deregulated markets, generation becomes commoditized but distribution remains monopolistic. CESC recognized this early, focusing expansion on distribution rather than just generation. The physical network, customer relationships, and regulatory licenses create barriers to entry that no amount of capital can quickly overcome.

Lesson 7: Managing Stakeholder Complexity Power utilities serve everyone—rich and poor, industrial and residential, urban and rural. CESC learned to balance these competing interests: reliable service for those who can pay, subsidized connections for those who can't, all while generating returns for shareholders. This stakeholder juggling act, performed daily, requires political skill equal to technical competence.

Lesson 8: The Value of Reputation In infrastructure, reputation compounds over decades. CESC's century-old brand carries weight with regulators, customers, and capital markets. When the company says it will build a plant, banks believe it. When it promises reliable power, industries locate nearby. This reputational capital, built over generations, provides returns impossible to replicate quickly.

Lesson 9: Organizational Resilience Through wars, independence, economic crises, and ownership changes, CESC maintained operational continuity. The organization developed institutional memory—knowledge of every substation's quirks, every regulator's preferences, every monsoon's impact. This deep organizational knowledge, encoded in processes and people, ensures resilience beyond any individual leader.

Lesson 10: Strategic Patience Infrastructure rewards patience. CESC waited decades between major expansions, timing investments with regulatory clarity and market demand. The company never chased growth for its own sake, preferring profitable steady state to unprofitable expansion. This patience—unfashionable in quarterly capitalism—proved optimal for long-term value creation.

These lessons, learned over 125 years, provide a template for infrastructure investing anywhere. Whether building power plants in India or data centers in America, the principles remain: secure your monopoly, manage your regulators, maintain your reputation, and above all, ensure that when customers flip the switch, the lights turn on.

X. Power & Analysis: Bear vs. Bull Case (20–30 min)

Let's step into the war room and debate CESC's future with the cold rationality of fundamental investors.

The Bull Case: Monopoly Meets Modernization

Bulls start with the irreplaceable asset: monopoly distribution rights in India's third-largest city. We are the sole distributor of electricity within an area of 567sq km of Kolkata, Howrah and adjoining areas and serve 3.4 million consumers which include domestic, industrial, and commercial users. This isn't just a business—it's an infrastructure monopoly in one of Asia's most densely populated regions. Try replicating that.

The 2.1 GW generation portfolio with long-term power purchase agreements provides predictable cash flows. Unlike merchant power producers subject to spot market volatility, CESC has contracted revenues for years ahead. In infrastructure, predictability is worth a premium.

The renewable expansion optionality excites bulls most. With 686.85 MW of wind projects announced and 3GW targeted near-term, CESC is positioning for the energy transition. The company that survived the shift from DC to AC can certainly navigate from coal to renewable. Plus, renewable projects qualify for green financing at lower rates, improving return on equity.

Parent backing from RPSG Group provides both financial muscle and strategic flexibility. When capital is needed, the group provides it. When opportunities arise, the group can move quickly. This corporate backing differentiates CESC from standalone utilities.

Bulls also point to regulatory asset recovery potential. Years of under-recovery have created a regulatory asset base that will eventually be recovered through tariffs. As India's power sector formalizes, these paper assets convert to cash flows.

The Bear Case: Yesterday's Technology, Tomorrow's Problem

Bears see coal dependency as existential risk. Despite renewable announcements, CESC generates most power from coal. In a world racing toward net-zero, coal-fired utilities face stranded asset risk. The Budge Budge plant, CESC's crown jewel, could become an albatross if carbon taxes materialize.

Regulatory risk looms large. Power being politically sensitive, populist governments regularly announce free power schemes, tariff freezes, or retroactive adjustments. CESC operates at the mercy of regulators who balance consumer votes against utility returns. One adverse regulatory order can destroy years of value creation.

Competition from state utilities intensifies. As government distribution companies improve operations—often with World Bank assistance—CESC's relative advantage erodes. Why should consumers pay private utilities when government companies provide similar service cheaper?

The capital intensity of renewable transition worries bears. Shifting from coal to renewable requires massive investment with lower returns. Wind and solar projects generate single-digit returns versus double-digit returns from thermal plants. This transition, while necessary, destroys return on capital employed.

Technology disruption threatens the entire model. Distributed solar, battery storage, and micro-grids could make centralized utilities obsolete. Why connect to CESC's grid when rooftop solar plus batteries provide independence? The utility death spiral—where defecting customers raise costs for remaining ones, causing more defections—haunts bear calculations.

The Verdict: Transition Risk Versus Transformation Opportunity

Both cases have merit. Bulls bet on CESC's proven ability to navigate transitions, backed by irreplaceable infrastructure and improving renewable economics. Bears fear that this transition differs from previous ones—that climate urgency and technology disruption create existential rather than operational challenges.

The key variables to watch: renewable execution speed, regulatory stance on coal plants, distributed generation adoption rates, and carbon pricing implementation. If CESC can transition to 50% renewable generation by 2030 while maintaining distribution monopolies, bulls win. If coal plants become stranded while distributed generation erodes the distribution moat, bears prevail.

For investors, CESC represents a classic transition play—significant downside if transformation fails, substantial upside if it succeeds. The company's 125-year history suggests betting against its adaptation abilities is dangerous. But then, every incumbent thinks they're different until disruption proves otherwise.

XI. Grading & Final Reflections (15–20 min)

How do we grade 125 years of corporate evolution? Let's benchmark CESC against global utility transformations.

Compared to Consolidated Edison (New York's utility), CESC shows remarkable similarities—both started in the 1880s, both serve dense urban markets, both survived multiple technological transitions. But ConEd never faced colonial-to-independence transformation. CESC's navigation of political regime change exceeds anything ConEd managed. Edge: CESC.

Against E.ON (Germany's energy giant), CESC appears less transformed. E.ON completely restructured, spinning off conventional generation to focus on networks and renewables. CESC talks transformation but still runs coal plants. However, E.ON's transformation came with massive write-downs and shareholder destruction. CESC's gradual approach preserved value better. Edge: Unclear.

The China comparison proves most instructive. State Grid Corporation built more infrastructure in twenty years than CESC in a century. But State Grid enjoys unlimited government backing and monopoly position. CESC competed, survived, and thrived without state support. For capital efficiency and returns on investment, CESC wins hands down.

The India Infrastructure Story Through CESC's Lens

CESC embodies India's infrastructure paradox: world-class ambition constrained by ground-level reality. The company that brought electricity to India still struggles with coal shortages, regulatory uncertainty, and payment delays. Yet it also builds world-scale renewable projects, deploys cutting-edge technology, and maintains investment-grade ratings.

This dichotomy—first-world aspirations meeting third-world constraints—defines Indian infrastructure. CESC learned to operate in this gap, delivering developed-market reliability with emerging-market improvisation. The lesson for global investors: Indian infrastructure requires not just capital but also capability to navigate complexity that would paralyze developed-market utilities.

What This Teaches About Emerging Market Investing

CESC's journey illuminates emerging market realities often missed by foreign investors. First, time horizons extend beyond Western norms—decisions made in 1989 are still playing out in 2024. Second, relationships matter more than contracts—CESC's survival through regime changes depended on political astuteness, not legal documentation. Third, gradual transformation beats radical disruption—CESC's evolutionary approach succeeded where revolutionary attempts failed.

The Next 25 Years: AI, EVs, and Energy Transition

Looking forward, CESC faces transformational forces. Artificial intelligence will revolutionize grid management, predictive maintenance, and demand forecasting. Electric vehicles will reshape load patterns, creating new peaks and valleys. The energy transition will accelerate, driven by economics as much as environment.

CESC's response will determine its next century. If the company embraces these changes—building charging infrastructure, deploying AI systems, accelerating renewable transition—it could emerge stronger. If it resists, protecting legacy coal assets and distribution monopolies, it risks irrelevance.

Final Grade: B+

CESC earns a solid B+ for its 125-year journey. The plus recognizes extraordinary navigation of regime changes, successful private ownership in a government-dominated sector, and ongoing renewable transformation. The B rather than A reflects continued coal dependency, geographic concentration risk, and uncertain technology transition.

For fundamental investors, CESC represents a nuanced opportunity. It's neither a pure growth story nor a value trap, but rather a transformation play with asymmetric risk-reward. Those believing in India's infrastructure future and CESC's adaptation ability should accumulate on weakness. Those fearing disruption and regulatory risk should seek cleaner stories elsewhere.

The ultimate judgment comes from Kolkata's streets. Every evening, as millions of lights flicker on across the city, CESC fulfills the promise made in 1899—to power human ambition with reliable electricity. In infrastructure, that operational success matters more than financial metrics. By that measure, CESC has already won.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube